ppt project part1

TRANSCRIPT

PART 1

PART 1

Travel Trends Across Indian Sub-Continent

Deepti Kochhar

Pooja Sharma

Agenda

Demand trends in terms of Foreign arrivals

Demand trends in terms of Domestic arrivals

Supply trends

Online and Offline travel market

Key trends

Forecast

On the job learnings

Travel Industry

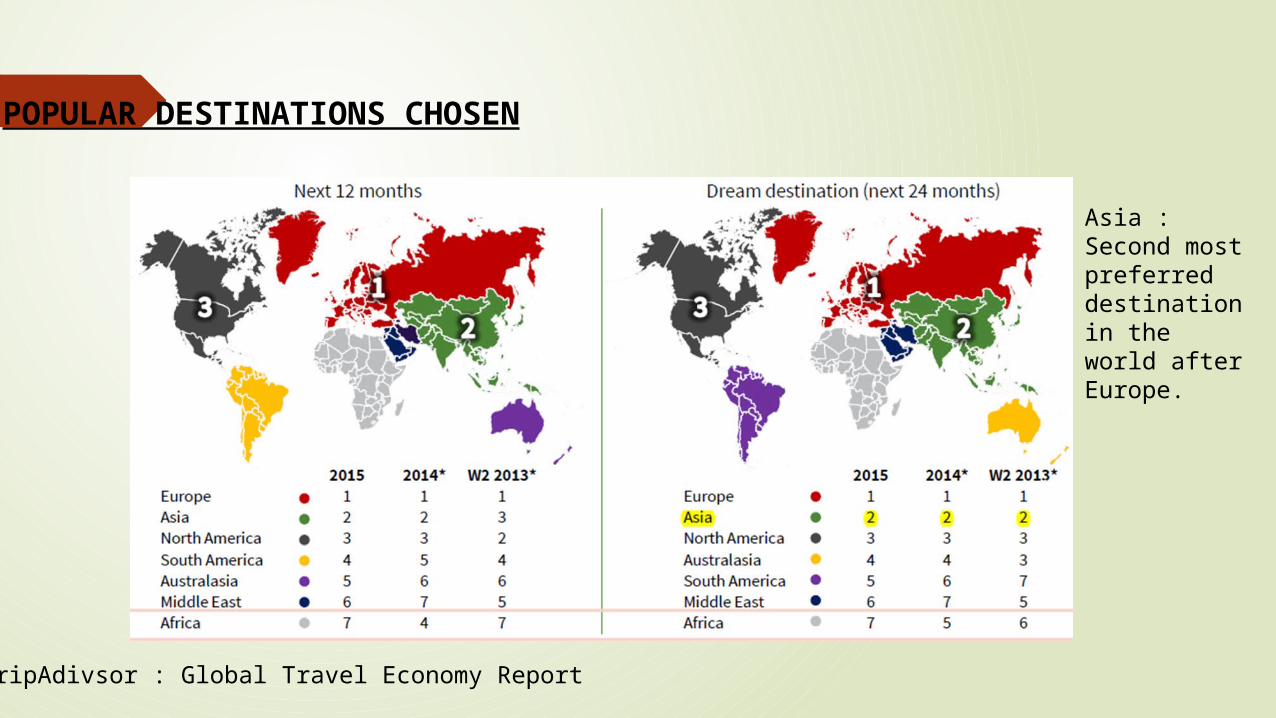

POPULAR DESTINATIONS CHOSEN

TripAdivsor : Global Travel Economy Report

Asia : Second most preferred destination in the world after Europe.

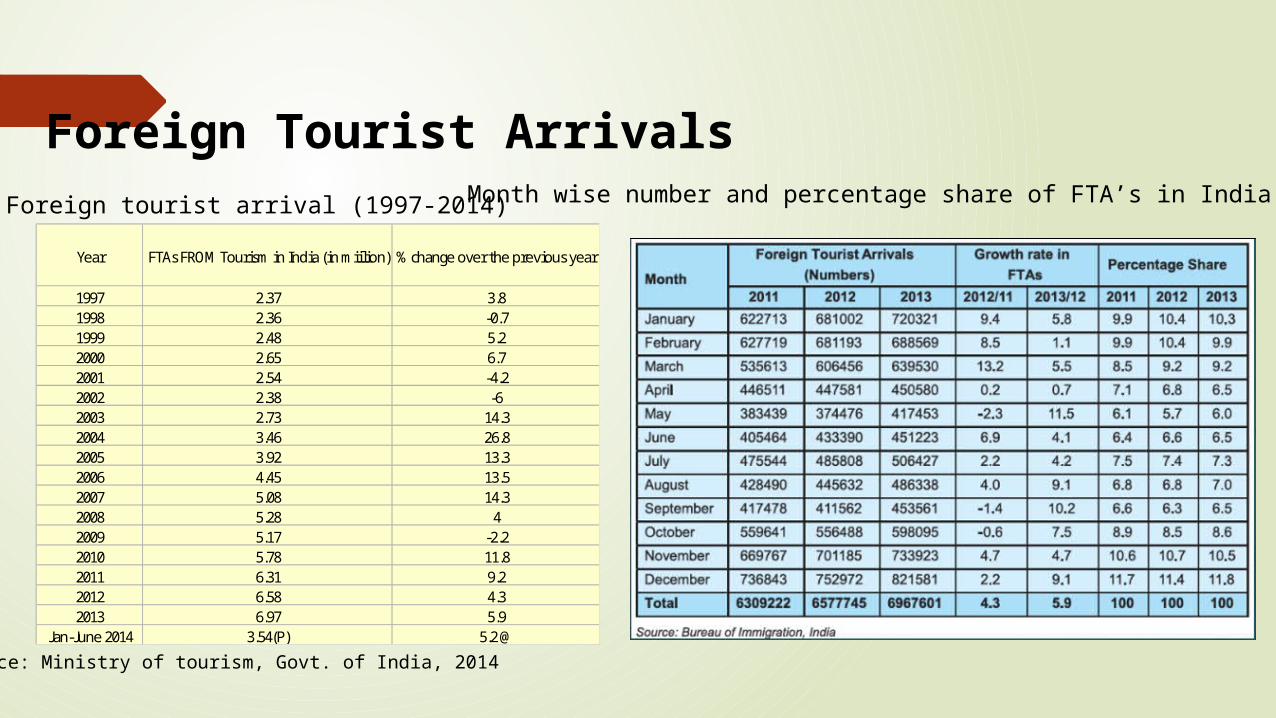

Foreign Tourist Arrivals

Year FTAs FROM Tourism in India (in miilion) % change over the previous year

1997 2.37 3.81998 2.36 -0.71999 2.48 5.22000 2.65 6.72001 2.54 -4.22002 2.38 -62003 2.73 14.32004 3.46 26.82005 3.92 13.32006 4.45 13.52007 5.08 14.32008 5.28 42009 5.17 -2.22010 5.78 11.82011 6.31 9.22012 6.58 4.32013 6.97 5.9

Jan-June 2014 3.54(P) 5.2 @

Foreign tourist arrival (1997-2014)

Source: Ministry of tourism, Govt. of India, 2014

Month wise number and percentage share of FTA’s in India

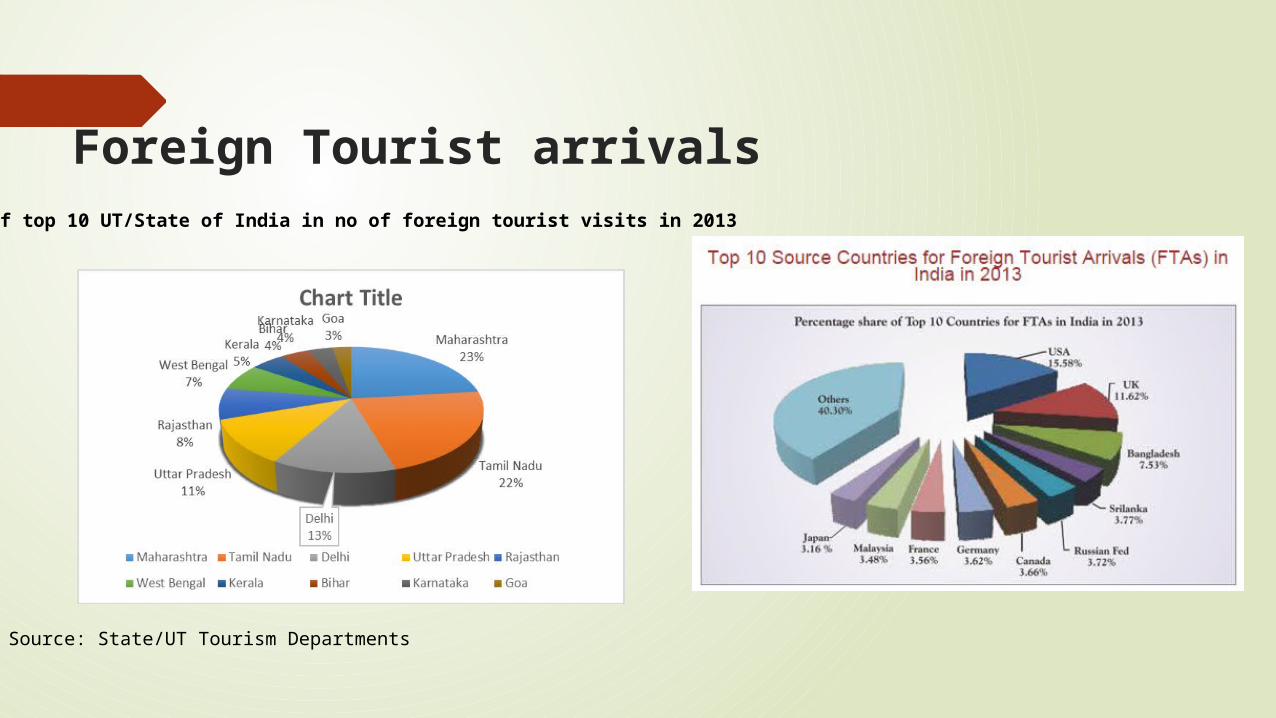

Foreign Tourist arrivals Share of top 10 UT/State of India in no of foreign tourist visits in 2013

Source: State/UT Tourism Departments

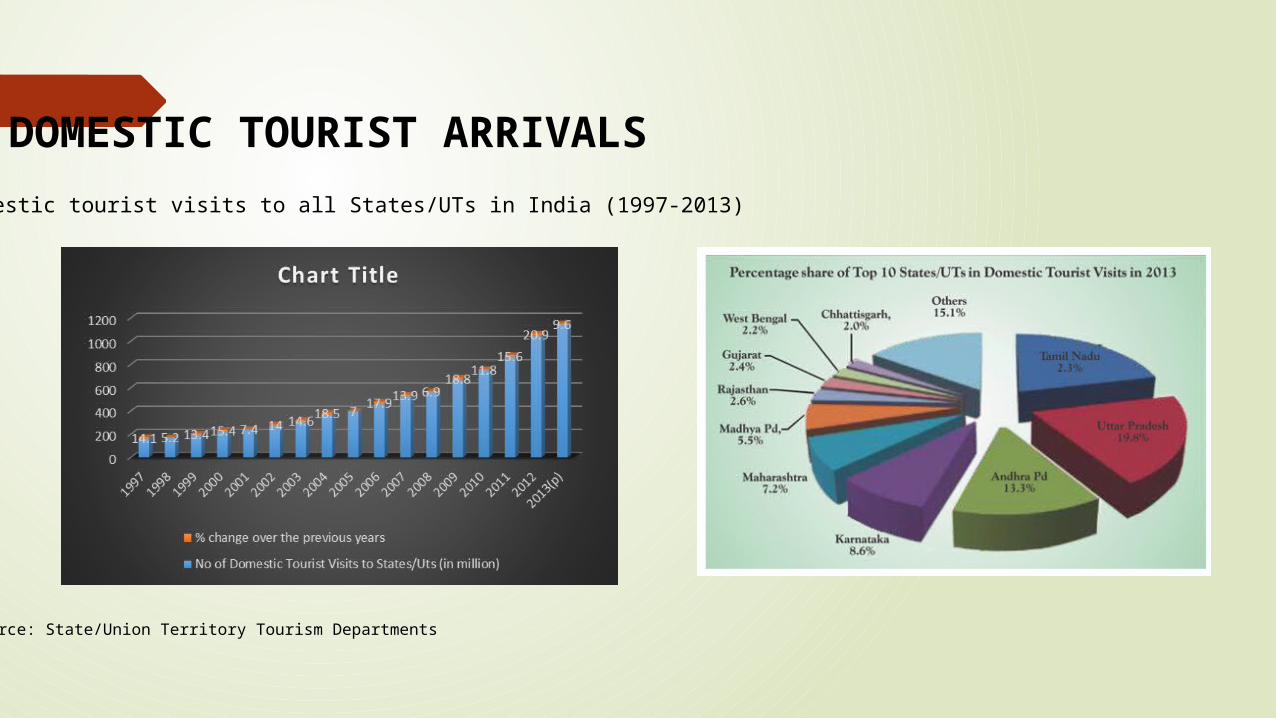

DOMESTIC TOURIST ARRIVALS

No of domestic tourist visits to all States/UTs in India (1997-2013)

Source: State/Union Territory Tourism Departments

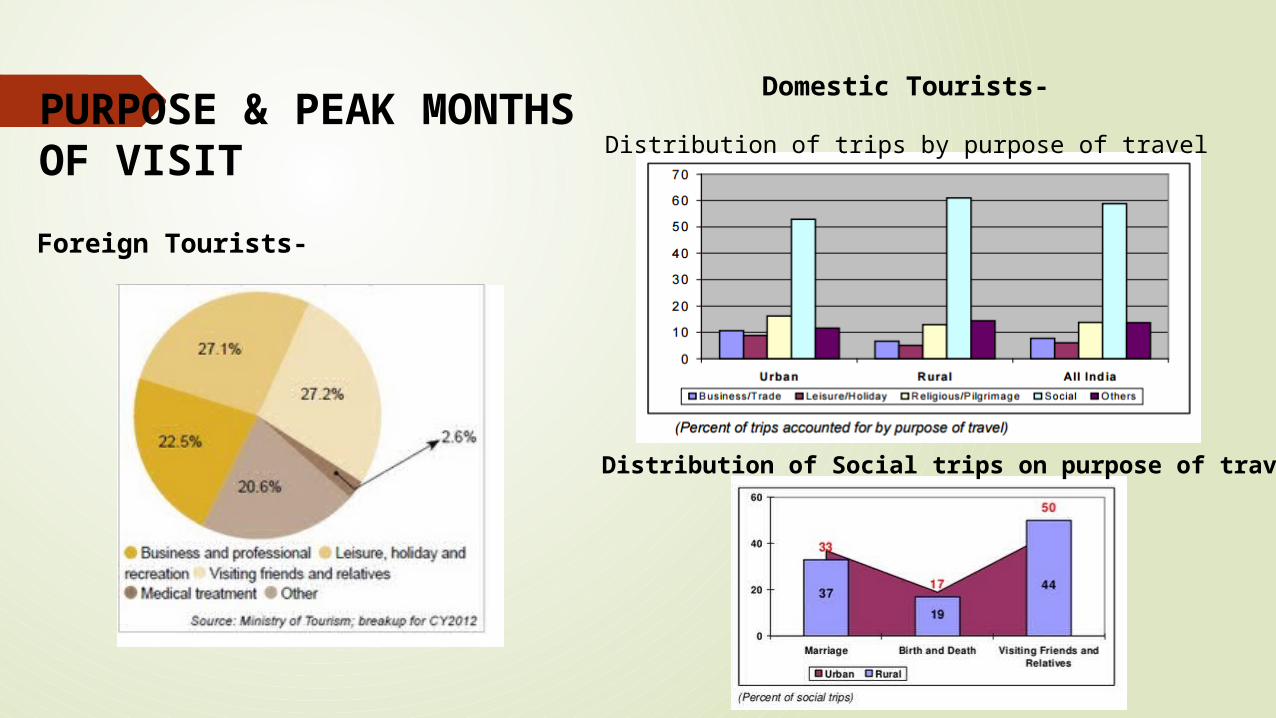

PURPOSE & PEAK MONTHS OF VISIT

Foreign Tourists-

Domestic Tourists-

Distribution of Social trips on purpose of travel

Distribution of trips by purpose of travel

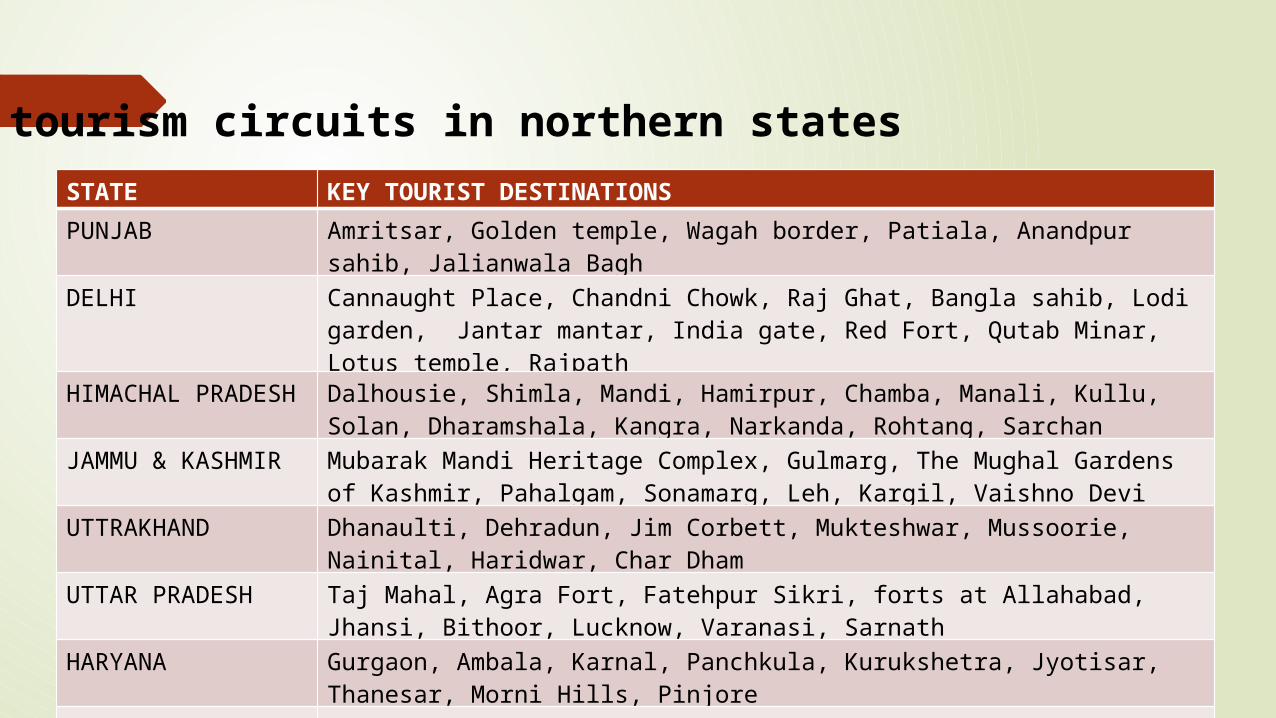

Key tourism circuits in northern statesSTATE KEY TOURIST DESTINATIONS

PUNJAB Amritsar, Golden temple, Wagah border, Patiala, Anandpur sahib, Jalianwala Bagh

DELHI Cannaught Place, Chandni Chowk, Raj Ghat, Bangla sahib, Lodi garden, Jantar mantar, India gate, Red Fort, Qutab Minar, Lotus temple, Rajpath

HIMACHAL PRADESH

Dalhousie, Shimla, Mandi, Hamirpur, Chamba, Manali, Kullu, Solan, Dharamshala, Kangra, Narkanda, Rohtang, Sarchan

JAMMU & KASHMIR Mubarak Mandi Heritage Complex, Gulmarg, The Mughal Gardens of Kashmir, Pahalgam, Sonamarg, Leh, Kargil, Vaishno Devi

UTTRAKHAND Dhanaulti, Dehradun, Jim Corbett, Mukteshwar, Mussoorie, Nainital, Haridwar, Char Dham

UTTAR PRADESH Taj Mahal, Agra Fort, Fatehpur Sikri, forts at Allahabad, Jhansi, Bithoor, Lucknow, Varanasi, Sarnath

HARYANA Gurgaon, Ambala, Karnal, Panchkula, Kurukshetra, Jyotisar, Thanesar, Morni Hills, Pinjore

RAJASTHAN Alwar, Dargah Sharif-tomb of the Sufi saint Khwaja Moinuddin Chisti at Ajmer Palaces and forts at Bundi, Diwan-e-aam, Hathia Pol, and Naubat Khana at Bundi, Bikaner, Jaisalmer fort, Jodhpur, Mount Abu, Ranthambor National Park, Udaipur, Jaipur

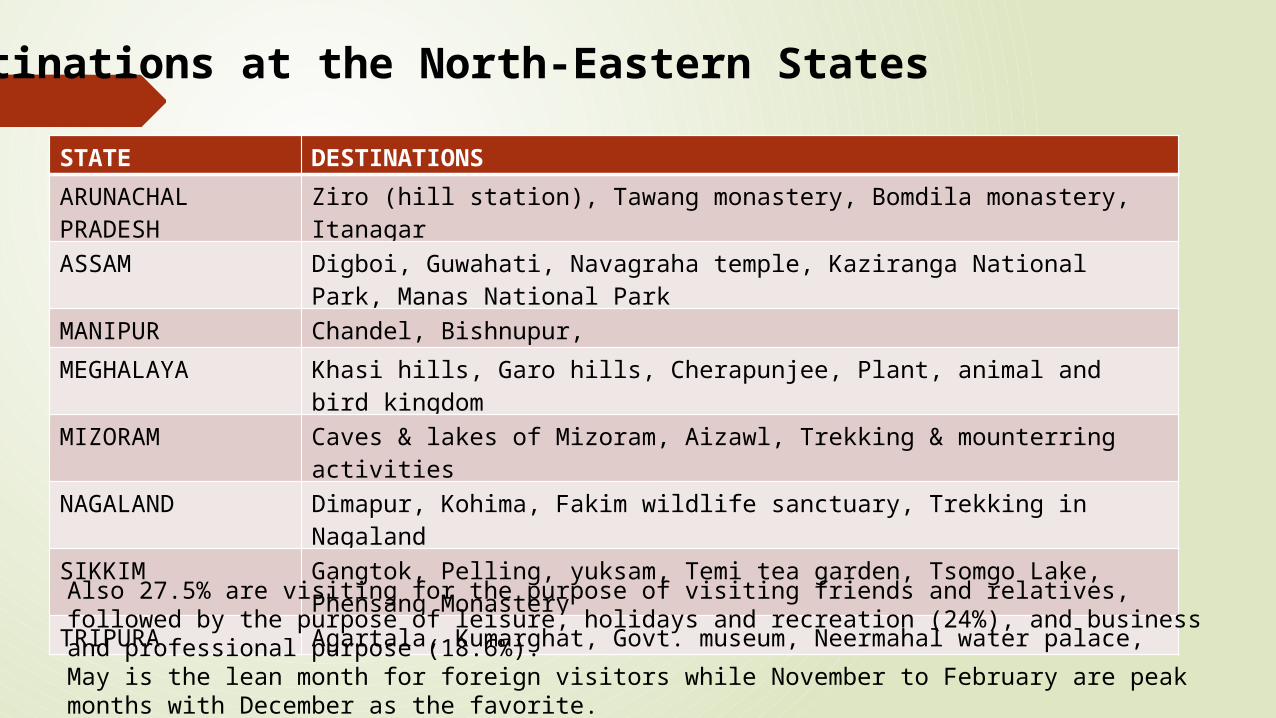

Destinations at the North-Eastern States

STATE DESTINATIONS

ARUNACHAL PRADESH

Ziro (hill station), Tawang monastery, Bomdila monastery, Itanagar

ASSAM Digboi, Guwahati, Navagraha temple, Kaziranga National Park, Manas National Park

MANIPUR Chandel, Bishnupur,

MEGHALAYA Khasi hills, Garo hills, Cherapunjee, Plant, animal and bird kingdom

MIZORAM Caves & lakes of Mizoram, Aizawl, Trekking & mounterring activities

NAGALAND Dimapur, Kohima, Fakim wildlife sanctuary, Trekking in Nagaland

SIKKIM Gangtok, Pelling, yuksam, Temi tea garden, Tsomgo Lake, Phensang Monastery

TRIPURA Agartala, Kumarghat, Govt. museum, Neermahal water palace,

Also 27.5% are visiting for the purpose of visiting friends and relatives, followed by the purpose of leisure, holidays and recreation (24%), and business and professional purpose (18.6%).May is the lean month for foreign visitors while November to February are peak months with December as the favorite.

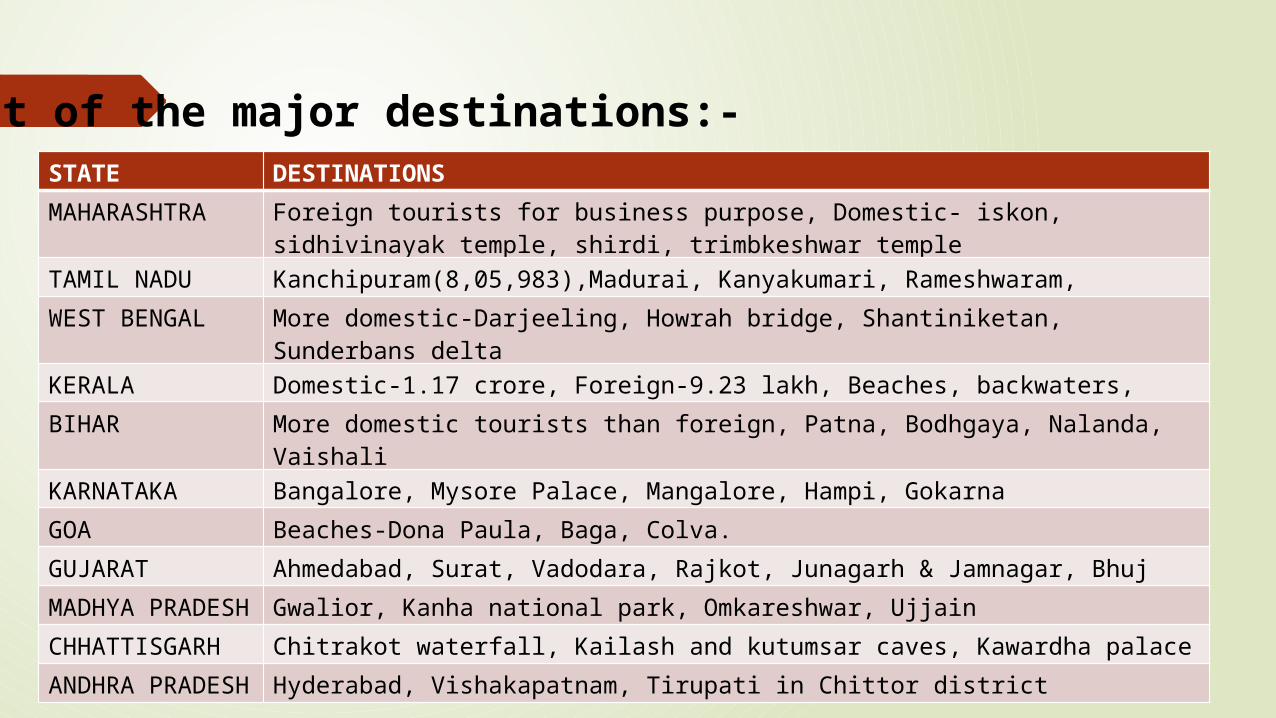

Rest of the major destinations:-STATE DESTINATIONS

MAHARASHTRA Foreign tourists for business purpose, Domestic- iskon, sidhivinayak temple, shirdi, trimbkeshwar temple

TAMIL NADU Kanchipuram(8,05,983),Madurai, Kanyakumari, Rameshwaram,

WEST BENGAL More domestic-Darjeeling, Howrah bridge, Shantiniketan, Sunderbans delta

KERALA Domestic-1.17 crore, Foreign-9.23 lakh, Beaches, backwaters,

BIHAR More domestic tourists than foreign, Patna, Bodhgaya, Nalanda, Vaishali

KARNATAKA Bangalore, Mysore Palace, Mangalore, Hampi, Gokarna

GOA Beaches-Dona Paula, Baga, Colva.

GUJARAT Ahmedabad, Surat, Vadodara, Rajkot, Junagarh & Jamnagar, Bhuj

MADHYA PRADESH

Gwalior, Kanha national park, Omkareshwar, Ujjain

CHHATTISGARH Chitrakot waterfall, Kailash and kutumsar caves, Kawardha palace

ANDHRA PRADESH

Hyderabad, Vishakapatnam, Tirupati in Chittor district

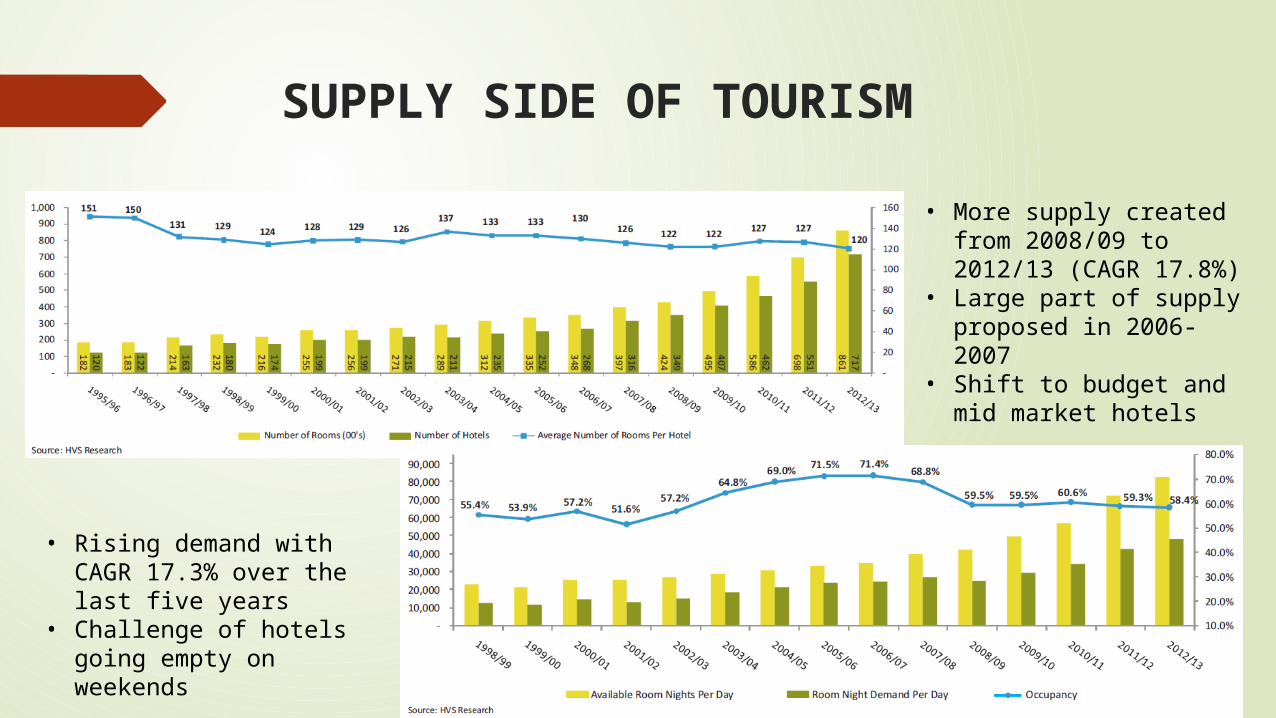

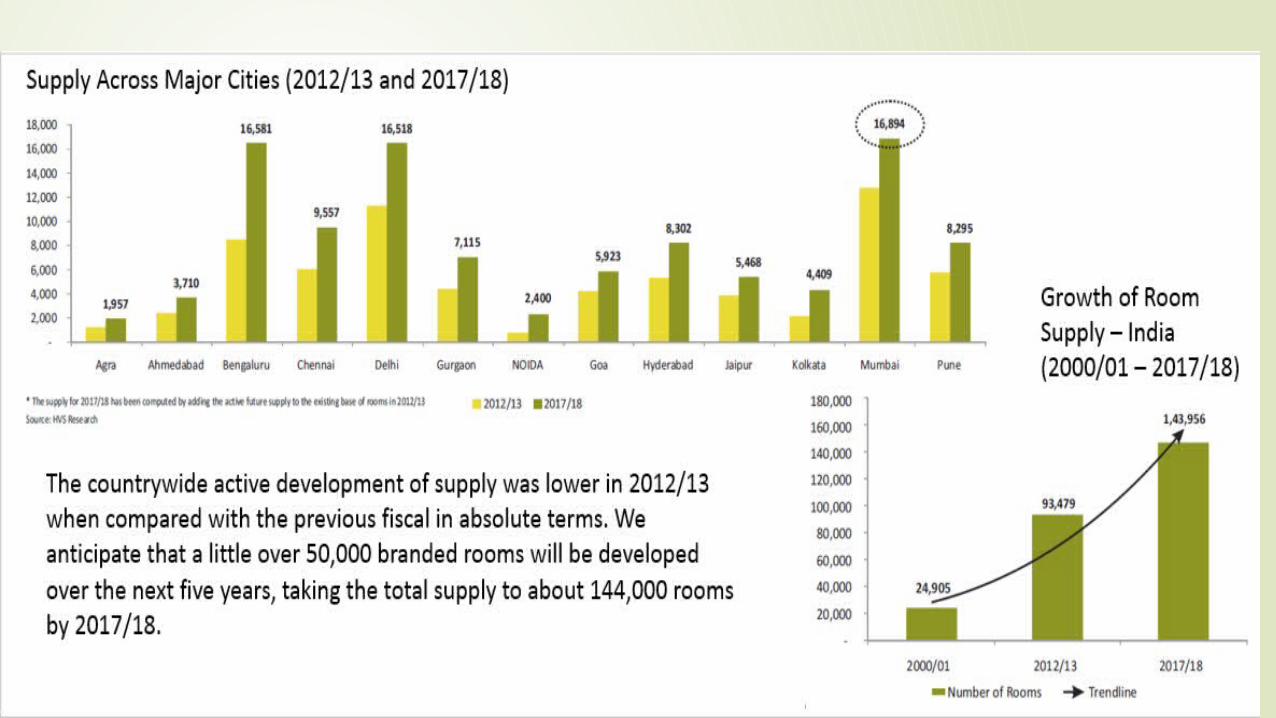

SUPPLY SIDE OF TOURISM

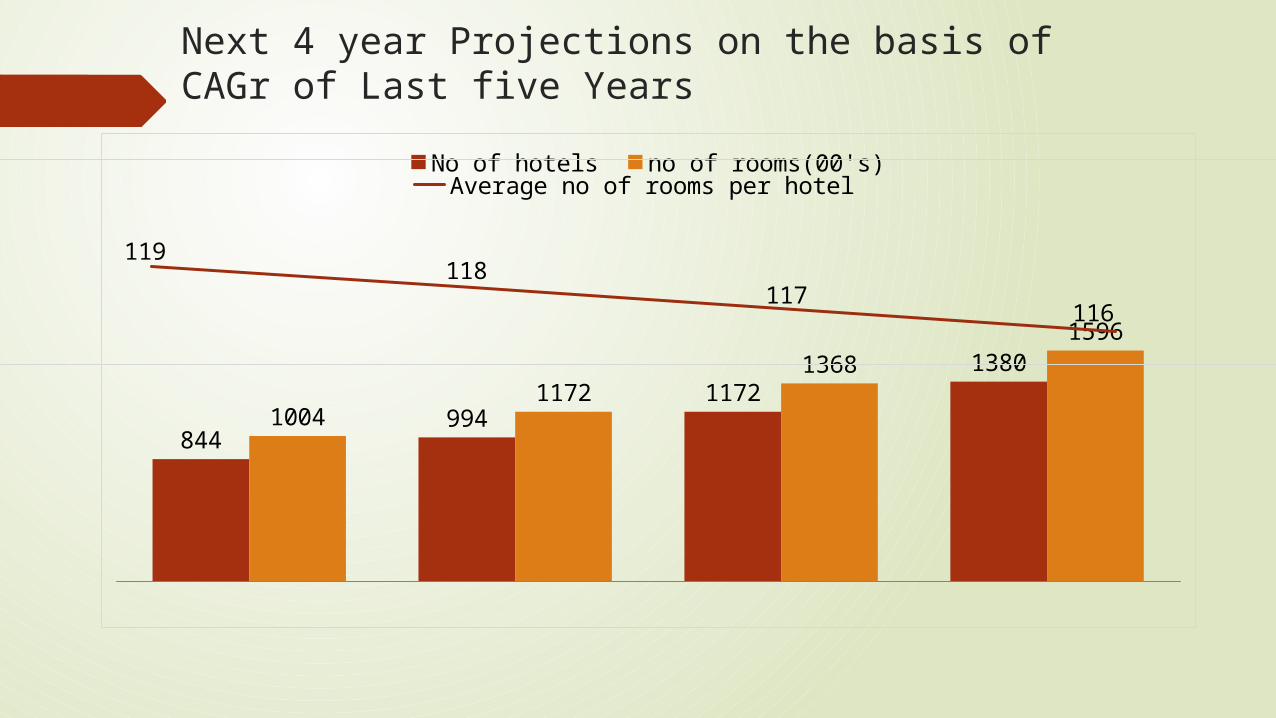

• More supply created from 2008/09 to 2012/13 (CAGR 17.8%)

• Large part of supply proposed in 2006-2007

• Shift to budget and mid market hotels

• Rising demand with CAGR 17.3% over the last five years

• Challenge of hotels going empty on weekends

2014 2015 2016 2017

844994

11721380

10041172

13681596

No of hotels no of rooms(00's)

119118

117116

Average no of rooms per hotel

Next 4 year Projections on the basis of CAGr of Last five Years

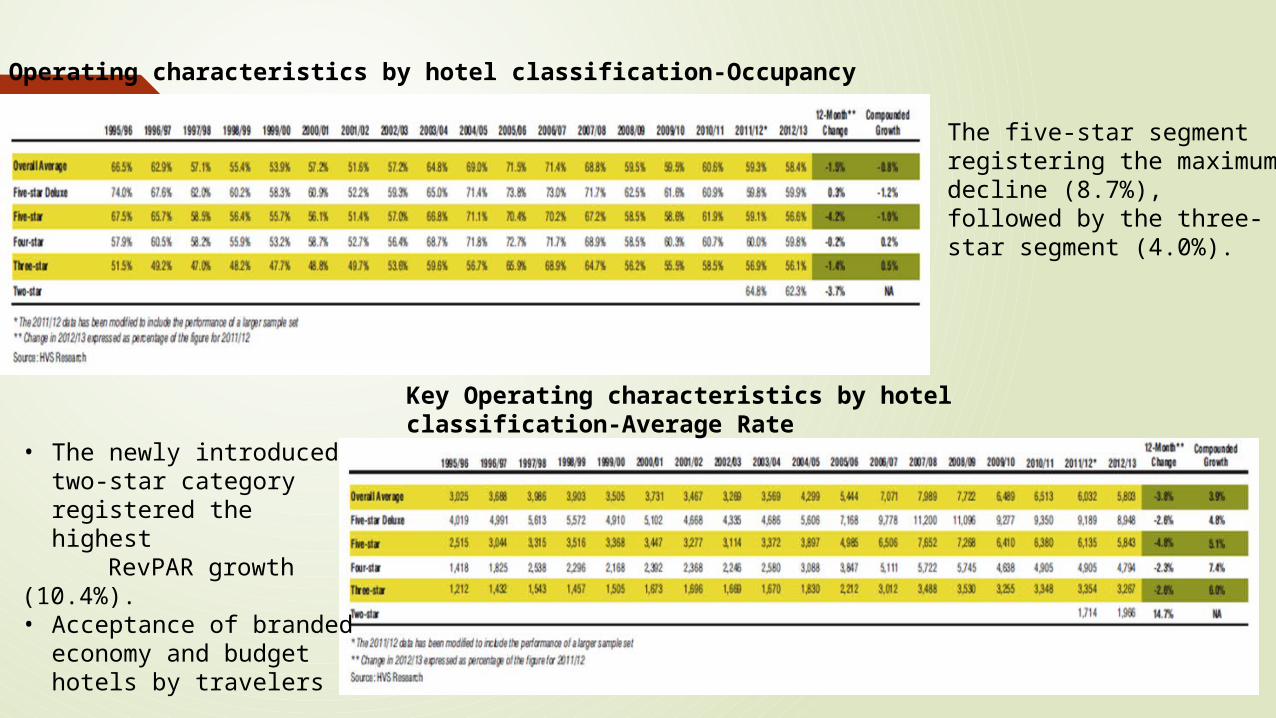

Key Operating characteristics by hotel classification-Occupancy

Key Operating characteristics by hotel classification-Average Rate

The five-star segment registering the maximum decline (8.7%), followed by the three-star segment (4.0%).

• The newly introduced two-star category registered the highest

RevPAR growth (10.4%).• Acceptance of branded

economy and budget hotels by travelers

FUTURE GROWTH-TRAVEL INDUSTRY

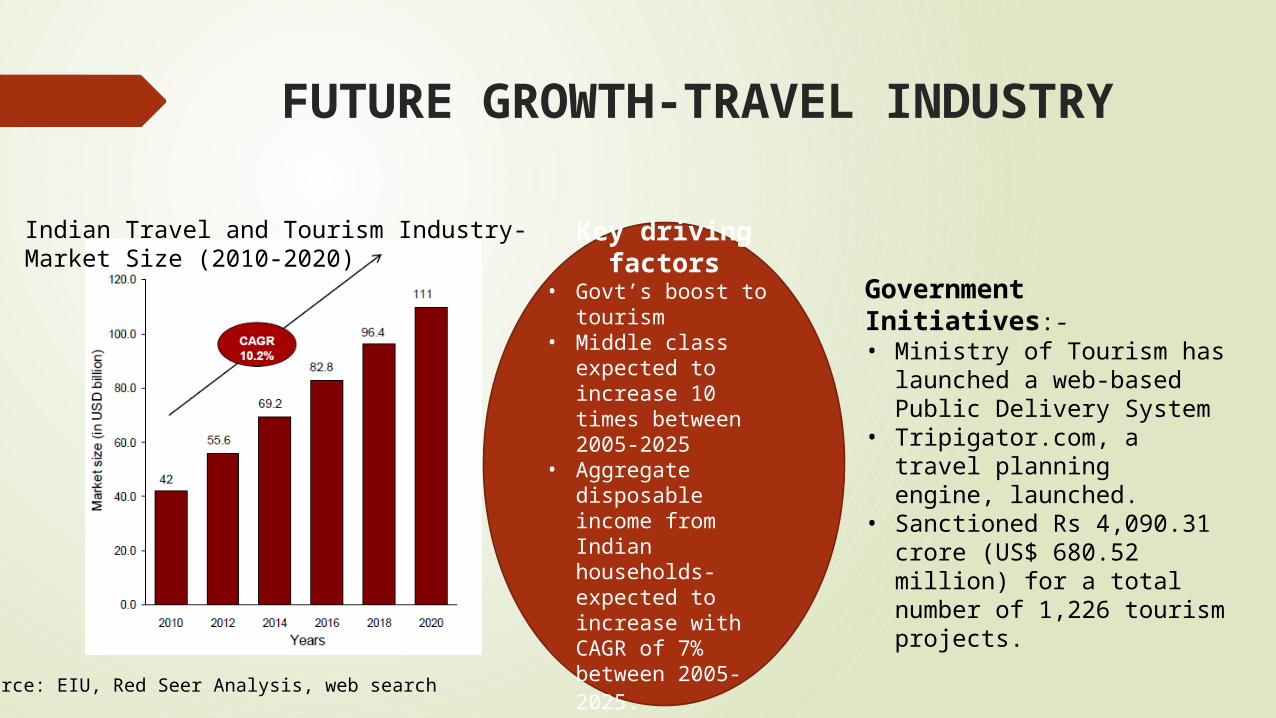

Indian Travel and Tourism Industry- Market Size (2010-2020)

Source: EIU, Red Seer Analysis, web search

Government Initiatives:-• Ministry of Tourism has

launched a web-based Public Delivery System

• Tripigator.com, a travel planning engine, launched.

• Sanctioned Rs 4,090.31 crore (US$ 680.52 million) for a total number of 1,226 tourism projects.

Key driving factors

• Govt’s boost to tourism

• Middle class expected to increase 10 times between 2005-2025

• Aggregate disposable income from Indian households-expected to increase with CAGR of 7% between 2005-2025.

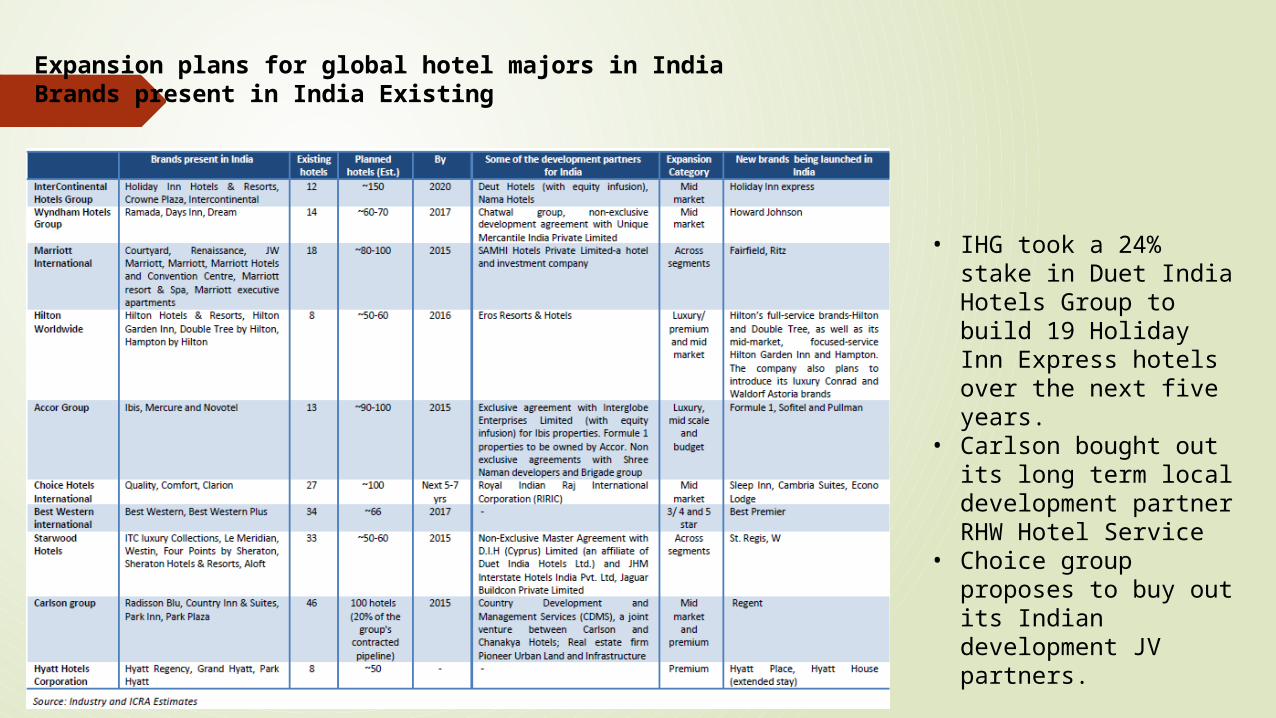

Expansion plans for global hotel majors in India Brands present in India Existing

• IHG took a 24% stake in Duet India Hotels Group to build 19 Holiday Inn Express hotels over the next five years.

• Carlson bought out its long term local development partner RHW Hotel Service

• Choice group proposes to buy out its Indian development JV partners.

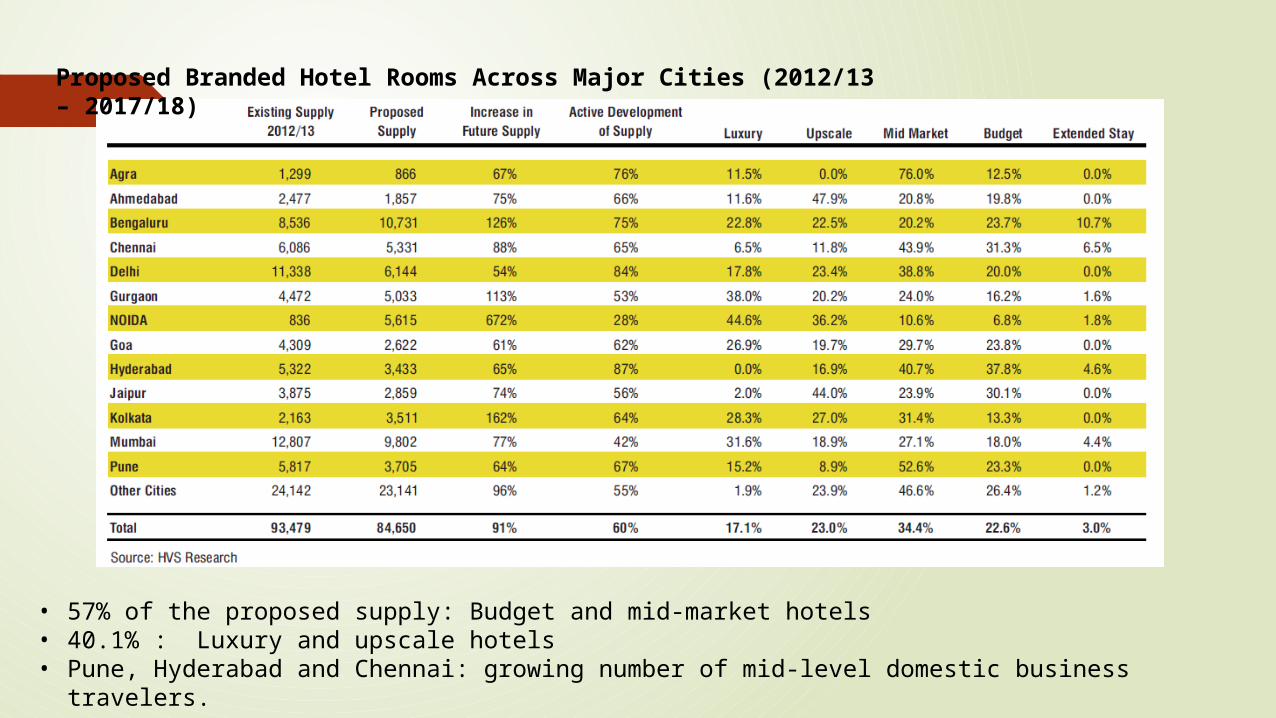

Proposed Branded Hotel Rooms Across Major Cities (2012/13 – 2017/18)

• 57% of the proposed supply: Budget and mid-market hotels • 40.1% : Luxury and upscale hotels• Pune, Hyderabad and Chennai: growing number of mid-level domestic business travelers.

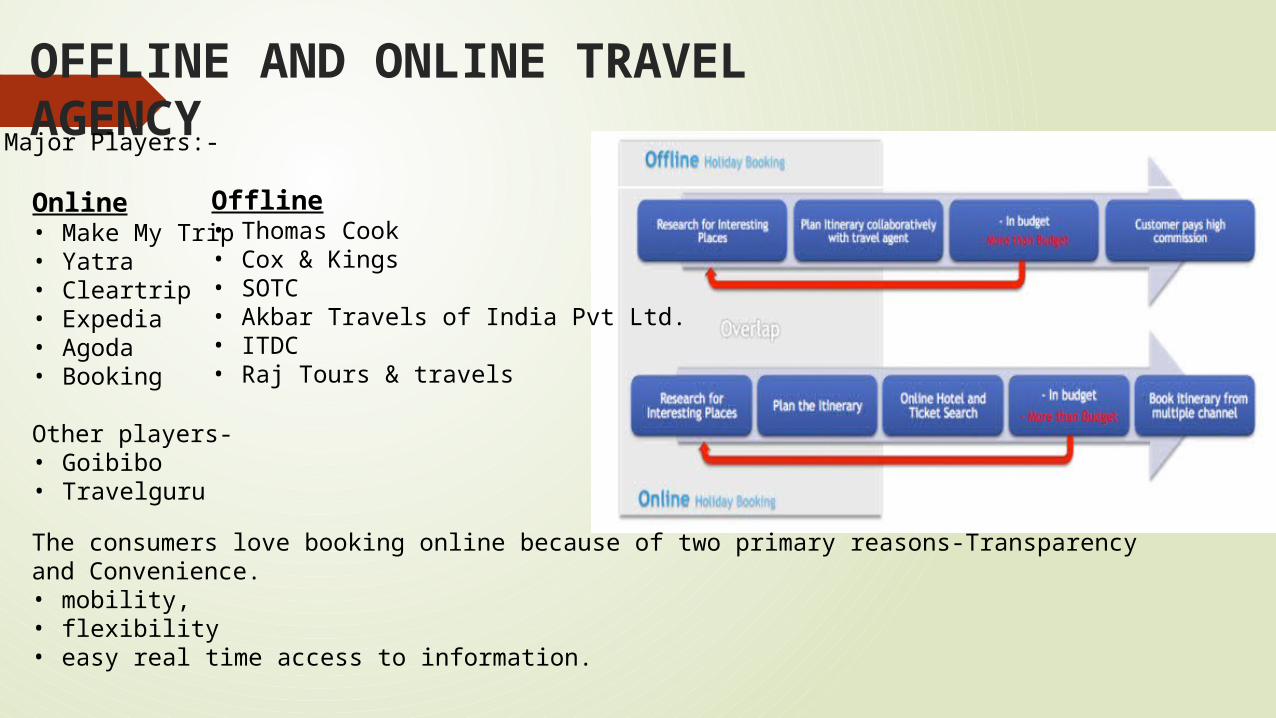

OFFLINE AND ONLINE TRAVEL AGENCYMajor Players:-

Online• Make My Trip• Yatra• Cleartrip• Expedia• Agoda• Booking

Other players-• Goibibo• Travelguru

Offline• Thomas Cook• Cox & Kings• SOTC• Akbar Travels of India Pvt Ltd.• ITDC• Raj Tours & travels

The consumers love booking online because of two primary reasons-Transparency and Convenience.• mobility, • flexibility • easy real time access to information.

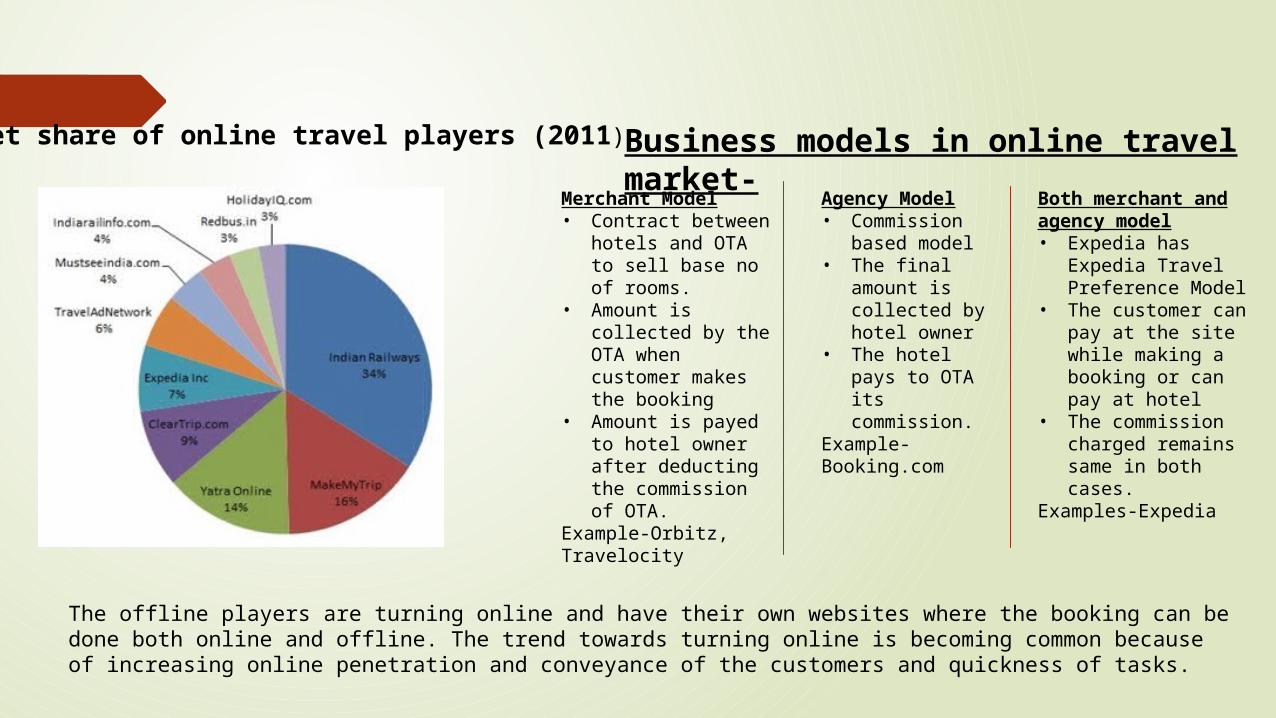

Market share of online travel players (2011) Business models in online travel market-

The offline players are turning online and have their own websites where the booking can be done both online and offline. The trend towards turning online is becoming common because of increasing online penetration and conveyance of the customers and quickness of tasks.

Merchant Model• Contract between

hotels and OTA to sell base no of rooms.

• Amount is collected by the OTA when customer makes the booking

• Amount is payed to hotel owner after deducting the commission of OTA.

Example-Orbitz, Travelocity

Agency Model• Commission

based model• The final

amount is collected by hotel owner

• The hotel pays to OTA its commission.

Example-Booking.com

Both merchant and agency model• Expedia has

Expedia Travel Preference Model

• The customer can pay at the site while making a booking or can pay at hotel

• The commission charged remains same in both cases.

Examples-Expedia

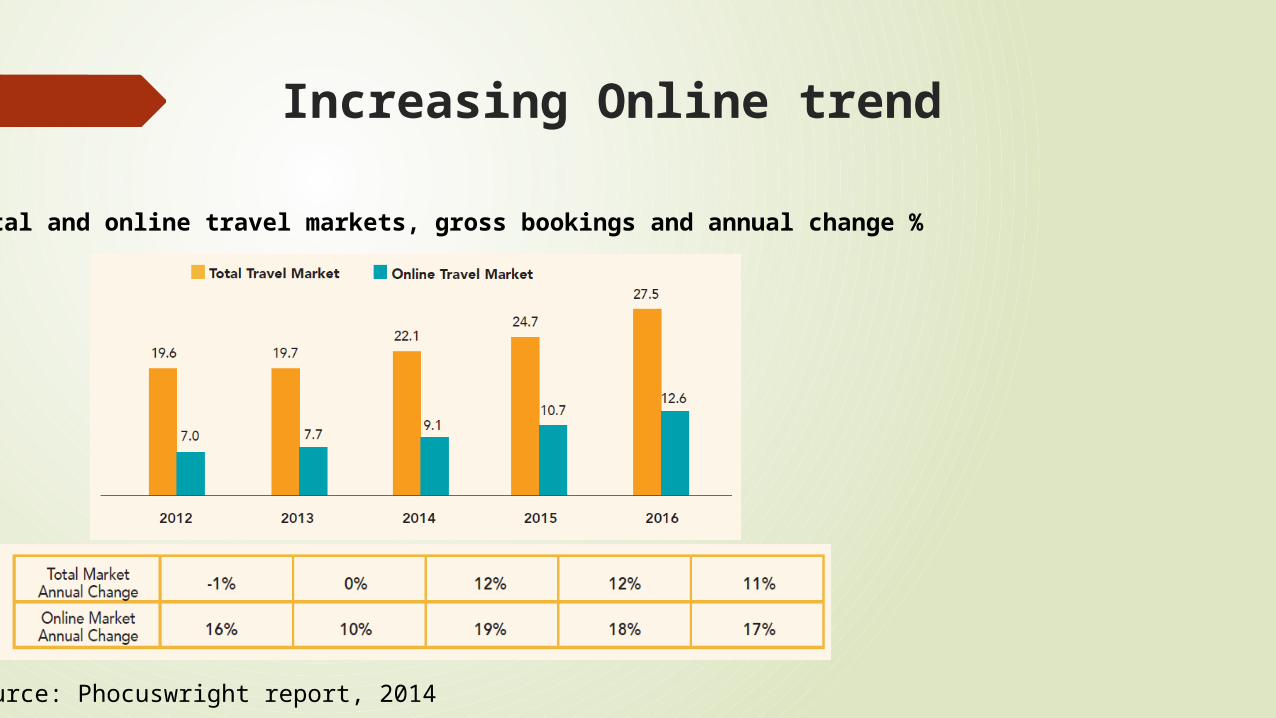

Increasing Online trend

India total and online travel markets, gross bookings and annual change %

Source: Phocuswright report, 2014

India online travel market, penetration by segment, 2013 vs 2016

Indian Online Travel Market, Annual Change by Online Channel, 2012-16

• Online air gross bookings will exceed $16.9 billion in 2016.

• Online gross bookings for the rail segment rose 13% to reach $2.6 billion in 2013.

• Online car rental bookings were $68 million in 2013 and will swell to $106 million by 2016.

• Online hotel gross bookings will increase more than 23% annually through 2016

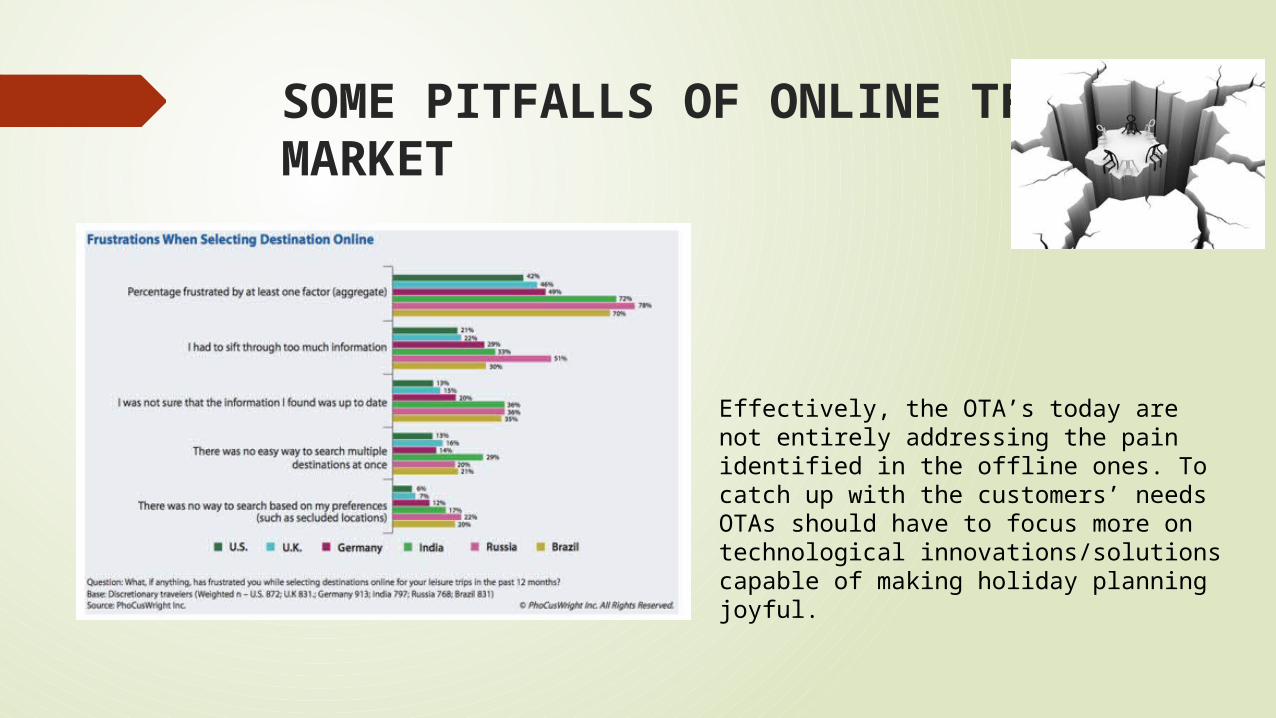

SOME PITFALLS OF ONLINE TRAVEL MARKET

Effectively, the OTA’s today are not entirely addressing the pain identified in the offline ones. To catch up with the customers’ needs OTAs should have to focus more on technological innovations/solutions capable of making holiday planning joyful.

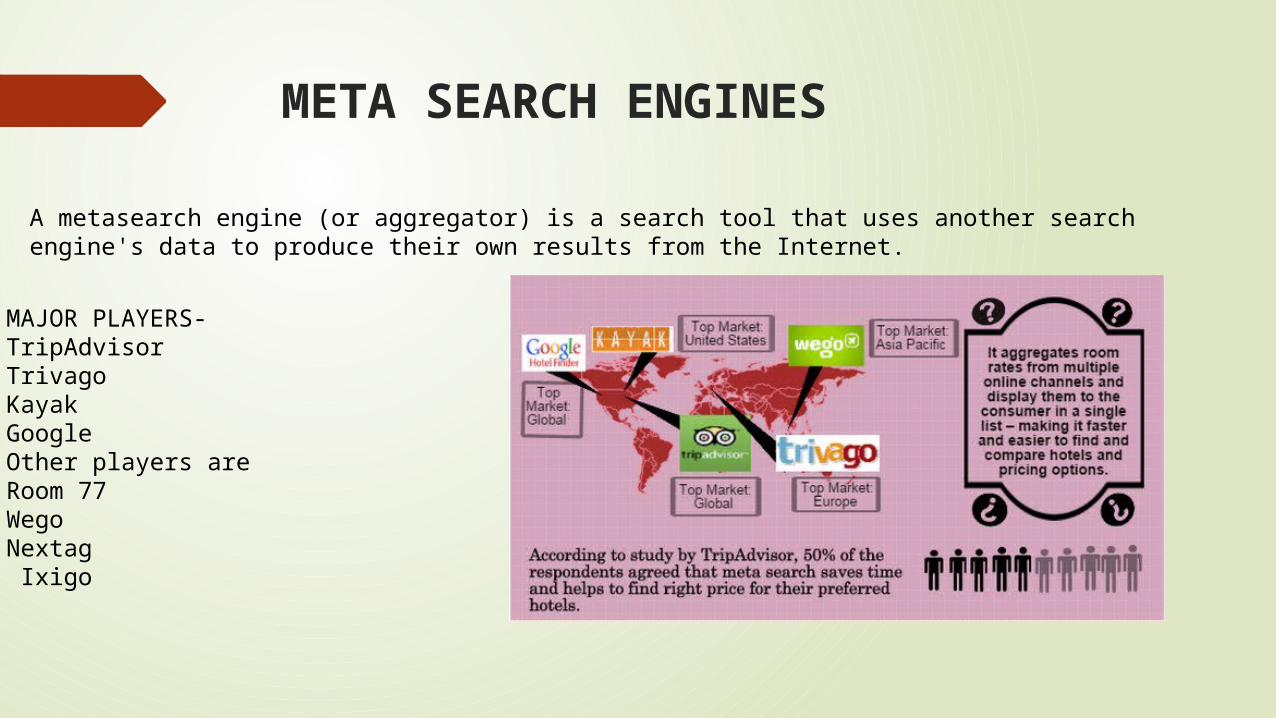

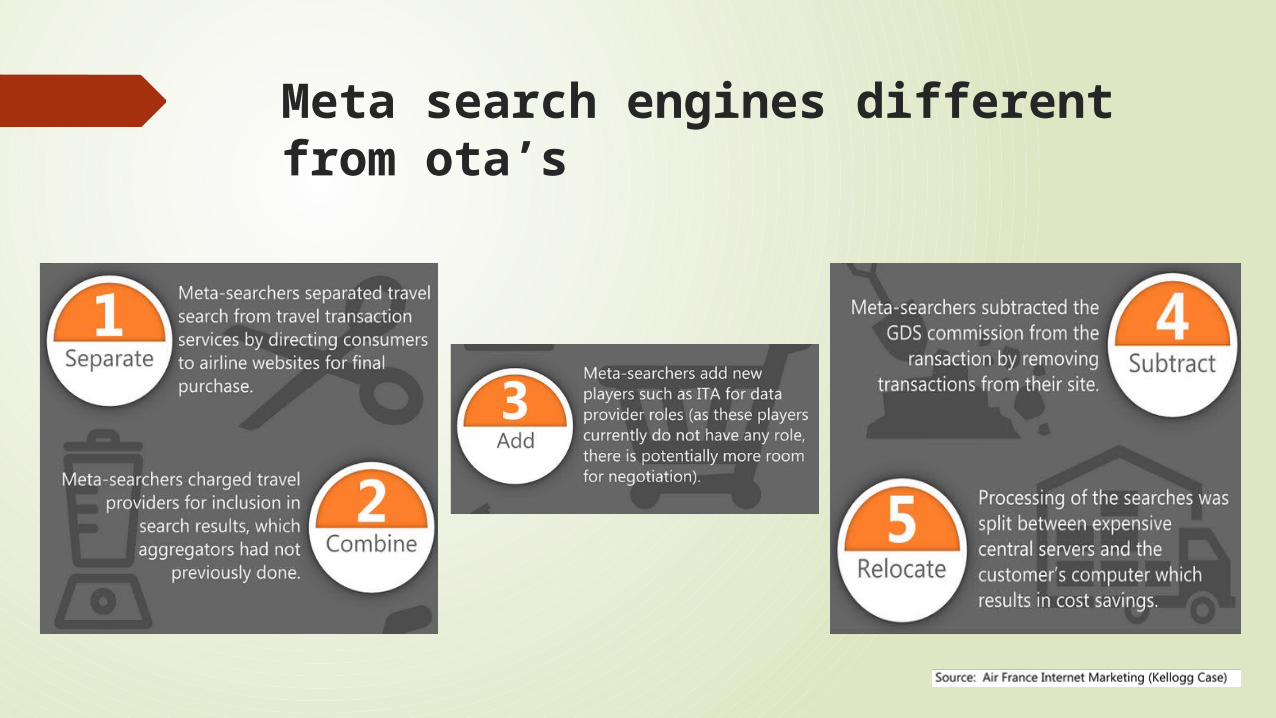

META SEARCH ENGINES

A metasearch engine (or aggregator) is a search tool that uses another search engine's data to produce their own results from the Internet.

MAJOR PLAYERS-TripAdvisorTrivagoKayakGoogleOther players areRoom 77WegoNextag Ixigo

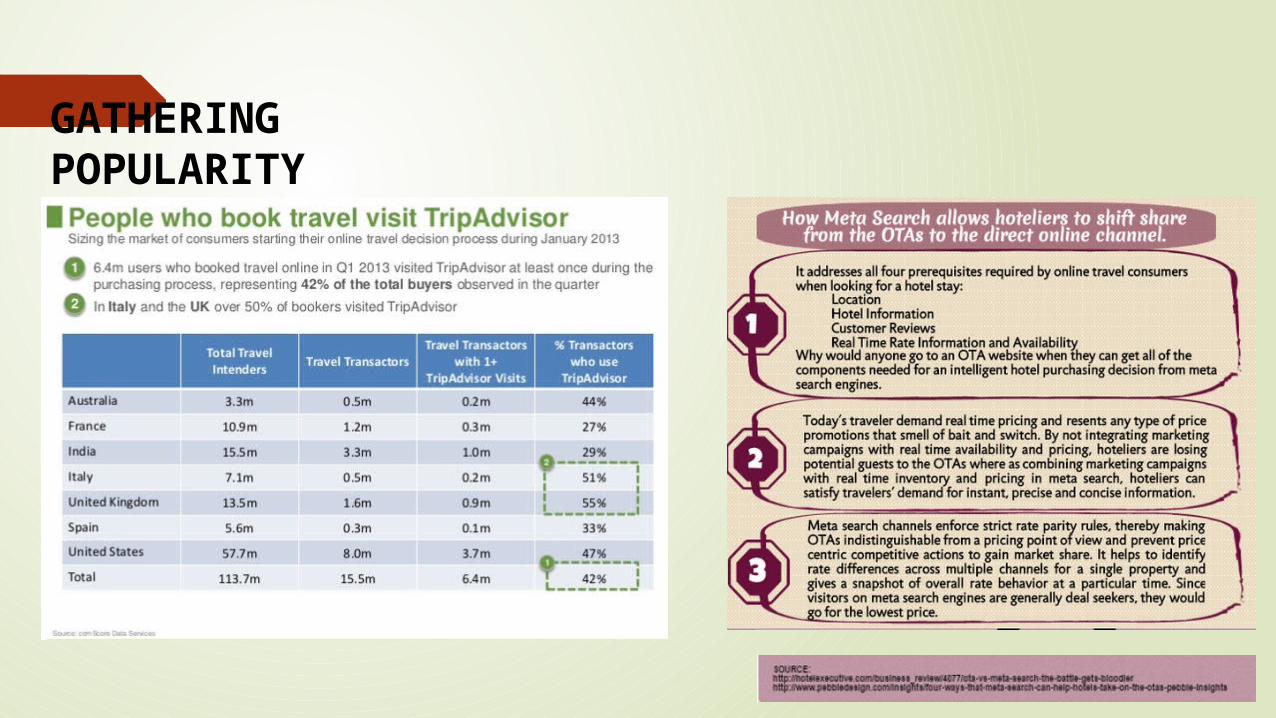

GATHERING POPULARITY

Meta search engines different from ota’s

Mobile applications

Mobile creates opportunity for in-trip touch points

Source: Flight view survey-June 2014

• Connect with your clients at the time and place they plan their trip

• Increased brand visibility-fully branded mobile app, deep Facebook integration.

• Perfect travel companion for clients-Detailed guides, offline maps and navigation, Daily itineraries.

Source: mtrip.com

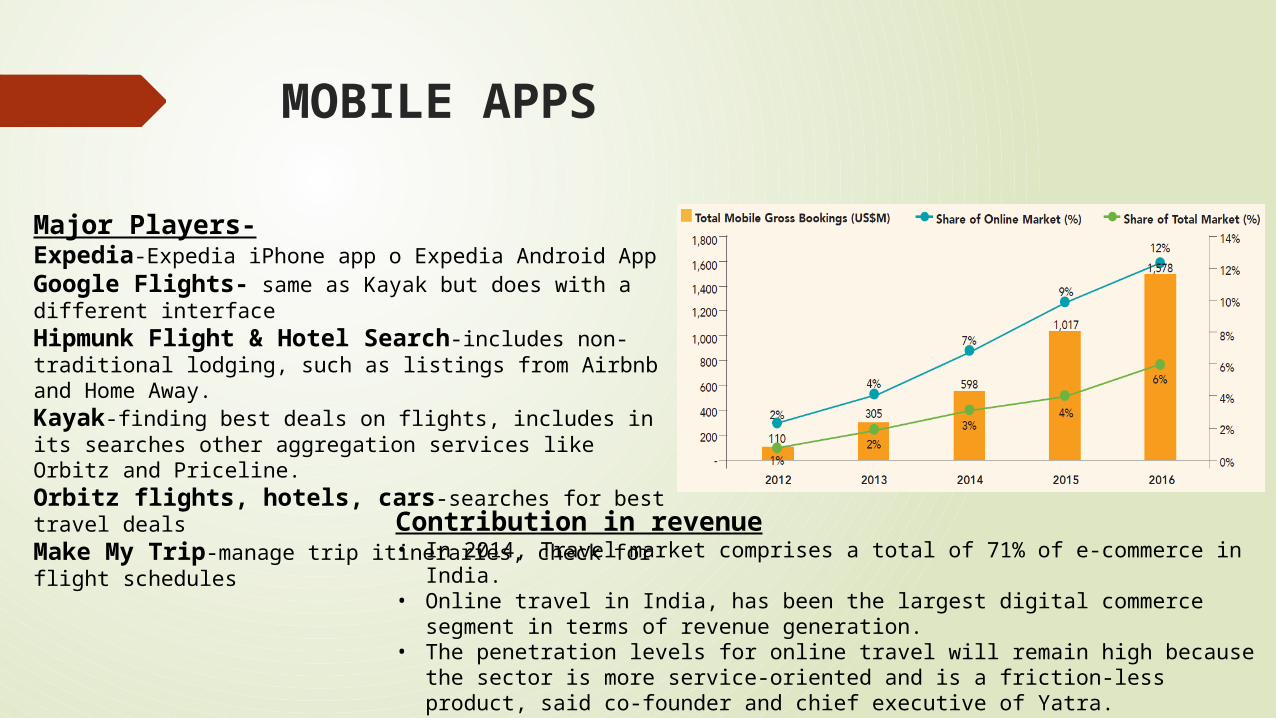

MOBILE APPS

Major Players-Expedia-Expedia iPhone app o Expedia Android AppGoogle Flights- same as Kayak but does with a different interfaceHipmunk Flight & Hotel Search-includes non-traditional lodging, such as listings from Airbnb and Home Away. Kayak-finding best deals on flights, includes in its searches other aggregation services like Orbitz and Priceline.Orbitz flights, hotels, cars-searches for best travel dealsMake My Trip-manage trip itineraries, check for flight schedules

Contribution in revenue• In 2014, Travel market comprises a total of 71% of e-commerce in India.• Online travel in India, has been the largest digital commerce segment in terms

of revenue generation.• The penetration levels for online travel will remain high because the sector is

more service-oriented and is a friction-less product, said co-founder and chief executive of Yatra.

OTHER NEW TRENDS

MEDICAL TOURISMThe citizens of countries that visit India for Medical purposes are mainly from Maldives (59% of 50,000 visitors), Nigeria (29% of 37000 visitors), Iraq (33% of 39000 visitors), Afghanistan (16% of 95000 visitors), Oman (11% of 50000 visitors), UAE (8% of 41000 visitors).

SPIRITUAL TOURISM

Some Government Initiatives

• ‘Spiritual Tourism’ programme.• Launching of E-Ticketing for Taj Mahal in Agra and

Humayun's Tomb in New Delhi • 500 crores embarked by P.M. for development of five

tourist circuits such as Ganga, Krishna, Buddha, northeast and Kerala.

• 100 crores earmarked for Pilgrimage Rejuvenation and Spirituality Augmentation Drive.

MICE TOURISM(M)Meetings-corporate conferences(I)Incentive(Travel)-reward or training to employees by companies(C)Convention-general assemblies, academic conferences(E)Event/Exhibition-cultural and sports events, trade shows, exhibitions

ADVENTURE AND WILDLIFE TOURISM

Adventure travel has been growing 65% year over year since 2009.57% of adventure travelers are male48% are single or have never been married.The average age of adventure travelers is 36

The wildlife tourism industry spans the globe and generates billions of dollars of revenue, while also providing an economic incentive for wildlife and habitat conservation and cultural preservation. The popular destinations for wildlife tourism protected key areas

CULINARY TOURISM

India Food Tour includes-• More than food tasting• Maximum varieties of food covered• Safe and hygienic• English speaking guides• Meeting with chefs, cooking classes

SHOPPING TOURISM

• India-5th largest shopping destination globally• Important Destinations-Delhi, Kashmir, M.P., Kerala & Rajasthan• Shopping festivals organized by some countries• Economic Impact of shopping tourism• Future Trends in shopping tourism

Introduction to Tools

Dashboard:

Rate

Availability

Content

To ensure right hotels are getting contracted

Summarize the important details about an activity with the partner

Technical terms :

Rate Parity

Avail Parity

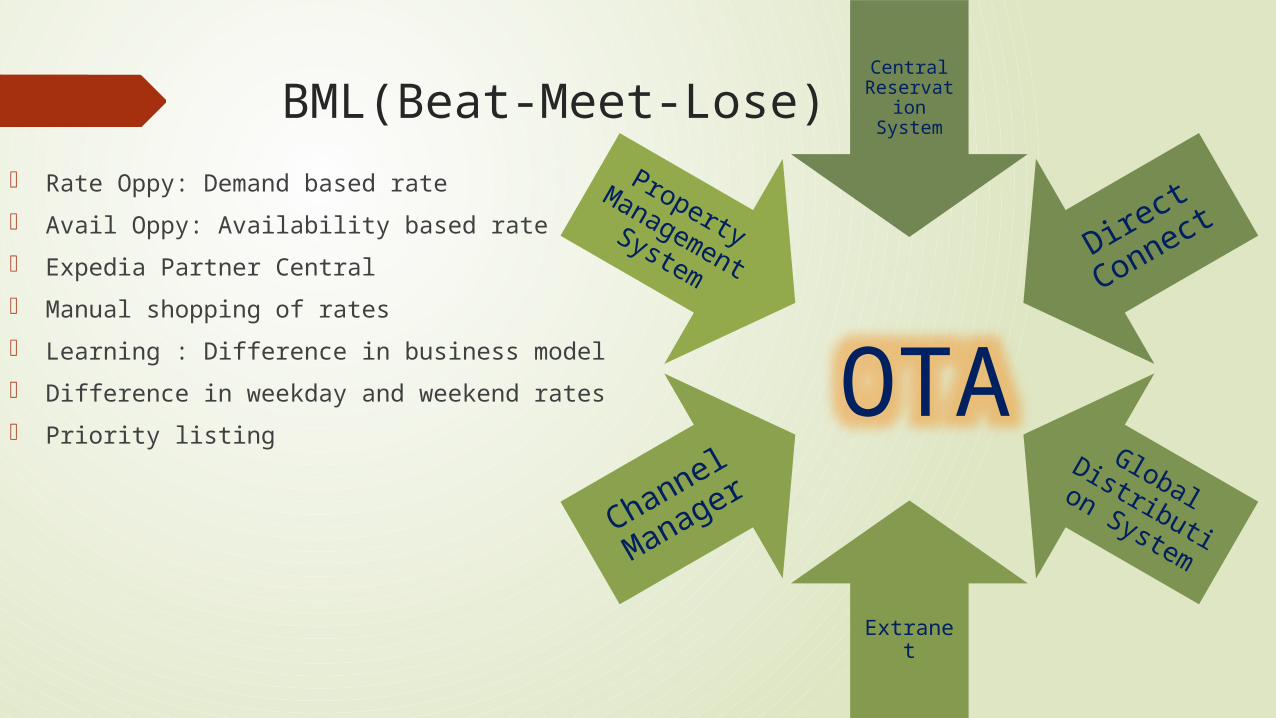

BML(Beat-Meet-Lose)

Rate Oppy: Demand based rate

Avail Oppy: Availability based rate

Expedia Partner Central

Manual shopping of rates

Learning : Difference in business model

Difference in weekday and weekend rates

Priority listing

Central Reservati

on System

Direct

Conn

ect

Global Distribution System

Extranet

Chan

nel

Man

ager

Property Management System

OTA

Acquisitions

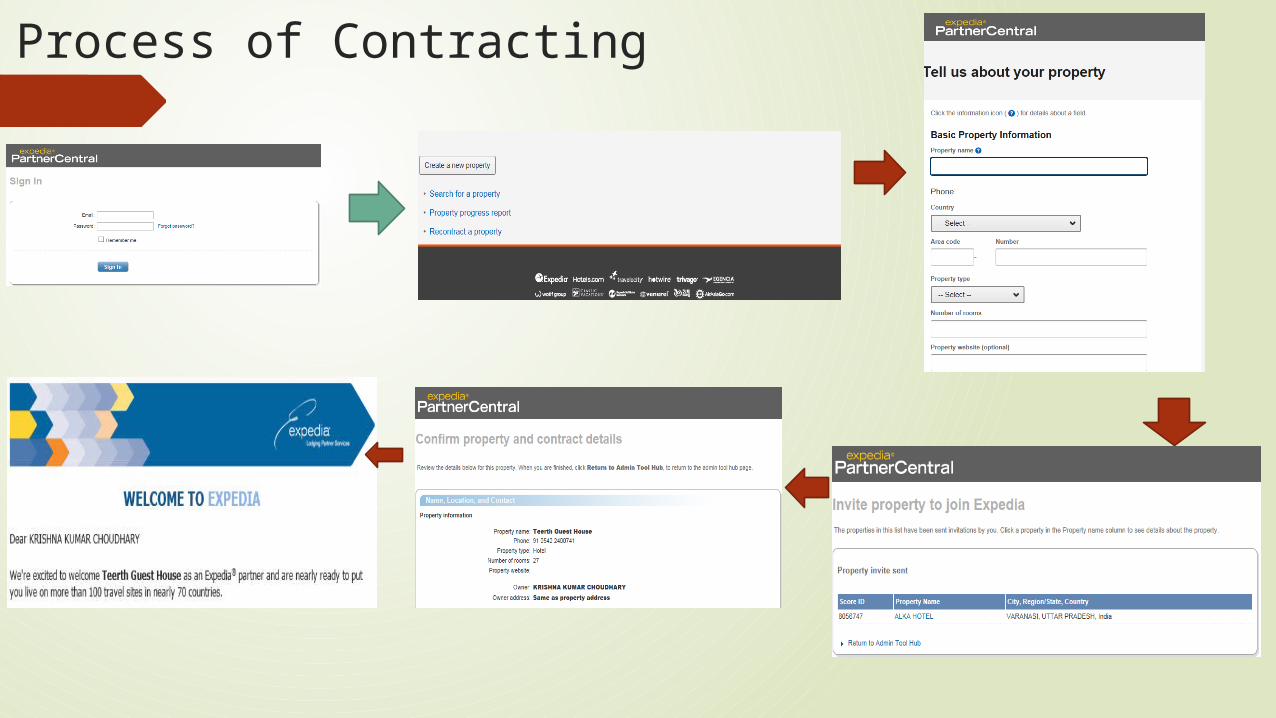

Process of registering property on Expedia

Contract clauses:

Rate Parity

ETP(Expedia Traveler Preference): Pay at hotel; Pay at Expedia

Compensation: Standalone, Package Rates

Sales Cycle:

Generate Lead Prepare Sales

PitchContract Loading

Sanity Check Live !

Process of Contracting

Learning: 4P’s

Proposal: Negotiating and communicating

Partner: Adaptation according to it

Patience

Perseverance