presentation - macquarie bank

TRANSCRIPT

Macquarie Group Limited

Presentation to Investors and Analysts

18-22 March 2013

Patrick Upfold, Chief Financial Officer

Stuart Green, Head of Corporate Communications and Investor Relations

Credit Suisse 16th Asian Investment Conference

Conrad Hotel, Hong Kong

2

Disclaimer This information has been prepared on a strictly confidential basis by Macquarie Group Limited ABN 94 122 169 279 (“Macquarie”) and may neither be reproduced in whole nor in part, nor may any of its contents be

divulged to any third party without the prior written consent of Macquarie. Other than Macquarie Bank Limited ABN 46 008 583 542 (Macquarie), any Macquarie group entity noted in this document is not an authorised

deposit-taking institution for the purposes of the Banking Act 1959 (Commonwealth of Australia). That entity‟s obligations do not represent deposits or other liabilities of Macquarie and Macquarie does not guarantee or

otherwise provide assurance in respect of the obligations of that entity, unless noted otherwise. This information is not intended to create legal relations and is not binding on Macquarie under any circumstances

whatsoever. This information has been prepared in good faith and is based on information obtained from sources believed to be reliable, however Macquarie does not make any representation or warranty that it is

accurate, complete or up to date. The information may be based on certain assumptions or market conditions, and if those assumptions or market conditions change, the information may change. No independent

verification of the information has been made. Any quotes given are indicative only. No part of this information is to be construed as a solicitation to buy or sell any product, or to engage in, or refrain from engaging in, any

transaction.

To the extent permitted by law, neither Macquarie nor its related bodies corporate (the “Macquarie Group”) nor any of its associates, directors, officers or employees, or any other person, makes any promise, guarantee,

representation or warranty (express or implied) to any person as to the accuracy or completeness of this information, or of any other information, materials or opinions, whether written or oral, that have been, or may be,

prepared or furnished by Macquarie Group, including, without limitation, economic and financial projections and risk evaluation. No responsibility or liability whatsoever (in negligence or otherwise) is accepted by any

person for any errors, mis-statements or omissions in this information or any other information or materials. Without prejudice to the foregoing, neither the Macquarie Group, nor any of its associates, directors, officers,

employees nor any other person shall be liable for any loss or damage (whether direct, indirect or consequential) suffered by any person as a result of relying on any statement in or omission from this information. Nothing

in this information should be construed as legal, financial, accounting, tax or other advice.

The Macquarie Group or its associates, directors, officers or employees may have interests in the financial products referred to in this information by acting in various roles including as provider of corporate finance,

underwriter or dealer, holder of principal positions, broker, lender or adviser and may receive fees, brokerage or commissions for acting in those capacities. In addition, the Macquarie Group and its associates, directors,

officers or employees may buy or sell the financial products as principal or agent and as such may effect transactions which are not consistent with any recommendations in this information.

Unless otherwise specified all information is for the half year ended 30 September 2012.

Certain financial information in this presentation is prepared on a different basis to the Macquarie Group Limited Financial Report, which is prepared in accordance with Australian Accounting Standards. Where financial

information presented within this presentation does not comply with Australian Accounting Standards, a reconciliation to the statutory information is provided.

This presentation provides further detail in relation to key elements of Macquarie Group Limited‟s financial performance and financial position. It also provides an analysis of the funding profile of the

Group because maintaining the structural integrity of the Group's balance sheet requires active management of both asset and liability portfolios. Active management of the funded balance sheet enables the Group to

strengthen its liquidity and funding position.

This presentation may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to Macquarie‟s businesses and operations, market conditions, results of

operation and financial condition, capital adequacy, specific provisions and risk management practices. Readers are cautioned not to place undue reliance on these forward looking statements. Macquarie does not

undertake any obligation to publicly release the result of any revisions to these forward looking statements to reflect events or circumstances after the date hereof to reflect the occurrence of unanticipated events. While due

care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside

Macquarie‟s control. Past performance is not a reliable indication of future performance.

Any additional financial information in this presentation which is not included in the Macquarie Group Limited Financial Report was not subject to independent audit or review by PricewaterhouseCoopers

3

Agenda

1. Overview

2. 3Q13 Update and Outlook

3. 1H13 Results

4. Appendix

5. Contacts

4

Overview 1 Macquarie Group Limited Presentation to Investors and Analysts March 2013

5

About Macquarie

Global provider of banking, financial, advisory, investment and funds management services

Main business focus is providing products and services to clients

Listed on Australian Securities Exchange (ASX: MQG; ADR: MQBKY)

Regulated by APRA, Australian banking regulator, as non-operating holding company of a licensed Australian bank

Assets under management $A341b1

Founded in 1969, currently operates in 28 countries and employs 13,5492 people

1. 30 Sep 12 2. 31 Dec 12

Macquarie Group Limited Macquarie Bank Limited

Short-term

rating

Long-term

rating

Long-term

rating outlook

Short-term

rating

Long-term

rating

Long-term

rating outlook

Fitch Ratings F-2 A- Stable F-1 A Stable

Moody’s P-2 A3 Stable P-1 A2 Stable

Standard and Poor’s A-2 BBB Stable A-1 A Stable

For further information on Macquarie, visit www.macquarie.com/mgl/com/investor-relations

6

Macquarie has a long history of profitability

0.0 0.4 0.8 1.2 1.6 2.0

1969 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979

Hill Samuel UK

opens branch

office in Sydney

Currency

Crisis

Recession

0

20

40

60

80

100

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995

Savings and

loan crisis

US banks

capital losses

Global debt

crisis US

recession $A floated

MBL

established

First listed

property trust

Enter

stockbroking

Stock

market

crash

London office

opens

Hills Motorway

Mortgage

securitisation Global real

estate crash Recession

0

500

1000

1500

2000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 1H13

Orion Securities

CIT Systems Leasing

Group Restructure

Significant Market Disruption

MBL

listed BT

Australia

acquired

Sydney

Airport

ING

Acquired Asian

Financial

Crisis

Russian

Debt

Crisis

Dot

Com

crash

9/11

US

Recession SARS

Thames Water

Giuliani Capital GFC

Constellation

Tristone

Delaware

FPK

Blackmont

Sal Opp.

ILFC

GMAC

Presidio

Innovest

REGAL Onstream

7

About Macquarie Macquarie Funds Group

1. Data as at 30 Sep 12. 2. Based on the amount of infrastructure direct investment capital formed in the last five years. 3. AsianInvestor 2012 Investment Performance Awards for institutional funds management. 4. The award, based in Hong Kong, assesses

funds that primarily sell into the Asian region and is judged on nominal and risk-adjusted performance over one, three and five year periods. 5. Financial Review Smart Investor Blue Ribbon Awards 2012

Provides clients with access to a

diverse range of capabilities and

products, including:

– Infrastructure and real asset

management

– Securities investment management

– Fund and equity-based solutions

Top 50 global asset manager with $337b1 of assets under management

Ranked 1st in Infrastructure Investor

magazine‟s list of top

infrastructure investors2 for

the third consecutive year

Macquarie Enhanced Global

Bond Fund was recognised

by AsianInvestor as the best

Global Fixed Income

Fund (Hedged)4

“Best Infrastructure”

and

“Best Real Estate” Fund Manager House Awards

for 2012 by AsianInvestor3

Macquarie

Investment

Management

Macquarie

Infrastructure

and Real Assets

Macquarie

Specialised

Investment

Solutions

AUM: $A229b1

AUM: $A106b1 AUM: $A2b1

Macquarie Funds Group

Best Diversified

Credit/Multi-Strategy

Income Fund

Macquarie Income

Opportunities Fund5

8

0

50

100

150

200

250

300

350

400

Mar 09 Mar 10 Mar 11 Mar 12 Sep 12

Fixed income Direct infrastructure

Equities Cash

Direct real estate Currency

Other

Assets under management of $A341b

AUM increased $A13.6b or 4% since 31 Mar 12, primarily driven by positive market and valuation

movements and investments in the infrastructure and real assets business

$A243b

$A326b $A310b

$A327b $A341b

$Ab

Data as at 30 Sep 12

9

About Macquarie Corporate and Asset Finance

Aircraft

Portfolio: $A3.2b1

Equipment

Finance

Portfolio: $A1.9b1

Meters

Portfolio: $A0.7b1

Motor Vehicles

Portfolio: $A6.7b1

Mining Equipment

Portfolio: $A0.4b1

Lending

Portfolio: $A8.1b1

Corporate and

Asset Finance

Rail

Portfolio: $A0.4b1

One of the

largest providers of motor

vehicle finance in

Australia

Provider of tailored finance and asset management

solutions to clients across specialised assets

through the cycles

– Niche positions in deep, attractive markets

– Origination through the cycles

– Strong credit and asset discipline

– Strong funder and investor demand for assets

– Cost management and returns focus

– Successfully converted opportunities during

cycles

Expertise in corporate debt and asset finance

including: aircraft, motor vehicles, technology,

healthcare, manufacturing, industrial, energy, rail

and mining equipment

One of North

America‟s

largest

independent lessors

of technology

equipment

Portfolio

diversified by geography, assets,

industries, product

types, exposures and

clients

$A21.4b1 of loans and assets under finance

1. Data as at 30 Sep 12.

10 1. Data as at 30 Sep 12 2. IRESS: consideration traded and volume 30 Sep 12. 3. Investment Executive Brokerage Report Card 2012 (Canada) 4. Fairfax Blue Ribbon Smart Investor Awards 2012 5. Money Magazine 2012 Best of the Best Awards‟

Cheapest Flexible Home Loan for Classic P&L Home Loan.

~1.1 million high net worth clients serviced by

625 Macquarie client advisers and our

Independent Financial Adviser partners

Leading provider of retail advisory services

and products

Extensive platform support services to

intermediaries in Australia

Specialist Relationship Banking provider to

Small to Medium Enterprises (SME)

$A30.8b1 retail on-balance sheet cash

Banking and

Financial

Services

About Macquarie Banking and Financial Services

No.1 full-service

Australian retail

stockbroker in terms of

volume and market

share2

Macquarie Super and

Pension Consolidator named

Super Platform of

the Year4

No.1 National

Independent Canadian

Advisory firm3

Macquarie Mortgages

awarded Money

Magazine‟s 2012 Best of

the Best awards5

Mortgages

Relationship

banking Financial advice

services

Cash Wrap

Insurance

11

About Macquarie Macquarie Securities Group

1. Peter Lee Associates Survey of Asian/Australian Institutional Investors – Australian Equities. 2. Greenwich Survey of US Institutional Investors – Australian Equities and Greenwich Survey of European Institutional Investors – Australian

Equities. 3. Abel Nosser 2012. 4. Bloomberg league tables 1 Jan – 30 Sep 12. 5. Local exchanges.

Global institutional securities house with

strong Asia-Pacific foundations covering

sales, research, ECM, execution and

derivatives activities

Full-service cash equities in Australia, Asia,

South Africa and Canada with offerings in US

and Europe. Specialised derivatives in key

locations globally

Key specialities: infrastructure and utilities,

TMET, resources (mining and energy),

industrials and financial institutions

Macquarie

Securities

Group

Research

Corporate

Access

Derivatives Arbitrage

Execution

Equity capital

markets

Equity finance

210+ equity research

analysts

2,215+ stocks under coverage

25+ years Knowledge and

experience in

Asia-Pacific

No.1 in Asia1,

US and Europe2, and

No.2 in Australia1

for Australian equities

No.1 warrants market

share Singapore5

No.3 in Australia5&

No.5 HK5

No.1 Execution

Quality Asia-Pacific3

No.3 Australian

ECM4

12

About Macquarie Macquarie Capital Group

1. 2012 Capital/CFO Awards. 2 Announced deals by value, any involvement, Bloomberg 1Jan – 30 Sep 12. 3. Completed Equity, Equity-linked & Pfd deals by value, Bloomberg 1 Jan- 30 Sep 12. 4. International M&A Advisor Awards (for deals between

$1-3b) 5. EMEA Finance. 6. Infrastructure Journal, Jan-Jun 12. 7. (Downtown Tunnel/Midtown Tunnel/MLK Extension Project) Global Finance Magazine.

Global corporate finance capability,

including M&A, capital markets and

principal investments

Key specialities: infrastructure, utilities

and renewables; resources (mining

and energy); real estate; TMET;

industrials and financial institutions

Winner of over 20 awards globally in

2012, including Best Investment Bank

(Australia) and Best Equity House

(Australia)1

FINANCIAL INSTITUTIONS

INDUSTRIALS

INFRASTRUCTURE, UTILITIES

& RENEWABLES

REAL ESTATE

RESOURCES

TELECOMMUNICATIONS, MEDIA

ENTERTAINMENT & TECHNOLOGY ME

RG

ER

S &

AC

QU

ISIT

ION

S

PR

OJ

EC

T F

INA

NC

E

EQ

UIT

Y C

AP

ITA

L M

AR

KE

TS

DE

BT

CA

PIT

AL

MA

RK

ET

S

PR

IVA

TE

CA

PIT

AL

MA

RK

ET

S

PR

INC

IPA

L I

NV

ES

TM

EN

TS

No.1 ANZ M&A2

No. 3 ANZ ECM3

M&A Deal of

the Year (Tokio

Marine/Delphi

Financial Group)4

No.1 Financial Adviser for

Project Finance

Deals (Americas)6

Best PPP

EMEA Deal of

the Year (Muharraq STP)5

Best Project &

Infrastructure

Finance

Sponsor (Global)7

13 1. Percentages are based on operating income before impairment charges on investment securities available for sale and associates and joint ventures. 2. Platts, June 12.

Global fixed income, currencies and

commodities provider of finance, risk solutions

and market access to producers/consumers

and financial institutions/investors

Approx. 60% of operating income1 for the 12

months to 30 Sep 2012 from Commodity

markets

Growing presence in physical commodities

(natural gas, LNG, power, oil, coal, base

metals, iron ore, sugar and freight)

Predominant in US and Australia, niche

offering in Canada and Latin America, growing

presence in Asia and EMEA

Specialties: commodities, Asian and emerging

markets, high yield and distressed debt

FICC

About Macquarie Fixed Income, Currencies and Commodities

A portfolio of businesses across Commodity and Financial markets

Specialist provider of FX

transactional

services

20+ years actively trading

in global

agricultural

markets

30+ years in metals markets

and as a global

full service

futures broker

10+ years in global

energy markets -

No.4 physical gas

marketer in North

America2

Energy markets

Metals markets

Futures

Environmental financial

products

Asian and

emerging markets

Fixed income,

currency and

credit markets

Agricultural

markets

Metals and

energy capital

14

Macquarie‟s risk management principles have remained largely stable over 30 years and served the Group well over the past few years

The key aspects of Macquarie‟s risk management approach are:

Macquarie‟s approach to risk is supported by the Risk Management Group

Macquarie determines aggregate risk appetite by assessing risk relative to earnings, more than by reference to capital

Business heads responsible for

identifying risks within their

businesses and ensuring these are

managed appropriately.

Seek a clear analysis of the risks

before taking decisions.

Risk management approach based

on examining the consequences of

worst case outcomes and

determining whether risks can be

tolerated.

Adopted for all material risk types and

often achieved by stress testing.

Risk Management Group (RMG) signs

off all material risk acceptance decisions.

For material proposals, RMG opinion

sought at the early stage in decision

making process, and independent input

from RMG on risk and return is included

in the approval document submitted to

senior management.

Ownership of risk at the business

level

Understanding worst case

outcomes

Requirement for independent

sign-off by Risk Management

Long standing conservative Risk Management

15

3Q13 Update and Outlook 2 Macquarie Group Limited Presentation to Investors and Analysts March 2013

16

Since our 1H13 result announcement, market conditions have shown some signs of improvement, however client activity remains

subdued for capital markets facing businesses

Macquarie‟s annuity-style businesses (Macquarie Funds, Banking and Financial Services and Corporate and Asset Finance) continue

to perform well with combined Dec 12 qtr net profit contribution1 up on pcp (Dec 11 qtr) and the prior period (Sep 12 qtr)

Whilst Macquarie‟s capital markets facing businesses (FICC, Macquarie Securities Group and Macquarie Capital) continued to face

subdued market conditions, combined Dec 12 qtr net profit contribution1 was up strongly on both weak pcp and prior period

Macquarie Securities: Cash equities business remains marginally profitable and legacy expenses continuing to decline

Macquarie Capital: Overall deal activity was up on both weak pcp and prior period, although ECM levels remain low, particularly

in Asia and Australia

FICC: Continued good performance from Energy Markets and Credit Trading, however Metals & Energy Capital and Metals &

Agriculture Sales and Trading continue to be impacted by market conditions

Benefits from operating efficiencies continue with Dec 12 qtr operating expenses down approx. 10% on pcp

3Q13 Overview

1. Net Profit Contribution is operating income less operating expenses and is reported before profit share and income tax.

17

FY13 outlook

Summarised below are the outlook statements for each Operating Group

FY13 results will vary with market conditions, particularly the capital markets facing businesses which

continue to experience subdued market conditions

1. Range excludes FY09 provisions for loan losses of $A135m related to Real Estate Structured Finance loans as this is a restructured business. 2. Range excludes FY09 loss on sale of Italian mortgages of $A248m as this is a discontinued business.

Net profit contribution

Operating Group FY07- FY12

historical range FY07-FY12

average FY12 FY13 outlook as updated in Oct 12 Update to FY13 outlook

Macquarie Funds $A0.3b – $A1.1b $A0.7b $A0.7b Up on FY12 No change

Corporate and Asset Finance $A0.1b – $A0.7b1 $A0.3b $A0.7b Broadly in line with FY12 No change

Banking and Financial Services $A0.1b – $A0.3b2 $A0.2b $A0.3b Up on FY12 No change

Macquarie Securities $A(0.2)b – $A1.2b $A0.5b $A(0.2)b Up on FY12 but unlikely to be profitable if current markets persist

No change

Macquarie Capital $A(0.1)b – $A1.6b $A0.6b $A0.1b Up on FY12 No change

FICC $A0.5b – $A0.8b $A0.6b $A0.5b Up on FY12 Broadly in line

Corporate

– Compensation ratio to be consistent with historical levels

– Continued higher cost of funding reflecting market conditions and high liquidity levels

No change No change

18

FY13 outlook

Subject to market conditions, FY13 net profit contribution from operating groups expected to be materially

up on FY12

FY13 contribution from Corporate expected to be down on FY12 due to the net impact of a number of

items including the receipt of $A295m from Sydney Airport in FY12

Tax rate is expected to increase from 28% in FY12 to over 30% for FY13 due to the ongoing strength of

US businesses and weakness in Asian capital markets facing businesses

Whilst market conditions remain uncertain, we currently expect Macquarie‟s result for FY13 to be up

approx. 10% on FY12 with the probability of a stronger result should improved market conditions persist

The FY13 result remains subject to market conditions, completion rate of transactions and impairment

testing as well as a range of other factors including

the cost of our continued conservative approach to funding and capital

regulation, including the potential for regulatory changes

increased competition in some markets

the overall cost of funding

19

EUROPE, MIDDLE EAST

& AFRICA2

Staff: 1,184

ASIA

Staff: 2,945

AMERICAS

Staff: 3,267

AUSTRALIA3

Staff: 6,153

13,5491 staff in over 28 countries

1. Staff numbers as at 31 Dec 12. 2. Excludes staff in Macquarie First South joint venture and staff seconded to Macquarie Renaissance joint venture (Moscow). 3. Includes New Zealand.

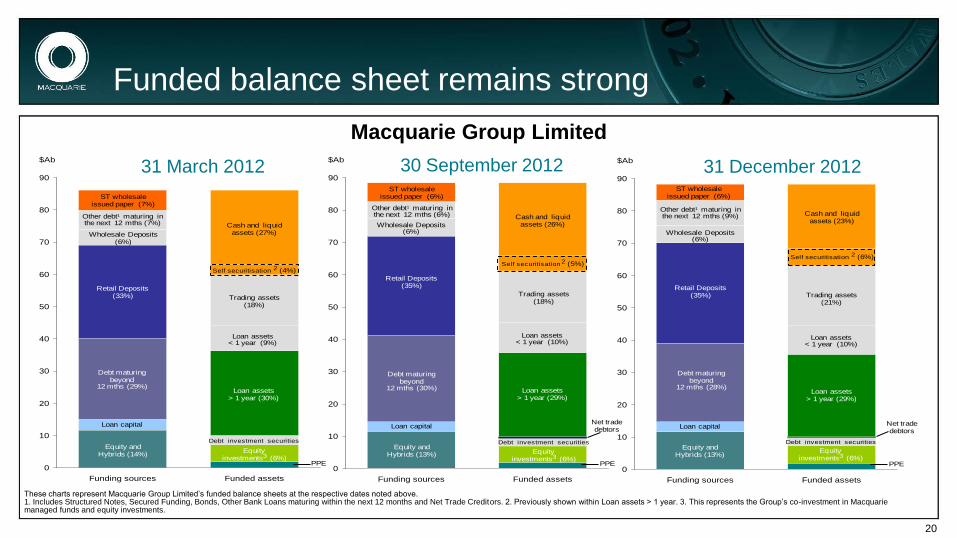

20

30 September 2012 31 March 2012 31 March 2012 31 December 2012 30 September 2012

Funded balance sheet remains strong

Macquarie Group Limited

0

10

20

30

40

50

60

70

80

90

Funding sources Funded assets

$Ab

Loan capital

Trading assets (18%)

Loan assets < 1 year (9%)

Loan assets > 1 year (30%)

Equity investments3 (6%)

Cash and liquidassets (27%)

Debt maturingbeyond

12 mths (29%)

Equity andHybrids (14%)

ST wholesaleissued paper (7%)

Other debt1 maturing in the next 12 mths (7%)

PPE

Debt investment securities

Retail Deposits (33%)

Wholesale Deposits (6%)

0

10

20

30

40

50

60

70

80

90

Funding sources Funded assets

$Ab

Loan capital

Trading assets (21%)

Loan assets < 1 year (10%)

Loan assets > 1 year (29%)

Equity investments3 (6%)

Cash and liquidassets (23%)

Debt maturingbeyond

12 mths (28%)

Equity andHybrids (13%)

ST wholesaleissued paper (6%)

Other debt1 maturing in the next 12 mths (9%)

PPE

Debt investment securities

Retail Deposits (35%)

Wholesale Deposits (6%)

Net tradedebtors

0

10

20

30

40

50

60

70

80

90

Funding sources Funded assets

$Ab

Loan capital

Trading assets (18%)

Loan assets < 1 year (10%)

Loan assets > 1 year (29%)

Equity investments3 (6%)

Cash and liquidassets (26%)

Debt maturingbeyond

12 mths (30%)

Equity andHybrids (13%)

ST wholesaleissued paper (6%)

Other debt1 maturing in the next 12 mths (6%)

PPE

Debt investment securities

Retail Deposits (35%)

Wholesale Deposits (6%)

Net tradedebtors

Self securitisation 2 (4%)Self securitisation 2 (5%)

Self securitisation 2 (6%)

These charts represent Macquarie Group Limited‟s funded balance sheets at the respective dates noted above. 1. Includes Structured Notes, Secured Funding, Bonds, Other Bank Loans maturing within the next 12 months and Net Trade Creditors. 2. Previously shown within Loan assets > 1 year. 3. This represents the Group‟s co-investment in Macquarie managed funds and equity investments.

21

3.4 3.3

2.1

4.3 4.2

3.0

0.1 (0.1) (0.1) (1.2)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Harmonised Basel III at Sep 12

Net capital generation Increased regulatory requirements

Other Harmonised Basel III at Dec 12

APRA Basel III 'super equivalence'

APRA Basel III at Dec 12

Group regulatory surplus: Basel III (Dec 12)

Based on 8.5%

(minimum Tier 1

ratio + CCB),

which is not

required by APRA

until 2016

$Ab

Group regulatory surplus at 8.5% RWA Group regulatory surplus at 7% RWA

Harmonised Basel III Banking Group capital ratios at Dec 12 Common Equity Tier 1: 11.3%; Tier 1: 12.3%

Stable Basel III capital surplus

1. „Harmonised‟ Basel III estimates assume alignment with BIS in areas where APRA differs from the BIS. 2. Includes 3Q12 P&L net of 1H13 dividend and movement in reserves. 3. Relating to Operational Risk. 4. APRA Basel III „super-equivalence‟ includes full CET1 deductions of equity investments ($A0.7b); deconsolidated subsidiaries ($A0.3b); and DTA‟s and other impacts ($A0.2b).

1

2

4 3

22

Medium term

Macquarie remains well positioned to deliver superior performance in the medium term

Deep expertise in major markets

Build on our strength in diversity and continue to adapt our portfolio mix to changing market conditions

Annuity-style income is provided by three significant businesses which are delivering superior returns following

years of investment and recent acquisitions

Macquarie Funds, Corporate and Asset Finance and Banking and Financial Services

Three capital markets facing businesses:

Macquarie Securities and Macquarie Capital are well positioned to benefit from improvements in market

conditions with strong platforms and franchise positions

FICC well placed to benefit from niche expertise and more normalised conditions

Ongoing benefits of continued cost initiatives

Strong and conservative balance sheet

Well matched funding profile with minimal reliance on short term wholesale funding

Surplus funding and capital available to support growth

Proven risk management framework and culture

23

Operating Group

APRA Basel III Capital

@ 8.5% ($Ab) Approx. 1H13 Return

on Ordinary Equity1

Annuity-style businesses (excluding legacy) Approx. 6-Year Average

Return on Ordinary Equity1

Macquarie Funds Group 1.6

22% 20%2 Corporate and Asset Finance 2.1

Banking and Financial Services 0.9

Capital markets facing businesses (excluding legacy) 6-Year Average

profit pre tax and

profit share ($Ab)

Approx. 6-Year

Average Return on

Ordinary Equity1

Macquarie Securities 0.5 -

0.5 30%

Macquarie Capital 1.4 0.6 20%

FICC 2.6 9% 0.6 15%

Corporate and Other

Legacy Assets 0.9

Corporate 0.5

Total regulatory capital requirement @ 8.5% 10.5

Comprising: Ordinary Equity

Hybrid

8.8

1.7

Add: Surplus Ordinary Equity 2.1

Total APRA Basel III capital supply 12.6

Approximate business Basel III & ROE

1. NPAT used in the calculation of approx. ROE is based on Operating Group‟s net profit contribution adjusted for indicative allocations of profit share, tax and other corporate expenses. Accounting equity is attributed to businesses based on regulatory capital requirements. 6-year average covers FY07 to FY12, inclusively. 2. CAF excluded from 6-year average as not meaningful given the significant increase in scale of CAF‟s platform over the 6-year period. As at 30 Sep 12.

24

1H13 Results 3 Macquarie Group Limited Presentation to Investors and Analysts March 2013

25

1H13 result

Net profit of $A361m, up 18% on 1H12 and down 15% on 2H12

Operating income $A3.1b, down 5% on 1H12 and down 17% on 2H12

Macquarie‟s annuity-style businesses, Macquarie Funds Group, Corporate and Asset Finance, Banking and Financial Services, continued to

perform well with 1H13 combined results broadly in line with a strong 1H12 and up on 2H12

As foreshadowed, Macquarie‟s capital markets facing businesses, Macquarie Securities, Macquarie Capital and FICC, although continuing to face

subdued market conditions, delivered a combined result up on 1H12 due to improved conditions for FICC

Macquarie Securities and Macquarie Capital continued to be impacted by low activity levels across ECM and M&A

Macquarie Securities impacted by low levels of client activity combined with run-off costs in its legacy businesses partially offset by ongoing

cost efficiencies

Operating expenses $A2.6b, down 9% on 1H12 and down 17% on 2H12, as a result of continued operating efficiencies

Increase in the half year effective tax rate to 30.2% up from 26.0% in 1H12 and 29.8% in 2H12

EPS $A1.06, up 22% on 1H12 and down 15% on 2H12

Return on equity 6.6%, up from 5.7% in 1H12 and down from 7.8% in 2H12

1H13 dividend of $A0.75 (unfranked), up on 1H12 dividend of $A0.65 (unfranked) and in line with 2H12 dividend of $A0.75 (unfranked)

26

1H13 result

Sep 12 v

Sep 11

Sep 12

$Am

Mar 12

$Am

Sep 11

$Am

Net operating income 5% 3,081 3,720 3,243

Total operating expenses 9% (2,564) (3,086) (2,828)

Operating profit before income tax 25% 517 634 415

Income tax expense 46% (156) (180) (107)

Profit attributable to non-controlling interests - (29) (3)

Profit attributable to MGL shareholders 18% 361 425 305

27

0

400

800

2H10 1H11 2H11 1H12 2H12 1H13

$Am

0

2,000

4,000

2H10 1H11 2H11 1H12 2H12 1H13

$Am

0.00

1.00

2.00

2H10 1H11 2H11 1H12 2H12 1H13

$A

0.00

1.00

2H10 1H11 2H11 1H12 2H12 1H13

$A

Financial performance

1H13 Profit of $A361m

1H13 up 18% on 1H12

1H13 Operating income of $A3,081m

1H13 down 5% on 1H12

1H13 EPS of $A1.06

1H13 up 22% on 1H12

1H13 DPS of $A0.75

1H13 up 15% on 1H12

28

Diversified income Operating income1 by source

11%

29%

2%

18%

9% 8%

23%

6 months to 30 Sep 12

$A3.3b

Operating income before impairments charges on equity investments and

non-financial assets

Institutional and retail

cash equities

Equity

derivatives

Securities funds management

and administration

M&A and advisory

income

Asset and equity

investments

Commodities, resources

and foreign exchange

Lending, leasing and margin

related income

12 months to 31 Mar 12

$A7.2b

4%

7% 12%

18%

25%

11%

26% 3%

18%

11% 8%

23%

14%

4%

20%

7% 14%

18%

23%

1. Operating income before impairments charges on equity investments and non-financial assets.

29

Diversified by region International income1 61% of total Total staff 13,463; International staff 54% of total

EUROPE, MIDDLE EAST

& AFRICA2

Income: $A625m (19% of total)

Staff: 1,229

ASIA

Income: $A353m (11% of total)

Staff: 2,813

AMERICAS

Income: $A1,006m (31% of total)

Staff: 3,276

AUSTRALIA3

Income: $A1,253m (39% of total)

Staff: 6,145

1. Operating income for half year to 30 Sep 12. Operating income in each region before impairment charges on equity investments and non-financial assets and income from the Corporate segment. 2. Excludes staff in Macquarie First South joint venture and staff seconded to Macquarie Renaissance joint venture (Moscow). 3. Includes New Zealand.

30

Diversified income Operating income1 by region

1. Operating income in each region before impairment charges on equity investments and non-financial assets and income from the Corporate segment.

61% of operating income1 in 1H13 is generated offshore

FX translation estimated to have a minimal impact on the 1H13 result compared to both 1H12 and 2H12

$Am

0

200

400

600

800

1,000

1,200

1,400

1,600

Australia Asia Americas Europe, Middle East & Africa

1H11

2H11

1H12

2H12

1H13

31

33 4 233 41

96

39

52

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,500

2,600

1H12 Investment in growth areas

Restructure MFG CAF BFS MSG Mac Cap FICC 1H13

Percentage reduction for each of the Operating Segments is based off 1H12 operating expenses (excluding brokerage and commissions expense). Restructuring includes incremental business rationalisation and restructuring costs.

Cost Performance

1H13 operating expenses (excluding brokerage and commissions expense) $A2.2b; down $A0.2b on 1H12

Achieved by ongoing cost reduction initiatives including centralisation of support functions and continued focus on costs

Select investment in growth areas including key markets, new products, processes and technologies

Macquarie Securities and Macquarie Capital continue to expect to reduce FY11 run rate costs by 20-25% by end of FY13

9%

14% 23%

16%

7% $A254m

reduction

10%

2%

$Am

2,442

2,217

32

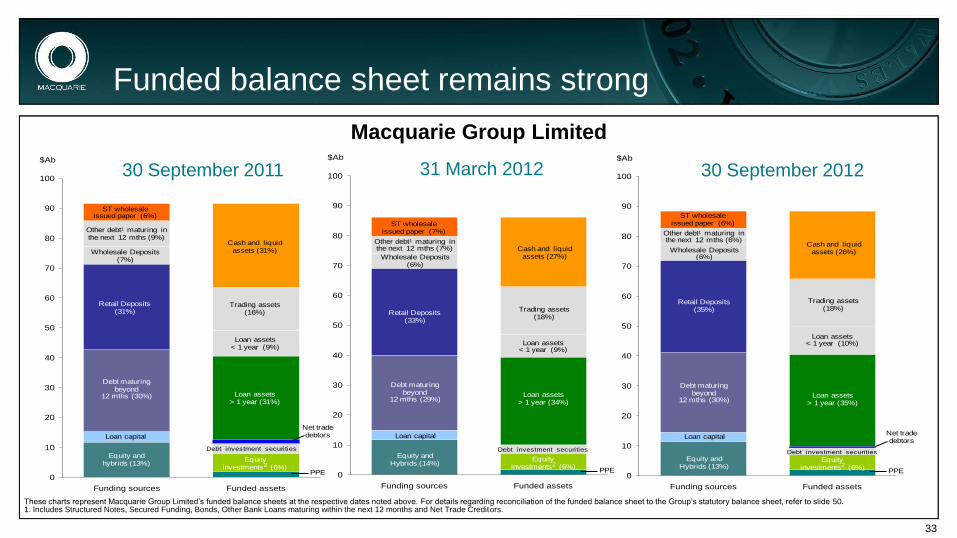

Strong funding and balance sheet position

1. These balances represent total deposits per the funded balance sheet, which differs from total deposits per the statutory balance sheet ($A40.0b at 30 Sep 12). The funded balance sheet excludes any deposits which do not represent a funding source for the Group. 2. Loan assets exclude Canadian mortgages which are funded via a government sponsored securitisation program. 3. Includes $A1.0b term secured finance in Oct 12.

Diverse and stable funding base, minimal reliance on short term wholesale funding markets

Total deposits1 increased to $A36.2b at Sep 12 from $A33.9b at Mar 12

Represents 41% of the Group‟s total funding sources

Group loan assets represent 88% of total deposits2

Retail deposits increased to $A30.8b at Sep 12 from $A29.0b at Mar 12, primarily driven by an

increase in the CMA

$A5.9b of new term funding raised since Mar 123

Continue to diversify funding base and develop new markets including Switzerland, South Africa,

Korea and Taiwan

$A2.1b raised through private placements and structured note issuance

33

30 September 2011 30 September 2012 31 March 2012 30 September 2011 30 September 2012 31 March 2012

Funded balance sheet remains strong

These charts represent Macquarie Group Limited‟s funded balance sheets at the respective dates noted above. For details regarding reconciliation of the funded balance sheet to the Group‟s statutory balance sheet, refer to slide 50. 1. Includes Structured Notes, Secured Funding, Bonds, Other Bank Loans maturing within the next 12 months and Net Trade Creditors.

Macquarie Group Limited

0

10

20

30

40

50

60

70

80

90

100

Funding sources Funded assets

$Ab

0

10

20

30

40

50

60

70

80

90

100

Funding sources Funded assets

$Ab

Loan capital

Trading assets (16%)

Loan assets < 1 year (9%)

Loan assets > 1 year (31%)

Equity investments2 (6%)

Cash and liquid assets (31%)

Debt maturingbeyond

12 mths (30%)

Equity andhybrids (13%)

ST wholesaleissued paper (6%)

Other debt1 maturing in the next 12 mths (9%)

Trading assets (18%)

Loan assets < 1 year (9%)

Loan assets > 1 year (34%)

Equity investments2 (6%)

Cash and liquidassets (27%)

Debt maturingbeyond

12 mths (29%)

Equity andHybrids (14%)

ST wholesaleissued paper (7%)

Other debt1 maturing in the next 12 mths (7%)

PPE PPE

Net tradedebtorsLoan capital

Debt investment securities Debt investment securities

Retail Deposits (31%)

Wholesale Deposits (7%)

Retail Deposits (33%)

Wholesale Deposits (6%)

0

10

20

30

40

50

60

70

80

90

100

Funding sources Funded assets

$Ab

Loan capital

Trading assets (18%)

Loan assets < 1 year (10%)

Loan assets > 1 year (35%)

Equity investments2 (6%)

Cash and liquidassets (26%)

Debt maturingbeyond

12 mths (30%)

Equity andHybrids (13%)

ST wholesaleissued paper (6%)

Other debt1 maturing in the next 12 mths (6%)

PPE

Debt investment securities

Retail Deposits (35%)

Wholesale Deposits (6%)

Net tradedebtors

34

Well diversified funding sources

1. Term facilities for the Group were fully drawn as at 31 Dec 12

Well diversified funding sources

Minimal reliance on short term wholesale funding markets

Deposit base represents 41% of total funding sources

MGL term funding (drawn and undrawn1)

maturing beyond one year (including equity

and hybrids)

Diversity of MGL funding sources

Term funding beyond one year (excluding equity) has

a weighted average term to maturity of 4.5 years

Wholesale issued paper Deposits -

corporate &

wholesale

Deposits - retail

Structured notes

Other loans

Secured funding

Senior credit facility

Bonds

Loan capital

Equity & hybrids

0

5

10

15

20

1-2 yrs <3 yrs <4 yrs <5 yrs 5 yrs+

$AbEquity & hybrids Loan capital Debt

35

10%

15%

20%

25%

30%

35%

40%

0

5

10

15

20

25

30

35

40

Mar 08 Mar 09 Mar 10 Mar 11 Mar 12 Sep 12

$Ab

Retail Corporate/wholesale

Continued retail deposit growth

Macquarie has been successful in pursuing its strategy of diversifying its funding sources through

growing its deposit base

In excess of 1 million retail clients, of which more than 641,000 are depositors

Focus on the composition and quality of the deposit base

Continue to grow deposits in the CMA product which has an average balance of $A39k

Retail Corporate/wholesale

% of total

funding source

36

3.5 3.9 3.9 4.2

3.4 3.0

2.1

4.4 4.3

3.0

0.2 0.2

(0.5)

(1.3)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Harmonised Basel III at Mar 12

MEREP and Buyback Net capital generation Other Harmonised Basel III at Sep 12

APRA Basel III 'super equivalence'

APRA Basel III at Sep 12

Group regulatory surplus: Basel III (Sep 12)

Based on 8.5%

(minimum Tier 1

ratio + CCB),

which is not

required by

APRA until 2016

$Ab

Group regulatory surplus at 8.5% RWA Group regulatory surplus at 7% RWA

2

3

4

Stable Basel III capital position

Harmonised Basel III Group capital of $A12.6b, Group surplus of $A3.4b at Sep 121

1. Calculated at 8.5% RWA which includes the 2.5% capital conservation buffer (CCB) not required to be met by APRA until 2016 and by BIS until 2019. 2. „Harmonised‟ Basel III estimates assume alignment with BIS in areas where APRA differs from the BIS, except that central counterparty (CCP) capital changes are not included in the estimates. 3. Includes 1H13 P&L net of FY12 dividend and movements in share based payment reserve. 4. APRA Basel III „super-equivalence‟ includes full CET1 deductions of equity investments ($A0.8b); deconsolidated subsidiaries ($A0.4b); and other impacts ($A0.1b).

37

0%

2%

4%

6%

8%

10%

12%

MBL Bank 2 Bank 3 Bank 4 Bank 5 Bank 6 Bank 7 Bank 8 Bank 9 Bank 10 Bank 11 Bank 12 Bank 13 Bank 14 Bank 15

CE

T1 R

atio

Harmonised Basel III CET1 Ratio

Australian Banks Overseas Banks

Macquarie Bank capital position relative to global peers

1. As at Dec 12 2. “Results of the Basel III monitoring exercise as of 30 June 2011”, Basel Committee on Banking Supervision, 12 Apr 12. Average of 103 Group 1 banks (i.e. those that have Tier 1 capital in excess of €3b and are internationally active). 3. The Harmonised Basel III CET1 ratio for each bank is sourced from their most recently available Basel III public disclosure. For Australian banks, this refers to the disclosed estimated Basel III BIS „harmonised‟ or „aligned‟ CET1 ratios, which include full phase-in of additional Basel III deductions. For overseas banks, banks have been included where the disclosure indicated that the CET1 ratio was based on full implementation of the 2019 BIS rules, which include full phase-in of additional Basel III deductions and excludes any future run-off, management action and growth. Banks included are ANZ, CBA, NAB and WBC for the Australian banks; Barclays, BMO, BoA ML, BNP, Citi, CS, Deutsche Bank, HSBC, JPMorgan and UBS for the overseas banks.

MBL Harmonised Basel III CET1 ratio is well above minimum CET1 + CCB and highest among peers

MBL‟s CET1 ratio of 11.3%1 compares favourably to the estimated global average of 7.1% reported by BIS in a

survey of 103 global banks² 3

Minimum BIS Basel III

CET1 Ratio + CCB = 7%

Minimum BIS Basel III

CET1 Ratio = 4.5%

38

MBL long term ratings stability

Standard & Poor‟s and Moodys Rating Movements from 1 May 2007

JPMorgan

Chase Bank

Credit Suisse AG

UBS AG

Barclays Bank

Deutsche Bank

Goldman Sachs Group

Bank of

America Citibank Morgan

Stanley Bank

Macquarie Bank

Ratin

g m

ovem

ent (n

otc

hes)

2007 2012 Intra

-

period ratings movement

AA -

A+

A

AA

AA+

A -

BBB+

Ratin

g m

ovem

ent (n

otc

hes)

Macquarie Bank

JPMorgan Chase Bank

Credit Suisse AG

UBS AG Barclays Bank

Deutsche Bank

Goldman Sachs Group

Bank of America

Citibank Morgan Stanley Bank

2007 2012 Intra - period ratings movement

Aa3

A1

A2

Aa2

Aa1

A3

AAA

Baa1

MBL has maintained its S&P rating for 21 years

MBL long term Moody’s rating stability

39

Appendix 4 Macquarie Group Limited Presentation to Investors and Analysts March 2013

40

Loan portfolio1 growth

0

100

200

300

400

500

600

700

800

900

0

5

10

15

20

25

30

35

40

45

Sep 09 Mar 10 Sep 10 Mar 11 Sep 11 Mar 12 Sep 12

Mortgages CAF lending Banking Aircraft leasing

Structured investment loans Motor Vehicle leasing Resources & commodities Equipment leasing

Other lending Other leasing Real Estate Total income (RHS)

1 . For the purposes of this disclosure, loan assets at amortised cost of $A47.6b at 30 Sep 12 per the statutory balance sheet are adjusted to include fundable assets not classified as loans on the statutory balance sheet (for example, assets subject to operating leases) and exclude loan assets that do not represent a funding requirement of the Group. 2. Total income includes net interest income from mortgages and other lending areas, and net operating lease income, net of funding costs.

Peak in 1H12 due to early loan

repayments in Corporate Lending

portfolio and higher income from

financing facilities to external funds

Volume

$Ab

Total Income

$Am

2

41

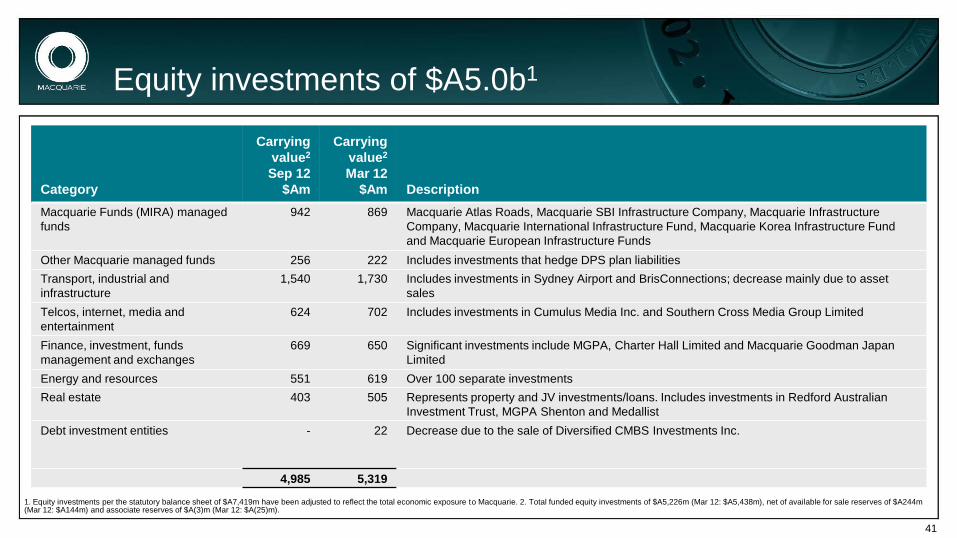

Equity investments of $A5.0b1

1. Equity investments per the statutory balance sheet of $A7,419m have been adjusted to reflect the total economic exposure to Macquarie. 2. Total funded equity investments of $A5,226m (Mar 12: $A5,438m), net of available for sale reserves of $A244m (Mar 12: $A144m) and associate reserves of $A(3)m (Mar 12: $A(25)m).

Category

Carrying

value2

Sep 12

$Am

Carrying

value2

Mar 12

$Am Description

Macquarie Funds (MIRA) managed

funds

942 869 Macquarie Atlas Roads, Macquarie SBI Infrastructure Company, Macquarie Infrastructure

Company, Macquarie International Infrastructure Fund, Macquarie Korea Infrastructure Fund

and Macquarie European Infrastructure Funds

Other Macquarie managed funds 256 222 Includes investments that hedge DPS plan liabilities

Transport, industrial and

infrastructure

1,540 1,730 Includes investments in Sydney Airport and BrisConnections; decrease mainly due to asset

sales

Telcos, internet, media and

entertainment

624 702 Includes investments in Cumulus Media Inc. and Southern Cross Media Group Limited

Finance, investment, funds

management and exchanges

669 650 Significant investments include MGPA, Charter Hall Limited and Macquarie Goodman Japan

Limited

Energy and resources 551 619 Over 100 separate investments

Real estate 403 505 Represents property and JV investments/loans. Includes investments in Redford Australian

Investment Trust, MGPA Shenton and Medallist

Debt investment entities - 22 Decrease due to the sale of Diversified CMBS Investments Inc.

4,985 5,319

42

Contacts 5 Macquarie Group Limited Presentation to Investors March 2013

43

Contact Details

Stuart Green

Head of Corporate Communications & Investor Relations

Macquarie Group Limited

Level 7, No.1 Martin Place

Sydney NSW 2000

Telephone: +612 8232 8845

Email: [email protected]

Patrick Upfold

Chief Financial Officer

Macquarie Group Limited

Level 7, No.1 Martin Place

Sydney NSW 2000

Telephone: +612 8232 7724

Email: [email protected]

Macquarie Group Limited