preparation, compilation, and review engagements

TRANSCRIPT

Preparation, Compilation, and Review EngagementsUpdate and Review

Kimberly Burke, Ph.D., and Hugh Parker, Ph.D., CPA

AICPAStore.com | CIMAglobal.com

CPE/CPD = 4 credit hours

PREPARATION, COMPILATION, AND

REVIEW ENGAGEMENTS: UPDATE AND REVIEW

BY KIMBERLY BURKE, PH.D., AND HUGH PARKER, PH.D., CPA

Notice to readers

Preparation, Compilation, and Review Engagements: Update and Review is intended solely for

use in continuing professional education and not as a reference. It does not represent an official

position of the Association of International Certified Professional Accountants, and it is

distributed with the understanding that the author and publisher are not rendering legal,

accounting, or other professional services in the publication. This course is intended to be an

overview of the topics discussed within, and the author has made every attempt to verify the

completeness and accuracy of the information herein. However, neither the author nor publisher

can guarantee the applicability of the information found herein. If legal advice or other expert

assistance is required, the services of a competent professional should be sought.

Special note: COVID-19 resources

The Association, the global voice of the American Institute of CPAs and the Chartered Institute

of Management Accountants, is taking the Coronavirus (COVID-19) very seriously. We are

continually monitoring the virus’ impact on our members and the profession. For the most up-to-

date information on this topic, please visit the AICPA's Coronavirus Resource Center at

https://future.aicpa.org/resources/toolkit/aicpa-coronavirus-resource-center. For topic-specific

updates, please visit the following resource centers.

COVID-19 Resource Center Website

Audit and assurance https://future.aicpa.org/topic/audit-

assurance/covid-19-audit-assurance

Accounting & reporting https://future.aicpa.org/topic/accounting-

reporting/covid-19-accounting-reporting

Forensic services https://future.aicpa.org/topic/forensic-

services/covid-19-forensic-services

Valuation services https://future.aicpa.org/topic/valuation-

services/covid-19-valuation-services

Management accounting https://future.aicpa.org/topic/management-

accounting/covid-19-management-accounting

Personal financial planning https://future.aicpa.org/topic/financial-

planning/covid-19-personal-finance-planning

Small firm https://future.aicpa.org/topic/firm-practice-

management/covid-19-small-firms

Tax https://future.aicpa.org/topic/tax/covid-19-tax

Technology https://future.aicpa.org/topic/technology/covid-

19-technology

Government https://future.aicpa.org/topic/government/covid-

19-government

© 2021 Association of International Certified Professional Accountants, Inc. All rights reserved.

For information about the procedure for requesting permission to make copies of any part of this

work, please email [email protected] with your request. Otherwise,

requests should be written and mailed to Permissions Department, 220 Leigh Farm Road,

Durham, NC 27707-8110 USA.

CL4COMP GS-0421-0A Revised: February 2021

Use of materials

This course manual accompanies all formats in which the course is offered, including self-study

text, self-study online, group study, in-firm, and other formats, as applicable. Specific

instructions for users of the various formats are included in this section.

CPAs are required to participate in continuing professional education (CPE) to maintain their

professional competence and provide quality professional services. CPAs are responsible for

complying with all applicable CPE requirements, rules, and regulations of state licensing bodies,

other governmental entities, membership associations, and other professional organizations or

bodies.

Professional standards for CPE programs are issued jointly by the American Institute of Certified

Public Accountants (AICPA) and the National Association of State Boards of Accountancy

(NASBA) to provide a framework for the development, presentation, measurement, and

reporting of CPE programs. The Statement on Standards for CPE Programs (CPE standards)

is available as part of AICPA Professional Standards, either in paperback or as an online

subscription through the Association’s Online Professional Library.

Review questions and exercises for self-study participants The CPE standards require that self-study programs include review questions/exercises that

provide feedback for both correct and incorrect responses. Note that these reviews are provided

only as learning aids and do not constitute a final examination.

Requirements for claiming and receiving CPE credit CPE standards place responsibility on both the individual participant and the program sponsor to

maintain a record of attendance at a CPE program. CPAs who participate in only part of a CPE

program, should claim CPE credit only for the portion that they attended or completed.

You must document your claims of CPE credit. Examples of acceptable evidence of completion

include:

For group and independent study programs, a certificate or other verification supplied by

the CPE program sponsor

For self-study programs, a certificate supplied by the CPE program sponsor after

satisfactory completion of an examination

When you participate in group study and other live presentations, you will receive a completion

certificate from the program sponsor. CPE program sponsors are required to keep documentation

on programs for five years, including records of participation.

When you participate in self-study, you must complete the exam within one year of the date of

course purchase to receive a certificate indicating satisfactory completion of the CPE program.

The exam for self-study in print format is located in the “Examination” section at the end

of the course manual.

You can find the course code number for both the self-study exam and the self-study evaluation in the examination’s introductory material. You will complete the self-study

exam and evaluation online at https://cpegrading.aicpa.org. You must provide the unique serial number printed on the inside front cover of this publication and you must achieve a minimum passing grade of at least 70 percent to qualify for CPE credit.

— Upon achieving a passing grade, you will receive a certificate displaying the number

of CPE credits earned based on a 50-minute learning segment, in compliance with

CPE standards. The grading system provides a completion certificate online, which

you may print or save as a PDF. The grading system maintains a transcript of your

completed courses.

— If you do not achieve a passing grade, the online grading system notifies you of this

and also provides instructions for retaking the exam. You have three attempts to pass

the exam. If you do not pass the exam in three attempts, please contact the Member

Service Center at 1.888.777.7077 to obtain additional attempts.

Program evaluations The information accumulated from participant evaluation forms is important in our continual

efforts to provide high quality continuing education for the profession. When you participate in

group study and other live presentations, please return your evaluation forms prior to departing

your program sessions. When you participate in self-study, please complete the course

evaluation online. Your comments are very important to us.

Customer service For help and support, including information on refund claims and complaint resolutions, please

call the Member Service Center at 1.888.777.7077, or visit the online help page at

https://future.aicpa.org/cpe-learning.

© 2021 Association of International Certified Professional Accountants. All rights reserved. Table of Contents 1

Table of Contents

Current Economic Environment 1

The U.S. business environment 2

Implications of the current economy 9

Summary 19

Solutions 21

Recent Statements on Standards for Accounting and Review Services Developments 23

SSARS No. 25, Materiality in a Review of Financial Statements and Adverse Conclusions – 2020 24

SSARS No. 24, Omnibus Statement on Standards for Accounting and Review Services – 2018 30

SSARS Nos. 22–23, Compiling pro forma and prospective financial information 41

Summary 47

Solutions 51

Current Practice Issues 57

AICPA resources 58

Current independence and ethics issues 62

Current issues from ARSC 72

QC section 10, A Firm’s System of Quality Control 76

Summary 79

Practice question — Quality control 80

Solutions 83

Current Accounting and Reporting Issues 89

Common deficiencies in peer reviews 90

Recent accounting standards overview 97

Other accounting frameworks 114

Summary 117

Practice questions 118

Solutions 119

© 2021 Association of International Certified Professional Accountants. All rights reserved. Table of Contents 2

On the Horizon 123

Resources 124

ARSC pipeline 126

FASB pipeline 127

Summary 131

Solutions 133

Glossary 135

© 2021 Association of International Certified Professional Accountants. All rights reserved. 1

Current Economic Environment

Learning objectives

Identify the key economic factors that may affect clients and their financial statements.

Identify financial reporting implications of the coronavirus pandemic.

Recall the accountant’s responsibility for going concern issues.

Recall the accountant’s responsibility for subsequent events.

Recall the accountant’s responsibility for fraud and recommendations for minimizing fraud-related risk.

Recognize the accountant’s responsibility for other engagement issues related to the coronavirus pandemic.

© 2021 Association of International Certified Professional Accountants. All rights reserved. 2

The U.S. business environment In performing a review engagement, accountants are required to have an understanding of the industry in

which the client operates. Economic factors, including interest rates, availability of credit, consumer

confidence, overall economic expansion or contraction, inflation, and labor market conditions are likely to

have an impact on clients and their financial statements. Specifically, adverse effects in these economic

factors may provide sufficient pressure or motivation for client managers to adopt more aggressive

accounting and financial reporting strategies. In the current year, accountants also must consider the

economic effects of the coronavirus pandemic on financial reporting decisions and the degree to which it

has left the economy vulnerable.

Globally, gross domestic product (GDP) growth is slowing down to an annual growth rate of around 3%,

with some countries, like the United States and Japan, offsetting weaker results in others’ advanced

economies such as Europe. Trade tensions, globally, are affecting business confidence and investment,

but these tensions are often offset by strong labor markets and consumer spending.

As described later, economic indicators such as GDP, unemployment, and the federal fund rate

demonstrate an economy that has not recovered from the coronavirus pandemic. There seems to be a

divergence, however, between the rallying stock market and the stumbling economy since April 2020.

Although the overall decline in the Dow Jones Industrial Average had a decline of 2.7% for 2020, as of the

third quarter, the average demonstrated a leap in the second quarter that increased it by about 10,000

points. The average grew another 7.6% in the third quarter. Overall, as of the third quarter of 2020, the

NASDAQ composite index is up 24.5%, gaining 11% in the third quarter, following a slight 5% decline in

September. As the government and Federal Reserve make great efforts to support the recovery in the

economy, stocks would be preferred option in a purchaser’s portfolio, especially when the interest rate is

expected to stay near zero. The Chicago Board Options Exchange Volatility Index (VIX) is considered an

indicator of investor sentiment, market volatility, and fear in the market. The VIX increased to above 66 in

March 2020, the highest level seen since the Great Recession of 2008. As of December 2020, the VIX has

dropped to 20.82. Although indicative of a relatively low risk environment, the VIX is still significantly

elevated when compared to the range of 15–17 during the previous decade.

One of the leading indicators of a country’s economic health is its GDP. GDP measures output of goods

and services by labor and property within the United States. It increases as the economy grows and

decreases as the economy slows and is a main indicator of a recessionary economy. The pandemic’s

effects are reflected in GDP during 2020, although it is not possible to isolate those effects. Generally

speaking, consumer and business spending both contributed to the decline as they followed government-

issued “stay at home” orders. Consumers reduced consumption of both goods and services, and

business spending declined or was redirected. In the first quarter of 2020, real GDP decreased at an

annual rate of 5%. The second quarter of 2020 continued to reflect the effects of the pandemic as real

GDP decreased at an annual rate of 31.7%. In the third quarter of 2020, real GDP increased at an annual

rate of 33.1% (second estimate). The increase reflects attempts of the economy to return to “normal”

following the shutdown in the previous quarters. More specifically, the increase has been attributed to

positive contributions from nonresidential fixed investment, residential investment, and exports. These

© 2021 Association of International Certified Professional Accountants. All rights reserved. 3

increases were partially offset by negative contributions from state and local government spending,

private inventory investment, and personal consumption expenditures. Imports that reduce the

calculation of GDP also increased.

The unemployment rate, reflecting the number of employable people who are actively seeking work, is

another indicator of economic health. The pandemic also contributed to significant changes in

unemployment rates during 2020 as captured by the Bureau of Labor Statistics. To offer some

perspective, the unemployment rate was 3.5% for December 2019, where a rate of between 4% and 6% is

generally considered to reflect a healthy economy. In April 2020, as government-issued “stay at home”

orders took effect, unemployment rose to 14.7%, representing 23.1 million people. Of those,

approximately 18.1 million were temporarily laid off. The unemployment rate increased steadily through

May, followed by steep reductions in unemployment in October 2020, when the unemployment rate fell to

6.9%, which represents approximately 11.1 million people. Of those, approximately 3.2 million people

were temporarily laid off. Although a significant improvement over the highest unemployment rate in May

of 2020, the October 2020 unemployment rate of 6.9% is almost twice the 3.5% rate of unemployment in

February 2020.

The federal funds rate is another important indicator of economic health in that it is used to manage

inflation, unemployment, and other interest rates, including the prime rate. During the financial crisis of

2008–2009, the Federal Reserve Board decreased the target rate for the federal funds rate more than 5.0

percentage points. From its high of 5.25% prior to the crisis, it was decreased to less than 0.25%, where it

remained through November 2015. In December 2015, the board raised the range of its benchmark

interest rate by a quarter of a percentage point to between 0.25% and 0.50%. The board noted that the

change resulted from considerable improvement in the labor market, citing an unemployment rate of

5.0%. After steadily raising the target rate throughout 2018, reaching a high of 2.5%, the Board of

Governors of the Federal Reserve System decreased the target for the federal funds rate in 2019 to

between 1.75% and 2.0%. During 2020, as the coronavirus pandemic continued to adversely affect the

economy, the Board of Governors reduced the target rate to between 0% and 0.25%. The Board of

Governors has indicated that they are likely to leave the rate at this level until 2023 when the labor market

conditions should reflect healthy employment and an inflation rate of 2%. In the meantime, the Federal

Reserve chairman reiterated that the Federal Reserve would use all the tools at its disposal to assist the

economy and market.

Although the U.S. economy is slowly coming back to life as businesses reopen, it may take years for the

economy to recover from the fallout due to the pandemic. Accountants should continue to monitor

economic factors such as interest rates, consumer confidence, overall economic expansion or

contraction, inflation, and the labor market. Accountants should also consider the effects of these

economic factors on their clients and the clients’ engagements this year.

Business confidence

The CPA Outlook Index (a measure of sentiment about the U.S. economy and key business performance

categories conducted by the AICPA) surveys members in business and industry holding executive

© 2021 Association of International Certified Professional Accountants. All rights reserved. 4

positions in both public and privately owned organizations of all sizes, and across a broad spectrum of

industries. The overall index reflects several measures, including optimism regarding (1) the U.S.

economy, (2) the respondent’s organization, and (3) prospects for expansion. Typically, an index of

greater than 50 indicates a generally positive outlook with increasing activity. The overall index decreased

from 76 in the first quarter of 2020 to 38 in the second quarter, rising to 54 in the third quarter of 2020.

Optimism about the U.S. economy decreased from 42% in the third quarter of 2019 to 24% in the third

quarter of 2020. Those respondents who were more optimistic about the U.S. economy cited low interest

rates, construction, consumer spending, and resilience of the economy. Those respondents who were more

pessimistic cited the pandemic’s effect on the economy, business closures, and unemployment.

Organizational optimism decreased from the third quarter of 2019 to the third quarter of 2020, from 58% to

41%, corresponding to decreases in expansion plan optimism 61% to 43%. Respondents noted that labor

costs remain the top concern influencing both organizational and expansion optimism.

Legislative and regulatory developments

Tax Cuts and Jobs Act

On December 22, 2017, President Donald Trump signed into law H.R. 1, known as the Tax Cuts and Jobs

Act (TCJA), which makes widespread changes to the Internal Revenue Code. Almost all of its provisions,

including a lower corporate tax rate of 21% and lower individual income tax rates, went into effect

January 1, 2018.

Among the many changes to current tax law was one that permanently lowered the corporate income tax

rate from 35% to 21%, effective for 2018. The Senate version lowered the rate to 20% but delayed its

effective date until 2019; the House bill originally had a 20% rate that would have been effective in 2018.

The bill also lowered the individual income tax rates through 2025. The new top rate will be 37%, lowered

from 39.6%. The law keeps the same number of brackets as under current law. It also keeps the

individual alternative minimum tax (AMT), with a higher exemption than under current law, but eliminates

the corporate AMT.

CARES Act

The global pandemic continues to adversely affect the global economy, causing significant business

disruption. As a result, the U.S. government introduced the Coronavirus Aid, Relief, and Economic

Security (CARES) Act to prevent economic downturn in various ways. The CARES Act was an over $2

trillion relief package that Congress passed at the end of March 2020. This act provides prompt

economic assistance for American workers and families, small businesses, and state and local

governments.

The relief package will have a huge impact on state and local government budgets. The CARES Act

provides economic impact payments to American households of $1,200 per adult ($2,400 for joint filers)

for individuals whose income was less than $99,000 (or $198,000 for joint filers) and $500 per child. The

© 2021 Association of International Certified Professional Accountants. All rights reserved. 5

credit begins to phase out for taxpayers with adjusted gross income above $150,000 for joint filers,

$112,500 for heads of households, and $75,000 for other individuals. Stimulus rebates are being treated

as advance refunds of a 2020 tax credit. Taxpayers will reduce the amount of the credit available on their

2020 tax return by the amount of the advance refund they receive. The credit is not available to

nonresident aliens, individuals who can be claimed as a dependent by another taxpayer, and estates and

trusts.

Additionally, the IRS will use the information for Forms SSA-1099 and RRB-1099 to generate $1,200

economic impact payments to Social Security recipients who did not file tax returns in 2018 or 2019.

Recipients will receive these payments as a direct deposit or by paper check, just as they would normally

receive their benefits.

The small business Paycheck Protection Program (PPP) is providing small businesses with necessary

resources to cover applicable overhead and payroll costs. According to the PPP report (round 2), the

overall average loan size is $108,000, and the top loan size category is between $350,000 and $1 million.

The top industry sectors by the North American Industry Classification System are health care and social

assistance, professional, scientific and technical services, and construction.

As part of the Families First Coronavirus Response Act (HR 6201), employers of fewer than 500

employees are required to provide mandatory sick time and paid family leave, and are eligible for payroll

tax credits to offset the costs. Eligible self-employed individuals also qualify for the credits. Health care

providers and emergency responders are excluded; employers with fewer than 50 employers can be

exempted.

The CARES Act offers great support to businesses to help them get back to business quickly. Eligible

employers who suffer economic hardship and face closure orders due to the pandemic will get a

refundable tax credit of 50% of qualified wages (up to $10,000) for employees. Employers with gross

receipts below 50% of the comparable quarter in 2019 are also eligible, until their gross receipts exceed

80% of the comparable quarter in the prior year. Qualifying wages are based on the average number of

employees in 2019. For employers with more than 100 employees, the credit is allowed if the employer

pays employees who are not providing services due to the suspension of the business or a drop in gross

receipts. For employers with 100 or fewer employees, all wages paid qualify for the credit. Employers can

reimburse the credit immediately by reducing the deposits of payroll taxes that have been withheld from

employees’ wages.

There are also other changes, such as payroll tax deferral. Employers and self-employed individuals can

delay payment of the employer share of the Social Security tax. The deferred employment tax can be paid

in two years – payment is delayed by 50% for the 2020 employer’s share of Social Security payroll taxes

until December 31, 2021; the other 50% will not be due until December 31, 2022. The CARES Act includes

provisions that are directly related to the risk of material misstatement such as unrecorded transactions,

fraud, and noncompliance with laws and regulations.

The CARES Act offers significant and temporary relief on retirement funds. According to the act,

taxpayers can take up to $100,000 in coronavirus-related distributions from retirement plans without

being subject to the 10% additional tax for early distributions. Eligible distributions can be made between

© 2021 Association of International Certified Professional Accountants. All rights reserved. 6

January 1 and December 31, 2020. In addition, the distribution may be exempted from 20% mandatory

withholdings for certain retirement plan distributions. Coronavirus-related distributions may be repaid

within three years. Any resulting income inclusion would be subject to tax over three years. Existing loans

of up to $100,000 from qualified plans and repayment can be delayed for one year. The required

minimum distribution rules are temporarily suspended for 2020. The bill delays 2020 minimum required

contributions for single-employer plans until 2021. Note that the required contributions are not waived

and accordingly should be accrued in the appropriate period.

These are some interesting tax traits in the CARES Act that are particularly important to insurers or the

affiliates, stakeholders, or brokers, such as net operating losses (NOLs) and AMT credit refunds. For tax

years beginning before 2021, the 80% income limitation for NOL deductions is temporarily repealed.

For losses arising in tax years 2018, 2019, and 2020, a five-year carryback is allowed (taxpayers can elect

to forgo the carryback). This law also applies to pass-through businesses and sole proprietorships.

In terms of the AMT credit refunds acceleration, the CARES Act allows corporations to claim 100% of

AMT credits in 2019 as fully refundable and provides an election to claim the AMT credit refund in 2018.

That means the AMT credit for corporations is now a refundable credit for the 2018 and 2019 tax years.

However, attention to the process (for instance, the due date) should be paid in order to select the best

relief method.

The CARES Act established the Coronavirus Relief Fund of $150 billion for states and local and tribal

governments, and it also creates guidance on eligible uses of fund disbursements by the government.

COVID-19 relief bill (December 2020)

In late December 2020, legislation passed to provide $900 billion in additional relief due to the global

pandemic. The bill provides aid for small businesses, including $284 billion for the PPP as well as $20

billion in economic injury disaster loans and grants for smaller businesses in low-income communities.

Additional PPP funding is available to previous recipients of PPP loans, even if they have returned part or

all of a previous PPP loan. Previous recipients can apply for another loan up to $2 million if they have 300

or fewer employees, have used or will use the full amount of their first PPP loan, and can show 25% gross

revenue decline in any 2020 quarter compared to the same quarter in 2019. In addition, the new bill

makes forgivable loans available to 501(c)(6) businesses such as chambers of commerce, visitors’

bureaus, and other organizations with 300 or fewer employees that do not receive more than 15% of

receipts from lobbying.

The new round of funding is available to first-time borrowers, including the following:

Businesses with 500 or fewer employees that are eligible for other SBA 7(a) loans Sole proprietors, independent contractors, and eligible self-employed individuals Not-for-profits Accommodation and food services operations with fewer than 300 employees per physical location

© 2021 Association of International Certified Professional Accountants. All rights reserved. 7

The new bill provides an expanded list of potentially forgivable expenses, including, for example, personal

protective equipment and software and cloud computing services. In addition, the bill also specifies that

business expenses paid with forgiven PPP loans are tax-deductible, superseding previous IRS guidance.

The legislation also includes the following key provisions:

Aid for entertainment and cultural organizations, including access for shuttered live venues, independent movie theaters, and cultural institutions to $15 billion in dedicated funding, while $12 billion is set aside to help businesses in low-income and minority communities.

Aid for individuals, including $166 billion for economic impact payments of $600 for individuals making up to $75,000 per year, and $1,200 for married couples making up to $150,000 per year, as well as a $600 payment for each dependent child.

Extension of unemployment benefits, including $120 billion to provide workers receiving unemployment benefits an addition $300 per week supplement from December 26, 2020–March 14, 2021. The bill also expands coverage to self-employed gig workers and others in nontraditional employments, as well as additional weeks of federally funded unemployment benefits to individuals who exhaust their regular state benefits.

Rental aid and eviction protection, including $25 billion in rental aid and extension of the national eviction moratorium through January 31, 2021.

Other support, including $45 billion in transportation funding for airlines, transit systems, state highways, etc.; $82 billion in funding for colleges and schools; $22 billion for health-related expenses incurred by state and local governments; $13 billion in emergency food assistance; and $7 billion in broad band expansion.

In addition, the bill extends the employee retention tax credit and several expiring tax provisions, and

temporarily allows a 100% business expense deduction for meals (increased from the current 50%) as

long as the expense is for food or beverages provided by a restaurant, applicable to expenses incurred

after December 31, 2020, and before December 31, 2022.

Unrecorded sales tax liabilities

In 1992, the Supreme Court ruled in Quill vs. North Dakota that states were not allowed to collect sales

taxes on retail sales made by sellers who did not have a physical presence in the state. Over time, e-

commerce increased dramatically from mail order retailers like Quill to online-only businesses, and states

were foregoing the tax revenues associated with those sales. In 2018, the Supreme Court reversed the

Quill ruling in the case of South Dakota vs. Wayfair Inc. In the Wayfair case, the Supreme Court ruled that

a physical presence is no longer required in order for a state to require a retailer to collect sales or use

tax. The court also ruled that its decision excluded businesses with fewer than 200 transactions or

$100,000 of in-state sales collected in the state.

Since the Wayfair decision, some taxing authorities have set thresholds that exceed those set by the

Supreme Court. Although the Wayfair decision was made in 2018, taxing authorities also have set

different effective dates for implementing the decision. As a result, online retailers that make sales in

different states must become familiar and compliant with the statutes in effect in the relevant states.

These circumstances could affect financial statements of retailers with sales in multiple states. When

those financial statements are the subject of a review engagement, accountants should include

© 2021 Association of International Certified Professional Accountants. All rights reserved. 8

questions about the appropriate collection of sales tax and multistate compliance in their inquiry

procedures. Analytical procedures could also be performed to determine the reasonableness of the sales

tax liability.

Knowledge check

1. Which statement about economic indicators is not correct?

a. The federal funds rate is used to manage inflation and unemployment. b. GDP measures output of goods and services by labor and property within the United States,

increasing as the economy grows and decreasing as the economy slows. c. When considering the CPA Outlook Index, an index of greater than 50 indicates a generally

positive outlook with increasing activity. d. A 7% unemployment rate is inside the range of what is typically considered healthy.

© 2021 Association of International Certified Professional Accountants. All rights reserved. 9

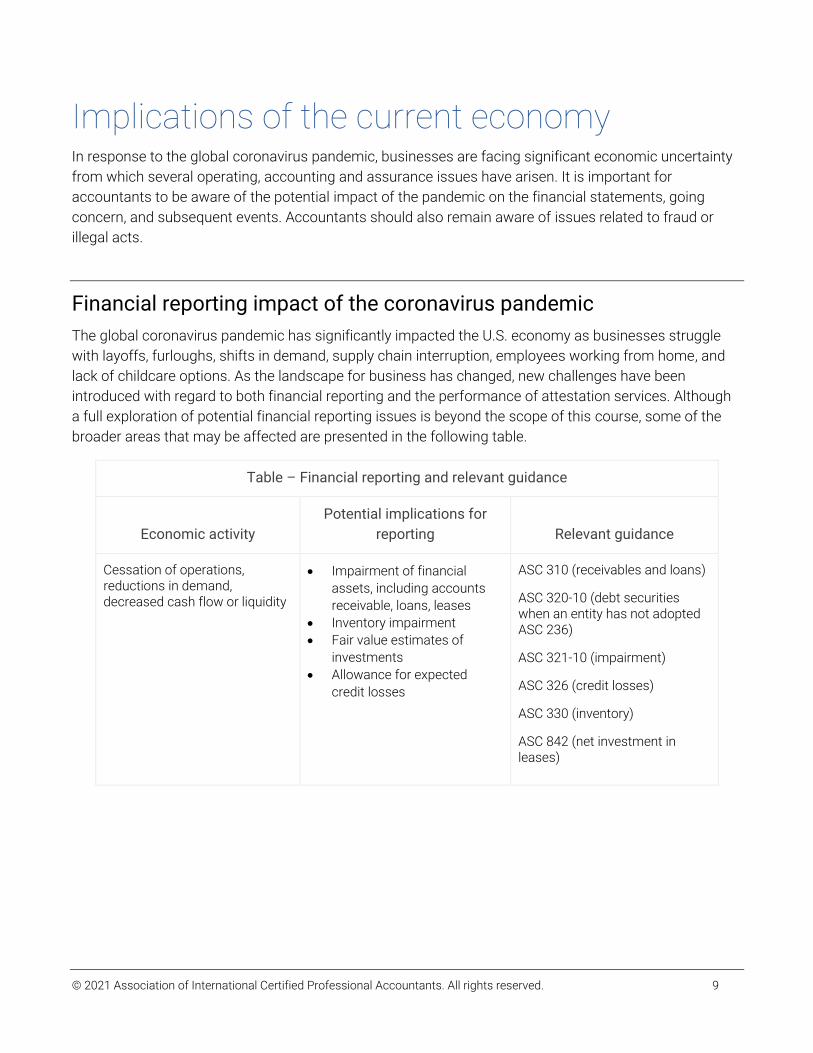

Implications of the current economy In response to the global coronavirus pandemic, businesses are facing significant economic uncertainty

from which several operating, accounting and assurance issues have arisen. It is important for

accountants to be aware of the potential impact of the pandemic on the financial statements, going

concern, and subsequent events. Accountants should also remain aware of issues related to fraud or

illegal acts.

Financial reporting impact of the coronavirus pandemic

The global coronavirus pandemic has significantly impacted the U.S. economy as businesses struggle

with layoffs, furloughs, shifts in demand, supply chain interruption, employees working from home, and

lack of childcare options. As the landscape for business has changed, new challenges have been

introduced with regard to both financial reporting and the performance of attestation services. Although

a full exploration of potential financial reporting issues is beyond the scope of this course, some of the

broader areas that may be affected are presented in the following table.

Table – Financial reporting and relevant guidance

Economic activity

Potential implications for

reporting Relevant guidance

Cessation of operations, reductions in demand, decreased cash flow or liquidity

Impairment of financial

assets, including accounts

receivable, loans, leases

Inventory impairment

Fair value estimates of

investments

Allowance for expected

credit losses

ASC 310 (receivables and loans)

ASC 320-10 (debt securities when an entity has not adopted ASC 236)

ASC 321-10 (impairment)

ASC 326 (credit losses)

ASC 330 (inventory)

ASC 842 (net investment in leases)

© 2021 Association of International Certified Professional Accountants. All rights reserved. 10

Table – Financial reporting and relevant guidance

Economic activity

Potential implications for

reporting Relevant guidance

Cessation of operations, decreased revenues, supply chain interruptions, decline in global equity markets

Change in circumstances

requiring impairment testing

of indefinite-lived assets

Triggering event for

recoverability test of long-

lived assets

Impairment of right-of-use

assets

Triggering event for testing

impairment of goodwill

ASC 350-20 (impairment of goodwill)

FASB Accounting Standards Codification (ASC) 350-30 (impairment of indefinite-lived assets

FASB ASC 360-10 (recoverability of long-lived assets)

FASB ASC 842-20 (impairment of leased assets)

Lease concessions, including reduced prices, deferral of payment terms, forgiveness of lease amounts

Contract no longer contains

a lease

Separate lease contract or a

modification of existing

contract

FASB ASC 842 (leases and lease modifications)

FASB Staff Q&A, Topic 842 and Topic 840: Accounting for Lease Concessions Related to the Effects of the Covid-19 Pandemic

Liquidity issues affecting collectability of sales, contract concessions to encourage continued purchases, delays in delivery of goods

Lack of a contract due to

changes in enforceable rights

or collectability

Contract modification due to

concessions

Variable consideration from

price concessions or

incentives

Significant financing

component introduced with

extended payment terms

Timing of revenue

recognition due to delays in

delivery

FASB ASC 606-10

© 2021 Association of International Certified Professional Accountants. All rights reserved. 11

Table – Financial reporting and relevant guidance

Economic activity

Potential implications for

reporting Relevant guidance

Reductions in workforce costs through voluntary and nonvoluntary employee furloughs, payment of voluntary or nonvoluntary termination benefits

Compensation expense

calculation and accrual

Estimation of related

compensation liability

FASB ASC 420-10 (involuntary termination benefits)

FASB ASC 710-10 (temporary layoff treated like compensated absences)

FASB ASC 712-10 (temporary layoff treated like postemployment benefit)

FASB ASC 715-30 (involuntary termination benefits

EITF Issue No. 01-10, Accounting for the Impact of the Terrorist Attacks of September 11, 2001

Business entities receive government assistance, as grants, loans, or tax credits

Consider whether the

transaction is an exchange or

contribution

Recognize revenue for

exchange transactions

Recognition of government

grants/contributions

FASB ASC 606 (accounting for exchange)

FASB ASC 958-605 (accounting for contribution) excludes for-profit businesses but may be used for purposes of analogy.

International Accounting Standards 20 (may be appropriate for accounting for contributions to businesses)

Reductions in revenues, incurrence of losses, reductions in forecasted cash flow

Realizability of deferred tax

assets

Need for valuation account

for deferred tax assets

FASB ASC 740 (income taxes)

CARES Act provisions related to income taxes for 2019 and 2020

5-year NOL carryback

provisions for losses created

in 2018–2020

Deferral of the 80% income

limitation for NOL carryovers

from 2018–2021

CARES Act

© 2021 Association of International Certified Professional Accountants. All rights reserved. 12

Table – Financial reporting and relevant guidance

Economic activity

Potential implications for

reporting Relevant guidance

Overall economic volatility Increased need for

disclosures because the

assumptions and estimates

underlying the financial

statements are likely to

change in the near term

Increased need for

disclosure of current

vulnerabilities due to

concentrations of risk

FASB ASC 275-10 (risks and uncertainties)

Engagement issues related to the coronavirus pandemic

The disruption caused by the pandemic has already dramatically changed business operations

worldwide. For entities that have survived the coronavirus pandemic, their operations may look very

different from prior years, or they may struggle to maintain compliance with debt covenants. For other

businesses, closure has resulted from the effects of the pandemic, and it is likely these closures will

continue, presenting concerns about an entity’s ability to continue as a going concern. In addition, as the

economy and business operations continue to change quickly, there is an increasing need for

accountants to be aware of and prepared for addressing subsequent events in the performance of a

review engagement. Unfortunately, accountants may also encounter situations that indicate fraud or an

illegal act in this particularly volatile environment as many businesses struggle to survive.

Going concern

Accountants performing review engagements are required to consider whether, during the performance

of review procedures, evidence or information came to the accountant’s attention indicating that there

could be an uncertainty about the entity’s ability to continue for a reasonable period of time, which is

typically within one year after the date that the financial statements are issued or within one year after

the date the financial statements are available to be issued.

Some financial reporting frameworks, such as generally accepted accounting principles (GAAP), require

management to evaluate an entity’s ability to continue as a going concern for a reasonable period of

time. When the financial reporting framework requires management’s evaluation, the accountant

reviewing those financial statements should perform procedures to determine the following:

© 2021 Association of International Certified Professional Accountants. All rights reserved. 13

Whether the going concern basis of accounting is appropriate Management’s evaluation of whether there are conditions or events that raised substantial doubt

about the entity’s ability to continue as a going concern If there are conditions or events that raised substantial doubt about the entity’s ability to continue as

a going concern, and management’s plans to mitigate those matters The adequacy of the related disclosures in the financial statements

When a financial reporting framework does not include a requirement for management to evaluate the

entity’s ability to continue as a going concern for a reasonable period of time, the accountant may

become aware of conditions or events that raise substantial doubt about an entity’s ability to continue as

a going concern for a reasonable period of time. Under these circumstances, the accountant should do

the following:

Inquire of management whether the going concern basis of accounting is appropriate Inquire of management about its plans for dealing with the adverse effects of the conditions and events Consider the adequacy of the disclosure about such matters in the financial statements

With regard to the adequacy of disclosures, the guidance focuses on providing sufficient detail of the

origin, possible magnitude of effect, and management’s response, including management’s plans and

information about the recoverability of recorded asset or liability accounts.

Typically, going concerns will be reflected in the accountant’s report using an emphasis-of-matter

paragraph. When the accountant concludes that substantial doubt about the entity’s ability to continue

as a going concern for a reasonable period of time remains, the emphasis-of-matter paragraph should be

expressed through the use of terms consistent with those included in the applicable financial reporting

framework but should not use conditional language such as “subject to.” When the accountant concludes

that substantial doubt has been alleviated by management’s plans, the accountant may include an

emphasis-of-matter paragraph referring to management’s disclosures related to the conditions and

events and management’s plans related to those conditions or events. When an accountant becomes

aware of a failure to perform a going concern evaluation or provide adequate disclosure of going

concern, and the client decides not to change the financial statements, the only reporting option is to

note the departure from the applicable financial reporting framework in the compilation or review report.

Subsequent events

Given the volatility of the economy and the speed with which events have occurred during the

coronavirus pandemic, accountants performing a review engagement should be prepared to consider

information that comes to light during the period between the date of the balance sheet and the date the

financial statements are issued. Evidence of subsequent events that may have a material effect on

reviewed financial statements may come to the accountant’s attention either during the performance of

the review procedures or subsequent to the date of the review report, but prior to the release of the

report. In either case, the accountant should first request management to consider the possible effects

of the subsequent event on the financial statements and related notes.

If the accountant determines that the subsequent event has been adequately reflected in the financial

statements, the accountant may choose to include an emphasis-of-matter paragraph drawing the

© 2021 Association of International Certified Professional Accountants. All rights reserved. 14

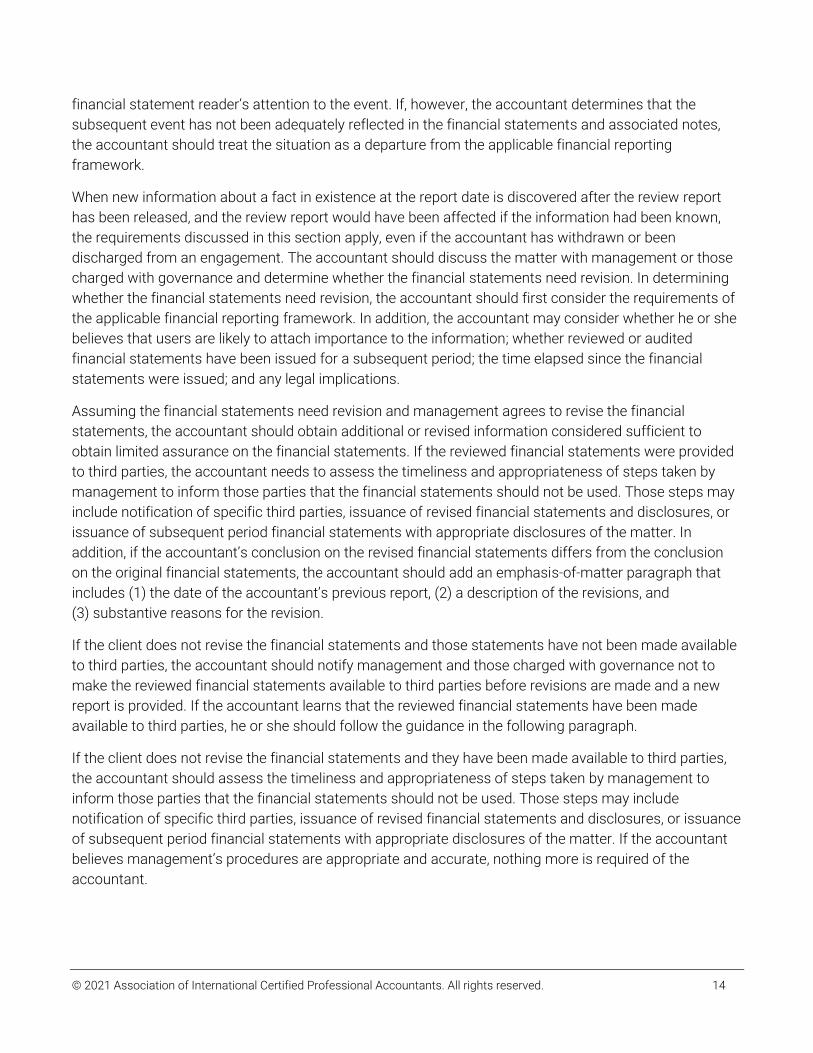

financial statement reader’s attention to the event. If, however, the accountant determines that the

subsequent event has not been adequately reflected in the financial statements and associated notes,

the accountant should treat the situation as a departure from the applicable financial reporting

framework.

When new information about a fact in existence at the report date is discovered after the review report

has been released, and the review report would have been affected if the information had been known,

the requirements discussed in this section apply, even if the accountant has withdrawn or been

discharged from an engagement. The accountant should discuss the matter with management or those

charged with governance and determine whether the financial statements need revision. In determining

whether the financial statements need revision, the accountant should first consider the requirements of

the applicable financial reporting framework. In addition, the accountant may consider whether he or she

believes that users are likely to attach importance to the information; whether reviewed or audited

financial statements have been issued for a subsequent period; the time elapsed since the financial

statements were issued; and any legal implications.

Assuming the financial statements need revision and management agrees to revise the financial

statements, the accountant should obtain additional or revised information considered sufficient to

obtain limited assurance on the financial statements. If the reviewed financial statements were provided

to third parties, the accountant needs to assess the timeliness and appropriateness of steps taken by

management to inform those parties that the financial statements should not be used. Those steps may

include notification of specific third parties, issuance of revised financial statements and disclosures, or

issuance of subsequent period financial statements with appropriate disclosures of the matter. In

addition, if the accountant’s conclusion on the revised financial statements differs from the conclusion

on the original financial statements, the accountant should add an emphasis-of-matter paragraph that

includes (1) the date of the accountant’s previous report, (2) a description of the revisions, and

(3) substantive reasons for the revision.

If the client does not revise the financial statements and those statements have not been made available

to third parties, the accountant should notify management and those charged with governance not to

make the reviewed financial statements available to third parties before revisions are made and a new

report is provided. If the accountant learns that the reviewed financial statements have been made

available to third parties, he or she should follow the guidance in the following paragraph.

If the client does not revise the financial statements and they have been made available to third parties,

the accountant should assess the timeliness and appropriateness of steps taken by management to

inform those parties that the financial statements should not be used. Those steps may include

notification of specific third parties, issuance of revised financial statements and disclosures, or issuance

of subsequent period financial statements with appropriate disclosures of the matter. If the accountant

believes management’s procedures are appropriate and accurate, nothing more is required of the

accountant.

© 2021 Association of International Certified Professional Accountants. All rights reserved. 15

If not, the accountant should notify the appropriate personnel at the highest levels in the entity (such as

the owner or those charged with governance) that, in the absence of disclosure by the client, the

accountant will take steps to prevent further use of the financial statements and, if applicable, the

accountant’s report. The authors recommend that the accountant immediately contact legal counsel.

Unless otherwise counseled by the accountant’s attorney, the accountant should

notify the client that the accountant’s review report must no longer be used. notify the regulatory agencies that have jurisdiction over the client that the accountant’s report should

no longer be used, including a request that the agency take whatever steps it deems appropriate. notify each person known to the accountant to be using the financial statements that the financial

statements and the accountant’s report should no longer be used. In many instances, it will not be practicable for the accountant to give appropriate individual notification to stakeholders whose identities ordinarily are unknown to him or her; notifying a regulatory agency that has jurisdiction over the client will usually be the only practicable way for the accountant to provide appropriate disclosure. The accountant should request the regulatory agency to take whatever steps it may deem appropriate to accomplish the necessary disclosure.

Any notification to persons other than the client should include a description of the nature of the

subsequently acquired information and its effects on the financial statements. In addition, the

information disclosed should be as precise, factual, and concise as possible, providing no more

information than that which is reasonably necessary. If the client has not cooperated, the accountant’s

disclosure does not need to detail the specific information, but can merely indicate that information has

come to his or her attention that the client has not cooperated in attempting to substantiate, and that, if

the information is true, the accountant believes that the review report must no longer be used.

Accountant’s responsibility for fraud or illegal acts

Accountants performing engagements in accordance with Statements on Standards for Accounting and

Review Services (SSARSs) are under no obligation to search for fraud or illegal acts. The engagement

letter should inform the client that such engagements cannot be relied upon to discover fraud or illegal

acts.

If the accountant becomes aware that fraud (including misappropriation of assets) may have occurred,

the accountant should communicate the matter to the appropriate level of management (at a level above

those involved with the suspected fraud, if possible). If the accountant becomes aware of matters

involving identified or suspected noncompliance with laws and regulations whose effects should be

considered when preparing financial statements, the accountant should communicate the matters to

management, other than when matters are clearly inconsequential. If the fraud or noncompliance with

laws or regulations involves senior management or results in a material misstatement of the financial

statements, the accountant should communicate the matter directly to those charged with governance.

The accountant should consider the need to obtain legal advice and take appropriate action, including

potential withdrawal, if management or (as appropriate) those charged with governance do not provide

sufficient information that supports that

© 2021 Association of International Certified Professional Accountants. All rights reserved. 16

the financial statements are not materially misstated due to fraud, or the entity is in compliance with laws and regulations, and in the accountant’s professional judgment,

the effect of the suspected noncompliance may be material to the financial statements.

Sarah Beckett Ference, CPA, is a risk control director at CNA and oversees risk controls services provided

to CPA firms in the AICPA Professional Liability Insurance Program. In the article “Failure to Detect Theft

or Fraud: It’s not just an audit issue,” originally published in the February 2014 issue of the Journal of

Accountancy, Ference noted several techniques that CPAs could use to protect themselves against risk

exposures related to failure to detect theft and fraud. These recommendations have been modified to be

applicable to SSARSs engagements, and include the following:

Regularly evaluate the risk of the client and the engagement. Client and engagement acceptance and continuance protocols are not simply for audit engagements. Regularly screen clients and consider the risks associated with both the client and the services you are being engaged to perform. It should raise a red flag for the CPA when clients dismiss internal control weaknesses brought to their attention. Is this a situation where the client has an unreasonable service expectation, or is it possibly one of questionable integrity? Either way, the CPA should take precautions.

Use engagement letters on all engagements. Even though SSARS No. 21, Statement on Standards for Accounting and Review Services: Clarification and Recodification, now requires an engagement letter or other suitable form of written agreement for review, compilation, and preparation services, claim experiences of the AICPA Professional Liability Insurance Program have indicated there is room for improvement. A well-crafted engagement letter can help reduce expectation gaps and can serve as key evidence in the defense of a professional liability claim. The engagement letter should include an understandable description of the scope and limitation of services to be performed, a statement that the engagement is not designed to detect theft or fraud, and the responsibilities of both the client and the CPA. The engagement letter should also be renewed and signed by the client annually.

Stay within the scope of the engagement. An engagement letter is useful only if the CPA adheres to the defined scope in rendering the professional services. Additional services, or modifications to agreed-upon services, should be memorialized in writing with the client, whether it’s through email, a new engagement letter, or an amendment to the existing engagement letter.

Be fraud aware. Train all firm personnel, not only auditors, about potential fraud risk factors and the “fraud risk triangle” (opportunity, rationalization, and incentive/pressure). Learn about the risk factors associated with common frauds, such as embezzlement by an unmonitored bookkeeper or controller with excessive authority or access, or use of business credit cards for personal expenses. Firm personnel should be educated about common internal control weaknesses that create an opportunity for fraud to occur, such as a lack of segregation of duties, poor tone at the top, or infrequent vacations taken by key financial employees.

Apply professional skepticism to all engagements. This is particularly important with engagements with longtime clients, in which a level of established comfort could threaten objectivity. Trust your instincts and follow up on matters that don’t seem quite right.

If you see something, say something, and follow up in writing. Management letters with suggestions for control or process improvements are not designed solely for audit clients. If you observe a weakness in internal controls or believe management should follow up on an observation noted, inform your client orally and in writing. If the weakness persists year after year, keep telling the client both orally and in writing until the deficiency is addressed.

Document, document, document. Contemporaneous documentation represents critical evidence in the defense of professional liability claims. Strong documentation includes, at a minimum, a well-crafted and detailed engagement letter, documentation regarding client inquiries made and responses received, and communication of internal control matters or suspicious activities noted.

© 2021 Association of International Certified Professional Accountants. All rights reserved. 17

Without documentation, many juries are more sympathetic to the client. Documentation provides defense counsel with something to defend.

Other issues

One of the primary performance requirements for review engagements is the application of analytical

procedures to the financial statements. These procedures involve comparisons of recorded amounts, or

ratios, developed from recorded amounts to expectations developed by the accountant conducting the

review. The accountant develops expectations by identifying and using plausible relationships that are

reasonably expected to exist based on his or her understanding of the client and the industry in which the

client operates. These expectations are most often based on comparable financial information from prior

periods.

Given the effects of the coronavirus pandemic on entities across most industries, it may not be

reasonable to develop expectations for the current year based on prior years. Instead, the accountant

may need to consider other sources of information to develop expectations. These other sources might

include the following:

Anticipated results. For example, budgets or forecasts including extrapolations from interim or annual data.

Relationships among elements of financial information with the period. For example, ratio analysis of gross profit percentage.

Information regarding the industry in which the client operates. For example, gross margin information.

Relationships of financial information with relevant nonfinancial information. For example, estimated interest expense based on principal and average rate of return.

With the ongoing uncertainty, entities may face challenges including delays in financial statement

issuance and financial ramifications of the pandemic. Breaches of financial covenants based on

calculations of income, earnings before interest, taxes, depreciation, and amortization (or EBITDA), or

some similar measure of earnings, will become more scrutinized as borrowers face lower revenues and

increased costs in dealing with the pandemic. Borrowing base calculations, which are often based on

levels of accounts receivable, may reduce amounts available to borrowers under existing lines of credit.

A covenant default might require the reclassification of long-term debt to short-term debt, which in turn

might cause violations of additional financial covenants, such as liquidity ratios. Accountants may want

to discuss whether there would be a need for waivers or amendment of the relevant terms of the loan

agreement with their clients as part of the engagement.

Given the number of issues specific to the pandemic, the accountant should consider additional

appropriate representations in the management representation letter for review engagements. For

example, the accountant may include additional representations for matters such as going concern,

subsequent events, risk and uncertainties, fraud, significant estimates, and so on.

In addition, accountants conducting a review engagement may also want to consider adding an

emphasis-of-matter paragraph to the review report. For example, an emphasis paragraph might be

appropriate to draw attention to subsequent events, or major catastrophes related to the pandemic.

© 2021 Association of International Certified Professional Accountants. All rights reserved. 18

Recall that these paragraphs are used to draw attention to items that are appropriately accounted for

and disclosed in the financial statements. They are not appropriate for missing information or inadequate

disclosure.

Connected concepts – Advising clients

Assume you are supervising a review engagement for a long-standing client in the restaurant industry. The client has a significant loan and is required to provide reviewed financial statements to her lender annually. This year, the client’s business has been struggling due to the global pandemic. Her restaurants closed temporarily due to government mandates, and once they reopened, the restrictions on seating, masks, and customer behavior resulted in significantly fewer customers. Currently, customer demand is insufficient to support a full contingent of employees, many of whom have been with the company for several years, and the client is concerned about making her lease payments. In addition, shortly before the shutdown, the client had ordered significant product, leaving her with excess inventory. What options could you offer your client regarding cost savings for the review engagement? What practical advice would you give the client to help her manage her relationship with the lender and protect her income?

Knowledge check

2. Which of the following statements about the financial reporting implications of the pandemic is correct?

a. The standards for revenue recognition have been revised due to the coronavirus pandemic. b. Volatile economic activity may indicate the need to consider the impairment of assets. c. Lessees may postpone implementation of the new lease standard due to the pandemic. d. The CARES Act has no impact on the carryback or carryforward provisions for net operating

losses.

3. What should an accountant do when he or she becomes aware that adequate disclosure of going concern issues has not been made by the preparer of the financial statements being reviewed and the client decides not to change the financial statements?

a. No mention of the going concern issues is necessary. b. The accountant should include an emphasis-of-matter paragraph. c. The accountant should modify the review report noting the nature and dollar magnitude (if

known) of the omitted disclosure. d. The accountant must withdraw from the engagement.

4. Which is not a way to limit risk exposure related to fraud in a preparation, compilation, or review engagement?

a. Use engagement letters only on riskier engagements. b. Stay within the scope of the engagement. c. Apply professional skepticism to all engagements. d. Regularly evaluate the risk of the client and the engagement.

© 2021 Association of International Certified Professional Accountants. All rights reserved. 19

Summary We have just discussed the following points:

Outlook for the U.S. business economy Financial reporting implications of the coronavirus pandemic Review engagement implications of the pandemic Accountant’s responsibility for considering going concern Accountant’s resposnbility for considering subsequent events Accountant’s responsibility for fraud Accountant’s responsibility for other engagement issues related to the pandemic

© 2021 Association of International Certified Professional Accountants. All rights reserved. 20

© 2021 Association of International Certified Professional Accountants. All rights reserved. 21

Solutions

Current Economic Environment

Knowledge check solutions

1.

a. Incorrect. This statement is accurate. The federal funds rate is used to manage inflation, unemployment, and other interest rates.

b. Incorrect. This statement is accurate. GDP measures national output and has a direct relationship with economic growth.

c. Incorrect. This statement is accurate. The CPA Outlook Index is a measure of sentiment that is generally positive when above 50.

d. Correct. This statement is not accurate. An unemployment rate between 4% and 6% is generally considered healthy. A 7% unemployment rate is outside the range.

2.

a. Incorrect. Although the pandemic may have implications for revenue recognition, the requirements of the revenue recognition standard have not changed.

b. Correct. Changes such as short-term cessation of operations, reductions in demand, etc. may indicate that the value of either financial or nonfinancial assets may have changed in such a way that requires impairment.

c. Incorrect. Although the pandemic may have implications for lease accounting, the requirements of the leasing standard have not changed and implementation has not been delayed.

d. Incorrect. The CARES Act changes the requirements for accounting for NOLs. It allows for a 5-year carryback for losses generated between 2018 and 2020. The act also defers the 80% limitation in NOLs for 2018–2021.

© 2021 Association of International Certified Professional Accountants. All rights reserved. 22

3.

a. Incorrect. If the accountant is aware that the financial statements are inaccurate regarding going concern, and the preparer does not plan to change them, the accountant must make reference to this inadequacy in the compilation or review report.

b. Incorrect. An emphasis-of-matter paragraph is used to draw attention to issues appropriately accounted for in the financial statements. Failure to refer to going concern in these circumstances is not appropriate.

c. Correct. When going concern disclosure is inadequate, the accountant should describe the nature of that omission in the accountant’s report. If possible, the accountant should describe the magnitude of the omission also.

d. Incorrect. The accountant is not required to withdraw from the engagement when a going concern disclosure has been omitted.

4.

a. Correct. Engagement letters should be used on all SSARSs engagements to establish scope of work, clarify limitations, and strengthen communications and understanding between the accountant and client.

b. Incorrect. CNA recommends staying within the scope of the engagement.

c. Incorrect. CNA recommends applying professional skepticism to all engagements.

d. Incorrect. CNA recommends regularly evaluating the risk of each client and engagement.

© 2021 Association of International Certified Professional Accountants. All rights reserved. 23

Recent Statements on Standards for Accounting and Review Services Developments

Learning objectives

Identify the performance and reporting requirements for Statement on Standards for Accounting and Review Services (SSARSs) for SSARS No. 25.

Identify the reporting requirements for compilation and review engagements from SSARS No. 24.

Recall the performance and reporting requirements for compilation engagements of pro forma financial information from SSARS No. 22.

Recall the performance and reporting requirements for compilation engagements of prospective financial information from SSARS No. 23.

© 2021 Association of International Certified Professional Accountants. All rights reserved. 24

SSARS No. 25, Materiality in a Review of Financial Statements and Adverse Conclusions – 2020 In February 2020, the Accounting and Review Services Committee (ARSC) issued SSARS) No. 25,

Materiality in a Review of Financial Statements and Adverse Conclusions. SSARS No. 25 resulted in two

primary and significant changes to the guidance for review engagements. The standard requires

practitioners to determine materiality for the financial statements as a whole and apply this materiality in

designing the procedures and evaluating the results obtained from those procedures, making the

concept of materiality consistent regardless of the level of service performed on financial statements.

The standard also allows accountants to issue modified conclusions in a review engagement, and aligns

with international standards for review engagements as included in the International Standard on Review

Engagements (ISRE) 2400 (Revised), Engagements to Review Historical Financial Statements. ARSC

believes convergence between the two standards facilitates an accountant’s ability to perform and report

on engagements in accordance with both sets of standards and reduces confusion about the levels of

assurance provided by both. In addition, SSARS No. 25 includes some smaller changes to preparation,

compilation, and review engagements.

SSARS No. 25 is effective for preparation, compilation, and review engagements of financial statements

for periods ending on or after December 15, 2021. Early implementation is permitted.

Materiality in review engagements

Currently, there is no requirement for an accountant to consider materiality in the guidance for review

engagements. However, the concept of materiality is embedded throughout review engagements,

including (1) a conclusion that notes the accountant is not aware of any material modifications

necessary for the financial statements, (2) the design and performance of inquiry and analytical

procedures that reflects a focus on material items, and (3) the evaluation of uncorrected misstatements

and inadequate disclosures in which the accountant considers their effects both individually and in the

aggregate. SSARS No. 25 adds an explicit requirement that the accountant determine materiality for the

financial statements as a whole, including disclosures, and apply this materiality in designing the

procedures and evaluating results obtained from those procedures.

An accountant’s consideration of materiality is made in the context of the applicable financial reporting

framework. The standard notes that different financial reporting frameworks often discuss the concept

of materiality in the context of preparation and presentation of financial statements. Although the

specifics may differ, the discussions of materiality share some common elements, including the

following:

© 2021 Association of International Certified Professional Accountants. All rights reserved. 25

Reasonable user test. Misstatements, including omissions, are considered to be material if there is a substantial likelihood that, individually or in the aggregate, they would influence the judgment made by a reasonable user based on the financil statements.

Contextually driven. Judgments about materiality are made in light of surrounding circumstances and affected by the size or nature of a misstatement or a combination of both.

Number and nature. Judgments about materiality involve both qualitative and quantitative considerations. Qualititative factors are those that are material due to their nature, but the dollar amount alone would be considered immaterial. For example, a small misstatement that converted a net loss to net income could be considered qualitatively material.

Collective needs. Judgements about matters that are material to users of the financial statements are based on a consideration of the common financial information needs of users as a group. The possible effect of misstatements on specific individual users, whose needs may vary widely, is not considered.

In circumstances when a financial reporting framework does not include a discussion of materiality,

accountants should consider these characteristics as a frame of reference.

In addition, similarly to the auditing literature, the SSARS No. 25 notes that determination of materiality is

a matter of professional judgement and is affected by the accountant’s perception of the financial

information needs of users of the financial statements. For purposes of determining materiality, the

accountant may assume that reasonable users

have a reasonable knowledge of business and economic activities and accounting, and are willing to study the financial information with reasonable diligence;

understand that financial statements are prepared, presented, and reviewed to levels of materiality; recognize the uncertainties inherent in the measurement of amounts based on the use of estimates,

judgment, and the consideration of future events; and make reasonable judgments based on the information in the financial statements.

Although materiality should be determined and applied before designing procedures and evaluating

results, the accountant may become aware of information during the review that would have affected the

materiality determination had it been known at the time. The accountant may become aware of this

information due to a change in circumstances for the entity that occurs during the review (e.g. the

deicison to dispose of a major segment), or as a result of performing review procedures (e.g. actual

financial results are going to be signficantly different than the anticipated results used to determine

materiality). In these circumstances, accountants should revise materiality for the financial statements

taken as a whole.

ARSC does not believe an explicit requirement for the accountant to determine materiality will result in a

significant change in practice because the accountant has always had to have an understanding of

materiality in order to conclude that he or she is not aware of any material modifications that should be

made to the financial statements in order for them to be in accordance with the applicable financial

reporting framework. However, the requirement that the accountant design and perform analytical

procedures and inquiries to address all material items may result in a change in practice for some

accountants as it precludes waiving procedures on items that, while material, may be considered low

risk.

© 2021 Association of International Certified Professional Accountants. All rights reserved. 26

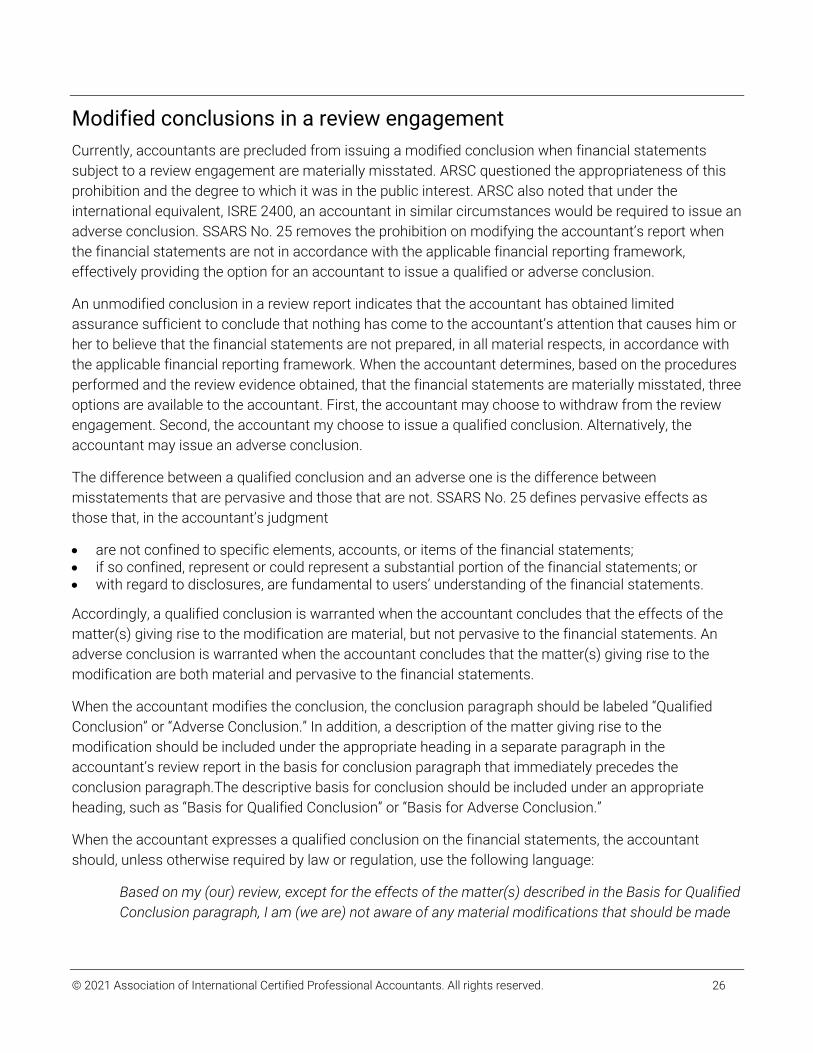

Modified conclusions in a review engagement

Currently, accountants are precluded from issuing a modified conclusion when financial statements

subject to a review engagement are materially misstated. ARSC questioned the appropriateness of this

prohibition and the degree to which it was in the public interest. ARSC also noted that under the

international equivalent, ISRE 2400, an accountant in similar circumstances would be required to issue an

adverse conclusion. SSARS No. 25 removes the prohibition on modifying the accountant’s report when

the financial statements are not in accordance with the applicable financial reporting framework,

effectively providing the option for an accountant to issue a qualified or adverse conclusion.

An unmodified conclusion in a review report indicates that the accountant has obtained limited

assurance sufficient to conclude that nothing has come to the accountant’s attention that causes him or

her to believe that the financial statements are not prepared, in all material respects, in accordance with

the applicable financial reporting framework. When the accountant determines, based on the procedures

performed and the review evidence obtained, that the financial statements are materially misstated, three

options are available to the accountant. First, the accountant may choose to withdraw from the review

engagement. Second, the accountant my choose to issue a qualified conclusion. Alternatively, the

accountant may issue an adverse conclusion.

The difference between a qualified conclusion and an adverse one is the difference between

misstatements that are pervasive and those that are not. SSARS No. 25 defines pervasive effects as

those that, in the accountant’s judgment

are not confined to specific elements, accounts, or items of the financial statements; if so confined, represent or could represent a substantial portion of the financial statements; or with regard to disclosures, are fundamental to users’ understanding of the financial statements.

Accordingly, a qualified conclusion is warranted when the accountant concludes that the effects of the

matter(s) giving rise to the modification are material, but not pervasive to the financial statements. An

adverse conclusion is warranted when the accountant concludes that the matter(s) giving rise to the

modification are both material and pervasive to the financial statements.

When the accountant modifies the conclusion, the conclusion paragraph should be labeled “Qualified

Conclusion” or “Adverse Conclusion.” In addition, a description of the matter giving rise to the

modification should be included under the appropriate heading in a separate paragraph in the

accountant’s review report in the basis for conclusion paragraph that immediately precedes the

conclusion paragraph.The descriptive basis for conclusion should be included under an appropriate

heading, such as “Basis for Qualified Conclusion” or “Basis for Adverse Conclusion.”

When the accountant expresses a qualified conclusion on the financial statements, the accountant

should, unless otherwise required by law or regulation, use the following language:

Based on my (our) review, except for the effects of the matter(s) described in the Basis for Qualified

Conclusion paragraph, I am (we are) not aware of any material modifications that should be made

© 2021 Association of International Certified Professional Accountants. All rights reserved. 27

to the accompanying financial statements in order for them to be in accordance with [the

applicable financial reporting framework].

When the accountant expresses an adverse conclusion on the financial statements, the accountant

should, unless otherwise required by law or regulation, use the following language:

Based on my (our) review, due to the significance of the matter(s) described in the Basis for