pricewaterhousecoopers zhong tian llp …telecommunications, media and technology (tmt) report...

TRANSCRIPT

www.pwccn.comwww.pwc.com/globalmoneytree

PricewaterhouseCoopers Zhong Tian LLP

MoneyTreeTM China TMT ReportQ1/Q2 2016 Data source: Zero2IPO Research

This MoneyTreeTM China Telecommunications, Media and Technology (TMT) Report includes information on private equity and venture capital (PE/VC) investment in the TMT industry for Q1/Q2 2016, as well as 2015, 2014, and Q3/Q4 2013.

Table of contents

1. Overview 4

2. PE/VC investments in the TMT industry 5

TMT industry investments compared with all industries 5

Investments by quarter 7

Investments by sector 8

First-time funding compared with follow-on funding 11

Investments by stage of development 13

Investments by region 16

3. PE/VC exits in the TMT industry 17

Exits by quarter 17

Exits by type 18

Exits by sector 20

4. Sector focus: Technology, Internet, and Telecommunications and Mobile

21

Investments in Technology 21

Investments in Internet 27

Investments in Telecommunications and Mobile 33

5. A close look at investments in Mobile 37

6. Methodology and definitions 40

7. Contacts 42

4 MoneyTreeTM China TMT Report Q1/Q2 2016

In the first half (H1) of 2016, private equity and venture capital (PE/VC) investment in the Telecommunications, Media and Technology (TMT) industry maintained the strong momentum of 2015, and remained on an upward trajectory. In H1 2016, total TMT deal value surpassed all other industries, accounting for over 50% of overall industry value. The proportion of total deal volume in H1 2016 matched that recorded in H2 2015. Actual deal volume decreased slightly, but remained high compared to recent years.

During the winter of 2015, investments in the TMT industry were unexpectedly active and the trend continued in H1 2016. In Q2 2016, total deal value exceeded US$20 billion for the first time, with an increase of 44% quarter over quarter (QoQ). The trend is closely related to a higher frequency of substantial investments in unicorns, and buoyed by strategic investors making investments in order to occupy stronger positions in the market. Also of note, in H1 2016, there were more than 20 investments that had a single-deal value of over US$100 million, with several of these involving an investment value above US$1 billion.

In H1 2016, the Internet continued to be the best performing TMT sector, with the highest deal volume and value. Both the Technology and the Telecommunications and Mobile sectors had investments with single-deal value of over US$1 billion. In light of the major investments, the performance of the Entertainment and Media sector was comparatively modest. Investments in TMT during H1 2016 tended to be concentrated in Internet Finance, E-commerce and Mobile Services, each of which pertain to smart, modern lifestyles.

1. OverviewWith the resumption of IPOs, the number of IPOs increased gradually, though the proportion didn’t exceed strategic sales, which proved to be the most popular type of exit in H1. The proportion of strategic sales in H1 2016 exceeded 60%, an increase of approximately 16% from the prior period, and representing the highest level reached by that category of exit since 2012. Regarding exit by sector, Entertainment and Media stood out in particular in H1 2016, having reached the highest number recorded since 2012, and exceeding the Technology sector for the first time.

As a whole, in H1, TMT stood out as a leading industry in the market, playing a notable role underpinning the technological progress characteristic of modern societies. This report brings you the details of the PE/VC investments and exits in the TMT industry and its three major sectors, serving as a tool that lets you follow the key trends and trajectories shaping TMT industry investments. We would welcome the opportunity to discuss the implications of this report with you, and encourage you to connect with us with any queries you have.

Wilson ChowPwC China & Hong Kong TMT Leader

Jianbin GaoPwC China TMT Leader

5MoneyTreeTM China TMT Report Q1/Q2 2016

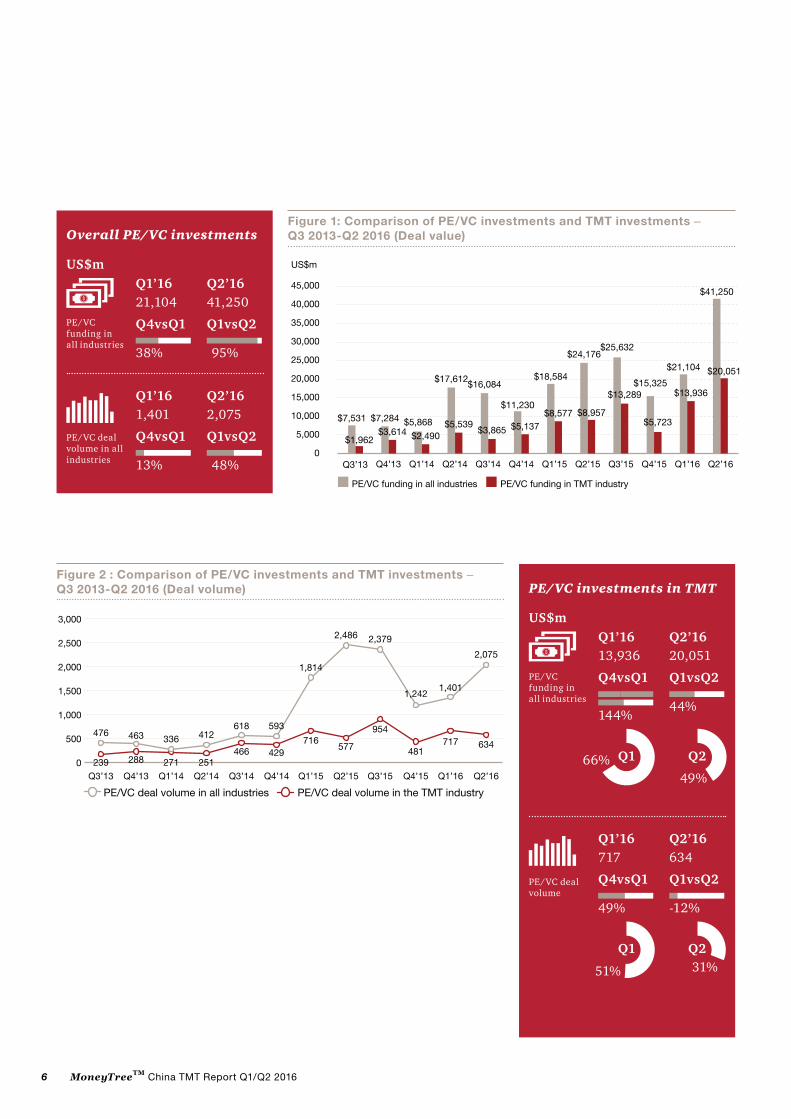

TMT industry investments compared with all industries

2. PE/VC investments in the TMTindustry

In H1 2016, overall PE/VC investments defied expectations by maintaining high growth. In Q2 2016, total deal value exceeded US$40 billion for the first time, an increase of almost 100% from Q1 2016. The trend closely relates to the frequent occurrence of huge investments in unicorn companies. Strategic investors made investments to occupy positions in the market. The TMT industry attracted over 50% of the total deal value in H1 2016, while Q2 total deal value exceeded US$20 billion for the first time, indicating just how hot the industry has been compared with others over the period.

PwC Viewpoints

Total industry investment in H1 2016 remained positive, continuing the upward trend of H2 2015. Total TMT deal value and volume accounted for 55% and 39% of overall industry investment, respectively.

Main findings:

1. In Q1 2016, the proportion oftotal deal value in the TMTindustry to overall industryinvestment reached ahistorical high since recordsstarted in 2012, reaching66%.

2. In Q2 2016, total deal value inthe TMT industry also reacheda historical high, exceedingUS$20 billion for the firsttime.

6 MoneyTreeTM China TMT Report Q1/Q2 2016

Figure 1: Comparison of PE/VC investments and TMT investments ‒ Q3 2013-Q2 2016 (Deal value)

Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13

45,000

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

$7,531

$1,962

$25,632

$15,325

$24,176$21,104 $20,051

$41,250

$13,936

$18,584

$5,723$8,957$8,577

$11,230

$16,084$17,612

$5,868$7,284

$3,614 $2,490$5,539

$3,865 $5,137

$13,289

US$m

PE/VC funding in all industries PE/VC funding in TMT industry

Figure 2 : Comparison of PE/VC investments and TMT investments – Q3 2013-Q2 2016 (Deal volume)

3,000

2,500

2,000

1,500

1,000

500

0Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13

476 463 336 412618

1,814

2,486 2,379

1,2421,401

2,075

481717 634

954

577716

429466251271288239

593

PE/VC deal volume in all industries PE/VC deal volume in the TMT industry

Overall PE/VC investments

PE/VC funding in all industries

PE/VC deal volume in all industries

Q1’1621,104

Q1’161,401

Q4vsQ1

Q4vsQ1

Q1vsQ2

Q1vsQ2

38%

13%

95%

48%

US$mQ2’1641,250

Q2’162,075

PE/VC investments in TMT

Q1’1613,936

Q1’16717

Q4vsQ1

Q4vsQ1

Q1vsQ2

Q1vsQ2

144%

49%

44%

49%

31%

66%

51%

-12%

US$mQ2’1620,051

Q2

Q2Q1

Q1

Q2’16634

PE/VC funding in all industries

PE/VC deal volume

7MoneyTreeTM China TMT Report Q1/Q2 2016

Investments by quarter

In Q1, deal value and volume rose continuously

In Q1, both the deal value and volume rose notably compared to the previous quarter, and the single-average-deal value increased by 89% compared to Q4 2015. There were 22 deals with investments that had a single-deal value of over US$100 million, twice as many as the previous quarter. The highest single-deal value amounted to US$3.3 billion.

In Q2, both the total deal value and the highest single-deal value set a new historical record

In Q2, deal value in the TMT industry broke the historical record, and was higher than the total deal value in H2 2015, maintaining the momentum. Single-average-deal value increased by 60% compared to the previous quarter. In Q2, there were 23 deals with investments that had a single-deal value over US$100 million. The highest single-deal value amounted to US$4.5 billion, which was also the highest since 2012.

In H1 2016, average deal value in the TMT industry increased from over US$4 million to US$36 million. The 800% rise indicates that investors have paid increasing attention to the TMT industry. In H1 2016, there were more than 20 investments with a single-deal value of over US$100 million. Further, the level of investment value escalated, with many deals seeing an investment value of over US$1 billion. Both the scale and range of investments gradually increased as unicorn companies emerged and newly-established companies developed into more mature companies.

In H1 2016, the core investment sectors in the TMT industry were predominantly in Internet Finance, E-commerce and Mobile Services, each being closely linked to smart, modern lifestyles. Notably, the majority of large investments were additional investments in companies with high valuations, rather than investments in emerging enterprises, reflecting investors’ prudence. We expect to see a continuation of large investments.

PwC Viewpoints

Figure 4: Volume of TMT investments with single value over US$100 million by quarter – Q3 2013-Q2 2016

25

20

15

10

5

0

Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13

3

97

11

1920 21

2223

11

7

9

Figure 3: TMT investments by quarter ‒ Q3 2013-Q2 2016 (Deal volume/Deal value)

25,000

20,000

15,000

10,000

5,000

0

1,200

1,000

800

600

400

200

0

Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13

$1,962$3,614

$2,490

$5,539

$3,865$5,137

$8,577 $8,957

$13,289

$13,936

$20,051

$5,723251239288 271

466429

716

954

481

717

634577

Deal value Deal volume

US$m

8 MoneyTreeTM China TMT Report Q1/Q2 2016

Investments by sector

The TMT industry sectors are: Technology, Internet, Telecommunications and Mobile, and Entertainment and Media.

Internet: The Internet was the hottest investment sector in the TMT industry over H1 2016, with total deal value above US$20 billion, an increase of 140% compared to H2 2015. The deal volume saw little change, indicating that there was a significant increase in single-deal value in the Internet sector over the period. There were 32 investments with a single-deal value over US$100 million. There was also gradual growth in the number of huge deals, including five deals that had a single-deal value exceeding US$1 billion.

Technology: Deal volume for Technology ranked second, only behind the Internet, although investment value for Technology was lower than Telecommunications and Mobile. Deal volume saw a slight slump QoQ, but investment value achieved a historical record by exceeding US$3 billion in Q2. The boost in sector value was aided by an investment of US$2.4 billion in an Electronics & Optoelectronics Devices company, which had a sizable impact on the overall investment scenario of Technology for the period.

Telecommunications and Mobile: This sector’s historically high deal value ranked second in the industry, positioned just after the top placed Internet sector. Deal volume was higher than the Technology sector. Investment volume saw little fluctuations from quarter to quarter, however, deal value witnessed more variations. Investment value in Q2 increased by 523% QoQ, as a consequence of a sizable investment of US$4.5 billion in a mobile service company in Q2.

Entertainment and Media: Investment remained stable in H1 2016 compared to H2 2015. Investments in 67 deals were made in Q2, the most since 2012.

In H1 2016, total deal value in the TMT industry was boosted by huge investments in a number of large Unicorn companies with enterprise value above US$1 billion. The Internet sector continued to be the hottest investment sector across the industry, exceeding other sectors in proportion of both deal volume and value. Huge investments, each with a single-deal value over US$1 billion also occurred in the Technology sector and the Telecommunications and Mobile sector. By comparison, the Entertainment and Media appeared to perform more modestly.

Besides the huge deals, investments in the TMT industry remained stable in H1 2016, with no major fluctuations in either volume or value. It appears that investors remained relatively measured in their approaches, with a range of advantageous investments made in companies that have continued to heat up over the period.

PwC Viewpoints

Figure 5: Deal value comparison in TMT sectors – Q3 2013-Q2 2016

25,000

20,000

15,000

10,000

5,000

0

$1,962$3,614

$2,490

$5,539$3,865

$5,137$5,718

$8,577 $8,957

$13,288 $13,936

$20,051

Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16

Telecommunications and Mobile

Technology Internet

Entertainment and Media

US$m

Figure 6: Deal volume comparison in TMT sectors – Q3 2013-Q2 2016

600

500

400

300

200

100

0

Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’1622 31

9 12 15 10 20 31 45 26

79 74 76112 113

94 78119

207

105152

269

6167

115 138 125

245

370

487

71 68

239

316

7448 40

125

228

154

50

136

426386

117

6467105

Telecommunicationsand Mobile

Technology Internet Entertainment and Media

In Q1 2016, of the 22 deals with a single-deal value over US$100 million, Internet, Technology, as well as Telecommunications and Mobile accounted for 77%, 18% and 5%, respectively.

In Q2 2016, of the 23 deals with a single-deal value over US$100 million, Internet, Technology, Entertainment and Media, and Telecommunications and Mobile accounted for 65%, 13%, 13% and 9%, respectively.

9MoneyTreeTM China TMT Report Q1/Q2 2016

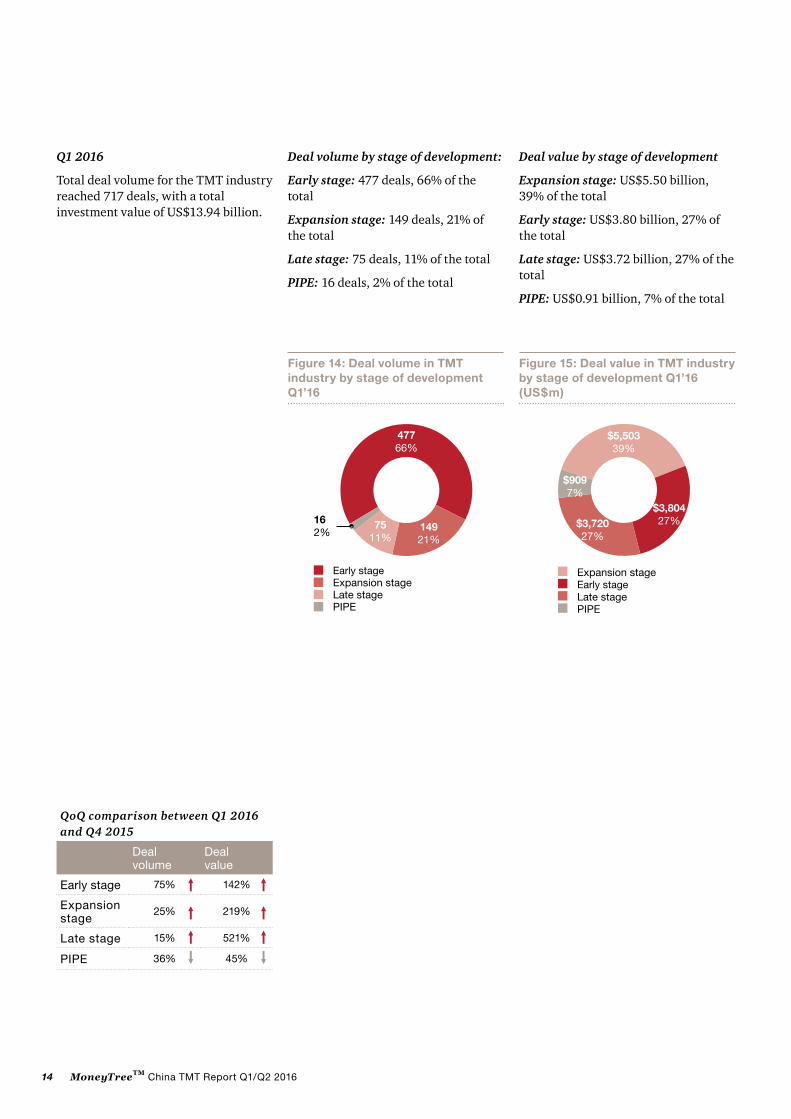

Q1 2016Total deal volume for the TMT industry reached 717 deals, with a total investment value of US$13.94 billion.

Figure 8: Deal value in TMT sectors Q1’16 (US$m)

Figure 7: Deal volume in TMT sectors Q1’16

Deal volume by sectors

Internet: 426 deals, 59% of the total

Technology: 136 deals, 19% of the total

Telecommunications and mobile: 105 deals, 15% of the total

Entertainment and Media: 50 deals, 7% of the total

Deal value by sectors

Internet: US$11.56 billion, 83% of the total

Technology: US$1.29 billion, 9% of the total

Telecommunications and mobile: US$0.79 billion, 6% of the total

Entertainment and Media: US$0.29 billion, 2% of the total

42659%

13619%105

15%

507%

TechnologyTelecommunications and Mobile

Internet

Entertainment and Media

$11,56383%

$1,2929%

$7946%

$2862%

Internet Technology Telecommunications and MobileEntertainment and Media

QoQ comparison between Q1 2016

and Q4 2015

Deal volume

Dealvalue

Technology技 12% 12%

Internet技技 78% 230%

Telecommunications and Mobile

72% 65%

Entertainmentand Media

92% 5%

10 MoneyTreeTM China TMT Report Q1/Q2 2016

QoQ comparison between Q2 2016 and

Q1 2016

Deal volume

Dealvalue

Technology技 14% 178%

Internet技技 9% 16%

Telecommunications and Mobile

39% 523%

Entertainmentand Media 传技

34% 527%

Deal volume by sector

Internet: 386 deals, 61% of the total

Technology: 117 deals, 19% of the total

Entertainment and Media: 67 deals, 10% of the total

Telecommunications and Mobile: 64 deals, 10% of the total

Deal value by sector

Internet: US$9.71 billion, 48% of the total

Telecommunications and Mobile: US$4.95 billion, 25% of the total

Technology: US$3.59 billion, 18% of the total

Entertainment and Media: US$1.79 billion, 9% of the total

Q2 2016

Total deal volume for the TMT industry reached 634 deals, with a total investment value of US$20.05 billion.

Figure 9: Deal volume in TMT sectors Q2’16

Figure 10: Deal value in TMT sectors Q2’16 (US$m)

38661%

11719%67

10%

6410%

Telecommunications and MobileTechnology Internet

Entertainment and Media

$9,71248%

$4,95125%$3,594

18%

$1,7949%

Entertainment and Media Technology

Internet Telecommunications and Mobile

11MoneyTreeTM China TMT Report Q1/Q2 2016

Figure 11: TMT follow-on funding compared with initial investments – Q3 2013-Q2 2016

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16

67%63% 61% 58%

78% 73%

65%60%

53% 55%

44% 45%

Initial investments Follow-on investments

First-time funding compared with follow-on funding

Q1 2016 Q2 2016

Q1’16First-round 3690Total investment 139.36

Q1’16First-round 466Total investment717

13%

60%

26%

65%

US$mQ2’16First-round 2571Total investment 200.51

Q2

Q2Q1

Q1

Q2’16First-round 379Total investment634

PE/VC funding in all industries

PE/VC deal volume in all industries

12 MoneyTreeTM China TMT Report Q1/Q2 2016

Q1 2016

Enterprises engaged in first-round funding by sector:

Internet: 292 enterprises, funding total US$3.20 billion

Telecommunications and Mobile: 76 enterprises, funding total US$0.2 billion

Technology: 69 enterprises, funding total US$0.22 billion

Entertainment and Media: 29 enterprises, funding total US$0.08 billion

For first-round funding, 400 enterprises were at the early stage, accounting for 86%; 46 enterprises were at the expansion stage, accounting for 10% and 20 enterprises were at the late stage, accounting for 4%.

Q2 2016

Enterprise engaged in first-round funding by sector:

Internet: 253 enterprises, funding total US$1.3 billion

Technology: 50 enterprises, funding total US$0.19 billion

Entertainment and Media: 40 enterprises, funding total US$1.03 billion

Telecommunications and Mobile: 36 enterprises, funding total US$0.11 billion

For first-round funding, 313 enterprises were at the early stage, accounting for 83%; 61 enterprises were at the expansion stage, accounting for 16% and 5 enterprises were at the late stage, accounting for 1%.

We have seen a continual emergence of new companies that have contributed to innovation and entrepreneurship in fields that are changing people’s lifestyles and living environments. This is the trend of the times, and so new projects in this arena have attracted attention from investors. In H1 2016, the proportion of the deal volume of initial investments remained high, at over 60%, but the proportion of deal value continued to drop. Indeed, these trends can be seen as an indication of how investors have assessed the future value of such new projects. For projects with a fair degree of uncertainty, deal value was relatively small.

PwC Viewpoints

Q1 2016

First-time funding summary (US$)

Number of enterprises

<= 1m 395

1m-5m 3

>5m-10m 0

>10m 1

N/A 67

Q2 2016

First-time funding summary (US$)

Number of enterprises

<= 1m 332

1m-5m 2

>5m-10m 1

>10m 0

N/A 54

69

76

29229

253 50

3640

13MoneyTreeTM China TMT Report Q1/Q2 2016

Investments by stage of development

Deal value for early-stage investments reached the highest point since 2012

Among the four stages of investment, the deal volume for early-stage investments took the lead as usual, accounting for over 50%. Deal volume declined slightly compared to H2 2015 though saw little fluctuation. Investments in Q1 reached US$5.5 billion, a historical high. There were two huge deals in H1 2016, both of which exceeded US$1 billion. One related to an Internet service company and the other to a high profile Internet Entertainment company.

In Q2, expansion-stage investments experienced explosive growth

The deal value of expansion-stage investments was less than that of early-stage investments in Q1, though in Q2 it exceeded that of early-stage investments, reaching US$12 billion, or 60% of the total, becoming the highest quarter on record since 2012. The figures were boosted by two unicorn investments in Q2, amounting to US$4.5 billion. These also happened to have the highest single-deal value in H1 2016, for the TMT industry. Deal volume in H1 2016 increased slightly from quarter to quarter and maintained steady growth of over 20%.

Quarterly deal value for late-stage investments hit the highest level since 2012

The deal value for investments in Q1 increased by 521% QoQ, the highest since 2012, but dropped by 70% in Q2. Major factors included an investment of US$3.3 billion in a high profile B2C company, which ranked as the third highest of all investments recorded in H1 2016. The deal volume of late-stage investments accounted for 10% of the industry total, and experienced little fluctuation.

Quarterly investments in PIPE experienced a slight initial fall but increased sharply in Q2

Deal value and volume declined in Q1, but both increased in Q2. Investment value in Q2 was nearly US$4 billion, benefitting from a deal worth US$2.4 billion in an Electronics & Optoelectronics Devices company.

Figure 12: TMT investments by stage of development – Q3 2013-Q2 2016 (Deal value)

25,000

20,000

15,000

10,000

5,000

0

Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16

$1,955$3,614

$2,490

$5,539$3,865

$5,137

$8,577 $8,957

$13,289 $13,936

$20,051

$5,723

PIPE Early stageLate stage Expansion stage

US$m

Figure 13: TMT investments by stage of development – Q3 2013-Q2 2016 (Deal volume)

700

600

500

400

300

200

100

0Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16

22 22 21 2962 65 75

16

57

25

119

447

371

149181

232

13312992

63

16

10

8169

122

100

138 147 165 160

314

312

544

367

603

272

109

1723

7 6 53 4

12 102518

PIPEEarly stage Late stageExpansion stage

14 MoneyTreeTM China TMT Report Q1/Q2 2016

Q1 2016

Total deal volume for the TMT industry reached 717 deals, with a total investment value of US$13.94 billion.

Deal volume by stage of development:

Early stage: 477 deals, 66% of the total

Expansion stage: 149 deals, 21% of the total

Late stage: 75 deals, 11% of the total

PIPE: 16 deals, 2% of the total

Figure 15: Deal value in TMT industry by stage of development Q1’16 (US$m)

$5,50339%

$3,80427%$3,720

27%

$9097%

PIPE

Early stageLate stage

Expansion stage

Deal value by stage of development

Expansion stage: US$5.50 billion, 39% of the total

Early stage: US$3.80 billion, 27% of the total

Late stage: US$3.72 billion, 27% of the total

PIPE: US$0.91 billion, 7% of the total

QoQ comparison between Q1 2016 and Q4 2015

Deal volume

Deal value

Early stage 75% 142%

Expansion stage

25% 219%

Late stage 15% 521%

PIPE 36% 45%

Figure 14: Deal volume in TMT industry by stage of development Q1’16

47766%

14921%

162%

7511%

PIPE

Early stage

Late stageExpansion stage

15MoneyTreeTM China TMT Report Q1/Q2 2016

Q2 2016

Total deal volume for the TMT industry reached 634 deals, with a total investment value of US$20.05 billion.

Deal volume by stage of development

Early stage: 371 deals, 59% of the total

Expansion stage: 181 deals, 28% of the total

Late stage: 57 deals, 9% of the total

PIPE: 25 deals, 4% of the total

Deal value by stage of development

Expansion stage: US$12.06 billion, 60% of the total

PIPE: US$3.83 billion, 19% of the total

Early stage: US$3.06 billion, 15% of the total

Late stage: US$1.10 billion, 6% of the total

Figure 16: Deal volume in TMT industry by stage of development Q2’16

37159%

18128%

579%

254%

PIPE

Early stage

Late stageExpansion stage

Figure 17: Deal value in TMT industry by stage of development Q2’16 (US$m)

$12,06060%

$3,83419%$3,054

15%

$1,1006%

PIPEEarly stageLate stage

Expansion stage

QoQ comparison between Q2 2016 and Q1 2016

Deal volume

Deal value

Early stage传 22% 44%

Expansion stage传传

21% 217%

Late stage传 24% 70%

PIPE 56% 332%

16 MoneyTreeTM China TMT Report Q1/Q2 2016

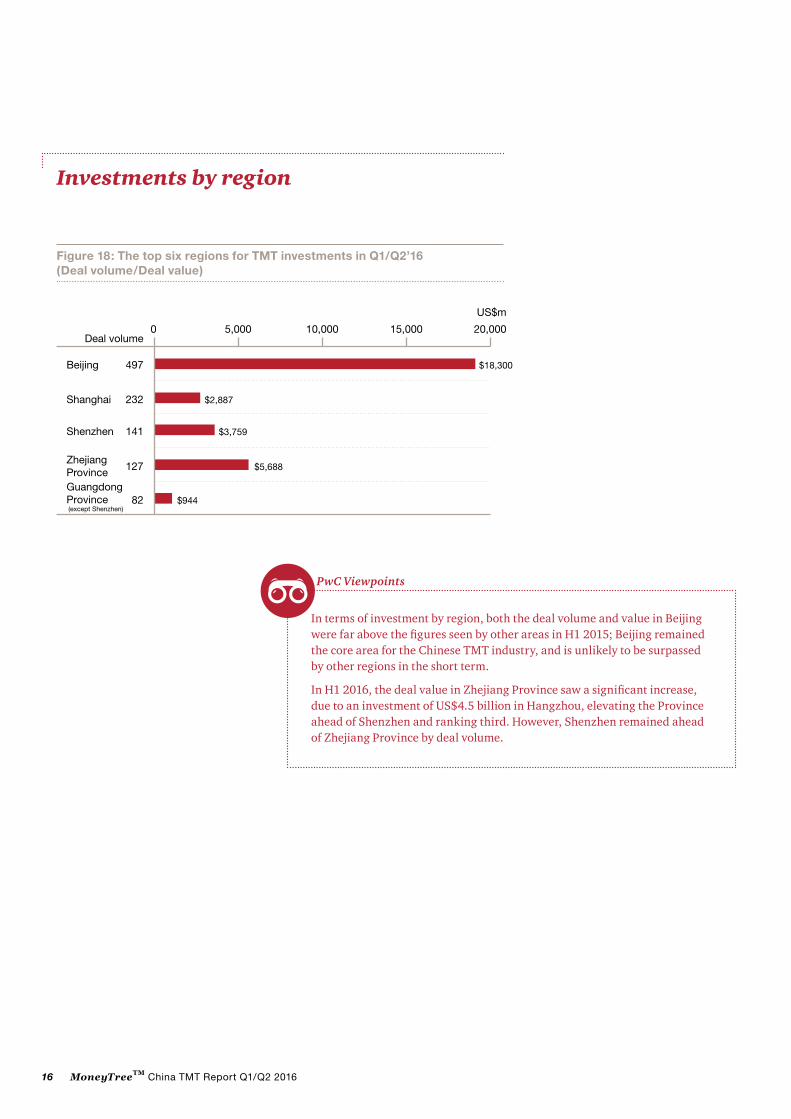

Investments by region

In terms of investment by region, both the deal volume and value in Beijing were far above the figures seen by other areas in H1 2015; Beijing remained the core area for the Chinese TMT industry, and is unlikely to be surpassed by other regions in the short term.

In H1 2016, the deal value in Zhejiang Province saw a significant increase, due to an investment of US$4.5 billion in Hangzhou, elevating the Province ahead of Shenzhen and ranking third. However, Shenzhen remained ahead of Zhejiang Province by deal volume.

PwC Viewpoints

Figure 18: The top six regions for TMT investments in Q1/Q2’16 (Deal volume/Deal value)

497

232

141

127

82

$18,300

$3,759

$5,688

$2,887

$944

0 5,000 10,000 20,00015,000

US$m

Deal volume

Beijing

Shanghai

Zhejiang Province

Shenzhen

Guangdong Province (except Shenzhen)

17MoneyTreeTM China TMT Report Q1/Q2 2016

Exits by quarter

3. PE/VC exits in the TMT industry

There were 46 exits in both Q1 and Q2 2016, following the 115 exits which occurred in H2 2015. In total, the amount of exits in H1 2016 decreased by 20% compared to H2 2015.

With the resumption of IPOs in H2 2015, the number of IPOs increased gradually, but the level still didn’t surpass that of strategic sales. In H1 2016, the number of strategic sales exceeded 60% of total exits, suggesting that there had been little if any affect from the resumption of IPOs. IPOs in A-shares are still facing a long waiting period at present, which is a big challenge for TMT companies that have seen relatively big fluctuations and this is a key factor underpinning the recent trends by TMT companies considering strategic sales, and other exit methods.

PwC Viewpoints

Figure 19: Exit volume in the TMT industry – Q3 2013-Q2 2016

80

70

60

50

40

30

20

10

0

Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16

23 2326

69

53

46 46

2014

18 16 17

18 MoneyTreeTM China TMT Report Q1/Q2 2016

The number of IPOs slightly increased in H1 2016 due to the resumption of IPOs in November 2015.

Strategic sales accounted for more than 60% of exits for the first time in H1 2016, an increase of approximately 12%.

Management buy-out and secondary sale made up only a small percentage of the exits in H1 2016, with no occurrences of either in Q2.

Exits by type

Figure 20: TMT exit trends by type – Q3 2013-Q2 2016

IPO

80

70

60

50

40

30

20

10

0

Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16

11

11 1 1

32

2

22 22 2

6 69 845 5

8

4

77

10

11

11

14 20 32

13

12

29 28

18

15

25

19

10

8

4

Strategic saleManagement buy-outSecondary sale

Q1 2016 Q2 2016

Strategic sale

Management buy-out

Secondary sale

IPO

29 28

18

3

12

2

63%

4%

26% 39%

7%

61%

PE/VC deal volume in all industries

19MoneyTreeTM China TMT Report Q1/Q2 2016

In 2016, the resumption of IPOs in the A-shares market led to increasing exits via IPOs, which rose by 20% from H2 2015.

As for the destination of IPOs, Shanghai Stock Exchange and the Growth Enterprise Board (GEM) of the Shenzhen Stock Exchange were the core areas for domestic IPOs, while the Hong Kong Main Board and the New York Stock Exchange were the main locations for IPOs overseas.

In Q1 2016, there were 46 exits in total, broken down as follows:

Strategic sale: 29 deals, 63% of the total

IPO: 12 deals, 26% of the total

Secondary sale: 3 deals, 7% of the total

Management buy-out (including buy-back): 2 deals, 4% of the total

In Q2 2016, there were 46 exits in total, broken down as follows:

Strategic sale: 28 deals, 61% of the total

IPO: 18 deals, 39% of the total

Figure 21: Comparison of TMT exits in mainland China, Hong Kong and US capital markets – Q3 2013-Q2 2016

Q3’13 50%50% Q4’13

43%

57%

Q1’14 Q2’14

90%

10%

64%

27%9%

Q4’14Q3’14

64%

27%9%

50% 57%

29%14%25%25%

Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16

86% 80%

10%10%14%

90%

10%

71%

29% 8%

92%

33%

67%

Mainland China Hong Kong US

Figure 22: Exit types in the TMT industry Q2’16

2963%

37%

1226%

24%

IPOStrategic sale

Secondary saleManagement buy-out

Figure 23: Exit types in the TMT industry Q2’16

2861%

1839%

IPOStrategic sale

PE/VC deal volume

Q1 2016

Q2 2016

Shanghai Stock Exchange

GEM Board of Shenzhen Stock Exchange

SME Board of Shenzhen Stock Exchange

Hong Kong Main Board

New York Stock Exchange

1

2 1

11

96

listed company

20 MoneyTreeTM China TMT Report Q1/Q2 2016

Exits by sectorQ1 2016

Exits by sector in the TMT industry:

Entertainment and Media: 22 deals, 48% of the total

Technology: 16 deals, 35% of the total

Internet: 5 deals, 11% of the total

Telecommunications and Mobile: 3 deals, 6% of the total

Figure 24: IPO exits in the TMT industry – Q3 2013-Q2 2016

40

35

30

25

20

15

10

5

0

Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14

0 02

22

2 2

13

9

9

6

12 11

1716

10

8 8 85

43

35

2722

16

22

11

57 7 7

33

34

4 4 4 4

11

Technology

InternetTelecommunications and Mobile

Entertainment and Media

Q2 2016

Exits by sector in the TMT industry:

Technology: 22 deals, 48% of the total

Internet: 11 deals, 24% of the total

Entertainment and Media: 8 deals, 20% of the total

Telecommunications and Mobile: 4 deals, 8% of the total

• Exits in the Technology, Internet, and Telecommunications and Mobile sector decreased significantly in Q1, but rose slightly in Q2.

• Exits in the Entertainment and Media sector increased greatly, the number of which reached a historical high since 2012, accounting for over 50% in Q1, but decreasing slightly in Q2.

21MoneyTreeTM China TMT Report Q1/Q2 2016

4. Sector focus: Technology, Internet, and Telecommunications and Mobile

Investments in Technology

The Technology sector includes IT Services, Hardware, Software, Electronics & Optoelectronics Devices and Semiconductor.

In Q2 2016, the deal value in the Electronics & Optoelectronics Devices subsector was the highest recorded since 2012

In Q2 2016, deal value in the Electronics & Optoelectronics Devices subsector increased by 907% compared to Q1 2016, reaching the highest level since 2012. The value was helped along by a deal worth US$2.4 billion in an Electronics & Optoelectronics Devices company.

In H1 2016, deal volume in the Software subsector accounted for the majority of the sector

In H1 2016, deal volume in the Software subsector experienced a decline, but still accounted for the majority of deals in the Technology sector. Deal value in Q1 2016 also surpassed other subsectors, but ranked second in Q2 2016, largely as a result of a huge investment in the Electronics & Optoelectronics Devices subsector.

In Q1 2016, deal value in the Hardware subsector reached the highest since 2012

In Q1 2016, deal volume and deal value in the Hardware subsector increased by 106% and 281%, respectively, compared to Q4 2015. This marked a substantial improvement from 2015, with the proportion of both surpassing the IT and the Semiconductor subsectors.

In H1 2016, investments in the IT and the Semiconductor sector decreased substantially

There were declines in investments in the IT and the Semiconductor subsectors in H1 2016, though the drops were minor compared to prior years.

Figure 25: Deal value in the Technology sector – Q3 2013-Q2 2016

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

$848

$1,583

$2,813

$2,389 $2,392

$1,632$1,461

$1,292

$3,594

$218

$1,001

$574

Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16

US$m

Hardware

Semiconductor IT Services

Software

Electronics & Optoelectronics Devices

Figure 26: Deal volume in the Technology sector – Q3 2013-Q2 2016

90

80

70

60

50

40

30

20

10

0

Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14

16

72 2

11

2326

26

35

44 44

79

70

34

34

18

59

3731

37

7 63 5

40

19

15

30 302522

23

16

2727

2421

13

5 5

23

22

153

3 32 2 27

15

15

21

13

913

1

26

HardwareSemiconductor

IT ServicesSoftwareElectronics & Optoelectronics Devices

22 MoneyTreeTM China TMT Report Q1/Q2 2016

QoQ comparison between Q1 2016

and Q4 2015

Deal volume

Deal value

Electronics & Optoelectronics Devices

24% 68%

Software 25% 88%

IT Services 30% 36%

Semiconductor传 50% 74%

Hardware 106% 281%

Deal volume and value

Q1 2016

There were a total of 136 deals in the Technology sector, with a total investment value of US$1.29 billion.

Software:44 deals, 33% of the total; deal value of US$0.51 billion, 40% of the total

Hardware:37 deals, 27% of the total; deal value of US$0.26 billion, 20% of the total

Electronics & Optoelectronics Devices:26 deals, 19% of the total; deal value of US$0.26 billion, 20% of the total

IT Services:26 deals, 19% of the total; deal value of US$0.22 billion, 17% of the total

Semiconductor:3 deals, 2% of the total; deal value of US$0.04 billion, 3% of the total

Figure 27: Deal volume by Technology subsector Q1’16

4433%3

2%

2619%

3727%

2619%

Hardware

SemiconductorIT Services

SoftwareElectronics & Optoelectronics Devices

Figure 28: Deal value by Technology subsector Q1’16 (US$m)

$51140%

$433%

$26420%

$25720%

$21717%

Hardware

SemiconductorIT Services

SoftwareElectronics & Optoelectronics Devices

23MoneyTreeTM China TMT Report Q1/Q2 2016

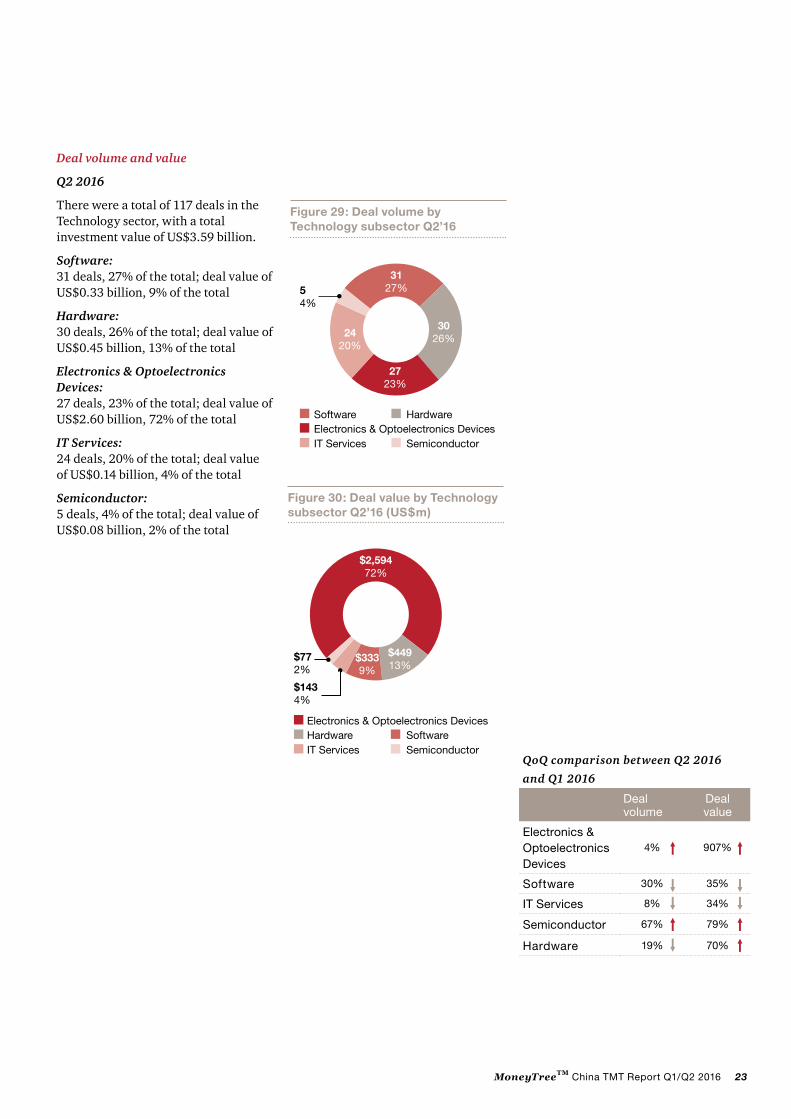

Deal volume and value

Q2 2016

There were a total of 117 deals in the Technology sector, with a total investment value of US$3.59 billion.

Software:31 deals, 27% of the total; deal value of US$0.33 billion, 9% of the total

Hardware:30 deals, 26% of the total; deal value of US$0.45 billion, 13% of the total

Electronics & Optoelectronics Devices:27 deals, 23% of the total; deal value of US$2.60 billion, 72% of the total

IT Services:24 deals, 20% of the total; deal value of US$0.14 billion, 4% of the total

Semiconductor:5 deals, 4% of the total; deal value of US$0.08 billion, 2% of the total

Figure 29: Deal volume by Technology subsector Q2’16

Figure 30: Deal value by Technology subsector Q2’16 (US$m)

3127%5

4%

3026%

2723%

2420%

Hardware

SemiconductorIT Services

SoftwareElectronics & Optoelectronics Devices

$2,59472%

$772%

$1434%

$3339%

$44913%

HardwareSemiconductorIT ServicesSoftware

Electronics & Optoelectronics Devices

QoQ comparison between Q2 2016

and Q1 2016

Dealvolume

Deal value

Electronics & Optoelectronics Devices 传传传传传

4% 907%

Software 30% 35%

IT Services传传 8% 34%

Semiconductor 传 67% 79%

Hardware 19% 70%

24 MoneyTreeTM China TMT Report Q1/Q2 2016

Investments by stage of development

PIPE investments continued to increase, and ranked first in terms of deal value

In H1 2016, PIPE investments maintained the robust momentum seen in H2 2015, with the deal volume and value repeatedly setting new records since 2012 and the deal value ranked the highest in the sector. The ranking benefited from a deal worth US$2.4 billion in an Electronics & Opto-electronics Devices company in Q2 2016.

Early-stage deal value increased while deal volume decreased slightly

In H2, early-stage deal volume accounted for the majority of the Technology sector as a whole, but total deal value was only slightly higher than that seen in late stage deals. From Q1, deal volume of early-stage investments decreased QoQ while deal value increased QoQ. The single-average-deal value rose sharply, but there was no investment with a single-deal value that was over US$100 million in H1 2016.

Investments at the expansion and late stages decreased in H1 2016

In H1 2016, volume in expansion and late stage deals decreased by 53% compared to H2 2015, while deal value decreased by 7% and 73%, respectively. There was only one deal with a single-deal value of over US$100 million in H1 2016. No huge investments were made in late-stage companies.

Figure 31: Deal value by stage of development in the Technology sector – Q3 2013-Q2 2016

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

$218$574

$2,813

$2,389

$1,001

$1,632$1,461

$1,292

$2,392

$3,594

$848

$1,583

Q1’16 Q2’16Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15

PIPE Early stageExpansion stageLate stage

US$m

Figure 32: Deal volume by stage of development in the Technology sector – Q3 2013-Q2 2016

120

100

80

60

40

20

0

Q1’16 Q2’16Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15

3126

2410 10

1714

40 40

106

6 715

54 54

37

48

98

88

76

48

8

3

21 21 21

11

4

8

25

3120

10

37

36

68

39

34 34

34

46 45

32

14

3

PIPEEarly stage Expansion stage Late stage

25MoneyTreeTM China TMT Report Q1/Q2 2016

QoQ comparison between Q2 2016

and Q1 2016

Deal volume

Deal value

Early stage 17% 84%

Expansion stage技

‒ 37%

Late stage 48% 62%

PIPE 113% 421%

Investments by stage of development

Q1 2016

Early stage:54 deals, 40% of the total; deal value of US$124 million, 10% of the total

Late stage:40 deals, 29% of the total; deal value of US$170 million, 13% of the total

Expansion stage:34 deals, 25% of the total; deal value of US$415 million, 32% of the total

PIPE:8 deals, 6% of the total; deal value of US$584 million, 45% of the total

Q2 2016

Early stage:45 deals, 39% of the total; deal value of US$228 million, 6% of the total

Expansion stage:34 deals, 29% of the total; deal value of US$262 million, 7% of the total

Late stage:21 deals, 18% of the total; deal value of US$64 million, 2% of the total

PIPE:17 deals, 14% of the total; deal value of US$3,040 million, 85% of the total

Figure 33: Deal volume by stage of development in the Technology sector Q1’16

Figure 34: Deal value by stage of development in the Technology sector Q1’16 (US$m)

5440%

86%

4029%34

25%

PIPEEarly stageExpansion stage

Late stage

$12410%

$58445%

$41532%$170

13%

PIPEEarly stageExpansion stage

Late stage

Figure 35: Deal volume by stage of development in the Technology sector Q2’16

Figure 36: Deal value by stage of development in the Technology sector Q2’16 (US$m)

4539%

3429%

2118%

1714%

PIPEEarly stage Expansion stageLate stage

$3,04085%

$642%

$2286%

$2627%

PIPEEarly stage

Expansion stageLate stage

QoQ comparison between Q1 2016

and Q4 2015

Deal volume

Deal value

Early stage 46% 4%

Expansion stage技

29% 124%

Late stage 26% 70%

PIPE 47% 2%

26 MoneyTreeTM China TMT Report Q1/Q2 2016

Investments by region

Figure 37: The top six regions for Technology investments Q1/Q2’16 (Deal volume/Deal value)

68

40 $514

$3,143

33 $254

25 $174

22 $351

0 3,0002,5002,0001,5001,000500 3,500Deal volume

Beijing

Shanghai

Shenzhen

Guangdong Province (except Shenzhen)

Zhejiang Province

US$m

27MoneyTreeTM China TMT Report Q1/Q2 2016

The total quarterly investment value of Internet Services in Q1 reached the highest level recorded since 2012

In H1 2016, investments in the Internet Services sector performed well and accounted for more than 40% of Internet sector investments, which was in line with the sector performance in H2 2015. The deal value in both Q1 and Q2 exceeded US$2 billion, with the deal value in Q1 reaching US$2.8 billion, the highest level recorded since 2012. In H1 2016, there were a total of seven deals in the Internet Services subsector, each with a single deal value of over US$100 million. Among the seven deals, the largest by value was worth US$1.5 billion, involving a well-known online network data company.

The total quarterly investment value of E-commerce in Q1 reached record highs

In H1 2016, E-commerce performed comparably to Internet Services. Although the deal volume kept basically the same as H2 2015, the deal value rose by 158% QoQ. The total investment value reached as high as US$4.6 billion in Q1, mainly due to a deal worth US$3.3 billion involving a

Investments in Internet

The Internet sector includes E-commerce, Online Education, Internet Services, Online Entertainment, Social Media, Internet Marketing and Internet Finance.

well-known B2C company.

Investments in Internet Finance developed rapidly in H1 2016

In H1 2016, the Internet Finance sector saw its biggest growth since 2012. The deal value in Q1 was four times that of Q4 2015, and deal value in Q2 was more than twice the level of Q1, with a total of more than US$5 billion. Among the 10 deals with a single deal value of over US$100 million each in H1 2016, two deals were worth US$1 billion or more, with one valued at US$4.5 billion and the other US$1 billion. The two deals played a key role in shaping investments in Internet Finance over

Figure 38: Deal value in the Internet sector – Q3 2013-Q2 2016

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

Q1’15

$578 $854$1,654 $1,782 $2,267 $1,996

$4,819$3,728

$5,361

$3,505

$11,563

$9,712

Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14

E-commerceInternet Services

Internet Marketing Social Media

Online Education

Online EntertainmentInternet Finance

US$m

Figure 39: Deal volume in the Internet sector – Q3 2013-Q2 2016

250

200

150

100

50

0Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14

47 55 55 55 54 5758

92

158

107

192

61 61

21 21

48

10

39 3939

80 82 87

154

219

90 9479

132

1723 1417

6 6

12

1616

1616

4 8 85 6 613

211 12 16 1611 1123

3129 2924

12

18 18 19 19 194 4 9

107 7 7 37

1426 24 24

2614

15

10

102

E-commerce Internet Services

Internet MarketingSocial Media

Online Education Online Entertainment

Internet Finance

the period.

The quarterly deal value of Online Entertainment in Q1 hit US$1 billion for the first time since 2012, with deal volume equalling the highest on record

The quarterly deal value of Online Entertainment in Q1 hit US$1 billion, a dramatic increase compared to 2015, and reaching the highest value seen since 2012. The deal volume in Q1 and Q2 was the same, equalling the record level set in Q2 2012. In H1 2016, Online Entertainment also saw a huge investment of US$1 billion, which was made in a well-known network video enterprise.

28 MoneyTreeTM China TMT Report Q1/Q2 2016

QoQ comparison between Q1 2016 and

Q4 2015

Deal volume

Dealvalue

E-commerce 89% 597%

Online Education 13% 88%

Internet Services 79% 82%

Online Entertainment

271% 2,846%

Social Media 233% 284%

Internet Marketing 85% 26%

Internet Finance 技技 49% 399%

Deal volume and value

Q1 2016

There were 426 deals in the Internet sector in Q1 2016, with a total investment value of US$11.56 billion.

Internet Services:192 deals, 45% of the total; deal value of US$2.79 billion, 24% of the total

E-commerce:102 deals, 24% of the total; deal value of US$4.56 billion, 39% of the total

Internet Finance:58 deals, 14% of the total; deal value of US$2.56 billion, 22% of the total

Online Entertainment: 26 deals, 6% of the total; deal value of US$1.33 billion, 12% of the total

Internet Marketing:24 deals, 6% of the total; deal value of US$0.23 billion, 2% of the total

Online Education:14 deals, 3% of the total; deal value of US$0.05 billion, 0.7% of the total

Social Media:10 deals, 2% of the total; deal value of US$0.03 billion, 0.3% of the total

Figure 40: Deal volume by Internet subsector Q1’16

19245%

266%

143%

246%

102%

10224%

5814%

E-commerceInternet Services

Internet MarketingSocial Media

Online Education Internet FinanceOnline Entertainment

Figure 41: Deal value by Internet subsector Q1’16 (US$m)

$2,79324%

$4,56139%

$270.3%

$2322%

$520.7%

$2,56422%

$1,33412%

E-commerce Internet Services

Internet MarketingSocial Media

Online Education Internet Finance Online Entertainment

29MoneyTreeTM China TMT Report Q1/Q2 2016

QoQ comparison between Q2 2016 and

Q1 2016

Deal volume

Dealvalue

E-commerce 10% 76%

Online Education 71% 89%

Internet Services 18% 15%

Online Entertainment

− 77%

Social Media 40% 209%

Internet Marketing 38% 73%

Internet Finance 技技 2% 122%

Deal volume and value

Q2 2016

There were 386 deals in the Internet sector in Q2 2016, with a total investment value of US$9.71 billion.

Internet Services:158 deals, 41% of the total; deal value of US$2.38 billion, 25% of the total

E-commerce:92 deals, 24% of the total; deal value of US$1.09 billion, 11% of the total

Internet Finance:57 deals, 15% of the total; deal value of US$5.69 billion, 59% of the total

Online Entertainment:26 deals, 7% of the total; deal value of US$0.31 billion, 3% of the total

Online Education:24 deals, 6% of the total; deal value of US$0.10 billion, 1% of the total

Internet Marketing:15 deals, 4% of the total; deal value of US$0.06 billion, 0.4% of the total

Social Media:14 deals, 3% of the total; deal value of US$0.08 billion, 0.6% of the total

Figure 42: Deal volume by Internet subsector Q2’16

Figure 43: Deal value by Internet subsector Q2’16 (US$m)

15841%

267%

154%246%

143%

9224%

5715%

E-commerceInternet Services

Internet Marketing

Social MediaOnline Education Internet Finance Online Entertainment

$2,38225%

$5,68959%

$630.4%

$820.6%

$981%

$3133%

$1,08511%

E-commerceInternet Services

Internet MarketingSocial MediaOnline Education

Internet FinanceOnline Entertainment

30 MoneyTreeTM China TMT Report Q1/Q2 2016

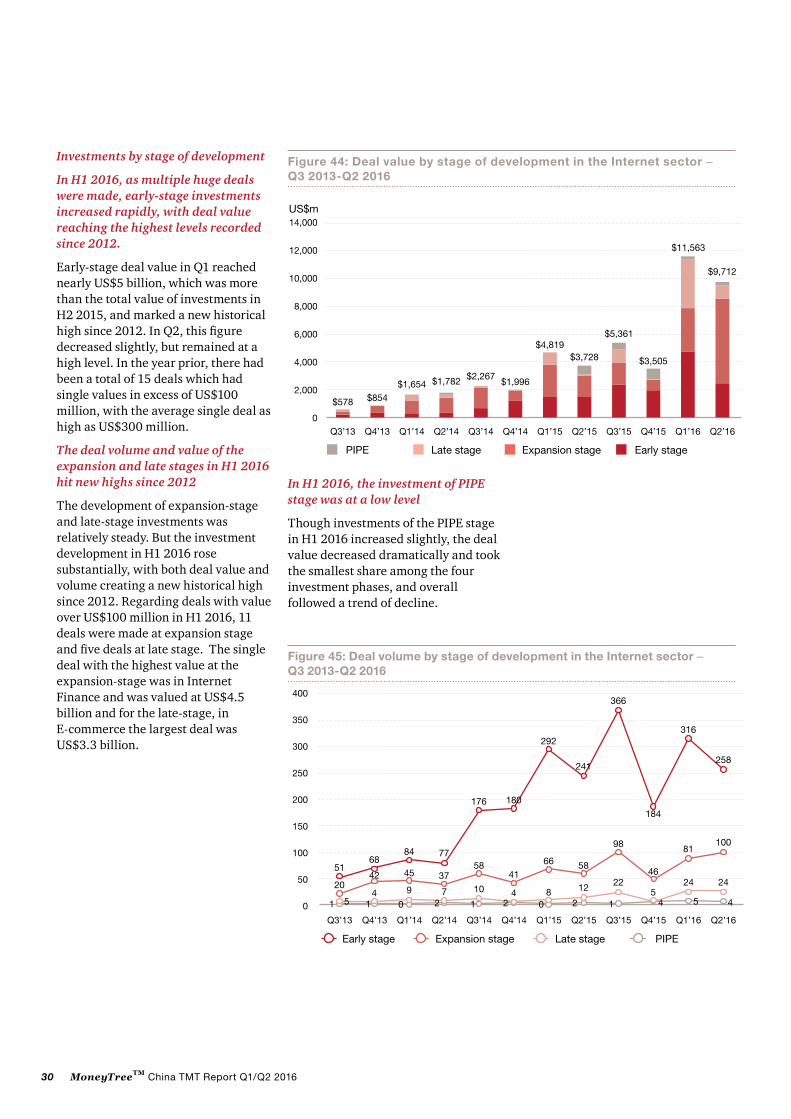

Investments by stage of development

In H1 2016, as multiple huge deals were made, early-stage investments increased rapidly, with deal value reaching the highest levels recorded since 2012.

Early-stage deal value in Q1 reached nearly US$5 billion, which was more than the total value of investments in H2 2015, and marked a new historical high since 2012. In Q2, this figure decreased slightly, but remained at a high level. In the year prior, there had been a total of 15 deals which had single values in excess of US$100 million, with the average single deal as high as US$300 million.

The deal volume and value of the expansion and late stages in H1 2016 hit new highs since 2012

The development of expansion-stage and late-stage investments was relatively steady. But the investment development in H1 2016 rose substantially, with both deal value and volume creating a new historical high since 2012. Regarding deals with value over US$100 million in H1 2016, 11 deals were made at expansion stage and five deals at late stage. The single deal with the highest value at the expansion-stage was in Internet Finance and was valued at US$4.5 billion and for the late-stage, in E-commerce the largest deal was US$3.3 billion.

Figure 44: Deal value by stage of development in the Internet sector – Q3 2013-Q2 2016

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0Q1’15

$578 $854$1,654 $1,782 $2,267

$1,996

$4,819$3,728

$5,361

$3,505

$11,563

$9,712

Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14

PIPE Expansion stageLate stage Early stage

US$m

Figure 45: Deal volume by stage of development in the Internet sector – Q3 2013-Q2 2016

400

350

300

250

200

150

100

50

0

Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14

0 01 1 1 12 2 255

54 49 7 44 8 12 22 24 24

102042 45 37

5841

66 58

98 81100

316

258

465168

84 77

176 180

292

241

366

184

PIPEExpansion stage Late stageEarly stage

In H1 2016, the investment of PIPE stage was at a low level

Though investments of the PIPE stage in H1 2016 increased slightly, the deal value decreased dramatically and took the smallest share among the four investment phases, and overall followed a trend of decline.

31MoneyTreeTM China TMT Report Q1/Q2 2016

Investments by stage of development

Q1 2016

There were 426 deals in the Internet sector, with a total investment value of US$5.36 billion.

Early stage:316 deals, 74% of the total; deal value of US$4.73 billion, 41% of the total

Expansion stage:81 deals, 19% of the total; deal value of US$3.11 billion, 27% of the total

Late stage:24 deals, 6% of the total; deal value of US$3.52 billion, 30% of the total

PIPE:5 deals, 1% of the total; deal value of US$0.20 billion, 2% of the total

Q2 2016

There were 386 deals in the Internet sector, with a total investment value of US$9.71 billion.

Early stage:258 deals, 67% of the total; deal value of US$2.47 billion, 25% of the total

Expansion stage:100 deals, 26% of the total; deal value of US$6.06 billion, 63% of the total

Late stage:24 deals, 6% of the total; deal value of US$0.96 billion, 10% of the total

PIPE:4 deals, 1% of the total; deal value of US$0.23 billion, 2% of the total

Figure 46: Deal volume by stage of development in the Internet sector Q1’16

Figure 47: Deal value by stage of development in the Internet sector Q1’16 (US$m))

Figure 48: Deal volume by stage of development in the Internet sector Q2’16

Figure 49: Deal value by stage of development in the Internet sector Q2’16 (US$m)

31674%

8119%

246%

51%

Expansion stageLate stageEarly stage

PIPE

$3,52230%

$3,10927%

$4,73141%

PIPE

2012%

Expansion stageLate stageEarly stage

25867%

41% 100

26%246%

Expansion stageLate stageEarly stage

PIPE

$2272%

$6,06363%

$2,46525%

$95710%

Expansion stageLate stage

Early stagePIPE

QoQ comparison between Q1 2016

and Q4 2015

Deal volume

Deal value

Early stage 72% 143%

Expansion stage

76% 308%

Late stage 380% 14,512%

PIPE 25% 74%

QoQ comparison between Q2 2016

and Q1 2016

Deal volume

Deal value

Early stage 18% 48%

Expansion stage

23% 95%

Late stage − 73%

PIPE 20% 13%

32 MoneyTreeTM China TMT Report Q1/Q2 2016

Investments by region

Figure 50: The top six regions for Internet sector investments in Q1/Q2’16 (Deal volume/Deal value)

309 $8,661

79 $5,352

75 $2,975

42 $711

148 $2,134

0 2,000 4,000 6,000 10,0008,000Deal volume

Beijing

Shanghai

Shenzhen

JiangsuProvince

ZhejiangProvince

US$m

33MoneyTreeTM China TMT Report Q1/Q2 2016

Investments in Telecommunications and MobileThe Telecommunications and Mobile sector includes Telecom Equipment and Terminals, Other Tele-communications Sectors and Mobile.

Deal volume and value

Q1 2016

There were 105 deals in the Telecommunications and Mobile sector, with a total investment value of US$794 million.

Mobile:96 deals, 91% of the total; deal value of US$697 million, 87.7% of the total

Telecom Equipment and Terminals:7 deals, 7% of the total; deal value of US$95 million, 12% of the total

Other Telecommunications Sectors:2 deals, 2% of the total; deal value of US$2 million, 0.3% of the total

Mobile: The largest single deal value was in Q2, which was the highest value recorded in the TMT industry since 2012

In Q1, the deal value increased by 77% QoQ compared to Q4 2015, and deal value in Q2 was nearly US$5 billion, almost six times that in Q1, a dramatic increase that represented the highest level recorded since 2012. The deal value in Mobile accounted for 98% of the total, mainly due to the US$4.5 billion invested in a well-known taxi hailing app enterprise in Q2. This deal value also reached the highest single-deal value in the TMT industry since 2012, equalling another large deal within Internet Finance.

Other Telecommunications Sectors and Telecom Equipment and Terminals: Investments remained stable in H1 2016

Other Telecommunications Sectors and Telecom Equipment and Terminals took a relatively small share compared to the Mobile sector, and both the deal value and volume in H1 2016 were at a relatively low level, without large fluctuations when compared with prior years.

Figure 51: Deal volume by subsegment in the Telecommunications and Mobile sector Q1’16

Figure 52: Deal value by subsegment in the Telecommunications and Mobile sector Q1’16 (US$m)

9691%

22%77%

MobileTelecom Equipment and TerminalsOther Telecommunications Sectors

$69788%

$20.3%

$9512%

MobileTelecom Equipment and TerminalsOther Telecommunications Sectors

34 MoneyTreeTM China TMT Report Q1/Q2 2016

Q2 2016

There were 64 deals in the Telecommunications and Mobile sector, with a total investment value of US$4.95 billion.

Mobile:56 deals, 87% of the total; deal value of US$4.84 billion, 97% of the total

Other Telecommunications Sectors:5 deals, 8% of the total; deal value of US$0.07 billion, 2% of the total

Telecom Equipment and Terminals:3 deals, 5% of the total; deal value of US$0.05 billion, 1% of the total

Figure 53: Deal volume by subsectors in the Telecommunications and Mobile sector Q2’16

Figure 54: Deal value by subsectors in the Telecommunications and Mobile sector Q2’16(US$m)

5687%

35%

58%

Mobile

Telecom Equipment and TerminalsOther Telecommunications Sectors

$4,83597%

$702%

$471%

Mobile

Telecom Equipment and TerminalsOther Telecommunications Sectors

QoQ comparison between Q1 2016

and Q4 2015

Deal volume

Dealvalue

Mobile 96% 77%

Telecom Equipment and Terminals

75% 417%

Other Telecommunications Subsectors 传传

75% 97%

QoQ comparison between Q2 2016

and Q1 2016

Deal volume

Dealvalue

Mobile 42% 594%

Telecom Equipment and Terminals

29% 27%

Other Telecommunications Subsectors 传传

50% 2,238%

35MoneyTreeTM China TMT Report Q1/Q2 2016

Investments by stage of development

Q1 2016

Early stage:79 deals, 75% of the total; deal value of US$450 million, 57% of the total

Expansion stage:21 deals, 20% of the total; deal value of US$261 million, 33% of the total

Late stage:4 deals, 4% of the total; deal value of US$7 million, 1% of the total

PIPE:1 deals, 1% of the total; deal value of US$77 million, 9% of the total

Q2 2016

Early stage:38 deals, 59% of the total; deal value of US$296 million, 6% of the total

Expansion stage:20 deals, 31% of the total; deal value of US$4.60 billion, 93% of the total

Late stage:6 deals, 10% of the total; deal value of US$52 million, 1% of the total

PIPE:No deals

Figure 55: Deal volume by stage of development in the Telecommunications and Mobile sector Q1’16

Figure 57: Deal volume by stage of development in the Telecommunications and Mobile sector Q2’16

Figure 56: Deal value by stage of development in the Telecommunications and Mobile sector Q1’16 (US$m)

Figure 58: Deal value by stage of development in the Telecommunications and Mobile sector Q2’16 (US$m)

7975%

2120%1

1%44%

PIPEEarly stage Expansion stageLate stage

$45057%

$26133%

$779%

$71%

PIPE Early stage Expansion stage

Late stage

3859%

2031%

610%

Early stage Expansion stageLate stage

QoQ comparison between Q1 2016

and Q4 2015

Deal volume

Deal value

Early stage 88% 127%

Expansion stage

62% 53%

Late stage 100% 40%

PIPE 75% 24%

QoQ comparison between Q2 2016

and Q1 2016

Deal volume

Deal value

Early stage 52% 34%

Expansion stage

5% 1,664%

Late stage 50% 691%

PIPE 100% 100%

$4,60393%

$521%$2966%

Early stage Expansion stageLate stage

36 MoneyTreeTM China TMT Report Q1/Q2 2016

Investments by region

Figure 59: The top six regions for investment in the Telecommunications and Mobile sector Q1/Q2'16 (Deal volume/Deal value)

73 $5,017

12

8

$7718

$136

6 $53

$42

35 $328

0 6,0005,0003,000 4,0002,0001,000

Beijing

Shanghai

Shenzhen

ZhejiangProvince

JiangsuProvince

Guangdong Province (except Shenzhen)

Deal volume

US$m

37MoneyTreeTM China TMT Report Q1/Q2 2016

The Mobile sector includes Mobile Entertainment, Mobile Advertising, Mobile Shopping, Mobile Healthcare, Mobile Technology, Mobile Education, Mobile Services, Mobile Social Media and Mobile Messaging.

5. A close look at investments in Mobile

MobileShopping

Mobile

MobileEntertainment Mobile

Technology

Mobile Services(Including Mobile TravelServices, Mobile Housekeeeping Services)

Mobile Messaging

Education

Mobile Social Media

Mobile Advertising

Mobile Healthcare

(Including Mobile Video, Mobile Music, Mobile Gaming, etc.)

Figure 59: The top six regions for investment in the Telecommunications and Mobile sector Q1/Q2'16 (Deal volume/Deal value)

73 $5,017

12

8

$7718

$136

6 $53

$42

35 $328

0 6,0005,0003,000 4,0002,0001,000

Beijing

Shanghai

Shenzhen

ZhejiangProvince

JiangsuProvince

Guangdong Province (except Shenzhen)

Deal volume

US$m

38 MoneyTreeTM China TMT Report Q1/Q2 2016

Deal volume and value

Q1 2016

There were 96 deals in the Mobile sector in Q1 2016, with a total investment value of US$697 million.

Mobile Services:35 deals, 37% of the total; deal value of US$243 million, 35% of the total

Mobile Social Media:17 deals, 18% of the total; deal value of US$28 million, 4% of the total

Mobile Entertainment:14 deals, 15% of the total; deal value of US$35 million, 5% of the total

Mobile Healthcare:10 deals, 10% of the total; deal value of US$131 million, 19% of the total

Mobile Shopping:8 deals, 8% of the total; deal value of US$136 million, 19% of the total

Mobile Advertising:6 deals, 6% of the total; deal value of US$87 million, 12% of the total

Mobile Technology:3 deals, 3% of the total; deal value of US$34 million, 5% of the total

Mobile Education:3 deals, 3% of the total; deal value of US$3 million, 1% of the total

Mobile Messaging:No deals

Deal volume and value

Q2 2016

There were 56 deals in the Mobile sector in Q2 2016, with a total investment value of US$4.84 billion.

Mobile Services:19 deals, 34% of the total; deal value of US$4.58 billion, 95% of the total

Mobile Social Media:13 deals, 23% of the total; deal value of US$171 million, 3% of the total

Mobile Entertainment:12 deals, 21% of the total; deal value of US$47 million, 1% of the total

Mobile Technology:3 deals, 5% of the total; deal value of US$5 million, 0.1% of the total

Mobile Education:3 deals, 5% of the total; deal value of US$8 million, 0.2% of the total

Mobile Advertising:2 deals, 4% of the total; deal value of US$2 million, 0.1% of the total

Mobile Shopping:2 deals, 4% of the total; deal value of US$13 million, 0.3% of the total

Mobile Healthcare:2 deals, 4% of the total; deal value of US$12 million, 0.3% of the total

Mobile Messaging:No deals

Figure 60: Deal value by Mobile Internet subsegments – Q3 2013-Q2 2016

6,000

5,000

4,000

3,000

2,000

1,000

0

Q1’15

$215 $175 $448 $482$859 $853

$393$697

$1,386 $1,239

$4,247

$4,835

Q2’15 Q3’15 Q4’15 Q1’16 Q2’16Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14

US$m

Mobile Entertainment Mobile Advertising Mobile Shopping

Mobile Healthcare Mobile TechnologyMobile Education

Mobile Services Mobile Social MediaMobile Messaging

39MoneyTreeTM China TMT Report Q1/Q2 2016

In H1 2016, Mobile Services, Mobile Social Media and Mobile Healthcare were the three pillars of the Mobile sector

Mobile Services: The top ranking subsector had huge investments once again in taxi-hailing APPs

Taxi-hailing apps have been the major investment area for the Mobile Services subsector since 2014. In Q2 2016, a single deal valued at US$4.5 billion for a taxi-hailing app company was the biggest single-deal value in the TMT industry since 2012, creating a historical high for the total investments in Q2. Deal volume accounted for over 30%, and though it decreased slightly, there were no significant fluctuations.

Mobile is by now widely recognised as a sector located at the forefront of development, with broad appeal stemming from innovative developments such as Mobile Services and Mobile Social Media. Additionally, mobile service apps for the O2O platform remain red hot, while many traditional enterprises are striving to formulate strategies to adapt to "Internet +" in order to seek new breakthroughs and fresh opportunities. In the near future, fields such as social media and entertainment will mature, while more attention will be paid to areas such as healthcare and education.

PwC Viewpoints

Figure 61: Deal volume by Mobile subsegments – Q3 2013-Q2 2016

60

50

40

30

20

10

0

Q1’16 Q2’16Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15

1 1 1 11 1 1 1 11

1011 12

118 8 8 8 8 87 77 76 6 6 6 6 6 65 5 5 5

1512

14 14 1416

201819 19 19 19

15

24

20 2023 23

29 29 29

44

53

3235

2931

2 2 2 2 2223 3 3 33 333 4 4 443

9 9 9 9

2 2

10 10 1010

6

17

12 13

Mobile Entertainment Mobile Advertising Mobile Shopping

Mobile Healthcare Mobile TechnologyMobile Education

Mobile Services Mobile Social MediaMobile Messaging

Mobile Social Media: Ranking second, deal value in Q2 surpassed the previous peak since 2012

In H1 2016, the deal volume in Mobile Social Media decreased slightly compared to H2 2015. However, the deal value in Q2 surpassed that of Q3 2015, the highest level recorded since 2012. Additionally, there was a B round with a huge investment amounting to US$100 million in Mobile Social Media in Q2.

Mobile Healthcare: Ranking third, with both deal value and volume reaching new highs since 2012

In H1 2016, Mobile Healthcare surpassed Mobile Entertainment and jumped to the third spot, with a dramatic QoQ increase in both deal volume and deal value, both reflecting new record highs since 2012. The deal volume reached 10 for the first time, while deal value exceeded US$100 million.

40 MoneyTreeTM China TMT Report Q1/Q2 2016

6. Methodology and definitions

TMT is an acronym for Telecommunications, Media and Technology. The three words represent Telecommunications and Mobile, Media and Technology, respectively. In this report, we have carried out analysis of the three most active sectors within TMT. They are Technology, Internet and Telecommunications and Mobile.

This report covers Q1 and Q2 2016. However, in order to show trends and make comparisons in the industry, we have included data from the year H2 2013 to 2015. In this report, only deals disclosing specific investment data were included in relevant analysis. Deals that did not disclose the specific investment period, deal value or investment stage were excluded from the relevant analysis in order to maintain the accuracy of the report.

All data in this report was provided by Zero2IPO Research.

DefinitionsTechnology sector

Hardware: Computer hardware, computer peripherals, network equipment, etc.

Software: Basic software, software applications, etc.

IT Services: IT consultation, software outsourcing, hosting services, computer and network security, etc.

Electronics & Optoelectronics Devices: Optoelectronic components, optoelectronics, electronics, power supply, etc.

Semiconductor: IC design, IC testing and packaging, IC equipment manufacturing, etc.

Internet sector

E-commerce: B2C, B2B, C2C, etc.

Internet Marketing: Information portal, search engine, advertising agency and Internet marketing services

Internet Services: Online travel services, online recruitment services, online housekeeping services, etc.

Online Education: E-learning, online classroom, etc.

Online Entertainment: Online gaming, online video and online music

Social Media: BBS/Forum, online networking, etc.

Internet Finance: I-finance, E-payment, etc.

Telecommunications and Mobile sector

Telecom Equipment and Terminals: Telecommunications and mobile equipment, telecommunications and mobile terminals, telecommunications and mobile software, etc.

Other Telecommunications Subsectors: Mobile operators, Fixed-line operators, Virtual network operator (VNO) and others

Mobile: Mobile entertainment, Mobile advertising, Mobile shopping, Mobile healthcare, Mobile technology, Mobile education, Mobile services, Mobile social media, and Mobile messaging

Entertainment and Media sector

Traditional Media: Newspaper, magazines, publishing, etc.

Outdoor Media: Outdoor print ads, outdoor LED TV, mobile TV, building TV, etc.

Video Production and Distribution: Film and television production and distribution, film projection, etc.

Advertising Creation/Agency: Ad creation, media buying, ad agency, etc.

Cultural Transmission: Culture brokerage and agency, etc.

Entertainment & Leisure: Animation and other industries

41MoneyTreeTM China TMT Report Q1/Q2 2016

Stage of development

Early stage: This stage varies from one to five years while the product or concept is under development and not yet in mass and commercial production. During this stage, funds are mainly used for acquiring production equipment and developing products as well as marketing and setting up management systems.

Expansion stage: The investment period at this stage usually lasts about two or three years. The products or services have been recognised by the market. The company generally needs more funds to further develop the product, as well as to expand facilities and production. Inventory planning and marketing efforts are also ramped up.

Late stage: During this stage, the company has grown its operating revenue, and is more likely to be, but not necessarily, profitable. The company may have plans to go public. The main purpose of financing is to seek capital to grow capacity, and to introduce shareholders with industry experience and influence, thereby increasing corporate recognition and attracting shareholders. The company will aim to improve its financial structure and management system in preparation for listing. At this stage, the investment risk is the lowest, but the chance of high returns is also lower.

PIPE (private investment in public equity): PE investments in publicly listed companies via preferential allotments or private placements, and the acquisition of shares by PE firms via the secondary market.

Exits

IPO: IPO is short for initial public offering. IPO refers to listing on the stock markets in Shanghai, Shenzhen, Hong Kong, and overseas.

Strategic sale: This includes the sale of the PE or VC investors’ equity stakes (or the entire investee company itself) to a third-party company.

Management buy-out: The purchase of a company by its management through either debt-credit finance or stock transaction, which results in relevant changes in corporate ownership, control, residual claim and assets, in order to alter the structure of corporate proprietary rights. Through management buy-out, the company’s operators become its owners.

Secondary sale: Any purchase of the PE or VC investors’ equity stakes by another PE or VC investors constitutes secondary sale.

42 MoneyTreeTM China TMT Report Q1/Q2 2016

If you’d like to discuss what’s happening in your particular TMT market or how PwC might be able to help your company meet its challenges, please reach out to one of the TMT industry leaders listed here.

7. Contacts

Shenzhen Wilson Chow

PwC China/Hong Kong TMT Leader+86 (755) 8261 8886 [email protected]

Beijing

Qin Zhang+86 (10) 6533 2098 [email protected]

Shanghai

Jianbin GaoPwC China TMT Leader+86 (21) 2323 3362 [email protected]

Roland Xu+86 (21) 2323 2588 [email protected]

Frank Lin+86 (21) 2323 [email protected]

MoneyTreeTM China TMT Report Editorial Team

Frank LinPartner, TMT [email protected]

Stacy ZhangMarketing Manager, Private Equity & [email protected]

Catherine GuSenior Associate, [email protected]

GlobalRaman Chitkara+1 408 817 [email protected]

AustraliaRod Dring+61 2 8266 [email protected]

BrazilEstela Vieira+55 1 3674 [email protected]

CanadaChristopher Dulny+1 416 869 [email protected]

ChinaJianbin Gao+86 (21) 2323 [email protected]

FrancePierre Marty+33 1 5657 [email protected]

GermanyWerner Ballhaus+49 211 981 [email protected]

IndiaSandeep Ladda+91 22 6689 [email protected]

JapanMasahiro Ozaki+81 3 5326 9090 [email protected]

KoreaHoonsoo Yoon+82 2 709 [email protected]

NetherlandsIlja Linnemeijer+31 (0) 88 792 49 [email protected]

RussiaYury Pukha+7 495 223 [email protected]

SingaporeMark Jansen+65 6236 [email protected]

TaiwanAndy Chang+886 (2) 2729 6666 ext [email protected]

UAEPhilip Shepherd+97 1 4304 [email protected]

UKJass Sarai+44 (0) 1895 52 [email protected]

USPierre-Alain Sur+1 646 471 [email protected]

43MoneyTreeTM China TMT Report Q1/Q2 2016

www.pwc.com This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

© 2016 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

PwC – Gobal

PwC helps organizations and individuals create the value they’re looking for. We’re a network of firms in 157 countries with more than 208,000 people who are committed to delivering quality in assurance, tax and advisory services. Tell us what matters to you and find out more by visiting us at www.pwc.com.

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure (http://www.pwc.com/structure) for further details.

PwC – Mainland China, Hong Kong and Macau

PwC in Mainland China, Hong Kong and Macau work together on a collaborative basis, subject to local applicable laws. Collectively, we have around 700 partners and a strength of around 18,000 people.

Providing organizations with the advice they need, wherever they may be located. Our highly qualified, experienced professionals listen to different points of view to help organizations solve their business issues and identify and maximize the opportunities they seek. Our industry specialization allows us to help co-create solutions with our clients for their sector of interest.

We are located in these cities: Beijing, Shanghai, Shenyang, Tianjin, Chongqing, Dalian, Xi’an, Qingdao, Nanjing, Suzhou, Hangzhou, Ningbo, Changsha, Xiamen, Guangzhou, Shenzhen, Wuhan, HongKong and Macau.

About PwC’s Technology Institute

The Technology Institute is PwC’s global research network that studies the business of technology and the technology of business with the purpose of creating thought leadership that offers both fact-based analysis and experience-based perspectives. Technology Institute insights and viewpoints originate from active collaboration between our professionals across the globe and their first-hand experiences working in and with the technology industry.