practical fatca implementation issues - c.ymcdn.com · with >$50k balance with ... specific form...

TRANSCRIPT

Practical FATCA Implementation Issues

IIB SEMINAR

June 14, 2011

Proshansky Auditorium

CUNY Graduate Center

Panelists

Thomas Prevost (Moderator)

Head of Americas Tax, Credit Suisse

Jacob Braun

Managing Director, The Bank of New York Mellon

Cyrus Daftary

Partner, Burt, Staples & Maner, LLP

Denise Marie Hintzke

Director, Deloitte Tax LLP

Ellen Zimiles

Managing Director, Navigant Consulting Inc.

Topics to be Discussed

Debunking the Myths of FATCA

Analyzing your Institution in Preparation for FATCA

Running an Effective FATCA Project

Client Data, Securities, Reporting and

Withholding Systems

Impact of FATCA on Legal Documentation

Role of Intermediaries in FATCA

Debunking the Myths of FATCA

Many in the foreign banking community are

saying FATCA does not apply to them for

various reasons. Below are a couple of

examples:

“I don’t have any US accounts”

“I don’t hold US assets”

Debunking the Myths of FATCA

Once reality sets in – FATCA affects nearly

every single financial institution, the next

question arises:

“So what do I do now?”

Analyzing your Institution in Preparation for FATCA

Compliance with FATCA requires either

having already collected or collecting new

information from clients.

– What has your institution collected from

clients as part of the KYC process

historically?

– How will FATCA change the global KYC

process?

Copyright © 2011 Deloitte Development LLC. All rights reserved.

Running an effective FATCA project

Setting up your Governance Team

•Who will be responsible

Setting up a Steering Committee

•What areas of the bank need to be involved for the project to be

successful?

Educating stakeholders and employees

Communicating with clients

• Institutional clients

• Private banking clients

Copyright © 2011 Deloitte Development LLC. All rights reserved.

Running an effective FATCA project

Running a project

•Identifying your team

•The different phases

•Special circumstances

–Small FFIs

–Providing services

Business as usual

Copyright © 2011 Deloitte Development LLC. All rights reserved.

FATCA roadmap

Risk assessment Develop strategy Account

identification

Withholding and

reporting

Project Management

Systems impact

Systems development

Maintenance

Consideration of single customer view and other disclosure regimes

Ongoing compliance program

• Audit

• Training

• Maintainability

2011 2012 2013 onwards

Scope of legislation

Group structure

• Affiliates

• Group locations

Nature of the business

• U.S. Source income

• Customers

• Products

• Qualified Intermediaries

• Local legal frameworks

Existing operations

• Policies and procedures

• Due diligence processes

• Existing tools

• Management information

Availability of data

Compliance approach

Governance structure

Stakeholder management

Customer communication

Compliance approach

• Centralization

• Definition of U.S. person

• Compliance process

• Due diligence approach

• Data sources

• Scope and prioritisation

• Local legal frameworks

• Withholding

• Reporting

Dialogue with IRS

Trade body representation

Training

Documentation process

• Understand policies and

procedures for current

documentation

• Develop communications

plan and account tracking

mechanism

• Validation process

• Management information

Remediation process

• Create remediation

policies and procedures

• Assess data availability

and quality

• Conduct gap analysis and

define search criteria

• Data analysis

Exception management

• Conduct client outreach

• Identification and tracking

• Escalation and resolution

Controls

• Roles and responsibilities

• Policies and procedures

• Monitoring

Withholding

• Communication

• Application

• Reconciliation

Reporting

• Process

• Aggregation of account

data

• Consistency

• Reconciliation

• Impact of local legal

frameworks

• Management of

undisclosed account

holders

Compliance

Framework

• Process review

• Internal audit

• Training

• Governance

• Industry

benchmarking

• Control of changes

in circumstance

Post implementation

• Post

implementation

review

• Systems

enhancement

• Process

integration

Op

timiz

atio

n M

on

ito

rin

g

Mo

nit

ori

ng

M

on

ito

rin

g

Copyright © 2011 Deloitte Development LLC. All rights reserved.

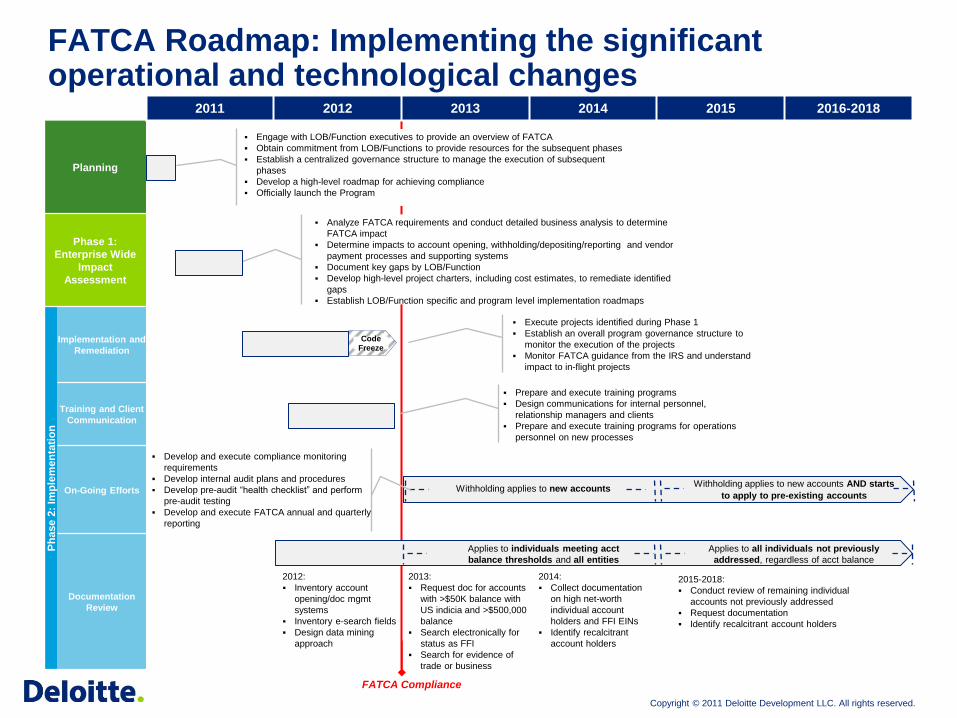

2011 2012 2013 2014 2015 2016-2018

Planning

Phase 1:

Enterprise Wide

Impact

Assessment

Ph

ase 2

: Im

ple

men

tati

on

Implementation and

Remediation

Training and Client

Communication

On-Going Efforts

Documentation

Review

FATCA Roadmap: Implementing the significant operational and technological changes

Engage with LOB/Function executives to provide an overview of FATCA

Obtain commitment from LOB/Functions to provide resources for the subsequent phases

Establish a centralized governance structure to manage the execution of subsequent

phases

Develop a high-level roadmap for achieving compliance

Officially launch the Program

Analyze FATCA requirements and conduct detailed business analysis to determine

FATCA impact

Determine impacts to account opening, withholding/depositing/reporting and vendor

payment processes and supporting systems

Document key gaps by LOB/Function

Develop high-level project charters, including cost estimates, to remediate identified

gaps

Establish LOB/Function specific and program level implementation roadmaps

Execute projects identified during Phase 1

Establish an overall program governance structure to

monitor the execution of the projects

Monitor FATCA guidance from the IRS and understand

impact to in-flight projects

Code Freeze

Withholding applies to new accounts

Prepare and execute training programs

Design communications for internal personnel,

relationship managers and clients

Prepare and execute training programs for operations

personnel on new processes

2012:

Inventory account

opening/doc mgmt

systems

Inventory e-search fields

Design data mining

approach

2013:

Request doc for accounts

with >$50K balance with

US indicia and >$500,000

balance

Search electronically for

status as FFI

Search for evidence of

trade or business

2014:

Collect documentation

on high net-worth

individual account

holders and FFI EINs

Identify recalcitrant

account holders

2015-2018:

Conduct review of remaining individual

accounts not previously addressed

Request documentation

Identify recalcitrant account holders

Withholding applies to new accounts AND starts

to apply to pre-existing accounts

Applies to individuals meeting acct

balance thresholds and all entities

Applies to all individuals not previously

addressed, regardless of acct balance

Develop and execute compliance monitoring

requirements

Develop internal audit plans and procedures

Develop pre-audit “health checklist” and perform

pre-audit testing

Develop and execute FATCA annual and quarterly

reporting

FATCA Compliance

Copyright © 2011 Deloitte Development LLC. All rights reserved.

Key FATCA project types

# Project Types Project ID# Example Project Name Example Project Description

1 Documentation DO1, DO2,

DO3…

Cure Documentation Curing documentation relates to re-solicitation of documents deemed to be

invalid by IRS standards (e.g., expired Form W-8)

Gather Documentation Gathering and/or soliciting documentation for required forms per types of

indicia of U.S. status

Validate Documentation

Ensuring appropriateness of Forms and documents provided (e.g., ensuring

Forms are signed, dated, specific form fields are filled out completely and

accurately)

2 Data D1, D2, D3…

Create Data Cleansing (Manual/Programmatic) of data where data currently exists, but is

unreliable

Cleanse/ Remediate Data Creating (Manual/Programmatic) data where missing

Validate Data Validating of data against 3rd party information or originator of data source

(e.g., following up directly with account holder or vendor)

3 Governance G1, G2, G3…

Create Procedures

Creating procedures that meet compliance requirements under FATCA. For

example:

The FATCA notice specifies that a Chief Compliance Officer or equivalent

level officer must certify that FFIs are in compliance with the FFI Agreement

Compliance Officer also required to certify that no procedures exist that

direct account holders to hide U.S. status

Establish a Monitoring and

Governance Program

Establishing an overall Monitoring and Governance program that defines how

compliance with FATCA will be monitored and roles and responsibilities for

meeting the requirements

4 Process P1, P2, P3… Update/Implement FATCA Required

Processes

Defining/updating processes (e.g., account opening) to meet FATCA

requirements. For example:

Forms W-8 Document Validation Process: Use of a checklist or online tools

to guide review of Form W-8 and validate requirements

Process to segregate responsibilities, such as separating document quality

assurance function from the validation function (person who validates the

Form does not QA the validation)

Documentation management processes that support obtaining, validating

and re-soliciting documentation required by FATCA

5 System S1, S2, S3…

Enhance System Functionality

Enhancing Account Opening system to provide the ability to flag accounts or

vendors as recalcitrant or non-participating FFIs

Enhancing Withholding, Depositing and Reporting system functionality to

identify deposit and report on FATCA withholdable payments

Create Fields To Capture Data Enhance systems to add fields to capture required data elements

FATCA will have impacts across documentation, data, governance, process and systems across the organization

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

Client Data, Securities, Reporting

and Withholding Systems

FATCA Requires a number of systems within an FFI/USFI to work together to allow the FFI/USFI to properly categorize account holders and potentially withhold and report on accounts where applicable.

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

What Systems May

Be Impacted By FATCA

Account master(client static data)

Income/payment processing system

Product master

AML/KYC system

Imaging system

Withholding system

Client communications

General ledger/balance sheet

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

Potential Required Capabilities

Account master(client static data)

Country information

Residence

Mailing

Citizenship (primary and secondary)

Birthplace

Incorporation details

Management & control

In care of addresses and P.O. Boxes

“Green card” status?

POA address

Tax Identification Numbers (TIN) (U.S. & non U.S.)

Client instructions (standing instructions, mailed instructions, hold mail)

Types of customers (individual vs. non-individual, FFI vs. NFFE)

Information about substantial U.S. owners of NFFEs

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

Potential Required Capabilities (cont’d)

Income/payment processing system

Income (interest, dividends, miscellaneous)

Gross proceeds

Balances/values

Product master

Source

Character

AML/KYC system

Identify >10% U.S. owners of non-U.S. entities

Imaging

No real requirements, rather need the ability to index and store documents as well as retain client communications for 10 years

Withholding

Withhold on “bad” FFIs and NFFEs

Withhold on recalcitrant account holders

Withholding on proceeds as well as U.S. source FDAP

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

Potential Required Capabilities (cont’d)

Client communications

Private bank: Maintain client communications (to or from client) related to existing account search under Notice 2011-34 for 10 years.

General ledger/balance sheet

Compute passthru payment percentage (“PPP”)

U.S. vs. non-U.S. assets.

PPP of other FFIs

Re-compute quarterly

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

Build/Buy… Go Manual…

Need to conduct an impact analysis.

Balance revenues / effort

Products

Projected viability of current systems

Going manual, is a business decision – but most will consider it only under limited circumstances

Perhaps ban bad FFIs/NFFEs (aka non participating FFIs and NFFEs).

Very low (or zero) volume of

Withholdable payments or

“U.S. accounts” (including non-U.S. entities with substantial U.S. owners)

Organization is not growing.

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

When To Start

Effective date is January 1, 2013.

FATCA statute provides substantial discretion to U.S. Treasury and IRS to define operative rules through regulations and other guidance.

The IRS has issued preliminary guidance outlining how FATCA enforcement will work, but nothing definitive yet.

Danger: Not enough time to comply if we wait until regulations are finalized before examining processes, procedures and systems likely to be affected by FATCA.

Start assessing gaps and gather basic requirements now.

Stay nimble – don’t overcommit to a build yet.

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

Assessing the Requirements

Start gap analysis on the following:

Customer account master(s)

What KYC/AML systems are used by the business unit?

What FATCA “U.S. indicia” elements (to be supplied in the

survey) are being captured by the system (e.g., U.S. address,

U.S. citizenship code, standing instructions, etc.)?

Is the system “electronically searchable” for existing account

data?

Can the system be modified to capture relevant FATCA

information?

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

Assessing the Requirements (cont’d)

Products and Payments

What payments are being made by the business unit (and

which ones are currently subject to withholding/reporting)?

What products (including structured products) are serviced

by the business unit?

What changes will be needed to security master (a/k/a

product master) to feed into payment/withholding systems?

Identification of U.S. source payments.

Identification of payments from securities giving rise to U.S. source

interest and dividends.

Grandfathered securities (March 18, 2012).

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

Assessing the Requirements (cont’d)

Withholding

Is the system an in-house or third-party system?

What are the data elements required for withholding?

What is the source of each data element identified above?

Reporting

Are customer statements issued on a monthly or quarterly

basis?

Can the business unit report to all account holders within an

account?

Can the business unit capture, on an annual basis, the

beginning and ending balance in an account?

2011, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP.

Unauthorized use and copying of this document are strictly forbidden.

FATCA Readiness

Need 18-24 months to build a system

Process and system changes will be needed

Realistically need requirements by 6/30/11 to be ready for a

1/1/2013 date

Need to devise a strategic readiness plan

Major change management initiative – as impact is well

beyond systems

May need to hedge – as firms did with Cost Basis

Impact of FATCA on Legal Documentation

A number of agreements, including loan agreements, note

indentures, master repo agreements, securities lending

agreements and ISDA Master agreements require

counterparties to gross-up payments for any taxes that are not

otherwise excluded.

In many of these agreements currently FATCA taxes would

require a gross-up.

Clearly this will be an issue as the party receiving the funds is

in control of whether it will be FATCA compliant.

However, given current uncertainty, do I put in FATCA

carveout or termination provisions now or wait for later

guidance?

Role of Intermediaries in FATCA

In a global capital market where many intermediaries and

agents typically are involved in the process between buyer

and seller, who is going to be responsible for reporting and

potentially withholding?

When is an account an account of an FFI instead of the

account of the FFI’s client, for whom the FFI is providing a

service?

FATCA operates under a system where the last FFI in the

chain will be required to handle the reporting and withholding

to the extent the account holder is a non-participating FFI

When is the last FFI in the chain ill-equipped to handle the

withholding and reporting on a transaction?

Role of Intermediaries in FATCA

FATCA operates under a system where the last FFI in the

chain will be required to handle the reporting and withholding

to the extent the account holder is a non-participating FFI or

a recalcitrant account holder.

When is the last FFI in the chain ill-equipped to handle the

withholding and reporting on a transaction?