preliminary results 2007 1 annual results 27 th june 2007

TRANSCRIPT

1 Preliminary Results 2007

Annual ResultsAnnual Results2727thth June 2007 June 2007

2 Preliminary Results 2007

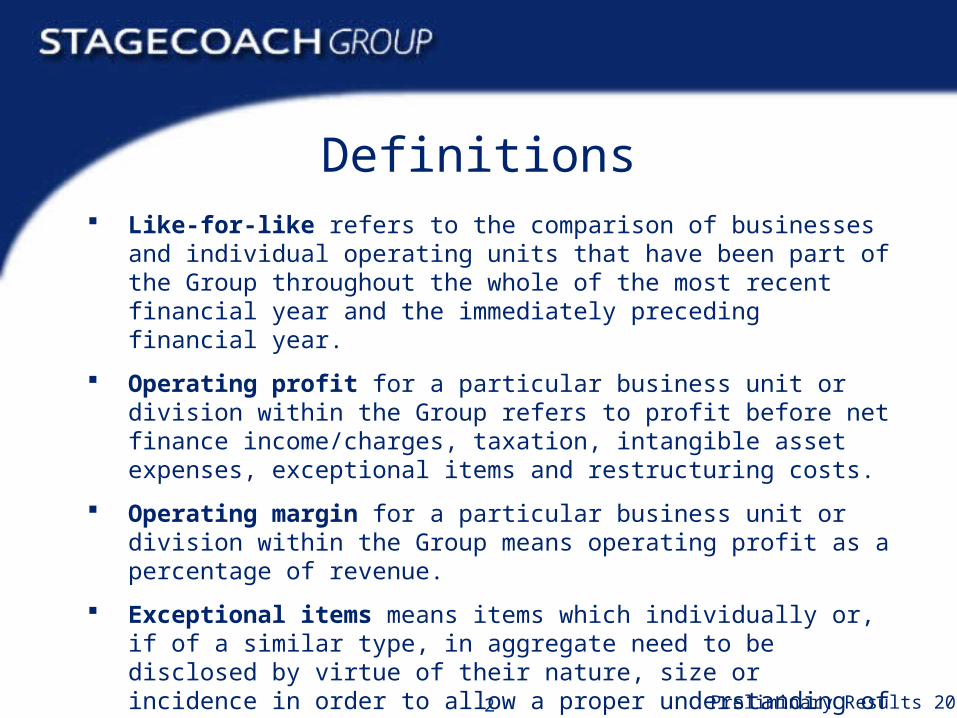

Definitions Like-for-like refers to the comparison of businesses and individual

operating units that have been part of the Group throughout the whole of the most recent financial year and the immediately preceding financial year.

Operating profit for a particular business unit or division within the Group refers to profit before net finance income/charges, taxation, intangible asset expenses, exceptional items and restructuring costs.

Operating margin for a particular business unit or division within the Group means operating profit as a percentage of revenue.

Exceptional items means items which individually or, if of a similar type, in aggregate need to be disclosed by virtue of their nature, size or incidence in order to allow a proper understanding of the underlying financial performance of the Group.

3 Preliminary Results 2007

Robert SpeirsRobert Speirs

ChairmanChairman

4 Preliminary Results 2007

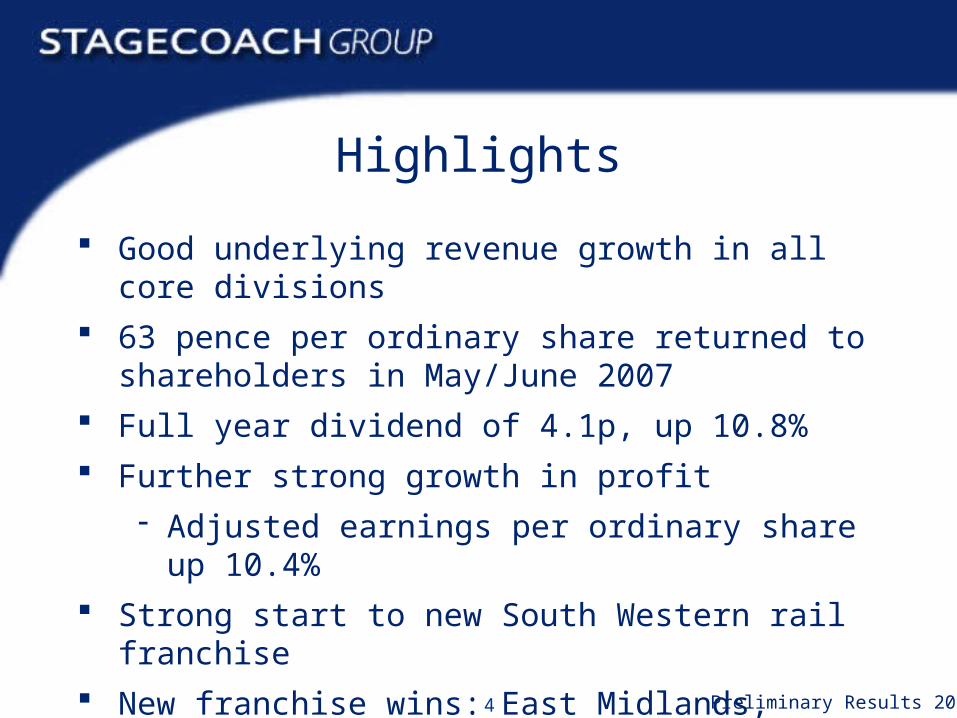

Highlights

Good underlying revenue growth in all core divisions

63 pence per ordinary share returned to shareholders in May/June 2007

Full year dividend of 4.1p, up 10.8%

Further strong growth in profit

Adjusted earnings per ordinary share up 10.4%

Strong start to new South Western rail franchise

New franchise wins: East Midlands, Manchester Metrolink

5 Preliminary Results 2007

Martin GriffithsMartin Griffiths

Finance DirectorFinance Director

6 Preliminary Results 2007

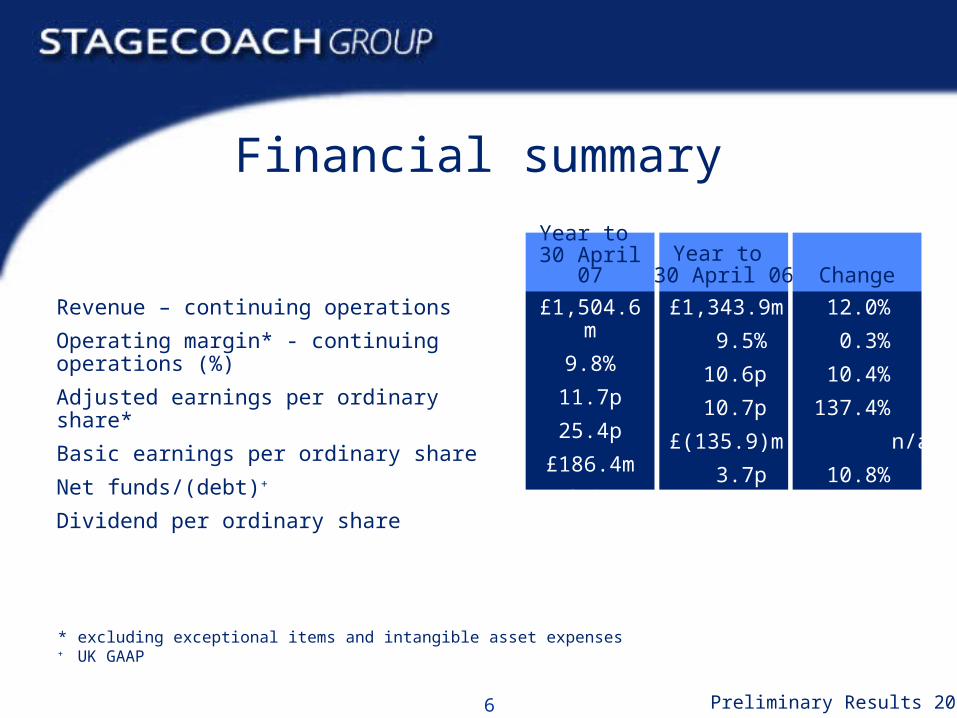

Financial summary

* excluding exceptional items and intangible asset expenses+ UK GAAP

Revenue – continuing operations

Operating margin* - continuing operations (%)

Adjusted earnings per ordinary share*

Basic earnings per ordinary share

Net funds/(debt)+

Dividend per ordinary share

Year to 30 April 07

Year to 30 April 06

£1,504.6m

9.8%

11.7p

25.4p

£186.4m

4.1p

£1,343.9m

9.5%

10.6p

10.7p

£(135.9)m

3.7p

Change

12.0%

0.3%

10.4%

137.4%

n/a

10.8%

7 Preliminary Results 2007

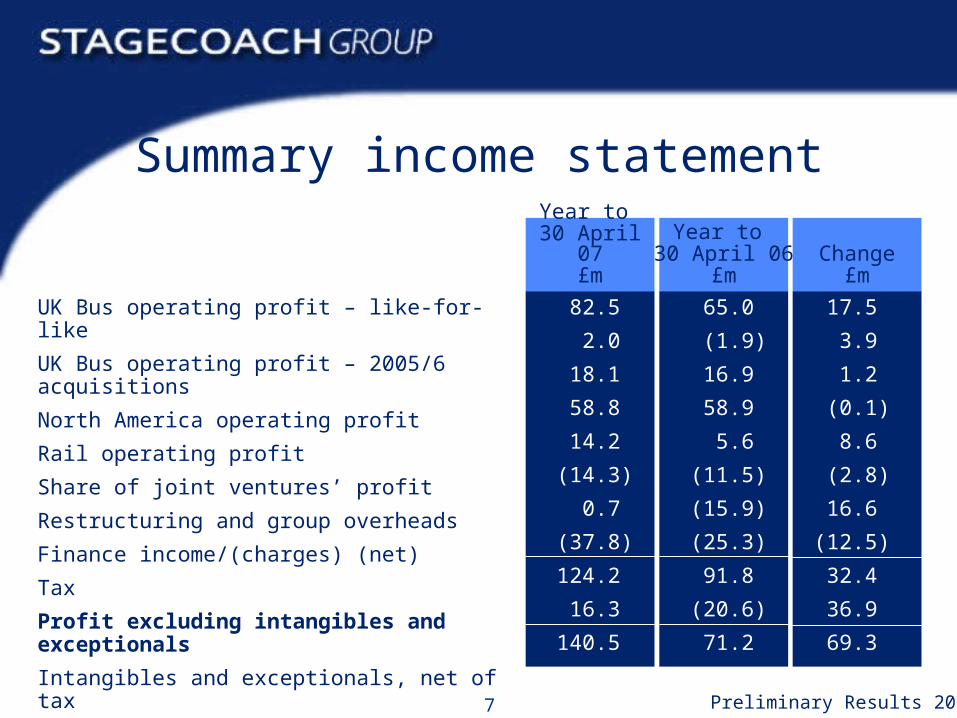

Summary income statement

UK Bus operating profit – like-for-like

UK Bus operating profit – 2005/6 acquisitions

North America operating profit

Rail operating profit

Share of joint ventures’ profit

Restructuring and group overheads

Finance income/(charges) (net)

Tax

Profit excluding intangibles and exceptionals

Intangibles and exceptionals, net of tax

Reported profit from continuing operations

Year to 30 April 07

£m

Year to 30 April 06

£m

82.5

2.0

18.1

58.8

14.2

(14.3)

0.7

(37.8)

124.2

16.3

140.5

65.0

(1.9)

16.9

58.9

5.6

(11.5)

(15.9)

(25.3)

91.8

(20.6)

71.2

Change£m

17.5

3.9

1.2

(0.1)

8.6

(2.8)

16.6

(12.5)

32.4

36.9

69.3

8 Preliminary Results 2007

Development of UK Bus

Operating profit increased

and £267.8m collected from London sale!

Operating profit:

Like-for-like

2005/06 acquisitions

London

Year to 30 April 07

£m

Year to 30 April 06

£m

82.5

2.0

5.2

89.7

65.0

(1.9)

23.6

86.7

Change£m

17.5

3.9

(18.4)

3.0

9 Preliminary Results 2007

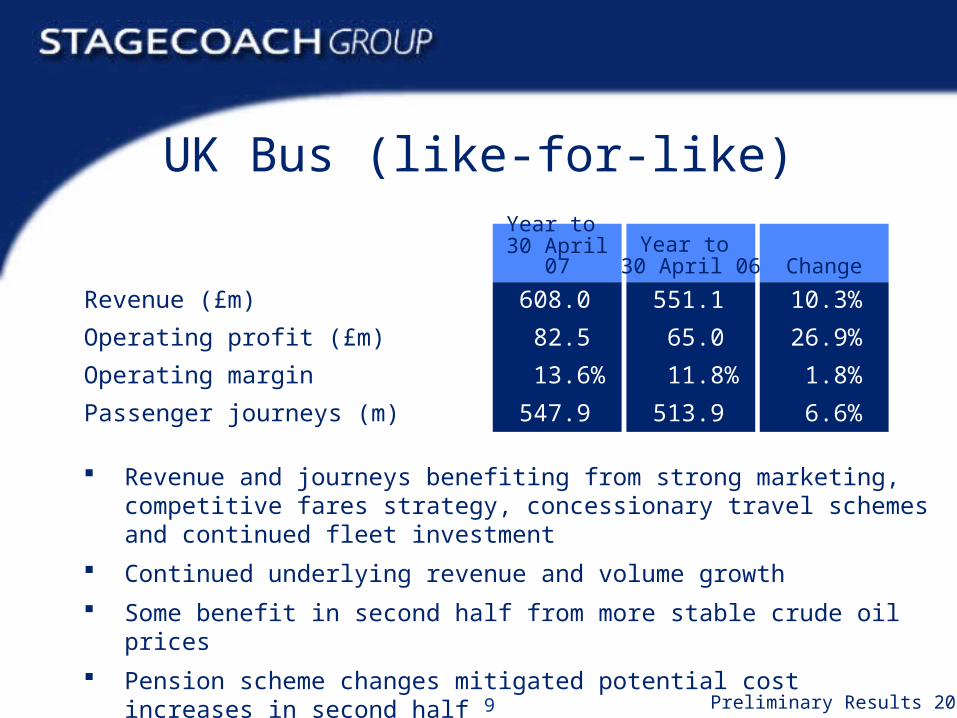

UK Bus (like-for-like)

Revenue and journeys benefiting from strong marketing, competitive fares strategy, concessionary travel schemes and continued fleet investment

Continued underlying revenue and volume growth

Some benefit in second half from more stable crude oil prices

Pension scheme changes mitigated potential cost increases in second half

Stable insurance & claims costs

Revenue (£m)

Operating profit (£m)

Operating margin

Passenger journeys (m)

Year to 30 April 07

Year to 30 April 06

608.0

82.5

13.6%

547.9

551.1

65.0

11.8%

513.9

Change

10.3%

26.9%

1.8%

6.6%

10 Preliminary Results 2007

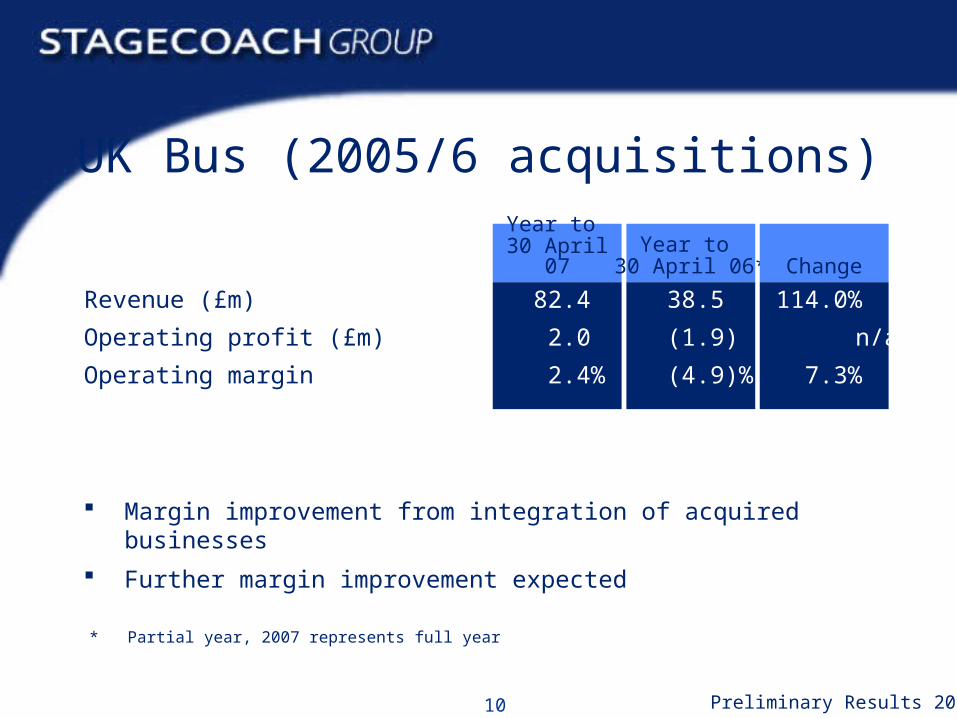

UK Bus (2005/6 acquisitions)

Margin improvement from integration of acquired businesses

Further margin improvement expected

Revenue (£m)

Operating profit (£m)

Operating margin

Year to 30 April 07

Year to 30 April 06*

82.4

2.0

2.4%

38.5

(1.9)

(4.9)%

Change

114.0%

n/a

7.3%

* Partial year, 2007 represents full year

11 Preliminary Results 2007

North America

Further margin improvement from optimising asset deployment

Double digit margin targeted by 30 April 2009

Excellent response in the US to Megabus

Launch of Splash Tours in New York

Revenue (US$m)

Like-for-like revenue (US$m)*

Operating profit (US$m)

Operating margin

Year to 30 April 07

Year to 30 April 06

463.6

455.6

34.6

7.5%

439.5

417.6

30.0

6.8%

Change

5.5%

9.1%

15.3%

0.7%

* Adjusted to exclude revenue from businesses sold or closed during the two years and to include revenue from Canada on a constant currency basis

12 Preliminary Results 2007

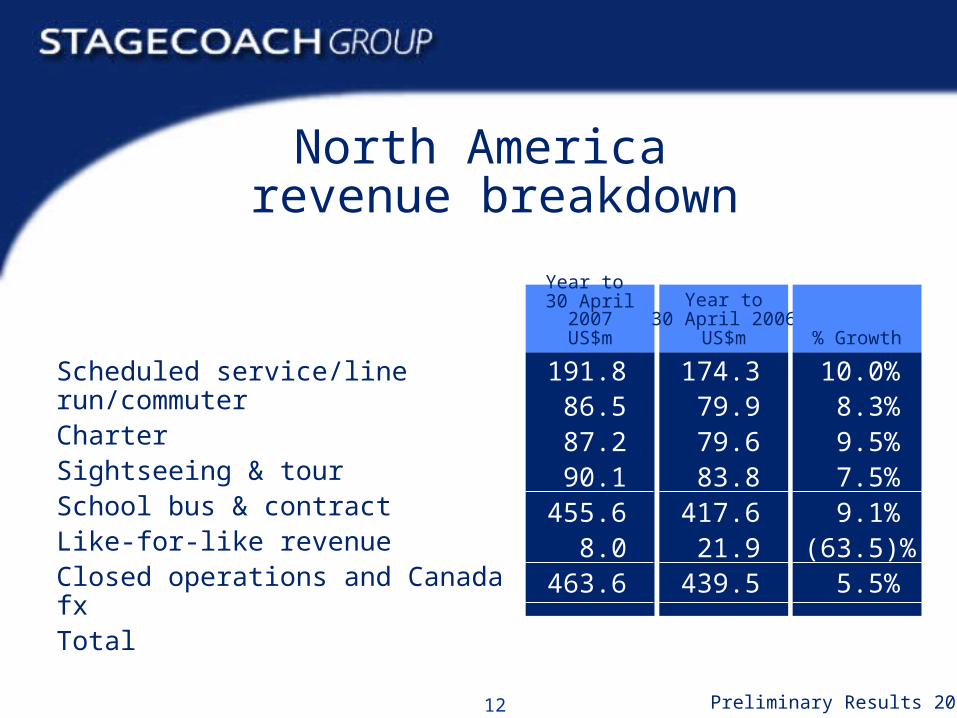

Scheduled service/line run/commuterCharterSightseeing & tourSchool bus & contractLike-for-like revenueClosed operations and Canada fxTotal

Year to 30 April

2007US$m

Year to30 April 2006

US$m

191.886.587.290.1

455.68.0

463.6

174.379.979.683.8

417.621.9

439.5

% Growth

10.0%8.3%9.5%7.5%9.1%

(63.5)%5.5%

North America revenue breakdown

13 Preliminary Results 2007

Rail (wholly-owned)

Strong start to new South Western franchise

Challenging but deliverable revenue and cost targets

Manchester Metrolink from July 2007

East Midlands from November 2007

Sheffield Supertram record passenger volumes

Revenue (£m)

Operating profit (£m)

Operating margin

Passenger miles (000’s)

Year to 30 April 07

Year to 30 April 06

571.5

58.8

10.3%

3,051.6

506.7

58.9

11.6%

2,802.1

Change

12.8%

(0.2)%

(1.3)%

8.9%

14 Preliminary Results 2007

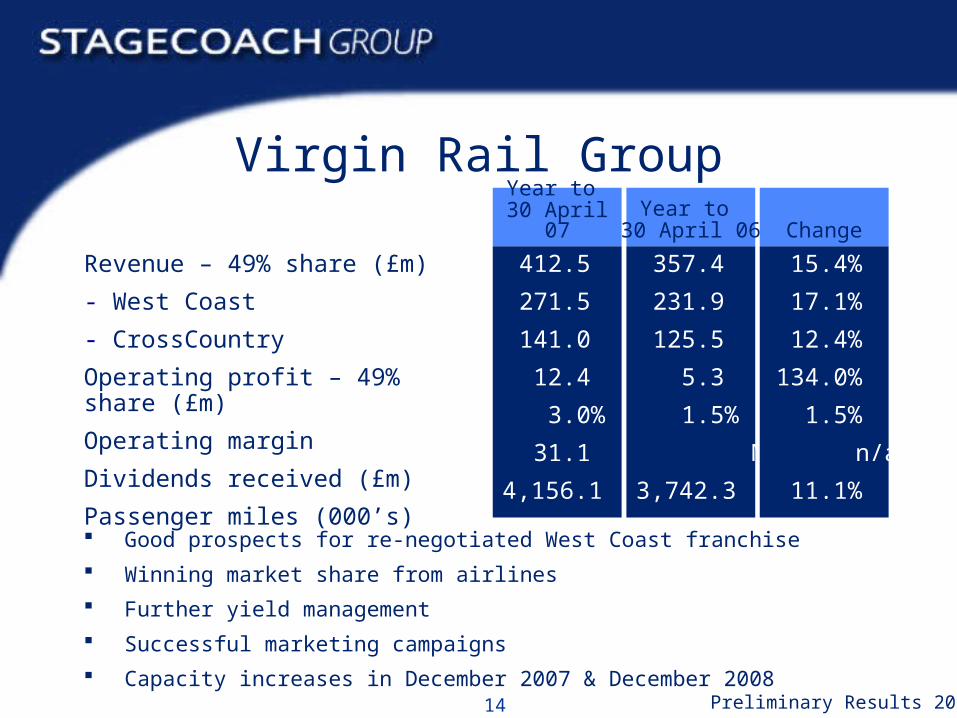

Virgin Rail Group

Good prospects for re-negotiated West Coast franchise

Winning market share from airlines

Further yield management

Successful marketing campaigns

Capacity increases in December 2007 & December 2008

Revenue – 49% share (£m)

- West Coast

- CrossCountry

Operating profit – 49% share (£m)

Operating margin

Dividends received (£m)

Passenger miles (000’s)

Year to 30 April 07

Year to 30 April 06

412.5

271.5

141.0

12.4

3.0%

31.1

4,156.1

357.4

231.9

125.5

5.3

1.5%

Nil

3,742.3

Change

15.4%

17.1%

12.4%

134.0%

1.5%

n/a

11.1%

15 Preliminary Results 2007

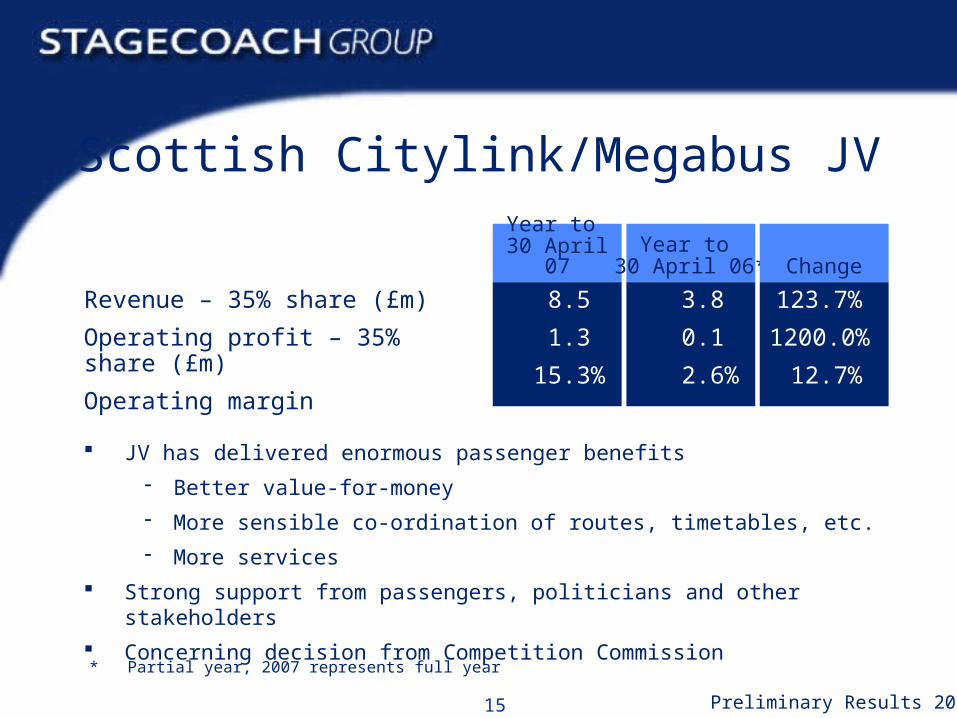

Scottish Citylink/Megabus JV

JV has delivered enormous passenger benefits

Better value-for-money

More sensible co-ordination of routes, timetables, etc.

More services

Strong support from passengers, politicians and other stakeholders

Concerning decision from Competition Commission

Revenue – 35% share (£m)

Operating profit – 35% share (£m)

Operating margin

Year to 30 April 07

Year to 30 April 06*

8.5

1.3

15.3%

3.8

0.1

2.6%

Change

123.7%

1200.0%

12.7%

* Partial year, 2007 represents full year

16 Preliminary Results 2007

Miscellaneous income statement items

Exceptional gains include sale of London Bus and restructuring of main Group pension scheme

£4.3m further gain in second half from London Bus completion accounts and tax finalisation

Further pension credit in second half of £6.1m

Intangible asset expenses (£m)

Group overheads (£m)

Restructuring costs (£m)

Pre-tax exceptional items (£m)

Year to 30 April 07

Year to 30 April 06

(14.7)

(11.1)

(3.2)

169.6

(20.5)

(10.0)

(1.5)

17.4

Change

28.3%

(11.0)%

(113.3)%

874.7%

17 Preliminary Results 2007

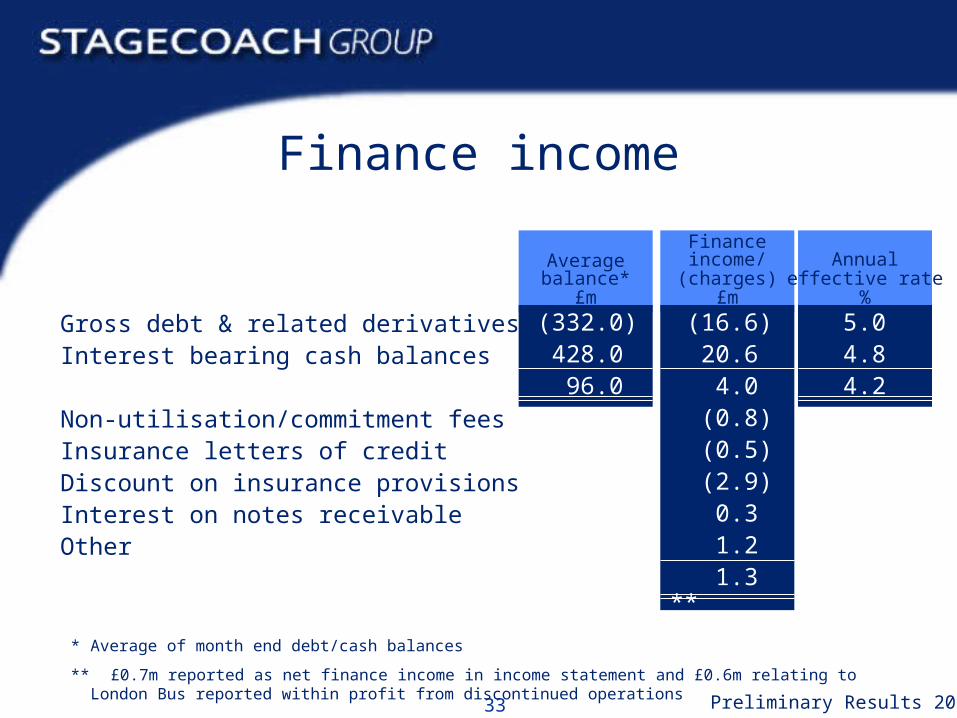

Finance income/(charges) and credit ratios

Net finance income/(charges) (£m)

EBITDA from continuing operations and joint ventures excl exceptional items (£m)

Year-end net funds/(debt) (£m)

Net Debt/EBITDA

- Net funds increased by £726m for Return of Value & special pension contributions

Year to 30 April 07

Year to 30 April 06

0.7

229.6

186.4

n/a

2.3

(15.9)

194.0

(135.9)

0.7

0.7

Change

16.6

35.6

322.3

n/a

1.6

18 Preliminary Results 2007

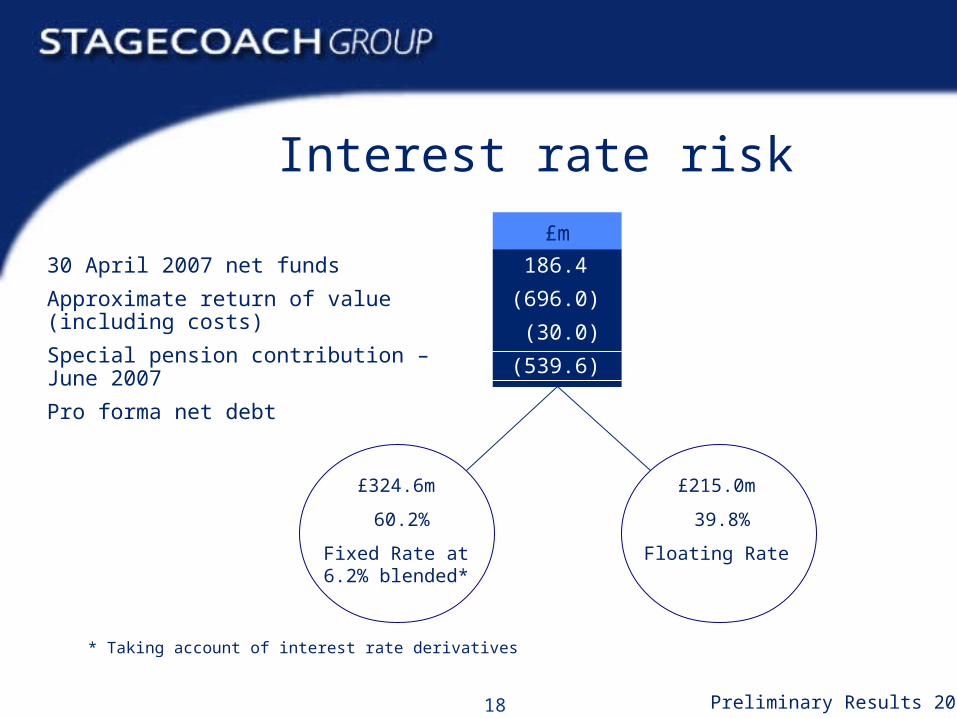

Interest rate risk

30 April 2007 net funds

Approximate return of value (including costs)

Special pension contribution – June 2007

Pro forma net debt

£m

186.4

(696.0)

(30.0)

(539.6)

£324.6m

60.2%

Fixed Rate at 6.2% blended*

£215.0m

39.8%

Floating Rate

* Taking account of interest rate derivatives

19 Preliminary Results 2007

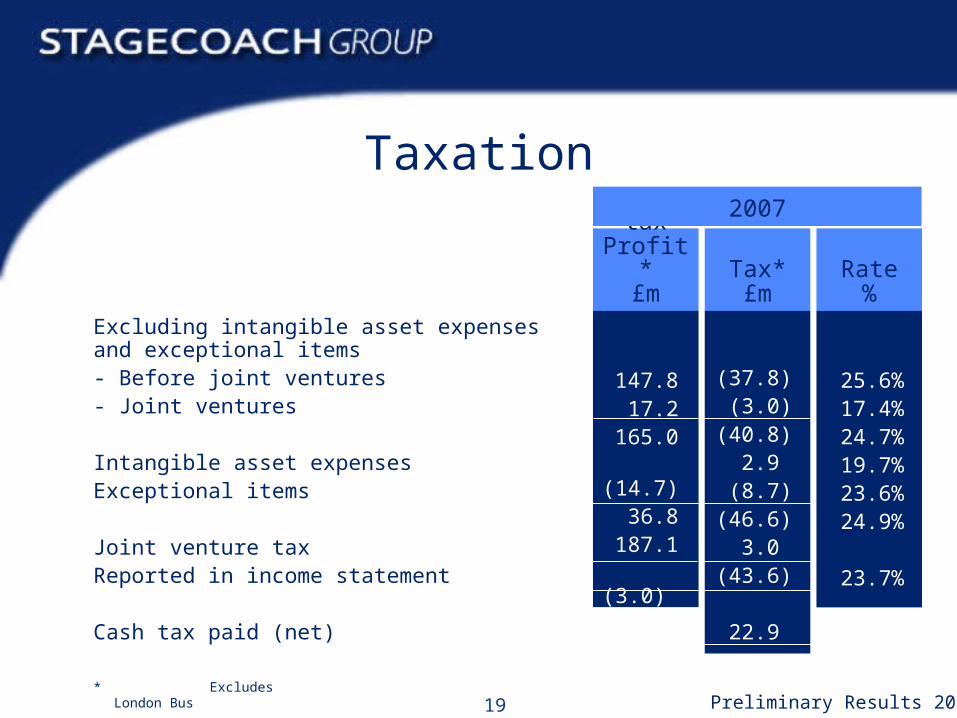

Taxation

Excluding intangible asset expenses and exceptional items- Before joint ventures- Joint ventures

Intangible asset expensesExceptional items

Joint venture taxReported in income statement

Cash tax paid (net)

Pre-taxProfit*

£mTax*£m

147.817.2

165.0(14.7)36.8

187.1(3.0)

184.1

(37.8)(3.0)

(40.8)2.9

(8.7)(46.6)

3.0(43.6)

22.9

Rate%

25.6%17.4%24.7%19.7%23.6%24.9%

23.7%

2007

* Excludes London Bus

20 Preliminary Results 2007

Capital structure

c.£700m return of value completed

Reflects robust business model

Quantum determined with reference to credit ratios, including Net Debt/EBITDA and Debt Service Cover

Ordinary shares currently in issue 707.9m

2007/08 pro forma average Ordinary shares in issue 724.3m

21 Preliminary Results 2007

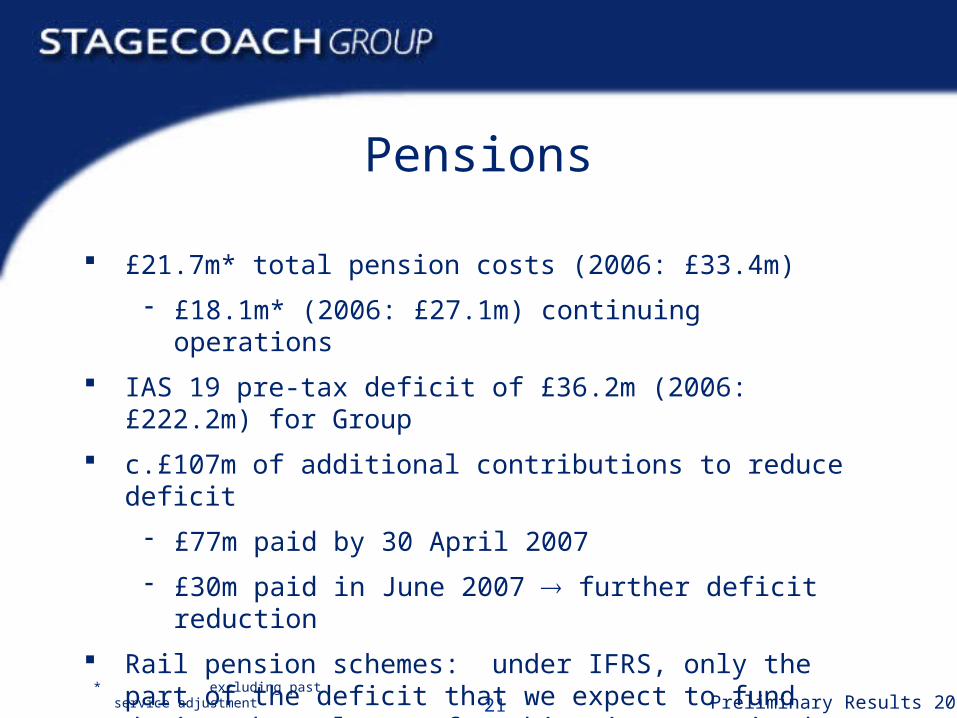

Pensions

£21.7m* total pension costs (2006: £33.4m)

£18.1m* (2006: £27.1m) continuing operations

IAS 19 pre-tax deficit of £36.2m (2006: £222.2m) for Group

c.£107m of additional contributions to reduce deficit

£77m paid by 30 April 2007

£30m paid in June 2007 further deficit reduction

Rail pension schemes: under IFRS, only the part of the deficit that we expect to fund during the relevant franchise is recognised

Positive changes to schemes* excluding past service adjustment

22 Preliminary Results 2007

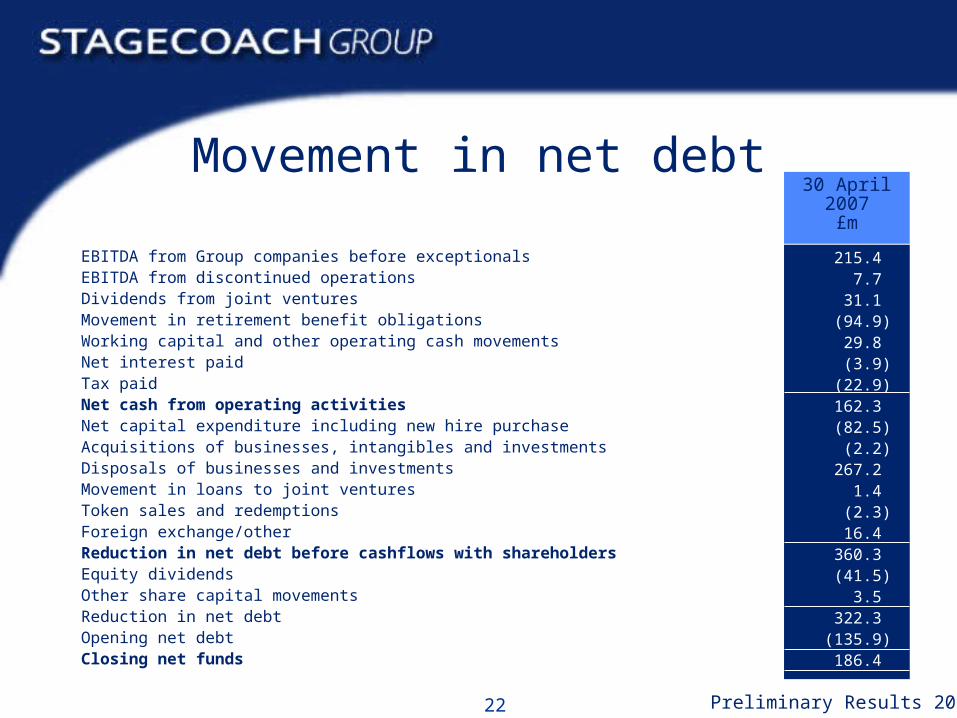

EBITDA from Group companies before exceptionals EBITDA from discontinued operationsDividends from joint venturesMovement in retirement benefit obligationsWorking capital and other operating cash movementsNet interest paidTax paidNet cash from operating activitiesNet capital expenditure including new hire purchaseAcquisitions of businesses, intangibles and investmentsDisposals of businesses and investmentsMovement in loans to joint venturesToken sales and redemptionsForeign exchange/otherReduction in net debt before cashflows with shareholdersEquity dividendsOther share capital movementsReduction in net debtOpening net debtClosing net funds

30 April2007£m

215.47.7

31.1(94.9)29.8(3.9)

(22.9)162.3(82.5)

(2.2)267.2

1.4(2.3)16.4

360.3(41.5)

3.5322.3

(135.9)186.4

Movement in net debt

23 Preliminary Results 2007

49.0 Nil Nil

49.0

68.121.4

4.093.5

(8.2)(2.8)

Nil(11.0)

59.918.6

4.082.5

19.121.4

4.044.5

Capital expenditure

UK BusNorth AmericaRail

Capex on new hire purchase

£m

Impact ofcapex onnet debt

£m

Disposalproceeds**

£mNet£m

Cash spent on capex*

£m

* Excludes capitalised intangible assets of £13.3m (2006: £0.6m)

** Excludes proceeds from selling businesses

Note: Vehicles with a capital value of £12.1m were acquired by UK Bus during the year on operating leases (2006: £Nil )

24 Preliminary Results 2007

Brian SouterBrian Souter

Chief ExecutiveChief Executive

25 Preliminary Results 2007

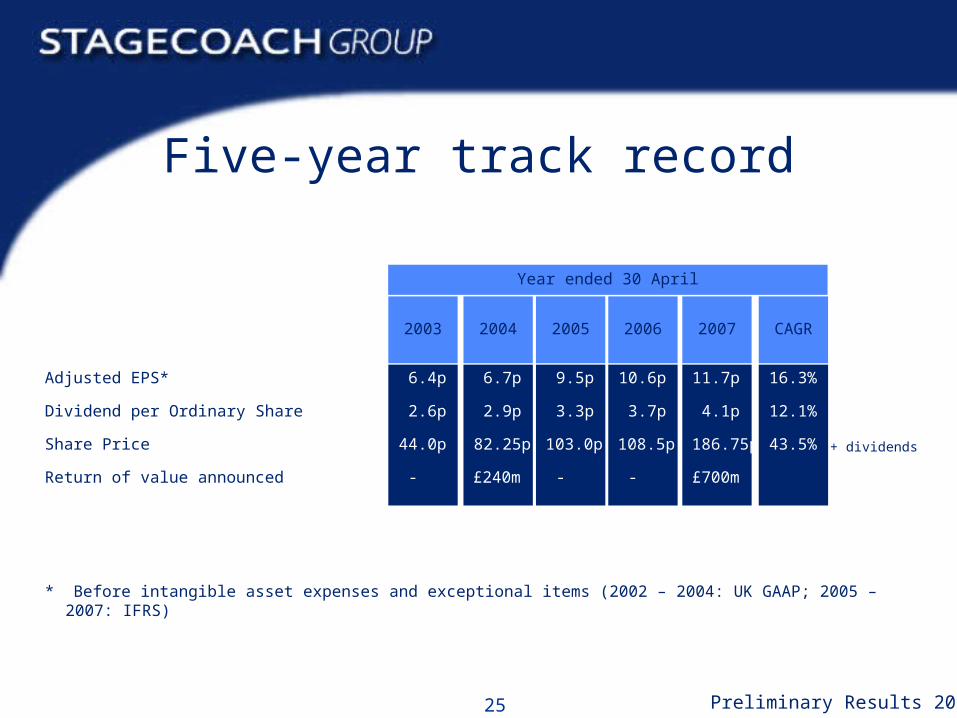

Five-year track record

Adjusted EPS*

Dividend per Ordinary Share

Share Price

Return of value announced

6.4p

2.6p

44.0p

-

6.7p

2.9p

82.25p

£240m

9.5p

3.3p

103.0p

-

10.6p

3.7p

108.5p

-

11.7p

4.1p

186.75p

£700m

16.3%

12.1%

43.5%

2003 2004 2005 2006 2007 CAGR

Year ended 30 April

* Before intangible asset expenses and exceptional items (2002 – 2004: UK GAAP; 2005 – 2007: IFRS)

+ dividends

26 Preliminary Results 2007

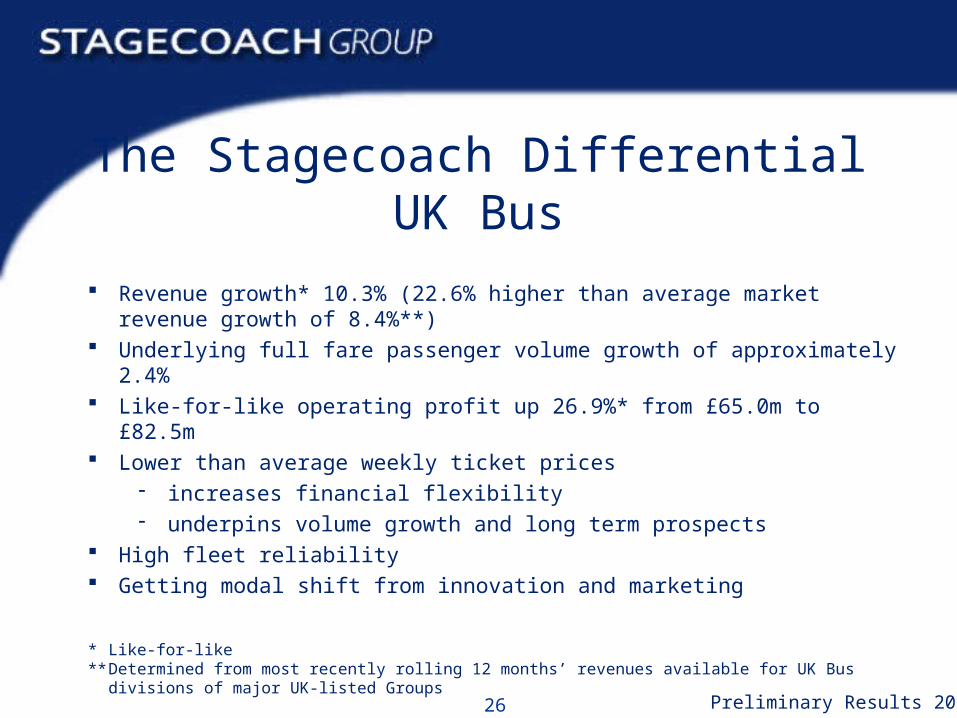

The Stagecoach DifferentialUK Bus

Revenue growth* 10.3% (22.6% higher than average market revenue growth of 8.4%**)

Underlying full fare passenger volume growth of approximately 2.4% Like-for-like operating profit up 26.9%* from £65.0m to £82.5m Lower than average weekly ticket prices

increases financial flexibility underpins volume growth and long term prospects

High fleet reliability Getting modal shift from innovation and marketing

* Like-for-like** Determined from most recently rolling 12 months’ revenues available for UK Bus divisions of major UK-listed

Groups

27 Preliminary Results 2007

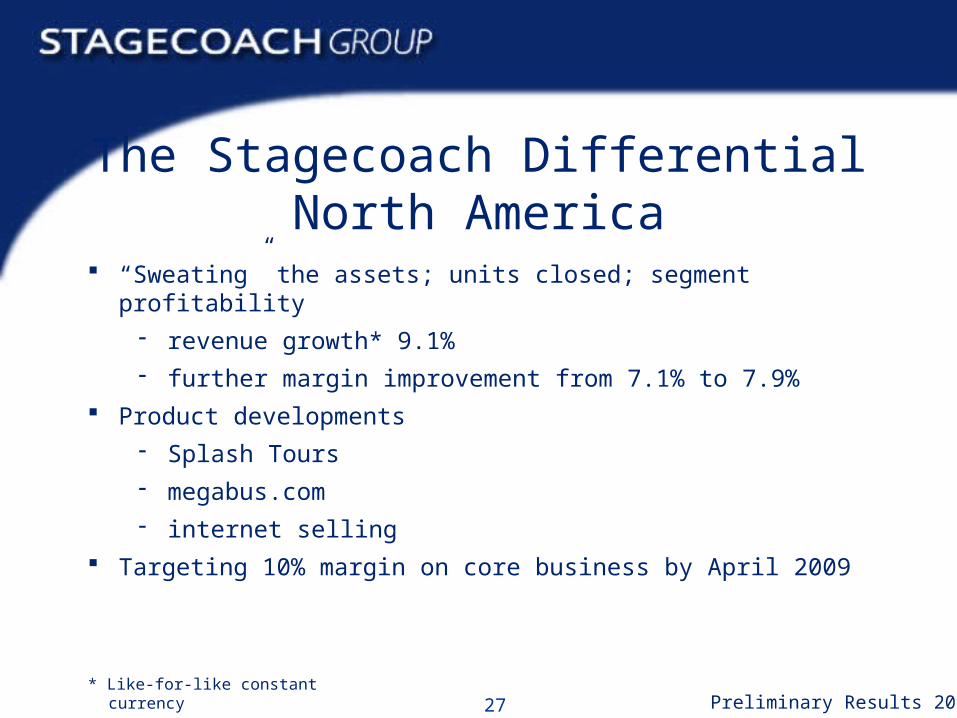

The Stagecoach DifferentialNorth America

“Sweating” the assets; units closed; segment profitability

revenue growth* 9.1%

further margin improvement from 7.1% to 7.9%

Product developments

Splash Tours

megabus.com

internet selling

Targeting 10% margin on core business by April 2009

* Like-for-like constant currency

28 Preliminary Results 2007

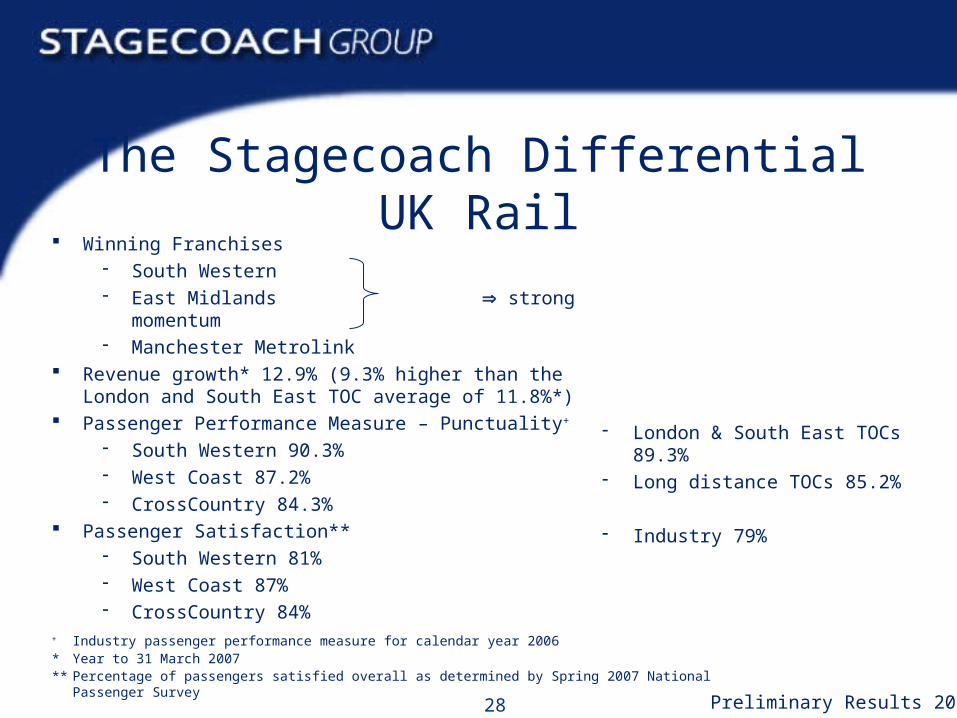

The Stagecoach DifferentialUK Rail

Winning Franchises South Western East Midlands strong

momentum Manchester Metrolink

Revenue growth* 12.9% (9.3% higher than the London and South East TOC average of 11.8%*)

Passenger Performance Measure – Punctuality+

South Western 90.3% West Coast 87.2% CrossCountry 84.3%

Passenger Satisfaction** South Western 81% West Coast 87% CrossCountry 84%

+ Industry passenger performance measure for calendar year 2006* Year to 31 March 2007** Percentage of passengers satisfied overall as determined by Spring 2007 National Passenger Survey

London & South East TOCs 89.3% Long distance TOCs 85.2%

Industry 79%

29 Preliminary Results 2007

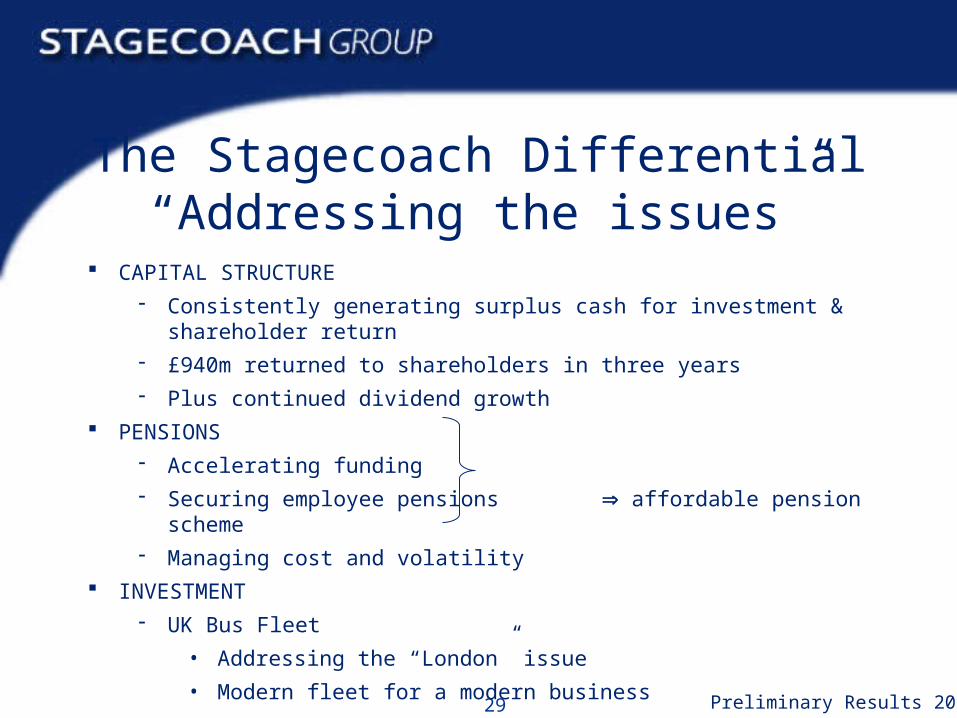

The Stagecoach Differential“Addressing the issues”

CAPITAL STRUCTURE

Consistently generating surplus cash for investment & shareholder return

£940m returned to shareholders in three years

Plus continued dividend growth

PENSIONS

Accelerating funding

Securing employee pensions affordable pension scheme

Managing cost and volatility

INVESTMENT

UK Bus Fleet

• Addressing the “London” issue

• Modern fleet for a modern business

30 Preliminary Results 2007

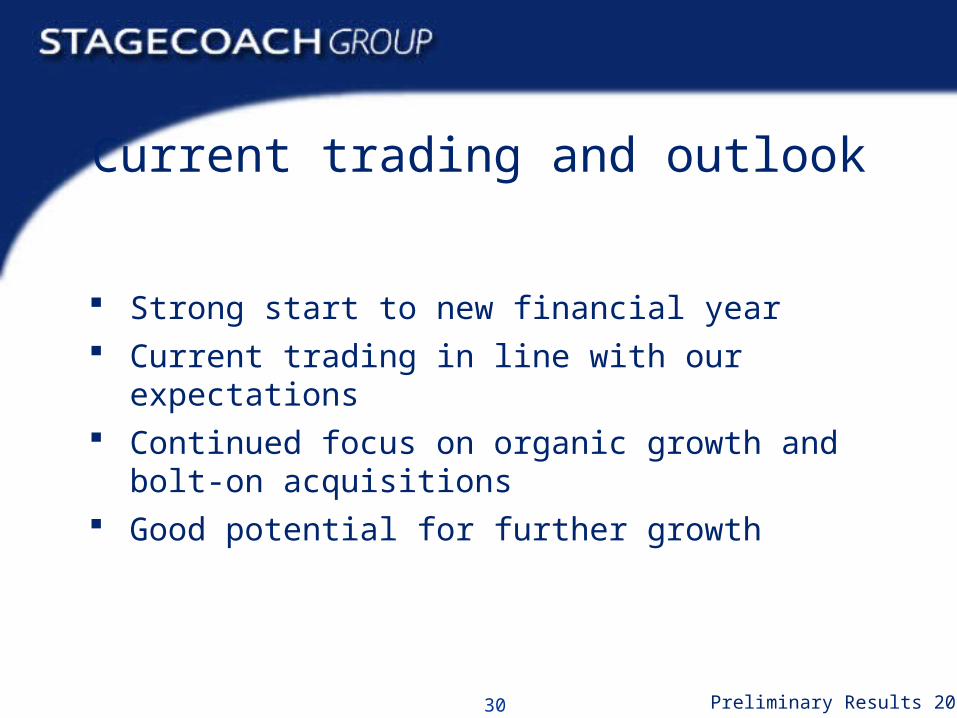

Current trading and outlook

Strong start to new financial year Current trading in line with our expectations Continued focus on organic growth and bolt-on

acquisitions Good potential for further growth

31 Preliminary Results 2007

Annual ResultsAnnual Results2727thth June 2007 June 2007

32 Preliminary Results 2007

Appendices

33 Preliminary Results 2007

Gross debt & related derivativesInterest bearing cash balances

Non-utilisation/commitment feesInsurance letters of creditDiscount on insurance provisionsInterest on notes receivableOther

Finance income/

(charges)£m

Annualeffective rate

%

(16.6)20.6

4.0(0.8)(0.5)(2.9)0.31.21.3 **

5.04.84.2

Finance income

Average balance*

£m

(332.0)428.096.0

* Average of month end debt/cash balances

** £0.7m reported as net finance income in income statement and £0.6m relating to London Bus reported within profit from discontinued operations

34 Preliminary Results 2007

Fuel hedging

% of Group fuel hedged - fixed

- cap/floor

Average hedge price (crude price US$/barrel) - fixed

- cap/floor

Forecast2007/08

37%

51%

$59

US$59/US$28

• Continuing Bus divisions use 1.6m barrels of fuel a year• Each US$10 per barrel movement in crude oil price impacts variable fuel costs by approximately

US$16m if no hedging in place• 2006/07 year-on-year increase of £21m in fuel costs of continuing operations

Forecast2008/09

Nil

44%

n/a

US$89/US$58

Forecast2009/10

Nil

Nil

n/a

n/a

35 Preliminary Results 2007

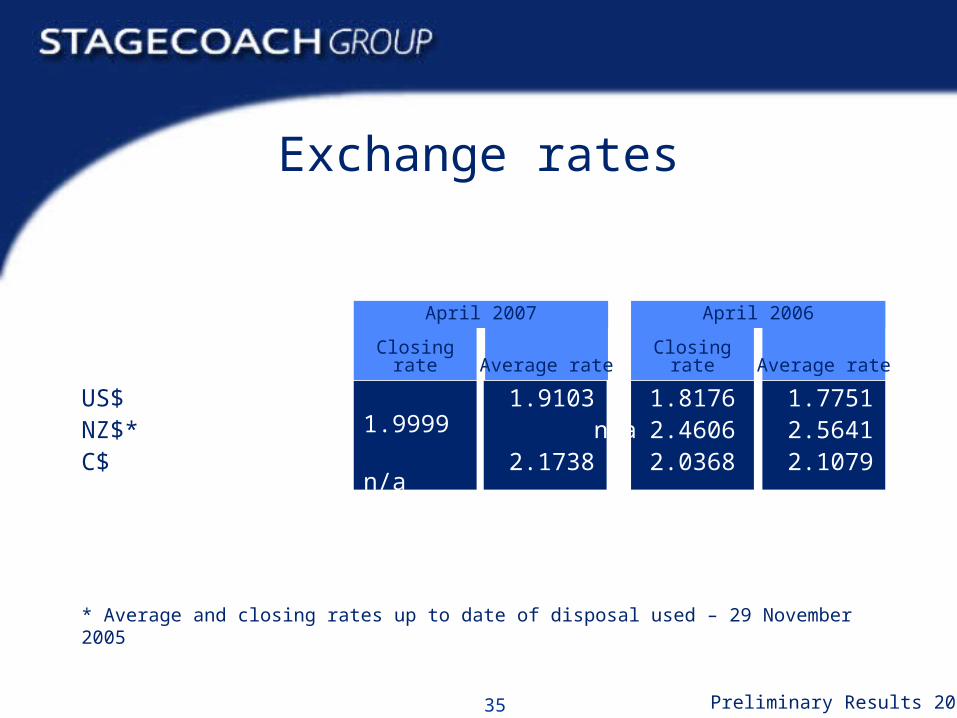

Exchange rates

US$NZ$*C$

Closing rate Average rate

1.81762.46062.0368

1.77512.56412.1079

April 2006

Closing rate Average rate

1.9999 n/a

2.2102

1.9103 n/a

2.1738

April 2007

* Average and closing rates up to date of disposal used – 29 November 2005

36 Preliminary Results 2007

Annual ResultsAnnual Results2727thth June 2007 June 2007