preliminary results - hibernia reit/media/files/h/hibernia-reit/2016 news items... · preliminary...

TRANSCRIPT

Preliminary Results

May 2016

2

Disclaimer

This presentation (hereinafter "this document") has been prepared by Hibernia REIT plc (the "Company“ or “Group”) for

information purposes only.

This document has been prepared in good faith but the information contained in it has not been independently verified and does

not purport to be comprehensive. This document is neither a prospectus nor an offer nor an invitation to apply for securities. No

representation or warranty, express or implied, is given by or on behalf of the Company, its group companies, or any of their

respective shareholders, directors, officers, employees, advisers, agents or any other persons as to the accuracy, completeness,

fairness or sufficiency of the information, projections, forecasts or opinions contained in this presentation. In particular, the

market data in this document has been sourced from third parties. Save in the case of fraud, no liability is accepted for any errors,

omissions or inaccuracies in any of the information or opinions in this document.

Certain information contained herein may constitute "forward-looking statements“. Due to various risks and uncertainties, actual

events or results or actual performance of the Company may differ materially from those reflected or contemplated in such

forward-looking statements. No representation or warranty is made as to the achievement or reasonableness of, and no reliance

should be placed on, such forward-looking statements. There is no guarantee that the Company will generate a particular rate of

return.

3

Market update

Acquisitions and developments

Portfolio management

Conclusion and outlook

Highlights

Financial results

Agenda

Highlights

4

• Excellent financial performance

– EPRA NAV per share +17% to 130.8c in year to March 2016

– Net income of €136.8m incl. revaluation gain of €125.1m

– Final dividend of 0.8c per share, bringing total for year to 1.5c per share

• Selective acquisitions enhancing portfolio

– Rental growth plays: e.g. Central Quay, Hardwicke and Montague

– Additions to development pipeline: e.g. Marine House, Earlsfort Terrace

• Development programme progressing well

– 3 completed schemes delivered profit on cost in excess of 30%

– 4 committed schemes delivering 354k(1) sq. ft. of office space in the next 24 months

– Longer term pipeline expanded to 6 schemes

• Letting activity growing rent roll substantially

– Over 157k sq. ft. of office lettings(2) in year

– Contracted rent roll now €39.0m, +72% on March 2015

• Management team and funding in place

(1) Office areas only (e.g excl. basement areas etc.). 345k sq. ft. includes: Cumberland House (127k sq. ft.), 1WML (50% share equating to 61k sq. ft.), 1 SJRQ (110k sq. ft.) and Guild House (56k of 72k is committed refurbishment). As at 31st of March, the entire of Guild House was part of the in-place office portfolio, not committed schemes. Conversely, 30k sq. ft. of 1DLC and the entire 11k sq. ft. of SOBO Works were committed developments at 31st March but have now completed and are considered in-place office. See slide 25 for more details

(2) Incl. storage spaces

In-place office portfolio*764k sq. ft.

Committed developments*340k sq. ft. (pre-let 105k sq. ft.)

Longer term development pipeline**371k sq. ft.

5

Portfolio overview as at 31 March 2016

Portfolio by sector (by value) Office and development portfolio (by net lettable area)

Office IFSC25%

Office South Docks19%Office Traditional Core

26%

CBD Office Development / Refurb

17%

Industrial1%

Residential12%

Total: €928m

• Portfolio of 25 properties (17 completed office(1) properties)

• Portfolio total passing rent of €30.0m(2) and total contracted rent of €39.0m(2,3)

• In-place office (excl. refurbishments and developments) average contracted rent of €33psf with an average ERV of €44psf(4)

• In-place office WAULT to rent review of 2.0yrs(5) and 4.3yrs to earlier of break or lease expiry

• In-place office vacancy rate of 6%

Total: 1.5m sq. ft.

Notes to the office development portfolio:*Office areas only (e.g. excl. basement areas etc.). This is the position as at 31st of March and included: Cumberland House (127k sq. ft.), 1WML (61k sq. ft. representing the 50% share), 1SJRQ (110k sq. ft.), 1DLC (30k sq. ft. of total 73.9k sq. ft. was still under refurbishment), SOBO Works (11k sq. ft.). Post 31st March 1DLC and SOBO Works completed and are now in-place office assets. Conversely, Guild House was classified as an in-place asset as at 31st of March but 56k of 72k is now committed refurbishment (see slide 25 for details)**Includes incremental additional sq. ft. from Harcourt Square, Hanover Building, Marine House & Earlsfort Terrace. It also includes the potential new offices at Gateway (c.115k sq. ft.) and the front site at Cumberland House. Note that there is also development potential at Gateway for a further c.130k sq. ft. of offices (see slide 29 for details)

(1) Includes Camden Street(2) Includes net rental income from residential(3) Includes pre-let refurbishments(4) All ERVs are CBRE assessments except for Harcourt Square which is an internal assessment(5) Earlier of review or expiry

6

Further opportunity

• Favourable market conditions

• Hibernia’s committed development schemes completing in next 24 months: longer term pipeline gives optionality

• In-place office portfolio has asset management angles and is heavily reversionary

• Selective recycling likely

• Further acquisition opportunities expected and flexible funding in place to exploit these

7

Agenda

Market update

Acquisitions and developments

Portfolio management

Conclusion and outlook

Highlights

Financial results

12 months to

31-Mar-16

12 months to

31-Mar-15 % change

Property income (1) 30,289 18,044 68%

Revaluation gain (2) 125,056 90,868 38%

Net income 136,797 92,232 48%

EPRA earnings 10,024 3,961 153%

EPRA EPS 1.5c 0.8c 88%

Dividend per share 1.5c 0.8c 88%

31-Mar-16 31-Mar-15 % change

Portfol io va lue 927,656 641,296 45%

Net debt/(cash) 52,918 (139,048) n/a

Loan to va lue 5.7% n/a n/a

Net assets 896,574 753,134 19%

EPRA NAV per share (cent) 130.8c 111.8c 17%

8

Financial highlights

(€’000)

96.4c

104.7c

111.8c

122.1c

130.8c

90c

95c

100c

105c

110c

115c

120c

125c

130c

135c

Mar-14 Sep-14 Mar-15 Sep-15 Mar-16

EPR

A N

AV

per

sh

are

(cen

t)

+9%

+7%

+9%

+36%

Valuation uplifts and income driving strong increases in NAV

(1) Includes receipt of €4.9m (FBD surrender) in 2016 and €2.4m (Commerzbank surrender) in 2015(2) Prior year figure includes €10m gain on conveyance of Block 3 which has been reclassified from ‘Other Gains’

Balance sheet EPRA NAV per share progression

Income statement

+7%

(€’000)

111.8

130.80.51.5

(1.2)

0.04

103

108

113

118

123

128

133

Mar-15 Investmentproperties reval.

Developmentproperties reval.

Non-core sales EPRA EPS Dividends paid Other Mar-16

EPR

A N

AV

cen

t p

er s

har

e

+17%

EPRA NAV per share movement since 31 March 15

EPRA NAV per share movement since 31 Mar 15

Traditional Core

IFSC

South Docks

Other

Cumberland House

1WML

1SJRQ

10.0

8.2

Valuation uplift: 18.2c

9

Impact of internalisation on financial statements

10

31-Mar-16 30-Mar-15

Revenue 32,786 18,769

Direct property costs (2,497) (725)

Property Income 30,289 18,044

IM base fee - (4,690)

IM performance fee (6,069) (5,772)

Adminis trative expenses (8,696) (1,584)

Net finance expense (4,087) (1,575)

Net rental profit 11,437 4,423

Revaluation & Other ga ins/(losses ):

Investment properties 125,056 90,868

Other losses (171) (2,368)

Tax credit / (expense) 475 (691)

Total revaluation/other losses: 125,360 87,809

Net income for the period 136,797 92,232

Diluted IFRS EPS (cents) 20.1 18.3

EPRA Earnings 10,024 3,961

Diluted EPRA EPS (cents) 1.5 0.8

(1) IM base fee

• Internalisation took effect from 1 April 2015 and consequently no base fees were paid in the year

(2) IM performance fee

• Existing arrangements remain in place until expiry of Investment Management Agreement in November 2018

(3) Administrative expenses

• Costs of Investment Manager of c.€2.6m per annum (mainly staff and office costs) now included

• Charge of €1.8m from amortisation of prepaid remuneration asset relating to €14.2m paid for base fee buyout. €11.6m remains to be amortised over period to November 2018 (c.€4.5m per annum)

• Non internalisation-related administrative expenses increased substantially over prior year due in particular to increased professional advisers fees and a change in general overhead VAT recovery rate

(1)

(2)

(3)

Internalisation expected to be earnings neutral over remaining life of IMA

Summary income statement

Net cash invested€711m

IPO€372m

Co

mm

itte

d c

apex

€1

04

m

P+OO€286m

RCF€400m

Remaining investment capacity€265m

1WML facility€22m

€0m €200m €400m €600m €800m €1000m €1200m

Uses of funds

Sources of funds

11

Substantial financial capacity in place

Current LTV of 5.7%: if current facilities fully invested, LTV would be 32.5%

Hedged€100m(1)

Hedged€22m(2)

(1) €50m hedged from May 16 to Nov 16 and €100m hedged from Nov 16 to Nov 20. Hedging instruments are a combination of interest rate caps and swaptions with strike rates of 1% (reference rate is 3M Euribor)(2) Facility fully hedged per expected drawing schedule using interest rate caps with a 1% strike rate (reference rate its 3M Euribor)

One Dockland Central€4m

Cumberland House€16m

1WML€14m

1WML€5m

1SJRQ€24m

1SJRQ€23m

1SJRQ€6m

Two Dockland Central€6m

Two Dockland Central€6m

€0m

€10m

€20m

€30m

€40m

€50m

€60m

€70m

Y/E March 2017 Y/E March 2018 Y/E March 2019

Project

Capex/Est. total

capex

€m

Spent at Mar-16

€m

Left to spend

€m

One Dockland Central(1) €10m €6m €4m

1WML(3) €26m €6m €20m

Cumberland House €27m €11m €16m

Two Dockland Central €12m - €12m

1SJRQ €55m €2m €53m

Total committed €130m €25m €104m

12

Forecast capital expenditure for committed development schemes

Forecast capital expenditure by financial year – committed developments

(1) 1DLC completed post 31st March 2016(2) €7.9m net of dilapidations received(3) 50% interest(4) Differences are due to rounding

(2)

(4)

€1.3m

€5.3m

€0.4m

€5.9m

€1.6m

€3.0m

€1.9m

€15m

€20m

€25m

€30m

€35m

€40m

€45m

€50m

€55m

€60m

€65m

Contracted in-place rent roll at31 Mar 16

Let To let Proforma

Purchases since Sep 15

One Dockland Central(1)

Cumberland House

€32.0m

One Dockland Central

1WML(2)

SOBO Works(1)

Cumberland House

1SJRQ

€51.4m

+€19.4m+61%

Total contracted rent: €39.0m

13

Potential incremental rent roll from committed development schemes

(1) Post 31st March: classified as in-place office(2) Commercial units only/based on 50% interest(3) At valuers’ ERV 31 Mar 16(4) Excl. additional basement and reception

Based on CBRE estimated rental values, Mar 16

Average office ERVs as per CBRE Mar 16:• One Dockland Central: €50.15psf• Cumberland House: €51.40psf(4)

• Windmill Lane: €47.00psf

• SJRQ €50.50psf• SOBO Works: €36.00psf

Committed schemes expected to add c.€19m to rent roll by mid 2018 of which €7m is already let

In-place office reversionary potential(3)

Potential incremental rent roll @ valuers’ ERV

14

Key financial messages

• Excellent financial results

– Investment portfolio and development schemes both contributing to NAV uplift

– Significant earnings growth even without €4.9m surrender premium allowing dividend of 1.5c for the year, up 88% up on prior year

– More to come from further lettings and completion of committed development schemes

• Substantial financial capacity in place

– Cash and undrawn facilities of €369m, €265m including committed spend

– Current LTV of 5.7%: target through cycle of 20%-30%

• Hedging strategy being implemented

– Intend to hedge at least 50% of all interest rate exposure on drawn debt facilities

– Hedged €100m of RCF to November 2020 at 1% Euribor strike rate(1)

– Hedged €22.1m Windmill Lane facility using interest rate caps with 1% Euribor strike rate

• Internalisation effective from 1 April 2015

– Expected to be earnings neutral to November 2018

(1) €50m hedged from May 16 to Nov 16 and €100m hedged from Nov 16 to Nov 20. Hedging instruments are a combination of interest rate caps and swaptions with strike rates of 1% (reference rate is 3M Euribor)

15

Market update

Acquisitions and developments

Portfolio management

Conclusion and outlook

Highlights

Financial results

Agenda

TMT23%

Financial services25%Professional

services24%

Other13%

Public sector15%

(10)k

(5)k

-

5k

10k

15k

20k

(15)k

(10)k

(5)k

-

5k

10k

15k

20k

25k

30k

20

10Q

1

20

10Q

2

20

10Q

3

20

10Q

4

20

11Q

1

20

11Q

2

20

11Q

3

20

11Q

4

20

12Q

1

20

12Q

2

20

12Q

3

20

12Q

4

20

13Q

1

20

13Q

2

20

13Q

3

20

13Q

4

20

14Q

1

20

14Q

2

20

14Q

3

20

14Q

4

20

15Q

1

20

15Q

2

20

15Q

3

20

15Q

4

Dublin Midlands** South East South West Border State (RHS)

16

Economic outlook

Dublin driving population* growth

Source: CSO, Goodbody *over 15yrs of age; **Midland, Mid-West & Mid-East (as per CSO)

Source: CSO, Q4 2010 = 100

Dublin office based employment making strong contribution to overall employment growth

Dublin office employment is broad based

Source: CSO @ Q4 2015

2013 2014 2015 2016F 2017F

Consumption (0.3%) 2.0% 3.5% 4.0% 3.2%

Government 1.4% 4.6% -0.8% 2.6% 2.0%

Investment (6.6%) 14.3% 28.2% 2.9% 9.4%

Domestic Demand (1.5%) 5.2% 8.6% 3.5% 4.7%

Core Domestic Demand* 2.4% 4.7% 4.3% 5.0% 4.4%

Exports 2.5% 12.1% 13.8% 7.6% 4.4%

Source: CSO, Goodbody*Core domestic demand = domestic demand excl. R&D and aircraft leasing

Core domestic demand is expected to remain robust in the coming years

95

100

105

110

115

120

20

10Q

4

20

11Q

1

20

11Q

2

20

11Q

3

20

11Q

4

20

12Q

1

20

12Q

2

20

12Q

3

20

12Q

4

20

13Q

1

20

13Q

2

20

13Q

3

20

13Q

4

20

14Q

1

20

14Q

2

20

14Q

3

20

14Q

4

20

15Q

1

20

15Q

2

20

15Q

3

20

15Q

4

Ind

ex le

vel (

Q4

20

10

= 1

00

)

Dublin office jobs Total Irish employment (less Dublin office jobs)

Q3 2007 peak Dublin office jobs

0%

2%

4%

6%

8%

10%

12%

14%

16%

Dublin1/3/7

Dublin 2/4Dublin 6/8 IFSC CityCentre

SouthSuburbs

NorthSuburbs

WestSuburbs

Overall vacancy rate Grade A vacancy rate

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016 YTD

<5k sq. ft. 5k-10k sq. ft. 10k-20k sq. ft.

20k-50k sq. ft. 50k-100k sq. ft. >100k sq. ft.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Q1

201

6

Mill

ion

s Sq

Ft

Annual Dublin Office Take Up 10 Year Average

17

Rental market: Dublin office dynamics

Broad based demand with little supply is driving vacancy rates down

Dublin office take-up reached 2.7m sq. ft. in 2015 and 0.6m sq. ft. in Q1 2016

Overall Dublin vacancy rate is 7.7% with the grade A vacancy rate down to 1.5% in D2/4 (core CBD location)

Source: CBRE

Source: CBRE Source: CBRE

Source: CBRE @ 31 Mar 16

Broad mix of occupier take-up in the Dublin office marketc.75% of take-up in Dublin is for space less than 50k sq. ft.

Other21%

Professional services

3%

TMT38%

Financial services

16%

Public sector

7%

Industry15%

2011 to 20142015 to

2016 YTD

Other29%

Professional services

5%TMT29%

Financial services

18%

Public sector

7%

Industry12%

18

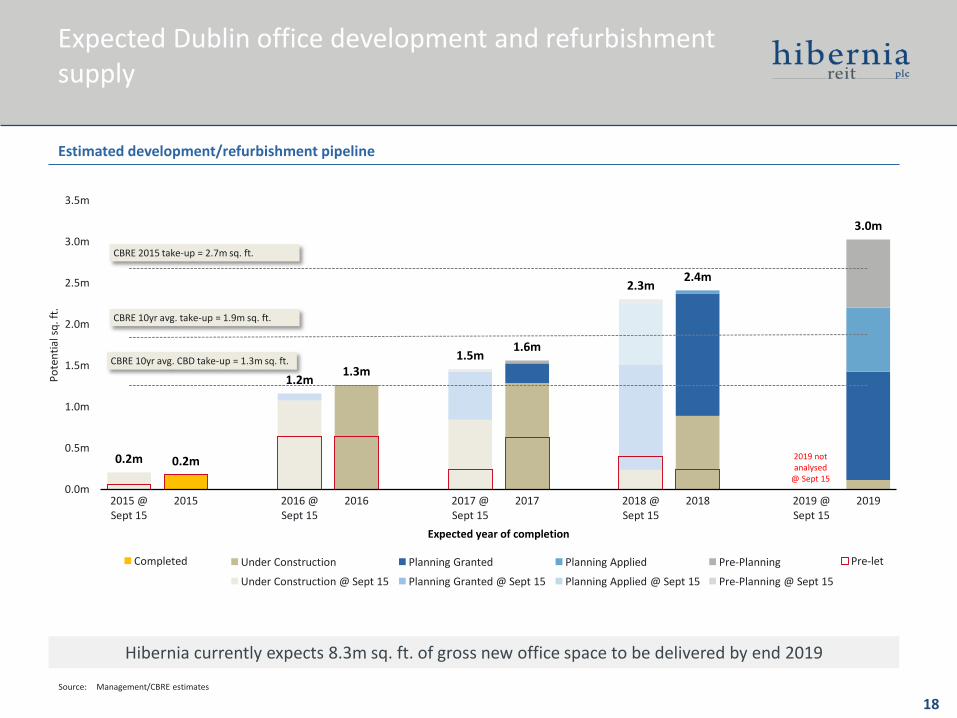

Hibernia currently expects 8.3m sq. ft. of gross new office space to be delivered by end 2019

Source: Management/CBRE estimates

Estimated development/refurbishment pipeline

Under Construction @ Sept 15 Planning Granted @ Sept 15 Planning Applied @ Sept 15 Pre-Planning @ Sept 15

Expected Dublin office development and refurbishment supply

0.2m

1.2m

1.5m

2.3m

0.2m

1.3m

1.6m

2.4m

3.0m

0.0m

0.5m

1.0m

1.5m

2.0m

2.5m

3.0m

3.5m

2015 @Sept 15

2015 2016 @Sept 15

2016 2017 @Sept 15

2017 2018 @Sept 15

2018 2019 @Sept 15

2019

Po

ten

tial

sq

. ft.

Expected year of completion

Under Construction Planning Granted Planning Applied Pre-PlanningCompleted Pre-let

CBRE 10yr avg. CBD take-up = 1.3m sq. ft.

CBRE 2015 take-up = 2.7m sq. ft.

CBRE 10yr avg. take-up = 1.9m sq. ft.

2019 not analysed

@ Sept 15

Investment sourcing

19(1) Was €9.6bn as at 30 Sept 2015 which included Project Jewel (c. €1.8bn) and Project Arrow (c. €0.8bn) which were sold in Q4 2015

NAMA

Private equity funds

Other

• >€7bn of loans still on balance sheet(1)

• 73% (€22.1bn) of NAMA’s original senior bonds redeemed at Q4 2015. Targeting redemption of all senior bonds before end of 2018 (i.e. additional €8bn to redeem before end 2018)

• Interesting Dublin CBD office (loan) assets remain within NAMA

• >€35bn invested in last 4 years

• Looking to dispose of certain assets to crystallise gains: funds may be coming to end of lives

• Hibernia has built a reputation with PE funds for offering execution certainty:

− Central Quay purchased from Blackstone

− Harcourt Square & Windmill Lane purchased from Starwood

• Certain assets held by PE owners fit Hibernia’s skill set and value-add strategy more than passive/income focused buyers

• Private investors & syndicates: looking for liquidity and deal certainty

• Forward funding opportunities: Speculative development finance remains scarce; owners of prime development sites may look to unlock developments through forward funding

• Loan acquisitions: Hibernia has proven its ability to purchase debt and resolve potentially complex loan transactions

Opportunities for selective acquisitions to enhance our existing portfolio

20

Agenda

Market update

Acquisitions and developments

Portfolio management

Conclusion and outlook

Highlights

Financial results

21

Summary of acquisitions since March 2015

Asset name SectorPurchase

datePurchase

price NIY (%)Avg. rent

€psf

WAULTyrs

SourceOn/offmarket

Direct/Loan

Break/expiry

Review/expiry

Dundrum View Residential Jun-2015 €28.1m(€350k per

unit)

4.7% €1,500 pertwo bed per

month

n/a n/a Private Off-market Direct

Hardwicke &Montague House

CBD Dublin Office

Jan-2016 €41.8m(1)

(€680psf)(2)

4.2% €30psf 7yrs 2yrs Private Off-market Direct

Central Quay CBD Dublin Office

Feb-2016 €51.3m(€890psf)

4.5% €47psf(3) 6yrs 3yrs Private equity

Off-market Direct

Marine House CBD Dublin Office

Mar-2016 €26.5m(€640psf)

4.3% €23psf 3yrs 2yrs Private Off-market Direct

One EarlsfortTerrace

CBD Dublin Office

Mar-2016 €19.2m(€880psf)

5.3%(4) €45psf(4) 10yrs <1yrs Private On-market Direct

Smaller ‘bolt-on’ acquisitions(5)

Various Various €4.8m - - - - Private Various Direct

€171.7m(6)

(1) Total consideration for the asset (incl. loan purchased) is €60m excl. costs(2) €725psf after all costs(3) €58psf after Indeed surrender and letting to Daqri on 1st floor (11k sq. ft.) post acquisition(4) After Sept-16 rent review which is agreed at €45psf(5) Lime Street (Residential) €1.4m, Camden Street (Dublin CBD Office) €1.6m, 39 Harcourt Street (Dublin CBD Office) €1.8m(6) €179m incl. costs

22

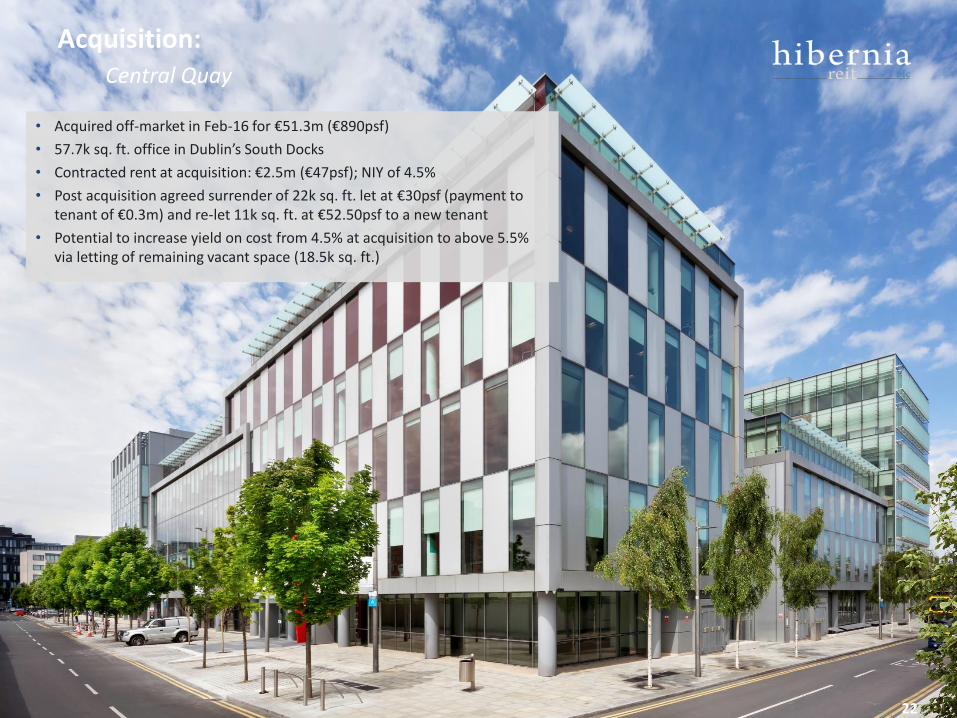

• Acquired off-market in Feb-16 for €51.3m (€890psf)

• 57.7k sq. ft. office in Dublin’s South Docks

• Contracted rent at acquisition: €2.5m (€47psf); NIY of 4.5%

• Post acquisition agreed surrender of 22k sq. ft. let at €30psf (payment to tenant of €0.3m) and re-let 11k sq. ft. at €52.50psf to a new tenant

• Potential to increase yield on cost from 4.5% at acquisition to above 5.5% via letting of remaining vacant space (18.5k sq. ft.)

Acquisition: Central Quay

• Acquired off-market in Mar-16 for €26.5m (€640psf)

• 1970’s office building located in the traditional core of Dublin facing onto the Grand Canal

• Forms part of Clanwilliam Court which consists of 7 separate blocks (6 office, 1 residential)

• Marine House comprises c.41k sq. ft. of office space

• Current rent is €1.2m (€23psf); NIY of 4.3%

• Adds to longer term pipeline of development assets

Acquisition: Marine House

23

Source: Google maps

Marine HouseClanwilliam Court

24

• Acquired in Mar-16 for €19.2m (€880psf)

• Located in Dublin’s traditional core less than 250m from St Stephen’s Green and opposite the National Concert Hall

• 21.7k sq. ft. of offices fully let to international law firm Eversheds on a lease to 2026

• The current rent is €0.6m p.a. (€26psf)

• Rent review in Sept-16 has been agreed at €1.0m p.a. (€45psf) which implies a yield on cost of 5.3%

Acquisition: One Earlsfort Terrace

Summary of committed development schemes

SectorTotal NIA post

completion (sq. ft.)Full purchase

priceCapex/Est.

capexEst. total cost

(incl. land) €psf ERV(1)

Office ERV psf(1) Expected PC Date

Completed schemes (post 31st March 2016)

One Dockland Central

Office 74k(2) €46m €10m(3) €736psf(4) €3.9m €50.15psf Completed after year end delivering profit on cost in

excess of 30%

SOBO Works Office 11k €2m €1.3m €275psf €0.4m €36.00psf Completed after year end delivering profit on cost in

excess of 50%

Total completed 85k €48m €11.3m €4.3m

Committed schemes

Cumberland House

Office 127k(5) €51m €27m €605psf €7.2m €51.40psf Q4 2016

Two Dockland Central (formerlyGuild House)

Office 72k(6) €46m €12m €790psf(4) €3.9m €50.50psf Q3 2017

Windmill Lane(7) Office 61k office3k retail

7.5 resi. Units

€4m €26m €420psf(8) €3.0m(9) €47.00psf late 2017

1SJRQ Office 110k office6k retail

€18m €55m €643psf(8) €5.9m €50.50psf mid 2018

Total committed 370k office(10)

9k retail7.5 units

€119m €120m €20m

CONCEPT IMAGE

CONCEPT IMAGE

CONCEPT IMAGE

CONCEPT IMAGE

CONCEPT IMAGE

(7) 50% interest; includes extensions to 4th & 5th floors (2.3k sq. ft.) planning granted in May 16(8) Office only(9) Commercial only(10) At 31st March: committed developments totaled 340k sq. ft. of office area. This was composed of: 1DLC (30k sq. ft.), SOBO

Works (11k sq. ft.), Cumberland House (127k sq. ft.), 1WML (61k sq. ft. for 50% share) and 1SJRQ (110k sq. ft.)Post 31st March: 1DLC and SOBO Works are completed schemes and in-place office assets. There are now 4 committed schemes which will deliver c.354k sq. ft. as follows: Cumberland House (127k sq. ft.), Guild House (2DLC; 56k sq. ft.), 1WML (61k sq. ft.) and 1 SJRQ (110k sq. ft.)

(1) Per CBRE valuation at 31 Mar 16(2) 30k sq. ft. was committed development/refurbishment at 31 Mar 16(3) €7.9m net of dilapidation charge received(4) Est. total cost psf is net of dilaps(5) Excl. additional basement areas (8k sq. ft.) and potential new block (c.50k sq. ft.)

but incl. new reception (1k sq. ft.), additional ground floor (5k sq. ft.) and design efficiencies of existing building (9k sq. ft.)

(6) 56k sq. ft. of entire 72k is committed refurbishment25

• Refurbishment works (budget of €27m) on schedule for completion in Q4 2016

• Twitter originally signed a lease for €4.6m but contracted rent increased to €5.3m via:

− €0.5m: extension space of c.14k sq. ft.

− €0.2m: design efficiencies of existing Twitter space in building of c.2.5k sq. ft.

• Total building will be c.135k sq. ft. (incl. the new additional areas)

• In discussions with potential tenants regarding the remaining 33k sq. ft. available on the top two floors

• Potential to add a new c.50k sq. ft. NIA office block at the front of the site subject to planning (see diagram)

Potential building

Existing building

Committed development: Cumberland House

26

• Situated within the SOBO (South of Beckett and O’Casey bridges) District of Dublin’s South Docks

• 1WML and 1SJRQ progressing well and on schedule:

− 1WML due to complete by late 2017

− 1SJRQ by mid 2018

• The spec for 1SJRQ has been finalized and 83% of the packages have now been agreed. The total budget for the project has been set at €55m

• Marketing campaign for both began in April 2016

• Multi-lets likely in which case pre-letting unlikely until 6-9 months prior to PC

Committed developments:1WML & 1SJRQ

Pictured: Site clearance of 1SJRQ Pictured: Construction works at 1WML 27

1WML

1SJRQ

1SJRQ 1WML

• Extensive refurbishment works at One Dockland Central (formerly Commerzbank House) completed after year end generating profit on cost in excess of 30%

• Agreed pre-let to HubSpot of 27.5k sq. ft. at a rent of €45 psf.

• In detailed discussion to let the remainder (30k sq. ft.) of available space

• Committed to carry out similar refurbishment works at Guild House which is to complete in late 2017 (and will be renamed Two Dockland Central)

Completed/committed developments:

One Dockland Central & Two Dockland Central

28Concept image

Pictured: final works to staircase in 1DLC

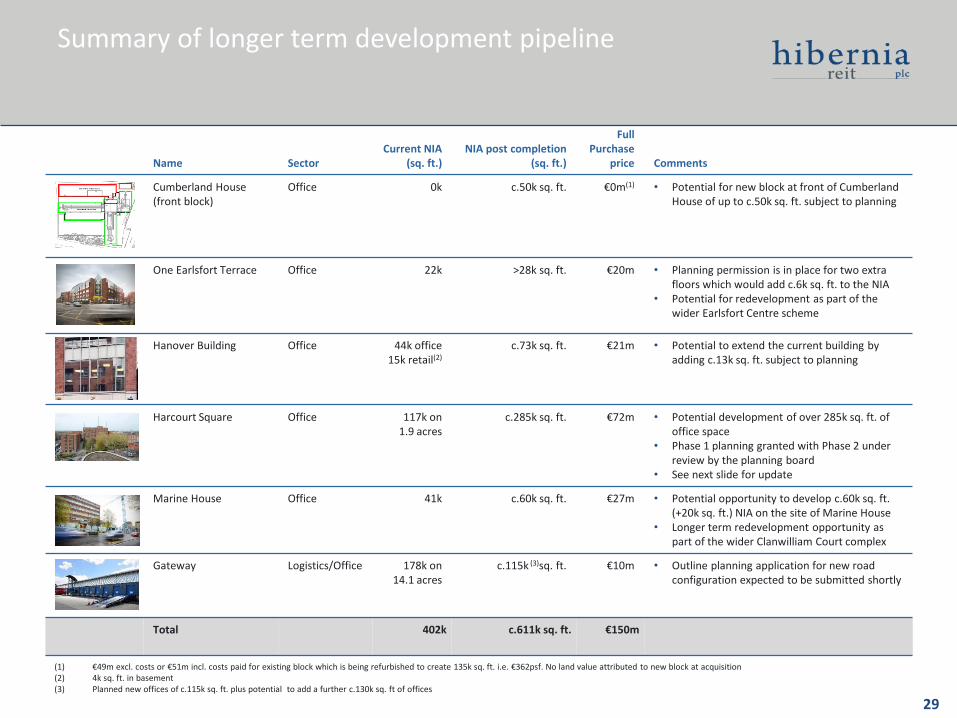

Summary of longer term development pipeline

Name SectorCurrent NIA

(sq. ft.)NIA post completion

(sq. ft.)

Full Purchase

price Comments

Cumberland House (front block)

Office 0k c.50k sq. ft. €0m(1) • Potential for new block at front of Cumberland House of up to c.50k sq. ft. subject to planning

One Earlsfort Terrace Office 22k >28k sq. ft. €20m • Planning permission is in place for two extra floors which would add c.6k sq. ft. to the NIA

• Potential for redevelopment as part of the wider Earlsfort Centre scheme

Hanover Building Office 44k office15k retail(2)

c.73k sq. ft. €21m • Potential to extend the current building by adding c.13k sq. ft. subject to planning

Harcourt Square Office 117k on 1.9 acres

c.285k sq. ft. €72m • Potential development of over 285k sq. ft. of office space

• Phase 1 planning granted with Phase 2 under review by the planning board

• See next slide for update

Marine House Office 41k c.60k sq. ft. €27m • Potential opportunity to develop c.60k sq. ft. (+20k sq. ft.) NIA on the site of Marine House

• Longer term redevelopment opportunity as part of the wider Clanwilliam Court complex

Gateway Logistics/Office 178k on14.1 acres

c.115k (3)sq. ft. €10m • Outline planning application for new road configuration expected to be submitted shortly

Total 402k c.611k sq. ft. €150m

(1) €49m excl. costs or €51m incl. costs paid for existing block which is being refurbished to create 135k sq. ft. i.e. €362psf. No land value attributed to new block at acquisition(2) 4k sq. ft. in basement(3) Planned new offices of c.115k sq. ft. plus potential to add a further c.130k sq. ft of offices

29

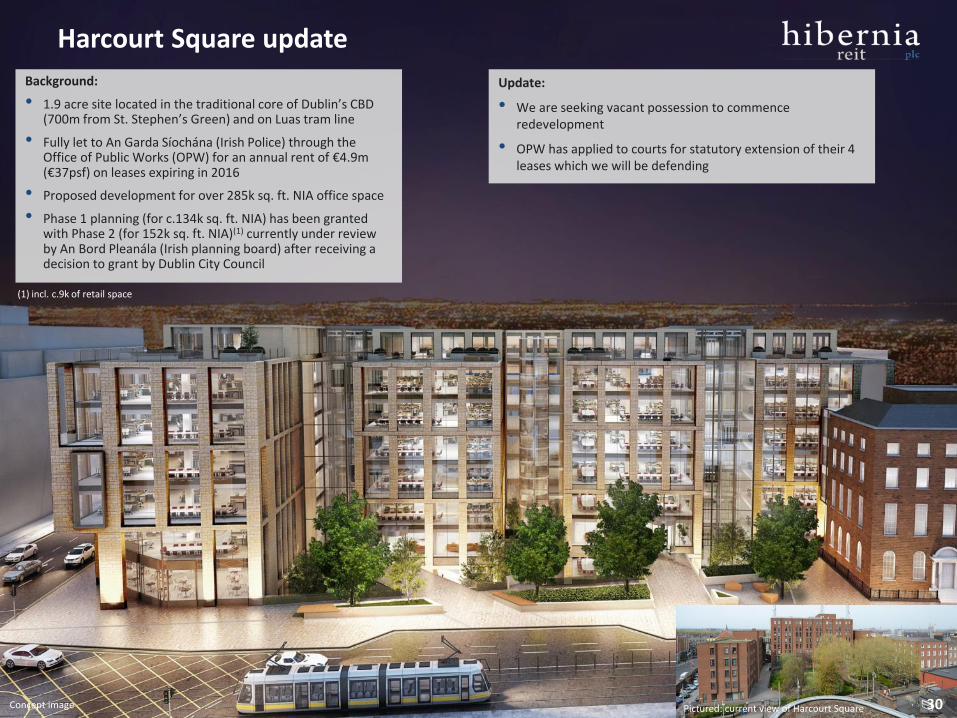

Harcourt Square update

Concept image

Background:

• 1.9 acre site located in the traditional core of Dublin’s CBD (700m from St. Stephen’s Green) and on Luas tram line

• Fully let to An Garda Síochána (Irish Police) through the Office of Public Works (OPW) for an annual rent of €4.9m (€37psf) on leases expiring in 2016

• Proposed development for over 285k sq. ft. NIA office space

• Phase 1 planning (for c.134k sq. ft. NIA) has been granted with Phase 2 (for 152k sq. ft. NIA)(1) currently under review by An Bord Pleanála (Irish planning board) after receiving a decision to grant by Dublin City Council

30Pictured: current view of Harcourt Square

Update:

• We are seeking vacant possession to commence redevelopment

• OPW has applied to courts for statutory extension of their 4 leases which we will be defending

(1) incl. c.9k of retail space

31

Agenda

Market update

Acquisitions and developments

Portfolio management

Conclusion and outlook

Highlights

Financial results

% of

portfolio Initial Equivalent Reversionary

1. Dublin CBD Offices

Traditional Core €237m 25.6% 4.4% 2.9% 16.6% 3.2%² 5.2%² 5.6%² €10.4m

IFSC €237m 25.5% 6.4% 6.4% 29.7% 3.1% 5.2% 5.4% €8.0m

South Docks €173m 18.6% 6.0% 4.4% 28.8% 2.7% 5.4% 5.7% €5.7m

Total Dublin CBD Offices €647m 69.7% 5.6% 4.5% 24.4% 3.0% 5.2% 5.6% €24.1m

2. Dublin CBD Office

Development/Refurbishment€155m 16.7% 24.4% 24.4% 69.0% – – – –

3. Dublin Residential €113m 12.2% 2.3% 2.3% 20.4% 4.6% 4.6% 4.6% €5.4m

4. Industrial €12m 1.3% 15.6% 15.6% 19.3% 3.9% 7.4% 7.9% €0.5m

Total Investment Properties

(incl. offices)€928m 100.0% 8.3% 7.2% 29.5% 3.3% 5.2% 5.4% €30.0m

Passing rent

(€m)

Value as at

Mar 16

(all assets)

Yield on value (%)

% uplift since

acquisition (all assets)

incl. costs(1)

% uplift since

Sep 15

incl. new acqusition

% uplift since

Sep 15

excl. new acqusition

32

Portfolio summary

Valuation uplift supported by letting activity and progress on development assets

(4)

(1) Includes capex(2) excludes Harcourt Square as this is valued by CBRE on a residual/development appraisal basis; excludes 39 Harcourt Street and Camden Street; includes One Dockland Central, of which c.77% is currently under

refurbishment and is therefore not income producing(3) Excl. Harcourt Square and all Dublin CBD Office Development/Refurbishment(4) South Docks excludes the value of space occupied by Hibernia in South Dock House

(2) (2) (2)

(3) (3) (3)

Banking & capital markets

40%

Government 20%

Insurance & reinsurance

5%

TMT10%

Other 13%

Professional services

12%

€27.3m

20%

11%

10%

8%5%4%

4%

4%

3%

2%

29%

Remainder

€27.3m

In-place office portfolio statistics

33

Industry split of in-place tenants Top 10 tenants of in-place portfolio (by contracted rent)

(1) Excl. the c.30k sq. ft. of 1DLC and entire 11k sq. ft. SOBO Works that were committed developments as at 31 Mar 2016 (1DLC valued at c.€25m and SOBO Works valued at c.€6m). 1DLC and SOBO Works were completed shortly after year end

(2) As per CBRE Mar 2016 except for Harcourt Square which is an internal estimate as it is valued on a development/residual basis(3) Weighted by contracted rent

• In-place office portfolio – i.e. portfolio excluding assets under development or refurbishment – has the following characteristics:

– Value at 31 Mar: €616m(1)

– Passing rent of €24.1m; contracted rent of €27.3m

– Average rent of €33psf vs ERV(2) of €44psf

– Average 2.0yrs to earlier of rent review or lease expiry

– 45% of leases(3) with break or expiry beyond 2019

34

Office leasing activity during the year and future lettings

Office leasing activity this year

Tenant Building Type

Contracted rent€m

Contracted rent €psf

% of Group

rent

Term

NotesTo expiry To break

Cumberland House

Office €5.3m €50psf(1) 14% 20yrs 12yrs • Lease which starts in Q4 2016 extended by a total of 16.5k sq. ft. through additional areas & design efficienciesgenerating additional rent of €0.7m

One DocklandCentral

Office €1.3m €45psf 3% 20yrs 10.5yrs • Lease commenced in February 2016 (6 month rent free)

SOBO Works Office €0.4m €35psf(2) 1% 13yrs(3) 6yrs • Lease commenced in April 2016 (10 month rent free)(4)

Central Quay Office €0.6m €52.50psf 2% 10yrs 3yrs • Lease commenced in April 2016

Various CBD offices €0.2m €32.85psf <1% N/A N/A • Flexible short term leases signed on Hanover St. East and rent review agreed with Morgan Stanley in Observatory Building

Total €7.8mFuture lettings

Building TypeOffice NIA

sq. ft. Available from Notes

1DLC Office 30k sq. ft. Immediately • In advanced discussions with potential tenant regarding the entire remaining space

Central Quay Office 18k sq. ft. Immediately • In discussions with potential occupiers

Cumberland House Office 33k sq. ft. Q4 2016 • In discussions with potential occupiers

1WML Office 122k sq. ft.(5) Late 2017 • Marketing commenced

1SJRQ Office 110k sq. ft. Mid 2018 • Marketing commenced

Total 313k sq. ft.

(5) Hibernia owns 50%(1) Office area only i.e. excl. additional basement(2) Stepped rent for 4yrs. €35psf is average over period(3) Weighted average. Main lease is for 15yrs(4) 6 months rent free plus an additional 4 months rent free in lieu of landlord credit

€0m

€1.0m

€2.0m

€3.0m

€4.0m

€5.0m

€6.0m

€7.0m

€8.0m

Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Sep-19 Mar-20 Sep-20 Mar-21

Co

ntr

acte

d R

ent

Six months ended

Valuers' ERV at 31 Mar 16

35

Schedule of rent reviews(1) for in-place office tenants

To earlier of rent review or lease expiry

(1) To earlier of rent review or lease expiry. Excludes various parking licenses, retail space in office buildings and Parkrite in the Forum(2) Harcourt Square ERV is internal assessment excl. redevelopment. All other ERVs are per CBRE as at 31 Mar 2016

Weighted average period to rent review or lease expiry of 2.0 years

Current in-place office contracted rent: €27.3m

Avg. rent: €26psf

Avg. rent: €46psf

Avg. rent: €50psf

Avg. rent: €30psf

Avg. rent: €48psf

Avg. rent: €24psf

Avg. rent: €36psf

Avg. rent: €26psfAvg. rent: €36psf

Avg. rent: €33psf

(2)

Remainder of non-core assets Units Carrying value

Residential assets 15 3,569

Total 15 3,569

Sale agreed at year end Units Carrying value Price agreed Expected profit(1)

Residential assets 1 354 460 106

Total 1 354 460 106

36

Progress on sale of non-core assets

Progress on sale of non-core assets in y/e Mar 16

Since period end the sale of the agreed unit has formally closed and the sale of a further 7 units (from the remainder) has also been agreed with a gross sale value of €1.8m

Sold or contracted in year Units Carrying value Sales price Profit

Residential assets 46 12,168 13,134 966

Commercial assets 3 2,410 3,580 1,170

Total 49 14,578 16,714 2,136

(€ in thousands)

(€ in thousands)

(€ in thousands)

(1) Excl. tax payable on net profits arising on disposal

37

Agenda

Market update

Acquisitions and developments

Portfolio management

Conclusion and outlook

Highlights

Financial results

38

Company delivering on strategy

Portfolio rich in development and asset management opportunities

Supportive property market and Irish economic backdrop

Hibernia well positioned to exploit further opportunities

Conclusion and outlook

Creating value through active management

39

Appendix

Location of portfolio

40

(1) property assets > €5m in value as at 31 March 2016 Key: Office Residential Industrial Office developmentSource: Google Maps, Visit Dublin, Jones Lang LaSalle

Croke ParkFairview Park

River Liffey

Kings Inns

St. Stephens

Green

9

8 7

6

212

13

14

4

5

11

10

15

Central Dublin portfolio(1)

1 Wyckham Point

2 New Century House

3 Gateway Site

4 Montague House

5 Hardwicke House

6 Chancery Building and Chancery Apartments

7 Hanover Building

8 1WML

9 Observatory

10 Guild House (Two Dockland Central)

11 One Dockland Central

12 The Forum

13 1SJRQ

14 Cumberland House

15 Harcourt Square

16 Dundrum View

17 Central Quay

18 One Earlsfort Terrace

19 Marine House

3

M1

M50

M50

N3/M3

N2/M2

M50

Dublin

N81

Howth

Clontarf

DublinAirport

North BullIsland

Portmarnock

Blanchardstown

Clondalkin

Tallaght

Blackrock

Ballsbridge

Rathfarnham

Phibsborough

DrumcondraCastleknock

Sutton

NorthernCross

Beaumont

Ballymun

The Ward

NorthwestBusiness Park

Glenageary

Dundrum

Palmerstown

Kimmage

N11

Ballymount

N4/M4

N7/M7

1 Wyckham Place

3 Gateway Site

16 Dundrum View

1 &16

3

Dublin Overview(1)

17

18

19

CBD

1 &16

Herbert Park

12 mths to

31-Mar-16

12 mths to

31-Mar-15

Revenue 32,786 18,769

Direct property costs (2,497) (725)

Property Income 30,289 18,044

IM base fee - (4,690)

IM performance fee accrual (6,069) (5,772)

Adminis trative expenses (8,696) (1,584)

Net finance income / (costs ) (4,087) (1,575)

Net rental profit 11,437 4,423

Revaluation/other ga ins :

Investment properties (2) 125,056 90,868

Other ga ins and losses(3) (171) (2,368)

Taxation 475 (691)

Total revaluation/other gains: 125,360 87,809

Net income for the period 136,797 92,232

Diluted IFRS EPS (cents) 20.1 18.3

EPRA Earnings 10,024 3,961

Diluted EPRA EPS (cents) 1.5 0.80

31-Mar-16 31-Mar-15

Investment Properties (1) 927,656 641,296

Assets held for sa le 3,921 18,499

Other non current assets 14,977 152

Cash and cash equiva lents 23,187 139,048

Trade and other receivables 18,880 9,046

Gross assets 988,621 808,041

Current l iabi l i ties (19,323) (54,907)

Financia l l iabi l i ties (72,724) -

Net assets 896,574 753,134

Equity share capita l 672,398 657,987

Reta ined earnings 226,161 91,388

Dividends pa id (8,121) (2,013)

Other reserves 6,136 5,772

Total equity 896,574 753,134

IFRS NAV per share (cents) 131.6 112.4

Diluted IFRS NAV per share (cents) 130.7 111.6

EPRA NAV per share (cents) 130.8 111.8

41

Summary financial statements

Balance sheet highlights Summary income statement

(€ in thousands)(€ in thousands)

(1) Incl. 50% interest in Windmill Lane(2) 12 months to March 2015 includes €10m gain from Block 3, Wyckham Point classified as ‘other gains’ in income statement (3) Profits arising on disposal of non-core properties offset by amortisation of base fee paid to “non-restricted” vendors

42

Further statistics

Contributions to Irish GDP growth

Source: CSO, Goodbody, Hibernia

Source: CBRE

Vacancies reducing and continued limited supply

-10%

-5%

0%

5%

10%

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

f

20

17

f

Consumption Government expenditure Investment Net exports

GDP growth

80

90

100

110

120

130

140

150

20

10Q

1

20

10Q

2

20

10Q

3

20

10Q

4

20

11Q

1

20

11Q

2

20

11Q

3

20

11Q

4

20

12Q

1

20

12Q

2

20

12Q

3

20

12Q

4

20

13Q

1

20

13Q

2

20

13Q

3

20

13Q

4

20

14Q

1

20

14Q

2

20

14Q

3

20

14Q

4

20

15Q

1

20

15Q

2

20

15Q

3

20

15Q

4

Dublin public transport trips Dublin port tonnage Dublin airport arrivals

Source: Dublin Economic Monitor

4 6 9 6

11 7 55

3 43

45

21

14 17

0

10

20

30

40

50

60

70

<5k sq. ft. 5k-10k sq. ft. 10k-20k sq. ft. 20k-50k sq. ft. 50k-100k sq. ft. >100k sq. ft.

No

of

Pro

per

ties

Dublin 1/3/7 Dublin 2/4 Dublin 6/8 IFSC Suburbs

Location of Grade A vacancies in Dublin CBD concentrated in suburbs

0

1

2

3

4

0

5

10

15

202530

35

40

45

50

Q4

04

Q4

05

Q4

06

Q4

07

Q4

08

Q4

09

Q4

10

Q4

11

Q4

12

Q4

13

Q4

14

Q4

15

Q1

16

Millio

ns Sq

FtMill

ion

s Sq

Ft

Occupied Stock Vacant Stock Completions (RHS)

Source: CBRE @ 31st March 2016

Dublin airport arrivals, port tonnage and public transport trips

43