presented to: july 29, 2013 managing interest rate risk the information contained herein was...

TRANSCRIPT

Presented to:

July 29, 2013

Managing Interest Rate Risk

The information contained herein was generated by an employee of PNC Bank’s Derivative Products Group. Such information is not a “research report” nor is it intended to constitute a “research report” (as defined by applicable regulations). The information contained herein is of general market, economic, and political conditions or statistical summaries of financial data and is not an analysis of the price or market for any derivative.

Agenda

I. Introduction to Interest Rate Swaps

II. Current Hedging Strategies

III. Recent Regulatory Changes

IV. Current Market Conditions

I. Introduction to Interest Rate Swaps

Pay Fixed Interest Rate Swaps

The borrower has an agreement to pay its lender a floating interest rate on the underlying debt.

The swap counterparty agrees to pay the borrower a floating index, in exchange for the borrower paying the swap counterparty the fixed swap rate.

Any difference between the floating index received and the floating rate paid is referred to as basis risk. This can be a cost or benefit to the borrower, depending on market conditions.

The Borrower can reduce its floating rate exposure, without impacting the underlying financing agreements.

Lender Borrower Swap Counterparty

Actual Floating Rate

Fixed Swap Rate

Floating Index

Underlying Debt Interest Rate Swap

Interest Rate Swaps

An interest rate swap is a contractual agreement in which two parties agree to exchange interest payments.

The swap agreement is a separate agreement from any underlying bond/loan agreements (although they may share collateral, cross-default, etc).

A swap can be used to convert a floating rate obligation to a fixed rate or a fixed rate obligation to floating (or convert from one floating index to another).

Principal payments are not exchanged; the swap ‘notional principal’ is used only for the calculation of interest payments.

There is no restriction on the size of the notional amount. By varying the notional amount, a borrower can hedge all, or just a portion of its debt.

A swap can be terminated at any time, where the borrower pays or receives a termination payment depending on the prevailing market rates at termination.

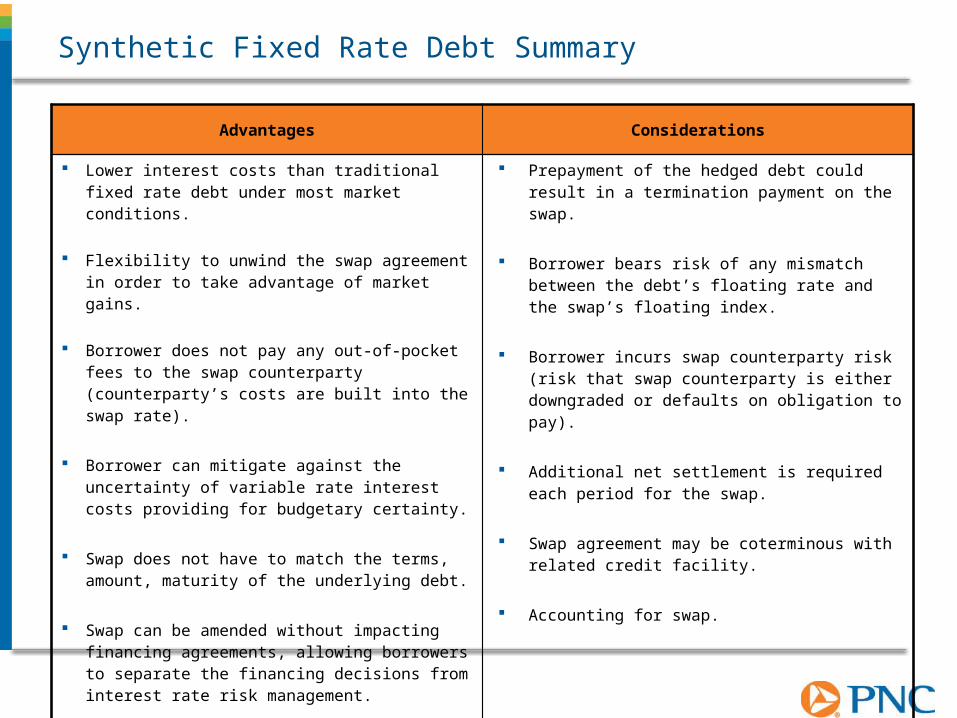

Synthetic Fixed Rate Debt Summary

Advantages Considerations

Lower interest costs than traditional fixed rate debt under most market conditions.

Flexibility to unwind the swap agreement in order to take advantage of market gains.

Borrower does not pay any out-of-pocket fees to the swap counterparty (counterparty’s costs are built into the swap rate).

Borrower can mitigate against the uncertainty of variable rate interest costs providing for budgetary certainty.

Swap does not have to match the terms, amount, maturity of the underlying debt.

Swap can be amended without impacting financing agreements, allowing borrowers to separate the financing decisions from interest rate risk management.

Prepayment of the hedged debt could result in a termination payment on the swap.

Borrower bears risk of any mismatch between the debt’s floating rate and the swap’s floating index.

Borrower incurs swap counterparty risk (risk that swap counterparty is either downgraded or defaults on obligation to pay).

Additional net settlement is required each period for the swap.

Swap agreement may be coterminous with related credit facility.

Accounting for swap.

Termination Values

Swap termination values are calculated in a similar way to traditional ‘prepayment’ or ‘make whole’ provisions in most fixed rate bank loans.

In the event of an early partial or full termination, the rate on the swap agreement would be compared to then prevailing market fixed rates for the remaining term.

For example, if a swap agreement was terminated with 2-years remaining to maturity, the swap rate would be compared to then prevailing 2-year swap rates.

– If the 2-year market rate is below the borrower’s swap rate, the borrower must make a termination payment.

– If the 2-year market rate is higher than the swap rate, the borrower receives a termination payment.

The calculation is as follows:

– The interest due on each remaining payment date is calculated at the existing swap rate and the current market rate.

– The termination value is the present value of the difference between those payment streams.

Transaction Process

When a borrower indicates an interest to lock a swap rate with PNC, we first must verify eligibility.

We then prepare an ISDA Master Agreement and Schedule (collectively, the ISDA) and complete our internal approvals.

Once the signed ISDA is received by PNC, the borrower can call the Derivatives Trading Desk any time for a live rate quote.

The borrower can accept the rate quote and authorize us to lock in the rate (via telephone, on a recorded telephone line) anytime they desire.

Upon locking the rate, we will generate the Confirmation letter detailing the terms of the agreement, and send it for signatures via email.

We ask for the confirmation letter to be signed and returned to PNC within one week of verbal execution.

ISDA Master & Schedule(and related documents)

Live Rate Quote

Borrrower Locks Rate

Trade Confirmation

ECP and W-9 Verification

II. Current Hedging Strategies

Hedging Direct Placement Bonds

Compared to traditional bank letter of credit-backed Variable Rate Demand Bonds, hedging a Direct Placement Bond with an interest rate swap has a number of advantages

Reduced basis and trading risk

The amount the borrower receives under the swap will match the amount paid by the borrower on the Bond (excluding credit spread). A downgrade of the bank’s credit rating would not impact the Bond’s trading price.

Longer term credit commitment

The term of the credit commitment on a Direct Placement Bond is likely to exceed the term offered on a letter of credit, allowing borrowers to take advantage of low, long-term fixed rates with less frequent credit renewal risks.

Tax efficient pricing reduces interest costs

A long-term swap priced against 70% of 1-Month LIBOR (Direct Placement) currently has a substantially lower rate than the same swap priced against SIFMA (LoC).

Long-Term Hedge on Shorter Credit Term

Historically low long-term fixed rates combined with the prospect for higher fixed rates in the future have compelled many borrowers to seek long-term rate protection.

However, most banks have an interest in protecting their balance sheet by providing shorter term credit commitments.

One possible solution to satisfy both parties can be executing a swap for the full amortization period while closing a shorter term loan (e.g. 7/20 loan with 20yr swap)

This strategy eliminates interest rate risk for the borrower but introduces credit renewal risk (either termination of the facility or an increase in the credit spread)

The swap may be cross-collateralized and coterminous with underlying financing.

If the financing is ever terminated for any reason, the swap counterparty would have the right to terminate the swap at its market value.

If the swap has a negative market value, the borrower will be required to pay the counterparty to terminate the swap, in addition to paying back the outstanding loan balance.

Borrowers can utilize a cancelable interest rate swap to mitigate credit renewal risk.

Cancelable Interest Rate Swaps

A cancelable interest rate swap combines a fixed interest rate with the option to terminate the agreement at no cost on a predetermined date or dates.

These dates can be aligned with the maturity of the underlying credit facility.

The borrower buys the cancelation option by way of a fixed interest rate above that of a traditional fixed rate swap.

If the swap has a negative market value on an Option Date, the borrower may terminate with no payment to PNC.

If the underlying loan is still in place, the borrower simply reverts back to the floating rate.

If the borrower chooses not to terminate on an Option Date, the swap stays in place until maturity, or at least until the next Option Date.

As with any swap agreement, the borrower retains the right to terminate the Cancelable Swap on non-Option Dates as well, where they either pay or receive the current market value of the agreement at the time of termination.

If the swap is in-the-money to the borrower (i.e. comparable rates are higher), the borrower still receives that value.

Novations

Counterparty risk and large collateral postings have caused many borrowers to consider the assignment of existing trades to a new counterparty.

Collateral postings under a bi-lateral Credit Support Annex that result from negative swap values and/or credit rating downgrades may be reduced or eliminated by transferring trades to a new counterparty.

Although the aggregate value of the swap portfolio has not changed, the allocation of that value across additional counterparties may keep each individual counterparty’s exposure under the threshold levels that trigger collateral posting.

The addition of another counterparty is often viewed as wise risk management following the recent history of large swap counterparty downgrades, mergers and bankruptcy.

A novation is a short, simple agreement that allows a third party to step between the two existing counterparties in an existing agreement.

This process allows swap users to replace an existing counterparty, potentially in conjunction with the take-out of a hedged credit facility, without incurring possible cash termination payments.

Once the novation has been completed, the originating financial institution’s role in the swap is substituted with a new counterparty.

Blend and Extend Strategies

Many borrowers with existing fixed rates would like to capitalize on today’s low rates

A hedge expiring in the near-term may expose the borrower to the risk of re-striking at a higher fixed rate upon maturity

Borrowers with above market fixed rates may want to immediately reduce interest expense

A blend and extend allows borrowers to immediately restructure by “blending” the swap’s existing market value into a new transaction and often “extending” the maturity date

Benefits:

An existing swap with a negative market value does not prevent restructuring

Borrowers may be able to reduce current fixed rates

Borrowers are not required to make an upfront payment to terminate the existing swap

Considerations:

Although the restructured swap rate may be lower than the borrower’s existing fixed rate, it will be higher than current market rates, due to the embedded market value

An alternative would be the termination of the existing swap, with out-of-pocket payment, and execution of the lower current market rate

Step-Up Swaps

A step-up swap converts the underlying debt from floating-to-fixed. Unlike a traditional swap, the borrower’s fixed rate on a step-up swap increases over time according to a predetermined schedule.

Rather than pay a traditional fixed rate that is, initially, significantly higher than the current floating rate, the step-up swap gives the borrower the benefit of a lower rate today, in exchange for paying a higher rate in the future.

For example, a traditional 10yr taxable swap rate is currently 2.75%. A step-up swap could be structured to pay 0.90% for the next 3 years and then 3.66% in years 4 through 10.

Over the life of the transaction, the fixed interest expense paid under the traditional vs. step-up will be the same. However, some borrowers would prefer a more gradual increase in their interest expense over time, particularly if the fixed rate paid is only slightly higher than the prevailing floating rate alternative.

Participating Swaps

A participating swap converts a portion of the debt to a fixed rate while leaving the remaining portion floating up to a maximum rate.

The structure incorporates the cost of an interest rate cap into the fixed rate of a traditional swap, requiring no upfront, out-of-pocket payment. The borrower has partial "participation" in floating rates under this approach.

Consider a traditional 10yr tax-exempt swap rate at 2.00% vs. 70% of 1ML. Rather than swap all of the debt to fixed, the borrower buys a 10yr 2.50% cap on half and executes a 10yr swap on the other half at a 2.60% fixed rate. The 2.60% swap rate includes the cost of the cap. With 50% of the debt fixed at 2.60% and 50% currently floating at 0.14%, the blended cost of capital is 1.37%.

As floating rates rise, the maximum blended rate would be 2.55%. Similar to an interest rate collar, the borrower has bound their interest rate between ~1.37% and 2.55%.

If rates play out as markets predict, the 1.96% mid-point of this range would make the borrower nearly indifferent between the participating and traditional swaps. But paying 1.37% today while 70% 1ML is 0.14% and 2.55% when 70% 1ML is 3.00% may be more palatable to some borrowers.

III. Recent Regulatory Changes

The Dodd-Frank Wall Street Reform and Consumer Protection Act (Commonly the Dodd-Frank Act or DFA) was signed into law on 7/21/10. The full title describes its broad purpose:

— “An Act to promote the financial stability of the United States by improving accountability and transparency in the financial system, to end ‘too big to fail’, to protect the American taxpayer by ending bailouts, to protect consumers from abusive financial services practices, and for other purposes”

The intention of this presentation is to summarize key elements that may be important to non-financial market participants. A full and complete explanation of Dodd-Frank and Title VII is not within the scope of this discussion. We encourage you to consult with your advisers and legal counsel for additional information.

Dodd-Frank Overview

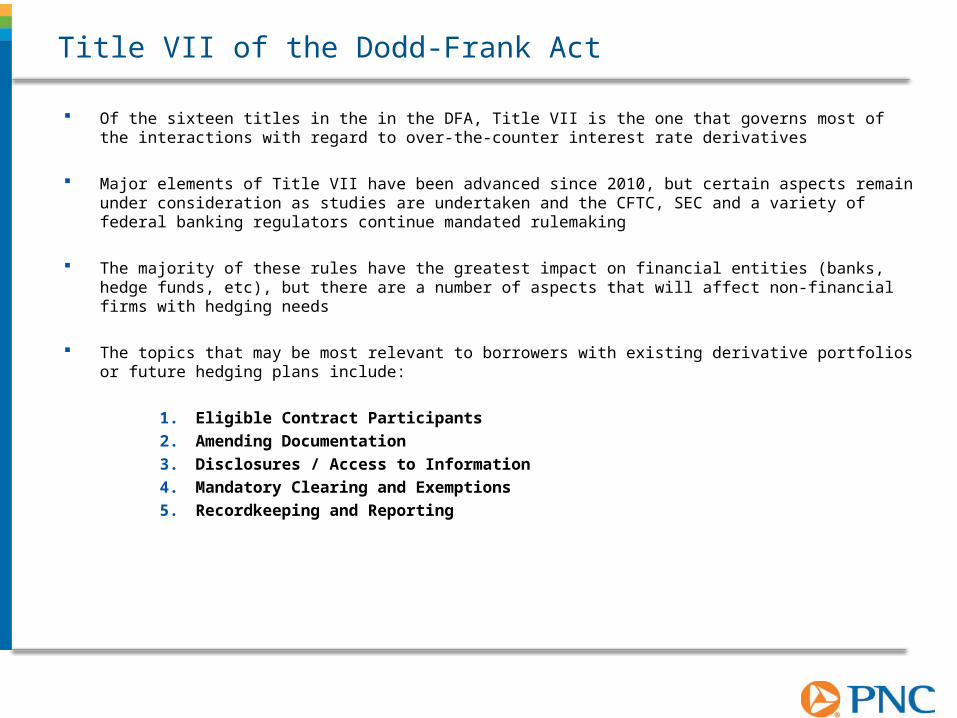

Of the sixteen titles in the in the DFA, Title VII is the one that governs most of the interactions with regard to over-the-counter interest rate derivatives

Major elements of Title VII have been advanced since 2010, but certain aspects remain under consideration as studies are undertaken and the CFTC, SEC and a variety of federal banking regulators continue mandated rulemaking

The majority of these rules have the greatest impact on financial entities (banks, hedge funds, etc), but there are a number of aspects that will affect non-financial firms with hedging needs

The topics that may be most relevant to borrowers with existing derivative portfolios or future hedging plans include:

1. Eligible Contract Participants2. Amending Documentation3. Disclosures / Access to Information4. Mandatory Clearing and Exemptions5. Recordkeeping and Reporting

Title VII of the Dodd-Frank Act

Effective: October 12, 2012

To lawfully enter into a new derivative transaction or a material amendment to an existing transaction, Title VII requires that all parties be Eligible Contract Participants (ECP) at the time of execution

— PNC must confirm each counterparty and any guarantor are ECPs— PNC must document ECP status before entering into the trade

• This includes all members of an Obligated Group structure

In addition to qualifications for financial institutions, individuals, and ERISA employee benefit plans, an ECP can be any one of the following:

— A corporate entity with • total assets > $10 Million (OR) • net worth > $1 Million AND the counterparty is entering into the transaction to manage

the risk in connection with the conduct of its business (OR) • May include ECP owners in combined net worth

• swap obligations are guaranteed by a qualifying entity that is itself an ECP

— A government entity1

• who is deriving its eligible contract participant status from the status of its counterparty as a United States financial institution

• that owns $50mm or more in discretionary investments (funds in its general account that are not otherwise specifically allocated for an obligation)

Eligible Contract Participants

1. the United States, any State or political subdivision thereof, or any agency or instrumentality of any of the foregoing

Corporate entities may include: Corporations, Partnerships, LLC, LLP, Proprietorships, Organizations, Trust, 501(c)(3), and Other Corporate Entities.

Eligible Contract Participants – Corporate Entities

Total Asset Test Guaranty TestAggregate TestNet Worth Test

Does the Corporate Entity have more than $10M in total assets?

Does the Corporate Entity have more than $1M in net worth?

Does the Corporate Entity have owners, all of whom are ECPs?

Does the Corporate Entity have an eligible ECP1 guaranteeing its

swap obligations?

If yes, continue. If no, go to the Net Worth Test

If yes, continue. If no, go to the Aggregate Test.

If yes, continue. If no, go to the Guaranty Test.

If yes, continue. If no, PNC can not trade with this entity.

Is the Corporate Entity entering into a swap for eligible hedging

purposes?

Is the combined net worth of all owners and the Corporate entity

greater than $1M?

If yes, continue. If no, go to the Aggregate Test.

If yes, continue. If no, go to the Guaranty Test.

Is the Corporate Entity entering into a swap for eligible hedging

purposes?

If yes, continue. If no, go to the Guaranty Test.

ECP

ECP

ECP

ECP

1. For purposes of the Guaranty Test, an individual is not an eligible ECP guarantor. Only corporate entities that meet the Total Asset Test are eligible ECP guarantors.

Effective: May 1, 2013

In order to comply with Title VII External Business Conduct Standards, swap market participants will need to amend existing documentation (typically ISDA Master Agreements) and exchange relevant information and disclosures

The amendment will allow the swap dealer to obtain client self-representations that provide certain legal protections, update the counterparty relationship and legal documents, provide required disclosures, and agree to the manner and format of delivering the disclosures

Existing documentation will need to be updated prior to the execution of any new trades, assignments or material amendments

Amending Documentation

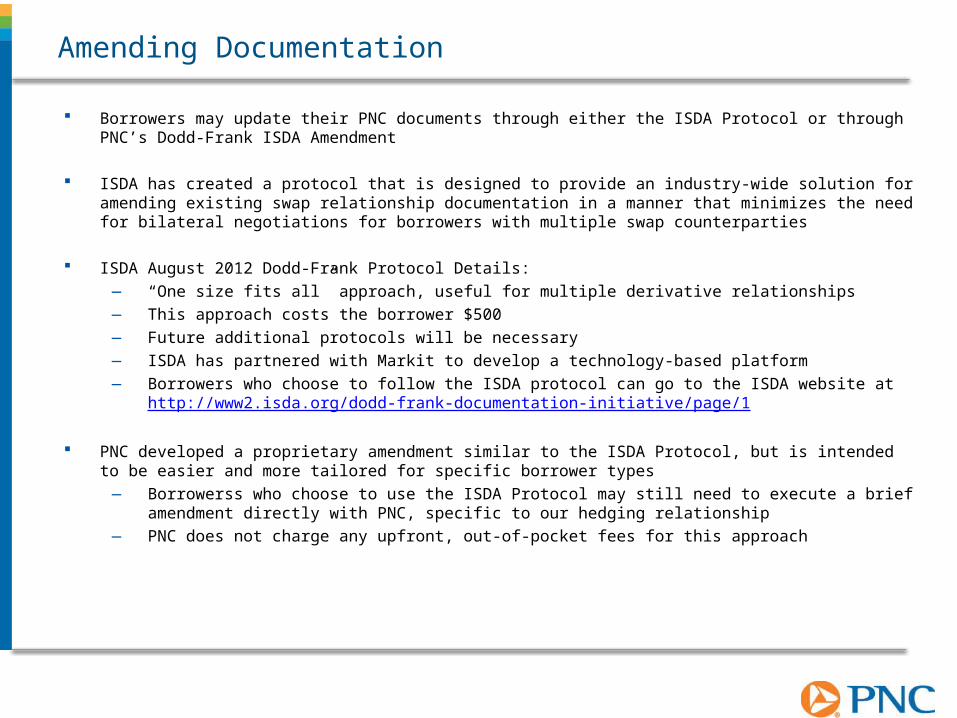

Borrowers may update their PNC documents through either the ISDA Protocol or through PNC’s Dodd-Frank ISDA Amendment

ISDA has created a protocol that is designed to provide an industry-wide solution for amending existing swap relationship documentation in a manner that minimizes the need for bilateral negotiations for borrowers with multiple swap counterparties

ISDA August 2012 Dodd-Frank Protocol Details:— “One size fits all” approach, useful for multiple derivative relationships— This approach costs the borrower $500— Future additional protocols will be necessary— ISDA has partnered with Markit to develop a technology-based platform — Borrowers who choose to follow the ISDA protocol can go to the ISDA website at

http://www2.isda.org/dodd-frank-documentation-initiative/page/1

PNC developed a proprietary amendment similar to the ISDA Protocol, but is intended to be easier and more tailored for specific borrower types

— Borrowerss who choose to use the ISDA Protocol may still need to execute a brief amendment directly with PNC, specific to our hedging relationship

— PNC does not charge any upfront, out-of-pocket fees for this approach

Amending Documentation

Effective: September 9, 2013 (Dealer to customer, if the customer is NOT relying on the Commercial End-User Exception)

Dodd-Frank requires that all CFTC-designated swaps be cleared through a registered “derivatives clearing organization” (DCO) unless:

1. At the time of execution, the DCO won’t accept the structure to clear— The DCO may not have the technical capabilities to clear certain trade types (e.g.

embedded options)

OR

2. If one of the counterparties meets all of the following (the “Commercial End-User Exception”) and elects the exception

— Not a financial entity (banks, broker/dealers, insurance company, etc)• Publicly-traded companies require Board approval to claim the exception

— Using the swap for hedging or mitigating commercial risk (not speculation)— Notifies the CFTC how it meets its financial obligations associated with non-cleared swaps

• The PNC Dodd-Frank ISDA amendment will include how the borrower meets its financial obligations (e.g. cash flow from operations) and allow PNC to report this to the CFTC on the borrower’s behalf

Mandatory Clearing and End-User Exception

Effective: Recordkeeping April 10, 2013Reporting The sooner of swap dealer registration or April 10,

2013

Title VII establishes formalized recordkeeping requirements and reporting obligations to the CFTC

Recordkeeping Requirement: both parties need to maintain records concerning all swaps — Includes trade confirmations and other swap documentation— May be in electronic or in paper form— Duration is maturity of the swap plus five years

Reporting Requirements: one party will be responsible for reporting trade information to a Swap Data Repository (SDR)

— Creation data: includes the primary economic terms of the swap at, or shortly after, execution— Continuation data: during the life of the swap, updated/changed information, must be reported

PNC, as your swap dealer, will report information regarding uncleared trades done with PNC

Recordkeeping and Reporting

Effective: Upon swap dealer registration (January 31, 2013 for PNC)

The CFTC’s final swap data and recordkeeping rule requires all counterparties to a swap to be identified by a CFTC Interim Compliant Identifier (CICI).

As a registered swap dealer, PNC is required to report this identifier to an SDR for both new and historical swaps

The CICI is a unique code associated with a single legal entity and is used to standardize how a counterparty is identified on financial transactions.

— Its goal is to help improve the measuring and monitoring of systemic risk and support more cost-effective compliance with regulatory reporting requirements.

To register and receive a CICI, visit https://www.ciciutility.org/index.jsp — There is one-time $200, non-refundable fee to register— There is a $100 annual maintenance charge

Borrowers will then provide their CICI to PNC for use in meeting reporting requirements

CFTC Interim Compliant Identifier

IV. Current Market Conditions

Executive Summary

Between May 2nd and July 5th, the 10yr fixed swap rate rose 116 basis points, a 66% increase.

Over the past 13 trading days, the 10yr swap rate has come back nearly 17 basis points as Bernanke sought to ease market tension over tapering QE3.

Despite recent volatility, the 10yr swap rate remains below the 5, 10 and 20yr averages.

Floating rates remain relatively unchanged at near historical lows, with expectations for increases not predicted until late 2014 or early 2015.

The shape of the curve has steepened to 233 basis points (10yr vs. 2yr) as long-term rates rose on tapering expectations while short-term rates remained anchored awaiting future Fed action.

Source: Bloomberg, PNC Derivative Products Group

Fixed Swap Rate Recent History

Current Swap Rates vs. Last Week, 2013 Low and 2013 High

Recent Rise in RatesAfter touching their 2013 lows on May 2nd, fixed swap rates began a rapid ascent higher. Hitting their highs for the year on July 5th, the 2yr, 10yr, and 30yr swap rates had increased 23, 116 and 95 basis points, respectively.

Just looking at the benchmark 10yr rate, during this 47 trading day period we saw the largest percentage increase in the previous 10 years (+65.9%).

The attribution for these gains is fairly straightforward--broadly positive economic data leading to expectations that the Fed will begin (sooner rather than later) to taper the $85B / month QE3 program. If we remove a stated buyer of that much Treasury and mortgage debt, the assumption is the lid that's been kept on longer-term rates may come off. Rates have relented more recently, with the 10yr falling 17 basis points from the July 5th high.

Current Last Week ∆ 2013 Low ∆ 2013 High ∆

2yr Swap vs. 1ML 0.42% 0.39% 3 bps 0.26% 16 bps 0.49% - 7 bps

10yr Swap vs. 1ML 2.75% 2.63% 12 bps 1.76% 99 bps 2.92% - 17 bps

30yr Swap vs. 1ML 3.61% 3.53% 8 bps 2.74% 87 bps 3.69% - 8 bps

2yr Swap vs. 70% 1ML 0.29% 0.27% 2 bps 0.18% 11 bps 0.34% - 5 bps

10yr Swap vs. 70% 1ML 1.93% 1.84% 8 bps 1.23% 69 bps 2.04% - 12 bps

30yr Swap vs. 70% 1ML 2.53% 2.47% 6 bps 1.92% 61 bps 2.58% - 6 bps

2yr Swap vs. SIFMA 0.30% 0.28% 2 bps 0.22% 8 bps 0.34% - 4 bps

10yr Swap vs. SIFMA 2.25% 2.16% 9 bps 1.46% 79 bps 2.39% - 14 bps

30yr Swap vs. SIFMA 3.31% 3.23% 8 bps 2.50% 81 bps 3.38% - 7 bps

Source: Bloomberg, PNC Derivative Products Group

Current Swap Rates and Historical Averages

Consider a Longer TimelineDespite the recent rise in swap rates, it’s useful to view them over a broader period. Compared to historical averages, swap rates are still below their long-term averages. The 10yr swap at 2.75% is still below a 5yr average that includes some of the lowest rates in history. During the start of the financial crisis, we regularly saw the 10yr swap north of 3.50%. Only since the end of 2011 have we consistently seen rates under 2.50%. Over a longer history, a 2.75% 10yr swap is exceptionally low.

Current Swap Rates vs. Historical Averages

Current 3 Year 5 Year 10 Year 20 Year

2yr Swap vs. 1ML 0.42% 0.49% 0.89% 2.41% 3.86%

10yr Swap vs. 1ML 2.75% 2.37% 2.84% 3.88% 5.10%

30yr Swap vs. 1ML 3.61% 3.19% 3.53% 4.40% 5.48%

2yr Swap vs. 70% 1ML 0.29% 0.34% 0.62% 1.69% 2.70%

10yr Swap vs. 70% 1ML 1.93% 1.66% 1.99% 2.72% 3.57%

30yr Swap vs. 70% 1ML 2.53% 2.23% 2.47% 3.08% 3.84%

2yr Swap vs. SIFMA 0.30% 0.62% 1.04% 2.02% 2.13%

10yr Swap vs. SIFMA 2.25% 2.01% 2.39% 3.03% 3.18%

30yr Swap vs. SIFMA 3.31% 2.92% 3.17% 3.66% 3.73%

Source: Bloomberg, PNC Derivative Products Group

6/26/2012 9/26/2012 12/26/2012 3/26/2013 6/26/20130.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Previous 12 Months

10yr Swap vs. 3ML

Fed announces QE3, buys $85B of bonds a month ($45B of Treasuries, $40B of MBS)

Obama is elected for a 2nd term

Congress passes bill averting tax increases and spending cuts

Turmoil in Europe returns with Italian elections

Concerns over Cyprus defaulting on sovereign debt emerges

Cyprus manages to avoid default by shrinking banking system

Consumer confidence reaches highest level since 2008

Bernanke announces potential schedule of tapering --Beginning Sept.

Payroll numbers come in stronger than expected – 195k

12-Month High 2.99%

12-Month Low 1.53%

Average 1.94%

7/22/2003 7/22/2006 7/22/2009 7/22/20120.00%1.00%2.00%3.00%4.00%5.00%6.00%7.00%

Previous 10 Years

10-Year High 5.93%

10-Year Low 1.53%

Average 3.90%

Details

Source: Bloomberg, PNC Derivative Products Group

History of Floating Rates

Current Swap Rates vs. Last Week, 2013 Low and 2013 High, and Historical Averages

LIBOR Remains Near All-Time LowsDespite the recent increase in fixed rates, there has been very little change to short-term rate indices. This is in line with communication from the Fed that tapering is just the first step in a multi-stage process that ends with increasing the Fed Funds Target rates (with other floating benchmarks likely to follow).By the time we arrive at an increase in floating rates, we would expect fixed rates to have already moved higher (as we just found with news of tapering).

7/1/2003 7/1/2006 7/1/2009 7/1/20120.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

1M LIBOR - Past 10 Years

Current Last Week ∆ 2013 Low ∆ 2013 High ∆

1M LIBOR 0.189% 0.192% 0 bps 0.189% 0 bps 0.246% - 6 bps

70% 1M LIBOR 0.133% 0.134% 0 bps 0.132% 0 bps 0.172% - 4 bps

SIFMA 0.050% 0.050% 0 bps 0.050% 0 bps 0.230% - 18 bps

Current 3 Year 5 Year 10 Year 20 Year

1M LIBOR 0.189% 0.232% 0.452% 1.960% 3.306%

70% 1M LIBOR 0.133% 0.162% 0.316% 1.372% 2.314%

SIFMA 0.050% 0.180% 0.420% 1.450% 2.240%

Source: Bloomberg, PNC Derivative Products Group

Expected Future Floating Rates

LIBOR Forward Curve Steepens As reflected in the graph above and Fed Funds

futures, the market believes floating rates will rise sharply from 2015 to 2019; there has been significant movement in the forward curve since May.

Floating rates are expected to remain low near-term, but long-term views have been adjusted significantly to account for a faster ascent once rates begin to rise.

Fed Funds Implied Probability

Meeting Date 0.00% 0.25% 0.50% 0.75% 1%

9/18/2013 56.4% 41.2% 2.4%

12/18/2013 53.1% 42.0% 4.7% 0.2%

4/30/2014 44.1% 43.4% 11.1% 1.3% 0.1%

9/17/2014 31.4% 42.2% 20.4% 5.1% 0.8%

1/28/2015 17.7% 35.0% 28.9% 13.5% 4.0%

7/1/2013 7/1/2015 7/1/2017 7/1/2019 7/1/20210.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

3-Month LIBOR Forward Curve

Current

5/1/2013

7/22/2008

7/22/2003

Source: Bloomberg, PNC Derivative Products Group

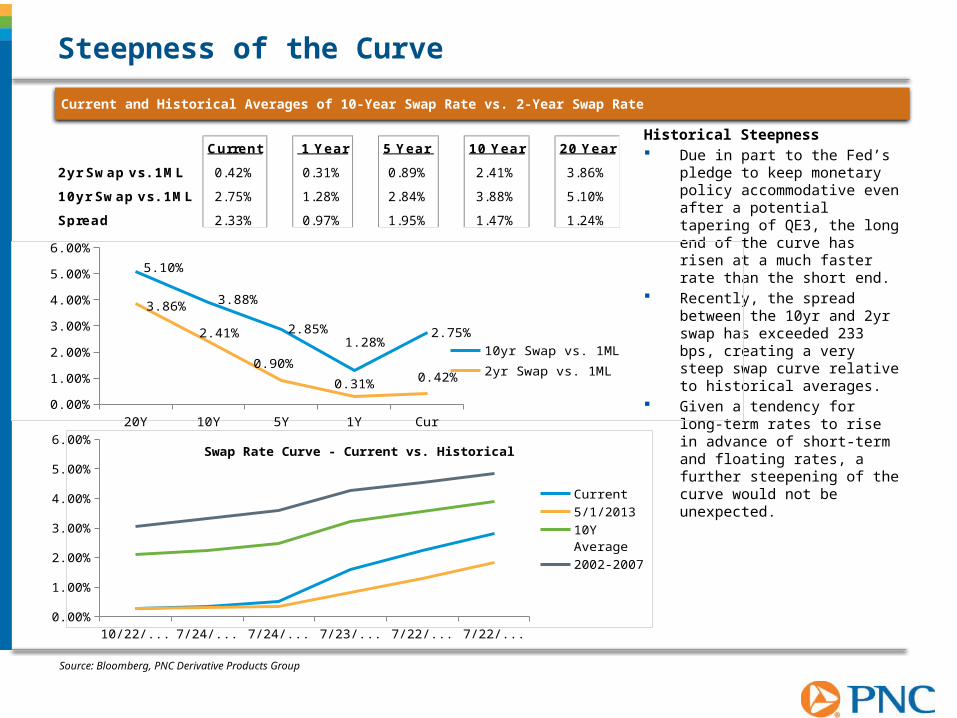

Steepness of the Curve

Current and Historical Averages of 10-Year Swap Rate vs. 2-Year Swap Rate

Historical Steepness Due in part to the Fed’s

pledge to keep monetary policy accommodative even after a potential tapering of QE3, the long end of the curve has risen at a much faster rate than the short end.

Recently, the spread between the 10yr and 2yr swap has exceeded 233 bps, creating a very steep swap curve relative to historical averages.

Given a tendency for long-term rates to rise in advance of short-term and floating rates, a further steepening of the curve would not be unexpected.

Current 1 Year 5 Year 10 Year 20 Year

2yr Swap vs. 1ML 0.42% 0.31% 0.89% 2.41% 3.86%

10yr Swap vs. 1ML 2.75% 1.28% 2.84% 3.88% 5.10%

Spread 2.33% 0.97% 1.95% 1.47% 1.24%

20Y 10Y 5Y 1Y Current0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

5.10%

3.88%

2.85%1.28%

2.75%

3.86%

2.41%

0.90%

0.31% 0.42%

10yr Swap vs. 1ML2yr Swap vs. 1ML

1/1/2013 1/1/2015 1/1/2017 1/1/2019 1/1/2021 1/1/20230.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%Swap Rate Curve - Current vs. Historical

Current

5/1/2013

10Y Average

2002-2007

Source: Bloomberg, PNC Derivative Products Group

Standard Disclosures

Swap Dealer Activities Standard Disclaimer

The information contained herein was generated by an employee of PNC Bank’s swaps trading unit. Such information is not a “research report” nor is it intended to constitute a “research report” (as defined by applicable regulations). The information contained herein is of general market, economic, and political conditions or statistical summaries of financial data and is not an analysis of the price or market for any derivative.

PNC is a registered service mark of The PNC Financial Services Group, Inc. (“PNC”). Foreign exchange and derivative products are obligations of PNC Bank, National Association (“PNC Bank”), Member FDIC and a wholly owned subsidiary of PNC. Foreign exchange and derivative products are not bank deposits and are not FDIC insured, nor are they insured or guaranteed by PNC Bank or any of its subsidiaries or affiliates. This document is intended for informational purposes only, and should not be construed as legal, accounting, tax or other professional advice. You should consult with your own independent legal, accounting, tax and other professional advisors before taking any action based on this information. Under no circumstances should this document or any information contained herein be construed as trading advice or be considered a recommendation or solicitation to buy or sell any products or services or a commitment to enter into any transaction. Eligibility for particular products or services is subject to PNC Bank’s subsequent formal agreement, which will be subject to internal approvals and binding transaction documents. The information contained herein on exchange and interest rates and market indices are gathered from sources PNC Bank believes to be reliable and accurate at the time of publication. Markets do and will change. Therefore, PNC Bank makes no representations or warranties regarding the information’s accuracy, timeliness, or completeness. Further, all performance, returns, prices, or rates are for illustrative purposes only, may not be achievable or indicative of future performance, actual results will vary, and may be adversely affected by exchange rates, interest rates or other factors. Any information, values, estimates, or opinions expressed or implied herein are subject to change without notice. Under no circumstances is PNC Bank liable for any lost profits, lost opportunities, or any indirect, consequential, incidental, special, punitive, or exemplary damages arising out of any use, reliance, or any opinion, estimate or information contained herein or any omission therefrom. PNC Bank, its predecessors, and affiliated companies may, within the previous three years or currently, serve as underwriter, placement agent, market maker, manager, initial purchaser, broker, or deal as principal in any security, derivative or other instruments mentioned in this document. Any such relationship may differ materially from transactions contemplated herein. In addition, PNC Bank, its affiliated companies, shareholders, directors, officers, or employees may at any time acquire, hold or dispose of positions similar or contrary to the positions contemplated herein (including hedging and trading positions) which may impact the performance of a product described in this document. The information contained herein is confidential and may not be disclosed, duplicated, copied, disseminated or distributed by any means to any other person or entity without PNC Bank’s prior written consent.

©2013 The PNC Financial Services Group, Inc. All rights reserved.