principles of macroeconomics - · pdf fileconsider the impact of government policies on the...

TRANSCRIPT

PrinciplesofMacroeconomicsModule4.1

Savings,Investment,andFinancialMarkets

161

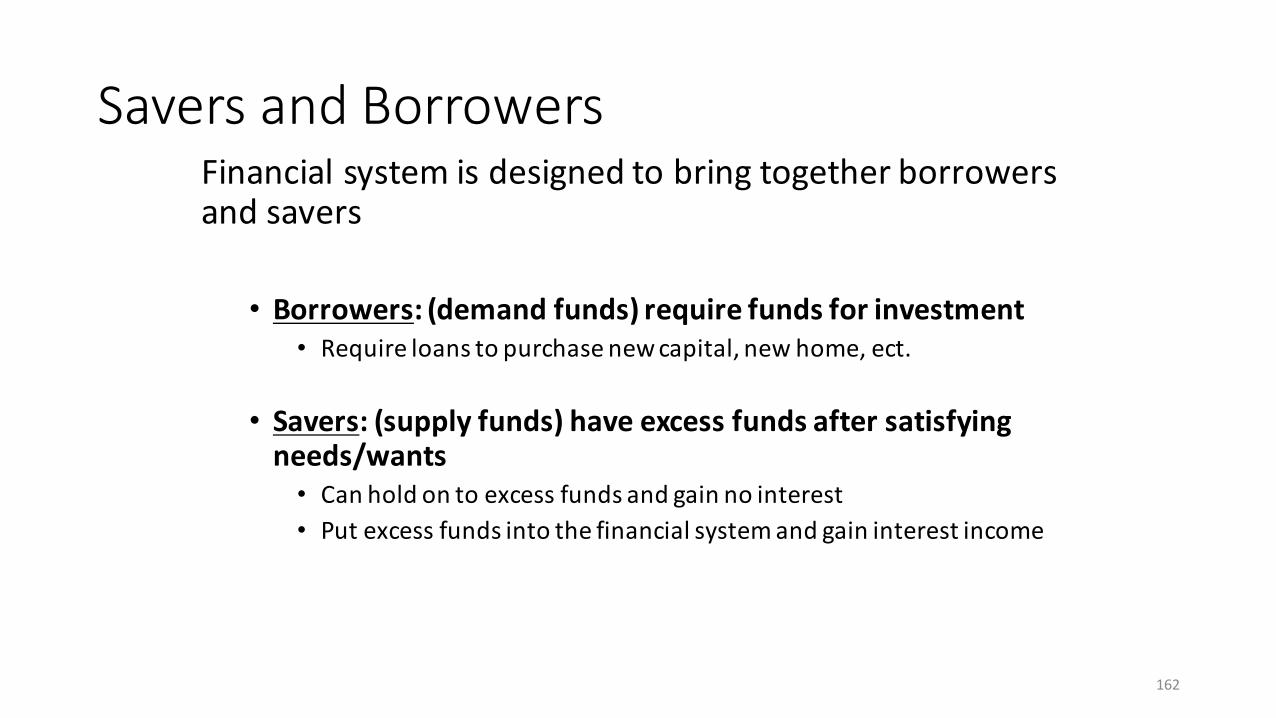

SaversandBorrowersFinancialsystemisdesignedtobringtogetherborrowersandsavers

• Borrowers:(demandfunds)requirefundsforinvestment• Requireloanstopurchasenewcapital,newhome,ect.

• Savers:(supplyfunds)haveexcessfundsaftersatisfyingneeds/wants

• Canholdontoexcessfundsandgainnointerest• Putexcessfundsintothefinancialsystemandgaininterestincome

162

TheMarketforLoanableFunds

Supplyanddemandmodelthatexplains• Howtodetermineinterestrates• Theallocationofloanstoborrowers

Assume:onlyonefinancialmarket• Allsaversdeposittheirsavinginthismarket.

• Allborrowerstakeoutloansfromthismarket.

• Thereisoneinterestrate,whichisboththereturntosavingandthecostofborrowing

163

SupplyofLoanableFundsInterest

Rate

Loanable Funds ($billions)

Supply comes from:• Households with extra

income • Positive public saving

164

Supply(Savings)

DemandforLoanableFundsInterest

Rate

Loanable Funds ($billions)

Demand(Investment)

Demand comes from:• Firms borrow the funds for new

capital • Households borrow to

purchase new houses

165

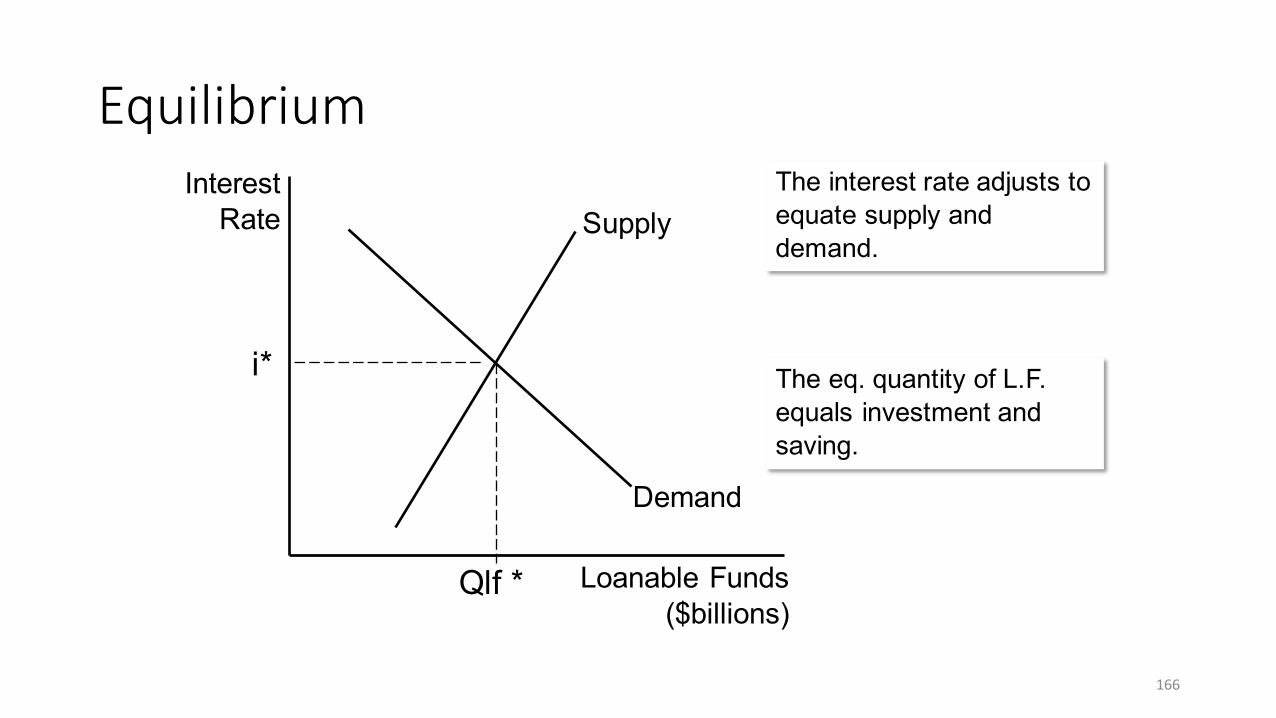

EquilibriumInterest

Rate

Loanable Funds ($billions)

Demand

The interest rate adjusts to equate supply and demand.

Supply

The eq. quantity of L.F. equals investment and saving.

i*

Qlf *

166

ChangesinLoanableFundsMarketConsidertheimpactofgovernmentpoliciesontheloanablefundsmarket:

(1) Supposethegovernmentdecreasestaxesoninterestincome

(2) Supposethegovernmentprovidesataxcreditforfirmsinvestingingreentechnology

• Whatistheimpactontheloanablefundsmarket?

• Decidewhichcurveshiftsandwhy.

• Drawouttheimpactofeachpolicyandanalyzethenewequilibrium.

167

ChangesinLoanableFundsMarket(1)

InterestRate

Loanable Funds ($billions)

Demand

Supply

(1) Supposethegovernmentdecreasestaxesoninterestincome

168

ChangesinLoanableFundsMarket(1)

InterestRate

Loanable Funds ($billions)

Demand

S.1

(1) Supposethegovernmentdecreasestaxesoninterestincome

169

S.2

ChangesinLoanableFundsMarket(1)

InterestRate

Loanable Funds ($billions)

Demand

S.1

(1) Supposethegovernmentdecreasestaxesoninterestincome

170

S.2

B

A

ChangesinLoanableFundsMarketConsidertheimpactofgovernmentpoliciesontheloanablefundsmarket:

(1) Supposethegovernmentdecreasestaxesoninterestincome

(2) Supposethegovernmentprovidesataxcreditforfirmsinvestingingreentechnology

• Whatistheimpactontheloanablefundsmarket?

• Decidewhichcurveshiftsandwhy.

• Drawouttheimpactofeachpolicyandanalyzethenewequilibrium.

171

ChangesinLoanableFundsMarket(2)

InterestRate

Loanable Funds ($billions)

Demand

Supply

(2)Supposethegovernmentprovidesataxcreditforfirmsinvestingingreentechnology

172

ChangesinLoanableFundsMarket(2)

InterestRate

Loanable Funds ($billions)

D.1

Supply

(2)Supposethegovernmentprovidesataxcreditforfirmsinvestingingreentechnology

173

D.2

ChangesinLoanableFundsMarket(2)

InterestRate

Loanable Funds ($billions)

D.1

Supply

(2)Supposethegovernmentprovidesataxcreditforfirmsinvestingingreentechnology

174

D.2

B

A

ImpactofGovernmentBudgetDeficit

Supposethegovernmentisrunningabudgetdeficitandneedstofinancetheshortfallintaxrevenuebyissuinggovernmentbonds.

• Whatistheimpactontheloanablefundsmarket?• Decidewhichcurveshiftsandwhy.• Drawouttheimpactofeachpolicyandanalyzethenewequilibrium

175

ChangesinLoanableFundsMarket(3)

InterestRate

Loanable Funds ($billions)

Demand

Supply

(3)Gov’tfinancesbudgetdeficitwithnewbonds

176

ChangesinLoanableFundsMarket(3)

InterestRate

Loanable Funds ($billions)

Demand

S.1

(3)Gov’tfinancesbudgetdeficitwithnewbonds

177

S.2

ChangesinLoanableFundsMarket(3)

InterestRate

Loanable Funds ($billions)

Demand

S.1

(3)Gov’tfinancesbudgetdeficitwithnewbonds

178

S.2

B

A

KeyTakeaways

• The loanable funds market is determined by the interaction between suppliers of loans (savers) and demand for loans (borrowers)

• Price of a loan = interest rates which is determined by:• How much people want to save at a given rate• How many loans will be taken out at that rate

• Gov’t policies can influence S/D of loans• Gov’t deficits cause crowding out and lower investment

179

Principles of MacroeconomicsModule 4.1 (B)

Money and the Federal Reserve

What is Money?Moneyisasetofassetsinaneconomythatpeople

regularlyusetobuygoodsandservicesfromotherpeople

ServesThreeFunctions:1. MediumofExchange-- abilitytopurchasewhatwe

want2. UnitofAccount– abilitytoassignavaluetoanitem3. Storeofvalue– abilitytocomparevaluesindifferent

timeperiods

HistoricalTypes ofMoneyCommodityMoney:theuseofacommodityasmoneywhichitselfholdsintrinsicvalue

à Goldcoins,cowryshells,diamonds

FiatMoney:moneythathasvaluebygovernmentdecree,initselfholdsnovalue

à currencybills(USdollar)

Money and Liquidity

Liquidity: Easewithwhichanassetcanbeconvertedintotheeconomy’smediumofexchange

à Cashisthemostliquidasset

Money in the Economy

M1:Mostliquidformofmoney

M2:M1+Time/Savingsdeposits

Determining Money SupplyThecentralbankinacountrycontrolsthemoney

supplyandsetsmonetarypolicyUSCentralBank:TheFederalReserve

Determining Money SupplyTheTwoObjectivesoftheFederalReserve:1. Controlmoneysupplythrough:–OpenMarketOperations– Lendingtobanks(lenderoflastresort)– Influencingreserveratios

2. Overseeandregulatethebankingsystem– Clearchecktransactions– Trackbankliquidityandhealth– Lendingtobankswhentheneedit(LenderofLastResort)

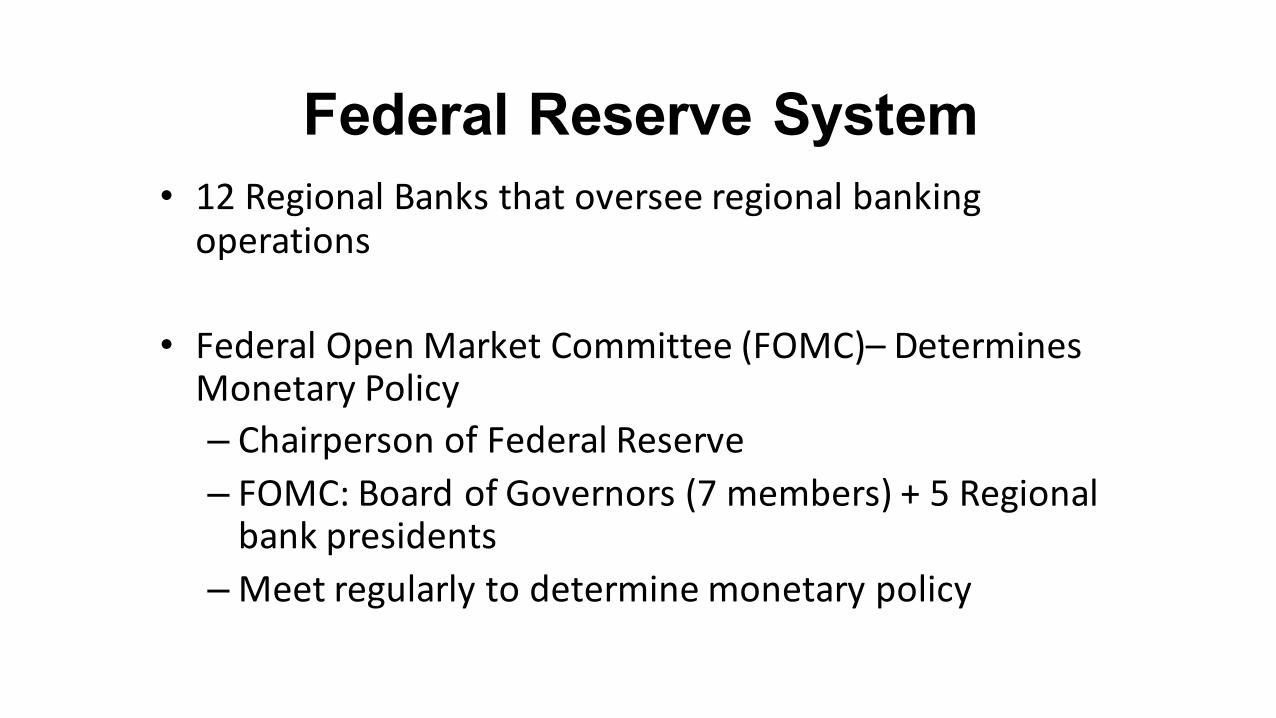

Federal Reserve System• 12RegionalBanksthatoverseeregionalbankingoperations

• FederalOpenMarketCommittee(FOMC)– DeterminesMonetaryPolicy– ChairpersonofFederalReserve– FOMC:BoardofGovernors(7members)+5Regionalbankpresidents

–Meetregularlytodeterminemonetarypolicy

Key Takeaways• Moneyisthemostliquidformofassetsavailabletopeople

• Peoplechoosebetweenmoreliquidityormorereturnwithdecidingwheretoputtheirwealth

• MoneySupplyisdeterminedbytheFederalReserve–CentralBankoftheUnitedStates

• TheFedplaysakeyroleintheeconomy– determiningthequantityofmoneyandinfluencinginterestrates

PrinciplesofMacroeconomicsModule4.1TimeValueofMoney

190

TimeValueofMoney

ValueofMoney:Moneytodayismorevaluabletodaythaninthefuture

Whatwouldyouchoose?- $500today- $500in3years

191

Time Value of Money• Present value: the amount of money needed today to yield that future value of money at

prevailing interest rates

#+%5%0)6('7% =87)7+%6('7%

1 + + :

• Future value: the amount the money will be worth at a given future date, when allowed to earn interest at the prevailing rate

87)7+%6('7% = #+%5%0)6('7% ∗ 1 + + :

Assumptions:• Inflation = 0%• Interest rates do not change over the given time period• Do no withdraw any funds from the account

192

Time Value of Money• Present value: the amount of money needed today to yield that future value of money at

prevailing interest rates

#+%5%0)6('7% =87)7+%6('7%

1 + + :

• Future value: the amount the money will be worth at a given future date, when allowed to earn interest at the prevailing rate

87)7+%6('7% = #+%5%0)6('7% ∗ 1 + + :

Assumptions:• Inflation = 0%• Interest rates do not change over the given time period• Do no withdraw any funds from the account 193

Testyourunderstanding

Suppose you receive $100 today and you put it in the bank where you can gain 5% interest. What will it be worth in 10 years?

194

TestyourunderstandingSuppose you receive $100 today and you put it in the bank where you can gain 5% interest. What will it be worth in 10 years?

PV = $100 i = 5% n = 10

86 = $100 ∗ 1 + 5% ?@

FV = $163

195

Testyourunderstanding

Suppose you are 20 years old today and your grandmother promises you $500 when you turn 25. How much is this gift worth to you today if the interest rate is 10%?

196

Testyourunderstanding

Suppose you are 20 years old today and your grandmother promises you $500 when you turn 25. How much is this gift worth to you today if the interest rate is 10%?FV = $500 i = 10% n = 5

P6 = $A@@

?B?@% C

PV = $310

197

KeyTakeaways

• Todeterminethefuturevaluevs.presentvalueofmoney– needtothinkintermsofopportunitycosts

• Interestrates– influencetheopportunitycostofmoneytodayvs.moneyinthefuture

• BecauseyoucangaininterestincomeonmoneyyoureceiveTODAY,itisworthmorethanthesameamountofmoneyyouwouldreceiveinthefuture

198

Principles of MacroeconomicsModule 4.1 (D)

Banks, Money Supply and Money Creation

Banks and Monetary Policy• Banksplayakeyroleinthefinancialsystem• Bylendingoutpartoftheirdeposits,banks“create”money:Loansgivemoneytopeoplethatpreviouslydidnothaveittobuygoodsandservices

àFractionalReserveBankingSystem• WhentheFedsetsmonetarypolicy,itmustconsiderthe

impactofthefractionalreservebankingsystem• Fedsetsminimumlimitfortheshareofdepositsbanksmust

holdinreserve(ie:cannotloanout)Reserveratio(R) – Shareofdepositsbanksholdasreserve

Totalreserves/Totaldeposits

Bank’s Assets & LiabilitiesBank A

Assets LiabilitiesReserves $ 10Loans $ 90

Deposits $100

Reserveratio(R)=10%

Byloaningoutashareofdepositstoborrowers,Bankscreatemoney!

Loansprovidemoneytopeoplewhodidnotpreviouslyhaveittopurchasegoodsandservices

• Loudeposits$100intohisbankaccount

• BankAholds10%asreserves($10)

• BankAloansout90%($90)toJane

• Janeusesthe$90tobuynewsuppliesforherbusinessfromBill

Bank AAssets Liabilities

Reserves $ 10Loans $ 90

Deposits $100

Bank BAssets Liabilities

Reserves $ 9Loans $ 81

Deposits $90

Bank CAssets Liabilities

Reserves $ 8.10Loans $ 72.90

Deposits $81

• Billdeposits$90intohisbankaccount

• BankBholds10%asreserves($9)

• BankAloansout90%($81)toTim

• Timusesthe$81tobuynewtoolsfromSal

Bank AAssets Liabilities

Reserves $ 10Loans $ 90

Deposits $100

Bank BAssets Liabilities

Reserves $ 9Loans $ 81

Deposits $90

Bank CAssets Liabilities

Reserves $ 8.10Loans $ 72.90

Deposits $81

• Saldeposits$81intohisbankaccount

• BankBholds10%asreserves($8.10)

• BankAloansout90%($72.90)toSara

• Sarausesthe$72.90tobuyanewmachineforhershop

Bank AAssets Liabilities

Reserves $ 10Loans $ 90

Deposits $100

Bank BAssets Liabilities

Reserves $ 9Loans $ 81

Deposits $90

Bank CAssets Liabilities

Reserves $ 8.10Loans $ 72.90

Deposits $81

ThemoneycontinuestofilterthroughthebankingsystemuntilthereisnomorelefttoloanoutThreebankscreated=$90+$81+$72.90=$243.90

Bank AAssets Liabilities

Reserves $ 10Loans $ 90

Deposits $100

Bank BAssets Liabilities

Reserves $ 9Loans $ 81

Deposits $90

Bank CAssets Liabilities

Reserves $ 8.10Loans $ 72.90

Deposits $81

Money Creation Through Banking SystemSupposeFedincreasesmoneysupplyby$100

– Increaseindepositsby$100– Increaseinloansby$90– NewMoneySupply=$100+$90=$190– IncreaseinMSwillfilterthroughthebankingsystemandmoneywillbecreatedthroughthedeposit-loanprocessofbanks

A fractional reserve banking system creates money, but not wealth.

Money Creation Through Banking System

Moneymultiplier(MM):theamountofmoneythebankingsystemgenerateswitheachdollarofreserves

Byhowmuchthemoneysupplyincreaseasitfiltersthroughthebankingsystem

Money Multiplier = 1 / Reserve Ratio

Bank AAssets Liabilities

Reserves $ 10Loans $ 90

Deposits $100

Bank BAssets Liabilities

Reserves $ 9Loans $ 81

Deposits $90

Bank CAssets Liabilities

Reserves $ 8.10Loans $ 72.90

Deposits $81

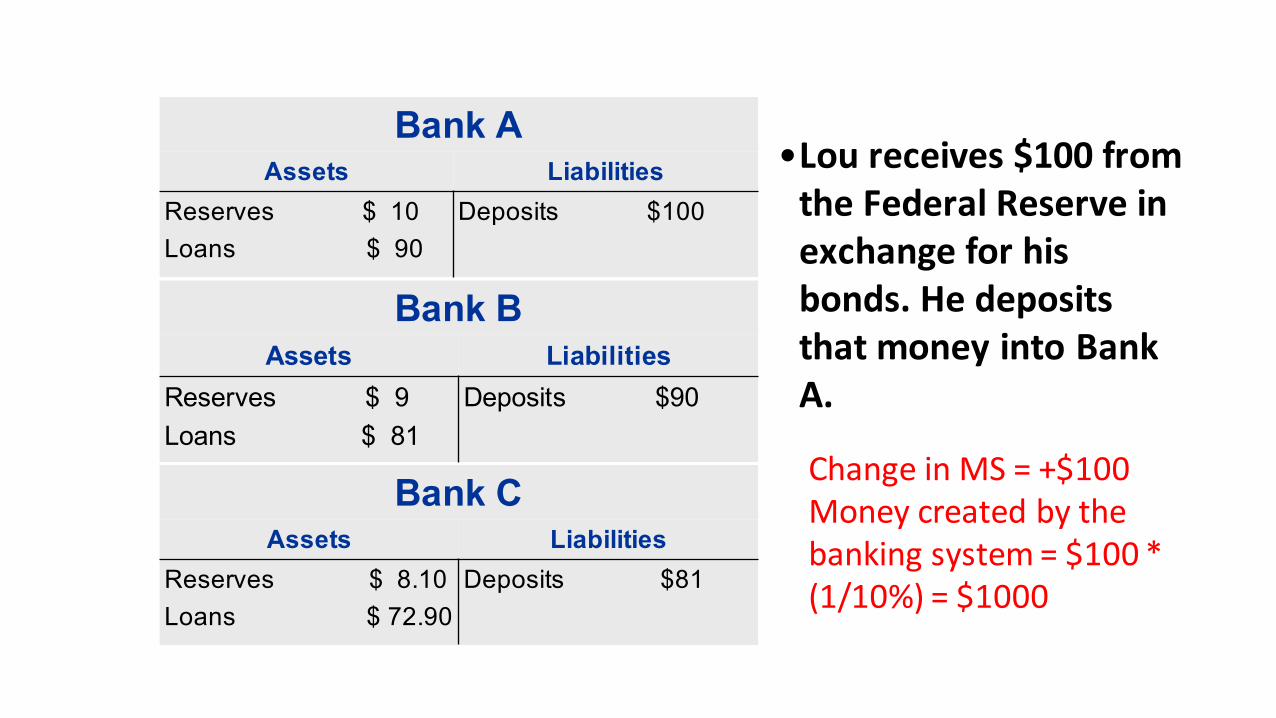

•Loureceives$100fromtheFederalReserveinexchangeforhisbonds.HedepositsthatmoneyintoBankA.

ChangeinMS=+$100Moneycreatedbythebankingsystem=$100*(1/10%)=$1000

Test your understanding SupposetheFederalReserveincreasesthemoneysupplyby$1000.Thereserverequirementis12.5%.

• Whatisthemoneymultiplier?• Whatisthenewmoneysupplyinthisfractionalreservebankingsystem

Test your understanding SupposetheFederalReserveincreasesthemoneysupplyby$1000.Thereserverequirementis12.5%.

• Whatisthemoneymultiplier?• MM=1/12.5%=8

• Whatisthenewmoneysupplyinthisfractionalreservebankingsystem

• NEWMS=($1000*8)=$8000

Key Takeaways• Thebankingsystemiscrucialinthemoneycreationprocess.Byloaningoutpartofdeposits– bankscreatemoney(butnotwealth)

• TheFed’ssettingofthemoneysupplyisnotperfect,sinceitcannotcontroltheamountofdepositsnorthelendingrateabovethereserverequirement

13

Principles of MacroeconomicsModule 4.1 (E)

MoneyMarketandEquilibrium

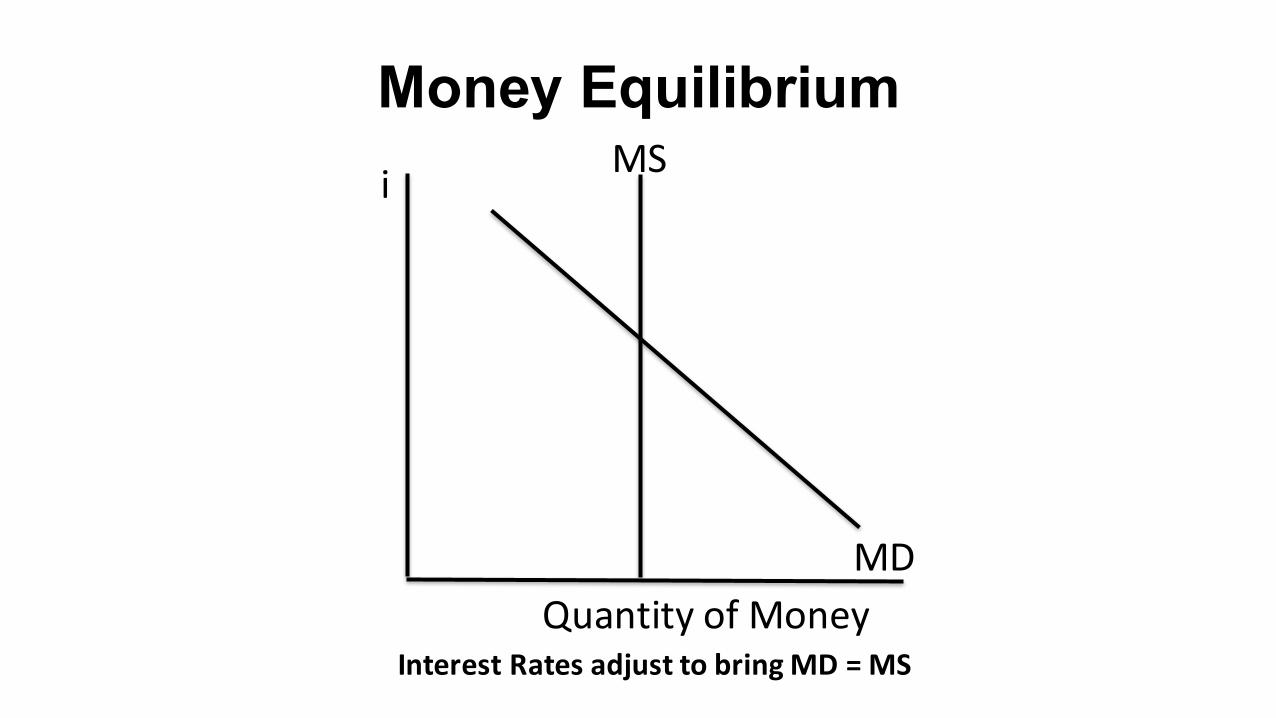

Money Supply and Money Demand• Moneysupply(MS)isdeterminedmainlybytheFederal

Reserve– Quantityofmoneyisfixed– WhentheFedadjustsMS:itimpactstheinterestrate– DiscountRate:InterestrateatwhichFedlendstobanks

• Moneydemand(MD)reflectshowmuchwealthpeoplewanttoholdinaliquidform– Maindeterminant:Interestrates– Athighinterestrates:peopleprefertokeepmorewealthininterest-bearingassets(lowMD)

– Atlowinterestrates:peopleprefertokeepmorewealthinliquidform(highMD)

P.2

MD

MSi

QuantityofMoney

Money Equilibrium

InterestRatesadjusttobringMD=MS

Changes in Money SupplySupposetheFeddecidestoincreasethemoneysupplythroughopenmarketoperations.Itdecidestobuybondsfromthepublic.• Whathappenstothenewequilibriumpricelevel,valueofmoneyandequilibriumquantityofmoney?

• Intheinterim(beforepriceleveladjusts),isthereasurplusorshortageofmoney?

P.2

MD

i.1

MSi

QuantityofMoney

Changes in Money SupplyMS.2

Qm.1 Qm.2

P.2

MD

i.1

MSi

QuantityofMoney

Changes in Money SupplyMS.2

Qm.1 Qm.2

MD<MSSURPLUS

P.2

MD

i.1

MSi

QuantityofMoney

Changes in Money SupplyMS.2

Qm.1 Qm.2

i.2

SURPLUS

B

Coping with Surplus of MoneyWhenthereisasurplusofmoney,peopletrytogetridofit:• Usingthesurplustopurchasegoodsandservicesàmoredemandà priceofgoodsincreases

• Puttingmoneyintheloanablefundsmarketà moreloansavailableà Increaseindemandforgoods

↑MS=↑savings=↓interestrates

↑MS=↑demandforgoods=↑pricelevel

Test your understanding - 1Supposecreditcardsbecomemorereadilyavailabletothegeneraladultpopulation,makingiteasiertopurchasegoodsandserviceswithoutcarryingcasharoundeverywhere.• GraphtheMd-Msdiagram• Whichcurveshiftsandwhy?• Illustratethechangethiswillhaveonthemoneymarket.• Whathappenstothenewequilibriumpricelevel,valueofmoneyandequilibriumquantityofmoney?

Creditcardsbecomemorereadilyavailabletothegeneraladultpopulation,makingiteasiertopurchasegoodsandservices

withoutcarryingcasharoundeverywhere.

P.2

MD

i.1

MSi

QuantityofMoney

MD.2

A

Qm.1

Creditcardsbecomemorereadilyavailabletothegeneraladultpopulation,makingiteasiertopurchasegoodsandservices

withoutcarryingcasharoundeverywhere.

P.2

MD

i.1

MSi

QuantityofMoneyMD.2

A

Qm.1

B

Test your understanding - 2Inresponsetothepreviousscenario,theFedbecomesconcernedaboutinflationandpreferstokeeptheinterestrateati.1(originalinterestrate).• WhatcantheFeddowiththemoneysupplytoimpactthemoneymarket?

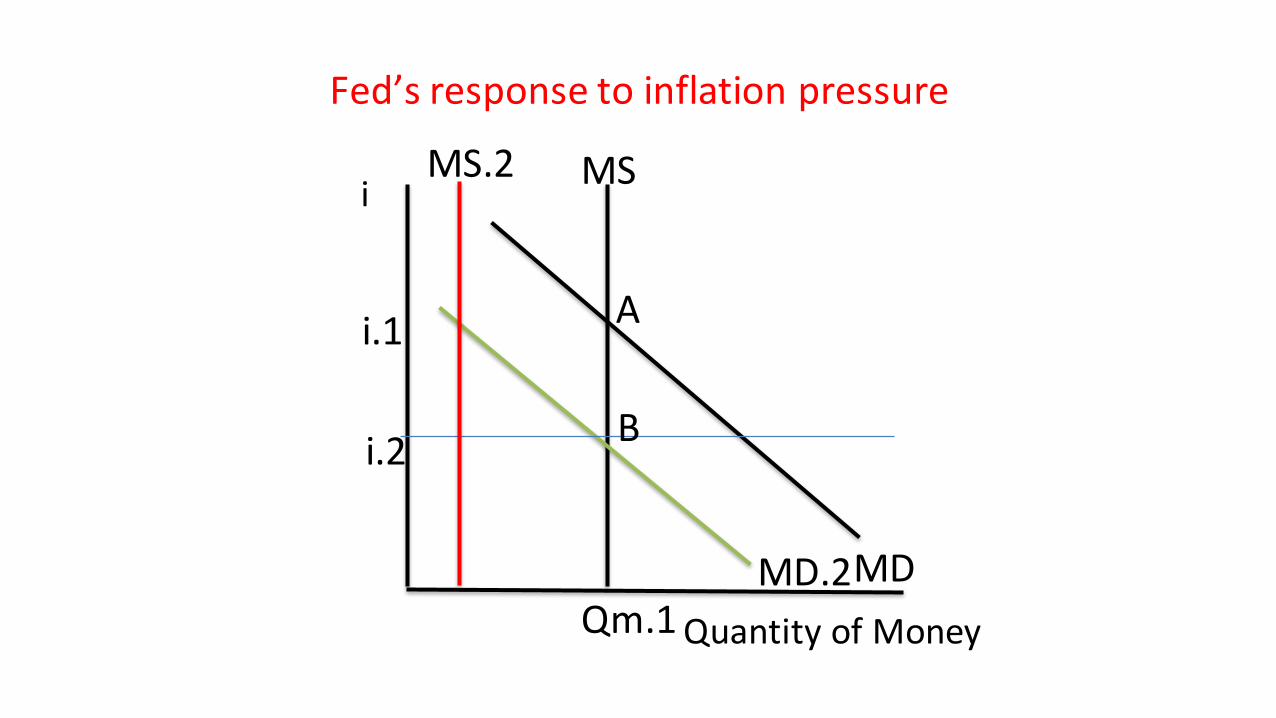

Fed’sresponsetoinflationpressure

P.2

MD

i.1

MSi

QuantityofMoneyMD.2

A

Qm.1

B

MS.2

i.2

Fed’sresponsetoinflationpressure

P.2

MD

i.1

MSi

QuantityofMoneyMD.2

A

Qm.1

B

MS.2

i.2

Qm.2

Key Takeaways• Moneygrowthinfluencespricelevelsandinflationintheeconomy

• ChangesinMDcomefromachangeinliquiditypreferencesinhouseholds– dotheywanttoholdmore/lesswealthinliquidform?

• ChangesinMSonlycomefromtheFederalReserve– noentityexceptforthecentralbankcanchangemoneysupply

Principles of MacroeconomicsModule 4.1 (F)

Financial Tools: Bonds, Stocks and Other

Financial Tools• Interestbearingassetscomeinmanyforms:• Bonds• Stocks• Savingsaccounts• CertificatesofDeposit• TimeDeposits

• Allofthesereturnsomeportionofpeople’sinvestmentasinterestincome

Bonds • Bondsarecertificatesofindebtedness• CorporateBonds:Corporationsissuebondstoraisefundsforaninvestmentproject• GovernmentBonds:Governmentsissuebondstoraisefundstocovertheshortfallintaxrevenue• Atthetimeofmaturity:Principleisrepaid• Overthetimetomaturity:Interestpaymentsmadebythebondissuertothebondholder• Bondholdersgivea“loan”tothebondissuer• Theydonotownpartofthecompanyorgovernment

Pricing Bonds• Factorsthataffectthebondprice:• Timetomaturity• Longertimetomaturityhasahigherbondprice

• Riskinessofrepayment•Moreriskybondshaveahigherbondprice

• Interestrates•Wheninterestratesarehigh–youcangainmoreinterestincomebyputtingyourmoneyinother(higher)interestbearingassetsthanthebond• Higherinterestrates:Lowerbondprices

Stocks• Ownersofstockhavepart-ownershipinacompany• Onlypubliclytradedcompaniesissuestocks• Thevalueofthestockreflects:• Theexpectationsonprofitabilityofthefirm• Supply/Demandforthestock

PrinciplesofMacroeconomicsModule4.2

CentralBankandControloftheMoneySupply

199

CentralBankandControloftheMoneySupply• MonetarypolicyandtheroleoftheFederalReserveindeterminingthemoneysupply• GoalstheFederalReserveare:• tocontrolthemoneysupplyintheeconomy• toregulatethebankingsystem

• Controloverthemoneysupply• influenceinterestrates

• Relationshipbetweenthemoneysupplyandtheinterestrateiswhatwecallthetheoryofliquiditypreferences• interestratesaregoingtoadjusttokeepmoneysupplyandmoneydemandtogether

CentralBankandControloftheMoneySupply• Themoneymarketequilibriumwherewehavethemoneydemandandmoneysupplygraphsaswellasthevalueofmoneyandthepriceleveldeterminingthisrelationship• Howcanwereconcilethegraphsthatwesawpreviouslywiththevalueofmoneyandthepricelevelwiththeadjustmentsinmoneysupplyimpactinginterestrates?• We'regoingtoseeisthatthemoneymarketandtheloanablefundsmarketaregoingtobecloselyrelatedinthesensethattheinterestrateeffectisgoingtobethestrongesteffectthatwesee.• Understandhowwecanlinkthemoneymarketwiththeloanablefundsmarketsothatwecanexplainchangesinthemoneysupplywithrespecttochangesininterestrates.

CentralBankandControloftheMoneySupply• Anincreaseinthemoneysupply• Wouldleadtoasurplusofmoneytemporarilyatthegivenpricelevel

• Thestrongestandmostprevalentwaythatpeoplegetridofthissurplusofmoney• Puttingthatmoneyintointerest-bearingassetssothatweseeashiftinthesupplyofloanablefunds• Thereforeweseeanincreaseinthemoneysupply.

• Soanincreaseinthemoneysupply• Asubsequentriseinthepricelevelandashiftoutofthesupplyofloanablefunds• adecreaseintheinterestrate

CentralBankandControloftheMoneySupply• Mergethesetwomarketstogether• anincreaseinthemoneysupplyisgoingtoleadtoadecreaseininterestrates.

• Ontheotherhand,adecreaseinthemoneysupply• leadtoashortageofmoney

• Peopletakemoneyoutoftheirsavings,outoftheirinterest-bearingassetstobuybondsfromtheFederalReserve• thisdecreasesthesupplyofloanablefundsandincreasestheinterestrate

CentralBankandControloftheMoneySupply• OneofthemostprevalentwaysthattheFederalReservecanimpactthemoneysupplyisthroughthebuyingandsellingofbondstothepublic• openmarketoperations

• Iftheywanttoincreasethemoneysupply• FederalReservewillbuybondsfromthepublicinexchangeformoney• Bydoingsoittakesbondsfromthepublicandgivesthepublicmoneyinexchangeandincreasesthemoneysupply

• Iftheywanttodecreasethemoneysupply• Theywillsellbondstothepublic• Theygivepeoplebondsandtaketheirmoneyinexchange,andbydoingsodecreasingthesupplyofmoneyintheeconomy

CentralBankandControloftheMoneySupply• Anotherwayisthroughsettingthediscountrate• Thediscountrateistherateatwhichbankslendtoeachother• Highdiscountrate,banksarenotgoingtowanttolendtoeachother• Moreexpensiveforthemtodoso,sothey'llholdontomorereservesjustincase• Sothemoneycreationprocessisgoingtobesmaller—thatmultipliereffectisgoingtobesmaller

CentralBankandControloftheMoneySupply• AnotherwaythattheFederalReservecaninfluencethemoneycreationprocessisthesettingreserverequirements• They'llsetaminimumofreserveratiosthatthebankshavetohold

• Ifthatminimumishighthenthemoneycreationprocessisgoingtobesmallerbecausethebanksaregoingtoberequiredtoholdontomorereserves• TheFederalReservetriesnottochangethereserverequirementsfrequentlybecauseyoucandisruptbankingbusiness

CentralBankandControloftheMoneySupply• Lastly,theFederalReservecanchoosetopayinteresttothebanks'reserves• Thehighertheinterestthattheyarepayingtobanksthemorereservesthebankswillhold• Thereforethesmallerthemoneycreationprocessis

• TheselastthreestepsareawayfortheFederalReservetoimpactthecreationofmoneyinthebankingsystemandindirectlyinfluencethemoneysupply

PrinciplesofMacroeconomicsModule4.2

RealandNominalInterestRates

208

ClassicalDichotomyReferstotheseparationofnominalandrealvariables

• NominalVariables: MeasuredinmonetarytermsThepriceofanappleis$2Thepriceofabananais$1

• RealVariables:Measuredinphysicalunits(orrelativeterms)Thepriceofanappleis2bananasThepriceofabananais½apple

Changesinthemoneysupply– Nominalchanges

MonetaryNeutrality:Changesinthemoneysupplywillnotimpactrealvariables

200

FischerEffect• Nominalinterestratesadjustone-for-onetotheinflationrate

Reali =nominali – inflation

• Changeininflationà impactsnominalinterestratenotrealinterestrate

• Importantimplicationsfortaxinginterestincome,debtrepayment,andsavings

201

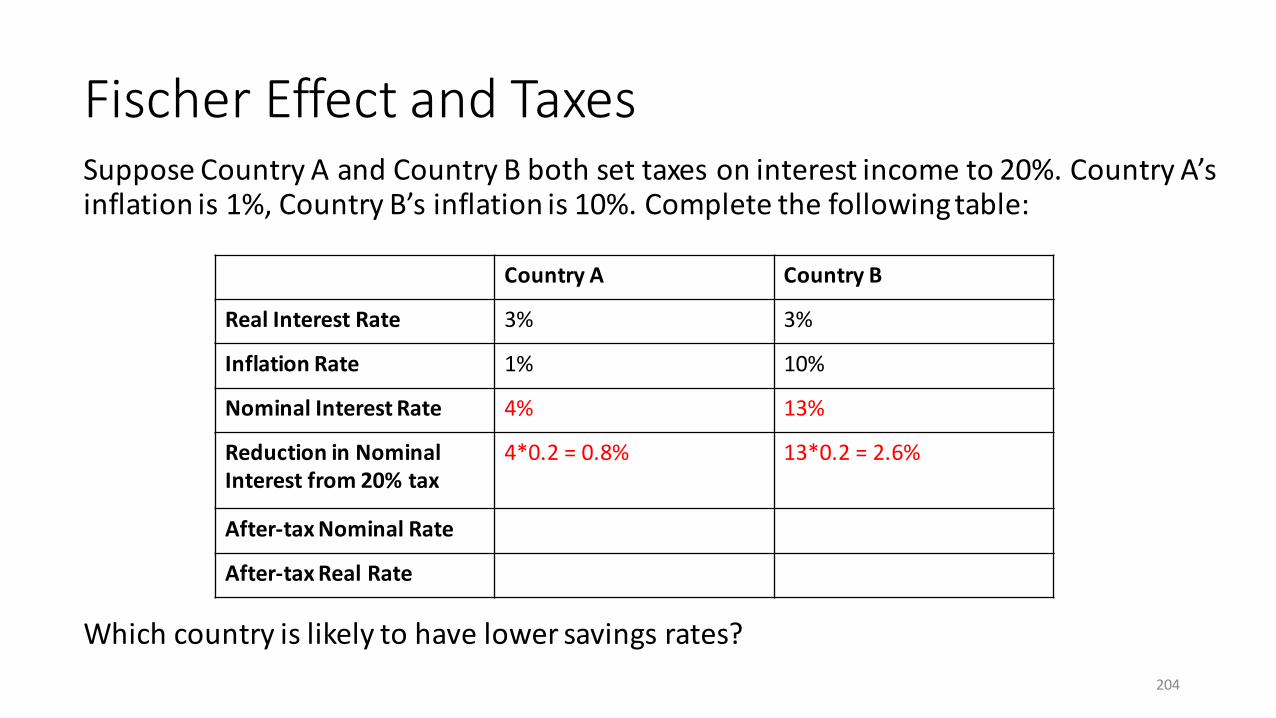

FischerEffectandTaxesSupposeCountryAandCountryBbothsettaxesoninterestincometo20%.CountryA’sinflationis1%,CountryB’sinflationis10%.Completethefollowingtable:

Whichcountryislikelytohavelowersavingsrates?

CountryA CountryBRealInterest Rate 3% 3%

InflationRate 1% 10%

NominalInterestRateReductioninNominalInterestfrom20%taxAfter-taxNominalRateAfter-tax RealRate

202

FischerEffectandTaxesSupposeCountryAandCountryBbothsettaxesoninterestincometo20%.CountryA’sinflationis1%,CountryB’sinflationis10%.Completethefollowingtable:

Whichcountryislikelytohavelowersavingsrates?

CountryA CountryB

RealInterest Rate 3% 3%

InflationRate 1% 10%

NominalInterestRate 3%+1%=4% 3%+10%=13%

ReductioninNominalInterestfrom20%tax

After-taxNominalRate

After-tax RealRate

203

FischerEffectandTaxesSupposeCountryAandCountryBbothsettaxesoninterestincometo20%.CountryA’sinflationis1%,CountryB’sinflationis10%.Completethefollowingtable:

Whichcountryislikelytohavelowersavingsrates?

CountryA CountryB

RealInterest Rate 3% 3%

InflationRate 1% 10%

NominalInterestRate 4% 13%

ReductioninNominalInterestfrom20%tax

4*0.2 =0.8% 13*0.2=2.6%

After-taxNominalRate

After-tax RealRate

204

FischerEffectandTaxesSupposeCountryAandCountryBbothsettaxesoninterestincometo20%.CountryA’sinflationis1%,CountryB’sinflationis10%.Completethefollowingtable:

Whichcountryislikelytohavelowersavingsrates?

CountryA CountryB

RealInterest Rate 3% 3%

InflationRate 1% 10%

NominalInterestRate 4% 13%

ReductioninNominalInterestfrom20%tax

0.8% 2.6%

After-taxNominalRate 4-0.8 =3.2% 13-2.6=10.4%

After-tax RealRate

205

FischerEffectandTaxesSupposeCountryAandCountryBbothsettaxesoninterestincometo20%.CountryA’sinflationis1%,CountryB’sinflationis10%.Completethefollowingtable:

Whichcountryislikelytohavelowersavingsrates?CountryB

CountryA CountryB

RealInterest Rate 3% 3%

InflationRate 1% 10%

NominalInterestRate 4% 13%

ReductioninNominalInterestfrom20%tax

0.8% 2.6%

After-taxNominalRate 3.2% 10.4%

After-tax RealRate 3.2% - 1%=2.2% 10.4% - 10%=0.4%

206

KeyTakeaways• Inflationimpactsinterestratesandthereforetherealvalueofmoney

• FischerEffecttellsusthatnominalrateswilladjustone-for-onetochanginginflation

• Highinflationisbadforsavers

207

Principles of MacroeconomicsModule 4.2 (C)

Quantity Theory of Money

Classical Dichotomy Referstotheseparationofnominalandrealvariables• NominalVariables: Measuredinmonetaryterms

Thepriceofanappleis$2Thepriceofabananais$1

• RealVariables:Measuredinphysicalunits(orrelativeterms)Thepriceofanappleis2bananasThepriceofabananais½apple

Changesinthemoneysupply– NominalchangesMonetaryNeutrality:Changesinthemoneysupplywillnotimpact

realvariables

The Velocity of MoneyVelocityofmoney:therateatwhichmoneychangeshandsNotation:P xY =nominalGDP

=(pricelevel)x(realGDP)M =moneysupplyV =velocity

Velocityofmoney: V = P x YM

QuantityEquation:M xV =P xY

Test your Understanding• IfthenominalGDPis$10,000andthemoneysupplyif$5,000,whatisthevelocityofmoney?

Test your Understanding• IfthenominalGDPis$10,000andthemoneysupplyif$5,000,whatisthevelocityofmoney?

• V=NGDP/MS• V=$10,000/$5,000• V=2

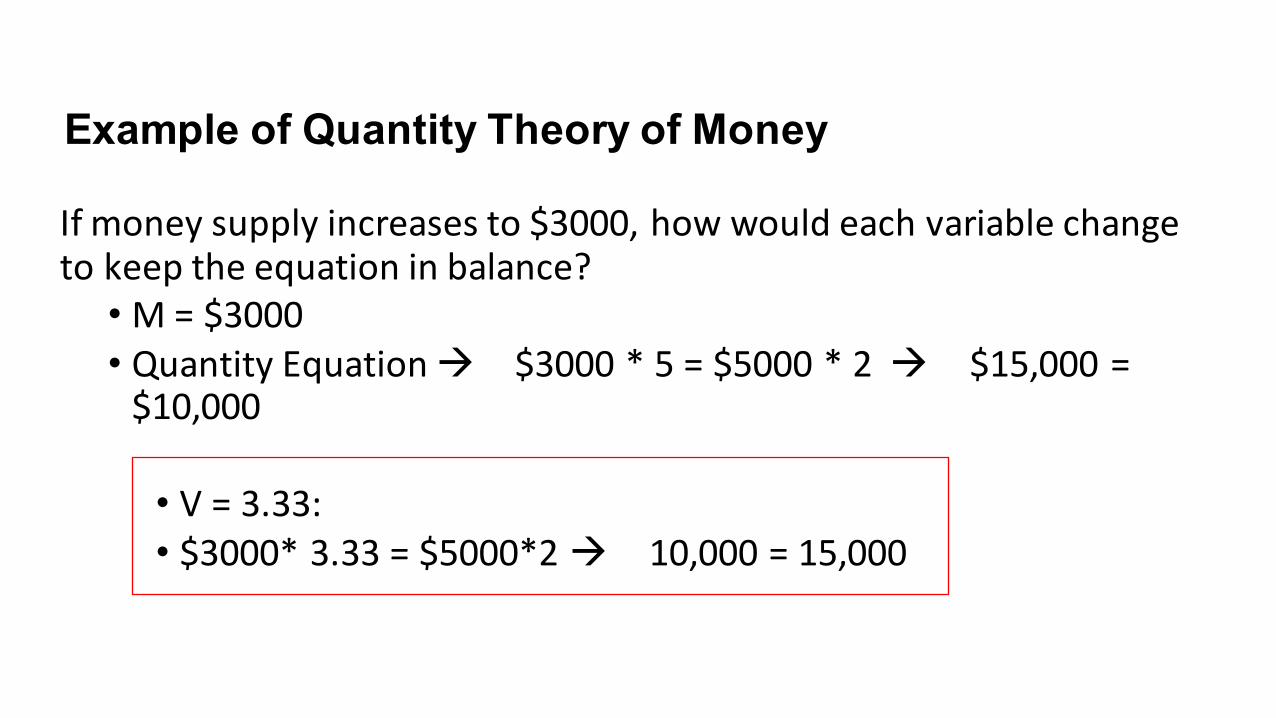

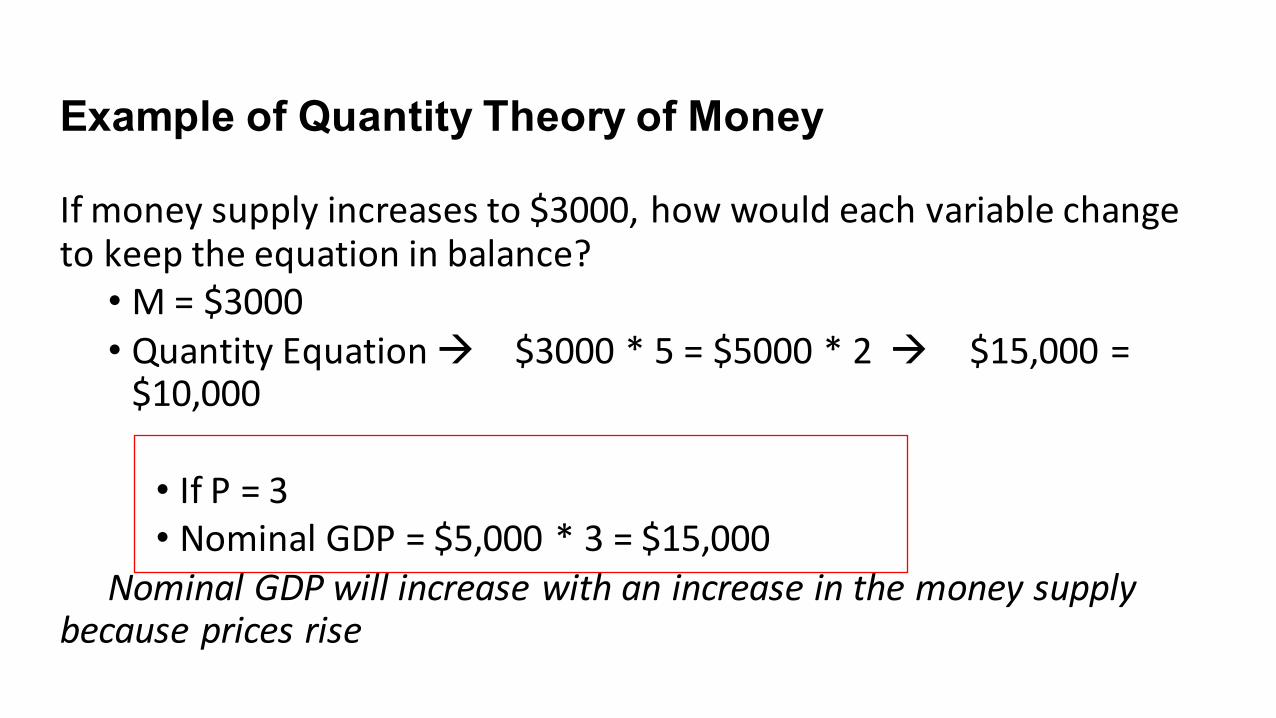

Example of Quantity Theory of MoneySupposewehavethefollowingvalues:Y=$5000;V=5;M=$2000;P=2

• QuantityEquationà MV=PY• $2000*5=$5000*2à $10,000=$10,000

Example of Quantity Theory of MoneySupposewehavethefollowingvalues:Y=$5000;V=5;M=$2000;P=2QuantityEquation=$10,000Ifmoneysupplyincreasesto$3000,howwouldeachvariablechangetokeeptheequationinbalance?•M=$3000• QuantityEquationà $3000*5=$5000*2à $15,000=/$10,000

Example of Quantity Theory of MoneyIfmoneysupplyincreasesto$3000,howwouldeachvariablechangetokeeptheequationinbalance?•M=$3000• QuantityEquationà $3000*5=$5000*2à $15,000=$10,000

• Y=7500:• $3000*5=$7500*2à 15,000=15,000

Example of Quantity Theory of Money

Ifmoneysupplyincreasesto$3000,howwouldeachvariablechangetokeeptheequationinbalance?•M=$3000• QuantityEquationà $3000*5=$5000*2à $15,000=$10,000

• V=3.33:• $3000*3.33=$5000*2à 10,000=15,000

Example of Quantity Theory of MoneyIfmoneysupplyincreasesto$3000,howwouldeachvariablechangetokeeptheequationinbalance?•M=$3000• QuantityEquationà $3000*5=$5000*2à $15,000=$10,000

• P=3:• $3000*5=$5000*3à 15,000=15,000

Pricesaretheonlyothernominalvariableinthisequation.Ifmoneysupplychanges,priceswilladjustaccordingly tokeepthequantityequationinbalance

Example of Quantity Theory of Money

Ifmoneysupplyincreasesto$3000,howwouldeachvariablechangetokeeptheequationinbalance?•M=$3000• QuantityEquationà $3000*5=$5000*2à $15,000=$10,000

• IfP=3• NominalGDP=$5,000*3=$15,000

NominalGDPwillincreasewithanincreaseinthemoneysupplybecausepricesrise

Key Takeaways

• Quantitytheoryofmoneyexplainsthatpriceswilladjusttobringmoneydemandandmoneysupplyintoequilibrium