presentation by the eu delegation to south africa at the

TRANSCRIPT

Presentation by the EU Delegation to South Africaat the Portfolio Committee

on Trade and Industry

"Challenges facing the poultry industry"

Cape Town, 2 May 2017

EU-SA TRADE RELATIONSHIP – AN OVERVIEW

� South Africa is among the few strategic partners of the EUworldwide – in 2017 we mark 10 years of our strategicpartnership. SA is an important regional and global partner

� South Africa is the EU's largest trading partner in Africa. TheEU is a major contributor of FDI for SA

� South Africa's trade relations and development co-operation withthe EU are governed by the Trade, Development and Co-operation Agreement (TDCA) and the EU-SADC EconomicPartnership Agreement (EPA)

� EU–SADC EPA entered into force on 10 October 2016 and newagriculture market access kicked in on 1 November (GInotifications)

� The trade provisions of TDCA are replaced by EU–SADC EPA

2

EU-SADC EPA – SOUTH AFRICA PERSPECTIVE

� Improved market access – agri-food sector in particular

� Regional integration

� Eliminate all export subsidies

� New rules of origin

� More effective (agriculture) safeguards

� Bilateral protocol on GIs and trade in wine and spirits

� Policy aspects: SPS, TBT and transformation

� Special provisions on cooperation on SPS

3

EU-SA TRADE - 10 YEAR EVOLUTION

4

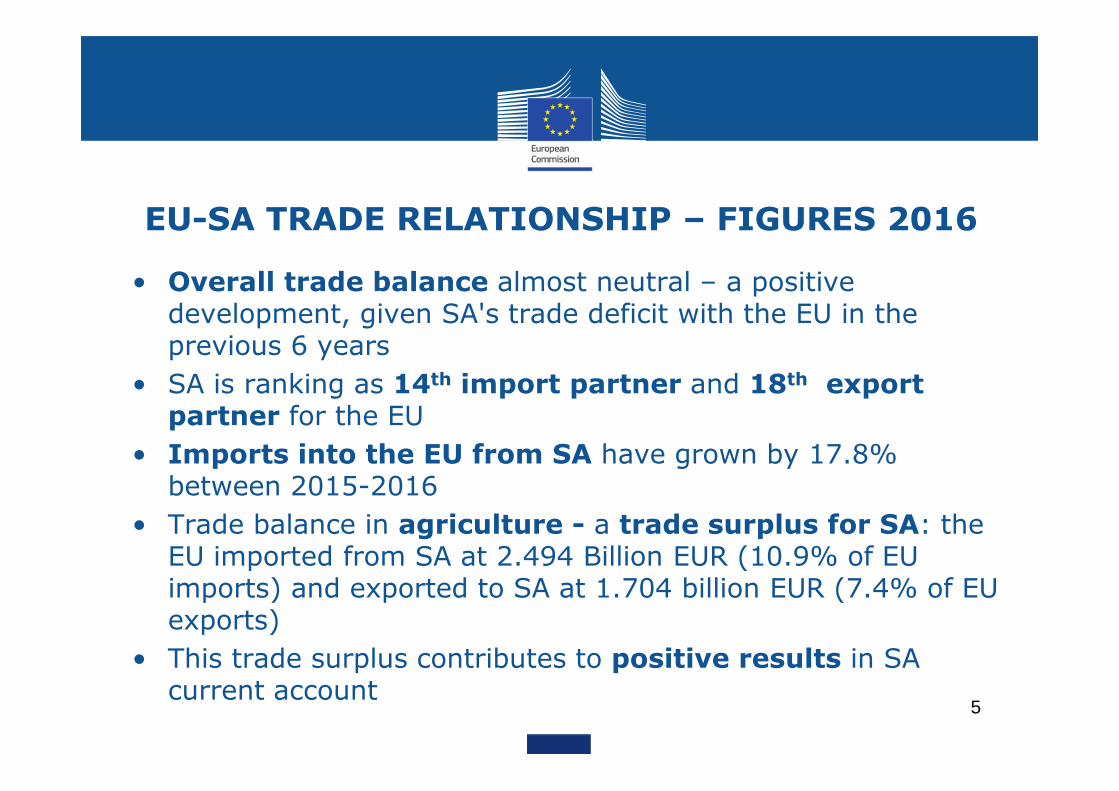

EU-SA TRADE RELATIONSHIP – FIGURES 2016

• Overall trade balance almost neutral – a positive development, given SA's trade deficit with the EU in the previous 6 years

• SA is ranking as 14th import partner and 18th export partner for the EU

• Imports into the EU from SA have grown by 17.8% between 2015-2016

• Trade balance in agriculture - a trade surplus for SA: the EU imported from SA at 2.494 Billion EUR (10.9% of EU imports) and exported to SA at 1.704 billion EUR (7.4% of EU exports)

• This trade surplus contributes to positive results in SA current account

5

6

EU POULTRY EXPORTS - OVERALL

7

FROZEN BONE-IN CHICKEN CUT IMPORTS INTO SA BY EU ('000 T)

8

EU POULTRY IMPORTS INTO SA cont.

• Since December 2016 – sharp decrease in EU imports

• Overall, EU imports' share in domestic SA poultry consumption has not exceeded 10% in 2016

• According to Country Bird, imports account for 26% of SA poultry consumption – less than 1/3 of market

• This is against a background of growing poultry consumption and demand globally (Econex)

• Consumption of white meat expected to expand by 34% by 2023 – need to supplement domestic supply by imports

• Domestic supply not enough – EU imports replaced by USA/BZ imports

9

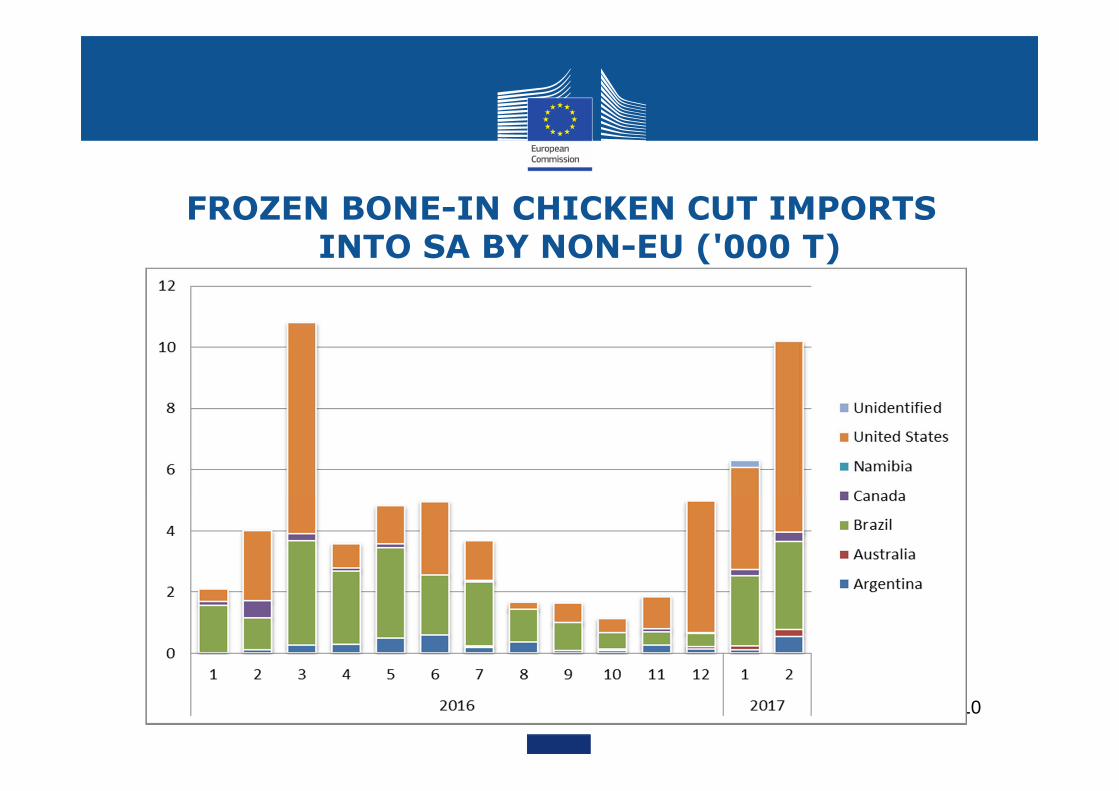

FROZEN BONE-IN CHICKEN CUT IMPORTS INTO SA BY NON-EU ('000 T)

10

SA POULTRY INDUSTRY CHALLENGES

• Challenges similar to the ones faced by EU poultry industry: high and volatile feed costs, changing demand patterns, need to adapt the value chains to fit new market reality and to optimise efficiency of the whole value chain

• Challenges different from those faced by the EU industry: costs of electricity, fluctuating Rand, oligopolistic character of the national market with vertical integration with an inherent interest to maintain profit margins and resist change

• The whole bird versus cuts myth – an artificial issue. Markets determine business and pricing models

• All poultry producers in the EU adapt to demand and try to sell to markets where they can maximise price for the same product –normal competitive behaviour:

11

OPTIMISING VALUE CHAINS AND BUSINESS MODELS

12

TRADE DEFENCE AND SPS MEASURES

• DTI has decided on a number of trade defence measures

• Anti-dumping duties on companies from DE, NL and UK

• Provisional safeguard duty of 13.9% under EPA

• ITAC investigation ongoing – EU submissions

• SPS measures - country-wide bans after the outbreak of HPAI in many EU Member States since last November

• Currently, only 3 out of 10 EU countries can still import

• Ongoing regionalisation discussions with DAFF

13

NO TRASH, NO DUMPING, NO BRINING, NO SUBSIDIES

� EU poultry imported into SA of the same high quality as that sold in the EU. EU food law and regulations impose high standards

� Dietary preferences important but change – markets change

� EU prices are consistently above those of other big importers – the US and Brazil

� Brining in the EU – if a poultry product is brined, it cannot be sold or exported as fresh/frozen meat but under a label "poultry preparation"

� EU does not subsidize either production or exports

14

PRICE COMPETITION

15

POULTRY IMPORTS INTO THE EU

16

Compared

tonnes % tonnes % tonnes % tonnes % tonnes % to Jan-Dec 15

Brazil 570 574 66.7% 506 374 62.7% 507 355 60.0% 498 869 57.2% 502 805 55.9% + 0%

Thailand 197 962 23.2% 228 238 28.3% 251 185 29.7% 274 507 31.5% 289 461 32.2% + 6%

Ukraine 276 0.0% 19 958 2.4% 42 412 4.9% 48 039 5.3% + 13%

Chile 42 192 4.9% 30 515 3.8% 25 815 3.1% 22 232 2.5% 28 875 3.2% + 30%

China 15 698 1.8% 18 145 2.2% 19 761 2.3% 18 396 2.1% 16 929 1.9% - 8%

Argentina 13 766 1.6% 10 783 1.3% 10 996 1.3% 8 529 1.0% 6 463 0.7% - 24%

Switzerland 3 812 0.4% 3 817 0.5% 4 307 0.5% 2 428 0.3% 2 542 0.3% + 5%

Israel 6 075 0.7% 6 306 0.8% 2 411 0.3% 1 285 0.1% 1 488 0.2% + 16%

Others 4 969 0.6% 2 820 0.3% 3 956 0.5% 3 697 0.4% 2 583 0.3% #N/A

Extra-EU 855 048 807 274 845 743 872 356 899 183

% change - 5.6% + 4.8% + 3.1% + 2.8%

2012 2013 2014 Jan-Dec 162015

POULTRY IMPORTS INTO THE EU

� DAFF letter requesting market access for SA poultry received on 11 April 2017 – reference to EU Ambassador meeting in February with Ministers Davis and Zokwana

� DAFF indicate that SA has already started preparing on basis of the ratite audit recommendations of June 2016

� No market barriers. Duty-free/quota-free under EPA

� Food safety/animal health (SPS) rules apply

� Residue and public health audits in February 2017 - problems with SA laboratories and official controls system – serious state veterinary understaffing - raised back in 2007/2008 audits!

� Need to manage exposure to prohibited medicines and growth hormones – future VPN on a split system. National priority to address – for all commodities!

� Importance of B2B/industry – SAPA and AVEC cooperation

17

CONCLUSIONS

• The EU has been and remains a reliable, trustworthy trading partner for SA

• The trade partnership has been mutually beneficial and is a relationship among equals - we engage in good faith

• The SA poultry industry challenges were obviated by the temporary raise in imports last year – but they are of a structural character. We welcome the SA government Poultry Task Team and its comprehensive approach

• We do and will cooperate in all ITAC investigations

• The EU-SA strategic partnership and the EPA are too important to be allowed to fail – mutually beneficial trade contributes to both SA and EU job creation and economic growth

18

Thank you for your attention

Dessislava Choumelova

Trade and Economics Counsellor

EU Delegation to South Africa

Dessislava@[email protected]

EU Delegation to South Africa

http://eeas.europa.eu/delegations/south_africa

Twitter: @EUinSA; #SA_EUtalk

19