presentation to the ncsl ynp’s next-gen legislators pre

TRANSCRIPT

Better Budgeting PracticesPresentation to the

NCSL YNP’s Next-Gen Legislators Pre-Conference

December 9, 2015

Luke E. Martel

Director of Strategic Initiatives

Presentation Outline

• State Budgeting 101

• Budgeting Approaches

– Types

– Pros and Cons

– ZBB

• Better Budgeting Principles

– Finding common ground

– Developing a system

– Common mistakes to avoid

2

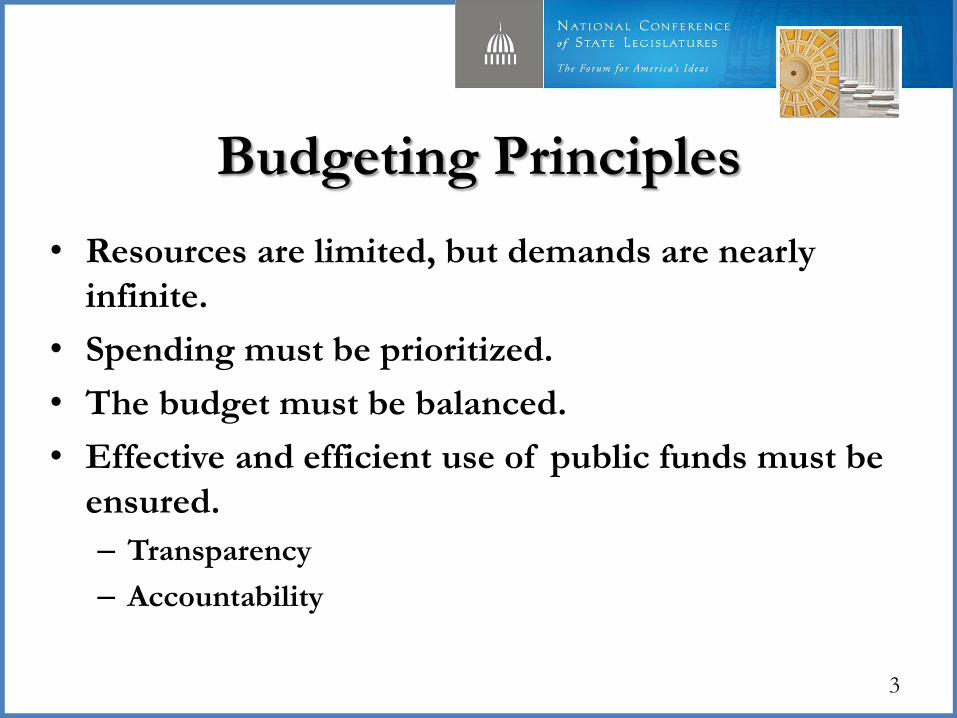

Budgeting Principles

• Resources are limited, but demands are nearly

infinite.

• Spending must be prioritized.

• The budget must be balanced.

• Effective and efficient use of public funds must be

ensured.

– Transparency

– Accountability

3

Major Components of General Fund

Appropriations, FY 2015

4

32.2%

9.1%

5.2%

20.6%

32.9%

K-12 Education

Higher Education

Corrections

Medicaid

Other

State Budget Roles

• Legislative branch– Establishes balanced budget: deliberates, prioritizes,

authorizes/appropriates funds, enacts budget bill(s)– Reviews results and provides oversight

• Executive branch– Prepares agency budget requests

– Approves or vetoes budget bills

– Implements enacted budget

• Judicial branch– Resolves disputes between the other two branches

5

Fiscal Years

• April 1 – March 31 — New York

• July 1 – June 30 — 46 states

• Sept. 1 – Aug. 31 — Texas

• Oct. 1 – Sept. 30 — Alabama and Michigan

• Oct. 1 – Sept. 30 — Federal Government

6

State Budget Calendars

7

Jan. Feb. Mar. Apr. May Jun.Jul. Aug. Sep. Oct. Nov. Dec.

Gov. submits

budget

Legislature

adopts budget

Agencies submit

requests

Agency

hearings

Fiscal year

begins

Agency hearings

continue

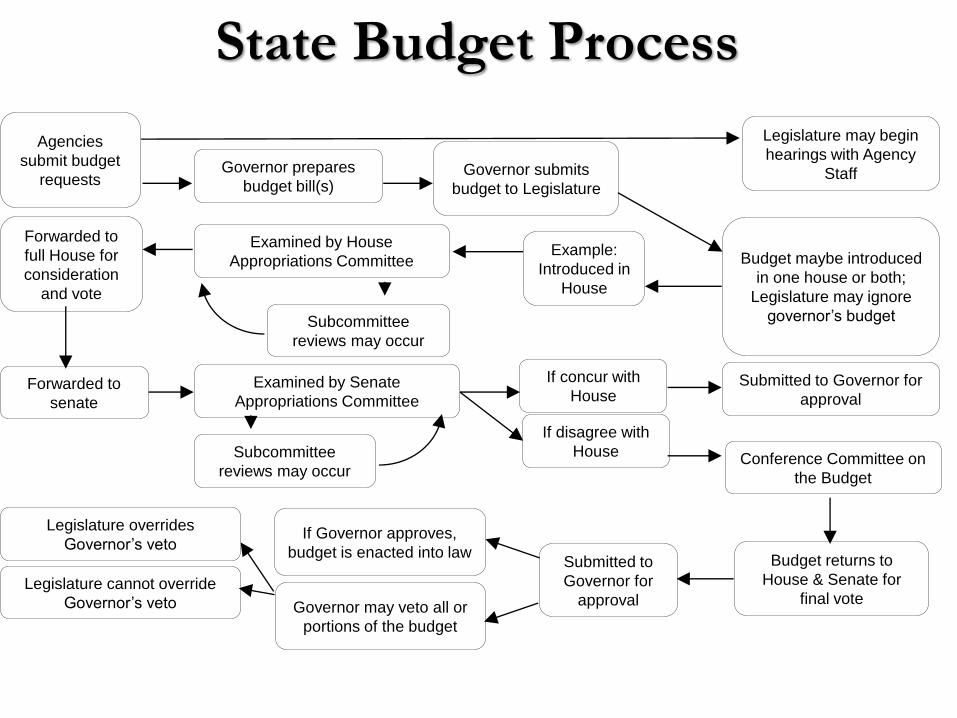

State Budget Process

Agencies

submit budget

requestsGovernor prepares

budget bill(s)Governor submits

budget to Legislature

Legislature may begin

hearings with Agency

Staff

Forwarded to

full House for

consideration

and vote

Examined by House

Appropriations Committee

Subcommittee

reviews may occur

Example:

Introduced in

House

Budget maybe introduced

in one house or both;

Legislature may ignore

governor’s budget

Forwarded to

senate

Examined by Senate

Appropriations Committee

Subcommittee

reviews may occur

Submitted to Governor for

approval

Conference Committee on

the Budget

Legislature overrides

Governor’s veto

Legislature cannot override

Governor’s veto

If Governor approves,

budget is enacted into law

Governor may veto all or

portions of the budget

Submitted to

Governor for

approval

Budget returns to

House & Senate for

final vote

If concur with

House

If disagree with

House

Budget Cycle

9

• Annual budget: 31 states

• Biennial with two annual budgets: 15 states

• True biennial budget: 4 states

The success of a budget cycle seems to depend on the commitment of state officials to good implementation rather than on the method

itself.

Number of Budget Bills

10

• Single budget bills: 18 states

• Multiple budget bills (3-1,500): 32 states

Revenue Forecasts

11

• Consensus forecast: 22

states

• Executive forecast: 17 states

• Other process: 11 states

• Official forecast binds the

budget: 26 states

When State Budgets are Late

12

• Continuing resolutions: 9 states

• Certain payments continue: 12 states

• Government shuts down: 23 states

• No provision/ untested: 12 states

• Other (e.g., session extended): 6 states

Executive Authority to Cut the

Enacted Budget

13

• No restrictions: 12 states

• Across-the-board cuts only: 10 states

• Maximum percentage reduction: 7 states

• Must consult legislature: 12 states

• Other: 29 states

Budgeting 101 - Summary

14

• A budget is the most important document

the legislature considers because it allocates

resources.

• The budget must be balanced.

• Approaches vary across the states.

• The process is ongoing.

Types of Budget Approaches

15

• Traditional/incremental– Line item – detailed, review changes

– Program – broader categories, review activities

• Performance – set goals, review effectiveness, provide flexibility

• Zero base – start each budget item at zero

• Hybrid approaches

Traditional/Incremental Budgeting

16

• In typical budget process, budget analysts:

– Review dollar changes in agency/program

– Look at FTE changes

– Calculate percentage changes

– Analyze cost per service recipient

– Review program history

– Other?

Traditional/Incremental Budgeting

17

• Focus is on what money buys (an input) rather than on the service that is provided (an outcome).

• Outcomes can be considered, but traditional budgeting does not encourage it.

Performance-Based Budgeting

18

• Tie budgets to performance

• Improve performance by counting,

measuring, comparing, benchmarking

• Reward success, penalize failure

• “What gets measured gets done”

- Peter Drucker, Management Consultant

What are the benefits of

performance budgeting?

19

• Better understanding of state programs;

• Explanations of previous funding decisions;

• Program effectiveness (outcomes);

• Program efficiency (costs and benefits);

• The justification for new funding decisions;

• The identification of potential savings;

• Quantitative evidence of program success and shortcomings; and

• Communicating what is received in return for the investment of tax dollars.

20

What does performance budgeting

do for legislators?• A powerful to tool to improve government

management

• Helps meet legislators’ and voters’ needs for:– Accountability

– Orientation to service

– Quality measurement

• Encourages long-term perspective

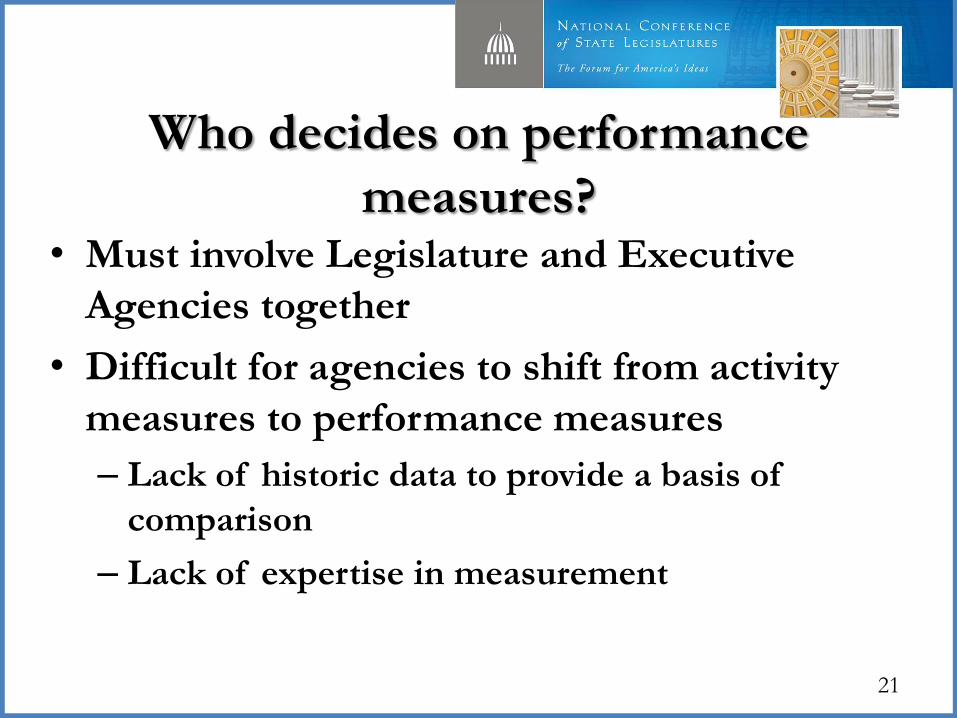

Who decides on performance

measures?

21

• Must involve Legislature and Executive

Agencies together

• Difficult for agencies to shift from activity

measures to performance measures

– Lack of historic data to provide a basis of

comparison

– Lack of expertise in measurement

Budget Process

22

• Focus on programs rather than line item

expenditures

• Focus on performance, not who-does-what

• Focus on outcomes, not what goes into

agency programs

23

Zero-Based Budgeting• Pure ZBB does not exist.

• Modified ZBB is also known as alternative budgeting or targeted budgeting.

• Agencies make requests at various percentages of their previous funding i.e., at 90%, 100% and 110% – and analyze what effects those levels would have on their programs.

Why Traditional Budgeting Survives

24

• Provides predictability and stability for agency and program planning.

• Time constraints

• Budgeting is complicated. Budgets must respond to many different competing needs and goals, which can be difficult to measure.

25

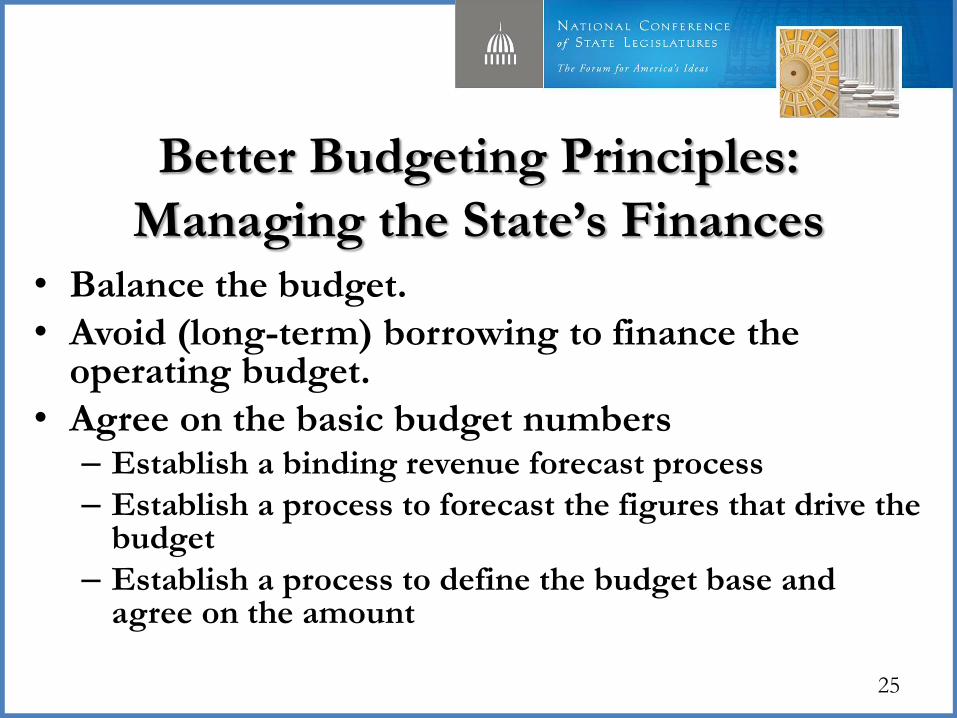

Better Budgeting Principles:

Managing the State’s Finances• Balance the budget.

• Avoid (long-term) borrowing to finance the operating budget.

• Agree on the basic budget numbers– Establish a binding revenue forecast process

– Establish a process to forecast the figures that drive the budget

– Establish a process to define the budget base and agree on the amount

26

Better Budgeting Principles:

Developing a system

• Account for and review tax expenditures:

– Account for all tax expenditures in a

comprehensive tax expenditure budget,

– Establish a process to review tax expenditures on a

regular cycle.

• Develop clear guidelines for capital budgeting.

27

Better Budgeting Principles

Common Mistakes to Avoid• Beware of quick fixes that create long-term problems

– Be very cautious when spending reserve funds.

– Don’t intentionally overestimate revenue or underestimate expenses, especially when it comes to the retirement system.

– Don’t expect too much from early retirement incentives.

– Don’t make short-term budget decisions without considering the long-term effects.

– Protect the tax base through good and bad times.

29

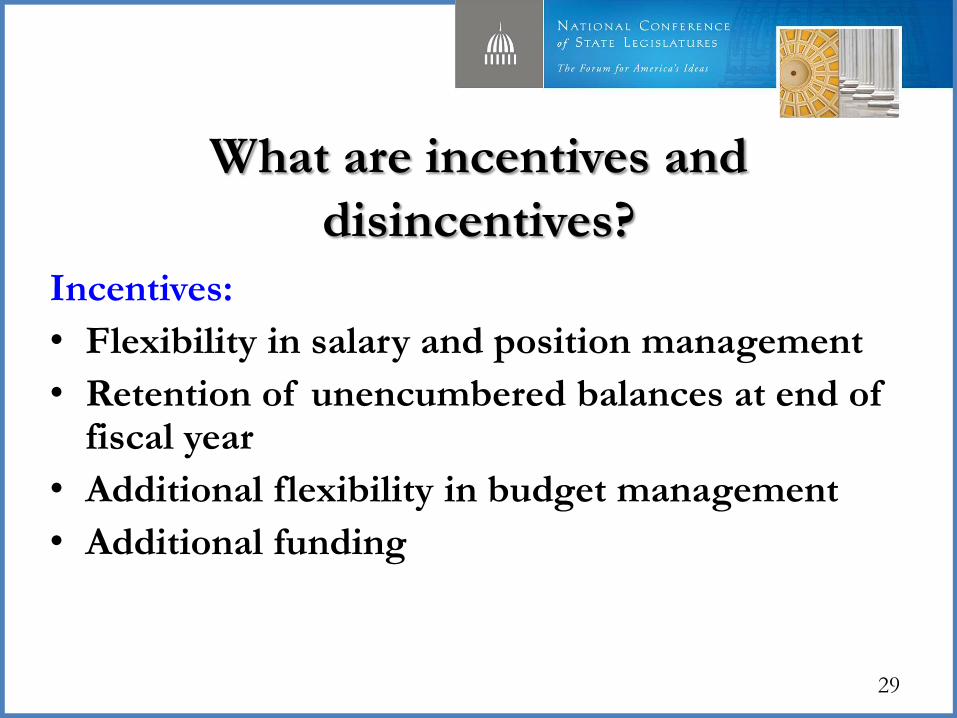

What are incentives and

disincentives?

Incentives:

• Flexibility in salary and position management

• Retention of unencumbered balances at end of fiscal year

• Additional flexibility in budget management

• Additional funding

30

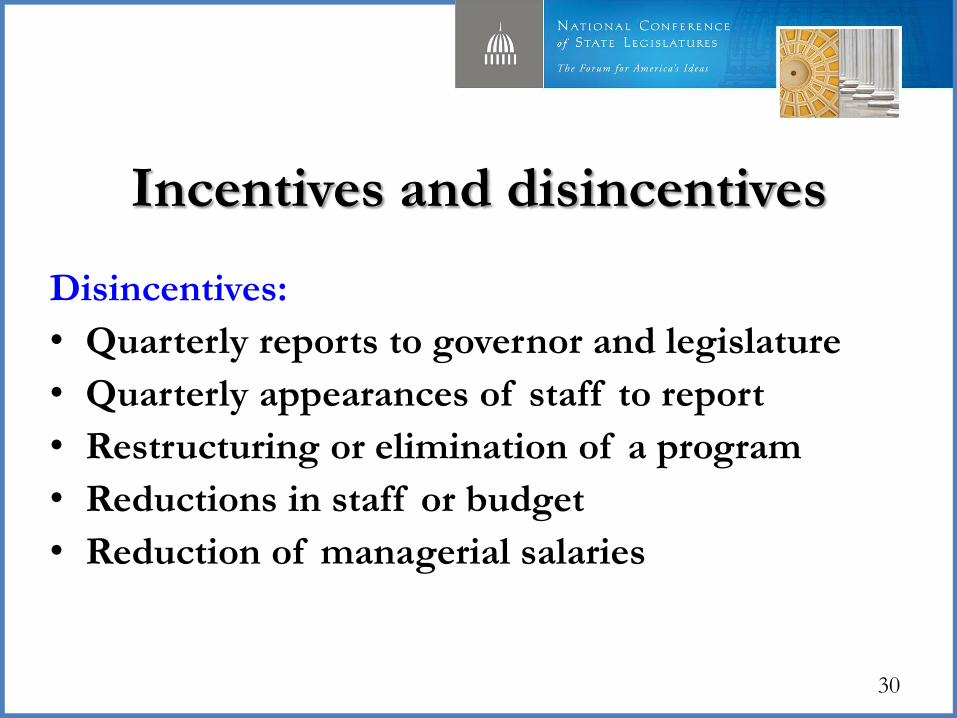

Incentives and disincentives

Disincentives:

• Quarterly reports to governor and legislature

• Quarterly appearances of staff to report

• Restructuring or elimination of a program

• Reductions in staff or budget

• Reduction of managerial salaries

What are the costs of performance

budgeting?

31

• Learning to use a completely different

process.

• Less direct legislative control of agencies.

• Shift power to executive branch.

• Heavy demands on legislators’ and staff

time.

Demands on state agencies

32

• Mission Statement (What’s the agency for?)

• Goals (General purposes)

• Objectives (Specific action plans)

• Performance measures (How well are they

doing?)

33

Performance budgeting can improve

agency management• Systematic review of agency organization and

purpose.

• Helps identify performing and non-performing parts of government.

• Encourages long-term planning.

• Makes everyone consider purposes of government.

34

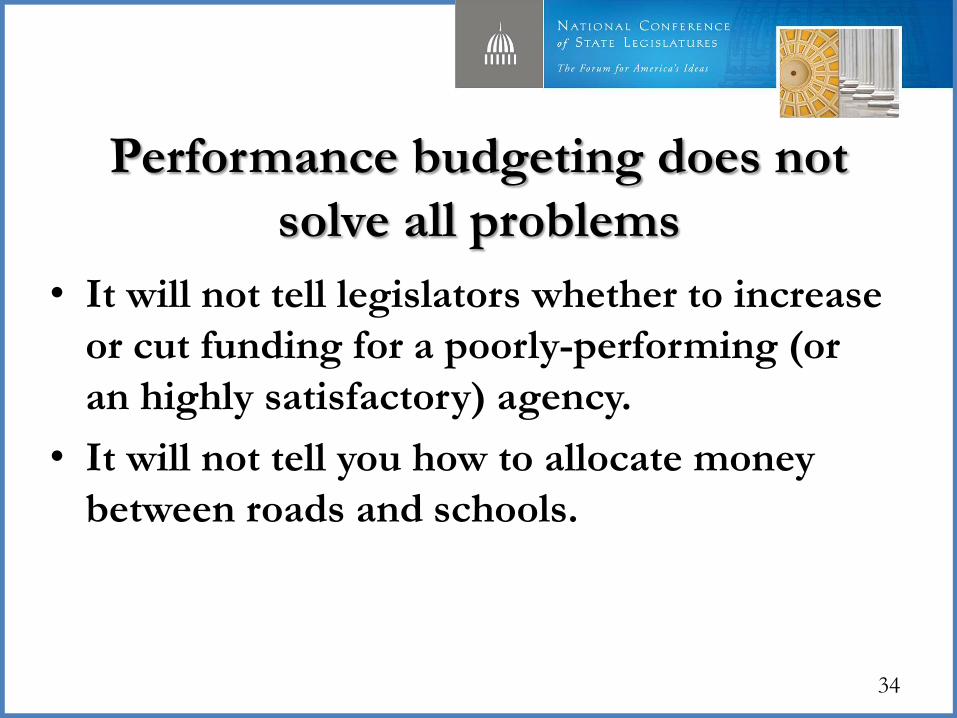

Performance budgeting does not

solve all problems

• It will not tell legislators whether to increase

or cut funding for a poorly-performing (or

an highly satisfactory) agency.

• It will not tell you how to allocate money

between roads and schools.

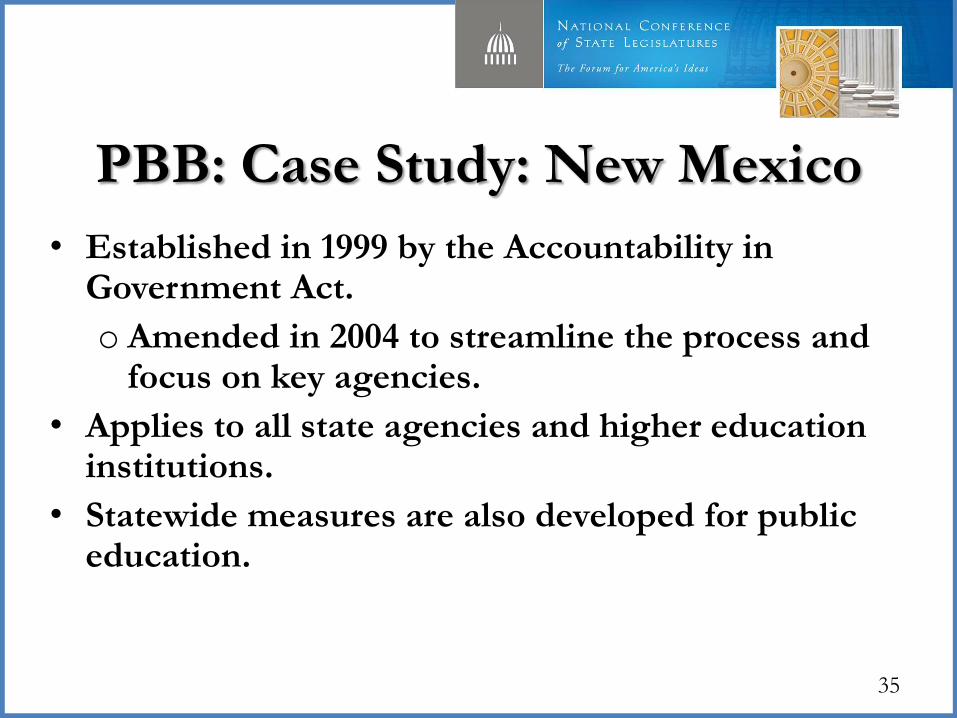

PBB: Case Study: New Mexico

• Established in 1999 by the Accountability in Government Act.

o Amended in 2004 to streamline the process and focus on key agencies.

• Applies to all state agencies and higher education institutions.

• Statewide measures are also developed for public education.

35

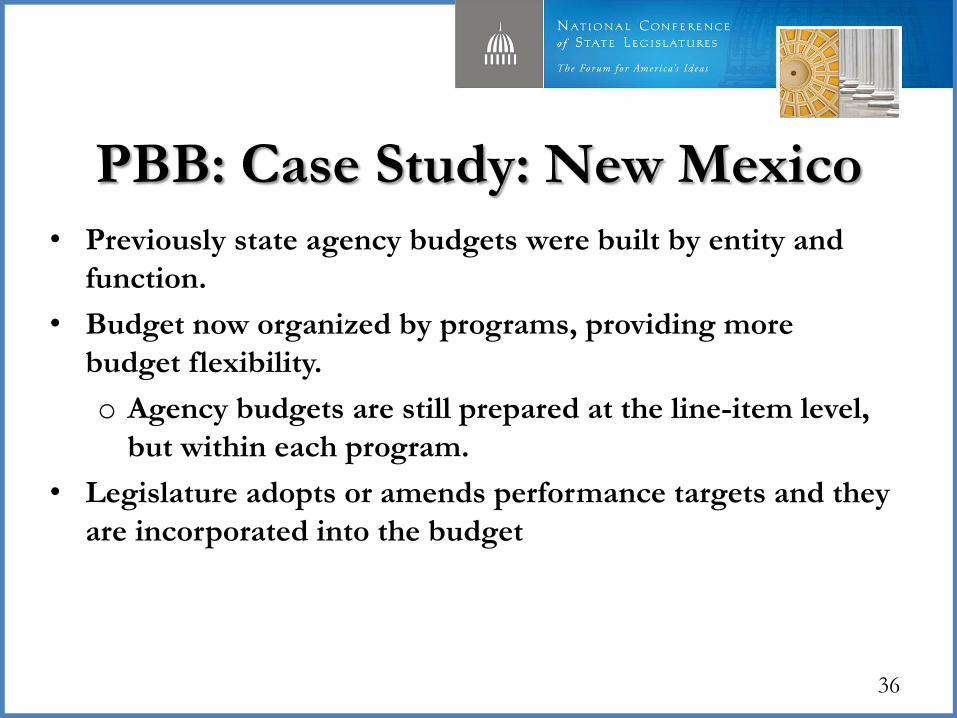

PBB: Case Study: New Mexico

• Previously state agency budgets were built by entity and

function.

• Budget now organized by programs, providing more

budget flexibility.

o Agency budgets are still prepared at the line-item level,

but within each program.

• Legislature adopts or amends performance targets and they

are incorporated into the budget

36

New Mexico “Report Card”

37

38

PBB: Case Study: Texas

• Biennial budgeting; legislature meets every

other year.

• Strong legislature vis-à-vis governor.

• Historic use of performance budgeting and

strategic planning.

Texas-State Agency Strategic Planning• Enacted in 1991 by H.B. 2009.

• Requires all executive branch

agencies to complete strategic

plans every 2 years.

• 5 year planning horizon.

• Plan rules promulgated by

Legislative Budget Board &

Governor's Office of Budget,

Planning & Policy.

http://www.lbb.state.tx.us/Instructions/Instructions%20for%20Preparing%20a

nd%20Submitting%20Agency%20Strategic%20Plans.pdf39

Texas-State Agency Strategic Planning

Plan instructions:

http://www.lbb.state.tx.us/Instructions/Instructions%20for%20Preparing%20an

d%20Submitting%20Agency%20Strategic%20Plans.pdf

TDHCA Plan: http://www.tdhca.state.tx.us/housing-

center/docs/12-stratplanFY13-17.pdf 40

41

Texas Sunset Advisory Commission

• 12-member legislative commission tasked with identifying

and eliminating waste, duplication, and inefficiency for

more than 130 Texas state agencies.

– Questions the need for each agency,

– Looks for potential duplication of other public services or programs,

– Considers new and innovative changes to improve each agency's

operations and activities.

• Since inception in 1977, 79 agencies have been abolished,

including 37 agencies that were completely abolished and

42 that were abolished with certain functions transferred to

existing or newly created agencies.

42

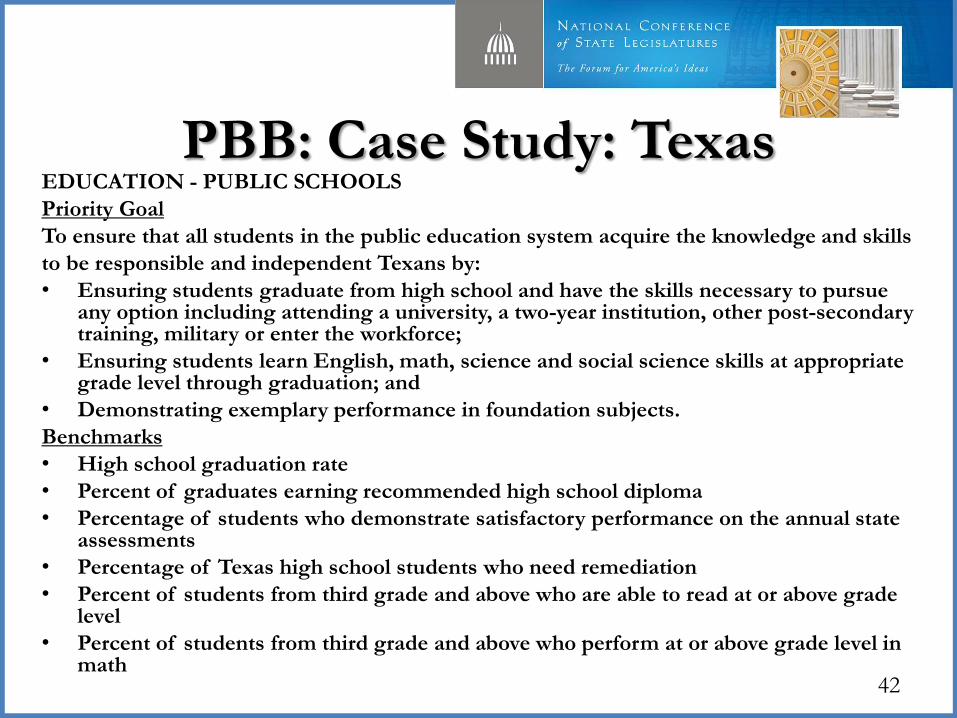

PBB: Case Study: TexasEDUCATION - PUBLIC SCHOOLS

Priority Goal

To ensure that all students in the public education system acquire the knowledge and skills

to be responsible and independent Texans by:

• Ensuring students graduate from high school and have the skills necessary to pursue any option including attending a university, a two-year institution, other post-secondary training, military or enter the workforce;

• Ensuring students learn English, math, science and social science skills at appropriate grade level through graduation; and

• Demonstrating exemplary performance in foundation subjects.

Benchmarks

• High school graduation rate

• Percent of graduates earning recommended high school diploma

• Percentage of students who demonstrate satisfactory performance on the annual state assessments

• Percentage of Texas high school students who need remediation

• Percent of students from third grade and above who are able to read at or above grade level

• Percent of students from third grade and above who perform at or above grade level in math

43

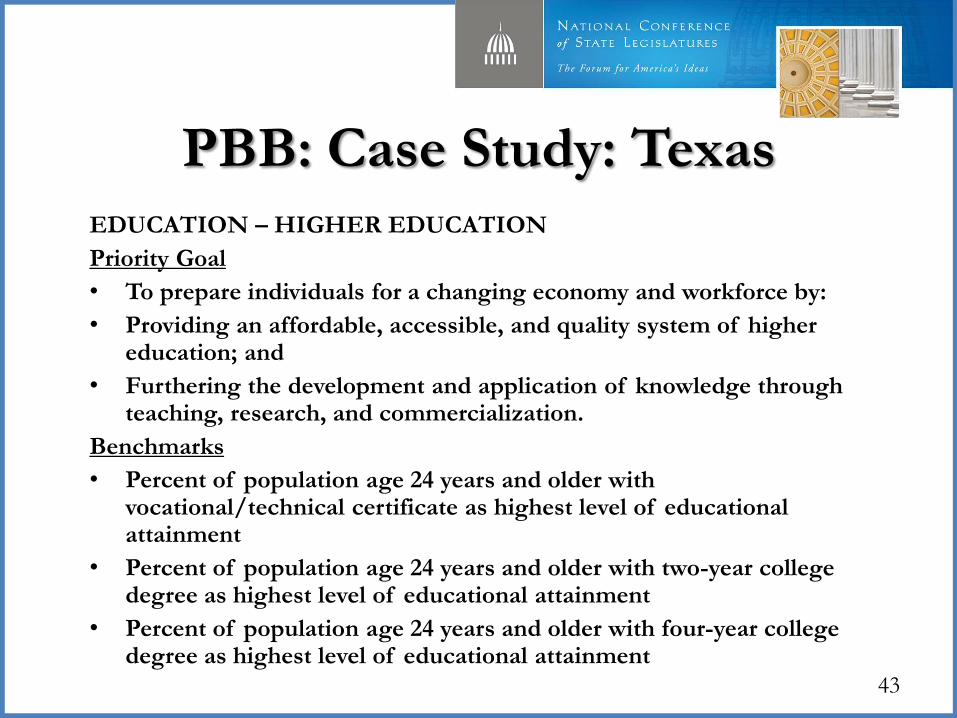

PBB: Case Study: TexasEDUCATION – HIGHER EDUCATION

Priority Goal

• To prepare individuals for a changing economy and workforce by:

• Providing an affordable, accessible, and quality system of higher education; and

• Furthering the development and application of knowledge through teaching, research, and commercialization.

Benchmarks

• Percent of population age 24 years and older with vocational/technical certificate as highest level of educational attainment

• Percent of population age 24 years and older with two-year college degree as highest level of educational attainment

• Percent of population age 24 years and older with four-year college degree as highest level of educational attainment

Tennessee Outcomes Based Funding Formula

• Complete College Tennessee Act (2010) instituted an

outcomes-based funding formula for higher education.

• Designed to encourage college degree completion and

other productivity goals.

• Unlike performance budgeting, the funding is not tied to

targets or measures, so an institution is not punished for

failing to meet a specific goal.

44