presentatie lighthouse 2014 prestatiebelonen een …...2014/06/24 · - staatsblad 15 mei 2014...

TRANSCRIPT

25/06/2014

1

PRESTATIEBELONEN

= EEN PERFORMANT

LOONBELEID?

24 JUNI 2014

25/06/2014

2

AGENDA

Prestatiebelonen = Een performant loonbeleid?

� Inleiding

� Generieke Salarisstudie Hudson

� Evolutie 2014 – 2013

� Genderanalyse

� Strategisch belonen

� From pay to performance

� Resultaten onderzoek CAO 90

� Receptie

AGENDA

Prestatiebelonen = Een performant loonbeleid?

� Inleiding

� Generieke Salarisstudie Hudson

� Evolutie 2014 – 2013

� Genderanalyse

� Strategisch belonen

� From pay to performance

� Resultaten onderzoek CAO 90

� Receptie

25/06/2014

3

AGENDA

Prestatiebelonen = Een performant loonbeleid?

� Inleiding

� Generieke Salarisstudie Hudson

� Evolutie 2014 – 2013

� Genderanalyse

� Strategisch belonen

� From pay to performance

� Resultaten onderzoek CAO 90

� Receptie

6

GENERIEKE SALARISSTUDIE HUDSONMETHODOLOGIE

1. Voorbereidingvan de studie

2. Opstart van de studie

3. Data-inzameling& datacleaning

4. Dataverwerkinganalyse

5. Rapporteringresultaten

6. Feedback verzamelen over

de survey

25/06/2014

4

7

GENERIEKE SALARISSTUDIE HUDSONSTEEKPROEFSAMENSTELLING

21ste editie

541 bedrijven

112.207 observaties

199 referentiefuncties

23 diploma’s

8

GENERIEKE SALARISSTUDIE HUDSONSTEEKPROEFSAMENSTELLING

25%

13%

21%

16%

15%

10%

Aantal werknemers < 50 Werknemers 50 - 99 Werknemers

100 - 249 Werknemers 250 - 499 Werknemers

500 - 999 Werknemers > 1000 Werknemers

28%

18%

12%

23%

19%

Omzet

< 15 Miljoen € 15 - 49,99 Miljoen €

50 - 124,99 Miljoen € 125 - 249,99 Miljoen €

> 250 Miljoen €

25/06/2014

5

9

GENERIEKE SALARISSTUDIE HUDSONSTEEKPROEFSAMENSTELLING

24%

2%

32%9%

7%

7%

19%

Industrie (29%)

Chemie/Farmacie Textiel

Metaal Voeding

Bouw Elektriciteit/Elektronica

Overige Productie

47%

17%4%

4%

1%

27%

Diensten (66%)

Financiële Diensten ICT

Vervoer/Logistiek Advies en bijstand

Non-profit Overige Diensten

28%

72%

Handel (5%)

Groothandel

Retail

AGENDA

Prestatiebelonen = Een performant loonbeleid?

� Inleiding

� Generieke Salarisstudie Hudson

� Evolutie 2014 – 2013

� Genderanalyse

� Strategisch belonen

� From pay to performance

� Resultaten onderzoek CAO 90

� Receptie

25/06/2014

6

EVOLUTIE 2014 – 2013VOORAF

Loonorm:

- Om de twee jaar vastgelegd

- Bepaalt hoeveel de loonkosten mogen stijgen

- Met als doel de loonkostenontwikkeling in België preventief aan te passen aan de verwachte

evolutie bij onze voornaamste handelspartners Duitsland, Nederland en Frankrijk

- 2013 - 2014: de loonnorm is 0%

- Uitzonderingen: o.a. Index, bestaande loonschalen (barema’s), verhoging loonmassa door

toename VTE, CAO afspraken gericht op wegwerken loonkloof mannen/vrouwen, CAO 90

plannen, …

- Een werkgever die de loonnorm niet respecteert kan een boete opgelegd krijgen van 250 tot

5.000 euro

Periode

1997-

1998

1999-

2000

2001-

2002

2003-

2004

2005-

2006

2007-

2008

2009-

2010

2011-

2012

2013-

2014

Norm 6,10% 5,90% 6,4-7% 5,40% 4,50% 5,00% 250 euro 0,30% 0,00%

EVOLUTIE 2014 – 2013VOORAF

De loonkloofwet van 22 april 2012:

- Voor bedrijven met minstens 50 werknemers

- Analyse van de bezoldigingsstructuur van de vrouwelijke en mannelijke werknemers binnen de

onderneming

- Als hieruit een ongelijkheid tussen mannen en vrouwen zou blijken, moeten werkgever en vakbonden samen een actieplan opstellen om dit op te lossen

- Staatsblad 15 mei 2014 (koninklijk en ministerieel besluit): details en modellen van het analyseverslag dat moet worden opgemaakt

- 1ste verslag slaat op het boekjaar dat in 2014 wordt afgesloten

- Deze analyse zal tweejaarlijks moeten gebeuren

- Analyseverslag moet worden overgemaakt aan de ondernemingsraad (indien niet aanwezig

aan de vakbondsafgevaardigde)

- Bij ongelijkheid inzake verloning is het wenselijk om een actieplan op te stellen met als doel

een genderneutrale bezoldigingsstructuur

- Aanstellen van een bemiddelaar: onderdersteunt o.a. de opmaak van het actieplan en de voortgangsrapportage bij de bestrijding van de loonkloof

25/06/2014

7

EVOLUTIE 2014 – 2013BELONINGSBELEID

Top 3 doelstellingen - 2014:

1. Retentie van medewerkers

2. Streven naar marktconforme beloning

3. Loonkostenbeheersing

Top 3 wijzigingen - 2013 & 2014:

1. Variabel loon

2. Bedrijfswagenbeleid

3. Basissalaris

Ondanks de verwachtingen dat het

eenheidsstatuut een meer prominente rol zou

innemen in 2014, blijkt dit minder het geval te zijn

(20%)

Verhogingen van Basissalaris in

2014 (incl. automatische, merit en

collectieve verhogingen, excl.

indexatie, promotie, nieuwe

werknemers)

Poll november ‘13

EVOLUTIE 2014 – 2013METHODOLOGIE

Trends in beloning gebaseerd op een analyse van dezelfde personen in dezelfde functie in dezelfde organisatie

2. Identieke

organisatiesA B C X B Y DD

Organisatie D:

- ID 1

- ID 2

- ID 3

- ID 4

- ID 6

- ID 7

3. Identieke

personen

4. Identieke

functies

2013 20141. Dataset

- functie A

- functie B

- functie C

- functie D

Company D:

- ID 1

- ID 2

- ID 3

- ID 4

- ID 8

- ID 9

- functie A

- functie B

- functie X

- functie Y

25/06/2014

8

EVOLUTIE 2014 – 2013BASISLOON

De gemiddelde salarisstijging voor basissalaris in de Belgische markt

tussen februari 2013 en februari 2014 (exclusief promoties)

BASISSALARIS

Salarisstijging bovenop indexatie: + 1,0%

BASISSALARIS

+ 2,0 %

2013 2014

Indexatie: + 1,0 %

EVOLUTIE 2014 – 2013BASISLOON

4,0%

3,5%

3,8%4,0%

4,3%

5,9%

0,9%

3,7%

4,4%

3,3%

2,0%2,0% 1,9% 1,8% 1,7% 1,8%

4,4%

0,2%

2,2%

3,3%

2,4%

1,0%

2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012 2012-2013 2013-2014

Base Salary Indexatie

De gemiddelde salarisstijging voor basissalaris in de Belgische markt 2004 - 2014

25/06/2014

9

EVOLUTIE 2014 – 2013BASISLOON

Het cumulatief effect van indexatie en salarisstijgingen 2004 - 2014

4,0%

3,5%

3,8%

4,0%

4,3%

5,9%0,9%

3,7%

4,4%

3,3%

2,0%

2,0%1,9%

1,8%1,7%

1,8%

4,4% 0,2%2,2%

3,3%2,3%

1,0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Base Salary Indexatie

+ 25,0%

+ 47,7%

EVOLUTIE 2014 – 2013BASISLOON

Grootorde van salarisstijgingen (excl. Index)

� 2/3de had een salarisevolutie van < 2%

� Wijziging ten opzichte van vorig jaar: - minder mensen hadden een salary freeze- meer mensen hadden een verhogingtussen 0% en 2%

� Het aantal mensen met een stijging van > 2% is gelijkaardig aan vorig jaar

0% 0% - 2% 2% - 4% 4% - 6% 6% - 10% > 10%

2013-2014 / 2012 - 2013

25/06/2014

10

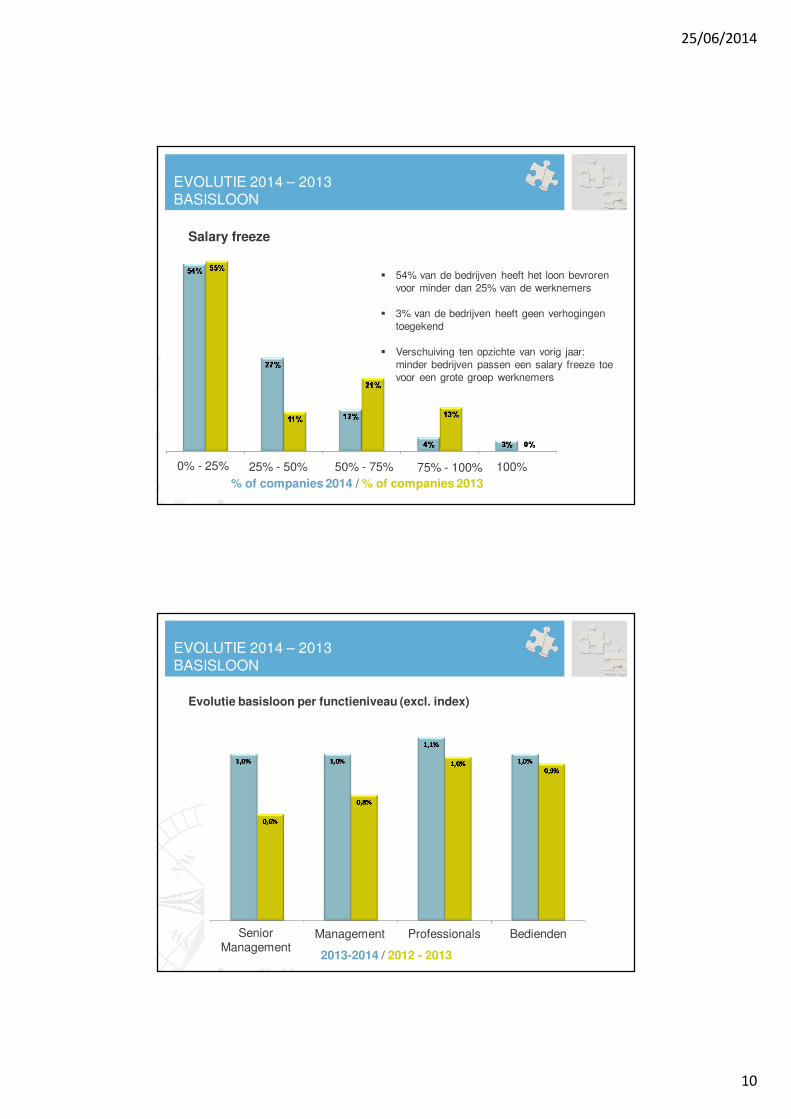

EVOLUTIE 2014 – 2013BASISLOON

Salary freeze

� 54% van de bedrijven heeft het loon bevroren

voor minder dan 25% van de werknemers

� 3% van de bedrijven heeft geen verhogingen

toegekend

� Verschuiving ten opzichte van vorig jaar:

minder bedrijven passen een salary freeze toe

voor een grote groep werknemers

0% - 25% 25% - 50% 50% - 75% 75% - 100% 100%

% of companies 2014 / % of companies 2013

Evolutie basisloon per functieniveau (excl. index)

EVOLUTIE 2014 – 2013BASISLOON

2013-2014 / 2012 - 2013

Senior Management

Management Professionals EmployeesBedienden

25/06/2014

11

EVOLUTIE 2014 – 2013BASISLOON

Evolutie basisloon per bedrijfsgrootte (excl. index)

2013-2014 / 2012 - 2013

Type I Type II Type III

Is er een verschillende loonevolutie tussen mannen en vrouwen?

22

EVOLUTIE 2014 – 2013BASISLOON

0,98% 0,98%

25/06/2014

12

Conclusie

� Er is nog steeds een evolutie in het basissalaris (exclusief indexatie),

van 1%, dit is een quasi status quo ten opzichte van 2012 – 2013, waar

0,94% gold

� Daaruit kunnen we concluderen dat de loonnorm zich laat gelden.

� In de voorbije drie jaar zien we dat grotere evoluties (> 5%) binnen

het basissalaris jaar na jaar afnemen

� Ten opzichte van vorig jaar passen minder bedrijven een salary

freeze toe, waarbij de groepen waarvoor een salary freeze geldt,

kleiner worden

� Er is geen onderscheid in stijging in basissalaris tussen vrouwelijke

en mannelijke werknemers

EVOLUTIE 2014 – 2013BASISLOON

EVOLUTIE 2014 – 2013TOTAL CASH

TOTAL CASHBASISSALARIS

VARIABEL LOON

VARIABEL LOON (cash uitbetaald)

- Target bonus

- Discretionaire bonus

- CAO 90 bonus

- Commissie

- Markttoeslag

- Winstparticipatie

25/06/2014

13

EVOLUTIE 2014 – 2013TOTAL CASH

De gemiddelde salarisstijging voor Total Cash in de Belgische markt

tussen februari 2013 en februari 2014 (exclusief promoties)

Basissalaris Basissalaris

2013 2014

+ 2,0 %

Variabel loon

TOTAL CASH TOTAL CASH

+ 2,8 %

Variabel loon

EVOLUTIE 2014 – 2013TOTAL CASH

4,0%

3,5%

3,8%4,0%

4,3%

5,9%

0,9%

3,7%

4,4%

3,3%

2,0%2,0% 1,9% 1,8% 1,7% 1,8%

4,4%

0,2%

2,2%

3,3%

2,4%

1,0%

4,0%

3,3%

4,2% 4,1%

4,7%

6,1%

1,1%

4,4% 4,3%

3,3%

2,8%

2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012 2012-2013 2013-2014

Base Salary Indexatie Total Cash

De gemiddelde salarisstijging voor Total Cash in de Belgische markt 2004 - 2014

25/06/2014

14

4,0%3,5%

3,8%

4,0%

4,3%

5,9%0,9%

3,7%

4,4%

3,3%

2,0%

2,0%1,9%

1,8%1,7%

1,8%

4,4% 0,2%2,2%

3,3%2,3%

1,0%

4,0%

3,3%

4,2%

4,1%

4,7%

6,1%1,1%

4,4%

4,3%

3,3%

2,8%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Base Salary Indexatie Total Cash

+ 51,2%

EVOLUTIE 2014 – 2013TOTAL CASH

+ 25,0%

+ 47,7%

Variabel loon

� Hoogte variabel loon: Variabel loon als % van Basissalaris

EVOLUTIE 2014 – 2013TOTAL CASH

2013-2014 / 2012 - 2013

Bedienden Professionals Management Senior Management

25/06/2014

15

Variabel loon

� Voorkomen Bonussen: toename voorkomen CAO 90

EVOLUTIE 2014 – 2013TOTAL CASH

Bediende

Professional

Management

Senior Management

2014 2013

Bonus

30% 28%

42% 44%

63% 66%

65% 68%

2014 2013

CAO 90

40% 30%

40% 30%

36% 31%

30% 29%

€ 1.969 € 1.899

€ 3.106 € 3.175

€ 7.702 € 6.203

€ 12.181 € 12.087

Variabel loon

� Hoogte Bonussen

EVOLUTIE 2014 – 2013TOTAL CASH

Bediende

Professional

Management

Senior Management

2014 2013

Bonus

2014 2013

CAO 90

€ 1.025 € 973

€ 1.742 € 1.527

€ 2.217 € 2.358

€ 2.358 € 2.430

25/06/2014

16

EVOLUTIE 2014 – 2013TOTAL CASH

Evolutie Total Cash per bedrijfsgrootte

Type I Type II Type III

2013-2014 / 2012 - 2013

32

EVOLUTIE 2014 – 2013TOTAL CASH

1,64%

1,83%

25/06/2014

17

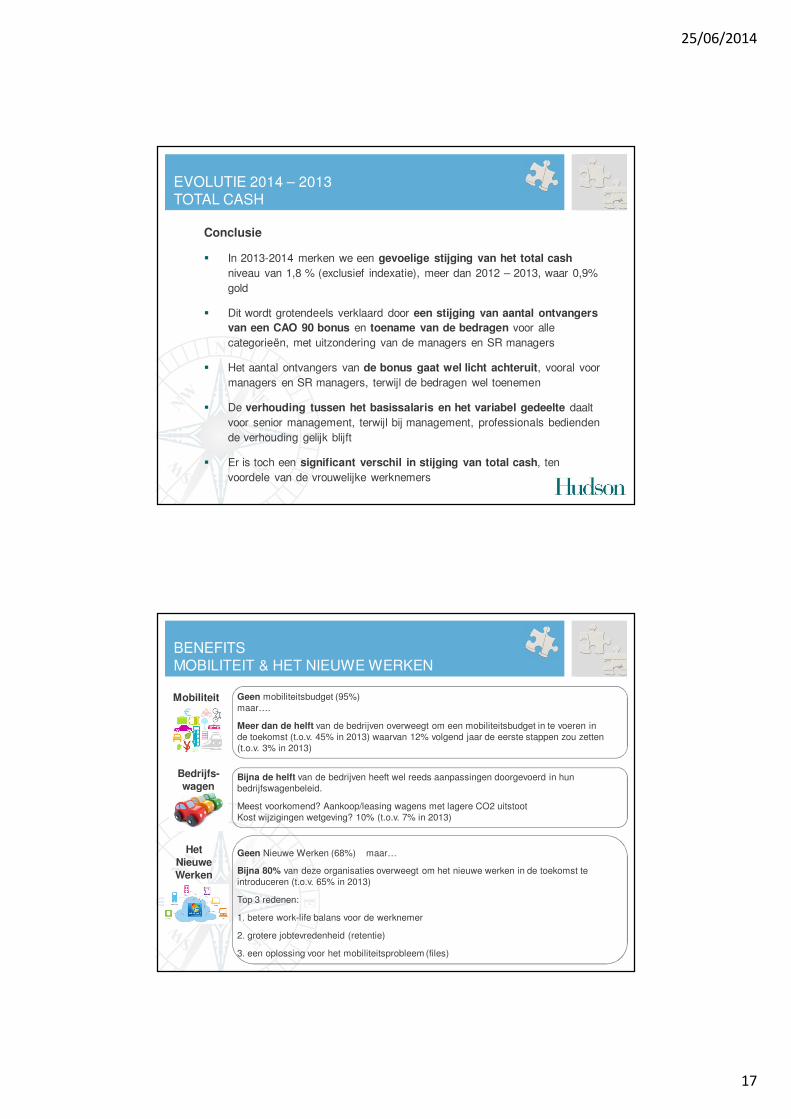

Conclusie

� In 2013-2014 merken we een gevoelige stijging van het total cash

niveau van 1,8 % (exclusief indexatie), meer dan 2012 – 2013, waar 0,9%

gold

� Dit wordt grotendeels verklaard door een stijging van aantal ontvangers

van een CAO 90 bonus en toename van de bedragen voor alle

categorieën, met uitzondering van de managers en SR managers

� Het aantal ontvangers van de bonus gaat wel licht achteruit, vooral voor

managers en SR managers, terwijl de bedragen wel toenemen

� De verhouding tussen het basissalaris en het variabel gedeelte daalt

voor senior management, terwijl bij management, professionals bedienden

de verhouding gelijk blijft

� Er is toch een significant verschil in stijging van total cash, ten

voordele van de vrouwelijke werknemers

EVOLUTIE 2014 – 2013TOTAL CASH

BENEFITSMOBILITEIT & HET NIEUWE WERKEN

Geen mobiliteitsbudget (95%)

maar….

Meer dan de helft van de bedrijven overweegt om een mobiliteitsbudget in te voeren in

de toekomst (t.o.v. 45% in 2013) waarvan 12% volgend jaar de eerste stappen zou zetten

(t.o.v. 3% in 2013)

Bijna de helft van de bedrijven heeft wel reeds aanpassingen doorgevoerd in hun

bedrijfswagenbeleid.

Meest voorkomend? Aankoop/leasing wagens met lagere CO2 uitstoot

Kost wijzigingen wetgeving? 10% (t.o.v. 7% in 2013)

Geen Nieuwe Werken (68%) maar…

Bijna 80% van deze organisaties overweegt om het nieuwe werken in de toekomst te

introduceren (t.o.v. 65% in 2013)

Top 3 redenen:

1. betere work-life balans voor de werknemer

2. grotere jobtevredenheid (retentie)

3. een oplossing voor het mobiliteitsprobleem (files)

Mobiliteit

Bedrijfs-

wagen

Het

Nieuwe

Werken

25/06/2014

18

AGENDA

Prestatiebelonen = Een performant loonbeleid?

� Inleiding

� Generieke Salarisstudie Hudson

� Evolutie 2014 – 2013

� Genderanalyse

� Strategisch belonen

� From pay to performance

� Resultaten onderzoek CAO 90

� Receptie

Vrouwen werken vaker deeltijds �maakt een groot deel uit van de ongelijkheid op de arbeidsmarkt

GENDERANALYSE

Bron: http://igvm-iefh.belgium.be/

Loonkloof bij leidinggevenden: 15%

Loonkloof stijgt met het aantal werknemers in de onderneming

Verschil op jaarbasis: 23%

Loonkloofrapport 2013 door Instituut voor de Gelijkheid van

Vrouwen en Mannen Vrouwen verdienen per uur gemiddeld 10% minder dan

mannen

Equal pay day: 18 maart 2014

25/06/2014

19

GENDERANALYSEBASISSALARIS

4%

-3%

-4%

-8%

Vrouwen

Mannen

Bedienden Professionals Management Senior Management

38

1%

-3%

-4%

-13%

GENDERANALYSETOTAL CASH

Vrouwen

Mannen

Bedienden Professionals Management Senior Management

Vrouwen

Mannen

25/06/2014

20

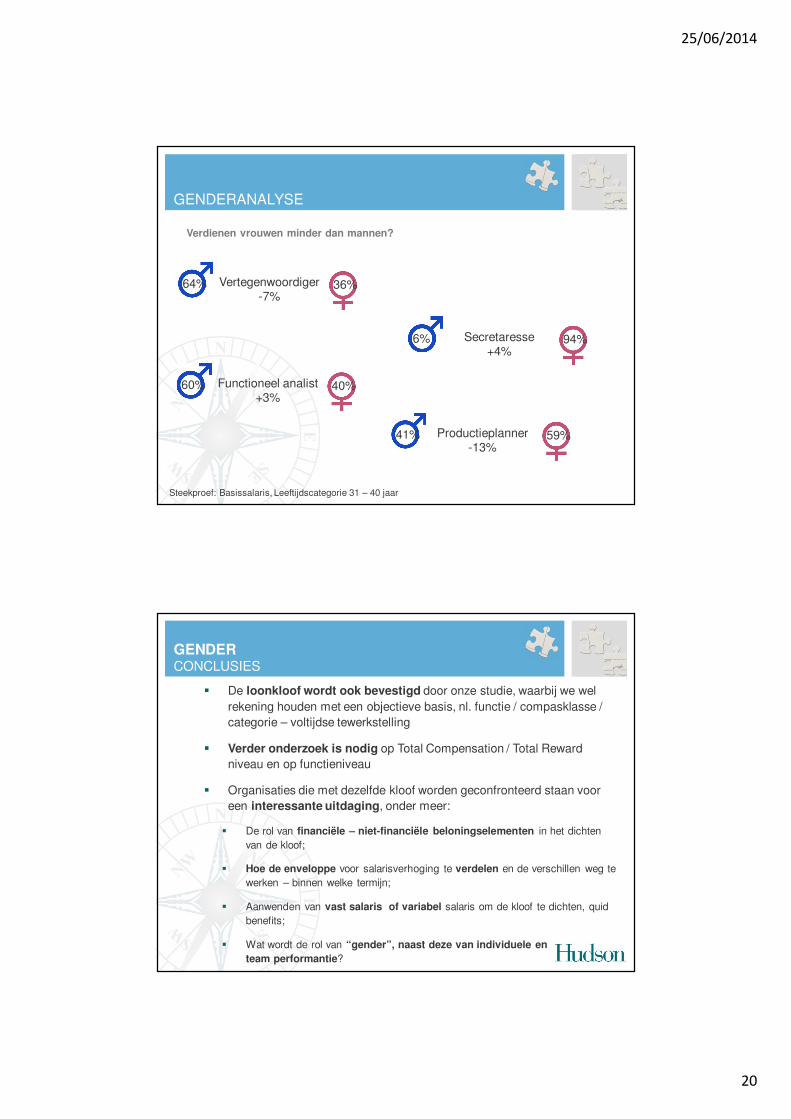

Verdienen vrouwen minder dan mannen?

GENDERANALYSE

Vertegenwoordiger-7%

64% 36%

Secretaresse+4%

6% 94%

Functioneel analist+3%

60% 40%

Steekproef: Basissalaris, Leeftijdscategorie 31 – 40 jaar

Productieplanner-13%

41% 59%

GENDERCONCLUSIES

� De loonkloof wordt ook bevestigd door onze studie, waarbij we wel

rekening houden met een objectieve basis, nl. functie / compasklasse /

categorie – voltijdse tewerkstelling

� Verder onderzoek is nodig op Total Compensation / Total Reward

niveau en op functieniveau

� Organisaties die met dezelfde kloof worden geconfronteerd staan voor

een interessante uitdaging, onder meer:

� De rol van financiële – niet-financiële beloningselementen in het dichten

van de kloof;

� Hoe de enveloppe voor salarisverhoging te verdelen en de verschillen weg te

werken – binnen welke termijn;

� Aanwenden van vast salaris of variabel salaris om de kloof te dichten, quid

benefits;

� Wat wordt de rol van “gender”, naast deze van individuele en

team performantie?

25/06/2014

21

AGENDA

Prestatiebelonen = Een performant loonbeleid?

� Inleiding

� Generieke Salarisstudie Hudson

� Evolutie 2014 – 2013

� Genderanalyse

� Strategisch belonen

� From pay to performance

� Resultaten onderzoek CAO 90

� Receptie

Beloningsstrategie

“Een verklaring die prioriteiten stelt voor de ontwikkeling en de opvolging van het

beloningsbeleid dat gealigneerd wordt op de organisatie- en HR-strategie en op

de noden van de mensen in de organisatie”

Een beloningsstrategie biedt een antwoord op volgende vragen:

� Waarvoor willen we belonen?

� Hoeveel willen we belonen?

� Hoe willen we belonen?

� Wie beslist er over de beloning?

STRATEGISCH BELONENDEFINITIE

25/06/2014

22

STRATEGISCH BELONENVLERICK MODEL

Functie Functiegewicht / Klasse

Anciënniteit Waarden

Kwalitatieve criteria Long term performantie

Individuele performantie Performantie van team

Kwantitatieve criteria Short term performantie

Competenties Technische expertise

STRATEGISCH BELONENSELECTEER DE RELEVANTE BELONINGSCRITERIA…

Objectieven

Potentieel

Mobiliteit

Performantie van

organisatie

Promotie

Diploma

25/06/2014

23

STRATEGISCH BELONENDE BELONINGSCRITERIA… VOORBEELD

0

0

0

1

5

6

7

0

6

1

3

6

4

4

2

0

4

0

6

0 1 2 3 4 5 6 7 8

niet-cijfermatige/kwalitatieve criteria

cijfermatige/objectieve criteria

short term

long term

performantie lokale organisatie

performantie van team/business unit

individuele performantie

performantie internationaleorganisatie

horizontale groei

verticale groei

technische expertise

potentieel

waarden

functiegewicht

functie

diploma

objectieven

anciënniteit

competenties

Strategisch belonen

Criteria

Waarvoor willen bedrijven belonen?

STRATEGISCH BELONENUITKOMST VAN RECENTE STRATEGISCHE WORKSHOPS

TOP 5 gekozen criteria TOP 5 niet gekozen criteria

Diploma Individuele prestaties

Bedrijfswaarden

Functiegewicht / klasse

Lange termijn prestaties

Teamprestaties

Kwantitatieve criteria

Competenties

Potentieel

Anciënniteit

25/06/2014

24

Hoeveel willen bedrijven verlonen?

� Voornaamste observatie: bescheidenheid heeft de bovenhand

� De keuze van referentiemarkt is gebaseerd op observaties uit de realiteit, op feiten en cijfers

� Beperkte differentiatie op vlak van positionering op de markt tussen verschillende

functieklassen of –families, keuze voor een meer egalitaire aanpak

� Bewuste positionering op de markt voor Basissalaris, Total Cash en Total Compensation

� Positionering op marktmediaan – voor een normaal prestatieniveau

� Voor hoge prestaties – mogelijkheid om tot het 75ste percentiel te verdienen van de referentiemarkt – Total Cash

� Meer regelmatige opvolging van de marktpraktijken voor specifieke profielen (IT, Accounting, …)

� Rekening houden met niet-financiële verloningselementen bij de aanpak van de markt:

� Employer branding, New Way of Work, carrièrekansen, training, ligging,…

� Redenen om iets onder de referentiemarkt te liggen voor het basisloon/ variabel loon

STRATEGISCH BELONENUITKOMST VAN RECENTE STRATEGISCHE WORKSHOPS

Hoe willen we belonen?

� De aanpak van “total reward” werd

volledig overgenomen

� Nadruk op marketing & communicatie

van het huidige pakket

� Veel aandacht voor de niet-financiële

elementen en de intrinsieke

motiveringsfactoren (leadership

programma’s, coaching, …) gegeven de

beperkte financiële ruimte

� Generatiebewust verloning waarbij de

“reward mix” in lijn ligt met de individuele

noden van de werknemers, op basis van

resultaten uit tevredenheidsenquêtes

� Keuze voor flexibele verloning, maar

nog veel aarzeling (budgettaire

beperkingen/ gebrek aan

zekerheid/juridische stabiliteit)…

STRATEGISCH BELONENUITKOMST VAN RECENTE STRATEGISCHE WORKSHOPS

25/06/2014

25

Wie beslist over de beloning?

� Er wordt veel aarzeling opgemerkt bij discussies over de rol van SR Managers

en eerstelijnsmanagers in beslissingen rond beloning

� Bevestiging van de rol van SR managers/ lijnmanagers in het performance &

development proces – succession management – workforce planning –

talent review

� Toenemende betrokkenheid van SR managers / lijnmanagers bij beslissingen

over functieclassificatie – meer autonomie om zelf het team samen te stellen

� Directiecomités willen SR managers de verantwoordelijkheid geven voor het

beheer van de loonmassa en de loonevolutie in co-ownership met Finance &

HR … maar twijfelen of dit op korte termijn haalbaar is

STRATEGISCH BELONENUITKOMST VAN RECENTE STRATEGISCHE WORKSHOPS

Wanneer we onze huidige klanten bekijken, zien we een duidelijke verschuiving in focus /investeringen:

Functie

Organisatie

Classificatiestructuur

Smalle functieclassificatie-

structuur / salarisbanden

Performance & Development

proces

Functiebeschrijving

Medewerker

Job crafting / design

Performance & Development

proces

Brede banden

/ brede salarisbanden

Leadership

Beschrijving rol/functiefamilie

STRATEGISCH BELONENUITKOMST VAN RECENTE STRATEGISCHE WORKSHOPS

25/06/2014

26

AGENDA

Prestatiebelonen = Een performant loonbeleid?

� Inleiding

� Generieke Salarisstudie Hudson

� Evolutie 2014 – 2013

� Genderanalyse

� Strategisch belonen

� From pay to performance

� Resultaten onderzoek CAO 90

� Receptie

FROM PAY TO PERFORMANCESPREKER: XAVIER BAETEN

Opleiding:

� 1987 - 1991 Universiteit Gent

Master in Economie

� 1991 - 1992 Vlerick Business School

Master na Master Tax & Accountancy

Huidige functie:

� Professor Vlerick Business School

� Head of the Center for Excellence in Strategic Rewards

Contactgegevens:

℡ 09 210 98 97

25/06/2014

27

FROM PAY TO PERFORMANCE

SPREKER: MAARTEN SIMON

Opleiding:

� 1995 – 2000 Universiteit GentMaster Rechten

Huidige functie:

� Counsel – lawyer: specialisatie in labour and employment law

Ervaring:

� He has assisted several clients during a number of important restructuring operations and offers assistance to companies in their queries concerning employment contracts, collective information and consultation, strikes, social elections, international employment and social security

� He is a regular speaker at Vlerick Business School and M&D Seminars

Contactgegevens:

℡ +32 (0)9 261 50 01

25/06/2014

28

FROM PAY TO PERFORMANCE!

PROF DR XAVIER BAETEN (VLERICK BUSINESS SCHOOL) &

MAARTEN SIMON (CLAEYS & ENGELS)

56

25/06/2014

29

© Vlerick Business School

AGENDA

57

Pay-for-performance: framing & research insights

CBA 90:

What?

Why?

CBA 90 as an instrument for strategic rewards

1PAY-FOR-PERFORMANCE:

FRAMING & RESEARCH INSIGHTS

58

25/06/2014

30

1.1PAY-FOR-PERFORMANCE: WHAT?

59

© Vlerick Business School

VARIABLE PAY: WHAT’S IN A NAME?

60

Meritpay/bonus

Stock appreciation

rights

Stock option plans

Share plans

Team incentives

GoalsharingGainsharing Profit sharing

Discretionarybonuses

Sales commissions

Piece rates

25/06/2014

31

© Vlerick Business School

VARIABLE PAY: STRUCTURING OUR THOUGHTS

61

Timeframe

Whichperformance?

Whoseperformance?

Payout

1.2PAY-FOR-PERFORMANCE:

SOME STAKEHOLDER OPINIONS

62

25/06/2014

32

© Vlerick Business School

COMP & BEN’S VOICE

63Centre for Excellence in Strategic Rewards

© Vlerick Business School

COMP & BEN’S VOICE

64Centre for Excellence in Strategic Rewards

25/06/2014

33

© Vlerick Business School

COMP & BEN’S VOICE

65Centre for Excellence in Strategic Rewards

© Vlerick Business School

THE EMPLOYEES’ VOICE -RATIO FIXED VERSUS VARIABLE PAY

On average, employees prefer 78% fixed pay and 22% variable

%0 20 40 60 80 100

Pct 25

Mean

Pct 75

Pct 25

Mean

Pct 75

DS

LL

Variable

Fixed

Centre for Excellence in Strategic Rewards

25/06/2014

34

© Vlerick Business School

THE EMPLOYEES’ VOICE -CRITERIA UNDERLYING VARIABLE PAY

1,0 1,5 2,0 2,5 3,0 3,5 4,0 4,5 5,0

Org./BU performance

Team performance

Behavioural measures

Competence/skill development

Individual performance

Centre for Excellence in Strategic Rewards

© Vlerick Business School

THE EMPLOYEES’ VOICE –KNOWLEDGE OF PAY

68Mulvey, LeBlanc, Heneman, & McInerney

25/06/2014

35

1.3PAY-FOR-PERFORMANCE:

INSIGHTS FROM ACADEMIC RESEARCH

69

© Vlerick Business School

RIGHT OR WRONG?

70

Yes No

Pay-for-performance increases performance

Rewards based on individual performance are more effective than team-based rewards

Merit pay has a stronger effect on futureperformance than bonuses

25/06/2014

36

© Vlerick Business School

“PAY-FOR-PERFORMANCE INCREASESPERFORMANCE”

71

• 44% increase in output• Increase in variance of output

Incentiveeffect

Sortingeffect

Rynes, Gerhart, & Minette

© Vlerick Business School

“PAY-FOR-PERFORMANCE INCREASESPERFORMANCE”

72

Meta-analysis – 146 studies:

Effect on performance: Yes!

Moderators

Task complexity

Qualitative measures

Garbers & Konradt

25/06/2014

37

© Vlerick Business School

“INDIVIDUAL INCENTIVES ARE MORE EFFECTIVE THAN TEAM-BASED REWARDS”

73

0,32

0,28

0,39

0,19

0,36 0,37

0,450,49

0,56

0,28

0,88

Hedge's g

Individual financial incentive Team-based rewards

Garbers & Konradt (2014)

© Vlerick Business School

“INDIVIDUAL INCENTIVES ARE MORE EFFECTIVE THAN TEAM-BASED REWARDS”

74Garbers & Konradt (2014)

Group characteristics

• Smaller teams• Interdependence• Strong groupperformance norms

• Collective self-efficacy

Procedure

• Feedback• Participative goal setting

• Involvement in design/ implementation

• Criteria under control by group

25/06/2014

38

© Vlerick Business School

“MERIT PAY HAS A STRONGER EFFECT ON FUTURE PERFORMANCE THAN BONUSES”

75Nyberg, Pieper, & Trevor

© Vlerick Business School

RIGHT OR WRONG?

76

Yes No

Pay-for-performance increases performance X

Rewards based on individual performance are more effective than team-based rewards

X

Merit pay has a stronger effect on futureperformance than bonuses

X

25/06/2014

39

2CBA 90: WHAT?

77

What is a CBA 90 bonus?

“non recurring advantages linked to results”

Bonus plan

• introduced through a specific procedure;

• which grants employees a tax-free bonus of up to € 3,131;

• Subject to realisation of predefined targets which must be:

– Transparant,

– Collective,

– Uncertain, and

– Objectively measurable.

78

25/06/2014

40

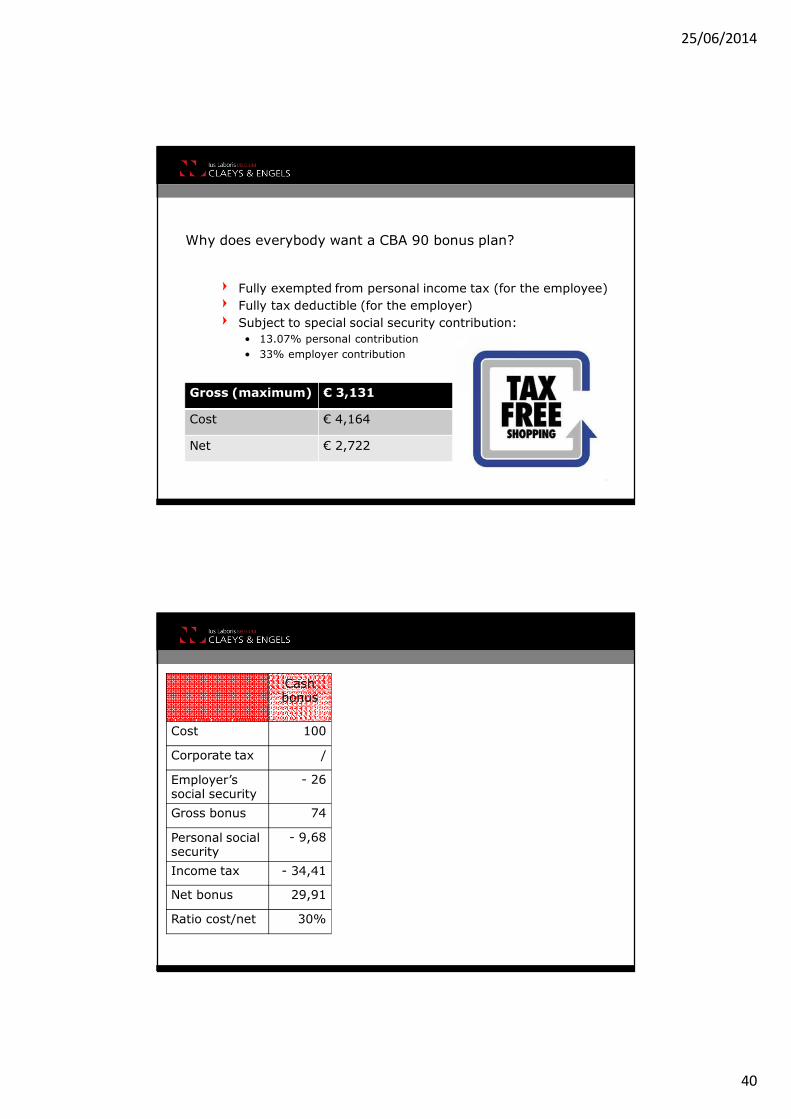

Why does everybody want a CBA 90 bonus plan?

Fully exempted from personal income tax (for the employee)

Fully tax deductible (for the employer)

Subject to special social security contribution:

• 13.07% personal contribution

• 33% employer contribution

79

Gross (maximum) € 3,131

Cost € 4,164

Net € 2,722

Cash bonus

Result bonus

(CBA 90)

Stock options

Benefit Participation

(Act 2001)

Bonus Pension Plan

Cost 100 100 100 100 100

Corporate tax / / / - 34 - 3,88

Employer’ssocial security

- 26 - 24,81 / / - 7,82

Gross bonus 74 75,19 100 66 88,29

Personal socialsecurity

- 9,68 -9,83 / - 8,63 - 4,90

Income tax - 34,41 / - 26,75 - 14,34 - 14,72

Net bonus 29,91 65,36 73,25 43,03 68,67

Ratio cost/net 30% 65% 73% 43% 69%

80

25/06/2014

41

81

Draft plan toemployees

15 days forcomments

Plan to FPS andregister toInspection

FPS checks formalities

Joint Committee or FPS check contents

If ok: approvalIf not ok: employermust amend within

1 month

Negotiate plan with(at least one) union

Sign CBA CBAto FPSFPS checks formalities

Contents are notchecked

If ok: registrationIf not ok: employermust amend within

1 month

Before 1/3rd of reference period

No trade union delegation

With trade union delegation

Procedure

3CBA 90: WHY?

82

25/06/2014

42

3.1SAMPLE

83 CBA 90: Why?

A unique partnership!

CBA 90: Why?

25/06/2014

43

459

CBA 90: Why?

© Vlerick Business School

SAMPLE

CBA 90: Why?

25/06/2014

44

© Vlerick Business School

Manufacturing (C) 27%

Other 24%

Wholesale & retail trade (G) 14%

Professional, scientific and technical activities (M)

8%

Financial and insurance activities (K) 8%

Administrative and supportive service activities (N)

8%

Information and communication (J) 6%

Construction (F) 5%

SAMPLE

CBA 90: Why?

3.2WHY (NOT) IMPLEMENTING CBA 90?

88 CBA 90: Why?

25/06/2014

45

© Vlerick Business School

SINCE WHEN?

89 CBA 90: Why?

© Vlerick Business School

NUMBER OF PLANS

CBA 90: Why?

25/06/2014

46

© Vlerick Business School

ELIGIBILITY

91 CBA 90: Why?

© Vlerick Business School

WHY?

92 CBA 90: Why?

25/06/2014

47

© Vlerick Business School

WHY?

93 CBA 90: Why?

© Vlerick Business School

WHY NOT?

94 CBA 90: Why?

25/06/2014

48

© Vlerick Business School

WHY NOT?

95 CBA 90: Why?

© Vlerick Business School

IMPACT

96 CBA 90: Why?

25/06/2014

49

© Vlerick Business School

IMPACT

97 CBA 90: Why?

Why?

Tax-friendly

Conversion of existing bonus schemes possible

If already partially collective

Flexible target setting

Why not?

98

No link to individualperformance – no differentiation

Union involvement

Examples: union refuses differencesin bonus amounts; union refuses the reduction of absenteeism as a target

Administrative burden

(often overestimated!)

Sceptisism from globalheadquarters

25/06/2014

50

Converting existing bonus scheme: option 1

99

Company

Team

Individual

CBA 90

Separate plan

Converting existing bonus scheme: option 2

100

Company

Team

Individual

CBA 90

25/06/2014

51

Individualizing CBA bonus schemes?

Target level?

Pay-out level?

• Bonus amount as a percentage of base pay / annual pay

• Bonus amount as a percentage of variable pay (?)

• Different bonus amounts, depending on function level / othercriteria (?)

Eligibility criteria?

• Bonus scheme limited to “good performers” (???)

101

Union involvement

Can be avoided if no trade union delegation (or if plan is limited to employees who are not represented by the tradeunion delegation)

Union involvment Involvement of FDS Employment

Be creative to encompass doctrinal refusals

102

25/06/2014

52

4CBA 90 AS AN INSTRUMENT

FOR STRATEGIC REWARDS

103

© Vlerick Business School

CRITERIA

104 CBA 90 as instrument for strategic rewards

25/06/2014

53

105

© Vlerick Business School

CHANGES OVER THE YEARS

38%

Changes:

Criteria: 39%

Target levels (same criteria): 42%

Reference period: 13%

Other: 6%

106 CBA 90 as instrument for strategic rewards

25/06/2014

54

107

- Reducing absenteeism- Reducing work accidents- Respecting safety procedures

- Client satisfaction- Employee satisfaction (?)- Quality standards

- Increase of profit > increase of personnel costs- Successful reorganisation

- Innovation

Examples of bonus targets

Reference period

Minimum 3 months, no maximum

Possibility to combine several plans

108

Plan 1: EBIT

Plan 2: work accidents Plan 3: production duringyear-end peak

25/06/2014

55

Changing the plan itself

CBA Accession Act

Targets Procedure definedin CBA

Not possible

Target levels Procedure definedin CBA

Procedure definedin Plan

Bonus amounts New CBA Not possible

109

> Only for future reference periods?

© Vlerick Business School

COMMUNICATION

Do you communicate on CBA 90 to youremployees?

76% yes

Interim communication on realisation of targets?

63% yes

110 CBA 90 as instrument for strategic rewards

25/06/2014

56

© Vlerick Business School

COMMUNICATION

111 CBA 90 as instrument for strategic rewards

Communication with employees: what does the law say?

Prior communication: only if no trade union delegation

• Draft plan

• Approval / rejection / modification of the plan

Communication during reference period: Bonus plan must contain a follow-up procedure

Communication after reference period: information sheet• Employee name

• Identification of the plan

• Reference period

• For each target: realization and methodology that was used to measure

• Calculation method

• Payment date

• Tax exemption112

25/06/2014

57

© Vlerick Business School

REJECTION BY ADMINISTRATION?

113 CBA 90 as instrument for strategic rewards

© Vlerick Business School

REJECTION BY ADMINISTRATION

Most ‘popular’:

Administration

Formalities (language, form, timeliness)

Targets

Too vague

Too brief

No objective enough

Eligibility

Description

Seniority is not acceptable

Only 1 person in plan

114 CBA 90 as instrument for strategic rewards

25/06/2014

58

Why does the administration refuse plans? (1/2)

Targets are insufficiently clear

Example: “at least the same revenue as last year”

Targets are not objectively measurable

Example: “realize client satisfaction”

Targets do not correspond to reference period

Example: in a plan for 2014: “project X should by realized by August 2014”

Reference period is shorter than three months

Example: “bonus of 100 EUR for every month without working accident”

Targets are not collective

Example: “every employee must have followed training X” (disputable)

115

Why does the administration refuse plans? (2/2)

Complaint procedure is insufficiently detailed

Example: “employee can file a complaint with the HR Manager, who will take a

decision”

Double pro rata

Example: “bonus is 5% of annual salary” + “bonus will be prorated for

part-time employees”

116

25/06/2014

59

© Vlerick Business School

HOW SATISFIED ARE HR MANAGERS WITH CBA 90?

CBA 90 as instrument for strategic rewards

© Vlerick Business School

HR MANAGERS’ SUGGESTIONS FOR CHANGE

118 CBA 90 as instrument for strategic rewards

25/06/2014

60

5CONCLUSIONS

119

© Vlerick Business School

CONCLUSIONS

Pay-for-performance is good for you!

Team-based rewards are even better

But do not forget broader HR context

CBA 90

Popular (and still growing), but still a way to go

Most popular: operational white collars & middlemanagement

Merits: optimisation + incentive effect

Drawbacks: administration + no differentiation

Strategic rewards perspective

No ‘real’ team-based pay

Communication - employee involvement?

No differentiation

120

25/06/2014

61

121

The most negative employee attitudes are those concerning performance pay.

So, what is the underlying problem here?

Is it also a case of

a bad idea gone predictably wrongor, alternatively,

of good ideas being poorly applied?

25/06/2014

62

BACKUP SLIDES

123

Which companies have adopted a CBA 90 bonus plan?

Results of survey

Other sources:

• 2012: 15% of all white-collar workers and 12% of all blue-collarworkers (source: SD Worx)

• 2009: about 190,000 employees (average amount of 260 EUR) (source: Minister of Social Affairs, QRVA 53 012)

Industry-level CBA’s

124

25/06/2014

63

Industry-level CBA 90 (2014)

Industry Target Bonus amount

102.01 (Hainaut) To be defined at company level 2 x 100 EUR

105 + 224 Return on capital employed> 5%> 20%

1 – 3.6% of grosssalary earned duringreference period

116 (Limburg) Profit / Revenue> 0 (minimum)> 10% (maximum)

100 EUR – 300 EUR

140.01 (TEC) (Revenue TEC year X / Revenue TEC year X-1) > (Salary cost TEC year X / Salary Cost TEC year X)1)

33% of the revenueincrease whichexceeds the salarycost increase

140.01 (VMM) Increase of revenue VMM comparedto last year

140 EUR

302 Tonnage of all Belgian sea harbours> 50M ton during reference period(1 April – 30 June)

500 EUR

125

AGENDA

Prestatiebelonen = Een performant loonbeleid?

� Inleiding

� Generieke Salarisstudie Hudson

� Evolutie 2014 – 2013

� Genderanalyse

� Strategisch belonen

� From pay to performance

� Resultaten onderzoek CAO 90

� Receptie

25/06/2014

64

NU BESCHIKBAAR…

� De resultaten van de Generieke Salarisstudie voor de Belgische markt –editie 2014 onder de vorm van:

– Software tools

� Income©

� Editor©

� Editor Advanced©

– Hard copy rapport

– Trendsrapport

– Kwalitatief rapport

� Te verwachten: De nieuw online rapporteringstool