presentation title slide - budgetbudget.gov.ie/budgets/2019/documents/7. economic... · 2016 q1...

TRANSCRIPT

Budget 19#Budget19

#Budget19

Section 1 Macroeconomic Developments

Section 2 Macroeconomic Outlook

Section 3 Developments in the Public Finances

3 An Roinn Airgeadais | Department of Finance

Economic Growth in Ireland’s key trading partners remains reasonably solid…

Key Points• Significant

acceleration of

US growth in Q2

• Euro Area growth

has moderated in

2018

• UK growth

remains modest

49

50

51

52

53

54

55

56

57

0.0

0.2

0.4

0.6

0.8

1.0

2016 Q

1

2016 Q

2

2016 Q

3

2016 Q

4

2017 Q

1

2017 Q

2

2017 Q

3

2017 Q

4

2018 Q

1

2018 Q

2

q-o

-q g

row

th

US

US GDP PMI

49

50

51

52

53

54

55

56

0.0

0.2

0.4

0.6

0.8

1.0

2016 Q

1

2016 Q

2

2016 Q

3

2016 Q

4

2017 Q

1

2017 Q

2

2017 Q

3

2017 Q

4

2018 Q

1

2018 Q

2

q-o

-q g

row

th

UK

UK GDP PMI

50

51

52

53

54

55

56

57

58

0.0

0.2

0.4

0.6

0.8

1.0

2016 Q

1

2016 Q

2

2016 Q

3

2016 Q

4

2017 Q

1

2017 Q

2

2017 Q

3

2017 Q

4

2018 Q

1

2018 Q

2

q-o

-q g

row

th

Euro Area

Euro Area GDP PMI

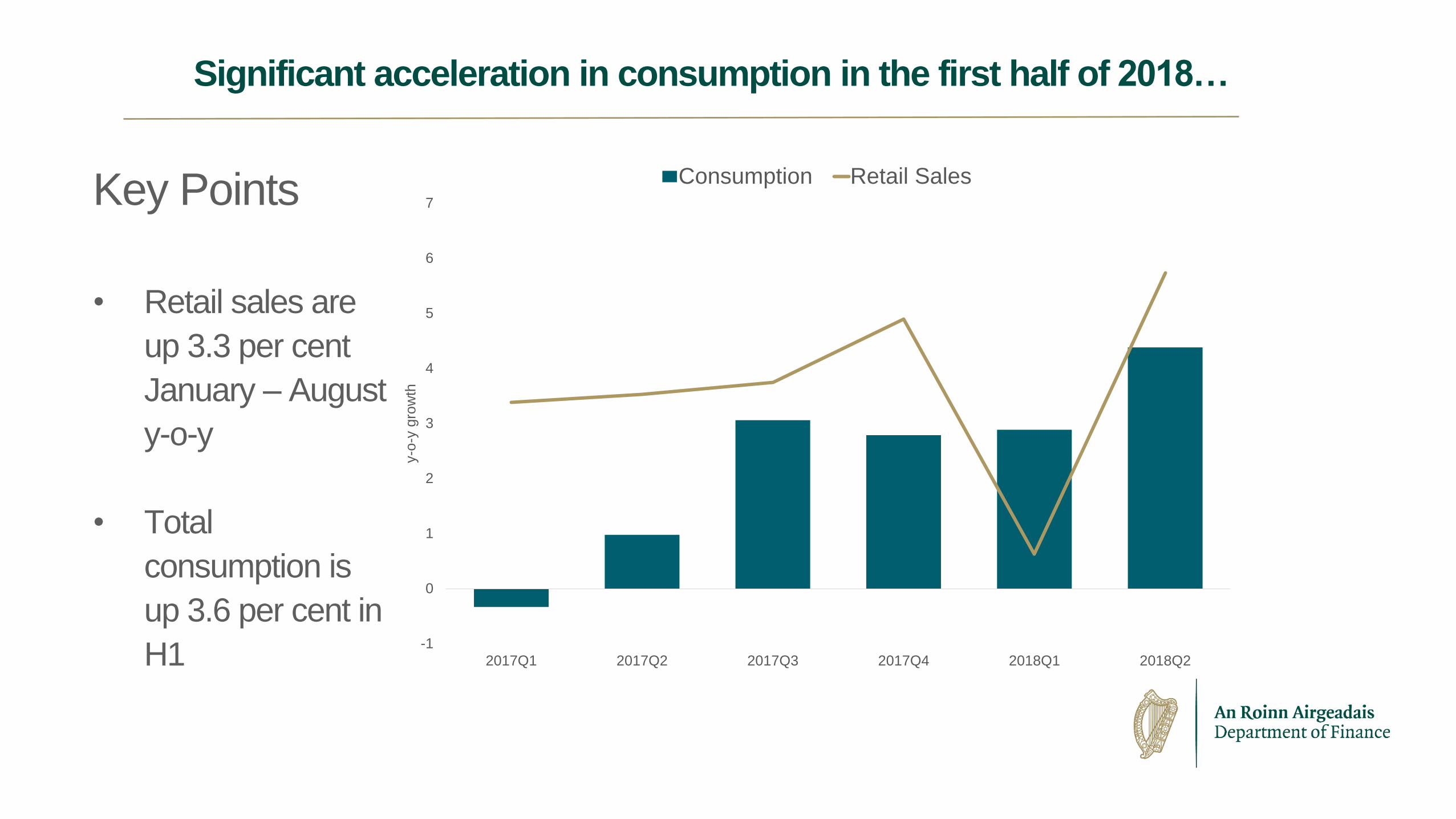

Significant acceleration in consumption in the first half of 2018…

Key Points

• Retail sales are

up 3.3 per cent

January – August

y-o-y

• Total

consumption is

up 3.6 per cent in

H1 -1

0

1

2

3

4

5

6

7

2017Q1 2017Q2 2017Q3 2017Q4 2018Q1 2018Q2

y-o

-y g

row

th

Consumption Retail Sales

Significant acceleration in modified investment in recent quarters…

Key Points• Headline investment

remains weak

reflecting less

“onshoring” of

intangibles by MNEs

• Modified

Investment, which

adjusts for volatile

components linked

to MNEs, is up 15.2

per cent in H1 y-o-y-60

-50

-40

-30

-20

-10

0

10

20

30

2017Q1 2017Q2 2017Q3 2017Q4 2018Q1 2018Q2

Contributions to Investment, pp

B&C Core M&E Aircraft

Intangibles GDFCF Mod Investment

Goods exports accelerating while services have moderated sharply…

Key Points• Goods exports

increased by 14.2

per cent in H1 y-o-y

driven by exports

from the

pharmaceutical

sector

• Services exports

increased by 2.2 per

cent, the slowest

rate of growth since

2012

-10

-5

0

5

10

15

20

25

2017Q1 2017Q2 2017Q3 2017Q4 2018Q1 2018Q2

y-o

-y g

row

th

Goods Services

Continued momentum in the labour market…

Key Points• Employment grew by

3.4 per cent in Q2, the

24th successive quarter

of employment growth

• Strong employment

growth has helped

reduce unemployment

which has fallen from a

peak of 16 per cent in

early 2012 to 5.4 per

cent in September. 5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

0

1

2

3

4

5

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2014 2015 2016 2017 2018

un

em

plo

ym

en

t ra

te (

%)

em

plo

ym

en

t g

row

th, y-o

y (

%)

Employment Growth (lhs) SA unemployment Rate (rhs)

Inflationary pressures remain relatively contained…

Key Points• Annual inflation in

Ireland on a HICP

basis has averaged

0.6 per cent over

January - August

• Core inflation, which

excludes energy

and unprocessed

food, averaged 0.3

per cent over the

same period.

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2015 2016 2017 2018 2019

HICP Quarterly profile

NEIG Unprocessed Processed Rents Energy Core Services HICP Core HICP

#Budget19

Section 1 Macroeconomic Developments

Section 2 Macroeconomic Outlook

Section 3 Developments in the Public Finances

Budget 2019 Macroeconomic Outlook…

Year-on-year % change 2018 2019 2020 2021 2022 2023GDP 7.5 4.2 3.6 2.5 2.6 2.7GNP 5.9 3.9 3.3 2.3 2.4 2.5Nominal GDP 9.3 6.2 5.4 4.4 4.4 4.5

Personal Consumption 3.5 3.0 2.6 2.1 2.2 2.4Govt Consumption 3.5 2.9 1.9 1.8 1.8 1.8Investment -8.9 7.1 5.7 4.4 4.3 4.3Exports 7.0 5.6 4.8 3.8 3.7 3.6Imports 0.9 6.2 5.3 4.5 4.3 4.1

HICP 0.7 1.5 1.7 2.9 2.4 2.6GDP Deflator 1.8 1.9 1.8 1.8 1.7 1.7Employment 3.0 2.8 2.2 1.5 1.6 1.7Unemployment (rate) 5.8 5.2 5.0 5.0 5.0 5.0

Contributions to growth (p.p)*Domestic Demand -0.5 2.7 2.2 1.8 1.8 1.9Change in Stocks 0.5 0.0 0.0 0.0 0.0 0.0Net Exports 7.5 1.4 1.3 0.7 0.8 0.8

Modified Domestic Demand (incl stocks) 3.5 2.4 1.9 1.6 1.6 1.7Modified Net Exports 3.9 1.8 1.7 1.0 1.0 1.0

Risks - firmly tilted to the downside…

External

• Hard-Brexit

• Trade protectionism/trade-war

• Global financial market conditions

• Geopolitical factors

Domestic

• Concentrated production base

• Overheating pressures

#Budget19

Section 1 Macroeconomic Developments

Section 2 Macroeconomic Outlook

Section 3 Developments in the Public Finances

Tax performance year to date…

Key points

• Tax revenues of €37.5

billion were received to end

Q3 2018, marginally below

target (down 0.3% or €0.1

billion).

• In year-on-year terms, tax

revenues are up 5.3% or

€1.9 billion.

0

10

20

30

40

50

60

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

€b

illio

ns

Total Taxes 2018 receipts 2018 Profile

Budget 2019…

• The central fiscal assumption of Budget 2019 is that

Ireland will achieve a broadly (in headline, general

government terms) balanced budget of 0.0% of GDP

next year.

• This is the first time the balance has not been in deficit

in 12 years.

• The economic forecasts underpinning this Budget

have been endorsed by the Irish Fiscal Advisory

Council (IFAC).

Budget 2019 Fiscal Outlook…

2018 2019 2020 2021 2022 2023

general government balance (% of GDP)

-0.1 0.0 0.3 0.4 1.1 1.4

general government primary balance (% of GDP)1.5 1.4 1.6 1.6 2.3 2.7

Debt-to-GDP ratio

64.0 61.4 56.5 55.3 53.1 51.1

Debt-to-GNI* ratio

105.2 101.0 93.1 91.2 87.8 84.5

Structural Budget Balance (% of GDP)

-1.0 -0.7 0.0 0.2 1.0 1.4

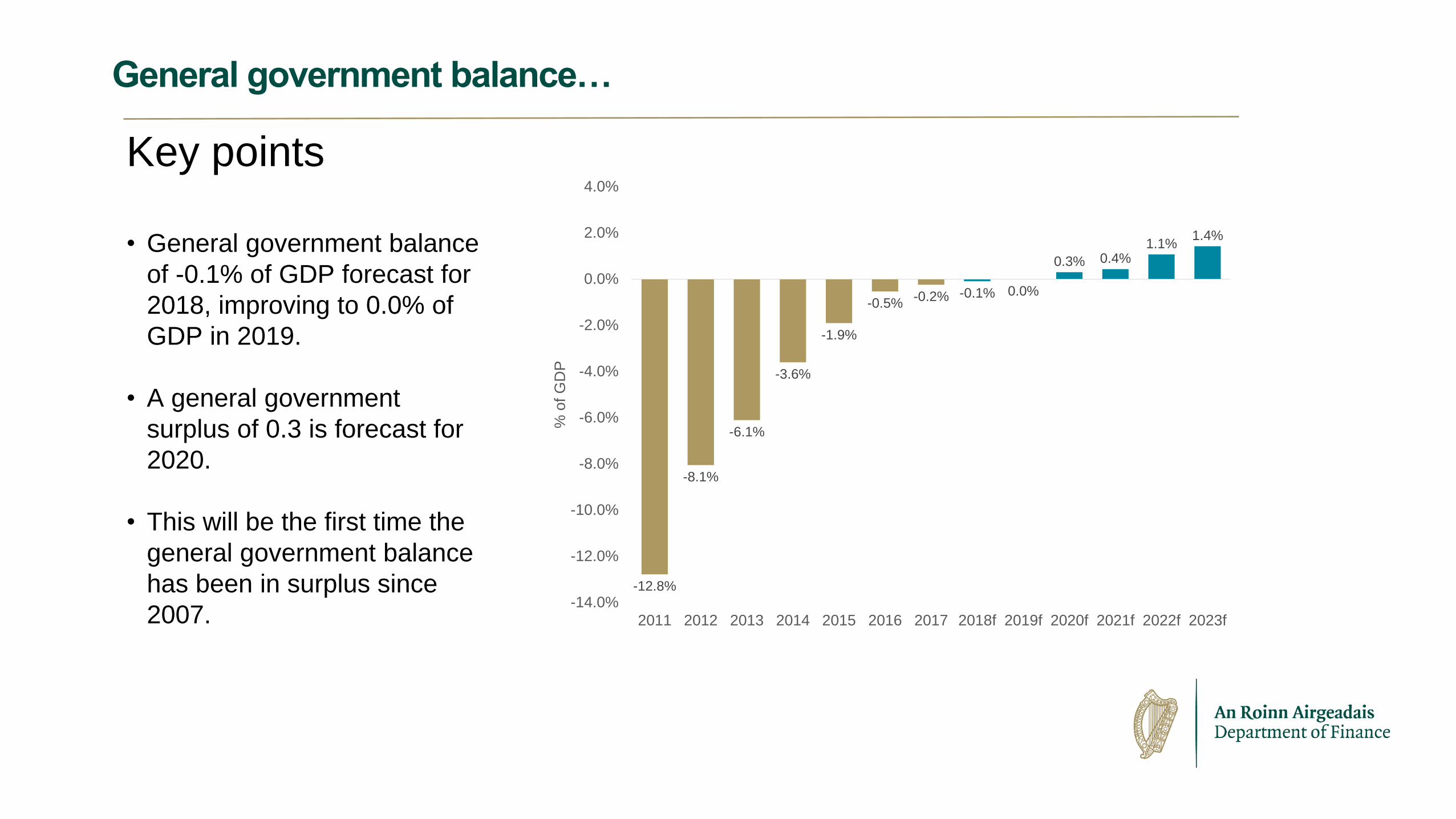

General government balance…

Key points

• General government balance

of -0.1% of GDP forecast for

2018, improving to 0.0% of

GDP in 2019.

• A general government

surplus of 0.3 is forecast for

2020.

• This will be the first time the

general government balance

has been in surplus since

2007.

-12.8%

-8.1%

-6.1%

-3.6%

-1.9%

-0.5%-0.2% -0.1% 0.0%

0.3% 0.4%1.1%

1.4%

-14.0%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

2011 2012 2013 2014 2015 2016 2017 2018f 2019f 2020f 2021f 2022f 2023f

% o

f G

DP

General government debt…

Key points

• General government debt of 64.0% of GDP forecast for 2018. This represents a 4.4 percentage point improvement on the end-2017 position. This compares to an expected 2.0 percentage point improvement at the time of the spring forecasts.

• This further improves to 61.4% of GDP in 2019.

• As a percentage of GNI* our debt ratio for 2018 is 105.2 improving by 4.2 percentage points to 101.0 in 2019.

0

20

40

60

80

100

120

140

160

180

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

General Government Debt to GDP and debt to GNI*

General Government Debt-to-GDP General Government Debt-to-GNI*

General government debt…

Key Points

• Debt interest payments as a percentage of total general government revenue is a useful way of assessing debt sustainability.

• As this measure is dependent on domestic revenue streams, it is less prone to distortion by the effects of globalisation on the Irish economy.

• Using this and alternate measures, such as debt-to-GNI* gives a more accurate read of Ireland’s level of indebtedness.

• Despite improvements the level of public debt in Ireland remains high by both historical and international standards.

• That is why it is crucial that we prioritise the reduction of this burden – a key factor in ensuring the continued stability of the public finances.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

Debt Interest to Revenue Ratio

Forecast

#Budget19

@IRLDeptFinance

www.finance.gov.ie

This presentation is for informational purposes only

No person should place reliance on the accuracy or completeness of

information which is contained in this document and which is stated to have

been obtained from or is based upon trade and statistical services or other third

party sources. Any data on past performance contained herein is no indication

as to future performances.

No representation is made as to the reasonableness of the assumptions made

within or the accuracy or completeness of any modelling, scenario analysis or

back-testing.

All opinions and estimates are given as of the date hereof and are subject to

change.

The information in this document is not intended to predict actual results and

no assurances are given with respect thereto.