private equity and real estate - eastnine abbusiness • kestutis sasnauskas founding partner, head...

TRANSCRIPT

Kestutis Sasnauskas, Partner and Head of Private Equity and Real Estate, East Capital

Private Equity and Real Estate

Private Equity

Gert Tiivas Head of Baltic Private Equity

Tallinn

• Estonian national • Chairman of Starman and Trev-2 • Previously CEO of East Capital

Explorer, Head of Growth Markets at NASDAQ OMX, and CEO of Tallinn Stock Exchange

• Bentley College, George Washington University

Julianna Sosnovska Senior Analyst

Stockholm

• Latvian national • Board member of FIA Bank • Previously at SEB • Fluent in English, Swedish,

Russian and Latvian • Stockholm University School of

Business

Kestutis Sasnauskas Founding Partner, Head of Private Equity and Real Estate

Stockholm

• Lithuanian national • Chairman of MFG and member of

several board of directors • Previously at Enskilda Securities • Fluent in Russian, Lithuanian,

English and Swedish • Stockholm School of Economics,

University of Vilnius

Margot Jacobs Senior Advisor

Stockholm

• American national • Board member of KBS, Macedonia • Previously at Charlemagne Capital

and United Financial Group • Fluent in English, Russian and

Swedish and Serbo-Croatian • Dartmouth College, George

Washington University

Hanna Loikkanen Senior Advisor

Moscow

• Finnish national • Member of several board of

directors in Russia • Previously at FIM Group in Russia

and Nordea across Eastern Europe • Fluent in English, Russian and

Finnish • Aalto University

Ekaterina Vasenina Senior Legal Counsel Moscow

• Russian national • Member of Board of Georgian

company • Previously at Interpipe Group,

Ukraine • Fluent in English and Russian • Moscow State University (Russia),

School of Law • Fordham University (USA), School

of Law 3

Lilia Kouzmina Senior Analyst

Stockholm

• Russian national • Previously within East Capital’s

public equity team, at Accenture and SITE

• Fluent in Russian, English and Swedish

• Stockholm School of Economics, Central European University

Stefano Grace Senior Legal Counsel

Tallinn

• American national • Board member of Siera Nams and

Real Estate investment vehicles • Previously General Counsel of East

Capital Explorer, Senior Associate at Sorainen, in-house Nasdaq OMX

• Fluent in English, conversational Estonian and Swedish

• University of Virginia, Florida State University

Private Equity Investment Team

4

Baltic Private Equity market on solid grounds

Supportive

investment climate

• Well-run public finances • Competitive tax regime • High level of transparency • Flexible labour market • Strong rule of law • Low political risk

Balanced economies

• Resilient economies • Quick recovery from crisis

driven by exports and domestic demand

• Highest GDP growth in EU • Increasing consumer

purchasing power • Inflation under control

Limited sources of financing

• Low competition for deals • Companies de-leveraging • Banks ready to finance only the

strongest companies and sponsors • Alternative financing limited

Opportunities

Melon Fashion Group

6

Exposure to fast growing market with vast potential through domestic market leaders with superior growth track record

The Melon Fashion Group investment case

• Exposure to the Russian consumer market

– Real disposable income growth drives consumer spending

– Fast developing but still non-saturated retail market allowing listed food retailers like X5, Magnit, Okey to grow at 30% per annum

• Exposure to attractive fast-growing retail segment

– Russian apparel market set to become one of the largest in Europe by 2017-2018

– Consolidation potential remains as top 10 retailers constitute only 12% of total market vs 49% in UK

– Russians spend more on apparel as % of income

• Exposure to one of largest domestic apparel retailers

– 2008-2014 selling space CAGR of 28%

– Focusing on regional expansion

– Supported by strong board and management team

Why we like apparel retail in Russia

8

Real disposable income growth fuels consumption

Low savings rate and consumer credit penetration contributes further to consumption growth

Source: Euromonitor

Consumption drivers in place

Growing disposable income growth boosting spending

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

450 000

Annual disposable income per capita, RUB Annual disposable income growth in %

Estimated by Euromonitor

9

Despite current slowdown Russia’s EUR 40bln (2012) apparel retail market set to grow long-term on rising disposable income and high fashion spend

Growing apparel retail segment

Clothing Retail Sales 2012 (USDbn)

0102030405060708090

100

Clothing Retail Sales per Capita 2012 (USD)

0%

1%

2%

3%

4%

5%

6%

7%

0

200

400

600

800

1000

1200

Clothing retail sales per capita, USD Spending on clothes as a% of income

Source: Euromonitor

10

By some forecasts Russian apparel market set to become second largest in Europe by 2017

On a way to become largest European market…

Russian apparel retail market size vs Europe total

Germany; 79; 20%

Italy; 66; 16%

UK; 59; 15%

Russia; 55; 14%

France; 50; 12%

Rest of Europe ; 90; 23%

2012 Apparel Market Europe, EUR bn

Total size EUR 309bn

Germany; 84; 15%

Russia; 81; 15%

Italy; 69; 13%

UK; 69; 12%

France; 53; 10%

Rest of Europe ; 196; 35%

2017E Apparel Retail Europe, EURbn

Total size EUR 355bn

CAGR 8.0%

Source: Market Line. *Apparel retail includes menswear, womenswear adn childrenwear

CAGR 2.8%

11

Shift from outdoor markets to shopping centers and online retailers with retail chains and online getting market share from unorganized retail

Consolidation still ahead

Market share by top 10 retailers still low by developed markets tandards

6%

Russia 2010

12%

Russia 2013

49%

UK 2013

Market formalization under way

28% 20%

17% 12%

54% 66%

2%

5% 8%

17%

Russia2010

Russia2012

Russia2013

China2012

UK2012

Other

Online Retailers

Chains/DepartmentStoresIndependent Retailers

Outdoor Markets

12

Untapped regional demand to be unlocked as shopping malls construction penetrates the regions

Shopping mall construction to facilitate further growth

Regional Breakdown of Shopping Mall Space, 2012

Moscow 24%

St. Petersburg 14%

4% 4%

4% 3% 3%

3% 3%

2%

Other 36%

MoscowSt. PetersburgKrasnodarEkaterinburgSamaraMoscow regionNizhny NovgorodOmskKazanRostov-on-DonOther

0

100

200

300

400

500

600

700

Norway Sweden Lithuania EU-27average

Poland Germany Russia Ukraine

Shopping Mall Space per 1,000 Inhabitants (sq m)

Why Melon Fashion Group?

13

14

One of the largest store networks in Russia

All brands among top 10 by number of stores

One of the largest and fastest growing players in Russian apparel retail…

One of the largest store networks in Russia as of Aug 2014

618

606

516

384

300

250

214

179

154

128

Gloria Jeans

O'STIN

Sela

Incity

Tvoe

befree

Zarina

Love Republic

Henderson

Mango

656 stores as of Sep 30 643

15

• Store Size: 100-470 sq m

• Concept: Teenagers’ brand

• Key Values: Happiness, youth, fashion, ease, price, colour

• Awareness: 70%

• Number of Stores: 259

• Number of Cities: 119

• Geographical Presence: Russia, Ukraine, Kazakhstan, Belarus

befree

• Store Size: 90-270 sq m

• Concept: ‘Real lady’ brand

• Key Values: Dignity, quality, service

• Awareness: 71%

• Number of Stores: 215

• Number of Cities: 99

• Geographical Presence: Russia

ZARINA

• Store Size: 100-370 sq m

• Concept: Fashion and style brand

• Key Values: Life, Personality, Sensuality, Femininity

• Awareness: 53%

• Number of Stores: 179

• Number of Cities: 76

• Geographical Presence: Russia, Ukraine, Kazakhstan

LOVE REPUBLIC

…with diverse brand portfolio

16

19

• 1926-1990

• In 1926 in Leningrad, a handicraft school for girls, opened in 1880, was converted into a manufacturer of women's clothing

• 1991-2001

• In 1991, the company was privatized and bought by its own employees, resulting in 400-500 shareholders

• Focus on outsourced production and wholesale of its own ZARINA collection

• In a few years, it opens Zarina stores in St Peterberg and thus starts a retail chain

• In 1996, the first foreign investment is made by the Swedish Kellerman family, engaged in apparel retail

• 2002-2007

• In 2002, East Capital buys a stake in the company

• In 2005, Melon Fashion Group is created and a young, ambitious team is put in place

• Shift from wholesale to retail, completed in 2009

• 2008-2011

• In 2008, East Capital Explorer makes its first investments

• A the beginning of the financial crisis, MFG’s strong financial position allows it to take advantage of the situation and expand, both organically and through two acquisitions

• 2012-

• Divestment of franchise brands and decision to focus on its own brands; befree, ZARINA and LOVE REPUBLIC

• MFG continues to pursue an aggressive organic expansion across Russia, and enter new CIS markets through franchise stores

“Early Days” Privatization Wholesale to Retail Expansion Focused Growth

… long and exciting history

17

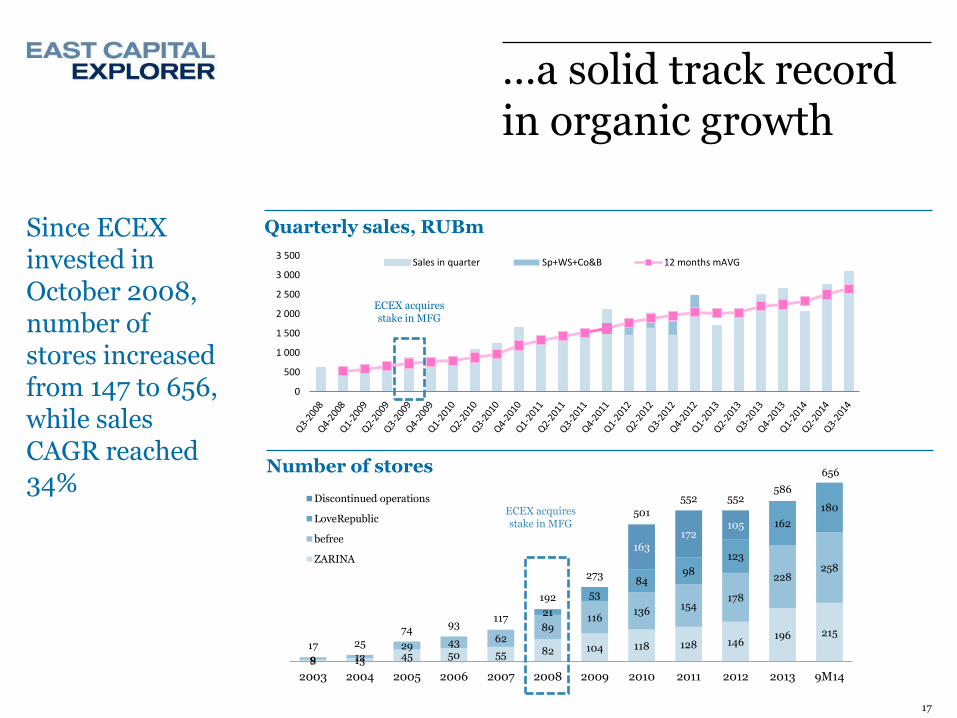

Since ECEX invested in October 2008, number of stores increased from 147 to 656, while sales CAGR reached 34%

…a solid track record in organic growth

Quarterly sales, RUBm

0

500

1 000

1 500

2 000

2 500

3 000

3 500Sales in quarter Sp+WS+Co&B 12 months mAVG

ECEX acquires stake in MFG

8 13 45 50 55 82 104 118 128 146 196 215

9 12 29 43 62

89 116

136 154

178

228 258

21

53

84 98

123

162

180

163 172

105

17 25

74 93

117

192

273

501

552 552 586

656

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 9M14

Discontinued operations

LoveRepublic

befree

ZARINA

ECEX acquires stake in MFG

Number of stores

…resulting in large geographic footprint from Ukraine to Far East

Number of stores as of 9M 2014

Own Retail Stores

Franchise Stores

Moscow Region

Kazakhstan

126 5

9

Center

105 46 Siberia

110 31

Far East

8

Belarus

2

Ukraine

22

South

68 10

North-West

92 19

MFG operates 656 stores in more than 110 cities in Russia and in Ukraine, Kazakhstan and Belarus

Own Retail Stores

Franchise Stores

19

Own retail space expanded at CAGR of 27% since 2008

Regional focus dominates recent years expansion

…and continuously expanding regional reach

Added stores by region, 9M 2014

Own Retail Stores, Net of Closed Stores

11

1

7

11

6

18

7 10

20

10

19 19 21

30

15 12

1 3

16 19

MoscowRegion

South North-West Siberia Center

2011

2012

2013

9M14

CAGR 2008-14

27%

37%

20%

29%

22 229 31 694

41 735 47 377

54 943

77 235

93 490

42,6%

31,7%

13,5% 16,0%

40,6% 38,0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

20000

40000

60000

80000

100000

2008 2009 2010 2011 2012 2013 9M2014befree ZARINA LOVE REPUBLIC Space Growth (%), yoy

Own Retail Selling Space (sq m)

20

• David Kellerman, Chairman

– Entrepreneur and shareholder in MFG

• Kestutis Sasnauskas

– CEO, East Capital partner

• Lennart Dahlgren

– Independent retail consultant, Former CEO of IKEA Russia

• Claes Heurlin

– Independent consultant with 20 years experience from fashion industry including H&M and R&B

• Christel Kinning

– Chairman of the Board of Directors of Zoundindustries International AB, Board member in Stadium, Hemtex, Reima, Hope

• Mathias Pedersen

– CFO East Capital AB

• Mikhail Urzhumtsev

– Former CEO of the group

Broad retail competence and industry experience

…supported by strong Board of Directors

Board of Directors

21

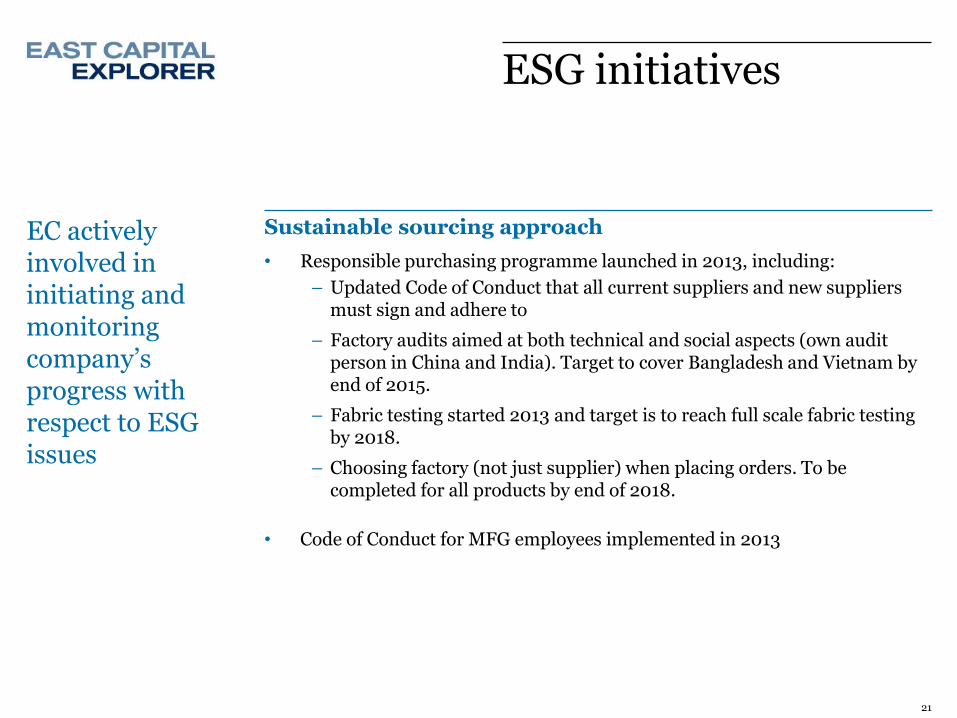

• Responsible purchasing programme launched in 2013, including:

– Updated Code of Conduct that all current suppliers and new suppliers must sign and adhere to

– Factory audits aimed at both technical and social aspects (own audit person in China and India). Target to cover Bangladesh and Vietnam by end of 2015.

– Fabric testing started 2013 and target is to reach full scale fabric testing by 2018.

– Choosing factory (not just supplier) when placing orders. To be completed for all products by end of 2018.

• Code of Conduct for MFG employees implemented in 2013

EC actively involved in initiating and monitoring company’s progress with respect to ESG issues

ESG initiatives

Sustainable sourcing approach

22

…but external environment puts pressure even on strongest players….

Massive RUB devaluation since beginning of 2014

20

25

30

35

40

45

50

55

60

65

70

Ja

n-0

3

Ju

n-0

3

No

v-0

3

Ap

r-0

4

Sep

-04

Feb

-05

Ju

l-0

5

De

c-0

5

Ma

y-0

6

Oct

-06

Ma

r-0

7

Au

g-0

7

Ja

n-0

8

Ju

n-0

8

No

v-0

8

Ap

r-0

9

Sep

-09

Feb

-10

Ju

l-10

De

c-10

Ma

y-1

1

Oct

-11

Ma

r-12

Au

g-1

2

Ja

n-1

3

Ju

n-1

3

No

v-1

3

Ap

r-14

Sep

-14

RUB USD RUB EUR

23

Real disposable income dipped to 2009 lows in 1Q14 taking a hit from accelerating inflation and FX effects

…but external environment puts pressure even on strongest players, cont.

Real disposable income growth, %

-10,0

-5,0

0,0

5,0

10,0

15,0

20,0

%

-10,0

0,0

10,0

20,0

30,0

40,0real wage growth, yoy nominal wage growth

Nominal and real wage growth, %

%

24

Nevertheless consumer confidence is not anywhere near 2009 levels indicating still relatively healthy consumer

Non-food retail sales growth slowed as weak RUB and accelerating inflation makes consumers cautious

…resulting in temporal consumer weakness

-15,0

-10,0

-5,0

0,0

5,0

10,0

15,0

20,0

25,0

%

Non-food retail sales growth, %

Consumer confidence index

-40

-35

-30

-25

-20

-15

-10

-5

0

5

Source: Rosstat

RUR million 2011 2012 2013 9M2014 Sales 5 103 7 061 8 966 7923 EBITDA 260 1 023 902 (231) Net Profit 50 687 630 (427)

Sales Growth (%) 27.9% 38.3% 27.0% 26.0% Gross Margin (%) 59.7% 60.9% 58.8% 53% EBITDA Margin (%) 5.1% 14.5% 10.1% (3%) Net Margin (%) 1.0% 9.7% 7.0% (5%)

Incl. discontinued operations

Cash Flow From Operations (92) 753 351 (270) Free Cash Flow (277) 564 (101) (392) Net Interest-bearing Debt 187 (387) (258) 395

25

Profitability plunged on RUB devaluation and high expansion cost leverage

…profitability suffered when macro weakened

MFG income statement

EBITDA by brand and space growth (RUBm)

-400

-200

0

200

400

600

800

1 000

1 200

2008 2009 2010 2011 2012 2013 9M2014

Discontinuedoperations

LOVE REPUBLIC

ZARINA

befree

space growth

42,6%

31,7%

13,5% 16,0%

40,6% 38,0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

0

0

0

0

1

1

1

1

1

1

26

• Operations

– Renegotiation of rental agreements

– Implementation of comprehensive “store profitability” project

– Implementation of flexible working schedule

– Implementation of new remuneration structure with profitability driven KPIs

• Product

– Higher flexibility in purchasing budget planning to achieve lower reduction rate

– Assortment consolidation to decrease fashion risk

– Reinforcement of product team with new competence to drive product improvement

Internal initiatives to drive cost efficiencies and ensure product improvement

Core drivers remain in place despite short-term weakness

How to deal with market weakness?

Focus on driving internal efficiencies and tight budgeting

27

Main Risks

• Macro / political risks

– The continuing Crimea /Ukraine crisis may lead to escalation of sanctions from both sides effecting economic activity and leading to deepening geopolitical instability. In the long term, increasing political instability and geopolitical tensions may lead to increasing isolation of the country hampering economic growth and effecting growth of real disposable income and individual consumption.

– Further drop in oil price resulting in recessionary trends instigated by budgetary pressures resulting in decrease in real disposable income

• Market & Industry -specific risks

– Delays in planned shopping center openings may adversely effect MFG’s expansion plans

– Weakening RUB may further adversely impact profitability due to USD/EUR denominated sourcing costs.

– Weakening profitability may put constraints on bank borrowing and FX hedging

– Increasing competition from new entrants and current local players may lead to market share loss

• Company-specific risks

– High fashion content implies high risk in terms of company’s ability to be able to offer attractive collections at all times. Failed collections lead to higher reduction rates and decrease in profitability

28

Devaluation of ruble may raise demand for cheaper clothes by domestic producers

Competition for attractive locations may ease in the short-term

Media reports on River Island, Esprit, Seppälä closing stores in Russia

Source: Rosstat

…and not to forget about opportunities

Clothes import growth yoy, %

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

mar

-06

jul-

06

no

v-0

6

mar

-07

jul-

07

no

v-0

7

mar

-08

jul-

08

no

v-0

8

mar

-09

jul-

09

no

v-0

9

mar

-10

jul-

10

no

v-1

0

mar

-11

jul-

11

no

v-1

1

mar

-12

jul-

12

no

v-1

2

mar

-13

jul-

13

no

v-1

3

mar

-14

jul-

14

Baltic Real Estate - Stable cash flow and strong outlook

30

MADIS RAIDMA – Head of Baltic Real Estate unit – Tallinn

CEO of East Capital Baltics AS

Joined East Capital in 2008

More than 13 years of experience in banking, corporate finance and investment management

ULF SIGFRIDSSON – Senior Advisor – Stockholm

More than 20 years of experience in banking, capital markets and corporate finance, including 10 years at Citibank in London

Former Deputy Managing Director of Orc Software AB

MARTIN OTSA – Investment Manager – Tallinn

Country asset manager – Estonia

Joined East Capital in 2008

More than 13 years experience in real estate including valuation, leasing, project development and investment management

Real Estate Management team

Local management team with a hands-on approach supported by a network of experienced advisors, analysts, finance- and legal team

East Capital Real Estate offices

JULIUS NIEDVARAS – Country Asset Manager – Lithuania

Joined East Capital in 2007

More than 15 years experience in real estate including project development, investment management, leasing, valuation and services outsourcing

Formerly general director of SEB real estate in Lithuania

MARIS SMILTENIEKS – Country Asset Manager – Latvia

Joined East Capital in 2006

More than 7 years experience in commercial real estate including acquisitions and property management, Former senior investment consultant in ARCO REAL ESTATE

KESTUTIS SASNAUSKAS – Founding Partner, Head of Private Equity and Real Estate – Stockholm

Chairman of MFG and member of several board of directors

More than 10 years of experience in private equity, M&A and corporate finance in Russia and Baltic States

Previously at Enskilda Securities

31

Domestic consumption drives Baltic growth

Source: Colliers, Eurostat

-2%

0%

2%

4%

6%

8%

10%

12%GDP growth

Estonia

Latvia

Lithuania

EU28

-1%0%1%2%3%4%5%6%

Harmonized Consumer Price Index

Estonia

Latvia

Lithuania

EU28

0%

5%

10%

15%

20%Unemployment rate

Estonia

Latvia

Lithuania

EU28

Wage growth drives domestic consumption

Modest inflation

Unemployment still high but decreasing

32

Latvia’s GDP growth was the fastest in the EU in 2013

Q2 y-o-y growth ranged between 2.4% and 3.3% for the Baltic countries

Average growth in the Baltics 2014-2018 expected to be in line with or better than Advanced economies and the Euro zone

GDP growth in the EU in 2013

Baltics among the fastest growing EU economies

Source: Eurostat / IMF

-6,0

-5,0

-4,0

-3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

4,0

La

tvia

Ro

ma

nia

Lit

hu

an

ia

Ma

lta

Lu

xe

mb

ou

rg

Un

ite

d K

ing

do

m

Po

lan

d

Sw

ed

en

Hu

ng

ary

Bu

lga

ria

Slo

va

kia

Est

on

ia

De

nm

ark

Ge

rma

ny

Bel

giu

m

Fra

nce

EU

28

Irel

an

d

Eu

ro a

rea

Net

he

rla

nd

s

Cze

ch R

epu

bli

c

Cro

ati

a

Slo

ven

ia

Sp

ain

Fin

lan

d

Po

rtu

ga

l

Ita

ly

Gre

ece

Cy

pru

s

%

33

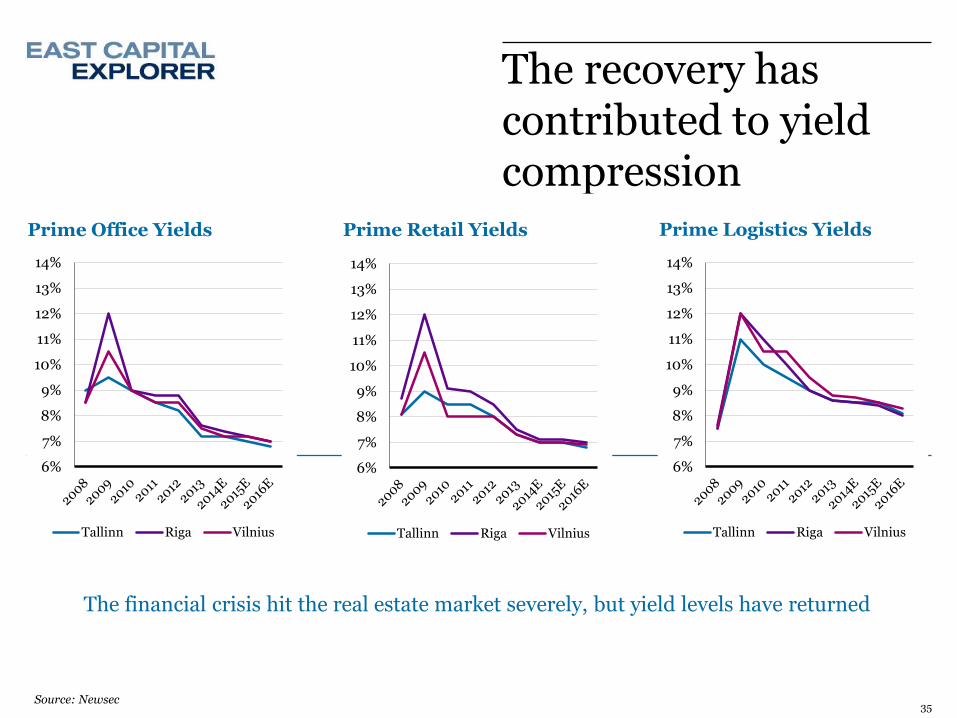

Yields in the Baltics have a premium of 200-300 bps vs the Nordic region in all segments

Source: Newsec

Prime yields still high compared to Nordic capitals

Capital growth index

34

Nordic property segments are 20-50% higher since pre-crisis levels

Baltic property segments are just back to same level (retail & logistics) or slightly below (office)

Source: Newsec

The recovery has contributed to yield compression

Source: Newsec

Prime Office Yields Prime Logistics Yields Prime Retail Yields

6%

7%

8%

9%

10%

11%

12%

13%

14%

Tallinn Riga Vilnius

6%

7%

8%

9%

10%

11%

12%

13%

14%

Tallinn Riga Vilnius

6%

7%

8%

9%

10%

11%

12%

13%

14%

Tallinn Riga Vilnius

The financial crisis hit the real estate market severely, but yield levels have returned

35

Decreasing vacancies and increasing rents provides attractive prospects

Source: Colliers, Newsec

Vacancy Offices Class A Vacancy Shopping Centers

Prime Office Rents (€ / sqm / year)

0

100

200

300

400

500

600

700

StockholmTallinnVilnius

0%

5%

10%

15%

20%

Estonia (Tallinn)

Latvia (Riga)

Lithuania(Vilnius)0%

2%

4%

6%

8%

10%

12%

Estonia (Tallinn)

Latvia (Riga)

Lithuania (Vilnius)

Rent levels still low compared to rest of Europe

36

37

Active investment market

Source: Colliers, DTZ

Asset managers, AUM in the Baltics Transaction volumes

0

50

100

150

200

250

300

Ea

st C

ap

ita

l

Eft

en

Ca

pit

al

No

rth

ern

Ho

rizo

nC

ap

ita

l (B

PT

)

Ca

pit

al

Mil

l

Lo

rds

LB

Ge

neb

a(H

om

bu

rg)

Ka

we

gro

up

EUR m

0

200

400

600

800

1000

1200

2006 2007 2008 2009 2010 2011 2012 2013 2014IHY

EUR m

Lithuania

Latvia

Estonia

Our Real Estate Portfolio

39

High quality commercial properties in the Baltic capitals

ESTONIA

LATVIA

LITHUANIA

Tallinn Tänassilma Logistics (BPFII) Rimi Logistics (BPFII) Metro Plaza (BPFII)

Vilnius Vilnius Business Harbour (DI) GO 9 Shopping Center (BPFII)

Riga Deglava Prisma (BPFII)

Strong cash flow and solid performance

NAV BPF II +26% since launch

90,0

100,0

110,0

120,0

130,0

•Yield levels 7-9%

Yields

•60-70%

Gearing

•Around or below 3%

Interest rates

•ROE target 15-20% (currently 16.5%)

Return on Equity

Real Estate portfolio’s key characteristics

40