predictive analytics milliman risk score and hannover re 4 - predictive... · predictive analytics...

TRANSCRIPT

Predictive AnalyticsMilliman Risk Score and Hannover Re

November 18, 2016Eric Carlson & Sean Conrad

Agenda

Why Risk Score

What is Risk Score

Retrospective Study Results

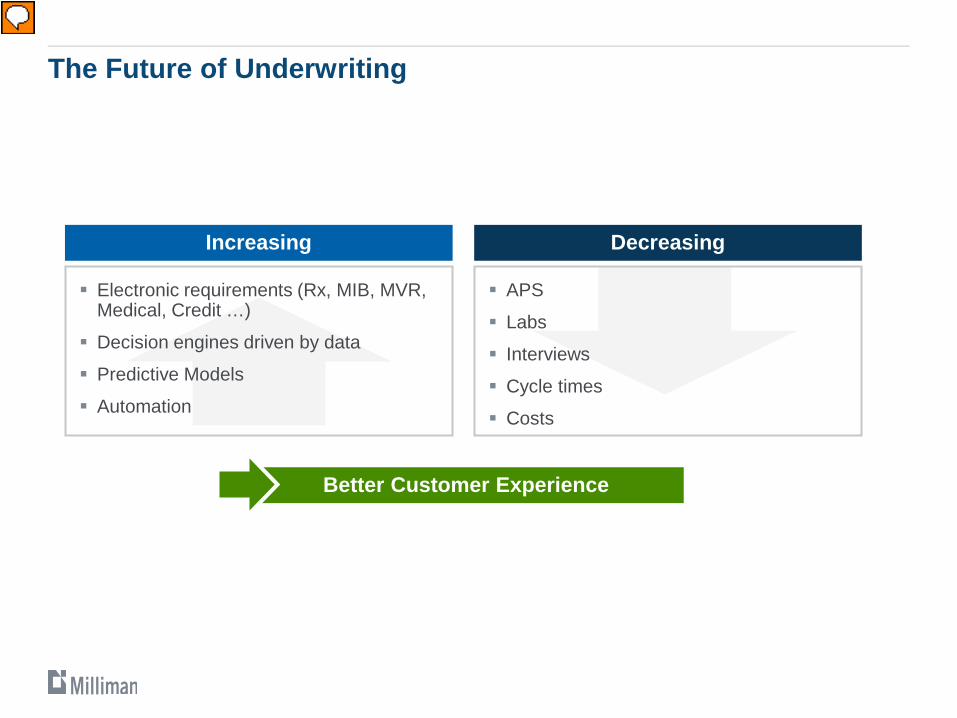

The Future of Underwriting

Electronic requirements (Rx, MIB, MVR, Medical, Credit …)

Decision engines driven by data

Predictive Models

Automation

Increasing

APS

Labs

Interviews

Cycle times

Costs

Decreasing

Better Customer Experience

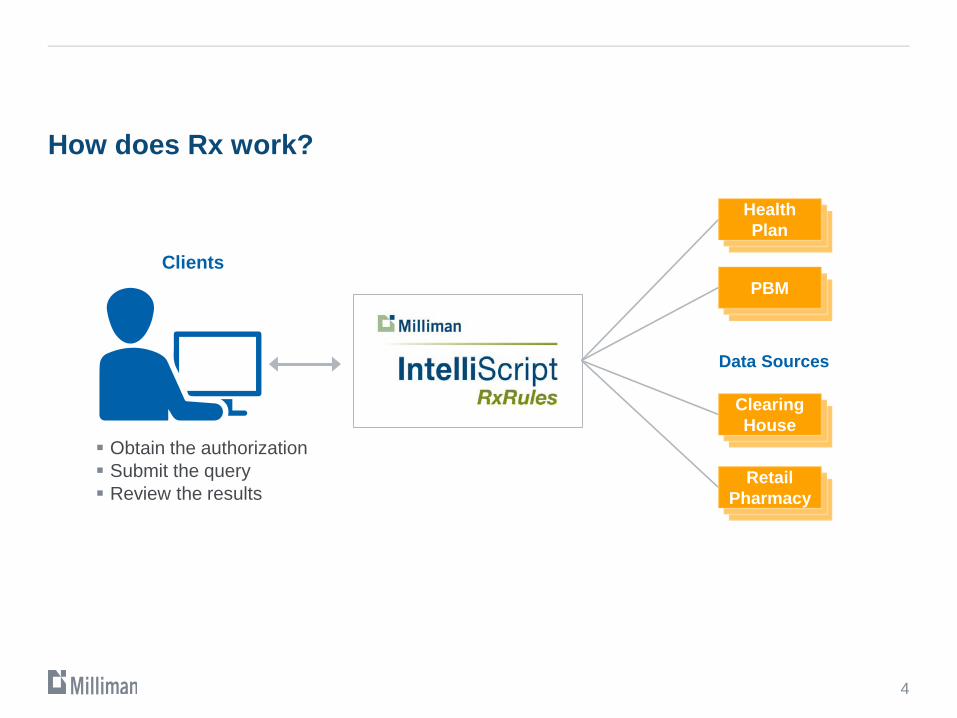

How does Rx work?

Obtain the authorization Submit the query Review the results

Clients

Health Plan

PBM

Clearing House

RetailPharmacy

Data Sources

4

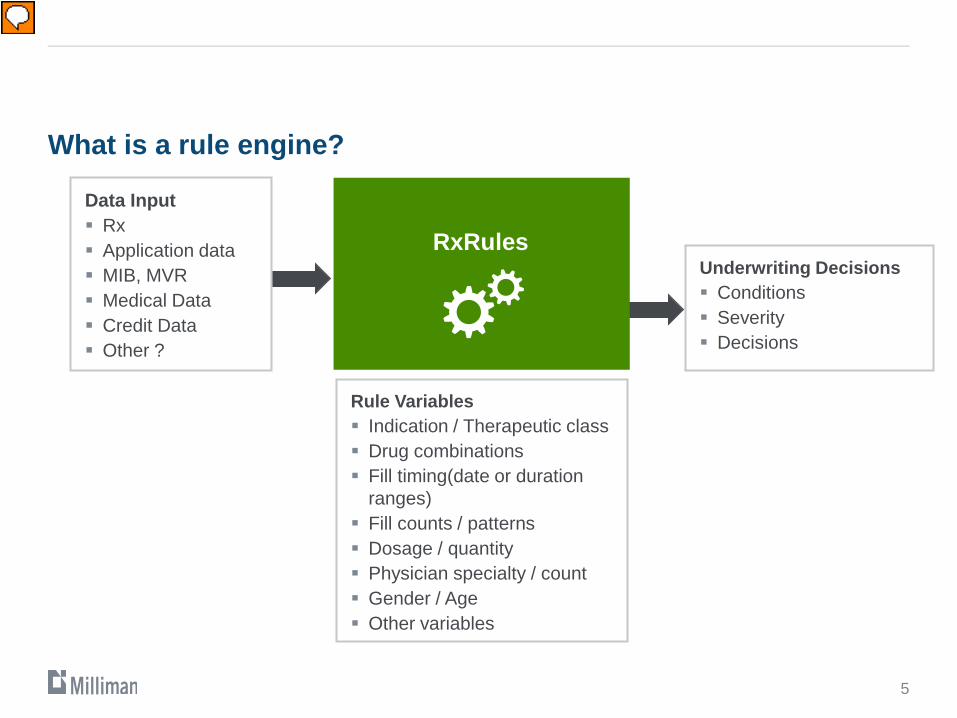

What is a rule engine?

RxRules

Data Input Rx Application data MIB, MVR Medical Data Credit Data Other ?

Underwriting Decisions Conditions Severity Decisions

Rule Variables Indication / Therapeutic class Drug combinations Fill timing(date or duration

ranges) Fill counts / patterns Dosage / quantity Physician specialty / count Gender / Age Other variables

5

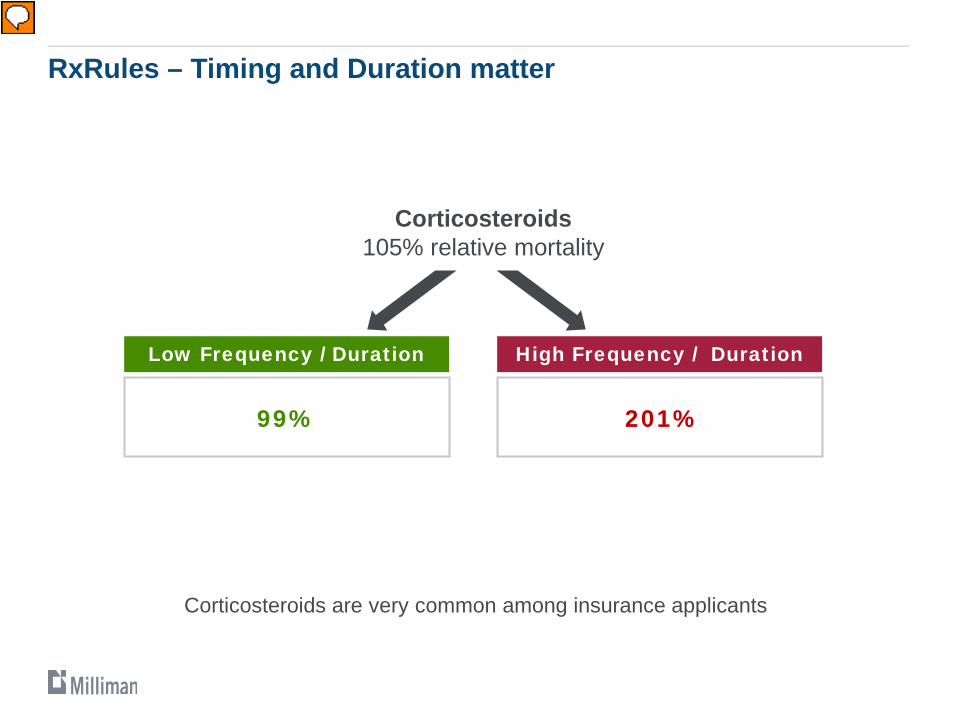

RxRules – Timing and Duration matter

Corticosteroids are very common among insurance applicants

Corticosteroids105% relative mortality

Low Frequency / Duration

99%

High Frequency / Duration

201%

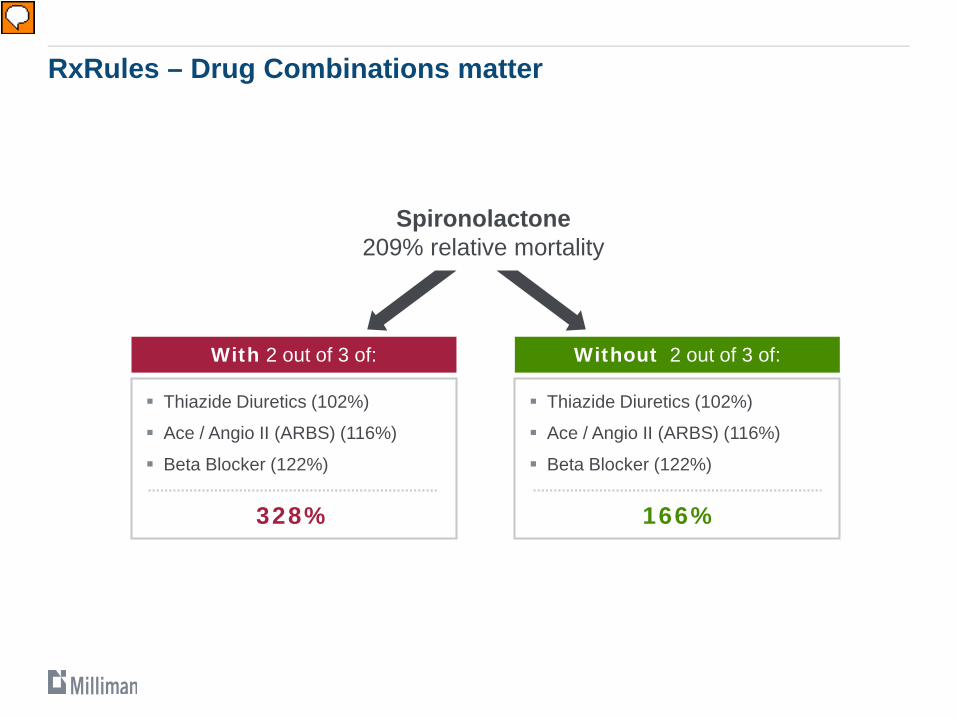

RxRules – Drug Combinations matter

Spironolactone209% relative mortality

Thiazide Diuretics (102%)

Ace / Angio II (ARBS) (116%)

Beta Blocker (122%)

With 2 out of 3 of:

328%

Thiazide Diuretics (102%)

Ace / Angio II (ARBS) (116%)

Beta Blocker (122%)

Without 2 out of 3 of:

166%

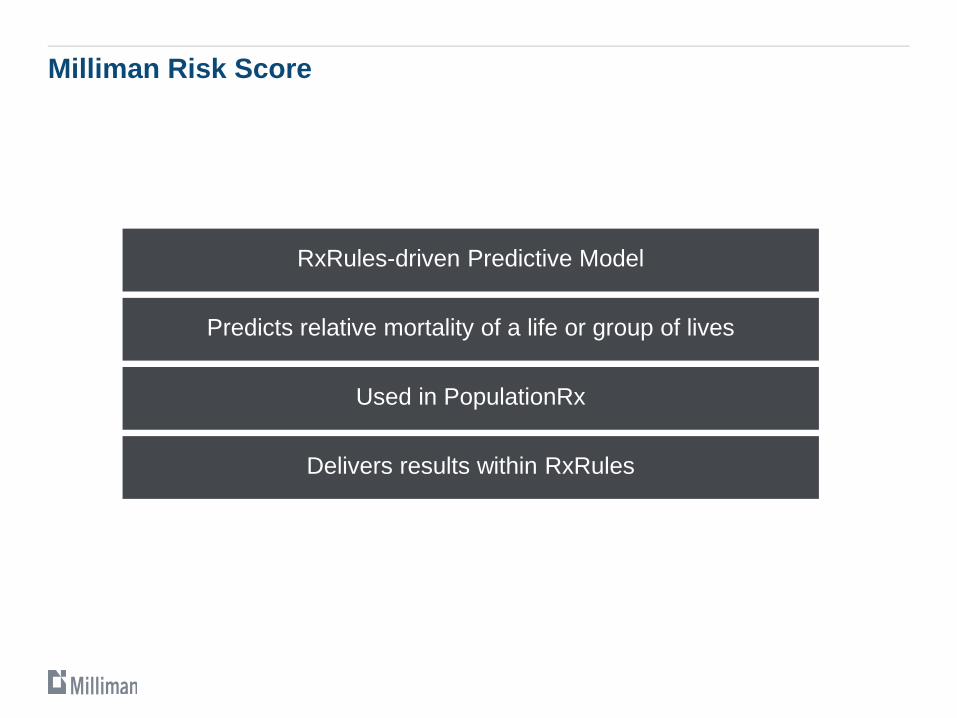

Milliman Risk Score

RxRules-driven Predictive Model

Predicts relative mortality of a life or group of lives

Used in PopulationRx

Delivers results within RxRules

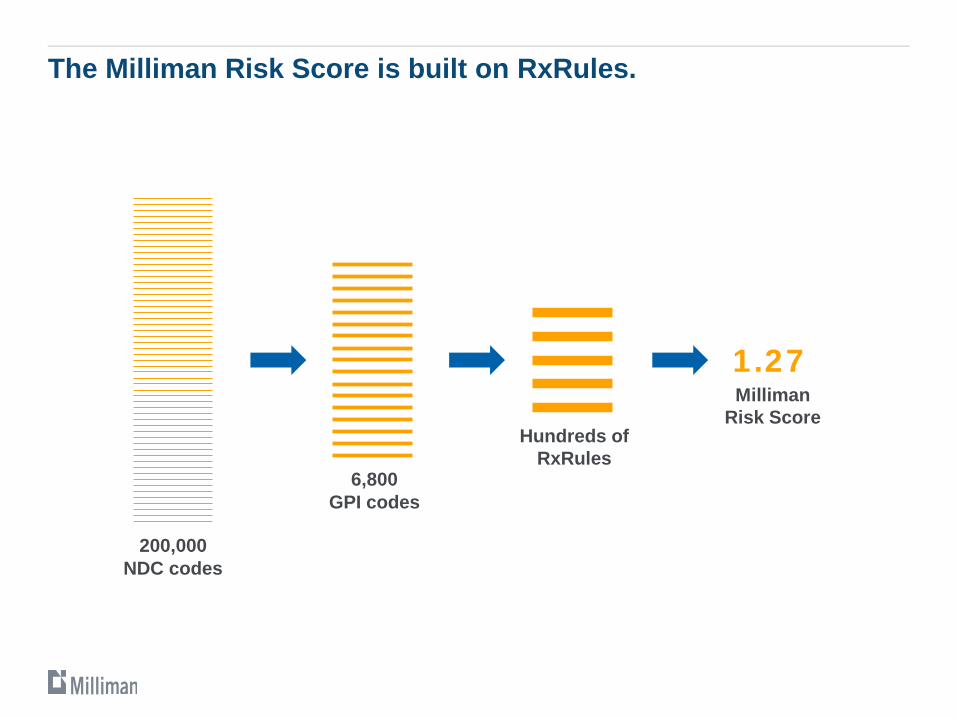

The Milliman Risk Score is built on RxRules.

Milliman Risk Score

200,000NDC codes

6,800GPI codes

Hundreds of RxRules

1.27

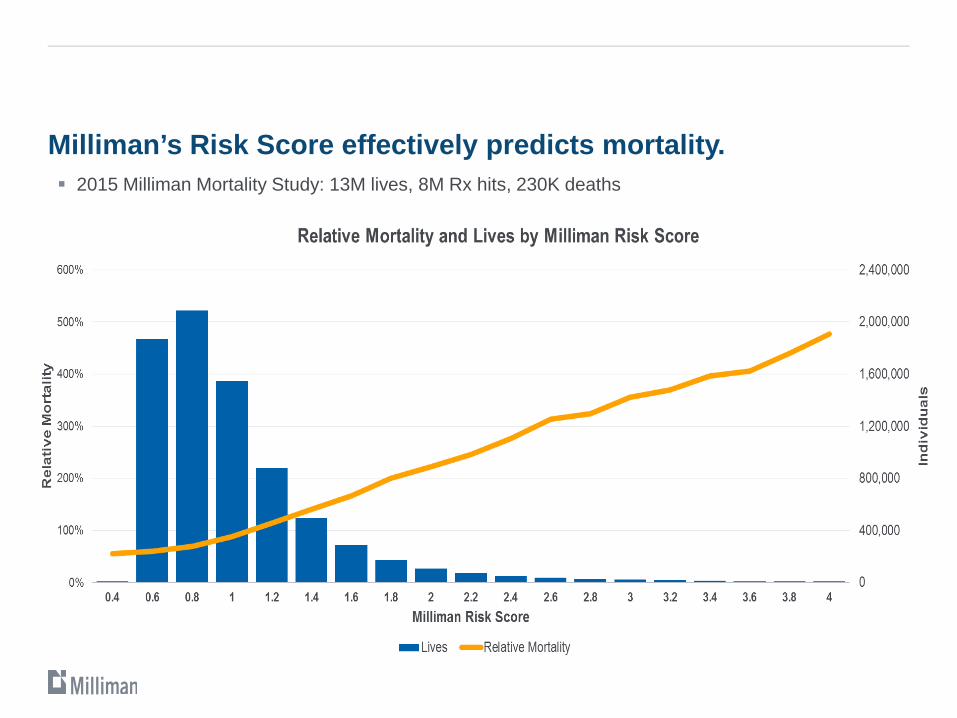

Milliman’s Risk Score effectively predicts mortality. 2015 Milliman Mortality Study: 13M lives, 8M Rx hits, 230K deaths

Hannover Re AnalysisIndependent Validation of Milliman Risk Score

Milliman RxRules & Risk ScoreModel Validation

Over 13 million records representing IntelliScript Rx queries

Entry years 2005 – 2013

Exposure period 2005 – 2014

230,000+ deaths

Over 52 million exposure years

6 lines of business: − Life− Health− LTC− Final Expense− Med supp− DI

Milliman included risk score, hit status, and most severe drug (red/yellow/green)12

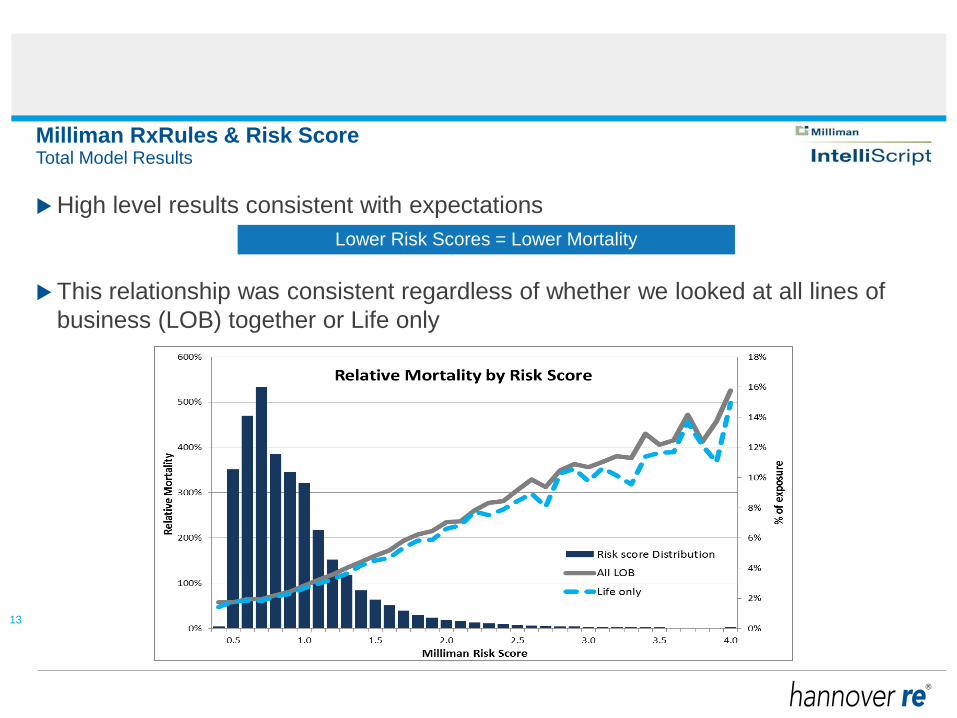

Milliman RxRules & Risk Score

High level results consistent with expectations

This relationship was consistent regardless of whether we looked at all lines of business (LOB) together or Life only

Total Model Results

13

Lower Risk Scores = Lower Mortality

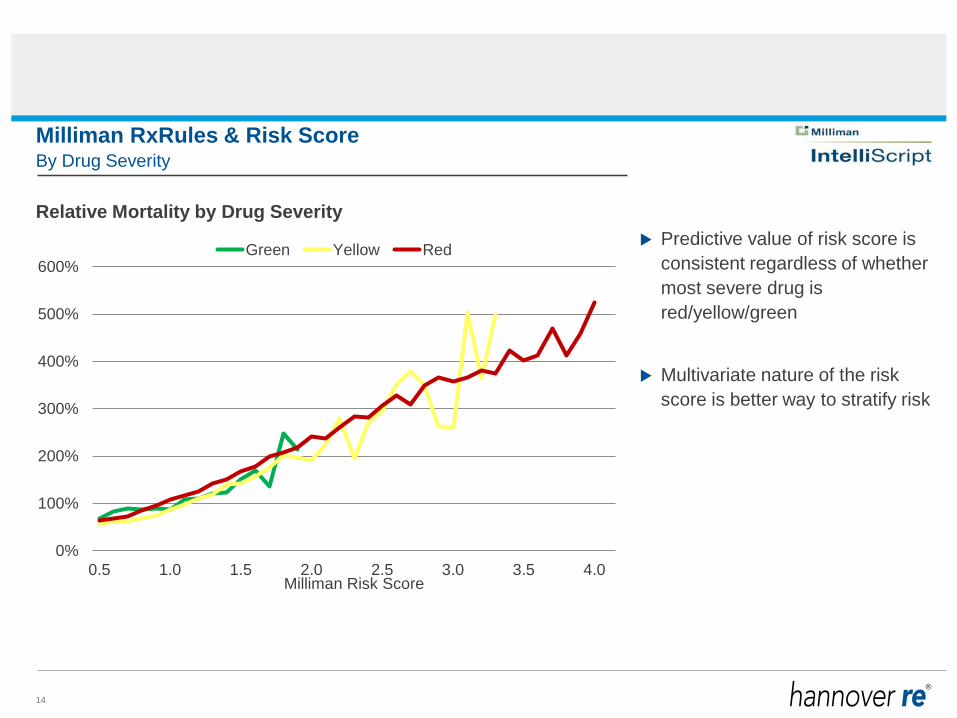

Milliman RxRules & Risk Score

Relative Mortality by Drug Severity Predictive value of risk score is

consistent regardless of whether most severe drug is red/yellow/green

Multivariate nature of the risk score is better way to stratify risk

By Drug Severity

0%

100%

200%

300%

400%

500%

600%

0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0Milliman Risk Score

Green Yellow Red

14

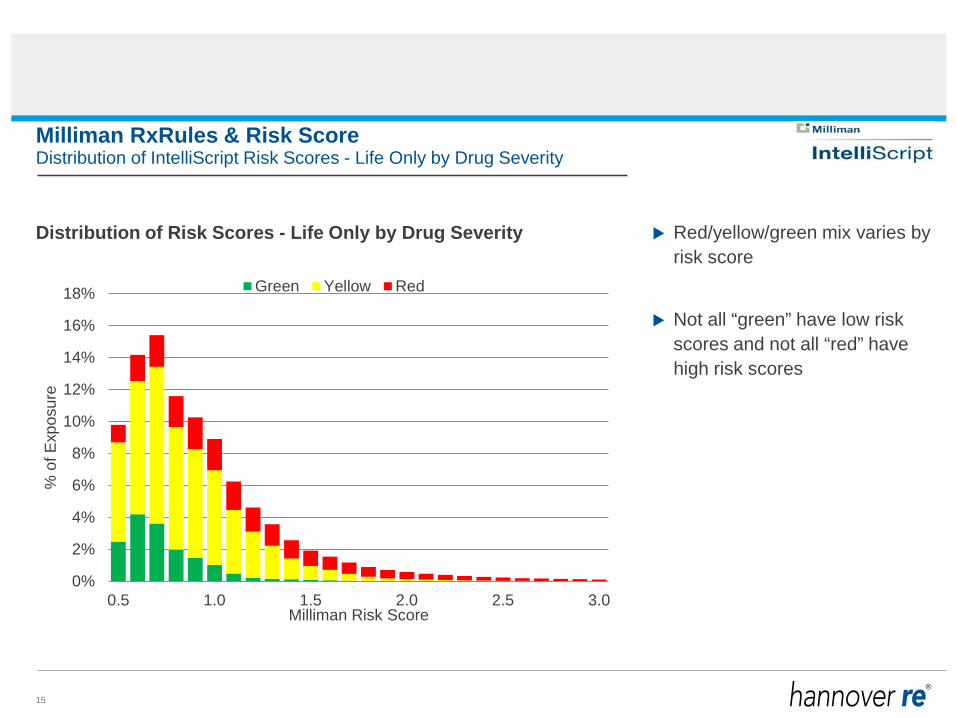

Milliman RxRules & Risk Score

Distribution of Risk Scores - Life Only by Drug Severity Red/yellow/green mix varies by risk score

Not all “green” have low risk scores and not all “red” have high risk scores

Distribution of IntelliScript Risk Scores - Life Only by Drug Severity

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0.5 1.0 1.5 2.0 2.5 3.0

% o

f Exp

osur

e

Milliman Risk Score

Green Yellow Red

15

Milliman RxRules & Risk Score

Quick, efficient, and consistent method for evaluating Rx

Synthesize complex aspects of Rx history (# of refills, who prescribed?, etc.)

Triage Rx info – identify “clean” Rx histories vs. those to review in more detail

Benefits & Potential Use Cases

Increase acceptance rates and/or decrease mortality expectation

Case Study Background

Simplified Issue writer

Cases are either issued or declined – no rate classes

Decisions are almost exclusively automatedUsed application, Rx / RxRules, plus MIB and MVR as decision elements

230,000 lives

1,200 deaths – deaths for issued policies AND declined policies

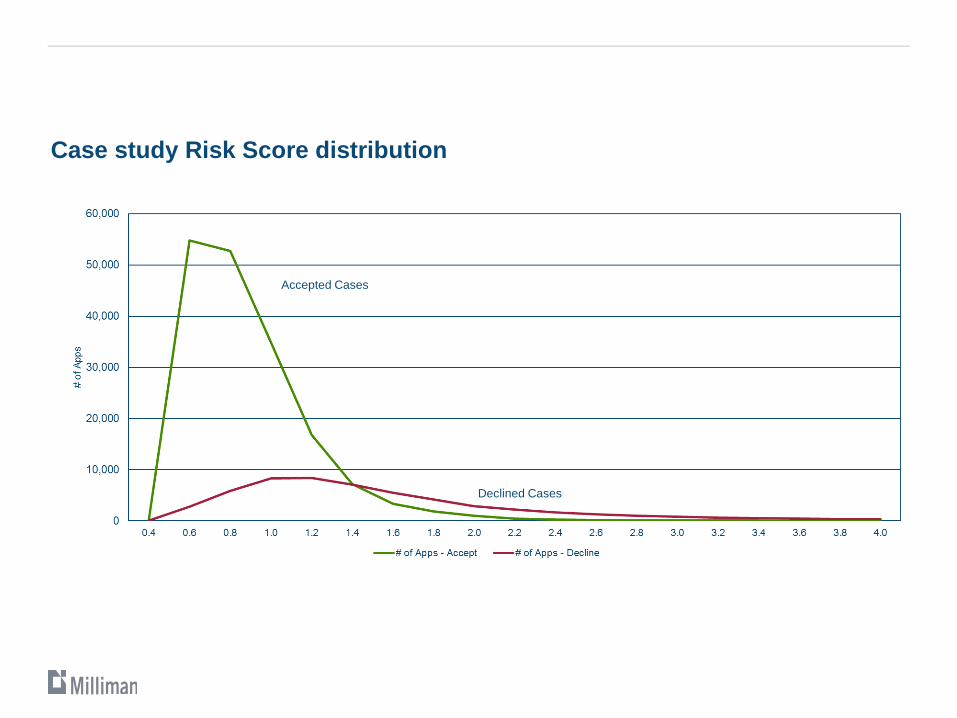

Case study Risk Score distribution

Accepted Cases

Declined Cases

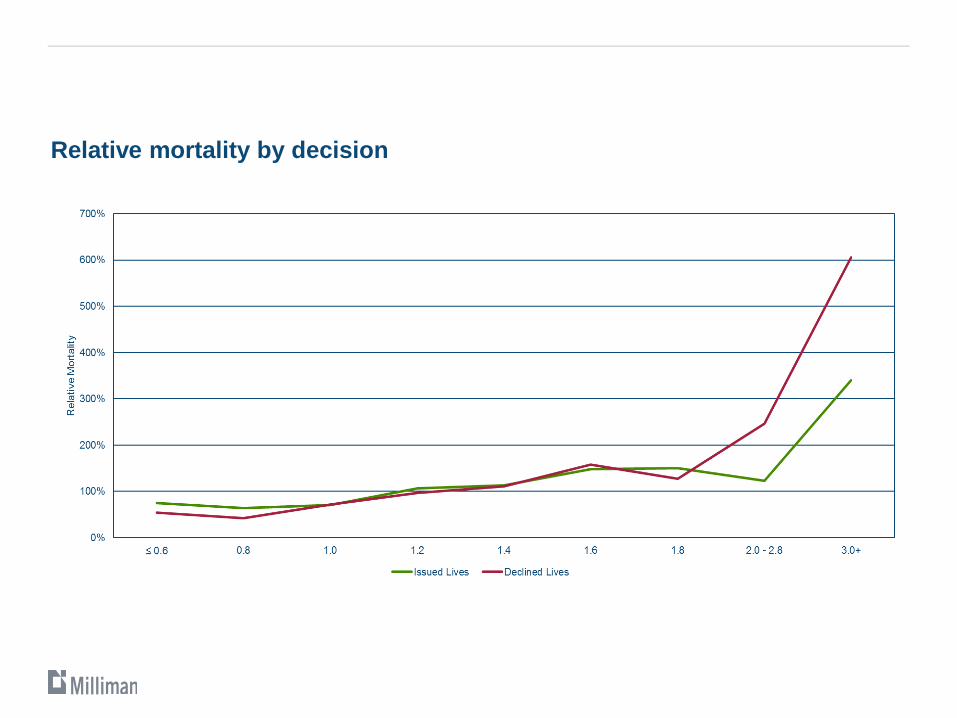

Relative mortality by decision

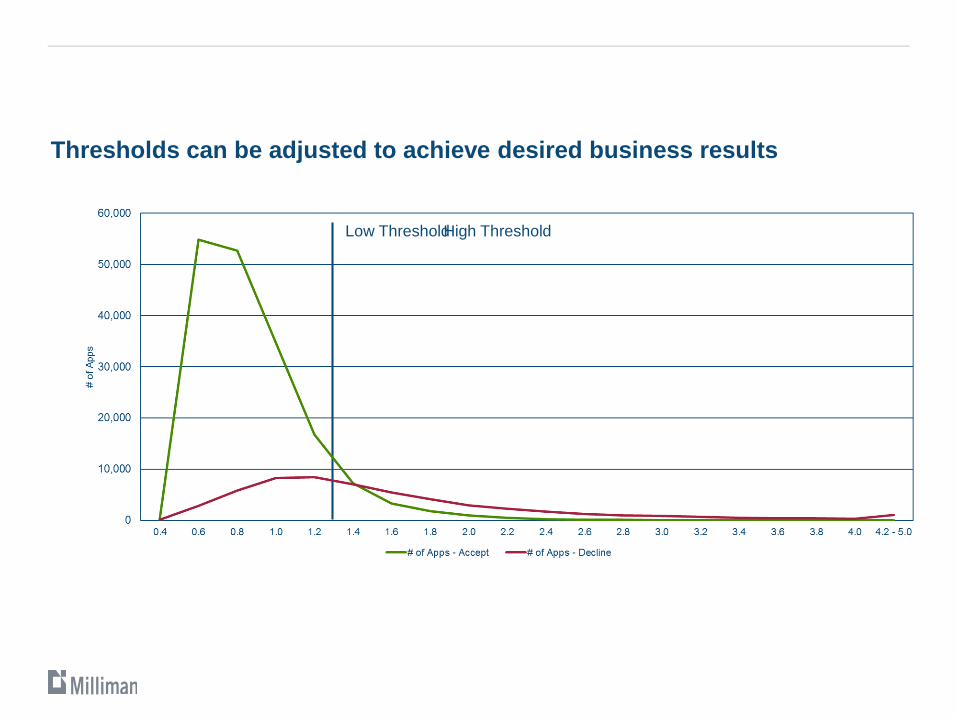

Thresholds can be adjusted to achieve desired business results

Low ThresholdHigh Threshold

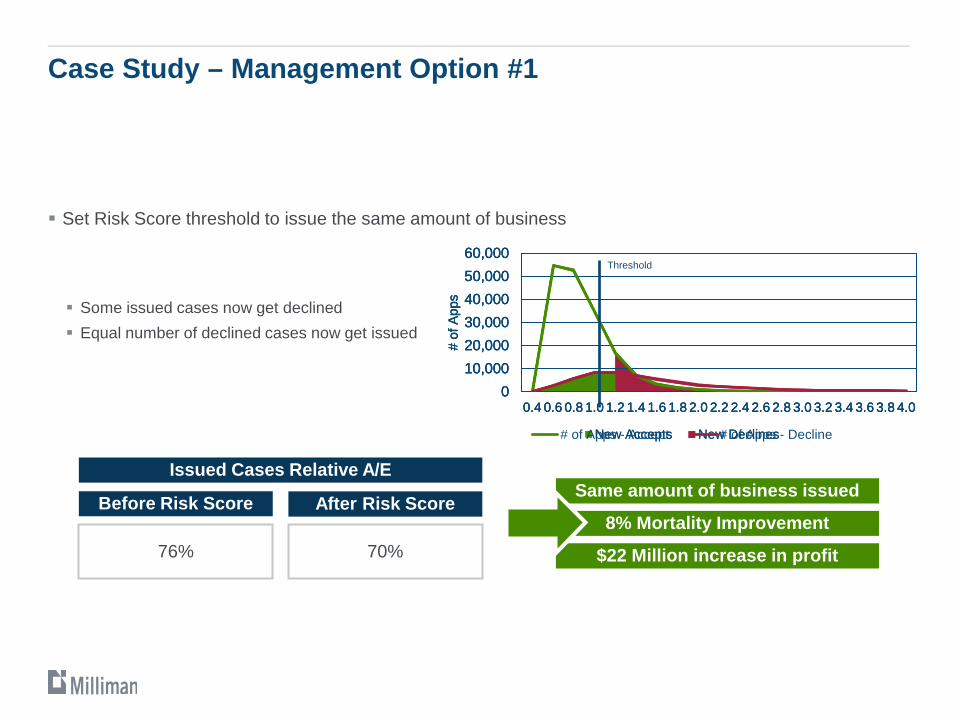

Case Study – Management Option #1

Set Risk Score threshold to issue the same amount of business

Some issued cases now get declined Equal number of declined cases now get issued

010,00020,00030,00040,00050,00060,000

0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8 4.0

# of

App

sNew Accepts New Declines

010,00020,00030,00040,00050,00060,000

0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8 4.0

# of

App

sNew Accepts New Declines

010,00020,00030,00040,00050,00060,000

0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8 4.0

# of

App

s# of Apps - Accept # of Apps - Decline

Threshold

76%

Before Risk Score

70%

After Risk Score

Issued Cases Relative A/ESame amount of business issued

$22 Million increase in profit

8% Mortality Improvement

Set Risk Score threshold to maintain the same mortality A/E

Some issued cases now get declined More declined cases now get issued

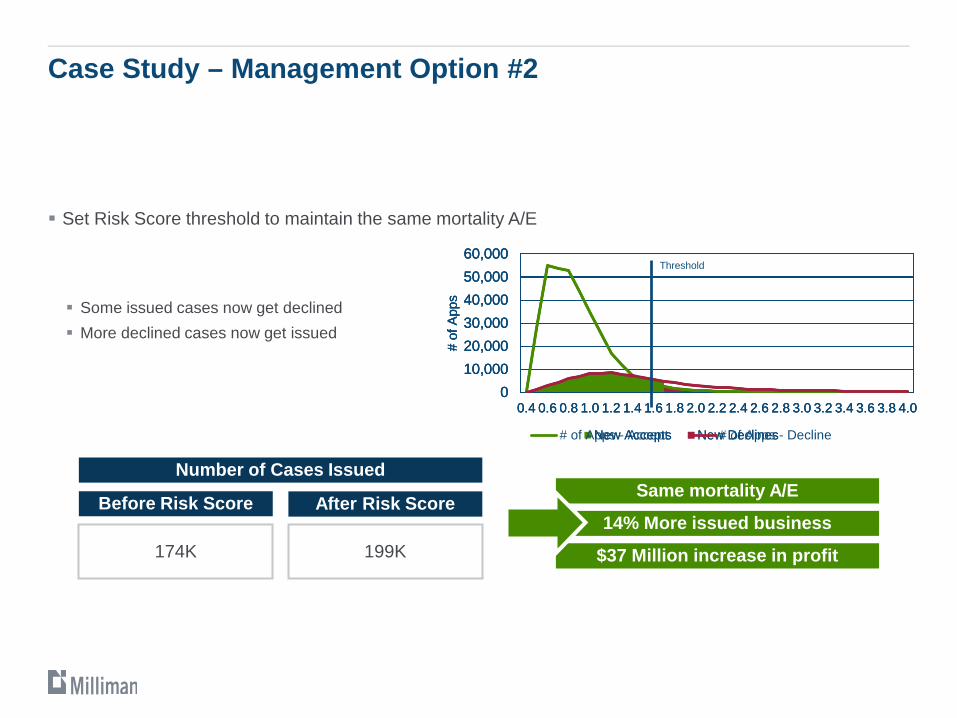

Case Study – Management Option #2

010,00020,00030,00040,00050,00060,000

0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8 4.0

# of

App

sNew Accepts New Declines

010,00020,00030,00040,00050,00060,000

0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8 4.0

# of

App

sNew Accepts New Declines

010,00020,00030,00040,00050,00060,000

0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8 4.0

# of

App

s# of Apps - Accept # of Apps - Decline

Threshold

174K

Before Risk Score

199K

After Risk Score

Number of Cases IssuedSame mortality A/E

$37 Million increase in profit

14% More issued business

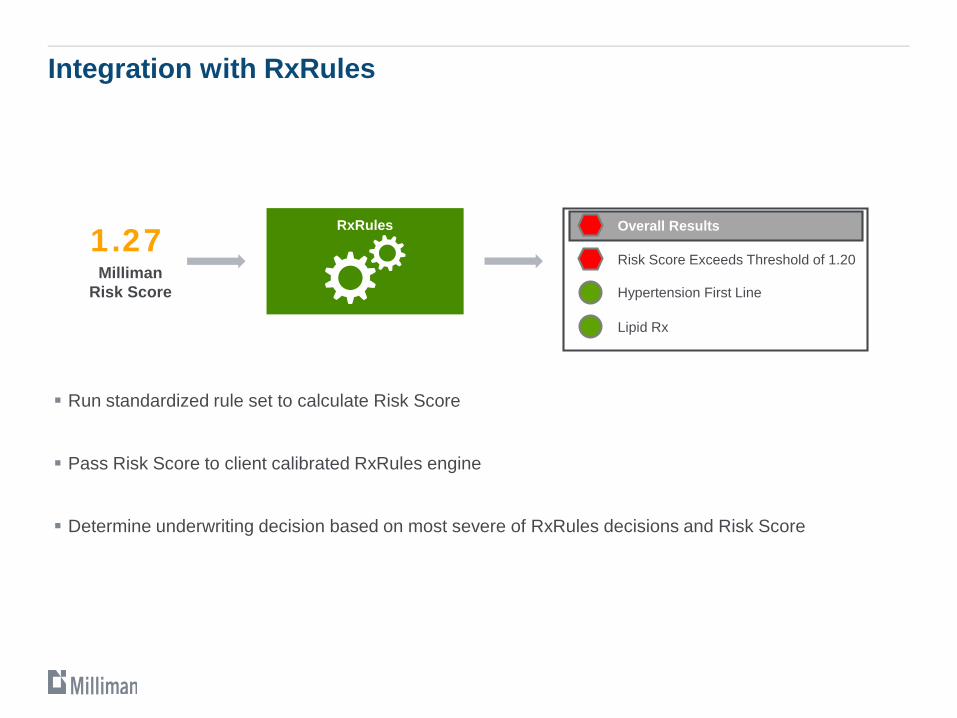

Integration with RxRules

Run standardized rule set to calculate Risk Score

Pass Risk Score to client calibrated RxRules engine

Determine underwriting decision based on most severe of RxRules decisions and Risk Score

RxRules

Milliman Risk Score

1.27Hypertension First Line

Lipid Rx

Risk Score Exceeds Threshold of 1.20

Overall Results

24

Proprietary and Confidential.

Contact Info

Eric Carlson, FSA, MAAA Life Actuary

[email protected] (262) 641-3537

Sean Conrad, FSA, MAAA, FIA, CFA VP & Actuary

[email protected] (704) 731-6382