predicting share price by using multiple linear regression692167/fulltext01.pdf · predicting share...

TRANSCRIPT

Predicting share price by using

Multiple Linear Regression A Bachelor Thesis in Mathematical Statistics

Gustaf Forslund & David Åkesson

Vehicle engineering KTH

May 21st, 2013

Abstract The aim of the project was to design a multiple linear regression model and use it to predict

the share’s closing price for 44 companies listed on the OMX Stockholm stock exchange’s

Large Cap list. The model is intended to be used as a day trading guideline i.e. today’s

information is used to predict tomorrow’s closing price. The regression was done in Microsoft

Excel 2010[18]

by using its built-in function LINEST. The LINEST-function uses the

dependent variable y and all the covariates x to calculate the β-value belonging to each

covariate. Several multiple linear regression models were created and their functionality was

tested, but only seven models were better than chance i.e. more than 50 % in the right

direction. To determine the most suitable model out of the remaining seven, Akaike’s

Information Criterion (AIC), was applied. The covariates used in the final model were; Dow

Jones closing price, Shanghai opening price, conjuncture, oil price, share’s opening price,

share’s highest price, share’s lowest price, lending rate, reports, positive/negative insider

trading, payday, positive/negative price target, number of completed transactions during one

day, OMX Stockholm closing price, TCW index, increasing closing price three days in a row

and decreasing closing price three days in a row.

The maximum average deviation between the predicted closing price and the real closing

price of all the 44 shares predicted were 6,60 %. In predicting the correct direction (increase

or decrease) of the 44 shares an average of 61,72 % were achieved during the time period

2012-02-22 to 2013-02-20. If investing 50.000 SEK in each company i.e. a total investment of

2.2 million SEK, the total yield when using the regression model during the year 2012-02-22

to 2013-02-20 would have been 259.639 SEK (11,80 %) compared to 184.171 SEK (8,37 %)

if the shares were never to be traded with during the same period of time. Of the 44

companies analysed, 31 (70,45 %) of them were profitable when using the regression model

during the year compared to 30 (68,18 %) if the shares were never to be sold during the same

period of time. The difference in yield in percentage between the model and keeping the

shares for the year was 40,98 %.

Table of Contents

Chapter 1 Introduction ............................................................................................................................. 1

1.1 Introduction ................................................................................................................................... 1

Chapter 2 Theory ..................................................................................................................................... 2

2.1 Econometrics ................................................................................................................................. 2

2.1.1 The Multiple Linear Regression Model theory ...................................................................... 2

2.2 Prediction....................................................................................................................................... 3

2.3 Regression channels ...................................................................................................................... 4

Chapter 3 Data ......................................................................................................................................... 6

3.1 Covariates ...................................................................................................................................... 6

3.1.1 Stock exchanges in the world ................................................................................................. 6

3.1.2 Conjuncture ............................................................................................................................ 6

3.1.3 TCW index ............................................................................................................................. 6

3.1.4 Lending rate ............................................................................................................................ 6

3.1.5 Pay day ................................................................................................................................... 7

3.1.6 Opening price ......................................................................................................................... 7

3.1.7 Highest/lowest price of the day .............................................................................................. 7

3.1.8 Positive/Negative insider trading ........................................................................................... 7

3.1.9 Quarterly and annual reports .................................................................................................. 7

3.1.10 Positive/negative price target ............................................................................................... 7

3.1.11 Oil price ................................................................................................................................ 8

3.1.12 Three positive/three negative days in a row ......................................................................... 8

3.1.13 P/E ratio ................................................................................................................................ 8

3.1.14 Positive/Negative press releases ........................................................................................... 8

3.1.15 Number of completed transactions ....................................................................................... 8

3.1.16 OMX Stockholm closing price ............................................................................................. 8

3.1.17 Split and reversed split ......................................................................................................... 8

3.2 Collecting data ............................................................................................................................... 9

Chapter 4 Modelling ................................................................................................................................ 9

4.1 Modelling ...................................................................................................................................... 9

4.2 AIC test ......................................................................................................................................... 9

4.2.1 First model ............................................................................................................................ 10

4.2.2 Second model: ...................................................................................................................... 11

4.2.3 Third model: ......................................................................................................................... 11

4.2.4 Fourth model: ....................................................................................................................... 12

4.2.5 Fifth model: .......................................................................................................................... 12

4.2.6 Sixth model: ......................................................................................................................... 12

4.2.7 Seventh model: ..................................................................................................................... 13

4.2 The final model ........................................................................................................................... 13

Chapter 5 Result .................................................................................................................................... 15

5.1 Plots of the residual and R2 value ................................................................................................ 15

5.2 Correct predicted directions ........................................................................................................ 16

5.3 Maximum and average deviation ................................................................................................ 17

5.4 Investing ...................................................................................................................................... 18

Chapter 6 Discussion ............................................................................................................................. 21

6.1 Discussion ................................................................................................................................... 21

Chapter 7 Appendix ............................................................................................................................... 23

7.1 Predicted closing price compared to real closing price ............................................................... 23

8.2 Yield using the model .................................................................................................................. 45

8.3 Stock exchange indexes ............................................................................................................... 67

8.4 Conjuncture ................................................................................................................................. 68

8.5 Oil price per barrel ...................................................................................................................... 69

8.6 TCW index .................................................................................................................................. 69

8.7 MATLAB code............................................................................................................................ 70

Chapter 9 References ............................................................................................................................. 91

9.1 References ................................................................................................................................... 91

1

Chapter 1 Introduction

1.1 Introduction Most people around the world dream of having more money in their pockets. The trick,

however, is not to work harder, but to work smarter. One way to make more money is to

invest on the stock exchange, but due to its seemingly random and unpredictable nature,

people are reluctant to do so. At first glance the stock exchange may seem random and

unpredictable, but that is not the entire truth. If the stock exchange is carefully analysed a

pattern will slowly emerge and it will be evident that there are a number of variables that

contributes to a company’s share price. Such variables are positive and negative news, price

target, conjuncture, oil price and other economic influential country’s stock exchange just to

name a few.

One of the most common share analysis tool used today is the so called regression channel.

These regression models are often sole based on the closing price vs. time and is more

reminiscent of a technical analysis rather than a prediction of the shares closing price. This

project aims to take it a step further by predicting a closing price for each day. The approach

is to determine which variables that has an influence on company’s share price, design a

multiple linear regression model and perform prediction using Microsoft Excel 2010’s[18]

built-in function LINEST to predict the closing price of 44 companies listed on the OMX

Stockholm stock exchange’s Large Cap list. The Large Cap list was at the time made up of 62

companies, but sufficient information was only found for 44 of them. Unlike the regression

channels that can be used for forecasting the direction of shares for several days ahead, even

weeks, this model will be used to analyse share prices on a daily basis for what resembles day

trading. The goal with the final model is to maximize the profit and minimize the losses based

on a daily analysis during the time period 2012-02-22 to 2013-02-20.

Since several multiple linear regression models were to be designed containing different sets

of covariates the Akaike Information Criterion (AIC) was used to determine the most suitable

model. One of the criterions for the model, set by us, were that it should be better than chance

in predicting if the share would increase or decrease in value i.e. have more than 50 % of the

predicted values in the correct direction. The other criterion was that the predicted closing

price should not deviate more than 10 % from the real closing price.

2

Chapter 2 Theory

2.1 Econometrics The term “econometrics” is believed to have been coined by the Norwegian man Ragnar

Frisch who lived between the years 1895-1973. He was one of the three principle founders of

the Econometric Society, first editor of the journal Econometrica and co-writer of the first

Nobel Memorial Prize in Economic Science in 1969[15]

.

Econometrics is used when it comes to applying statistical methods to problems when the data

available is observational rather than experimental, meaning the data obtained does not come

from controlled and planned experiments. Common fields where econometrics is applied are

economics, biology, medicine, social science and astronomy[16]

. The latter is a perfect

example of a natural science where data are typically observational and not experimental.

2.1.1 The Multiple Linear Regression Model theory

The basic model for econometric work and modelling for experimental design is the multiple

linear regression model[16]

. The specification is

(2.1)

where iy is the observation of the dependent random variable y whose expected value

depends on the covariates Cjx where C is a constant that denotes that i does not change. ie

represents the error terms and is assumed to be independent between observations and such

that

( |{ }) 0i jkE e x and 2 2( |{ })i jkE e x (2.2) (2.3)

where is unknown. Usually the covariate 0Cx is a constant 1 and 0 is the intercept.

If written

0( ... ), 1,...,i i ikx x x i n and 0( ... )T

k

then the specified model may be written as

i i iy x e (2.4)

The covariates may be deterministic (predetermined) values or outcomes of random

variables[16]

.

0

, 1,...,k

i ij j i

j

y x e i n

3

Sometimes it is convenient to use the matrix notation

Y X e where ( | ) 0E e X and 2( | )TE ee X I (2.5) (2.6)

where Y is a 1n -matrix of random variables, X is an ( 1)n k -matrix and e is an 1n -

matrix of random variables.

In the regression model above the parameters j and the variance 2 are unknown and it is

these parameters that are to be estimated from obtained data. The model can be used for either

prediction or it can be used to give a structural interpretation, which allows for hypotheses

testing. Since the project aims at predicting shares’ closing price the interesting part was

therefore only prediction.

2.2 Prediction When performing a prediction the linear model is often used

[16]. The covariates 0x makes up a

row matrix and with known covariates the predicted value of the corresponding ,y ,py is

0

ˆpy x . (2.7)

The prediction contains two unknown components; the estimated value of is used

instead of the real and the error term, which is set to zero in the prediction equation.

However, the error term is never zero in reality so to calculate it in the prediction the

following equation is used

0 0ˆ( )pe e x (2.8)

whose total variance is

1 2

0 0( ) (1 ( ) )T T

pVar e x X X x (2.9)

which is estimated to

1 2

0 0ˆ ( ) (1 ( ) )T T

pVar e x X X x s (2.10)

where s is an unbiased estimate of 2

2 21ˆ| |

1s e

n k

(2.11)

4

where n is the number of observations, k is the number of covariates in the prediction model

and 2 ˆˆ ˆ ˆ ˆ| | ,Te e e e Y X .

2.3 Regression channels On today’s stock exchange one of the most common analysis tools is the regression channel.

It uses historic values to forecast the future. The regression channel is based on a form of

chaos theory i.e. trying to predict something that springs from total chaos. A metaphoric

example can be made to illustrate how the regression channel works. Imagine a cigarette,

which stands straight up in a room where the air is perfectly still. The chaos theory says that

there is no way of predicting the smoke’s trails and loops as it leaves the cigarette. However,

if 10.000 cigarettes were to be observed in a row it would be noticed that the smoke trails of

one cigarette would never behave the same way as another cigarette’s, but at the same time it

would also be noticed that the smoke trails would never move outside a conical boundary on

their way up in the air. In chaos theory this boundary is known as a chaotic attractor.

Regression channels are based on the same principle, but instead of the smoke trail they use a

share’s closing price and the channel’s boundary is the chaotic attractor, which the share price

is not allowed to cross for a longer period of time. If the share moves outside the regression

channel it indicates that an unforeseen event has occurred, such as positive or negative news

or a new price target has been released and it is time to sell or buy the share.

One of the most common regression channels in use today is the Raff Regression Channel. It

uses time and closing price to draw up the channel. A regression line is created by analysing a

share’s closing price between certain days, say for example 100 days. Once the regression line

is drawn two more parallel lines are drawn, one above the regression line and one below it, at

equal distance from the regression line, see Figure 2.1. The distance is determined by the

highest or lowest share closing price from the regression line during the 100 days analysed[12]

.

The top line is seen as resistance and the bottom line is seen as support. The share may cross

these two lines for a short moment but if it stays outside for a longer period of time it

indicates that a new trend is coming.

5

Figure 2.1. Raff Regression Channel with 100 days analysed of Volvo B share between

2008-01-02 to 2013-02-21

As seen in Figure 2.1 the 100 days analysed is between day 400 and day 500, marked with

two red stars. In this case it was the maximum value at day 473 that set the distance between

the resistance line and the regression line. The red circle at day 579 indicates the point in time

when something unexpected happened and it was time to sell the shares and collect the profit

or to buy more shares and make a new regression channel. Even though the share returns to

the regression channel it has been more than 10 days since it crossed the support line and a

new regression channel has to be made.

Since the project aims to take it a bit further the multiple linear regression model was intended

to predict a closing price for each day instead of looking at the interval the share may stay

within. The difference between the regression channel and the multiple linear regression

model is that the regression channel can be used to see for how long the shares are worth

keeping, while the multiple linear regression model was intended to be used as a guideline for

day trading i.e. keep the shares if the model predicts a higher closing price tomorrow

compared to today otherwise sell them.

0 200 400 600 800 1000 1200 140030

40

50

60

70

80

90

100

110

120

130C

losin

g p

rice [

SE

K]

Days

VOLVO AB, B share

6

Chapter 3 Data

3.1 Covariates How the stock exchange move during a day depends on several different factors. For instance,

if the lending rate is raised the shares should go down, but on the same day a company could

announce a quarterly report, which should make the shares increase in value. Here all the

different covariates that have been used for the different models are listed and explained what

kind of impact they have on the shares.

3.1.1 Stock exchanges in the world

Dow Jones and Shanghai are two of the largest stock exchanges in the world. Because of this,

and the fact that both USA and China are two of the most economic influential countries in

the world, it makes Sweden and the OMX Stockholm stock exchange in particular very

dependent on how these two countries economy develops[13]

. Because of the time difference

the closing price for Dow Jones and the opening price for Shanghai were used. The index

prices for Dow Jones and Shanghai are given in USD and CYN respectively meaning they

had to be converted into SEK using Oanda[11]

for the exchange rates over the time period that

was analysed.

3.1.2 Conjuncture

The conjuncture for Sweden is given by the so called Barometerindikatorn which is given at

the end of every month by Konjunkturinstitutet. It is based on studies where the present and

future prospects of the economy are explored by both companies and households. It has an

average of 100 meaning that if the value is lower than 100 it is economic recession and over

100 it is economic boom in Sweden. The conjuncture gives a good indication of peoples

approach on wanting to buy or sell shares at the moment. Since the value is only given at the

end of every month a linear interpolation was performed to obtain values for every day. The

last month was extrapolated, since the value for it was not yet given.

3.1.3 TCW index

The TCW index stands for Total Competiveness Weights and is an index calculated by

International Monetary Fund, IMF. It is a weighted average of several currencies, which

measures the Swedish currency against other currencies. A currency’s weight is based on

Sweden’s trading with a particular country relative all the other countries. If the TCW index

increases it means that the Swedish currency (SEK) has decreased in value and if the index

decreases the SEK will increase in value. The TCW has a large impact on companies, which

is why it was considered a variable in the model.

3.1.4 Lending rate

The lending rate is the rate that banks have to pay Riksbanken when lending money. If the

lending rate is low it means that the banks can lower their interest rate leading to that;

1) companies will invest more,

2) and consumers will have more money to consume and invest,

The lending rate is given by Riksbanken and retains the value until a new is given.

7

3.1.5 Pay day

A dummy variable where a one indicated that salary was given on that day, normally on the

25th

every month. The hypothesis was that when people get their salary they might have some

extra money over after paying their bills, which could be used for investing in shares leading

to an increase in value.

3.1.6 Opening price

The opening price is the value that each share has when the OMX Stockholm stock exchange

opens for trading. The opening price gives a good indication of where the stock will move

during the day. Since the Stock exchange can be likened with an auction market i.e. buyers

and sellers meet to make deals with the highest bidder, the opening price does not have to be

the same as the last day’s closing price.

3.1.7 Highest/lowest price of the day

The highest and the lowest price of the day are taken the day before and gives an indication of

how much the shares usually move during a day and how this in the end will affect the closing

price. It also shows the general cyclical movement for each share.

3.1.8 Positive/Negative insider trading

Insider trading refers to trading done by people with good insight in how the company is

doing e.g. what kind of result they may present in the near future. People with good insight

could be the CEO, CEO of subsidiary, members of the board, people that own a lot of shares

in the company etc. This covariate was made up of two dummy variables; one for positive

insider trading where a one indicated that people with good insight in the company bought

shares, and one for negative insider trading where a one indicated that people with good

insight sold their shares. If people with good insight in the company sell their shares it might

indicate that the company is not doing as well as they thought and vice versa.

3.1.9 Quarterly and annual reports

The quarterly and annually reports are reports that present each company’s results for a

certain period. Usually when a company makes their reports public the share will increase in

value. This is often explained by the expectations that the investors have on the companies.

In this covariate only the release date was of interest i.e. the date that the report was released

so a dummy variable was created where a one indicated a released report.

3.1.10 Positive/negative price target

The price target is set by different analysts. Usually investors that do not have the time to

analyse the shares for themselves trust the analysts meaning that it gives a good indication of

when the shares will go up or down. The price target regards the share with the largest volume

i.e. the share that most people trade with, normally B shares. This covariate was made up of

two dummy variables; one for positive price target where a one indicated that the analysts

gave a price target larger than the actual price for the share and one for negative price target

where a one indicated that analysts gave a price target lower than the actual price for the

share.

8

3.1.11 Oil price

The oil price gives a good indication of how strong the USD is and the condition of the USD

has a big impact on the worldwide stock market. Since the oil price is given as USD/barrel it

was converted it into SEK/barrel to match the model. Another effect the oil price has on

shares is that if the oil price rises a company’s share value normally decreases since nearly

every company depends on oil for production[14]

. Therefore if the oil price rises the

company’s expenses increases and their profit will decrease.

3.1.12 Three positive/three negative days in a row

The hypothesis was that when a share moved in one direction for several days it would have a

big impact on peoples feeling toward the company. This covariate was made up of two

dummy variables; one for three positive days in a row where a one indicated that the share’s

closing price had increased in the last three days, and one for three negative days in a row

where a one indicated that the share had decreased in the last three days.

3.1.13 P/E ratio

This is a ratio calculated by

//

Current share priceP E

Earnings share (3.1)

and is a measurement of how long it will take to get the investment back, provided that the

earnings remain unchanged. The P/E-ratio is given in years. From where were the data was

collected the P/E-ratio was given once a year for each company so the values were linear

interpolated to obtain them for every day.

3.1.14 Positive/Negative press releases

Whenever a company makes a press release it will have an impact on their shares. These

releases can be about letting people go or that the company has just made a huge profitable

deal. This covariate was made up of two dummy variables; one for positive press releases

where a one indicated that a positive release had been made, and one for negative press

releases where a one indicated that a negative release had been made.

3.1.15 Number of completed transactions

This is the number of completed trading transactions that has been done with a company’s

share during one day. This number usually increases when a report is about to be released. It

gives a good indication of how popular a company’s shares are at the moment.

3.1.16 OMX Stockholm closing price

This is the value of how the total OMX Stockholm exchange has moved during the day.

3.1.17 Split and reversed split

A split is when a share is divided into several others and reverse is when several shares are

made into one. This covariate was made up of two dummy variables; one for split where a one

9

indicated a split had been made and one for reversed split where a one indicated a reversed

split had been made.

3.2 Collecting data The historical data for all of the shares and the press releases was collected from

Nasdaqomxnordic[1] [2]

The data for the conjuncture and TCW index was collected from Ekonomifakta[4] [6]

.

The index for Dow Jones was collected from Stloisfed[8]

and for Shanghai from Yahoo

finance[9]

.

The insider trading was collected from Finansinstitutionen[5]

Target prices and P/E-ratio was both found at Dagens ndustry[3]

The Oil price per barrel was collected from Eia[10]

The lending rate was collected from Riksbanken[7]

All of the exchange rates for converting foreign currencies into SEK was collected from

Oanda[11]

The data was then processed in Microsoft Excel 2010[18]

using its built-in function LINEST to

make the regression. For making the plots MATLAB[17]

and Minitab 16[19]

was used.

Chapter 4 Modelling

4.1 Modelling Before designing the multiple linear regression models a number of covariates had to be

evaluated to see what kind of impact they had on the share prices. The modelling process

consisted of testing different types of covariate combinations until a satisfactory result had

been achieved. What was learned during the modelling process was that theory put into

practice does not always yield a perfect result. Covariate combinations that should have

yielded a better result sometimes turned out to be worse. When seven satisfactory multiple

linear regression models had been designed Akaike’s Information Criterion, AIC, was applied

to determine which model that was most suitable.

4.2 AIC test Since multiple linear regression modelling often results in several different model designs it is

important to choose the best model suitable. One way of settling for a model is to use

Akaike’s Information Criterion, AIC. The AIC provides an index that can be used to

10

determine which of several competing models to go with. The multiple linear regression

model with the lowest AIC index should be the model of choice.

The general formula for AIC is

) 2 log( ( ) 2 ( )( )i i iAIC L p (4.1)

where ( )iL is the likelihood function of the parameters in model i evaluated at the

maximum likelihood estimators and p is the number of covariates in the model. According to

stat.stanford[20]

the general formula can rewritten as

) (log(2 ) log( ( )) log( )) 2 ( 1)( n SSE nAI pC n (4.2)

where stands for the model that is tested, n is number of observations, p number of

covariates and SSE is the sum squared error. The models that were tested and their AIC

indexes were the following.

4.2.1 First model

0 1 2 3

4 5 6 7

8 9 10 11

( ) ( ) ( )

( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

(

Closing price Dow Jones closing price conjuncture TCW

lending rate payday opening price highest price

lowest price positive insider negative insider reports

pos

12 13

14 15

16 17

) ( )

( ) ( )

( ) ( )

itive price target negative price target

Shanghai opening price oil price

three positive days in a row three negative days in a row

1

1

( ) 167993,61

) 333904,69

45892

17

(

AIC

n

p

SSE

11

4.2.2 Second model:

0 1 2 3

4 5 6 7

8 9 10 11

( ) ( ) ( )

( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

(

Closing price Dow Jones closing price conjuncture TCW

lending rate payday opening price highest price

lowest price positive insider negative insider reports

pos

12 13

14 15

16 17

18 19

) ( )

( ) ( )

( ) ( )

( ) ( )

itive price target negative price target

Shanghai opening price oil price

three positive days in a row three negative days in a row

positive press negative press

2

2

( ) 167996,15

) 333880,19

45892

19

(

AIC

n

p

SSE

4.2.3 Third model:

0 1 2 3

4 5 6 7

8 9 10 11

( ) ( ) ( )

( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

(

Closing price Dow Jones closing price conjuncture TCW

lending rate payday opening price highest price

lowest price positive insider negative insider reports

pos

12 13

14 15

16 17

18 19 2

) ( )

( ) ( )

( ) ( )

( ) ( ) ( )

itive price target negative price target

Shanghai opening price oil price

three positive days in a row three negative days in a row

positive press negative press positive report

0

21 22 23 24( ) ( ) ( ) ( )negative report dividend split reversed split

3

3

( ) 168001,00

) 333793,87

45892

24

(

AIC

n

p

SSE

12

4.2.4 Fourth model:

0 1 2 3

4 5 6 7

8 9 10 11

( ) ( ) ( )

( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

(

Closing price Dow Jones closing price conjuncture TCW

lending rate payday opening price highest price

lowest price positive insider negative insider reports

pos

12 13

14 15

16 17

18

) ( )

( ) ( )

( ) ( )

( )

itive price target negative price target

Shanghai opening price oil price

three positive days in a row three negative days in a row

number of clompleted transactions

4

4

( ) 167990,50

) 333818,93

45892

18

(

AIC

n

p

SSE

4.2.5 Fifth model:

0 1 2 3

4 5 6 7

8 9 10 11

( ) ( ) ( )

( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

(

Closing price Dow Jones closing price conjuncture TCW

lending rate payday opening price highest price

lowest price positive insider negative insider reports

pos

12 13

14 15

16 17

18 19

) ( )

( ) ( )

( ) ( )

( ) ( )

(

itive price target negative price target

Shanghai opening price oil price

three positive days in a row three negative days in a row

number of completed transactions positive press

n

20)egative press

5

5

( ) 167993,17

) 333796,81

45892

20

(

AIC

n

p

SSE

4.2.6 Sixth model:

0 1 2 3

4 5 6 7

8 9 10 11

( ) ( ) ( )

( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

(

Closing price Dow Jones closing price conjuncture TCW

lending rate payday opening price highest price

lowest price positive insider negative insider reports

pos

12 13

14 15 16

17 18

) ( )

( ) ( ) ( )

( ) ( / )

itive price target negative price target

Shanghai opening oil price three positive days in a row

three negative days in a row P E ratio

6

6

( ) 167995,55

) 333903,67

45892

18

(

AIC

n

p

SSE

13

4.2.7 Seventh model:

0 1 2 3

4 5 6 7

8 9 10 11

( ) ( ) ( )

( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

(

Closing price Dow Jones closing price conjuncture TCW

lending rate payday opening price highest price

lowest price positive insider negative insider reports

pos

12 13

14 15

16 17

18

) ( )

( ) ( )

( ) ( )

( )

(

itive price target negative price target

Shanghai opening price oil price

three positive days in a row three negative days in a row

number of completed transactions

OMX Stockholm opening p

19)rice

7

7

( ) 167929,88

) 332771,86

45892

19

(

AIC

n

p

SSE

Summary of the AIC indexes were as follows.

1( )AIC 2( )AIC 3( )AIC 4( )AIC 5( )AIC 6( )AIC 7( )AIC

167993,61 167996,15 168001,00 167990,50 167993,17 167995,55 167929,88

As mentioned above the model with the lowest AIC index should be the best model of choice.

Here the multiple linear regression model with the lowest AIC index is number seven hence

the model to go with.

4.2 The final model

The aim was to create a general multiple linear regression model that could be applied to all

44 shares analysed. To achieve this four years (2008-01-02 to 2012-02-21) of data from every

share was collected and inserted into a single Microsoft Excel 2010[18]

sheet. The amount of

data made up 45892 observations. Microsoft Excel 2010’s built-in function LINEST was used

to perform the regression. The LINEST-function gives the i :s value and the corresponding

error term for every covariate used. The final model that was used had the following design.

0 1 2 3

4 5 6 7

8 9 10 11

( ) ( ) ( )

( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

(

Closing price Dow Jones closing price conjuncture TCW

interest rate payday opening price highest value

lowest value positive insider negative insider reports

po

12 13

14 15

16 17

18

) ( )

( ) ( )

( ) ( )

( )

(

sitive price target negativ price target

Shanghai opening price oil price

three positive days in a row three negative days in a row

number of completed transactions

OMX Stockholm opening p

19)rice

14

i -values corresponding residuals, ie

β0 7,33539 e0 1,00779

β1 1,4295 10-5

e1 3,62151 10-6

β2 0,01035 e2 0,00240

β3 – 0,04664 e3 0,005639

β4 – 0,24109 e4 0,01902

β5 0,25977 e5 0,06065

β6 0,96488 e6 0,00398

β7 – 0,04321 e7 0,00652

β8 0,07893 e8 0,00659

β9 0,04293 e9 0,06880

β10 0,06856 e10 0,11282

β11 0,26392 e11 0,09203

β12 – 0,09910 e12 0,05644

β13 – 0,16703 e13 0,09102

β14 0,00024 e14 3,48251 10-5

β15 0,00076 e15 0,00020

β16 0,02782 e16 0,04033

β17 0,08593 e17 0,03795

β18 1,3626 10-5

e18 5,17749 10-6

β19 – 0,00433 e19 0,99883

Table 4.1. β-values and corresponding residuals from the regression of the final model

(2008-01-02 to 2012-02-21).

The i :s where then used to calculate the estimated y (closing price) by the formula

19,192,21,10 ...ˆ jjj xxxy (4.3)

where j denotes the jth

row i.e. jth

day predicted in Microsoft Excel 2010[18]

.

15

Chapter 5 Result

5.1 Plots of the residual and R2 value

Figure 5.1. Normal probability plot from the regression (2008-01-02 to 2012-02-21).

Figure 5.2. Plot of the residual vs. fits from the regression (2008-01-02 to 2012-02-21).

According to Microsoft Excel 2010[18]

the model had an R2 value of 99,88 %.

16

5.2 Correct predicted directions The project was made for 44 companies on the OMX Stockholm stock exchange Large Cap

list. The aim was that the model should predict the direction of the shares at least 50 %

correctly i.e. better than chance. The predicted closing price was compared with yesterday’s

to determine if the predicted value was an increase or decrease. If the real closing price was

an increase and the predicted value as well it was considered a correct prediction. Table 5.1

displays the result for each share.

Share Correct predicted directions [%]

Alfa Laval 62,8

Alliance Oil 60,0

Assa Abloy 62,0

Atlas Copco 62,4

Axfood 58,0

Axis 55,2

Billerudkorsnäs 56,8

Boliden 68,8

Castellum 58,8

Electrolux 66,0

Elekta 64,4

Ericsson 66,0

Fabegé 63,6

Getinge 60,8

H&M 63,6

Hakon invest 59,2

Hexagon 65,2

Holmen 62,4

Hufvudstaden 54,4

Husqvarna 60,8

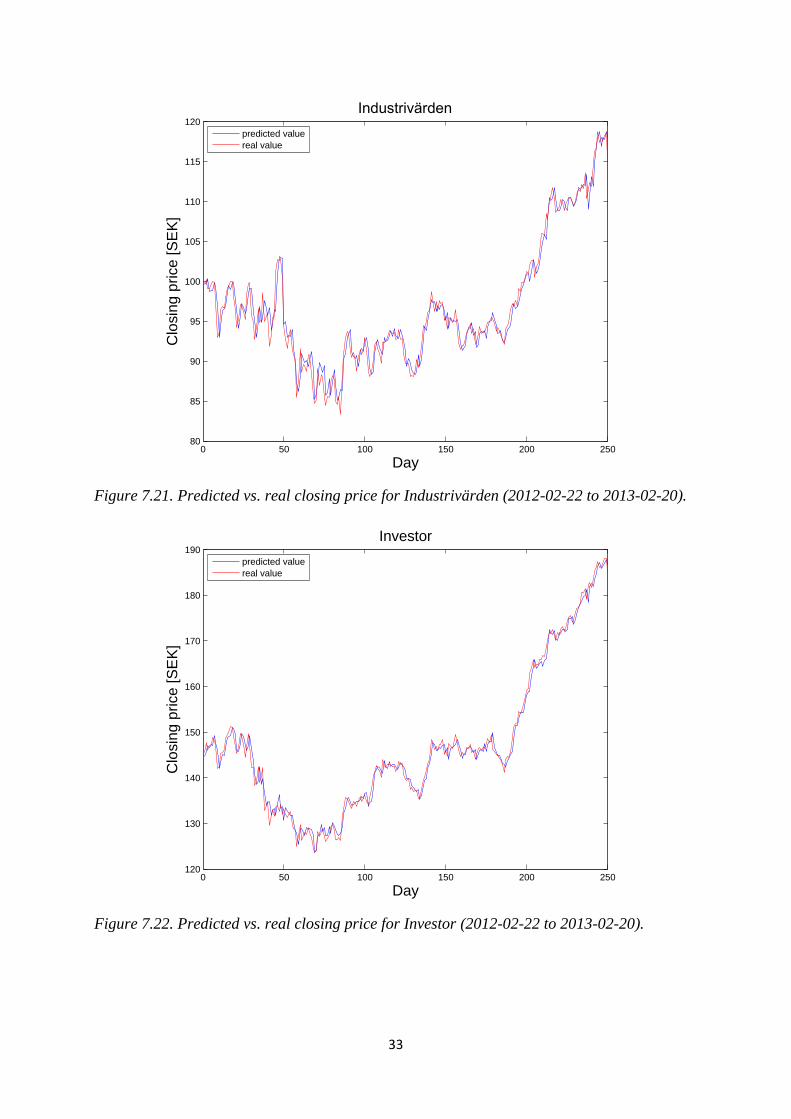

Industrivärden 62,4

Investor 61,2

Kinnevik 62,0

Latour 57,6

Lundbergföretagen 66,0

Meda 59,6

MTG 58,8

Peab 56,4

Ratos 57,2

SAAB 56,0

Sandvik 70,4

SCA 64,0

Scania 62,0

SEB 65,2

Securitas 56,4

Skanska 68,0

SKF 66,8

17

SSAB 62,4

Swedbank 62,4

Swedish Match 58,4

TeliaSonera 58,8

Trelleborg 66,4

Volvo 70,8

Wallenstam 55,2

Table 5.1. Correct predicted directions in percentage for each share

(2012-02-22 to 2013-02-20).

Each share was over 50 % which was the project aim, meaning that the model is profitable on

a day by day basis in the long term. Since the model is intended to be applicable on all shares

an average correct predicted direction was calculated

Average correct predicted direction = 62,8 60,0 ... 55,2

61,71%44

5.3 Maximum and average deviation Since the average predicted direction gives insufficient information on the model’s ability

alone a maximum and average deviation in percentage from the real closing price was

calculated for each share. The calculation was done using Microsoft Excel 2010[18]

and the

result is displayed in Table 5.2.

Share Maximum deviation [%] Average deviation [%]

Alfa Laval 6,80 1,07

Alliance Oil 10,24 1,52

Assa Abloy 4,17 1,04

Atlas Copco 4,44 1,19

Axfood 4,76 0,79

Axis 7,51 1,39

Billerudkorsnäs 9,76 1,48

Boliden 5,24 1,24

Castellum 4,66 0,82

Electrolux 6,14 1,25

Elekta 11,73 1,15

Ericsson 5,85 1,04

Fabegé 4,50 1,05

Getinge 5,60 0,91

H&M 4,53 0,76

Hakon invest 9,79 0,98

Hexagon 6,15 1,38

Holmen 3,73 0,83

Hufvudstaden 4,21 0,80

Husqvarna 11,63 1,30

Industrivärden 5,28 1,11

18

Investor 4,02 0,83

Kinnevik 6,82 0,83

Latour 5,42 1,19

Lundbergföretagen 4,66 0,82

Meda 4,81 0,85

MTG 29,19 1,47

Peab 5,59 1,36

Ratos 8,81 1,38

SAAB 4,52 1,09

Sandvik 6,27 1,21

SCA 8,10 0,88

Scania 5,11 1,20

SEB 4,68 1,09

Securitas 4,99 1,04

Skanska 3,47 0,82

SKF 8,48 1,10

SSAB 5,57 1,56

Swedbank 5,31 1,01

Swedish Match 6,72 0,91

TeliaSonera 3,78 0,76

Trelleborg 7,02 1,27

Volvo 5,80 1,20

Wallenstam 4,33 1,11

Table 5.2. Maximum and average deviation in percentage for each share (2012-02-22 to

2013-02-20).

The average maximum deviation was 6,60 % and the average deviation was 1,03 %.

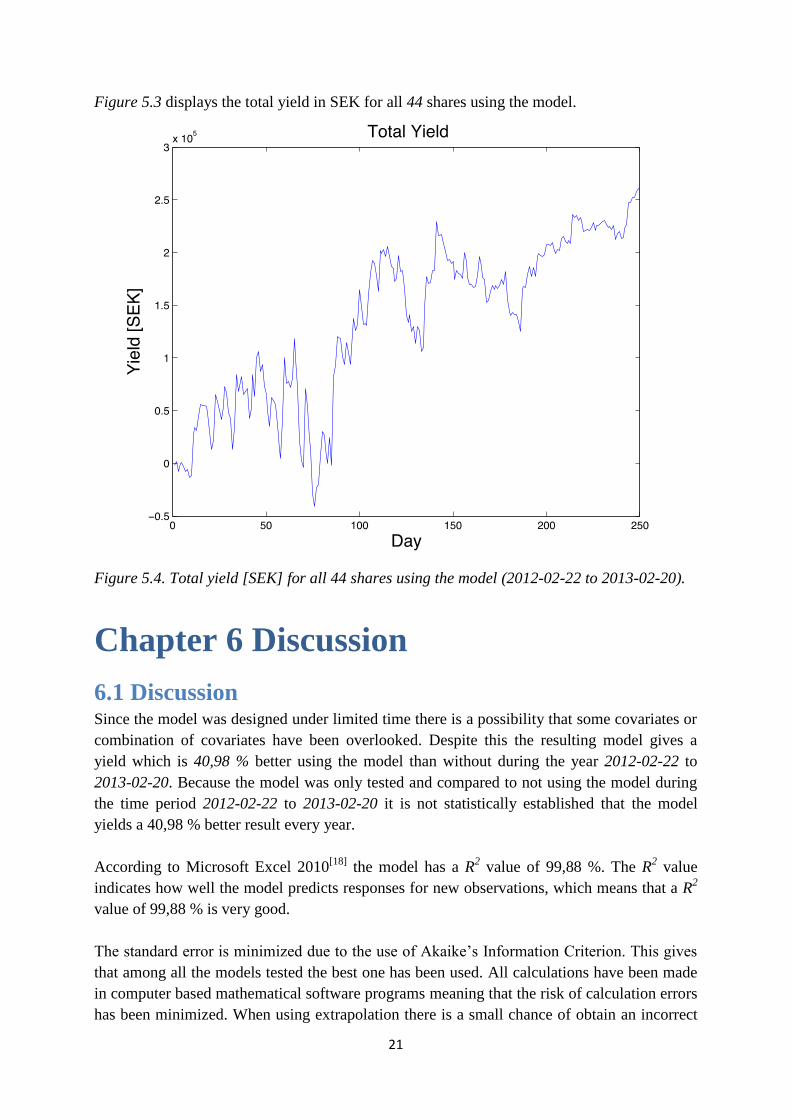

5.4 Investing To evaluate the model further an investment test was conducted. If 50.000 SEK had been

invested in each share, a total investment of 2.2 million SEK, and the model had been applied

over the year 2012-02-22 to 2013-02-20 the total yield would have been 259.639 SEK

corresponding to 11,8 %. If the same investment had been done and the shares were never to

be traded with during the same period of time i.e. the investment would have been done at

2012-02-22 and then sold at 2013-02-20, the total yield would have been 184.171 SEK

corresponding to 8,37 %. This means that the model would have generated a 40,98 % greater

yield that year. In Table 5.3 the shares’ result after a year is presented both using the model

and without.

To calculate each share’s yield Microsoft Excel 2010[18]

was used. First a prediction column

was created were a one indicated that the predicted closing price would be higher than

yesterday’s real closing price, if the predicted value was lower or equal to yesterday’s real

closing price a zero was shown. The four red columns to the right of the prediction column

indicates if the prediction column goes from zero to one, one to one, one to zero or zero to

zero. Each day there was a one present in the zero to one column shares was bought to the real

opening price. Each day there was a one present in the one to one column the shares bought

19

earlier were kept and the profit/loss was added to yesterday’s daily value. Each day there was

a one present in the one to zero column the shares were sold to the real opening price. Each

day there was a one present in the zero to zero column nothing happened since the share was

not of interest. To get an overview of how the calculation was made see Figure 5.3.

Figure 5.3. Extract of how the calculations of Sandvik’s yield was made in Microsoft Excel

2010[18]

using the model (2012-02-22 to 2013-02-20)

Share

How much the investment

of 50.000 SEK is worth

after the year using the

model [SEK]

How much the investment

of 50.000 SEK is worth

after the year not using the

model [SEK]

Alfa Laval 59970,21 55875,00

Alliance Oil 44225,26 33261,30

Assa Abloy 58206,55 63075,00

Atlas Copco 59086,73 53941,30

Axfood 45873,00 55540,80

Axis 42776,07 44362,50

Billeurdkorsnäs 46192,24 52641,75

Boliden 67020,51 47523,00

Castellum 52277,52 55265,85

Electrolux 68260,31 57024,00

Elekta 64516,28 64085,40

Ericsson 57895,17 59969,40

Fabege 59531,77 60455,25

20

Getinge 48817,93 52796,00

H&M 55803,67 48214,40

Hakon 60942,62 79165,00

Hexagon 75416,53 67369,20

Holmen 43163,71 48588,80

Hufvudstaden 44869,93 60253,00

Husqvarna 68619,69 50751,80

Industrivärden 64668,24 57450,00

Investor 62327,47 63790,50

Kinnevik 53983,50 50832,60

Latour 43729,87 53246,70

Lundbergföretagen 59566,70 58426,00

Meda 50952,34 55803,10

MTG 43150,95 41164,20

Peab 51134,95 48963,84

Ratos 43780,77 37388,25

SAAB 39568,02 52749,60

Sandvik 81024,52 51931,80

SCA 56428,23 68853,60

Scania 55887,09 52899,00

SEB 68538,51 67743,35

Securitas 43642,22 46154,85

Skanska 59587,12 47444,40

SKF 59139,09 47288,50

SSAB 59390,02 35585,55

Swedbank 55984,63 69615,00

Swedish Match 51485,73 42061,60

TeliaSonera 48099,77 45426,15

Trelleborg 72091,30 64696,25

Volvo 57681,16 50453,20

Wallenstam 54331,33 64044,10

Total yield 259.639,23 184.170,89

Table 5.3. Each share’s yield in SEK both using the model and without (2012-02-22 to

2013-02-20).

21

Figure 5.3 displays the total yield in SEK for all 44 shares using the model.

Figure 5.4. Total yield [SEK] for all 44 shares using the model (2012-02-22 to 2013-02-20).

Chapter 6 Discussion

6.1 Discussion Since the model was designed under limited time there is a possibility that some covariates or

combination of covariates have been overlooked. Despite this the resulting model gives a

yield which is 40,98 % better using the model than without during the year 2012-02-22 to

2013-02-20. Because the model was only tested and compared to not using the model during

the time period 2012-02-22 to 2013-02-20 it is not statistically established that the model

yields a 40,98 % better result every year.

According to Microsoft Excel 2010[18]

the model has a R2 value of 99,88 %. The R

2 value

indicates how well the model predicts responses for new observations, which means that a R2

value of 99,88 % is very good.

The standard error is minimized due to the use of Akaike’s Information Criterion. This gives

that among all the models tested the best one has been used. All calculations have been made

in computer based mathematical software programs meaning that the risk of calculation errors

has been minimized. When using extrapolation there is a small chance of obtain an incorrect

22

result. However the difference between the extrapolated value and the real is small and it will

only affect the predicted value with approximately 0,1-0,2 SEK. The reason for linear

interpolation of the conjuncture was since the values were only given once a month they had

to be linear between two months.

The reason for designing a general model was because of the fact that it is intended to be used

as a day trading guideline in the mornings when the opening price is known. It is of great

importance that the calculations can be completed quickly so that decisions regarding selling

or buying shares can be done fast. This is where the general model has an advantage

compared to several tailor made models. Security is found in numbers when it comes to share

trading.

Four years (2008-01-02 to 2012-02-21) of data from every share was collected and inserted

into a single Microsoft Excel 2010[18]

sheet. The amount of data made up 45892 observations.

Microsoft Excel 2010’s[18]

built-in function LINEST was used to perform the regression. The

LINEST-function gives the i :s value and the corresponding error term for every covariate

used. The data was collected for four years due to the fact that more observations lead to a

better reliability of the model. Another reason was to include the worldwide stock market

crash of 2008. The β-values of the model will then be more accurate towards TCW index,

conjuncture, oil price, Dow Jones index, Shanghai index and OMX Stockholm index which

make the model more reliable.

Another approach to predict share’s closing price is to use Markov processes. Unlike multiple

linear regression which analyses historical data the Markov process uses the present to predict

the future. Since shares are memoryless i.e. they are not affected by yesterday’s cyclic

movement, it is possible that Markov processes would have yielded a better result. The reason

why multiple linear regression yields such a good result after all could be that four years of

historical data from 44 shares displays people’s irrational behaviour which is the main reason

why shares are considered random and unpredictable.

23

Chapter 7 Appendix

7.1 Predicted closing price compared to real closing price

Figure 7.1. Predicted vs. real closing price for Alfa Laval (2012-02-22 to 2013-02-20).

Figure 7.2. Predicted vs. real closing price for Alliance Oil (2012-02-22 to 2013-02-20).

0 50 100 150 200 250110

115

120

125

130

135

140

145

150

155

Alfa laval

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25045

50

55

60

65

70

75

80

85

90

Alliance Oil

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

24

Figure 7.3. Predicted vs. real closing price for Assa Abloy (2012-02-22 to 2013-02-20).

Figure 7.4. Predicted vs. real closing price for Atlas Copco (2012-02-22 to 2013-02-20).

0 50 100 150 200 250170

180

190

200

210

220

230

240

250

260

Assa Abloy

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 250130

140

150

160

170

180

190

Atlas Copco

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

25

Figure 7.5. Predicted vs. real closing price for Axfood (2012-02-22 to 2013-02-20).

Figure 7.6. Predicted vs. real closing price for Axis (2012-02-22 to 2013-02-20).

0 50 100 150 200 250210

220

230

240

250

260

270

280

Axfood

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 250130

140

150

160

170

180

190

Axis

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

26

Figure 7.7. Predicted vs. real closing price for BillerudKorsnäs (2012-02-22 to 2013-02-20).

Figure 7.8. Predicted vs. real closing price for Boliden (2012-02-22 to 2013-02-20).

0 50 100 150 200 25050

55

60

65

70

75

BillerudKorsnäs

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25085

90

95

100

105

110

115

120

125

130

Boliden

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

27

Figure 7.9. Predicted vs. real closing price for Castellum (2012-02-22 to 2013-02-20).

Figure 7.10. Predicted vs. real closing price for Electrolux (2012-02-22 to 2013-02-20).

0 50 100 150 200 25075

80

85

90

95

100

Castellum

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 250120

130

140

150

160

170

180

Electrolux

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

28

Figure 7.11. Predicted vs. real closing price for Elekta (2012-02-22 to 2013-02-20).

Figure 7.12. Predicted vs. real closing price for Ericsson (2012-02-22 to 2013-02-20).

0 50 100 150 200 25050

100

150

200

250

300

350

400

Elekta

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25055

60

65

70

75

80

Ericsson

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

29

Figure 7.13. Predicted vs. real closing price for Fabege (2012-02-22 to 2013-02-20).

Figure 7.14. Predicted vs. real closing price for Getinge (2012-02-22 to 2013-02-20).

0 50 100 150 200 25045

50

55

60

65

70

75

Fabege

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 250160

170

180

190

200

210

220

230

Getinge

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

30

Figure 7.15. Predicted vs. real closing price for H&M (2012-02-22 to 2013-02-20).

Figure 7.16. Predicted vs. real closing price for Hakon Invest (2012-02-22 to 2013-02-20).

0 50 100 150 200 250200

210

220

230

240

250

260

H&M

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25090

100

110

120

130

140

150

160

170

180

Hakon Invest

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

31

Figure 7.17. Predicted vs. real closing price for Hexagon (2012-02-22 to 2013-02-20).

Figure 7.18. Predicted vs. real closing price for Holmen (2012-02-22 to 2013-02-20).

0 50 100 150 200 250110

120

130

140

150

160

170

180

190

Hexagon

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 250165

170

175

180

185

190

195

200

Holmen

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

32

Figure 7.19. Predicted vs. real closing price for Hufvudstaden (2012-02-22 to 2013-02-20).

Figure 7.20. Predicted vs. real closing price for Husqvarna (2012-02-22 to 2013-02-20).

0 50 100 150 200 25065

70

75

80

85

90

95

Hufvudstaden

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25028

30

32

34

36

38

40

42

Husqvarna

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

33

Figure 7.21. Predicted vs. real closing price for Industrivärden (2012-02-22 to 2013-02-20).

Figure 7.22. Predicted vs. real closing price for Investor (2012-02-22 to 2013-02-20).

0 50 100 150 200 25080

85

90

95

100

105

110

115

120

Industrivärden

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 250120

130

140

150

160

170

180

190

Investor

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

34

Figure 7.23. Predicted vs. real closing price for Kinnevik (2012-02-22 to 2013-02-20).

Figure 7.24. Predicted vs. real closing price for Latour (2012-02-22 to 2013-02-20).

0 50 100 150 200 250120

125

130

135

140

145

150

155

Kinnevik

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 250110

115

120

125

130

135

140

145

150

Latour

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

35

Figure 7.25. Predicted vs. real closing price for Lundbergföretagen

(2012-02-22 to 2013-02-20).

Figure 7.26. Predicted vs. real closing price for Meda (2012-02-22 to 2013-02-20).

0 50 100 150 200 250190

200

210

220

230

240

250

260

270

280

Lundbergföretagen

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25060

62

64

66

68

70

72

74

76

78

Meda

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

36

Figure 7.27. Predicted vs. real closing price for MTG (2012-02-22 to 2013-02-20).

Figure 7.28. Predicted vs. real closing price for Peab (2012-02-22 to 2013-02-20).

0 50 100 150 200 250180

200

220

240

260

280

300

320

340

360

380

MTG

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25029

30

31

32

33

34

35

36

37

38

39

Peab

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

37

Figure 7.29. Predicted vs. real closing price for Ratos (2012-02-22 to 2013-02-20).

Figure 7.30. Predicted vs. real closing price for SAAB (2012-02-22 to 2013-02-20).

0 50 100 150 200 25050

55

60

65

70

75

80

85

90

95

Ratos

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 250100

105

110

115

120

125

130

135

140

145

SAAB

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

38

Figure 7.31. Predicted vs. real closing price for Sandvik (2012-02-22 to 2013-02-20).

Figure 7.32. Predicted vs. real closing price for SCA (2012-02-22 to 2013-02-20).

0 50 100 150 200 25080

85

90

95

100

105

110

Sandvik

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25090

100

110

120

130

140

150

160

SCA

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

39

Figure 7.33. Predicted vs. real closing price for Scania (2012-02-22 to 2013-02-20).

Figure 7.34. Predicted vs. real closing price for SEB (2012-02-22 to 2013-02-20).

0 50 100 150 200 250110

115

120

125

130

135

140

145

Scania

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25035

40

45

50

55

60

65

70

SEB

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

40

Figure 7.35. Predicted vs. real closing price for Securitas (2012-02-22 to 2013-02-20).

Figure 7.36. Predicted vs. real closing price for Skanska (2012-02-22 to 2013-02-20).

0 50 100 150 200 25048

50

52

54

56

58

60

62

64

66

Securitas

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25090

95

100

105

110

115

120

125

Skanska

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

41

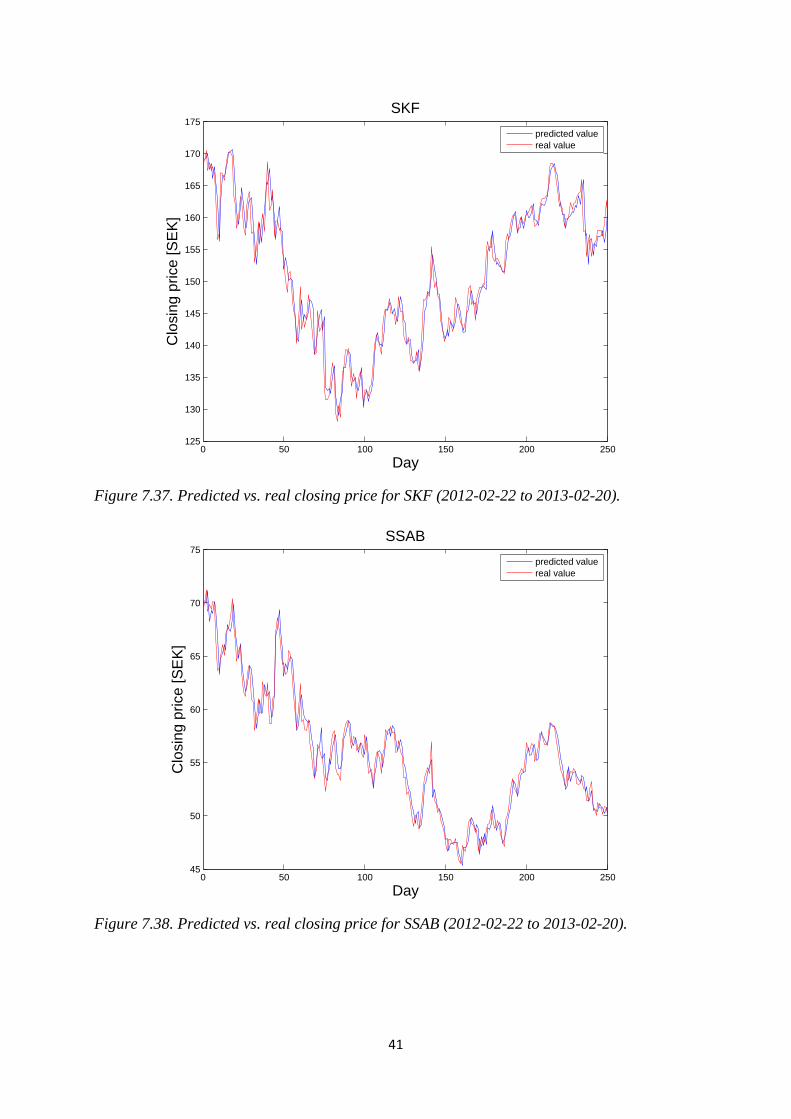

Figure 7.37. Predicted vs. real closing price for SKF (2012-02-22 to 2013-02-20).

Figure 7.38. Predicted vs. real closing price for SSAB (2012-02-22 to 2013-02-20).

0 50 100 150 200 250125

130

135

140

145

150

155

160

165

170

175

SKF

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25045

50

55

60

65

70

75

SSAB

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

42

Figure 7.39. Predicted vs. real closing price for Swedbank (2012-02-22 to 2013-02-20).

Figure 7.40. Predicted vs. real closing price for Swedish Match (2012-02-22 to 2013-02-20).

0 50 100 150 200 25090

100

110

120

130

140

150

160

Swedbank

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 250200

210

220

230

240

250

260

270

280

290

300

Swedish Match

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

43

Figure 7.41. Predicted vs. real closing price for TeliaSonera (2012-02-22 to 2013-02-20).

Figure 7.42. Predicted vs. real closing price for Trelleborg (2012-02-22 to 2013-02-20).

0 50 100 150 200 25041

42

43

44

45

46

47

48

49

50

TeliaSonera

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25055

60

65

70

75

80

85

90

95

Trelleborg

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

44

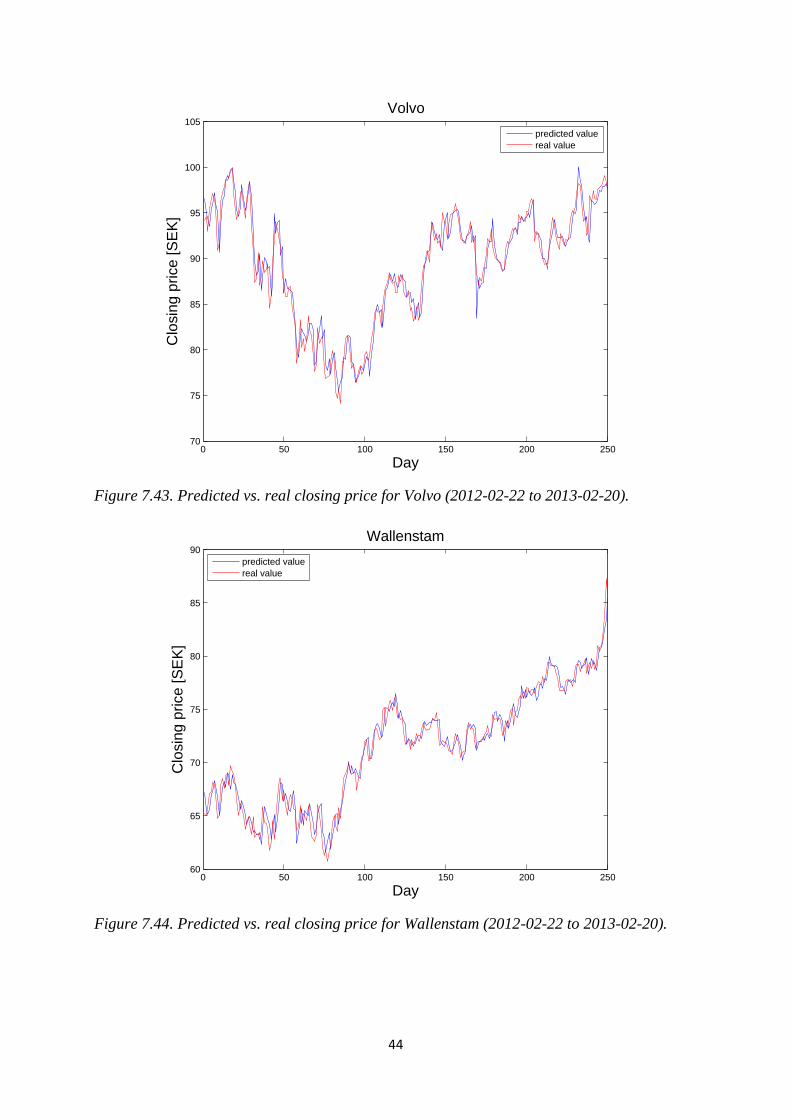

Figure 7.43. Predicted vs. real closing price for Volvo (2012-02-22 to 2013-02-20).

Figure 7.44. Predicted vs. real closing price for Wallenstam (2012-02-22 to 2013-02-20).

0 50 100 150 200 25070

75

80

85

90

95

100

105

Volvo

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

0 50 100 150 200 25060

65

70

75

80

85

90

Wallenstam

Day

Clo

sin

g p

rice

[S

EK

]

predicted value

real value

45

8.2 Yield using the model

Figure 7.45. Yield for Alfa Laval using the model (2012-02-22 to 2013-02-20).

Figure 7.46. Yield for Alliance Oil using the model (2012-02-22 to 2013-02-20).

46

Figure 7.47. Yield for Assa Abloy using the model (2012-02-22 to 2013-02-20).

Figure 7.48. Yield for Atlas Copco using the model (2012-02-22 to 2013-02-20).

47

Figure 7.49. Yield for Axfood using the model (2012-02-22 to 2013-02-20).

Figure 7.50. Yield for Axis using the model (2012-02-22 to 2013-02-20).

48

Figure 7.51. Yield for BillerudKorsnäs using the model (2012-02-22 to 2013-02-20).

Figure 7.52. Yield for Boliden using the model (2012-02-22 to 2013-02-20).

49

Figure 7.53. Yield for Castellum using the model (2012-02-22 to 2013-02-20).

Figure 7.54. Yield for Electrolux using the model (2012-02-22 to 2013-02-20).

50

Figure 7.55. Yield for Elekta using the model (2012-02-22 to 2013-02-20).

Figure 7.56. Yield for Ericsson using the model (2012-02-22 to 2013-02-20).

51

Figure 7.57. Yield for Fabege using the model (2012-02-22 to 2013-02-20).

Figure 7.58. Yield for Getinge using the model (2012-02-22 to 2013-02-20).

52

Figure 7.59. Yield for H&M using the model (2012-02-22 to 2013-02-20).

Figure 7.60. Yield for Hakon Invest using the model (2012-02-22 to 2013-02-20).

53

Figure 7.61. Yield for Hexagon using the model (2012-02-22 to 2013-02-20).

Figure 7.62. Yield for Holmen using the model (2012-02-22 to 2013-02-20).

54

Figure 7.63. Yield for Hufvudstaden using the model (2012-02-22 to 2013-02-20).

Figure 7.64. Yield for Husqvarna using the model (2012-02-22 to 2013-02-20).

55

Figure 7.65. Yield for Industrivärden using the model (2012-02-22 to 2013-02-20).

Figure 7.66. Yield for Investor using the model (2012-02-22 to 2013-02-20).

56

Figure 7.67. Yield for Kinnevik using the model (2012-02-22 to 2013-02-20).

Figure 7.68. Yield for Latour using the model (2012-02-22 to 2013-02-20).

57

Figure 7.69. Yield for Lundbergföretagen using the model (2012-02-22 to 2013-02-20).

Figure 7.70. Yield for Meda using the model (2012-02-22 to 2013-02-20).

58

Figure 7.71. Yield for MTG using the model (2012-02-22 to 2013-02-20).

Figure 7.72. Yield for Peab using the model (2012-02-22 to 2013-02-20).

59

Figure 7.73. Yield for Ratos using the model (2012-02-22 to 2013-02-20).

Figure 7.74. Yield for SAAB using the model (2012-02-22 to 2013-02-20).

60

Figure 7.75. Yield for Sandvik using the model (2012-02-22 to 2013-02-20).

Figure 7.76. Yield for SCA using the model (2012-02-22 to 2013-02-20).

0 50 100 150 200 2500

0.5

1

1.5

2

2.5

3

3.5x 10

4 Sandvik

Day

Yie

ld [

SE

K]

61

Figure 7.77. Yield for Scania using the model (2012-02-22 to 2013-02-20).

Figure 7.78. Yield for SEB using the model (2012-02-22 to 2013-02-20).

62

Figure 7.79. Yield for Securitas using the model (2012-02-22 to 2013-02-20).

Figure 7.80. Yield for Skanska using the model (2012-02-22 to 2013-02-20).

63

Figure 7.81. Yield for SKF using the model (2012-02-22 to 2013-02-20).

Figure 7.82. Yield for SSAB using the model (2012-02-22 to 2013-02-20).

0 50 100 150 200 2500

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2x 10

4 SSAB

Day

Yie

ld [

SE

K]

64

Figure 7.83. Yield for Swedbank using the model (2012-02-22 to 2013-02-20).

Figure 7.84. Yield for Swedish Match using the model (2012-02-22 to 2013-02-20).

65

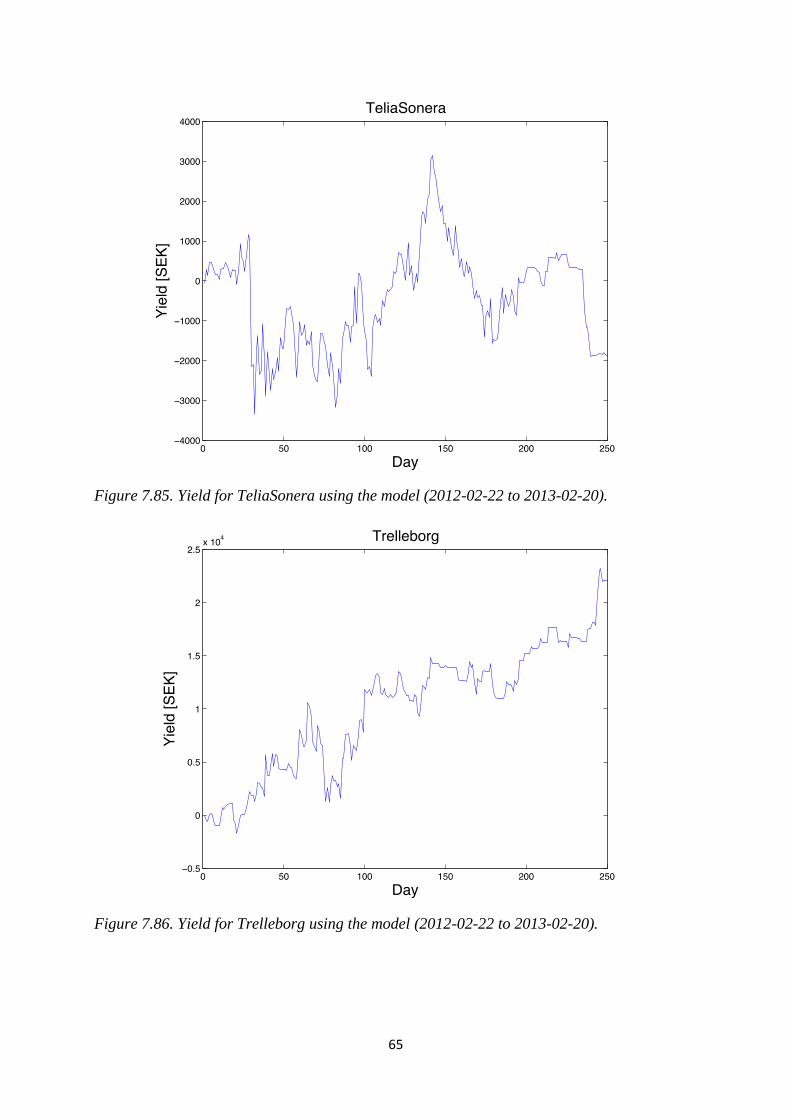

Figure 7.85. Yield for TeliaSonera using the model (2012-02-22 to 2013-02-20).

Figure 7.86. Yield for Trelleborg using the model (2012-02-22 to 2013-02-20).

66

Figure 7.87. Yield for Volvo using the model (2012-02-22 to 2013-02-20).

Figure 7.88. Yield for Wallenstam using the model (2012-02-22 to 2013-02-20).

67

8.3 Stock exchange indexes

Figure 7.89. OMX Stockholm index (2008-01-02 to 2013-02-21).

Figure 7.90. Shanghai index (2008-01-02 to 2013-02-21).

0 200 400 600 800 1000 1200 1400500

600

700

800

900

1000

1100

1200

1300

OMX Stockholm

Day

Inde

x [

SE

K]

0 200 400 600 800 1000 1200 14001500

2000

2500

3000

3500

4000

4500

5000

Shanghai index

Inde

x [

SE

K]

Day

68

Figure 7.91. Dow Jones index (2008-01-02 to 2013-02-21).

8.4 Conjuncture

Figure 7.92. Conjuncture index (Barometerindikatorn, 2008-01-02 to 2013-02-21).

0 200 400 600 800 1000 1200 14005.5

6

6.5

7

7.5

8

8.5

9

9.5x 10

4 Dow jones index

Inde

x [

SE

K]

Day

0 200 400 600 800 1000 1200 140070

75

80

85

90

95

100

105

110

115

120

Day

Inde

x

Conjuncture

69

8.5 Oil price per barrel

Figure 7.93. Oil price per barrel (2008-01-02 to 2013-02-21).

8.6 TCW index

Figure 7.89. TCW index (2008-01-02 to 2013-02-21).

0 200 400 600 800 1000 1200 1400200

300

400

500

600

700

800

900

Oil price per barrel

Day

Oil

price [

SE

K]

0 200 400 600 800 1000 1200 1400110

115

120

125

130

135

140

145

150

155

160

TCW index

Inde

x

Day

70

8.7 MATLAB code clc

clear all

close all

x = 1:250

load yalfa %Vector with predicted closing prices for 2012-02-22 to 2013-02-

20

load yalfa2 %Vector with real closing prices for 2012-02-22 to 2013-02-20

plot(x,yalfa)

hold on

plot(x,yalfa2,'r')

title('Alfa laval','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value')

set(gcf,'color',[1 1 1])

load yalliance %Vector with predicted closing prices for 2012-02-22 to

2013-02-20

load yalliance2 %Vector with real closing prices for 2012-02-22 to 2013-02-

20

figure()

plot(x,yalliance)

hold on

plot(x,yalliance2,'r')

title('Alliance Oil','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value')

set(gcf,'color',[1 1 1])

load yassa %Vector with predicted closing prices for 2012-02-22 to 2013-02-

20

load yassa2 %Vector with real closing prices for 2012-02-22 to 2013-02-20

figure()

plot(x,yassa)

hold on

plot(x,yassa2,'r')

title('Assa Abloy','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value','Location','NorthWest')

set(gcf,'color',[1 1 1])

71

load yatlas %Vector with predicted closing prices for 2012-02-22 to 2013-

02-20

load yatlas2 %Vector with real closing prices for 2012-02-22 to 2013-02-20

figure()

plot(x,yatlas)

hold on

plot(x,yatlas2,'r')

title('Atlas Copco','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value','Location','NorthWest')

set(gcf,'color',[1 1 1])

load yaxfood %Vector with predicted closing prices for 2012-02-22 to 2013-

02-20

load yaxfood2 %Vector with real closing prices for 2012-02-22 to 2013-02-20

figure()

plot(x,yaxfood)

hold on

plot(x,yaxfood2,'r')

title('Axfood','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value','Location','NorthWest')

set(gcf,'color',[1 1 1])

load yaxis %Vector with predicted closing prices for 2012-02-22 to 2013-02-

20

load yaxis2 %Vector with real closing prices for 2012-02-22 to 2013-02-20

figure()

plot(x,yaxis)

hold on

plot(x,yaxis2,'r')

title('Axis','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value')

set(gcf,'color',[1 1 1])

load ybillerud %Vector with predicted closing prices for 2012-02-22 to

2013-02-20

load ybillerud2 %Vector with real closing prices for 2012-02-22 to 2013-02-

20

figure()

plot(x,ybillerud)

hold on

plot(x,ybillerud2,'r')

title('BillerudKorsn‰s','fontsize',16)

xlabel('Day','fontsize',16)

72

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value')

set(gcf,'color',[1 1 1])

load yboliden %Vector with predicted closing prices for 2012-02-22 to 2013-

02-20

load yboliden2 %Vector with real closing prices for 2012-02-22 to 2013-02-

20

figure()

plot(x,yboliden)

hold on

plot(x,yboliden2,'r')

title('Boliden','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value','Location','NorthWest')

set(gcf,'color',[1 1 1])

load ycastellum %Vector with predicted closing prices for 2012-02-22 to

2013-02-20

load ycastellum2 %Vector with real closing prices for 2012-02-22 to 2013-

02-20

figure()

plot(x,ycastellum)

hold on

plot(x,ycastellum2,'r')

title('Castellum','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value')

set(gcf,'color',[1 1 1])

load yelectro %Vector with predicted closing prices for 2012-02-22 to 2013-

02-20

load yelectro2 %Vector with real closing prices for 2012-02-22 to 2013-02-

20

figure()

plot(x,yelectro)

hold on

plot(x,yelectro2,'r')

title('Electrolux','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value','Location','NorthWest')

set(gcf,'color',[1 1 1])

load yelekta %Vector with predicted closing prices for 2012-02-22 to 2013-

73

02-20

load yelekta2 %Vector with real closing prices for 2012-02-22 to 2013-02-20

figure()

plot(x,yelekta)

hold on

plot(x,yelekta2,'r')

title('Elekta','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)

legend('predicted value','real value')

set(gcf,'color',[1 1 1])

load yeric %Vector with predicted closing prices for 2012-02-22 to 2013-02-

20

load yeric2 %Vector with real closing prices for 2012-02-22 to 2013-02-20

figure()

plot(x,yeric)

hold on

plot(x,yeric2,'r')

title('Ericsson','fontsize',16)

xlabel('Day','fontsize',16)

ylabel('Closing price [SEK]','fontsize',16)