pricoa global funding i $15,000,000,000 global … · and analysis of financial condition ... to...

TRANSCRIPT

PRICOA Global Funding I

$15,000,000,000 Global Medium Term Note Program

This base prospectus supplement, including Annexes 1, 2 and 3 attached hereto (this “First Base Prospectus Supplement”), supplements and must be read in conjunction with the Offering Circular dated May 10, 2017 (the “Base Prospectus”), prepared by PRICOA Global Funding I, a statutory trust organized in series under the laws of the State of Delaware (the “Issuer”), under the Program (as defined in the Base Prospectus).

This document constitutes a base prospectus supplement for purposes of Article 16 of Directive 2003/71/EC (the “Prospectus Directive 2003/71/EC”). This First Base Prospectus Supplement has been approved by the Central Bank of Ireland, as competent authority under the Prospectus Directive 2003/71/EC. The Central Bank of Ireland only approves this First Base Prospectus Supplement as meeting the requirements imposed under Irish and EU law pursuant to the Prospectus Directive 2003/71/EC.

Annex 1 of this First Base Prospectus Supplement includes the unaudited financial statements of The Prudential Insurance Company of America, a New Jersey, United States stock life insurance company (“PICA”), as of and for the three months ended March 31, 2017 and 2016, (including any notes thereto, the “First Quarter Financial Statements”), prepared on the basis of statutory accounting principles, and Management’s Discussion and Analysis of Financial Condition and Results of Operations of PICA (prepared based upon the First Quarter Financial Statements), as of and for the three months ended March 31, 2017 and 2016 (the “First Quarter MD&A”).

Annex 2 of this First Base Prospectus Supplement includes the unaudited financial statements of PICA, as of and for the six months ended June 30, 2017 and 2016, (including any notes thereto, the “Second Quarter Financial Statements”), prepared on the basis of statutory accounting principles, and Management’s Discussion and Analysis of Financial Condition and Results of Operations of PICA (prepared based upon the Second Quarter Financial Statements), as of and for the six months ended June 30, 2017 and 2016 (the “Second Quarter MD&A”).

Annex 3 of this First Base Prospectus Supplement includes the Capitalization of the Issuer as of June 30, 2017, prepared in conformity with generally accepted accounting principles in the United States of America (the “Capitalization of the Issuer”).

Copies of the First Quarter Financial Statements, First Quarter MD&A, the Second Quarter Financial Statements, Second Quarter MD&A and Capitalization of the Issuer will also be made available for inspection at the offices of the Irish Listing Agent of the Issuer at A&L Listing Limited, International Financial Services Centre, North Wall Quay, Dublin 1, Ireland.

Moody’s Investors Service, Inc. (“Moody’s”) is not established in the European Economic Area but the ratings assigned by it are endorsed by Moody’s Investors Service Limited.

S&P Global Ratings, acting through Standard & Poor’s Financial Services, LLC (“S&P”), is not established in the European Economic Area but the ratings assigned by it are endorsed by Standard & Poor’s Credit Market Services Europe Limited.

A.M. Best Company (“A.M. Best”) is not established in the European Economic Area but the ratings assigned by it are endorsed by A.M. Best Europe-Rating Services Ltd.

Fitch Ratings, Inc. (“Fitch”) is not established in the European Economic Area but the ratings assigned by it are endorsed by Fitch Ratings Ltd.

Each of Moody’s, S&P, Fitch and A.M. Best is a rating agency not established in the European Economic Area and not registered under Regulation (EC) No. 1060/2009 (the “CRA Regulation”) by the relevant competent authorities and not included in the list of

credit rating agencies published by the European Securities and Market Authority on its website in accordance with the CRA Regulation.

The rating of certain Series of Notes to be issued under the Program may be specified in the applicable Final Terms (as defined in the Base Prospectus). Whether or not each rating applied for in relation to the relevant Series of Notes will be issued by a credit rating agency established in the European Economic Area and registered under the CRA Regulation will be disclosed in the applicable Final Terms.

A rating is not a recommendation to buy, sell or hold securities and may be subject to revision, suspension or withdrawal at any time by the assigning rating agency. In general, European regulated investors are restricted under the CRA Regulation from using credit ratings for regulatory purposes, unless such ratings are issued by a credit rating agency established in the EU and registered under the CRA Regulation (and such registration has not been withdrawn or suspended), subject to transitional provisions that apply in certain circumstances while the registration application is pending. Such general restriction will also apply in the case of credit ratings issued by non-EU credit rating agencies, unless the relevant credit ratings are endorsed by an EU-registered credit rating agency or the relevant non-EU rating agency is certified in accordance with the CRA Regulation (and such endorsement action or certification, as the case may be, has not been withdrawn or suspended).

Except as disclosed in this First Base Prospectus Supplement, there are no significant new factors, material mistakes or inaccuracies relating to the information included in the Base Prospectus affecting the assessment of the Notes to be offered under the Base Prospectus, as so supplemented, that have arisen since the publication of the Base Prospectus. Each of the Issuer and PICA accepts responsibility that, having taken all reasonable care to ensure that such is the case, the information contained in this First Base Prospectus Supplement, to the best of its knowledge, is in accordance with the facts and contains no omission likely to affect the import of such information.

To the extent that there is any inconsistency between any statement in this First Base Prospectus Supplement and any statement in or incorporated by reference in the Base Prospectus, the statements in this First Base Prospectus Supplement will prevail.

The Issuer is not a subsidiary of PICA or of any affiliate of PICA. The obligations of the Issuer evidenced by the Notes will not be obligations of, and will not be guaranteed by, any person, including, but not limited to, PICA or Prudential Financial, Inc. (“PFI”), or any of their respective subsidiaries or affiliates. PICA and PFI of the United States are not affiliated with Prudential plc, which is headquartered in the United Kingdom. THE NOTES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE UNITED STATES SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), OR ANY APPLICABLE STATE OR FOREIGN SECURITIES LAWS, AND MAY NOT BE OFFERED OR SOLD EXCEPT TO (1) PERSONS REASONABLY BELIEVED TO BE QUALIFIED INSTITUTIONAL BUYERS (AS DEFINED IN RULE 144A UNDER THE SECURITIES ACT) OR (2) PERSONS WHO ARE NOT U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT (“REGULATION S”)) OUTSIDE THE UNITED STATES IN ACCORDANCE WITH REGULATION S. All transfers of the Notes in the United States, whether in the initial distribution or in secondary trading, will be limited to transferees who are Qualified Institutional Buyers. The Notes are not transferable except as described in the Base Prospectus, as supplemented, and in the relevant Terms and Conditions of each Series of the Notes.

Supplement dated October 26, 2017

Annex 1

MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF PICA

AS OF AND FOR THE THREE MONTHS ENDED MARCH 31, 2017

(See Annex A for definitions of certain terms used in this Management’s Discussion and Analysis)

Summary of Principal Differences between SAP and GAAP

The financial information for The Prudential Insurance Company of America (“PICA”) in this

Management’s Discussion and Analysis has been prepared and presented in accordance with SAP. Certain

differences exist between SAP and GAAP which might be material to the financial information herein. The

matters described below summarize certain differences between SAP and GAAP that may be material. The

Company is responsible for preparing the summary below. The Company has not prepared a complete

reconciliation of its consolidated financial statements and related footnote disclosures between SAP and

GAAP and has not quantified such differences. Accordingly, no assurance is provided that the following

summary of differences between SAP and GAAP is complete. In making an investment decision, investors

must rely upon their own examination of the Company, the terms of the offering and the financial information.

Potential investors should consult their own professional advisors for an understanding of the differences

between SAP and GAAP, and how those differences might affect the financial information herein.

The significant differences between SAP and GAAP are noted below:

The SAP financial statements of PICA do not consolidate its subsidiaries. The equity value of its

subsidiaries are recorded as preferred stock, common stock and other invested assets.

Under SAP, policy acquisition costs, such as commissions, and other costs incurred in connection

with acquiring new business, are expensed when incurred; under GAAP, such costs are deferred

and amortized either over the expected lives of the contracts or based on the level and timing of

either gross margins, gross profits or gross premiums, depending on the type of contract.

Under SAP, CRVM is used for the majority of individual insurance reserves; under GAAP, individual

insurance policyholder liabilities for traditional forms of insurance are generally established using

the net level premium method. For interest-sensitive policies, a liability for policyholder account

balances is established under GAAP based on the contract value that has accrued to the benefit of

the policyholder. Policy valuation assumptions used in the estimation of policyholder liabilities

are generally prescribed under SAP; under GAAP, policy valuation assumptions are based upon

best estimates as of the date the policy is issued, with provisions for the risk of adverse deviation.

Under SAP, CARVM is used for the majority of individual deferred annuity reserves; under GAAP,

individual deferred annuity policyholder liabilities are generally equal to the contract value that

has accrued to the benefit of the policyholder, in addition to liabilities for certain guarantees under

variable annuity contracts.

Under SAP, reinsurance reserve credits taken by ceding entities as a result of reinsurance contracts

are netted against the ceding entity’s policy and claim reserves and unpaid claims; under GAAP,

reinsurance recoverables are reported as assets.

Under SAP, IMR is established to capture realized investment gains and losses, net of tax, on the sale

of bonds and interest-related other-than-temporary impairment of bonds resulting from changes

in the general levels of interest rates, and is amortized into income over the remaining years to

2

expected maturity of the assets sold or impaired; under GAAP, no such reserve is required.

Under SAP, AVR based upon a formula prescribed by the NAIC is established as a liability to offset

potential non-interest related investment losses, and changes in the AVR are charged or credited

directly to surplus; under GAAP, no such reserve is required.

Under SAP, investments in bonds and preferred stocks are generally carried at amortized cost; under

GAAP, investments in bonds and preferred stocks, other than those classified as held to maturity,

are carried at fair value.

Under SAP, certain assets designated as non-admitted are excluded from assets by a direct charge to

surplus; under GAAP, such assets are carried on the balance sheet with appropriate valuation

allowances.

Under SAP, surplus notes are recorded as a component of surplus; under GAAP, surplus notes are

recorded as debt.

Under SAP, an extraordinary distribution approved by PICA’s regulator may be recorded as a return

of capital; under GAAP, the distribution is recorded as a dividend when PICA has undistributed

retained earnings.

Under SAP, goodwill is subject to admissibility limits and is amortized over a period not to exceed

ten years; under GAAP, goodwill is subject to impairment testing and not amortized.

Under SAP, income tax expense is based upon taxes currently payable. Changes in deferred taxes are

generally reported in surplus and subject to admissibility limits; under GAAP, changes in deferred

taxes are generally recorded in income tax expense.

Under SAP, deposits to universal life contracts and immediate annuity contracts without life

contingencies are credited to revenue; under GAAP, such deposits are reported as increases to the

policyholder account balances.

Under SAP, certain contracts, in particular deferred annuities with mortality risk, are considered “life

contracts” and, accordingly, premiums associated with these contracts are reported as revenues.

Under GAAP, the Company’s deferred annuities are classified as either “insurance contracts” or

“investment contracts” and, accordingly, those annuities classified as investment contracts are not

reported as revenues. Amounts received for investment contracts are not reported as policy

liabilities and insurance reserves.

Under SAP, interest-related other-than-temporary impairments for bonds are determined based

primarily upon PICA’s intent to sell or inability to assert its intent and ability to hold the security

until recovery; under GAAP, other-than-temporary impairments for debt securities are based

primarily upon whether PICA intends to sell the security or more likely than not will be required

to sell the security before recovery of its amortized cost basis.

Under SAP, there is no concept of value of business acquired ("VOBA"); under GAAP, VOBA is

recorded as an asset.

Under SAP, an embedded derivative instrument shall not be separated from the host contract and

accounted for separately as a derivative instrument; under GAAP, the accounting and bifurcation

for embedded derivatives follows Accounting Standards Codification ("ASC") 815 - "Derivatives

and Hedging", with the change in fair value during each reporting period recorded within

“Realized investment gains (losses)."

3

Overview

PICA is one of the largest insurance companies in the United States. The principal products and services of

PICA include individual life insurance and annuities, group insurance and pension and retirement products and

related services and administration. The results in the analysis below include the results of the Closed Block

division, which comprises the assets and related liabilities of the Closed Block. The principal executive offices

of PICA are located in Newark, New Jersey.

As of March 31, 2017 and December 31, 2016, PICA's admitted assets were $260 billion (including $136

billion held in separate accounts). Excluding separate accounts, assets were primarily comprised of a mix of

bonds, mortgage loans, contract loans, cash and short-term investments, other invested assets, and equity

investments designed to match the cash flow requirements of insurance liabilities.

Results of Operations

Net Income

2017 to 2016 Three Month Comparison. Net income for the three months ended March 31, 2017 was $228

million compared to $24 million for the three months ended March 31, 2016. The increase of $204 million

between periods includes a $416 million increase in operating income before income taxes, from $76 million for

the three months ended March 31, 2016 to $492 million for the three months ended March 31, 2017, which was

primarily driven by the following:

• A $271 million increase in the individual life and annuity business primarily driven by lower reserves in

the annuities business due to more favorable market conditions in the current period compared to the same

period of 2016. Also, contributing to the increase were higher asset management fees and surrender

charges assumed from an affiliate, PLNJ, partially offset by higher assumed commissions. The

reinsurance agreement with PLNJ became effective in the second quarter of 2016;

• A $146 million increase in the retirement business primarily driven by higher spread income mainly due

to growth in the pension risk transfer business. Also contributing to the increase was higher income from

alternative investments;

• A $23 million increase in the international insurance business primarily driven by the renewal business

assumed from PGFL partially offset by an increase in commissions as a result of growth of U.S. dollar

denominated business assumed from PLICJ;

• A $14 million increase in the group insurance business primarily driven by higher spread income mainly

due to an increase in invested assets as a result of business growth; and

Partially offset by:

• A $38 million decrease in the corporate and other business primarily driven by higher compensation

related expenses.

The above increase in net income was partially offset by a $136 million increase in net realized capital losses,

from $27 million for the three months ended March 31, 2016 to $163 million for the three months ended March

31, 2017. The components of net realized capital losses are discussed below under “Capital (Losses)/Gains.”

Net income also included a $76 million increase in the income tax provision from $25 million for the three

months ended March 31, 2016 to $101 million for the three months ended March 31, 2017, which is further

discussed below under “Income Tax Provision.”

4

Change in Statutory Capital and Surplus

For the three months ended March 31, 2017. Statutory capital (surplus plus AVR) increased $397 million,

from $13,445 million at December 31, 2016 to $13,842 million at March 31, 2017. The increase in capital for the

period ended March 31, 2017 was primarily driven by:

• Net income of $228 million, as discussed above under “Net Income”; and

• A $159 million change in unrealized capital gains (excluding deferred tax) primarily due to gains from

affiliated common stocks. The change in net unrealized capital gains are further discussed below under

“Capital (Losses)/Gains.”

Revenues

2017 to 2016 Three Month Comparison. Total revenues increased $129 million from $6,327 million for the

three months ended March 31, 2016 to $6,456 million for the three months ended March 31, 2017. The increase

in total revenues was primarily driven by a $179 million increase in premiums between periods from $4,565

million for the three months ended March 31, 2016 to $4,744 million for the three months ended March 31, 2017.

The increase in premiums was primarily driven by:

• A $187 million increase in the international insurance business primarily driven by the reinsurance of

PGFL and PLICJ’s U.S. dollar denominated business as a result of business growth;

• A $132 million increase in the individual life and annuity business primarily driven by assumed premiums

from PLNJ in the annuities business;

Partially offset by:

• A $129 million decrease in the retirement business primarily driven by lower sales of structured settlement

contracts; and

• A $16 million decrease in the group insurance business primarily driven by lower premiums on existing

experience rated contracts in the group life business. Partially offsetting this activity were higher sales

in the life and long-term disability businesses.

Additionally, contributing to the increase in total revenue was an increase in net investment income, which

includes IMR amortization, of $86 million from $1,237 million for the three months ended March 31, 2016 to

$1,323 million for the three months ended March 31, 2017. This increase was primarily driven by higher income

from alternative investments in the retirement business. Additionally, net investment income increased in the

international insurance business primarily due to an increase in invested assets as a result of continued business

growth.

Partially offsetting these increases in total revenue was a decrease in other income of $136 million, from $525

million for the three months ended March 31, 2016 to $389 million for the three months ended March 31, 2017.

The decrease in other income was primarily driven by lower gains from separate accounts in the retirement

business.

5

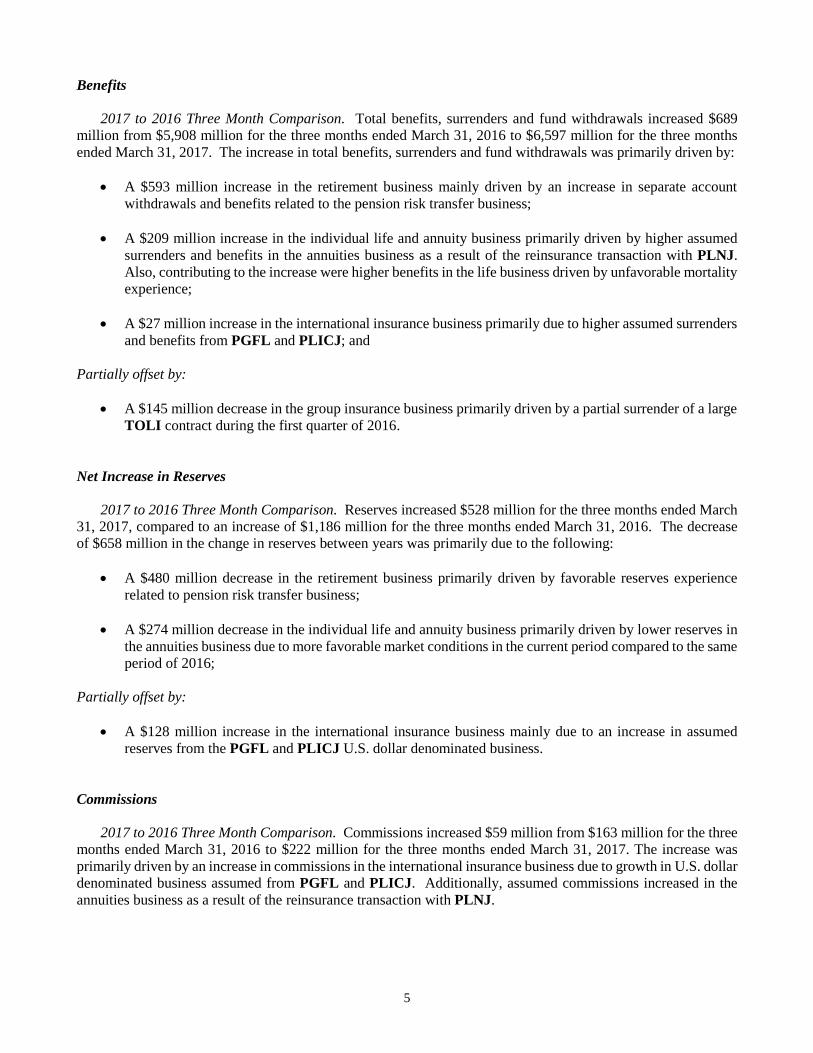

Benefits

2017 to 2016 Three Month Comparison. Total benefits, surrenders and fund withdrawals increased $689

million from $5,908 million for the three months ended March 31, 2016 to $6,597 million for the three months

ended March 31, 2017. The increase in total benefits, surrenders and fund withdrawals was primarily driven by:

• A $593 million increase in the retirement business mainly driven by an increase in separate account

withdrawals and benefits related to the pension risk transfer business;

• A $209 million increase in the individual life and annuity business primarily driven by higher assumed

surrenders and benefits in the annuities business as a result of the reinsurance transaction with PLNJ.

Also, contributing to the increase were higher benefits in the life business driven by unfavorable mortality

experience;

• A $27 million increase in the international insurance business primarily due to higher assumed surrenders

and benefits from PGFL and PLICJ; and

Partially offset by:

• A $145 million decrease in the group insurance business primarily driven by a partial surrender of a large

TOLI contract during the first quarter of 2016.

Net Increase in Reserves

2017 to 2016 Three Month Comparison. Reserves increased $528 million for the three months ended March

31, 2017, compared to an increase of $1,186 million for the three months ended March 31, 2016. The decrease

of $658 million in the change in reserves between years was primarily due to the following:

• A $480 million decrease in the retirement business primarily driven by favorable reserves experience

related to pension risk transfer business;

• A $274 million decrease in the individual life and annuity business primarily driven by lower reserves in

the annuities business due to more favorable market conditions in the current period compared to the same

period of 2016;

Partially offset by:

• A $128 million increase in the international insurance business mainly due to an increase in assumed

reserves from the PGFL and PLICJ U.S. dollar denominated business.

Commissions

2017 to 2016 Three Month Comparison. Commissions increased $59 million from $163 million for the three

months ended March 31, 2016 to $222 million for the three months ended March 31, 2017. The increase was

primarily driven by an increase in commissions in the international insurance business due to growth in U.S. dollar

denominated business assumed from PGFL and PLICJ. Additionally, assumed commissions increased in the

annuities business as a result of the reinsurance transaction with PLNJ.

6

Other Expenses

2017 to 2016 Three Month Comparison. Other expenses increased $39 million from $364 million for the

three months ended March 31, 2016 to $403 million for the three months ended March 31, 2017. The increase

between periods was primarily driven by higher compensation related expenses in the corporate and other

business. Partially offsetting these increases were lower expenses in the annuities business driven by adjustments

on reinsurance assumed related to the reinsurance transaction with PLNJ.

Net Transfer From Separate Accounts

2017 to 2016 Three Month Comparison. The net transfer from the separate accounts was ($1,824) million for

the three months ended March 31, 2017, compared to a net transfer from the separate accounts of ($1,423) million

for the three months ended March 31, 2016. The $401 million change was primarily driven by an increase in

separate account withdrawals as well as the impact of new pension risk transfer transactions in the retirement

business completed since the first quarter of 2016. Partially offsetting this activity was as a partial surrender in

the group insurance business of a large TOLI contract during the first quarter of 2016.

Dividends to Policyholders

2017 to 2016 Three Month Comparison. Dividends to policyholders decreased $15 million from $53 million

for the three months ended March 31, 2016 to $38 million for the three months ended March 31, 2017 primarily

driven by adjustments related to participating contracts in the group insurance business as well as the continued

run-off of the Closed Block.

Income Tax Provision

2017 to 2016 Three Month Comparison. The income tax expense increased $76 million from $25 million for

the three months ended March 31, 2016 to $101 million for the three months ended March 31, 2017 primarily due

to the increase in pretax book income. The income tax provision is calculated in accordance with SSAP No. 101,

Income Taxes. For interim periods, income taxes are computed using an estimated annual effective tax rate. The

rate is computed as the ratio of projected income tax provision for the entire year over projected statutory net gain

from operations for the year.

7

Capital (Losses)/Gains

2017 to 2016 Three Month Comparison. Net realized capital losses, after taxes and contribution to the IMR,

increased $136 million, from $27 million for the three months ended March 31, 2016 to $163 million for the three

months ended March 31, 2017. The following table sets forth the components of net realized capital losses:

Three Months Three Months

Ended

March 31,

Ended

March 31,

2017 2016 Change

Bonds…………………….……………………………… $ (6) $ (111) $ 105

Equity securities…………………………………………. - - -

Derivative instruments…………………………………… (39) 4 (43)

Other invested assets…………………………………….. (10) 1 (11)

Other………………………………….………………….. 3 43 (40)

Gross realized capital losses……….…………………. (52) (63) 11

Less capital gains tax…...………..……..………………… 101 (16) (117)

Less IMR transfers, net of tax ………....………………… 10 (20) (30)

Net realized capital losses……….…...……………….. $ (163) $ (27) $ (136)

Net realized capital losses for the three months ended March 31, 2017 were primarily driven by capital gains

tax, losses on derivatives and other-than-temporary impairments on bonds. For interim periods, the capital gains

tax is derived as the difference between the total tax and the income tax provision. The total tax is a function of

pre-tax book income and the use of the effective tax rate method. Derivative losses of $39 million were primarily

driven by equity swap settlements on short positions due to favorable market conditions in the current period. The

losses on bonds of $6 million include $21 million of other-than-temporary impairments.

Net realized capital losses for the three months ended March 31, 2016 were primarily driven by realized capital

losses on bonds, partially offset by gains on other assets related to short-term investments and real estate. The

losses on bonds of $111 million include $52 million of other-than-temporary bond impairments. The IMR

transfers of $20 million were primarily driven by losses on bonds, partially offset by gains on short-term

investments and derivatives.

Change in net unrealized capital gains was $160 million for the three months ended March 31, 2017, and was

mainly due to affiliated common stock gains primarily driven by admittance of a previously non-admitted loan as

well as earnings from PICA’s insurance subsidiary, PRIAC.

Change in net unrealized capital gains was $646 million for the three months ended March 31, 2016, and was

mainly due to gains from derivatives as a result of a decrease in interest rates during the period. In addition,

affiliated common stock gains were driven by earnings from PICA’s insurance subsidiary, PLI. These gains were

partially offset by deferred taxes.

8

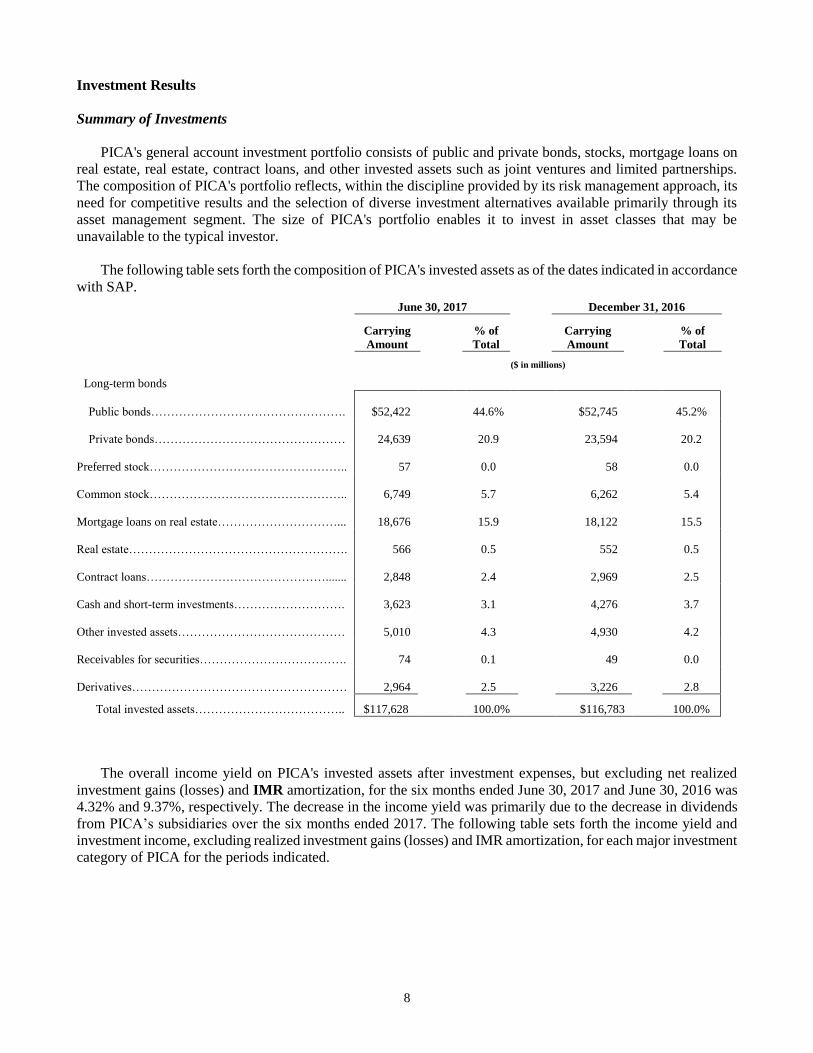

Investment Results

Summary of Investments

PICA's general account investment portfolio consists of public and private bonds, stocks, mortgage loans on

real estate, real estate, contract loans, and other invested assets such as joint ventures and limited partnerships.

The composition of PICA's portfolio reflects, within the discipline provided by its risk management approach, its

need for competitive results and the selection of diverse investment alternatives available primarily through its

asset management segment. The size of PICA's portfolio enables it to invest in asset classes that may be

unavailable to the typical investor.

The following table sets forth the composition of PICA's invested assets as of the dates indicated in accordance

with SAP.

Long-term bonds

Public bonds………………………………………….

$52,816 45.2%

$52,745 45.2%

Private bonds…………………………………………

24,201 20.7%

23,594 20.2%

Preferred stock…………………………………………..

58 0.0%

58 0.0%

Common stock…………………………………………..

6,642 5.7%

6,262 5.4%

Mortgage loans on real estate…………………………

18,270 15.6%

18,122 15.5%

Real estate……………………………………………….

548 0.5%

552 0.5%

Contract loans……………………………………….......

3,007 2.6%

2,969 2.5%

Cash and short-term investments……………………….

3,398 2.9%

4,276 3.7%

Other invested assets……………………………………

4,953 4.2%

4,930 4.2%

Receivables for securities……………………………….

34 0.0%

49 0.0%

Derivatives………………………………………………

3,029 2.6%

3,226 2.8%

Total invested assets……………………………… $116,956 100.0%

$116,783 100.0%

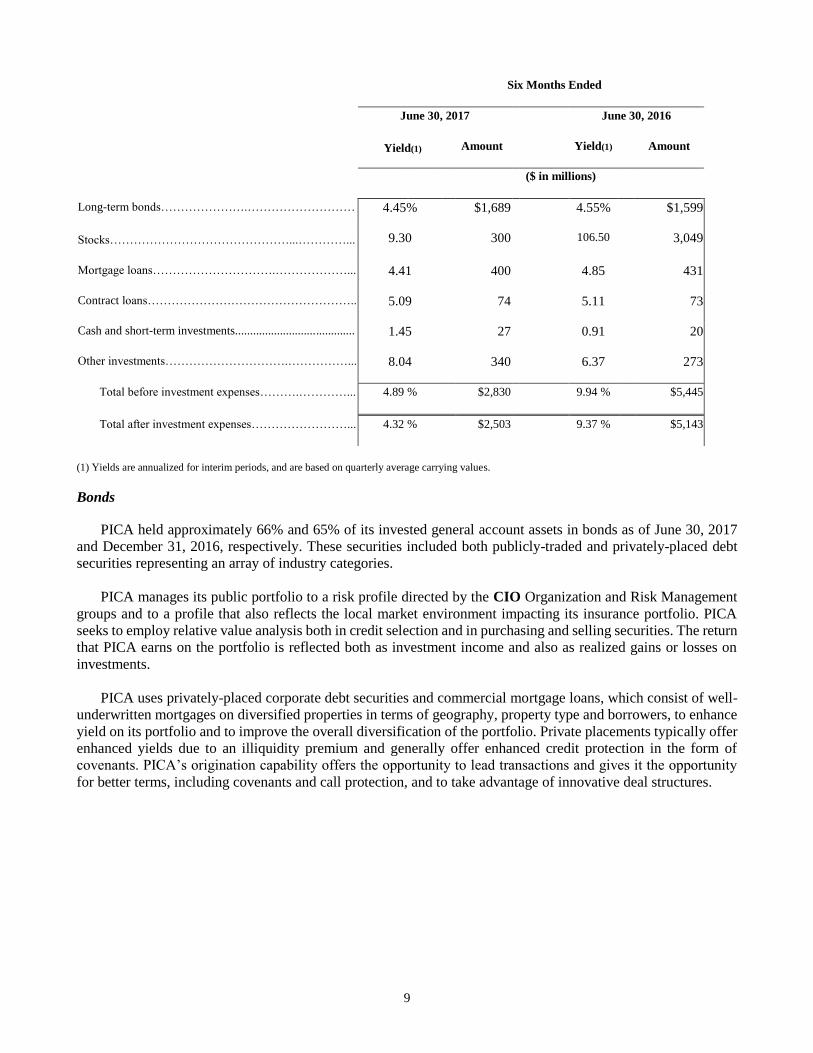

The overall income yield on PICA's invested assets after investment expenses, but excluding net realized

investment gains (losses) and IMR amortization, for the three months ended March 31, 2017 and March 31, 2016

was 4.51% and 4.39%, respectively. The increase in the income yield was primarily driven by higher yield from

non-coupon investments for the three months ended 2017. The following table sets forth the income yield and

investment income, excluding realized investment gains (losses) and IMR amortization, for each major investment

category of PICA for the periods indicated.

March 31, 2017 December 31, 2016

Carrying

Amount

% of

Total

Carrying

Amount

% of

Total

($ in millions)

9

Bonds

PICA held approximately 66% and 65% of its invested general account assets in bonds as of March 31, 2017

and December 31, 2016, respectively. These securities included both publicly-traded and privately-placed debt

securities representing an array of industry categories.

PICA manages its public portfolio to a risk profile directed by the CIO Organization and Risk Management

groups and to a profile that also reflects the local market environment impacting its insurance portfolio. PICA

seeks to employ relative value analysis both in credit selection and in purchasing and selling securities. The return

that PICA earns on the portfolio is reflected both as investment income and also as realized gains or losses on

investments.

PICA uses privately-placed corporate debt securities and commercial mortgage loans, which consist of well-

underwritten mortgages on diversified properties in terms of geography, property type and borrowers, to enhance

yield on its portfolio and to improve the overall diversification of the portfolio. Private placements typically offer

enhanced yields due to an illiquidity premium and generally offer enhanced credit protection in the form of

covenants. PICA’s origination capability offers the opportunity to lead transactions and gives it the opportunity

for better terms, including covenants and call protection, and to take advantage of innovative deal structures.

Three Months Ended

March 31, 2017 March 31, 2016

Yield Amount Yield Amount

($ in millions)

Long-term bonds………………….……………………… 4.45 % $849 4.51%

$788

Stocks………………………………………...…………... 10.98 176 8.75 169

Mortgage loans………………………….………………... 4.33 196 4.71 210

Contract loans…………………………………………….. 5.02 37 4.99 36

Cash and short-term investments........................................ 1.36 13 1.08 11

Other investments………………………….……………... 8.68 186 6.64 134

Total before investment expenses……….…………... 5.02 % $1,457 4.88 %

$1,348

Total after investment expenses……………………... 4.51 %

$1,311 4.39 %

$1,215

10

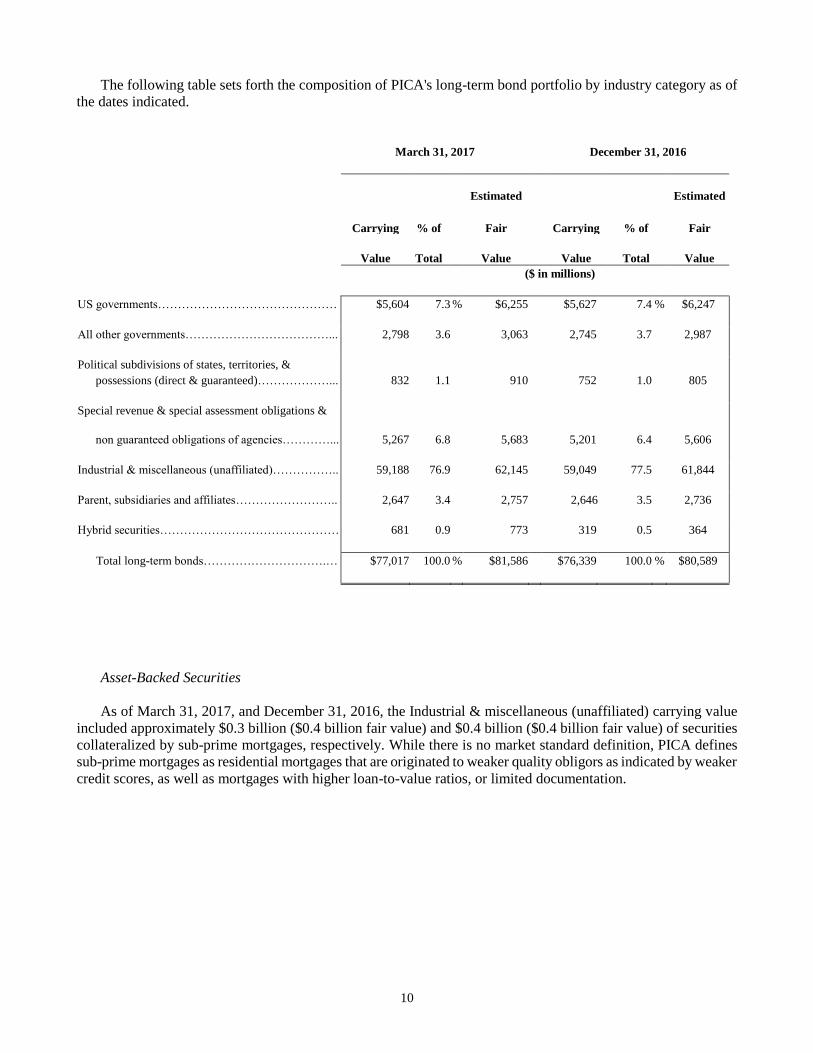

The following table sets forth the composition of PICA's long-term bond portfolio by industry category as of

the dates indicated.

March 31, 2017 December 31, 2016

Estimated Estimated

Carrying % of Fair Carrying % of Fair

Value Total Value Value Total Value

($ in millions)

US governments……………………………………… $5,604 7.3 % $6,255 $5,627 7.4 % $6,247

All other governments………………………………... 2,798 3.6 3,063 2,745 3.7 2,987

Political subdivisions of states, territories, &

possessions (direct & guaranteed)………………... 832 1.1 910 752 1.0 805

Special revenue & special assessment obligations &

non guaranteed obligations of agencies…………... 5,267 6.8 5,683 5,201 6.4 5,606

Industrial & miscellaneous (unaffiliated)…………….. 59,188 76.9 62,145 59,049 77.5 61,844

Parent, subsidiaries and affiliates…………………….. 2,647 3.4 2,757 2,646 3.5 2,736

Hybrid securities……………………………………… 681 0.9 773 319 0.5 364

Total long-term bonds………………………….… $77,017 100.0 % $81,586 $76,339 100.0 % $80,589

Asset-Backed Securities

As of March 31, 2017, and December 31, 2016, the Industrial & miscellaneous (unaffiliated) carrying value

included approximately $0.3 billion ($0.4 billion fair value) and $0.4 billion ($0.4 billion fair value) of securities

collateralized by sub-prime mortgages, respectively. While there is no market standard definition, PICA defines

sub-prime mortgages as residential mortgages that are originated to weaker quality obligors as indicated by weaker

credit scores, as well as mortgages with higher loan-to-value ratios, or limited documentation.

11

The following table sets forth the carrying value and fair value of PICA’s asset-backed securities by credit

quality as of the date indicated.

(1) Bonds are carried at amortized cost, excluding NAIC 6 rated bonds, which are carried at the lower of amortized cost or fair market value.

The table above provides ratings assigned by nationally recognized rating agencies as of March 31, 2017,

including S&P, Moody’s and Fitch. In making its investment decisions, rather than relying solely on the rating

agencies’ evaluations, PICA assigns internal ratings to its asset-backed securities based upon its dedicated asset-

backed securities unit’s independent evaluation of the underlying collateral and securitization structure, including

any guarantees from monoline bond insurers.

The carrying value of asset-backed securities collateralized by sub-prime mortgages decreased from $0.4

billion ($0.4 billion fair value) as of December 31, 2016, to $0.3 billion ($0.4 billion fair value) as of March 31,

2017, primarily reflecting sales and paydowns.

Commercial Mortgage-Backed Securities

As of March 31, 2017, and December 31, 2016, Industrial & miscellaneous (unaffiliated) carrying value

included approximately $4.6 billion ($4.7 billion fair value) and $4.7 billion ($4.8 billion fair value) of commercial

mortgage-backed securities, respectively.

March 31, 2017

Lowest Rating Agency Rating

AAA AA A BBB

BB and

below

Carrying

Value (1)

Total

Fair

Value

(in millions)

Collateralized by sub-prime

mortgages………………………………….. $ 0 $ 0 $ 16 $ 29 $ 293 $ 338 $ 433

Collateralized by auto loans ......... ………… 661

0 0 0 0 661 662

Collateralized by credit cards ...................... 114

0 0 0 0 114 116

Other asset-backed securities ...................... 4,890

408

25

16 42

5,381

5,417

Total asset-backed securities ............... $ 5,665

$ 408

$ 41

$ 45 $ 335 $ 6,494

$ 6,628

12

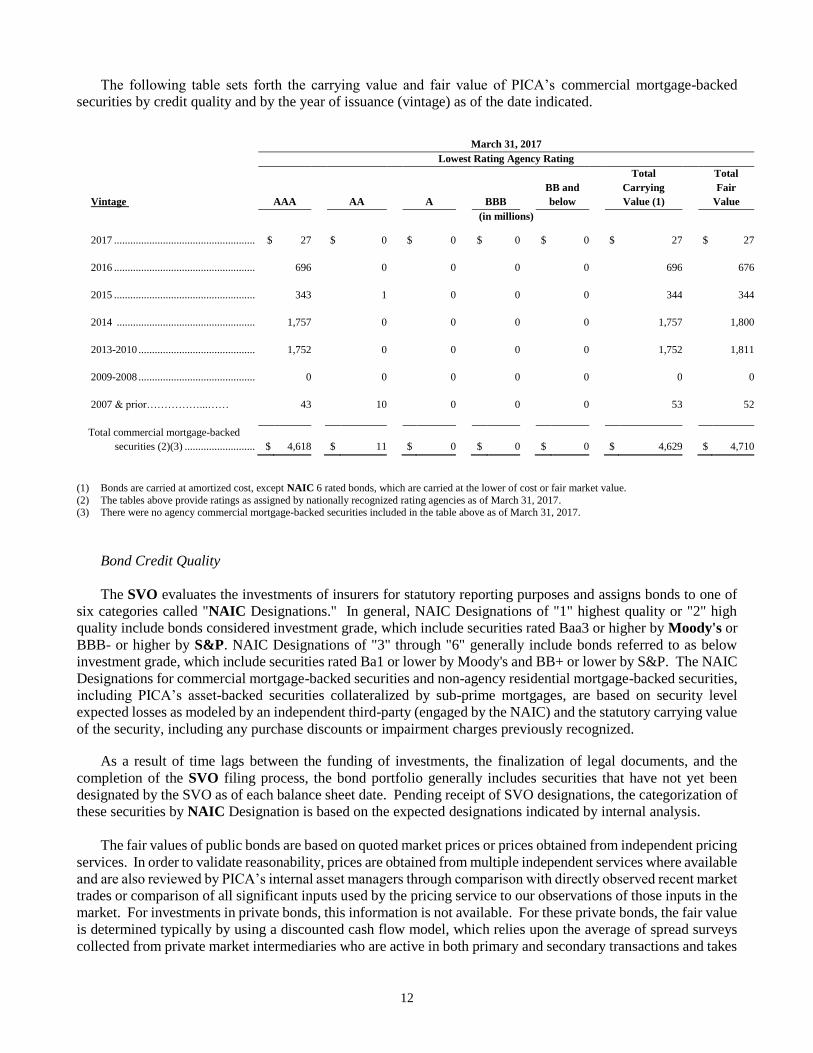

The following table sets forth the carrying value and fair value of PICA’s commercial mortgage-backed

securities by credit quality and by the year of issuance (vintage) as of the date indicated.

(1) Bonds are carried at amortized cost, except NAIC 6 rated bonds, which are carried at the lower of cost or fair market value.

(2) The tables above provide ratings as assigned by nationally recognized rating agencies as of March 31, 2017. (3) There were no agency commercial mortgage-backed securities included in the table above as of March 31, 2017.

Bond Credit Quality

The SVO evaluates the investments of insurers for statutory reporting purposes and assigns bonds to one of

six categories called "NAIC Designations." In general, NAIC Designations of "1" highest quality or "2" high

quality include bonds considered investment grade, which include securities rated Baa3 or higher by Moody's or

BBB- or higher by S&P. NAIC Designations of "3" through "6" generally include bonds referred to as below

investment grade, which include securities rated Ba1 or lower by Moody's and BB+ or lower by S&P. The NAIC

Designations for commercial mortgage-backed securities and non-agency residential mortgage-backed securities,

including PICA’s asset-backed securities collateralized by sub-prime mortgages, are based on security level

expected losses as modeled by an independent third-party (engaged by the NAIC) and the statutory carrying value

of the security, including any purchase discounts or impairment charges previously recognized.

As a result of time lags between the funding of investments, the finalization of legal documents, and the

completion of the SVO filing process, the bond portfolio generally includes securities that have not yet been

designated by the SVO as of each balance sheet date. Pending receipt of SVO designations, the categorization of

these securities by NAIC Designation is based on the expected designations indicated by internal analysis.

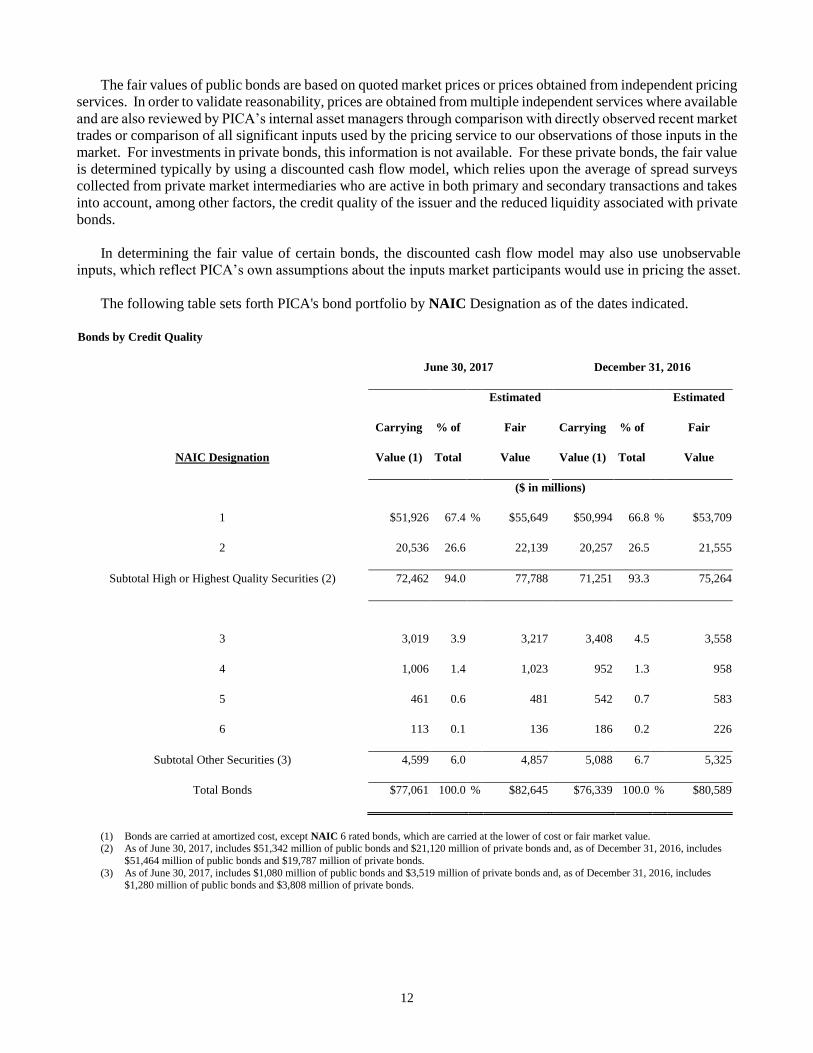

The fair values of public bonds are based on quoted market prices or prices obtained from independent pricing

services. In order to validate reasonability, prices are obtained from multiple independent services where available

and are also reviewed by PICA’s internal asset managers through comparison with directly observed recent market

trades or comparison of all significant inputs used by the pricing service to our observations of those inputs in the

market. For investments in private bonds, this information is not available. For these private bonds, the fair value

is determined typically by using a discounted cash flow model, which relies upon the average of spread surveys

collected from private market intermediaries who are active in both primary and secondary transactions and takes

March 31, 2017

Lowest Rating Agency Rating

Vintage AAA AA A BBB

BB and

below

Total

Carrying

Value (1)

Total

Fair

Value

(in millions)

2017 .................................................... $ 27

$ 0

$ 0

$ 0

$ 0

$ 27

$ 27

2016 ....................................................

696

0

0

0

0

696

676

2015 ....................................................

343 1 0 0

0 344 344

2014 ...................................................

1,757 0 0 0

0 1,757 1,800

2013-2010 ...........................................

1,752 0 0 0

0 1,752 1,811

2009-2008 ...........................................

0 0 0 0

0 0 0

2007 & prior……………...……

43 10 0 0

0 53 52

Total commercial mortgage-backed

securities (2)(3) .......................... $ 4,618 $ 11 $ 0 $ 0 $ 0 $ 4,629

$ 4,710

13

into account, among other factors, the credit quality of the issuer and the reduced liquidity associated with private

bonds.

In determining the fair value of certain bonds, the discounted cash flow model may also use unobservable

inputs, which reflect PICA’s own assumptions about the inputs market participants would use in pricing the asset.

The following table sets forth PICA's bond portfolio by NAIC Designation as of the dates indicated.

Bonds by Credit Quality

March 31, 2017 December 31, 2016

Estimated Estimated

Carrying % of Fair Carrying % of Fair

NAIC Designation Value (1) Total Value Value (1) Total Value

($ in millions)

1 $51,584 67.0 % $54,473 $50,994 66.8 % $53,709

2 20,436 26.5 21,860 20,257 26.5 21,555

Subtotal High or Highest Quality Securities (2) 72,020 93.5 76,333 71,251 93.3 75,264

3 3,189 4.1 3,367 3,408 4.5 3,558

4 1,026 1.4 1,035 952 1.3 958

5 564 0.7 593 542 0.7 583

6 218 0.3 258 186 0.2 226

Subtotal Other Securities (3) 4,997 6.5 5,253 5,088 6.7 5,325

Total Bonds $77,017 100.0 % $81,586 $76,339 100.0 % $80,589

(1) Bonds are carried at amortized cost, except NAIC 6 rated bonds, which are carried at the lower of cost or fair market value.

(2) As of March 31, 2017, includes $51,614 million of public bonds and $20,406 million of private bonds and, as of December 31, 2016, includes $51,464 million of public bonds and $19,145 million of private bonds.

(3) As of March 31, 2017, includes $1,202 million of public bonds and $3,795 million of private bonds and, as of December 31, 2016, includes

$1,280 million of public bonds and $3,808 million of private bonds.

Other-Than-Temporary Impairments of Bonds

PICA maintains separate monitoring processes for public and private bonds and creates watch lists to highlight

bonds that require special scrutiny and management. The public bond asset managers review on a quarterly basis

and more frequently when necessary to identify potential credit deterioration whether due to ratings downgrades,

unexpected price variances, and/or company or industry specific concerns.

For private placements, PICA’s credit and portfolio management processes help ensure prudent controls over

valuation and management. PICA has separate pricing and authorization processes to establish "checks and

balances" for new investments. PICA applies consistent standards of credit analysis and due diligence for all

transactions, whether they originate through its own in-house origination staff or through agents. PICA's regional

14

offices closely monitor the portfolios in their regions. PICA sets all valuation standards centrally, and assesses the

fair value of all investments quarterly. PICA’s private bond asset managers formally review all private bond

holdings on a quarterly basis or more frequently when necessary to identify potential credit deterioration whether

due to ratings downgrades, unexpected price variances, and/or company or industry specific concerns.

All bonds with unrealized losses are subject to review to identify other-than-temporary impairments in value.

In evaluating whether a decline in value is other-than-temporary, PICA considers several factors including, but

not limited to, the following:

• the reasons for the decline in value (credit event, currency or interest rate related, including general credit

spread widening);

• PICA's ability and intent to hold its investment for a period of time to allow for recovery of value;

• PICA's intent to sell its investment before recovery of the cost of the investment;

• the financial condition of and near-term prospects of the issuer; and

• the extent and duration of the decline.

In determining whether a decline in value is other-than-temporary, PICA places a greater emphasis on analysis

of the underlying credit versus the extent and duration of a decline in value. PICA’s credit analysis of an

investment includes determining whether the issuer is current on its contractual payments, evaluating whether it

is probable that PICA will be able to collect all amounts due according to the contractual terms of the security,

and analyzing PICA’s overall ability to recover the carrying value of the investment. PICA continues to utilize

valuation declines as a potential indicator of credit deterioration, and applies additional levels of scrutiny in its

analysis as the severity and duration of the decline increases.

Under SSAP No. 43R, an other-than-temporary impairment occurs when the entity does not expect (on a

discounted basis) to recover the entire cost basis of a loan-backed or structured security. The amount of the other-

than-temporary impairment recognized as a realized loss equals the difference between the investment's cost basis

and the present value of cash flows expected to be collected, discounted at the effective interest rate implicit in

the debt security prior to impairment. The present value of cash flows expected to be collected becomes the new

cost basis of the investment. Additionally, if an entity wrote the security down to fair value due to the intent to

sell or because it does not have the ability and intent to hold a security in an unrealized loss position for a period

of time sufficient to recover the cost of the security, the non-interest related portion of the other-than-temporary

impairment losses is recorded through the AVR while the interest related other-than-temporary impairment losses

is recorded through the IMR.

Preferred Stock

PICA held less than 1% of its invested general account assets in preferred stock as of both March 31, 2017

and December 31, 2016.

Common Stocks

PICA held approximately 6% and 5% of its invested general account assets in common stock as of March 31,

2017 and December 31, 2016, respectively. Substantially all of PICA's unaffiliated common stocks are publicly-

traded on national securities exchanges.

Impairments of Common Stocks

Common stocks with unrealized losses are subject to review to identify other-than-temporary impairments in

value. In evaluating whether a decline in value is other-than-temporary, PICA consistently considers several

factors including, but not limited to, the following:

15

• the extent and the duration of the decline; including, but not limited to, the following general guidelines:

o declines in value greater than 20%, maintained for six months or greater;

o declines in value maintained for one year or greater; and

o declines in value greater than 50%.

• the reasons for the decline in value (credit event, currency or market fluctuation);

• PICA’s ability and intent to hold the investment for a period of time to allow for a recovery of value,

including common stock managed by independent third parties where we do not have management

discretion; and

• the financial condition of and near-term prospects of the issuer.

PICA generally recognizes other-than-temporary impairments for securities with declines in value greater

than 50% maintained for six months or greater or with any decline in value maintained for one year or greater. In

addition, in making its determinations PICA continues to analyze the financial condition and near-term prospects

of the issuer, including an assessment of the issuer’s capital position, and considers its ability and intent to hold

the investment for a period of time to allow for a recovery of value.

When it has been determined that there is an other-than-temporary impairment, PICA records a write down

in its Statement of Operations and Changes in Capital and Surplus within "Net Realized Capital Gains (Losses)"

to the estimated fair value, which reduces the cost basis. The new cost basis of an impaired security is not adjusted

for subsequent increases in estimated fair value. Estimated fair values for publicly traded common stock are based

on quoted market prices or prices obtained from independent pricing services. Estimated fair values for privately

traded common stock are determined using valuation and discounted cash flow models that require a substantial

level of judgment.

Mortgage Loans on Real Estate

Investment Mix

PICA held approximately 16% of its invested general account assets in mortgage loans on real estate as of

both March 31, 2017 and December 31, 2016.

The following table sets forth the composition of PICA’s general account investments in mortgage loans on

real estate, as of the dates indicated.

March 31,

December 31,

2017 2016

(in millions)

Commercial mortgage loans……………………... $ 16,770 $ 16,628

Agricultural property loans………………………. 1,498

1,492

Residential property loans………………………..

2

2

Total (1)………………………………………….. $ 18,270 $ 18,122

(1) The portfolio consisted of 1,112 commercial mortgage loans and 459 residential and agricultural loans as of March 31, 2017 and consisted of

1,105 commercial mortgage loans and 461 residential and agricultural loans as of December 31, 2016.

PICA originates mortgage loans on real estate using a dedicated investment staff through various regional

offices in the U.S. and International offices primarily in London. All loans are underwritten consistently to PICA's

standards using a proprietary quality rating system that has been developed from its experience in real estate and

mortgage lending.

16

PICA’s loan portfolio strategy emphasizes diversification by property type and geographic location. The

following table sets forth the breakdown of the mortgage loan portfolio by geographic region as of the dates

indicated.

March 31, 2017 December 31, 2016

Carrying % of Carrying % of

U.S. Regions: (1)

Value Total Value Total

($ in millions)

Pacific $5,947 32.5 % $5,959 32.9 %

South Atlantic 3,445 18.9 3,431 18.9

Middle Atlantic 2,645 14.5 2,647 14.6

West South Central 1,910 10.5 1,914 10.6

East North Central 1,022 5.6 1,032 5.7

Mountain 690 3.8 643 3.5

New England 789 4.3 789 4.4

West North Central 270 1.5 267 1.5

East South Central 238 1.3 235 1.3

Subtotal – U.S. Regions $16,956 92.9 % $16,917 93.4 %

Other 1,314 7.1 1,205 6.6

Total mortgage loans $18,270 100.0 % $18,122 100.0 %

(1) Regions as defined by the United States Census bureau.

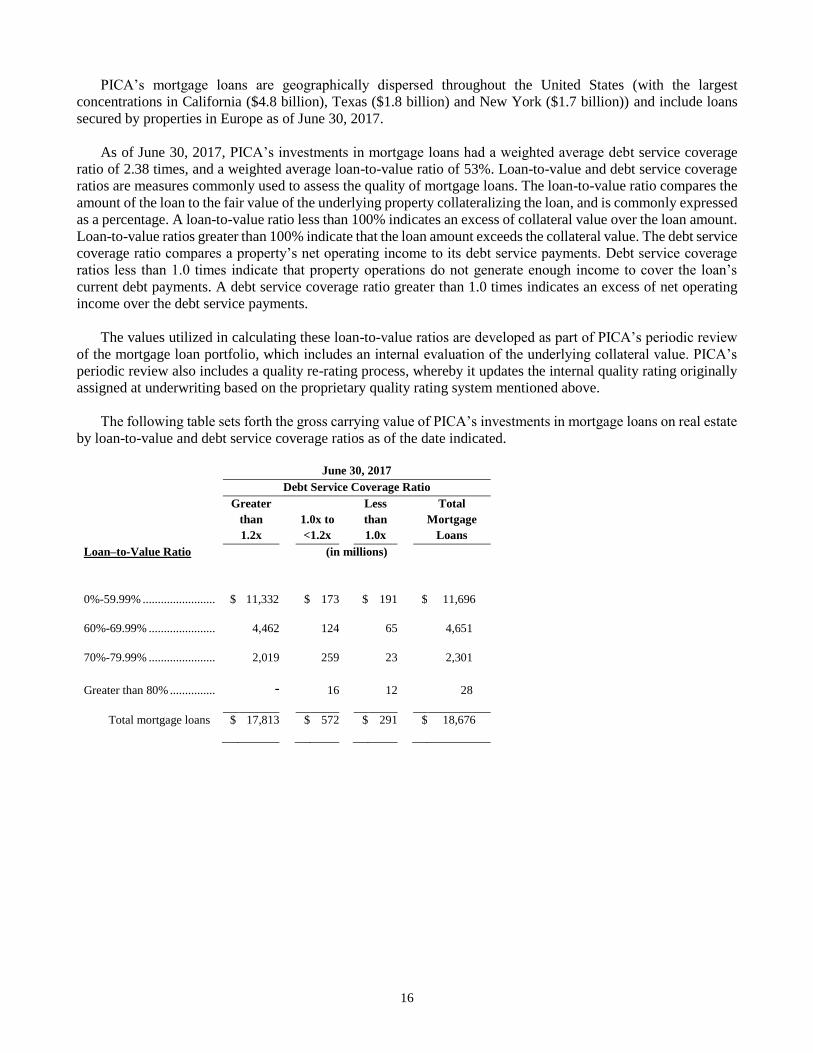

PICA’s mortgage loans are geographically dispersed throughout the United States (with the largest

concentrations in California ($4.9 billion), New York ($1.7 billion), and Texas ($1.7 billion)) and include loans

secured by properties in Europe as of March 31, 2017.

As of March 31, 2017, PICA’s investments in mortgage loans had a weighted average debt service coverage

ratio of 2.37 times, and a weighted average loan-to-value ratio of 52%. Loan-to-value and debt service coverage

ratios are measures commonly used to assess the quality of mortgage loans. The loan-to-value ratio compares the

amount of the loan to the fair value of the underlying property collateralizing the loan, and is commonly expressed

as a percentage. A loan-to-value ratio less than 100% indicates an excess of collateral value over the loan amount.

Loan-to-value ratios greater than 100% indicate that the loan amount exceeds the collateral value. The debt service

coverage ratio compares a property’s net operating income to its debt service payments. Debt service coverage

ratios less than 1.0 times indicate that property operations do not generate enough income to cover the loan’s

current debt payments. A debt service coverage ratio greater than 1.0 times indicates an excess of net operating

income over the debt service payments.

The values utilized in calculating these loan-to-value ratios are developed as part of PICA’s periodic review

of the mortgage loan portfolio, which includes an internal evaluation of the underlying collateral value. PICA’s

periodic review also includes a quality re-rating process, whereby it updates the internal quality rating originally

assigned at underwriting based on the proprietary quality rating system mentioned above.

17

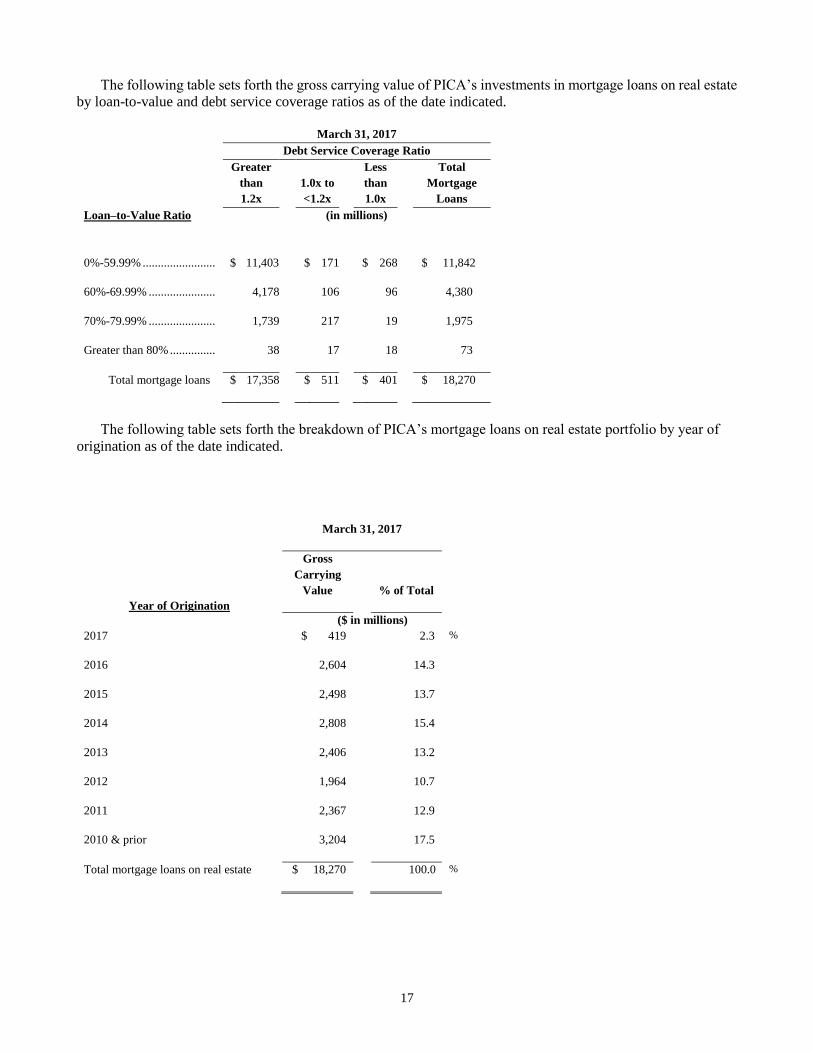

The following table sets forth the gross carrying value of PICA’s investments in mortgage loans on real estate

by loan-to-value and debt service coverage ratios as of the date indicated.

March 31, 2017

Debt Service Coverage Ratio

Greater

than

1.2x

1.0x to

<1.2x

Less

than

1.0x

Total

Mortgage

Loans

Loan–to-Value Ratio (in millions)

0%-59.99% ........................ $

11,403 $ 171 $ 268

$ 11,842

60%-69.99% ......................

4,178

106

96

4,380

70%-79.99% ......................

1,739

217

19

1,975

Greater than 80% ...............

38

17

18

73

Total mortgage loans $ 17,358 $ 511 $ 401 $ 18,270

The following table sets forth the breakdown of PICA’s mortgage loans on real estate portfolio by year of

origination as of the date indicated.

March 31, 2017

Year of Origination

Gross

Carrying

Value

% of Total

($ in millions)

2017 $ 419 2.3 %

2016 2,604 14.3

2015 2,498 13.7

2014 2,808 15.4

2013 2,406 13.2

2012 1,964 10.7

2011 2,367 12.9

2010 & prior 3,204 17.5

Total mortgage loans on real estate $ 18,270 100.0 %

18

Mortgage Loans on Real Estate Quality

Ongoing review of the portfolio is performed and loans are placed on watch list status based on a predefined

set of criteria, where they are assigned to one of the following categories. PICA classifies loans as closely

monitored when it determines there is a collateral deficiency or other credit events that may lead to a potential

loss of principal or interest. Loans not in good standing are those loans where PICA has concluded that there is a

high probability of loss of principal, such as when the loan is in the process of foreclosure or the borrower is in

bankruptcy. PICA’s workout and special servicing professionals manage the loans on the watch list. As described

below, in determining PICA’s allowance for losses, it evaluates each loan on the watch list to determine if it is

probable that amounts due according to the contractual terms of the loan agreement will not be collected.

PICA establishes an allowance for losses to provide for the risk of credit losses inherent in the lending process.

The allowance includes loan-specific reserves for loans that are determined to be impaired as a result of PICA’s

loan review process. PICA defines an impaired loan as a loan for which it estimates it is probable that amounts

due according to the contractual terms of the loan agreement will not be collected. The loan specific loss allowance

is based on PICA’s assessment as to ultimate collectability of loan principal and interest. Valuation allowances

for an impaired loan are recorded based on the present value of expected future cash flows discounted at the loan’s

effective interest rate or based on the fair value of the collateral less the estimated costs to obtain and sell. The

valuation allowance for mortgage loans can increase or decrease from period to period based on these factors.

The following table sets forth the breakdown of PICA's mortgage loans on real estate portfolio by quality as

of the dates indicated.

March 31, December 31,

2017 2016

Carrying Carrying

Value Value

(in millions)

Good standing $ 18,270 $ 18,121

Good standing with restructured terms 0 0

Interest overdue more than three months, not in foreclosure 0 1

Foreclosure in process 0 0

Total mortgage loans $ 18,270 $ 18,122

19

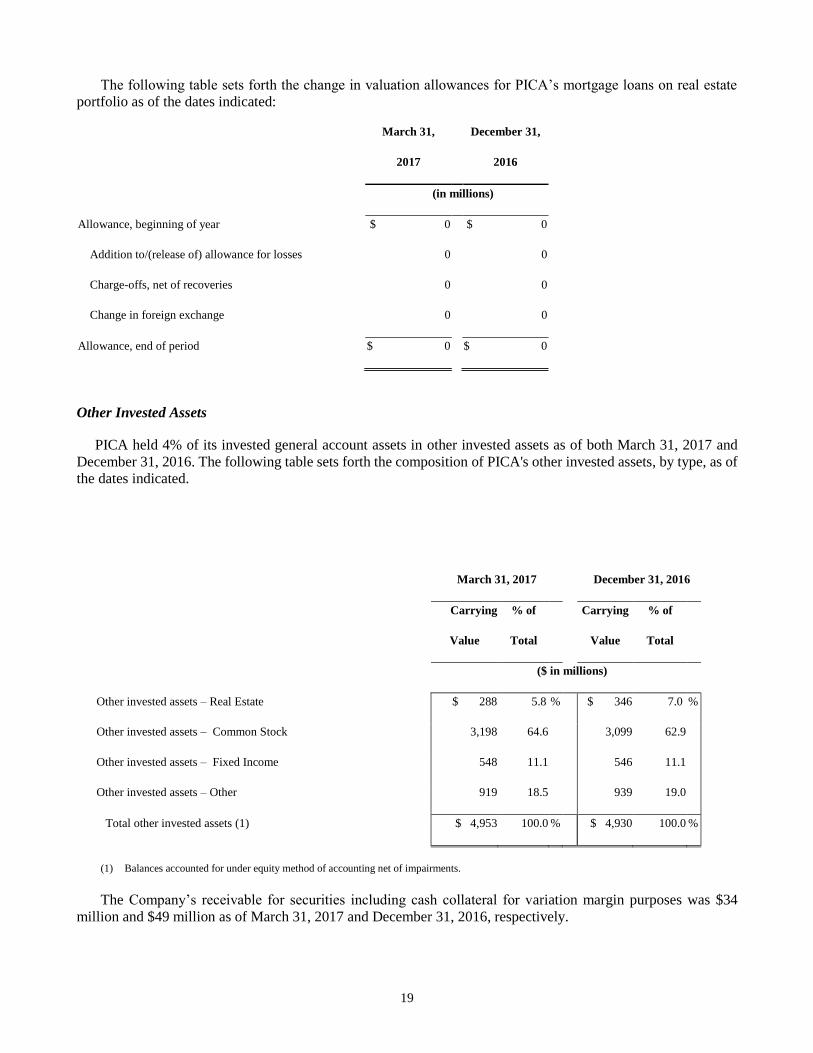

The following table sets forth the change in valuation allowances for PICA’s mortgage loans on real estate

portfolio as of the dates indicated:

March 31, December 31,

2017 2016

(in millions)

Allowance, beginning of year $ 0 $ 0

Addition to/(release of) allowance for losses 0 0

Charge-offs, net of recoveries 0 0

Change in foreign exchange 0 0

Allowance, end of period $ 0 $ 0

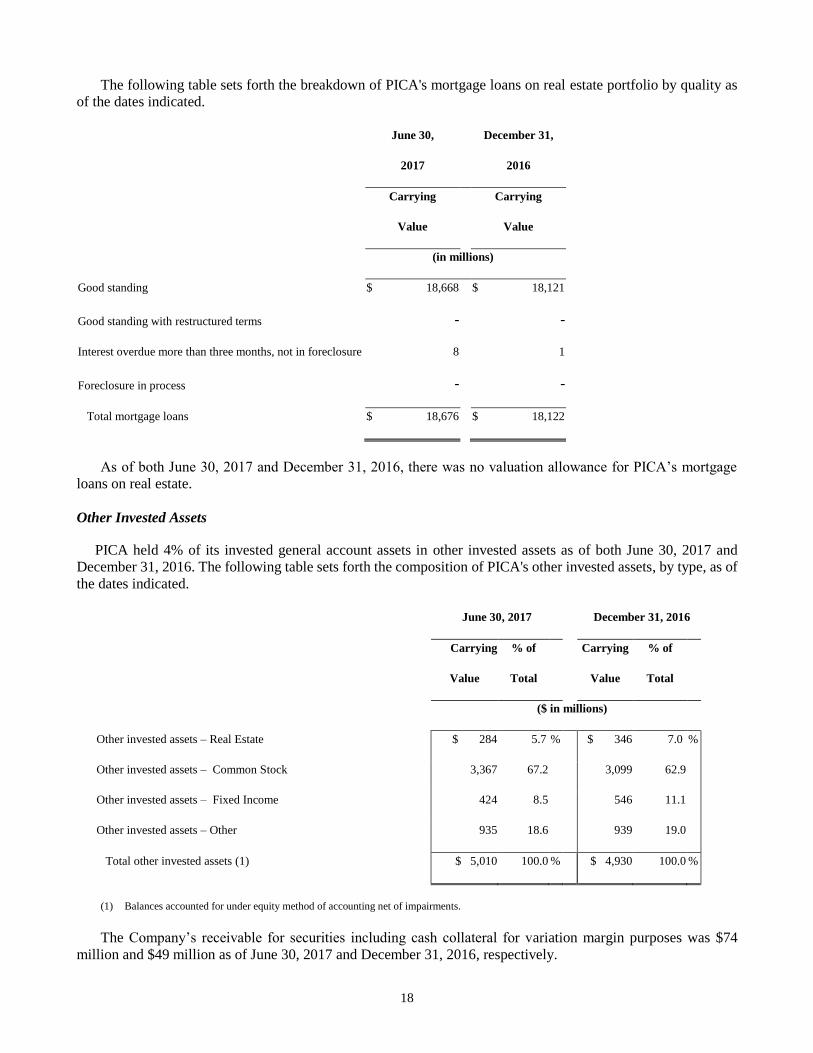

Other Invested Assets

PICA held 4% of its invested general account assets in other invested assets as of both March 31, 2017 and

December 31, 2016. The following table sets forth the composition of PICA's other invested assets, by type, as of

the dates indicated.

March 31, 2017 December 31, 2016

Carrying % of Carrying % of

Value Total Value Total

($ in millions)

Other invested assets – Real Estate $ 288 5.8 % $ 346 7.0 %

Other invested assets – Common Stock 3,198 64.6 3,099 62.9

Other invested assets – Fixed Income 548 11.1 546 11.1

Other invested assets – Other 919 18.5 939 19.0

Total other invested assets (1) $ 4,953 100.0 % $ 4,930 100.0 %

(1) Balances accounted for under equity method of accounting net of impairments.

The Company’s receivable for securities including cash collateral for variation margin purposes was $34

million and $49 million as of March 31, 2017 and December 31, 2016, respectively.

20

Liquidity and Capital Resources

Liquidity

Liquidity refers to the ability to generate sufficient cash resources to meet the payment obligations of PICA.

Capital refers to the long term financial resources available to support the operation of PICA’s businesses, fund

business growth, and provide a cushion to withstand adverse circumstances.

PICA's principal cash flow sources from insurance, annuities and guaranteed products are premiums and

annuity considerations, investment and fee income, and investment maturities and sales. PICA supplements these

cash inflows with financing activities. PICA’s cash outflow requirements principally relate to benefits, claims,

dividends paid to policyholders, and payments to contract holders in connection with surrenders, withdrawals and

net policy loan activity. Benefits include the payment of benefits under life insurance, annuity and guaranteed

products. PICA’s uses of cash also include commissions, general and administrative expenses, purchases of

investments, and debt service and repayments in connection with financing activities, as well as dividend

payments to its parent, PFI.

Some of PICA's products, such as guaranteed products offered to institutional customers, provide for payment

of accumulated funds to the contract holder at a specified maturity date unless the contract holder elects to roll

over the funds into another contract with PICA. PICA regularly monitors its liquidity requirements associated

with policyholder and contract holder obligations so that it can manage cash inflows to match anticipated cash

outflow requirements.

In addition, PICA has several subsidiaries that are subject to regulatory limitations on the payment of

dividends to PICA.

PICA is subject to regulatory limitations on the payment of dividends. New Jersey insurance law provides

that, except in the case of extraordinary dividends (as described below), all dividends or distributions paid by

PICA may be paid only from unassigned surplus, as determined pursuant to SAP, less unrealized capital gains

and revaluation of assets. PICA must give prior notification to the Commissioner of its intent to pay any dividend

or distribution. Also, if any dividend, together with other dividends or distributions made within the preceding

twelve months, exceeds the greater of (i) 10% of the prior calendar year’s statutory surplus or (ii) the prior calendar

year’s statutory net gain from operations (excluding realized capital gains), the dividend is considered to be an

“extraordinary dividend” and the prior approval of the Commissioner is required for payment of the dividend.

Moreover, the Commissioner is authorized to disallow the payment of any dividend or distribution, even if the

dividend is not an “extraordinary dividend”, if it determines that PICA does not have a reasonable surplus as to

policyholders relative to its outstanding liabilities and adequate to its financial needs or if it finds PICA to be in a

hazardous financial condition.

In June 2016, PICA paid a dividend of $900 million to its parent, PFI, of which $463 million was an

extraordinary dividend and $437 million was an ordinary dividend. Of the $900 million dividend, $542 million

was recorded as a return of capital and $358 million was recorded as dividend to stockholders. The extraordinary

dividend was approved by the Commissioner in May 2016.

In April 2016, PICA paid a dividend of $2,118 million to its parent, PFI, of which $1,513 million was an

extraordinary dividend and $605 million was an ordinary dividend. The dividend was recorded as dividend to

stockholders. The extraordinary dividend was approved by the Commissioner in April 2016.

Net cash provided by operations was $224 million and $374 million for the three months ended March 31,

2017 and March 31, 2016, respectively. The fluctuation between periods was primarily driven by a decrease in

other income, partially offset by a decrease in federal income taxes paid.

21

Net cash (used in) investing activities was ($973) million and ($3,259) million for the three months ended

March 31, 2017 and March 31, 2016, respectively. The fluctuation between periods was principally driven by a

decrease in net investments in bonds. PICA’s cash flows from investment activities result from repayments of

principal, proceeds from maturities and sales of invested assets and investment income, net of amounts reinvested.

The primary liquidity risks with respect to these cash flows are the risk of default by debtors or bond insurers,

PICA counterparties’ willingness to extend repurchase and/or securities lending arrangements and market

volatility. PICA closely manages these risks through our credit risk management process and regular monitoring

of our liquidity position.

Net cash (used in) provided by financing activities was ($129) million and $1,247 million for three months

ended March 31, 2017 and March 31, 2016, respectively. The fluctuation between periods was principally driven

by a change in collateralization of derivatives between periods.

Included in financing activity above were contractually scheduled withdrawals and prepayments of general

account GICs totaling $1,620 million for the three months ended March 31, 2017. Because these contractual

withdrawals, as well as the level of surrenders experienced, were consistent with PICA's assumptions in asset

liability management, the associated cash outflows did not have an adverse impact on PICA’s overall liquidity.

PICA believes that cash flows from its insurance, annuity and guaranteed products operations are adequate to

satisfy the current liquidity requirements of these operations based on its current liability structure and considering

a variety of reasonably foreseeable stress scenarios. The continued adequacy of this liquidity will depend upon

factors including future securities market conditions, changes in interest rate levels, policyholder perceptions of

PICA's financial strength and the relative safety of competing products, each of which could lead to reduced cash

inflows or increased cash outflows. In addition, market volatility can impact the level of capital required to support

PICA’s businesses, particularly PICA’s annuity business.

As of March 31, 2017 and December 31, 2016, PICA had cash and short-term investments of approximately

$3.4 billion and $4.3 billion, respectively, and investment grade bonds with a fair market value of $76 billion and

$75 billion, respectively.

Financing

PF, a wholly owned subsidiary of PICA, continues to serve as a source of financing for PICA and its

subsidiaries, as well as for other subsidiaries of PFI. PF operates under a support agreement with PICA whereby

PICA has agreed to maintain PF's positive tangible net worth at all times. PF borrows funds primarily through

the direct issuance of commercial paper. PF’s outstanding loans to other subsidiaries of PFI have declined over

time as it transitions into a financing company primarily for PICA and its remaining subsidiaries. As of March

31, 2017, PF had a tangible net worth of $20 million and short-term and long-term notes outstanding of $657

million and $221 million, respectively.

PF maintains a commercial paper program with an authorized capacity of $7 billion. PF's outstanding

commercial paper was $657 million as of March 31, 2017, representing an increase of $131 million from

December 31, 2016. As of March 31, 2017, the weighted average maturity of PF’s outstanding commercial paper

was 34 days, none of which was due overnight. As of March 31, 2017, the majority of these proceeds were utilized

to fund short-term cash flow timing mismatches and the working capital needs of PF’s affiliates, while the

remainder was primarily held in cash and cash equivalents. The daily average commercial paper outstanding for

the three months ended March 31, 2017 under this program was $940 million. The weighted average interest rates

on these borrowings were 0.69% and 0.37% for the three months ended March 31, 2017 and 2016, respectively.

PFI has issued a subordinated guarantee covering PF’s commercial paper program.

As of March 31, 2017, PFI and PF maintained a $4.0 billion unsecured committed credit facility expiring in

April 2020. Borrowings under this credit facility may be used for general corporate purposes, and PFI expects that

22

it may borrow under this facility from time to time to fund its working capital needs. In addition, amounts under

this credit facility may be drawn in the form of standby letters of credit that can be used to meet PFI’s operating

needs. The credit facility contains customary representations and warranties, covenants and events of default and

borrowings under the facility are not contingent on PFI’s credit ratings nor subject to material adverse change

clauses. As of March 31, 2017, there were no outstanding borrowings under the credit facility.

Borrowings under this credit facility are conditioned on the continued satisfaction of customary financial

covenants, including PFI’s maintenance of consolidated net worth of at least $18.985 billion, which is calculated

as U.S. GAAP equity, excluding accumulated other comprehensive income (loss), equity of noncontrolling

interests and equity attributable to the Closed Block. As of March 31, 2017, PFI was in compliance with the

covenants under this credit facility.

PICA maintains a Funding Agreement Notes Issuance Program pursuant to which Delaware statutory trusts

issue medium-term notes and commercial paper secured by funding agreements issued to the trusts by the

Company. Under this program, the maximum authorized amount is $15 billion of medium-term notes and $3

billion of commercial paper. The outstanding commercial paper and notes have fixed or floating interest rates

that range from 0.0% to 2.6% and original maturities ranging from seven days to five years. As a result, the

medium-term notes and commercial paper are included, along with liabilities relating to other funding agreements,

in the line item “Policyholders’ account balances” and not in the line item “Notes payable and other borrowings”

on PICA’s Statutory Statements of Admitted Assets, Liabilities and Capital and Surplus.

As of March 31, 2017, and December 31, 2016, the outstanding aggregate principal amount of such notes and

commercial paper totaled $4.1 billion and $3.8 billion, respectively. Included in the amounts at March 31, 2017

and December 31, 2016 is the medium-term note liability, which is carried at amortized cost, of $3.2 billion and

$3.2 billion, respectively, and short-term note liability of $0.9 billion and $0.6 billion, respectively.

On September 13, 2016, a Delaware trust issued in a private placement $350 million in aggregate principal

amount of 1.450% Medium-Term Notes due September 13, 2019.

On June 27, 2016, a Delaware trust issued in a private placement $100 million in aggregate principal amount

of Floating Rate Medium-Term Notes due June 27, 2018.

On June 3, 2016, a Delaware trust issued in a private placement $500 million in aggregate principal amount

of 2.200% Medium-Term Notes due June 3, 2021.

PICA’s ability to issue new notes under this program will depend on market conditions. PICA intends to

repay the maturing notes and commercial paper through a combination of cash flows from asset maturities, asset

sales, and internal sources of funds such as PF.

PICA is a member of the FHLBNY. Membership allows PICA access to the FHLBNY’s financial services,

including the ability to obtain collateralized advances and to issue collateralized funding agreements. FHLBNY

borrowings and funding agreements are collateralized by qualifying mortgage-related assets or U.S. Treasury

securities, the fair value of which must be maintained at certain specified levels relative to outstanding borrowings.

FHLBNY membership requires PICA to own member stock and borrowings require the purchase of activity-based

stock in an amount equal to 4.5% of outstanding borrowings. Under FHLBNY guidelines, if PICA’s financial

strength ratings decline below A/A2/A Stable by S&P/Moody’s/Fitch, respectively, and the FHLBNY does not

receive written assurances from the NJDOBI regarding PICA’s solvency, new borrowings from the FHLBNY

would be limited to a term of 90 days or less. Currently there are no restrictions on the term of borrowings from

the FHLBNY. All FHLBNY stock purchased by PICA is classified as restricted general account investments

within “Other invested assets” and the carrying value of these investments was $78 million and $78 million as of

March 31, 2017 and December 31, 2016, respectively.

23

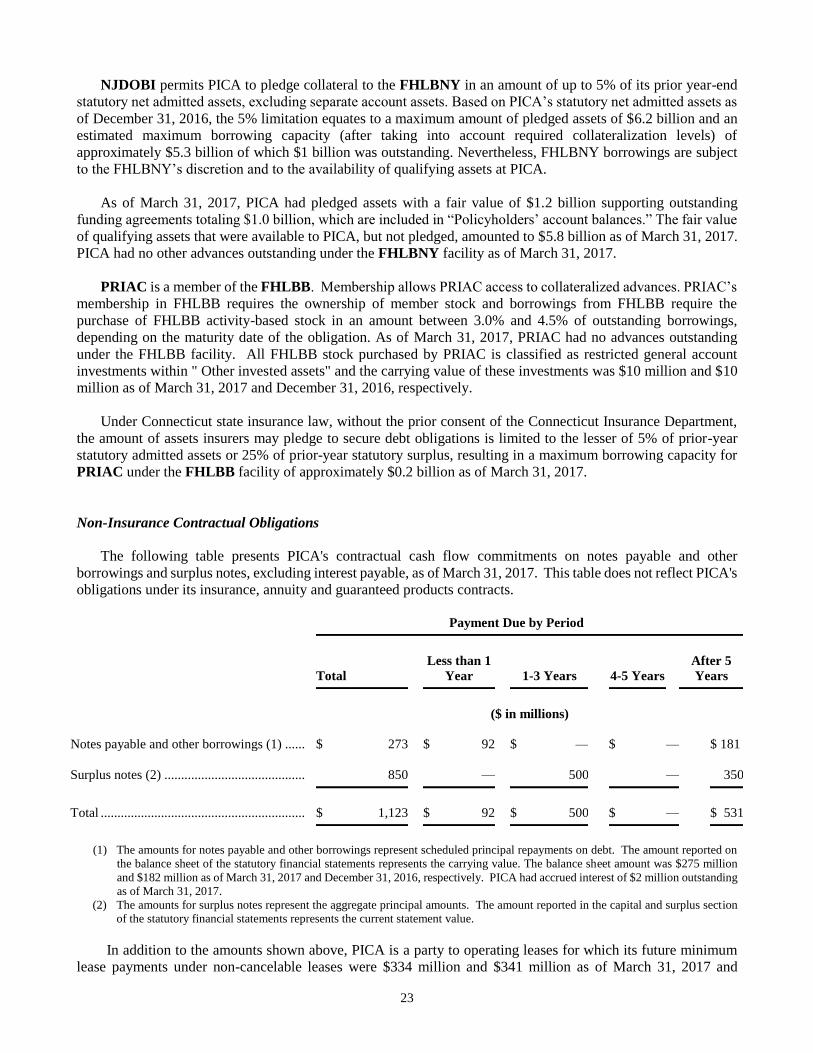

NJDOBI permits PICA to pledge collateral to the FHLBNY in an amount of up to 5% of its prior year-end

statutory net admitted assets, excluding separate account assets. Based on PICA’s statutory net admitted assets as

of December 31, 2016, the 5% limitation equates to a maximum amount of pledged assets of $6.2 billion and an

estimated maximum borrowing capacity (after taking into account required collateralization levels) of

approximately $5.3 billion of which $1 billion was outstanding. Nevertheless, FHLBNY borrowings are subject

to the FHLBNY’s discretion and to the availability of qualifying assets at PICA.

As of March 31, 2017, PICA had pledged assets with a fair value of $1.2 billion supporting outstanding

funding agreements totaling $1.0 billion, which are included in “Policyholders’ account balances.” The fair value

of qualifying assets that were available to PICA, but not pledged, amounted to $5.8 billion as of March 31, 2017.

PICA had no other advances outstanding under the FHLBNY facility as of March 31, 2017.

PRIAC is a member of the FHLBB. Membership allows PRIAC access to collateralized advances. PRIAC’s

membership in FHLBB requires the ownership of member stock and borrowings from FHLBB require the

purchase of FHLBB activity-based stock in an amount between 3.0% and 4.5% of outstanding borrowings,

depending on the maturity date of the obligation. As of March 31, 2017, PRIAC had no advances outstanding

under the FHLBB facility. All FHLBB stock purchased by PRIAC is classified as restricted general account

investments within " Other invested assets" and the carrying value of these investments was $10 million and $10

million as of March 31, 2017 and December 31, 2016, respectively.

Under Connecticut state insurance law, without the prior consent of the Connecticut Insurance Department,

the amount of assets insurers may pledge to secure debt obligations is limited to the lesser of 5% of prior-year

statutory admitted assets or 25% of prior-year statutory surplus, resulting in a maximum borrowing capacity for

PRIAC under the FHLBB facility of approximately $0.2 billion as of March 31, 2017.

Non-Insurance Contractual Obligations

The following table presents PICA's contractual cash flow commitments on notes payable and other

borrowings and surplus notes, excluding interest payable, as of March 31, 2017. This table does not reflect PICA's

obligations under its insurance, annuity and guaranteed products contracts.

Payment Due by Period

Total

Less than 1

Year

1-3 Years

4-5 Years

After 5

Years

($ in millions)

Notes payable and other borrowings (1) ...... $ 273 $ 92 $ — $ — $ 181

Surplus notes (2) ..........................................

850

—

500 — 350

Total ............................................................. $ 1,123 $ 92 $ 500 $ — $ 531

(1) The amounts for notes payable and other borrowings represent scheduled principal repayments on debt. The amount reported on

the balance sheet of the statutory financial statements represents the carrying value. The balance sheet amount was $275 million

and $182 million as of March 31, 2017 and December 31, 2016, respectively. PICA had accrued interest of $2 million outstanding

as of March 31, 2017.

(2) The amounts for surplus notes represent the aggregate principal amounts. The amount reported in the capital and surplus section

of the statutory financial statements represents the current statement value.

In addition to the amounts shown above, PICA is a party to operating leases for which its future minimum

lease payments under non-cancelable leases were $334 million and $341 million as of March 31, 2017 and

24

December 31, 2016, respectively.

During the normal course of its business, PICA utilizes financial instruments with off-balance sheet credit

risk such as commitments and financial guarantees. Commitments primarily include commitments to fund

investments in private placement securities, limited partnerships and other investments, as well as commitments

to originate mortgage loans. As of March 31, 2017 and December 31, 2016, these commitments were $3,385

million and $4,636 million, respectively.

Certain contracts underwritten by the Retirement business include guarantees related to financial assets owned

by the guaranteed party. These contracts are accounted for as derivatives, at fair value. As of March 31, 2017,

these contracts in force carried a total guaranteed value of $78 billion. These guarantees are supported by collateral

that is not reflected on PICA’s balance sheet. This collateral had a fair value of $78 billion as of March 31, 2017.

Contingencies

PICA has entered into reinsurance agreements with PLICJ, PGFL, PLICK, and other foreign entities, all of

which are affiliates of PICA. In each case, PICA has agreed to reinsure certain individual life insurance policies

through excess risk term contracts. Furthermore, PICA has agreed to co-insure U.S. dollar-denominated policies

sold by PLICJ and PGFL. For these reinsurance policies assumed, PICA has retroceded a portion of these risks

to affiliated companies.

PICA has committed to repurchase securities under master repurchase agreements in the amount of $4,921

million and holds cash collateral for loaned securities of $1,210 million as of March 31, 2017. PICA conducts

asset-based or secured financing, including transactions such as securities lending, repurchase agreements and

mortgage dollar rolls, to earn spread income, to borrow funds, or to facilitate trading activity. These programs are

primarily driven by portfolio holdings of securities that are lendable based on counterparty demand for these

securities in the marketplace. The collateral received in connection with these programs is primarily used to

purchase securities in PICA’s short-term spread portfolios. Investments held in the short-term spread portfolio

include cash and cash equivalents, short-term investments, mortgage loans and fixed maturities, including

mortgage- and asset-backed securities, with a weighted average life at time of purchase by the short-term