presented by- ca amitoz singh kamboj tax faculty: ca – ipcc, final edushelf innovations pvt. ltd....

TRANSCRIPT

Presented by- CA Amitoz Singh KambojTAX Faculty: CA – IPCC, FINALEdushelf Innovations Pvt. Ltd.Ascend Edusys Pvt. Ltd.www.cawebworld.com

INTRODUCTION

2

Capital Gain Tax was introduced in the year 1946.Capital Gain Tax was introduced in the year 1946.

It was scrapped in the year 1948.It was scrapped in the year 1948.

However, it was resurrected in the year 1956 by Prof. Nicholas Kaldor as a part of his tax reform process.

However, it was resurrected in the year 1956 by Prof. Nicholas Kaldor as a part of his tax reform process.

INTRODUCTION – Contd.

3

The main principle of taxing the Capital Gains is that apart from revenue gains, the gains of

capital in nature shall also be taxed u/s 45 of the Income-Tax Act, 1961

The main principle of taxing the Capital Gains is that apart from revenue gains, the gains of

capital in nature shall also be taxed u/s 45 of the Income-Tax Act, 1961

The gain arising out of transfer of Capital Asset will be charged to Tax under the head Capital

Gains.

The gain arising out of transfer of Capital Asset will be charged to Tax under the head Capital

Gains.

Capital Gain is covered between Section 45 to Section 55A

Capital Gain is covered between Section 45 to Section 55A

Conditions to be satisfied for taxation of Gains

4

There must be a Capital Asset which is ownedThere must be a Capital Asset which is owned

by the Assessee.by the Assessee.

There must be gain or loss as a result of such transfer.There must be gain or loss as a result of such transfer.

by the assessee during the previous year.by the assessee during the previous year.

The Capital Asset must have been transferredThe Capital Asset must have been transferred

This transaction is known as Capital Gains under I. Tax Act.This transaction is known as Capital Gains under I. Tax Act.

What is a Capital Asset

5

As per Section 2(14), Capital Asset means property of any kind held by the assessee.

Exception to Section 2(14): Any stock-in-trade or raw materials or consumable stores, Personal effects (movable), Agricultural land in India which is not an urban agricultural

land, 6.5% Gold bonds 1977, 7% Gold bonds 1980 or National

defence Gold Bonds, 1980 issued by Central Government, Special Bearer Bonds, 1991 issued by the Government, Gold Deposit Bonds issued under Gold Deposit Scheme,

1999.

Personal effects are excluded from Capital Assets:

6

Personal assets are excluded from the Capital Assets itself and any gain on transfer of personal assets is not taxable at all.

What is a Personal Effects

7

In Personal assets some degree of connection between the assessee and the item is necessary. The assessee need not necessarily be able to wear the items on his or her person.

House Hold items and utensils can also be personal effects.

A distinction is to be borne in mind as between the personal effects and the assets intended for use in the Business or profession.

Smt. Shree Kumari Mundra v/s. CIT (1997) 228 ITR 548 (Cal)

Personal assets which shall be taxable under Capital Gains

8

Silver bars and Bullion even held personally are not personal assets.

(H.H. Maharaja Hemant Singhjee v/s. CIT (1976) 103 ITR 51 (SC)

Loose diamonds which are held for personal use or not are taxable Capital Assets.

(CIT v/s. Smt. Saroj Goenka (1983) 140 ITR 88 (Mad.) Gold utensils are not personal effects.

What are held to be personal effects

9

Silver utensils held by the assessee that were not in daily use but only on occasion is personal effects. All that was required is that the article should be meant for personal use of the assessee in ordinary course and it was not necessary that they should be used daily.

Jayantilal A. Shah v/s. CIT (1985) 156 ITR 448 (Bom.)

Personal Effects : Question

10

The assessee purchased a race horse for Rs. 15000/-. The horse gave birth to a colt and filly. The assessee sold the horse, colt and filly for Rs. 50,000/-. The Assessing Officer wants to tax Rs. 35,000/- as Capital Gains.

The assessee has incurred Rs. 21,000/- on the maintenance of the horse during the period of pregnancy.

The assessee also incurred expenses of Rs. 5,000/- on the training of the horse, colt and filly.

The assessee claims Rs. 26,000/- as a deduction while computing the Capital Gains.

Personal Effects : Answer

11

The amount spent by the assessee on the maintenance of the horse during the pregnancy period was really for protecting, preserving and keep the horse in good health, so that, the healthy off-springs are born.

The maintenance expenses on the horse during the pregnancy period are in fact to bring into existence colt & filly and therefore can be regarded as cost of acquisition of colt and filly.

It was held in CIT vs. Ramaswamy Mudaliar (Mad.) that the expenses incurred above shall be allowed as deduction while computing the Capital Gains.

Meaning of Property

12

Property of any kind used in section 2(14) is of widest amplitude which includes tangible as well as intangible rights.

Right to manage one’s business is not only a property but the same is also an asset in the nature of Fixed Asset. CIT vs. National Insurance Co. Ltd. (1978) 113 ITR 37 (Cal.)

Rural Agricultural land – Section 2(14)(iii) w.e.f. Assessment Year 2014-15

13

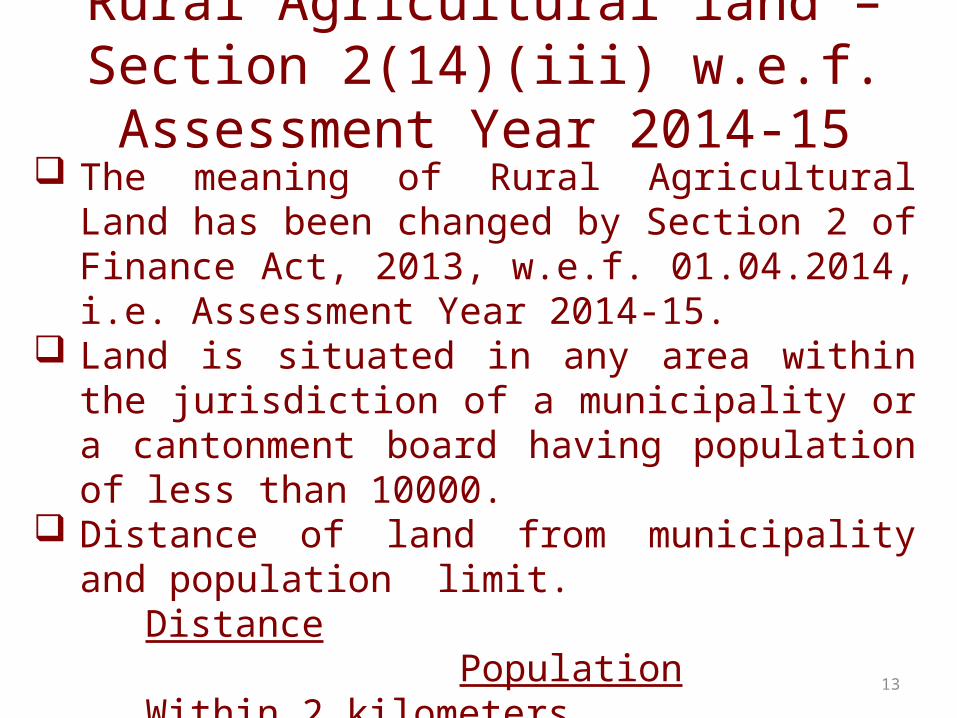

The meaning of Rural Agricultural Land has been changed by Section 2 of Finance Act, 2013, w.e.f. 01.04.2014, i.e. Assessment Year 2014-15.

Land is situated in any area within the jurisdiction of a municipality or a cantonment board having population of less than 10000.

Distance of land from municipality and population limit.

Distance Population Within 2 kilometers 10,000-1,00,000

Within 6 kilometers 1,00,000-10,00,000

Within 8 kilometers More than 10,00,000

Whether the following shall be treated as Capital Asset

14

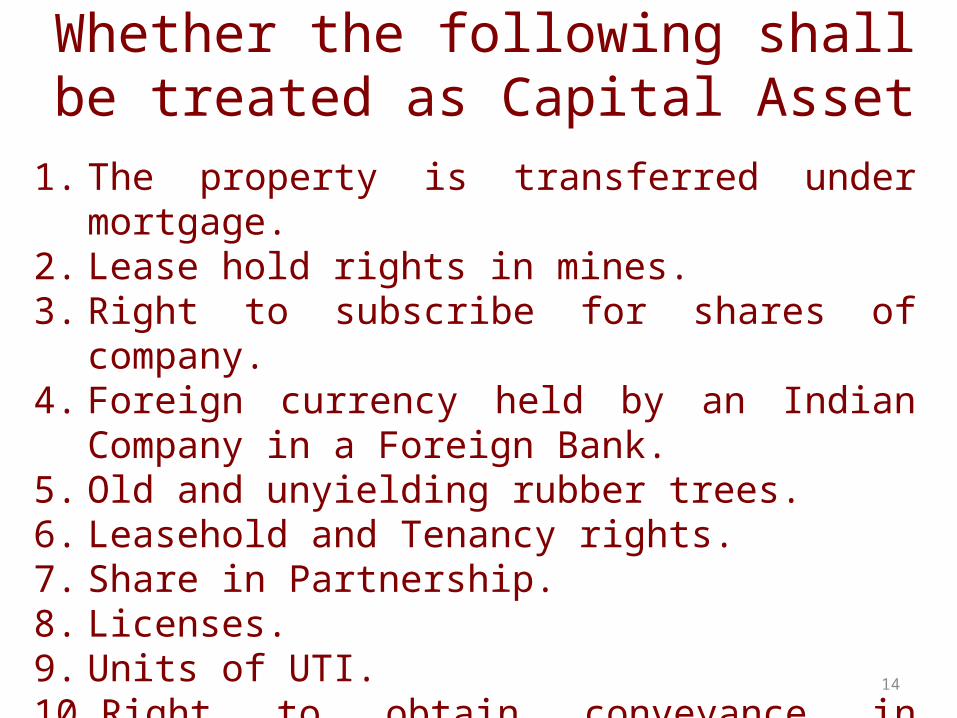

1. The property is transferred under mortgage.2. Lease hold rights in mines.3. Right to subscribe for shares of company.4. Foreign currency held by an Indian Company in a

Foreign Bank.5. Old and unyielding rubber trees.6. Leasehold and Tenancy rights.7. Share in Partnership.8. Licenses.9. Units of UTI.10. Right to obtain conveyance in immovable property.11. Right to claim specific performance

Whether the following shall be treated as Capital Asset – Contd.

15

12. Precious Stones13. Fixed Deposit in Bank14. National Saving Certificates15. Compensation received by the lessor of agricultural

land for removing the trees from the land16. Trees standing on Agricultural Land17. Industrial Licenses18. Goodwill of the Business

Extended meaning of Capital Asset u/s 2(14)

16

To nulify the Judgment of Apex Court in the case of Vodafone International Holdings B.V. vs. Union of India (2012) 204 Taxman 408 (SC), the following explanation has been inserted by the Finance Act 2012, w.r.e.f. 1.4.1962.

For removal of doubts it is hereby clarified that property includes and shall be deemed to have always included, any rights in or in relation to an Indian Company, including rights of management or control or any other rights whatsoever.

Salient features of Capital Assets

17

The property transferred must be a Capital Asset on the date of transfer even though it was not a Capital Asset at the time of acquisition. – Nachiappan vs. CIT (1998) 230 ITR 98 (Mad.)

If the asset on the date of transfer is not a capital asset, the question of Capital Gains does not arise. – (CIT vs. Jitender Ram Mittal (1980) 162 ITR 271 (Guj.)

PERSONAL EFFECTS

18

Movable personal effects including wearing apparel and furniture which are held for personal use shall not be treated as Capital Assets u/s 2(14).

However, even the following assets are held personally and the same are movable also, they will be considered as Capital Assets u/s 2(14):

Jewellery, Archaeological Collection, Drawings, Painting, Sculptures, Work of art.

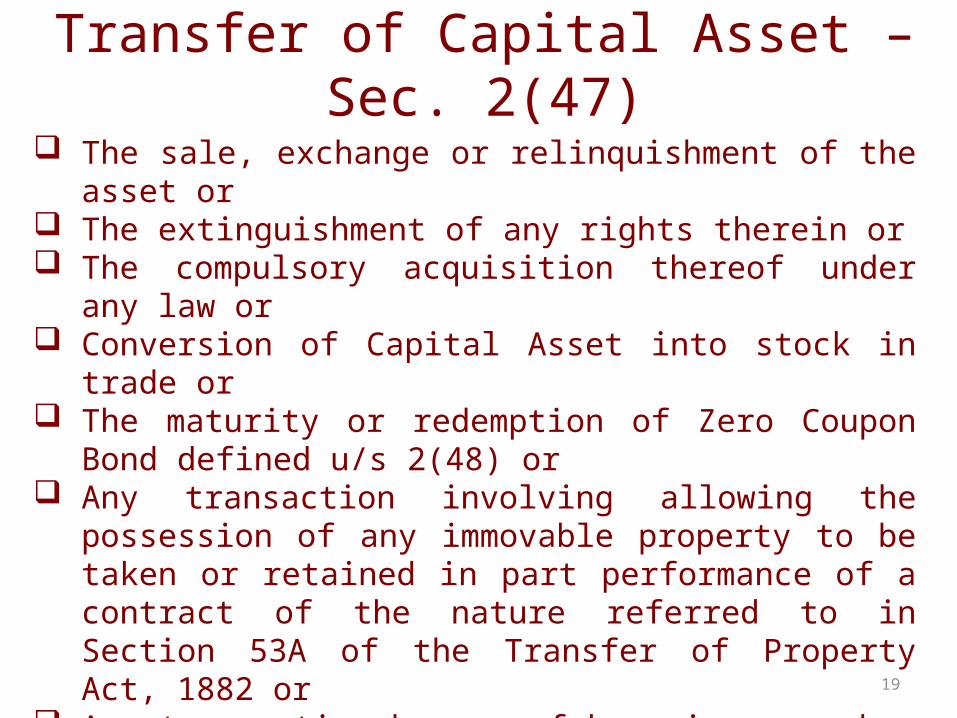

Transfer of Capital Asset – Sec. 2(47)

19

The sale, exchange or relinquishment of the asset or The extinguishment of any rights therein or The compulsory acquisition thereof under any law or Conversion of Capital Asset into stock in trade or The maturity or redemption of Zero Coupon Bond defined u/s

2(48) or Any transaction involving allowing the possession of any

immovable property to be taken or retained in part performance of a contract of the nature referred to in Section 53A of the Transfer of Property Act, 1882 or

Any transaction by way of becoming a member of or acquiring shares in a co-operative society, company, or other association of person by way of any agreement which has the effect of transferring or enabling to enjoyment of any immovable property.

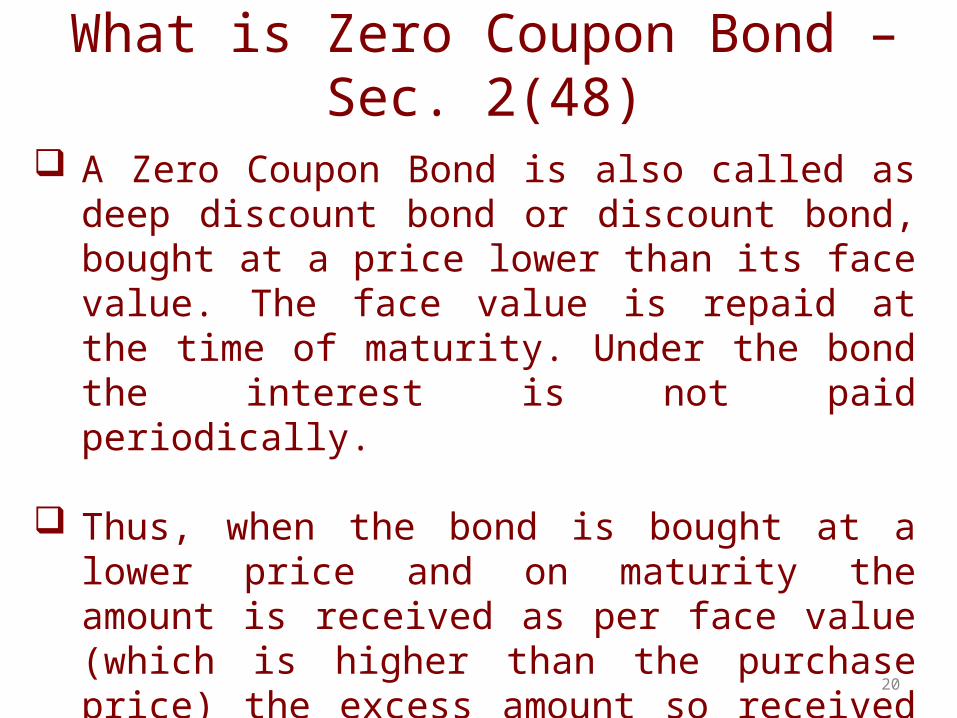

What is Zero Coupon Bond – Sec. 2(48)

20

A Zero Coupon Bond is also called as deep discount bond or discount bond, bought at a price lower than its face value. The face value is repaid at the time of maturity. Under the bond the interest is not paid periodically.

Thus, when the bond is bought at a lower price and on maturity the amount is received as per face value (which is higher than the purchase price) the excess amount so received shall be treated as transfer u/s 2(47) and shall be chargeable to Capital Gains.

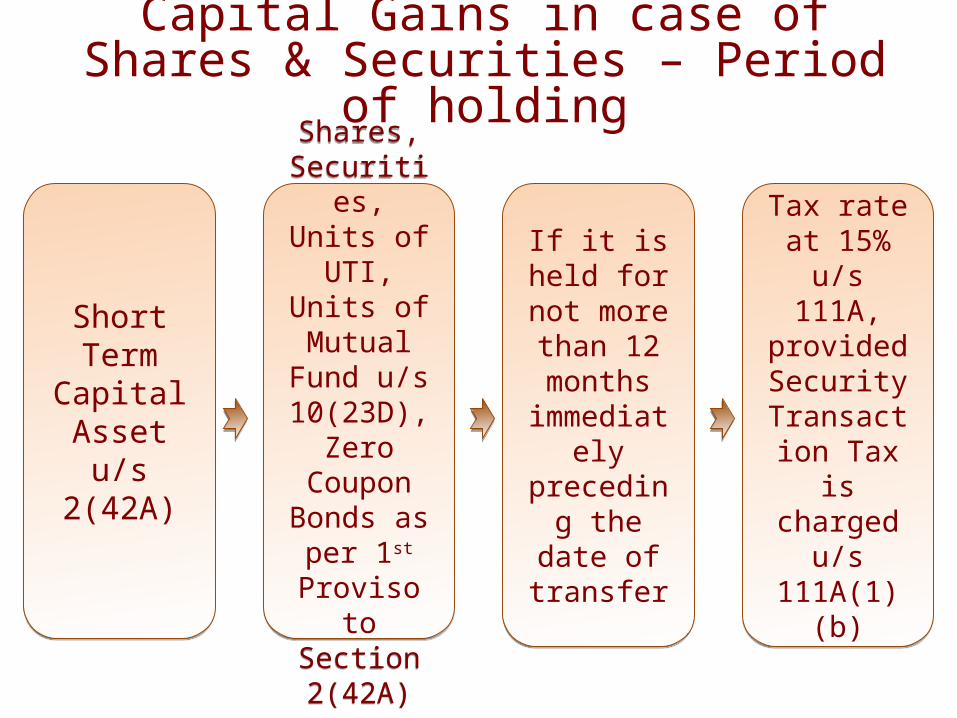

Types of Capital Assets

21

There are two types of Capital Assets:

Section 2(42A)Section 2(42A)

Exception – Proviso 1 to Sec. 2(42A)

Exception – Proviso 1 to Sec. 2(42A)

Short Term Capital Assets are those which are held by the assessee for not more than 36 months, immediately preceding the date of its transfer.

Short Term Capital Assets are those which are held by the assessee for not more than 36 months, immediately preceding the date of its transfer.

In case of a share or any other security listed in RSE in India or a unit of UTI, or a unit of Mutual Fund or a Zero Coupon Bonds if held for not more than twelve months, the same shall be treated as STCA.

In case of a share or any other security listed in RSE in India or a unit of UTI, or a unit of Mutual Fund or a Zero Coupon Bonds if held for not more than twelve months, the same shall be treated as STCA.

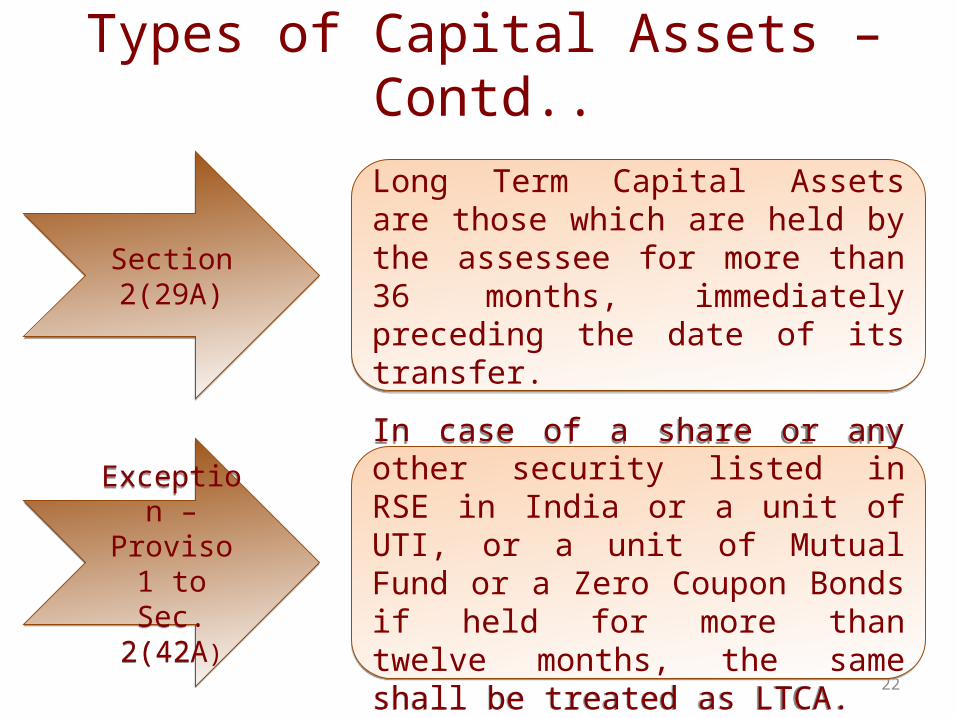

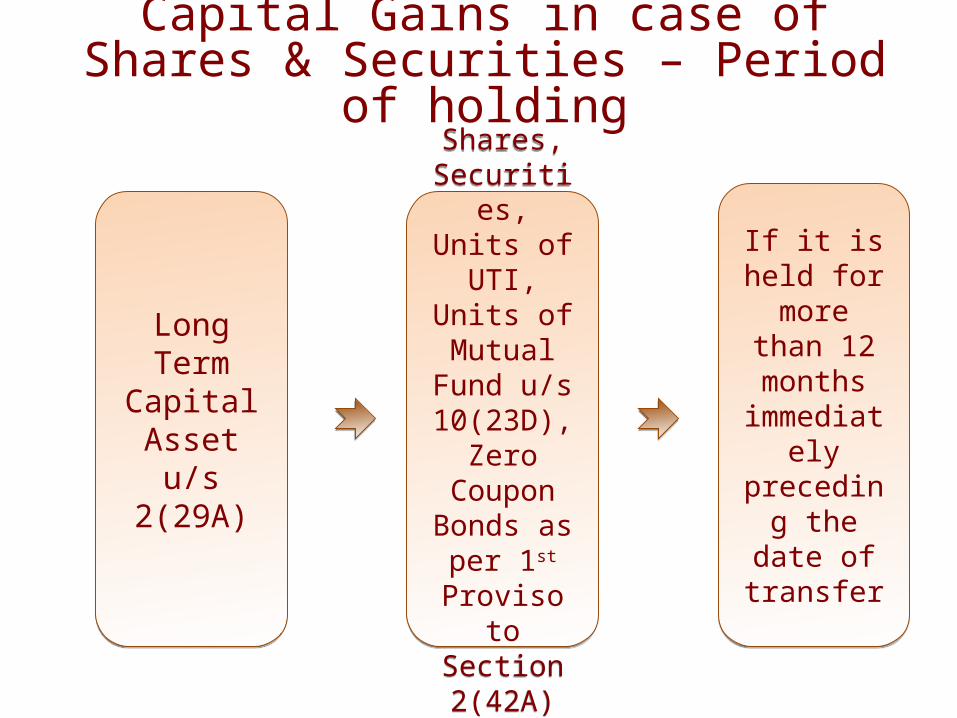

Types of Capital Assets – Contd..

22

Section 2(29A)Section 2(29A)

Exception – Proviso 1 to Sec. 2(42A)

Exception – Proviso 1 to Sec. 2(42A)

Long Term Capital Assets are those which are held by the assessee for more than 36 months, immediately preceding the date of its transfer.

Long Term Capital Assets are those which are held by the assessee for more than 36 months, immediately preceding the date of its transfer.

In case of a share or any other security listed in RSE in India or a unit of UTI, or a unit of Mutual Fund or a Zero Coupon Bonds if held for more than twelve months, the same shall be treated as LTCA.

In case of a share or any other security listed in RSE in India or a unit of UTI, or a unit of Mutual Fund or a Zero Coupon Bonds if held for more than twelve months, the same shall be treated as LTCA.

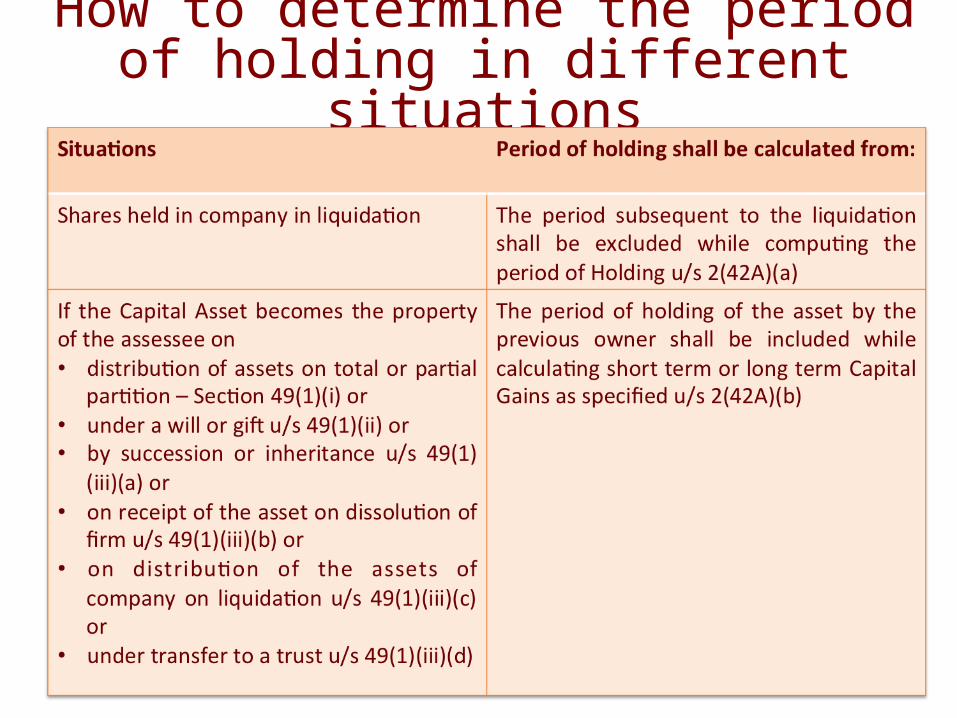

How to determine the period of holding in different situations

23

How to determine the period of holding in different situations

Capital Gains in case of Shares & Securities – Period of holding

Short Term Capital

Asset u/s 2(42A)

Short Term Capital

Asset u/s 2(42A)

Shares, Securities,

Units of UTI, Units of

Mutual Fund u/s 10(23D), Zero Coupon Bonds as per 1st Proviso to

Section 2(42A)

Shares, Securities,

Units of UTI, Units of

Mutual Fund u/s 10(23D), Zero Coupon Bonds as per 1st Proviso to

Section 2(42A)

If it is held for not more

than 12 months

immediately preceding the date of

transfer

If it is held for not more

than 12 months

immediately preceding the date of

transfer

Tax rate at 15% u/s

111A, provided Security

Transaction Tax is

charged u/s 111A(1)(b)

Tax rate at 15% u/s

111A, provided Security

Transaction Tax is

charged u/s 111A(1)(b)

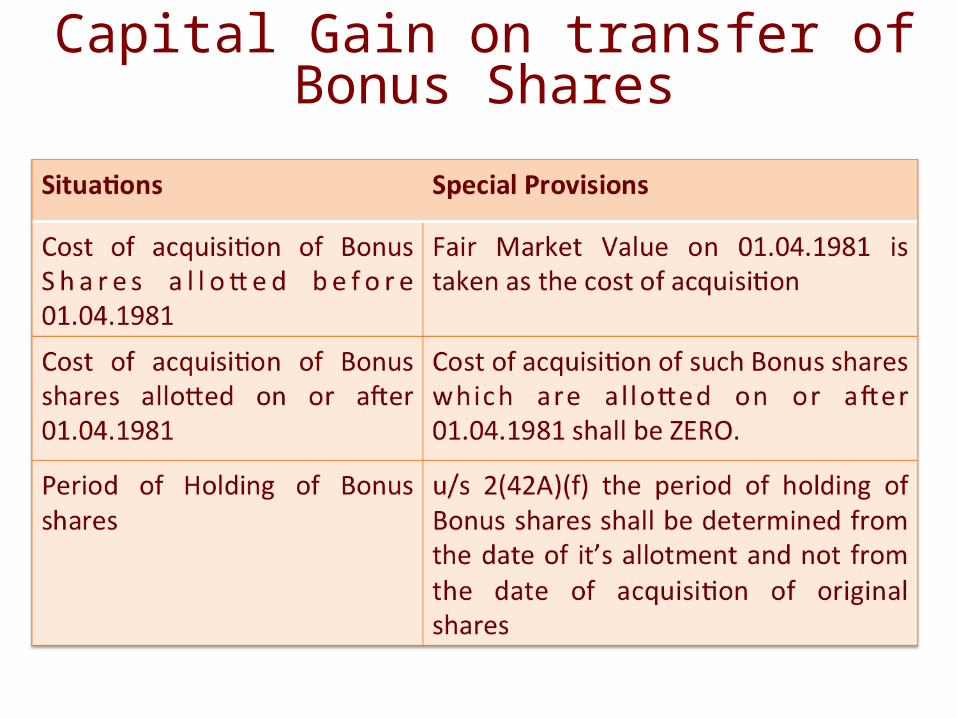

Capital Gain on transfer of Bonus Shares

Capital Gains in case of Shares & Securities – Period of holding

Long Term Capital

Asset u/s 2(29A)

Long Term Capital

Asset u/s 2(29A)

Shares, Securities,

Units of UTI, Units of

Mutual Fund u/s 10(23D), Zero Coupon Bonds as per 1st Proviso to

Section 2(42A)

Shares, Securities,

Units of UTI, Units of

Mutual Fund u/s 10(23D), Zero Coupon Bonds as per 1st Proviso to

Section 2(42A)

If it is held for more than 12 months

immediately preceding the date of

transfer

If it is held for more than 12 months

immediately preceding the date of

transfer

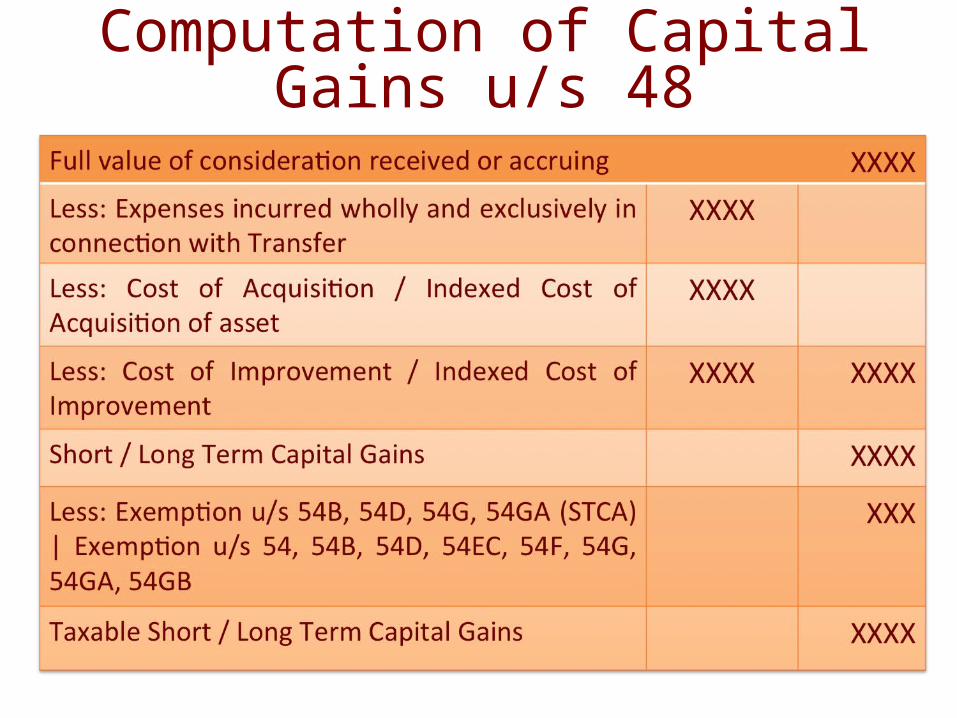

Computation of Capital Gains u/s 48

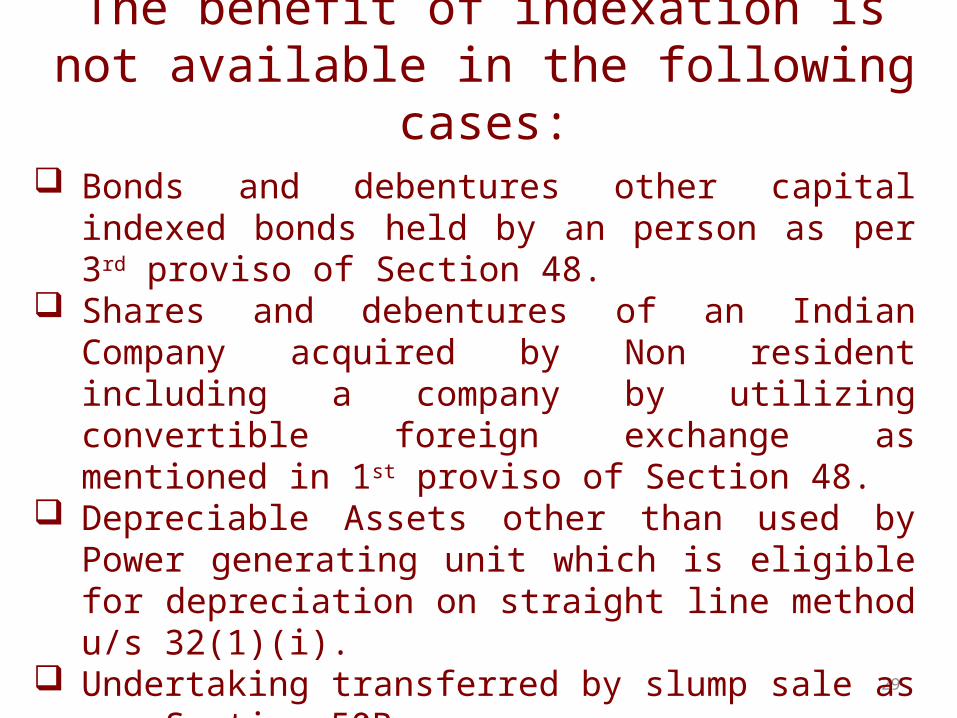

The benefit of indexation is not available in the following cases:

29

Bonds and debentures other capital indexed bonds held by an person as per 3rd proviso of Section 48.

Shares and debentures of an Indian Company acquired by Non resident including a company by utilizing convertible foreign exchange as mentioned in 1st proviso of Section 48.

Depreciable Assets other than used by Power generating unit which is eligible for depreciation on straight line method u/s 32(1)(i).

Undertaking transferred by slump sale as per Section 50B. Units purchased in Foreign currency u/s 115AB. GDR purchased in Foreign currency u/s 115ACA. Securities as per Section 115AD.

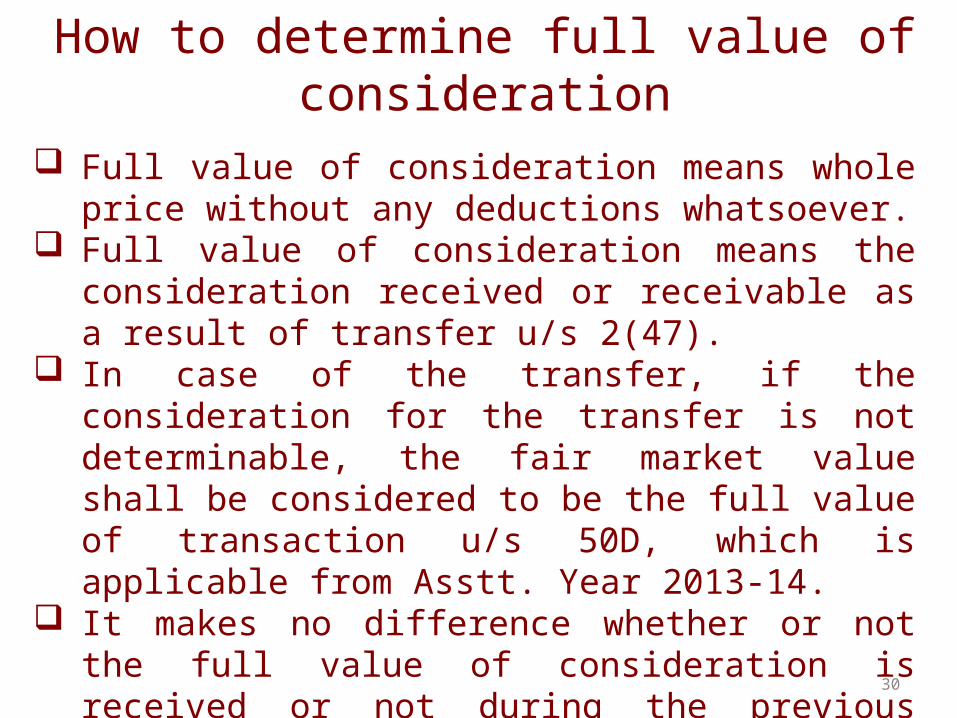

How to determine full value of consideration

30

Full value of consideration means whole price without any deductions whatsoever.

Full value of consideration means the consideration received or receivable as a result of transfer u/s 2(47).

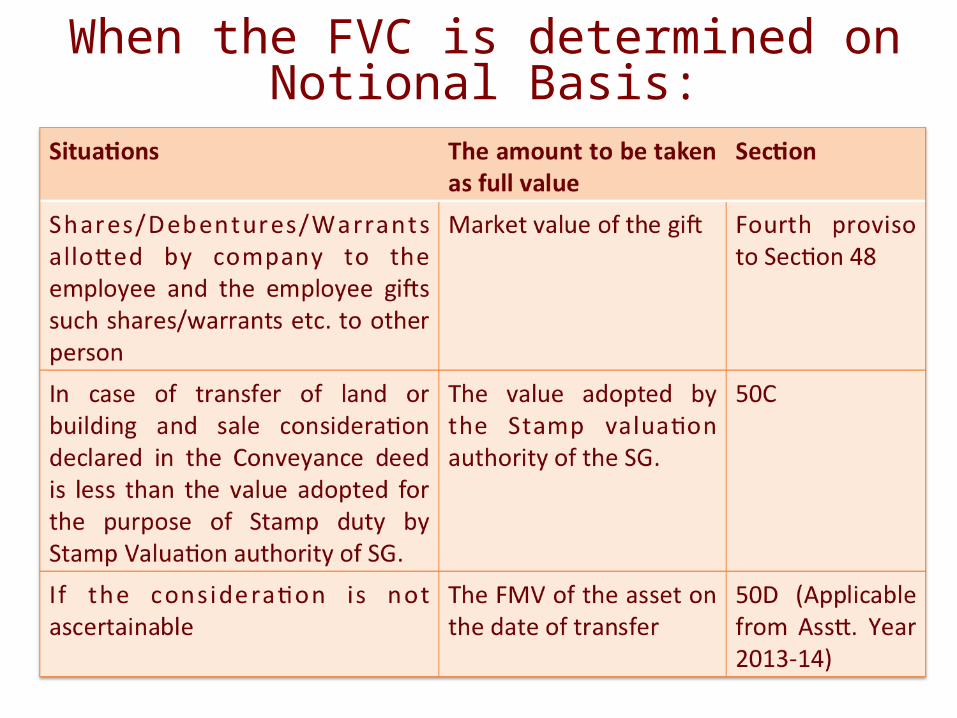

In case of the transfer, if the consideration for the transfer is not determinable, the fair market value shall be considered to be the full value of transaction u/s 50D, which is applicable from Asstt. Year 2013-14.

It makes no difference whether or not the full value of consideration is received or not during the previous year.

Even if the consideration is received in installment in the other previous year, still the Capital Gains shall be chargeable to tax u/s 45 in the year of transfer.

How to determine full value of consideration

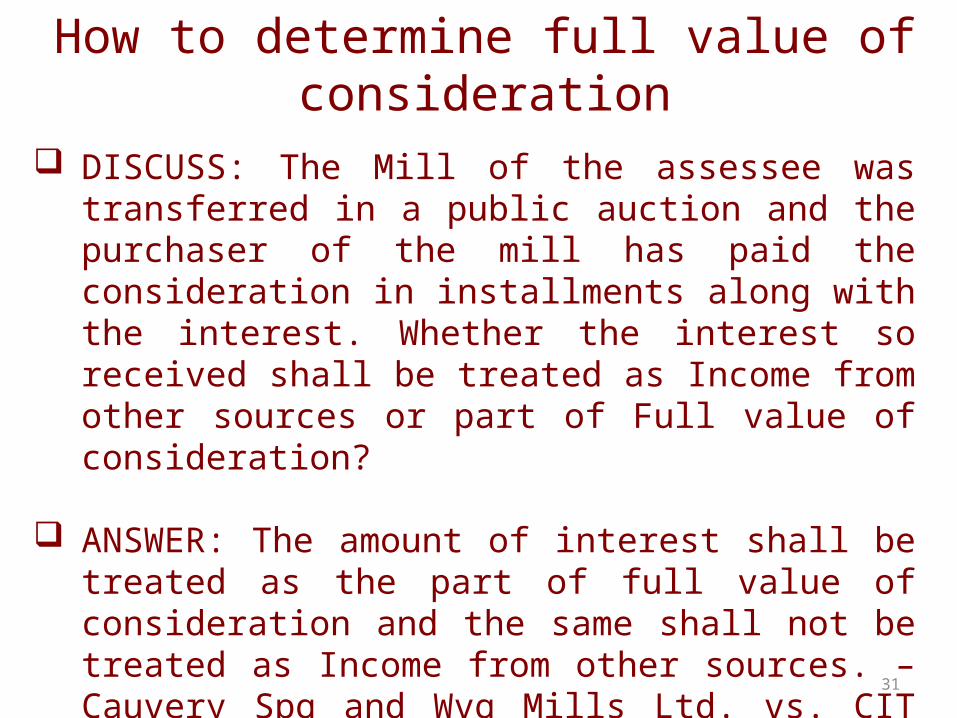

31

DISCUSS: The Mill of the assessee was transferred in a public auction and the purchaser of the mill has paid the consideration in installments along with the interest. Whether the interest so received shall be treated as Income from other sources or part of Full value of consideration?

ANSWER: The amount of interest shall be treated as the part of full value of consideration and the same shall not be treated as Income from other sources. – Cauvery Spg and Wvg Mills Ltd. vs. CIT (2011) 200 Taxman 22 (Mad.)

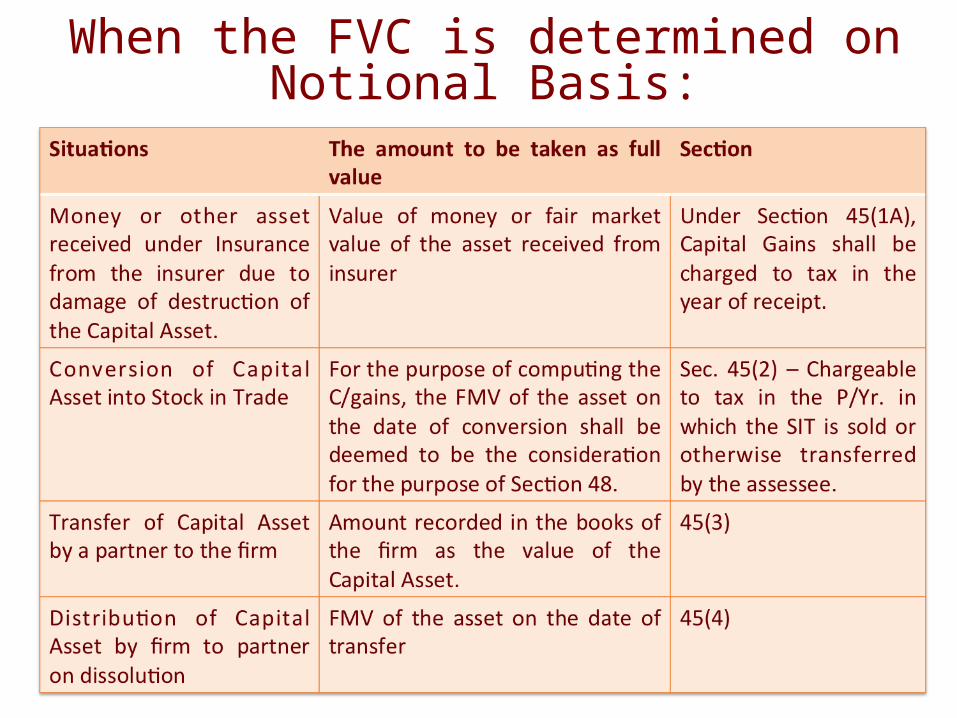

When the FVC is determined on Notional Basis:

When the FVC is determined on Notional Basis:

COST OF ACQUISITION

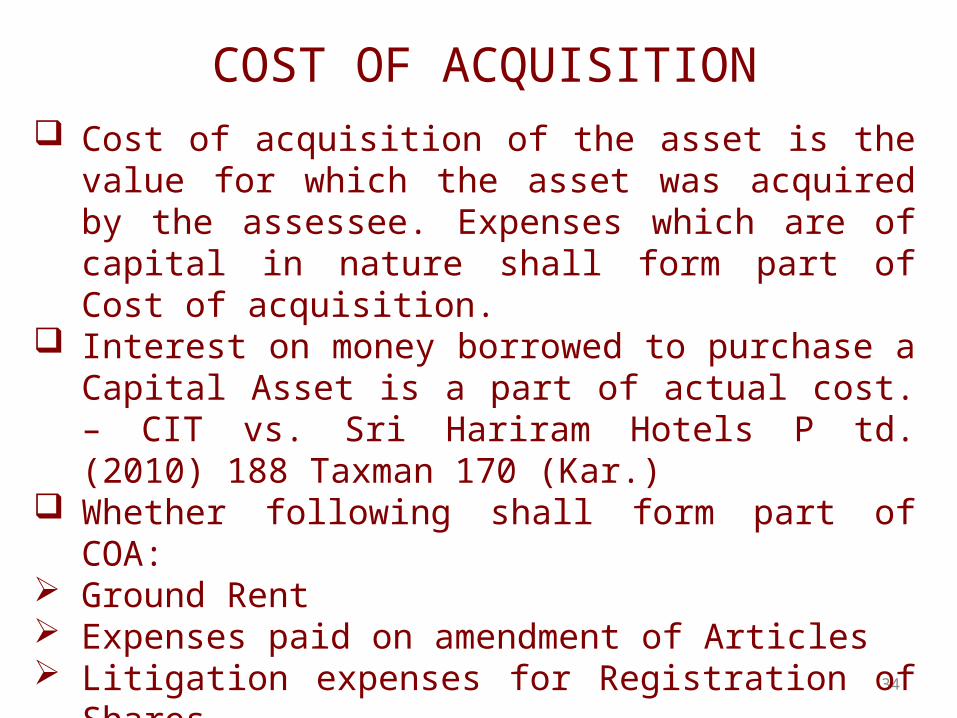

34

Cost of acquisition of the asset is the value for which the asset was acquired by the assessee. Expenses which are of capital in nature shall form part of Cost of acquisition.

Interest on money borrowed to purchase a Capital Asset is a part of actual cost. – CIT vs. Sri Hariram Hotels P td. (2010) 188 Taxman 170 (Kar.)

Whether following shall form part of COA: Ground Rent Expenses paid on amendment of Articles Litigation expenses for Registration of Shares Mortgage Conversion of Agr. Land into Non Agr. Land Advocate fees and brokerage

What is expenditure on Transfer

35

Expenditure incurred wholly and exclusively in connection with the transfer of Capital Asset is deductible from the FVC. – Sita Nanda vs. CIT (2001) 119 Taxman 227 (Delhi)

Expenditure incurred wholly and exclusively in connection with the transfer as specified u/s 48(i) has wider connation than expenses “for the transfer” – Gopeenath Paul & Sons vs. CIT (2005) 147 Taxman 629 (Cal)

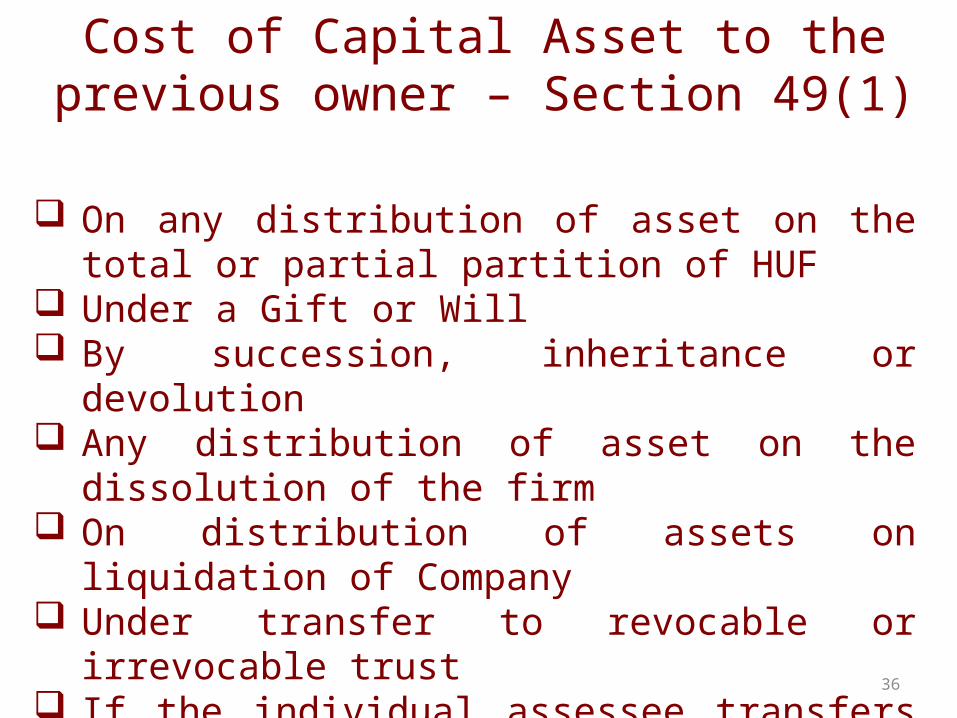

Cost of Capital Asset to the previous owner – Section 49(1)

36

On any distribution of asset on the total or partial partition of HUF

Under a Gift or Will By succession, inheritance or devolution Any distribution of asset on the dissolution of the firm On distribution of assets on liquidation of Company Under transfer to revocable or irrevocable trust If the individual assessee transfers his separate

property after 31st December 1969 u/s 64(2)

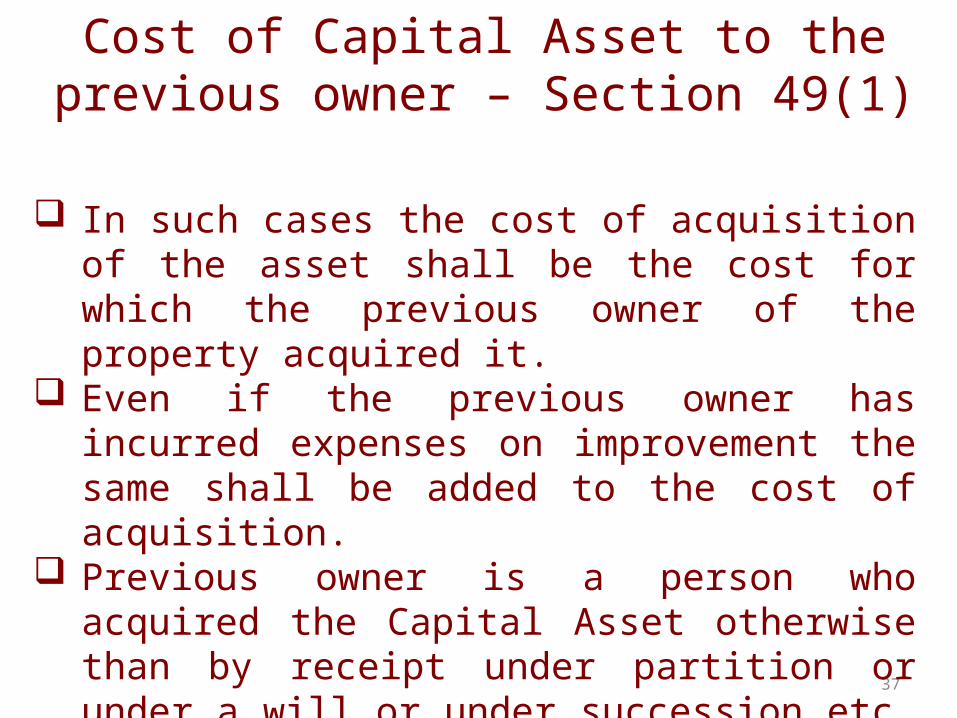

Cost of Capital Asset to the previous owner – Section 49(1)

37

In such cases the cost of acquisition of the asset shall be the cost for which the previous owner of the property acquired it.

Even if the previous owner has incurred expenses on improvement the same shall be added to the cost of acquisition.

Previous owner is a person who acquired the Capital Asset otherwise than by receipt under partition or under a will or under succession etc. Thus previous owner means the person who pays for the assets.

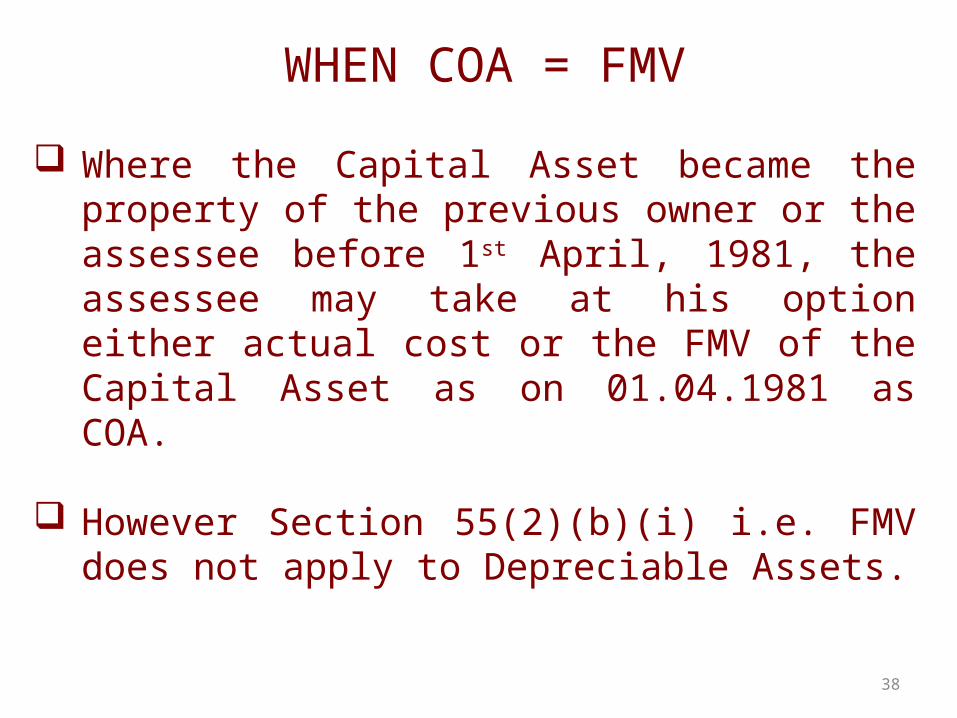

WHEN COA = FMV

38

Where the Capital Asset became the property of the previous owner or the assessee before 1st April, 1981, the assessee may take at his option either actual cost or the FMV of the Capital Asset as on 01.04.1981 as COA.

However Section 55(2)(b)(i) i.e. FMV does not apply to Depreciable Assets.

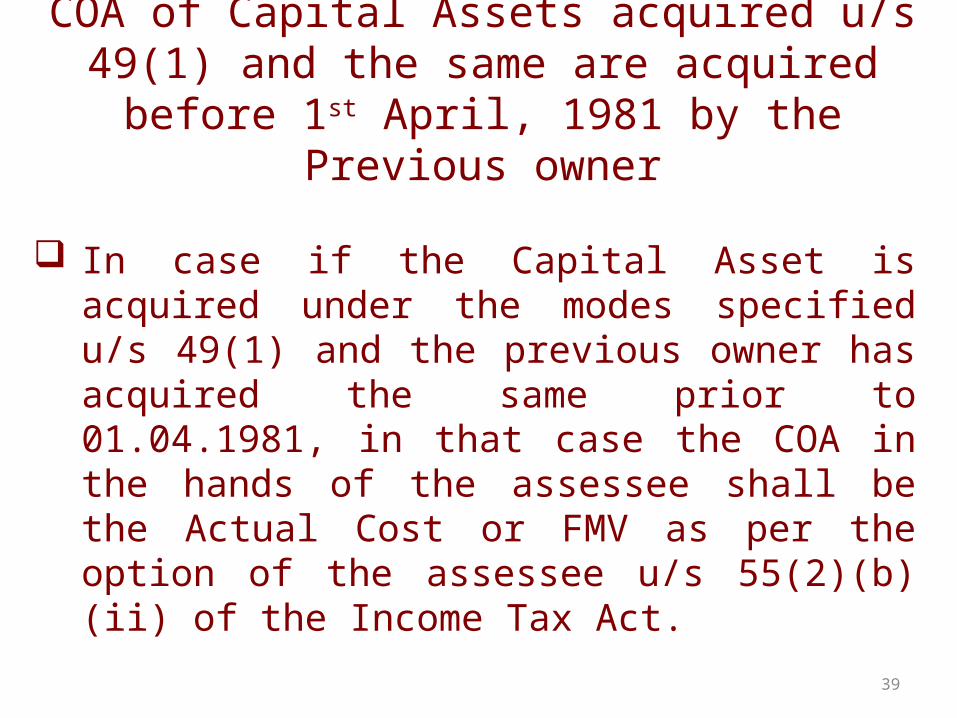

COA of Capital Assets acquired u/s 49(1) and the same are acquired before 1st April, 1981 by the

Previous owner

39

In case if the Capital Asset is acquired under the modes specified u/s 49(1) and the previous owner has acquired the same prior to 01.04.1981, in that case the COA in the hands of the assessee shall be the Actual Cost or FMV as per the option of the assessee u/s 55(2)(b)(ii) of the Income Tax Act.

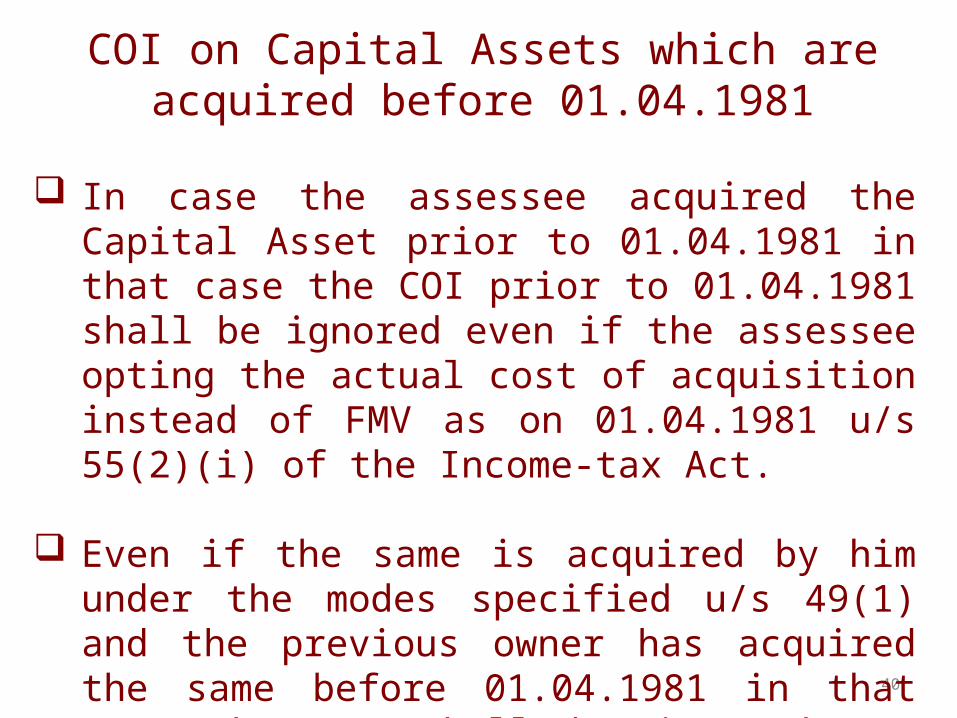

COI on Capital Assets which are acquired before 01.04.1981

40

In case the assessee acquired the Capital Asset prior to 01.04.1981 in that case the COI prior to 01.04.1981 shall be ignored even if the assessee opting the actual cost of acquisition instead of FMV as on 01.04.1981 u/s 55(2)(i) of the Income-tax Act.

Even if the same is acquired by him under the modes specified u/s 49(1) and the previous owner has acquired the same before 01.04.1981 in that case the COI shall be ignored u/s 55(2)(i) of the Income Tax Act.

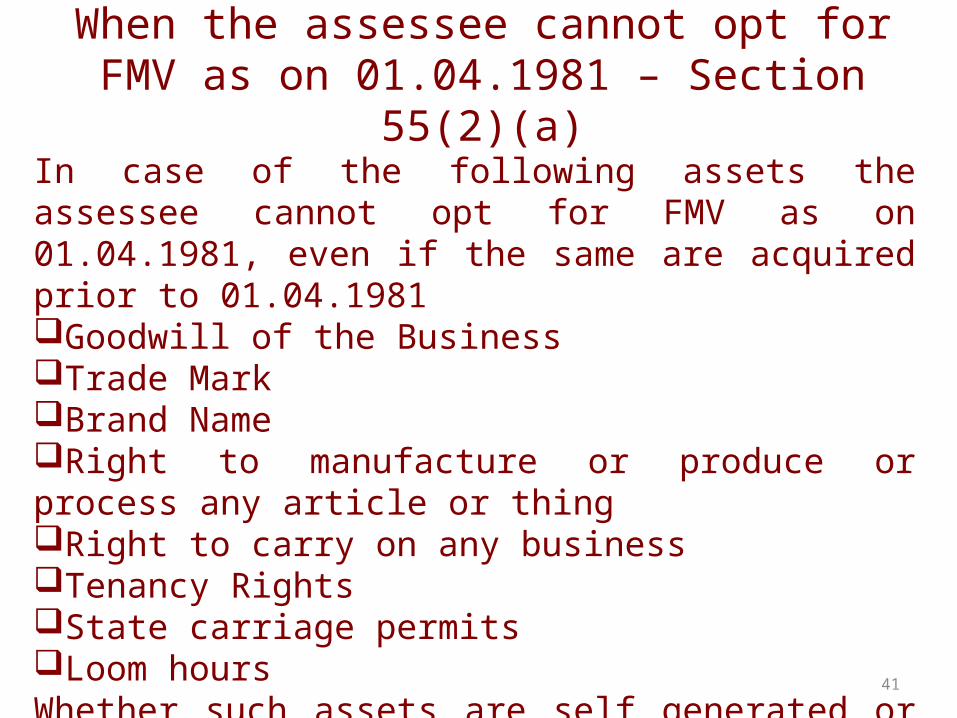

When the assessee cannot opt for FMV as on 01.04.1981 – Section 55(2)(a)

41

In case of the following assets the assessee cannot opt for FMV as on 01.04.1981, even if the same are acquired prior to 01.04.1981Goodwill of the BusinessTrade MarkBrand NameRight to manufacture or produce or process any article or thingRight to carry on any businessTenancy RightsState carriage permitsLoom hoursWhether such assets are self generated or not.

Conversion of Capital Asset into Stock in Trade – Section 2(47)(iv)

42

The assessee converts his Capital Asset into SITThe assessee converts his Capital Asset into SIT

Such conversion is treated as transfer under Section 2(47)(iv) of Income-Tax Act

Such conversion is treated as transfer under Section 2(47)(iv) of Income-Tax Act

However, Capital Gains shall be calculated only when such asset is sold by the business

However, Capital Gains shall be calculated only when such asset is sold by the business

Points to remember in case of Intangible Assets:

43

WHETHER BRAND NAME IS GOODWILL: It has been decided in the case of Vyasali Chemotherapeutics Pvt. Ltd. vs. CIT (2004) 134 Taxman 445 (Ker) that brand is GOODWILL.

In case the intangible asset is acquired without making actual payment i.e. – Intangible asset acquired on distribution of the same under partition of HUF u/s 49(1) or under a will /gift u/s 49(ii) or by succession or inheritance or devolution etc., in such cases the COA shall be NIL u/s 55(2)(a)(i) of the Income Tax Act.

Points to remember in case of Intangible Assets:

44

In case the Intangible Asset is acquired by making actual payment to the previous owner in that case u/s 55(2)(a)(i), the actual COA shall be the amount paid to the previous owner.

COI in certain Intangible Assets specified u/s 55(1)(b): If the Intangible asset in the form of goodwill or any right to manufacture, produce or process any article or thing, or any right to carry on any business is acquired in such cases the COI shall not be considered and the same shall be taken as Nil, by virtue of provision in Section 55(1)(b)

Capital Gains on Insurance Claims on damage or destruction of Capital Asset – Section 45(1A)

45

Where any person receives at any time during the previous year any money or other asset under an insurance from the Insurer on account of damage or destruction of any Capital Asset on account of:

Flood, typhoon, hurricane, cyclone, earthquake, or other convulsion of nature

Riots or civil disturbance Accidental fire or explosion Action by enemy or action taken in combating enemy.

In such case any profit arising from receipt of such money or other asset shall be chargeable to tax under the Capital Gains. It shall be deemed to be the Income of such person in the P/Yr. in which such money is received.

Capital Gains on Insurance Claims on damage or destruction of Capital Asset – Section 45(1A) –

Contd…

46

To calculate Capital Gains u/s 48, the value of money so received or the asset received from the Insurance Company shall be treated as FVC.

Exceptions to Section 45(1A): Not attracted if the assets have been destroyed but no compensation is received from Insurance Company. In such a case the cost of Capital Asset destroyed shall be a capital loss without any tax treatment thereto.

Capital gains u/s 45(1A) shall not be taxable in the year in which the asset is destroyed but the same shall be taxable in the year in which the insurance amount is received.

Capital Gains on conversion of Capital Asset into SIT – Section 45(2)

47

Transfer includes conversion of Capital Asset into SIT u/s 2(47)(iv) of the Income Tax Act.

U/s 45(2), Capital Gains arising from the conversion of Capital Asset into SIT shall be charged to tax in the P/Yr. in which the SIT is sold or otherwise transferred by the assessee.

For the purposes of computing Capital Gains, the FMV of the assets on the date of conversion shall be deemed to be the sale consideration for the purpose of Section 48.

Capital Gains shall be computed as per the provisions of law applicable in the previous year in which the stock is sold.

Example: Mr. A acquired a land on 01.08.1990, for Rs. 2,00,000. He converts this land into SIT for dealing in plots on 01.04.2000. The FMV as on the date of conversion of the plot into SIT was at Rs. 7,00,000. The SIT is sold on 01.03.2013 for Rs. 22,00,000. Compute C/Gains.

Transfer of Securities by depositories – Section 45(2A)

48

Where any person has had at any time during the previous year any beneficial interest in any securities, then, any profit or gains arising from transfer made by the depository or participants of such beneficial interest in respect of securities shall be chargeable to tax as income of the beneficial owner in the previous year in which such transfer took place and shall not be regarded as income of the depository who is deemed to be registered owner of securities by virtue of Section 10(1) of the Depositories Act, 1996 and for the purpose of Section 48 and for determining Period of Holding – FIFO Method shall be adopted (Circular No. 768, Dt. 24.06.1998)

Where any person has had at any time during the previous year any beneficial interest in any securities, then, any profit or gains arising from transfer made by the depository or participants of such beneficial interest in respect of securities shall be chargeable to tax as income of the beneficial owner in the previous year in which such transfer took place and shall not be regarded as income of the depository who is deemed to be registered owner of securities by virtue of Section 10(1) of the Depositories Act, 1996 and for the purpose of Section 48 and for determining Period of Holding – FIFO Method shall be adopted (Circular No. 768, Dt. 24.06.1998)

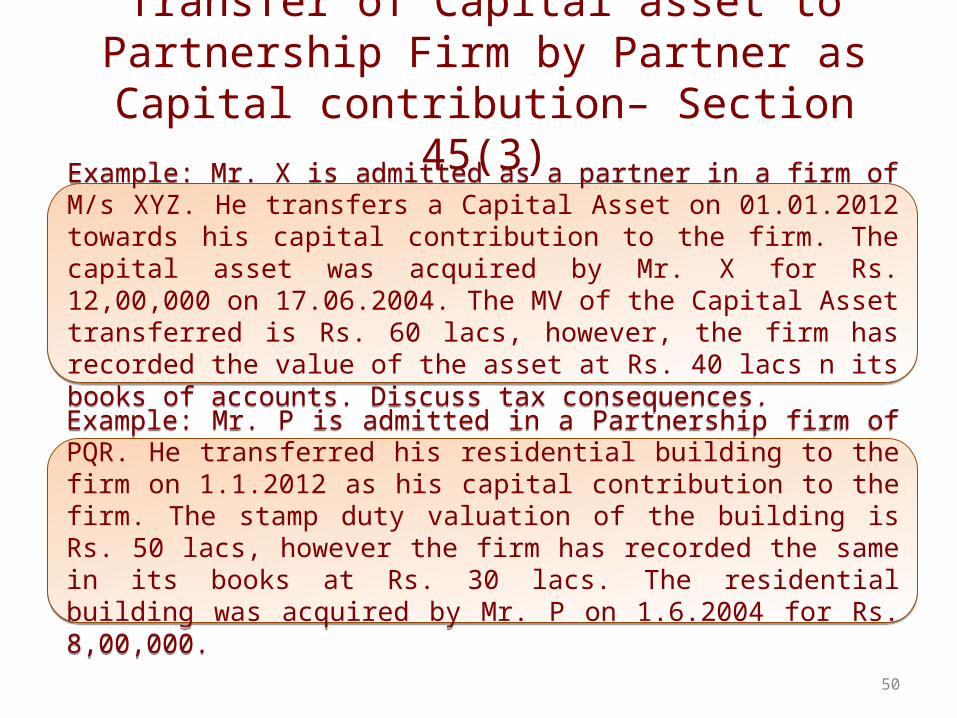

Transfer of Capital asset to Partnership Firm by Partner as Capital contribution– Section 45(3)

49

The profits and gains arising from the transfer of a Capital Asset by the assessee to the firm/AOP/BOI by way of capital contribution or otherwise shall be taxable in the P/yr. in which such transfer takes place.

The profits and gains arising from the transfer of a Capital Asset by the assessee to the firm/AOP/BOI by way of capital contribution or otherwise shall be taxable in the P/yr. in which such transfer takes place.

The amount recorded in the books of accounts of the firm as the value of Capital Asset shall be deemed to be the sales consideration for the purposes of Capital Gains.

The amount recorded in the books of accounts of the firm as the value of Capital Asset shall be deemed to be the sales consideration for the purposes of Capital Gains.

Transfer of Capital asset to Partnership Firm by Partner as Capital contribution– Section 45(3)

50

Example: Mr. X is admitted as a partner in a firm of M/s XYZ. He transfers a Capital Asset on 01.01.2012 towards his capital contribution to the firm. The capital asset was acquired by Mr. X for Rs. 12,00,000 on 17.06.2004. The MV of the Capital Asset transferred is Rs. 60 lacs, however, the firm has recorded the value of the asset at Rs. 40 lacs n its books of accounts. Discuss tax consequences.

Example: Mr. X is admitted as a partner in a firm of M/s XYZ. He transfers a Capital Asset on 01.01.2012 towards his capital contribution to the firm. The capital asset was acquired by Mr. X for Rs. 12,00,000 on 17.06.2004. The MV of the Capital Asset transferred is Rs. 60 lacs, however, the firm has recorded the value of the asset at Rs. 40 lacs n its books of accounts. Discuss tax consequences.

Example: Mr. P is admitted in a Partnership firm of PQR. He transferred his residential building to the firm on 1.1.2012 as his capital contribution to the firm. The stamp duty valuation of the building is Rs. 50 lacs, however the firm has recorded the same in its books at Rs. 30 lacs. The residential building was acquired by Mr. P on 1.6.2004 for Rs. 8,00,000.

Example: Mr. P is admitted in a Partnership firm of PQR. He transferred his residential building to the firm on 1.1.2012 as his capital contribution to the firm. The stamp duty valuation of the building is Rs. 50 lacs, however the firm has recorded the same in its books at Rs. 30 lacs. The residential building was acquired by Mr. P on 1.6.2004 for Rs. 8,00,000.

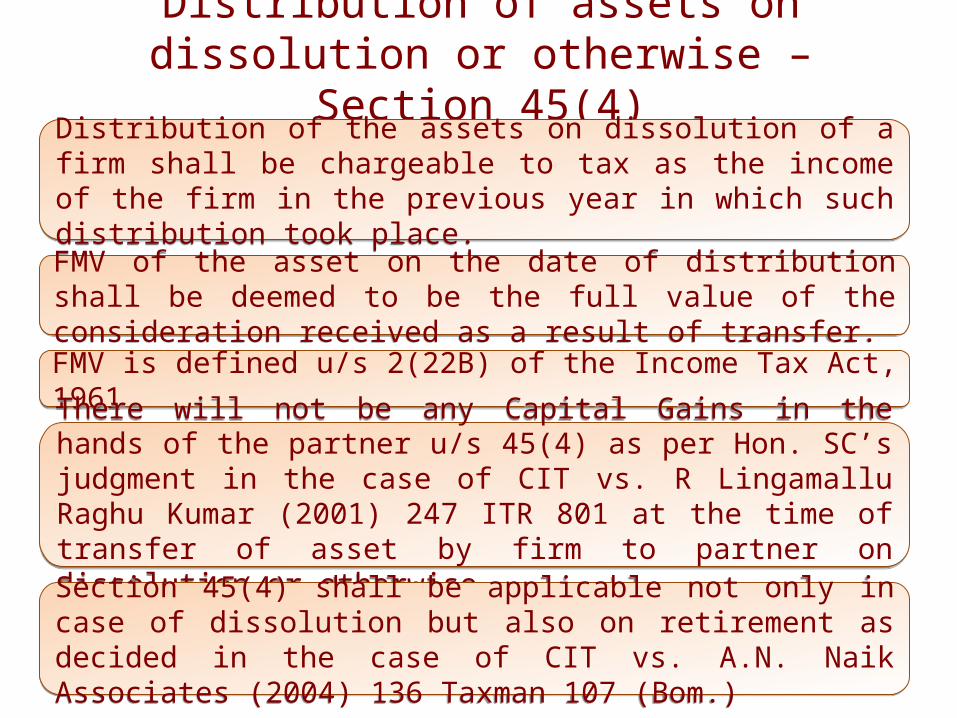

Distribution of assets on dissolution or otherwise – Section 45(4)

51

Distribution of the assets on dissolution of a firm shall be chargeable to tax as the income of the firm in the previous year in which such distribution took place.

Distribution of the assets on dissolution of a firm shall be chargeable to tax as the income of the firm in the previous year in which such distribution took place.

FMV is defined u/s 2(22B) of the Income Tax Act, 1961FMV is defined u/s 2(22B) of the Income Tax Act, 1961

FMV of the asset on the date of distribution shall be deemed to be the full value of the consideration received as a result of transfer.FMV of the asset on the date of distribution shall be deemed to be the full value of the consideration received as a result of transfer.

There will not be any Capital Gains in the hands of the partner u/s 45(4) as per Hon. SC’s judgment in the case of CIT vs. R Lingamallu Raghu Kumar (2001) 247 ITR 801 at the time of transfer of asset by firm to partner on dissolution or otherwise.

There will not be any Capital Gains in the hands of the partner u/s 45(4) as per Hon. SC’s judgment in the case of CIT vs. R Lingamallu Raghu Kumar (2001) 247 ITR 801 at the time of transfer of asset by firm to partner on dissolution or otherwise.

Section 45(4) shall be applicable not only in case of dissolution but also on retirement as decided in the case of CIT vs. A.N. Naik Associates (2004) 136 Taxman 107 (Bom.)

Section 45(4) shall be applicable not only in case of dissolution but also on retirement as decided in the case of CIT vs. A.N. Naik Associates (2004) 136 Taxman 107 (Bom.)

Distribution of assets on dissolution or otherwise – Section 45(4) – Tax effects in the hands of Partner

52

The difference between the FMV and the credit balance standing in the books shall be treated as “Income from other sources u/s 56(2)(vii)” in the hands of the partner.

The difference between the FMV and the credit balance standing in the books shall be treated as “Income from other sources u/s 56(2)(vii)” in the hands of the partner.

Example: A partnership firm ABC exists, which consists the partners A,B & C. Mr. C retires from the partnership firm from 02.06.2012 and on that day the balance standing credited to his capital account is Rs. 15,00,000. The firm settles the accounts of the retiring partner by transferring Jewellery which was acquired by the firm on 13.12.1991 at Rs. 3,00,000. The FMV of jewellery as on 02.06.2012 is Rs. 45,00,000. Mr. C sells the said jewellery at Rs. 48,00,000 on 15.06.2012. Discuss the tax consequences.

Example: A partnership firm ABC exists, which consists the partners A,B & C. Mr. C retires from the partnership firm from 02.06.2012 and on that day the balance standing credited to his capital account is Rs. 15,00,000. The firm settles the accounts of the retiring partner by transferring Jewellery which was acquired by the firm on 13.12.1991 at Rs. 3,00,000. The FMV of jewellery as on 02.06.2012 is Rs. 45,00,000. Mr. C sells the said jewellery at Rs. 48,00,000 on 15.06.2012. Discuss the tax consequences.

If the partner sells the Capital Asset which he received from the firm the same shall be treated as Capital Gains in the hands of the partner.If the partner sells the Capital Asset which he received from the firm the same shall be treated as Capital Gains in the hands of the partner.

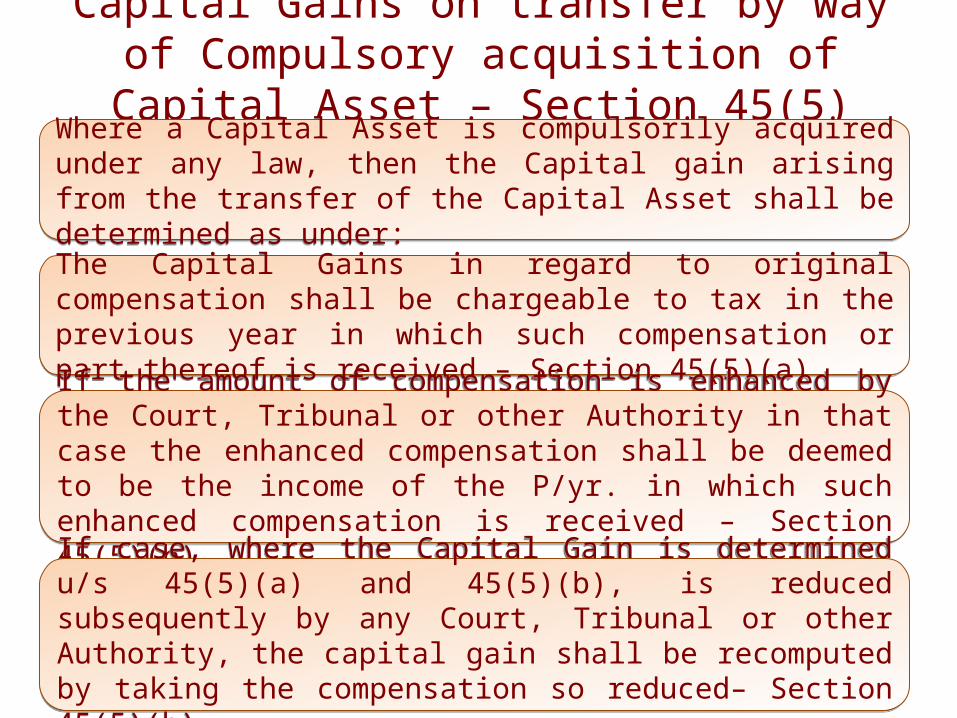

Capital Gains on transfer by way of Compulsory acquisition of Capital Asset – Section 45(5)

53

Where a Capital Asset is compulsorily acquired under any law, then the Capital gain arising from the transfer of the Capital Asset shall be determined as under:

Where a Capital Asset is compulsorily acquired under any law, then the Capital gain arising from the transfer of the Capital Asset shall be determined as under:

The Capital Gains in regard to original compensation shall be chargeable to tax in the previous year in which such compensation or part thereof is received – Section 45(5)(a)

The Capital Gains in regard to original compensation shall be chargeable to tax in the previous year in which such compensation or part thereof is received – Section 45(5)(a)

If the amount of compensation is enhanced by the Court, Tribunal or other Authority in that case the enhanced compensation shall be deemed to be the income of the P/yr. in which such enhanced compensation is received – Section 45(5)(b)

If the amount of compensation is enhanced by the Court, Tribunal or other Authority in that case the enhanced compensation shall be deemed to be the income of the P/yr. in which such enhanced compensation is received – Section 45(5)(b)

If case, where the Capital Gain is determined u/s 45(5)(a) and 45(5)(b), is reduced subsequently by any Court, Tribunal or other Authority, the capital gain shall be recomputed by taking the compensation so reduced– Section 45(5)(b)

If case, where the Capital Gain is determined u/s 45(5)(a) and 45(5)(b), is reduced subsequently by any Court, Tribunal or other Authority, the capital gain shall be recomputed by taking the compensation so reduced– Section 45(5)(b)

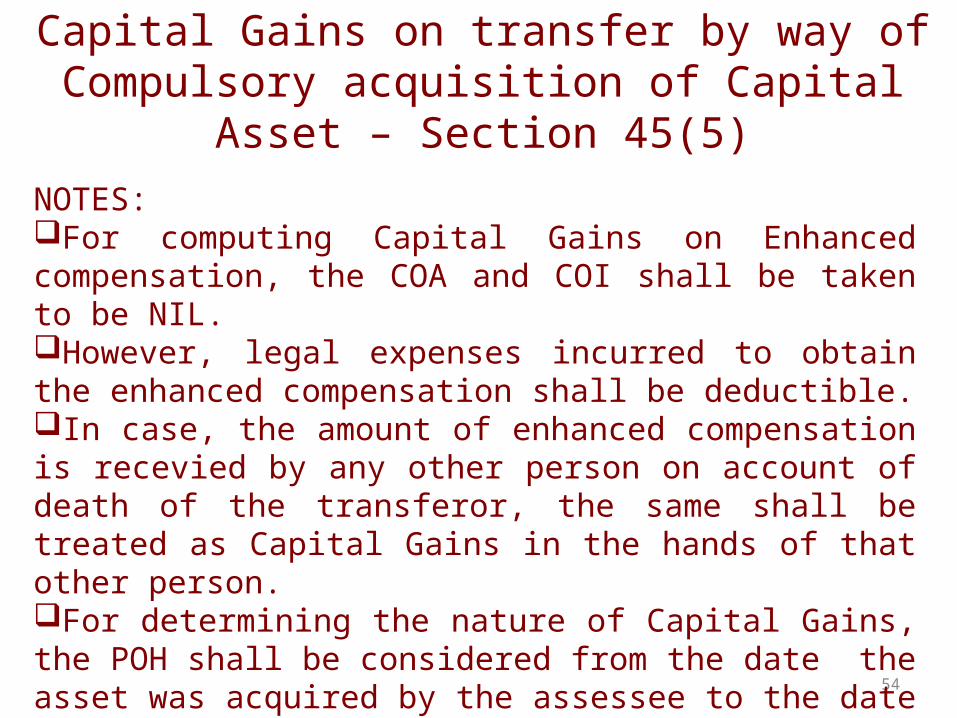

Capital Gains on transfer by way of Compulsory acquisition of Capital Asset – Section 45(5)

54

NOTES:For computing Capital Gains on Enhanced compensation, the COA and COI shall be taken to be NIL.However, legal expenses incurred to obtain the enhanced compensation shall be deductible.In case, the amount of enhanced compensation is recevied by any other person on account of death of the transferor, the same shall be treated as Capital Gains in the hands of that other person.For determining the nature of Capital Gains, the POH shall be considered from the date the asset was acquired by the assessee to the date the asset was compulsorily acquired under the Law.

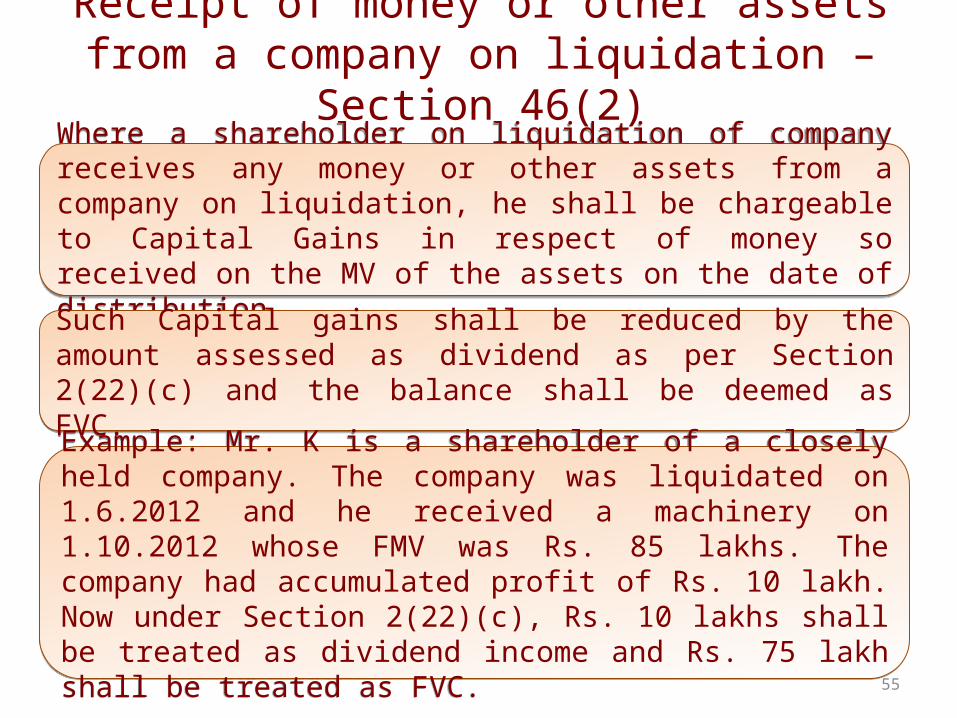

Receipt of money or other assets from a company on liquidation – Section 46(2)

55

Where a shareholder on liquidation of company receives any money or other assets from a company on liquidation, he shall be chargeable to Capital Gains in respect of money so received on the MV of the assets on the date of distribution.

Where a shareholder on liquidation of company receives any money or other assets from a company on liquidation, he shall be chargeable to Capital Gains in respect of money so received on the MV of the assets on the date of distribution.

Such Capital gains shall be reduced by the amount assessed as dividend as per Section 2(22)(c) and the balance shall be deemed as FVC.

Such Capital gains shall be reduced by the amount assessed as dividend as per Section 2(22)(c) and the balance shall be deemed as FVC.

Example: Mr. K is a shareholder of a closely held company. The company was liquidated on 1.6.2012 and he received a machinery on 1.10.2012 whose FMV was Rs. 85 lakhs. The company had accumulated profit of Rs. 10 lakh. Now under Section 2(22)(c), Rs. 10 lakhs shall be treated as dividend income and Rs. 75 lakh shall be treated as FVC.

Example: Mr. K is a shareholder of a closely held company. The company was liquidated on 1.6.2012 and he received a machinery on 1.10.2012 whose FMV was Rs. 85 lakhs. The company had accumulated profit of Rs. 10 lakh. Now under Section 2(22)(c), Rs. 10 lakhs shall be treated as dividend income and Rs. 75 lakh shall be treated as FVC.

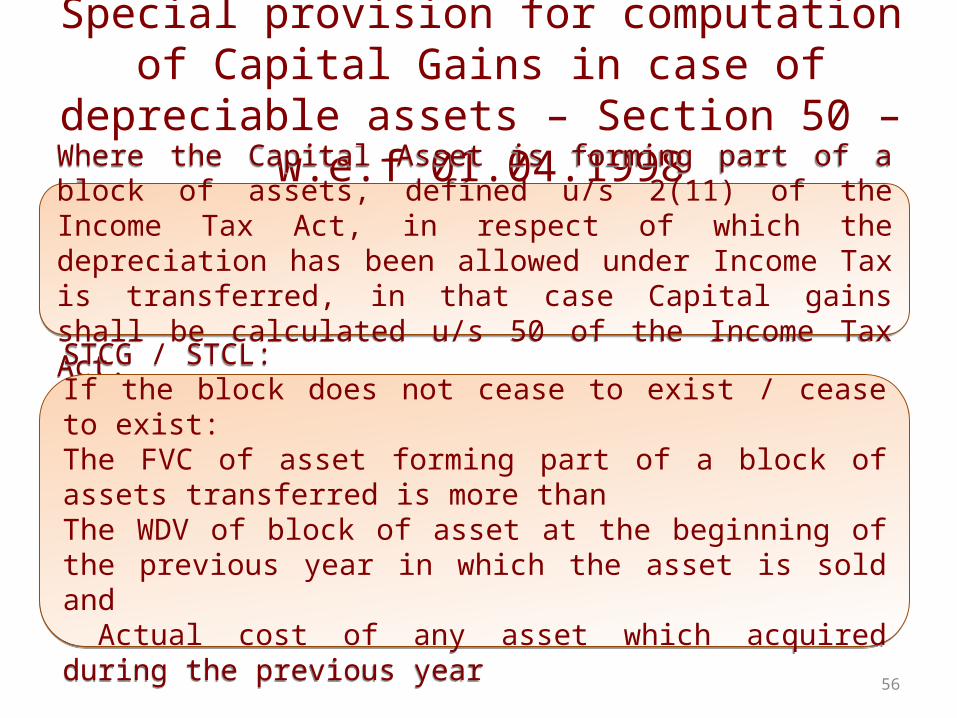

Special provision for computation of Capital Gains in case of depreciable assets – Section 50 – w.e.f

01.04.1998

56

Where the Capital Asset is forming part of a block of assets, defined u/s 2(11) of the Income Tax Act, in respect of which the depreciation has been allowed under Income Tax is transferred, in that case Capital gains shall be calculated u/s 50 of the Income Tax Act.

Where the Capital Asset is forming part of a block of assets, defined u/s 2(11) of the Income Tax Act, in respect of which the depreciation has been allowed under Income Tax is transferred, in that case Capital gains shall be calculated u/s 50 of the Income Tax Act.

STCG / STCL: If the block does not cease to exist / cease to exist: The FVC of asset forming part of a block of assets transferred is more than The WDV of block of asset at the beginning of the previous year in which the asset is sold and Actual cost of any asset which acquired during the previous year

STCG / STCL: If the block does not cease to exist / cease to exist: The FVC of asset forming part of a block of assets transferred is more than The WDV of block of asset at the beginning of the previous year in which the asset is sold and Actual cost of any asset which acquired during the previous year

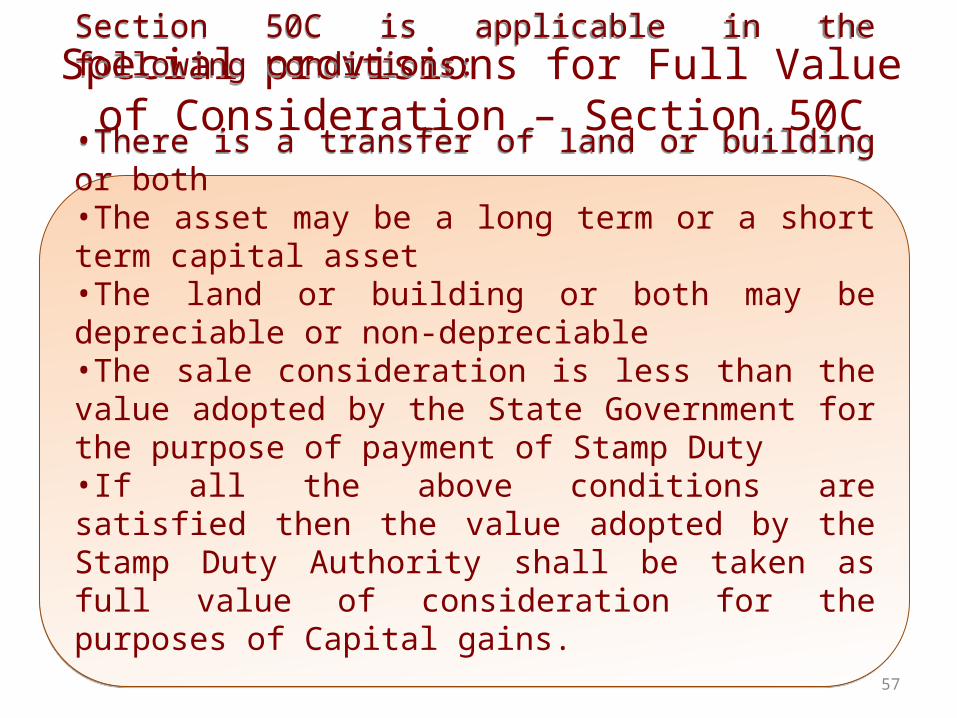

Special provisions for Full Value of Consideration – Section 50C

57

Section 50C is applicable in the following conditions:

•There is a transfer of land or building or both•The asset may be a long term or a short term capital asset•The land or building or both may be depreciable or non-depreciable•The sale consideration is less than the value adopted by the State Government for the purpose of payment of Stamp Duty•If all the above conditions are satisfied then the value adopted by the Stamp Duty Authority shall be taken as full value of consideration for the purposes of Capital gains.

Section 50C is applicable in the following conditions:

•There is a transfer of land or building or both•The asset may be a long term or a short term capital asset•The land or building or both may be depreciable or non-depreciable•The sale consideration is less than the value adopted by the State Government for the purpose of payment of Stamp Duty•If all the above conditions are satisfied then the value adopted by the Stamp Duty Authority shall be taken as full value of consideration for the purposes of Capital gains.

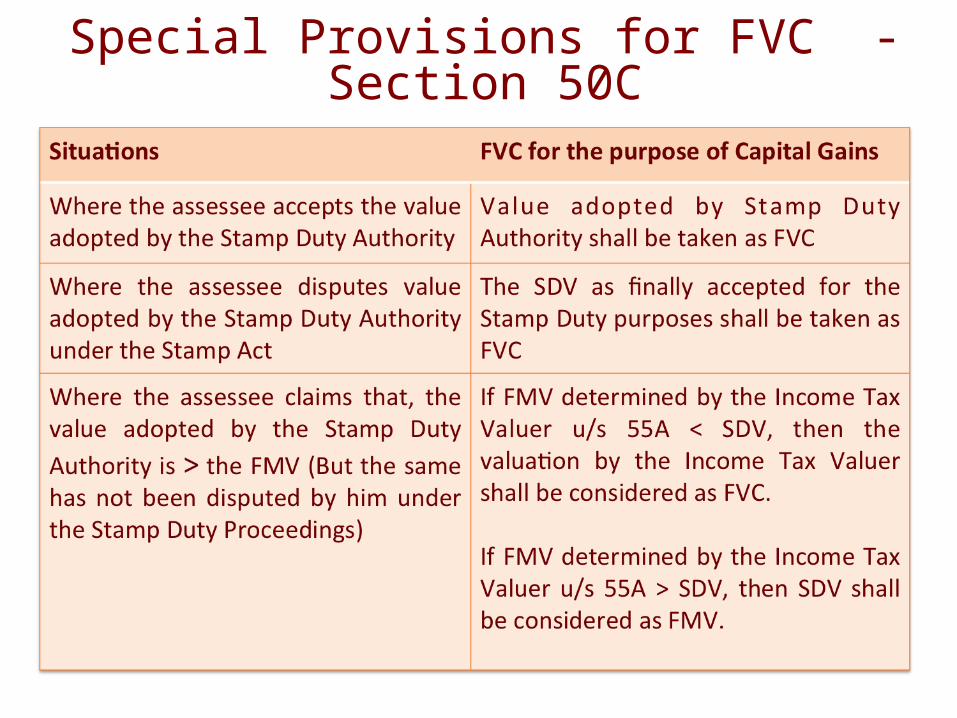

Special Provisions for FVC - Section 50C

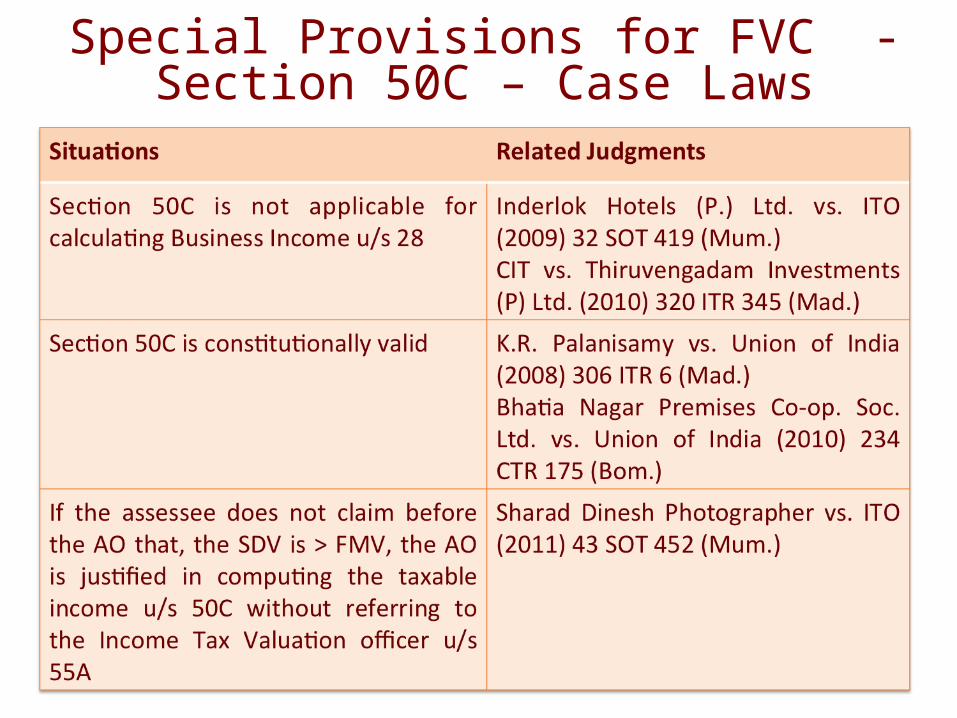

Special Provisions for FVC - Section 50C – Case Laws

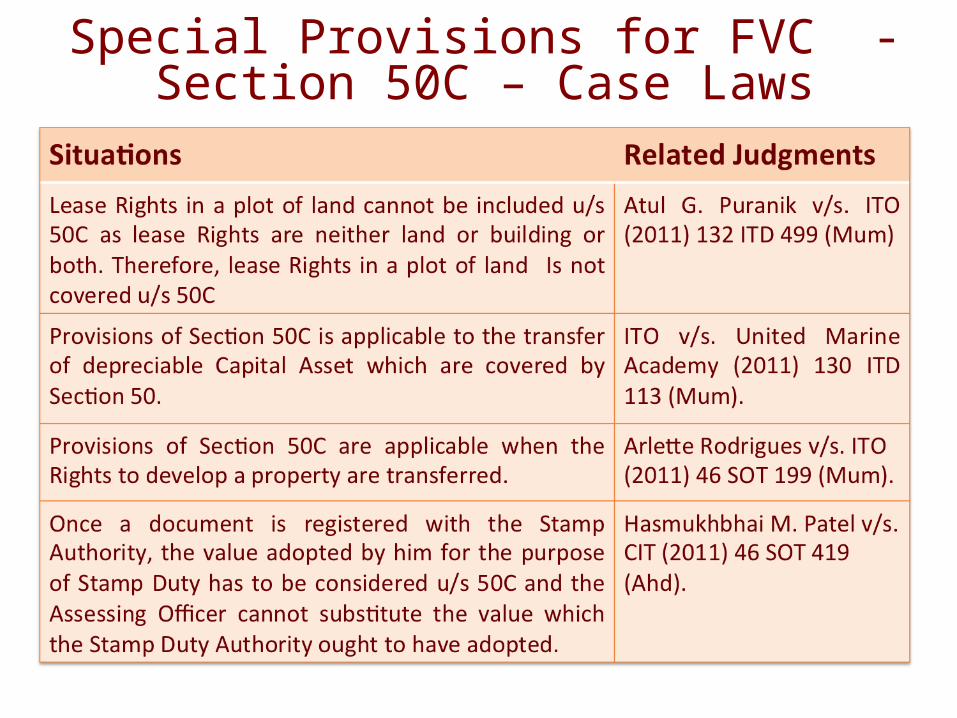

Special Provisions for FVC - Section 50C – Case Laws

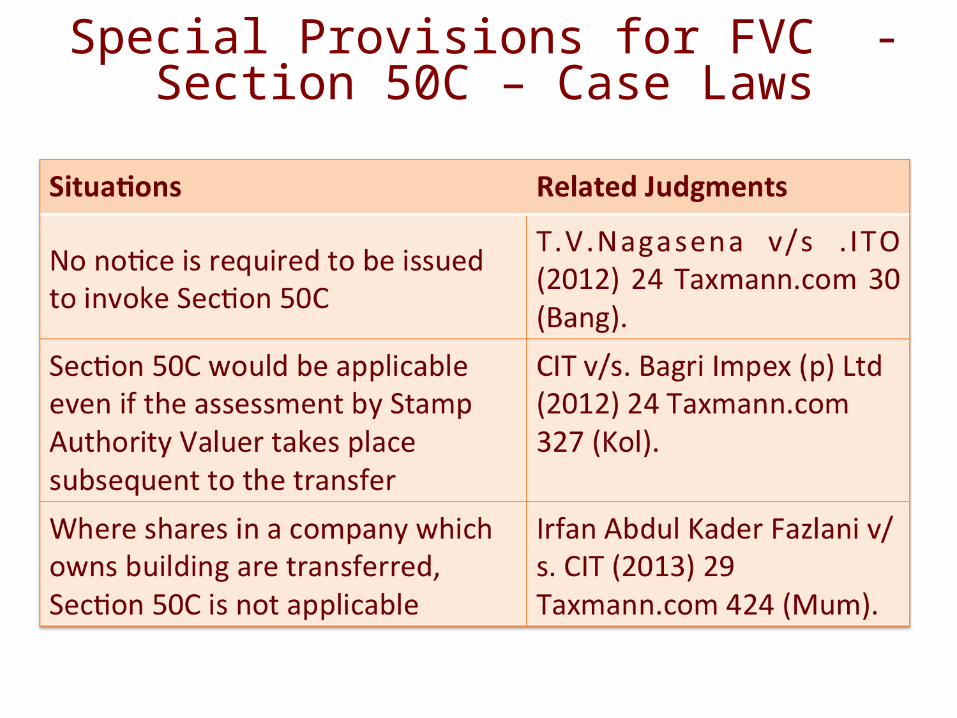

Special Provisions for FVC - Section 50C – Case Laws

Section 51 – Forfeiture of Advance Money

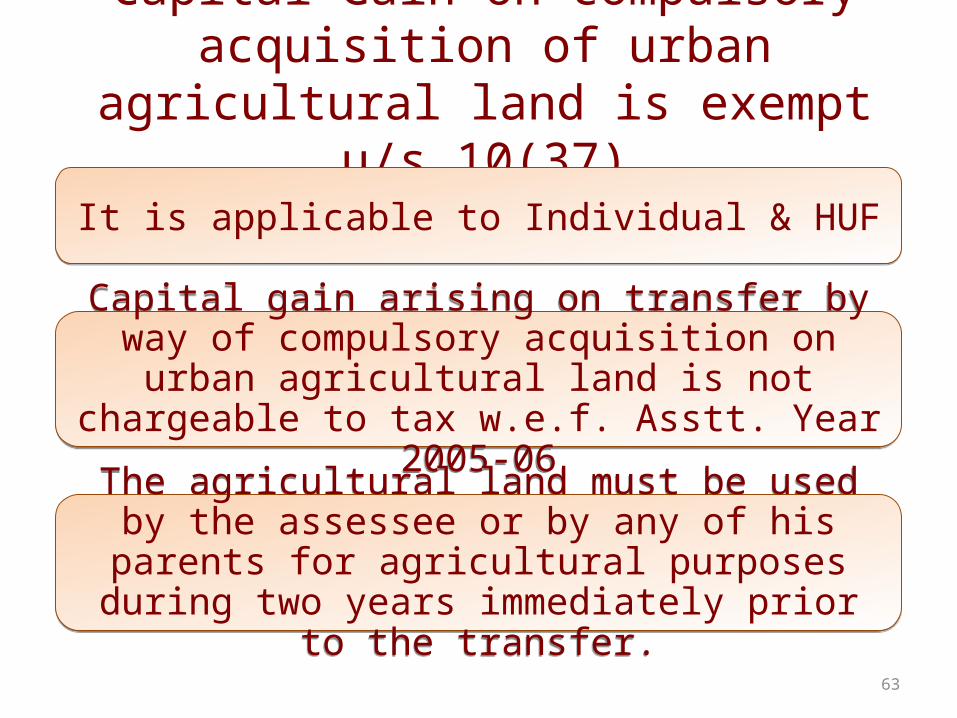

Capital Gain on compulsory acquisition of urban agricultural land is exempt u/s 10(37)

63

It is applicable to Individual & HUFIt is applicable to Individual & HUF

Capital gain arising on transfer by way of compulsory acquisition on urban agricultural land is not chargeable to tax w.e.f. Asstt. Year 2005-06

Capital gain arising on transfer by way of compulsory acquisition on urban agricultural land is not chargeable to tax w.e.f. Asstt. Year 2005-06

The agricultural land must be used by the assessee or by any of his parents for agricultural purposes during

two years immediately prior to the transfer.

The agricultural land must be used by the assessee or by any of his parents for agricultural purposes during

two years immediately prior to the transfer.

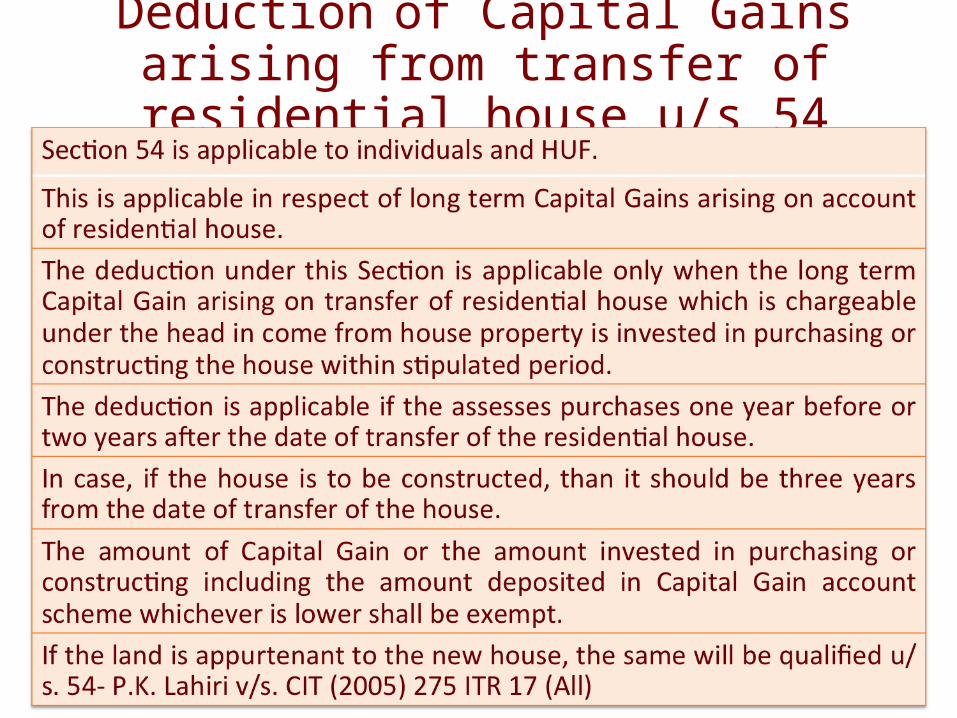

Deduction of Capital Gains arising from transfer of residential house u/s 54

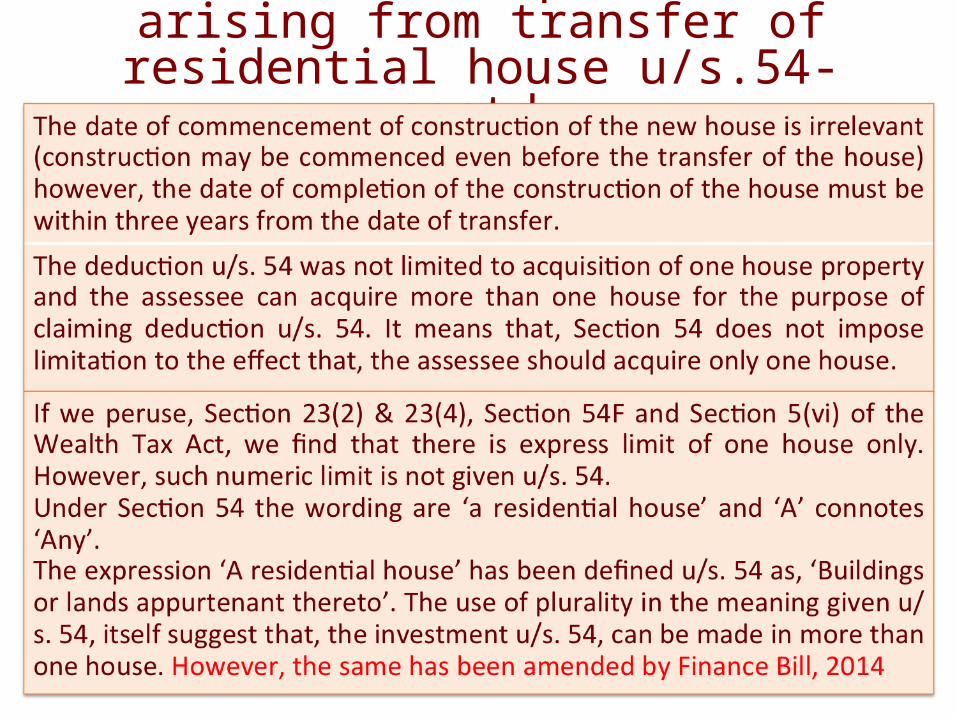

Deduction of Capital Gains arising from transfer of residential house u/s.54- contd…

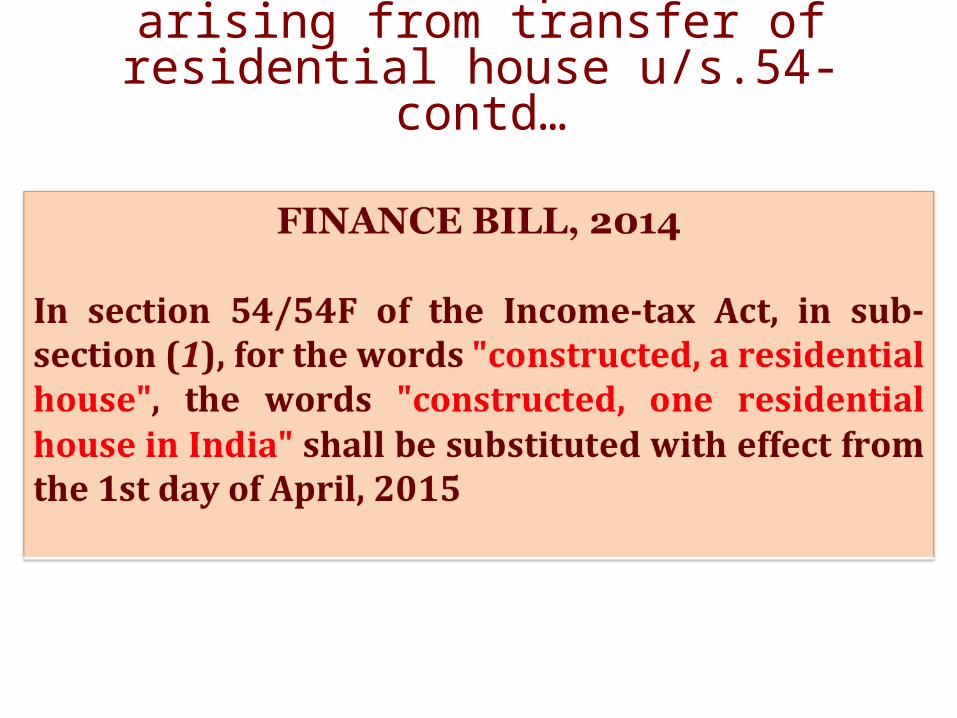

Deduction of Capital Gains arising from transfer of residential house u/s.54- contd…

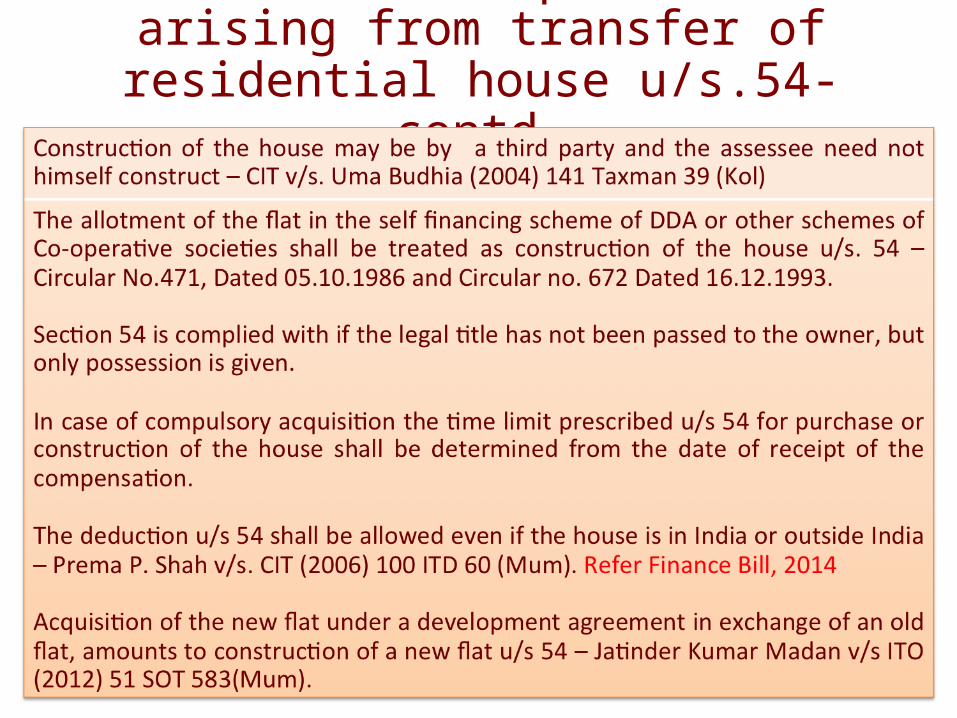

Deduction of Capital Gains arising from transfer of residential house u/s.54- contd…

Deduction of Capital Gains arising from transfer of residential house u/s. 54- contd…

Deduction of Capital Gains arising from transfer of residential house u/s. 54- contd…

Deduction of Capital Gains arising from transfer of residential house u/s. 54- contd…

Deduction of Capital Gains arising from transfer of residential house u/s. 54- contd…

Deduction of Capital Gains arising from transfer of residential house u/s. 54- contd…

6

73

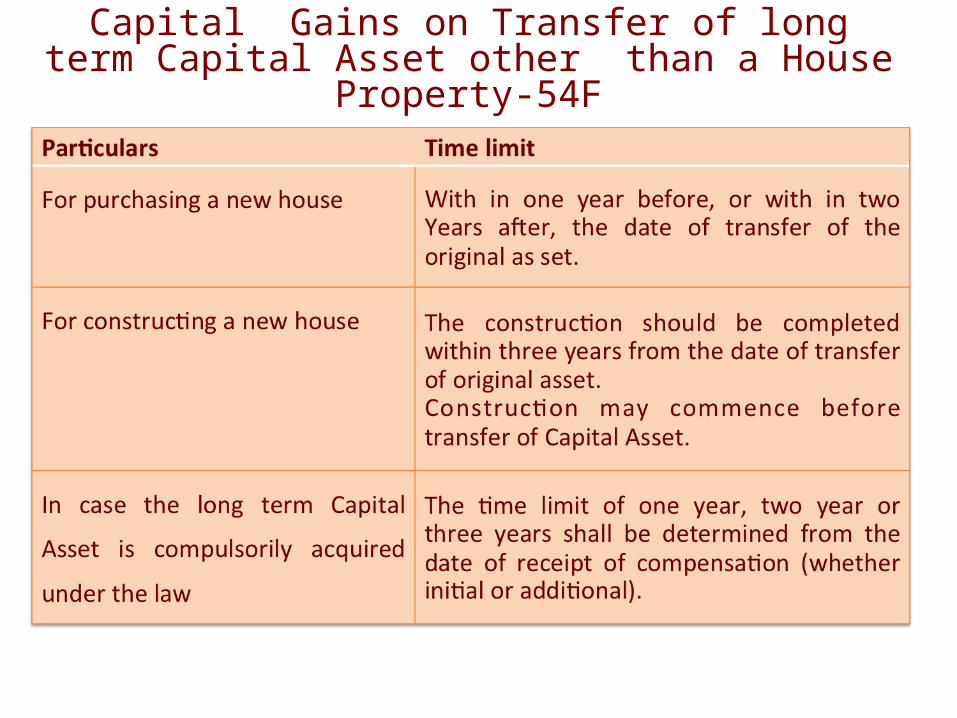

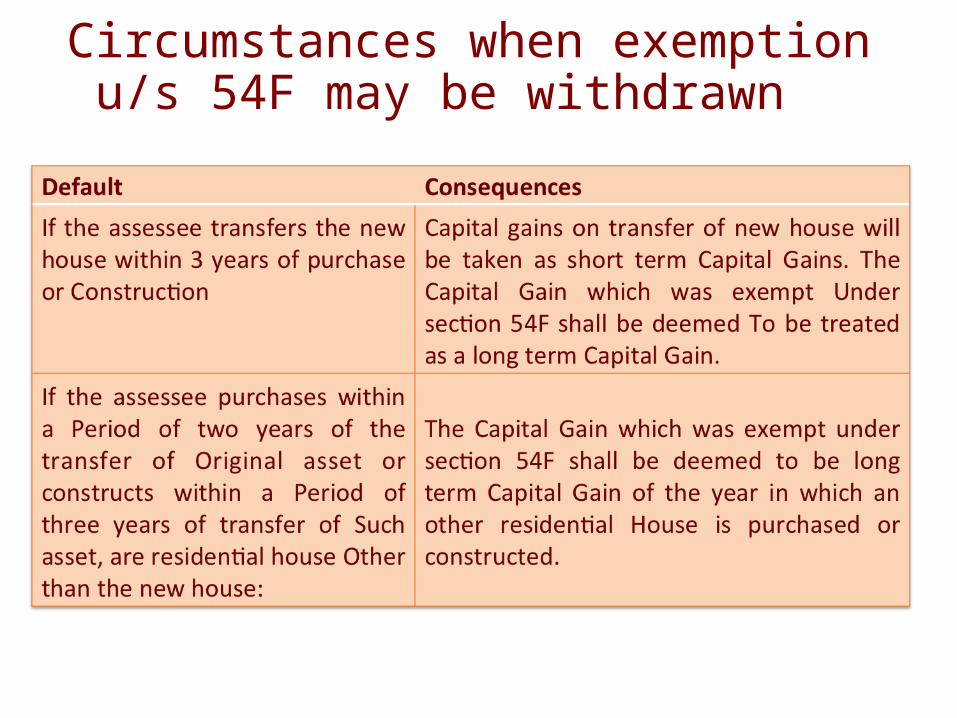

Section 54 – if the new house is transferredwithin three years.

If the new residential property is transferred within three years from the date of it’s acquisition the amount of exemption given earlier, would be taken back – Section 54(1) (ii).

If the new residential property is transferred within three years from the date of it’s acquisition the amount of exemption given earlier, would be taken back – Section 54(1) (ii).

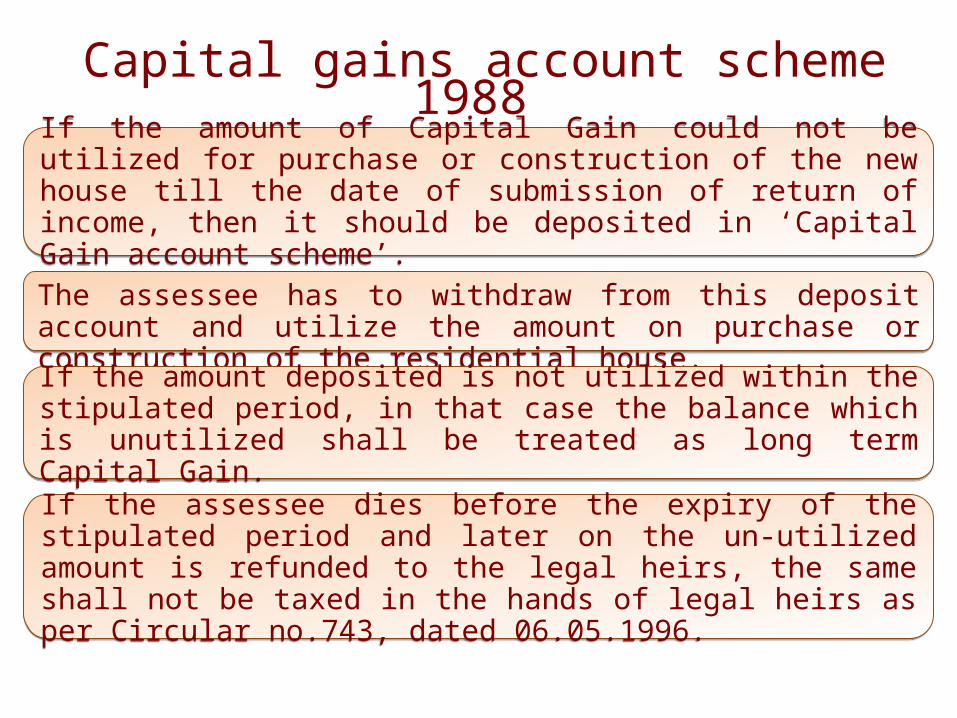

Capital gains account scheme 1988 (Notification vide GSR No. 724(E) Dated 22.6.1988

74

If the amount of Capital Gain could not be utilized for purchase or construction of the new house till the date of submission of return of income, then it should be deposited in ‘Capital Gain account scheme’.

If the amount of Capital Gain could not be utilized for purchase or construction of the new house till the date of submission of return of income, then it should be deposited in ‘Capital Gain account scheme’.

The assessee has to withdraw from this deposit account and utilize the amount on purchase or construction of the residential house.The assessee has to withdraw from this deposit account and utilize the amount on purchase or construction of the residential house.

If the amount deposited is not utilized within the stipulated period, in that case the balance which is unutilized shall be treated as long term Capital Gain.

If the amount deposited is not utilized within the stipulated period, in that case the balance which is unutilized shall be treated as long term Capital Gain.

If the assessee dies before the expiry of the stipulated period and later on the un-utilized amount is refunded to the legal heirs, the same shall not be taxed in the hands of legal heirs as per Circular no. 743, dated 06.05.1996

If the assessee dies before the expiry of the stipulated period and later on the un-utilized amount is refunded to the legal heirs, the same shall not be taxed in the hands of legal heirs as per Circular no. 743, dated 06.05.1996

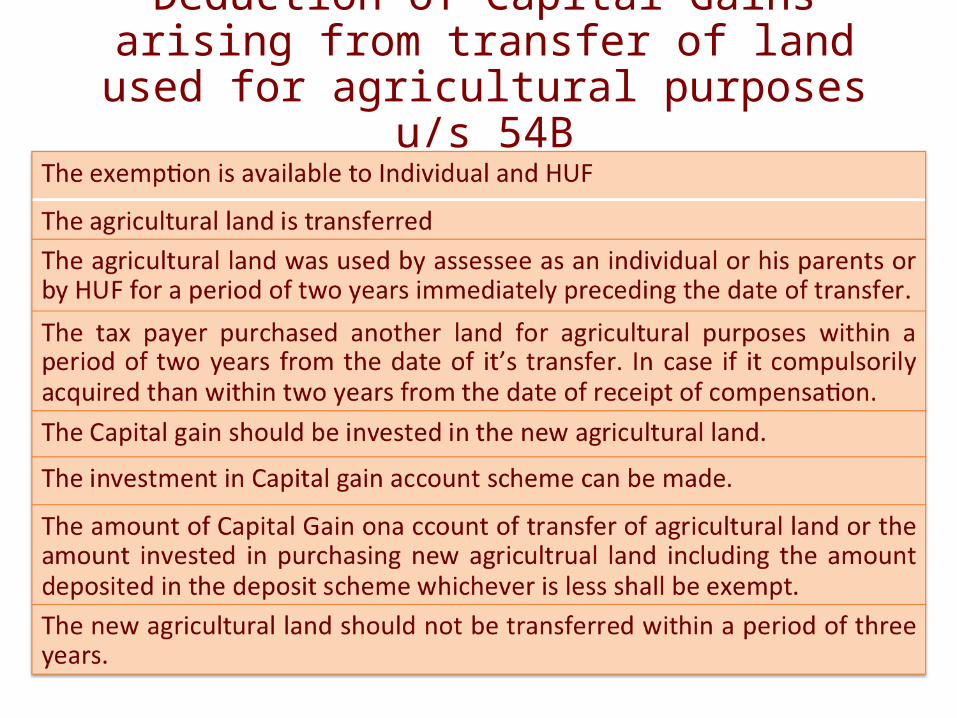

Deduction of Capital Gains arising from transfer of land used for agricultural purposes u/s 54B

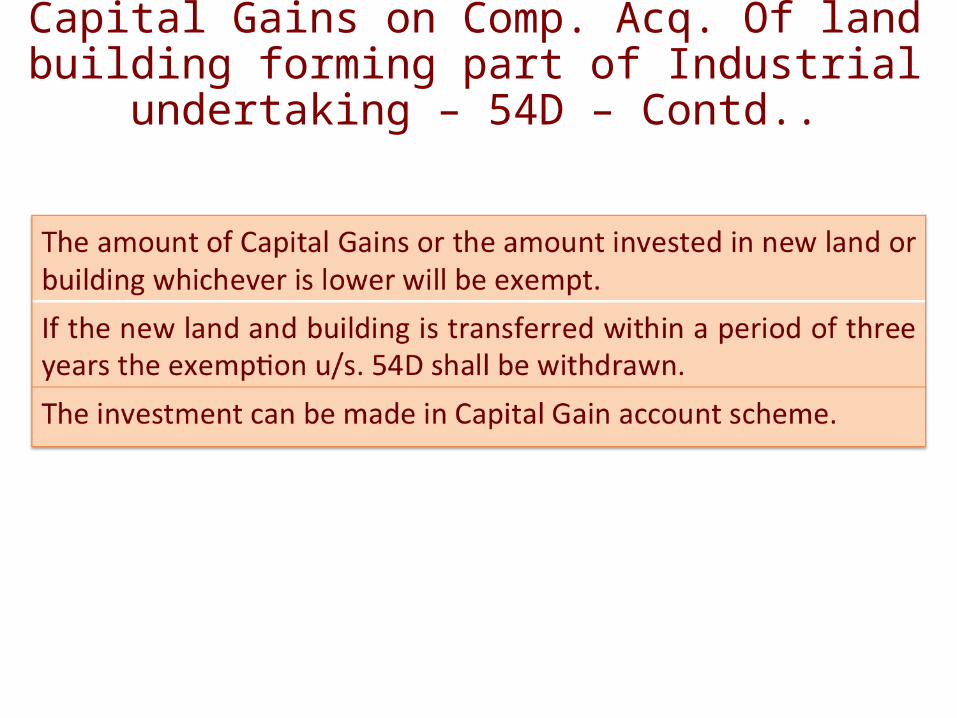

Capital Gains on Comp. Acq. Of land building forming part of Industrial undertaking – 54D

Capital Gains on Comp. Acq. Of land building forming part of Industrial undertaking – 54D –

Contd..

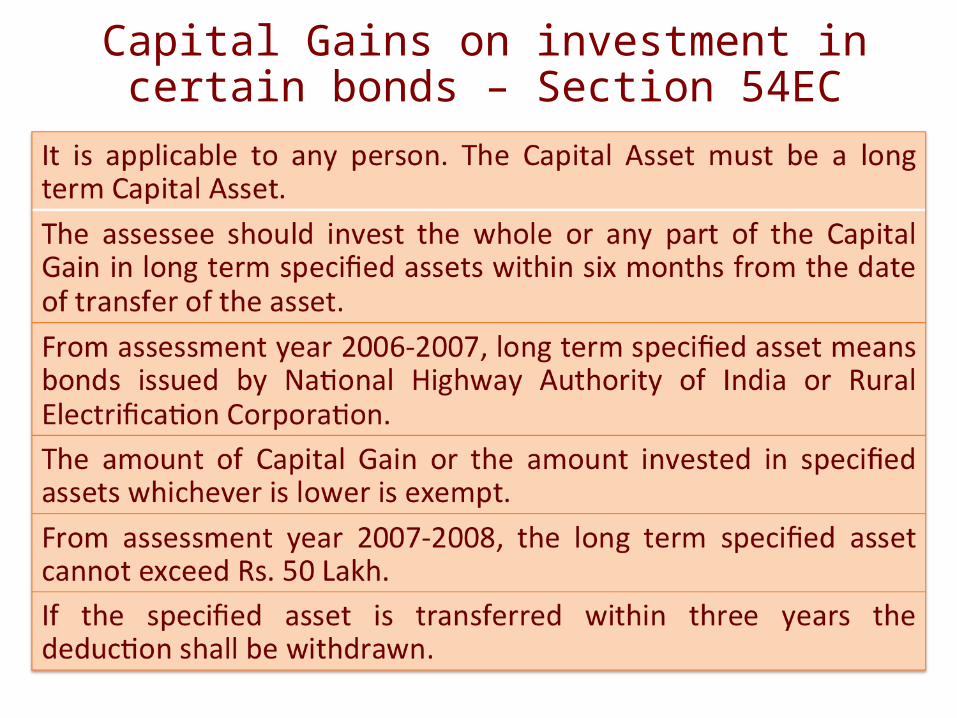

Capital Gains on investment in certain bonds – Section 54EC

Capital Gains on investment in certain bonds – Section 54EC

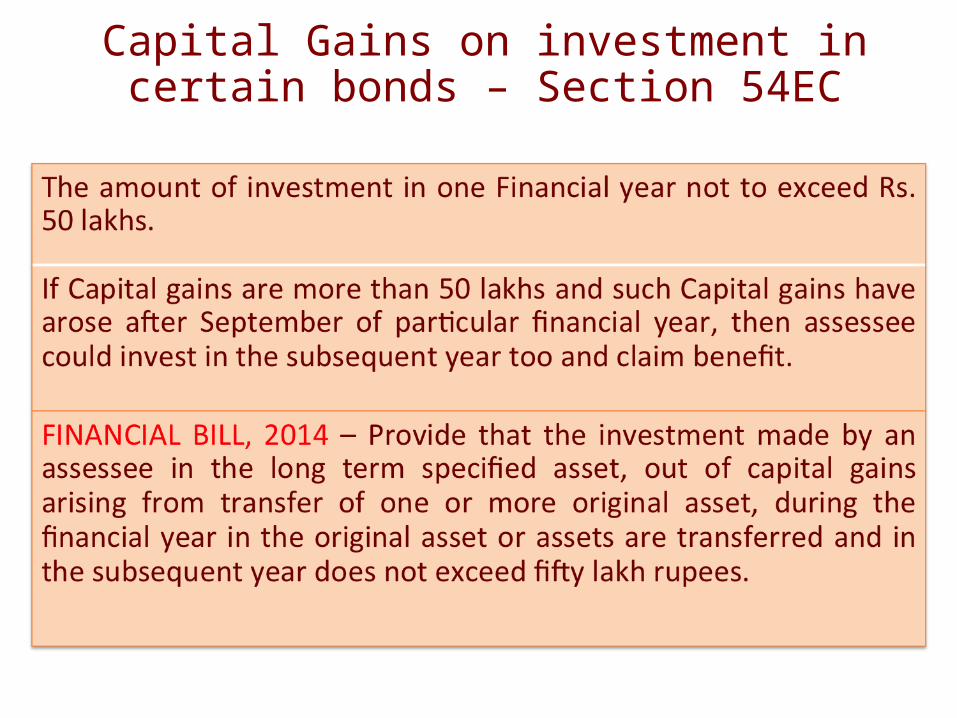

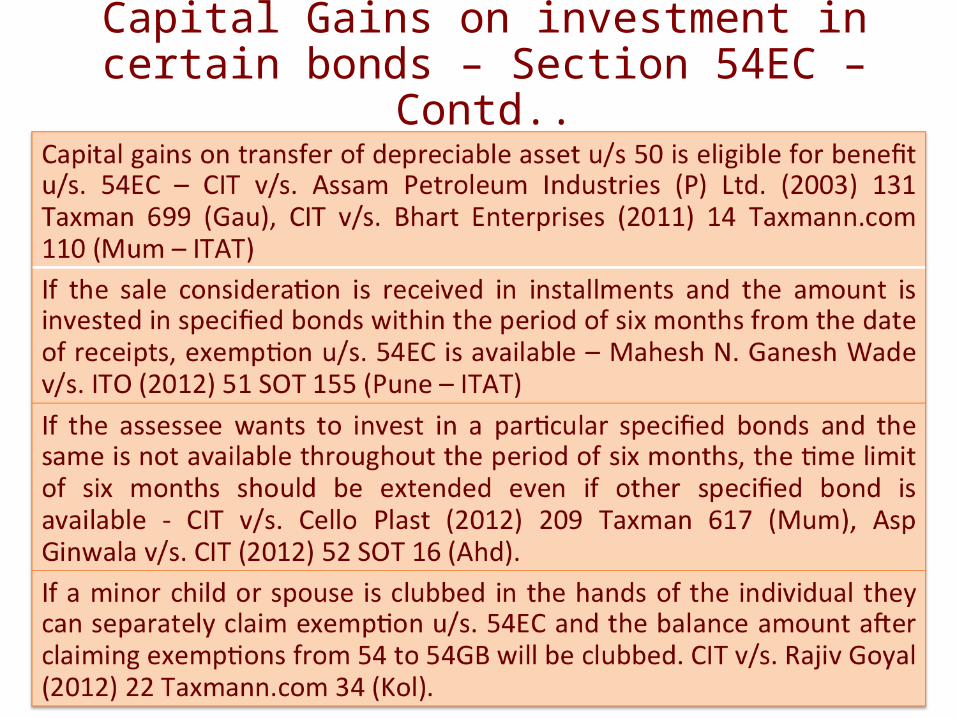

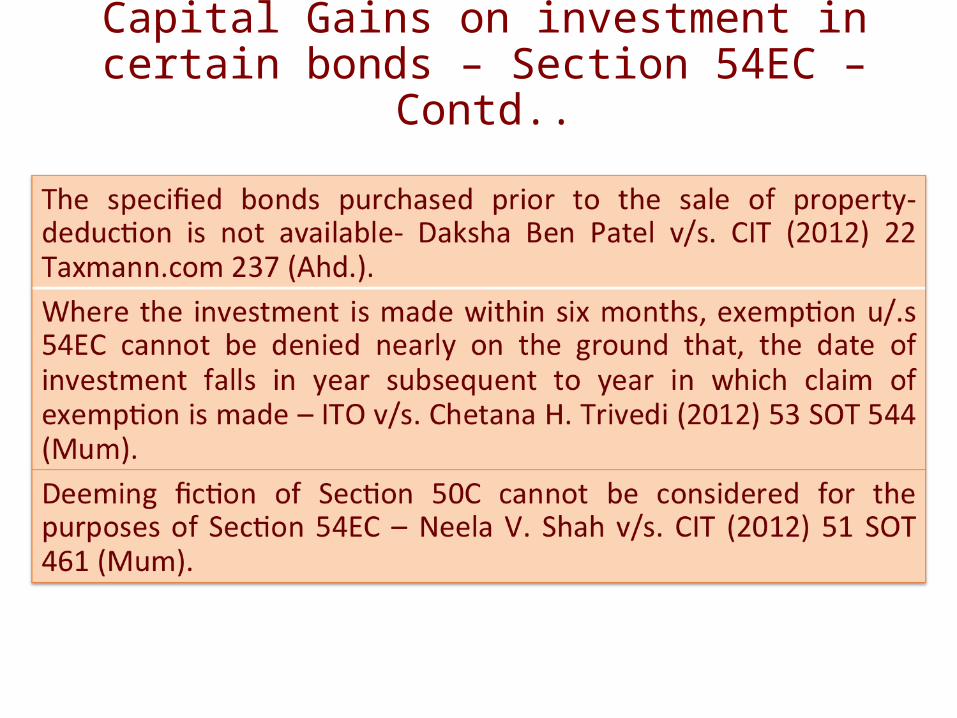

Capital Gains on investment in certain bonds – Section 54EC – Contd..

Capital Gains on investment in certain bonds – Section 54EC – Contd..

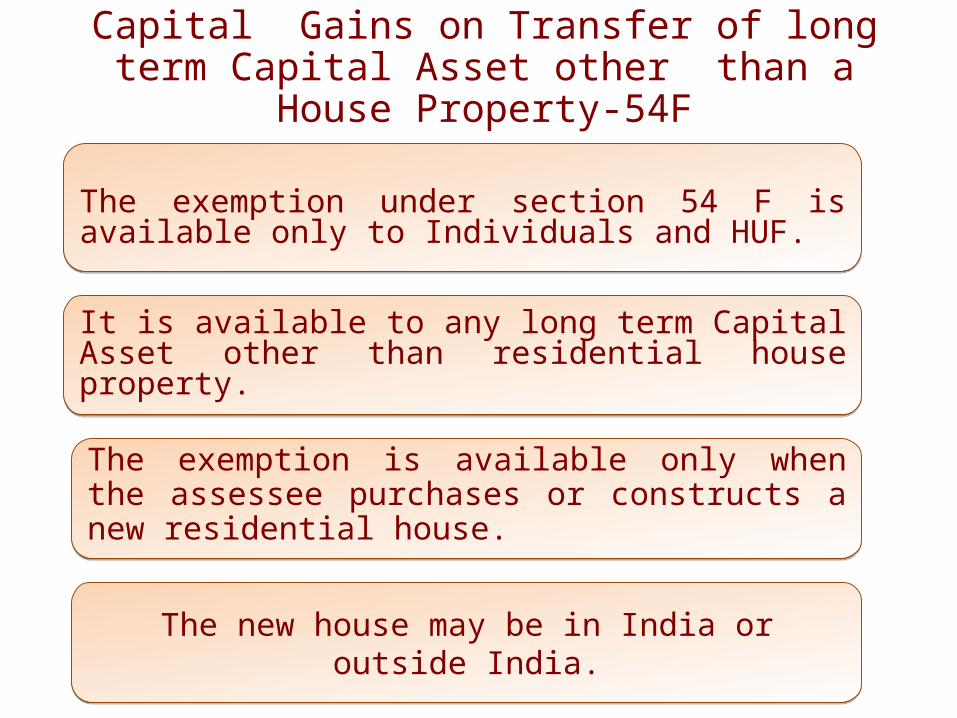

Capital Gains on Transfer of long term Capital Asset other than a House Property-54F

The exemption under section 54 F is available only to Individuals and HUF.The exemption under section 54 F is available only to Individuals and HUF.

It is available to any long term Capital Asset other than residential house property.It is available to any long term Capital Asset other than residential house property.

The exemption is available only when the assessee purchases or constructs a new residential house.The exemption is available only when the assessee purchases or constructs a new residential house.

The new house may be in India or outside India.The new house may be in India or outside India.

Capital Gains on Transfer of long term Capital Asset other than a House Property-54F

Capital Gains on Transfer of long term Capital Asset other than a House Property - 54F

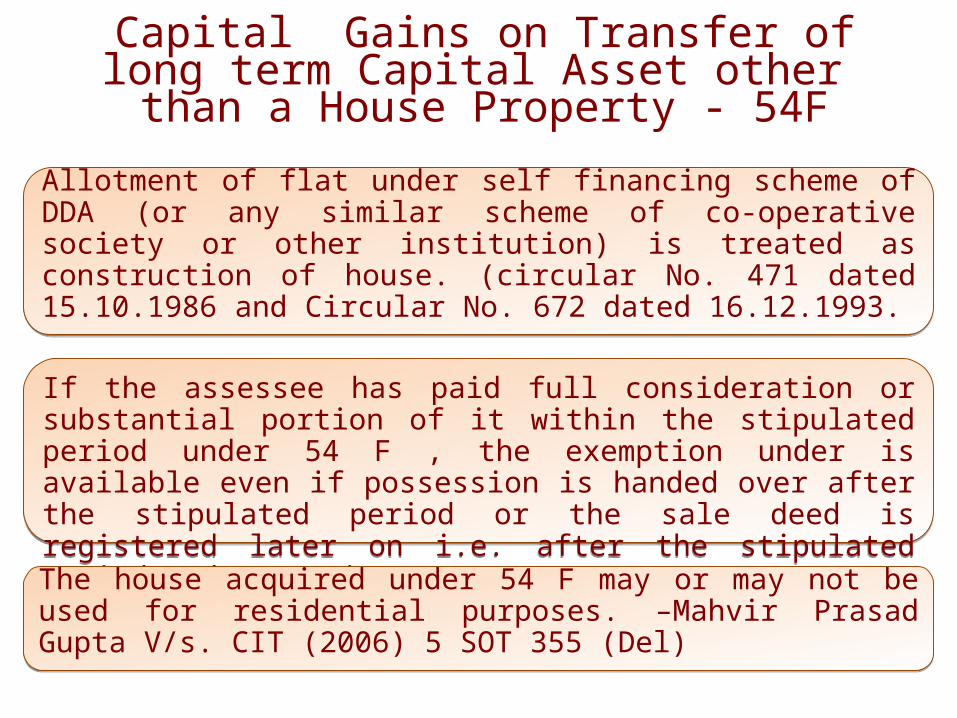

Allotment of flat under self financing scheme of DDA (or any similar scheme of co-operative society or other institution) is treated as construction of house. (circular No. 471 dated 15.10.1986 and Circular No. 672 dated 16.12.1993.

Allotment of flat under self financing scheme of DDA (or any similar scheme of co-operative society or other institution) is treated as construction of house. (circular No. 471 dated 15.10.1986 and Circular No. 672 dated 16.12.1993.

If the assessee has paid full consideration or substantial portion of it within the stipulated period under 54 F , the exemption under is available even if possession is handed over after the stipulated period or the sale deed is registered later on i.e. after the stipulated period under section 54F.

If the assessee has paid full consideration or substantial portion of it within the stipulated period under 54 F , the exemption under is available even if possession is handed over after the stipulated period or the sale deed is registered later on i.e. after the stipulated period under section 54F.

The house acquired under 54 F may or may not be used for residential purposes. –Mahvir Prasad Gupta V/s. CIT (2006) 5 SOT 355 (Del)The house acquired under 54 F may or may not be used for residential purposes. –Mahvir Prasad Gupta V/s. CIT (2006) 5 SOT 355 (Del)

Capital Gains on Transfer of long term Capital Asset other than a House Property - 54F

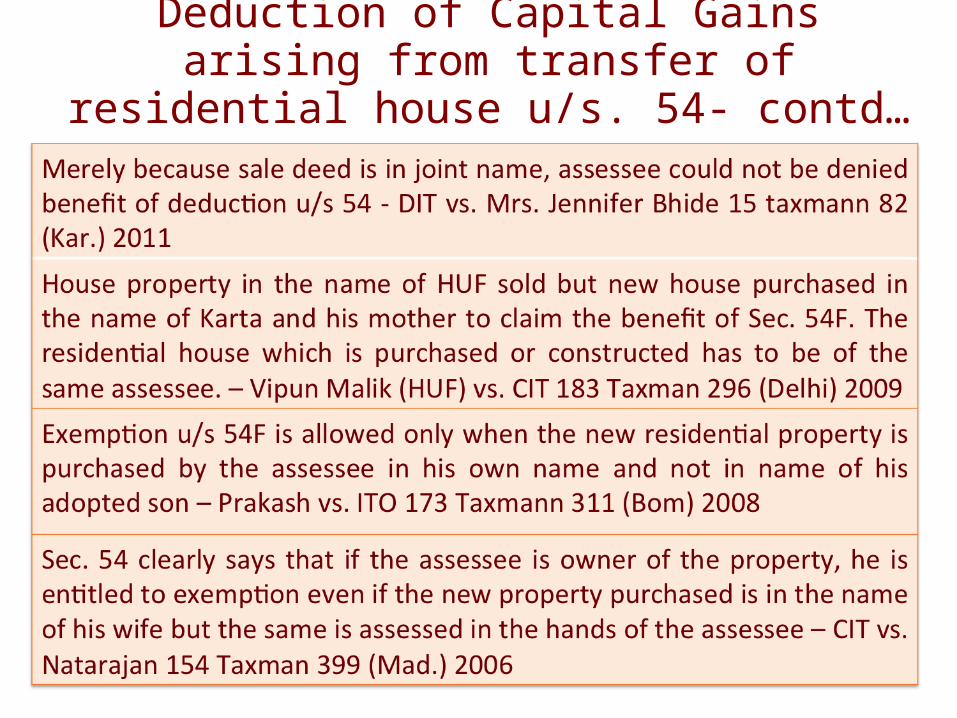

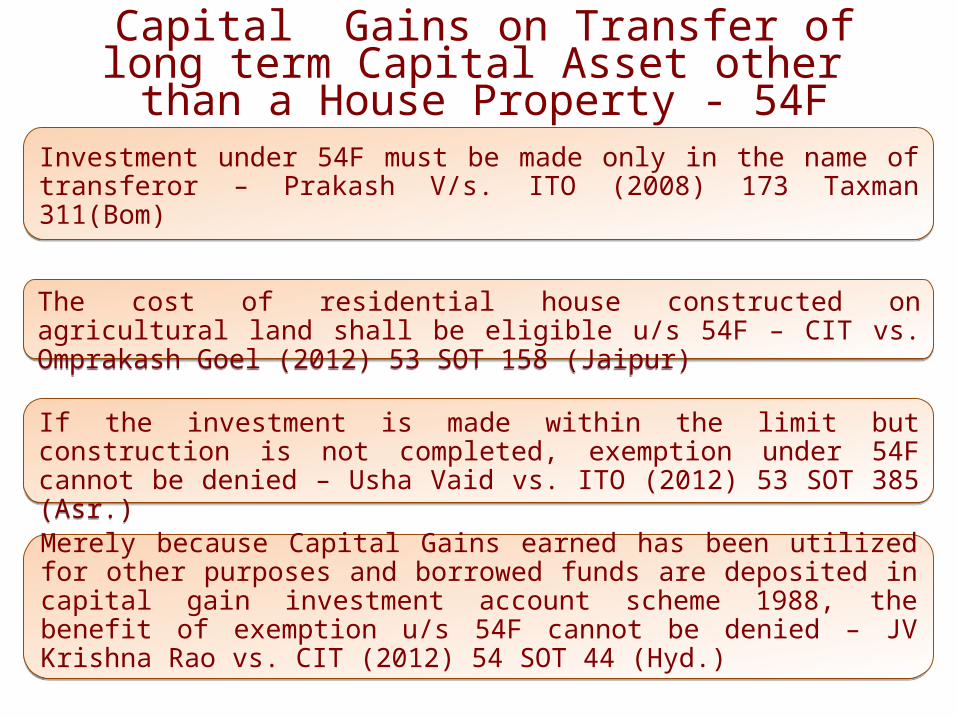

Investment under 54F must be made only in the name of transferor – Prakash V/s. ITO (2008) 173 Taxman 311(Bom)Investment under 54F must be made only in the name of transferor – Prakash V/s. ITO (2008) 173 Taxman 311(Bom)

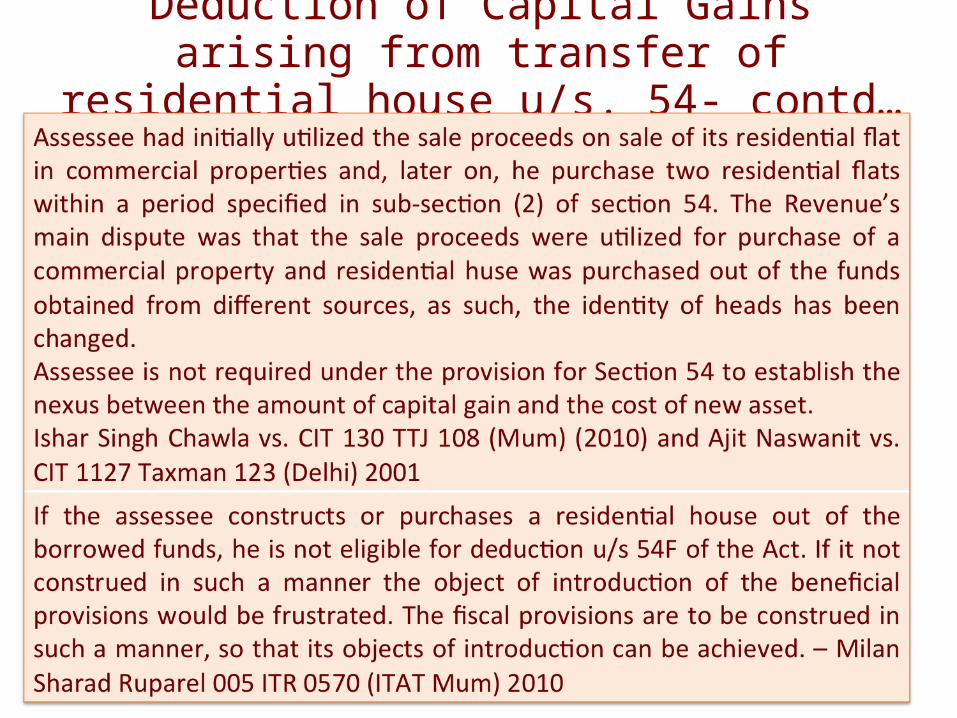

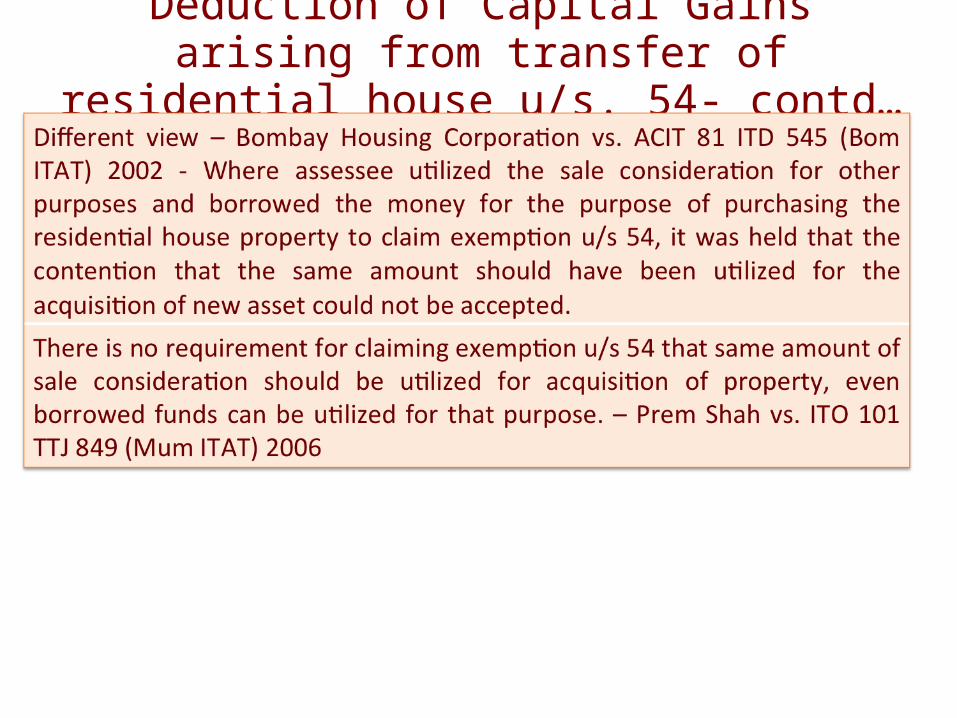

Merely because Capital Gains earned has been utilized for other purposes and borrowed funds are deposited in capital gain investment account scheme 1988, the benefit of exemption u/s 54F cannot be denied – JV Krishna Rao vs. CIT (2012) 54 SOT 44 (Hyd.)

Merely because Capital Gains earned has been utilized for other purposes and borrowed funds are deposited in capital gain investment account scheme 1988, the benefit of exemption u/s 54F cannot be denied – JV Krishna Rao vs. CIT (2012) 54 SOT 44 (Hyd.)

The cost of residential house constructed on agricultural land shall be eligible u/s 54F – CIT vs. Omprakash Goel (2012) 53 SOT 158 (Jaipur)The cost of residential house constructed on agricultural land shall be eligible u/s 54F – CIT vs. Omprakash Goel (2012) 53 SOT 158 (Jaipur)

If the investment is made within the limit but construction is not completed, exemption under 54F cannot be denied – Usha Vaid vs. ITO (2012) 53 SOT 385 (Asr.)

If the investment is made within the limit but construction is not completed, exemption under 54F cannot be denied – Usha Vaid vs. ITO (2012) 53 SOT 385 (Asr.)

Capital Gains on Transfer of long term Capital Asset other than a House Property - 54F

Section 54F does not provide for exemption on investment in renovation or modification of an existing hose. On the other hand, construction of a house only qualified for exemption on the investment. Even addition of a floor of a self contained type to the existing house would have qualified for exemption. However, since the assessee has only made addition to the plinth area, which is in the form of modification of an existing house, the assessee has not contruction any separate apartment or house, she is not entitled to deduction claiemd u/s 54F of the Act. – Mrs. Meera Jacob vs. ITO 313 ITR 411 (Kerala)

Section 54F does not provide for exemption on investment in renovation or modification of an existing hose. On the other hand, construction of a house only qualified for exemption on the investment. Even addition of a floor of a self contained type to the existing house would have qualified for exemption. However, since the assessee has only made addition to the plinth area, which is in the form of modification of an existing house, the assessee has not contruction any separate apartment or house, she is not entitled to deduction claiemd u/s 54F of the Act. – Mrs. Meera Jacob vs. ITO 313 ITR 411 (Kerala)

Section 54F does not provide for renovation or modification of an existing house. Pushpa vs. ITO (2013) 213 Taxman 191 (Ker)Section 54F does not provide for renovation or modification of an existing house. Pushpa vs. ITO (2013) 213 Taxman 191 (Ker)

Capital Gains on Transfer of long term Capital Asset other than a House Property - 54F

Assessee owned two residential houses. He sold one house and utilized its sale proceeds to construct first floor on his second house after demolishing old structure, in this case exemption will be allowable u/s 54 – CIT vs. P.V. Narsimhan (1989) 47 taxman 89 – Mad.

Assessee owned two residential houses. He sold one house and utilized its sale proceeds to construct first floor on his second house after demolishing old structure, in this case exemption will be allowable u/s 54 – CIT vs. P.V. Narsimhan (1989) 47 taxman 89 – Mad.

Assessee owned two residential houses. He sold one house and utilized its sale proceeds to construct first floor on his second house after demolishing old structure, in this case exemption will be allowable u/s 54 – CIT vs. P.V. Narsimhan (1989) 47 taxman 89 – Mad.

Assessee owned two residential houses. He sold one house and utilized its sale proceeds to construct first floor on his second house after demolishing old structure, in this case exemption will be allowable u/s 54 – CIT vs. P.V. Narsimhan (1989) 47 taxman 89 – Mad.

Capital Gains on Transfer of long term Capital Asset other than a House Property-

54F.

88

• Not more than one residential house property (other than the new house) should be owned by taxpayer on the date of transfer of original Capital Asset.

• The assessee should also not purchase another new house within a period of two years or construct another house within a period of three years from the date of new house.

• Amount of exemption

• Cost of new house x Capital Gains *Net sale Consideration

*Net sale consideration = Full value of consideration received or accrued as a result of transfer of the Capital Asset after deduction of any expenditure incurred wholly and exclusively in connection with the transfer.

Capital Gains on Transfer of long term Capital Asset other than a House Property - 54F

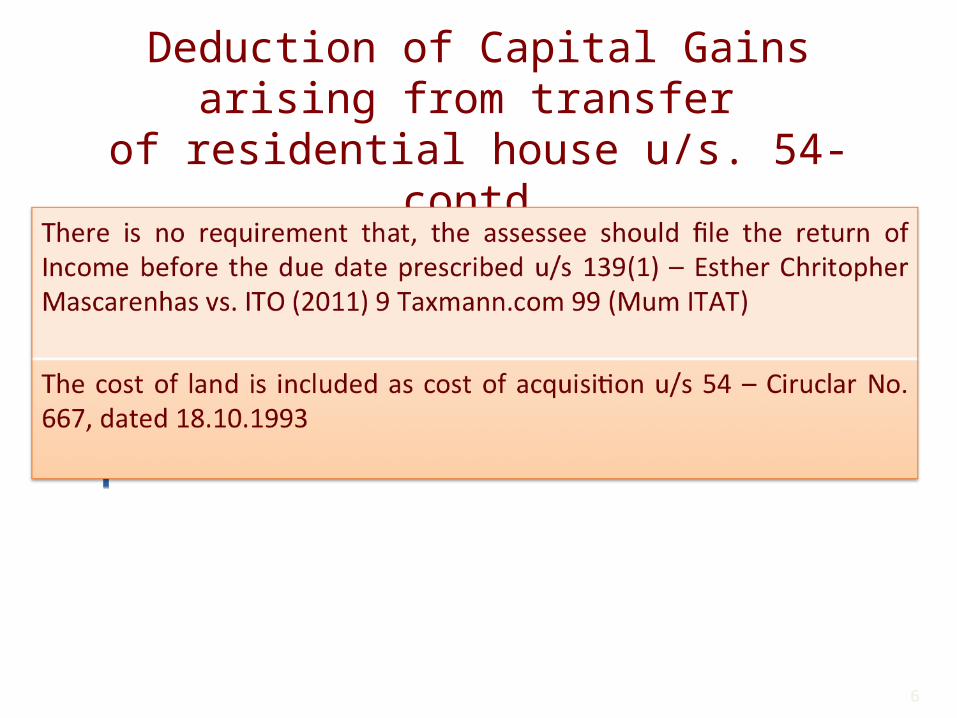

Cost of new house includes cost of land – Circular no.667 dated 18.10.1993.Cost of new house includes cost of land – Circular no.667 dated 18.10.1993.

Cost of vacant land appurtenant to ,and forming part of a residential unit is to be considered for claim of exemption u/s. 54 F, even if no construction has been done on appurtenant land. –CIT v/s Narendra Mohan Uniyal (2009) 34 SOT 152 (Del).

Cost of vacant land appurtenant to ,and forming part of a residential unit is to be considered for claim of exemption u/s. 54 F, even if no construction has been done on appurtenant land. –CIT v/s Narendra Mohan Uniyal (2009) 34 SOT 152 (Del).

If the transferor allows the transferee to retain and apply a part of total consideration to discharge the mortgage to which the property has been subjected to, the amount so applied for discharge of mortgage would have to be excluded from the full value of consideration. CIT V/s. N.M.A Mohammed Haniffa (2001) 115 Taxman 181 (Mad).

If the transferor allows the transferee to retain and apply a part of total consideration to discharge the mortgage to which the property has been subjected to, the amount so applied for discharge of mortgage would have to be excluded from the full value of consideration. CIT V/s. N.M.A Mohammed Haniffa (2001) 115 Taxman 181 (Mad).

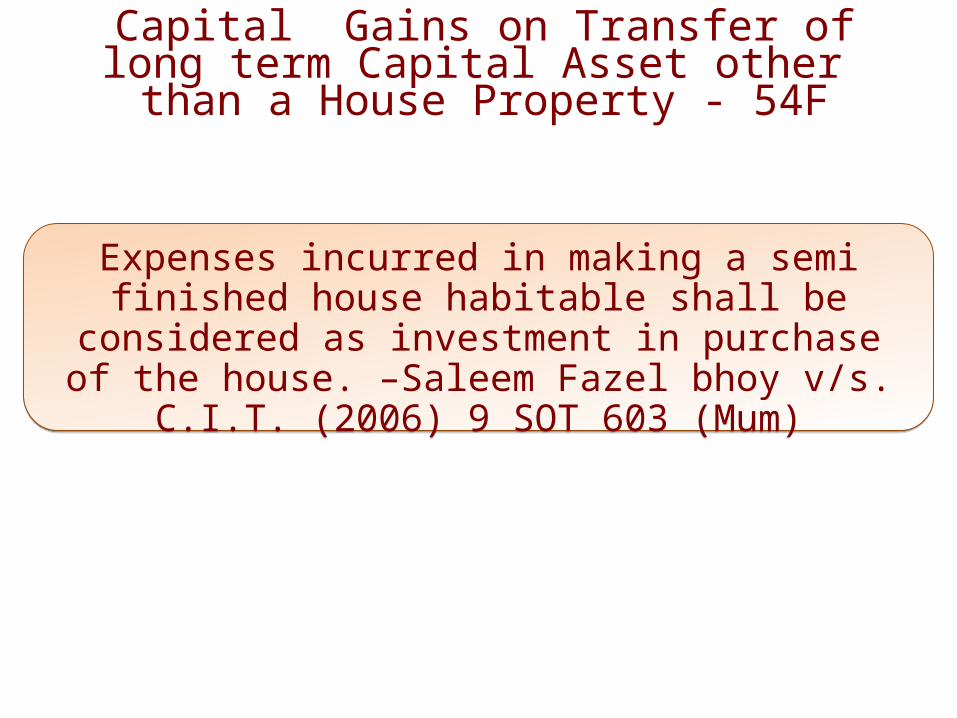

Capital Gains on Transfer of long term Capital Asset other than a House Property - 54F

Expenses incurred in making a semi finished house habitable shall be considered as investment in purchase of the house. –Saleem Fazel bhoy v/s. C.I.T. (2006) 9 SOT

603 (Mum)

Expenses incurred in making a semi finished house habitable shall be considered as investment in purchase of the house. –Saleem Fazel bhoy v/s. C.I.T. (2006) 9 SOT

603 (Mum)

Circumstances when exemption u/s 54F may be withdrawn

Capital gains account scheme 1988

If the amount of Capital Gain could not be utilized for purchase or construction of the new house till the date of submission of return of income, then it should be deposited in ‘Capital Gain account scheme’.

If the amount of Capital Gain could not be utilized for purchase or construction of the new house till the date of submission of return of income, then it should be deposited in ‘Capital Gain account scheme’.

The assessee has to withdraw from this deposit account and utilize the amount on purchase or construction of the residential house.The assessee has to withdraw from this deposit account and utilize the amount on purchase or construction of the residential house.

If the amount deposited is not utilized within the stipulated period, in that case the balance which is unutilized shall be treated as long term Capital Gain.

If the amount deposited is not utilized within the stipulated period, in that case the balance which is unutilized shall be treated as long term Capital Gain.

If the assessee dies before the expiry of the stipulated period and later on the un-utilized amount is refunded to the legal heirs, the same shall not be taxed in the hands of legal heirs as per Circular no.743, dated 06.05.1996.

If the assessee dies before the expiry of the stipulated period and later on the un-utilized amount is refunded to the legal heirs, the same shall not be taxed in the hands of legal heirs as per Circular no.743, dated 06.05.1996.

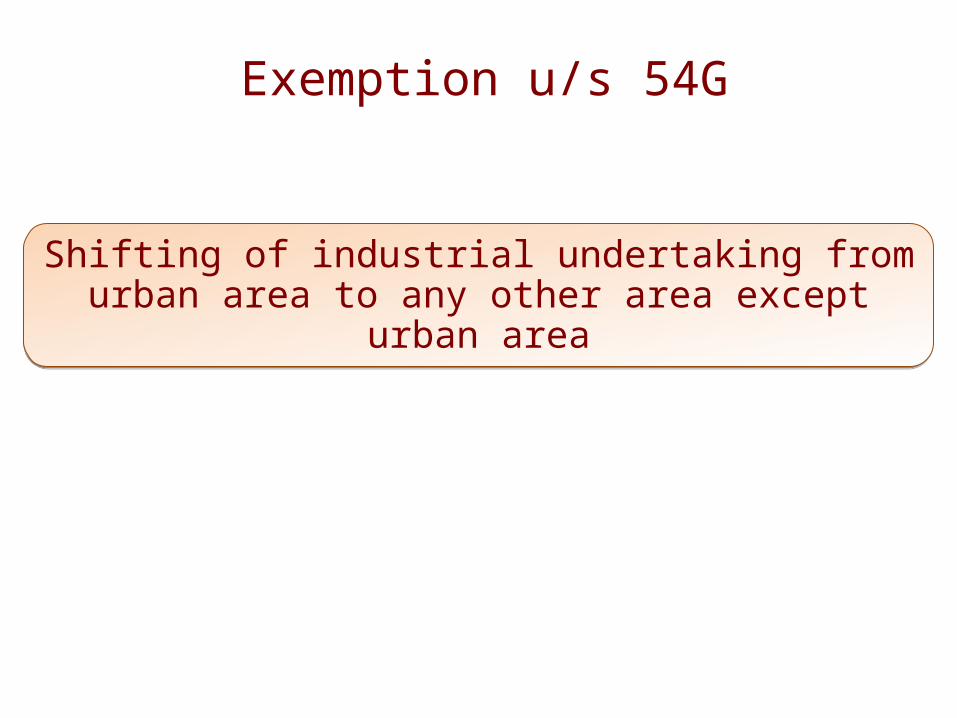

Exemption u/s 54G

Shifting of industrial undertaking from urban area to any other area except urban area

Shifting of industrial undertaking from urban area to any other area except urban area

Exemption u/s 54GA

Exemption of Capital Gain on transfer of assets in case of shifting of industrial undertaking from urban area to any

SEZ

Exemption of Capital Gain on transfer of assets in case of shifting of industrial undertaking from urban area to any

SEZ

-

95

THANKING YOUTHANKING YOU

CA Amitoz Singh KambojTAX Faculty: CA – IPCC, FINAL

You can contribute your suggestions/views on [email protected], 98720-27526

EDUSHELF INNOVATIONS PVT. LTD.WWW.CAWEBWORLD.COM