president message - icsi nitor april 1st issue.pdf · president message dear professional ... fraud...

TRANSCRIPT

.l

PRESIDENT MESSAGE

Dear Professional Colleagues,

“I am not bound to win, but I am bound to be true. I am not bound to

succeed, but I am bound to live by the light that I have. I must stand with

anybody that stands right, and stand with him while he is right, and part

with him when he goes wrong.”

-Abraham Lincoln

Standing of a profession does not lie merely in technical competency of its practitioners but also in their ethical conduct. As governance professionals, we must serve the broader interest of the stakeholders and contribute towards promoting a culture of good governance. We must have a quest for holistic professional growth, explore new horizon and aspire for a higher degree of professionalism, which is beyond mere fulfilment of the legal requirements. It is also pertinent to consider that when upholding the values of righteousness, one may even face setbacks and adversaries; however, what is right should not be forgotten for what is convenient.

The Institute has a great responsibility towards the development and regulation of the profession; where members play a crucial role by regulating their own actions. Being governance professionals, we must essentially ensure self governance so that we are able to strike a right balance between conflicting demands and rising expectations of the stakeholders.

Regards,

CS Atul H. Mehta President [email protected]

Images

Comparison Between SEBI (Prohibition of Insider Trading) Regulations, 2015 & SEBI (Prohibition of Insider Trading) Regulations, 1992

Establishment and Functioning of the Serious Fraud Investigation Office in India and Fraud Prevention and Investigation in India

Circulars, Notifications, Orders, Amendments

Office of the Commissioner of Service Tax VI, Mumbai

25th World Congress on Leadership for Business Excellence & Innovation – Dubai Global Convention, 20-22 April 2015, Dubai (UAE)

Communication to the Esteemed Members regarding Chartered Secretary Journal.

Issue No. 21 Volume 01 April 1, 2015

Images

Student’s Meet with CS Atul H. Mehta, President, ICSI

at Hyderabad on 4th March 2015

CS Atul H. Mehta, President, ICSI addressing at

National Conclave on Critical Issues of Securities Laws held on 13 March, 2015

Sitting from L to R : CS Rishikesh Vyas, Chairman, ICSI-WIRC, Shri Atul Desai, Senior Partner, Kanga & Co. and CS Sutanu Sinha, CE & OS, ICSI

CS Atul H. Mehta, President, ICSI and CS Sutanu Sinha, CE & OS, ICSI Meeting with Shri Bandaru Dattatreya, Minister of State for Labour

and Employment (Independent Charge) on 18 March, 2015

CS Atul H. Mehta, President, ICSI inaugurating the 42nd Foundation Day of Pune Chapter of WIRC of Institute of Company Secretaries of India at

YASHADA, MDC Auditorium on 22 March, 2015

CS Sutanu Sinha, CE & OS, ICSI, CS Alka Kapoor, JS, ICSI, Council Member

CS Vineet K Chaudhary Meeting with Additional Secretary, MCA, Mr. Pritam Singh on 25 March, 2015

CS Atul H Mehta, President ICSI addressing the gathering at National

Seminar on Secretarial Audit held on 27 March, 2015 Seen on the dias (From L to R): CS Sutanu Sinha, CE & OS, ICSI

CS Vineet Chaudhary, Council Member, ICSI and CS N.P.S. Chawla, Chairman, NIRC of the ICSI

Comparison Between SEBI (Prohibition Of Insider Trading) Regulations, 2015 &

SEBI (Prohibition Of Insider Trading) Regulations, 1992

CS Kiran Mukadam * Company Secretary, Hercules Hoists Limited

The Securities and Exchange Board of India ("SEBI") notified the SEBI (Prohibition of Insider Trading Regulations) 2015 on January 15, 2015 replacing the two-decade old insider trading norms in India. The Regulations are based on the recommendations made by an 18 member committee constituted by SEBI under the chairmanship of Justice N.K. Sodhi, former Chief Justice of the High Courts of Kerala and Karnataka, which were approved by the SEBI Board in its meeting held on November 19, 2014. The comparison between old and new regulations are as under:

S.No Particulars SEBI (PROHIBITION OF INSIDER TRADING) REGULATIONS, 2015

SEBI (PROHIBITION OF INSIDER TRADING) REGULATIONS, 1992

1 Compliance officer “compliance officer” means a) any senior officer, designated so

and reporting to the board of directors or head of the organization in case board is not there;

b) who is financially literate and is capable of appreciating requirements for legal and regulatory compliance under these regulations;

c) who shall be responsible for compliance of policies, procedures, maintenance of records, monitoring adherence to the rules for the preservation of unpublished price sensitive information, monitoring of trades and the implementation of the codes specified in these regulations under the overall supervision of the board of directors of the listed company or the head of an organization, as the case may be;

No such definition

* The views expressed are personal views of the author and do not necessarily reflect those of the Institute.

2 Connected Person & Deemed to Connected Person

Connected Persons and Deemed to connected Persons includes- a) Director; b) occupies the position as an officer

or an employee of the company or holds a position involving a professional or business relationship between himself and the company on temporary or permanent, that allows him, directly or indirectly, access to unpublished price sensitive information;

c) an immediate relative of connected persons above;

d) a holding company or associate company or subsidiary company; or

e) Broker /Sub broker/RTA or an employee or director thereof; or

f) an investment company, trustee company, asset management company or an employee or director thereof; or

g) an official of a stock exchange or of clearing house or corporation; or

h) a member of board of trustees of a mutual fund or a member of the board of directors of the asset management company of a mutual fund or is an employee thereof; or

i) a member of the board of directors or an employee, of a public financial institution; or

j) an official or an employee of a self-regulatory organization recognised or authorized by the Board; or

k) a banker of the company; or l) A concern, firm, trust, Hindu

undivided family, company or association of persons wherein a director of a company or his immediate relative or banker of the company, has more than ten per cent. of the holding or interest;

Connected Persons and Deemed to connected Persons includes- a) Director; b) occupies the

position as an officer or an employee of the company or holds a position involving a professional or business relationship between himself and the company on temporary or permanent;

c) is a company under the same management or group, or any subsidiary company under section 370 or 372 of the Companies Act, 1956;

d) Broker/Sub-broker merchant banker, share transfer agent, registrar to an issue, debenture trustee, broker, portfolio manager, Investment Advisor, sub-broker, Investment Company or an employee thereof, or is member of the Board of Trustees of a mutual fund or a

This definition is intended to bring into its ambit persons who may not seemingly occupy any position in a company but are in regular touch with the company and its officers and are involved in the know of the company’s operations.

member of the Board of Directors of the Asset Manage-ment Company of a mutual fund or is an employee thereof who have a fiduciary rela-tionship with the company;

e) is an official or an employee of a Self-regulatory Organisation recognised or authorised by the Board of a regulatory body;

f) is a banker of the company;

g) Relative of above;

h) Persons mentioned in (d) holds more than 10 % shares in firm, trust, Hindu undivided family, company or association of persons

3 Trading "Trading" means and includes subscribing, buying, selling, dealing, or agreeing to subscribe, buy, sell, deal in any securities, and "trade" shall be construed accordingly.

Dealing in securities” means an act of subscribing, buying, selling or agreeing to subscribe, buy, sell or deal in any securities by any person either as principal or agent.

4 Insider "Insider" means any person who is: i. a connected person; or

ii. in possession of or having access to unpublished price sensitive information;

This is intended to bring within its reach any person who is in receipt of or

Insider includes- a) is or was connected

with the company or is deemed to have been connected with the company and have

has access to unpublished price sensitive information.

access to unpublished price sensitive information in respect of securities of company;

b) has received or has had access to such unpublished price sensitive information.

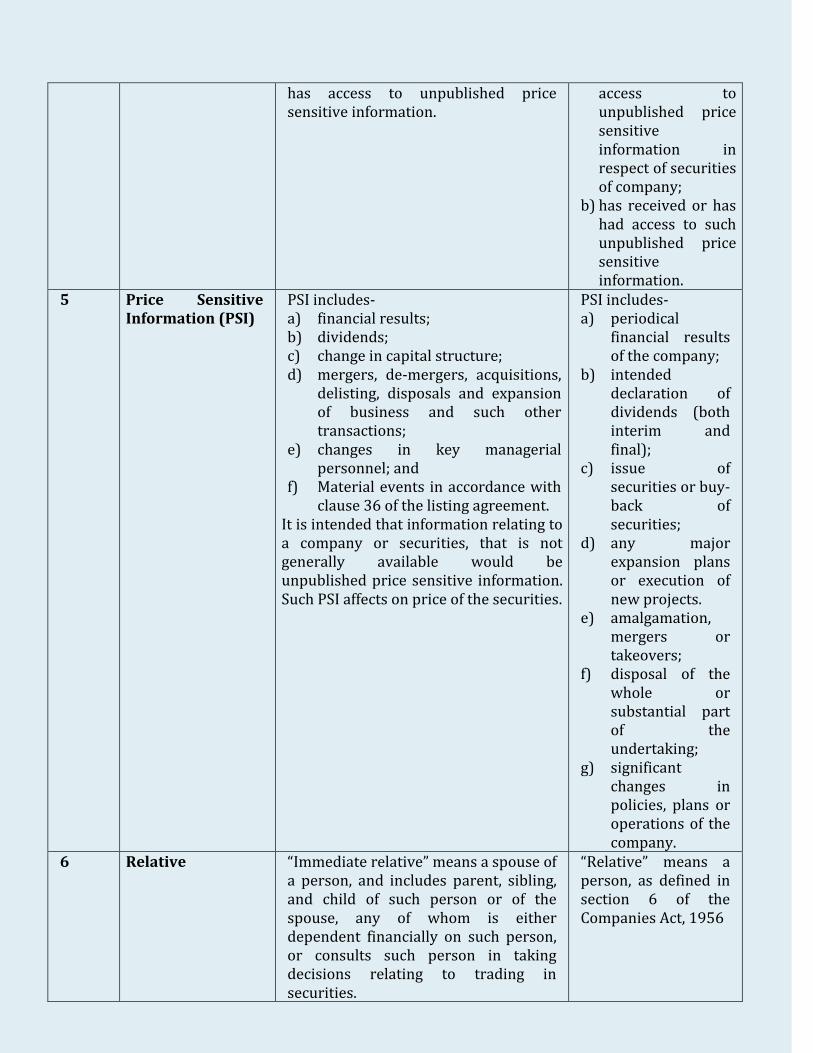

5 Price Sensitive Information (PSI)

PSI includes- a) financial results; b) dividends; c) change in capital structure; d) mergers, de-mergers, acquisitions,

delisting, disposals and expansion of business and such other transactions;

e) changes in key managerial personnel; and

f) Material events in accordance with clause 36 of the listing agreement.

It is intended that information relating to a company or securities, that is not generally available would be unpublished price sensitive information. Such PSI affects on price of the securities.

PSI includes- a) periodical

financial results of the company;

b) intended declaration of dividends (both interim and final);

c) issue of securities or buy-back of securities;

d) any major expansion plans or execution of new projects.

e) amalgamation, mergers or takeovers;

f) disposal of the whole or substantial part of the undertaking;

g) significant changes in policies, plans or operations of the company.

6 Relative “Immediate relative” means a spouse of a person, and includes parent, sibling, and child of such person or of the spouse, any of whom is either dependent financially on such person, or consults such person in taking decisions relating to trading in securities.

“Relative” means a person, as defined in section 6 of the Companies Act, 1956

7 Communication or procurement of unpublished price sensitive information

Insider shall not a) communicate, provide, or allow

access to any unpublished PSI , relating to a company or securities listed or proposed to be listed, to any person including other insiders;

b) procure from or cause the communication by any insider of unpublished PSI relating to a company or securities;

c) Unpublished PSI may be communicated, provided, allowed access to or procured, in connection with a transaction that would entail an obligation to make an open offer under the takeover regulations where the board of directors of the company is of informed opinion that the proposed transaction is in the best interests of the company. In such cases, the board of directors shall require the parties to execute agreements to contract confidentiality and non-disclosure obligations ;

d) trade in securities that are listed or proposed to be listed on a stock exchange when in possession of unpublished PSI.

Insider shall not- a) his own behalf or

on behalf of any other person, deal in securities of a company, if he have any unpublished PSI;

b) communicate/ counsel or procure directly or indirectly any unpublished PSI to any person who deal in securities, while in possession of such unpublished PSI;

c) Company shall deal in the securities of another company or associate of that other company while in possession of any unpublished PSI.

8 Trading Plans a) An insider shall be entitled to formulate a trading plan and present it to the compliance officer for approval and public disclosure pursuant to which trades may be carried out on his behalf in accordance with such plan;

b) This provision would enable the formulation of a trading plan by an insider to enable him to plan for trades to be executed in future;

c) Trading plan shall not entail commencement of trading on behalf of the insider earlier than six months from the public disclosure of the plan;

No such concept

d) Insider shall not execute trading plan between second trading day after the disclosure of such financial results and before 20th day of prior to last day of financial period. For ex. For Quarter 4 [Jan to March] financial result and result announcement date is 28th May, then Insider cannot execute his trading plan between 20th March to 29th May;

e) Trading plan should be for 12 months;

f) Not entail overlap of any period for which another trading plan is already in existence;

g) The trading plan may set out the value of securities or the number of securities to be invested or divested. Specific dates or specific time intervals may be set out in the plan;

h) The compliance officer shall review the trading plan and to approve and monitor the implementation of the plan;

i) The trading plan once approved shall be irrevocable and the insider shall mandatorily have to implement the plan;

j) If the very same unpublished price sensitive information is still in the insider’s possession, the commencement of execution of the trading plan ought to be deferred;

k) Upon approval of the trading plan, the compliance officer shall notify the plan to the stock exchanges on which the securities are listed.

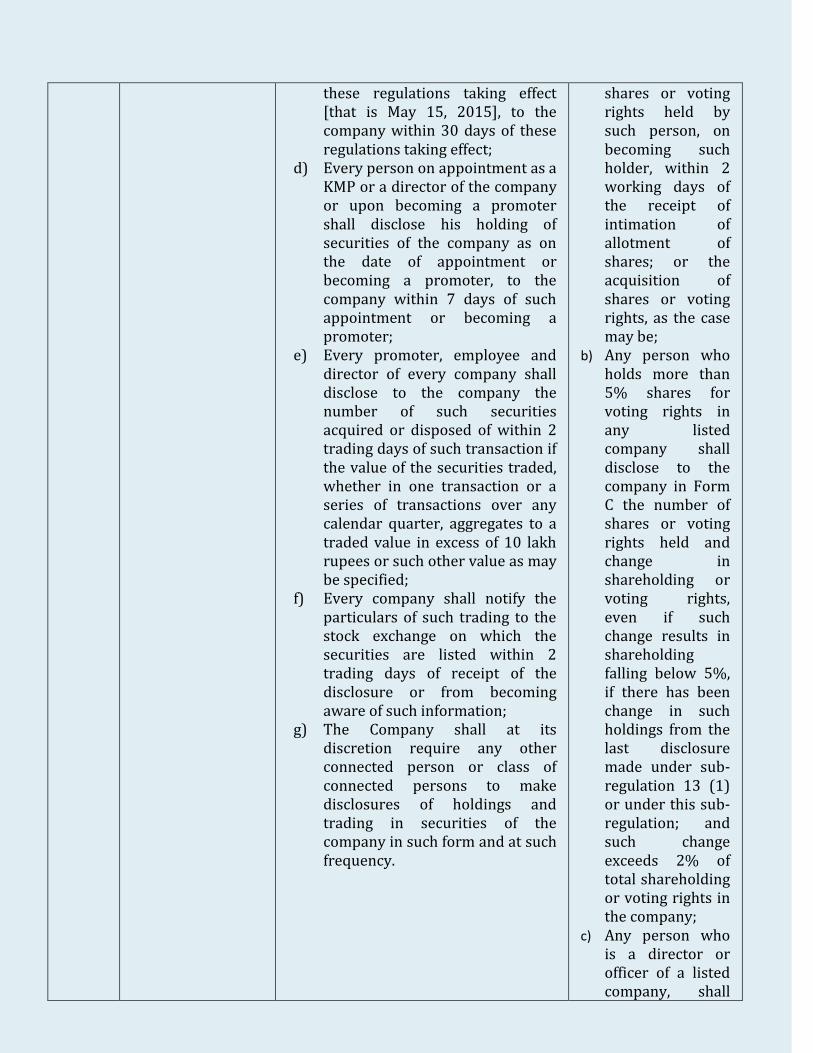

9 Disclosure a) Insider including immediate relative would give the disclosures;

b) Disclosures should be maintained by the Company for five years;

c) Every promoter, KMP and director of every company shall disclose his holding of securities of the company as on the date of

a) Any person who holds more than 5% shares or voting rights in any listed company shall disclose to the company in Form A, the number of

these regulations taking effect [that is May 15, 2015], to the company within 30 days of these regulations taking effect;

d) Every person on appointment as a KMP or a director of the company or upon becoming a promoter shall disclose his holding of securities of the company as on the date of appointment or becoming a promoter, to the company within 7 days of such appointment or becoming a promoter;

e) Every promoter, employee and director of every company shall disclose to the company the number of such securities acquired or disposed of within 2 trading days of such transaction if the value of the securities traded, whether in one transaction or a series of transactions over any calendar quarter, aggregates to a traded value in excess of 10 lakh rupees or such other value as may be specified;

f) Every company shall notify the particulars of such trading to the stock exchange on which the securities are listed within 2 trading days of receipt of the disclosure or from becoming aware of such information;

g) The Company shall at its discretion require any other connected person or class of connected persons to make disclosures of holdings and trading in securities of the company in such form and at such frequency.

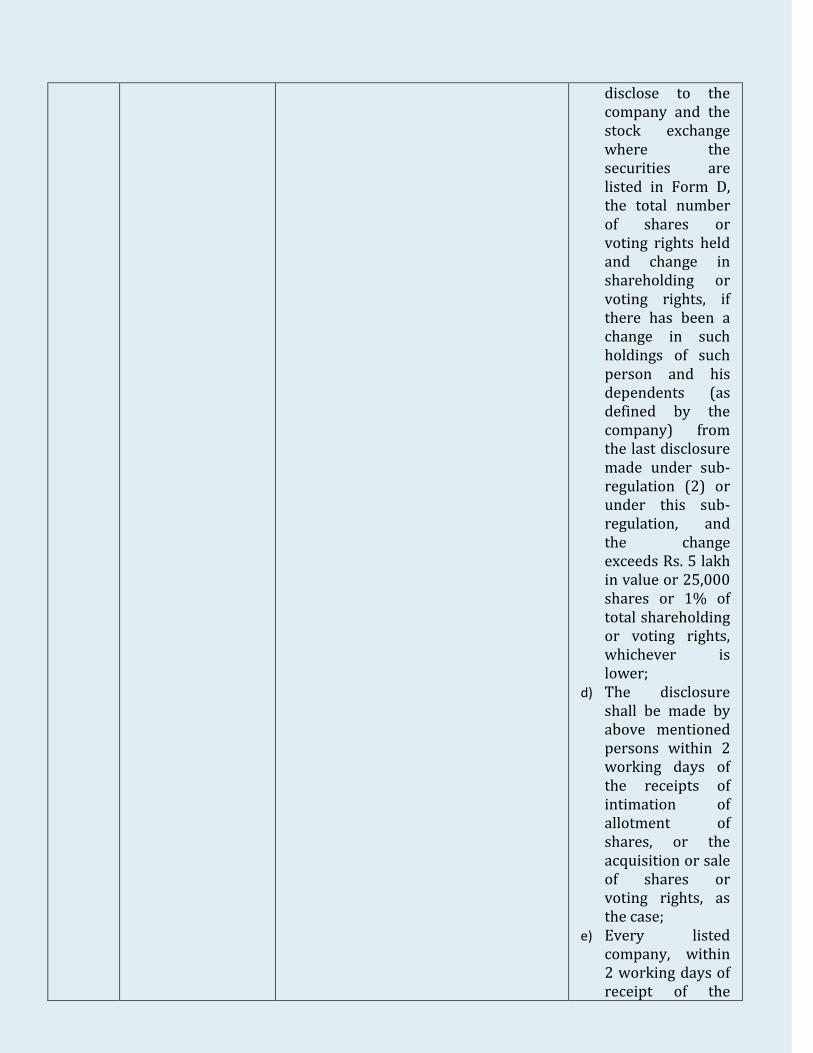

shares or voting rights held by such person, on becoming such holder, within 2 working days of the receipt of intimation of allotment of shares; or the acquisition of shares or voting rights, as the case may be;

b) Any person who holds more than 5% shares for voting rights in any listed company shall disclose to the company in Form C the number of shares or voting rights held and change in shareholding or voting rights, even if such change results in shareholding falling below 5%, if there has been change in such holdings from the last disclosure made under sub-regulation 13 (1) or under this sub-regulation; and such change exceeds 2% of total shareholding or voting rights in the company;

c) Any person who is a director or officer of a listed company, shall

disclose to the company and the stock exchange where the securities are listed in Form D, the total number of shares or voting rights held and change in shareholding or voting rights, if there has been a change in such holdings of such person and his dependents (as defined by the company) from the last disclosure made under sub-regulation (2) or under this sub-regulation, and the change exceeds Rs. 5 lakh in value or 25,000 shares or 1% of total shareholding or voting rights, whichever is lower;

d) The disclosure shall be made by above mentioned persons within 2 working days of the receipts of intimation of allotment of shares, or the acquisition or sale of shares or voting rights, as the case;

e) Every listed company, within 2 working days of receipt of the

information, shall disclose to all stock exchanges on which the company is listed.

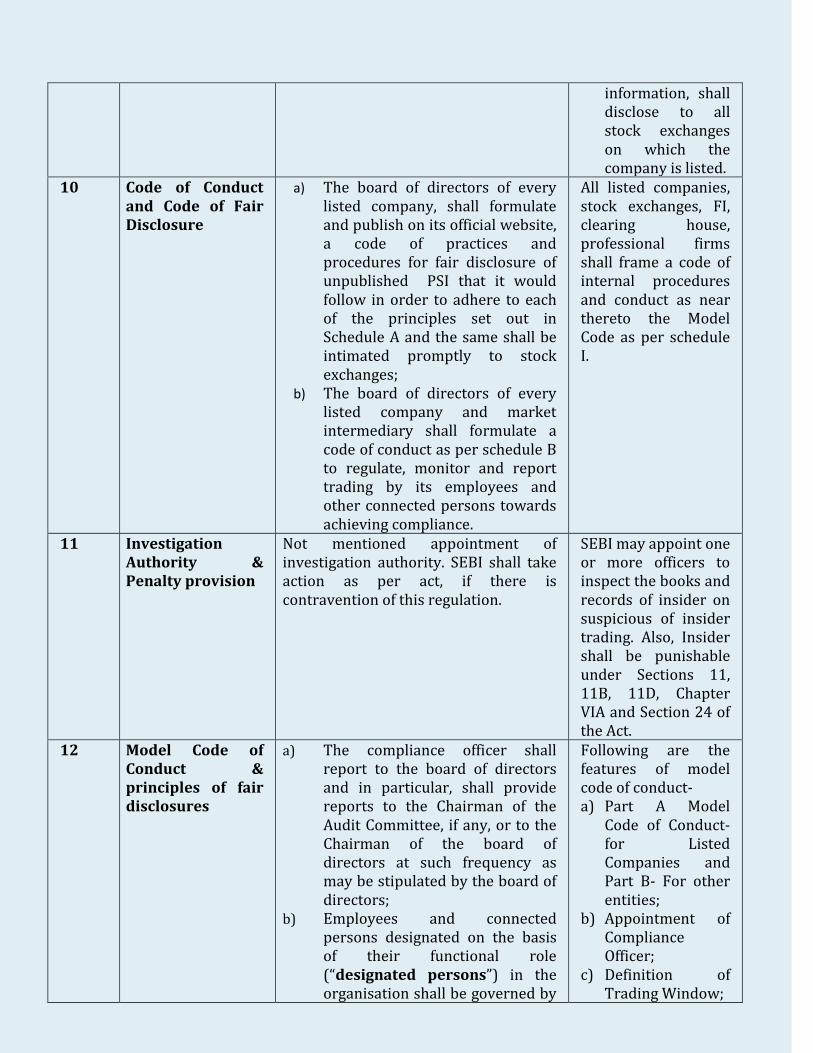

10 Code of Conduct and Code of Fair Disclosure

a) The board of directors of every listed company, shall formulate and publish on its official website, a code of practices and procedures for fair disclosure of unpublished PSI that it would follow in order to adhere to each of the principles set out in Schedule A and the same shall be intimated promptly to stock exchanges;

b) The board of directors of every listed company and market intermediary shall formulate a code of conduct as per schedule B to regulate, monitor and report trading by its employees and other connected persons towards achieving compliance.

All listed companies, stock exchanges, FI, clearing house, professional firms shall frame a code of internal procedures and conduct as near thereto the Model Code as per schedule I.

11 Investigation Authority & Penalty provision

Not mentioned appointment of investigation authority. SEBI shall take action as per act, if there is contravention of this regulation.

SEBI may appoint one or more officers to inspect the books and records of insider on suspicious of insider trading. Also, Insider shall be punishable under Sections 11, 11B, 11D, Chapter VIA and Section 24 of the Act.

12 Model Code of Conduct & principles of fair disclosures

a) The compliance officer shall report to the board of directors and in particular, shall provide reports to the Chairman of the Audit Committee, if any, or to the Chairman of the board of directors at such frequency as may be stipulated by the board of directors;

b) Employees and connected persons designated on the basis of their functional role (“designated persons”) in the organisation shall be governed by

Following are the features of model code of conduct- a) Part A Model

Code of Conduct- for Listed Companies and Part B- For other entities;

b) Appointment of Compliance Officer;

c) Definition of Trading Window;

an internal code of conduct governing dealing in securities.

c) Designated persons and their immediate relatives shall not trade in securities when the trading window is closed;

d) The timing for re-opening of the trading window shall be determined by the compliance officer, but it shall not be earlier than forty-eight hours after the information becomes generally available;

e) The code of conduct shall specify any reasonable timeframe, which in any event shall not be more than seven trading days;

f) The code shall stipulate such formats as the board of directors deems necessary for making applications for pre-clearance, reporting of trades executed, reporting of decisions not to trade after securing pre-clearance, recording of reasons for such decisions and for reporting level of holdings in securities at such intervals as may be determined as being necessary to monitor compliance with these regulations;

g) Prompt public disclosure of unpublished price sensitive information that would impact price discovery;

h) Designation of a senior officer as a chief investor relations officer to deal with dissemination of information and disclosure of unpublished PSI;

i) Appropriate and fair response to queries on news reports and requests for verification of market rumours by regulatory authorities;

j) Ensuring that information shared with analysts and research personnel is not unpublished price sensitive information.

d) All directors/ officers / designated employees and their dependents (as defined by the company shall execute their order in respect of securities of the company within one week after the approval of pre-clearance is given;

e) All directors/ officers/ designated employees who buy or sell any number of shares of the company shall not enter into an opposite transaction i.e. sell or buy any number of shares during the next six months following the prior transaction;

f) The Compliance Officer shall maintain records of all the declarations in the appropriate form given by the directors / officers / designated employees for a minimum period of three years;

g) Any employee/ officer/director who trades in securities or communicates

any information for trading in securities in contravention of the code of conduct may be penalized and appropriate action may be taken by the company.

Highlights of SEBI (Prohibition of Insider Trading) Regulations, 2015

1) Insider includes connected person and any person who have knowledge of unpublished price sensitive information.

2) Connected Persons include Directors, Holding Company, Subsidiary Company, Associate Company, RTA, Broker/Sub Broker., Officers of Stock Exchanges, A concern, firm, trust, Hindu undivided family, company or association of persons wherein a director of a company or his immediate relative or banker of the company, has more than ten per cent. of the holding or interest, Banker of the Company

3) Immediate Relative includes Spouse and Children who depends financially 4) Insider shall not deal during the closing of trading window period. 5) Price sensitive information scope increased. Now, it includes Strike, Lock Outs, commencement

of commercial production, all material events which affects on financial position of the Company

6) The Company shall prepare model code of conduct and follow the principals of fair disclosures. 7) An insider shall be entitled to formulate a trading plan and present it to the compliance officer

for approval and public disclosure pursuant to which trades may be carried out on his behalf in accordance with such plan

8) Disclosures: Insider including immediate relative would give the disclosures. Every promoter, KMP and director of every company shall disclose his holding of

securities of the company as on the date of these regulations taking effect [that is May 15, 2015], to the company within 30 days of these regulations taking effect.

Every person on appointment as a KMP or a director of the company or upon becoming a promoter shall disclose his holding of securities of the company as on the date of appointment or becoming a promoter, to the company within 7 days of such appointment or becoming a promoter.

Every promoter, employee and director of every company shall disclose to the company the number of such securities acquired or disposed of within 2 trading days of such transaction if the value of the securities traded, whether in one transaction or a series of transactions over any calendar quarter, aggregates to a traded value in excess of 10 lakh rupees or such other value as may be specified.

Every company shall notify the particulars of such trading to the stock exchange on which the securities are listed within 2 trading days of receipt of the disclosure or from becoming aware of such information.

***

Establishment and Functioning of the Serious Fraud Investigation Office in India and Fraud Prevention and

Investigation in India

CS Mandar Karnik* Executive – Legal and Secretarial, Kores

Introduction

“Fraud” is defined as a deception deliberately practiced in order to secure unfair or unlawful gain. As a legal construct, fraud is both a civil wrong (i.e., a fraud victim may sue the fraud perpetrator to avoid the fraud and/or recover monetary compensation) and a criminal wrong (i.e., a fraud perpetrator may be prosecuted and imprisoned by governmental authorities).

Rising instances of corporate fraud have set the alarm bells ringing within India Inc. As high as 75% of the top corporate executives interviewed in a KPMG study, consider fraud as their highest concern, followed by inadequacy of measures to curb them.

Around 60% of the companies approached for the study confirm having experienced fraud in the past two years. While 14% of these report more than 10 instances of fraud, 75% experienced a maximum of five such mishaps. The losses directly attributable to these frauds ranged between Rs 1 crore and Rs 10 crore for 11% of the companies while 5% peg their losses as exceeding Rs 10 crore.

More than 50% of the country's top executives feel that rise in corporate frauds over the next two years could outpace the efforts to mitigate it, says a recent survey by Deloitte. According to the Deloitte’s India Fraud Survey Report, nearly 56 percent executives believed that incidents of fraud would continue to rise over the next two years. In this scenario the office of the Serious Fraud Investigation Office (SFIO), a fraud investigating agency in India, under the jurisdiction of the Government of India, assumes a great significance in combating this threat of fraud hanging like a loose sword over Corporate India’s head.

Establishment of SFIO [Section 211 of the Companies Act, 2013]

The Section 211 of the newly enacted Companies Act, 2013 provides for the establishment and continuance of the Serious Fraud Investigation Office by giving it authority under the Companies Act, 2013.

The Central Government shall, by notification, establish an office to be called the Serious Fraud investigation office to investigate frauds related to a company. The SFIO has been set up under the aegis of the Ministry of Corporate Affairs. It is conceived as a multi-disciplinary unit capable of investigating corporate white collar crime professionally and is a co-ordinating agency with the Income Tax authorities and the CBI in dealing with corporate fraud.

* The views expressed are personal views of the author and do not necessarily reflect those of the Institute.

The SFIO shall be headed by a Director and consist of experts of following fields from amongst persons of ability, integrity and experience in:

a) Banking, b) Corporate Affairs, c) Taxation, d) Forensic auditing, e) Capital Market, f) Information Technology, g) Law, or (here as ‘or’ and ‘and’ both) h) Other fields.

The idea behind the appointment of these experts is to efficiently discharge the functions of SFIO under the Companies Act, 2013. The Central Government may appoint persons having expertise in the fields of accounting, investigations, cyber forensics, financial accounting, cost accounting, management accounting and any other fields as may be necessary for the efficient discharge of Serious Fraud Investigation Office functions under the Act.

The Director shall be an officer not below to the rank of a Joint Secretary. The Central Government may appoint such officers and other officers and employees in the SFIO as it considers necessary for the efficient discharge of its functions under this Act. The terms and conditions of service of Directors and other officers and employees will be prescribed by the Central Government.

Responsibilities of the SFIO

The SFIO will investigate only “corporate frauds.” The SFIO will only take up investigation of frauds characterized by:

(a) complexity and having inter departmental and multi-disciplinary ramifications; (b) substantial involvement of public interest in terms of monetary misappropriation or in terms of

number of persons affected; and (c) the possibility of investigations leading to, or contributing towards a clear improvement in

systems, laws of procedures.

Status of Existing SFIO

Proviso to S. 211(1) of the 2013 Act provides that the Serious Fraud Investigation Office already set up by the Central Government by its resolution dated 02-07-2003 shall continue to the SFIO for the purpose of Section 211 of the Companies Act, 2013 until a new SFIO as mentioned under the 2013 Act is established.

Investigation into Affairs of a company by SFIO

The provision of this section is in addition to the provision of Section 210. The Central Government may by order assign investigation into the affairs of a company by the Serious Fraud Investigation Office –

(a) On receipt of a report of the Registrar or inspector under Section 208; (b) On intimation of a Special Resolution passed by a company that its affairs are required to

be investigated; (c) In the public interest, or (d) On request from any department of Central Government or State Government.

Once, a case has been assigned to the Serious Fraud Investigation Office, the same case shall not be investigated by any other department of Central Government or State Government and all existing investigation shall also be transferred to the Serious Fraud Investigation Office. The Director may

designate such number of inspectors as he may consider necessary for the purpose of such investigation.

Once the investigation into the affairs of the company has been assigned by the Central Government to the Serious Fraud Investigation Office, it shall conduct the investigation in the manner prescribed and follow proper procedure provided in this chapter.

The Investigation Officer of the Serious Fraud Investigation Office has power of inspector under Section 217 of the Companies Act, 2013. No firm, body corporate or other association shall be appointed as an inspector.

Provision of Section 210, 213 and 216 shall be applicable to the company, its officer and employees. It shall be their responsibility to provide all information, explanation, documents and assistance to the Investigation Officer as he may require for conduct of the investigation.

The Offence contained under the Companies Act, which attract punishment for fraud under Section 447 of the Act, shall be cognizable and non – bailable. The Special court shall not take cognizance of any office but upon a complaint in writing made by –

(a) The Director, Serious Fraud Investigation Office; or (b) Any officer of the Central Government authorised by a general or special order in writing in this

behalf.

The Director, Additional Director or Assistant Director of Serious Fraud Investigation Office are empowered to arrest a person. They shall inform the person so arrested the grounds for such arrest as soon as it may be. Further, the Director, Additional Director or Assistant Director of SFIO, as the case may be, shall immediately after arrest of such person forward a copy of the order of arrest to the SFIO in a sealed envelope in such manner as may be prescribed.

Every person so arrested shall within twenty four hours be taken to a Judicial Magistrate or Metropolitan Magistrate having jurisdiction and on completion of the investigation, the SFIO shall submit the investigation report to the Central Government. Where Central Government direct to submit an interim report, then such interim report shall also be submitted to the Central Government. On receipt of the investigation report, the Central Government may direct the SFIO to initiate prosecution against the company and its past or present officers or employees or any other person directly or indirectly connected with the affairs of the company. A copy of the above mentioned investigation report may be obtained by any person concerned by making an application in this regard to the court.

Section 212 of the Companies Act, 2013 provides statutory status to SFIO and lays down procedure for investigation by SFIO. Detailed powers have been laid down with regard to assignment of cases of fraud by the Central Government, procedure of investigation and making of report by the SFIO. The Investigation report of SFIO has been accorded the status of a report filed by the police officer under section 173 of the Code of Criminal Procedure, 1973 when filed with the Special Court for framing of charges.

With respect to the transfer of cases to SFIO for investigation, it may be noted that the aim of setting up of the SFIO is to investigate into the affairs of companies involved in fraud. The focus is to ensure proper investigation into cases of fraud by employing experts from various fields. Thus, investigation into cases involving fraudulent conduct of affairs in various fields will be transferred to SFIO. However this would not imply that any case under investigation under other special statutes like Customs Act or Income Tax and other similar laws, would also be transferred to SFIO.

Effect of SFIO on Corporate Landscape

Findings of a survey conducted by Deloitte have showed that a majority of respondents in a survey on corporate fraud felt that a strict regulatory environment, particularly legislations like the new Companies Act, could help reduce instances of fraud in the future.

The Companies Act 2013 was identified as a key legislation that could accomplish a strict corporate regulatory environment and provisions such as the mandatory establishment of a vigil mechanism for listed companies, and greater accountability on board and directors to prevent and detect fraud. However, responses indicated that limited efforts were being taken to comply with these provisions. To detect fraud, survey respondents indicated relying on internal audit reviews (62 percent), whistle blower hotlines (53 percent) and IT Controls (51 percent). However, the survey noted that actions taken upon the detection of fraud "continue to remain conservative".

Stricter norms of corporate governance under the Companies Act, 2013 as well as increasing application of technology for early detection of frauds through data analysis surveillance and usage of forensic tool are among the other steps taken by the government to prevent fraud by companies. A Market Research and Analysis Unit has been set up in SFIO to analyse media reports relating to financial frauds and for conducting market surveillance of such corporates. Further, in order to strengthen MRAU's functioning, an expert committee was constituted and on the basis of its recommendations a forensic lab with appropriate technology and skilled technical manpower has been set up in SFIO.

Case Study

Satyam Scam: The Serious Fraud Investigation Office conducted its inquiry and investigation into the Satyam scam. It concluded that the Independent Directors of the Company were not involved in the multi-crore accounting fraud in the company and were kept in the dark by the Chairman Ramalinga Raju. The SFIO submitted a 14000 page report after 3 months of investigation into the scam. The SFIO was well appreciated for its investigation and report on the Satyam scam.

Reebok Fraud Case: According to SFIO’s complaint, the modus operandi of the fraud involved filing fictitious invoices to show inflated sales, recording fictitious sales by raising prices of goods sold, premature recognition of revenue and bills raised but goods not dispatched, etc.

SFIO investigations reveal Reebok India ran a “franchisee referral programme”, through which it collected Rs 88.11 crores from 60-odd high net worth individuals, including former attorney general Soli J Sorabjee, promising interest of 16-20 per cent. The SFIO investigators say these funds were recycled by Reebok India employees as part of effort to boost cash flow.

SFIO said there was a lapse in corporate governance practices at Reebok India by the Adidas group, citing instances of Section 58A of the Companies Act being violated, forensic reports ignored, internal control failure and no heed to Foreign Investment Promotion Board norms. SFIO didn’t state a final figure for the fraud at Reebok India. It relied on the figure of $221 million (Rs 1,477 core) cited by Adidas as its stated losses in its 2012 annual report.

Conclusion

The Serious Fraud Investigation Office has been given statutory recognition under the Companies Act, 2013. This has enhanced the reputation of the SFIO and brought it on par with other Central Government investigating agencies. Global companies are increasingly realising that corruption is the biggest threat to do business in India. As a result, they are investing in building up controls and processes that address the direct and indirect risks of corruption and bribery in India. The office of the SFIO has assumed greater significance in India’s fight against corporate fraud which casts a pall of gloom over the business environment of India. It is being considered as India’s sword arm to cut off and destroy corporate fraud which is causing losses and heartburn to many people in India today.

***

Circulars, Notifications, Orders, Amendments

.

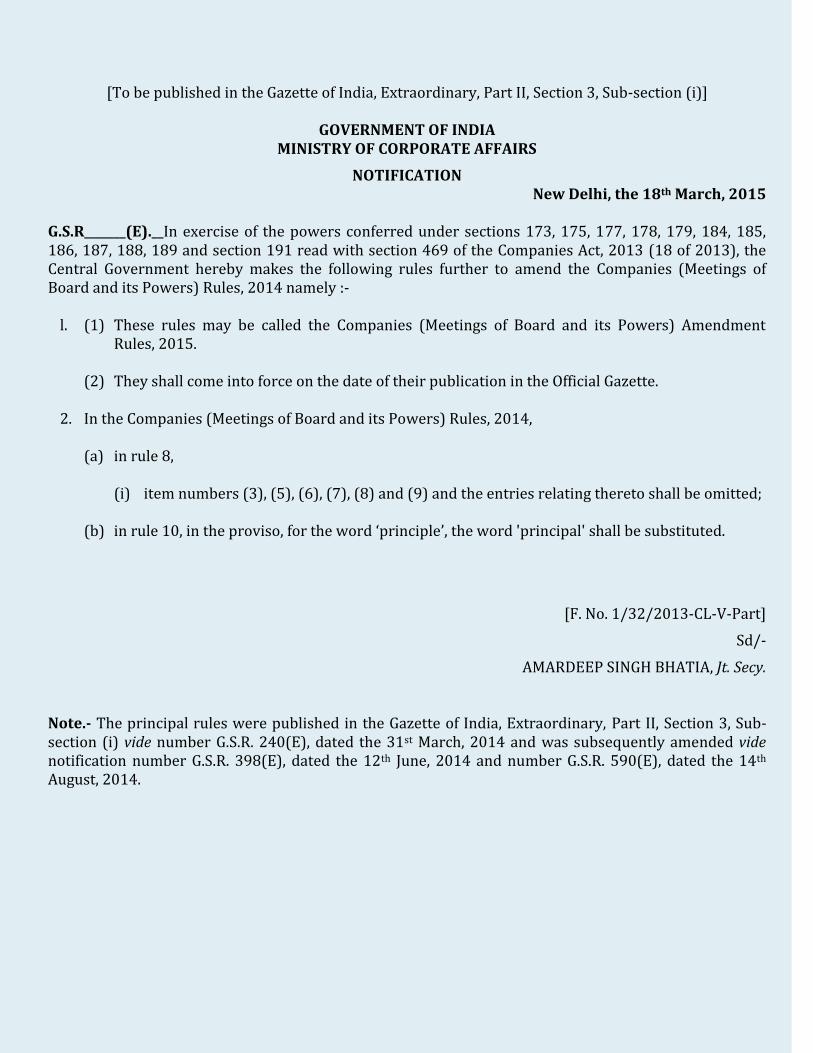

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)]

GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS

NOTIFICATION New Delhi, the 18th March, 2015

G.S.R_______(E).__In exercise of the powers conferred under sections 173, 175, 177, 178, 179, 184, 185, 186, 187, 188, 189 and section 191 read with section 469 of the Companies Act, 2013 (18 of 2013), the Central Government hereby makes the following rules further to amend the Companies (Meetings of Board and its Powers) Rules, 2014 namely :-

l. (1) These rules may be called the Companies (Meetings of Board and its Powers) Amendment Rules, 2015.

(2) They shall come into force on the date of their publication in the Official Gazette. 2. In the Companies (Meetings of Board and its Powers) Rules, 2014, (a) in rule 8, (i) item numbers (3), (5), (6), (7), (8) and (9) and the entries relating thereto shall be omitted; (b) in rule 10, in the proviso, for the word ‘principle’, the word 'principal' shall be substituted.

[F. No. 1/32/2013-CL-V-Part]

Sd/-

AMARDEEP SINGH BHATIA, Jt. Secy.

Note.- The principal rules were published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i) vide number G.S.R. 240(E), dated the 31st March, 2014 and was subsequently amended vide notification number G.S.R. 398(E), dated the 12th June, 2014 and number G.S.R. 590(E), dated the 14th August, 2014.

[To be published in the Gazette of India, Extraordinary, part II, Section 3, Sub section (i)]

Government of India Ministry of Corporate Affairs

Notification

New Delhi, Dated 18th March, 2015

G.S.R. _(E).- In exercise of the powers conferred under sub-clause (ii) of clause (a) of section 43, sub-clause (d) of sub-section (1) of section 54, sub-section (2) of section 55, sub-section (l) of section 56, sub-section (3) of section 56, sub-section (1) of section 62, sub-section (2) of section 42, clause (f) of sub-section (2) of section 63, sub-section (1) of section 64 , clause (b) of sub-section (3) of section 67, sub-section (2) of section 68, sub-section (6) of section 68, sub-section (9) of section 68, sub-section (10) of section 68, sub-section (3) of section 71, sub-section (6) of section 71, sub-section (13) of section 71 and sub-sections (1) and (2) of section 72, read, with sub-sections (1) and (2) of section 469 of the Companies Act, 2013 (18 of 2013), the Central Government hereby makes the following rules further to amend the Companies (Share Capital and Debentures) Rules, 2014, namely:-

1. (1) These rules may be called the Companies (Share Capital and Debentures) Amendment Rules, 2015.

(2) They shall come into force from the date of their publication in the Official Gazette.

2. In the Companies (Share Capital and Debenture) Rules, 2014,-

(1) for rule 3, the following rule shall be substituted namely:-

3. Application- The provisions of these rules shall apply to -

(a) all unlisted public companies;

(b) all private companies: and

(c) listed companies so far as they do not contradict or conflict with any other regulation framed in this regard by the Securities and Exchange Board of India;

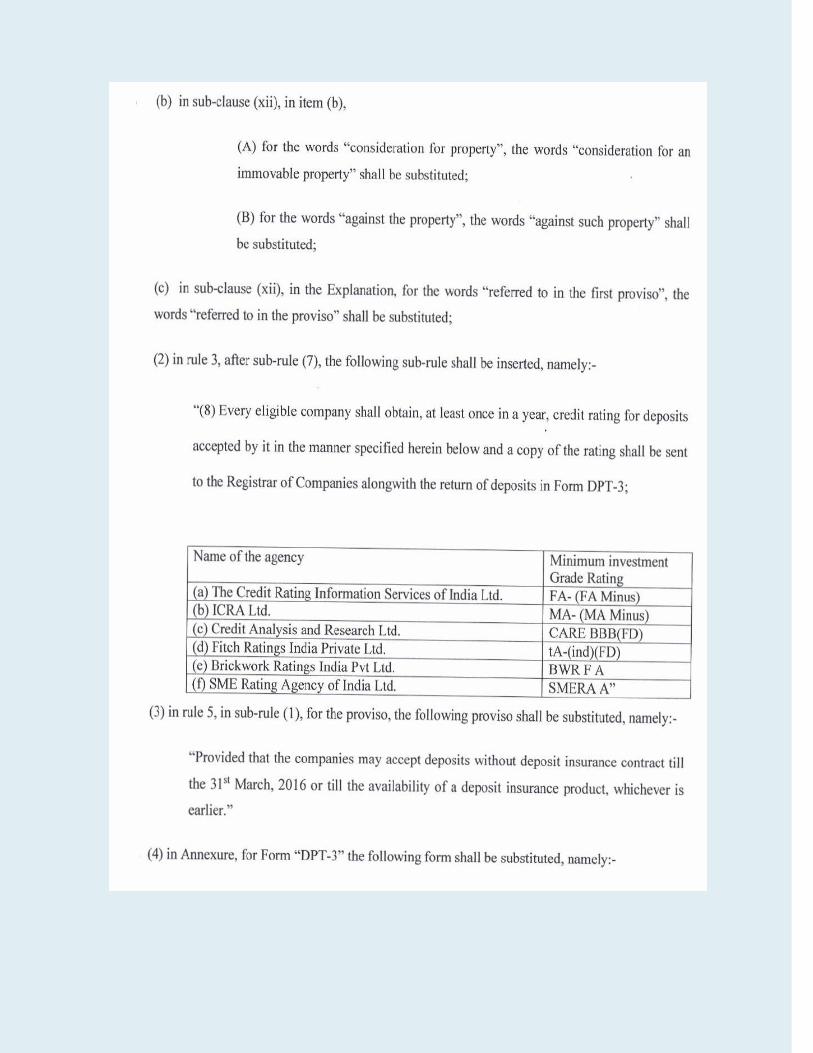

(2) in rule 5, in sub-rule (3), in clause (b),

(a) the first proviso shall be omitted;

(b) in the second proviso for the words "provided further that", the words “provided that” shall be substituted;

(c) in the third proviso for the words "provided also that" the words “provided further that” shall be substituted;

(3) in rule 6, in sub-rule (2), in clause (c), for the words “within fifteen days”, the words "within forty-five days" shall be substituted;

(4) in rule 12, in sub-rule (1), in the Explanation, in clause (c), the words “or of an associate company” shall be omitted;

(5) in rule 13, in sub-rule (1), -

(a) in the proviso, for the words “provided that” the words “provided further that" shall be substituted and before the proviso as so amended, the following proviso shall be inserted namely:-

"Provided that in case of any preferential offer made by a company to one or more existing members only, the provisions of sub-rule (1) and proviso to sub-rule (3) of rule 14 of Companies (Prospectus and Allotment of Securities) Rules, 2014 shall not apply."

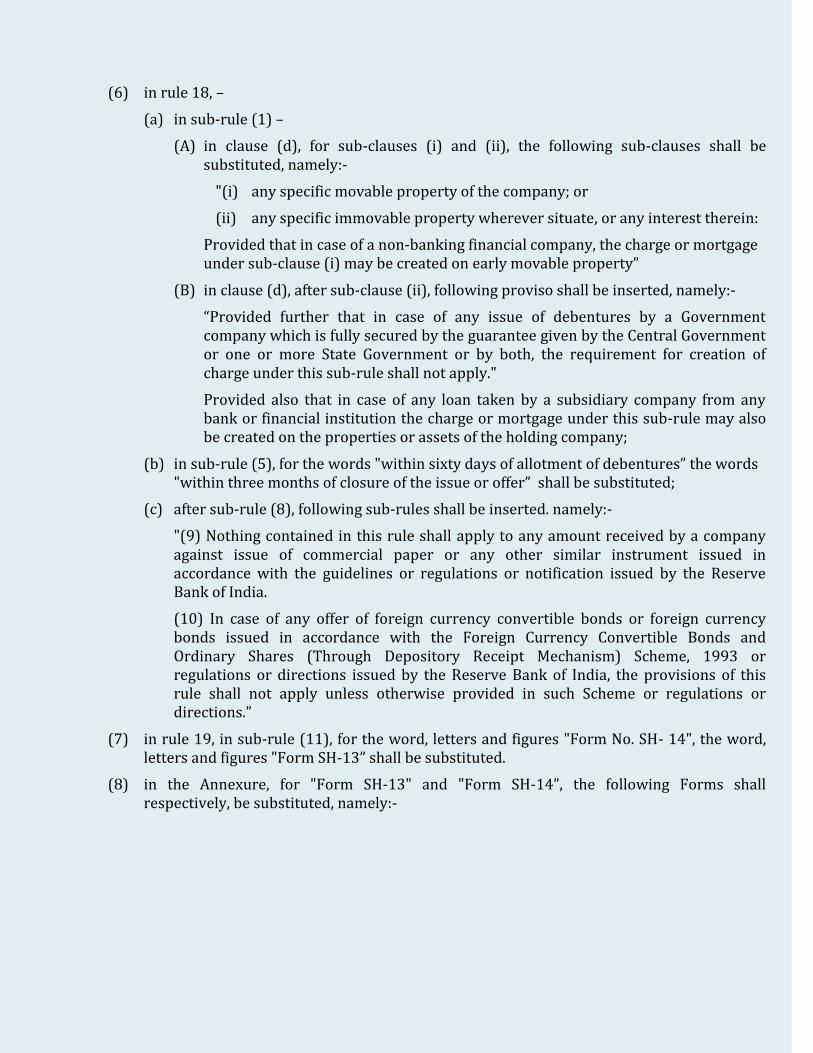

(6) in rule 18, –

(a) in sub-rule (1) –

(A) in clause (d), for sub-clauses (i) and (ii), the following sub-clauses shall be substituted, namely:-

"(i) any specific movable property of the company; or

(ii) any specific immovable property wherever situate, or any interest therein:

Provided that in case of a non-banking financial company, the charge or mortgage under sub-clause (i) may be created on early movable property”

(B) in clause (d), after sub-clause (ii), following proviso shall be inserted, namely:-

“Provided further that in case of any issue of debentures by a Government company which is fully secured by the guarantee given by the Central Government or one or more State Government or by both, the requirement for creation of charge under this sub-rule shall not apply."

Provided also that in case of any loan taken by a subsidiary company from any bank or financial institution the charge or mortgage under this sub-rule may also be created on the properties or assets of the holding company;

(b) in sub-rule (5), for the words "within sixty days of allotment of debentures” the words "within three months of closure of the issue or offer” shall be substituted;

(c) after sub-rule (8), following sub-rules shall be inserted. namely:-

"(9) Nothing contained in this rule shall apply to any amount received by a company against issue of commercial paper or any other similar instrument issued in accordance with the guidelines or regulations or notification issued by the Reserve Bank of India.

(10) In case of any offer of foreign currency convertible bonds or foreign currency bonds issued in accordance with the Foreign Currency Convertible Bonds and Ordinary Shares (Through Depository Receipt Mechanism) Scheme, 1993 or regulations or directions issued by the Reserve Bank of India, the provisions of this rule shall not apply unless otherwise provided in such Scheme or regulations or directions.”

(7) in rule 19, in sub-rule (11), for the word, letters and figures "Form No. SH- 14", the word, letters and figures "Form SH-13” shall be substituted.

(8) in the Annexure, for "Form SH-13" and "Form SH-14”, the following Forms shall respectively, be substituted, namely:-

Form No. SH-13

Nomination Form

[Pursuant to section, 72 of the Companies Act, 2013 and rule 19(1) of the Companies (Share Capital and Debentures) Rules 20I4]

To Name of the company: Address of the company: l/We ......................................... the holder(s) of the securities particulars of which are given hereunder wish to make nomination and do hereby nominate the following persons in whom shall vest, all the rights in respect of such securities in the event of my/our death.

(1) PARTICULARS OF THE SECURITIES (in respect of which nomination is being made) Nature of Securities

Folio No. No. of securities Certificate No. Distinctive No.

(2) PARTICULARS OF NOMINEE/S –

(a) Name:

(b) Date of Birth:

(c) Father's/Mother’s/Spouse's name:

(d) Occupation:

(e) Nationality:

(f) Address:

(g) E-mail id:

(h) Relationship with the security holder:

(3) IN CASE NOMINEE IS A MINOR—

(a) Date of birth: (b) Date of attaining majority (c) Name of guardian: (d) Address of guardian:

(4) PARTICULARS OF NOMINEE IN CASE MINOR NOMINEE DIES BEFORE ATTAINING AGE OF MAJORITY

(a) Name:

(b) Date of Birth

(c) Father’s/Mother’s/Spouse's name:

(d) Occupation:

(e) Nationality:

(f) Address:

(g) E-mail id:

(h) Relationship with the security holder: (i) Relationship with the minor nominee

Name:

Address:

Name of the Security Signature Witness with name and address Holder (s)

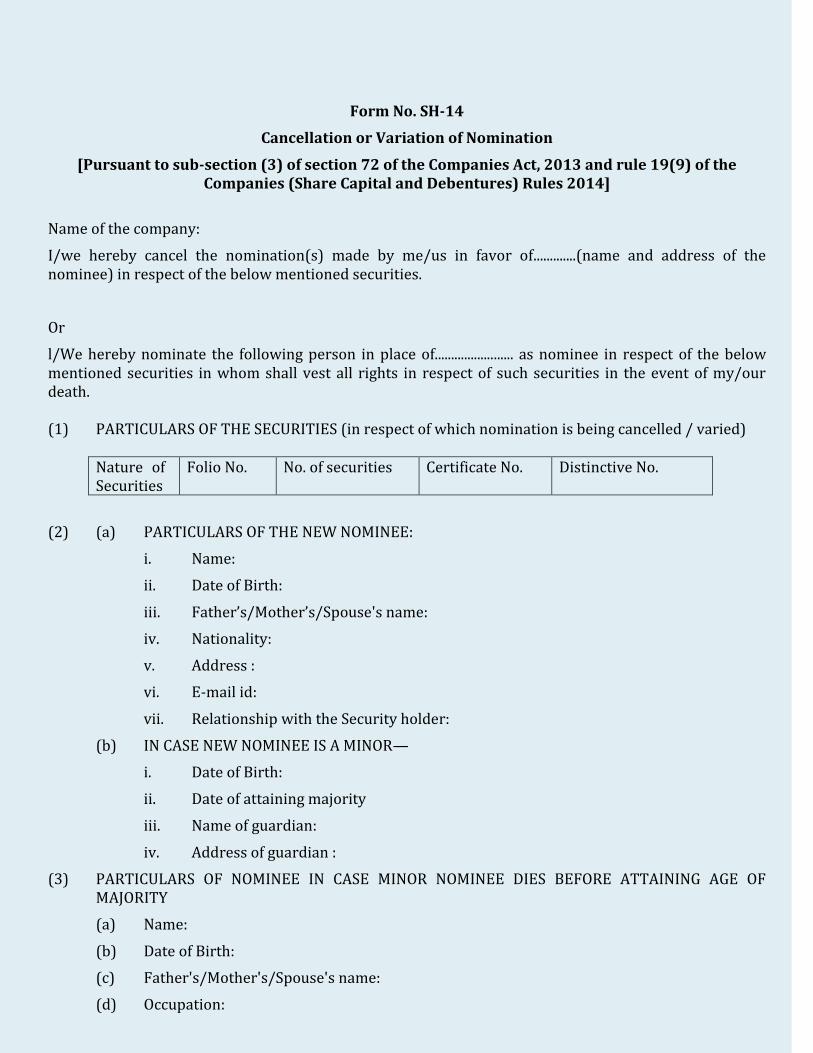

Form No. SH-14

Cancellation or Variation of Nomination

[Pursuant to sub-section (3) of section 72 of the Companies Act, 2013 and rule 19(9) of the Companies (Share Capital and Debentures) Rules 2014]

Name of the company:

I/we hereby cancel the nomination(s) made by me/us in favor of.............(name and address of the nominee) in respect of the below mentioned securities.

Or

l/We hereby nominate the following person in place of........................ as nominee in respect of the below mentioned securities in whom shall vest all rights in respect of such securities in the event of my/our death. (1) PARTICULARS OF THE SECURITIES (in respect of which nomination is being cancelled / varied)

Nature of Securities

Folio No. No. of securities Certificate No. Distinctive No.

(2) (a) PARTICULARS OF THE NEW NOMINEE:

i. Name:

ii. Date of Birth:

iii. Father’s/Mother’s/Spouse's name:

iv. Nationality:

v. Address :

vi. E-mail id:

vii. Relationship with the Security holder:

(b) IN CASE NEW NOMINEE IS A MINOR—

i. Date of Birth:

ii. Date of attaining majority

iii. Name of guardian:

iv. Address of guardian :

(3) PARTICULARS OF NOMINEE IN CASE MINOR NOMINEE DIES BEFORE ATTAINING AGE OF MAJORITY

(a) Name:

(b) Date of Birth:

(c) Father's/Mother's/Spouse's name:

(d) Occupation:

(e) Nationality:

(f) Address:

(g) E-mail id:

(h) Relationship with the security holder (i) Relationship with the minor nominee

Signature

Name of the Security

Holder (s)

Witness with name and address

[F. No. 1/4/2013-CL-V (Pt I)]

Sd/- Amardeep S. Bhatia

(Joint Secretary) Note. - The principal rules were published in the Gazette of India, Part II, section 3, sub-section (i) vide number GSR 265(E) dated 31st March, 2014 and subsequently amended vide GSR Number 413 (E) dated 18th June, 2014.

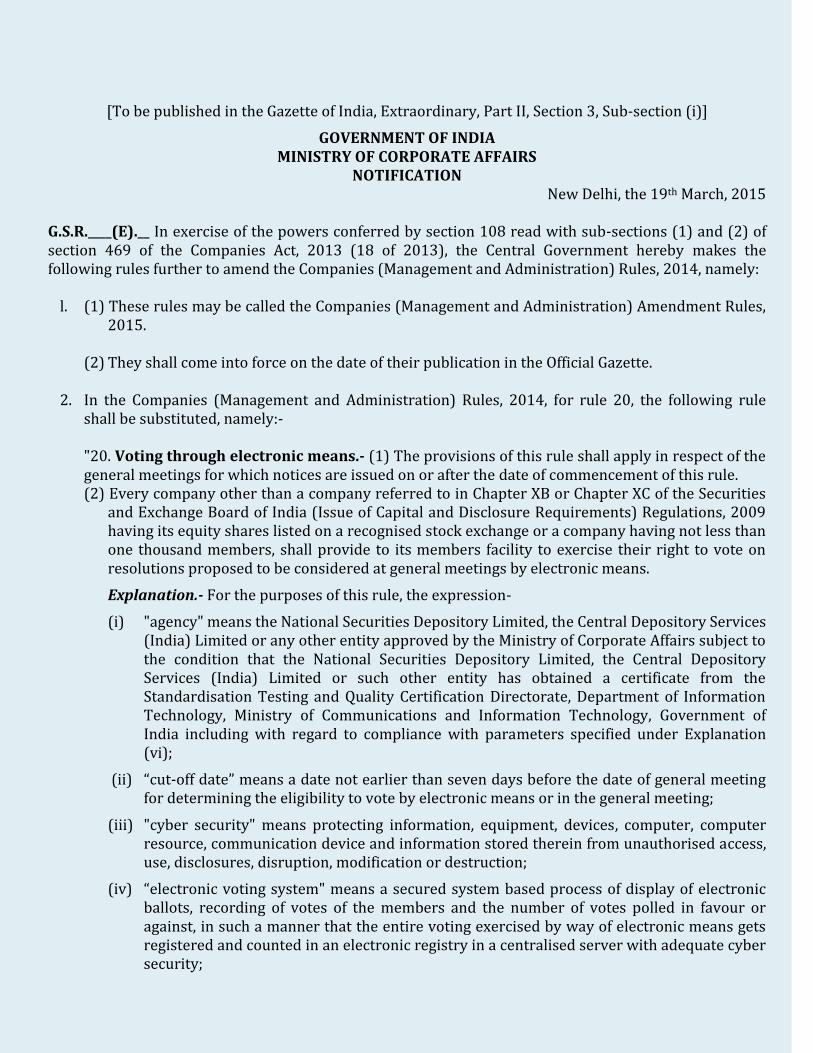

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)]

GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS

NOTIFICATION New Delhi, the 19th March, 2015

G.S.R.____(E).__ In exercise of the powers conferred by section 108 read with sub-sections (1) and (2) of section 469 of the Companies Act, 2013 (18 of 2013), the Central Government hereby makes the following rules further to amend the Companies (Management and Administration) Rules, 2014, namely:

l. (1) These rules may be called the Companies (Management and Administration) Amendment Rules, 2015.

(2) They shall come into force on the date of their publication in the Official Gazette. 2. In the Companies (Management and Administration) Rules, 2014, for rule 20, the following rule

shall be substituted, namely:-

"20. Voting through electronic means.- (1) The provisions of this rule shall apply in respect of the general meetings for which notices are issued on or after the date of commencement of this rule.

(2) Every company other than a company referred to in Chapter XB or Chapter XC of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009 having its equity shares listed on a recognised stock exchange or a company having not less than one thousand members, shall provide to its members facility to exercise their right to vote on resolutions proposed to be considered at general meetings by electronic means.

Explanation.- For the purposes of this rule, the expression-

(i) "agency" means the National Securities Depository Limited, the Central Depository Services (India) Limited or any other entity approved by the Ministry of Corporate Affairs subject to the condition that the National Securities Depository Limited, the Central Depository Services (India) Limited or such other entity has obtained a certificate from the Standardisation Testing and Quality Certification Directorate, Department of Information Technology, Ministry of Communications and Information Technology, Government of India including with regard to compliance with parameters specified under Explanation (vi);

(ii) “cut-off date” means a date not earlier than seven days before the date of general meeting for determining the eligibility to vote by electronic means or in the general meeting;

(iii) "cyber security" means protecting information, equipment, devices, computer, computer resource, communication device and information stored therein from unauthorised access, use, disclosures, disruption, modification or destruction;

(iv) “electronic voting system" means a secured system based process of display of electronic ballots, recording of votes of the members and the number of votes polled in favour or against, in such a manner that the entire voting exercised by way of electronic means gets registered and counted in an electronic registry in a centralised server with adequate cyber security;

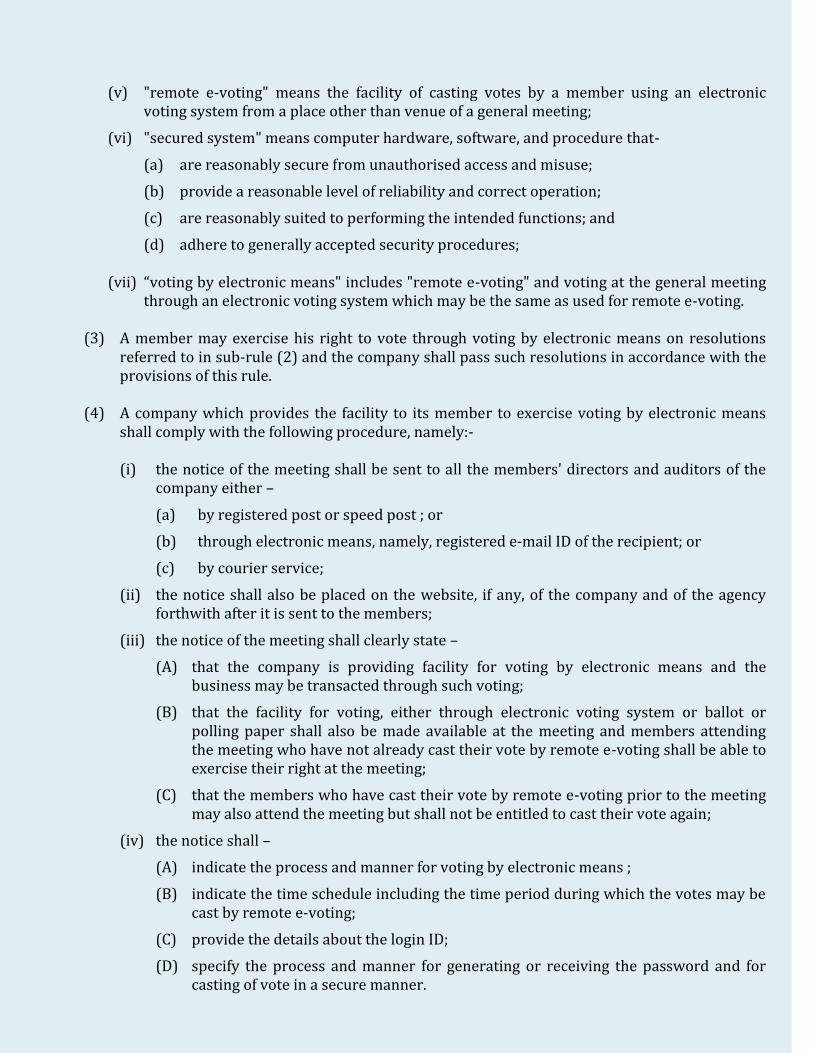

(v) "remote e-voting" means the facility of casting votes by a member using an electronic voting system from a place other than venue of a general meeting;

(vi) "secured system" means computer hardware, software, and procedure that-

(a) are reasonably secure from unauthorised access and misuse;

(b) provide a reasonable level of reliability and correct operation;

(c) are reasonably suited to performing the intended functions; and

(d) adhere to generally accepted security procedures; (vii) “voting by electronic means" includes "remote e-voting" and voting at the general meeting

through an electronic voting system which may be the same as used for remote e-voting.

(3) A member may exercise his right to vote through voting by electronic means on resolutions referred to in sub-rule (2) and the company shall pass such resolutions in accordance with the provisions of this rule.

(4) A company which provides the facility to its member to exercise voting by electronic means

shall comply with the following procedure, namely:-

(i) the notice of the meeting shall be sent to all the members' directors and auditors of the company either –

(a) by registered post or speed post ; or

(b) through electronic means, namely, registered e-mail ID of the recipient; or

(c) by courier service;

(ii) the notice shall also be placed on the website, if any, of the company and of the agency forthwith after it is sent to the members;

(iii) the notice of the meeting shall clearly state –

(A) that the company is providing facility for voting by electronic means and the business may be transacted through such voting;

(B) that the facility for voting, either through electronic voting system or ballot or polling paper shall also be made available at the meeting and members attending the meeting who have not already cast their vote by remote e-voting shall be able to exercise their right at the meeting;

(C) that the members who have cast their vote by remote e-voting prior to the meeting may also attend the meeting but shall not be entitled to cast their vote again;

(iv) the notice shall –

(A) indicate the process and manner for voting by electronic means ;

(B) indicate the time schedule including the time period during which the votes may be cast by remote e-voting;

(C) provide the details about the login ID;

(D) specify the process and manner for generating or receiving the password and for casting of vote in a secure manner.

(v) the company shall cause a public notice by way of an advertisement to be published, immediately on completion of despatch of notices for the meeting under clause (i) of sub-rule (4) but at least twenty-one days before the date of general meeting, at least once in a vernacular newspaper in the principal vernacular language of the district in which the registered office of the company is situated, and having a wide circulation in that district, and at least once in English language in an English newspaper having country-wide circulation, and specifying in the said advertisement, inter alia, the following matters namely :-

(a) statement that the business may be transacted through voting by electronic means;

(b) the date and time of commencement of remote e-voting;

(c) the date and time of end of remote e-voting;

(d) cut-off date;

(e) the manner in which persons who have acquired shares and become members of

the company after the despatch of notice may obtain the login ID and password;

(f) the statement that –

(A) remote e-voting shall not be allowed beyond the said date and time;

(B) the manner in which the company shall provide for voting by members present at the meeting; and

(C) a member may participate in the general meeting even after exercising his right to vote through remote e-voting but shall not be allowed to vote again in the meeting; and

(D) a person whose name is recorded in the register of members or in the register of beneficial owners maintained by the depositories as on the cut-off date only shall be entitled to avail the facility of remote e-voting as well as voting in the general meeting;

(g) website address of the company, if any, and of the agency where notice of the meeting is displayed; and

(h) name, designation, address, email id and phone number of the person responsible to address the grievances connected with facility for voting by electronic means:

Provided that the public notice shall be placed on the website of the company, if any, and of the agency;

(vi) the facility for remote e-voting shall remain open for not less than thee days and shall close at 5.00 p.m. on the date preceding the date of general meeting;

(vii) during the period when facility for remote e-voting is provided, the members of the company, holding shares either in physical form or in dematerialised form, as on the cut-off date, may opt for remote e-voting:

Provided that once the vote on a resolution is cast by the member, he shall not be allowed to change it subsequently or cast the vote again;

Provided further that a member may participate in the general meeting even after exercising his right to vote through remote e-voting but shall not be allowed to vote again;

(viii) at the end of the remote e-voting period, the facility shall forthwith be blocked:

Provided that if a company opts to provide the same electronic voting system as used

during remote e-voting during the general meeting, the said facility shall be in operation till all the resolutions are considered and voted upon in the meeting and may be used for voting only by the members attending the meeting and who have not exercised their right to vote through remote e-voting.

(ix) the Board of Directors shall appoint one or more scrutiniser, who may be Chartered

Accountant in practice, Cost Accountant in practice, or Company Secretary in practice or an Advocate or any other person who is not in employment of the company and is a person of repute who, in the opinion of the Board can scrutinize the voting and remote e-voting process in a fair and transparent manner:

Provided that the scrutiniser so appointed may take assistance of a person who is not in employment of the company and who is well-versed with the electronic voting system;

(x) the scrutiniser shall be willing to be appointed and be available for the purpose of ascertaining the requisite majority;

(xi) the Chairman shall, at the general meeting. at the end of discussion on the resolutions on

which voting is to be held, allow voting as provided in clauses (a) to (h) of sub-rule (1) of rule 21, as applicable, with the assistance of scrutiniser, by use of ballot or polling paper or by using an electronic voting system for all those members who are present at the general meeting but have not cast their votes by availing the remote e-voting facility.

(xii) the scrutiniser shall, immediately after the conclusion of voting at the general meeting,

first count the votes cast at the meeting, thereafter unblock the votes cast through remote e-voting in the presence of at least two witnesses not in the employment of the company and make, not later than three days of conclusion of the meeting, a consolidated scrutiniser's report of the total votes cast in favour or against, if any, to the Chairman or a person authorised by him in writing who shall countersign the same:

Provided that the Chairman or a person authorised by him in writing shall declare the result of the voting forthwith;

Explanation.- It is hereby clarified that the manner in which members have cast their votes, that is, affirming or negating the resolution, shall remain secret and not available to the Chairman, Scrutiniser or any other person till the votes are cast in the meeting.

(xiii) For the purpose of ensuring that members who have cast their votes through remote e-voting do not vote again at the general meeting, the scrutiniser shall have access, after the closure of period for remote e-voting and before the start of general meeting, to details relating to members, such as their names, folios, number of shares held and such other information that the scrutiniser may require, who have cast votes through remote e-voting but not the manner in which they have cast their votes:

(xiv) the scrutiniser shall maintain a register either manually or electronically to record the assent or dissent received, mentioning the particulars of name, address, folio number or

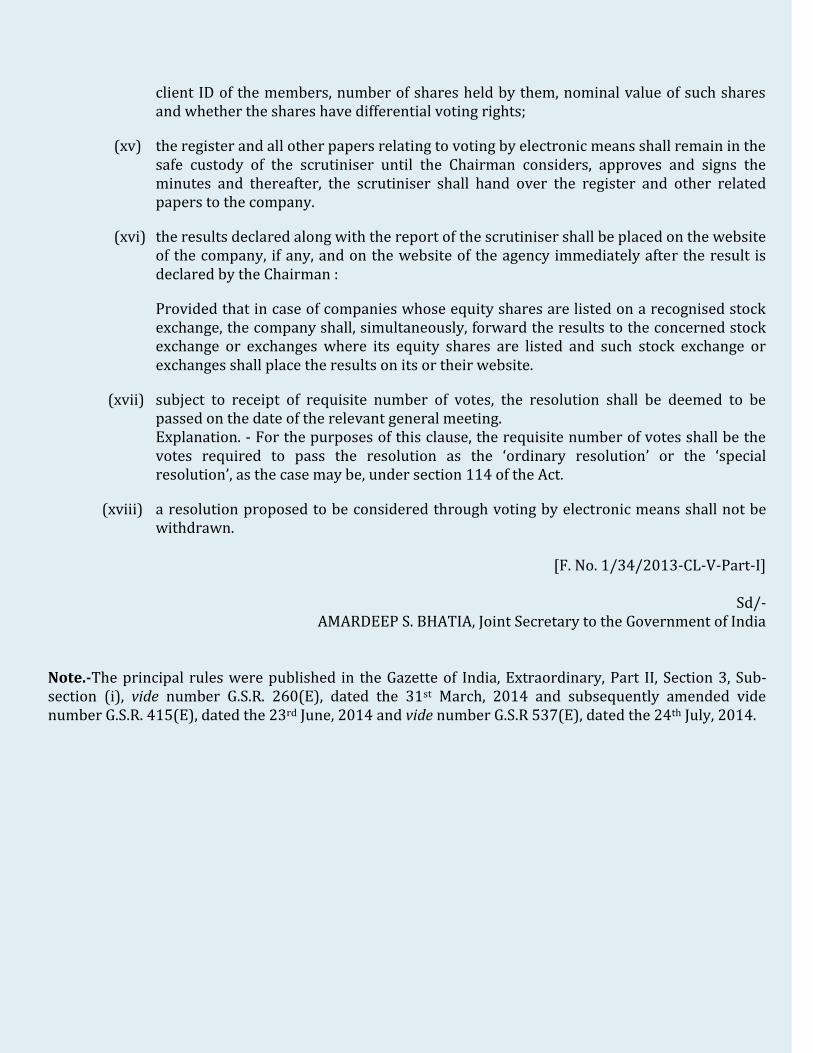

client ID of the members, number of shares held by them, nominal value of such shares and whether the shares have differential voting rights;

(xv) the register and all other papers relating to voting by electronic means shall remain in the safe custody of the scrutiniser until the Chairman considers, approves and signs the minutes and thereafter, the scrutiniser shall hand over the register and other related papers to the company.

(xvi) the results declared along with the report of the scrutiniser shall be placed on the website of the company, if any, and on the website of the agency immediately after the result is declared by the Chairman :

Provided that in case of companies whose equity shares are listed on a recognised stock exchange, the company shall, simultaneously, forward the results to the concerned stock exchange or exchanges where its equity shares are listed and such stock exchange or exchanges shall place the results on its or their website.

(xvii) subject to receipt of requisite number of votes, the resolution shall be deemed to be passed on the date of the relevant general meeting. Explanation. - For the purposes of this clause, the requisite number of votes shall be the votes required to pass the resolution as the ‘ordinary resolution’ or the ‘special resolution’, as the case may be, under section 114 of the Act.

(xviii) a resolution proposed to be considered through voting by electronic means shall not be withdrawn.

[F. No. 1/34/2013-CL-V-Part-I]

Sd/-

AMARDEEP S. BHATIA, Joint Secretary to the Government of India Note.-The principal rules were published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 260(E), dated the 31st March, 2014 and subsequently amended vide number G.S.R. 415(E), dated the 23rd June, 2014 and vide number G.S.R 537(E), dated the 24th July, 2014.

[To be published in the Gazette of India, Extraordinary, Part II Section 3, Sub-section (ii)]

Government of India

Ministry of Corporate Affairs

NOTIFICATION Shastri Bhawan, ‘A’ Wing, 5th Floor,

New Delhi, the 24th March, 2015

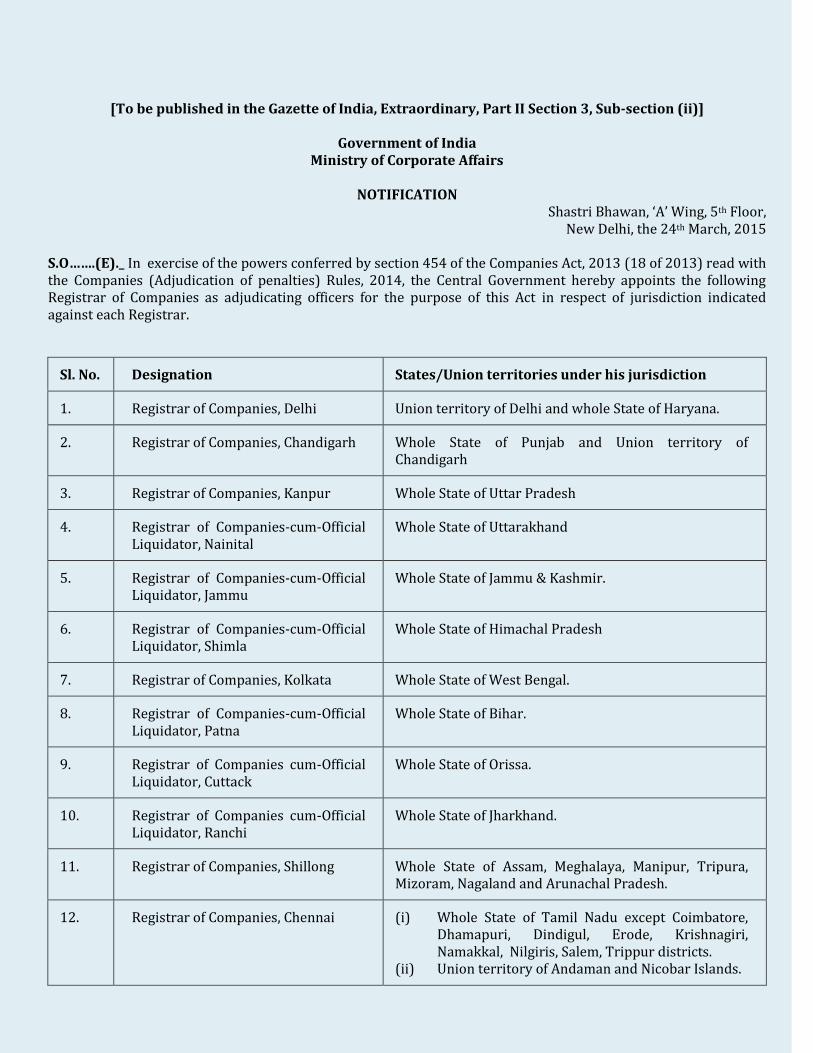

S.O…….(E)._ In exercise of the powers conferred by section 454 of the Companies Act, 2013 (18 of 2013) read with the Companies (Adjudication of penalties) Rules, 2014, the Central Government hereby appoints the following Registrar of Companies as adjudicating officers for the purpose of this Act in respect of jurisdiction indicated against each Registrar.

Sl. No. Designation States/Union territories under his jurisdiction

1. Registrar of Companies, Delhi Union territory of Delhi and whole State of Haryana.

2. Registrar of Companies, Chandigarh Whole State of Punjab and Union territory of Chandigarh

3. Registrar of Companies, Kanpur Whole State of Uttar Pradesh

4. Registrar of Companies-cum-Official Liquidator, Nainital

Whole State of Uttarakhand

5. Registrar of Companies-cum-Official Liquidator, Jammu

Whole State of Jammu & Kashmir.

6. Registrar of Companies-cum-Official Liquidator, Shimla

Whole State of Himachal Pradesh

7. Registrar of Companies, Kolkata Whole State of West Bengal.

8. Registrar of Companies-cum-Official Liquidator, Patna

Whole State of Bihar.

9. Registrar of Companies cum-Official Liquidator, Cuttack

Whole State of Orissa.

10. Registrar of Companies cum-Official Liquidator, Ranchi

Whole State of Jharkhand.

11. Registrar of Companies, Shillong Whole State of Assam, Meghalaya, Manipur, Tripura, Mizoram, Nagaland and Arunachal Pradesh.

12. Registrar of Companies, Chennai (i) Whole State of Tamil Nadu except Coimbatore, Dhamapuri, Dindigul, Erode, Krishnagiri, Namakkal, Nilgiris, Salem, Trippur districts.

(ii) Union territory of Andaman and Nicobar Islands.

13. Registrar of Companies, Coimbatore Coimbatore, Dharmapuri, Dindigul, Erode, Krishnagiri, Namakkal, Nilgiris, Salem, Trippur districts

14. Registrar of Companies, Puducherry Union territory of Puducherry

15. Registrar of Companies, Ernakulam Whole State of Kerala and Union territory of Lakshwadweep Islands

16. Registrar of Companies, Hyderabad Whole State of Andhra Pradesh and Telangana.

17. Registrar of Companies, Bangalore Whole State of Karnataka.

18. Registrar of Companies, Mumbai Whole State of Maharashtra except Pune, Ahmednagar, Kolhapur, Solahpur, Satara, Sangli, Ratnagiri, Sindhudurg.

19. Registrar of Companies, Pune Pune, Ahmednagar, Kolhapur, Solahpur, Satara, Sangli, Ratnagiri, Sindhudurg districts the State of Maharashtra.

20. Registrar of Companies cum-Official Liquidator, Goa

Whole State of Goa and Union territory of Daman and Diu.

21. Registrar of Companies, Ahmedabad Whole State of Gujarat and Union territory of Dadra and Nagar Haveli.

22. Registrar of Companies, Gwalior Whole State of Madhya Pradesh.

23. Registrar of Companies –cum-Official Liquidator, Bilaspur

Whole State of Chhattisgarh.

24. Registrar of Companies–cum-Official Liquidator, Jaipur

Whole State of Rajasthan.

2. The Appeals, if any, filed before the concerned Regional Director having jurisdiction over the adjudicating offices shall be disposed of in accordance with the notification of Government of India in the Ministry of Corporate affairs published in the Gazette of India, Extraordinary, Part II, Section 3 Sub-section (i), vide number G.S.R. 887 (E), dated the 14th December, 2011 and G.S.R. 763 (E), dated the 15th October, 2012. 3. This notification shall come into force with immediate effect.

[F.No. A-42011/112/2014-Ad.II]

Sd/- (AMARDEEP SINGH BHATIA)

Joint Secretary to the Government of India

© The Institute of Company Secretaries of India.

All rights reserved. No part of this Journal may be translated or copied in any form or by any means without

the prior written permission of The Institute of Company Secretaries of India.

Disclaimer :

Although due care and diligence have been taken in preparation and uploading this e-journal, the Institute shall not be responsible for any loss or damage, resulting from any action taken on the basis of the contents of this e-journal. Any one wishing to act on the basis of the material contained herein should do so after cross checking with the original source. For views/suggestions/feedback please write to : [email protected].

Editorial Advisory Board

Mr. R. R. Shastri, Legal Advisor, Tata Sons Ltd.

Mr. V Sreedharan, Practising Company Secretary

Ms. Sonia Baijal, Director (Academics), ICSI

Mr. A K Sil, Joint Director (Academics), ICSI

Dr. Rahul Chandra, Joint Director (Academics), ICSI

Articles / Reviews invited for e-CS Nitor

We invite the members to contribute articles/checklist/reviews/points of view or any other relevant material pertaining to the Corporate Laws, Securities Laws, Corporate Governance, Taxation, Insurance etc. for inclusion in the coming issues of e-CS nitor through e-mail at: [email protected]. The article should ordinarily have 1500 to 2000 words.