presentation to investors dec 2010 - cge

TRANSCRIPT

Presentation to Investors

As of Dec. 2010

Grupo CGE One of the most important energy groups in Chile

• More than 105 years of history

• Development of long-term businesses, in key sectors

• Corporate Governance with a business view prevailing the strategic

development of its companies.

• Consolidated Group has grown strongly in the past 10 years

• Group aware of its environment and new challenges

1

Grupo CGE

• Annual Revenues for US$ 4.3 billion and Ebitda of US$ 619 million consolidated

• Main electricity distributor in Chile (2.4 million clients)

• Relevant player in Chile in liquefied and natural gas distribution

• Our electricity and gas services reach more than half of total homes in Chile

• Since June 2009, present in electricity generation in the SIC

• Presence in Argentina in the electricity and natural gas distribution

• Recently participating in the distribution of liquefied gas in Colombia

2

In process of adaptation to changes in the environment and size

One of the most important energy groups in Chile

Grupo CGE Major shareholder committed to the growth and

development of its subsidiaries

3

3.503

accionistas

Indiver

11,1%

Grupo Familia

Marín

22,3%

Grupo Almería

20,7%

Grupo Familia

Pérez Cruz

10,8%

Soc. del Canal del

Maipo

7,6%

Inv. Inst. y AFP

4,9%

Otros

22,6%

Ownership Structure - CGE Group (Dec. 2010)

Electricity Distribution

in Chile

Electricity Transmission

Electricity Generation

ServicesLiquefied Gas

& Natural Gas

Electricity and Gas

Distribution in Argentina

Liquefied Gas Distribution in Colombia

Grupo CGE A Group with Focused and Strategic Business Units

4

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Patrimonio Neto

Pasivos

Grupo CGE Taking opportunities for strategic growth

• More than US$ 3.6 billion invested during the past 10 years.

• CGE Groups invests around US$ 300 million a year for vegetative growth (capex).

• Ebitda has grown consistently.

Evolution of Consolidated Assets ($ billion)

5

Evolución of Consolidated Ebitda ($ billion)

0

50

100

150

200

250

300

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Ebitda Consolidated Dec-10MM$ 289.671 (US$ 619 million)

Ebitda Electricity Sector Dec-10MM$ 159.882 (US$ 342 million)

Grupo CGE Ebitda (1) of Electricity Sector

(1) Operating Result + Depreciation + Amortization

(2) Figures for transmission only considers Transnet S.A.

6

43%

55%

2%

Electricity

Gas

Others

Distribution

63%

Transmission

29%

Generation

8%

(2)

• In terms of physical sales, CGE Group is the second player, distributing over 11,300 GWh per year in Chile.

• CGE Group is the leading player in terms of number of clients.

• In these same terms, CGE Group supplies to a significant portion of Chile’s population.

Grupo CGE

40,2%

Grupo CGE Electricity Distribution – Market position

7

Source: Empresas Eléctricas A.G.

Physical sales

CGE Distribución

23,1%

Otras Emp. Grupo

CGE

17,0%

Chilquinta

7,8%

Enersis

40,7%

Otros

2,2%

Saesa

9,1%

Grupo CGE

43,8%

CGE Distribución

24,4%

Otras Emp. Grupo

CGE

19,4%

Chilquinta

9,9%

Enersis

30,2%

Otros

3,2%

Saesa

12,9%

Number of Customers

• Generates an Ebitda of US$ 216 million per year, 63% of CGE’s Ebitda in the electricity sector.

• CGE Group’s subsidiaries supply more than 2.3 million clients in Chile, with physical sales reaching 11,304 GWh as of December 2010.

• Group with most coverage nationwide.

• In Argentina it supplies close to 781 thousand clients, with physical sales of 3,476 GWh as of

December 2010.

Grupo CGE

332 thsd clients1.404 GWh

1.301 thsd clients6.447 GWh

53 thsd clients245 GWh

64 thsd clients235 GWh

84 thsd clients444 GWh

152 thsd clients745 GWh

87 thsd clients681 GWh

11 thsd clients43 GWh

232 thsd clients976 GWh

25 thsd clients84 GWh

8Figures as of Dec. 2010

Electricity Distribution

Grupo CGE Key figures of electricity distribution business in Chile

* Operating Result + Depreciation + Amortization

9

419478

711

1.175 1.1891.126

0

200

400

600

800

1.000

1.200

1.400

2005 2006 2007 2008 2009 2010

Grupo Emel

Edelmag

Conafe

CGE D

Evolution No. of Clients (thsd) Evolution of Physical Sales (GWh)

Operating Revenues ($ bn) Ebitda * ($ bn)

7.148 7.297

11.031 11.041 11.047 11.304

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

2005 2006 2007 2008 2009 2010

Grupo Emel

Edelmag

Conafe

CGE D

1.478 1.526

2.163 2.238 2.300 2.342

-

500

1.000

1.500

2.000

2.500

2005 2006 2007 2008 2009 2010

Grupo Emel

Edelmag

Conafe

CGE D

76 83

100

140

119

95

0

20

40

60

80

100

120

140

160

2005 2006 2007 2008 2009 2010

Grupo Emel

Edelmag

Conafe

CGE D

With the acquisition of Emel, CGE advanced its customer growth by 12 years.

Source: World Bank; data at 2007

Grupo CGE Great potential of growth of electricity sector in

Chile, moved by economic developmentk

Wh

pe

r ca

pit

a

GDP per capita in US$

Correlation between electricity consumption and GDP

Argentina

Australia

Brasil

Canadá

Chile

Colombia

DinamarcaFrancia

Alemania

Italia

Japón

Corea

México

NuevaZelandia

Perú

Portugal

Singapur

España Reino Unido

EEUU

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

0 5.000 10.000 15.000 20.000 25.000 30.000 35.000 40.000 45.000 50.000 55.000 60.000

10

� We are recovering from stable growth of electricity demand

• 2008 – 2009 � economic crisis (-)

• 2010 � earthquake (-)

� 2009 effects of VAD tariff setting and of services non-related to electricity supply (-)

� 2010 effects of tariff setting for Related Services (-), earthquake (-), IT plataform

� 2011 we expect important growth of energy consumption

• GDP between 6% and 7% (+)

• Consumption growth (+)

• Low unemployment (+)

� Correlation between electricity consumption and GDP – We expect sustained growth of electricity consumption

� Our infrastructure is prepared to move along with future growth (+)

� Growth perspectives in Argentina with fixed tarifs for the coming five years (+)

� 1Q11 – Physical sales of electricity distribution in Chile +9,1% as a reference

Grupo CGE Electricity Distribution – Perspectives & Conclusions

11

• CGE Group is the 2nd player in Chile, with 3.485 kms of sub-transmission lines extended throughout great part of the country.

• This activity generates an Ebitda of US$ 120 million a year, becoming one of the most important businesses of the CGE Group.

• Main subsidiary in the sector Transnet, which total assets reach nearly US$ 890 million.

Grupo CGE Electricity Transmission ���� Strategic support for

electricity distribution

75 km lines

2.604 km lines8.749 GWh energy withdrawn (*)

4 km lines128 km lines

209 km lines

457 km lines

9 km lines

Empresas EMEL873 km lines

(*) Corresponds to energy withdrawn from the subtransmission system.

Figures as of Dec. 2010

12

Grupo CGE Transnet S.A. is the main subsidiary of CGE Group in

this activity

Energy Withdrawn (GWh)

(*) Operating Result + Depreciation + Amortization13

7.497

8.347 8.817 8.803 8.780 8.749

0

1.500

3.000

4.500

6.000

7.500

9.000

10.500

12.000

2005 2006 2007 2008 2009 2010

Operating Revenues ($ million)

34.086

40.149

46.984

55.316 59.805

62.516

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

2005 2006 2007 2008 2009 2010

Ebitda ($ million) *

24.857

29.286

34.332

40.428 43.565

46.769

0

10.000

20.000

30.000

40.000

50.000

60.000

2005 2006 2007 2008 2009 2010

Total Assets ($ million)

PCGA IFRS

153.993 179.685

201.042

234.456

359.796

415.923

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000

450.000

2005 2006 2007 2008 2009 2010

� Stable business, highly specialized and strategic for CGE.

� Growth of this sector is correlated to the growth of the country.

� There is room to keep growing, beyond vegatative growth.

� Our infrastructured is prepared to face the future demand growth of electricity.

� 1Q11 – Withdrawal of energy + 20 %

Grupo CGE Electricity Transmission – Perspectives & Conclusions

14

Grupo CGE Electricity Generation

Potential growth through acquisitions and own

portfolio of proyects

• ENERPLUS (ex CGE GENERACIÓN) acquired from Iberdrola

100% of IBENER in June 2009.

• Total investment of US$ 294 million

• Two hydroelectric run-of-the-river power plants: Peuchén and

Mampil, with 84 MW and 49 MW of installed capacity.

• Repowering capacity to 140 MW

• Average generation of approximately 440 GWh/year.

• During 2010 Ebitda reached US$ 25 million.

IBENER

15

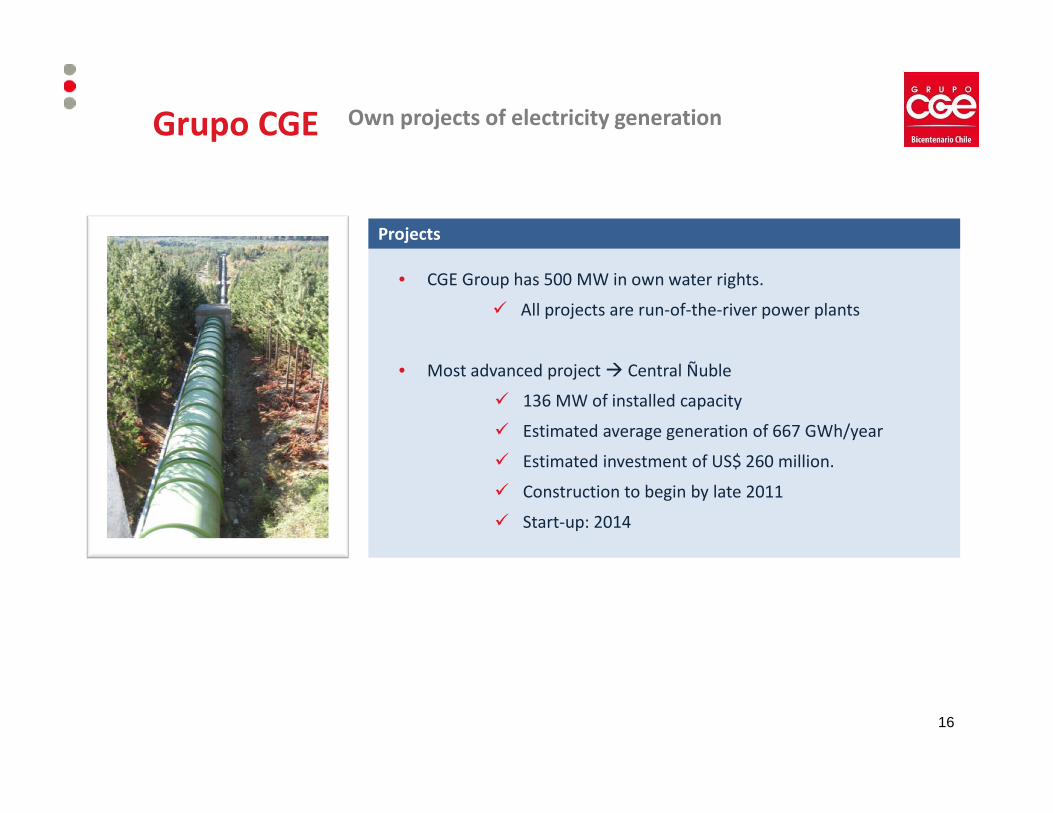

Grupo CGE Own projects of electricity generation

• CGE Group has 500 MW in own water rights.

� All projects are run-of-the-river power plants

• Most advanced project � Central Ñuble

� 136 MW of installed capacity

� Estimated average generation of 667 GWh/year

� Estimated investment of US$ 260 million.

� Construction to begin by late 2011

� Start-up: 2014

Projects

16

� One of the business units with most perspectives of growth for CGE Group

• Through own portfolio of projects � we have water rights (scarce resourse).

• A portfolio of projects is currently under studty.

• Sector growth algo through acquisitions.

• Chile needs more generation capacity, due to future demand growth and economic development.

Grupo CGE Electricity Generation – Perspectives & Conclusions

17

Consolidated Ebitda as of Dec-10MM$ 289.671 (US$ 619 million)

Ebitda Gas Sector as of Dec-10MM$ 124.223 (US$ 265 million)

Grupo CGE Ebitda (1) of Gas Sector

(1) Operating Result + Depreciation + Amortization

(2) Corresponds to the Ebitda of Gasmar

18

43%

55%

2%

Electricity

Gas

Others

Natural Gas

61%

Liquefied Gas

26%

Storage

Liquefied Gas

13%

(2)

• In this sector, CGE Group is one of the main players in Chile.

• Annual Ebitda generation in Chile of US$ 265 million, representing 43% of consolidated Ebitda.

• In Chile, we supply natural gas to more than 544 thousand customers.

• In Argentina, we distribute natural gas in the provinces of Salta, Jujuy, Tucumán and Santiago del Estero � 420 thousand customers.

• GASCO entered the Colombian market of liquefied gas distribution business through the brands VIDAGAS and UNIGAS.

Grupo CGE Distribution of natural and liquefied gas

19

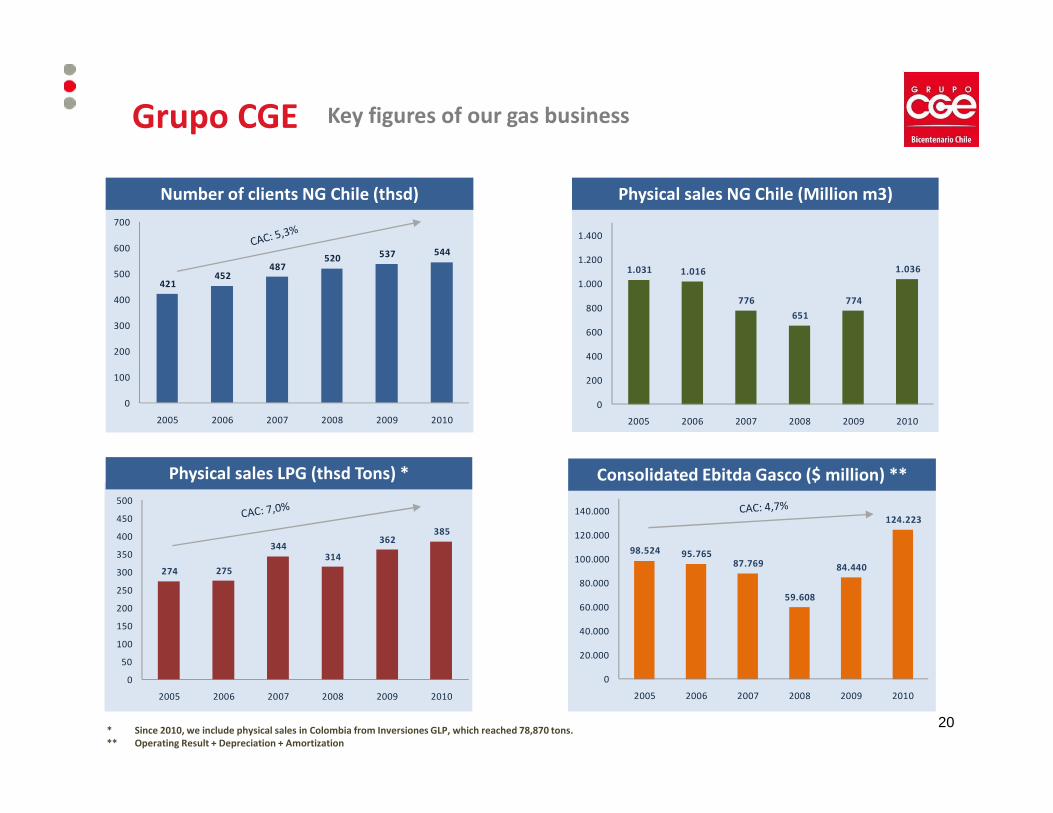

Grupo CGE Key figures of our gas business

Number of clients NG Chile (thsd)

Physical sales LPG (thsd Tons) *

Physical sales NG Chile (Million m3)

Consolidated Ebitda Gasco ($ million) **

20

421 452

487 520 537 544

0

100

200

300

400

500

600

700

2005 2006 2007 2008 2009 2010

1.031 1.016

776

651

774

1.036

0

200

400

600

800

1.000

1.200

1.400

2005 2006 2007 2008 2009 2010

274 275

344 314

362 385

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010

98.524 95.765 87.769

59.608

84.440

124.223

0

20.000

40.000

60.000

80.000

100.000

120.000

140.000

2005 2006 2007 2008 2009 2010

* Since 2010, we include physical sales in Colombia from Inversiones GLP, which reached 78,870 tons.

** Operating Result + Depreciation + Amortization

� Natural Gas

• Today we have certainty of supply � LNG terminal.

• Recovery of customers during the gas crisis � especially industrial customers.

• Electricity generators have consumed NG from the LNG Terminal in Quintero.

• We notice an important demand growth.

� Liquefied Gas

• Mature business with gradual growth expectations.

• Potential growth and expansion to other regions and countries.

• Important market share.

� Clean fuel

� GASCO promoting the use of gas as fuel for public and private transportation.

Grupo CGE Sector Gas – Perspectivas y Conclusiones

21

Grupo CGE Service activities

22(*) Operating Result + Depreciation + Amortization

ActivityEbitda *

$ million

(4.626)

7.464

3.437

2.618

1.428

1.716

Business focused on retail, call center

and satellite television

Company under development

Activities focused on IT and telecom

Supply and logistics services

Manufacturer of transformers and

electric equipment

Electricity services for distributors of

electricity

Management of CGE Group's real estate

65

75

94

107113

60

0

20

40

60

80

100

120

2005 2006 2007 2008 2009 2010

Grupo CGE Evolution of CGE Group’s Results

Ebitda ($ bn)*Operating Revenues ($ bn)

PCGA IFRS

Net Income ($ bn)

23

852 942

1.286

1.825 1.812

2.012

0

500

1.000

1.500

2.000

2.500

2005 2006 2007 2008 2009 2010

212 219 236

262 271

290

0

50

100

150

200

250

300

350

2005 2006 2007 2008 2009 2010

Total Assets ($ bn)

PCGA IFRS

1.702 1.802

2.578

3.014

3.411

3.762

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

2005 2006 2007 2008 2009 2010

(*) Operating Result + Depreciation + Amortization

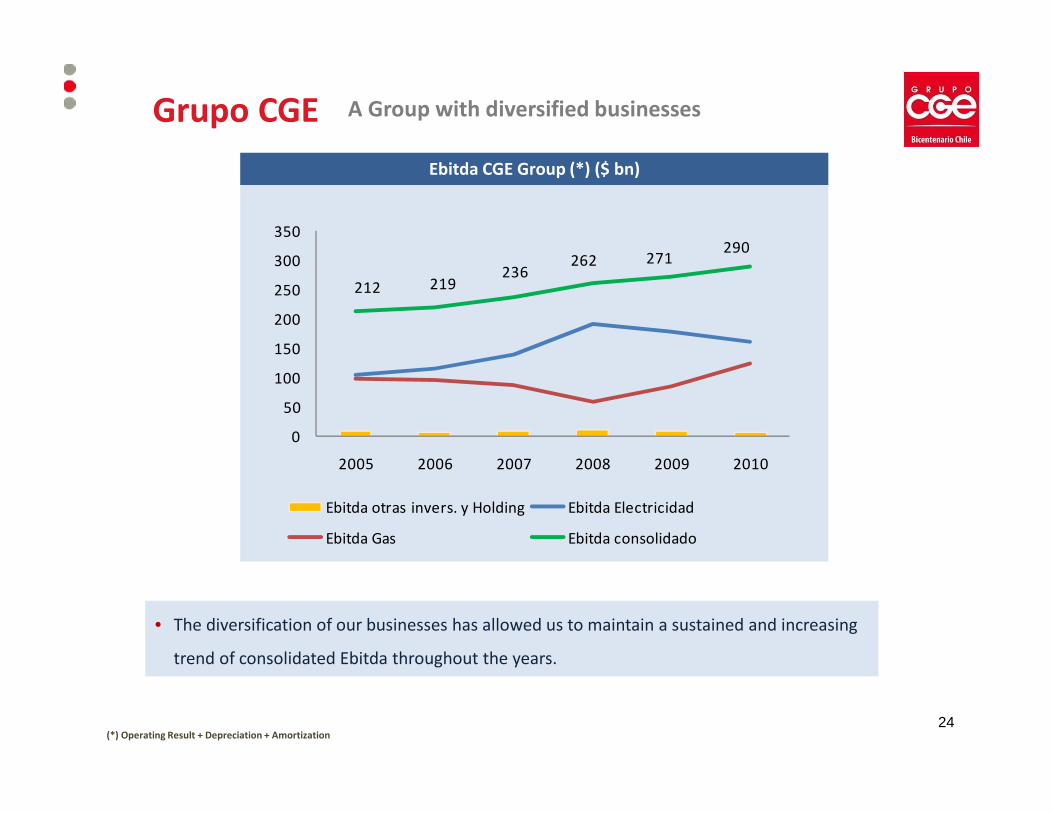

Grupo CGE A Group with diversified businesses

24

Ebitda CGE Group (*) ($ bn)

• The diversification of our businesses has allowed us to maintain a sustained and increasing

trend of consolidated Ebitda throughout the years.

212 219236

262 271290

0

50

100

150

200

250

300

350

2005 2006 2007 2008 2009 2010

Ebitda otras invers. y Holding Ebitda Electricidad

Ebitda Gas Ebitda consolidado

(*) Operating Result + Depreciation + Amortization

Grupo CGE Financial Summary

25

CGE Consolidated Dec. Dec. Dec. 2009 Dec. 2010

($ billion) 2009 2010 MMUS$ MMUS$

Total Assets 3.411 3.762 6.726 8.038

Liabilities 2.092 2.299 4.125 4.913

Equity 1.319 1.463 2.601 3.125

Operating Revenues 1.812 2.012 3.573 4.298

Operating Result 186 197 367 421

Ebitda 271 290 535 619

Ebitda Margin 15,0% 14,4% 15,0% 14,4%

Net Income 113 60 223 128

Tenor

Debt by Currency Debt by Interest Rate

Grupo CGE Financial Debt Structure as of Dec. 2010 (*)

Debt by Type

26* Financial Debt as of December 2010 reached $ 1.763 billion (~ USD 3.8 billion)

Long-

term

80%

Short-

term

20%

UF/$

94%

Foreign

6%

Fixed

66%

Floating

34%

Banks

44%

Com.

Papers

4%

Bonds

52%

Grupo CGE Ratios financieros

27

Debt Coverage (1) Interest Coverage (2) Leverage (3)

(1) Financial Debt / Ebitda(2) Ebitda / Net Interest Expenses (3) Total Debt / Total Equity

5,765,46 5,35

4,334,60

0,00

1,00

2,00

3,00

4,00

5,00

6,00

7,00

2006 2007 2008 2009 2010

1,50

1,70

1,73

1,591,57

1,35

1,40

1,45

1,50

1,55

1,60

1,65

1,70

1,75

1,80

2006 2007 2008 2009 2010

3,7

5,2 5,5

5,7 6,0

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

2006 2007 2008 2009 2010

Main fundamentals:

Grupo CGE An Investment Grade Company

• Low risk and stable cash flows

• Geographic diversification of the Group’s businesses

• Main business operates under a consolidated regulatory framework

• Recovery and natural gas business due to the start-up of GNL Quintero

• Good access to the financial market

28

Local Rating Shares BondsCommercial

Papers

Feller-Rate Nivel 2 AA- AA-/Nivel 1+

Fitch Ratings Nivel 2 A+ A+/F1+

International RatingDebt

Local Currency

Debt

Foreign Currency

Standard & Poor's BBB- BBB-

Fitch Ratings BBB BBB

Grupo CGE Main Conclusions and Challenges

• Consolidated Group and has grown strong over the past 10 years

• Strategic view with a long-term perspective to continue responding to the energy needs of the country.

• In a stage to achieve return on our investments

• Adapting to changes – organizing business units for higher efficiency and synergies

• Investment plan for US$ 330 million for maintenance and US$ 250 million for special projects

29

We have the energy for Chile’s development