prepa’s integrated resource plan suffers from the...

TRANSCRIPT

PREPA’s integrated resource plan suffers from the fundamental flaw that it does not explore the

possibility of a future in which the island is not primarily dependent on imported fuels. The only

futures contemplated are those in which at least half a billion dollars is transferred out of the

island every year to pay for fossil fuels. Certainly, a plan to “do nothing” and stick with the status

quo is not wise, but neither is a plan to invest over a billion dollars in infrastructure to move the

island from reliance on one fossil fuel to another. PREPA’s most recent modeling exercise,

submitted on April 26, 2016, confirms that the benefits of its plan are largely dependent on a

differential in fuel prices between natural gas and fuel oil. When that differential narrows, as it

has recently, the benefit of PREPA’s plan including constructing the Aguirre Offshore Gas Port

largely evaporates. This fact should be extremely concerning to the Commission. We

appreciate the urgency that the parties may feel and the need to “do something”, but

investing huge amounts of money into infrastructure that makes Puerto Rico reliant on natural

gas and from which Puerto Rico cannot extricate itself should that reliance turn out to be a bad

bet is not the solution.

We would like to see the Commission direct PREPA to engage in a stakeholder-based process

with the goal of producing a plan that provides flexibility in the face of uncertainty about key

assumptions such as fuel prices and future demand; takes into account rate impacts; and

leverages cost-effective, less risky resources like renewables, energy efficiency, and demand

response.

Given the absence of such a plan in the current IRP, these comments focus on flaws in the

Company’s current modeling such as risks overlooked and resources inappropriately modeled.

Our comments address what we see as the major deficiencies in PREPA’s IRP modeling,

including

a. a lack of modeling integrated supply and demand-side resources;

b. the failure to consider a lower load forecast sensitivity;

c. the unnecessarily high reserve margin that results in an overbuilding of thermal

generation;

d. capital cost assumptions which favor thermal generation;

e. the failure to adequately consider renewable resources; and

f. the unrealistic assessment of the costs and risks of AOGP.

If PREPA had conducted meaningful IRP modeling, all generation resources – including supply

side and demand side resources – would have been treated on a consistent and integrated

basis as resources that can be used to meet electricity demand. Different resources –

conventional generation, energy efficiency, demand response and renewables – would have

been assigned a cost and a generation expansion model run to find the portfolio of resources

that meets projected demand at the lowest system cost, subject to whatever constraints are

externally imposed on the system (such as constraints of capital availability, for example). This

was not done in this case. Instead, PREPA pre-selected generation expansion plans, layered a

fixed amount of energy efficiency on top of them and then added varying amounts of

renewable energy generation. Even in scenarios in which PREPA included higher amounts of

renewable energy to achieve full compliance with the RPS, these additions were not

accompanied by any reduction in the buildout of central station generation. Thus, there was no

attempt to determine how much renewables, energy efficiency and demand response could

be added, with a reduced amount of central station generation, to meet projected load at the

lowest system cost.

Because of this failure to integrate supply-side and demand-side resources, both PREPA’s

August and Supplemental March IRPs are largely focused on changes or additions to its central

station fleet. More distributed resources including wind, solar, demand response, and energy

efficiency, to the extent they were included, generally have little influence on the treatment of

the central station generators.

This presents a missed opportunity for PREPA. It consigns Puerto Rico to indefinite reliance on

imported fuels and their associated risks simply because the alternative was not considered.

A scenario that relies on fossil fuel-free resource additions rather than investment in central

station generators requires more creativity and effort to model than was required by PREPA’s

methodology, but cannot be dismissed out of hand as unachievable or uneconomic. The high

cost of supplying electricity in Puerto Rico and uncertain economic growth and population

should make PREPA wary of pursuing large-scale capital projects with unguaranteed costs and

benefits. Rather PREPA should be pursuing a portfolio of resources that reduces reliance on

imported fuel, allows flexibility of build-out, and leverages innovative solutions on both the

demand and supply-sides.

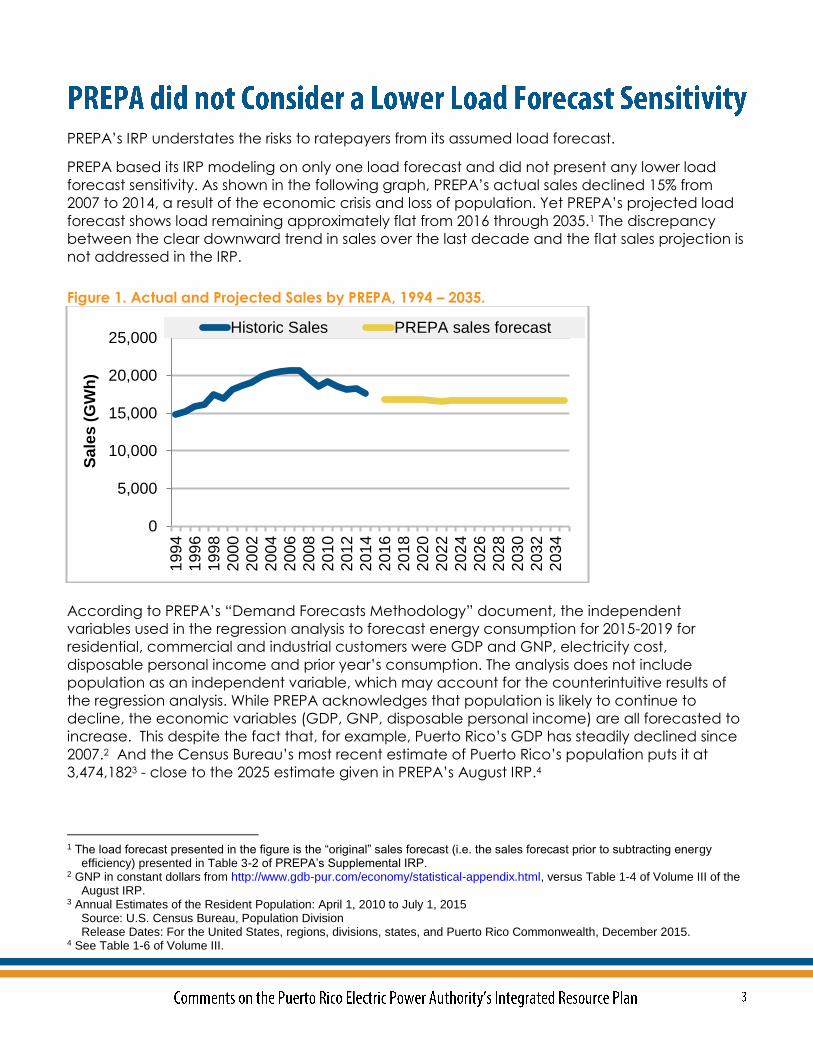

PREPA’s IRP understates the risks to ratepayers from its assumed load forecast.

PREPA based its IRP modeling on only one load forecast and did not present any lower load

forecast sensitivity. As shown in the following graph, PREPA’s actual sales declined 15% from

2007 to 2014, a result of the economic crisis and loss of population. Yet PREPA’s projected load

forecast shows load remaining approximately flat from 2016 through 2035.1 The discrepancy

between the clear downward trend in sales over the last decade and the flat sales projection is

not addressed in the IRP.

Figure 1. Actual and Projected Sales by PREPA, 1994 – 2035.

According to PREPA’s “Demand Forecasts Methodology” document, the independent

variables used in the regression analysis to forecast energy consumption for 2015-2019 for

residential, commercial and industrial customers were GDP and GNP, electricity cost,

disposable personal income and prior year’s consumption. The analysis does not include

population as an independent variable, which may account for the counterintuitive results of

the regression analysis. While PREPA acknowledges that population is likely to continue to

decline, the economic variables (GDP, GNP, disposable personal income) are all forecasted to

increase. This despite the fact that, for example, Puerto Rico’s GDP has steadily declined since

2007.2 And the Census Bureau’s most recent estimate of Puerto Rico’s population puts it at

3,474,1823 - close to the 2025 estimate given in PREPA’s August IRP.4

1 The load forecast presented in the figure is the “original” sales forecast (i.e. the sales forecast prior to subtracting energy

efficiency) presented in Table 3-2 of PREPA’s Supplemental IRP. 2 GNP in constant dollars from http://www.gdb-pur.com/economy/statistical-appendix.html, versus Table 1-4 of Volume III of the

August IRP. 3 Annual Estimates of the Resident Population: April 1, 2010 to July 1, 2015

Source: U.S. Census Bureau, Population Division Release Dates: For the United States, regions, divisions, states, and Puerto Rico Commonwealth, December 2015.

4 See Table 1-6 of Volume III.

0

5,000

10,000

15,000

20,000

25,000

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

201

6

201

8

202

0

202

2

202

4

202

6

202

8

203

0

203

2

203

4

Sa

les

(G

Wh

)

Historic Sales PREPA sales forecast

For modeling purposes, the above forecast of energy sales must be converted into a forecast of

electricity to be generated by PREPA’s plants by adding technical and non-technical losses.

PREPA assumes these technical and non-technical losses are constant through the forecast

period, meaning that generation is approximately 20% higher than sales for the entire forecast

period. Non-technical losses are assumed to be constant at 7% of sales, or more than 1,100

GWh per year. We know of no other U.S. utility that experiences that level of “non-technical”

losses; in fact, “unbilled” or “unaccounted for” energy is generally so trivial that it is not

separately estimated. At the April 6, 2016 technical conference, PREPA representatives stated

that they are aggressively trying to reduce non-technical losses. It would have been reasonable

to consider a scenario in which PREPA is successful in reducing its non-technical losses to a lower

level.

The fact that PREPA’s load forecast departs markedly from the last decade of historical data,

relies on a limited set of explanatory variables and does not include any of PREPA’s attempts to

reduce non-technical losses, suggest that a lower load forecast would have been more

realistic.

PREPA argued during the technical conference that it was not necessary to run a sensitivity

analysis with a lower load forecast because the energy efficiency scenario used in its

Supplemental IRP sufficiently models the impacts of lower load. Energy efficiency should not be

seen as a substitute for an accurate load forecast. PREPA should aim to obtain cost-effective

energy efficiency resources in any scenario, regardless of the levels of forecasted loads. If the

load forecast turns out to be lower than PREPA anticipates, that does not mean that PREPA

should not continue to procure cost-effective energy efficiency. In developing an IRP, PREPA

should consider the possibility that the level of energy efficiency considered in the supplemental

IRP could be obtained on top of a lower load forecast.

Thus, PREPA’s IRP does not provide any modeling of the optimum generation buildout, including

cost-effective energy efficiency, to meet a lower load forecast.

By failing to model a lower demand forecast sensitivity, PREPA’s IRP does not fully explore the risk

to ratepayers of overbuilding its system. Under PREPA’s preferred buildout plan, if the load

forecast does not materialize, the costs of underutilized capacity must still be recovered from

ratepayers. PREPA’s preferred plan lacks flexibility because it appears that it must immediately

make financial commitments totaling more than $1.5 billion in order to meet its timeline (Figure 2

below). That figure includes transmission, AOGP, and central station generator costs. PREPA’s

ratepayers are on the hook for this investment even if the load to support it does not materialize

as forecasted.

Figure 2. Many of the Key Resource Decisions in PREPA’s Preferred Plan Appear to Require

Immediate Financial Commitments

An assessment of need is a key part of any resource planning. The prior section discusses a key

input to the needs assessment – the load forecast. In this section, we explain why the additional

steps in PREPA’s need assessment – namely the determination of capacity needed to maintain

an adequate reserve margin - may not be appropriate and impose significant, unnecessary

costs on customers.

Like any other utility, PREPA seeks to provide customers with a reliable power supply. A utility

may do so by reducing or shifting demand and by providing power in a pattern that matches

customer demand. Apart from what seems to be PREPA’s recent commitment to meet the

Commission’s energy efficiency scenario of an incremental 0.2 percent per year from 2017 to

2024 and stabilizing thereafter at 1.5% per year, the IRP is focused on meeting demand through

supply-side measures only, i.e., providing power that matches customer demand. This

approach undoubtedly raises costs to customers because it ignores lower-cost demand side

options and the ability of demand-side management improve the value of generation to which

PREPA has already committed.

Using demand response (DR), PREPA can shift or shave peak demand so that the peak occurs

when its solar facilities are operating, enabling it to assign capacity credit to those solar

resources. Demand response can take many forms, but a common DR program focuses on air

conditioning (both residential and commercial) and cycles units more frequently during peak

demand times and/or increases their setback temperature. Such a program would likely be

appropriate for Puerto Rico given its climate.

Demand response can also take the place of “steel in the ground”, a scenario that PREPA

never discusses. In fact, PREPA’s analysis of demand response seems entirely focused on

demand response’s ability to avoid curtailment of renewables. It dismisses demand response

out of hand as uneconomic because, PREPA contends, demand response’s cost would have to

be combined with high cost PV generation, making both more expensive than a combined

cycle unit. However, there is no reason that demand response must be paired with any

resource; instead, it should be evaluated on its own merits for its ability to compete with any

supply or demand side resource.

PREPA views demand response as providing no value other than that illustrated in Figure 3 – it

moves consumption from hours 20 – 24 and 1 – 3 to hours 8 – 16. That is, the hourly demand

curve moves from the blue line to the red line.

Figure 3. Projected Hourly Demand on Maximum Demand Day in 2025 with and without DR5

In this example, while DR shifts the peak to daytime hours, it does nothing else. It does not, for

example, as the above-mentioned residential air conditioning DR program would do,

contribute to reducing the peak load. In addition to failing to consider the ability of DR to shave

peak load, PREPA’s IRP also underestimates the capability of many other resources to meet its

peak load. This leads PREPA to inflate its reserve margin and to plan to build more generation

resources than are necessary.

One of the benefits of DR that PREPA does not consider is that, by shifting the peak from

evening to daytime hours, DR opens up the possibility that solar can contribute towards

5 From page 7-2 of IRP Supplement.

meeting the peak system demand. PREPA’s IRP currently does not give any “capacity credit”6

to its solar generators. It also, inexplicably, does not give credit to wind or landfill gas plants. This

leaves new thermal generation as the only resource that can be built to fill any identified

capacity need.

PREPA’s need is also inflated by the assumption that hundreds of megawatts worth of its existing

generators provide no capacity credit despite the fact that they provide energy. And several

of PREPA’s units are accredited at a capacity much lower than their nameplate capacity either

for reasons that are unknown or because of extremely high forced outage rates. Inexplicably,

PREPA never analyzes the possibility of improving its fleet forced outage rates, which could be

much more cost-effective than building new capacity.

While PREPA provides an estimate of reserve margins in its Supplemental IRP, e.g. Figure 8-1, it’s

our understanding that those graphs demonstrate a reserve margin metric that is essentially

meaningless because they are based on the installed capacity of PREPA’s units. Rather,

something PREPA terms “firm capacity” was used as the benchmark to determine whether a

portfolio had sufficient capacity resources to meet a 25 – 30 percent reserve margin

requirement. It is the firm capacity metric that ignores renewables and existing peaking

capacity.

In order to demonstrate how much of a difference alternative assumptions about the capacity

credit of renewables and existing peaking resources and the peak capacity value of demand

response makes, we’ve attempted to rework PREPA’s firm capacity estimates using new

assumptions. Because we do not have access to the same data that PREPA does, our

assumptions cannot be definitive, but rather are indicative of how the firm capacity

contribution of each resource might be more fairly treated. Table 1, below, describes the

assumptions we made with respect to demand response, solar, wind, landfill gas, hydro, and

certain existing thermal generators.

6 Capacity credit is generally assigned to generators in accordance with the probability of their producing energy (in the case of

renewables) or being available to produce energy (in the case of thermal power plants) at the time of system peak demand. In effect, the purpose of evaluating generators from the perspective of their “accredited capacity” rather than installed capacity is to assess how reliably those generators can meet peak needs.

Table 1. Description of Firm Capacity Contribution Assumptions in Figure 4

Resource “Firm” Capacity Contribution Assumption

Demand Response (DR)

About 200 MW of DR is necessary to shift nighttime load such

that the peak is now during the day. Less would be necessary if

DR also “shaved” the peak.

Solar7

If total solar installed capacity remains below 20 percent of

thermal generation capacity then solar’s firm capacity

contribution is 50 percent, otherwise it is 7 percent.

Wind

Wind’s firm capacity contribution is 8 percent of installed

capacity.

Landfill Gas

Landfill gas’ firm capacity contribution is 90 percent of installed

capacity.

Hydro

Hydro’s firm capacity contribution is 90 percent of installed

capacity.

Gas Turbines

Rather than contributing no firm capacity, their outage rate is

assumed to be 50 percent so 50 percent of installed capacity is

considered “firm.”

Cambalache Turbines

Rather than contributing no firm capacity, their capacity

contribution is consistent with the Mayaguez units at 79

percent.

All Other Resources

Consistent with PREPA assumptions.

Under the assumptions outlined in Table 1, PREPA does not need to add as much new thermal

generating capacity as it claims. In fact, with the assumptions in Table 1, the generation

capacity buildout envisioned in PREPA’s preferred scenario, P3MF1M, will result in significantly

overbuilding the generation system.

7 The accredited capacity value of solar is assumed to decrease at high penetration levels, though there is no consensus as to

what constitutes a “high” level. Based on work by the Lawrence Berkeley National Lab and current accredited values in the Midcontinent Independent System Operator (MISO), we picked the values in Table 1.

Figure 4. By Leveraging Existing Resources and Adding in Demand Response, PREPA would

Need Far Fewer New Resources to Meet its Peak Needs.8

As Figure 4 demonstrates, accounting for the ability of existing resources to meet peak needs

implies that PREPA’s preferred plan will result in far more capacity than is necessary. PREPA

could greatly reduce the level of thermal generation necessary to meet the peak. If fewer

thermal generators are built or repowered, then less capital investment is also needed. Figure 4

has some conservatism built into it in that it does not account for all 2,100 MW of potential

renewables, since those renewables are also not part of PREPA’s modeling.9 And it does not

account for the possibility that energy efficiency could also shift peak needs to the daytime or

that demand response could shave as well as shift the peak from the nighttime.

8 The PREPA estimate of firm capacity was developed using a spreadsheet provided in response to the Commission’s 3rd Requirement of Information with modifications for the changes in timing and capacity envisioned under the P3MF1M plan. This was done since the yearly firm capacity estimates were not provided by PREPA in its Supplemental IRP. 9 See Supplemental IRP at 5-5.

0

1000

2000

3000

4000

5000

6000

Cap

ac

ity (

MW

)

Realistic Estimate of Firm Capacity

PREPA Estimate of Firm Capacity

Capacity Needed to Meet Reserve Margin

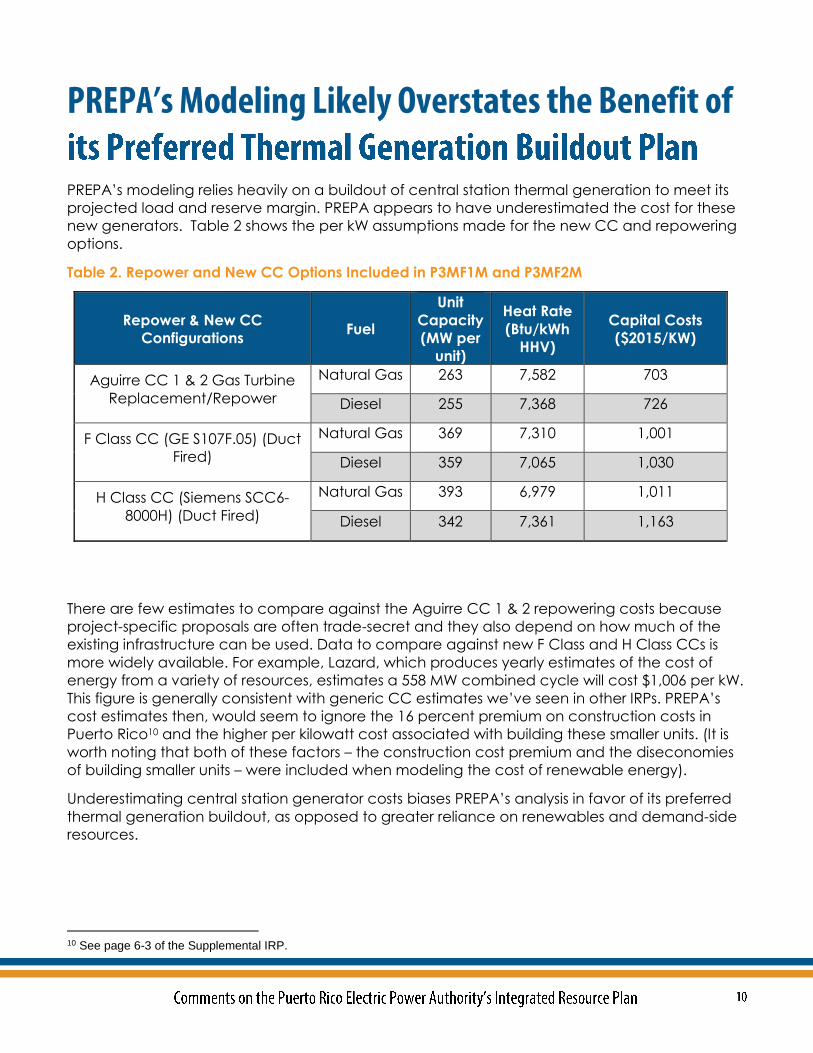

PREPA’s modeling relies heavily on a buildout of central station thermal generation to meet its

projected load and reserve margin. PREPA appears to have underestimated the cost for these

new generators. Table 2 shows the per kW assumptions made for the new CC and repowering

options.

Table 2. Repower and New CC Options Included in P3MF1M and P3MF2M

Repower & New CC

Configurations Fuel

Unit

Capacity

(MW per

unit)

Heat Rate

(Btu/kWh

HHV)

Capital Costs

($2015/KW)

Aguirre CC 1 & 2 Gas Turbine

Replacement/Repower

Natural Gas 263 7,582 703

Diesel 255 7,368 726

F Class CC (GE S107F.05) (Duct

Fired)

Natural Gas 369 7,310 1,001

Diesel 359 7,065 1,030

H Class CC (Siemens SCC6-

8000H) (Duct Fired)

Natural Gas 393 6,979 1,011

Diesel 342 7,361 1,163

There are few estimates to compare against the Aguirre CC 1 & 2 repowering costs because

project-specific proposals are often trade-secret and they also depend on how much of the

existing infrastructure can be used. Data to compare against new F Class and H Class CCs is

more widely available. For example, Lazard, which produces yearly estimates of the cost of

energy from a variety of resources, estimates a 558 MW combined cycle will cost $1,006 per kW.

This figure is generally consistent with generic CC estimates we’ve seen in other IRPs. PREPA’s

cost estimates then, would seem to ignore the 16 percent premium on construction costs in

Puerto Rico10 and the higher per kilowatt cost associated with building these smaller units. (It is

worth noting that both of these factors – the construction cost premium and the diseconomies

of building smaller units – were included when modeling the cost of renewable energy).

Underestimating central station generator costs biases PREPA’s analysis in favor of its preferred

thermal generation buildout, as opposed to greater reliance on renewables and demand-side

resources.

10 See page 6-3 of the Supplemental IRP.

PREPA’s modeling treats renewables as essentially an afterthought. The modeling runs that

have incorporated higher levels of renewables simply include those renewables on top of the

thermal generators, rather than as a substitute for them. In fact, PREPA claims that full RPS

compliance “requires [the] three new H class 1x1 CCs to be built on an accelerated schedule in

parallel”.11 PREPA ignores the possibility of using demand-side management strategies such as

demand response to incorporate those renewables or energy storage technology including

batteries. Despite this flaw, which tends to artificially increase the cost of higher levels of

renewables, PREPA’s run that includes the greatest amount of renewables (i.e. full compliance

with the RPS), P3MF1M_S5, is still only $251 million or 1 percent more expensive that PREPA’s

preferred scenario.

PREPA’s main argument against renewables is that additional renewable energy would result in

an unacceptable level of curtailment (because PREPA’s system peaks in the evening and,

according to PREPA, there must be enough thermal generation capacity to meet this evening

peak). PREPA does not consider any new additions of wind energy, even though wind is

available during evening hours. And as we just discussed, PREPA writes off demand response as

too expensive and serving no use except to limit curtailment.

PREPA also does not consider any additions of energy storage, even though energy storage will

be built in other, lower cost jurisdictions in mainland12 U.S. PREPA has provided no compelling

evidence demonstrating that the technology cannot be economically deployed in Puerto Rico

as well. In the one instance we are aware of in which PREPA examined battery storage costs,

they relied upon a 2008 paper despite the fact that battery prices have declined significantly in

the last eight years.13 It is worth noting that Kauai Island Utility Cooperative in Hawaii recently

signed a contract for a combined PV (17 MW DC) and battery (13 MW AC) system with a fixed

price of $145 per MWh.14

The technical conference revealed that all the renewables PREPA may be obligated to take

are not included in its modeling. It appears that 1,056 MW of renewables, listed in Table 5-6 of

the Supplemental IRP, are included, but a total of approximately 1600 MW is contracted and a

further 600 MW is governed by master agreements.15 While it is unfortunate, indeed, that these

contracts were signed for at above market prices,16 if they must be taken then they ought to be

included in the modeling so that the uncontracted-for resources can be developed around this

11 Page 2-2 of Supplemental IRP. 12 For example, SCE awarded contracts to 260 MW worth of energy storage projects in a 2014 solicitation for capacity

resources. See https://www.sce.com/wps/portal/home/procurement/solicitation/lcr/!ut/p/b1/hc_BCoJAEAbgZ-nQMXdsw7TbWouORFYG6V5CwzbB3DBLevss7BJlc5vh-4cZIkhIRBHfMhlXmSri_NkLY-fhjOnOaIi-rXNgAZoz7nIIfKMBUQPgRzH4l98S0UWmc6MFuukwFwNAGM8tQHu55tbGouaYtsBygLueD-hsVhSQrmARMEYB3hs6jvSIkLlKXg9HrEioKYko00NapqV2LZvxsarOl0kf-lDXtSaVknmq7dXpW-CoLhUJP9z5FEKGA5Hc694DHo9VOA!!/dl4/d5/L2dBISEvZ0FBIS9nQSEh/

13 See for example: Bellero, Lauren. “Moody’s: Batteries could soon become ‘economically viable’ for energy use.” 25

September 2015, SNL Financial, available at: https://www.snl.com/InteractiveX/article.aspx?ID=33984003&KPLT=4 14 Bandyk, Matthew. “Kauai battery project to deliver solar energy to co-op’s customers after sunset.” 30 March 2016, SNL

Financial. 15 According to page 5-5 of the Supplemental IRP, existing contracts, PPOAs and Master Agreements total 2,1601. MW of

renewable capacity. 16 It’s not clear why this might be the case, although we would note that these contracts do not seem to be the result of a

competitive Request for Proposals (RFP) process since one has not been conducted by PREPA since at least January 1, 2009 (see response to ELAC Request No. 10).

portfolio. It doesn’t make sense to pretend they don’t exist and develop a thermal generator

portfolio that ignores them. These additional renewables make it even more critical that more

creative methods for integrating renewables, apart from gas CCs, be seriously explored and

considered; otherwise curtailment charges across all portfolios will be underestimated.

If, on the other hand, PREPA has the opportunity to renegotiate some of these renewables

contracts17, we see no reason why it should not be able to do so at much lower prices. Xcel

Energy in Minnesota, which has a demonstrably worse solar potential than Puerto Rico (see

Figure 5), believes that the all-in cost of solar in 2016 will be $67.30 per MWh.18 This price

accounts for both the renewable attributes of that solar (the RECs) and the federal investment

tax credit just as PREPA’s estimate of about $140 per MWh in 2016 would seem to.

Figure 5. Puerto Rico has a Much Better Solar Resource than much of Mainland U.S.19

Jurisdictions further south are seeing even lower per MWh costs. Over the summer of 2015,

Austin Energy reported receiving at least one bid to provide solar at a cost of less than $40 per

MWh.20 We attempted to get, but never received the calculations PREPA performed to

determine the levelized cost of solar, so cannot say why PREPA arrives at such a markedly

higher figure ($140/MWh). One reason seems to be the assumption that PREPA would have to

17 A review of the contracts indicates that PREPA has the option to terminate contracts which have not come online within a

certain timeframe. It appears that this deadline has passed or is upcoming within the next year for many projects. With regard to 442MW of the 1,062MW of renewables included in Table 4-2 of Volume 1 of the August 2015 IRP, PREPA notes that there is “significant uncertainty about the actual future of these projects in their current contractual form.”

18 Xcel 2015 IRP Supplement filed January 29, 2016. 19 From AWS Truepower: https://go.pardot.com/l/71132/2015-06-

29/c5bfm?kc_referrer=https://www.awstruepower.com&kc_file=http://ww2.awstruepower.com/SOLAR-Resource-Map-North-America

20 Trabish, Herman K. “Austin Energy gets record low solar bids at under 4 cents per kWh.” 2 July 2015. Utility Dive. Available at: http://www.utilitydive.com/news/austin-energy-gets-record-low-solar-bids-at-under-4-centskwh/401642/

pay an additional $30 per MWh in order to also receive the renewable attributes of the solar.

Perhaps if it purchased RECs alone rather than in combination with energy, this might be the

case, but an additional charge at that level ($30 per MWh) is not consistent with the experience

of other U.S. utilities of which we are aware. We know many, perhaps all, of PREPA’s recently

executed renewables contracts include a provision to pay for RECs at a cost of $30 per MWh,

but again, this is not typical for utility-scale renewables contracts executed with other utilities of

which we are aware.

It is also possible that PREPA’s capital cost figures for solar are already out of date. While the

NREL report PREPA references was published in September 2015, the prices are linked to systems

installed in the first quarter of 2015 that presumably would have locked in equipment prices in

2014 or even earlier.

Renewables have the added benefit of having no fuel price volatility risk. Whether PREPA

continues to burn large quantities of natural or diesel fuel, it cannot guarantee that its

customers would not have to bear further rate increases due to higher fuel costs. Because

renewables are “fuel-free” this risk is entirely removed.

In summary, a build-out strategy centered around renewables provides an enormous risk

reduction benefit to PREPA and its ratepayers. There is great uncertainty around Puerto Rico’s

economic future and its population and thus great uncertainty in PREPA’s load forecast. Once

PREPA’s thermal fleet is built, those costs will have to be borne by customers regardless of

whether population continues to decline. The fewer customers, the higher the charge that will

be assessed on its remaining customers. While the same would be true of any renewables that

are built, their smaller MW size compared to the proposed thermal fleet greatly reduces the

resulting rate shock compared to a thermal generator. Additionally, the smaller size of

renewable units means that there is more flexibility in building out the generation system in an

incremental manner, and fewer renewables can be built if load does not materialize as

forecast.

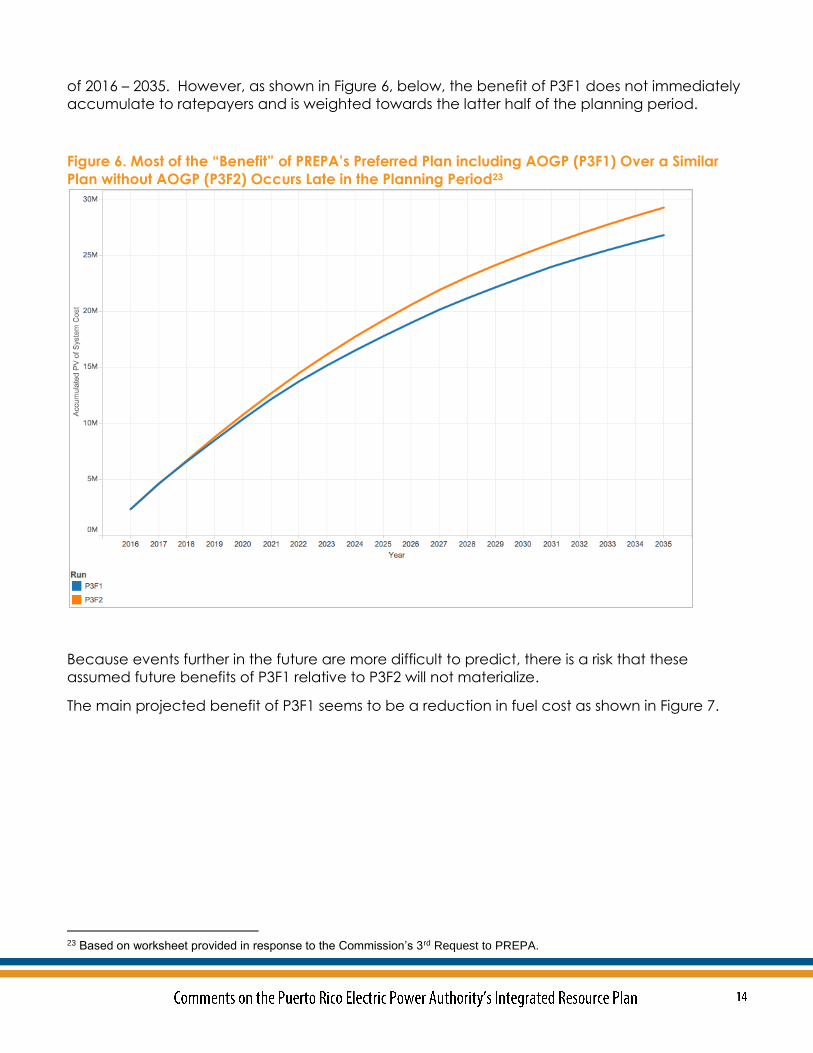

As discussed previously, most of PREPA’s modeling for its August 2015 IRP is focused on different

combinations of central station generators. The Company’s preferred plan in the August 2015

IRP is known as “P3F1” and includes construction of the Aguirre Offshore Gas Port (AOGP) by

mid-2017, allowing a transition of much of PREPA’s fleet to natural gas. A similar, but alternative

plan, “P3F2” does not include AOGP.21 Generally, the generator replacement and repowering

options included in this plan rely on light diesel as the fuel source. In its August 2015 modeling,

PREPA estimated the present value of total system cost22 of P3F1 at $26.842 billion and P3F2 at

$29.301 billion, a difference of 9 percent. These totals are calculated over a “planning period”

21 PREPA presented modified versions of these plans, P3MF1M and P3MF2M in its Supplemental IRP, but we did not have

access to the annual cost data for these plans to perform a similar analysis though we would expect similar magnitudes of differences, if not the same absolute difference between plans.

22 Present value is a measure of cost that takes into account the “time value of money.” Future expenditures are discounted in PREPA’s model by its chosen “discount rate” – 6.86%.

of 2016 – 2035. However, as shown in Figure 6, below, the benefit of P3F1 does not immediately

accumulate to ratepayers and is weighted towards the latter half of the planning period.

Figure 6. Most of the “Benefit” of PREPA’s Preferred Plan including AOGP (P3F1) Over a Similar

Plan without AOGP (P3F2) Occurs Late in the Planning Period23

Because events further in the future are more difficult to predict, there is a risk that these

assumed future benefits of P3F1 relative to P3F2 will not materialize.

The main projected benefit of P3F1 seems to be a reduction in fuel cost as shown in Figure 7.

23 Based on worksheet provided in response to the Commission’s 3rd Request to PREPA.

There is a small difference in

“amortized capital costs” (defined

as the PV of capital expenditures

made on fossil-fuel facilities during

the planning period), a slightly larger

difference in regasification fixed

costs due to the cost of AOGP in

P3F1, but most of the difference has

to do with fuel costs.,

In response to a Commission

discovery request, PREPA admitted

that “[d]ue to the downturn of the

oil and other fuel prices in the

second half of year 2015” it had

“requested Siemens Industry, Inc. to

prepare a fuel price forecast for a

“Low Oil Price” scenario.”24 When

PREPA reran its model with these

lower fuel costs, the cost advantage

of AOGP essentially disappears. The

cost differential between P3F1 and

P3F2 under a lower fuel price

scenario was less than 1% over

twenty years. Similarly, the cost

differential between P3MF1M and

P3MF2M (which contain higher levels

of energy efficiency, slightly less

thermal capacity, and different

online years for certain resources)

was also less than 1% over twenty

years.

These modeling results show that the

cost advantage of AOGP is highly

sensitive to future fuel prices. The

benefit of AOGP is thus as volatile as

oil and natural gas prices, which in

turn places significant risk on

ratepayers that no cost benefit will

be realized under PREPA’s preferred

plan.

24 Puerto Rico Energy Commission Fourth Requirement of Information, Request No. 1.

Figure 7. Present Value Cost of P3F1 and P3F2

by Cost Category

During the technical conference held on April 6, 2016, PREPA seemed to express a belief that

AOGP was cost-effective for ratepayers regardless of what the future might hold. This is at odds

with the fact that its own modeling identified a specific, not infinite, cost differential between

portfolios with and without AOGP and ignores the uncertainty of that benefit due to fuel price

uncertainty.

PREPA’s attitude that AOGP will be cost-effective no matter what the cost suggests that PREPA

will fall victim to many of the problems that cause large infrastructure projects to be overtime

and over budget. As described by Flyberg et al in a 2009 paper, large infrastructure projects

often start late, come in over budget, and perform below expectations:25

There are some phenomena that have no cultural bounds such as maternal love and a

healthy fear of large predators. We can add to this list the fact that, across the globe,

large infrastructure projects almost invariably arrive late, over-budget, and fail to perform

up to expectations. Cost overruns and benefit shortfalls of 50 percent are common; cost

overruns above 100 percent are not uncommon. For example, in one study of major

projects in 20 countries, nine out of ten projects had cost overruns. Similarly, a study of 44

urban rail projects—in North America, Europe, and developing nations, including

London’s Tube and the metros in Washington, D.C., and Mexico City—found that the

average construction cost overrun in constant prices was 45 percent; for a quarter of the

projects, cost overruns were at least 60 percent. In addition, passenger ridership was, on

average, 50 percent lower than forecast. Furthermore, for a quarter of the projects,

ridership was at least 70 percent lower than estimated. An appropriate slogan seems to

be “over budget, over time, over and over again.” As comforting as it is to know that we

are not alone in our folly, it would be even better to minimize the gap between

expectations and performance for projects that consume such a large share of the

private and, especially, public purse.

Executives typically attribute project underperformance to numerous uncertainties such

as project complexity, technological uncertainty, demand uncertainty, lack of scope

clarity, unexpected geological features, and negative plurality (i.e., opposing

stakeholder voices). No doubt, all of these factors at one time or another contribute to

cost overruns, benefit shortfalls, and time delays. The goal of this article, however, is not

to explain, for example, how to implement complex projects more efficiently by over-

coming these uncertainties. Rather, we explain why costs, benefits, and time forecasts for

more complex projects are systematically over-optimistic in the planning phase in

comparison to less-complex projects. In other words, “why do project planners, on

average, fail to anticipate the greater costs of complex projects or those based on new

technologies?”

The underlying reasons for all forecasting errors can usefully be grouped into three

categories: delusions or honest mistakes; deceptions or strategic manipulation of

information or processes; or bad luck. Bad luck or the unfortunate resolution of one of the

major project uncertainties is the attribution typically given by management for a poor

25 Flyvbjerg, Bent and Garbuio, Massimo and Lovallo, Dan, Delusion and Deception in Large Infrastructure Projects: Two

Models for Explaining and Preventing Executive Disaster (February 2009). California Management Review, vol. 51, no. 2, pp. 170-193. Available at SSRN: http://ssrn.com/abstract=2229781

outcome. While not denying such a salient explanation, this article explores the

underlying psychological and governance reasons for mis-estimation rather than

proximate engineering causes.

Deliberately or not, risks of scope changes, high complexity, and unexpected geological

features are systematically underestimated during project preparation. Both delusion

and deception see the high failure rates for ventures as a consequence of flawed

decision making. According to the first explanation—delusion—the flaw consists in

executives falling victim to what psychologists call the planning fallacy. In its grip,

managers make decisions based on delusional optimism rather than on a rational

weighting of gains, losses, and probabilities. They overestimate benefits and

underestimate costs and time. They involuntarily spin scenarios of success and overlook

the potential for mistakes and miscalculations. As a result, managers pursue initiatives

that are unlikely to come in on budget or on time, or to ever deliver the expected

returns. These biases are often the result of the inside view in forecasting: decision makers

have a strong tendency to consider problems as unique and thus focus on the

particulars of the case at hand when generating solutions. Adopting an outside view of

the problem has been shown to mitigate delusion. It is applied by ignoring the specific

details of the project at hand and uses a broad reference class of similar projects to

forecast outcomes for the current project.

According to the second explanation—deception—decision making is flawed by

strategic misrepresentation or the presence of what economists refer to as principal-

agent problems. Whereas the first explanation is psychological, the second is due to the

different preferences and incentives of the actors in the system. In this situation,

politicians, planners, or project champions deliberately and strategically overestimate

benefits and underestimate costs in order to increase the likelihood that their projects,

and not their competition’s, gain approval and funding. These actors purposely spin

scenarios of success and gloss over the potential for failure. This results in managers

promoting ventures that are unlikely to come in on budget or on time, or to deliver the

promised benefits. However, this misrepresentation and failure can be moderated by

measures that enhance transparency, provide accountability, and align incentives.

[More specifically], those measures are: private financiers should participate, without a

sovereign guarantee, for at least one third of the total capital needs; financial and non-

financial rewards for planners who proposed realistic estimates; strict forecasts audit;

criminal penalties for purposely misleading forecasts; place financial responsibility with

bidders [i.e. the EPC contractor for Aguirre]; and place financial responsibility with

contractors for delays and scope increases.

PREPA performed no sensitivity analysis in which AOGP came online at a later date and/or with

a higher cost. This despite the fact that it only has 14 months in which to construct and bring

online the project in order to meet its July 2017 date – which is itself another delay from the mid-

2014 in-service date projected in 2013.26 And in 2014, PREPA estimated AOGP would have $66

million in fixed operating expenses. It now says the cost will be $77 million a year.

The $385 million capital cost estimate is exclusive of financing costs, other than those incurred

during construction, which also poses risk in that it is not clear at what terms AOGP could be

26 See http://www.platts.com/im.platts.content/productsservices/conferenceandevents/2013/pc302/presentations/mike_trammel.pdf

financed. PREPA’s discount rate, equal to its weighted average cost of capital, is assumed to

be 6.86 percent and is based on the assumption that “PREPA is able to resolve its current

financial issues, and can borrow the capital required to finance cost-effective capacity at 9

percent nominal rate.” A December 2015 agreement with Assured Guaranty is presumably the

mechanism by which “PREPA is able to resolve its current financial issues” and borrow capital at

reasonable rates, meaning that the assumed 6.86 percent rate is also in limbo. Part of the

agreement required PREPA to file a petition to create a customer fee that would help repay

PREPA’s debt, and approval of that petition is pending before the Commission.

PREPA’s preferred generation portfolio imposes significant risks on PREPA ratepayers:

The risk to ratepayers of paying for stranded, underutilized generation capacity. The

combination of PREPA’s optimistic load forecast and PREPA’s unnecessarily high reserve

margin mean that the generation system will almost certainly be overbuilt under PREPA’s

preferred plan.

The risk that the cost savings from switching to natural gas will not justify the high capital

costs of the AOGP project.

The risk that the AOGP project will be delayed and come in significantly over budget.

By failing to treat renewable energy, energy efficiency and demand response on a consistent

and integrated basis with conventional generation, both in terms of modeling and in terms of

capital cost assumptions, PREPA has underestimated the benefits to ratepayers of greater

reliance on renewable and demand-side resources. Specifically, PREPA’s IRP does not consider:

The enhanced flexibility of relying on these resources in a situation of highly uncertain

future load.

The reduced volatility of fossil fuel prices to be passed through to ratepayers and

reduced risk of rate shock.

The economic development benefits for the island of greatly reducing the at least half a

billion dollars a year that would be spent outside the island to pay for imported fuel.

We recommend that the Commission reject PREPA’s IRP and ask it to initiate a stakeholder

based process27 that would develop a vision and a plan for electricity supply in the

Commonwealth that is more robust, flexible, sensitive to rates, and less risky.

27 The Department of Energy’s Energy Transition Initiative provides one possible framework, the Islands Playbook, under which

such a plan could be developed. See http://www.eere.energy.gov/islandsplaybook/ for more detail. The framework has been used successfully on other Caribbean islands such as the U.S. Virgin Islands.

The Institute for Energy Economics and Financial Analysis (IEEFA) conducts research and

analyses on financial and economic issues related to energy and the environment. The

Institute’s mission is to accelerate the transition to a diverse, sustainable and profitable energy

economy and to reduce dependence on coal and other non-renewable energy resources.

More can be found at www.ieefa.org.

. For over ten years, she has provided

technical assistance and expert witness testimony to clients working on a variety of electric

utility issues. Her recent work has focused on utility resource planning, power plant in-service

requirements, and energy efficiency planning.

Ms. Sommer holds a BS in Economics and Environmental Studies from Tufts University and an MS

in Energy and Resources from UC Berkeley.

is an independent West Virginia-based consultant focusing on

energy efficiency and utility regulation. She has testified on multiple occasions before the West

Virginia Public Service Commission for the nonprofit coalition Energy Efficient West Virginia. She

has done graduate work for the Energy and Resources Group at the University of California-

Berkeley and is a former senior research associate at Lawrence Berkeley National Laboratory.

Kunkel has an undergraduate degree in physics from Princeton University and graduate degree

in physics from Cambridge University.