primary uses of deferred compensation · 2016-06-26 · primary uses of deferred compensation...

TRANSCRIPT

Primary Uses of Deferred Compensation

Blaine Laverick,

CEBS, CLU, ChFC, CRPS, CMS Managing RVP

NONQUALIFIED DEFERRED COMPENSATION (NQDC)

Updated April 2016

For Registered Representative Information Only. Not for Use with the General Public.

1

For Registered Representative Information Only. Not for Use with the General Public. 2

• Restore contribution limits HCEs face in qualified plan testing and employer contributions

• Employee deferrals and employer contributions

• Performance based contributions and vesting

• Defined contribution and defined benefit

• The 4th “R” - Not just Recruit, Retain & Reward, it’s also “Retire”…

• Not just the “C” suite anymore, expanded eligibility

Use of NQ Solutions

For Registered Representative Information Only. Not for Use with the General Public.

Growth in NQ Top Hat Plans Cumulative Plans Adopted Since 1995

source: U.S. Dept. of Labor

# of Plans

3

For Registered Representative Information Only. Not for Use with the General Public.

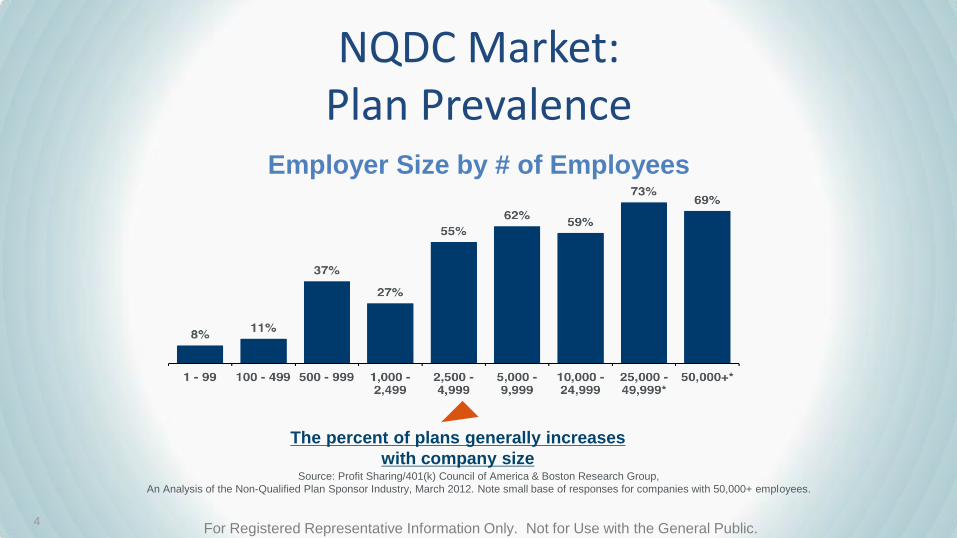

NQDC Market: Plan Prevalence

Employer Size by # of Employees

The percent of plans generally increases

with company size Source: Profit Sharing/401(k) Council of America & Boston Research Group,

An Analysis of the Non-Qualified Plan Sponsor Industry, March 2012. Note small base of responses for companies with 50,000+ employees.

4

For Registered Representative Information Only. Not for Use with the General Public.

• Nonqualified defined contribution plan

• Not subject to qualified plan restrictions due to contribution or compensation limits, or to coverage and discrimination testing

• An “unfunded” contractual agreement between a Plan Sponsor and a Plan Participant to pay compensation at a future date

• A plan not subject to the fiduciary and reporting requirements of ERISA

5

What is an “Excess” Plan?

For Registered Representative Information Only. Not for Use with the General Public.

NQ Plan Financing A Deferred Compensation Plan is an unfunded and unsecured contractual

obligation (liability) to pay a future benefit, subject to general creditors

Liability (Deferred Comp Account)

Asset (Life Insurance / mutual funds,

or unfinanced)

6

For Registered Representative Information Only. Not for Use with the General Public.

Financially stable – Established, Profitable, Good cash flow

• C corporations – Owners and employees

• S corporations, LLCs – Only for key employees (non-shareholders)

• Not-for-Profit organizations

Not appropriate for governmental employers and certain other tax exempt entities.

* Contributions to the plan are subject to FICA when benefits vest. Deferrals may not be treated as

deferred for state income tax purposes in all states. Distributions are taxable to participants upon receipt.

Client company characteristics

7

For Registered Representative Information Only. Not for Use with the General Public.

Flexibility

• Can pick and choose plan participants

• Plan design – Offer participants a plan that feels similar to complementary qualified plans

• Control vesting schedules

• Plan may provide tax free key person protection for the company

• Clear legal and regulatory environment (IRC 409(a))

• Employer receives a tax deduction when the benefit is paid

* Contributions to the plan are subject to FICA when benefits vest. Deferrals may not be treated as

deferred for state income tax purposes in all states. Distributions are taxable to participants upon receipt.

Benefits for the employer

8

For Registered Representative Information Only. Not for Use with the General Public.

• Options for financing plans - unfinanced, taxable, or tax deferred – Effect of financing option on current and future deductions

• Administration and reporting requirements – Principal provides comprehensive administrative services

– Generally fee based, depending on financing solution

Issues to consider for the employer

9

For Registered Representative Information Only. Not for Use with the General Public.

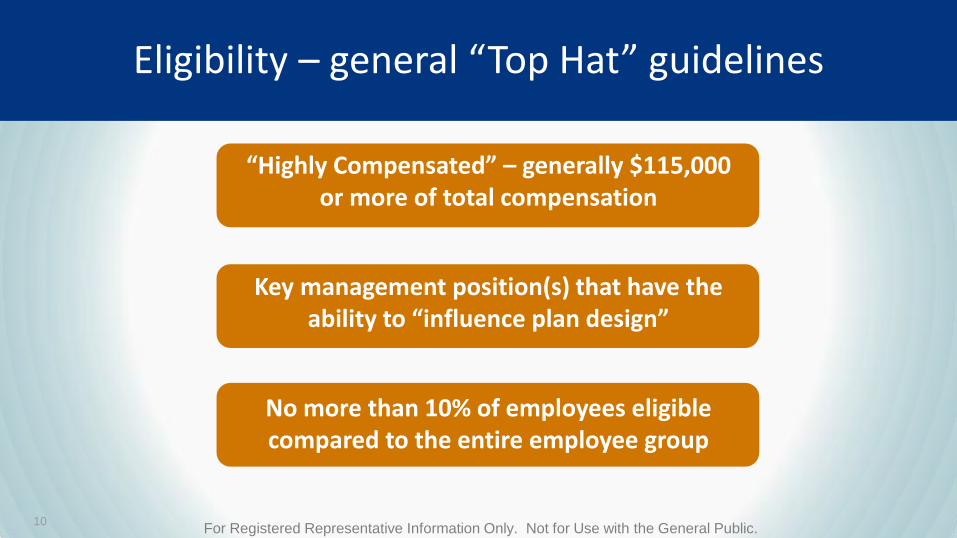

“Highly Compensated” – generally $115,000 or more of total compensation

Key management position(s) that have the

ability to “influence plan design”

No more than 10% of employees eligible compared to the entire employee group

Eligibility – general “Top Hat” guidelines

10

For Registered Representative Information Only. Not for Use with the General Public.

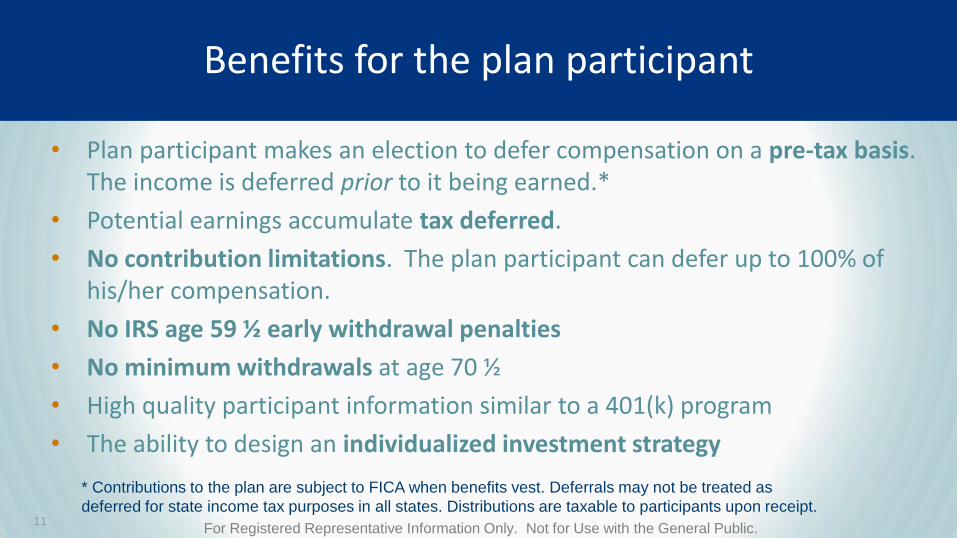

• Plan participant makes an election to defer compensation on a pre-tax basis. The income is deferred prior to it being earned.*

• Potential earnings accumulate tax deferred.

• No contribution limitations. The plan participant can defer up to 100% of his/her compensation.

• No IRS age 59 ½ early withdrawal penalties

• No minimum withdrawals at age 70 ½

• High quality participant information similar to a 401(k) program

• The ability to design an individualized investment strategy

* Contributions to the plan are subject to FICA when benefits vest. Deferrals may not be treated as

deferred for state income tax purposes in all states. Distributions are taxable to participants upon receipt.

Benefits for the plan participant

11

For Registered Representative Information Only. Not for Use with the General Public.

• Contractual obligation vs. fiduciary liability

• Assets are owned by the company and are subject to company’s creditors in the event of bankruptcy

• Election to defer income only once per year in advance of earning income

• No loan provisions

• No rollover provisions into an IRA, a qualified plan or a nonqualified plan

• Nonqualified deferrals may reduce wages for qualified plan contributions

Issues to consider for the plan participant

12

For Registered Representative Information Only. Not for Use with the General Public.

401(k) Restoration & Retirement Savings

Taxation Timing

Compensation Management

PRIMARY USES OF NONQUALIFIED DEFERRED COMPENSATION

PRIMARY USES OF DEFERRED COMPENSATION 13

For Registered Representative Information Only. Not for Use with the General Public.

401(k) Restoration & Retirement Savings

PRIMARY USES:

PRIMARY USES OF NONQUALIFIED DEFERRED COMPENSATION

For Registered Representative Information Only. Not for Use with the General Public.

14

For Registered Representative Information Only. Not for Use with the General Public.

More than 8 in 10 participants say NQDC plans are important in reaching their retirement goals.

2014 Trends in Nonqualified Deferred Compensation Among Plan Sponsors and

Participants, the Principal Financial Group.

15

For Registered Representative Information Only. Not for Use with the General Public.

401(k) Restoration & Retirement Savings

16

For Registered Representative Information Only. Not for Use with the General Public.

Employer contributions can “restore” benefits that are

limited under a qualified retirement plan

• Allows eligible key employees to defer into

an NQDC plan

• Any amount restricted by qualified plan

non-discrimination testing

• Up to the maximum qualified plan amount

• Company contributions follow deferrals

401(k) restoration

17

For Registered Representative Information Only. Not for Use with the General Public.

Retirement Savings Going beyond 401(k) restoration

Addressing the retirement gap higher earners face

• Deferral limits can be raised, or more commonly, eliminated

• May or may not include company matching amounts and/or

discretionary profit share contributions

• Employer has the ability to choose which key employees

to reward and how much.

▪ Plan design may allow ability to create tiers of the

Top Hat Group with different deferral limits,

employer contributions and vesting schedules

18

For Registered Representative Information Only. Not for Use with the General Public.

Taxation Timing PRIMARY USES:

PRIMARY USES OF NONQUALIFIED DEFERRED COMPENSATION

For Registered Representative Information Only. Not for Use with the General Public.

19

For Registered Representative Information Only. Not for Use with the General Public.

NQDC offers participants considerable flexibility and

control over distributions to meet their objectives but

also provides the distribution flexibility to control when

they take receipt of the money

Taxation Timing

Of those participants planning to increase their annual contribution,

67% identified

‘helping manage their current income tax‘ as a factor in the decision

• Eligible key employees may use NQDC plans to

choose when they take distributions

including the option to take installments.

They can also delay distributions beyond the

originally scheduled timing.

* 2014 Trends in Nonqualified Deferred Compensation Among Plan Sponsors and Participants, the Principal Financial Group.

20

For Registered Representative Information Only. Not for Use with the General Public.

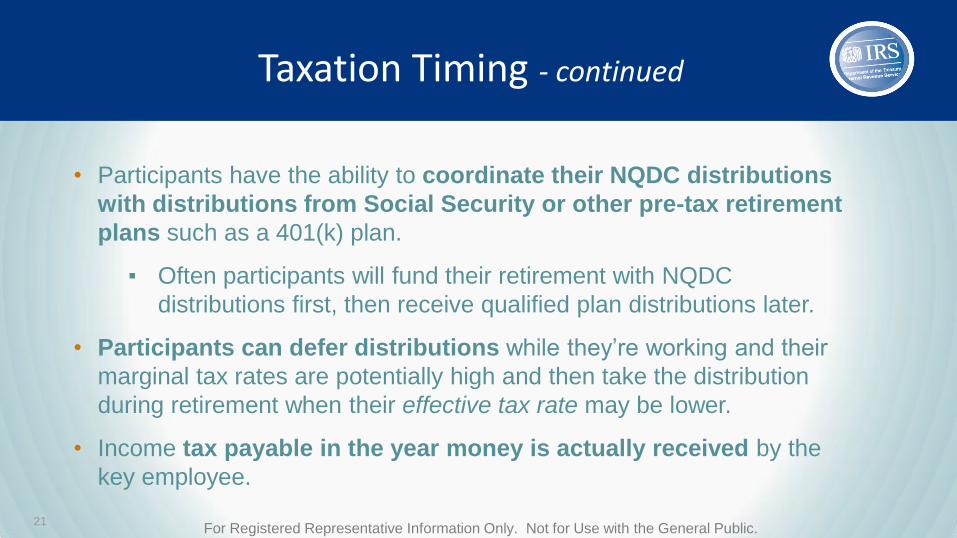

• Participants have the ability to coordinate their NQDC distributions

with distributions from Social Security or other pre-tax retirement

plans such as a 401(k) plan.

▪ Often participants will fund their retirement with NQDC

distributions first, then receive qualified plan distributions later.

• Participants can defer distributions while they’re working and their

marginal tax rates are potentially high and then take the distribution

during retirement when their effective tax rate may be lower.

• Income tax payable in the year money is actually received by the

key employee.

Taxation Timing - continued

21

For Registered Representative Information Only. Not for Use with the General Public.

Key Employee Base Income $120,000 Bonus $40,000

• elects to defer 10% of base pay & 50% of bonus Deferral Amounts:

• Base = $12,000

• Bonus = $20,000

• Total = $32,000

Objectives:

• 2 Kids need College $$

• Planning Second Home

• Secure Retirement Annual Deferral Elections Allocation

20% College Mary 20% College Michael 20% Beach House 30% Retirement

$9,600 $6,400 $6,400 $6,400

July

2019

July

2020

July

2024 Retire

4 Payments 4 Payments 1 Payments 10 Payments

Taxation Timing - continued

10% Retirement

$3,200

Retire

1 Payments Conservative

Portfolio

Moderate

Portfolio

Moderate

Portfolio

Aggressive

Portfolio

Aggressive

Portfolio 22

For Registered Representative Information Only. Not for Use with the General Public.

NQDC provides the ability to reduce current taxes by deferring compensation and paying

taxes when distributions are received.

• Marginal Tax Rate: The percentage of tax paid on the next dollar of incremental

taxable income.

o For NQDC this tax rate would typically apply to any current deferrals into the

plan, as each dollar of deferral is coming off the top of the participant’s total

taxable income.

• Effective Tax Rate: The tax paid in total divided by total taxable income on the NQDC

distribution. This takes into account all tax brackets affecting the distributions to the

taxpayer.

o These tax brackets would typically apply to distributions from NQDC plans in

the early years of retirement, when many participants use NQDC distributions as

a primary source of retirement income.

Taxation Timing Marginal vs. Effective Tax Rates

23

For Registered Representative Information Only. Not for Use with the General Public. For Registered Representative Information Only. Not for Use with the General Public. 24

For Registered Representative Information Only. Not for Use with the General Public.

Compensation Management

PRIMARY USES:

PRIMARY USES OF NONQUALIFIED DEFERRED COMPENSATION

For Registered Representative Information Only. Not for Use with the General Public.

25

For Registered Representative Information Only. Not for Use with the General Public.

NQDC plans can provide employers with a program to help

recruit, retain, reward and/or provide incentives for the

people on whom the success of your business depends.

• Use performance-based contribution and

performance-based vesting to influence the

behavior you want from key performers

• Customize contribution and vesting schedules

to use as performance rewards for key employees

Compensation Management

26

For Registered Representative Information Only. Not for Use with the General Public.

Use discretionary employer contributions based on the

particular needs of your organization

Compensation Management

27

For Registered Representative Information Only. Not for Use with the General Public.

2020 2016 2017 2018 2019 2021

ER Contribution

2016 Vested 2017 Vested 2018 Vested

Laddering Employer Contributions

“Roll Forward Vesting”

ER Contribution

ER Contribution

Example shows 3 year cliff rolling vesting

28

For Registered Representative Information Only. Not for Use with the General Public.

Key benefits of NQDC

However the plan sponsor chooses to design your plan, some key

benefits are universal. An NQDC plan:

Allows participants the opportunity to defer compensation in excess of qualified

retirement plan limits on a pre-tax basis (up to 100 percent deferral depending

on plan design)

Can allow organizations to make discretionary contributions to retain and

motivate key employees — including incentive-based contributions.

Restores contributions/benefits limited by IRS restrictions in retirement plans

Can give participants more flexibility in tax planning with flexible distribution

options

29

For Registered Representative Information Only. Not for Use with the General Public.

Key benefits of NQDC - continued

Offers flexible distribution options including ability to take

prior to age 59½

Allows participants to design an individualized investment

strategy

Is not subject to contribution and participation limits

Has simplified government reporting and disclosure

rules, or none at all, depending on plan design

30

For Registered Representative Information Only. Not for Use with the General Public.

• Are key employees concerned about saving enough for

retirement on a tax-advantaged basis?

• Do their retirement plans restrict their ability to discriminate

in favor of their most profitable employees?

• Are their compensation plans motivating the behavior they

want from their top executives?

• Are they concerned about turn-over of key people?

How can a plan sponsor evaluate if a new nonqualified plan is right for their business?

31

For Registered Representative Information Only. Not for Use with the General Public.

Look for:

• Plans that are three or more years old

• Sponsors who are dissatisfied with current plan’s

performance

Your key to success:

• Identify the pain points and provide solutions

Opportunities to help with existing nonqualified plans

32

For Registered Representative Information Only. Not for Use with the General Public.

Look closer at their plan. Key areas to evaluate:

• Plan design

• Plan financing options

• Unfinanced

• Taxable investments

• Variable corporate-owned life insurance (COLI)

• Plan administrative services

• Employee/employer service

Opportunities to help with existing nonqualified plans

33

For Registered Representative Information Only. Not for Use with the General Public.

Action steps

Ask questions

Set up conference calls

Schedule client meetings

Schedule client seminars

34

For Registered Representative Information Only. Not for Use with the General Public. 35

For Registered Representative Information Only. Not for Use with the General Public.

Required to sell training prior to presenting a solution

• Primary Uses of Deferred Compensation (this presentation)

Recognize advisor roles and responsibilities

Account Profile Form

Signed client disclosure

• Involvement of client’s own tax/legal consultants to provide advice for plan

establishment

• Selection of top-hat group to meet ERISA exemption

• Selection of financing option

─ Unfinanced, taxable investments, or variable corporate-owned life insurance

(COLI)

Requirements

36

For Registered Representative Information Only. Not for Use with the General Public.

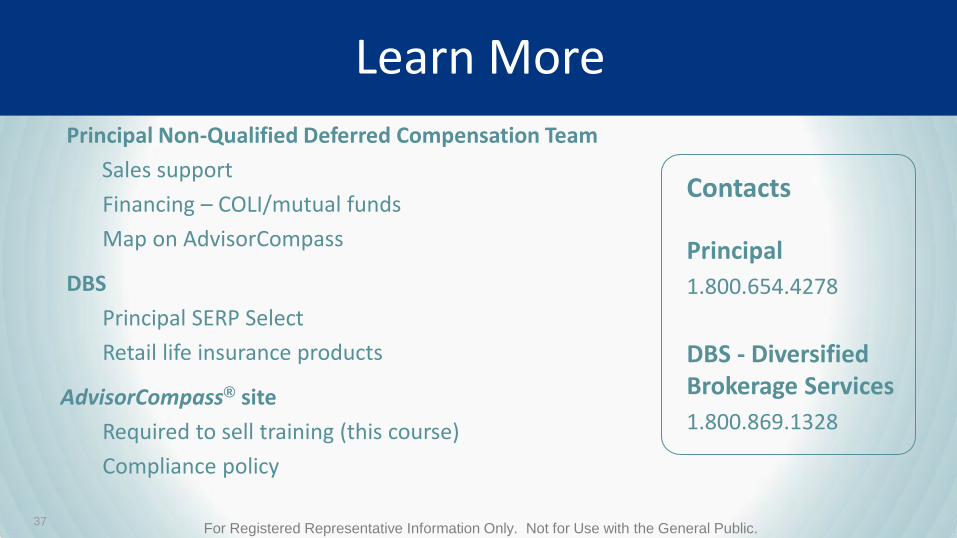

Learn More

Principal Non-Qualified Deferred Compensation Team

Sales support

Financing – COLI/mutual funds

Map on AdvisorCompass

DBS

Principal SERP Select

Retail life insurance products

AdvisorCompass® site

Required to sell training (this course)

Compliance policy

Contacts

Principal

1.800.654.4278

DBS - Diversified Brokerage Services

1.800.869.1328

37

For Registered Representative Information Only. Not for Use with the General Public.

PRIMARY USES OF DEFERRED COMPENSATION

The subject matter in this communication is provided with the understanding that The Principal® is not rendering legal,

accounting, or tax advice. You should consult with appropriate counsel or other advisors on all matters pertaining to legal, tax,

or accounting obligations and requirements.

The Principal Financial Group® is registered with the National Association of State Boards of Accountancy as a sponsor of

continuing education on the National Registry of CPE Sponsors. State Boards of accountancy have final authority on the

acceptance of individual courses. Complaints regarding registered sponsors may be addressed to NASBA, 150 Fourth Avenue

North, Nashville, TN 37219-2471, 615-880-4200

Insurance products issued by Principal National Life Insurance Co (except in NY) and Principal Life Insurance Co. Plan

administrative services offered by Principal Life. Principal Funds, Inc. is distributed by Principal Funds Distributor, Inc.

Securities offered through Principal Securities, Inc. 800-247-1737, Member SIPC and/or independent broker/dealers. Principal

National, Principal Life, Principal Funds Distributor, Inc. and Principal Securities are members of the Principal Financial Group

®, Des Moines, IA 50392.

Copyright © 2016 Principal Financial Services, Inc.

38

Click the X in the upper right corner to close the presentation.

For Registered Representative Information Only. Not for Use with the General Public.

Q&A

Questions?

39