presentation title set in arial italic, 46pt, black

TRANSCRIPT

© 2011 Sprint © 2011 Sprint

Sprint Nextel

3Q11 Earnings Conference Call

October 26, 2011

© 2011 Sprint

This presentation includes “forward-looking statements” within the meaning of the securities laws. The statements in this presentation regarding the business outlook, expected performance and forward-looking

guidance, as well as other statements that are not historical facts, are forward-looking statements. The words "estimate," "project," "forecast," "intend," "expect," "believe," "target," "providing guidance" and

similar expressions are intended to identify forward-looking statements. Forward-looking statements are estimates and projections reflecting management's judgment based on currently available information

and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. With respect to these forward-looking statements,

management has made assumptions regarding, among other things, customer and network usage, customer growth and retention, pricing, operating costs, the timing of various events and the economic and

regulatory environment.

Future performance cannot be assured. Actual results may differ materially from those in the forward-looking statements. Some factors that could cause actual results to differ include:

• our ability to attract and retain subscribers;

• the ability of our competitors to offer products and services at lower prices due to lower cost structures;

• the effects of vigorous competition on a highly penetrated market, including the impact of competition on the price we are able to charge subscribers for services and equipment we provide and our

ability to attract new subscribers and retain existing subscribers; the impact of subsidy costs; the impact of increased purchase commitments, the overall demand for our service offerings, including the

impact of decisions of new or existing subscribers between our postpaid and prepaid services offerings and between our two network platforms; and the impact of new, emerging and competing

technologies on our business;

• the ability to generate sufficient cash flow to fully implement our network modernization plan, Network Vision, to improve and enhance our networks and service offerings, implement our business

strategies and provide competitive new technologies;

• the effective implementation of Network Vision, including timing, execution, technologies, and costs;

• the ability to consummate the LightSquared transaction and obtain the associated financial benefits;

• changes in available technology and the effects of such changes, including product substitutions and deployment costs;

• our ability to obtain additional financing on terms acceptable to us, or at all;

• volatility in the trading price of our common stock, current economic conditions and our ability to access capital;

• the impact of unrelated parties not meeting our business requirements, including a significant adverse change in the ability or willingness of such parties to provide devices or infrastructure equipment

for our CDMA network, or Motorola Mobility, Inc.'s or Motorola Solutions Inc.'s ability or willingness to provide related devices, infrastructure equipment and software applications for our iDEN network;

• the costs and business risks associated with providing new services and entering new geographic markets;

• the financial performance of Clearwire and its ability to operate and maintain its 4G network;

• the effects of mergers and consolidations and new entrants in the communications industry and unexpected announcements or developments from others in the communications industry;

• unexpected results of litigation filed against us or our suppliers or vendors;

• the impact of adverse network performance;

• the costs or potential customer impacts of compliance with regulatory mandates including, but not limited to, compliance with the FCC's Report and Order to reconfigure the 800 MHz band;

• equipment failure, natural disasters, terrorist acts or other breaches of network or information technology security;

• one or more of the markets in which we compete being impacted by changes in political, economic or other factors such as monetary policy, legal and regulatory changes or other external factors over

which we have no control; and .other risks referenced from time to time in our filings with the Securities and Exchange Commission, including in Part I, Item IA “Risk Factors” of our annual report on

Form 10-K for the year ended December 31, 2010 and our subsequent quarterly reports on Form 10-Q.

Sprint Nextel believes these forward-looking statements are reasonable; however, you should not place undue reliance on forward-looking statements, which are based on current expectations and speak only as of the

date of this presentation. Sprint Nextel is not obligated to publicly release any revisions to forward-looking statements to reflect events after the date of this presentation.

Clearwire’s third quarter 2011 results from operations have not yet been finalized. As a result, the amount reflected for Sprint’s share of Clearwire’s results of operations for the quarter ended September 30, 2011, is an

estimate and, based upon the finalization of Clearwire’s results, may need to be revised if our estimate materially differs from Clearwire’s actual results. Changes in our estimate, if any, would affect the carrying

value of our investment in Clearwire, net loss and basic and diluted loss per common share but would have no effect on Sprint’s operating income, OIBDA*, Adjusted OIBDA* or consolidated statement of cash

flows.

Cautionary Statement

2

© 2011 Sprint

*Non-GAAP Financial Measures

3

Sprint Nextel provides financial measures determined in accordance with accounting principles generally accepted in the United

States (GAAP) and adjusted GAAP (non-GAAP). The non-GAAP financial measures reflect industry conventions, or standard

measures of liquidity, profitability or performance commonly used by the investment community for comparability purposes. These

measurements should be considered in addition to, but not as a substitute for, financial information prepared in accordance with

GAAP. We have defined below each of the non-GAAP measures we use, but these measures may not be synonymous to similar

measurement terms used by other companies.

Sprint Nextel provides reconciliations of these non-GAAP measures in its financial reporting. Because Sprint Nextel does not predict

special items that might occur in the future, and our forecasts are developed at a level of detail different than that used to prepare

GAAP-based financial measures, Sprint Nextel does not provide reconciliations to GAAP of its forward-looking financial measures.

The measures used in this presentation include the following:

OIBDA is operating income/(loss) before depreciation and amortization. Adjusted OIBDA is OIBDA excluding severance, exit costs,

and other special items. Adjusted OIBDA Margin represents Adjusted OIBDA divided by non-equipment net operating revenues for

Wireless and Adjusted OIBDA divided by net operating revenues for Wireline. We believe that Adjusted OIBDA and Adjusted OIBDA

Margin provide useful information to investors because they are an indicator of the strength and performance of our ongoing business

operations, including our ability to fund discretionary spending such as capital expenditures, spectrum acquisitions and other

investments and our ability to incur and service debt. While depreciation and amortization are considered operating costs under

GAAP, these expenses primarily represent non-cash current period costs associated with the use of long-lived tangible and definite-

lived intangible assets. Adjusted OIBDA and Adjusted OIBDA Margin are calculations commonly used as a basis for investors,

analysts and credit rating agencies to evaluate and compare the periodic and future operating performance and value of companies

within the telecommunications industry.

Free Cash Flow is the cash provided by operating activities less the cash used in investing activities other than short-term

investments and equity method investments during the period. We believe that Free Cash Flow provides useful information to

investors, analysts and our management about the cash generated by our core operations after interest and dividends and our ability

to fund scheduled debt maturities and other financing activities, including discretionary refinancing and retirement of debt and

purchase or sale of investments.

© 2011 Sprint

Consolidated Earnings per Share

4

Sprint Nextel CorporationIncome Statement on a per Share basis (Unaudited)

Quarter To Date

September 30, June 30, September 30,

2011 2011 2010

Operating Income (Loss) per share 0.07$ 0.03$ (0.07)$

Interest expense per share (0.08) (0.08) (0.12)

Equity in losses of unconsolidated

investments and other, net per share(0.09) (0.20) (0.09)

Loss before Income Taxes per share (1) (0.10)$ (0.25)$ (0.29)$

Income tax expense per share (0.00) (0.03) (0.01)

Net Loss per share (0.10)$ (0.28)$ (0.30)$

(1) Loss before Incomes Tax per share is presented gross excluding the effect of income taxes.

© 2011 Sprint 5

© 2011 Sprint

6

• Best Ever Postpaid Brand Health measures

(Ipsos)

- Most Want to Investigate

- Purchase Consideration

- Positive Brand Momentum

- First Brand Preference

Brand

6

© 2011 Sprint

3,414

1,232

1,861

1,000

1,500

2,000

2,500

3,000

3,500

Q4 0

5

Q1 0

6

Q2 0

6

Q3 0

6

Q4 0

6

Q1 0

7

Q2 0

7

Q3 0

7

Q4 0

7

Q1 0

8

Q2 0

8

Q3 0

8

Q4 0

8

Q1 0

9

Q2 0

9

Q3 0

9

Q4 0

9

Q1 1

0

Q2 1

0

Q3 1

0

Q4 1

0

Q1 1

1

Q2 1

1

Q3 1

1

000s

Good

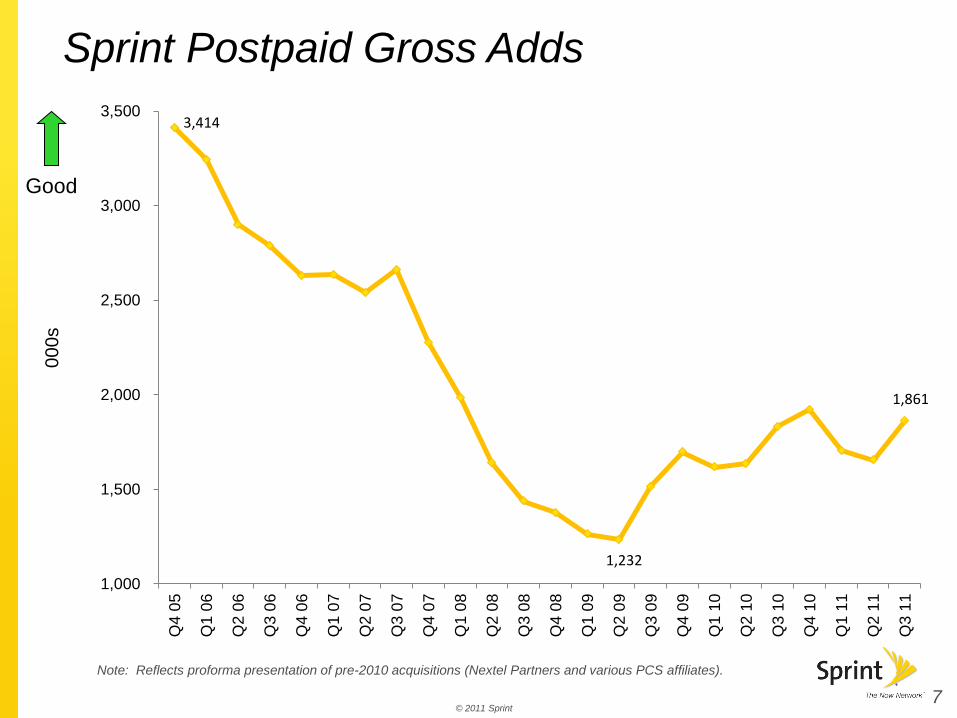

Sprint Postpaid Gross Adds

7

Note: Reflects proforma presentation of pre-2010 acquisitions (Nextel Partners and various PCS affiliates).

© 2011 Sprint

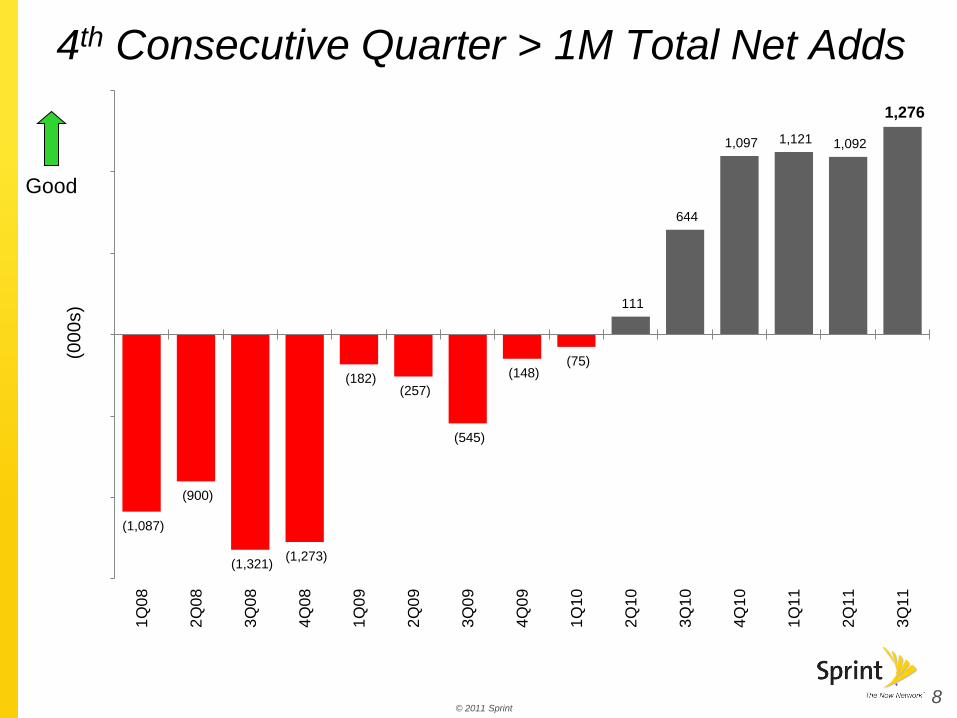

4th Consecutive Quarter > 1M Total Net Adds

(1,087)

(900)

(1,321) (1,273)

(182) (257)

(545)

(148) (75)

111

644

1,097 1,121 1,092

1,276

(1,500)

(1,000)

(500)

-

500

1,000

1,500

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

(00

0s)

Good

8

© 2011 Sprint

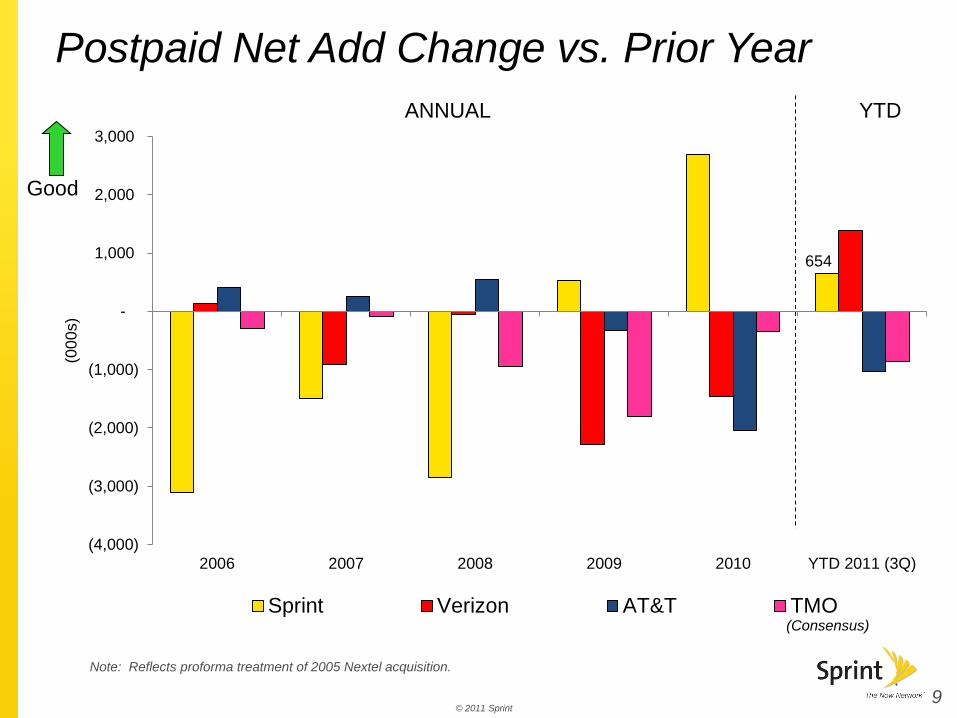

654

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,000

2006 2007 2008 2009 2010 YTD 2011 (3Q)

(00

0s)

Sprint Verizon AT&T TMO

ANNUAL YTD

Postpaid Net Add Change vs. Prior Year

Good

(Consensus)

9

Note: Reflects proforma treatment of 2005 Nextel acquisition.

© 2011 Sprint

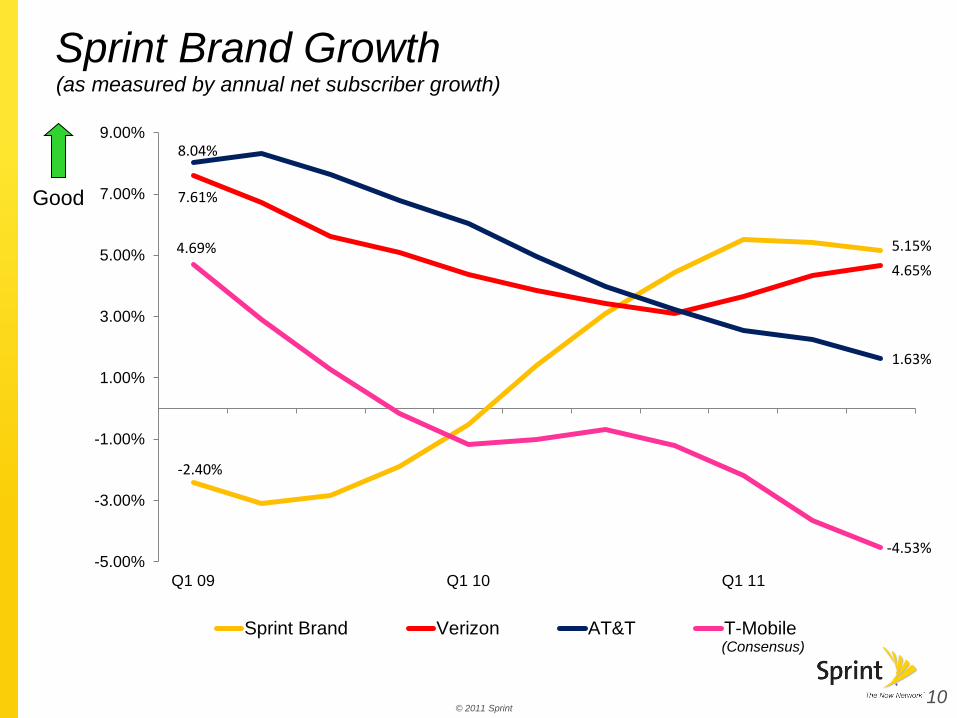

-2.40%

5.15%

7.61%

4.65%

8.04%

1.63%

4.69%

-4.53% -5.00%

-3.00%

-1.00%

1.00%

3.00%

5.00%

7.00%

9.00%

Q1 09 Q1 10 Q1 11

Sprint Brand Verizon AT&T T-Mobile

(as measured by annual net subscriber growth)

Good

Sprint Brand Growth

10

(Consensus)

© 2011 Sprint

11

11

© 2011 Sprint

Postpaid ARPU

• Largest year-over-year improvement this

century

• Highest sequential improvement in 6 years

• All-time record year-over-year CDMA ARPU

growth

Cash

12

© 2011 Sprint

• Total Operating Revenues up year-over-year for

fifth consecutive quarter

• Total Service Revenues and Wireless Service

Revenues saw largest year-over-year

percentage increases since 2006

• Drove best Q3 OIBDA sequential improvement

percentage in 6 years

Cash (cont’d)

13

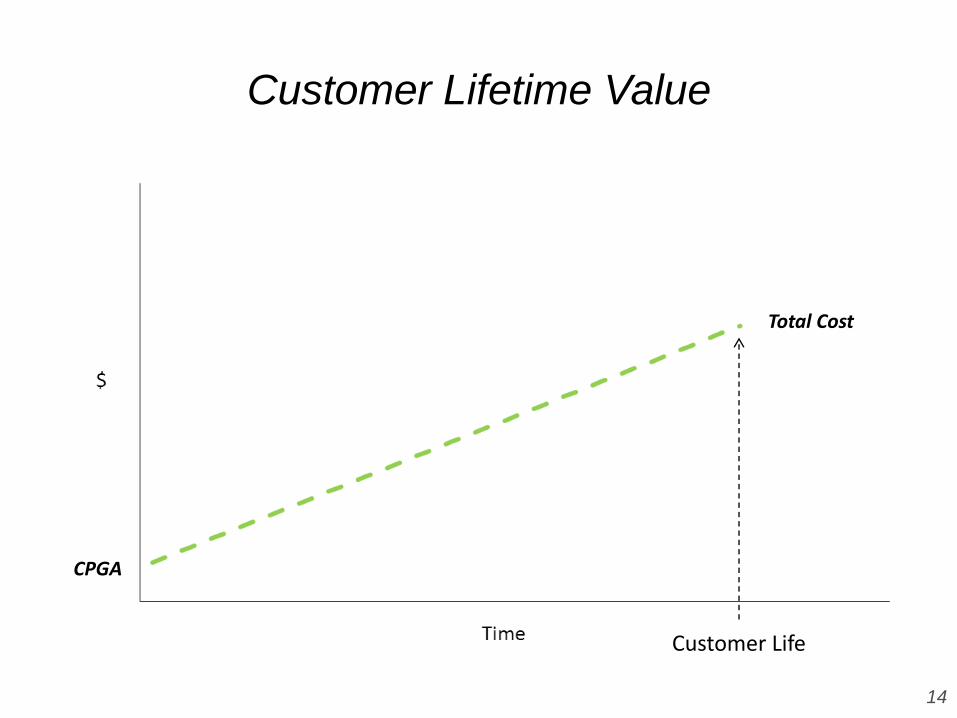

Customer Lifetime Value

Total Cost

Customer Life

CPGA

14

CLV

Breakeven

Total Revenue

Total Cost

CPGA

Customer Life

Customer Lifetime Value

15

Customer Lifetime Value Expected iPhone CLV is more than 50% Greater

CLV

Total Revenue

Total Cost

CPGA

Breakeven Customer Life

16

© 2011 Sprint

$5,500

$6,000

$6,500

$7,000

$7,500

$ M

illio

ns

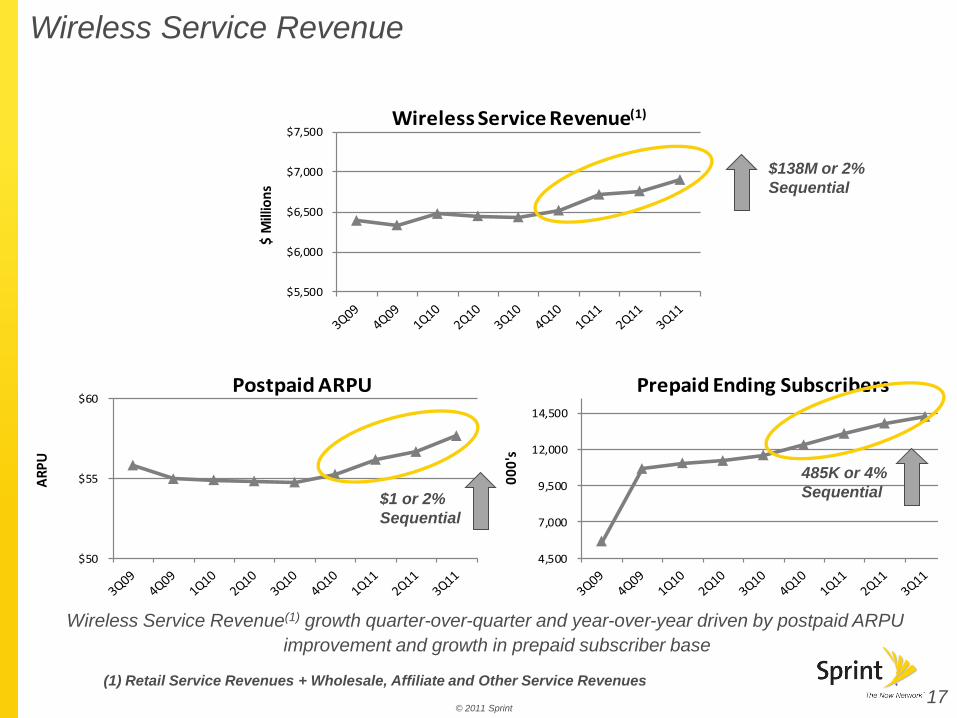

Wireless Service Revenue(1)

$50

$55

$60

AR

PU

Postpaid ARPU

4,500

7,000

9,500

12,000

14,500

00

0's

Prepaid Ending Subscribers

Wireless Service Revenue(1) growth quarter-over-quarter and year-over-year driven by postpaid ARPU

improvement and growth in prepaid subscriber base

Wireless Service Revenue

(1) Retail Service Revenues + Wholesale, Affiliate and Other Service Revenues

$138M or 2%

Sequential

17

$1 or 2%

Sequential

485K or 4%

Sequential

© 2011 Sprint

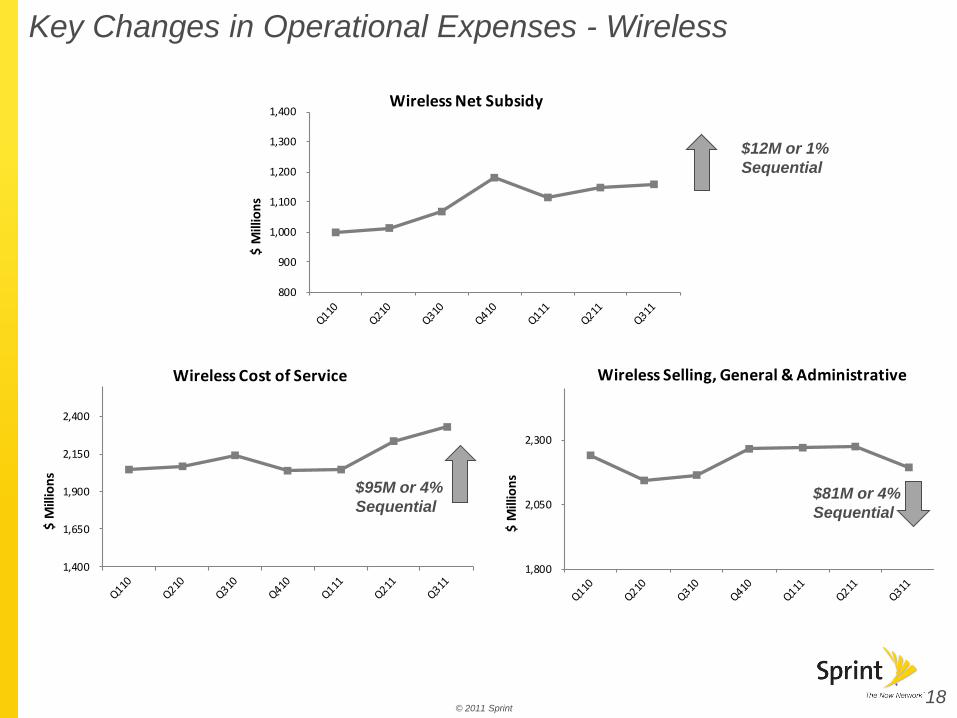

Key Changes in Operational Expenses - Wireless

18

800

900

1,000

1,100

1,200

1,300

1,400

$ M

illio

ns

Wireless Net Subsidy

1,400

1,650

1,900

2,150

2,400

$ M

illio

ns

Wireless Cost of Service

1,800

2,050

2,300

$ M

illio

ns

Wireless Selling, General & Administrative

$12M or 1%

Sequential

$95M or 4%

Sequential $81M or 4%

Sequential

© 2011 Sprint

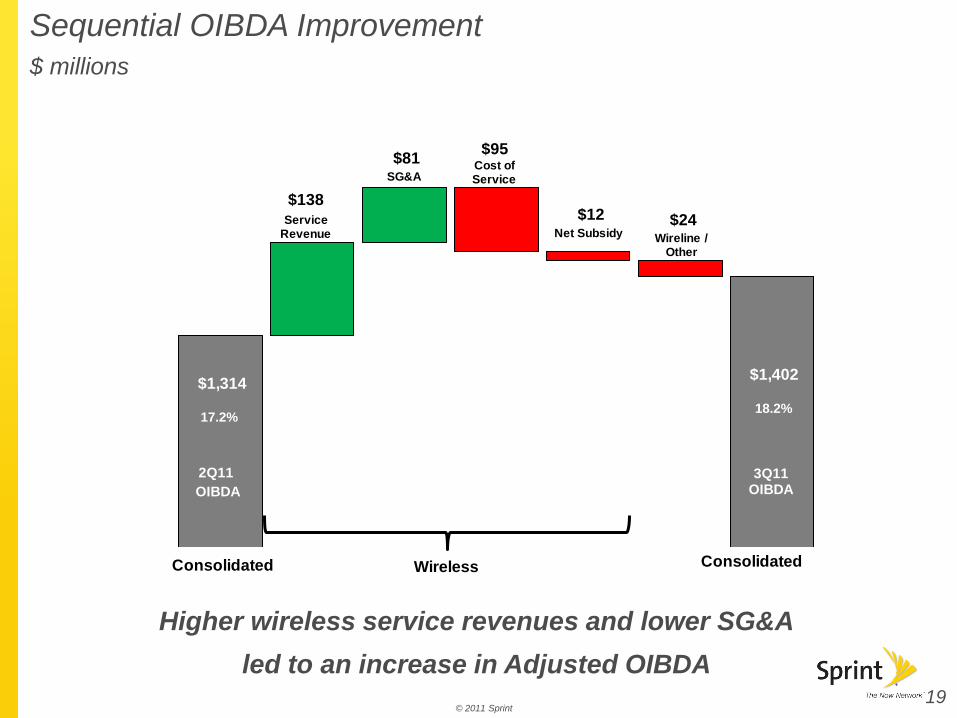

$1,314

$138

$81 $95

$12 $24

$1,402

Servic

2Q11

OIBDA

3Q11 OIBDA

SG&ACost of Service

Wireless

Wireline / Other

2Q11

Adjusted OIBDA*

Service Revenue Net Subsidy

Consolidated Consolidated

Sequential OIBDA Improvement

$ millions

Higher wireless service revenues and lower SG&A

led to an increase in Adjusted OIBDA 19

17.2%

18.2%

© 2011 Sprint

• $4.0B cash, cash equivalents and short-term investments

and $5.0B of liquidity exiting 3Q11

• Next note and loan maturities of $2.25B are due March 2012

Liquidity Position $ billions

20

$0.7

$0.7

$0.8 $0.9

$1.0

$4.7 $5.5

$4.0 $4.3 $4.0

3Q10 4Q10 1Q11 2Q11 3Q11

AvailableRevolver

Cash

© 2011 Sprint

Free Cash Flow

21

(Millions)

See accompanying Notes to the Financial Information (Unaudited) in the Press Release

September 30, 2011 June 30, 2011 September 30, 2010 3Q11 vs 2Q11 3Q11 vs 3Q10

Adjusted OIBDA 1,402$ 1,314$ 1,339$ 88$ 63$

Net Cash Provided by Operating Activities 608$ 1,075$ 971$ (467)$ (363)$

Capital Expenditures (818) (759) (490) (59) (328)

Expenditures Related to FCC Licenses (71) (54) (108) (17) 37

Other investing activities, net 8 5 11 3 (3)

Free Cash Flow* (273)$ 267$ 384$ (540)$ (657)$

September 30, 2011 June 30, 2011 September 30, 2010 3Q11 vs 2Q11 3Q11 vs 3Q10

Accounts Receivable, Net 3,054$ 3,082$ 3,042$ 28$ (12)$

Inventory 923 1,160 562 237 (361)

Prepaid & Other Current Assets 516 504 770 (12) 254

Accounts Payable (2,188) (3,035) (2,423) (847) (235)

Accrued Expenses & Other (3,237) (3,340) (3,366) (103) (129)

Working Capital (932)$ (1,629)$ (1,415)$ (697)$ (483)$

Quarter Ended

Quarter Ended

Key Working Capital Elements

© 2011 Sprint

OIBDA Estimate

$7 to $8 billion NPV

over expected

customer life

iPhone Estimates

$1.0B to

$1.2B

$6.0B to

$6.8B

Higher Subscriber Profitability

Metrics

• Churn Improvement (> 10%)

• Network Efficiency (> 50%)

Incremental Gross Adds

22

FY 11 FY 12 FY 13 FY 14 FY 15

Contribution margin from iPhone $(0.0) $0.8 $1.7 $2.6 $3.4

Cost of upgrades and handset sales,including commissions

$(0.6) $(1.9) $(2.8) $(3.3) $(2.9)

OIBDA Impact $(0.6) $(1.1) $(1.1) $(0.7) $0.5

OIBDA Margin Impact (2.1%) (3.7%) (3.9%) (2.8%) 0.3%

$(3.7)

$(2.7)

$(1.7)

$(0.7)

$0.3

$1.3

$2.3

$3.3

$ B

illio

ns

Contribution margin from iPhone

Cost of upgrades and handset

sales, including commissions

OIBDA Impact

© 2011 Sprint

Network Vision Estimated OIBDA Impacts

Gross Operating Costs and Gross Benefits

23

• Project NPV of ~ $6 billion

2011 2012 2013 2014 2015 2016 2017

Network Vision Operating Expenses ($0.1) ($1.4) ($1.4) ($0.6) ($0.4) ($0.2) ($0.2)

Network Vision Benefits ($0.0) $0.3 $1.3 $2.5 $3.0 $3.7 $4.4

Network Vision Net OIBDA Benefits ($0.1) ($1.1) ($0.1) $1.9 $2.7 $3.4 $4.3

OIBDA Margin Impact 0.0% (3.5%) (0.2%) 5.2% 6.6% 8.0% 9.2%

($2.0)

($1.0)

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$B

Network Vision Benefits

Network Vision Operating Expenses

Network Vision Net OIBDA Benefits

© 2011 Sprint

Illustrative Funding Needs

24

($9,000)

($3,000)

$3,000

$9,000

2011 2012 2013 2014 2015

$ M

illio

ns

Network Vision Benefits Network Vision Costs

iPhone Benefits iPhone Costs

Illustrative Ending Cash without Financing

Projected funding needs of $5 - $7 billion

(assuming $2 billion target cash balance)

- $4B Refinancing

- $1 - $3B Vendor Financing

Target Cash Balance

$5B $7B

© 2011 Sprint

Q&A

25

© 2011 Sprint

Non-GAAP Reconciliations – Consolidated

(Unaudited)

26

(Millions, except Margin Data)

See accompanying Notes to the Financial Information (Unaudited) in the Press Release

Quarter To Date Year To Date

September 30, June 30, September 30, September 30, September 30,

2011 2011 2010 2011 2010

Net Loss (301)$ (847)$ (911)$ (1,587)$ (2,536)$

Income tax expense (12) (99) (53) (148) (171)

Loss before Income Taxes (289) (748) (858) (1,439) (2,365)

Depreciation 1,114 1,121 1,304 3,357 3,840

Amortization 80 114 248 327 1,022

Interest expense 236 239 361 724 1,114

Equity in losses of unconsolidated investments and other, net 261 588 284 1,261 795

OIBDA* 1,402 1,314 1,339 4,230 4,406

Severance and exit costs (3)

- - - - (4)

Access costs (4)

- - - - (84)

Adjusted OIBDA* 1,402 1,314 1,339 4,230 4,318

Capital expenditures (1)

760 640 462 1,955 1,318

Adjusted OIBDA* less Capex 642$ 674$ 877$ 2,275$ 3,000$

Adjusted OIBDA Margin* 18.2% 17.2% 18.1% 18.4% 19.3%

Selected item:

Deferred tax asset valuation allowance 121 337 365 654 1,032

© 2011 Sprint

Non-GAAP Reconciliations – Wireless

(Unaudited)

27

(Millions, except Margin Data)

See accompanying Notes to the Financial Information (Unaudited) in the Press Release

Quarter To Date

September 30, June 30, September 30, September 30, September 30,

2011 2011 2010 2011 2010

Operating Income (Loss) 131$ (27)$ (345)$ 244$ (962)$

Severance and exit costs (3)

- - - - (1)

Depreciation 1,006 1,018 1,164 3,036 3,433

Amortization 77 111 246 319 1,015

Adjusted OIBDA* 1,214 1,102 1,065 3,599 3,485

Capital expenditures (1)

647 546 341 1,642 971

Adjusted OIBDA* less Capex 567$ 556$ 724$ 1,957$ 2,514$

Adjusted OIBDA Margin* 17.6% 16.3% 16.6% 17.7% 18.0%

Year To Date

© 2011 Sprint

Non-GAAP Reconciliations – Wireline

(Unaudited)

28

(Millions, except Margin Data)

See accompanying Notes to the Financial Information (Unaudited) in the Press Release

Quarter To Date

September 30, June 30, September 30, September 30, September 30,

2011 2011 2010 2011 2010

Operating Income 76$ 105$ 131$ 300$ 502$

Severance and exit costs (3)

- - - - (3)

Access costs (4)

- - - - (84)

Depreciation 108 105 140 322 408

Adjusted OIBDA* 184 210 271 622 823

Capital expenditures (1)

36 35 59 124 164

Adjusted OIBDA* less Capex 148$ 175$ 212$ 498$ 659$

Adjusted OIBDA Margin* 17.3% 19.3% 21.8% 19.0% 21.6%

Year To Date