ppt 20120208 pb study media conference en

TRANSCRIPT

Performance

through focus

Seizing the global private

banking opportunity

February 8, 2012

1© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

Agenda

10.00 Welcome Andreas Hammer, Head of

Public Relations & Public Affairs,

KPMG Switzerland

Introduction Daniel Senn, Head of Financial

Services and Member of the Executive

Committee, KPMG Switzerland

Scientific Framework Prof. Dr. Dr. Tomi Laamanen,

Institute of Management,

University St. Gallen

Study Results Dr. Christian Hintermann,

Head of Transactions &

Restructuring Financial Services,

KPMG Switzerland

Daniel Senn

11.00 Questions & Answers

Lunch

Current Situation of

Swiss Private Banking

Daniel Senn

Head of Financial Services and Member of the

Executive Committee, KPMG Switzerland

«Wer zu spät kommt,

den bestraft das

Leben…»Michail Sergejewitsch Gorbatschow

Ost-Berlin, 7. Oktober 1989

Scientific Framework

Prof. Dr. Dr. Tomi Laamanen

Chair of Strategic Management,

Institute of Management,

University of St.Gallen

5© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

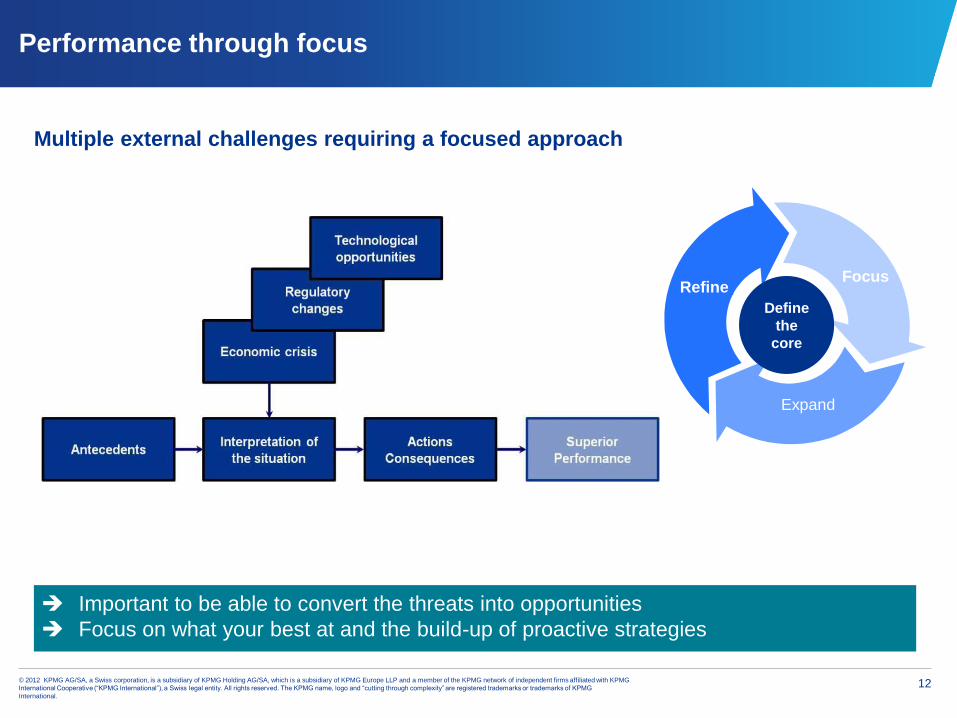

Overall Strategic Analysis Framework

AntecedentsInterpretation of

the situation

Actions

Consequences

Economic crisis

Regulatory

changes

Technological

opportunities

6© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

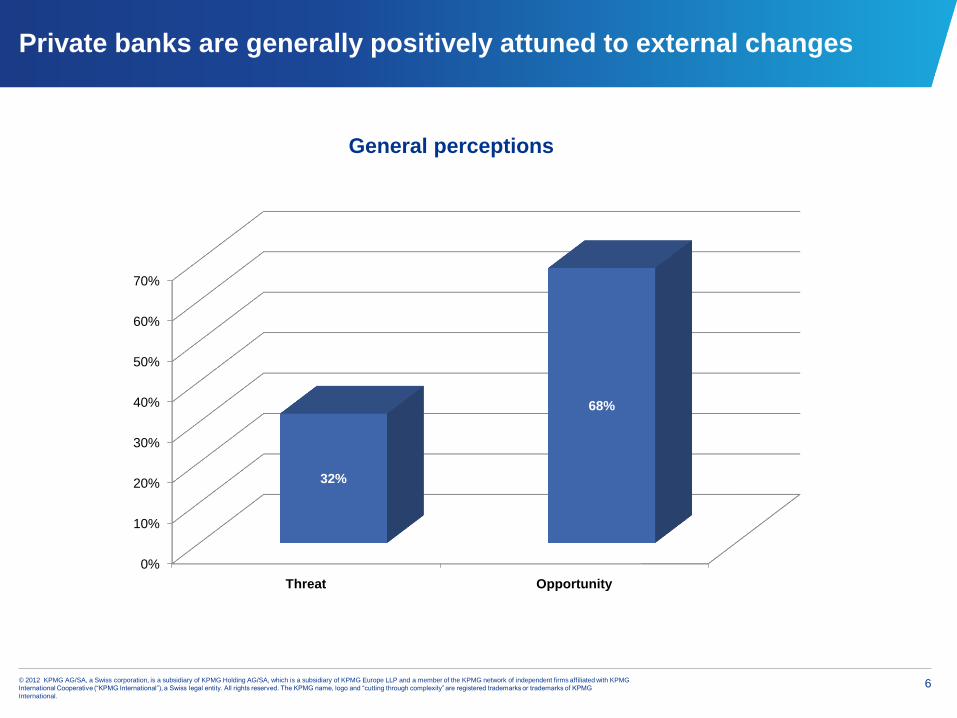

Private banks are generally positively attuned to external changes

0%

10%

20%

30%

40%

50%

60%

70%

Threat Opportunity

32%

68%

General perceptions

7© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

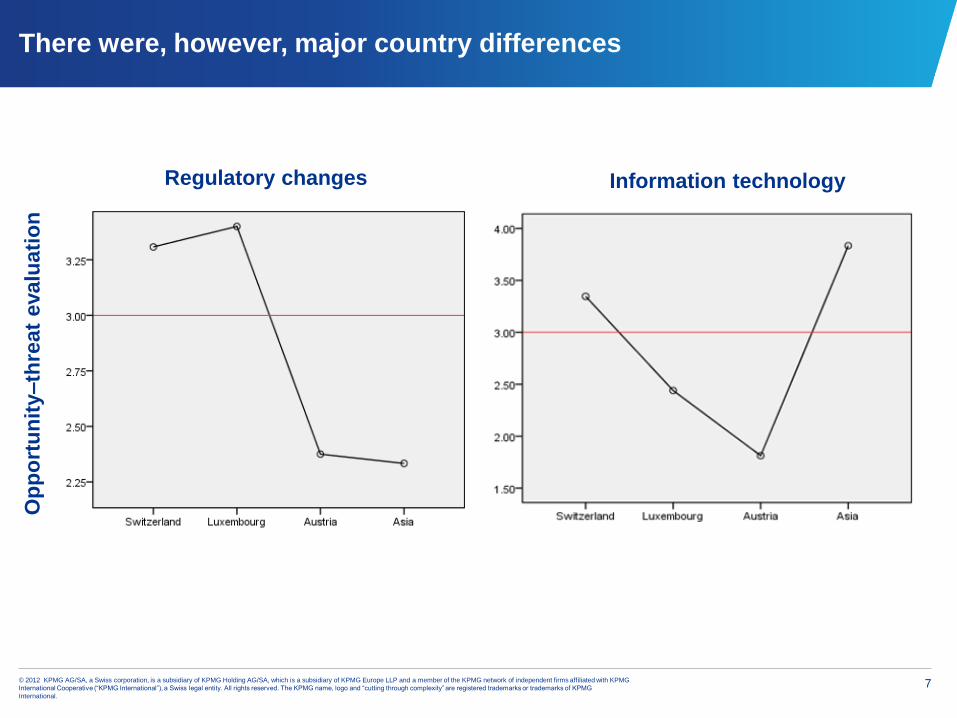

There were, however, major country differences

Regulatory changes Information technology

Op

po

rtu

nit

y–

thre

at

evalu

ati

on

8© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

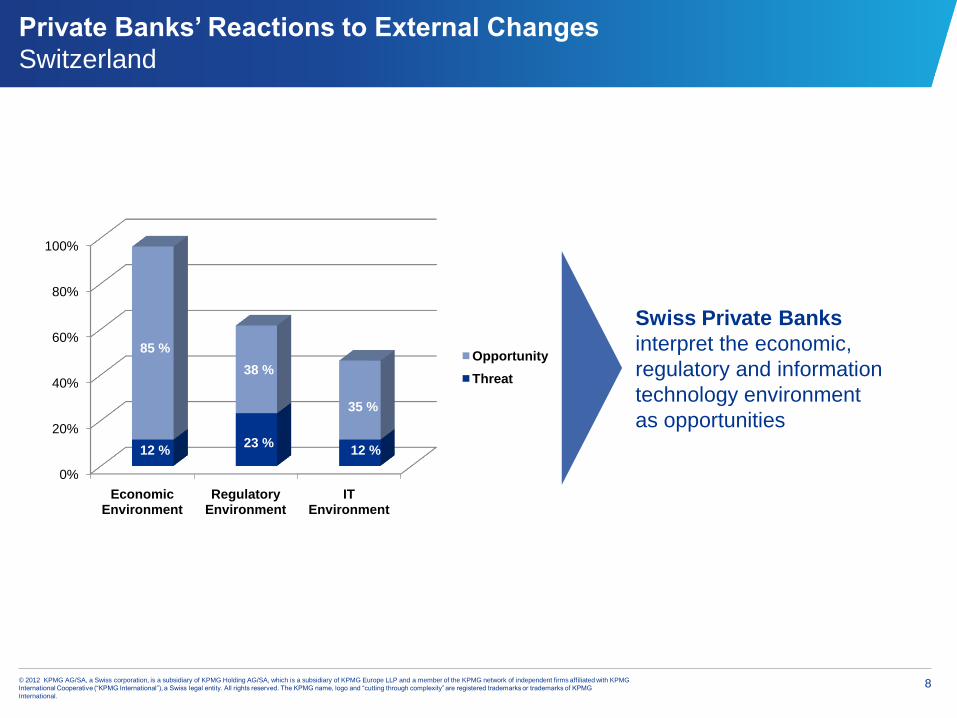

Swiss Private Banks

interpret the economic,

regulatory and information

technology environment

as opportunities

Private Banks’ Reactions to External Changes

Switzerland

0%

20%

40%

60%

80%

100%

Economic Environment

Regulatory Environment

IT Environment

12 %23 %

12 %

85 %

38 %

35 %

Opportunity

Threat

9© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

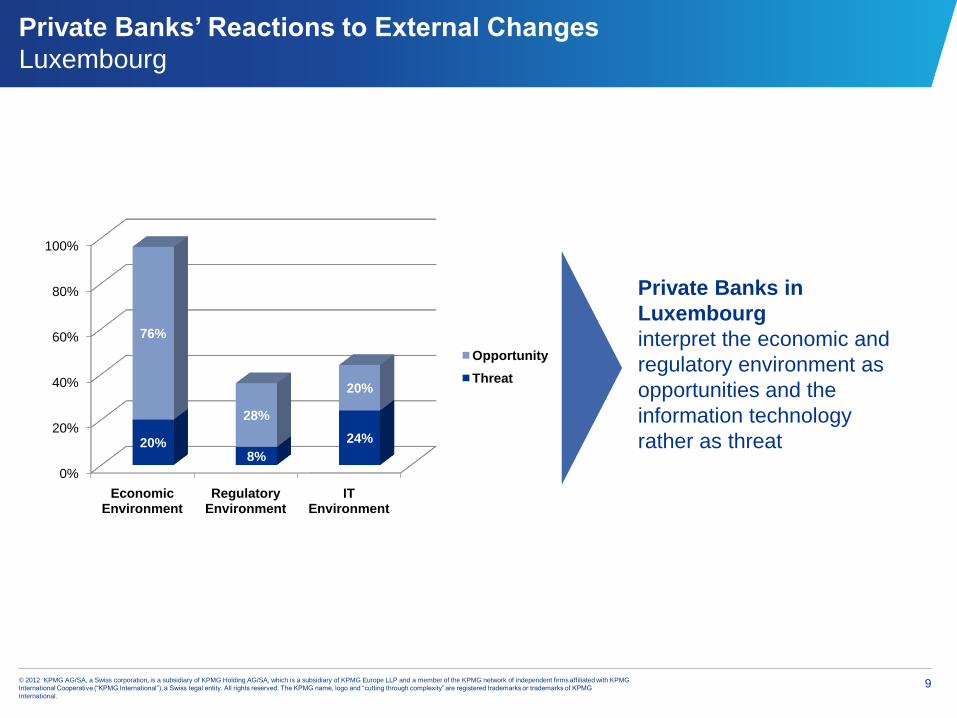

Private Banks’ Reactions to External Changes

Luxembourg

0%

20%

40%

60%

80%

100%

Economic Environment

Regulatory Environment

IT Environment

20%8%

24%

76%

28%

20%

Opportunity

Threat

Private Banks in

Luxembourg

interpret the economic and

regulatory environment as

opportunities and the

information technology

rather as threat

10© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

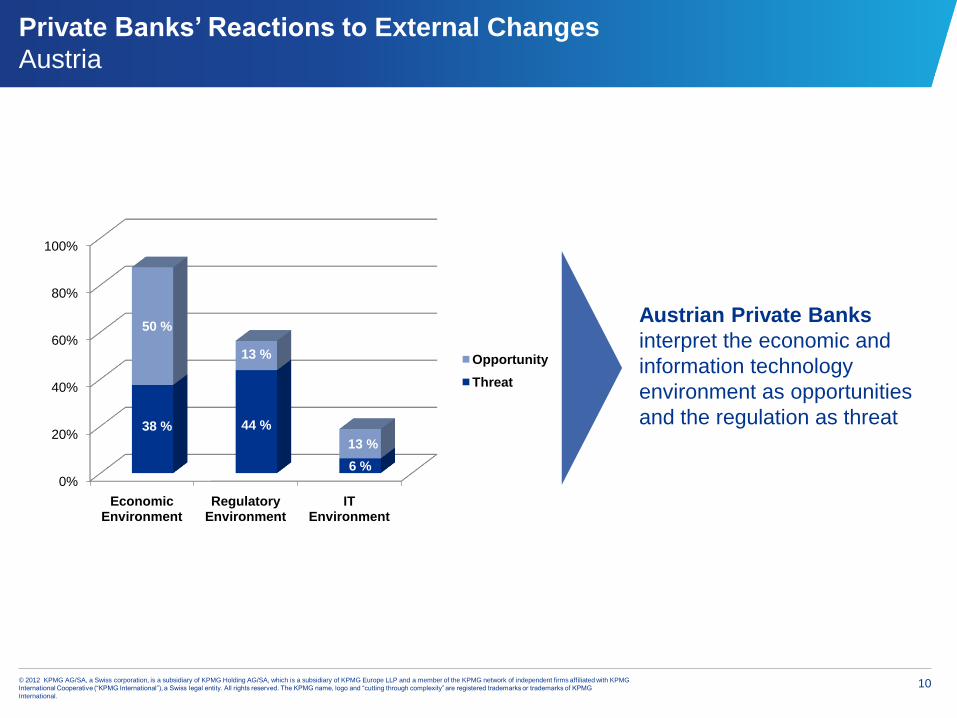

Austrian Private Banks

interpret the economic and

information technology

environment as opportunities

and the regulation as threat

Private Banks’ Reactions to External Changes

Austria

0%

20%

40%

60%

80%

100%

Economic Environment

Regulatory Environment

IT Environment

38 % 44 %

6 %

50 %

13 %

13 %

Opportunity

Threat

11© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

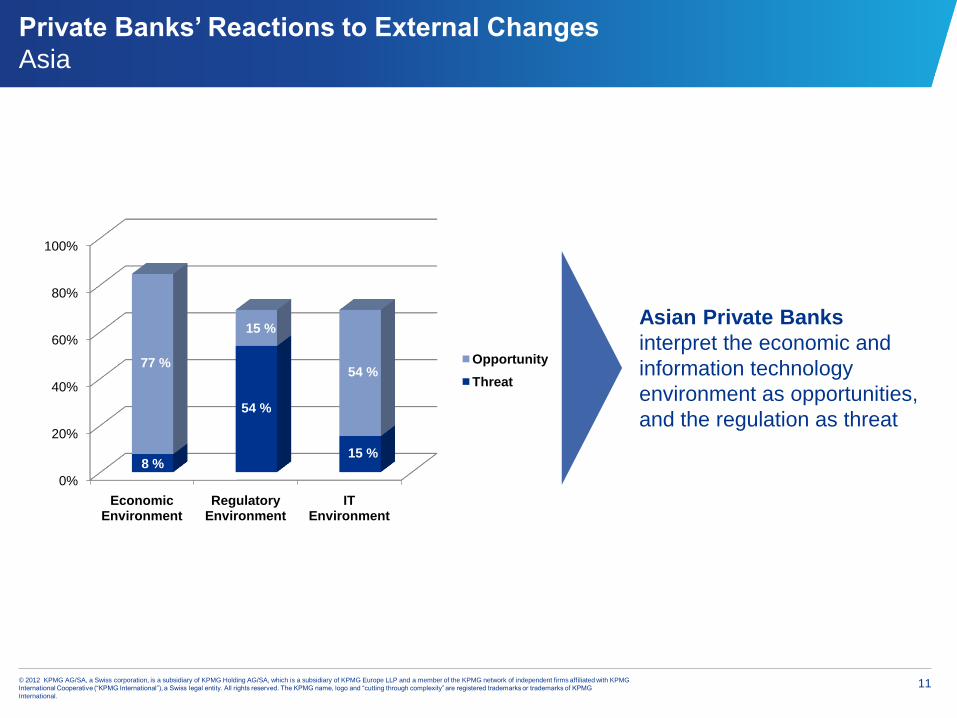

Asian Private Banks

interpret the economic and

information technology

environment as opportunities,

and the regulation as threat

Private Banks’ Reactions to External Changes

Asia

0%

20%

40%

60%

80%

100%

Economic Environment

Regulatory Environment

IT Environment

8 %

54 %

15 %

77 %

15 %

54 %Opportunity

Threat

12© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

Performance through focus

Multiple external challenges requiring a focused approach

RefineFocus

Expand

Define

the

core

Important to be able to convert the threats into opportunities

Focus on what your best at and the build-up of proactive strategies

Study Results

Dr. Christian Hintermann

Head of Transactions & Restructuring Financial

Services, KPMG Switzerland

Daniel Senn

Head of Financial Services and Member of the

Executive Committee, KPMG Switzerland

14© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

AppleNokia

Performance through focus

15© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

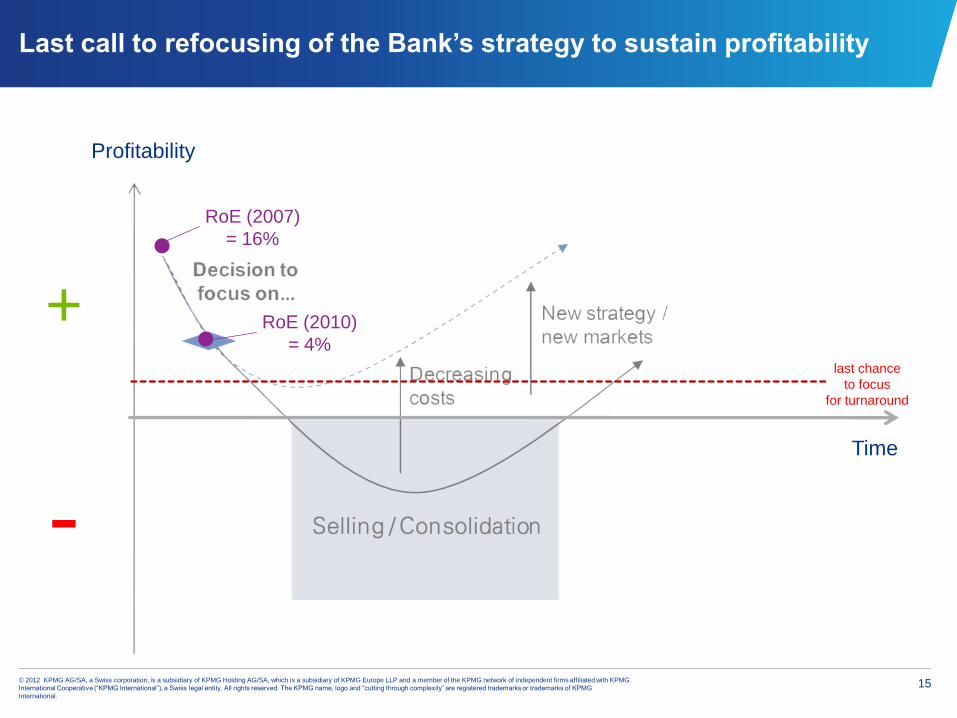

Last call to refocusing of the Bank’s strategy to sustain profitability

Profitability

+

-

RoE (2007)

= 16%

RoE (2010)

= 4%

Time

last chance

to focus

for turnaround

16© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

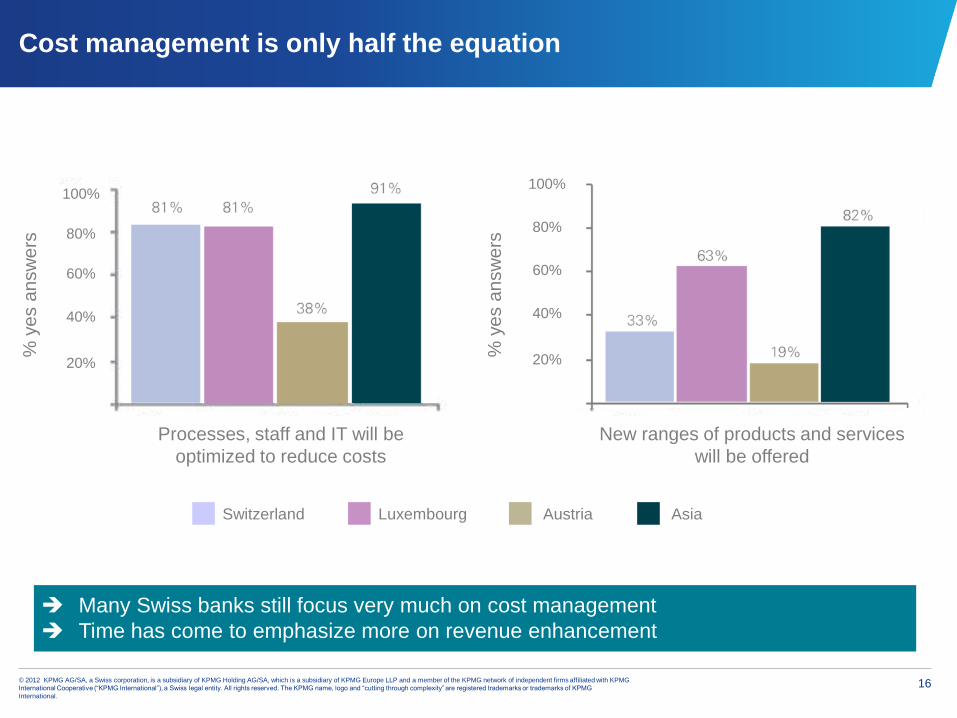

Cost management is only half the equation

Many Swiss banks still focus very much on cost management

Time has come to emphasize more on revenue enhancement

Processes, staff and IT will be

optimized to reduce costs

% y

es

an

sw

ers

100%

80%

60%

40%

20%

81% 81%

38%

91%

New ranges of products and services

will be offered

% y

es

an

sw

ers

100%

80%

60%

40%

20%

81% 81%

38%

91%

Switzerland Luxembourg Austria Asia

17© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

Seven areas that are key to sustained success

18© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

Differentiators

Confidentiality Political stability Tax stability Capabilities /

expertise (of local

service provider)

% y

es

an

sw

ers

100%

80%

60%

40%

20%

Switzerland

Luxembourg

Austria

Asia

Key selling propositions of home jurisdiction

Client confidentiality and political stability as key selling proposition

Banks will struggle to differentiate only based on national characteristics

19© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

Differentiators

Key selling propositions for your bank

Switzerland Luxembourg Austria Asia

Financial Branding CRMs Products Culture Pricing Technology

engineering

% y

es

answ

ers

100%

80%

60%

40%

20%

Swiss Private Banks want to differentiate mainly through their culture – pricing and

technology not relevant

Do the banks invest enough to build a clear profile in the increasingly competitive market?

20© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

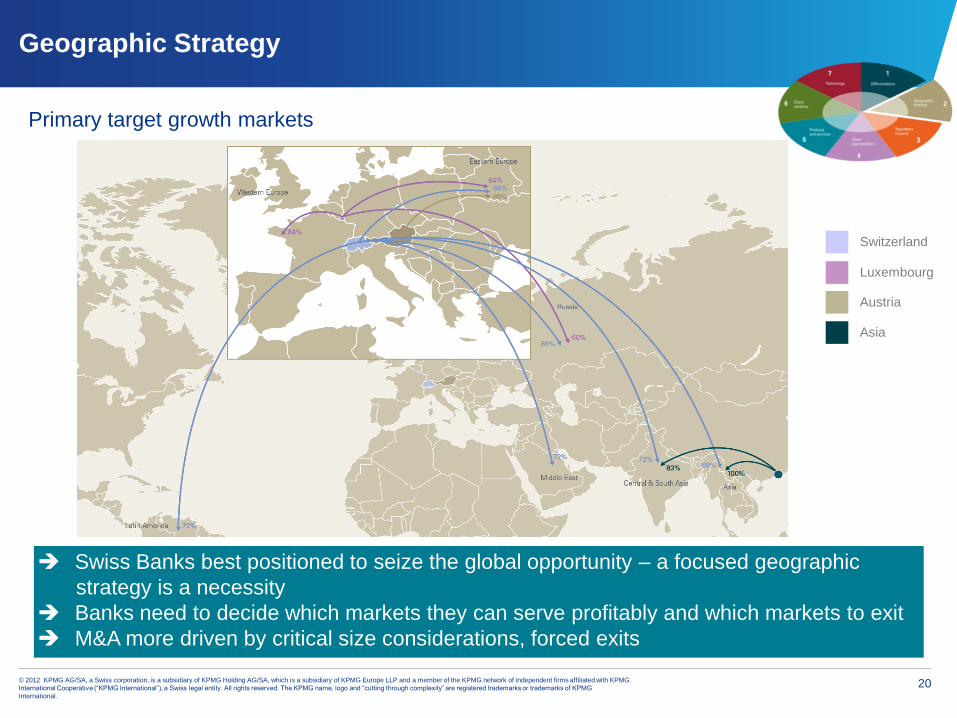

Geographic Strategy

Swiss Banks best positioned to seize the global opportunity – a focused geographic

strategy is a necessity

Banks need to decide which markets they can serve profitably and which markets to exit

M&A more driven by critical size considerations, forced exits

Switzerland

Luxembourg

Austria

Asia

Primary target growth markets

21© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

Geographic Strategy

Local regulation as key inhibitor for approaching clients

Many banks still rely/have to rely on classical cross border banking to do business

Large banks Small banks Large banks Small banks

Local regulation in the foreign country

Tone from the top, general strategy of

the group

Culture differences

IT infrastructure

Size of your own operation

% yes answers % yes answers

22© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

Regulatory Impacts

Implementation of tax transparency strategy in light of increasing regulation

26%

71% 70%

92%

Tax transparency strategy

within 1 year

Tax transparency strategy

within 5 years

Switzerland Luxembourg Switzerland

Yes Yes

% o

fto

tal

Luxembourg

0 %

20 %

100 %

40 %

80 %

60 %

Luxembourg Banks perceive a stronger sense of urgency achieving tax transparency

Early adoption may be a competitive advantage and with ever increasing pressure a

pre-requirement

23© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

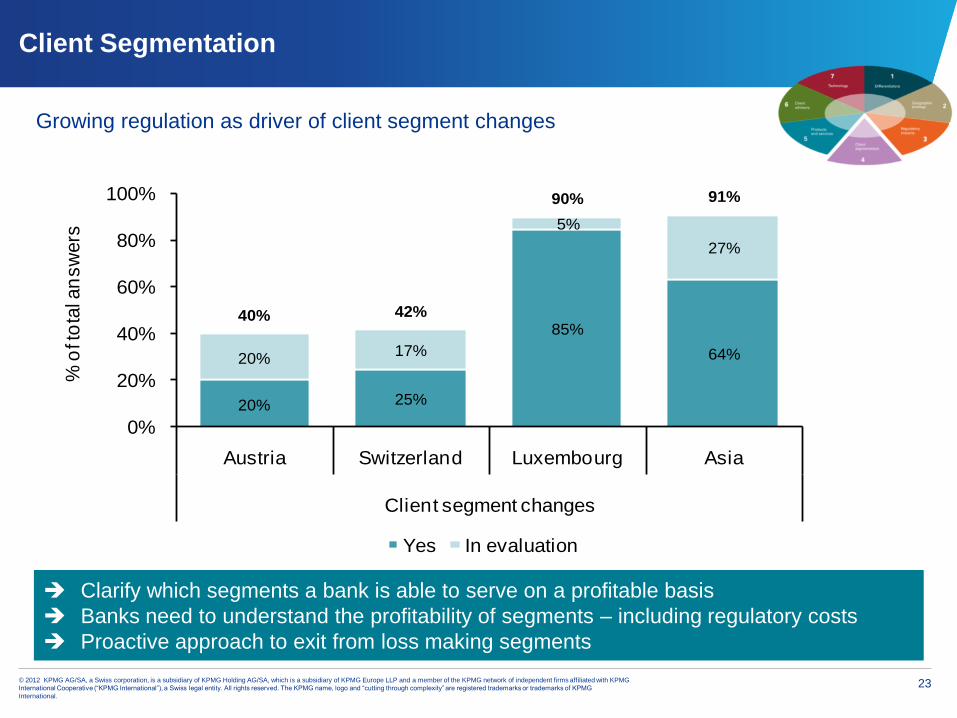

Client Segmentation

20% 25%

85%

64%20%17%

5%

27%

40% 42%

90% 91%

0%

20%

40%

60%

80%

100%

Austria Switzerland Luxembourg Asia

Client segment changes

% o

f to

tal a

nsw

ers

Growing regulation as driver of client segment changes

Yes In evaluation

Growing regulation as driver of client segment changes

Clarify which segments a bank is able to serve on a profitable basis

Banks need to understand the profitability of segments – including regulatory costs

Proactive approach to exit from loss making segments

24© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

Products and Services

Switzerland Luxembourg Austria Asia

Clients’ demands for more services for less money

Significant need to adjust fees?

Clients demand more specific services (including support on tax side). Banks need to

focus offering

25© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

‘Relationship managers

who are client-oriented

and have manager as well

as acquisition skills are

rare on the market'

Switzerland based

Interviewee

Client Advisory

Disillusion of Assets under Management that newly hired CRM can bring

Increased focus on development of CRM

The shortage of skilled client relationship managers

‘Sociologist, economist,

police officer, entrepreneur,

with a minimum of 15 years

of experience'

Switzerland based

Interviewee

26© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

Client Advisory

Ways to interact with clients

Direct interaction

Events

Marketing publications

Philantrophy & charity

Sponsorship

Europe Asia

Direct interaction still dominant way to interact with clients

Direct interaction

Usage of `classical`

information technology

Marketing publications

Events

Social networks &

online fora

Sponsorship

Direct interaction

Usage of `classical`

information technology

Marketing publications

Events

Social networks &

online fora

Sponsorship

High importance High importance Increased importanceIncreased importance

% of total answers % of total answers

0 % 50 % 100 % 0 % 50 % 100 %

27© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

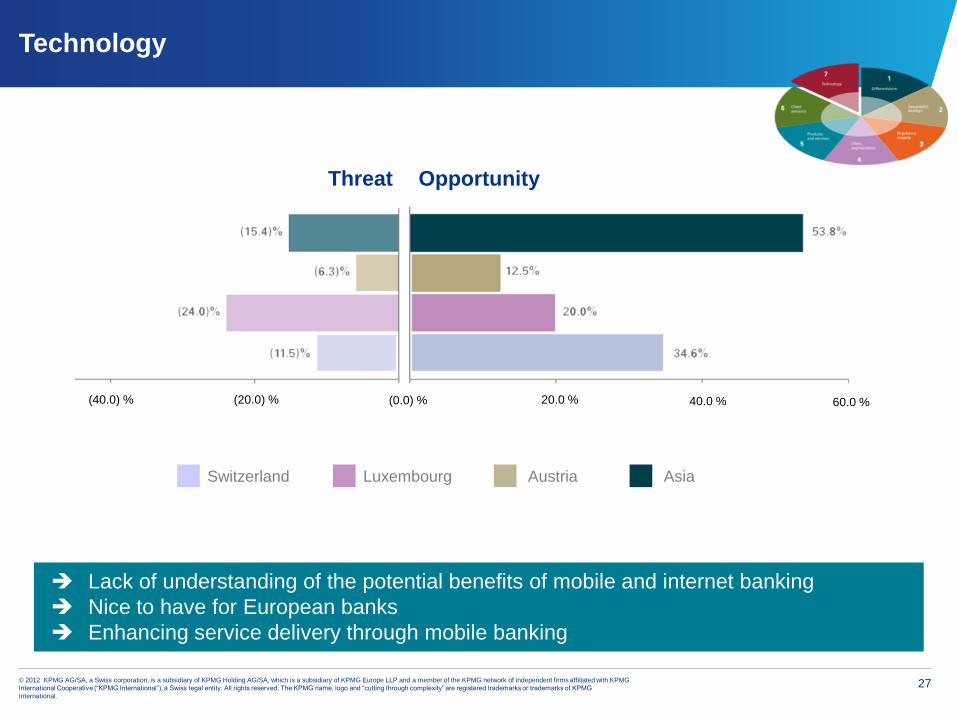

Technology

Lack of understanding of the potential benefits of mobile and internet banking

Nice to have for European banks

Enhancing service delivery through mobile banking

Opportunity

Switzerland Luxembourg Austria Asia

Threat

(0.0) %(20.0) % 20.0 %(40.0) % 40.0 % 60.0 %

Conclusion

Daniel Senn

Head of Financial Services and

Member of the Executive

Committee, KPMG Switzerland

29© 2012 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG

International.

Conclusion

Banks need to...

1. ... have a clear view of their own differentiators

2. ... identify their key geographic markets and define how to service them

3. ... define the path to become fully tax transparent

4. ... understand the performance of their client segments and focus on the profitable ones

5. ... differentiate through products and services for specific target clients’ needs

6. ... invest in CRM’s technical and regulatory skills to meet the client’s individual needs

7. ... understand the potential of enhancing the service delivery through internet and mobile

banking

Questions &

Answers

© 2012 KPMG AG/SA, a Swiss corporation, is a

subsidiary of KPMG Holding AG/SA, which is a

subsidiary of KPMG Europe LLP and a member of

the KPMG network of independent firms affiliated

with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights

reserved. The KPMG name, logo and “cutting

through complexity” are registered trademarks or

trademarks of KPMG International.