prestigious executives, directors and backers of ipos: enduring advantage or fading gloss? eric m....

Post on 20-Dec-2015

215 views

TRANSCRIPT

Prestigious Executives, Directors and Backers of IPOs:Enduring Advantage or Fading Gloss?

Eric M. JacksonColumbia University

Graduate School of Business

Donald C. HambrickPennsylvania State University

Smeal College of Business

Background

a. Interorganizational Ties Focal Firm’s Behavior • board seats • prior employment affiliations • officerships in trade associations • strategic alliances

Background

a. Interorganizational Ties Focal Firm’s Behavior • board seats • prior employment affiliations • officerships in trade associations • strategic alliances

b. Prestigious Ties Focal Firm’s Legitimacy and Performance • access to high-quality information

• access to superior resources• signal of worthiness

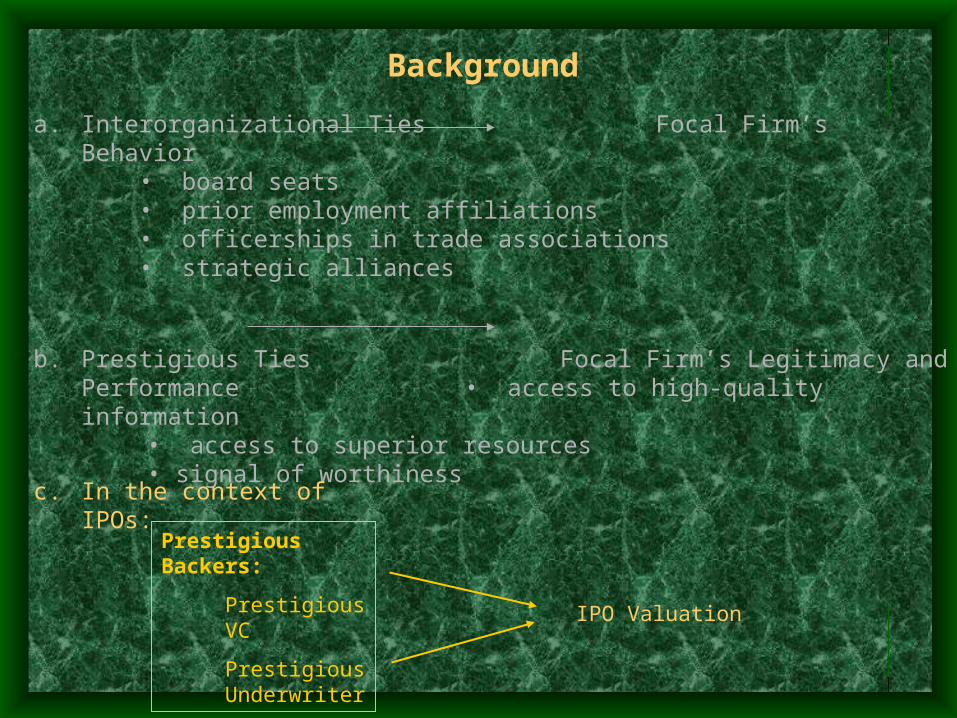

Background

a. Interorganizational Ties Focal Firm’s Behavior • board seats • prior employment affiliations • officerships in trade associations • strategic alliances

b. Prestigious Ties Focal Firm’s Legitimacy and Performance • access to high-quality information

• access to superior resources• signal of worthiness

Prestigious Backers:

Prestigious VC

Prestigious Underwriter

IPO Valuation

c. In the context of IPOs:

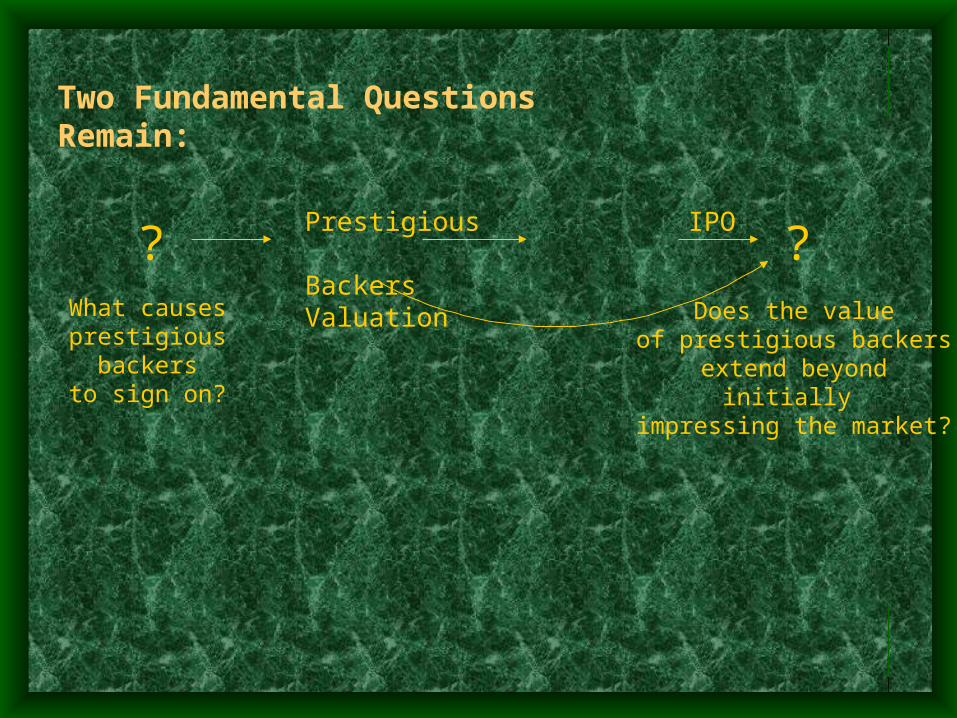

Two Fundamental Questions Remain:

Prestigious IPOBackers Valuation? ?

What causesprestigious backers

to sign on?

Does the valueof prestigious backers

extend beyond initially impressing the market?

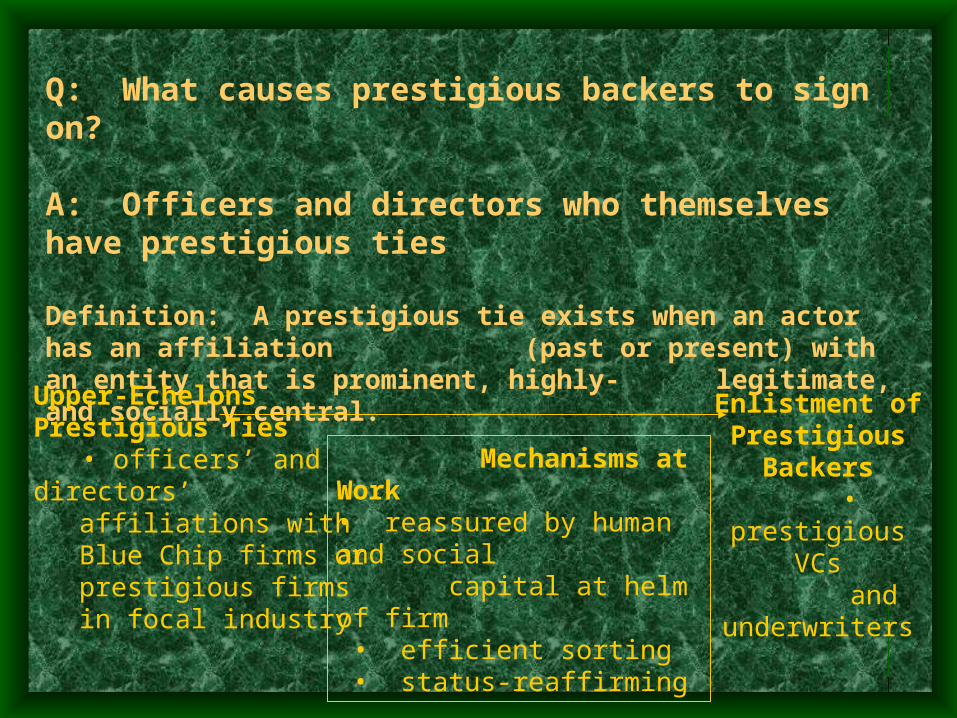

Q: What causes prestigious backers to sign on?

A: Officers and directors who themselves have prestigious ties

Definition: A prestigious tie exists when an actor has an affiliation (past or present) with an entity that is prominent, highly- legitimate, and socially central.

Upper-EchelonsPrestigious Ties • officers’ and directors’

affiliations with Blue Chip firms or prestigious firms in focal industry

Mechanisms at Work • reassured by human and social capital at helm of firm • efficient sorting • status-reaffirming

Enlistment ofPrestigious

Backers • prestigious VCs and underwriters

Propositions

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

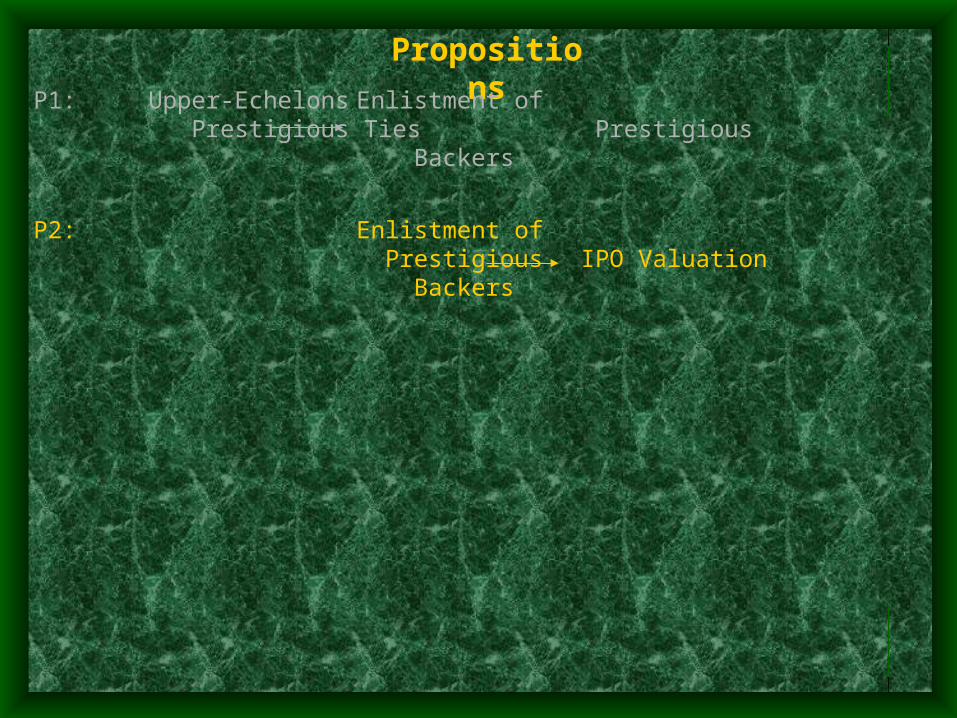

Propositions

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

P2: Enlistment of Prestigious IPO Valuation Backers

Propositions

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

P2: Enlistment of Prestigious IPO Valuation Backers

P3: Upper-Echelons Enlistment ofPrestigious Ties Prestigious IPO Valuation

Backers

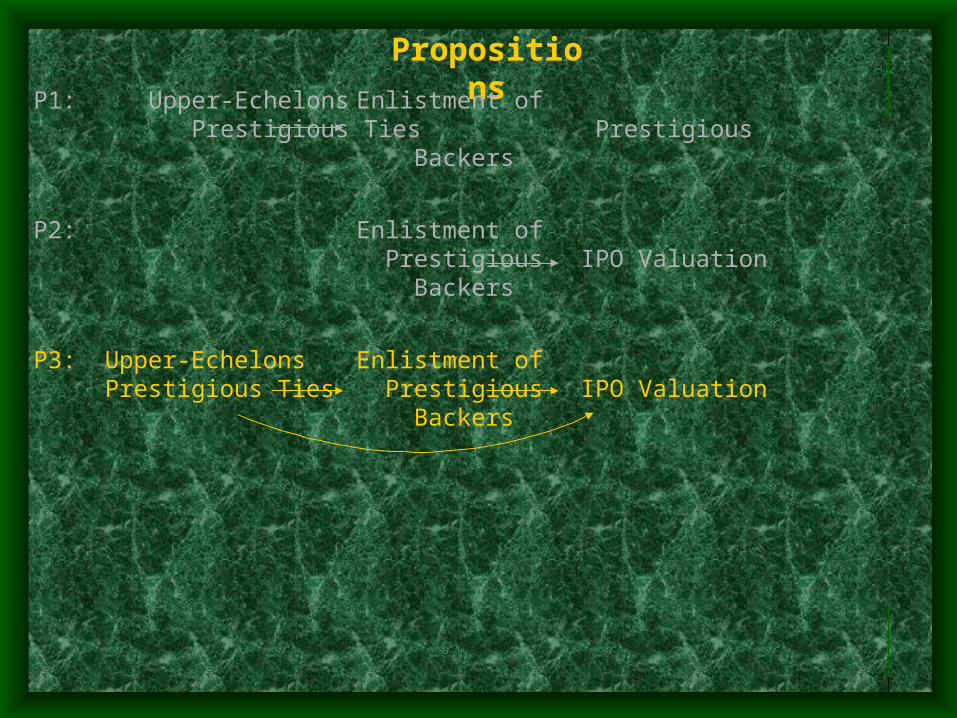

Propositions

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

P2: Enlistment of Prestigious IPO Valuation Backers

P3: Upper-Echelons Enlistment ofPrestigious Ties Prestigious IPO Valuation

Backers

P4: Upper-Echelons Enlistment of Post-IPOPrestigious Ties Prestigious IPO Valuation Performance

Backers

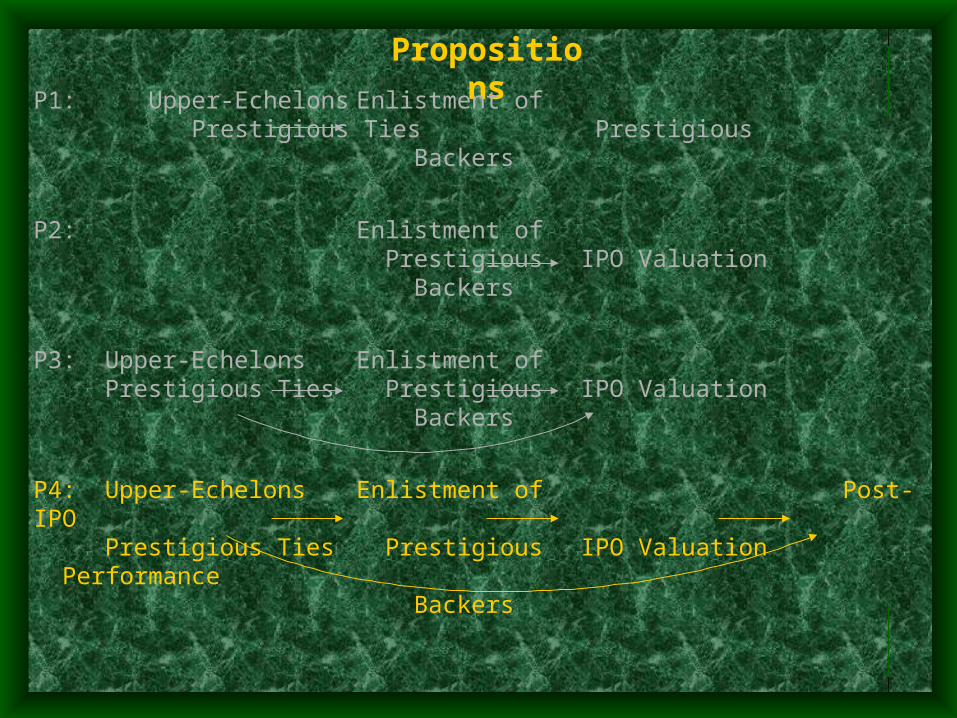

Propositions

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

P2: Enlistment of Prestigious IPO Valuation Backers

P3: Upper-Echelons Enlistment ofPrestigious Ties Prestigious IPO Valuation

Backers

P4: Upper-Echelons Enlistment of Post-IPOPrestigious Ties Prestigious IPO Valuation Performance

Backers

P5: A moderating effect: stronger patterns in uncertain situations

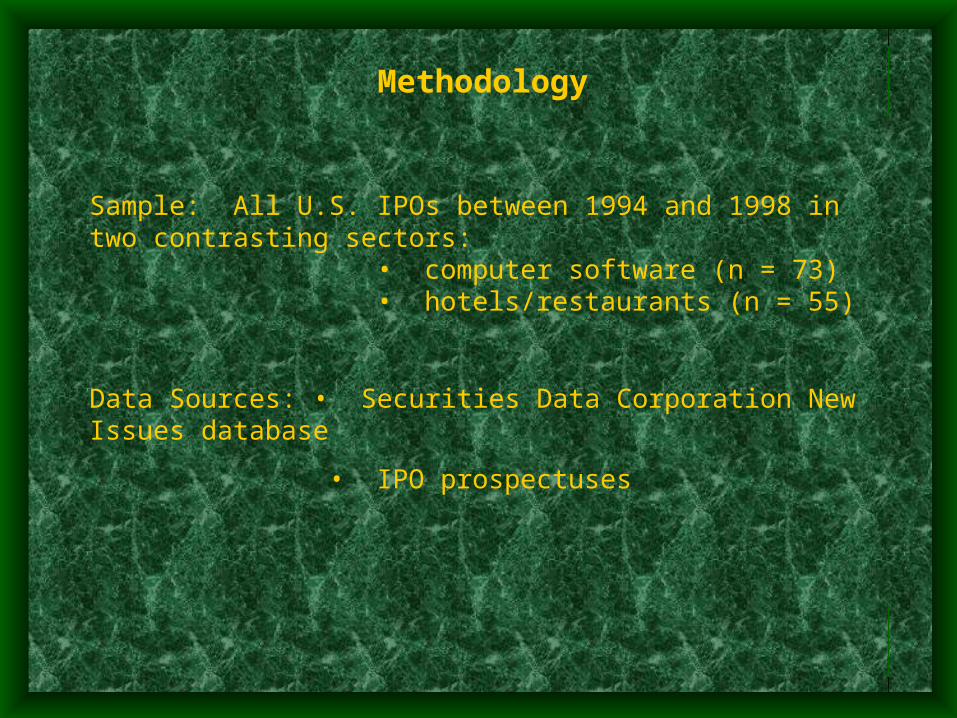

Methodology

Sample: All U.S. IPOs between 1994 and 1998 in two contrasting sectors:

• computer software (n = 73)• hotels/restaurants (n = 55)

Data Sources: • Securities Data Corporation New Issues database

• IPO prospectuses

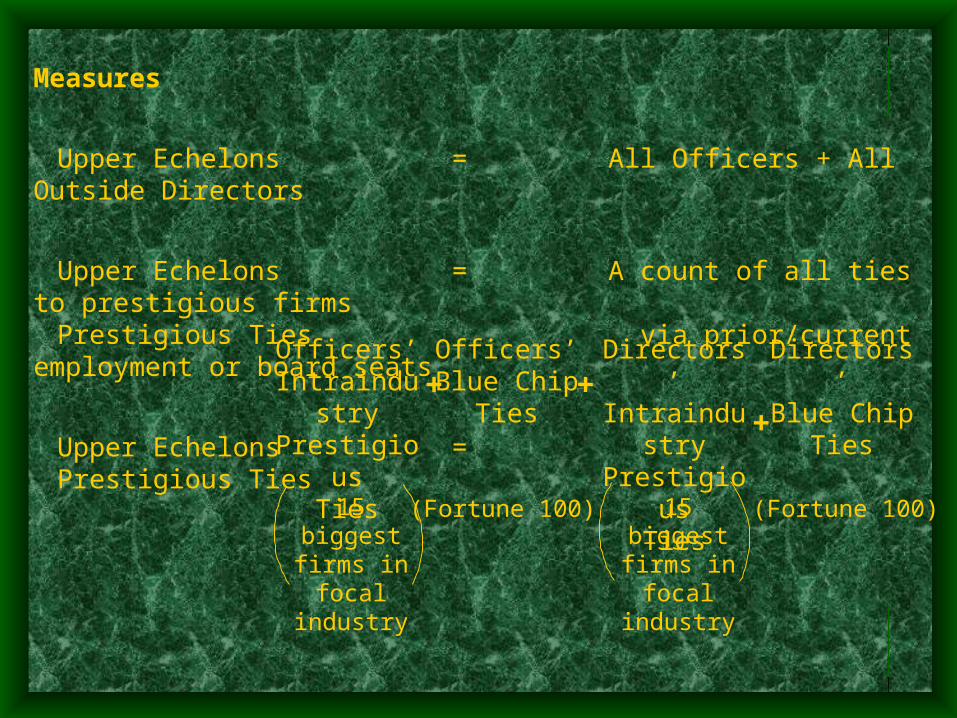

Measures

Upper Echelons = All Officers + All Outside Directors

Upper Echelons = A count of all ties to prestigious firms Prestigious Ties via prior/current employment or board seats

Upper Echelons =Prestigious Ties + + +

Officers’IntraindustryPrestigious

Ties

15 biggestfirms in

focal industry

(Fortune 100)

Directors’IntraindustryPrestigious

Ties

Officers’Blue Chip

Ties

Directors’Blue Chip

Ties

15 biggestfirms in

focal industry

(Fortune 100)

Measures

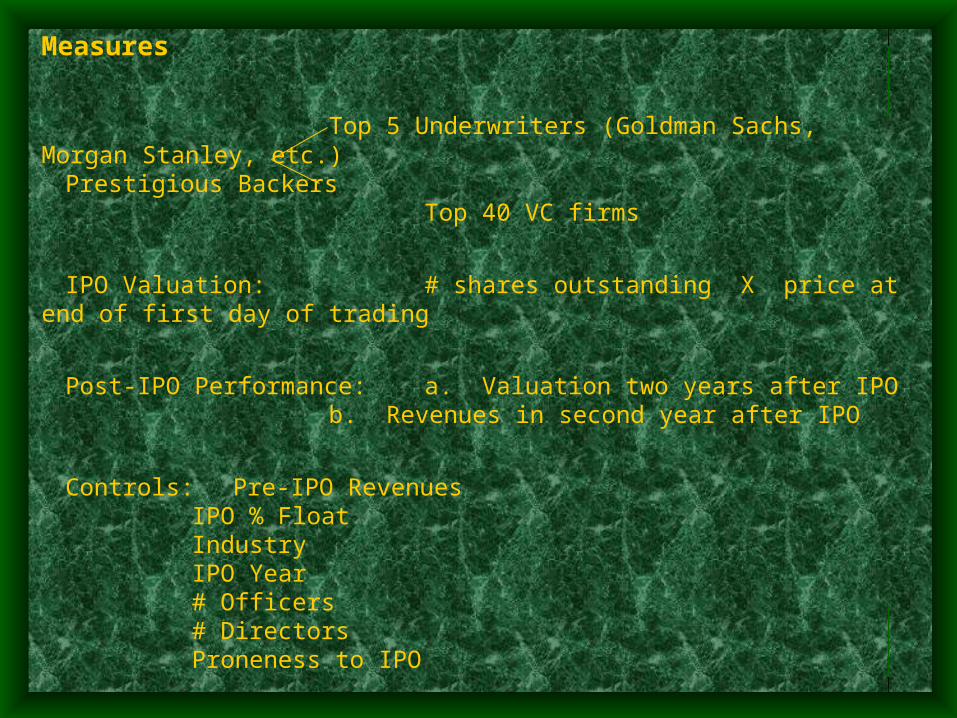

Top 5 Underwriters (Goldman Sachs, Morgan Stanley, etc.)Prestigious Backers

Top 40 VC firms

IPO Valuation: # shares outstanding X price at end of first day of trading

Post-IPO Performance: a. Valuation two years after IPOb. Revenues in second year after IPO

Controls: Pre-IPO RevenuesIPO % FloatIndustryIPO Year# Officers# DirectorsProneness to IPO

Data Analysis: Multiple Regression

Results

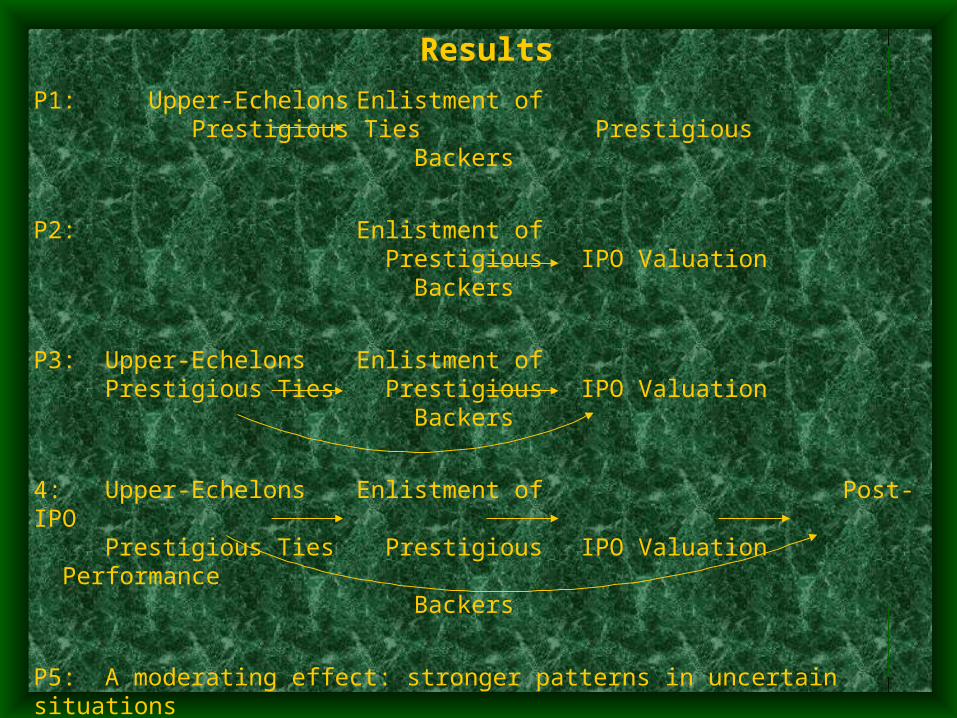

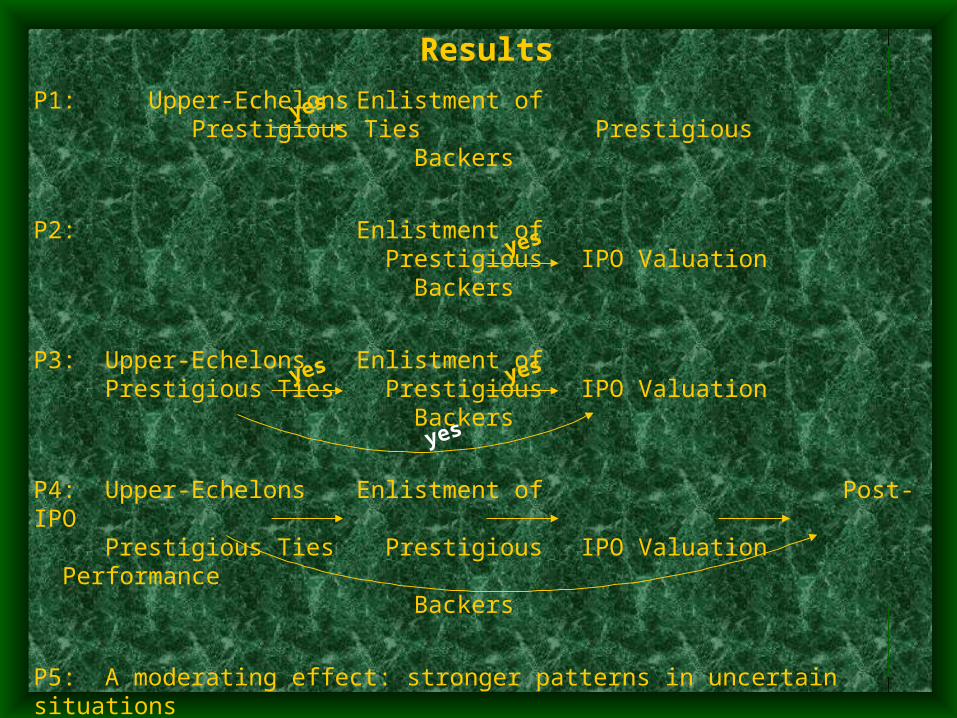

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

P2: Enlistment of Prestigious IPO Valuation Backers

P3: Upper-Echelons Enlistment ofPrestigious Ties Prestigious IPO Valuation

Backers

4: Upper-Echelons Enlistment of Post-IPOPrestigious Ties Prestigious IPO Valuation Performance

Backers

P5: A moderating effect: stronger patterns in uncertain situations

Results

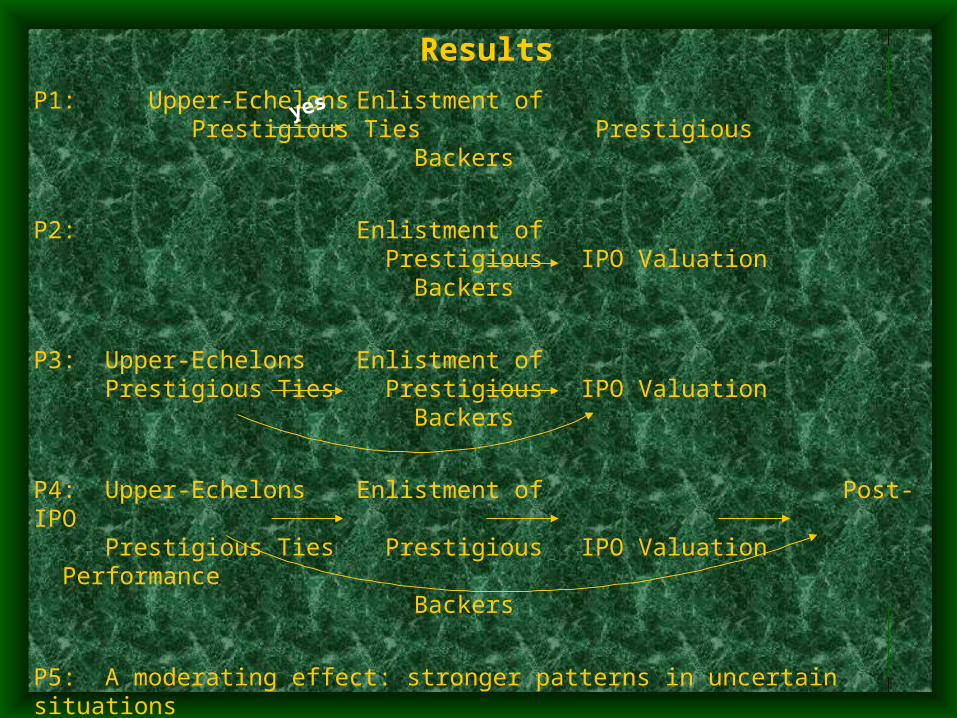

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

P2: Enlistment of Prestigious IPO Valuation Backers

P3: Upper-Echelons Enlistment ofPrestigious Ties Prestigious IPO Valuation

Backers

P4: Upper-Echelons Enlistment of Post-IPOPrestigious Ties Prestigious IPO Valuation Performance

Backers

P5: A moderating effect: stronger patterns in uncertain situations

yes

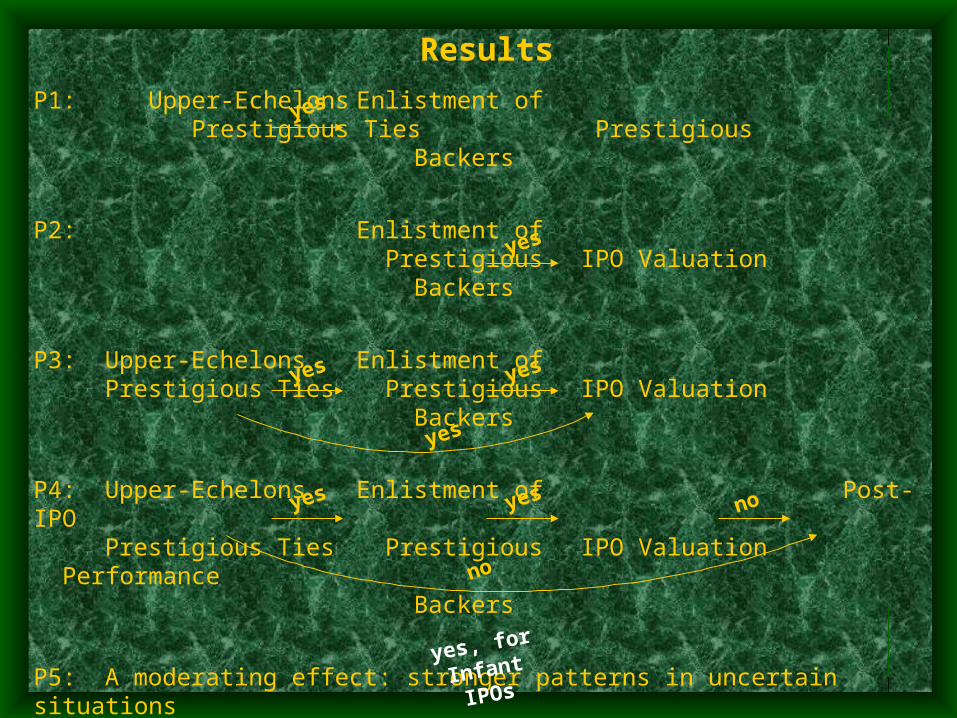

Results

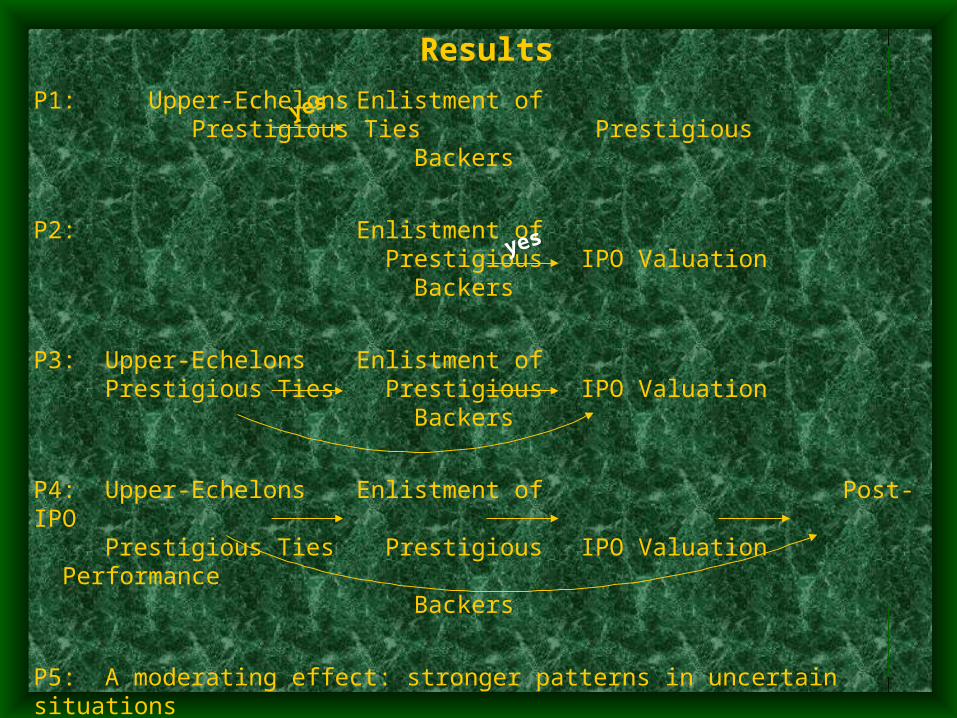

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

P2: Enlistment of Prestigious IPO Valuation Backers

P3: Upper-Echelons Enlistment ofPrestigious Ties Prestigious IPO Valuation

Backers

P4: Upper-Echelons Enlistment of Post-IPOPrestigious Ties Prestigious IPO Valuation Performance

Backers

P5: A moderating effect: stronger patterns in uncertain situations

yes

yes

Results

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

P2: Enlistment of Prestigious IPO Valuation Backers

P3: Upper-Echelons Enlistment ofPrestigious Ties Prestigious IPO Valuation

Backers

P4: Upper-Echelons Enlistment of Post-IPOPrestigious Ties Prestigious IPO Valuation Performance

Backers

P5: A moderating effect: stronger patterns in uncertain situations

yes

yes

yes yes

yes

Results

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

P2: Enlistment of Prestigious IPO Valuation Backers

P3: Upper-Echelons Enlistment ofPrestigious Ties Prestigious IPO Valuation

Backers

P4: Upper-Echelons Enlistment of Post-IPOPrestigious Ties Prestigious IPO Valuation Performance

Backers

P5: A moderating effect: stronger patterns in uncertain situations

yes

yes

yes

yes yes

yes

yes

no

no

Results

P1: Upper-Echelons Enlistment of Prestigious Ties Prestigious

Backers

P2: Enlistment of Prestigious IPO Valuation Backers

P3: Upper-Echelons Enlistment ofPrestigious Ties Prestigious IPO Valuation

Backers

P4: Upper-Echelons Enlistment of Post-IPOPrestigious Ties Prestigious IPO Valuation Performance

Backers

P5: A moderating effect: stronger patterns in uncertain situations

yes

yes

yes

yes yes

yes

yes, for

Infant IPOs

yes

no

no

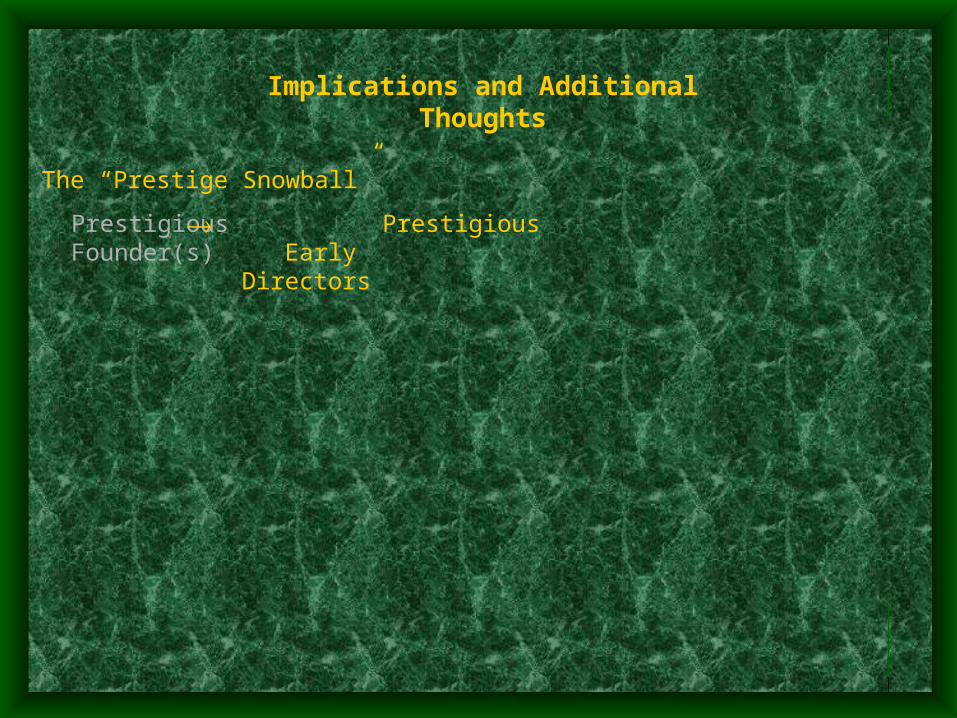

Implications and Additional Thoughts

The “Prestige Snowball”

Implications and Additional Thoughts

The “Prestige Snowball”

PrestigiousFounder(s)

Implications and Additional Thoughts

The “Prestige Snowball”

Prestigious Prestigious Founder(s) Early

Directors

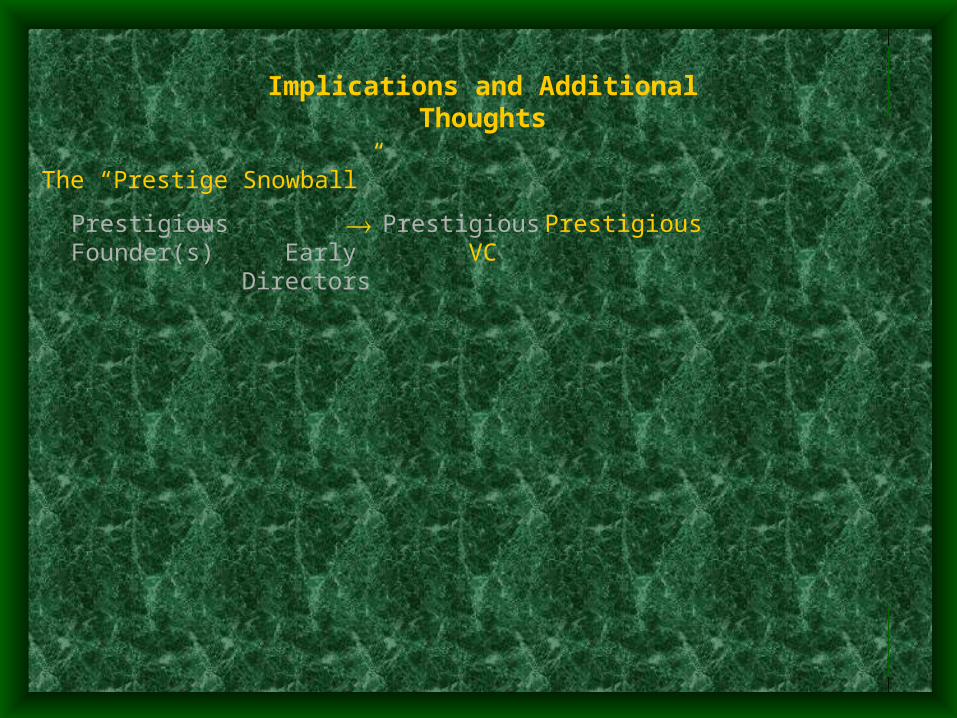

Implications and Additional Thoughts

The “Prestige Snowball”

Prestigious Prestigious Prestigious Founder(s) Early VC

Directors

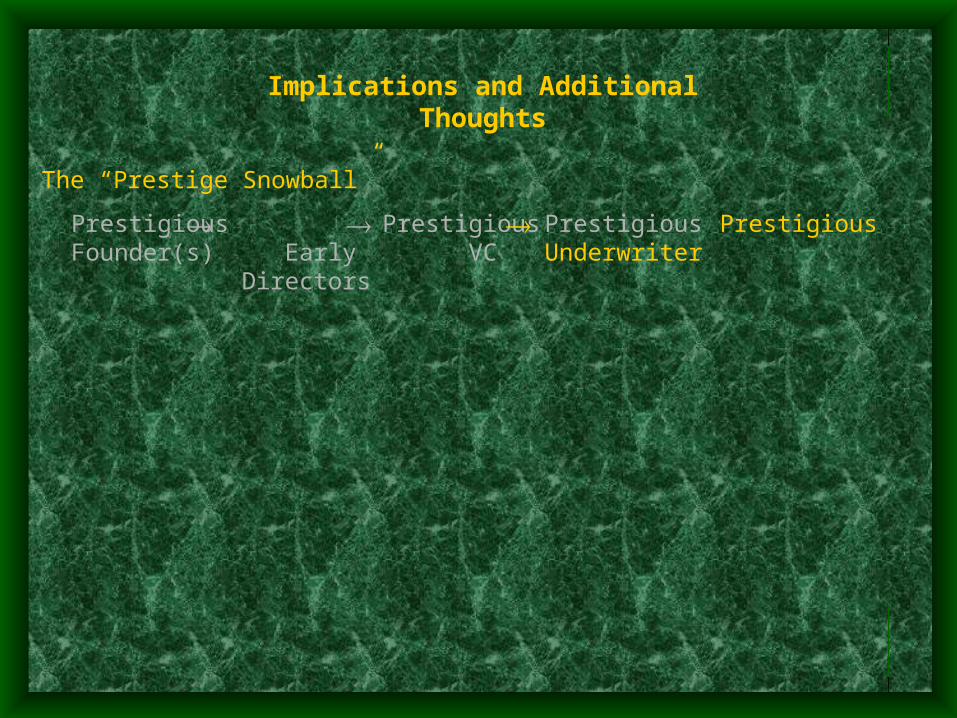

Implications and Additional Thoughts

The “Prestige Snowball”

Prestigious Prestigious Prestigious PrestigiousFounder(s) Early VC Underwriter

Directors

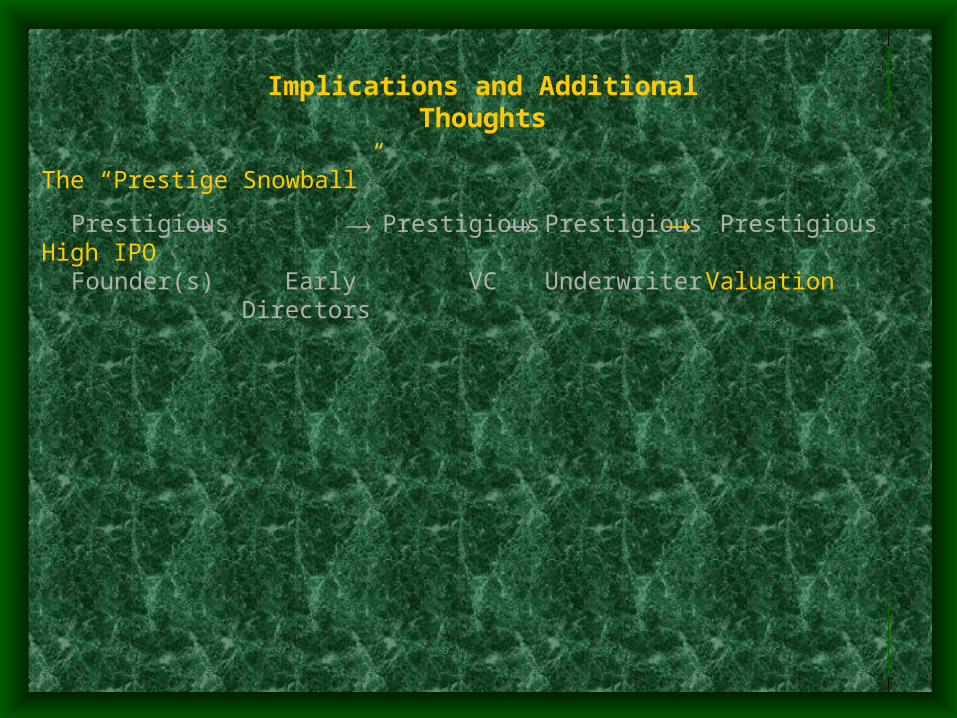

Implications and Additional Thoughts

The “Prestige Snowball”

Prestigious Prestigious Prestigious Prestigious High IPOFounder(s) Early VC Underwriter Valuation

Directors

Implications and Additional Thoughts

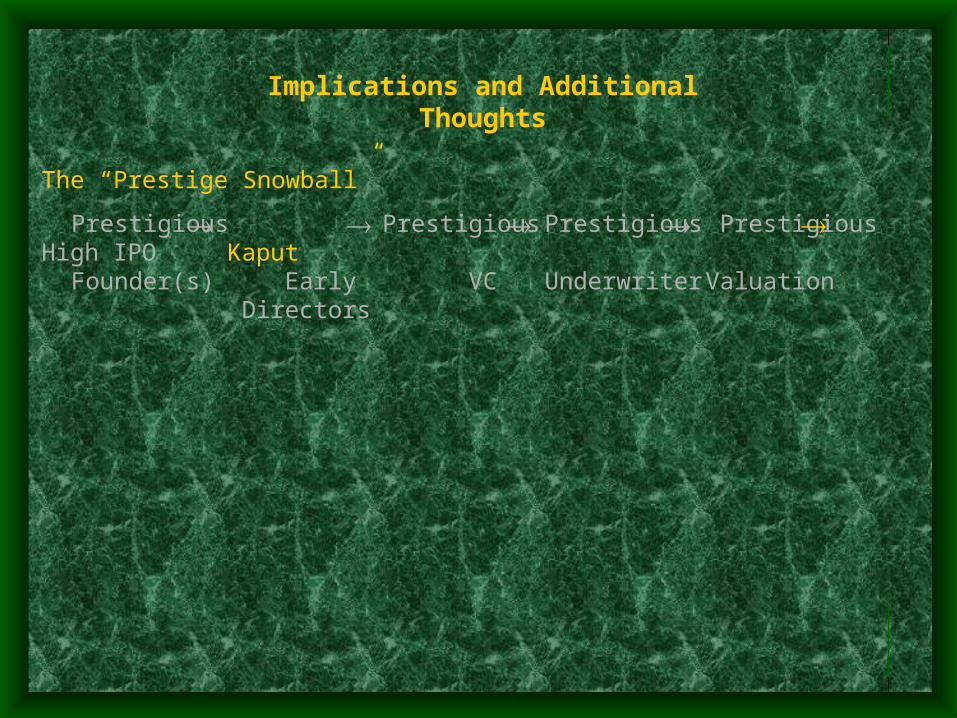

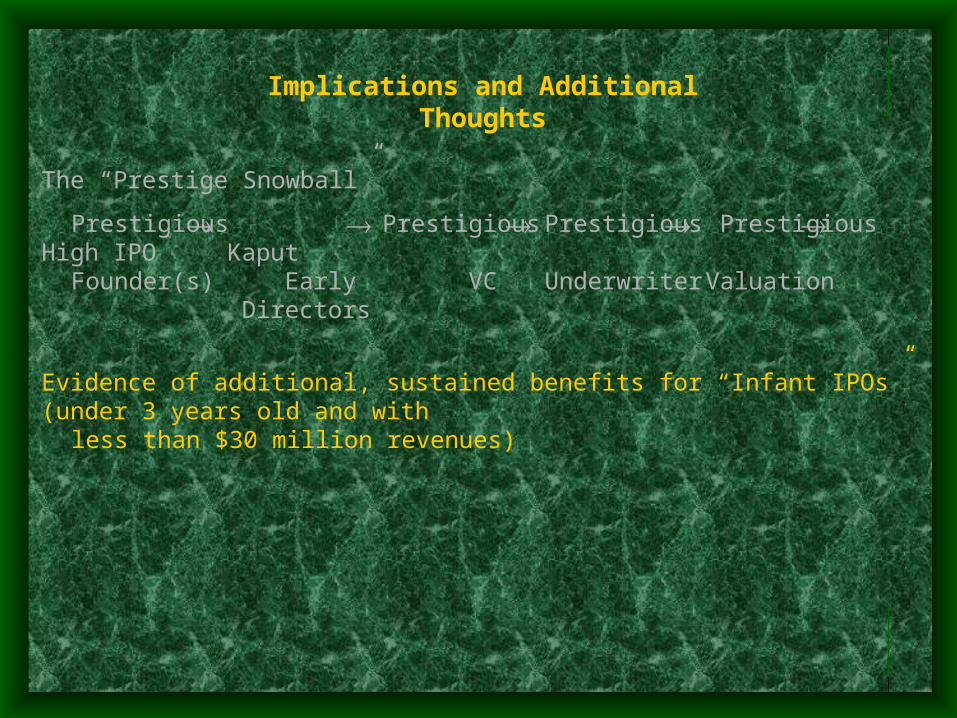

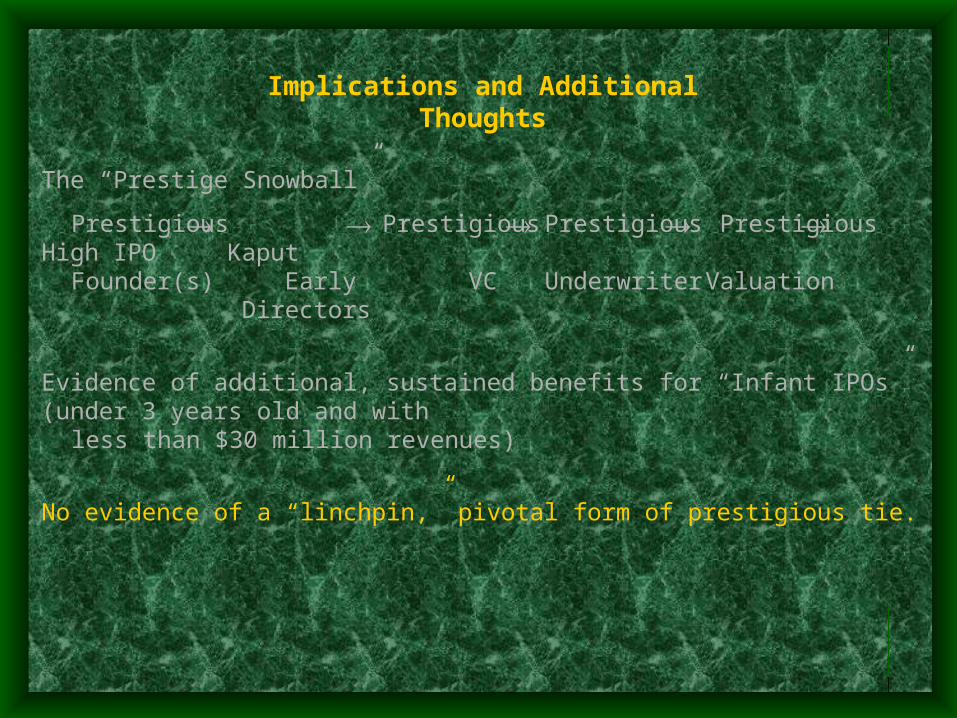

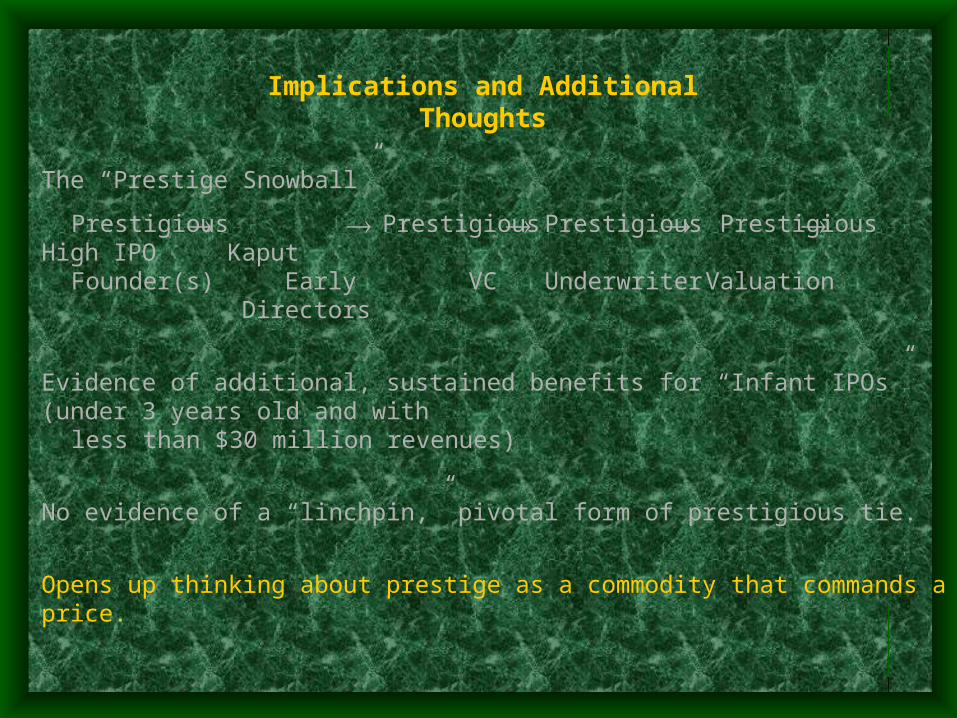

The “Prestige Snowball”

Prestigious Prestigious Prestigious Prestigious High IPO KaputFounder(s) Early VC Underwriter Valuation

Directors

Implications and Additional Thoughts

The “Prestige Snowball”

Prestigious Prestigious Prestigious Prestigious High IPO KaputFounder(s) Early VC Underwriter Valuation

Directors

Evidence of additional, sustained benefits for “Infant IPOs” (under 3 years old and with less than $30 million revenues)

Implications and Additional Thoughts

The “Prestige Snowball”

Prestigious Prestigious Prestigious Prestigious High IPO KaputFounder(s) Early VC Underwriter Valuation

Directors

Evidence of additional, sustained benefits for “Infant IPOs” (under 3 years old and with less than $30 million revenues)

No evidence of a “linchpin,” pivotal form of prestigious tie.

Implications and Additional Thoughts

The “Prestige Snowball”

Prestigious Prestigious Prestigious Prestigious High IPO KaputFounder(s) Early VC Underwriter Valuation

Directors

Evidence of additional, sustained benefits for “Infant IPOs” (under 3 years old and with less than $30 million revenues)

No evidence of a “linchpin,” pivotal form of prestigious tie.

Opens up thinking about prestige as a commodity that commands a price.