presentation to investors q1 2011€¦ · presentation to investors life sciences and materials...

TRANSCRIPT

Address:DSM Investor RelationsP.O. Box 6500, 6401 JH HeerlenThe NetherlandsPhone: +31 45 5782864Fax: +31 10 45 90275Email: [email protected]

www.dsm.com

Presentation to Investors Life Sciences and Materials Sciences

Royal DSM N.V.Q1 2011 Results

DSM – Bright Science. Brighter Living.™

Royal DSM N.V. is a global science-based company active in health, nutrition and materials. By connecting its unique competences in Life Sciences and Materials Sciences DSM is driving economic prosperity, environmental progress and social advances to create sustainable value for all stakeholders. DSM delivers innovative solutions that nourish, protect and improve performance in global markets such as food and dietary supplements, personal care, feed, pharmaceuticals, medical devices, automotive, paints, electrical and electronics, life protection, alternative energy and bio-based materials. DSM’s 22,000 employees deliver annual net sales of around € 9 billion. The company is listed on NYSE Euronext. More information can be found at www.dsm.com.

➤ Operational performance Q1 2011

➤ Progress on strategy and outlook

DSM Investor Relations P.O. Box 6500 6401 JH Heerlen The Netherlands

Tel. (31) 45 5782864 Fax (31) 10 45 90275 E-mail: [email protected]

www.dsm.com

1

2

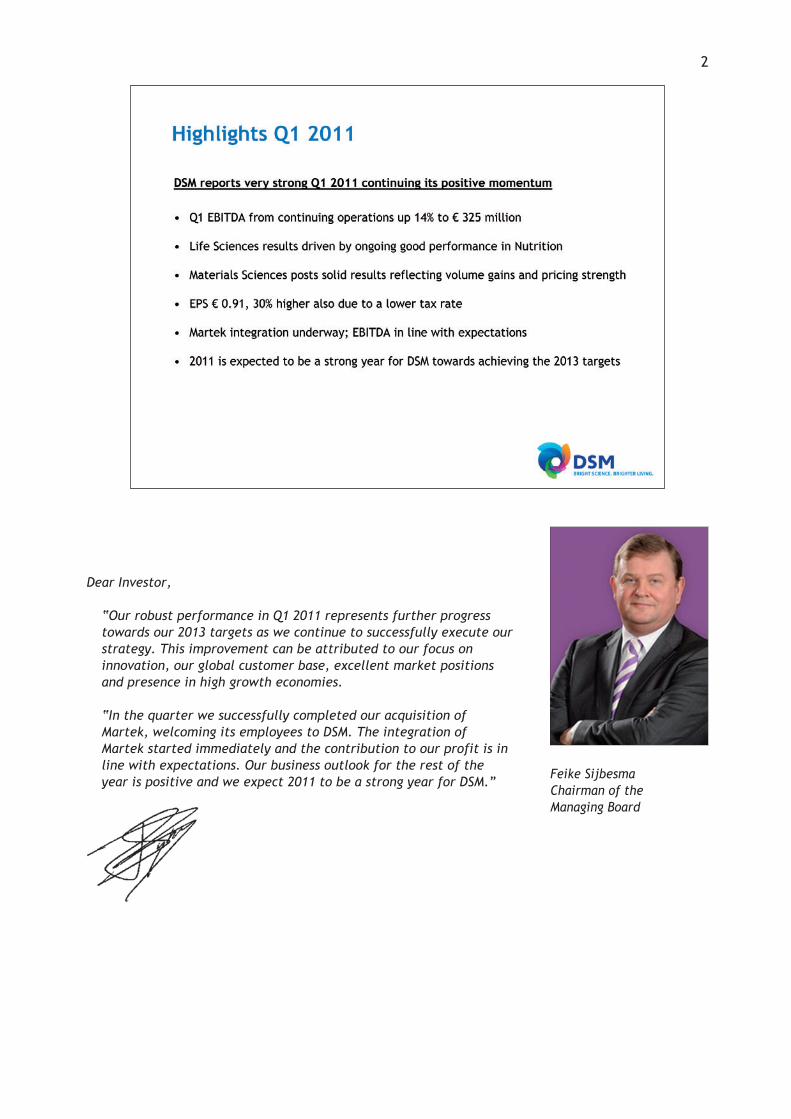

Dear Investor,

“Our robust performance in Q1 2011 represents further progresstowards our 2013 targets as we continue to successfully execute ourstrategy. This improvement can be attributed to our focus oninnovation, our global customer base, excellent market positionsand presence in high growth economies.

“In the quarter we successfully completed our acquisition ofMartek, welcoming its employees to DSM. The integration ofMartek started immediately and the contribution to our profit is inline with expectations. Our business outlook for the rest of theyear is positive and we expect 2011 to be a strong year for DSM.”

Feike SijbesmaChairman of theManaging Board

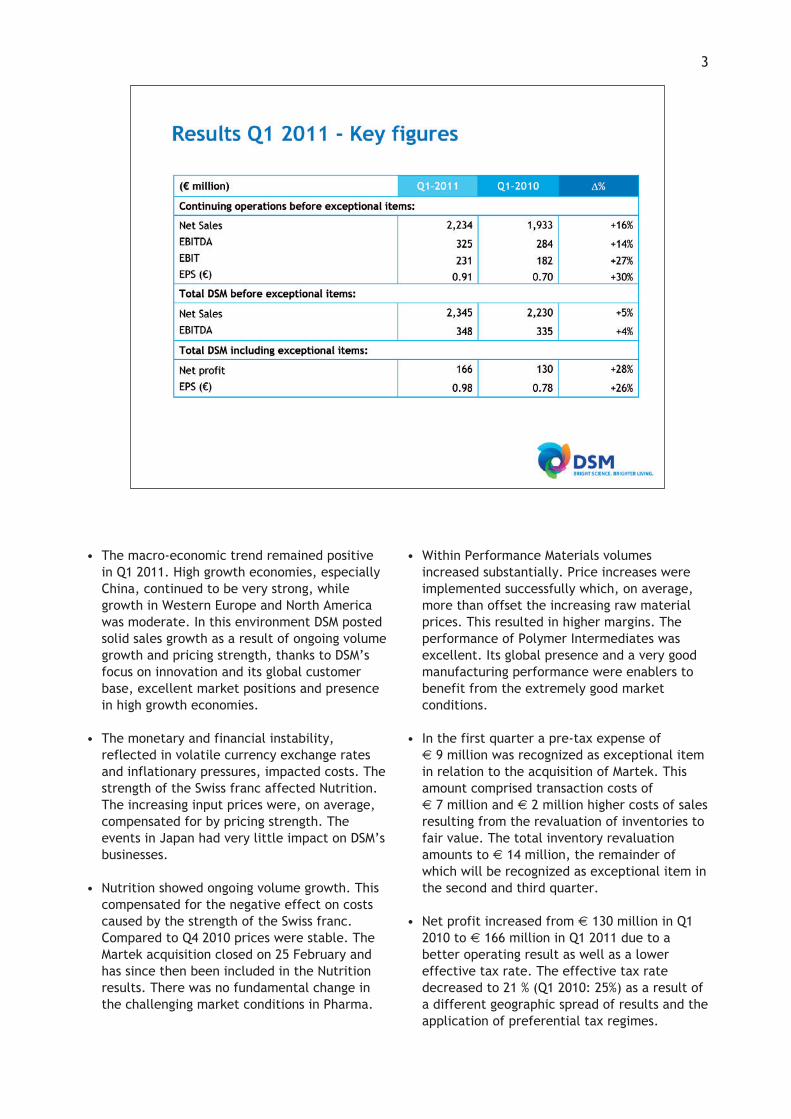

• The macro-economic trend remained positivein Q1 2011. High growth economies, especiallyChina, continued to be very strong, whilegrowth in Western Europe and North Americawas moderate. In this environment DSM postedsolid sales growth as a result of ongoing volumegrowth and pricing strength, thanks to DSM’sfocus on innovation and its global customerbase, excellent market positions and presencein high growth economies.

• The monetary and financial instability,reflected in volatile currency exchange ratesand inflationary pressures, impacted costs. Thestrength of the Swiss franc affected Nutrition.The increasing input prices were, on average,compensated for by pricing strength. Theevents in Japan had very little impact on DSM’sbusinesses.

• Nutrition showed ongoing volume growth. Thiscompensated for the negative effect on costscaused by the strength of the Swiss franc.Compared to Q4 2010 prices were stable. TheMartek acquisition closed on 25 February andhas since then been included in the Nutritionresults. There was no fundamental change inthe challenging market conditions in Pharma.

• Within Performance Materials volumesincreased substantially. Price increases wereimplemented successfully which, on average,more than offset the increasing raw materialprices. This resulted in higher margins. Theperformance of Polymer Intermediates wasexcellent. Its global presence and a very goodmanufacturing performance were enablers tobenefit from the extremely good marketconditions.

• In the first quarter a pre-tax expense of € 9 million was recognized as exceptional itemin relation to the acquisition of Martek. Thisamount comprised transaction costs of € 7 million and € 2 million higher costs of salesresulting from the revaluation of inventories tofair value. The total inventory revaluationamounts to € 14 million, the remainder ofwhich will be recognized as exceptional item inthe second and third quarter.

• Net profit increased from € 130 million in Q12010 to € 166 million in Q1 2011 due to abetter operating result as well as a lowereffective tax rate. The effective tax ratedecreased to 21 % (Q1 2010: 25%) as a result ofa different geographic spread of results and theapplication of preferential tax regimes.

3

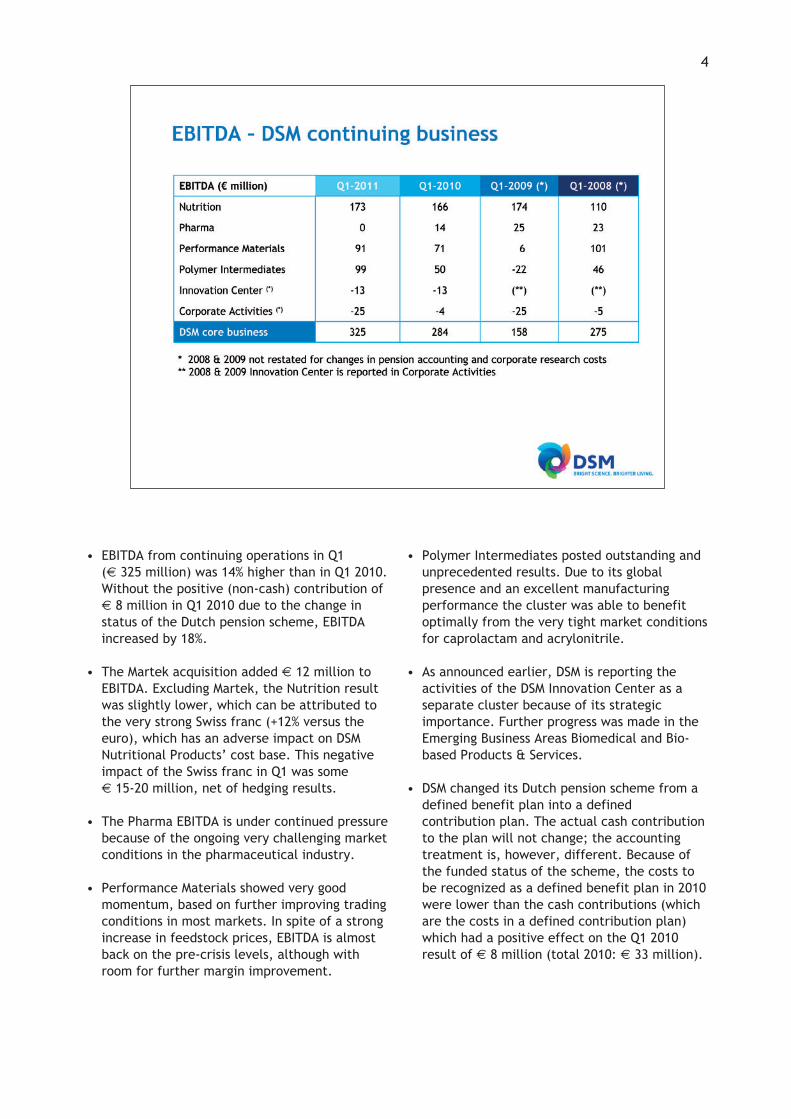

• EBITDA from continuing operations in Q1 (€ 325 million) was 14% higher than in Q1 2010.Without the positive (non-cash) contribution of€ 8 million in Q1 2010 due to the change instatus of the Dutch pension scheme, EBITDAincreased by 18%.

• The Martek acquisition added € 12 million toEBITDA. Excluding Martek, the Nutrition resultwas slightly lower, which can be attributed tothe very strong Swiss franc (+12% versus theeuro), which has an adverse impact on DSMNutritional Products’ cost base. This negativeimpact of the Swiss franc in Q1 was some € 15-20 million, net of hedging results.

• The Pharma EBITDA is under continued pressurebecause of the ongoing very challenging marketconditions in the pharmaceutical industry.

• Performance Materials showed very goodmomentum, based on further improving tradingconditions in most markets. In spite of a strongincrease in feedstock prices, EBITDA is almostback on the pre-crisis levels, although withroom for further margin improvement.

• Polymer Intermediates posted outstanding andunprecedented results. Due to its globalpresence and an excellent manufacturingperformance the cluster was able to benefitoptimally from the very tight market conditionsfor caprolactam and acrylonitrile.

• As announced earlier, DSM is reporting theactivities of the DSM Innovation Center as aseparate cluster because of its strategicimportance. Further progress was made in theEmerging Business Areas Biomedical and Bio-based Products & Services.

• DSM changed its Dutch pension scheme from adefined benefit plan into a definedcontribution plan. The actual cash contributionto the plan will not change; the accountingtreatment is, however, different. Because ofthe funded status of the scheme, the costs tobe recognized as a defined benefit plan in 2010were lower than the cash contributions (whichare the costs in a defined contribution plan)which had a positive effect on the Q1 2010result of € 8 million (total 2010: € 33 million).

4

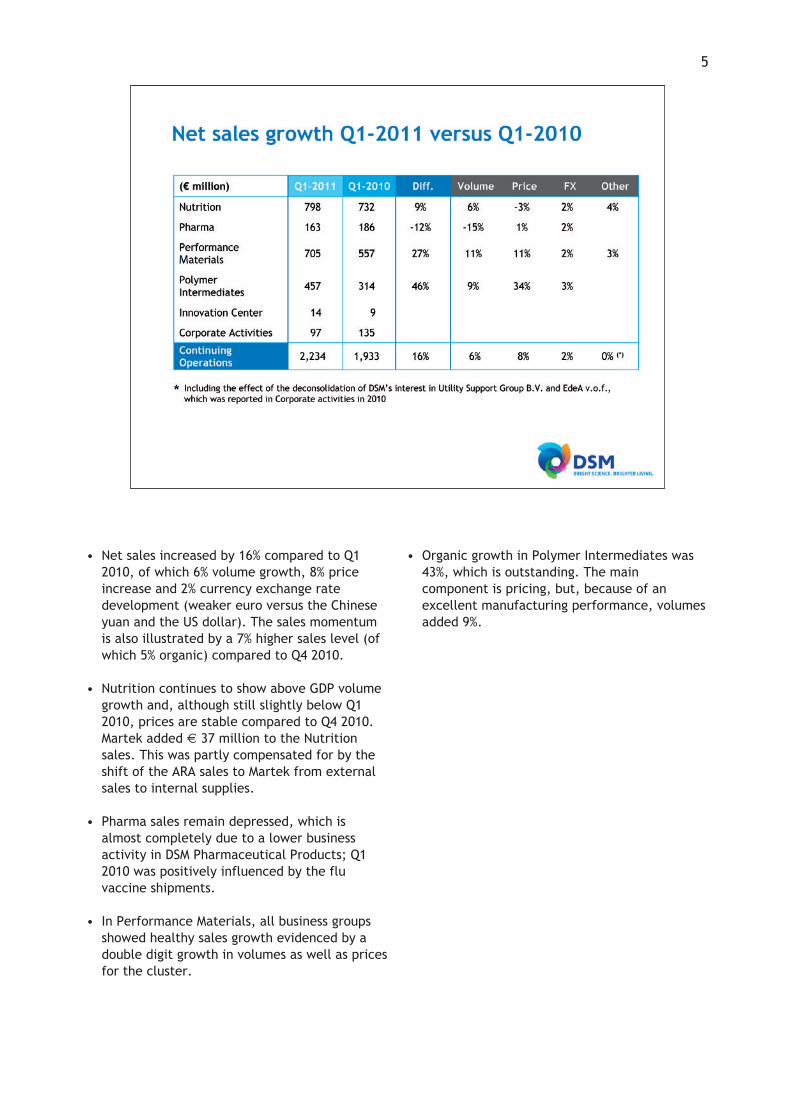

• Net sales increased by 16% compared to Q12010, of which 6% volume growth, 8% priceincrease and 2% currency exchange ratedevelopment (weaker euro versus the Chineseyuan and the US dollar). The sales momentumis also illustrated by a 7% higher sales level (ofwhich 5% organic) compared to Q4 2010.

• Nutrition continues to show above GDP volumegrowth and, although still slightly below Q12010, prices are stable compared to Q4 2010.Martek added € 37 million to the Nutritionsales. This was partly compensated for by theshift of the ARA sales to Martek from externalsales to internal supplies.

• Pharma sales remain depressed, which isalmost completely due to a lower businessactivity in DSM Pharmaceutical Products; Q12010 was positively influenced by the fluvaccine shipments.

• In Performance Materials, all business groupsshowed healthy sales growth evidenced by adouble digit growth in volumes as well as pricesfor the cluster.

• Organic growth in Polymer Intermediates was43%, which is outstanding. The maincomponent is pricing, but, because of anexcellent manufacturing performance, volumesadded 9%.

5

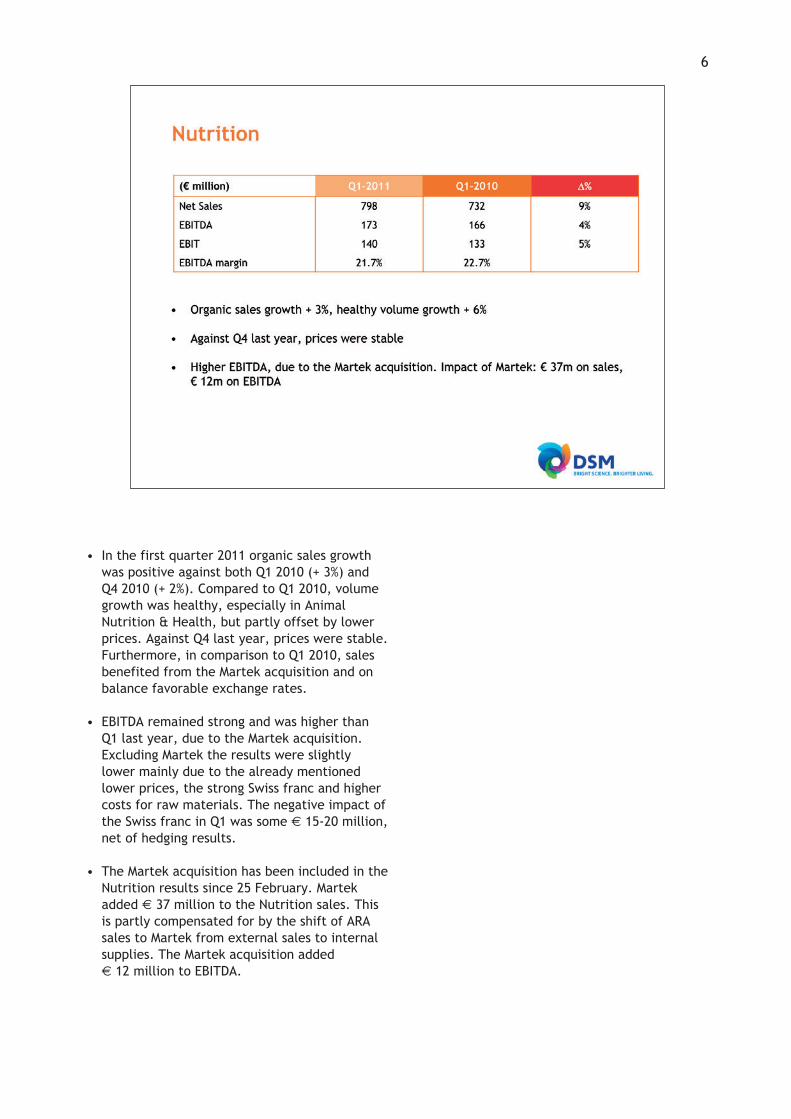

• In the first quarter 2011 organic sales growthwas positive against both Q1 2010 (+ 3%) andQ4 2010 (+ 2%). Compared to Q1 2010, volumegrowth was healthy, especially in AnimalNutrition & Health, but partly offset by lowerprices. Against Q4 last year, prices were stable.Furthermore, in comparison to Q1 2010, salesbenefited from the Martek acquisition and onbalance favorable exchange rates.

• EBITDA remained strong and was higher thanQ1 last year, due to the Martek acquisition.Excluding Martek the results were slightlylower mainly due to the already mentionedlower prices, the strong Swiss franc and highercosts for raw materials. The negative impact ofthe Swiss franc in Q1 was some € 15-20 million,net of hedging results.

• The Martek acquisition has been included in theNutrition results since 25 February. Martekadded € 37 million to the Nutrition sales. Thisis partly compensated for by the shift of ARAsales to Martek from external sales to internalsupplies. The Martek acquisition added € 12 million to EBITDA.

6

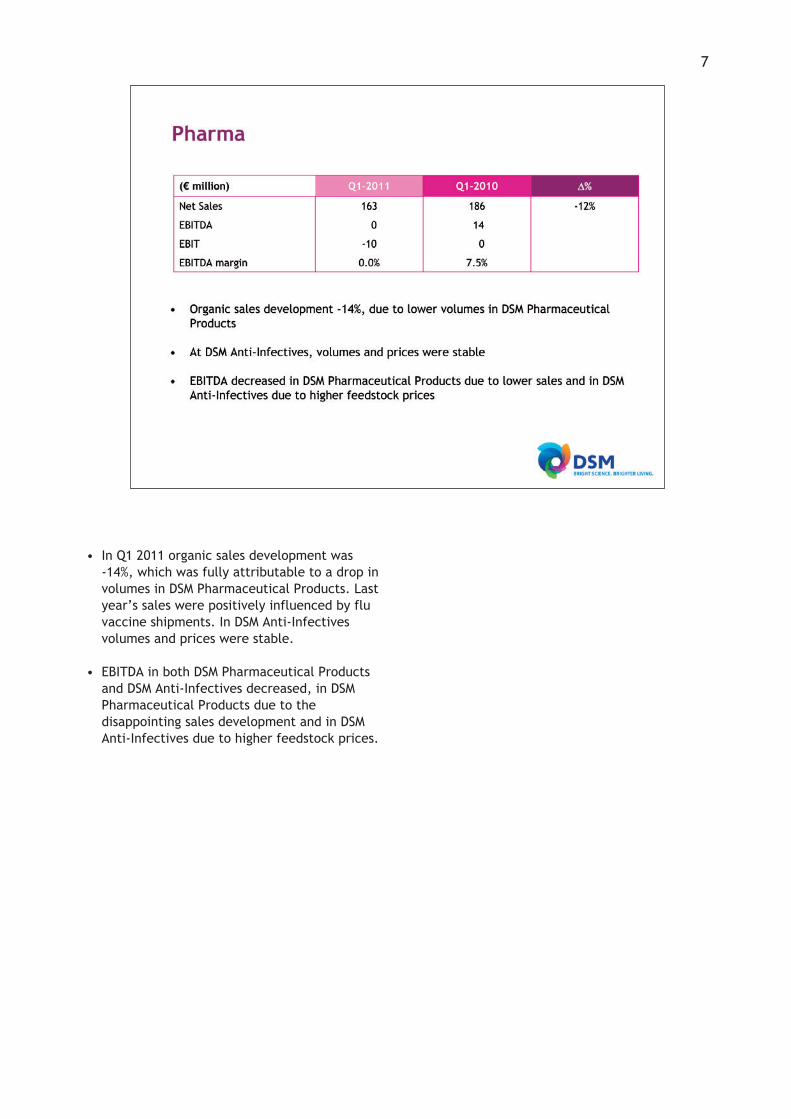

• In Q1 2011 organic sales development was -14%, which was fully attributable to a drop involumes in DSM Pharmaceutical Products. Lastyear’s sales were positively influenced by fluvaccine shipments. In DSM Anti-Infectivesvolumes and prices were stable.

• EBITDA in both DSM Pharmaceutical Productsand DSM Anti-Infectives decreased, in DSMPharmaceutical Products due to thedisappointing sales development and in DSMAnti-Infectives due to higher feedstock prices.

7

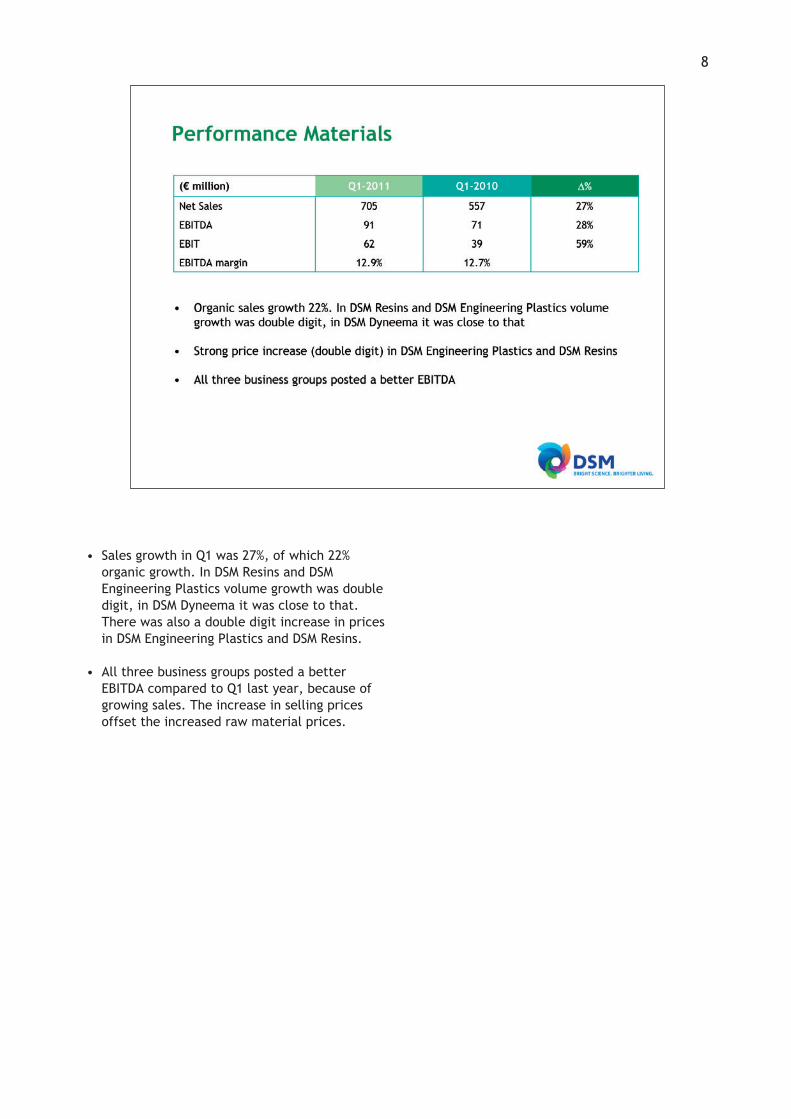

• Sales growth in Q1 was 27%, of which 22%organic growth. In DSM Resins and DSMEngineering Plastics volume growth was doubledigit, in DSM Dyneema it was close to that.There was also a double digit increase in pricesin DSM Engineering Plastics and DSM Resins.

• All three business groups posted a betterEBITDA compared to Q1 last year, because ofgrowing sales. The increase in selling pricesoffset the increased raw material prices.

8

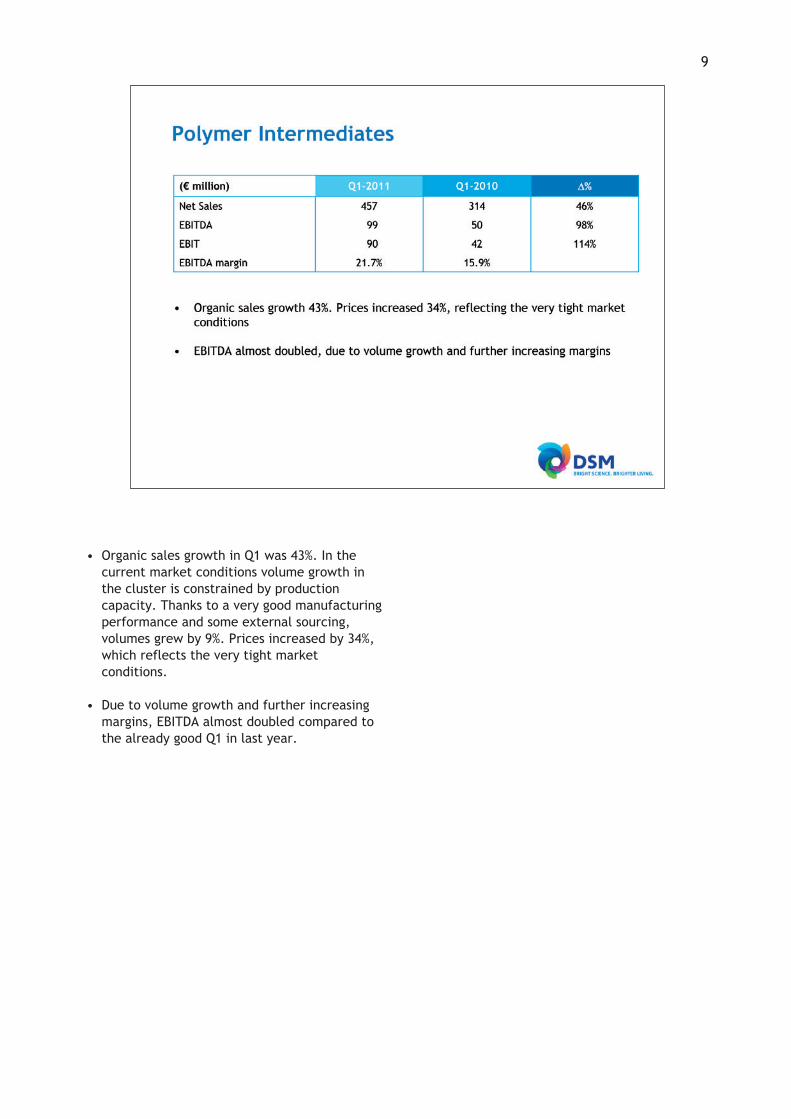

• Organic sales growth in Q1 was 43%. In thecurrent market conditions volume growth inthe cluster is constrained by productioncapacity. Thanks to a very good manufacturingperformance and some external sourcing,volumes grew by 9%. Prices increased by 34%,which reflects the very tight marketconditions.

• Due to volume growth and further increasingmargins, EBITDA almost doubled compared tothe already good Q1 in last year.

9

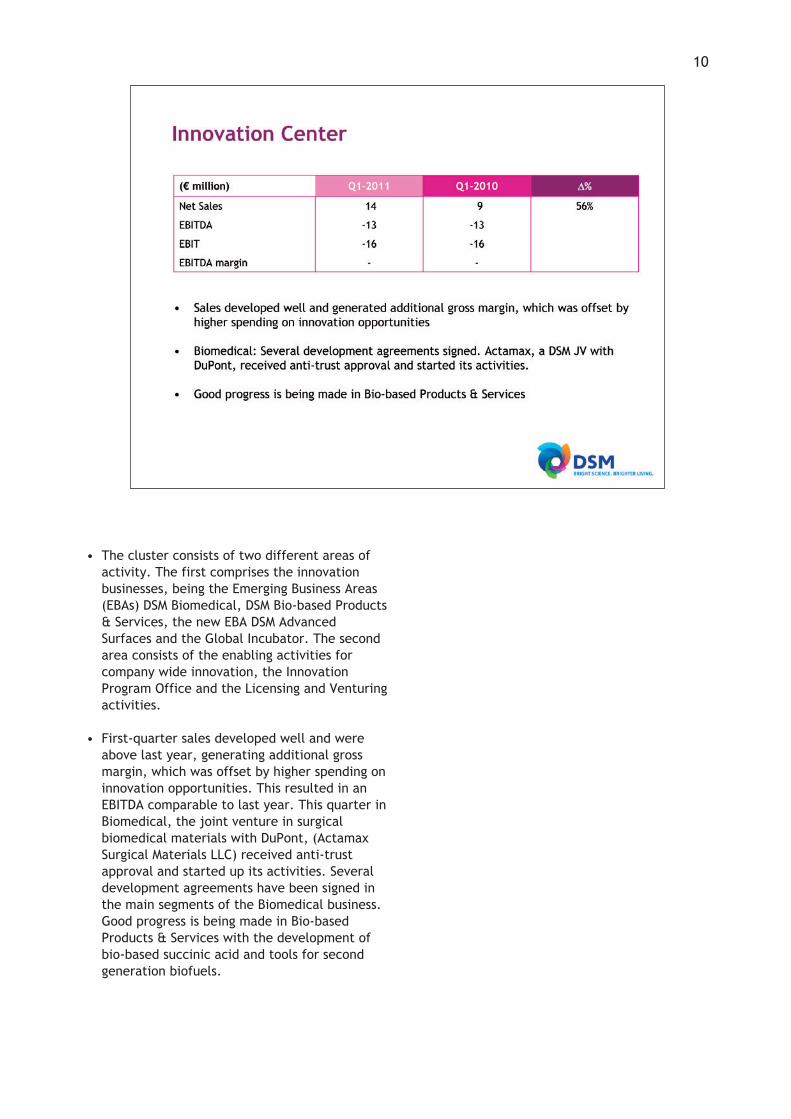

• The cluster consists of two different areas ofactivity. The first comprises the innovationbusinesses, being the Emerging Business Areas(EBAs) DSM Biomedical, DSM Bio-based Products& Services, the new EBA DSM AdvancedSurfaces and the Global Incubator. The secondarea consists of the enabling activities forcompany wide innovation, the InnovationProgram Office and the Licensing and Venturingactivities.

• First-quarter sales developed well and wereabove last year, generating additional grossmargin, which was offset by higher spending oninnovation opportunities. This resulted in anEBITDA comparable to last year. This quarter inBiomedical, the joint venture in surgicalbiomedical materials with DuPont, (ActamaxSurgical Materials LLC) received anti-trustapproval and started up its activities. Severaldevelopment agreements have been signed inthe main segments of the Biomedical business.Good progress is being made in Bio-basedProducts & Services with the development ofbio-based succinic acid and tools for secondgeneration biofuels.

10

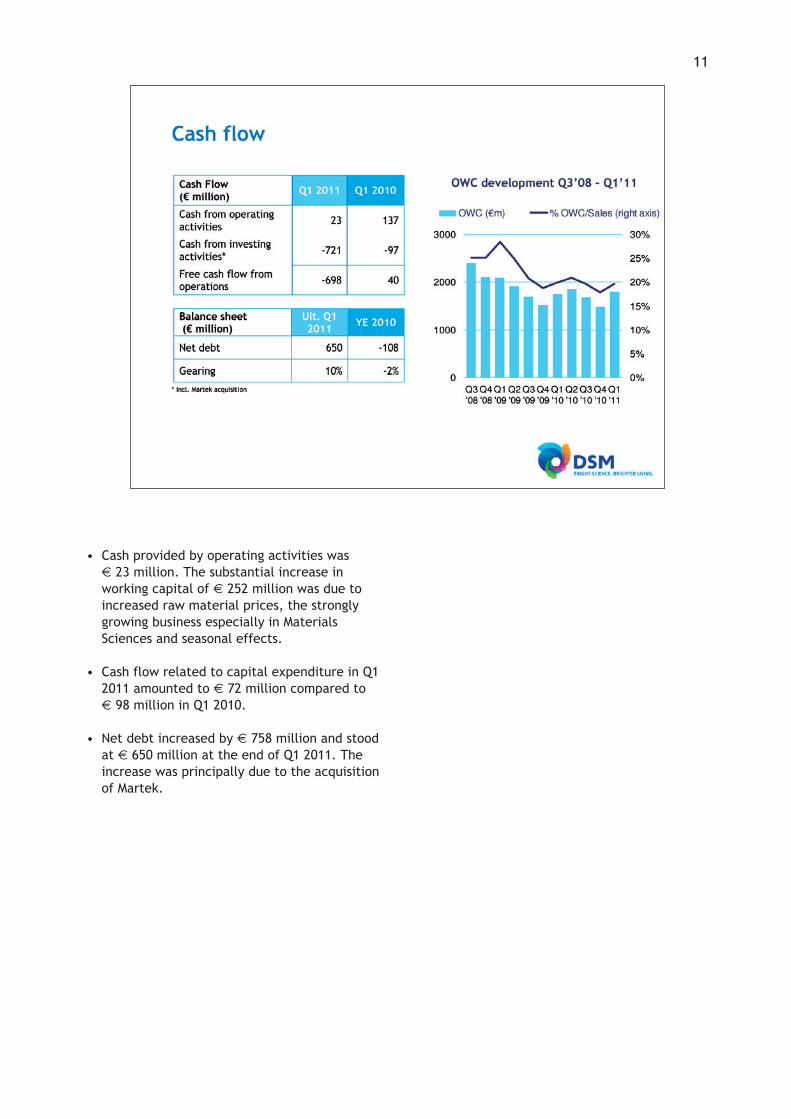

• Cash provided by operating activities was € 23 million. The substantial increase inworking capital of € 252 million was due toincreased raw material prices, the stronglygrowing business especially in MaterialsSciences and seasonal effects.

• Cash flow related to capital expenditure in Q12011 amounted to € 72 million compared to € 98 million in Q1 2010.

• Net debt increased by € 758 million and stoodat € 650 million at the end of Q1 2011. Theincrease was principally due to the acquisitionof Martek.

11

13

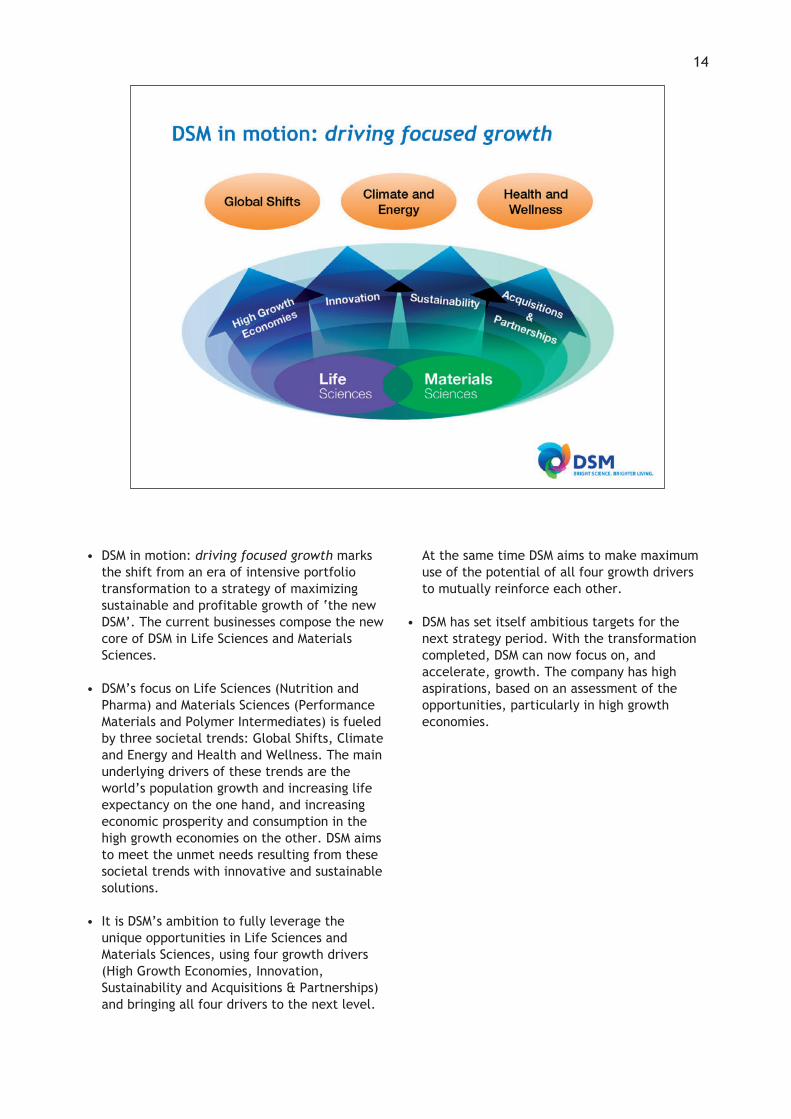

• DSM in motion: driving focused growth marksthe shift from an era of intensive portfoliotransformation to a strategy of maximizingsustainable and profitable growth of ‘the newDSM’. The current businesses compose the newcore of DSM in Life Sciences and MaterialsSciences.

• DSM’s focus on Life Sciences (Nutrition andPharma) and Materials Sciences (PerformanceMaterials and Polymer Intermediates) is fueledby three societal trends: Global Shifts, Climateand Energy and Health and Wellness. The mainunderlying drivers of these trends are theworld’s population growth and increasing lifeexpectancy on the one hand, and increasingeconomic prosperity and consumption in thehigh growth economies on the other. DSM aimsto meet the unmet needs resulting from thesesocietal trends with innovative and sustainablesolutions.

• It is DSM’s ambition to fully leverage theunique opportunities in Life Sciences andMaterials Sciences, using four growth drivers(High Growth Economies, Innovation,Sustainability and Acquisitions & Partnerships)and bringing all four drivers to the next level.

At the same time DSM aims to make maximumuse of the potential of all four growth driversto mutually reinforce each other.

• DSM has set itself ambitious targets for thenext strategy period. With the transformationcompleted, DSM can now focus on, andaccelerate, growth. The company has highaspirations, based on an assessment of theopportunities, particularly in high growtheconomies.

14

• 37% of DSM’s Q1 2011 sales are destined for tothe high growth economies. Net sales in China(continuing operations, in USD) increased by21% from USD 377 million in Q1 2010 to USD 458 million in Q1 2011. In India, DSMrecorded a sales increase (in Euro) of 30%.

• The DSM joint venture Jinling DSM Resins Co.,Ltd. (JDR) will invest approximately € 50 million in a new production facility forcomposite resins in Nanjing, China. The newfacility, which will replace the current facility,will be among the largest manufacturing plantsfor composite resins in the world. DSM’s sharein the investment is 75%.

• DSM signed an agreement to acquire themajority shareholding in Shandong ICD HighPerformance Fibre Co. Ltd. based in Laiwu,Shandong province, China. Closing of thistransaction is expected in the course of 2011.The agreement with ICD, a manufacturer ofUHMWPE (ultra high molecular weightpolyethylene) fiber and a potential strongplayer in the Chinese market for highperformance fibers, concludes an extensiveselection process by DSM to find the rightcompany in the Chinese market.

• DSM also announced a partnership withKemrock Industries in India for the production

of specialty composite resins in India. DSM andKemrock together will invest USD 25 million ina joint venture. DSM will focus on the supply ofinnovative specialized composite resin solutionsto the fast growing Indian market whileKemrock will concentrate on the production ofhigh end composite parts. DSM will hold 51%and Kemrock 49% in the joint venture, whichwill be based in Pune.

• In India DSM opened its first Animal Nutrition &Health premix plant, located in Ambernath,Mumbai. This enables DSM to capitalize onopportunities that arise from the rapidlydeveloping animal nutrition and health industryin the country. India is currently ranked 5th inthe world as a broiler producer and is theworld’s 4th largest egg producer.

• DSM and KuibyshevAzot OJSC announced astrategic cooperation in which DSM EngineeringPlastics will enter into two joint ventures withthe Russian company. In both joint venturesDSM Engineering Plastics will hold a majorityshare. In addition, KuibyshevAzot will begranted a license under DSM FibreIntermediates’ technology for the productionof cyclohexanone. With this partnership DSM isexpected to be in an excellent position tocapitalize on this anticipated growth in Russia.

15

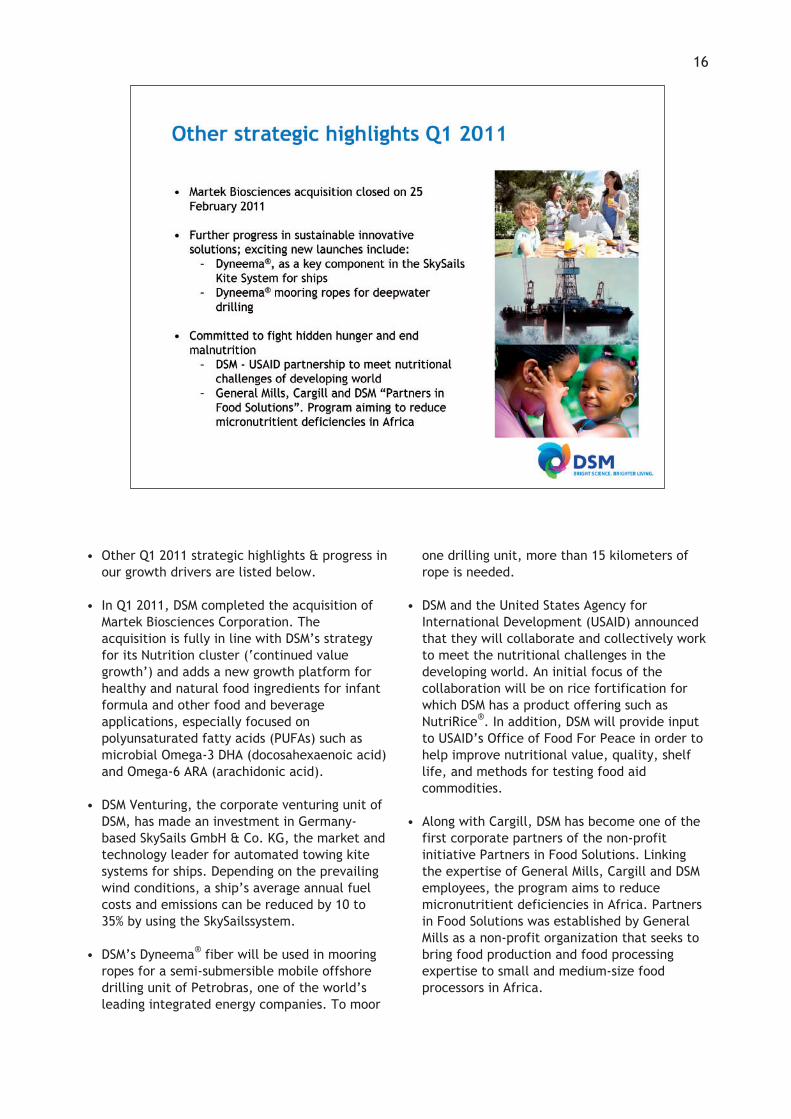

• Other Q1 2011 strategic highlights & progress inour growth drivers are listed below.

• In Q1 2011, DSM completed the acquisition ofMartek Biosciences Corporation. Theacquisition is fully in line with DSM’s strategyfor its Nutrition cluster (‘continued valuegrowth’) and adds a new growth platform forhealthy and natural food ingredients for infantformula and other food and beverageapplications, especially focused onpolyunsaturated fatty acids (PUFAs) such asmicrobial Omega-3 DHA (docosahexaenoic acid)and Omega-6 ARA (arachidonic acid).

• DSM Venturing, the corporate venturing unit ofDSM, has made an investment in Germany-based SkySails GmbH & Co. KG, the market andtechnology leader for automated towing kitesystems for ships. Depending on the prevailingwind conditions, a ship’s average annual fuelcosts and emissions can be reduced by 10 to35% by using the SkySailssystem.

• DSM’s Dyneema® fiber will be used in mooringropes for a semi-submersible mobile offshoredrilling unit of Petrobras, one of the world’sleading integrated energy companies. To moor

one drilling unit, more than 15 kilometers ofrope is needed.

• DSM and the United States Agency forInternational Development (USAID) announcedthat they will collaborate and collectively workto meet the nutritional challenges in thedeveloping world. An initial focus of thecollaboration will be on rice fortification forwhich DSM has a product offering such asNutriRice®. In addition, DSM will provide inputto USAID’s Office of Food For Peace in order tohelp improve nutritional value, quality, shelflife, and methods for testing food aidcommodities.

• Along with Cargill, DSM has become one of thefirst corporate partners of the non-profitinitiative Partners in Food Solutions. Linkingthe expertise of General Mills, Cargill and DSMemployees, the program aims to reducemicronutritient deficiencies in Africa. Partnersin Food Solutions was established by GeneralMills as a non-profit organization that seeks tobring food production and food processingexpertise to small and medium-size foodprocessors in Africa.

16

• DSM has successfully completed the acquisitionof Martek Biosciences Corporation. DSM will beable to utilize its global market reach,technology base and application skillcapabilities to channel and accelerate thegrowth of Martek’s product portfolio into otherregions, applications and market segmentsbeyond Martek’s existing strong US-basedposition in infant formula ingredients andgrowing position in food and beverage anddietary supplement applications worldwide.

• DSM will also benefit from Martek’s recentacquisition of Amerifit, an attractive consumerbusiness for branded dietary supplements withvery specific health benefits, which it will beable to use as an additional marketing channelfor both Martek and DSM ingredients.

• Furthermore, Martek’s algal and othermicrobial-based biotechnology platform and itsrobust biotechnology pipeline whichcomplements DSM’s own portfolio are expectedto deliver new nutritional and non-nutritional(industrial) growth opportunities in for instancebiochemicals and biofuels.

• Planning for the integration of DSM and Martekstarted when the deal was first announced inDecember and now a full scale integration ofthe two businesses is in progress. A dedicatedintegration team consisting of both DSM andMartek representatives is in place to assess thebest way to combine the two organizations.

• The Martek acquisition is included in theNutrition results for one month. Martek added€ 37 million to the Nutrition sales. This ispartly compensated for by the shift of ARAsales to Martek from external sales to internalsupplies. The net sales effect is € 28 million.The Martek acquisition added € 12 million toEBITDA.

• Martek’s sales growth is expected to be at thedouble digit level with stable to rising margins.

17

• DSM is uniquely involved in all three main stepsof the value chain: the production of pureactive ingredients; their incorporation intosophisticated forms, and the production oftailored premixes. Being the only fullyintegrated player allows DSM to differentiateitself all the way through the chain. Managingthe interdependencies between activeingredients, forms and premixes, which haveimportant implications for innovation, logistics,and value delivery, is a core competence ofDSM.

• Even in the production of ‘straights’ (untreatedvitamins, carotenoids, enzymes and othernutritional ingredients), where cost is a moreimportant factor, significant added value isgenerated by differentiation, through forexample quality management, traceability,reliability of supply, sustainable productionpractices, and physical product attributes suchas polymorphisms, influencing stability and bio-availability.

• In the following step of the chain, where activeingredients are incorporated into so-called“forms”, DSM has an array of sophisticatedtechnologies to deliver a range of applicationproperties. Forms are single product

formulations, which can be solid particles inwhich the active ingredients are dispersed orencapsulated in an inert matrix to providestability, extended shelf life, bio-availability ordispersability — the ability to form stablesuspensions in a liquid matrix, for instance forbeverages.

• In the next step shown here, a range of blendsare produced in so-called premix operations. Inaddition, DSM also meets specific customers’needs through tailored solutions. Only 15% ofDSM Nutritional Products’ revenue is derivedfrom sales of pure active ingredients, while 85%of revenue is based on sales of forms andpremix.

18

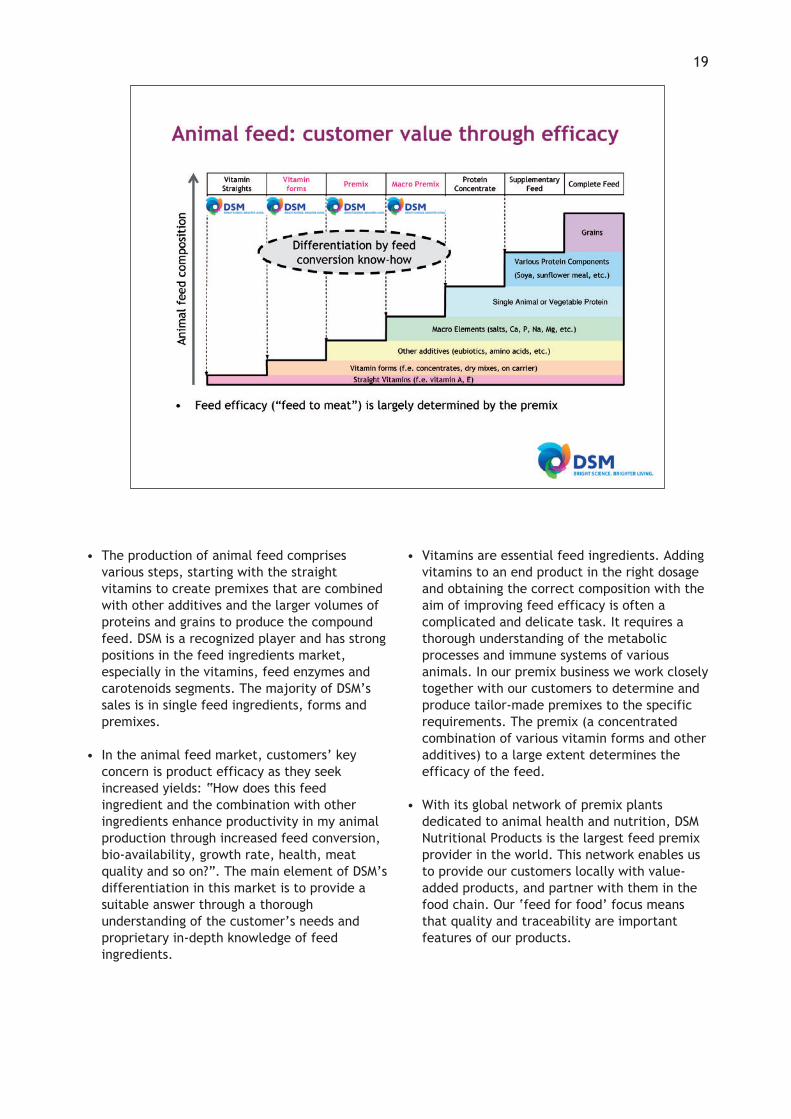

• The production of animal feed comprisesvarious steps, starting with the straightvitamins to create premixes that are combinedwith other additives and the larger volumes ofproteins and grains to produce the compoundfeed. DSM is a recognized player and has strongpositions in the feed ingredients market,especially in the vitamins, feed enzymes andcarotenoids segments. The majority of DSM’ssales is in single feed ingredients, forms andpremixes.

• In the animal feed market, customers’ keyconcern is product efficacy as they seekincreased yields: “How does this feedingredient and the combination with otheringredients enhance productivity in my animalproduction through increased feed conversion,bio-availability, growth rate, health, meatquality and so on?”. The main element of DSM’sdifferentiation in this market is to provide asuitable answer through a thoroughunderstanding of the customer’s needs andproprietary in-depth knowledge of feedingredients.

• Vitamins are essential feed ingredients. Addingvitamins to an end product in the right dosageand obtaining the correct composition with theaim of improving feed efficacy is often acomplicated and delicate task. It requires athorough understanding of the metabolicprocesses and immune systems of variousanimals. In our premix business we work closelytogether with our customers to determine andproduce tailor-made premixes to the specificrequirements. The premix (a concentratedcombination of various vitamin forms and otheradditives) to a large extent determines theefficacy of the feed.

• With its global network of premix plantsdedicated to animal health and nutrition, DSMNutritional Products is the largest feed premixprovider in the world. This network enables usto provide our customers locally with value-added products, and partner with them in thefood chain. Our ‘feed for food’ focus meansthat quality and traceability are importantfeatures of our products.

19

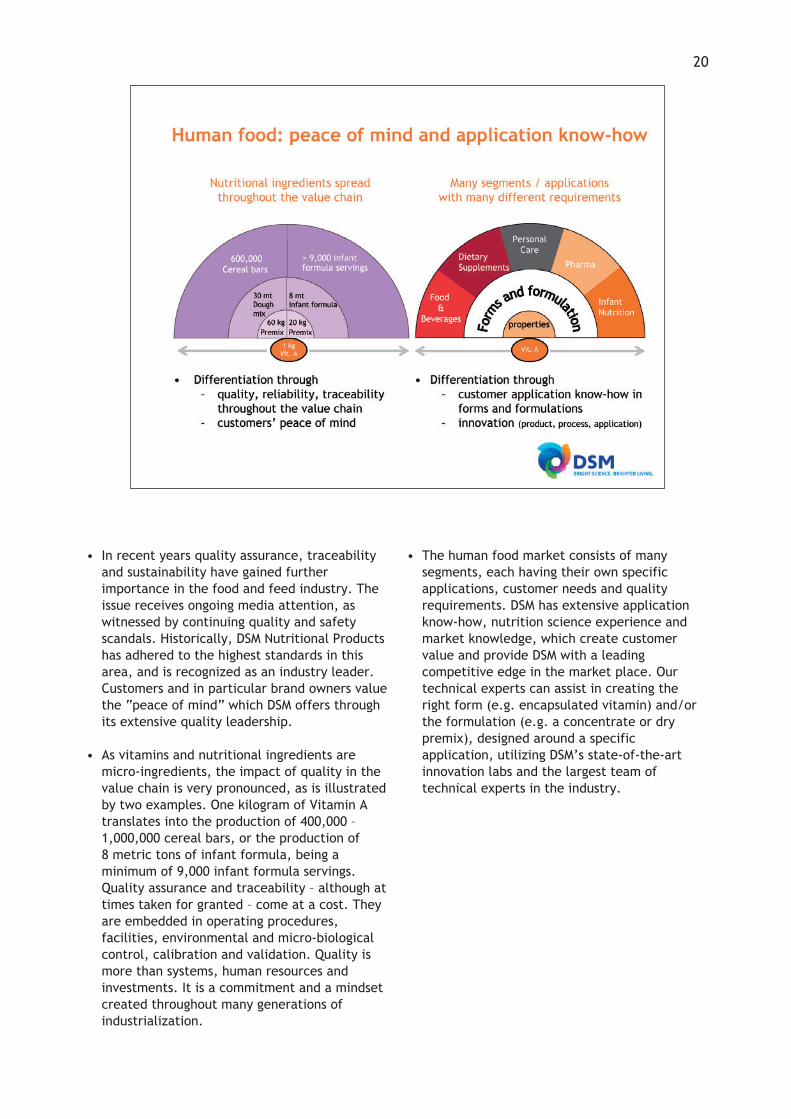

• In recent years quality assurance, traceabilityand sustainability have gained furtherimportance in the food and feed industry. Theissue receives ongoing media attention, aswitnessed by continuing quality and safetyscandals. Historically, DSM Nutritional Productshas adhered to the highest standards in thisarea, and is recognized as an industry leader.Customers and in particular brand owners valuethe “peace of mind” which DSM offers throughits extensive quality leadership.

• As vitamins and nutritional ingredients aremicro-ingredients, the impact of quality in thevalue chain is very pronounced, as is illustratedby two examples. One kilogram of Vitamin Atranslates into the production of 400,000 —1,000,000 cereal bars, or the production of 8 metric tons of infant formula, being aminimum of 9,000 infant formula servings.Quality assurance and traceability — although attimes taken for granted — come at a cost. Theyare embedded in operating procedures,facilities, environmental and micro-biologicalcontrol, calibration and validation. Quality ismore than systems, human resources andinvestments. It is a commitment and a mindsetcreated throughout many generations ofindustrialization.

• The human food market consists of manysegments, each having their own specificapplications, customer needs and qualityrequirements. DSM has extensive applicationknow-how, nutrition science experience andmarket knowledge, which create customervalue and provide DSM with a leadingcompetitive edge in the market place. Ourtechnical experts can assist in creating theright form (e.g. encapsulated vitamin) and/orthe formulation (e.g. a concentrate or drypremix), designed around a specificapplication, utilizing DSM’s state-of-the-artinnovation labs and the largest team oftechnical experts in the industry.

20

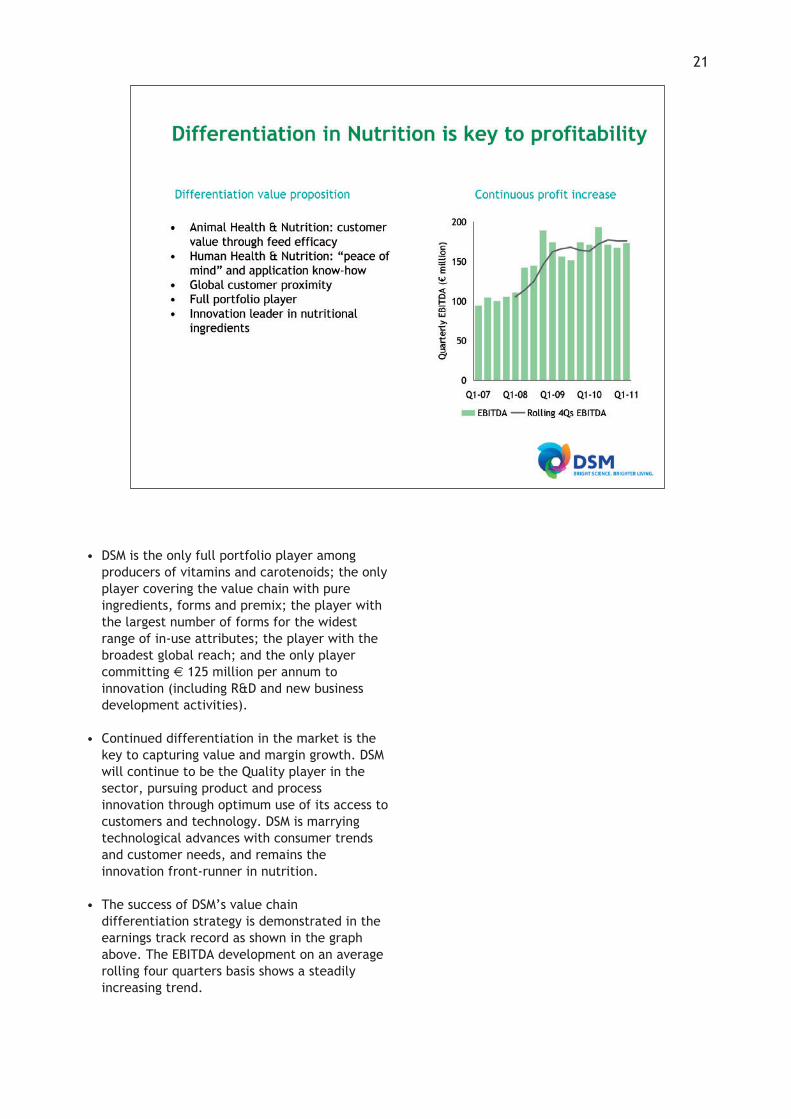

• DSM is the only full portfolio player amongproducers of vitamins and carotenoids; the onlyplayer covering the value chain with pureingredients, forms and premix; the player withthe largest number of forms for the widestrange of in-use attributes; the player with thebroadest global reach; and the only playercommitting € 125 million per annum toinnovation (including R&D and new businessdevelopment activities).

• Continued differentiation in the market is thekey to capturing value and margin growth. DSMwill continue to be the Quality player in thesector, pursuing product and processinnovation through optimum use of its access tocustomers and technology. DSM is marryingtechnological advances with consumer trendsand customer needs, and remains theinnovation front-runner in nutrition.

• The success of DSM’s value chaindifferentiation strategy is demonstrated in theearnings track record as shown in the graphabove. The EBITDA development on an averagerolling four quarters basis shows a steadilyincreasing trend.

21

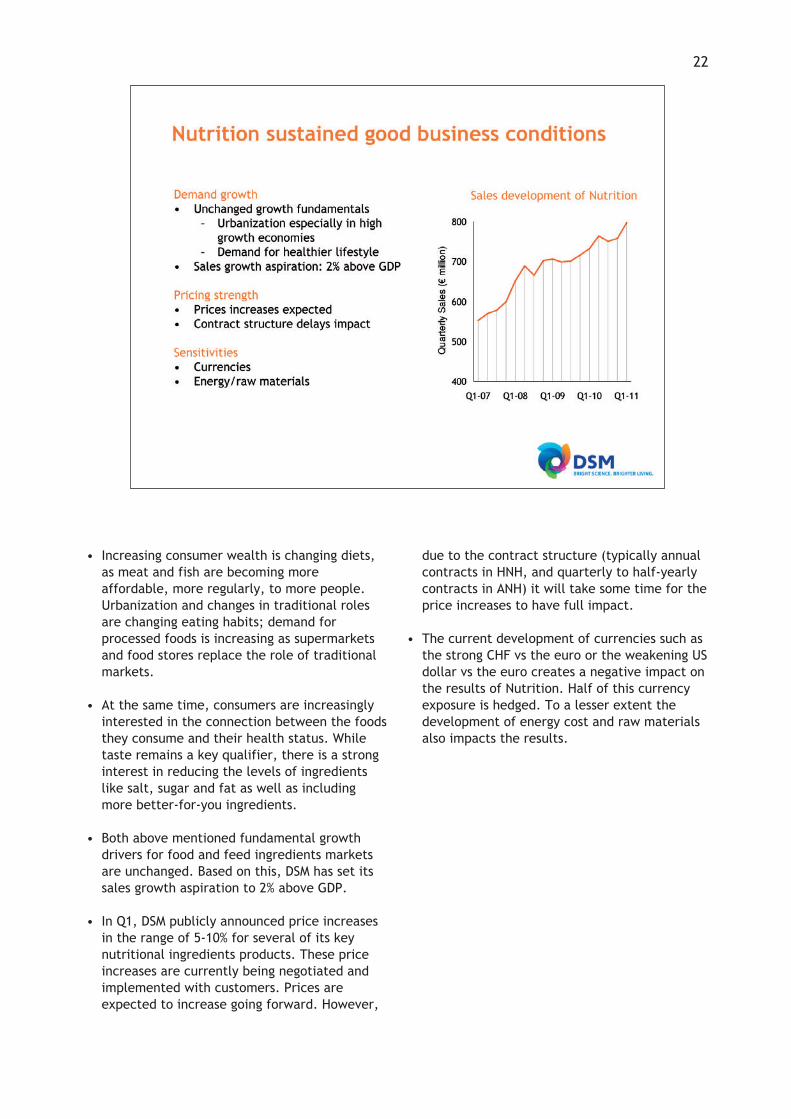

• Increasing consumer wealth is changing diets,as meat and fish are becoming moreaffordable, more regularly, to more people.Urbanization and changes in traditional rolesare changing eating habits; demand forprocessed foods is increasing as supermarketsand food stores replace the role of traditionalmarkets.

• At the same time, consumers are increasinglyinterested in the connection between the foodsthey consume and their health status. Whiletaste remains a key qualifier, there is a stronginterest in reducing the levels of ingredientslike salt, sugar and fat as well as includingmore better-for-you ingredients.

• Both above mentioned fundamental growthdrivers for food and feed ingredients marketsare unchanged. Based on this, DSM has set itssales growth aspiration to 2% above GDP.

• In Q1, DSM publicly announced price increasesin the range of 5-10% for several of its keynutritional ingredients products. These priceincreases are currently being negotiated andimplemented with customers. Prices areexpected to increase going forward. However,

due to the contract structure (typically annualcontracts in HNH, and quarterly to half-yearlycontracts in ANH) it will take some time for theprice increases to have full impact.

• The current development of currencies such asthe strong CHF vs the euro or the weakening USdollar vs the euro creates a negative impact onthe results of Nutrition. Half of this currencyexposure is hedged. To a lesser extent thedevelopment of energy cost and raw materialsalso impacts the results.

22

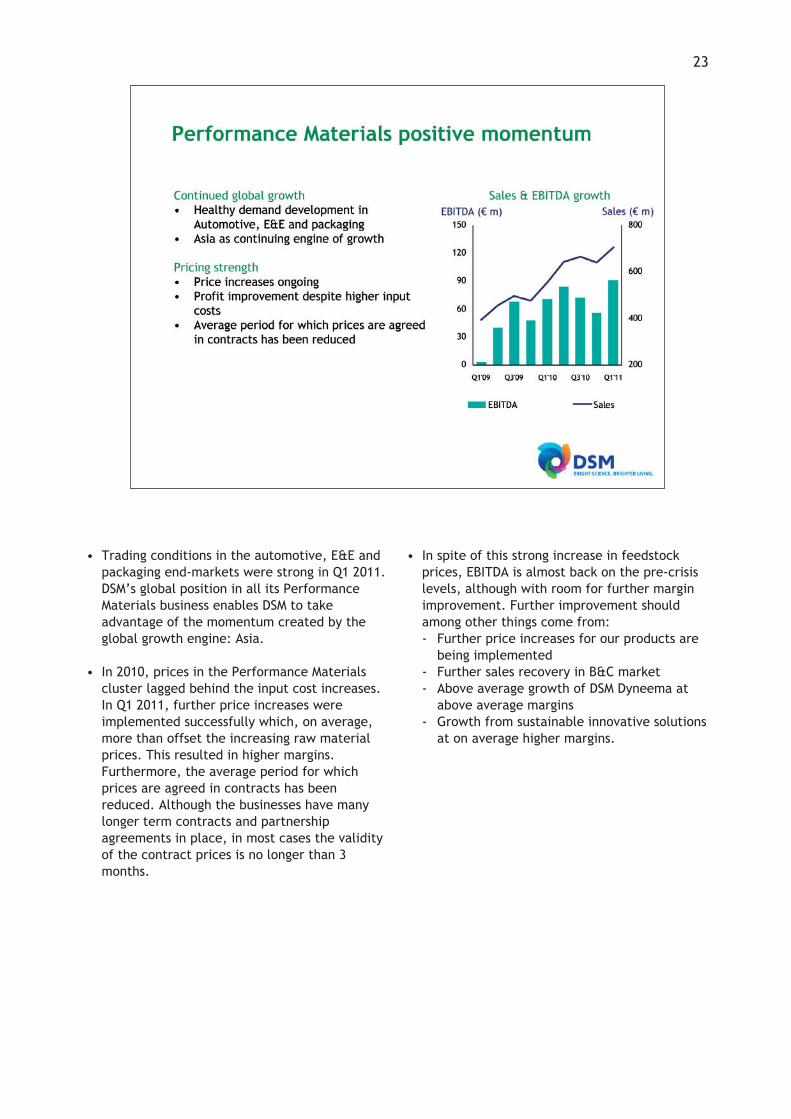

• Trading conditions in the automotive, E&E andpackaging end-markets were strong in Q1 2011.DSM’s global position in all its PerformanceMaterials business enables DSM to takeadvantage of the momentum created by theglobal growth engine: Asia.

• In 2010, prices in the Performance Materialscluster lagged behind the input cost increases.In Q1 2011, further price increases wereimplemented successfully which, on average,more than offset the increasing raw materialprices. This resulted in higher margins.Furthermore, the average period for whichprices are agreed in contracts has beenreduced. Although the businesses have manylonger term contracts and partnershipagreements in place, in most cases the validityof the contract prices is no longer than 3months.

• In spite of this strong increase in feedstockprices, EBITDA is almost back on the pre-crisislevels, although with room for further marginimprovement. Further improvement shouldamong other things come from: - Further price increases for our products are

being implemented - Further sales recovery in B&C market - Above average growth of DSM Dyneema at

above average margins - Growth from sustainable innovative solutions

at on average higher margins.

23

• Caprolactam showed another quarter ofhealthy demand. Demand was strong in allregions. Supply was already tight last year andbecame even tighter due to planned andunplanned shutdowns in the industry. This hasresulted in high GURs and record margins.

• Healthy demand for caprolactam is expected tocontinue the coming years. Consumptiongrowth is driven by among other things, theincreased use of polyamide 6 (PA6) inengineering plastics, PA6 film for foodpackaging and PA6 for the fiber segments(textiles, carpets, industrial). Demand forcaprolactam is expected to grow by > 3% peryear, with highest growth being expected (~ 6%annual growth) for the engineering plastics andfilm segments combined.

• DSM’s strong position in China is veryimportant. DSM is the only caprolactamproducer with production assets on 3continents. In the Chinese region (China andTaiwan), consumption of PA6 is expected togrow rapidly in the coming years, primarilydriven by strong growth in engineering plasticsand film segments (CAGR > 10%). Being the onlyWestern producer with production assets in

China, in combination with a partnership with astrong Chinese company (SinoPec), DSM has anexcellent position to growth in Asia. DSM’snewest and best-in-class technology, which isbeing implemented in the 2nd line in China, isexpected to demonstrate that lower costs(economy) goes hand in hand with better eco-foot print (reduction of waste, reduction ofenergy use).

• Until 2015, some 300-500kt of caprolactamcapacity might come on stream. Not all is,however, confirmed. Apart from DSM-SinoPec’s200kt second line in China in 2014, some 100ktto 300kt might come on stream including somesmaller debottlenecking. As the global marketis expected to grow by more than 3%, globalutilization rates are expected to stay above thehealthy level of 90%.

24

• Overall, the consensus economic outlook for2011 is positive. DSM expects the tradingconditions experienced during the first quarterto continue in the remainder of the year, withstrong growth in China and the other highgrowth economies, together with moderategrowth in mature economies.

• DSM is conscious of the macro-economicuncertainties. The unrest in the Middle East hashad no impact on DSM’s business, except forthe higher oil price causing the prices forenergy and certain raw materials to increase.DSM continues to pass on these higher coststhrough further price increases. At this time,DSM believes that the tragic events in Japanare likely to have only a limited impact on full-year earnings.

• The Nutrition cluster is expected to achievesustained good sales performance with healthyvolume growth and price increases. Currencyexchange rates are expected to remainvolatile; the weaker US dollar and especiallythe strong Swiss franc are unfavorable for theNutrition cluster. The EBITDA with the inclusionof Martek is expected to be clearly above lastyear.

• The focus within the Pharma cluster will be onstrategy execution such as the announced anti-infectives joint venture with Sinochem. Overallbusiness conditions remain challenging andresults are expected to be lower than in 2010.

• The Performance Materials cluster is benefitingsignificantly from continued global growth inthe relevant end-markets such as automotive,electronics and packaging. Results areexpected to be clearly above last year.

• Polymer Intermediates is expected to continueits excellent performance in 2011 based onDSM’s unique global presence and veryfavorable trading conditions, although thecurrent very tight demand-supply balancemight ease somewhat. In Q2 2011 amaintenance shutdown is planned foracrylonitrile.

• Despite the headwinds from higher input costsand on balance unfavorable currencies, 2011 isexpected to be a strong year for DSM. Thisgives DSM confidence that it will meet theEBITDA target of € 1.4 to 1.6 billion in 2013,with ROCE expected to exceed 15%.

25

DISCLAIMER

This document may contain forward-looking statements with respect to DSM’s future (financial) performanceand position. Such statements are based on current expectations, estimates and projections of DSM andinformation currently available to the company.

Examples of forward-looking statements include statements made or implied about the company’s strategy,estimates of sales growth, financial results, cost savings and future developments in its existing business aswell as the impact of future acquisitions, and the company’s financial position. These statements can bemanagement estimates based on information provided by specialized agencies or advisors.

DSM cautions readers that such statements involve certain risks and uncertainties that are difficult topredict and therefore it should be understood that many factors can cause the company’s actualperformance and position to differ materially from these statements.

These factors include, but are not limited to, macro-economic, market and business trends and conditions,(low-cost) competition, legal claims, the ability to protect intellectual property, changes in legislation,changes in exchange and interest rates, changes in tax rates, pension costs, raw material and energy prices,employee costs, the implementation of the company’s strategy, the company’s ability to identify andcomplete acquisitions and to successfully integrate acquired companies, the company’s ability to realizeplanned disposals, savings, restructuring or benefits, the company’s ability to identify, develop andsuccessfully commercialize new products, markets or technologies, economic and/or political changes andother developments in countries and markets in which DSM operates.

As a result, DSM’s actual future performance, position and/or financial results may differ materially fromthe plans, goals and expectations set forth in such forward-looking statements.

DSM has no obligation to update the statements contained in this document, unless required by law. TheEnglish language version of this document is leading.

A more comprehensive discussion of the risk factors affecting DSM’s business can be found in the company’slatest Annual Report, a copy of which can be found on the company’s corporate website, www.dsm.com

26

27

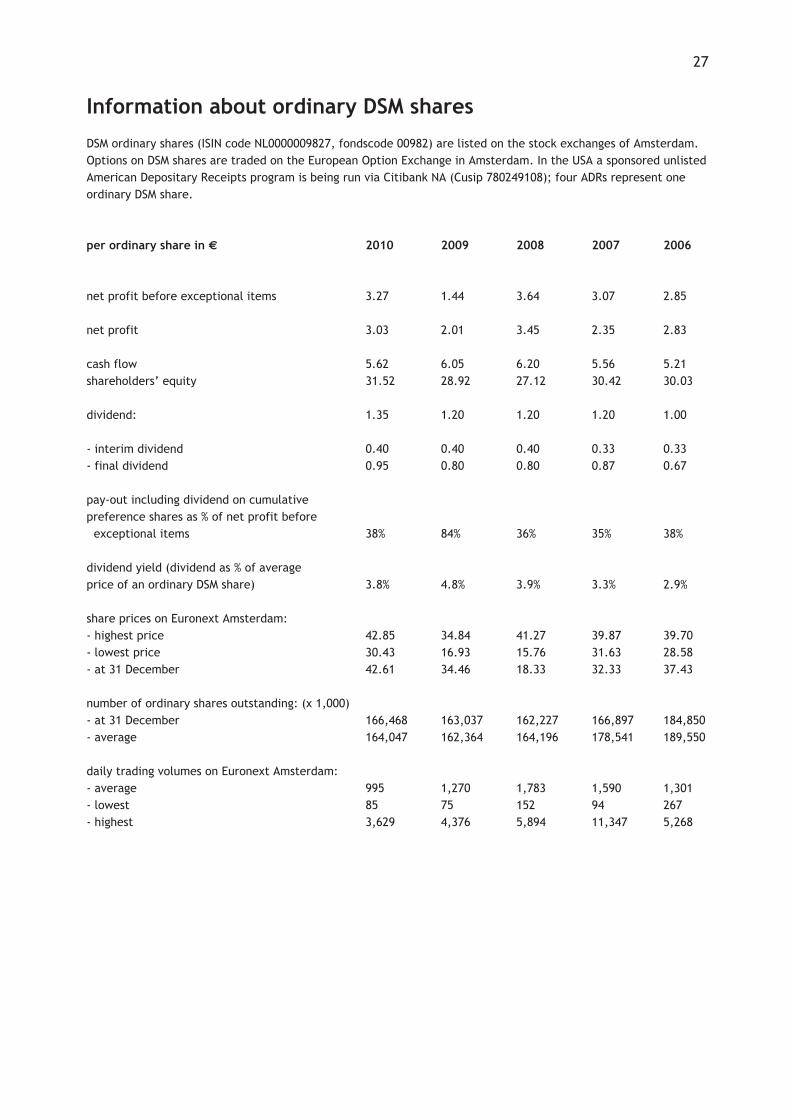

Information about ordinary DSM shares

DSM ordinary shares (ISIN code NL0000009827, fondscode 00982) are listed on the stock exchanges of Amsterdam.Options on DSM shares are traded on the European Option Exchange in Amsterdam. In the USA a sponsored unlistedAmerican Depositary Receipts program is being run via Citibank NA (Cusip 780249108); four ADRs represent oneordinary DSM share.

per ordinary share in € 2010 2009 2008 2007 2006

net profit before exceptional items 3.27 1.44 3.64 3.07 2.85

net profit 3.03 2.01 3.45 2.35 2.83

cash flow 5.62 6.05 6.20 5.56 5.21shareholders’ equity 31.52 28.92 27.12 30.42 30.03

dividend: 1.35 1.20 1.20 1.20 1.00

- interim dividend 0.40 0.40 0.40 0.33 0.33 - final dividend 0.95 0.80 0.80 0.87 0.67

pay-out including dividend on cumulative preference shares as % of net profit before

exceptional items 38% 84% 36% 35% 38%

dividend yield (dividend as % of average price of an ordinary DSM share) 3.8% 4.8% 3.9% 3.3% 2.9%

share prices on Euronext Amsterdam: - highest price 42.85 34.84 41.27 39.87 39.70 - lowest price 30.43 16.93 15.76 31.63 28.58- at 31 December 42.61 34.46 18.33 32.33 37.43

number of ordinary shares outstanding: (x 1,000) - at 31 December 166,468 163,037 162,227 166,897 184,850- average 164,047 162,364 164,196 178,541 189,550

daily trading volumes on Euronext Amsterdam:- average 995 1,270 1,783 1,590 1,301 - lowest 85 75 152 94 267- highest 3,629 4,376 5,894 11,347 5,268

Address:DSM Investor RelationsP.O. Box 6500, 6401 JH HeerlenThe NetherlandsPhone: +31 45 5782864Fax: +31 10 45 90275Email: [email protected]

www.dsm.com

Presentation to Investors Life Sciences and Materials Sciences

Royal DSM N.V.Q1 2011 Results