presentation 04 - risk and return 2012.11.15

DESCRIPTION

Introduction into Corporate Finance slidesTRANSCRIPT

Risk and Return

- expected return- notion of risk- measuring risk- risk and portfolio- risk free rate- beta and CAPM

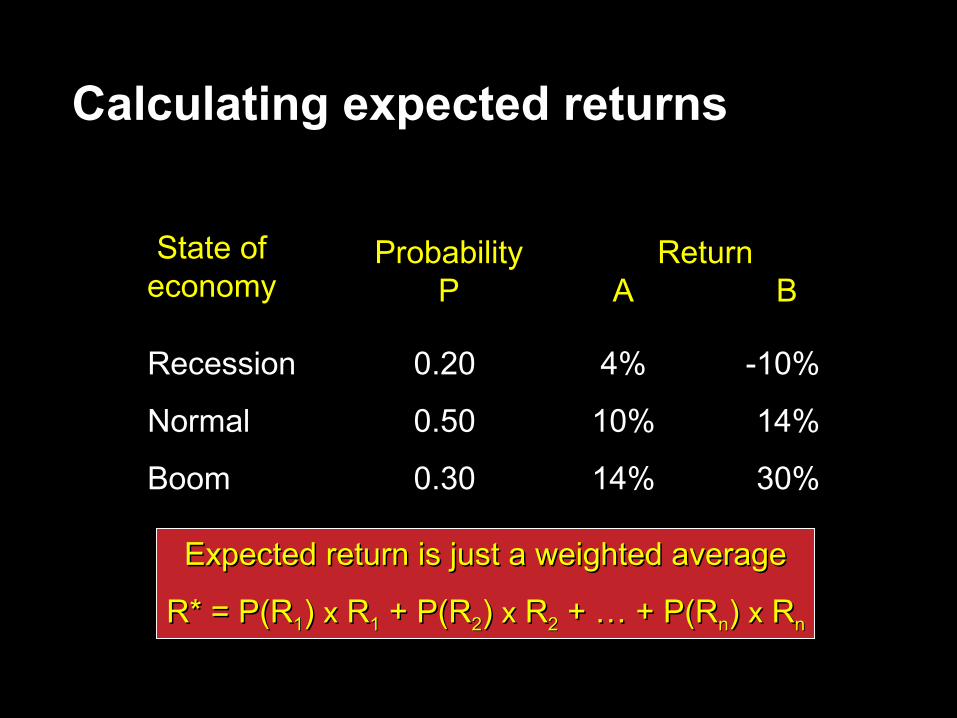

State ofState ofeconomyeconomy

RecessionRecession

NormalNormal

BoomBoom

ProbabilityProbabilityPP

0.200.20

0.500.50

0.300.30

ReturnReturn A B A B

4%4%

10%10%

14%14%

-10%-10%

14%14%

30%30%

Expected return is just a weighted averageExpected return is just a weighted average

R* = P(RR* = P(R11) ) xx R R11 + P(R + P(R22) ) xx R R22 + … + P(R + … + P(Rnn) ) xx R Rnn

Calculating expected returns

State ofState ofeconomyeconomy

RecessionRecession

NormalNormal

BoomBoom

ProbabilityProbabilityPP

0.200.20

0.500.50

0.300.30

ReturnReturn A B A B

4%4%

10%10%

14%14%

-10%-10%

14%14%

30%30%

Company ACompany AR* = P(RR* = P(R11) ) xx R R11 + P(R + P(R22) ) xx R R22 + … + P(R + … + P(Rnn) ) xx R Rnn

RRAA* = 0.2 * = 0.2 xx 4% + 0.5 4% + 0.5 xx 10% + 0.3 10% + 0.3 xx 14% = 10% 14% = 10%

Example

State ofState ofeconomyeconomy

RecessionRecession

NormalNormal

BoomBoom

ProbabilityProbabilityPP

0.200.20

0.500.50

0.300.30

ReturnReturn A B A B

4%4%

10%10%

14%14%

-10%-10%

14%14%

30%30%

Company BCompany BR* = P(RR* = P(R11) ) xx R R11 + P(R + P(R22) ) xx R R22 + … + P(R + … + P(Rnn) ) xx R Rnn

RRBB* = 0.2 * = 0.2 xx -10% + 0.5 -10% + 0.5 xx 14% + 0.3 14% + 0.3 xx 30% = 14% 30% = 14%

Example

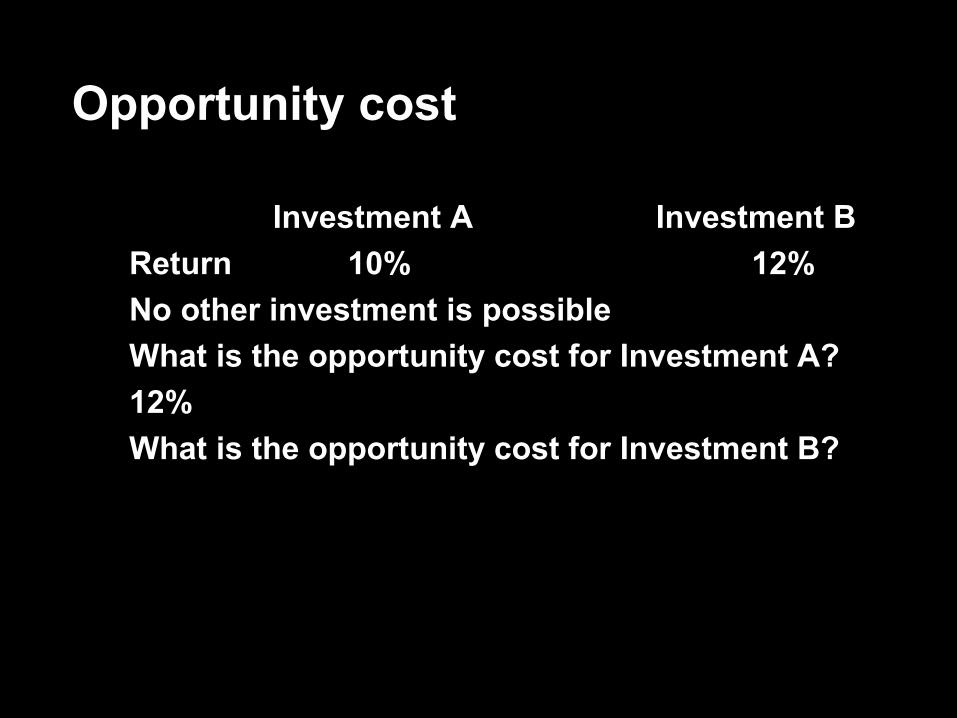

Opportunity cost

� Investment A Investment B� Return 10% 12%� No other investment is possible� What is the opportunity cost for Investment A?

Opportunity cost

� Investment A Investment B� Return 10% 12%� No other investment is possible� What is the opportunity cost for Investment A?� 12%� What is the opportunity cost for Investment B?

Opportunity cost

� Investment A Investment B� Return 10% 12%� No other investment is possible� What is the opportunity cost for Investment A?� 12%� What is the opportunity cost for Investment B?� 10%� Minimise the opportunity cost

Opportunity cost

� Investment A Investment B� Return 10% 12%� No other investment is possible� What is the opportunity cost for Investment A?� 12%� What is the opportunity cost for Investment B?� 10%� Minimise the opportunity cost� RISK?

Petty, Keown, Scott Jr., Martin, Burrow, Martin & Nguyen: Financial Management 4e © 2006 Pearson Education Australia

Financial Risk

� How to measure riskVariance, standard deviation, beta

� How to reduce riskDiversification

� How to price riskSecurity market line, CAPM, APM

What is risk?

� The possibility that an actual return will differ from our expected return

� Uncertainty in the distribution of possible outcomes

0

0.05

0.1

0.15

0.2

-10 -5 0 5 10 15 20 25 30

returnreturn (%) (%)

Company Company 22Company Company 11

0

0.1

0.2

0.3

0.4

0.5

6 10 14

returnreturn (%) (%)

Uncertainty in the distribution of possible outcomes

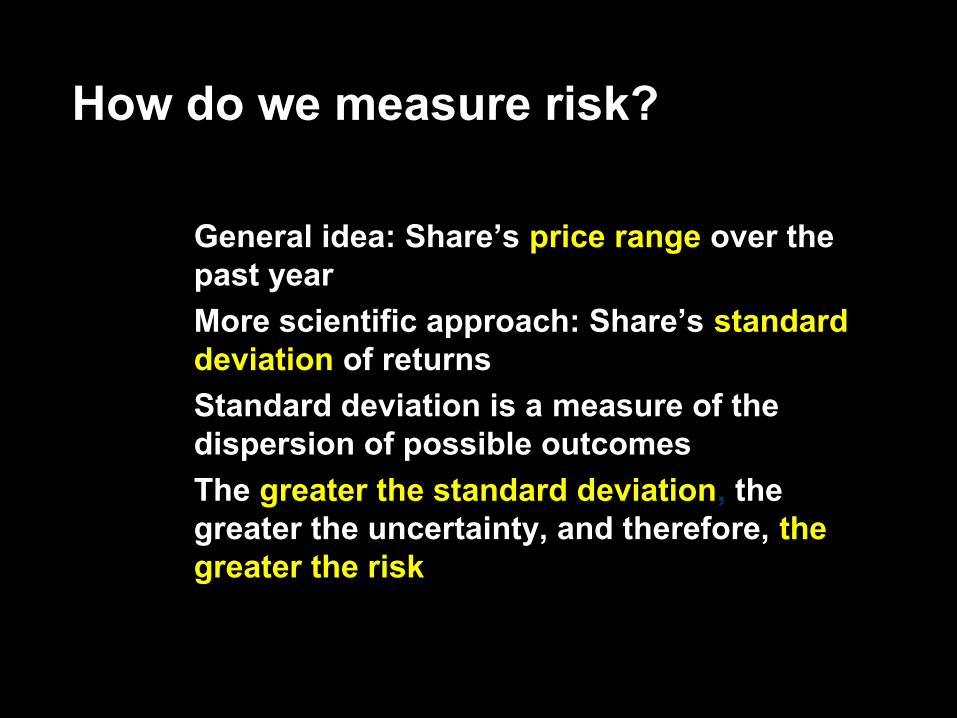

� General idea: Share’s price rangeprice range over the past year

� More scientific approach: Share’s standard standard deviationdeviation of returns

� Standard deviation is a measure of the dispersion of possible outcomes

� The greater the standard deviationgreater the standard deviation, the greater the uncertainty, and therefore, the the greater the riskgreater the risk

How do we measure risk?

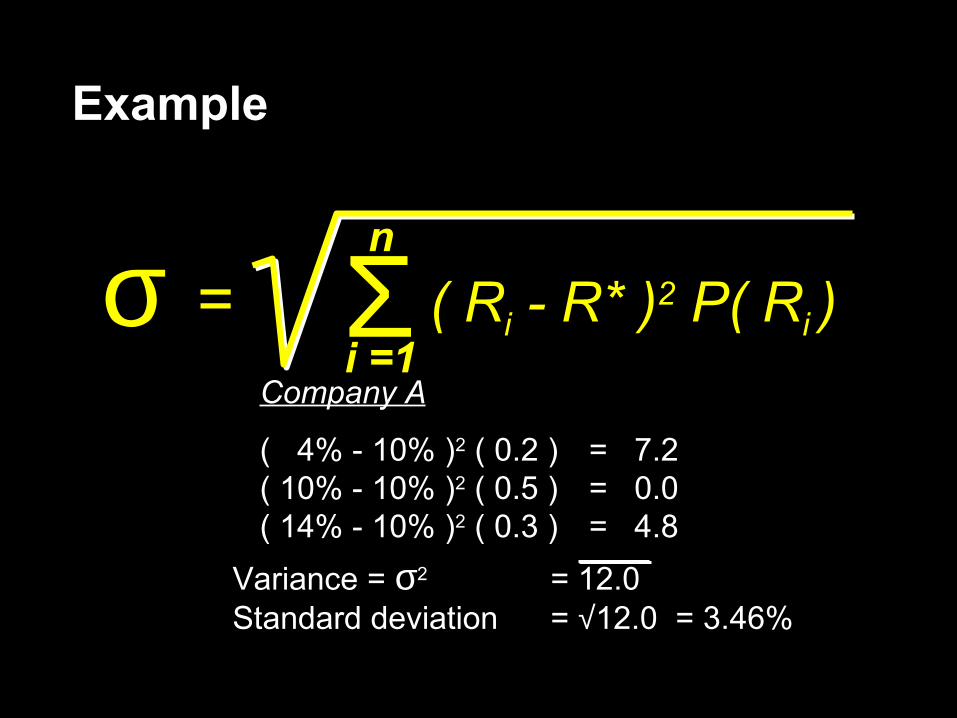

= = (( RRii - - R*R* ))22 P( P( RRii ))σσ ΣΣ nn

i i =1=1

Standard deviation – probability data

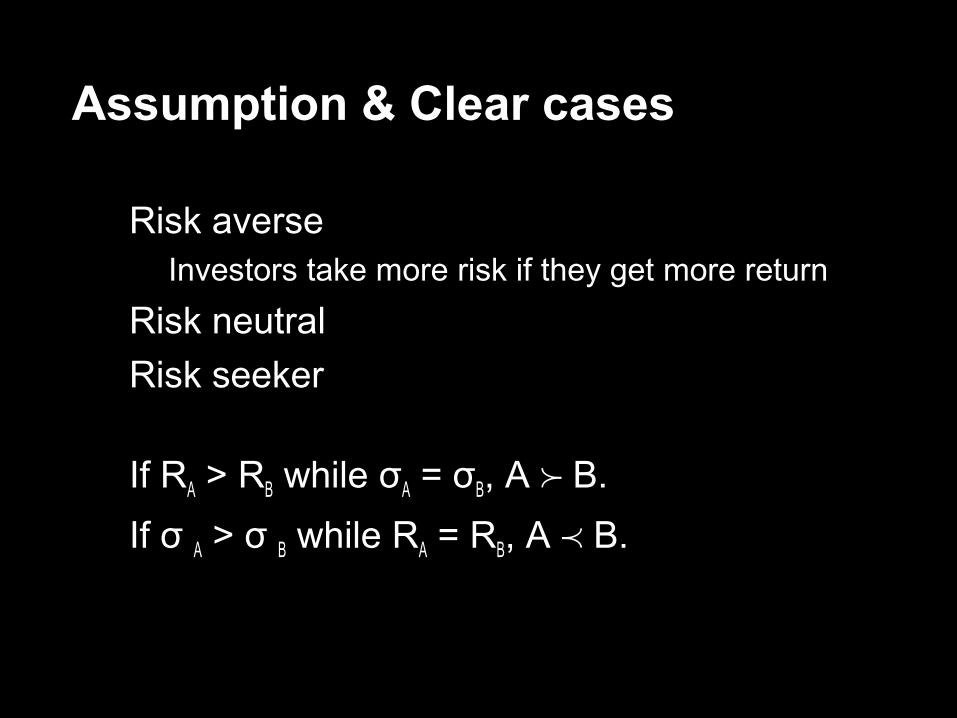

Assumption & Clear cases

� Risk averse� Investors take more risk if they get more return

� Risk neutral� Risk seeker

� If RA > RB while σσAA = = σσBB, A , A B. B.� If σσ A > σσ B while RRAA = R = RBB, A , A B. B.

State ofState ofeconomyeconomy

RecessionRecession

NormalNormal

BoomBoom

ProbabilityProbabilityPP

0.200.20

0.500.50

0.300.30

ReturnReturn A B A B

4%4%

10%10%

14%14%

-10%-10%

14%14%

30%30%

Company ACompany A R* = 10%R* = 10%Company BCompany B R* = 14%R* = 14%

Example

Example

= = (( RRii - - R*R* ))22 P( P( RRii ))σσ ΣΣ nn

i i =1=1Company ACompany A

( 4% - 10% )( 4% - 10% )22 ( 0.2 ) ( 0.2 ) = 7.2= 7.2( 10% - 10% )( 10% - 10% )22 ( 0.5 ) ( 0.5 ) = 0.0= 0.0( 14% - 10% )( 14% - 10% )22 ( 0.3 ) ( 0.3 ) = 4.8= 4.8

Variance = Variance = σσ22 = 12.0= 12.0Standard deviationStandard deviation = = √√12.0 = 3.46% 12.0 = 3.46%

Example

= = (( RRii - - R*R* ))22 P( P( RRii ))σσ ΣΣ nn

i i =1=1Company BCompany B

( -10% - 14% )( -10% - 14% )22 ( 0.2 ) ( 0.2 ) = 115.2= 115.2( 14% - 14% )( 14% - 14% )22 ( 0.5 ) ( 0.5 ) = 0.0= 0.0( 30% - 14% )( 30% - 14% )22 ( 0.3 ) ( 0.3 ) = 76.8= 76.8Variance = Variance = σσ22 = 192.0= 192.0Standard deviationStandard deviation == √√192.0 = 13.86%192.0 = 13.86%

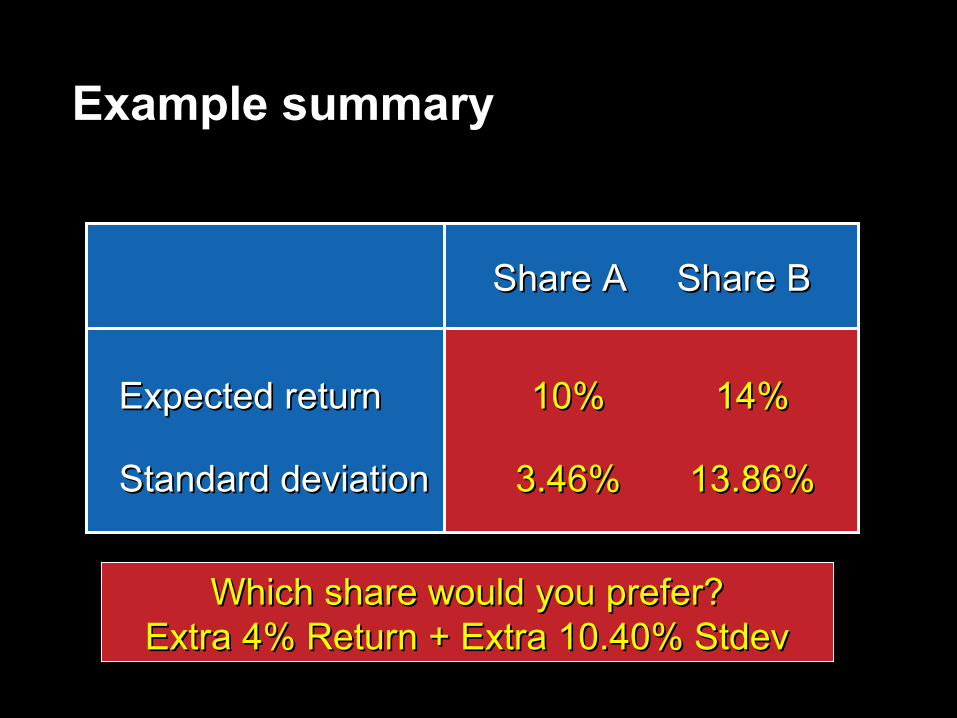

Share AShare A Share BShare B

Expected returnExpected return 10%10% 14%14%

Standard deviationStandard deviation 3.46%3.46% 13.86%13.86%

Example summary

Which share would you prefer?Which share would you prefer?Extra 4% Return + Extra 10.40% StdevExtra 4% Return + Extra 10.40% Stdev

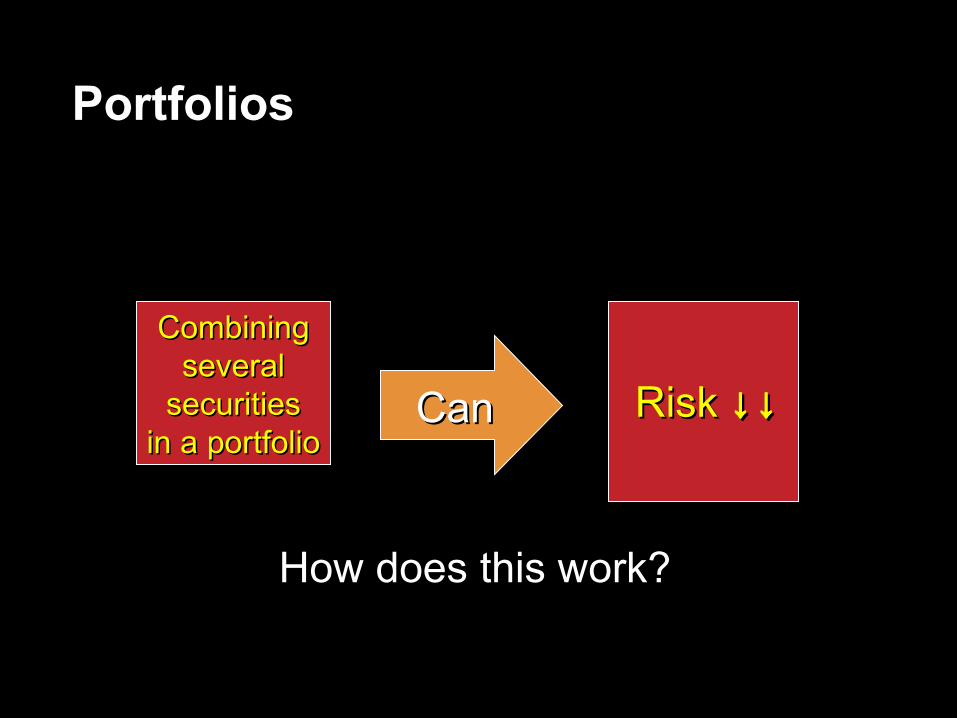

CombiningCombiningseveralseveral

securitiessecuritiesin a portfolioin a portfolio

CanCan Risk Risk ↓↓↓↓

How does this work?How does this work?

Portfolios

PerfectPerfectdiversification.diversification.

Risk isRisk isminimisedminimised

No effectNo effecton riskon risk

perfectlyperfectlypositivelypositivelycorrelatedcorrelated

perfectlyperfectlynegativelynegativelycorrelatedcorrelated

IfIfsecurities securities

areare

Investing in Investing in two securitiestwo securitiesto reduce riskto reduce risk

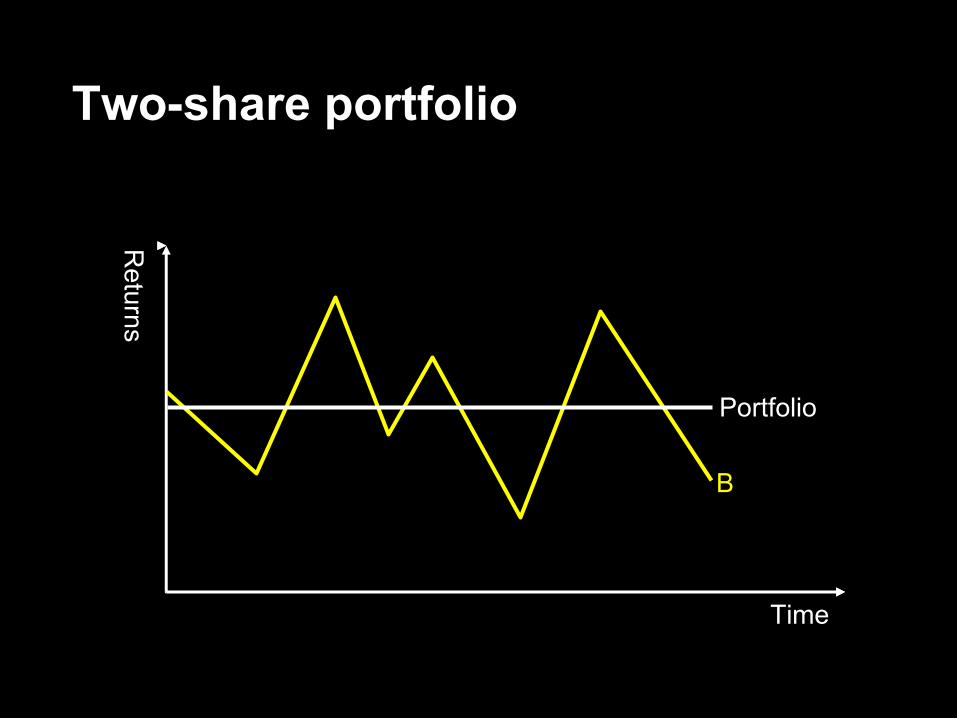

Simple diversification

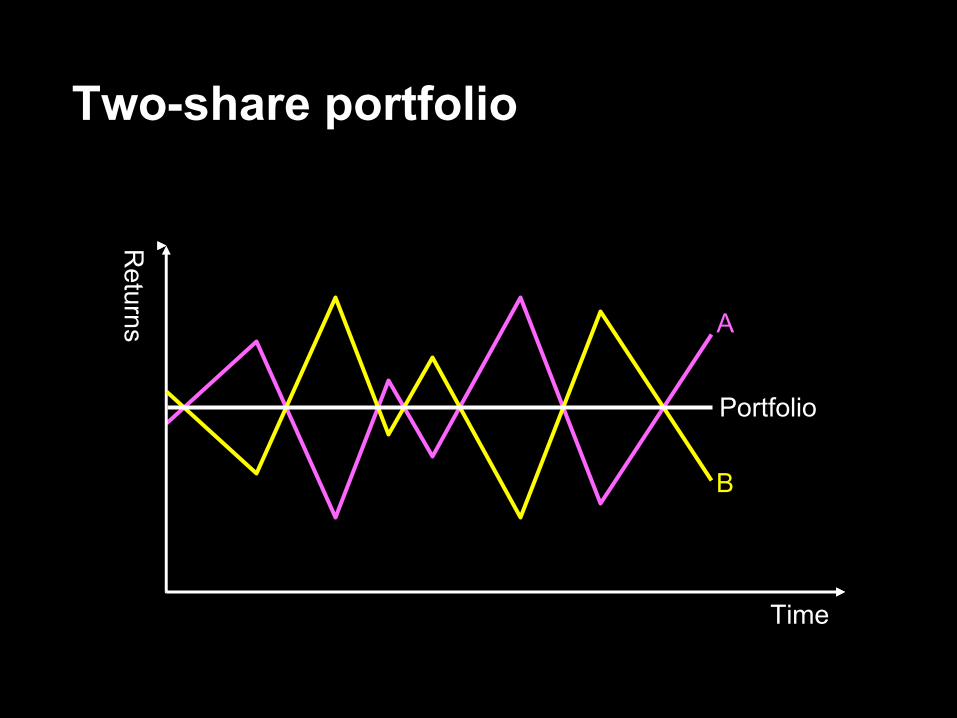

Two-share portfolio

Returns

Returns

TimeTime

BB

PortfolioPortfolio

AA

Two-share portfolio

Returns

Returns

TimeTime

BB

PortfolioPortfolio

AA

Two-share portfolio

Returns

Returns

TimeTime

BB

PortfolioPortfolio

Perfec

t neg

ative

Perfec

t neg

ative

corre

lation

corre

lation

remov

es ris

k

remov

es ris

k

Combining two shares

� Changing proportions � Share A: 100% Share B: 0%� Share A: 99% Share B: 1%� ….

� Correlation is measured by correlation coefficient [-1;1]

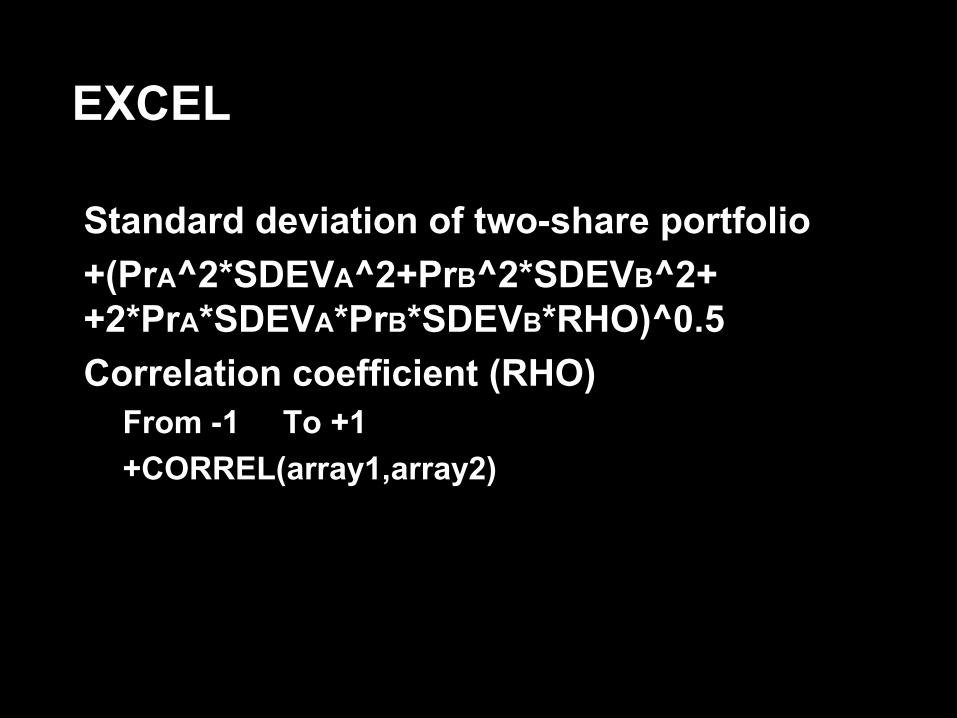

� EXCEL

EXCEL

� Standard deviation of two-share portfolio� +(PrA^2*SDEVA^2+PrB^2*SDEVB^2+

+2*PrA*SDEVA*PrB*SDEVB*RHO)^0.5� Correlation coefficient (RHO)

� From -1 To +1� +CORREL(array1,array2)

Portfolio risk

Depends on:� Proportion of funds invested in each asset� The risk associated with each asset in the

portfolio� The relationship between each asset in the

portfolio with respect to risk� No perfect negative correlation in real life

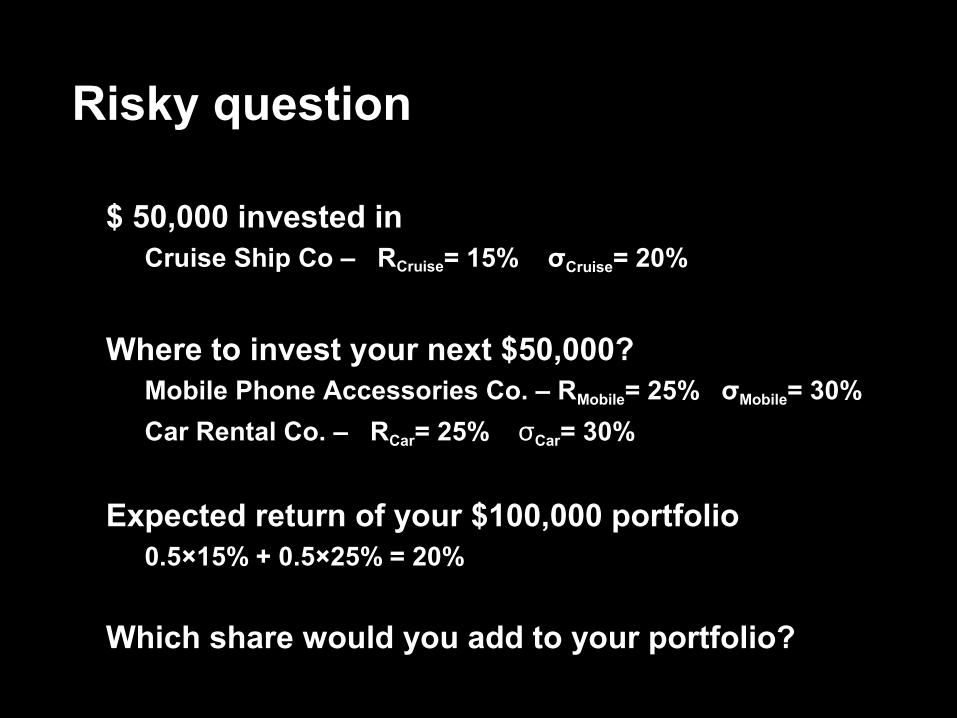

Risky question

� $ 50,000 invested in� Cruise Ship Co – RCruise= 15% σCruise= 20%

� Where to invest your next $50,000?� Mobile Phone Accessories Co. – RMobile= 25% σMobile= 30%� Car Rental Co. – RCar= 25% σσCar= 30%

� Expected return of your $100,000 portfolio � 0.5×15% + 0.5×25% = 20%

� Which share would you add to your portfolio?

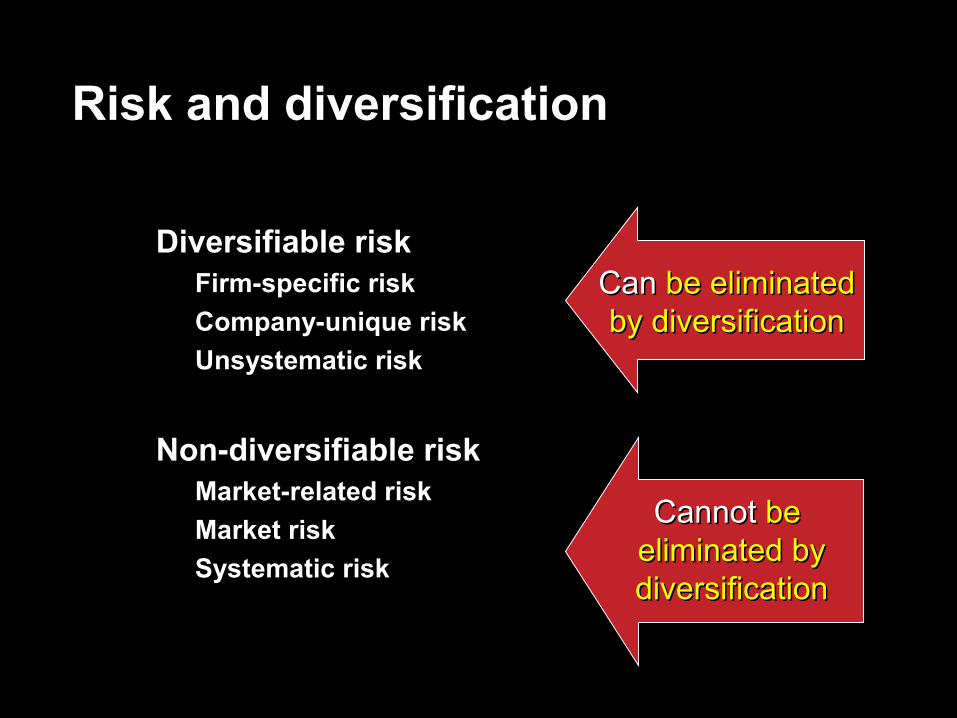

� Diversifiable risk� Firm-specific risk� Company-unique risk� Unsystematic risk

� Non-diversifiable risk� Market-related risk� Market risk� Systematic risk

CanCan be eliminated be eliminated by diversificationby diversification

CannotCannot be be eliminated by eliminated by diversificationdiversification

Risk and diversification

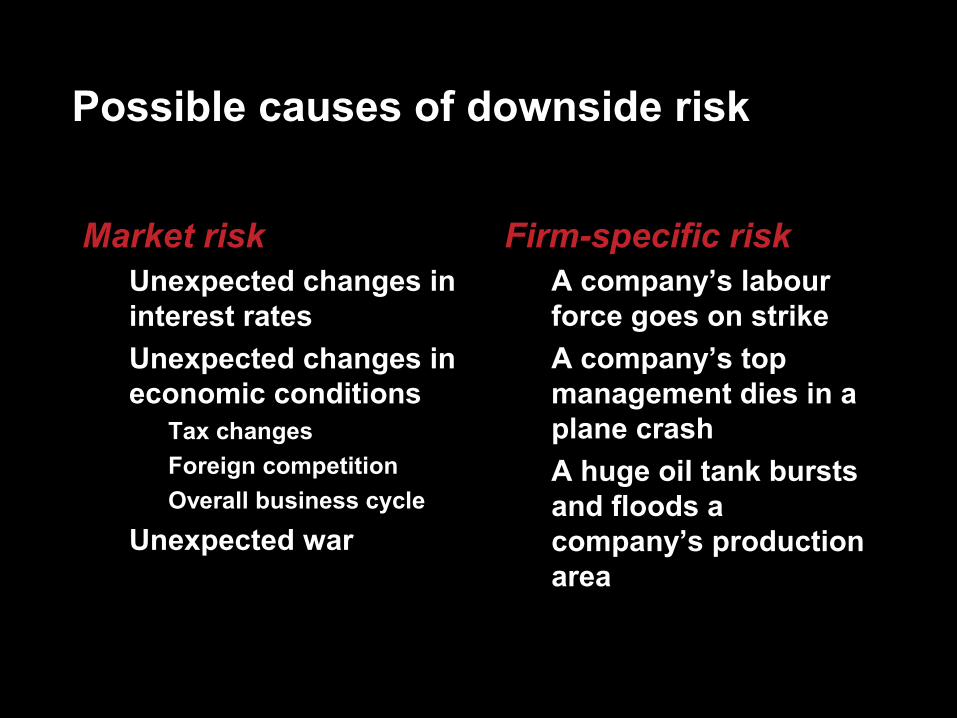

Market risk� Unexpected changes in

interest rates� Unexpected changes in

economic conditions� Tax changes� Foreign competition� Overall business cycle

� Unexpected war

Firm-specific risk� A company’s labour

force goes on strike� A company’s top

management dies in a plane crash

� A huge oil tank bursts and floods a company’s production area

Possible causes of downside risk

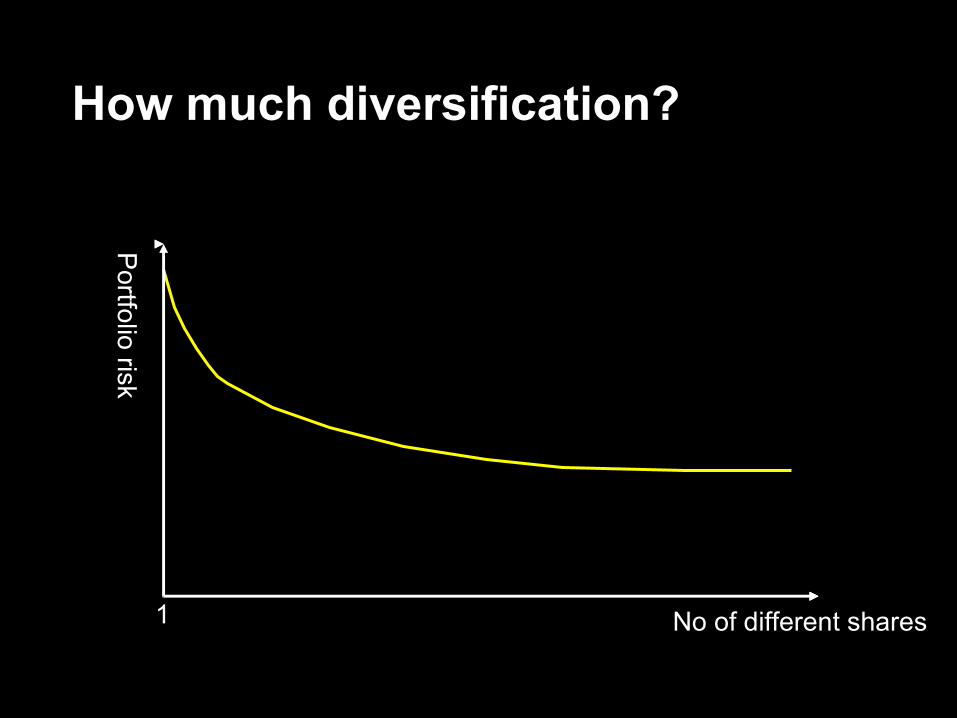

No of different sharesNo of different shares

Portfolio risk

Portfolio risk

11

How much diversification?

Nondiversifiable riskNondiversifiable risk

No of different sharesNo of different shares

Portfolio risk

Portfolio risk

11 3030

How much diversification?

Diversifiable riskDiversifiable risk

Nondiversifiable riskNondiversifiable risk

No of different sharesNo of different shares

Portfolio risk

Portfolio risk

11 3030

How much diversification?

Diversifiable riskDiversifiable risk

Nondiversifiable riskNondiversifiable risk

No of different sharesNo of different shares

Portfolio risk

Portfolio risk

11 3030

Almost all possible gains Almost all possible gains from diversification are from diversification are

achieved with a achieved with a carefully carefully chosenchosen portfolio of 30 portfolio of 30

sharesshares

How much diversification?

Do some firms Do some firms have more have more market risk market risk

than others?than others?

ExampleExampleInterest rate changesInterest rate changesaffect all firms, but which affect all firms, but which would be more affected:would be more affected:

a) Retail food chaina) Retail food chain b) Commercial bankb) Commercial bank

Level of market risk

Do some firms Do some firms have more have more market risk market risk

than others?than others?

YESYES

ExampleExampleInterest rate changesInterest rate changesaffect all firms, but which affect all firms, but which would be more affected:would be more affected:

a) Retail food chaina) Retail food chain b) Commercial bankb) Commercial bank

Level of market risk

Risk and return

� Investors are only compensated for accepting market risk

� Firm-specific risk should be diversified away

A need A need to to

measure measure market market

risk for a risk for a firmfirm

A measure of:

� How an individual share’s returns vary with market returns

� The “sensitivity” of an individual share’s returns to changes in the market

� For the market: Beta = 1Beta = 1� A firm with Beta =1Beta =1 has

average market risk. It has the same volatilitysame volatility as the market

� A firm with Beta > 1Beta > 1 is more volatilemore volatile than the market

� A firm with Beta < 1Beta < 1 is less volatileless volatile than the market

Beta: A measure of market risk

Calculating beta

MarketMarketindexindexreturnreturn(%)(%)

Company XYZ return (%)Company XYZ return (%)

Characteristic lineCharacteristic line Beta = slope of Beta = slope of characteristiccharacteristic

lineline

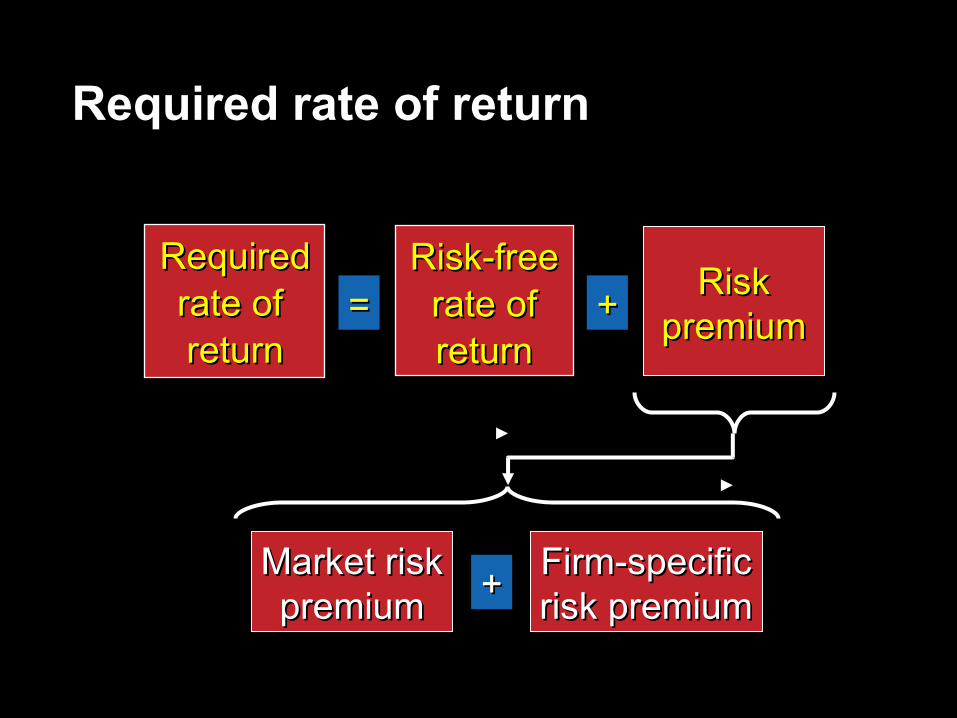

RequiredRequiredrate of rate of returnreturn

==Risk-freeRisk-free

rate ofrate ofreturnreturn

ReasonReason::Treasury securities are free of default riskTreasury securities are free of default risk

For a Treasury security, what is the required rate of return?

RequiredRequiredrate of rate of returnreturn

==Risk-freeRisk-free

rate ofrate ofreturnreturn

How large a risk premium should we How large a risk premium should we require to buy a corporate security?require to buy a corporate security?

++RiskRisk

premiumpremium

For a company security, what is the required rate of return?

RequiredRequiredrate of rate of returnreturn

==Risk-freeRisk-free

rate ofrate ofreturnreturn

++ RiskRiskpremiumpremium

++Market riskMarket riskpremiumpremium

Firm-specificFirm-specificrisk premiumrisk premium

Required rate of return

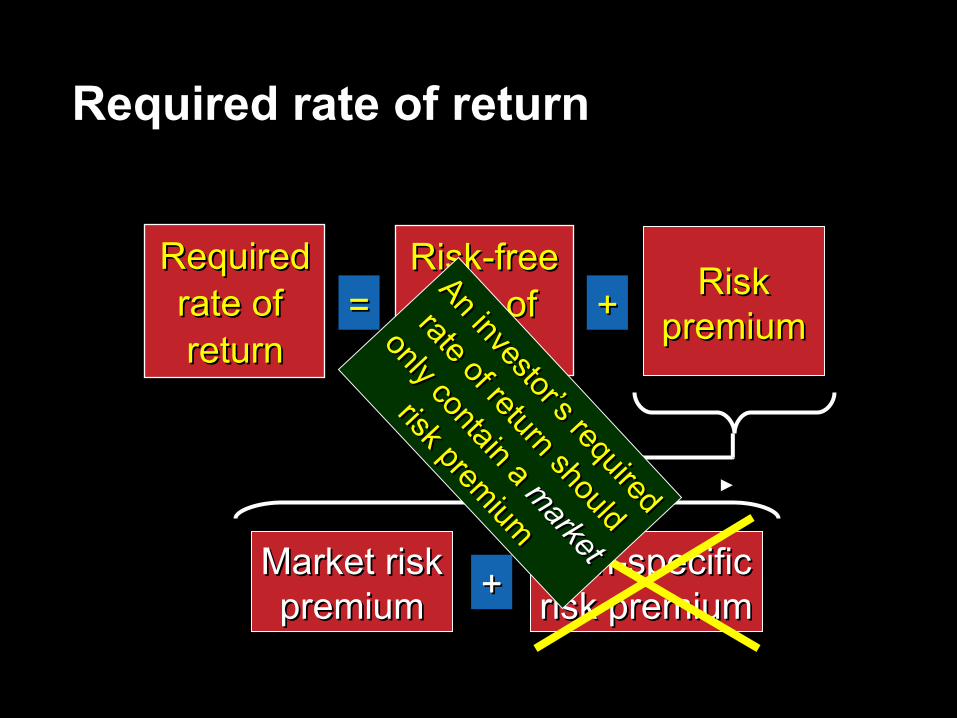

RequiredRequiredrate of rate of returnreturn

==Risk-freeRisk-free

rate ofrate ofreturnreturn

++ RiskRiskpremiumpremium

++Market riskMarket riskpremiumpremium

Firm-specificFirm-specificrisk premiumrisk premium

An investor’s required

An investor’s required

rate of return should

rate of return should

only contain a

only contain a market

market

risk premium

risk premium

Required rate of return

BetaBeta

RequiredRequiredrate ofrate ofreturnreturn

00 11

4%4%

11%11%MarketMarketreturnreturn

Risk-freeRisk-freerate ofrate ofreturnreturn

SMLSML

Known as theKnown as theCAPMCAPM

Graphing this relationship

RRjj = R = Rff + + ββjj ( R ( Rmm – R – Rff ) )

wherewhereRRjj = the required return on security j= the required return on security j

RRff = the risk-free rate of interest= the risk-free rate of interest

ββjj = the beta of security j= the beta of security j

RRmm = the return on the market index= the return on the market index

The CAPM equation

Assumptions

One investment periodRisk averse investorsMany risky assets and devisableRisk free rate is the same for each market playerNo tax and transaction costs involvedAll information is available for freeInvestors' expectations are homogenous

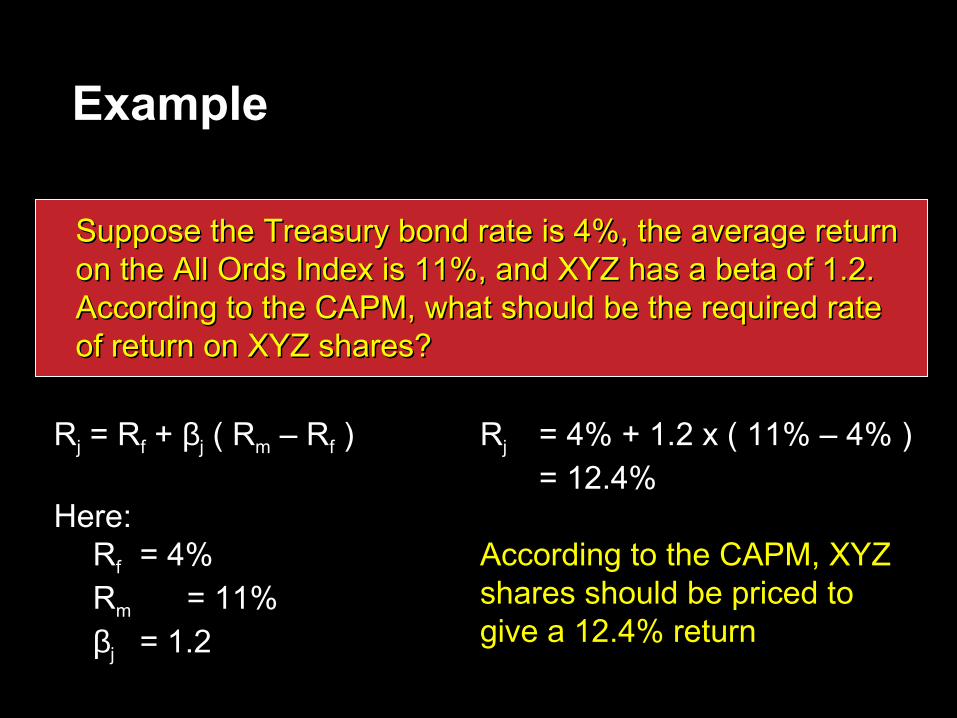

Example

Suppose the Treasury bond rate is 4%, the average return Suppose the Treasury bond rate is 4%, the average return on the All Ords Index is 11%, and XYZ has a beta of 1.2. on the All Ords Index is 11%, and XYZ has a beta of 1.2. According to the CAPM, what should be the required rate According to the CAPM, what should be the required rate of return on XYZ shares?of return on XYZ shares?

RRjj = R = Rff + + ββjj ( R ( Rmm – R – Rff ) )Here: Here:

RRff = 4%= 4%RRmm = 11%= 11%ββjj = 1.2= 1.2

Example

Suppose the Treasury bond rate is 4%, the average return Suppose the Treasury bond rate is 4%, the average return on the All Ords Index is 11%, and XYZ has a beta of 1.2. on the All Ords Index is 11%, and XYZ has a beta of 1.2. According to the CAPM, what should be the required rate According to the CAPM, what should be the required rate of return on XYZ shares?of return on XYZ shares?

RRjj = R = Rff + + ββjj ( R ( Rmm – R – Rff ) )

Here: Here: RRff = 4%= 4%RRmm = 11%= 11%ββjj = 1.2= 1.2

RRjj = 4= 4%% + 1.2 x ( 11 + 1.2 x ( 11%% – 4 – 4%% ) )= 12.4%= 12.4%

According to the CAPM, XYZ According to the CAPM, XYZ shares should be priced to shares should be priced to give a 12.4% returngive a 12.4% return

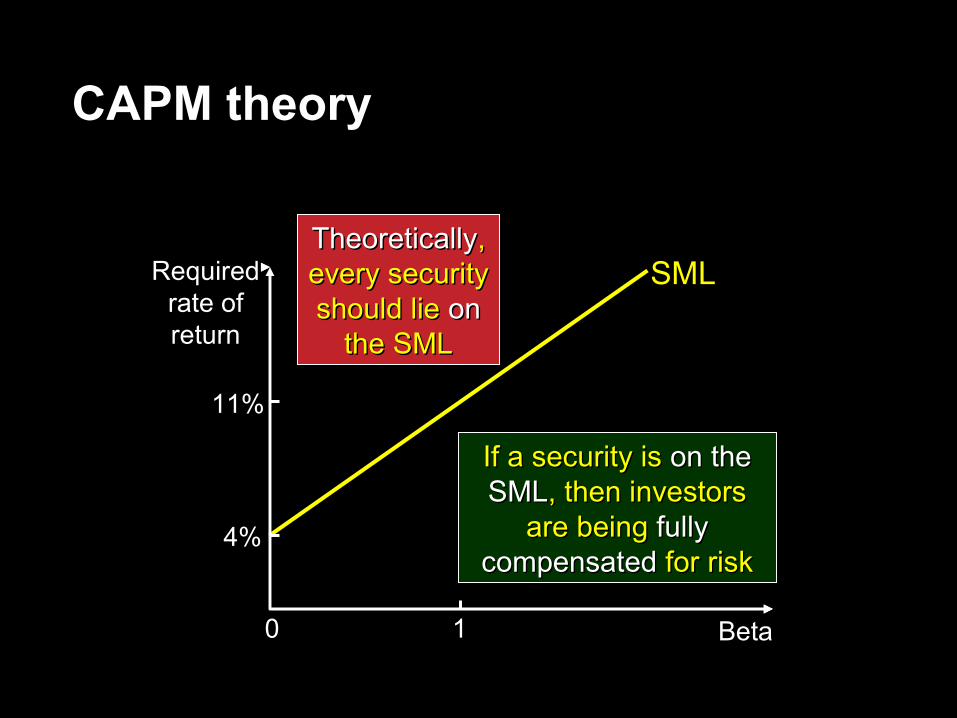

CAPM theory

BetaBeta

RequiredRequiredrate ofrate ofreturnreturn

00 11

4%4%

11%11%

SMLSMLTheoreticallyTheoretically, , every security every security should lie should lie onon

the SMLthe SML

If a security is If a security is on the on the SMLSML, then investors , then investors

are being are being fullyfully compensatedcompensated for risk for risk

CAPM theory

BetaBeta

RequiredRequiredrate ofrate ofreturnreturn

00 11

4%4%

11%11%

SMLSML

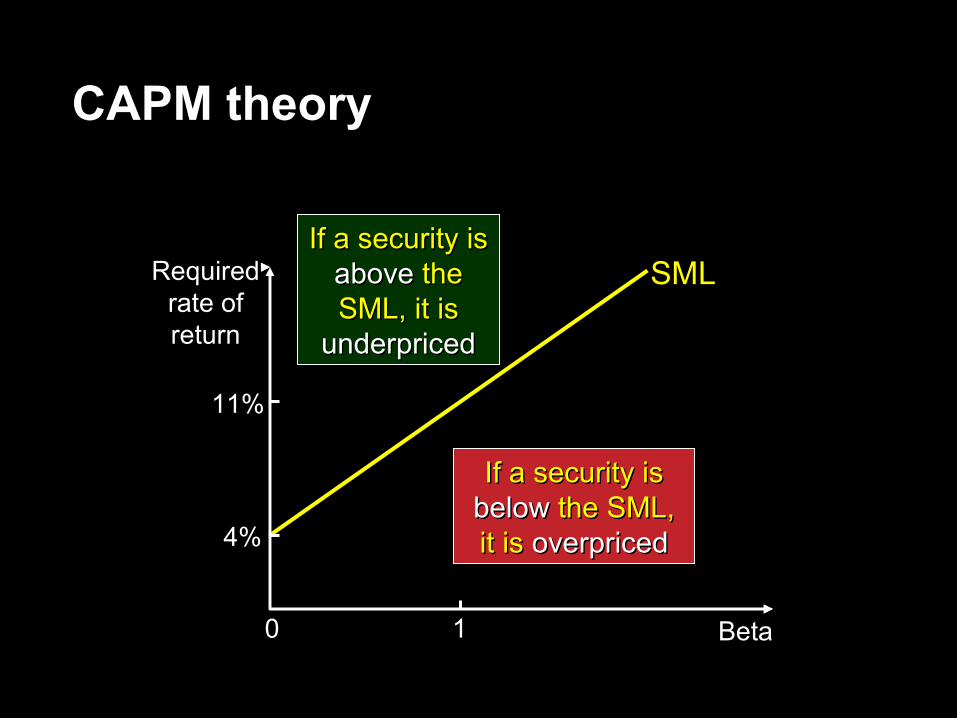

CAPM theory

BetaBeta

RequiredRequiredrate ofrate ofreturnreturn

00 11

4%4%

11%11%

SMLSMLIf a security is If a security is

aboveabove the the SML, it is SML, it is

underpricedunderpriced

If a security is If a security is belowbelow the SML, the SML, it is it is overpricedoverpriced

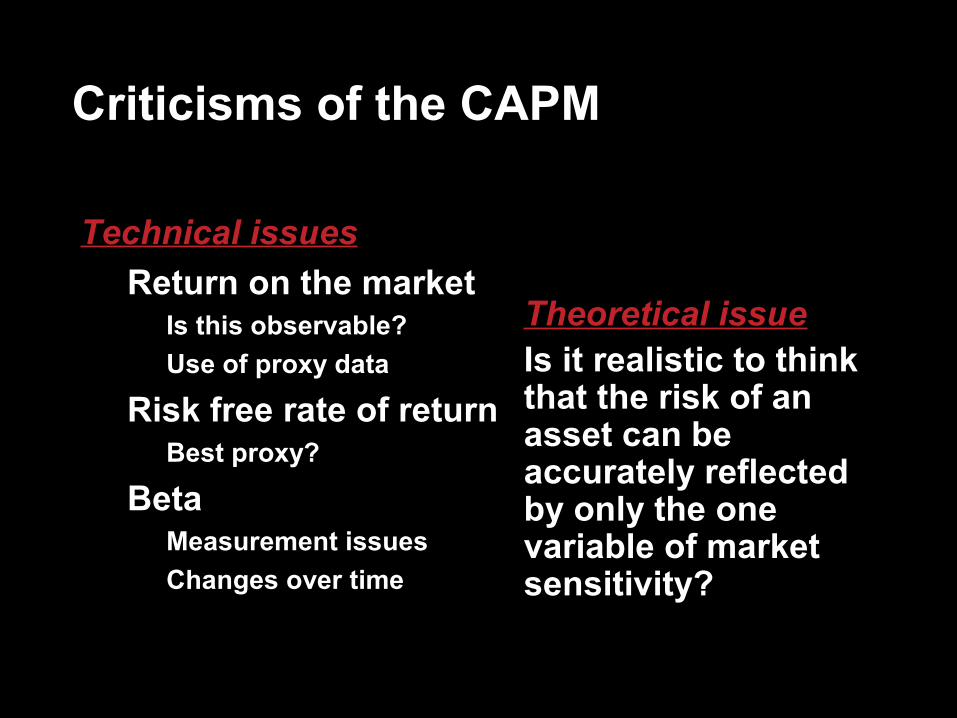

Theoretical issueIs it realistic to think that the risk of an asset can be accurately reflected by only the one variable of market sensitivity?

Technical issues� Return on the market

� Is this observable?� Use of proxy data

� Risk free rate of return� Best proxy?

� Beta� Measurement issues� Changes over time

Criticisms of the CAPM

Theoretical issueIs it realistic to think that the risk of an asset can be accurately reflected by only the one variable of market sensitivity?

Technical issues� Return on the market

� Is this observable?� Use of proxy data

� Risk free rate of return� Best proxy?

� Beta� Measurement issues� Changes over time

AA widely used

widely used

and important

and important

tooltool

Criticisms of the CAPM