présentation powerpoint - kering.com · this presentation does not constitute an offer of...

TRANSCRIPT

2015 September 2015

I n v e s t o r

P r e s e n t a t i o n

2

Disclaimer

3

This presentation does not constitute an offer of securities for sale in the United States of America or any other jurisdiction.

Certain information contained in this document may include projections and forecasts. They express objectives based on current assessments and estimates of the Group’s executive management which are subject to numerous factors, risks and uncertainties. Consequently, reported figures and assessments may differ significantly from projected figures. The following factors among others set out in the Reference Document (Document de Référence) filed with the French Financial Markets Authority (Autorité des Marchés Financiers - AMF) on April 1st, 2015 which is available on Kering’s website at www.kering.com may cause actual figures to differ materially from projected figures: any unfavourable development affecting consumer spending in the activities of the Group in France and abroad, notably for products and services sold by the Luxury Goods and Sport & Lifestyle brands, the events, crises, fears, and resulting costs of complying with environmental, health and safety regulations and all other regulations with which Group companies are required to comply; the competitive situation on each of our markets; exchange rate and other risks related to international activities; risks arising from current or future litigation. Kering gives no commitment to updating and/or revising and/or commenting any projections and forecasts, or their impact on the results and perspectives of the Group, which may be contained in this presentation.

The information contained in this document has been selected by the Group’s executive management to present Kering’s First-Half 2015 results. This document has not been independently verified. Kering makes no representation or undertaking as to the accuracy or completeness of such information. None of the Kering or any of its affiliates representatives shall bear any liability (in negligence or otherwise) for any loss arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.

IN NO WAY DOES KERING ASSUME ANY RESPONSIBILITY FOR ANY INVESTMENT OR OTHER DECISIONS MADE BASED UPON THE INFORMATION PROVIDED IN THIS PRESENTATION. READERS ARE ADVISED TO REVIEW THE COMPANY'S REFERENCE DOCUMENT AND THE COMPANY'S APPLICABLE AMF FILINGS BEFORE MAKING ANY INVESTMENT OR OTHER DECISION.

4

K e r i n g

E m p o w e r i n g P r e m i u m B r a n d s

Investor Presentation

I n v e s t o r P r e s e n t a t i o n

Empowering premium brands ∞ A world leader in apparel and accessories, developing an ensemble of powerful brands

Kering Luxury

Kering Sport & Lifestyle

5

6

Analys is o f 2015 f i rs t -ha l f resu l ts

Investor Presentation

Key highlights

7

2 0 1 5 f i r s t - h a l f r e s u l t s

∞ H1 2015: Solid performances in an environment that remains volatile

– Group revenues up 17% as reported and up 3.5% comparable, with sharp contrasts between quarters

– Positive FX movements boosting reported sales but mixed impact on Group H1 results due to hedging

• Gross profit up 13%, gross profit margin unchanged at constant FX (-200bps reported)

• EBITDA stable at €972m

• Recurring operating income down 5%, at €773m

– Consolidated Net income, Group share, more than doubling

∞ Luxury: A resilient first half with marked rebound in revenue in Q2

– Gucci, Bottega Veneta, YSL and Other brands all posting growth in Q2, driven by mature markets, notably Western Europe

– Robust operating performance: Recurring operating income stable at €806m

– Further significant improvement in Luxury FCF from operations

∞ Sport & Lifestyle: Sustained top-line growth trajectory

– High single-digit growth at Puma in Q2

– Recurring operating income: Impact from ongoing investments in brand-building initiatives at Puma, adverse currency

situation a drag on profits

Operating performances

8

2 0 1 5 f i r s t - h a l f r e s u l t s

-0.6%

-2.6%

+3.7%

+7.7% +8.0% +7.1%

+3.5% +2.8%

+5.3%

Kering Group Luxury Sport & Lifestyle

Q1 2015 Q2 2015 H1 2015

Group H1 Revenue: +17% reported, + 3.5% comparable Group H1 Revenue by quarter (% in comparable growth)

In €m

Revenue

Change (%)

Reported Comparable (*)

Luxury 3,762 +17.8% +2.8%

Sport & Lifestyle 1,731 +15.5% +5.3%

Corporate & others 20 - -

Kering total 5,513 +17.0% +3.5%

In €m

Recurring

Operating Income

H1 2015

Reported change

(%)

Recurring

Operating margin

(%)

Luxury 806 +0.0% 21.4%

Sport & Lifestyle 38 -45.8% 2.2%

Corporate & others (71) +19.9% -

Kering total 773 -5.4% 14.0%

Group H1 Recurring operating income: €773m Group H1 Recurring operating income bridge (in €m)

(*) At constant perimeter and exchanges rates

(**) restated for Sergio Rossi classification under IFRS 5

773

H1 15 Corporate

(12)

S&L

(33)

Other

Brands

(10)

Saint

Laurent

+20

BV

+17

Gucci

(26)

H1 14

817 (**)

Stable Luxury EBIT

In €m H1 15

Reported

change (*)

Revenue 3,762 +17.8%

Recurring operating income Recurring operating income margin

806 21.4%

+0.0% -3.8pt

EBITDA EBITDA margin

961 25.5%

+3.8%

Gross CAPEX 161 +9.9%

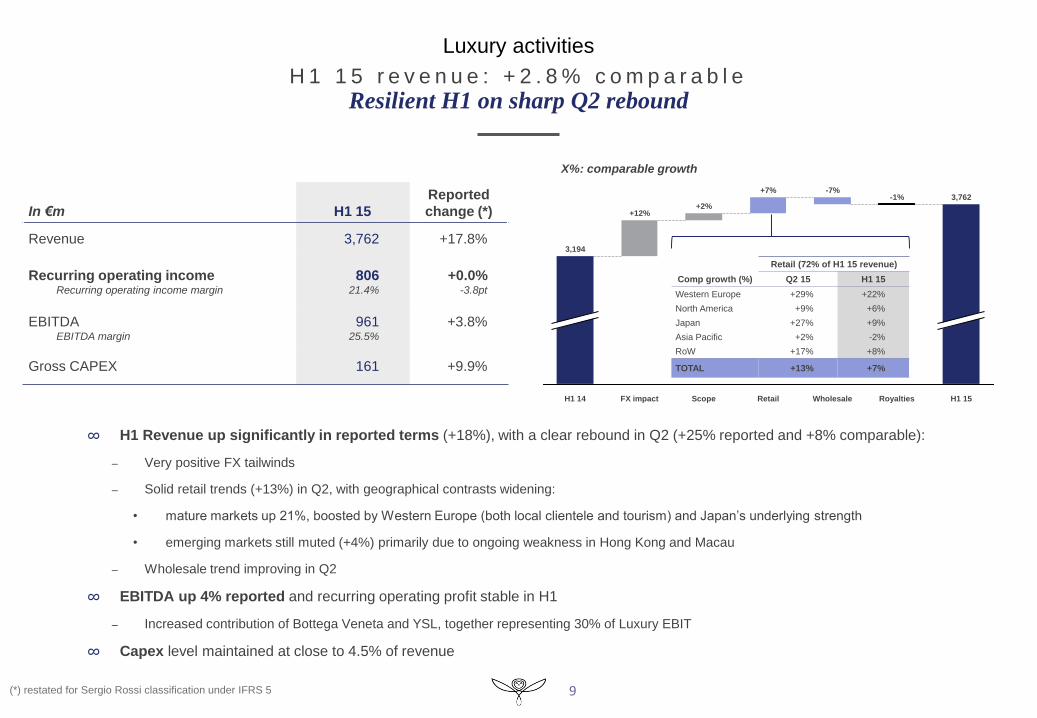

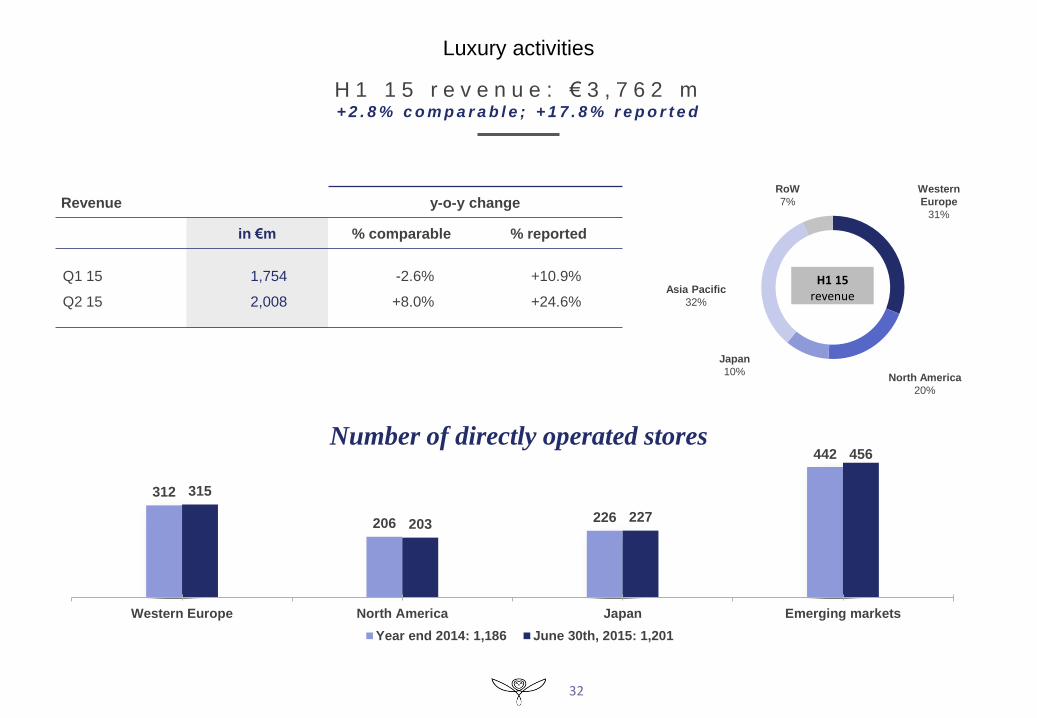

H 1 1 5 r e v e n u e : + 2 . 8 % c o m p a r a b l e

Resilient H1 on sharp Q2 rebound

∞ H1 Revenue up significantly in reported terms (+18%), with a clear rebound in Q2 (+25% reported and +8% comparable):

– Very positive FX tailwinds

– Solid retail trends (+13%) in Q2, with geographical contrasts widening:

• mature markets up 21%, boosted by Western Europe (both local clientele and tourism) and Japan’s underlying strength

• emerging markets still muted (+4%) primarily due to ongoing weakness in Hong Kong and Macau

– Wholesale trend improving in Q2

∞ EBITDA up 4% reported and recurring operating profit stable in H1

– Increased contribution of Bottega Veneta and YSL, together representing 30% of Luxury EBIT

∞ Capex level maintained at close to 4.5% of revenue

Luxury activities

9

X%: comparable growth

Royalties

3,762

H1 15

-1%

Wholesale

-7%

Retail

+7%

Scope

+2%

FX impact

+12%

H1 14

3,194

Comp growth (%)

Retail (72% of H1 15 revenue)

Q2 15 H1 15

Western Europe

North America

Japan

Asia Pacific

RoW

+29%

+9%

+27%

+2%

+17%

+22%

+6%

+9%

-2%

+8%

TOTAL +13% +7%

Retail (72% of revenue)

% comparable

Western Europe

North America

Japan

Asia Pacific

RoW

+22%

+6%

+9%

-2%

+8%

+13% -4% +2% Of which

Q2 15

Comp growth (%)

Retail (72% of H1 15 revenue)

Q2 15 H1 15

Western Europe

North America

Japan

Asia Pacific

RoW

+29%

+9%

+27%

+2%

+17%

+22%

+6%

+9%

-2%

+8%

TOTAL +13% +7%

(*) restated for Sergio Rossi classification under IFRS 5

10

H 1 1 5 r e v e n u e : - 1 . 6 % c o m p a r a b l e

Renewed brand momentum taking shape

In €m H1 15

Reported

change

Revenue 1,874 +11.8%

Recurring operating income Recurring operating income margin

502 26.8%

-4.9% -4.7pt

EBITDA EBITDA margin

587 31.3%

-1.6%

Gross CAPEX 77 +14.7%

H1 15

1,874

Royalties

-13%

Retail (84% of sales): +3%

Wholesale

-21%

Other

Countries

+10%

Asia Pacific

-4%

Japan

+2%

North

America

+6%

Western

Europe

+13%

H1 14

1,676

X%: comparable growth

∞ Improving revenue trends in second quarter as Gucci deploys new creative vision and executes action plans

– Solid progression in retail across all regions and key categories

– Wholesale streamlining carried on as expected

– Rejuvenation of Gucci brand image, new collections presented in H1 gathering enthusiastic reception

∞ Contained decline in recurring operating income:

– Positive FX impact but anticipated dilution in margin stemming from hedging

– Sustained underlying gross profit margin

∞ Capex up on phasing of investments and FX movements

+20% +11% +19% +3% +20% -19% -11% TOTAL

Q2: +5%

Of which

Q2 15

Q2 15 retail: +10%

Update on action plans and first achievements

11

Timing of

collections

Fir

st

ach

iev

em

en

ts

January / February Men & Women Fashion Show

F/W 15-16

June Cruise 2016

collection

presentation

End of Q3/ Early Q4 Cruise collection

progressively in stores

September Women Fashion

Show S/S 16

June Men Fashion

Show S/S 16

H1 2015 H2 2015

From end of June M&W Fashion Show

F/W 15-16 first

products in stores

Starting from December M&W S/S 16 Fashion Show

progressively in stores

Creation

Products &

Merchandising

Distribution &

Customers

Build a clear message, a more focused and relevant offer for the

customers

Introduce new products, discontinue selected lines

Reduce number of SKUs

Balance price offer range to exploit opportunities, upgrading of GG

Retail merchandising: be closer to market signals

Visual merchandising: a readable message

Store network refreshment

Achieve excellence in delivering retail experience to create uplift

in sales productivity

Seamless one-brand, one-store experience across all touchpoints

Refreshed website

12

H 1 1 5 r e v e n u e : + 6 . 4 % c o m p a r a b l e

Another strong first half, fueled by Western Europe

In €m H1 15

Reported

change

Revenue 629 +19.7%

Recurring operating income Recurring operating income margin

180 28.6%

+10.4% -2.4pt

EBITDA EBITDA margin

199 31.6%

+11.8%

Gross CAPEX 21 +11.3%

X%: comparable growth

Wholesale Royalties

+17%

H1 15

Retail (83% of sales): +7%

629 +2%

Other

Countries

+39%

Asia Pacific

-8%

Japan

+11%

North

America

-1%

Western

Europe

+44%

H1 14

525

∞ Q2 bounce, yielding solid revenue growth in H1

– Back to double-digit retail progression in Q2 (+12%), led by Western Europe and Japan, more than compensating for continued soft

conditions in Asia Pacific

– Great appeal of Leather Goods novelties

– Slight wholesale decline in Q2 vs. very high comps (Q2 14: +47%)

∞ Double-digit increase in Recurring operating income (+10%), consistent with the brand’s mid-term development plan

– Achieved despite adverse impact of hedging and less favorable geographic mix

∞ Ongoing brand building investments; strong FCF generation

+52% -2% +27% -8% +65% -3% +13% TOTAL

Q2: +9%

Of which

Q2 15

Q2 15 retail: +12%

13

H 1 1 5 r e v e n u e : + 2 4 . 3 % c o m p a r a b l e

Sustained growth across the board

In €m H1 15

Reported

change

Revenue 443 +38.2%

Recurring operating income Recurring operating income margin

61 13.7%

+47.9% +1.0pt

EBITDA EBITDA margin

80 18.0%

+52.2%

Gross CAPEX 28 +19.8%

X%: comparable growth

+22%

Other

Countries

H1 15 Royalties

Retail (64% of sales): +26%

443

Wholesale

+22% -12%

Asia Pacific

+15%

Japan

+45%

North

America

+32%

Western

Europe

+38%

H1 14

321

∞ Revenue growth accelerating in Q2, consistent across all distribution channels

– Retail channel consistently powering on quarter after quarter

– Solid increase in wholesale, in line with long-term strategy

– All categories contributing to revenue growth in H1: Leather goods up 23%, Women’s RTW up 30%, Men’s RTW up 23%, Shoes up

16%

∞ Recurring operating income up nearly 50%, with further 100 bp expansion in margin

– Operating leverage allowing to fully absorb hedging impact

∞ Continued investment in brand expansion

+45% +26% +82% +15% -14% +24% +24% TOTAL

Q2: +27%

Of which

Q2 15

Q2 15 retail: +29%

Other Luxury brands

14

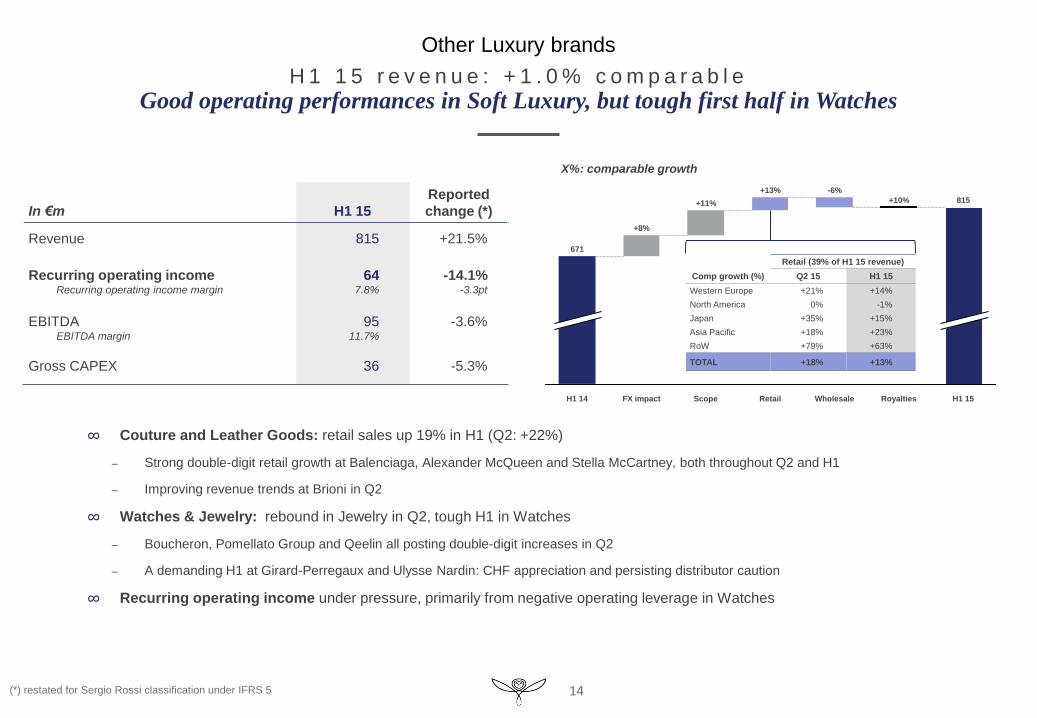

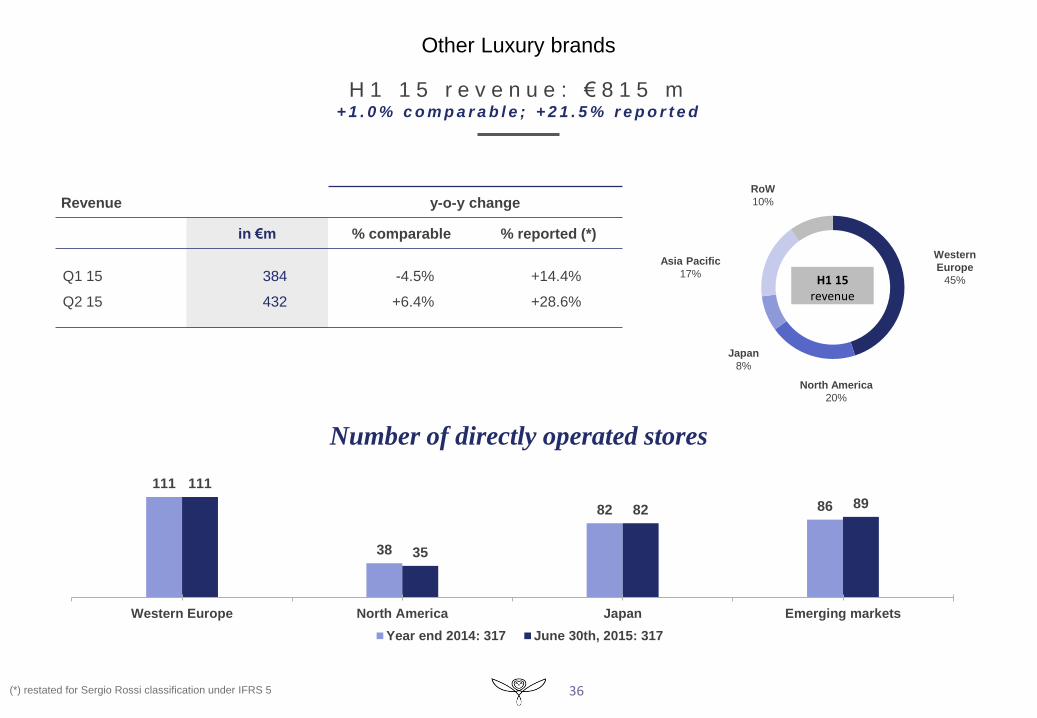

H 1 1 5 r e v e n u e : + 1 . 0 % c o m p a r a b l e

Good operating performances in Soft Luxury, but tough first half in Watches

In €m H1 15

Reported

change (*)

Revenue 815 +21.5%

Recurring operating income Recurring operating income margin

64 7.8%

-14.1% -3.3pt

EBITDA EBITDA margin

95 11.7%

-3.6%

Gross CAPEX 36 -5.3%

X%: comparable growth

∞ Couture and Leather Goods: retail sales up 19% in H1 (Q2: +22%)

– Strong double-digit retail growth at Balenciaga, Alexander McQueen and Stella McCartney, both throughout Q2 and H1

– Improving revenue trends at Brioni in Q2

∞ Watches & Jewelry: rebound in Jewelry in Q2, tough H1 in Watches

– Boucheron, Pomellato Group and Qeelin all posting double-digit increases in Q2

– A demanding H1 at Girard-Perregaux and Ulysse Nardin: CHF appreciation and persisting distributor caution

∞ Recurring operating income under pressure, primarily from negative operating leverage in Watches

815

H1 15 Royalties

+10%

Wholesale

-6%

Retail

+13%

Scope

+11%

FX impact

+8%

H1 14

671

Retail (39% of revenue)

% comparable

Western Europe

North America

Japan

Asia Pacific

RoW

+14%

-1%

+15%

+23%

+63%

Retail (72% of H1 15 revenue)

% comparable

Q2 15

% comparable

H1 15

Western Europe

North America

Japan

Asia Pacific

RoW

+21%

0%

+35%

+18%

+79%

+14%

-1%

+15%

+23%

+63%

Comp growth (%)

Retail (39% of H1 15 revenue)

Q2 15 H1 15

Western Europe

North America

Japan

Asia Pacific

RoW

+21%

0%

+35%

+18%

+79%

+14%

-1%

+15%

+23%

+63%

TOTAL +18% +13%

Comp growth (%)

Retail (39% of H1 15 revenue)

Q2 15 H1 15

Western Europe

North America

Japan

Asia Pacific

RoW

+21%

0%

+35%

+18%

+79%

+14%

-1%

+15%

+23%

+63%

TOTAL +18% +13%

(*) restated for Sergio Rossi classification under IFRS 5

Sport & Lifestyle

15

Puma €1,474m

Puma €1,386m

H 1 1 5 r e v e n u e : + 5 . 3 % c o m p a r a b l e

Sustained growth trajectory

In €m H1 15

Reported

change

Revenue 1,731 +15.5%

Recurring operating income Recurring operating income margin

o/w Puma

o/w Other Brands

38 2.2%

41

(3)

-45.8% -2.5pt

EBITDA EBITDA margin

70 4.0%

-27.6%

Gross CAPEX 45 +8.7%

1,499

1,731

RoW H1 15

+11%

Asia Pacific

+13%

Japan

+1%

North America

+4%

Western Europe

+0%

H1 14

X%: comparable growth

∞ Puma: convincing revenue performance in first half

– Revenue acceleration further confirmed in Q2, up 8% comparable, driven by Footwear (+16%) thanks to new product introductions

– All regions contributing to H1 performance (+6% comparable), with North America and Western Europe gaining traction in Q2

– Sustained Gross Margin in constant currency; Recurring operating income reflecting ongoing investment in brand building along with

currency headwinds

∞ Volcom and Electric:

– Trends improving in Q2 (+3% comparable), driven by strong e-commerce

% change

% comparable % reported

Puma

Other brands

+5.9%

-1.4%

+15.5%

+15.3%

+4% +8% +2% +8% +12% Of which

Q2 15 TOTAL

Q2: +7%

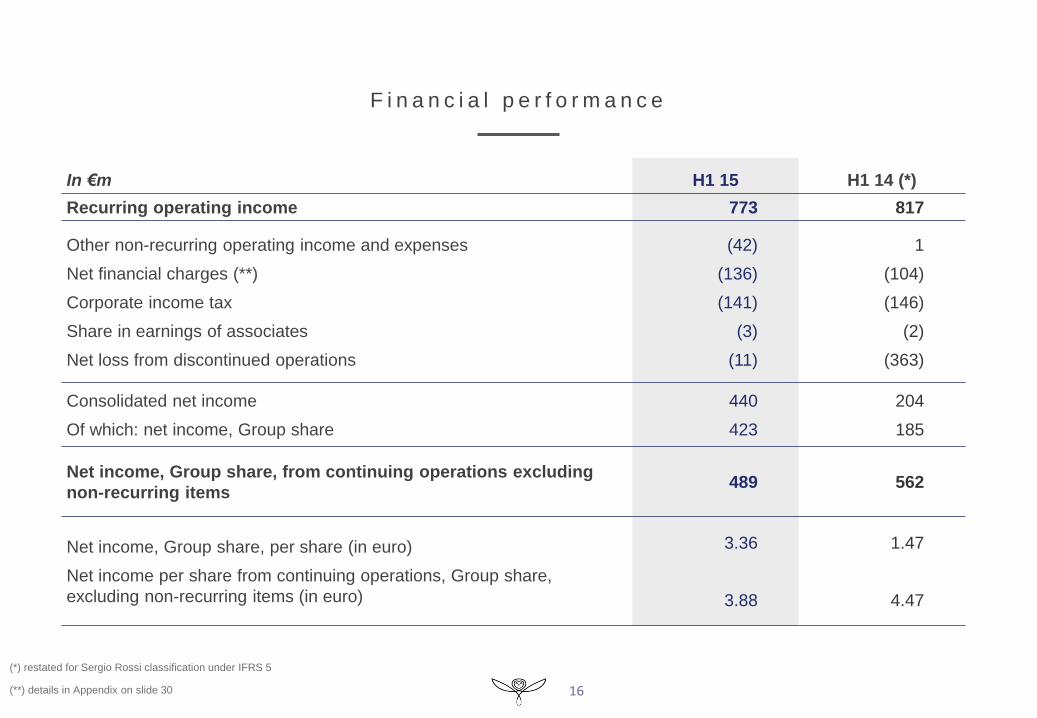

F i n a n c i a l p e r f o r m a n c e

In €m H1 15 H1 14 (*)

Recurring operating income 773 817

Other non-recurring operating income and expenses

Net financial charges (**)

Corporate income tax

Share in earnings of associates

Net loss from discontinued operations

(42)

(136)

(141)

(3)

(11)

1

(104)

(146)

(2)

(363)

Consolidated net income

Of which: net income, Group share

440

423

204

185

Net income, Group share, from continuing operations excluding

non-recurring items 489 562

Net income, Group share, per share (in euro)

Net income per share from continuing operations, Group share,

excluding non-recurring items (in euro)

3.36

3.88

1.47

4.47

16 (**) details in Appendix on slide 30

(*) restated for Sergio Rossi classification under IFRS 5

F r e e c a s h f l o w f r o m o p e r a t i o n s

17

58

299

160

309

635

Free cash flow

from operations

H1 15

Safilo early

termination

payment

-30

H1 15 hedge

impact

-211

FCF H1 15 before

hedge impact &

other changes

Other operations

and corporate

FCF change

-90

SLS FCF change

-80

Luxury FCF

change

FCF H1 14 excl.

real estate

disposal

H1 14 non-

recurring cash

inflow (real

estate disposal)

-326

Free cash flow

from operations

H1 14

H1 15 Free cash flow bridge (change in €m)

C h a n g e i n n e t f i n a n c i a l d e b t

18

209

8581

537

92

5,337

Dividends paid Net debt at

June 30, 2015

Other movements

(translation FX-

denominated debt)

Financing related

to discontinued

activities

5,043

Purchases of

Kering shares

and financial

investments

Net interest paid

and dividend

received

Free cash flow

from operations

-58

Net debt at

December

31, 2014

4,391

H1 15 net financial debt bridge (in €m)

19

Conclus ion and Out look

Investor Presentation

20

2 0 1 5 f i r s t - h a l f r e s u l t s

Conclusion & Outlook

∞ Commendable performance in H1 2015

– Sharp Q2 top-line rebound; solid operating profitability in Luxury

∞ Gucci on track to deploy new creative vision and execute action plans

– New dynamic and promising developments – Contemporary vision expressed across all customer touch points and enthusiastic reception from

industry and customers

– Active H2 schedule to anchor brand rejuvenation

∞ Additional milestones on steady profitable growth trajectory

– Kering Eyewear

– Digital platform

– Operating cost review

∞ Reiterated confidence in multi-brand strategy and prospects

21

Pr inc ip les for Susta inable Invest ing and

Corporate Governance overv iew

Investor Presentation

F r a n ç o i s - H e n r i P i n a u l t

Foreword

22

G o v e r n a n c e

Operation of the Board of Directors

5 Committees

Audit committee

– Jean-Pierre DENIS (Chairman)*

– Patricia BARBIZET

– Yseulys COSTES*

Board of Directors

Remuneration committee

- Philippe LAGAYETTE (Chairman)*

- Patricia BARBIZET

- Laurence BOONE*

- Yseulys COSTES*

- Jean-Pierre DENIS*

Nomination Committee

– Patricia BARBIZET (Chairwoman)

– Luca CORDERO DI MONTEZEMOLO*

– Baudouin PROT

Sustainability committee

– Jochen ZEITZ ( Chairman )

– Patricia BARBIZET

– Luca CORDERO DI MONTEZEMOLO*

– Jean-François PALUS

– François-Henri PINAULT

Strategy and development committee – Patricia BARBIZET (Chairwoman)

– Yseulys COSTES*

– Philippe LAGAYETTE*

– François-Henri PINAULT

* Independent director

11 Directors

5 Independent

4 Women

23

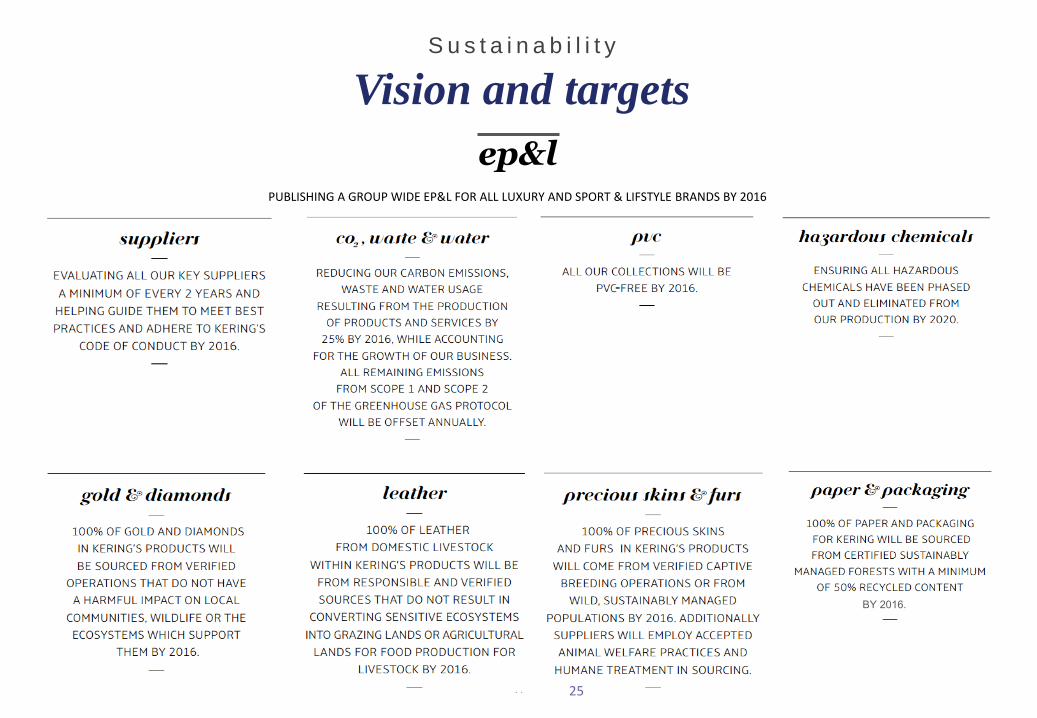

S u s t a i n a b i l i t y

Vision and targets

24

S u s t a i n a b i l i t y

Vision and targets

ep&l

PUBLISHING A GROUP WIDE EP&L FOR ALL LUXURY AND SPORT & LIFSTYLE BRANDS BY 2016

BY 2016.

25

S u s t a i n a b i l i t y

Targets: progress to date

26

S u s t a i n a b i l i t y

Environmental Profit & Loss account

€

27

28

KERING ENVIRONMENTAL PROFIT & LOSS

Group

EP&L

results

D I S C O V E R

M O R E

www.kering.com/en/sustai

nability/epl

29

Appendices

2015 first-half results

H 1 1 5 o p e r a t i n g p e r f o r m a n c e s

R e p o r t e d f i g u r e s

30

In €m

CONTINUING OPERATIONS

H1 15 H1 14 (*) Change

Revenue 5,513 4,710 +17.0%

Gross profit

Gross profit margin

3,399

61.7%

3,002

63.7%

+13.2%

Recurring operating income

Recurring operating income margin

773

14.0%

817

17.4%

-5.4%

EBITDA

EBITDA margin

972

17.6%

972

20.6%

-

(*) restated for Sergio Rossi classification under IFRS 5

H 1 1 5 r e v e n u e

Change

In €m, continuing operations H1 15 H1 14 (*) €m %

Gucci

Bottega Veneta

Saint Laurent

Other brands

1,874.2

629.2

443.1

815.5

1,676.3

525.5

320.6

671.2

197.9

103.7

122.5

144.3

+11.8%

+19.7%

+38.2%

+21.5%

Luxury 3,762.0 3,193.6 568.4 +17.8%

Puma

Other brands

1,601.2

129.8

1,386.1

112.6

215.1

17.2

+15.5%

+15.3%

Sport & Lifestyle 1,731.0 1,498.7 232.3 +15.5%

Corporate & Others 19.5 18.1 1.4 +7.7%

Kering 5,512.5 4,710.4 802.1 +17.0%

31 (*) restated for Sergio Rossi classification under IFRS 5

H 1 1 5 r e v e n u e : € 3 , 7 6 2 m + 2 . 8 % c o m p a r a b l e ; + 1 7 . 8 % r e p o r t e d

Western

Europe

31%

North America

20%

Japan

10%

Asia Pacific

32%

RoW

7%

Number of directly operated stores

312

206 226

442

315

203 227

456

Western Europe North America Japan Emerging markets

Year end 2014: 1,186 June 30th, 2015: 1,201

32

Luxury activities

Revenue y-o-y change

in €m % comparable % reported

Q1 15

Q2 15

1,754

2,008

-2.6%

+8.0%

+10.9%

+24.6%

H1 15 revenue

+14% € 838m

Western

Europe

24%

North America

21%

Japan

10%

Asia Pacific

38%

RoW

7%

Number of directly operated stores

33

116 117

65

207

118 119

64

211

Western Europe North America Japan Emerging markets

Year end 2014: 505 June 30th, 2015: 512

H 1 1 5 r e v e n u e : € 1 , 8 7 4 m - 1 . 6 % c o m p a r a b l e ; + 11 . 8 % r e p o r t e d

Revenue y-o-y change

in €m % comparable % reported

Q1 15

Q2 15

869

1,005

-7.9%

+4.6%

+3.7%

+19.9%

H1 15 revenue

Western

Europe

29%

North America

13%

Japan

15%

Asia Pacific

40%

RoW

3%

Number of directly operated stores

34

52

29

58

97

53

28

59

100

Western Europe North America Japan Emerging markets

Year end 2014: 236 June 30th, 2015: 240

H 1 1 5 r e v e n u e : € 6 2 9 m + 6 . 4 % c o m p a r a b l e ; + 1 9 . 7 % r e p o r t e d

Revenue y-o-y change

in €m % comparable % reported

Q1 15

Q2 15

290

339

+3.1%

+9.3%

+15.6%

+23.5%

H1 15 revenue

Western

Europe

39%

North America

24%

Japan

7%

Asia Pacific

23%

RoW

7%

Number of directly operated stores

35

33

22 21

52

33

21 22

56

Western Europe North America Japan Emerging markets

Year end 2014: 128 June 30th, 2015: 132

H 1 1 5 r e v e n u e : € 4 4 3 m + 2 4 . 3 % c o m p a r a b l e ; + 3 8 . 2 % r e p o r t e d

Revenue y-o-y change

in €m % comparable % reported

Q1 15

Q2 15

211

232

+21.2%

+27.3%

+33.8%

+42.5%

H1 15 revenue

Other Luxury brands

Western

Europe

45%

North America

20%

Japan

8%

Asia Pacific

17%

RoW

10%

Number of directly operated stores

36

111

38

82 86

111

35

82 89

Western Europe North America Japan Emerging markets

Year end 2014: 317 June 30th, 2015: 317

H 1 1 5 r e v e n u e : € 8 1 5 m + 1 . 0 % c o m p a r a b l e ; + 2 1 . 5 % r e p o r t e d

Revenue y-o-y change

in €m % comparable % reported (*)

Q1 15

Q2 15

384

432

-4.5%

+6.4%

+14.4%

+28.6%

H1 15 revenue

(*) restated for Sergio Rossi classification under IFRS 5

Western

Europe

28%

North America

29%

Japan

7%

Asia Pacific

15%

RoW

21%

37

Revenue y-o-y change

in €m % comparable % reported

Q1 15

Q2 15

890

841

+3.7%

+7.1%

+12.7%

+18.6%

Sport & Lifestyle

H 1 1 5 r e v e n u e : € 1 , 7 3 1 m + 5 . 3 % c o m p a r a b l e ; + 1 5 . 5 % r e p o r t e d

H1 15 revenue

H 1 1 5 r e c u r r i n g o p e r a t i n g i n c o m e

Change

In €m, continuing operations H1 15 H1 14 (*) €m %

Gucci

Bottega Veneta

Saint Laurent

Other brands

501.6

180.1

60.5

63.8

527.6

163.1

40.9

74.3

(26.0)

17.0

19.6

(10.5)

-4.9%

+10.4%

+47.9%

-14.1%

Luxury 806.0 805.9 0.1 +0.0%

Puma

Other brands

40.7

(2.3)

70.8

0.1

(30.1)

(2.4)

-42.5%

-

Sport & Lifestyle 38.4 70.9 (32.5) -45.8%

Corporate & Others (71.2) (59.4) (11.8) -19.9%

Kering 773.2 817.4 (44.2) -5.4%

38 (*) restated for Sergio Rossi classification under IFRS 5

Change

In €m, continuing operations H1 15 H1 14 (*) €m %

Gucci

Bottega Veneta

Saint Laurent

Other brands

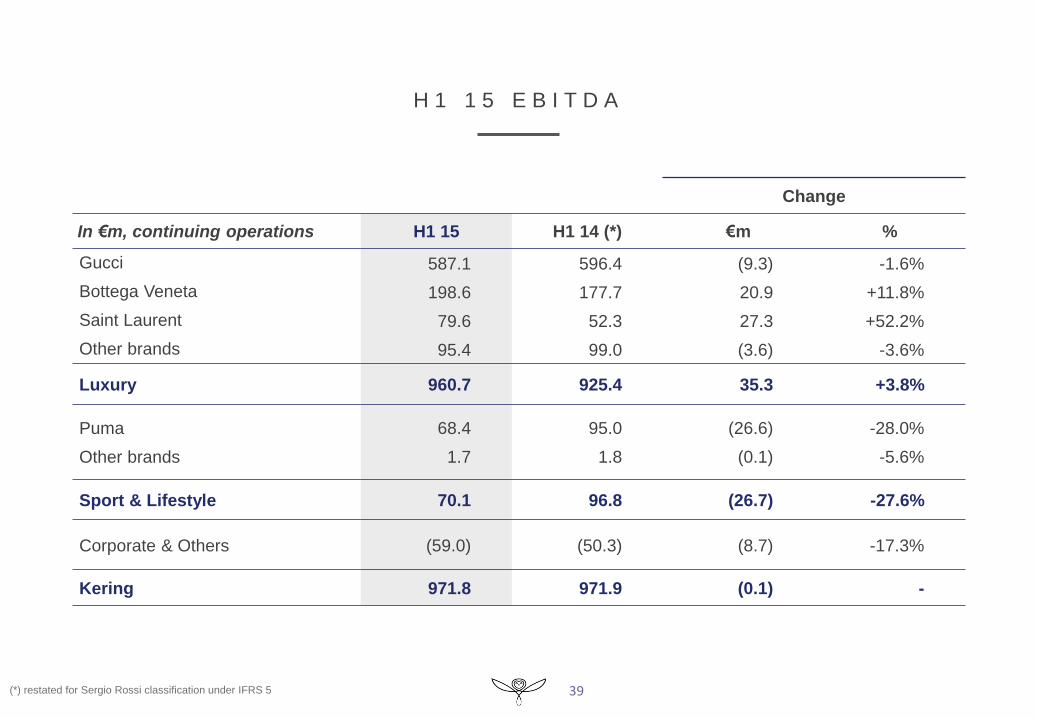

587.1

198.6

79.6

95.4

596.4

177.7

52.3

99.0

(9.3)

20.9

27.3

(3.6)

-1.6%

+11.8%

+52.2%

-3.6%

Luxury 960.7 925.4 35.3 +3.8%

Puma

Other brands

68.4

1.7

95.0

1.8

(26.6)

(0.1)

-28.0%

-5.6%

Sport & Lifestyle 70.1 96.8 (26.7) -27.6%

Corporate & Others (59.0) (50.3) (8.7) -17.3%

Kering 971.8 971.9 (0.1) -

39

H 1 1 5 E B I T D A

(*) restated for Sergio Rossi classification under IFRS 5

H 1 1 5 n e t f i n a n c i a l c o s t s

a n d i n c o m e t a x

In €m H1 15 H1 14 (*)

Cost of net debt

Other financial income and expenses

(64.2)

(72.0)

(86.0)

(18.3)

Financial costs (net) (136.2) (104.3)

In €m H1 15 H1 14 (*)

Tax on recurring income

Tax on non-recurring items

(126.3)

(15.1)

(129.9)

(16.1)

Total tax charge (141.4) (146.0)

Effective tax rate 23.8% 20.4%

Recurring tax rate 19.8% 18.2%

40 (*) restated for Sergio Rossi classification under IFRS 5

H 1 1 5 F r e e c a s h f l o w f r o m o p e r a t i o n s

In €m H1 15 H1 14 (*)

Cash flow before taxes, dividends and interest

Change in working capital requirement (excluding taxes)

Corporate income tax paid

895

(428)

(148)

944

(261)

(175)

Net cash flow from operating activities 319 508

Acquisition of fixed operating assets

Sale of fixed operating assets

(303)

42

(214)

341

Free cash flow from operations 58 635

41 (*) restated for Sergio Rossi classification under IFRS 5

H 1 1 5 c o n d e n s e d c o n s o l i d a t e d b a l a n c e s h e e t

In €m H1 15 H1 14 (*)

Goodwill, brands & other intangible assets – Net

Other net non-current assets

Net current assets

Provisions

15 100

503

1 555

(365)

14 361

4

1 039

(391)

CAPITAL EMPLOYED 16 793 15 013

Net assets held for sale 28 (66)

SHAREHOLDERS’ EQUITY 11 483 11 042

NET DEBT 5 337 3 905

42 (*) restated for Sergio Rossi classification under IFRS 5