preserving rural america’s affordable rental...

TRANSCRIPT

Preserving Rural America’sAffordable Rental Housing: Current Issues

A Report from the National Rural Housing Coalition

October 2004

Preserving Rural America’sAffordable Rental Housing: Current Issues

A Report from the National Rural Housing Coalition

October 2004

Robert A. Rapoza, Executive Secretary

Cornelia Tietke, Principal Author

National Rural Housing Coalition

1250 Eye Street, NW, Suite 902

Washington, DC 20005

(202) 393-5229

The National Rural Housing Coalition (NRHC) is a national membership organization. NRHC is the prin-

cipal advocate for federal policies and programs aimed at promoting better housing and community

facilities in rural America. Since 1969, NRHC has defended the principle that rural people have the right,

regardless of income, to a decent and affordable place to live, clean drinking water, and basic com-

munity services. NRHC sponsors regular conferences at which specific policies and legislative proposals

are developed. Over the years, NRHC has worked to: design new programs and improve existing pro-

grams to improve services to the rural poor; ensure adequate funding levels for rural housing programs;

promote a non-profit delivery system for rural housing and community development

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .i

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

The 515 Program: A Priceless Asset for Rural America . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

Overview of Prepayment Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

• Incentives to Participate in the 515 Program . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

• The Prepayment Process: Evolution to Today’s System . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

• Lack of Funding for Incentives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

• Prepayment Lawsuits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

• Scope of the Problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11

Overview of Recapitalization Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

• Quantifying the Needs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

• Portfolio-wide Recapitalization Obstacles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14

• Overview of RHS’s Recapitalization Approaches . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18

• Prepayment Prevention Incentives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

• Transfers outside of Prepayment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

• 515 Rehabilitation Loans and Other Tools to Recapitalize Properties that Owners Retain . . . . . . .25

Policy and Funding Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27

Sources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29

Contents

Acknowledgements

The following individuals have provided generous amounts of their time and other resources to aid in the

preparation of this report:

Beekman Advisors: Shekar Narasimham and Tom White

Council for Affordable and Rural Housing: Colleen Fisher

Fannie Mae Foundation: Eileen Fitzgerald

Goulston & Storrs: Linda Goldstein and Cynthia Paine

Highland Property Development, LLC: Bill Rice

Larry Goldstein, Consulting: Larry Goldstein

Mercy Housing: Grace Buckley, Stan Keasling, and Chuck Wehrwein

National Affordable Housing Trust: Bob Snow

USDA: Larry Anderson, Don Colburn, Jeff Deiss, Melinda Price, Cynthia Reese Foxworth, Karrie Sayer,

Susan Sherman, George von Pless, and Carl Wagner

Volunteers of America: Pat Sheridan.

This report was made possible by a generous grant from the Fannie Mae Foundation. The National Rural

Housing Coalition wishes to offer special thanks to Laura Lucs, the Fannie Mae Foundation program officer

who oversaw the funding of this report; and to Art Collings of the Housing Assistance Council and Gideon

Anders of the National Housing Law Project for their extensive comments on a draft of the report.

The views expressed in this report are those of the National Rural Housing Coalition and do not necessarily

represent the views of any of the above individuals or their employers. The National Rural Housing Coalition

is responsible for errors of fact and welcomes any comments on this report.

Cover Photo by: Thurber Photographic

Report design: amp&rsand graphic design, inc.

i

The U.S. Department of Agriculture’s (USDA’s)Section 515 Rural Rental Housing Program providessafe and affordable homes to almost half a million ofAmerica’s most vulnerable residents: elderly women,people with disabilities, and mothers with children, allof whom on average earn less than $10,000 a year. Atits peak in the early 1980s, the program created about1,000 new properties a year. Since the mid-1990s,however, the program has faced severe budget cut-backs, limiting USDA’s ability to finance much-neededrehabilitation of existing properties and the construc-tion of new properties to serve the 900,000 ruralrenters who live in substandard housing.

In the face of the shrinking 515 budget, USDAhas undertaken creative measures to improve theefficiency of its program delivery and to facilitate theinfusion of capital from state and private sources.However, while these third-party sources make a valu-able contribution to the preservation of the 515portfolio, they are not a substitute for federal funds—including 515 loans, rental assistance, and grants suchas CDBG and HOME—which provide the deep andconsistent subsidies necessary to house families withincomes well below the poverty line.

The purpose of this report is to demonstrate theimportance of the Section 515 program, explain theobstacles to preserving its almost 16,400 properties,highlight local preservation efforts, and recommendchanges to maintain America’s rural rental housingsupply.

Background

In 1962, Congress amended Title V of theHousing Act of 1949 to create the Section 515 RuralRental Housing Program. Originally administered bythe USDA Farmers Home Administration (FmHA),

the program is run today by FmHA’s successor, RuralDevelopment (RD), through the Rural HousingService (RHS). This Agency delivers the programthrough its Washington, D.C.-based national officeand RD’s state-based field offices.

The Section 515 program makes subsidizedloans—1 percent interest rate, 30-year term, 50-yearamortization—to developers to build, acquire, andrehabilitate rural rental housing. About 75 percent ofthese loans are further subsidized by RHS’s Section521 Rental Assistance (RA) program and theDepartment of Housing and Urban Development’s(HUD’s) Section 8 program, both of which providerent subsidies to ensure that tenants pay no more than30 percent of their income toward rent. Fifty-sevenpercent of Section 515 households are elderly, handi-capped, or disabled; 26 percent are headed by personsof color; and 73 percent are headed by women. Theaverage annual household income is $9,168.

Since its inception, the Section 515 program hasfinanced more than 526,000 units and today servesalmost 475,000 families. During the program’s peakyears, 1979–1985, annual funding levels rangedbetween $864 million and $954 million, producing atotal of 9,622 loans. Since 1995, however, annualfunding levels have never exceeded $184 million, andfrom 1999–2004 they have hovered between $113 and$119 million per year — far below a level that couldmeet demonstrated need. Demand for Section 515loans and rental assistance funds consistently exceedsavailability by wide margins.

Challenges

Recent administrations and Congress have notprovided adequate Section 515 or rental assistancefunds to rehabilitate the portfolio, deliver sufficient

Executive Summary

ii Preserving Rural America’s Affordable Rental Housing

long-term preservation incentives, or protect tenantsfrom rent overburden. As the Section 515 budgetshrinks, RHS finds itself struggling with two majorpreservation challenges.

The first is the increasing number of owners whowish to prepay their loans, a trend that is occurringwhile the program has started to lose more units toprepayment than it produces. Congress created a loanprepayment regulation process between 1979 and1992—after RHS made the bulk of 515 loans—thatintroduced restrictions on the right to prepay. It alsocreated prepayment prevention incentives for ownersbased on the amount of equity in their properties.Unfortunately, RHS has not had sufficient 515 orrental assistance funding to meet the demand forincentives. As a result, it currently faces numerous law-suits brought by owners seeking the right to prepay orcompensation for not being allowed to prepay. Recentrulings on two key cases, Franconia Associates et al. v.United States and Kimberly Associates v. United Statesmay have significant consequences. The Franconiadecision requires the government to pay damages forrestricting the right to prepay. The Kimberly decisionopens the way for owners in some states to use theirstate property laws to exit the Section 515 program.

The second problem arises from the aging anddeterioration of the properties in the loan portfolio.Some 89 percent of these properties are at least 10years old, and 64 percent are at least 15 years old.Their major infrastructure systems are at or near obso-lescence and need rehabilitation or replacement.

The way to meet this challenge is through recap-italization — an injection of new debt or equity tofinance repairs and upgrades. However, Section 515and rental assistance funding limitations allow fewerthan 3 percent of all Section 515 units to be recapital-ized each year. Because RHS’s recapitalization toolstypically result in increased debt, they rely on rentalassistance to protect tenants from rent overburden.Thus they do not lend themselves to the more than4,000 properties that do not have full rental assistancecoverage (they are said to have “partial rental assis-

tance”) or to projects that cannot afford new debt.Consequently, such properties do not get recapitalized.

RHS has commissioned a study to quantify therecapitalization needs of the 515 portfolio as well as torecommend innovative preservation strategies. RHSexpects to release the report during the Fall of 2004.Creation of a comprehensive, fully funded recapitaliza-tion strategy is critical for both owners and tenants,and for the future of the Section 515 loan portfolio.Such a strategy must overcome five obstacles:

1. Lack of capital to rehabilitate the property:Project reserves at most properties are inade-quate and the Section 515 program cannotmeet the demand for rehab loans. Bonds,including tax-exempt bonds plus 4-percentLow Income Housing Tax Credits(LIHTCs), and private bank debt, whileavailable, work best for properties larger thanthe typical Section 515 complex. Small andisolated properties need deep subsidies such asthose provided by the 9-percent Low-IncomeHousing Tax Credit program and HUD’sCommunity Development Block Grant(CDBG) and HOME programs. These threeprograms are vastly oversubscribed.

2. Limited revenue opportunities: Many develop-ers and third-party funders find theopportunity costs of participating in 515deals too high. The average property has 27units, which does not allow for theeconomies of scale needed to create ade-quate profit for many potential participants.In addition, the 515 program allows devel-oper fees only when a deal includes taxcredits; it caps return on investment at 8percent of original equity; and it does notallow nonprofits a return on equity. Finally,management fees vary widely by state.

3. Lack of adequate rental assistance and Section 8subsidies: As discussed, rent subsidies ensurethat eligible tenants spend no more than 30

Current Issues iii

percent of their income for rent. Recapital-ization typically results in increased project debt and thus in increased rents.Without rental assistance, tenants mustshoulder the full weight of a rent increase.More than 100,000 Section 515 units do nothave rental assistance subsidies, making themextremely difficult to recapitalize withoutrent-overburdening their tenants.

4. Unsustainably low rents: The average Section515 rent is $314 per unit per month, includ-ing both the tenant’s contribution and anyrental assistance. This low rental incomeresults in a lack of capital for rehabilitationand is an indicator of potentially large capitalneeds, particularly at properties lacking fullrental assistance subsidy. Two factors havekept rents low: (1) some rural markets do notsupport higher rents; and (2) many RHSoffices have denied rent increase requests,both to avoid increasing the per-unit cost ofrental assistance and, at properties with partialRA, to protect unsubsidized tenants from rentoverburden.

5. Phantom income and exit taxes: Many ownersof older 515 properties must pay taxes onphantom income, and their properties do notgenerate enough revenue to compensate forthese tax payments. At the same time, owners’exit options are limited. If they try to sell theirproperties and take depreciation in excess oftheir original investments, they may face exittaxes greater than their equity. Thus they donot sell, nor do they have the financial where-withal for recapitalization, and the propertiesdeteriorate. The Tax Issues and PreservationTask Forces of the Millennial HousingCommission estimate that if a tax incentivewere created to allow exit tax relief at time ofsale to an affordable housing preservationowner, as many as 68,000 Section 515 unitscould be preserved.

Recommendations

The biggest problem that RHS faces in preserv-ing the Section 515 portfolio is chronically inadequateprogram funding. However, RHS could make itsrecapitalization processes more efficient and equitable,and it should also take steps to protect properties leftout of its current recapitalization strategy. The follow-ing recommendations address the Section 515portfolio’s most pressing preservation needs:

1. RHS should create and Congress should fully funda national preservation plan for the 515 portfoliothat addresses prepayment, transfers, and rehabil-itation of properties that do not changeownership. The plan should also address thoseproperties currently not well served by RHS’srecapitalization tools: small, isolated properties;those in poor markets that cannot afford a rentincrease; and those with partial rental assistance.

For several years, the National Rural HousingCoalition has recommended a minimumannual Section 515 funding level of $250 mil-lion to address the recapitalization needs andto add enough new units to replace those lostto prepayment. In addition to this recommen-dation, the Coalition also advocates theprovision of rental assistance to all rent-over-burdened tenants; grant funding, such asCDBG or HOME set-asides, to recapitalizeproperties that cannot afford new debt; andbudget-based rents for performing propertiesin markets where market-based rents areinsufficient to cover operating costs.

2. Congress should provide rent vouchers for tenantsdisplaced as a result of prepayment lawsuits. Inone recent lawsuit, for example, tenants weredisplaced as RHS and the plaintiff workedthrough their settlement agreement. Tenantsshould be protected from rent overburdenresulting from legal decisions.

iv Preserving Rural America’s Affordable Rental Housing

3. Congress should provide exit tax relief for Section515 owners who transfer their properties to pur-chasers who will preserve long-term affordability.As noted above, this step could preserve asmany as 68,000 Section 515 units.

4. Congress should create a permanent set-aside of9-percent Low Income Housing Tax Credits forSection 515 preservation. These LIHTCs pro-vide the deep subsidy necessary to preserveproperties that cannot afford rent increases,and they drive many Section 515 preservationtransactions. However, they are oversub-scribed and without a set-aside will not beavailable in the numerous states that do notprioritize the housing needs of their rural resi-dents through their tax credit qualifiedallocation plans. A 10-percent set-aside wouldbe appropriate.

5. RHS should provide field staff with better guid-ance on how to protect minority residents from theadverse impacts of prepayment. While RHS hasprocedures to protect minority residents,many of RD’s field staff are unfamiliar withthem. They need additional training.

6. Congress should open the prepayment transferprocess to low-income housing tax credit partner-ships with nonprofit general partners. Thischange would allow tax credit funding forpreservation transfers in cases where RHSmandates the sale of a property to a nonprofitto protect minority tenants.

7. RHS should allow nonprofit purchasers to receivea return on any equity they bring to the property,including government funds that do not requirerepayment. This change would put nonprofitpurchasers on an equal footing with for-profitpurchasers that bring equity to a 515 transac-tion. It would also give nonprofits anothertool to finance affordable housing.

8. RHS should streamline its transfer process andcodify it in regulations. The more RHS can doto standardize and streamline the process, themore developers will be willing to participatein it. RHS could start by imposing uniformnationwide management fees and timelinesfor processing transfer requests. It should alsoreplace the current Administrative Noticeswith comprehensive regulations. Finally, itshould make regulatory and automationchanges that facilitate the consolidation ofloans and properties under one managementstructure, so that properties can benefit fromeconomies of scale to minimize developmentand operating costs.

9. Fannie Mae and Freddie Mac should facilitatepreservation of the Section 515 portfolio. Toimprove the process of purchasing 515 preser-vation loans, they should standardizepaperwork; minimize participation fees; mini-mize loan interest rates and maximize loanterms; encourage their lenders to participate;and work with more nonprofit preservationorganizations. They should also commit topurchasing Low Income Housing Tax Creditsused to finance 515 preservation deals.

■

The Section 515 Rural Rental HousingProgram — the principal source of affordable housingfor low-income rural renters — is a national asset. Itdeserves stronger support from Congress and moreresourceful administration by the Department ofAgriculture. The recommendations above, if promptlyacted upon, will recapitalize the Section 515 loan port-folio, make the program more attractive to ruralhousing developers, and — most important — keepfaith with the half-million rural Americans who relyon the Section 515 program to put a sound roof overtheir heads at an affordable cost.

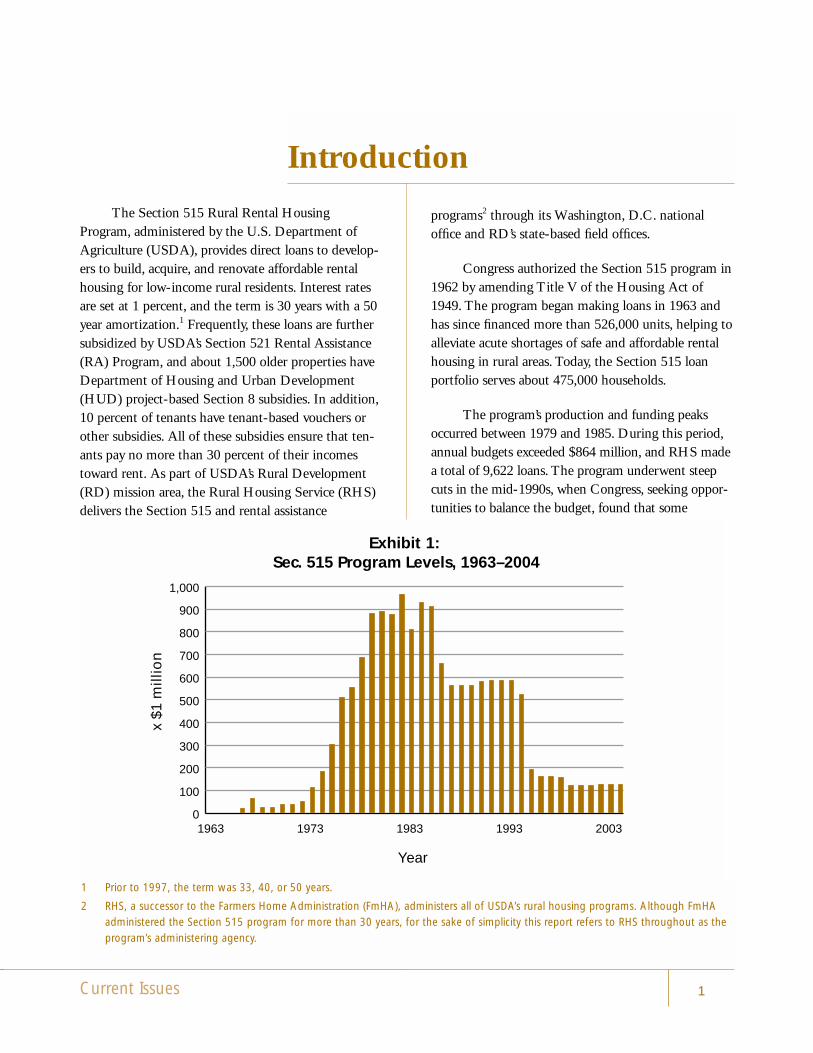

Current Issues 1

The Section 515 Rural Rental HousingProgram, administered by the U.S. Department ofAgriculture (USDA), provides direct loans to develop-ers to build, acquire, and renovate affordable rentalhousing for low-income rural residents. Interest ratesare set at 1 percent, and the term is 30 years with a 50year amortization.1 Frequently, these loans are furthersubsidized by USDA’s Section 521 Rental Assistance(RA) Program, and about 1,500 older properties haveDepartment of Housing and Urban Development(HUD) project-based Section 8 subsidies. In addition,10 percent of tenants have tenant-based vouchers orother subsidies. All of these subsidies ensure that ten-ants pay no more than 30 percent of their incomestoward rent. As part of USDA’s Rural Development(RD) mission area, the Rural Housing Service (RHS)delivers the Section 515 and rental assistance

programs2 through its Washington, D.C. nationaloffice and RD’s state-based field offices.

Congress authorized the Section 515 program in1962 by amending Title V of the Housing Act of1949. The program began making loans in 1963 andhas since financed more than 526,000 units, helping toalleviate acute shortages of safe and affordable rentalhousing in rural areas. Today, the Section 515 loanportfolio serves about 475,000 households.

The program’s production and funding peaksoccurred between 1979 and 1985. During this period,annual budgets exceeded $864 million, and RHS madea total of 9,622 loans. The program underwent steepcuts in the mid-1990s, when Congress, seeking oppor-tunities to balance the budget, found that some

Introduction

Exhibit 1: Sec. 515 Program Levels, 1963–2004

0

100

200

300

400

500

600

700

800

900

1,000

20031993198319731963

x $1

mill

ion

Year

1 Prior to 1997, the term was 33, 40, or 50 years.

2 RHS, a successor to the Farmers Home Administration (FmHA), administers all of USDA’s rural housing programs. Although FmHAadministered the Section 515 program for more than 30 years, for the sake of simplicity this report refers to RHS throughout as theprogram’s administering agency.

2 Preserving Rural America’s Affordable Rental Housing

property owners had defrauded the program. AlthoughRHS eliminated these abuses and made the regulatorychanges that Congress mandated, Congress neverrestored the program’s funding. Since 1999, the Section515 budget has hovered between $113 million and$119 million. Because of reduced funding, productionof new units has almost halted. In 2003, for the firsttime in its history, the program lost more than twice asmany units to prepayment (1,848) as it produced(826).3

Given the significantly reduced funding levelsand its consequent inability to build new units, RHSmust preserve the assets it has developed. However, itfaces major obstacles. Numerous owners wish to prepaytheir loans. Statutory restrictions impede their ability todo so, but they are also eligible for RHS-funded mone-tary incentives to remain in the 515 program. Inaddition, 89 percent of 515 properties are 10 years oldor older and in need of significant rehabilitation. RHSlacks sufficient funding to meet the demand either forincentives or rehabilitation. Its preservation effortsrehabilitate only 3 percent of all units in the portfolioeach year, and it now faces lawsuits from owners whowant compensation and/or the right to prepay.

Exhibit 2:Section 515 Descriptive Statistics4

Size

Total properties...................................................16,432Total units.........................................................450,880Total households ..............................................418,508Total tenants ....................................................474,371Average number of units per property ......................27Occupancy Rate.....................................................93%

Age

Properties 10 years old or older .............................89%Properties 15 years old or older .............................64%

Tenants

Average annual income......................................$9,168Average annual income of RA tenants...............$7,224Elderly households .................................................36%Handicapped or disabled households ....................21%Race by household

White..............................................................74%African American ............................................17%Hispanic/Latino..................................................7%Native American................................................1%Asian or Pacific Islander .................................<1%

Gender by householdSingle female households ...............................44%Female-headed households.............................29%Single male households...................................15%Male-headed households................................12%

Rent Overburdened Households .......................20%

Pay 30-40% of income for rent ........................8%Pay 41-50% of income for rent ........................5%Pay 51% of income or more for rent................7%

Distribution of Rental Assistance by Household

No rent subsidy ...............................................25%Section 521 rental assistance ..........................58%Section 8 vouchers............................................8%Project-based Section 8.....................................7%Other rent subsidy.............................................2%

Portfolio Management

Number of properties in inventory ........................8Loan delinquency rate....................................1.6%

3 Housing Assistance Council, “About Rural Rental Housing Prepayment and Preservation,” 2 (accessed March 30, 2004); availablefrom http://www.ruralhome.org/pubs/infoshts/inforpreserv.htm.

4 All statistics except Age and Portfolio Management are from U.S. Department of Agriculture, Rural Development, Rural HousingService, 2003 Multi-Family Housing Annual Fair Housing Occupancy Report (Washington, D.C.: U.S. Department of Agriculture, May2003). Age and Portfolio Management data are from U.S. Department of Agriculture, Rural Development, Rural Housing Service,Office of Rural Housing Preservation, untitled PowerPoint presentation, January 2004.

Current Issues 3

The nation’s 16,432 Section 515 properties constitute a priceless asset for rural America, wheremore than 900,000 renters live in moderately orseverely inadequate housing, and 1.9 million are rent-overburdened.5 These 515 properties offer decent, safe,modestly priced housing to almost half a million ofAmerica’s most vulnerable residents: the elderly, peoplewith disabilities, people of color, and women.

The average annual tenant income in 2003 was$9,168. Seventy-five percent of tenants received rentalassistance subsidy, either through project-based rentalassistance or Section 8 or through vouchers. Althoughrents were extremely low, averaging $314 per unit permonth, 20 percent of tenants were nevertheless rent-overburdened, and 7 percent paid more than half theirincome toward rent.

In many rural communities, Section 515 housingis the only affordable and sound option. It is an essen-tial resource for elderly people, single-parent families,the disabled, and other less mobile residents. It pro-vides them with an alternative to living alone inhousing they cannot maintain; living in overcrowded

or other substandard conditions; living in their cars; ormoving to a nursing home.

As Betty McAfee of Belfast, Maine, wrote toRHS in 1995, when she was 82:

Before moving to [the local Section 515property] I lived alone in a two-roomcabin — no foundation, no plumbing andheated by a small wood-burning stove. I hada long walk to the rural mail box over arough dirt lane. If this [515] complex didnot exist, I would still be living there. Manyother low-income elderly people in Maineare living under those conditions, or worse.

Section 515 housing is generally well managed.Property managers often invest much of their own freetime and creativity in providing tenants with a safe and cohesive community. They organize social get-togethers and, at some elderly properties, they arrangefor services such as health screenings and grocery andpharmaceutical delivery.6 The 515 portfolio is alsofinancially sound, with a loan delinquency rate of just1.6 percent and only eight properties in inventory.7 Itis an asset worth saving.

The 515 Program: A PricelessAsset for Rural America

5 These tenants pay more than 30 percent of their incomes toward rent.

6 U.S. Department of Agriculture, Rural Development, Rural Housing Service, Rural Housing Service 1997 Progress Report (Washington,D.C.: U.S. Department of Agriculture, 1998),12, 24.

7 Rural Housing Service, Office of Rural Housing Preservation, untitled PowerPoint presentation, January 2004.

4 Preserving Rural America’s Affordable Rental Housing

Current Issues 5

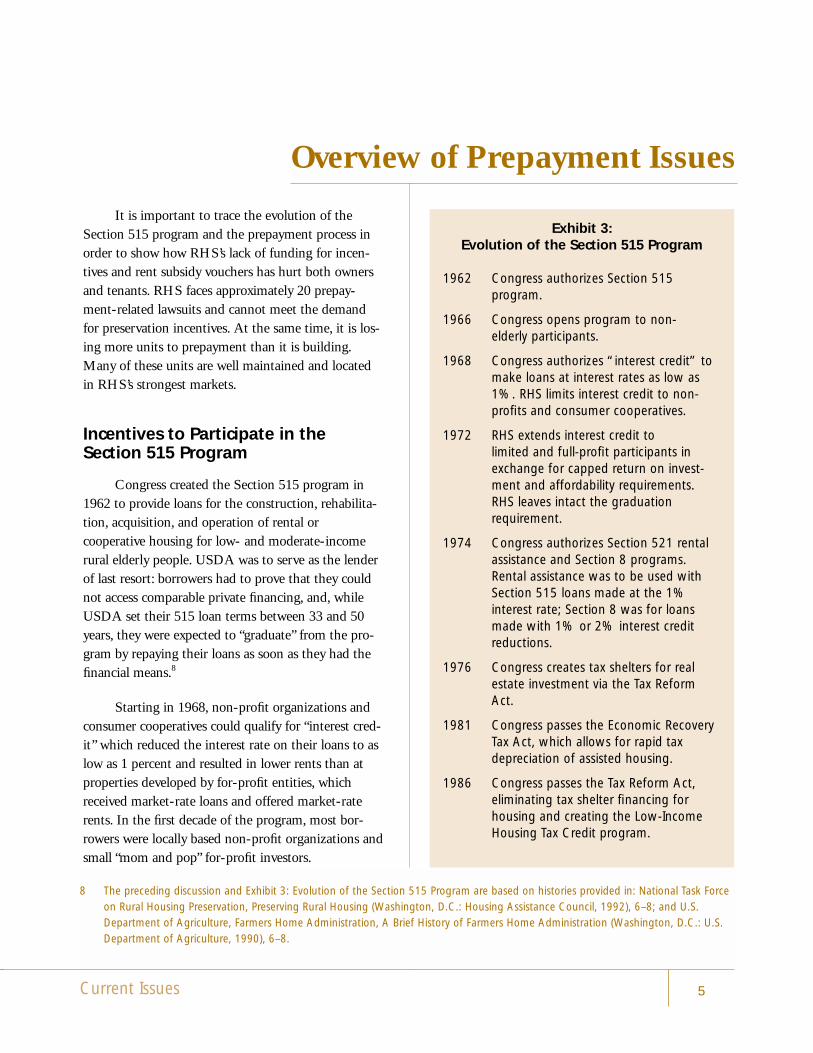

It is important to trace the evolution of theSection 515 program and the prepayment process inorder to show how RHS’s lack of funding for incen-tives and rent subsidy vouchers has hurt both ownersand tenants. RHS faces approximately 20 prepay-ment-related lawsuits and cannot meet the demandfor preservation incentives. At the same time, it is los-ing more units to prepayment than it is building.Many of these units are well maintained and locatedin RHS’s strongest markets.

Incentives to Participate in theSection 515 Program

Congress created the Section 515 program in1962 to provide loans for the construction, rehabilita-tion, acquisition, and operation of rental orcooperative housing for low- and moderate-incomerural elderly people. USDA was to serve as the lenderof last resort: borrowers had to prove that they couldnot access comparable private financing, and, whileUSDA set their 515 loan terms between 33 and 50years, they were expected to “graduate” from the pro-gram by repaying their loans as soon as they had thefinancial means.8

Starting in 1968, non-profit organizations andconsumer cooperatives could qualify for “interest cred-it” which reduced the interest rate on their loans to aslow as 1 percent and resulted in lower rents than atproperties developed by for-profit entities, whichreceived market-rate loans and offered market-raterents. In the first decade of the program, most bor-rowers were locally based non-profit organizations andsmall “mom and pop” for-profit investors.

Overview of Prepayment Issues

Exhibit 3:Evolution of the Section 515 Program

1962 Congress authorizes Section 515 program.

1966 Congress opens program to non-elderly participants.

1968 Congress authorizes “interest credit” tomake loans at interest rates as low as1%. RHS limits interest credit to non-profits and consumer cooperatives.

1972 RHS extends interest credit to limited and full-profit participants inexchange for capped return on invest-ment and affordability requirements.RHS leaves intact the graduation requirement.

1974 Congress authorizes Section 521 rentalassistance and Section 8 programs.Rental assistance was to be used withSection 515 loans made at the 1% interest rate; Section 8 was for loansmade with 1% or 2% interest creditreductions.

1976 Congress creates tax shelters for realestate investment via the Tax ReformAct.

1981 Congress passes the Economic RecoveryTax Act, which allows for rapid taxdepreciation of assisted housing.

1986 Congress passes the Tax Reform Act,eliminating tax shelter financing forhousing and creating the Low-IncomeHousing Tax Credit program.

8 The preceding discussion and Exhibit 3: Evolution of the Section 515 Program are based on histories provided in: National Task Forceon Rural Housing Preservation, Preserving Rural Housing (Washington, D.C.: Housing Assistance Council, 1992), 6–8; and U.S.Department of Agriculture, Farmers Home Administration, A Brief History of Farmers Home Administration (Washington, D.C.: U.S.Department of Agriculture, 1990), 6–8.

6 Preserving Rural America’s Affordable Rental Housing

However, the borrower profile changed whenRHS revised its no-credit-elsewhere test to provideinterest credit to limited- and full-profit borrowers,and when Congress introduced housing and real estatetax incentives. Because tax incentives are accessedthrough partnership structures, today, partnershipsown about 90 percent of all Section 515 properties.9

The exhibit on the previous page shows a series ofprogrammatic and legislative initiatives that trans-formed the borrower profile. While both Congress andRHS offered substantial incentives for private-sectorparticipation in the Section 515 program, RHS didnot in return eliminate the graduation requirement,which set the stage for today’s prepayment problems,discussed at length in the next sections.

With passage of the Tax Reform Act in 1986,Congress changed direction, eliminating tax sheltersand replacing them with the Low-Income HousingTax Credit (LIHTC) program. According to the TaxIssues Task Force of the Millennial Housing Com-mission, “It is clear that [prior to 1986] investment inthe [HUD and RHS 515] assisted stock was pursuedlargely, perhaps almost exclusively, because of taxbenefits. It is also clear that the actual tax benefitsreceived by many investors were typically less thanwere anticipated at the time the investments weremade.”10

Although the 1986 Act left many investors with-out their anticipated tax benefits, the LIHTC programit created transformed the funding of low-incomerental housing in the United States. The LIHTC pro-gram is responsible for creating approximately 50 to 70percent of all new “contractually affordable” housingeach year.11

The program works by allocating tax credits todevelopment partnerships, which then sell the creditsto investors and use the proceeds to inject equity intotheir affordable housing properties. There are twokinds of credits: 9 percent and 4 percent. Nine percentcredits offer a deeper equity subsidy, and developersusually combine them with hard debt, either subsi-dized or market-rate. Many of the first 9-percent dealswere coupled with Section 515 loans.12 A developermay receive 4-percent credits only as a result of receiv-ing a tax-exempt bond allocation. LIHTCs havebecome essential tools to finance Section 515 newconstruction and rehabilitation.

The LIHTC program allows investors to exitafter 15 years, once all tax benefits have expired andthe affordability period has ended. Thus, like a consid-erable number of pre-1986 owners, many of the earlySection 515 LIHTC investors have received all taxbenefits from participation and would like to leave the515 program. They face numerous obstacles, however,including the prepayment process outlined in the fol-lowing section and the portfolio-wide preservationobstacles outlined in the Overview of RecapitalizationIssues.

The Prepayment Process: Evolution toToday’s System

In the late 1970s, RHS found itself balancingcompeting pressures. Rising property values in ruralareas enabled a growing number of owners to prepaytheir loans, and, given the Agency’s history of enforc-ing the graduation requirement, the owners expectedto do so. As a result, there was a sharp increase in pre-payment activity, with 55 percent of all prepayments

9 U.S. General Accounting Office, “Prepayment Potential and Long-Term Rehabilitations Needs for Section 515 Properties,” Report tothe Chairwoman, Subcommittee on Housing and Community Opportunity, Committee on Financial Services House ofRepresentatives (GAO-02-397: May 2002), 5.

10 Charles S. Wilkins, Jr., “Background Paper: Preservation Tax Incentive,” Millennial Housing Commission Tax Issues Task Force, 1(accessed March 30, 2004); available from http://www.mhc.gov/papers/bgtpr.doc.

11 David A. Smith, “The Low Income Housing Tax Credit Effectiveness and Efficiency: A Presentation of the Issues,” March 4, 2002, 4(accessed March 30, 2004); available from http://www.mhc.gov/papers/lihtc.doc.

12 Ibid., 3.

Current Issues 7

from program inception to 1979 occurring between1977 and 1979.13

At the same time, tenant advocates began mobi-lizing to halt this trend, since prepayments often led todramatically increased rents and the eviction of verylow-income tenants. Advocates argued that owners hadreaped tax and other benefits at the taxpayers’ expense,and that they should not be allowed to profit evenmore by converting their properties to market use.

Congress responded by passing the Housing andCommunity Development Amendments of 1979 (P.L.96-153). This law requires that properties with Section515 loans made on or after December 21, 1979, servelow-income residents for 15 or 20 years, depending onthe level of Section 515 interest rate subsidy. Congressalso placed prepayment restrictions on existing, pre-1979 loans, but repealed these restrictions in 1980.

As the tax benefits to participating in the 515program began to expire during the 1980s, more own-ers prepaid. The resulting displacement of largenumbers of tenants, many of them elderly, generatedmuch publicity and controversy. In response, Congressmandated a moratorium on prepayments in October1986, which remained in effect until the EmergencyLow-Income Housing Preservation Act (ELIHPA,P.L. 100-242) became law in 1988. While creatingfinancial incentives for borrowers with pre-’79 loansnot to prepay, ELIHPA also restricted their prepay-ment rights, a provision that directly contradictedRHS’s mandate that these owners graduate as soon asfinancially feasible.14

To eliminate the prepayment issue for all newhousing, Congress passed the Department of Housingand Urban Development Reform Act of 1989 (P.L.101-235), precluding prepayment for all Section 515loans made on or after December 15, 1989. Congressthen extended prepayment prevention incentives to

borrowers with loans made between December 21,1979 and December 14, 1989 through the CommunityDevelopment Act of 1992 (P.L. 102-550).

Exhibit 4 on the following page shows RHS’sframework to process prepayment requests, whichcombines statutory and regulatory requirements. Whatthis process means for owners qualified to prepay isthat (a) they may be able to receive financial incentivesto stay in the program; (b) they may be able to prepaywithout any further obligations; (c) they may berequired to carry out the remainder of their restrictiveuse provisions or protect the existing tenants, afterwhich point they can do what they want with theproperties; and (d) they may be required to sell at fairmarket value to a nonprofit or public agency. Thus,eventually, owners who do not accept incentives andare not required to sell may convert their properties tomarket-rate use.

Lack of Funding for Incentives

Preservation incentives include equity loans;increased return on investment; Section 8 rents inexcess of the amount needed to meet annual operating,maintenance, debt service, and reserve expenses;increased rental assistance; and interest rate write-downs to 1 percent and/or loan reamortization overthe remaining life of the property. Demand for incen-tives always exceeds supply, and owners have waited aslong as eight years to receive the incentives RHSpromised them. From 1989 to 1994, RHS’s total equi-ty loans ranged between $11 and $27 million annually.In 1995, however, when appropriations for the 515program dropped from $512 million to $183 million,the amount of funding for prepayment equity fell aswell. Since this time, the Agency has made approxi-mately $5.4 million in prepayment prevention equityloans each year, thereby preserving approximately1,000 units annually.15

13 National Task Force on Rural Housing Preservation, p. 8.

14 Ibid., p. 9.

15 In Fiscal Year 2003, RHS provided a total of $21.5 million in equity loans. However, only $5.8 million was for prepayment preventionincentives. RHS also made $10.5 million in equity loans to transfer 20 Idaho properties to a new owner, per the settlement agree-ment of Atwood-Liesman v. United States. Finally, RHS made $5.2 million in equity loans to support innovative transfers outside ofthe prepayment process.

8 Preserving Rural America’s Affordable Rental Housing

Exhibit 4:RHS’s Prepayment Process

1. Borrowers with loans approved on or after December 15, 1989 may not prepay their loans. These borrow-ers must maintain their loans for the full term: 50 years for loans made before 1997; 30 years for loansmade thereafter. Exception: properties that RHS deems unnecessary. Approximately 36 percent of the prop-erties were financed after this date; most have 50 year terms.

2. Borrowers with loans approved on or prior to December 14, 1989 that are not currently subject to a userestriction and who have not previously accepted prepayment prevention incentives (“unrestricted proper-ties”), may request to prepay their loans. Currently, this category includes most loans made through 1984and some made through 1989. Borrowers must submit their request at least 180 days before they wish toprepay. Upon receiving the request, RHS notifies the current tenants and other stakeholders, and evaluatesthe borrower’s financial ability to prepay. If the borrower can prepay, RHS makes an incentive offer basedon the property’s equity. The incentive offer may include: an equity loan; increased return on investment;Section 8 rents in excess of the amount needed to meet annual operating, maintenance, debt service, andreserve expenses; increased rental assistance; an interest rate write-down to 1 percent; and a loan reamor-tization over the remaining life of the property.

If the borrower accepts the offer, RHS obligates funding for the incentives and the owner agrees to a 20-year restrictive use provision. If the borrower rejects the offer, RHS determines whether the project is stillneeded, assessing: (1) whether current tenants will have access to adequate housing at the same rent; and(2) whether prepayment will result in a material impact on minorities either at the project or in the marketarea. If the property is not needed under either criterion, the borrower may prepay without restrictions.

If housing opportunities for minorities will not be affected, but there is a need for the housing, the borrower may prepay. The borrower must agree to maintain the housing for the current eligible tenantsfor the life of the project, until these tenants vacate the property, or until they lose eligibility for RHS assistance.

If housing opportunities for minorities will be affected, the borrower must agree to sell the property at fairmarket value to a qualified non-profit or public agency. If a qualified buyer is not found within 180 days,the borrower may prepay without restrictions. There have been about a dozen cases in which RHSrequired sale to a non-profit, and in half of them, no non-profit was found and the owner prepaid. If aqualified buyer is found within 180 days but there are insufficient federal appropriations to finance thetransfer, the borrower may prepay without restrictions. To date, RHS has had sufficient funds to financethese sales.

3. Borrowers with loans made on or prior to December 15, 1989, that have restrictive use provisions(“restricted properties”) may request to prepay their loans. Currently, this category includes most of theapproximately 5,500 loans made between 1985 and 1989. RHS may not offer these borrowers incentivesto remain in the program. Instead, RHS must ask whether the borrower will sell the property to a qualifiednon-profit or public agency. If the borrower declines, RHS must determine whether the project is needed,based on the criteria explained above. If it is not needed, the borrower may prepay by carrying out theremaining years of restrictions. If there is an impact on minorities, then the borrower must offer to sell theproperty to a qualified non-profit or public agency at the end of the remaining use restrictions. If there isno impact on minorities, but there is a need for the housing, then the borrower must follow the sametenant protection requirements as for a needed, unrestricted loan.

Current Issues 9

Today, the waiting time for Section 515 prepay-ment prevention equity loans and incentive rentalassistance is about a year, the shortest it has been sinceat least 1990. It is important to note, however, thatthis waiting time is in no way predictive of futuretimes. RHS has met some of the demand for equity bysteering owners into its loan transfer process, whichrelies mainly on third-party funds and works for prop-erties that have full rental assistance subsidy. Thetransfer process is explained in more detail in theOverview of Recapitalization Issues section of thisreport. In addition, demand has been depressed inrecent years because RHS has continued to discourageprepayments and owners are pessimistic about thelikelihood of receiving incentives. This situation maychange, however, as new owners become eligible toprepay and a number of prepayment lawsuits againstRHS reach their conclusions. Supply is also uncertainbecause the amount of rental assistance Congressappropriates varies from year to year. For example, inFY 2004, it cut the amount of “debt forgiveness” RAdown to $3 million, from its long-standing level of$5.9 million. RHS uses debt forgiveness RA to sup-plement equity loans. It is vital to making prepaymentprevention incentives work for properties that do nothave full RA coverage.

Prepayment Lawsuits

RHS faces approximately 20 lawsuits arisingfrom the change in the graduation policy, therescinding of the automatic prepayment right, andthe lack of funding for incentives. Some of these suitshave been brought by tenant advocates who challengeRHS’s handling of prepayment requests and prepaidloans. Others have been brought by property ownerswho challenge the applicability of ELIHPA to theright to prepay; try to circumvent ELIHPA by seek-ing quiet (unrestricted) title to their property whenthe government rejects their tender of the balance ofthe loan; and seek damages for ELIHPA’s impair-ment of the right to prepay. Recently, federal courtshanded down rulings on two high-profile cases,

Franconia Associates et al. v. United States andKimberly Associates v. United States.

In the Franconia case, the plaintiffs argued thatthe government’s restriction of the right to prepay—imposed after the 515 loans were made—constituted abreech of contract and a taking of property. OnAugust 30, 2004, the U.S. Court of Federal Claimsruled that the federal government breached its mort-gage contracts with owners of 37 of 42 propertiesnamed in the suit. Some 11,500 Section 515 proper-ties financed before December 15, 1989 could beaffected by this ruling.

The Court found in part that the owners wouldnot have sought a loan if the prepayment restrictionsapplied by Congress were in effect when the loan wasmade. Further, the opinion states that RHS did notadequately fund incentives to owners for extensions oflong-term use and that the delays in gaining incentiveswere substantial. The Court found that the plaintiffsowning those projects would have realized profits hadthey been allowed to prepay.

The next steps in the case include computa-tions by both parties of the lost profits. If RHS andthe plaintiffs cannot agree on a settlement, then thecase will go back to court for a binding determina-tion of damages. The finding that the governmentbreeched its contract and therefore is liable for dam-ages could have enormous financial implications forthe government.

In the Kimberly case, an Idaho District Courtgranted the DBSI Group quiet title to their Section515 properties. Consequently, the government andDBSI settled and recorded a deed of conveyance forthe property. Two tenants appealed the Idaho DistrictCourt’s decision to the Ninth Circuit Court ofAppeals. In an unpublished memorandum issued July22, 2004, the court dismissed the appeal because thetwo parties to the suit had settled. As a result of theserulings, many borrowers have a new tool to gain con-trol of their Section 515 properties, with their rights toquiet title being dependent on the laws in their states.

10 Preserving Rural America’s Affordable Rental Housing

In cases where owners secure quiet title, RHS wouldhave no mechanism to protect tenants from rentincreases; once RHS is removed from the deed, afford-ability restrictions end, as does rental assistance.16

The Kimberly case made a considerable impacteven before the issuance of the July 22, 2004, memo-randum. Based on the District Court decision, DBSIGroup sought quiet title at 26 other properties that itowns in Idaho and Oregon in a case titled Atwood-Leisman v. United States. RHS also settled this suit,and, as a result, a nonprofit organization has purchasedthe 20 properties located in Idaho, receiving approxi-mately $10 million in Section 515 loan funds tofacilitate the transfers and rehabilitation. All 20 prop-erties have full rental assistance, and the tenants willcontinue to be subsidized under the new ownership.However, preservation of the six Oregon propertieshas created hardships for some tenants as RHS and the owners slowly implement the settlementagreement.

Problems with the appraisals of the two of thesix properties prevented RHS from approving thesales. Per the terms of the settlement agreement, DBSIpaid off the two loans, obtained quiet title, and soldthe properties to a related entity, Northwest RealEstate Capital Corporation. Because the loans wereprepaid, both of the projects lost their rental assistance.

According to an April 6, 2004, article in TheOregonian, the new owner then tripled the rents,bringing them up to market rate. Several of the resi-dents at the two properties moved because they couldnot afford the new rents without a subsidy. Some ofthe elderly tenants face monthly medication bills ashigh as $400, leaving little of their Social Securityincome for other living expenses, including rent.17

Exhibit 5:How Section 515 Provides Relief FromExtreme Rural Isolation in Tennessee18

Before they moved into the Section 515-fundedClearview Apartments in White House, Tennessee,Jean and Willie Meador, both 64, were living in asmall mobile home on a steep hill in rural SumnerCounty. The Meadors were paying $450 in renteach month, which was 70 percent of their ad-justed income. Compounding this burden werethe high medical expenses involved in treatingMrs. Meader’s diabetes and blood clots. Becausetheir car could not negotiate the road down theirhill, the couple relied on a local transportationservice to take Mrs. Meador to dialysis three timesa week. When bad weather made their roadimpassable, the Meadors grew desperate for aplace to live nearer the dialysis treatment center.

Their new home at the Clearview Apartments pro-vided them with exactly what they needed. Theirrent dropped to 30 percent of their adjustedincome. Transportation became manageablebecause they were near the treatment center, andthey could use the pharmacy and grocery deliveryservices that manager Nancy Robinson hadarranged for all Clearview residents. Their homewas almost maintenance-free, and it had an emer-gency alert system. They were among caringneighbors and could count on Mrs. Robinson tolook after them when necessary.

Although Mrs. Meador has since died, her hus-

band is grateful that she was able to spend her

last days in a safe and comfortable home.

16 RHS may provide rental assistance only at those properties that have a 515 loan.

17 “Lack of Ruling Leaves Rent Subsidy Unresolved,” The Oregonian, April 6, 2004 (accessed May 7, 2004); available from www.knowl-edgeplex.org/news/19309.html.

18 Adapted from U.S. Department of Agriculture, Rural Development, Rural Housing Service, Rural Housing Service 1996 ProgressReport (Washington, D.C.: U.S. Department of Agriculture, 1997), 4.

Current Issues 11

Fortunately, DBSI, Northwest Real EstateCapital Corporation, and RHS later agreed on the saleof one of the two properties to a nonprofit owner, andthey reversed the prepayment. RHS provided Section515 funds to cover the transaction and restored therental assistance that was previously available to theproject. The second property will remain outside theSection 515 program with Northwest Properties. Allthe current tenants will receive Section 8 vouchers.Rents at both properties will remain at market rates.

RHS and DBSI are in discussions to resolvetheir differences and arrange for sale of the remainingfour properties to new nonprofit owners. In the meantime, however, the implementation of theAtwood-Liesman settlement in Oregon illustrates thesudden rent burden that tenants may bear whenSection 515 owners receive quiet title.

Scope of the Problem

The issue of prepayment has garnered consider-able attention in recent years, driven by numerouslawsuits, continual pay-offs of loans, and by the factthat more than 64 percent of Section 515 propertiesare eligible for prepayment. It remains unclear, howev-er, exactly how many properties actually can be prepaidbecause prepayment is dependent upon an owner’shaving the financial ability, without RHS assistance, topay off the loan.

The U.S. General Accounting Office (GAO)examined this issue in a 2002 study, Multifamily RuralHousing: Prepayment Potential and Long-TermRehabilitation Needs for Section 515 Properties. GAOestimated that if statutory restrictions on prepaymentfor loans made before December 15, 1989 were liftedto allow prepayment after 20 years from the date ofthe loan, “prepayment could be an option for the own-ers of about 3,900, or about 24 percent, of all Section

515 properties over the next 8 years. Owners of about950 of these properties would immediately become eli-gible to prepay.”

GAO based this conclusion on its analysis of (1)nonprofit ownership, assuming that nonprofit ownerswould not be interested in prepayment; (2) heavydependence on rental assistance that would cease uponprepayment; and (3) location of properties in areas ofpopulation decline. GAO estimated that the actualnumber would probably be smaller but was unable tomeasure the other factors that go into the prepaymentdecision, including whether the owners could operatewithout a subsidized 515 loan; whether they couldfund capital needs; whether they could meet tax conse-quences; and whether rents could increase. GAO alsoacknowledged that its calculations did not take intoaccount owner fatigue, which RHS managers believe isa considerable incentive to exit the program.19

GAO characterized the prepayment activity todate as minimal. However, the National RuralHousing Coalition responded that the report down-played the urgency of the risk “by only presentingnumbers contingent upon possible statutory changesand other hypothetical calculations, and omitting theportfolio’s reality.” The Coalition’s view is that anyprepayment activity is significant given the unmetneed for housing for the most vulnerable ruralAmericans, the continuing decline in the Section 515budget, and the unmet demand for rehabilitation andequity funds. A loss of 3,900 properties would affectmore than 100,000 tenants, a large number of low-income families.20

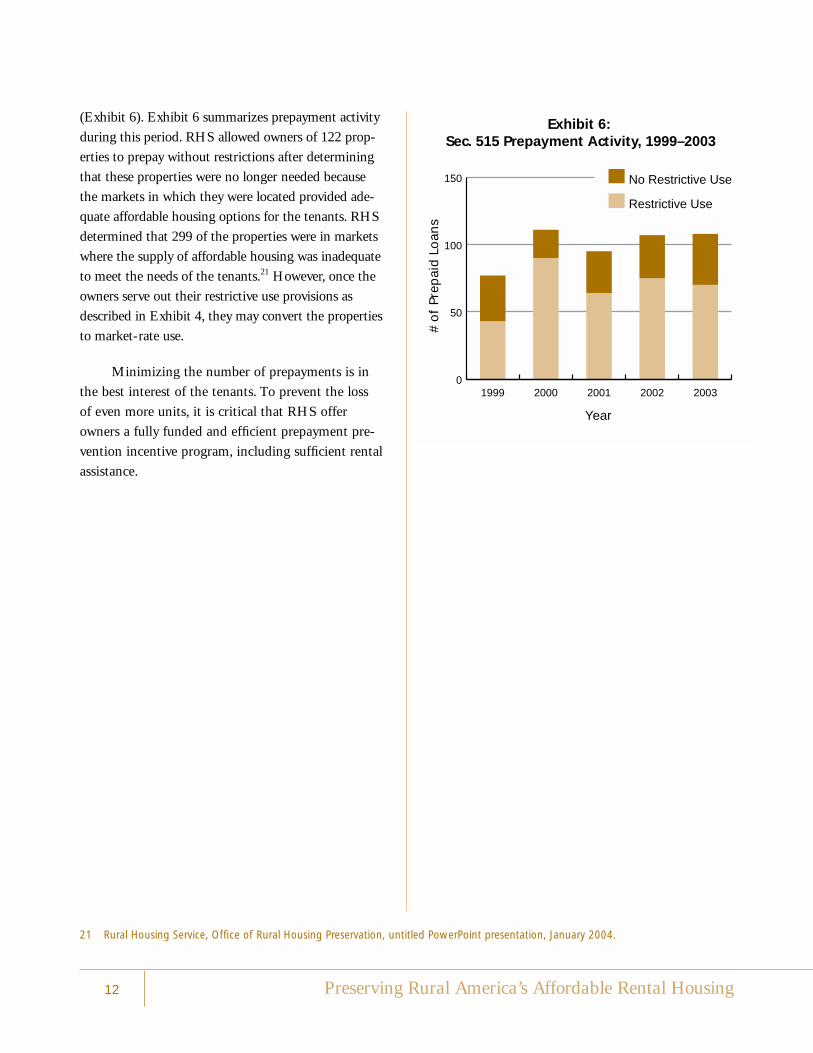

From the program’s inception through the end offiscal year 2003, owners of 2,477 properties prepaidtheir loans, representing a loss of approximately 44,600units. Between 1999 and 2003, 421 loans were pre-paid, 299 of which had restrictive use provisions

19 GAO, 9–10.

20 Letter to Stanley J. Czerwinski, Director, Physical Infrastructure Issues, General Accounting Office from Bob Rapoza, ExecutiveSecretary, National Rural Housing Coalition, June 14, 2002.

12 Preserving Rural America’s Affordable Rental Housing

(Exhibit 6). Exhibit 6 summarizes prepayment activityduring this period. RHS allowed owners of 122 prop-erties to prepay without restrictions after determiningthat these properties were no longer needed becausethe markets in which they were located provided ade-quate affordable housing options for the tenants. RHSdetermined that 299 of the properties were in marketswhere the supply of affordable housing was inadequateto meet the needs of the tenants.21 However, once theowners serve out their restrictive use provisions asdescribed in Exhibit 4, they may convert the propertiesto market-rate use.

Minimizing the number of prepayments is inthe best interest of the tenants. To prevent the lossof even more units, it is critical that RHS offer owners a fully funded and efficient prepayment pre-vention incentive program, including sufficient rentalassistance.

21 Rural Housing Service, Office of Rural Housing Preservation, untitled PowerPoint presentation, January 2004.

Exhibit 6: Sec. 515 Prepayment Activity, 1999–2003

0

50

100

150 No Restrictive Use

Restrictive Use

20032002200120001999

# o

f Pr

epai

d L

oan

sYear

Current Issues 13

Preserving the portfolio is not just a matter offunding prepayment prevention incentives; it alsorequires recapitalization funds, including adequatereserves, to rehabilitate the aging housing stock, andrental assistance subsidies to relieve tenants of rentoverburden. However, USDA has not requested andCongress has not provided sufficient funding for anyof these needs.

As previously noted, 89 percent of Section 515properties are at least 10 years old, and 64 percent are15 years old or older. As these properties age, impor-tant parts of their physical infrastructure wear out.Components that typically must be replaced after adecade or two include roofs, windows, heating andcooling systems, plumbing, siding, and pavement, aswell as major appliances such as refrigerators andranges. To pay for the replacement of these systems,owners must attract new funding. This process iscalled recapitalization.

There is no single solution to recapitalizingSection 515 housing. Project reserves are generallyinadequate to the task, typically supplying between one-third and one-half of a 515 property’s recapitalizationneeds.22 Market and physical conditions vary widely. Inaddition, while some owners of aging properties wish toremain in the 515 program, many others would like toleave it. These factors influence the recapitalizationoptions. This section of the report examines the scopeof the recapitalization problem, describes the obstaclesthat RHS must overcome to develop a portfolio-widepreservation strategy, discusses RHS’s recapitalizationtools, and identifies ways to improve them.

Quantifying the Needs

Eventually, every property must be recapitalized.However, RHS lacks a clear understanding of the totalrecapitalization needs of the Section 515 portfolio. Inits 2002 study, GAO noted that RHS’s estimates ofrecapitalization needs range from $800 million to $3.2billion — a range too broad to be useful for policy-making purposes. GAO recommended that “RHSundertake a comprehensive assessment of the Section515 portfolio’s capital and rehabilitation needs, use theresults to set priorities for the portfolio’s immediaterehabilitation requirements, and provide Congress withan estimate of the portfolio’s long-term rehabilitationneeds.”23

In response, RHS has commissioned a study thatis intended to address all of GAO’s recommendations.Using a sampling methodology devised by USDA’sEconomic Research Service, RHS’s contractors areassessing 334 representative Section 515 properties interms of their immediate health and safety needs andthe cost to rehabilitate and maintain them over thenext 20 years. In addition, they will analyze the rela-tionship between the market value and debt load atone percent of the properties in order to determinetheir likelihood to prepay. They will determine whatincentives might be appropriate to prevent prepay-ment. Finally, they will provide recommendations onhow to recapitalize the portion of the portfolio that isnot likely to prepay, as well as assess the impacts ontenants of recapitalizing this housing, maintaining it asis, or letting it go.24 USDA expects to release thereport during the Fall of 2004.

Overview of Recapitalization Issues

22 GAO, 12.

23 GAO, 3.

24 Shekar Narasimham and Tom White, Beekman Advisors, telephone interview, January 22, 2004.

14 Preserving Rural America’s Affordable Rental Housing

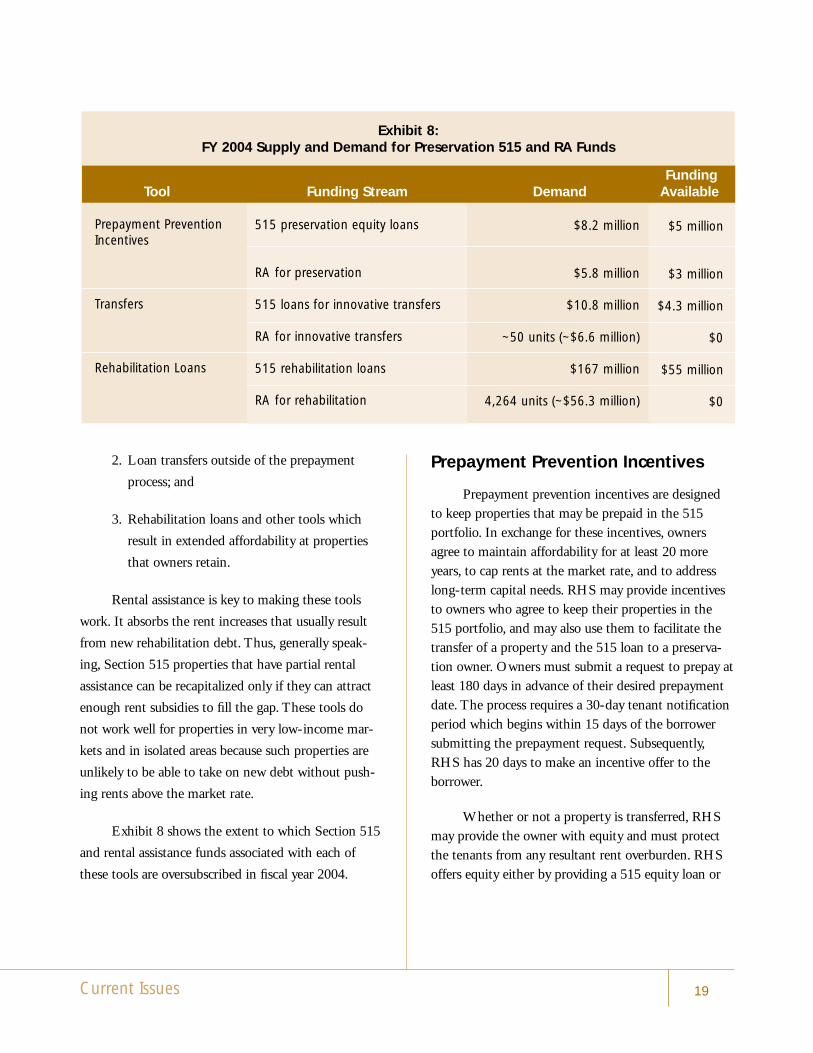

The study should provide a more detailed pictureof the portfolio’s recapitalization needs. Meanwhile,however, it is clear that if even the most conservativeof RHS’s recapitalization estimates are at all accurate,RHS has been unable to meet the need. Because of itsextremely limited Section 515 and rental assistancebudgets, RHS has recapitalized only about 9,150Section 515 units each year over the past five years, orless than 3 percent of all units in the portfolio.Another indication that RHS’s preservation dollars areinadequate is the subscription rate for its 515 andrental assistance funds. In FY 2004, for example,demand for 515 funds exceeds supply by almost threeto one, while demand for rental assistance exceeds sup-ply by almost 23 to one.

Portfolio-Wide RecapitalizationObstacles

RHS’s Section 515 portfolio faces five majorrehabilitation obstacles: (1) a lack of capital, (2) limitedrevenue opportunities, (3) lack of adequate rental assis-tance and Section 8 subsidies, (4) unsustainably lowrents, and (5) phantom income and exit taxes.

Lack of capital: In the absence of sufficient proj-ect reserves and Section 515 loan funds to recapitalizethe portfolio, RHS relies increasingly on third-partyfinancing. The principal funding sources are:

■ 9-percent Low-Income Housing Tax Credits,which provide a deep equity subsidy

■ tax-exempt bonds plus 4-percent LIHTCs,which provide low-cost debt and a shallowerequity subsidy

■ other bonds, such as 501(c)(3), which providelow-cost debt

■ private debt

■ grant funds such as those available throughthe CDBG and HOME programs.

State agencies issue tax credits, bonds, and ruralCDBG and HOME funds. Banks issue private debt.

Exhibit 7 outlines the types of projects for whichthese recapitalization sources are best suited and anynoteworthy issues. As the exhibit shows, non-RHSdebt funding sources work best for properties able toachieve economies of scale. The average Section 515property has only 27 units, however, so developersseeking to use these funding sources must find larger-than-average Section 515 properties or combine small,close-by properties under one management plan.

Debt financing — including tax-exempt bondsplus 4-percent LIHTCs — has the advantage of beingrelatively easy to obtain but the disadvantage that itincreases total debt service and, therefore, rents.25

Tenants at properties with full rent subsidy are pro-tected from rent overburden because both rentalassistance and Section 8 assistance increase to pay forthe additional debt service (thus, when new debt isadded to a property with rental assistance, the per-unitcost of RA increases). Without rent subsidies, tenantsmust bear the rent increases. If low-income tenants areto be protected from rent overburden, these debt toolscan be used only at properties with 100 percent rentsubsidy.

Poor candidates for debt-financed recapitaliza-tion include small properties that cannot be bundledwith other properties to achieve economies of scale,properties in flat markets that cannot afford significantrent increases, and properties that are not fully rentsubsidized. RHS cannot currently quantify the numberof such properties in the Section 515 portfolio, but therecapitalization study discussed earlier will help answerthis question, as well as determine the percentage thatshould be preserved. RHS may be able to generateadditional cash flow at some of these propertiesthrough its loan servicing tools, including small rentincreases, reamortization, interest-rate reduction, andpossibly writing off a portion of its debt or convertingit to soft debt repayable upon sale of the property.

25 RHS can reduce the debt service on the Section 515 loan by reamortizing or writing off a portion of it, but the resulting reduction isalmost never enough to offset the new rehabilitation debt service.

Current Issues 15

RHS is investigating whether and how it can use thelast two tools. It is unclear whether these servicingtools can generate enough cash flow to recapitalizeproperties operating on the margins of profitability.

In some cases, the only way to preserve a proper-ty is through 9-percent tax credit equity or grantfunding such as that provided by the CDBG andHOME programs. However, these programs are vastlyoversubscribed and currently do not meet the 515preservation need. To illustrate, there are 12 states inwhich no 515 loan transfers have occurred in the pastthree years. RHS has identified the lack of 9-percenttax credits as the primary cause. If the RHS recapital-ization study reveals that there are significant numbers

of economically marginal properties worth preserving,it would make sense for state and local governmentsand Congress to provide preservation grant funds.Possibilities include local, state, and Federal preserva-tion set-asides in the CDBG and HOME programsand new recapitalization grant programs. Congressshould, in addition, provide a set-aside of 9-percent taxcredits for 515 preservation.

Limited revenue opportunities: Participants inaffordable housing deals earn part of their incomethrough fees that are a percentage of the debt or equitythey bring to a deal. Since small deals yield small feesrelative to the amount of labor they require, manydevelopers, lenders, and tax credit syndicators will not

Exhibit 7:Sources of Section 515 Recapitalization Funding

9% tax credit equity

Tax-exempt bond debtplus 4% tax creditequity

Bond debt

Third-party debt

CDBG, Home andother grant equity

Facilitates large share of 515 loan transfers. Offers muchdeeper equity subsidy than 4% tax credits, so can work forsmall deals.

High transaction costs limit usefulness of this tool to proper-ties with economies of scale. See “Case Study 2: Replicatinga Preservation Model in California” for an example of howthis tool can be used.

High transaction costs limit usefulness of this tool to proper-ties with economies of scale, but it can be very efficient. Forexample, the Denver, Colorado-based non-profit organiza-tion Mercy Housing used $15 million worth of 501(c)(3)bonds to purchase and renovate 17 Section 515 propertiesin Washington State as part of a two-phased deal that willeventually include 30 properties and 925 units.

The cost of this debt is greater than Section 515 debt, butRHS supports using third-party debt because it lackssufficient 515 funds.26

Grant funds are necessary for projects that cannot absorbrent increases and for gap financing for larger deals.

All

Large-scale projects

Large-scale projects

Usually, projects thatcan afford a significantrent increase

All

Funding Projects for Which Source Source Is Best Suited Comments

26 Grace Buckley, Mercy Housing, telephone interview, March 11, 2004.

16 Preserving Rural America’s Affordable Rental Housing

participate in recapitalizing the typical 515 propertyunless they are mission-driven or stand to gain abenefit such as Community Reinvestment Act credit.Property managers face similar problems with smalldeals. In addition, the opportunity costs of Section 515transactions — that is, the costs of committing fundsto such transactions rather than to other purposes —

are too high for many participants in affordable hous-ing. RHS allows developers to collect developer feesonly when their projects have LIHTC financing, andit caps their return on investment at 8 percent of thestarting equity. The return cannot escalate as the equi-ty grows and may be accessed only if there is sufficientcash flow. The program does not allow nonprofit own-

Case Study 1: Innovative Transfers in Michigan

In 2001, a Michigan-based limited partnership used RHS’s Innovative Transfers program to secure equity andrental assistance to preserve two adjacent family properties in Huron County, an economically stable communityof about 3,500 people. The unrelated owners of the two properties, Port Crescent Apartments I and II, werepaying taxes on phantom income and wanted to leave the Section 515 program. Port Crescent I had 48 units,of which 20 had rental assistance and the rest were unsubsidized. Port Crescent II had 56 units, all of whichwere subsidized by project-based Section 8. The partnership wanted to purchase both properties and consoli-date their management and operations. In order to do so and to make necessary repairs, it needed both equityand 28 additional units of rental assistance.

The partnership secured two allocations of 9-percent low-income housing tax credits, for a total of $1.4 millionin equity. It also obtained a private bank loan to cover repairs at both properties. RHS agreed to reamortize andsubordinate its debt to this mortgage. To get the necessary rental assistance as well as a Section 515 equityloan, the partnership participated in RHS’s Innovative Transfers program. It requested 14 units of rental assis-tance from the RHS national office, which the RHS Michigan state office matched with unused units from fourproperties. RHS also agreed to a $67-per-unit-per-month rent increase. Tenants were protected from rent over-burden by the properties’ full rent subsidies.

Although both owners could have requested to prepay their loans and would probably have received prepay-ment prevention incentives, they were better served by participating in the transfer process because they wereable to get their equity more quickly. The Innovative Transfers program is competitive and RHS makes fundingdecisions within about two months of announcing the competition each year. Once RHS announced that it hadselected the developer’s proposal for funding, the Michigan state office was able to close the deal within threemonths.

The partnership has spent $3 million to rehab the 104 units, including replacing roofs, siding, boilers, furnaces,windows, the parking lot, and interior finishes and cabinets. It also installed playground equipment and broughtthe properties into compliance with handicap access laws. In return, it has received a developer fee from taxcredit proceeds. It also owns the management company that managed the two properties before the partner-ship acquired them. The company earns a management fee, and the property is performing as projected. Finally,the partnership owns the construction company that did the rehab work and was able to receive a builder’sprofit of up to 10 percent. The partnership has self-imposed a restriction that the return on investment may notexceed $10,000 per year, although rents could support a much higher return.

Because the RHS national office can offer no rental assistance units for transfers in 2004, and state offices havealmost no RA, it is unlikely that this transfer could have been completed this year.

Current Issues 17

ers a return on equity. Finally, each RHS state officehas its own management fee policy, which means thatin some states it is considerably more profitable tomanage a Section 515 property than in others.

Lack of adequate rental assistance and Section 8 subsidies: The Section 515 portfolio is not fully rent-subsidized.27 Twenty percent of tenants are rent-overburdened. More than 100,000 units (25 percent)have no rental subsidy, and the subsidy distribution isnot uniform across properties. In California, for exam-ple, 14 percent of Section 515 properties have no RAor project-based Section 8 subsidy; 40 percent havefull or close-to-full RA or Section 8; and the remain-ing 46 percent are somewhere in between. Rentalsubsidy protects tenants from rent overburden and iscritical when recapitalization results in rent increases,as it generally does. Thus the availability of rentalassistance drives most recapitalization strategies.Rental assistance is also critical to maintaining highoccupancy rates: those properties that have only partialRA and are not located in strong markets often havevacancy problems.

FY 2004 is the first year in which RHS lacksfunding to provide rental assistance in conjunctionwith its rehabilitation loans or with transfers, and thereis currently a year-long waiting list for prepaymentincentive rental assistance. Some units may becomeavailable if RD state offices can recapture unusedrental assistance funds from properties in their portfo-lios, but because of increasingly efficient use of RAthere are few such units. The result of this shortage ofrental assistance is that this year RHS will providerehabilitation funds only to those properties with full

rental assistance, and there will be few if any transfersof projects with partial rental assistance.

Eventually RHS must confront the issue of howto recapitalize projects with partial RA without creat-ing rent-overburden for the unsubsidized tenants.Making this issue more difficult is the statutory prohi-bition on using rental assistance to cross-subsidizeunits without RA. As a result of this law, RHS is pro-hibited from charging different rents on units offeringthe same amenities, or, in other words, from targetingrents to match tenant incomes. Nor can it spread theRA subsidy across all the units in a property with par-tial RA.

Unsustainably low rents: The average Section 515rent is $314 per unit per month,28 or $3,768 per year.This is the full amount that the average propertyreceives for each unit, including both the tenant con-tribution and any rental assistance the tenant has. Fora property to operate in the black, rent revenues mustexceed expenses, which include maintenance, utility,salary, insurance, and administrative costs; taxes; anddebt service. Even at larger properties with economiesof scale, $3,768 would be considered a fairly low per-unit operating expense. For a small property with nosuch economies and with an income of only $3,768per unit, it is practically a given that the owner mustcut operating costs in order to operate in the black.The two most likely places are maintenance and thereturn to owner, which the owner may collect only ifthere is sufficient cash flow. Stakeholders ranging fromthe Housing Assistance Council29 to the Council forAffordable and Rural Housing30 complain that Section515 rents cannot sustain project operations. This prob-

27 Properties that have rental assistance for fewer than 100 percent of their units are said to have “partial rental assistance.”

28 2003 Multi-Family Housing Annual Fair Housing Occupancy Report, 34.

29 The Housing Assistance Council is a nonprofit advocacy organization that owns a small portfolio of Section 515 properties and advo-cates for affordable housing for low-income rural Americans. See “About Rural Rental Housing Prepayment and Preservation”(accessed March 30, 2004); available from http://www.ruralhome. org/pubs/infoshts/infopreserv.htm.

30 The Council for Affordable and Rural Housing is a national trade association that represents 300 companies, including owners andmanagers at approximately 2,000 Section 515 properties. The owners it represents are mainly for-profit organizations. See“Testimony of Betty Bridges, President, Council for Affordable and Rural Housing Before the US House of Representatives,Committee on Financial Services, Subcommittee on Housing and Community Opportunity, June 19, 2003,” 5 (accessed March 15,2004); available from http://financialservices. house.gov/media/pdf/061903bb.pdf.

18 Preserving Rural America’s Affordable Rental Housing

lem is exacerbated by the portfolio-wide issue of inad-equately funded reserves.

While this $314-per-month rent is the averagenational rent, actual project rents range widely,depending on the market area, the availability of rentalsubsidy, and RD state office policies. Many Section515 properties have rents that are high enough tocover maintenance costs and are in good condition.However, the $314 figure is a potential indicator ofcapital needs across portions of the portfolio, especiallyat those properties that have partial rental assistance.

At least two factors contribute to keepingSection 515 rents low: (1) some low-income ruralmarkets do not support higher rents because they havea high incidence of substandard housing and very fewif any properties comparable to their 515 property; and(2) many RD field offices have denied rent increasesboth to avoid increasing the per-unit cost of rentalassistance, and, at properties with partial rental assis-tance, to protect the tenants who do not have RAfrom rent overburden.

Phantom income and exit taxes: Phantom incomeis taxable income in excess of cash flow distributionsactually received. It occurs when a property’s non-deductible expenditures exceed taxable deductions.Non-deductible expenditures include mortgage prin-cipal payments, deposits to reserves, and excess cashflow, which RHS requires owners to reinvest in theirproperties. Non-cash deductions include depreciationand amortization. Phantom income is likely to occurat many aging RHS properties because they do notprovide returns greater than their tax liabilities. To theextent that refinancing reduces non-deductible mort-gage principal payments, it can reduce or eliminatephantom income taxes.31

Exit options are limited. Many Section 515owners face steep exit taxes if they sell their propertiesbecause they have taken depreciation substantially inexcess of their original investments. Unless a propertycan generate a sales price that covers the exit taxes, itsowners are usually better off retaining the property.This means that owners in some appreciating marketsas well as in flat and declining markets have limitedincentive to sell their properties, and limited ability torecapitalize them. In considering any sale transaction,owners must weigh the continual taxes on phantomincome against the one-time exit tax hit, and potentialbuyers must ensure that they can meet the owner’sprice and still accomplish the necessary rehabilitation.

While some owners have decided that accept-ing an exit tax loss by selling their properties is moreadvantageous than remaining in the Section 515 pro-gram, many opt to retain their properties. Accordingto the Tax Issues and Preservation Task Forces of theMillennial Housing Commission, “Experiencedaffordable housing professionals generally agree thatthe single largest barrier to transfer and preservationof pre-1986 properties is the seller’s income tax dueon sale . . , usually exceeding the cash proceeds of thesale.”32 The task forces concluded that if a preserva-tion tax incentive were created to provide full taxrelief at the time of sale, as many as 68,000 Section515 units in 2,510 properties could be recapitalizedand preserved.33

Overview of RHS’s RecapitalizationApproaches