presentación de powerpoint - isa€¦ · transversal del sisga – usd 482 ... management of...

TRANSCRIPT

Investor Presentation

9th Annual Andean Conference 2015

Santiago de Chile. March 17-19, 2015

Disclaimer

Certain statements contained in this report constitute "forward-looking statements" within the meaning of

the Private Securities Litigation Reform Act of 1995.

These forward-looking statements reflect our current views with respect to future events and are based

on assumptions and subject to risks and uncertainties. Also, these forward-looking statements present

our estimates and assumptions only as of the date of this report. Except for our ongoing obligation to

disclose material information as required by federal securities laws, we do not intend to update you

concerning any future revisions to any forward-looking statements to reflect events or circumstances

occurring after the date of this report.

Amounts expressed in US dollars are for information purposes only, and do not reflect

accounting conversion techniques usually applied.

2

AGENDA

3

Corporate Strategy ISA 2020

4

Aspirations and General Definitions

Ratification of countries and businesses

Higher Profitability

Growth based on profitability

ISA Vocation: Generate value from the operation

and excellency in infrastructure development Vision 2020

By 2020, ISA will have tripled its profits, by capturing the most

profitable growth opportunities in its businesses existing in Latin

America, the boost of operational efficiency and the optimization of its

business portfolio.

For the long-term cycle, 2014 was

established as a key year to seize early

victories

Significant advancement of Strategic Plan: two years from its implementation

reached 2,2x

Growth with higher

profitability Current business

profitability Management of

business portfolio

~60% Success Rate

~470 USD million

Investment

3

12

17

32

Brazil 1, Chile 1, Colombia 11, Peru 4

MANAGED

BIDS

18

30

52

100

Probable¹ Identified² Required Total

Business 65%, Support 35%

OPEX SAVINGS

BY 2020

1 Eventual savings: Achieved in Opex and with contract in CAPEX 2 Identified savings: With strategic project under execution

Methodology developed and applied

to investment portfolio.

Internexa scale increase in operations.

159 USD million

Savings (with agreements) in

CAPEX

1 2 3

5

Corporate Strategy ISA 2020

AGENDA

6

Proposition 2015

Ordinary $ 208

Extraordinary $ 60

Total $ 268

Shareholders Structure and Dividend Policy

The Colombian State is the controller

…31.44% is the free float

160 172 179 188 214

0

50

100

150

200

250

2010 2011 2012 2013 2014

Dividend

December, 2014 SHARES %

STATE INVESTORS 682.078.108 61,58%

THE COLOMBIAN STATE 569.472.561 51,41%

EMPRESAS PÚBLICAS DE MEDELLÍN 112.605.547 10,17%

COMPANIES WITH PUBLIC AND PRIVATE CAPITAL 77.373.530 6,99%

ECOPETROL 58.925.480 5,32%

EMPRESA DE ENERGÍA DE BOGOTA 18.448.050 1,67%

PRIVATE INVESTORS 348.226.256 31,44%

INSTITUTIONAL INVESTORS 202.887.650 18,32%

INDIVIDUALS 66.712.392 6,02%

LEGAL PERSONS 16.645.184 1,50%

FOREIGN INVESTORS 60.971.105 5,50%

ISA ADR PROGRAM 1.009.925 0,09%

SUBSCRIBED AND PAID CAPITAL INTO

CIRCULATION 1.107.677.894 100,00%

7

ISA’s Board of Directors

Principal members Alternative members

Ministry of Mines and Energy: Minister Ministry of Mines and Energy: Vice-Minister

Ministry of Finance and Public Credit: Ministry of Finance and Public Credit:

General Vice-Minister Director General of Public Credit and National

Treasury

Carlos Mario Giraldo Moreno* Henry Medina González*

EPM: General Manager Jesús Aristizábal Guevara*

Santiago Montenegro Trujillo* Camilo Zea Gómez*

Alejandro Linares Cantillo

Bernardo Vargas Gibsone* Carlos Felipe Londoño Álvarez*

*Independent members

President: Mr. Santiago Montenegro Trujillo

Secretary: Sonia Margarita Abuchar Alemán, ISA's Secretary General.

8

AGENDA

9

ISA in Latin America is focused on four

businesses…

ISA, directly and through its 33 affiliates and subsidiaries, is currently implementing

important infrastructure projects that boost the continent's progress and contribute to

the development of the inhabitants of Colombia, Brazil, Peru, Chile, Bolivia, Ecuador,

Argentina, Panama, and Central America.

10

2010 2011 2012 2013 2014

Energy Transportation 90% 80% 80% 68% 70%

Toll road concessions 5% 16% 17% 26% 21%

Telecommunications Transport 3% 2% 3% 4% 6%

Smart Management of Real

Time Systems 2% 2% 2% 2% 3%

Energy Transportation

• 19 companies in Colombia, Peru, Central America, Bolivia,

Brazil and Chile.

• 41.650 km circuits of transmission lines in operation (40,630

km in 2013), 8.071 km circuits under development (includes

Chile’s projects).

• Transformation capacity: 77.710 MVA (75.960 MVA in 2013).

• Majority participation in Colombia and Peru, greater

transmission operator in the state of Sao Paulo in Brazil, and

an important participation in Bolivia.

• Network availability in 2014: ISA 99,86%, TRANSELCA

99,91%, REP 99,60%, Transmantaro 99,52%, ISA Peru

99,90%, ISA Bolivia 99,64% and CTEEP 99,95%.

Strategy

OPEX and CAPEX efficiencies

Evaluate investment opportunities and invest in

those that are relevant for ISA.

MAP: March 2014

11

Energy Transportation

12

New Projects 2014 Estimated investment: USD 1.100 million

Colombia, UPME projects: Caracolí substation. Caracolí – Las Flores (22 km) and Caracolí – Sabana (31 km) lines. (1 USD 7,54)

Montería substation, Chinú substation expansion. Montería - Chinú (71 km) and Montería - Urabá (124 km) lines. (1 USD 9,00)

Reforma to Guavio – Tunal circuit conection. (1 USD 0,50)

Peru, Proinversión projects: Planicie – Industriales (11,7 km) line and associated substations. (1 USD 5,50)

Friaspata – Mollepata (90 km) line and associated substations. Orcotuna substation and Huayucachi - Carabayllo connection.

(1 USD 5,70)

ISA Perú expansion 3

Chile: Installation of autotransformers banks at Cardones, Maitland and Sugarloaf substations and second circuit at Encounter –

Lagunas line. (1 USD 2,60)

1.3

30

1.4

64

1.4

01

1.0

23

1.1

43

98

7

1.0

73

1.0

01

53

6

65

3

86

0

59

5

45

0

44

7

42

6

7.082 7.441 7.229 6.671

7.531

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

0

500

1.000

1.500

2.000

2010 2011 2012 2013 2014

revenues EBITDA investments assets

Business evolution

74,2% 73,3% 71,4% 52,4% 57,1%

2010 2011 2012 2013 2014

EBITDA Margin

1 Estimated revenues in million

USD million. Exchange rate: COP 2.392,46

Energy Transportation

13

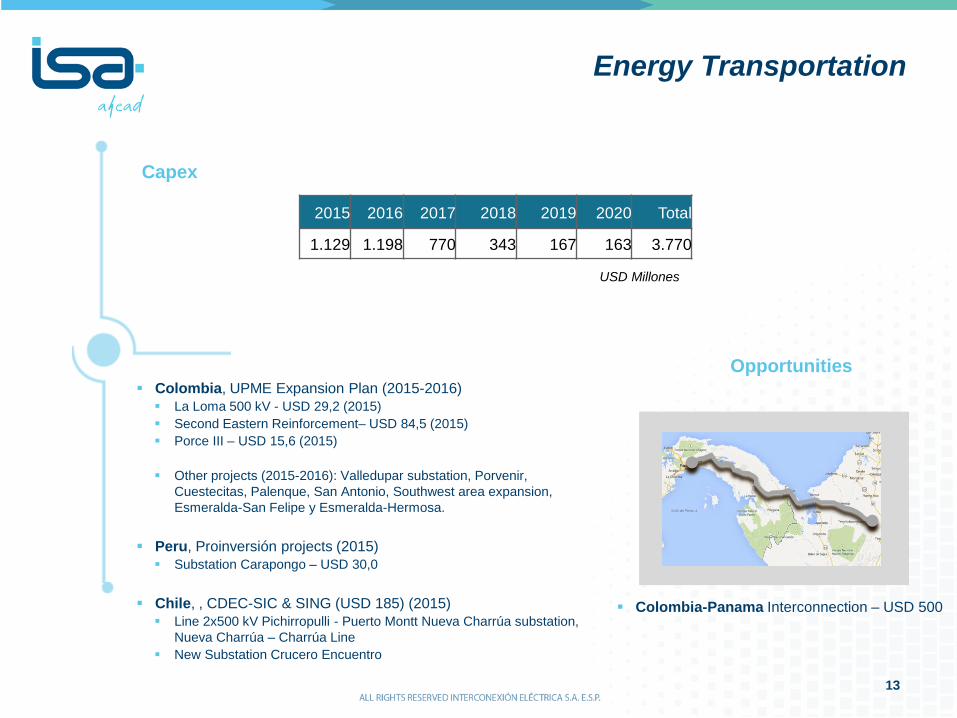

Colombia, UPME Expansion Plan (2015-2016)

La Loma 500 kV - USD 29,2 (2015)

Second Eastern Reinforcement– USD 84,5 (2015)

Porce III – USD 15,6 (2015)

Other projects (2015-2016): Valledupar substation, Porvenir,

Cuestecitas, Palenque, San Antonio, Southwest area expansion,

Esmeralda-San Felipe y Esmeralda-Hermosa.

Peru, Proinversión projects (2015)

Substation Carapongo – USD 30,0

Chile, , CDEC-SIC & SING (USD 185) (2015)

Line 2x500 kV Pichirropulli - Puerto Montt Nueva Charrúa substation,

Nueva Charrúa – Charrúa Line

New Substation Crucero Encuentro

Opportunities

Capex

2015 2016 2017 2018 2019 2020 Total

1.129 1.198 770 343 167 163 3.770

USD Millones

Colombia-Panama Interconnection – USD 500

Toll road concessions

• Largest toll road concession operator in Chile.

• 907 km of toll road infrastructure in operation.

• Used by over 100 million vehicles in 2014. (99 million in

2013)

• 95 toll plazas.

• 293 bridges, 368 structures (overpasses, connections,

among others), 188 pedestrian walkways.

• Design speed is 120 km/hour.

• Award for road safety in all concessions during 2014, which

implies higher revenues.

Enter the toll road concession operation in

Colombia.

Develop service and security works in existing

roads.

Strategy

14

MAP: March 2014

Opportunities

Capex

USD Millones

Toll road concessions

Colombia, ANI Projects – 4G bids. Concessions

where ISA is prequalified (figures in million) (2015-

2016)

Girardot Neiva 191 km - USD 648

Cruz del Viso-Carreto-Palmar de Varela

204 km– USD 644

Popayán-Santander de Quilichao 76 km -

USD 884

Other concessions: (2015-2016)

Villavicencio-Yopal – USD 1.525

Rumichaca-Pasto – USD 1.104

Transversal del Sisga – USD 482

Chile, third runways in Maipo, pedestrian

connections in Maule and Bosque (USD 200

million) and Third runaways in Maipo (USD 200

million) (2015).

15

2015 2016 2017 2018 2019 2020 Total

44 22 66

Business evolution

69

29

1

31

3

38

4

35

2

51

17

3

19

6

29

1

25

9

25

17

6

13

18

22

3.477 3.440 3.295 3.634

4.150

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

0

100

200

300

400

500

2010 2011 2012 2013 2014

revenues EBITDA investments assets

73,9% 59,4% 62,8%

75,9% 73,5%

2010 2011 2012 2013 2014

EBITDA Margin

USD million. Exchange rate: COP 2.392,46. 2010: 3 months

Telecommunication Infrastructure

• 26,717 km in operation, the largest open information

transportation network in South America. (2013:

25.465 km)

• Presence in Colombia, Ecuador, Peru, Chile,

Argentina and Brazil and connections with

Venezuela and Bolivia.

• 460 operators serviced, in local as well as national,

regional and international needs.

• 2.5 Tbps in capacity in the region, served from local

nodes and international connections via agreements

with the most important agents in the industry.

• 2014 average service availability 97,53% in the

region.

Strategy

Consolidate operations in Chile, Argentina and Brazil

and keep the position reached in Colombia, Ecuador y

Peru. MAP: March 2014

16

Capex

2015 2016 2017 2018 2019 2020 Total

64 38 13 20 18 15 169

Telecommunication Infrastructure

Deepen into the leadership achieved in the

distribution of Internet traffic in the region.

Increase regional traffic and fidelity of operators

on INTERNEXA's network.

USD Millones

Opportunities

Business evolution

37

41

48

62

97

14

15

11

11

31

20

23

25

36

43

125 156 155

274 307

0

50

100

150

200

250

300

350

0

20

40

60

80

100

120

2010 2011 2012 2013 2014

revenues EBITDA investments assets

12.029

19.912 22.730 25.465 26.717

0

10.000

20.000

30.000

2010 2011 2012 2013 2014

37,5% 37,8%

22,8% 17,6% 31,5%

2010 2011 2012 2013 2014

EBITDA Margin

Fiber optic km

USD million. Exchange rate: COP 2.392,46

17

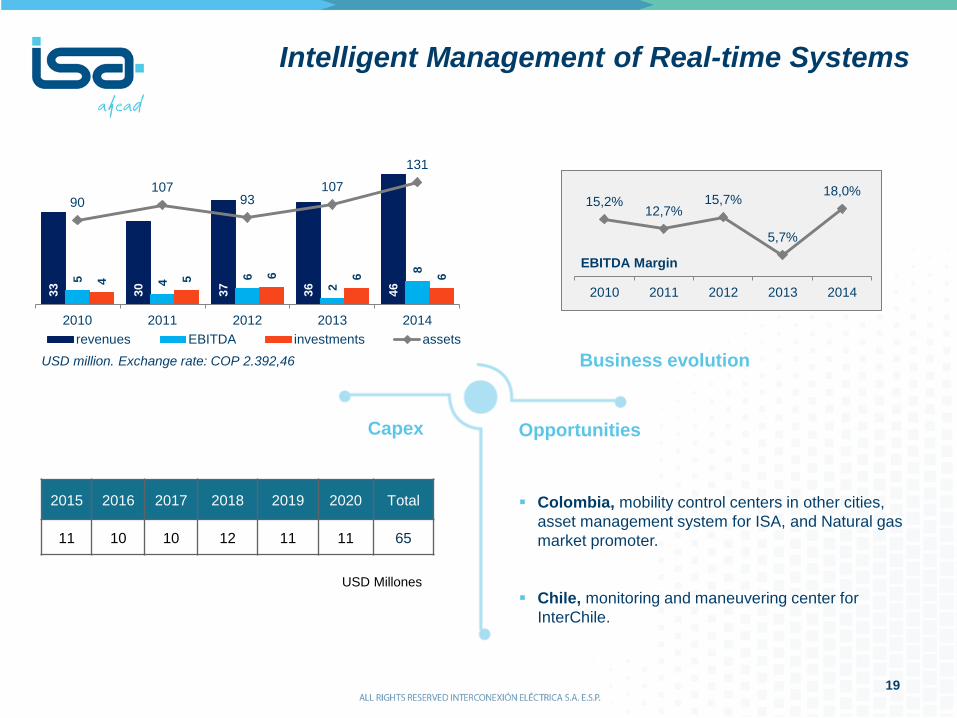

Intelligent Management of Real-time Systems

REAL TIME SYSTEMS

Planning, coordination and supervision of the SIN operation in

Colombia. 24.912 km in lines, 38.646 MVA of transformation, 15.489

MW in installed capacity.

Planning and operation of the mobility control center of affiliates in

Medellin, Colombia.

Support and maintenance service in control centers in Colombia and

Peru.

Projects under construction: Control Center for toll road information

Antioquia, Colombian.

MARKET MANAGEMENT

Management of comercial exchange programs of the wholesale energy market (Colombia). Payment,

management of accounts and billing 49.5% of property in DERIVEX – negotiations system and registering of

operations of financial energy products in Colombia.

7.18% of property in CRCC – Central risk agency of the counterparty – compensation service as central

operations counterparty

Strategy

Expand services to other sectors and strengthen synergistic services within Grupo ISA.

18

Opportunities Capex

2015 2016 2017 2018 2019 2020 Total

11 10 10 12 11 11 65

Intelligent Management of Real-time Systems

Colombia, mobility control centers in other cities,

asset management system for ISA, and Natural gas

market promoter.

Chile, monitoring and maneuvering center for

InterChile.

USD Millones

Business evolution

33

30

37

36

46

5

4 6

2

8

4 5 6

6

6

90 107

93 107

131

0

50

100

150

0

10

20

30

40

50

2010 2011 2012 2013 2014

revenues EBITDA investments assets

15,2% 12,7%

15,7%

5,7%

18,0%

2010 2011 2012 2013 2014

EBITDA Margin

USD million. Exchange rate: COP 2.392,46

19

AGENDA

20

2010 2011 2012 2013 2014

Revenues

EBITDA

Consolidated Income Statement

AOM

USD million. Exchange rate: COP 2.392,46

1.469 1.826 1.799

1.505 1.639

2010 2011 2012 2013 2014

561 585 664 688

2010 2011 2012 2013 2014

1.056 1.265 1.213

841 951

413

21

2010 2011 2012 2013 2014

Net

Income

Consolidated Income Statement

Margins

144 141 114

181

248

USD million. Exchange rate: COP 2.392,46

53% 50% 47%

43% 48%

72% 69% 68%

56% 58%

10% 8% 6% 12% 15%

2010 2011 2012 2013 2014

Operating EBITDA Net

22

3.114 3.638

1.549 1.774

6.024

6.707

2013 2014

Equity Minority interest Liabilities

Consolidated Balance Sheet

Assets by Country

Assets by Business

Asse

ts

Assets in December 2014 totaled USD 12.119 million, -

13,4% increase compared to 2013

Assets 10.687 12.119

USD million. Exchange rate: COP 2.392,46

13,4%

11,4%

16,8%

14,5%

Energy 62,1%

Roads 34,2%

Telecommunications

2,5%

SMRTS 1,1%

COLOMBIA 28,1%

CHILE 34,4%

BRAZIL 23,9%

PERU 13,1%

OTHERS 0,5%

23

BRL 11,3%

COP 17,6%

USD 23,7%

UF + CLP 47,4%

Others 0,1%

Consolidated Financial Debt

USD million. Exchange rate: COP 2.392,46

millions 2013 2014 Change

%

2014

USD

CHILE 4.217.278 4.482.666 6,3% 1.874

COLOMBIA 1.788.574 1.784.963 -0,2% 746

BRAZIL 1.169.464 1.164.658 -0,4% 487

PERU 1.464.947 1.934.281 32,0% 808

BOLIVIA 51.134 51.947 1,6% 22

ARGENTINA 7.071 6.994 -1,1% 3

TOTAL 8.698.468 9.425.510 8,4% 3.940

Breakdown by Rate Breakdown by Source Breakdown by Currency

4,1 4,5

4,7 4,7 4,5 4,3 4,2

4,5

3,2 3,4 3,4 3,1

3,6 3,7

4,2 4,4

1Q13 2Q13 3Q13 2013 1Q14 2Q14 3Q14 4Q14

Debt / EBITDA EBITDA / Interest

Fixed 19,9%

CDI 5,4%

ICP 13,5%

TJLP 3,9%

TAB 6,8%

Libor 5,2%

DTF 4,1%

UF 40,6%

Other 0,6%

Capital Market 73,1%

Banks 26,1%

Other 0,8%

24

ISA's ratings reflect the strong financial profile of

the company, with stable and predictable cash

flows.

25

Rating for bonds issued

AAA(col)

International Corporate Ratings

BBB

Stable outlook

May 2014

International Corporate Ratings

Baa2

Stable outlook

August 2014

International Corporate Ratings

BBB

Stable outlook

August 2014

An investment of USD 4.070 million supports future

growth ...

Investment by country COP %

Colombia 4.249 42,8%

Peru 1.739 17,6%

Brazil 2.448 24,6%

Chile 1.442 14,6%

Others 29 0,3%

Investment by business COP %

Energy 9.176 92,6%

Toll Roads 159 1,6%

Telecommunications 412 4,2%

SMRTS 161 1,6%

COP billions

Projections February 2015

COP 9.908 billion

(USD 4.070 million)

Long-term investment plan ensures ongoing companies growth

2015 2016 2017 2018 2019 2020

Colombia Perú Brasil Chile Otros

3.075

1.939

927 488 475

3.004

26

Investor Relations

Contact

Email [email protected]

Website www.isa.co

Telephone +574 315 7470

@ISA_Avanza /ISAAvanza Interconexión

Eléctrica ISA /CanalISAAvanza

27

ANEXOS

Taxes

29

Colombia 34% + 5% CREE surcharge

Brazil 34%

Chile In the semi-integrated system 27% (as of 2018). From 2014 to 2017 will

rise progressively from 20% to 25,5%.

Bolivia 25%

Peru REP:27% ISA Perú: 22% CTM: 30% PDI: 30% (2015 and 2016: 28%;

2017 and 2018: 27%, and from 2019 hereinafter 26%) in REP, Peru and

CTM ISA rates will not change because they have stability agreement .

Nominal tax rate by country:

2014 breakdown by country and business

Colombia Brasil Perú Chile Otro Total

Energy Transportation 55% 18% 14% 0% 2% 88%

Toll road concessions 0% 0% 0% 9% 0% 9%

Telecommunications Transport 0% 0% 0% -1% 0% 1%

Smart Management of Real Time

Systems 2% 0% 0% 0% 0% 2%

57% 19% 14% 8% 2% 100%

consolidated

effective tax 29%

Compensation for unamortized and/or depreciated

assets existing as of May 2000 at CTEEP

30

08/13/14: A technical assessment report was submitted to ANEEL, which amounted to BRL 5.186 million (*).

01/08/15: CTEEP received the fiscalization report with an estimated compensation amount of BRL 3.605

million (*).

01/06/15: Reconsideration petition was filed to object the value informed in the fiscalization report.

To be done: Definition of the compensation value, monetary restatement, form and term of payment and tax

treatment.

March 2015 SFF will issue pronouncement with its final position

March 2015 CTEEP may file recourse before ANEEL’s Directorship

April 24, 2015 ANEEL’s Directorship approval of compensation value

(CTEEP will have an instance before the Directorship to defend its position)

June 2015 Definition by the Ministry of Mines and Energy –MME– of monetary restatement, term and form

of payment, eventually through tariff for final consumer payable as from July 2015

NEXT STEPS (estimated dates)

Tariff Revision in Colombia

31

2014: CREG issued official letters based on the consulting surveys that were published

regarding remuneration methodologies and Constructive Units, as well as the resolution

draft with the methodology proposal for rate calculation.

02/19/14: CREG published Resolution 178 introducing the resolution draft with the

methodology proposal for transmission remuneration.

What’s next: Review of project by ISA, in order to issue observations and comments (3

months) and issuance of the final resolution by CREG’s Regulatory Agenda (2Q15 –

estimated date).

Aspects under review:

Methodology to calculate remuneration of assets:

Value of Replacement to New Asset Depreciated

Optimized Replacement Cost (DORC)

Methodology to calculate AOM:

From VRN * 3.41% to an efficient methodology

Review of WACC parameters

Aspects not yet defined or not ruled:

Methodology to calculate seniority of assets.

Definition of AOM efficiency factor.

How are new investments for expansions and

replacements approved?

Compensation and energy not provided where CREG and

UPME have not approved reinforcements, investments or

replacements

It affects (related to 2014):

58% of the transmission

revenues in Colombia.

27% of the transmission

revenues

19% of the consolidated

revenues