presentation to investors november ... - the navigator …

TRANSCRIPT

P r e s e n t a t i o n t o I n v e s t o r s

N o v e m b e r 2 0 2 0

This presentation is intended to provide a general overview of The Navigator Company S.A.’s business and does not purport to deal with all aspects and details regarding The Navigator Company S.A.. Accordingly, no representation, undertaking or warranty, expressed or implied, is given by The Navigator Company S.A. or any of its subsidiaries’ undertakings, affiliates, directors, officers, employees or advisors or any other person as to the fairness, accuracy, completeness or correctness of the information or opinions contained in this presentation or of the views given or implied or any other material discussion in connection with this presentation.

This presentation has been prepared by The Navigator Company S.A. for information purposes only. The Navigator Company S.A. or any of its affiliates, directors, officers, employees or advisers or any other person shall not have any liability whatsoever (including in case of omission, negligence or otherwise) for any losses, errors or omissions howsoever arising, directly or indirectly, from any use of this presentation or its contents or otherwise arising in connection therewith or with respect to their reliance upon the completeness and accuracy of any such information, as well as any damages resulting hereof.

DISCLAIMER

1

T A B L E O F C O N T E N T S

2

Solid & Resilient Business Model

Expansion & Diversification

01 02 03 04Sustainability at

the Core

Performance, Market Update

& Outlook

<<

3

NAVIGATOR IN BRIEF

A solid business model, with significant resilience in adverse market conditions

Expansion and diversification of business portfolio into the growing tissue segment, with other growth options available

Focused on efficiency and committed to additional cost reduction programs

Sustainability at the core – investing in people, aiming to be a leader in sustainability and delivering sustainable returns

Performance, Market update & Outlook

<<

THE NAVIGATOR COMPANY an integrated producer

R & D

F O R E S T

P U L PE N E R G Y

P A P E R

T I S S U E

130,000 ton Reels;120,000 ton Converting*

1.6 M tonof UWF paper

2.5 TWhof electricity

Leader in Eucalyptus globulus cloning

108,000 ha of forest(under management)

1.6 M ton of BEKP pulp(0.350 M market pulp)

4

(*total nominal capacity)

<<

NAVIGATOR IS THE LEADING MANUFACTURER of UWF paper in Europe

19%

16%

12%12%

10%

31%

Nº1 in European UWF fine paper by capacity, with the largest and most modern mills

European uncoated fine paper* Main players

Uncoated woodfree (UWF)European mills

Velsen-Noord

Stockstadt

Alizay

Hernani

Fabriano

Munkedal

Etival

Theresienthal

Nymolla

Figueira da Foz

Kymi

Others

Others

Kostrzyn**

Ruzomberok **

Veitsiluoto

Setúbal

Nordland

Kwidzyn**

Syktyvkar*

0 200 400 600 800 1000 1200 1400 1600

SAPPI

Crown Van Gelder

Zicuñaga

Clairefontaine

Fedrigoni

Double A

Arctic Paper

UPM

International Paper

Stora Enso

Mondi

Capacity, 1000 ton/year

Saillat Svetogorsk *

The Navigator Company

Mondi

IP

Stora Enso

UPM

Other

*Excluding value-added products (ex.: carbonless papers, termal papers,colorful papers, engineering papers, specialty papers, etc)

Integrated

Non Integrated

5

Kematen

5* Mill located in Russia; ** mill located in Poland and Slovakia

<<

BASED ON LARGE SCALE PRODUCTION MILLS with state-of-the-art technology

FIGUEIRA DA FOZ

• Pulp (Integrated) – 650,000 tAD

• Paper – 790,000 ton

The Navigator Company operates world class state-of-the-art-assets with a global capacity of:

1.6 Mtons of UWF - 1.6 Mtons of BEKP – 130 ktons of Tissue Reels

VILA VELHA DE RÓDÃO

• Tissue – 60,000 ton reels;65,000 ton converting

SETÚBAL

• Pulp (Integrated) – 550,000 tAD

• Paper – 775,000 ton

CACIA

• Pulp (Market) – 350,000 tAD

• Tissue – 70,000 ton reels; 55,000 ton converting*

6(*total nominal capacity)

<<

*Other includes forest **Revenues by geography of pulp, paper and tissue ***Includes all energy sales in Portugal

The Group exports around 83% of pulp, paper and tissue products

WITH A MORE DIVERSIFIED BUSINESS AND GLOBAL SALES TO 130 DIFFERENT COUNTRIES

Revenue diversification over the last 5 years with the entry into the tissue business and pulp debottlenecking, with a diversified customer base selling across 130 different countries

7

76% 71%

7% 10%

15%10%8%

2% 2%

2014 2019

Other

Tissue

Energy

Pulp

Paper

15% 19%

62% 50%

12%11%

11% 20%

2014 2019

Other

America

Rest ofEurope

Portugal***

Revenue by Geography**Revenue by business area

<<

78%Total Sales

1,2 MReams/day

WITH A DIFFERENTIATION STRATEGY based on the highest quality paper products and own brands

Product and brand differentiation strategy have skewed the Group’s product mix to the high end market, allowing up to 7% price premium advantage (in Europe)

2019 The Navigator Company

Europe industry average*

Premium products 52% 14%

Mill Brands 70% 20%

Sheets 75% 69%

Operating rates 100% 90%

* Estimated industry average including Navigator

Source: Euro-Graph; EMGE

8

Mill Brand Sales equivalent to:

930M€

<<

9

A STRONG POSITIONING IN UWF MARKET

The use of an excellent raw material such as the Eucaliptus Globulus fiber, modern and efficient plants and an experienced workforce – allows the production of high quality paper and the emphasis on premium

products

50-60%

30-45%

0-10%

10-15%

20-30%

60-70%

Premium

Standard

Economy

World Market (e) Navigator NVG market share in Western Europe

20%

22%

21%

13%

~50%

Total

Cut-size

Folio

Reels

Premium

<<

9%

50%

LEADING MARKET PLAYER IN UWF SEGMENT

10

For every 3 office paper reams exported from Europe

2 are made by Navigator

2%

52%

2% 4%2%

57%

14%

55%

3%

5%

North America

17%

Europe

Wes

tern Eastern

Middle East

Latin America

Africa World

UWFOffice Paper

Market Share

*) Market Share - indicates the Share of Navigator’s Sales per Consumption (Risi); Share of European Exports – indicates the share of Navigator’s Deliveries per European Deliveries (Euro-Graph).

NVG Market Share* Share of European Exports* (exc.RU)

60%16%

11%

8%5%

Paper Sales Distribution

Europe

Africa

Middle East

North America

Latin America

<<

ATF FIG

SET

300

350

400

450

500

550

600

650

700

750

800

850

900

0% 20% 40% 60% 80% 100%

€/ton

Capacity

AND WITH A VERY EFFICIENT CASH COST STRUCTURE

4Q 2019 UWF Cash costs, Europe, €/t

Navigator’s mills are very well positioned in the cash cost curve

Partial/Non Integrated

Changes in demand might accelerate closures from less efficient (and smaller) players and conversions to other types of products

NVG estimates that roughly:

• 2.5 M tons with cash costs above 550 €/ton (38% of European capacity*)

• During Q2 many paper machines reduced production and YTD August operating rates in the European industry stand at 75% (NVG OR- 80%)

*excluding Russia, UWF specialties papers and recycled grades

Source: Fast Markets RISI

11

Mills located in Russia and

Eastern Europe

<<

Source: Euro-Graph; EMGE; RISI 12

Evolution of UWF Europeanapparent consumption

8.7 8.7 8.7 8.1 8.2 8.2 8.1 7.7 7.5 7.5 7.5

7.2 7.6 7.3 7.0 7.0 7.0 6.9 6.7 6.6 6.4 6.1

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Capacity Apparent consumption

Mill

ion

of t

ons

Evolution of UWF USAapparent consumption

10.8 10.0 9.8 9.4 9.1 8.1 8.0 7.9 7.8 7.4 6.89.2 9.1 8.7 8.2 8.2 7.8 7.8 7.5 7.0 7.0 6.5

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Capacity Apparent consumption

Mill

ion

of t

ons

PRODUCING ONE OF THE BEST PERFORMING GRADES IN PRINTING AND WRITING: UWF

2009-2019:Change in capacity of -1.2 MtonsChange in demand of -1.1 MtonsAverage operating rate of 90%

2009-2019:Change in capacity of -4 Mtons

Change in demand of -2.7 MtonsAverage operating rate of 90%

In the last 10 years, UWF capacity has been adjusting to the reduction in consumption

UWF resilience comes from its:

Universality: available for purchase by many

different customer segments, from both B2B

and B2C

Versatility: end use options are wide

13

Uncoated

Woodfree Mechanical

CoatedHigh-end magazines &

Communication materials(flyers, brochures, posters…)

UncoatedTrade books, directories

CoatedMagazines &

communication materials

Printing & Writing

Graphic Papers

UWF IS LESS EXPOSED TO DIGITALIZATIONThere are different grades to different uses and UWF is less dependent on media and advertising

<<

ECONOMICAL SOCIAL / CULTURAL

PAPER ROLES PAPER APPLICATIONS

Demand Drivers

Emp. in Services (esp. Knowledge sector)

Population growthEducation attainmentAgeingPublicity spending

EducationScience ProductionIndustrial ActivityReading habitsInformation SocietyContent CreationPlastic PhobiaDigital Fatigue

To Think

To Present

External CommunicationsLetter & AgreementsDirect MailBooksPackagingPaper to writeDraw & create

GDP, ExRate, Public Finances, (Un)Employment, Inflation, Credit Coverage, Political Stability,Social Tensions

ECONOMICAL/POLITICAL

To Protect - Storage /

Archival

+ Packaging/ Envelope for Direct Marketing/Tags /Bags /Cards + etc.

Source: NVG

UWF is Universal (everywhere to everybody) and Versatile (addressing multiple applications)

14

UWF MARKET DEMAND DRIVERS <<

0

5

10

15

20

25

30

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

M tAD

China BEKP (% of World)4%

12%

20%

30%

41%

China SW (% of World)

7%

35%

Source: PPPC; NVG *Other include Hardwood other than BEKP, UKP and Sulphite.

13% 21%30%

PULP DEMANDMarket Pulp by main grade

15

ChinaM tAD 2000 2019 L5Y (Mt/y)SW 1.4 9.1 0.5

BEK 0.3 10.3 0.9

Other 0.7 4.5 0.3

Total 2.4 24.0 1.6

WorldM tAD 2000 2019SW 18.9 26.4

BEK 6.6 25.5

Other 13.1 12.5

Total 38.6 64.3

<<

16

Pulp Sales300 - 400

ktons

Market ShareWorld Europe

1.2% 2.7%

BEKP

Focus on Value Added Segments in Europe

Decor & Specialities allows for a 5-6% price premium over other segments:

32% 73%Of total demand in Europe* In NVG mix**

6.1% MS in Europe

Decor & Specialities

6%

21%

73%

0%

Fine Papers

Decor & Spec

32%23%

41%

4%

Tissue Fine Papers

Decor & Spec

Others Tissue Others

Indu

stry

Navigator

European leader in BEKP production

Source: NVG; PPPC; RISI * Euca Demand by End-Use in Europe in 2019 (PPPC) ** NVG sales 2019 in Europe

PULP NAVIGATOR POSITIONING <<

UWF PAPER VS PULP: REDUCED VOLATILITY & MORE STABLE RETURNS

Index FOEX PIX (Europe) – Gross Prices

A4 – B Copy: index for uncoated woodfree paper (80 g/m2)

BHKP: index for bleached hardwood kraft pulp (eucalyptus or birch)17

EUROPEAN MARKET PAPER PRICE – A4 B-COPY AND BHKP (IN €)

500

550

600

650

700

750

800

850

900

950

1000

1 9 17 25 33 41 49 4 12 20 28 36 44 52 8 16 24 32 40 48 4 12 20 28 36 44 52 8 16 24 32 40 48 4 12 20 28 36 44 52

Eur

/Ton

Week

A4 B-copy BHKP

2015 2019 20202016 2017 2018

18

Navigator has been permanently focus on optimizing its production processes and its cost reduction initiatives

Cost optimization and operational efficiency plan implemented at the start of 2020:

Bringing together the existing M2 and Corporate ZBB programs Launching a Digital Transformation project in the corporate sector

Covid-19 pandemic compelled a reassessment and extension of the scope and depth of the cost reduction initiatives originally envisaged

Target for 2020 to reduce fixed costs by € 46 million

€ 30 million achieved already in 9M 2020

FOCUS ON COST EFFICIENCY <<

T A B L E O F C O N T E N T S

19

Solid & Resilient Business Model

Expansion & Diversification

01 02 03 04Sustainability at

the Core

Performance, Market Update

& Outlook

<<

20

€131 M

ORGANIC DEVELOPMENT AND DIVERSIFICATION IN THE LAST GROWTH CYCLE

25 36 4387

143127 93 72

129 15

2015 2016 2017 2018 2019

Capex (M€)

GrowthCycle

CurrentBusiness

€158 M€152 M

€129 M

€115 M

€216 M

Tissue: 190 M€

Pellets: 115 M€

Pulp expansion:

125 M€

Heavyweights: 12 M€

Growth cycle included:

• From 2015 until 2018, Capex included essentially growth projects that have allowed NVG to diversify its business

• In 2019, capex included mainly maintenance /efficiency, regulatory/environment (~33 M€ for environment) and completion of expansion projects

• In light of the Covid-19 the capex plan for 2020 was significantly revised downward from 158 M€ to circa 90 M€; 2020 plan will include mainly maintenance /efficiency and regulatory/environment (80% of investment spending in 2020 is related to maintenance and projects that started in previous years)

<<

Diversification of The Navigator Company’s

portfolio(Representing currently 10% of

Navigator’s sales, tissue business is an important

growth platform option for the future)

Synergies with our core business

(raw material Eucalyptus globulus)

Ability to develop a competitive advantage with pulp integration

(cost and quality advantage)

State-of-the-art technological

solution

(The Navigator Company’s DNA)

After entering the tissue business in 2015, Navigator doubled its capacity in 2018, with the construction of a new 70 Ktons integrated machine in Aveiro.The growth in the tissue business has a strong strategic rational:

21

GROWTH IN THE TISSUE BUSINESS <<

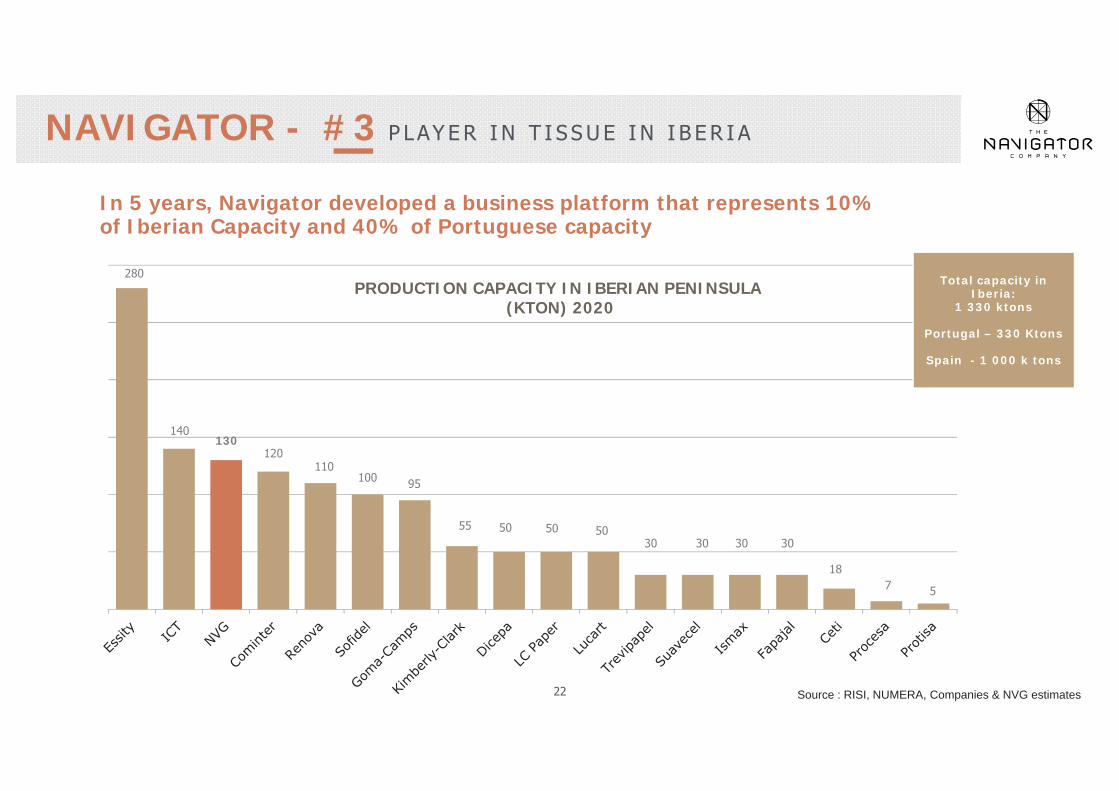

NAVIGATOR - #3 P LAY E R I N T I S S U E I N I B E R I A

PRODUCTION CAPACITY IN IBERIAN PENINSULA (KTON) 2020

22

280

140130

120110

100 95

55

718

30303030505050

5

Source : RISI, NUMERA, Companies & NVG estimates

Total capacity in Iberia:

1 330 ktons

Portugal – 330 Ktons

Spain - 1 000 k tons

In 5 years, Navigator developed a business platform that represents 10% of Iberian Capacity and 40% of Portuguese capacity

<<

Growth opportunity driven by increased demand in Asia and worldwide supply limitations

Attractive fundamentals of Mozambique:• High Forest productivity • Proximity to Asia• Land available at competitive costs

Geographic diversification within the core business of The Navigator Company

23

MOZAMBIQUE PROJECT

P h a s e 1 :W o o d c h i p M i l l

Project Phases Strategic Rationale

P h a s e 2 :P u l p M i l l

Investment: USD 260 M(USD 100 M already invested)

40 000 ha planted area

Investment: USD 2.5 B

8000 jobs opportunities

<<

MOZAMBIQUE PROJECT UPDATE

• Navigator has been working with the Mozambique Government under the terms of the MoU signed in 2018, in particular on infrastructures and logistics and land and development issues.

• This has included the first Outgrower Support program in Mozambique, a government initiative funded by the World Bank, with the aim to promote small and medium scale sustainable commercial private forestry plantations, and restoration of degraded areas. In the first 2019-2020 season, plantations were established over an area of approximately 550 hectares and 1200 hectares are estimated for the next season 2020-2021.

• Portucel Moçambique (PM) played an active role providing wide-range support by designing the silviculture model, supplying clonal plants and offering access to fertilizers. When the plantations are ready for harvest, PM will have first option on purchase of the wood.

• The Government of Mozambique referred the strategic importance to the country and to the Zambéziaprovince of building the port of Macuse, in order to develop commercial farming and forestry.

24

<<

FOCUSED ON BUILDING THE FUTURE BIO-ECONOMY

RAIZ & Inpactusproject

Plantation trees Forestry residues

Biorefinery

Biomass deconstruction & separation

processes

1 ton wood Pulp

Fibers

Chemicals & energy recovery

(combustion)Pulping By-products

Biomass components

Paper

Tissue

Market pulp

Heat and electricity

BiochemicalsBioproductsBiomaterials

Examples of possible bioproducts from biorefinery

Essential oils

Sugars for bioethanol and bioplastics

Thermoplastic bio composites

Lignin-based foams for thermo insulation

Bacterial cellulose for biomedical applications

Nanocellulose for paper coating and food additives

25

CREATING INNOVATIVE PRODUCTS & TECHNOLOGIES

A co-promotion R&D project between industry and academia.A step forward to a green, global, sustainable and competitive bioeconomic environment in Portugal, based on eucalyptus pulp and paper industry!

RAIZ & Inpactus project

180Researchers/Technicians

50Research grants

2Invited chairs

15.3M€Total budget

26

T A B L E O F C O N T E N T S

27

Solid & Resilient Business Model

Expansion & Diversification

01 02 03 04Sustainability at

the Core

Performance, Market Update

& Outlook

<<

SUSTAINABILITY AGENDA

Navigator’s sustainability goals for 2020-25 (based on materiality assessment):

• Sustainable forest management

• Energy and climate

• Industrial environmental management

• Talent Management and development of

human capital

• Occupational health and safety

• Sustainable supplier Management

• Customer satisfaction

• Community engagement

• Innovation, Research & Development

28

“It´s thinking about people, their quality of life and the future of the planet that inspires and motivates us. We want to share the wealth we create, but also our knowledge, our experience and our resources, all in the name of a better future.

That is why we are committed to creating sustainable value for our shareholders, and for society as a whole, leaving a better planet for future generations, through natural products that are sustainable, recyclable and biodegradable, that help to capture carbon and produce oxygen, that protect biodiversity, improve the soil and

combat climate change.”

<<

Forest

• ≥ 75% national certified wood by 2025

• ≤ 1% of burned area

Industrial Operations

• 87% of waste recovery by 2025

• 15% reduction in specific water consumption

Community engagement (Mozambique

Project)

• Inclusive business model with the local communities

• Investment in infrastructures

Talent• Develop H.Resources

with skills needed to pursue Company Strategy: 75% of critical areas covered by internal trainees

• Internal succession: target to achieve 75% of succession places filled by 2025

Climate

• Carbon Neutral Mills by 2035

• 85% of Renewable energy by 2035

• over 10% reduction of specific energy consumption

29

MAIN SUSTAINABILITY GOALS FOR 2020-25 <<

AT THE HEART OF WHAT WE DO IS THE FOREST, a natural and renewable resource

5.3 Million t CO2 eq

12 MillionPlants produced at Portuguese

Nurseries

108.269ha

Forest under management in Portugal

Million3.3 Investment in protection

against forest fires

RAIZForest and Paper Research Institute

Improve foresty management

Increase eucalyptus Yields

30

234Species of Fauna

740Species of Flora

ADDRESSING CLIMATE CHANGE BY BECOMING ACARBON NEUTRAL COMPANY

The Navigator Company is committed to achieve Carbon Neutrality at its industrial sites by 2035,15 years ahead of schedule, by investing € 154 million in the implementation of changes in its production processes in order to minimize the use of fossil fuels

GOAL 1100% of electrical energy production from renewable sources

GOAL 2Reduce fossil fuelCO2 emissions with implementation of cleaner technologies

GOAL 3Reduction of 10% of the specific energy consumption from 2015 until 2025

GOAL 4Carbon offsettingfor unavoidablecarbon emissions

31

ROADMAP TO CARBON NEUTRALITY BY 2035

86% reduction of CO2 emissions, approximately 667 ktCO2/ from 2018 until 2035, with an investment of 154 million €

CO2 Expected Emissions

774 744 730

512 512 488 460 455378 350 350 308

107

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2035

CAPEXIn Million €

8

1928

1220 17

4 5 813

19

1

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2035

Reduction of

667kton CO2

CAPEX

154M€

Ktons86%

32

<<

33

Navigator is already the biggest national producer of renewable energy through biomass and subproducts of wood, representing up to 60% of the Group´s total energy capacity

The new biomass boiler will increase significantly the capacity production based on renewable resources (from 60% to 70%)

Installed capacity

2,5 TWh/Year(enough to supply the entire region of the

Algarve for a year ).

3 Biomass cogeneration

plants

+2 Natural Gas cogeneration

plants

+2 Biomass plants

~5%Of the National electricity

production

(produce exclusively electricity to the

portuguese network)

=

NEW BIOMASS BOILER AT F.FOZ

Biomass Boiler – Capex of € 55 million

Steam generation capacity of 128 MWth, to supply paper machines 1 and 2

Project is being finalized and testing began at the end of Q3; ramp-up will last from Q4 2020 and Q2 2021

Reduction of CO2 emissions by 20% for Navigator as a whole (reduction of 155 ktons of CO2/year). F.Foz mill steam an electricity generation will be 100% from renewable

Expected significant savings in costs (reduction in purchase of natural gas and maintenance costs)*

Total Capex of € 55 million

* 2018 Feasability study estimated €14 million savings / year; depends on natural gas prices

<<

ENERGY – SOLAR PHOTOVOLTAIC

RAIZ Institute (2019)342 solar panels

94 kW of installed capacity(satisfies 30-35% of the institute’s

consumption).

The energy generation through renewable energy sources constitutes one of the company’s strategic axis, this is shown through relevant investments in solar plants in self consumption regime.

Navigator Paper Setúbal (2016)8 800 solar panels

2.2 MW of installed capacity(the biggest solar photovoltaic plant installed in

industrial environment in Portugal, enough to supply 850 households for a year).

1 140 t CO2 emissions/year avoided

Herdade de Espirra (2018)352 solar panels

112.6 kW installed capacity(supplies ~30% of the consumption

of the Herdade de Espirra).

U P C O M I N G P R O J E C T S ( 2 0 2 2 )• Navigator Pulp Setúbal: 4 680 solar panels

(installed capacity 1.8 MW);

• PM2 Figueira da Foz: 7 700 solar panels (installed capacity 2.7 MW).

34

<<

80%Waste

Recovery Rate

90%Renewable

raw materials

Solar power plant 3,1 GWh/year

Saving1.140 t CO2 /year

80% of water intake is returned to

the environment

64%of paper is sold with FSC*, PEFC or Ecobel

seals of approval

More than

67%Primary energy used

from renewable sources (biomass)

I N D U S T R I A L O P E R A T I O N S

Fiber optimization

Bioproducts and biofuels research

*pulp and paper

35

<<

Mozambique project

36

$6 Million invested

In the Community Development

Program

250 employees90% Mozambicans

30% women

Increasing household

income And decreasing the poverty rate in the

provinces of Zambezia& Manica

5300 km of new roads and

rural pathsAllowing better access to public transportation, to healthcare & to markets

Securing families welfare

Delivering food security and

generating income to 7.000 families

24 new water boreholes

Making potable water available to communities

2300 families received solar lamps

Can also be used to charge devices and allows children to study after sunset

I M P A C T O F S O C I A L P R O G R A M *

* Reference to the end of 2019

<<

INVESTING IN PEOPLE & TALENT MANAGEMENT

37

G E N D E R D I V E R S I TY

G E N D E R D I V E R S I TY 3280

Employees in 2019

W O R K F O R C E R E J U V E N AT I O N

( 2 0 1 3 - 2 0 1 9 )

W O R K F O R C E R E J U V E N AT I O N

( 2 0 1 3 - 2 0 1 9 )

T R A I N I N G&

L E A R N I N G C E N T E R

T R A I N I N G&

L E A R N I N G C E N T E R

Middle and Senior management

70% - Male 30% - Female

Training Hours: 182,740h59h/ Employee

Management Courses: 117 courses/300 hours

Internal Training: 200 courses/165 hours

Average reduction of 6.5 years

Distribution by age:11% < 30 years

56% between 30 – 50 years33% > 50 years

Headcount 3280*

Setúbal1,157

Figueira da Foz1,008

Aveiro503

Vila Velha de Ródão226Portucel

Mozambique157Others

locations in Portugal

146

International sales offices

83

* Dec.2019

<<

ENGAGING WITH STAKEHOLDERS

Main forest certification schemes

Currently Vice-President of PEFC Portugal

38

WWF lead initiative to share knowledge about well-managed plantations and learn from others' good examples with top P&P companies and Governments

SteerCo member of this Yale University based initiative focusing on forests and their role in promoting improving the livelihoods of local communities

Members and part of the WBCSD’s ExCoForest Solutions Group – core members

C o r p o r a t e i n i t i a t i v e s t o d r i v e S u s t a i n a b l e D e v e l o p m e n t

M u l t i s t a k e h o l d e r i n i t i a t i v e s

Engaging in projects to debate SDG implementation, the Future ofWork, Human Rights, Circular Bio-Economy and a Vision for 2050

Presidency of BCSD Portugal, anaffiliate of WBCSD

<<

T A B L E O F C O N T E N T S

39

Solid & Resilient Business Model

Expansion & Diversification

01 02 03 04Sustainability at

the Core

Performance, Market Update

& Outlook

<<

40

FINANCIAL INDICATORS

2 0 1 5 2 0 1 6 2 0 1 7 2 0 1 8 2 0 1 9Million euros

Turnover 1,628 1,577 1,637 1,692 1,688

EBITDA 390 397 404 455 372

EBITDA/Sales (%) 24% 25% 25% 27% 22%

CAPEX 148 139 115 216 158

Free Cash Flow 81 184 198 211 186

Net Debt 655 640 692 683 715

Net debt/EBITDA 1.68 1.61 1.72 1.50 1.92

ROCE 16% 12% 14% 16% 13%

ROE 15% 18% 17% 19% 15%

<<

41

MAIN FINANCIAL AND OPERATIONAL HIGHLIGHTS

1,542

1,628

1,577

1,637

1,692 1,688

2014 2015 2016 2017 2018 2019

Turnover (M €)

328390 397 404

455

372

2014 2015 2016 2017 2018 2019

EBITDA (M €)

292 304

385 357 377307

2014 2015 2016 2017 2018 2019

Operational Cash Flow (M €)

1,564 1,555 1,587 1,5781,513

1,447

2014 2015 2016 2017 2018 2019

Paper sales (ktons)

257 253291 311

253314

2014 2015 2016 2017 2018 2019

Pulp sales (ktons)

37 3951 55 63

96

2014 2015 2016 2017 2018 2019

Tissue sales (ktons)

<<

24%

14% 18

%

13%

13% 16

%

25%

12%

15%

16%

14% 15

%

24,7

%

11%

17%

16%

16%

16%

27%

13%

18%

17,4

%

18% 20

%22%

10%

17%

18%

15%

15%

The NavigatorCompany

Competitor 1 Competitor 2 Competitor 3 Competitor 4 Competitor 5

2015 2016 2017 2018 2019

VERY FAVOURABLE COMPARISON WITH PEERS

Source:Euro-Graph; EMGE* Average does not include Navigator

EBITDA Margin - Paper Peers (2015-2019) Average for 2015-2019*: 15%

42

<<

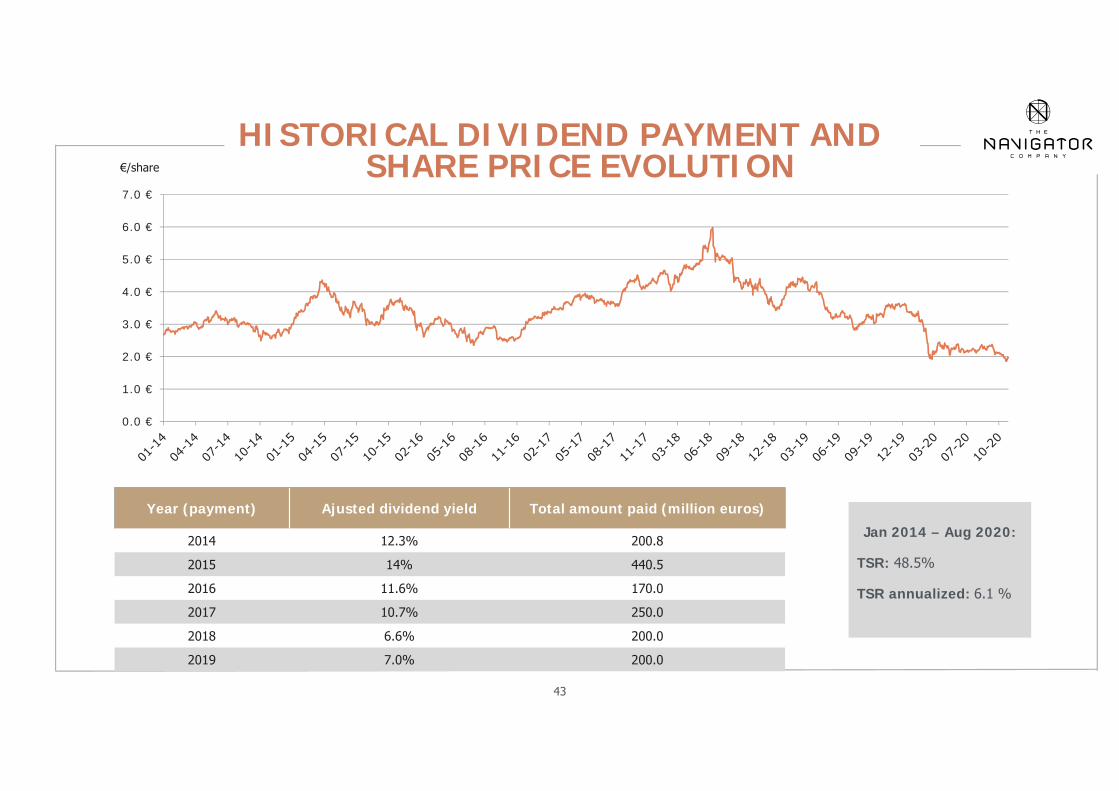

HISTORICAL DIVIDEND PAYMENT AND SHARE PRICE EVOLUTION

Year (payment) Ajusted dividend yield Total amount paid (million euros)

2014 12.3% 200.8

2015 14% 440.5

2016 11.6% 170.0

2017 10.7% 250.0

2018 6.6% 200.0

2019 7.0% 200.0

43

Jan 2014 – Aug 2020:

TSR: 48.5%

TSR annualized: 6.1 %

€/share

0.0 €

1.0 €

2.0 €

3.0 €

4.0 €

5.0 €

6.0 €

7.0 €

<<

1Protect the

core business

2 Consolidate and clarify the options of organic

growth

3Reinforce the

focus on efficiency and

cost management

4 Continue to

invest on our people as a

key asset for the future

5 Align the

company’s external

positioning with the core

priorities

Financial Goal: Preserve company’s value, operating under the norms of shareholder’s remuneration.

MANAGEMENT PRIORITIES

44

<<

45

• Gradual reopening of economies and progressive recovery of paper demand during Q3

• Navigator registered significant improvement in paper volumes, with all its paper machines working at full capacity since July

• Strong operating performance in pulp and tissue continued during Q3, even though pulp prices remained under pressure

• Continuous focus on cost reduction and efficiency improvements allowed a 36% growth in EBITDA vs Q2 2020, to € 70 million and a margin of EBITDA / Sales above 20%

• Navigator maintains a strong ability to generate cash flow: € 56 million FCF achieved in the Quarter, totaling € 170 million YTD September

• Continuous reduction in Net Debt, with Net Debt / EBITDA at comfortable levels; successful renegotiation of debt maturing in 2021

• Q3 performance reflects the resilience of Navigator´s business model

Q3 2020 PERFORMANCE OVERVIEW

<<

46

Performance in 2020 was negatively impacted by a severe decline in consumption of UWF across the world due to the Covid-19 pandemic and the general lockdowns of economies

Turnover in the first 9 months declined 18% YoY on the back of decreased paper volumes and lower pulp and paper prices

Increase in pulp and tissue volume and significant improvement in production costs (variable & fixed) mitigated sales and price drops

EBITDA reached € 210 million with a margin EBITDA / Sales above 20%

Significant free cash flow generation of €170 million sustained by efficient working capital management and reduced capex disbursements

Strong balance sheet, with Net Debt reducing by € 132 million YoY to € 644 million; 100 M€in reserves paid to shareholders in January

9M 2020 Financial Highl ights

In millions € 9M2020

9M2019

ChangeQ1-Q319/20

Q32020

Q22020

Change QoQ

Turnover 1.044 1.274 -18% 348 290 +20%

EBITDA 210 300 -30% 70 52 +36%

EBITDA /Sales 20.2% 23.6% -3.4pp 20.2% 17.8% + 2.4pp

CAPEX* 70 119 -49 21 26 -5

Free Cash Flow 170 125 +50 56 99 -43

Net Debt 644 776 -132 644 700 -56

Net Debt/EBITDA 2.28 1.87 0.41 2.28 2.29 - 0.01

* Capex cash out was 43M€

<<

Source: FOEX

EUROPEAN MARKET PAPER PRICE – A4 B-COPY AND BHKP (IN €)

47

PULP & PAPER PRICES IN 9M 2020 <<

Average A4 B-Copy price

2014-18 2019 Q1-Q3 2020

EUR 832 903 846

500

550

600

650

700

750

800

850

900

950

1000

1 9 17 25 33 41 49 4 12 20 28 36 44 52 8 16 24 32 40 48 4 12 20 28 36 44 52 8 16 24 32 40 48 4 12 20 28 36 44 52

Eur

/Ton

Week

A4 B-copy BHKP

2015 2019 20202016 2017 2018

With market discounts increasing, net pulp prices are currently at the lowest level since the begining of 2000 (and 2009); the recent devaluation of the USD vs the Euro impacted significantly European pulp producers margins.

Paper prices reflect current market conditions and declined 7% YoY

Average Pulp prices

2014-18 2019 Q1-Q3 2020

USD 817 855 680

EUR 701 762 606

48

NAVIGATOR PAPER & PULP PERFORMANCE9M 2020

PAPER PERFORMANCE

• UWF sales volume increased 45% QoQ to 366 ktons, with strong performance in Europe; YTD Sep. volumesdeclined 13.8% YoY to 933 ktons;

• Average selling price in Europe for Cut-Size evolved in line with the PIX Index, but average selling price wasnegatively impacted by lower prices in overseas markets, product mix and exchange rate;

• Paper turnover stood at € 238 million in Q3 (+36% vs Q2) and at € 706 million in the first 9M (-22% YoY);

• Order book recovered in September to 26 days, close to normal levels for this period, and 19% higher thancompetitors;

• Increase in market share among European producers of 2 p.p. vs 2019 both in European and export markets;

• NVG inventories reduced significantly at the end of September and were in line with 2019 level, representing almosthalf of European competitors inventories. Stocks in the pipeline are believed to be below normal.

PULP PERFORMANCE

• Sales volume totaled 297 Ktons in 9M 2020, recording the highest volume sold since 2010, increasing 39% vs 9M2019; Sales turnover was € 117.5 million in 9M2020, falling 3.2% YoY, negatively impacted by decline in pulp price;

• Increase in volume was sustained by higher availability of pulp (in Q2) and by sales diversification into othergeographies, taking advantage of market opportunities in tissue and packaging, as well as inventory optimizaton.

<<

49

• Sales turnover increased to € 106.7 million, representing a growth of 5% YoY and 6% in Q3 2020 vs Q2 2020, (+1% vs Q3 2019)

• Global volume of tissue sold increased to 79 kton (+7% YoY), sustained by strong sales in finished products, whichled to an improvement in product mix: 77% of finished products in 2020 vs 75% in 2019

• Good industrial performance of both Aveiro and Vila Velha Rodão mills and improvement in fixed costs

44% Consumer (At-Home)(vs 35% 9M2019)

40% Away-from-Home +C&C(vs.40% 9M2019)

16% Parent Reels(vs.25% 9M2019)

42% Portugal (vs. 37%)

34% Spain(vs.28%)

24% Extra-Iberia(vs.35%)

Revenue by segment

(9M 2020)

Revenue by geography

(9M 2020)

<<RECORD PERFORMANCE IN TISSUEIncreased weight of Consumer Products

50

CONTINUING TO GENERATE STRONG FREE CASH FLOW

Strong generation of Free Cash Flow was maintained throughout Q3 (+56 M€) totaling € 170 million YTD September, comparing favorably with FCF of € 125.4 million in 9M2019; efficient management of working capital, with both strong cash conversion of clients receivables and

careful management of suppliers, with recourse to financial solutions to support their liquidity

M €

<<

186.1170.4

6.57.7

16.7

23.7

Operating Cash Flow

CAPEX Inventories SuppliersClients State & Public

Entities

Other Free Cash Flow R20

-69,7

-0,6

-15,7(-8%)

Current Average Cost of Debt

51

Debt Rate Profile

Fixed Variable

71% 29%

Short term liquidity increased to 345 M€ at the end of SeptemberDuring Q3, NVG has already refinanced 80% of its long-term financial debt

maturing in 2021

Debt maturity profileTotal debt: € 1,225 million

Average maturity: 2.9 years

27

292

54

430

107 83

254

2020 2021 2022 2023 2024 2025 2026-2028

<<Conservative Debt Profile

52

SuppliersBalance mill’s needs while securing suppliers’ activities

Improve working capital while supporting suppliers through financial instruments

LiquidityIncrease immediate cash liquidity and preserve Company´s financial strength:

Short term liquidity increased to € 345 million + € 95 million of unused available lines

Successful renegotiation of 80% of debt maturing in 2021

Capex Significant capital expenditure revision:

Capex for 2020 revised downwards to € 55 million (cash outflow perspective)

Total capex YTD Sept. €70 million; total capex forecasted for FY of € 90 million

Efficiency and cost reduction programmesStrong commitment to reduce costs:

€ 30 million reduction achieved in fixed costs YTD September

Improvement in variable production costs of € 44 million, related to price renegotiations and reduction in specific consumption

Responsive measures taken to secure business well being

Positive results from measures undertaken in response to Covid-19

<<

PULP PAPER• Supply may be impacted by

production and maintenance stoppages planned for Q4 in total estimated at 420 ktons (NVG will also have pulp maintenance in Q4)

• Prices remain at historical low levels and recent price increases were announced in Harwood for beginning of November in China and Europe by several Latin American producers

TISSUE• Navigator expects to maintain

a healthy level of industrial performance and to continue to deliver volumes in line with previous quarters

• Annual maintenance stoppage planned for Q4 in Aveiro

53

• Stocks among European distributors are estimated to be balanced or even low, and order book in Europe in the first weeks of October showed positive signs;

• Navigator ended Q3 with low stocks and healthy order book, well positioned to take advantage of improvement in demand expected for Q4

• Maintenance stoppage expected for Q4 in Setúbal Paper mill

OUTLOOK FOR Q4 2020 <<

Recovery of UWF business in Q4 expected to continue, albeit depending on the evolution of the pandemic situation and any further measures restricting economic activity

Navigator will continue with its strong commercial effort, cost efficiency programs and effective management of liquidity; with a geographically diversified business, NVG´s UWF product mix continues to present a strong versatility and higher resilience when compared to other P&W grades

P r e s e n t a t i o n t o I n v e s t o r s

N o v e m b e r 2 0 2 0