private equity, infrastructure funds workshop equity, infrastructure funds seminar •chancen &...

TRANSCRIPT

Private Equity, Infrastructure Funds Workshop

Private Equity, Infrastructure Funds Seminar•Chancen & Auswirkungen auf die operativen Set-ups•Neue Vertriebsmodelle•Bewertung

Moderator: Gilbert Schintgen, CEO, UBS Fund Management (Luxembourg) S.A.

Panélistes: Marc Dellmann, Managing Director, UBS Global Asset Management, ZurichGilles Dusemon, Partner, Arendt & Medernach, LuxembourgChristian Hertz, Managing Associate, Linklaters LLP, LuxembourgJean-Christian Six, Partner, Allen & Overy, Luxembourg

The USD 57 trillion challenge

Source: OECD, IHS Global Insight, IEA, Mc Kinsey Global Institute January 2013.

Roads Rail Ports Airports Power Water Telecom Total

16.64.5 0.7

2.0

12.2

11.7

9.5 57.3Estimated infrastructure investment requirements 2013 – 2030 USD 57 trillion or approximately 3.5% of global GDP

Infrastructure investment needs meet limited government budgets

4

Definition• Physical facilities and structures necessary for the functioning of an economy

• Real assets providing essential services

• Often monopolies and regulated sectors with high barriers to entry

Sectors

Energy & Utilities Transport Communication PPP

Characteristics

Investor requirements Purpose

• Stable cash flows • Coverage of regular liabilities and liquidity needs

• Recession resilience • De‐correlated performance relative to GDP• Protection of wealth in recession phases

• Inflation protection • Preservation of purchasing power

Investment considerations for a diversified infrastructure exposure

Real assets for the functioning of any economy

5

Infrastructure"Filling the financing gap"

Private Equity"Owning and investing into companies"

Investment rationale Realizing cash yields Realizing capital gains

Investment universe 140 GPs, annual fundraising of USD 20‐30 billion 1'800 GPs, annual fundraising of USD 300‐400 billion

Investment horizon >10 years <10 years

Segmentation Energy and Utilities Transport Venture Growth

Communication Social Buyout Special Situation

Value generation Contractual fees Inelastic demand Top line growth Bottom line growth

Financing gap Inflation linked tariffs Multiple expansion Leverage

Risks Illiquidity Illiquidity

Event specific (political / regulatory)Asset specific (environmental / operational)Stage specific (brownfield / Greenfield)

Manager specific (skill / operational / style drift)Market specific (access to debt / IPO activity)

Asset class characteristics

Infrastructure and Private Equity

6

18% 22%

36%

31%

46%

39%

51%

32%25%

0%

25%

50%

75%

100%

1980s 1990s 2000s 2010s

Source: Thomson Reuters, Buyout funds; S&P; as of January 2012 UBS database: Strategy composite performance for all vintages including 2009 per December 31st 2012.

Operational improvement as main value driver in low growth environment

Private equity value drivers: development over time

Operational improvement

Multiplearbitrage

Leverage

Changing value drivers in the private equity place

7

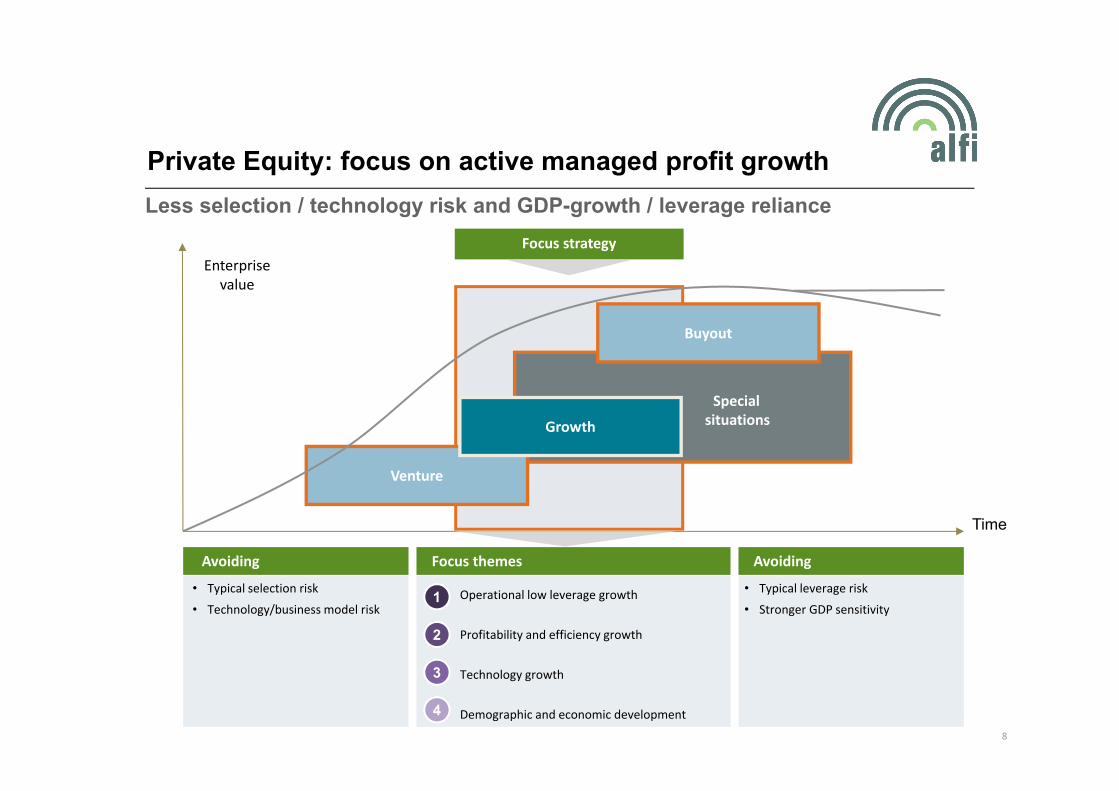

Private Equity: focus on active managed profit growth

Avoiding Focus themes Avoiding

• Typical selection risk

• Technology/business model riskOperational low leverage growth

Profitability and efficiency growth

Technology growth

Demographic and economic development

• Typical leverage risk

• Stronger GDP sensitivity

Less selection / technology risk and GDP-growth / leverage reliance

4

2

3

Enterprisevalue

Time

Special situations

Venture

Buyout

Growth

Focus strategy

1

8

Adding different asset classes to a pension fund portfolio

Schematic diagram. Source: UBS Global Asset Management Global Investment Solutions team, time horizon: 5 years. Investments in Infrastructure (unlisted Brownfield infrastructure,globally diversified) and Private Equity have been modelled without currency fluctuations. Figures as of January 2013.Risk is indicated as volatility of returns in percent. However, volatility is not the only relevant measure of risk. Further measures of risk which can be drawn on are e.g., the maximum loss(drawdowns), the corresponding length of the recovery period as well as situations of extreme market turbulences / turmoils (analysed with stress test scenarios).There is no guarantee on the side of UBS Global Asset Management that these projected returns can be achieved and are for indicative purposes only

Expe

cted

ann

ual r

etur

n ov

er a

5 y

ear i

nves

tmen

t hor

izon

Expected risk p.a.

+ 10% Global Bonds

+ 10% Infrastructure

+ 10% Infrastructure

+ 10% Private Equity

+ 10% Private Equity

+ 10% Global Equities

Pension FundPortfolio

Infrastructure and Private Equity in a portfolio context

9

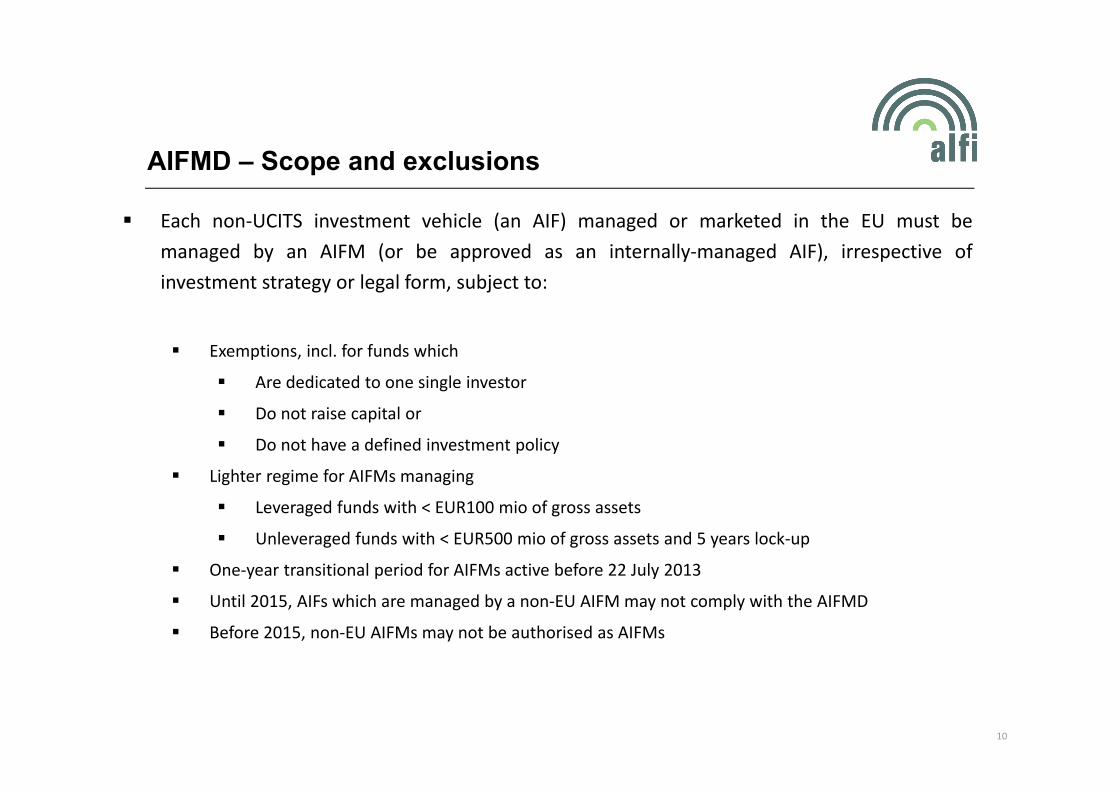

AIFMD – Scope and exclusions

Each non‐UCITS investment vehicle (an AIF) managed or marketed in the EU must bemanaged by an AIFM (or be approved as an internally‐managed AIF), irrespective ofinvestment strategy or legal form, subject to:

Exemptions, incl. for funds which

Are dedicated to one single investor

Do not raise capital or

Do not have a defined investment policy

Lighter regime for AIFMs managing

Leveraged funds with < EUR100 mio of gross assets

Unleveraged funds with < EUR500 mio of gross assets and 5 years lock‐up

One‐year transitional period for AIFMs active before 22 July 2013

Until 2015, AIFs which are managed by a non‐EU AIFM may not comply with the AIFMD

Before 2015, non‐EU AIFMs may not be authorised as AIFMs

10

11

A. Minimum share capital and own funds requirements Minimum initial share capital = ‐ EUR125k for an AIFM

‐ EUR300k for an internally‐managed AIF Additional own funds requirements

B. Operating conditions and organisational requirements Procedures and policies Human and technical resources (proportionality principle)

Conducting officers requirement

Establishment of a Lux AIFM – Key requirements

Market update – PE funds

Success of SIF and SICAR vehiclesNumber of units investing in private equity and unlisted securities

Source: CSSF

Origin of General Partnersbased on # of SICARs

Source: CSSF annual report 2011Luxembourg

9%

Fund administrators and banks are building up their PE servicing capacities:

Global players /banks Independent fund administration players

12

The PE fund toolbox - Snapshot on structures

SIF / SICARDirect Funds

Umbrella Funds

SIF / SICAR

PE‐FundsPE‐FundsFundsFunds

Master‐Feeder

SIF / SICAR

PE FundsPE Funds PE FundsPE Funds PE FundsPE Funds

Funds of Funds

SIF / SICAR

SF1 SF2 SF3

13

The PE fund toolbox - Latest updates and innovations

The New Luxembourg Limited Partnership

What are the objectives?

To follow in the tracks of the English/Scottish LP regimes

To promote a single jurisdiction for capital raising and investment structuring

To ensure tax transparency

14

The PE fund toolbox - Latest updates and innovations

Modernization of current LP structure (S.C.S.) and creation of new LP structure with no legal personality (S.C.sp.)

Tax transparent (no corporate income or wealth tax)

Not subject to Luxembourg trade tax if GP < 5% of partnership interests

New flexible provisions relating to management

Contractual freedom

Confidentiality

AIF (SIF)

Optional: SPV

Investments

SOPARFI

Investments

Luxembourg Limited Partnership

Investors

FundS.C.S. / S.C.sp.

GPInvestment Adviser

15

Tax update – Snapshot: PE acquisition structuring

Hybrids

Shareholder loans

Bank Loans

SOPARFI structures

Lux HoldCo / BidCo

Investments

AIF

SOPARFI

Leading structuring hub:

Short time to market Proven track record

Tax efficiency:

In general, dividend and capital gains tax exemption available based on domestic regulations Efficient taxation structuring leads to reduced or no

withholding tax on redemption of hybrids, liquidation proceeds and interest payments

Efficient capital structure:

Low gross margin on financing activities (to be confirmed by the tax authorities in view of the amounts and risks taken)

Management

BANK

16

Tax update – Snapshot: PE fund structuring

All asset classes/strategies

No WHT No taxation at Fund level 1bp levy on NAV for SIF only

Minimum tax leakage on capital gains and income

End investor usually achieves same result as direct investment

EU Directives and DTT access No or optimally reduced WHT Certainty around tax exposure

AIF (SIF)

Optional: SPV

FUN

D S

TRU

CTU

RE

SPV

Investments

Optional: SOPARFI

Investments

PE fund structures

Investors

SIF / SICAR

17

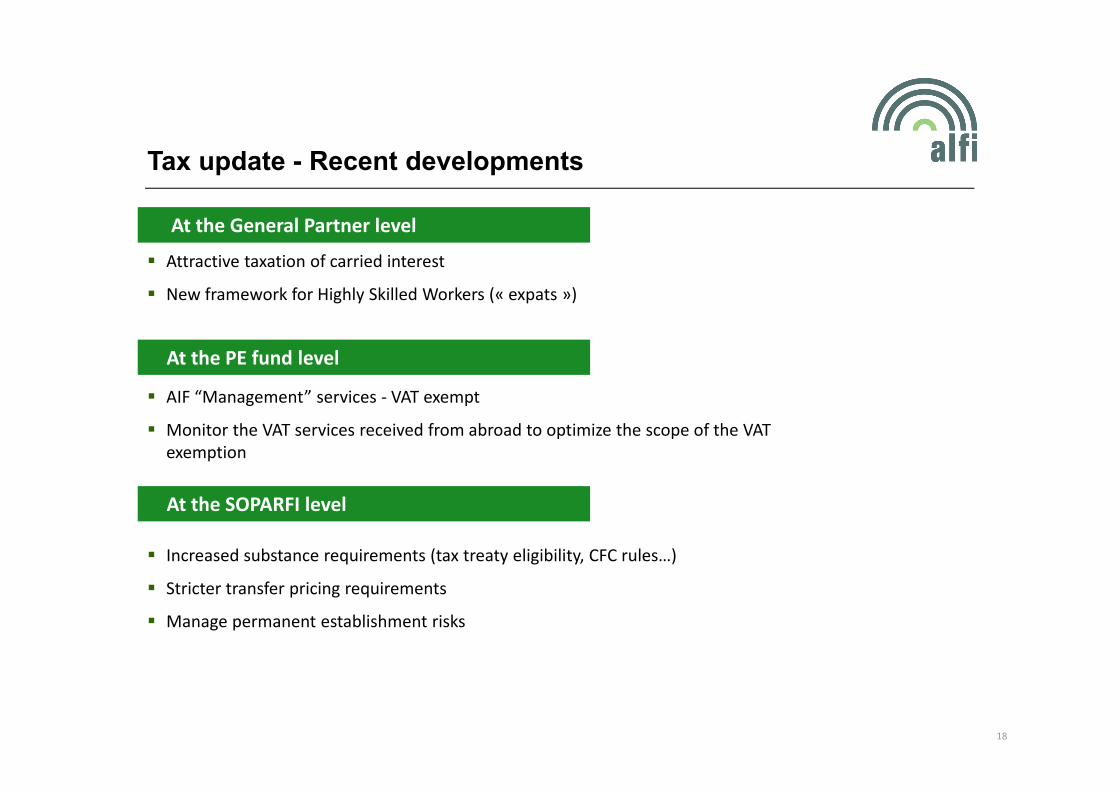

Tax update - Recent developments

Attractive taxation of carried interest

New framework for Highly Skilled Workers (« expats »)

At the General Partner level

Increased substance requirements (tax treaty eligibility, CFC rules…)

Stricter transfer pricing requirements

Manage permanent establishment risks

At the PE fund level

At the SOPARFI level

AIF “Management” services ‐ VAT exempt

Monitor the VAT services received from abroad to optimize the scope of the VAT exemption

18

1. Option 1: Fund appoints Swiss manager as AIFM and avoids AIFMD compliance

Swiss manager must be authorised as an asset manager by the FINMA

Investment decisions are taken by the Swiss manager

Swiss manager may appoint one ore more investment adviser(s)

Fund does not benefit from AIFMD passport and marketing within the EU must be made on the basis of local PPRs

Transitional exemption from the AIFMD expected to be waived as from 2015

19

FUND (SCA)

Swiss AIFM

GP (Sàrl)

Structuring options – Swiss manager / Lux PE fund.1

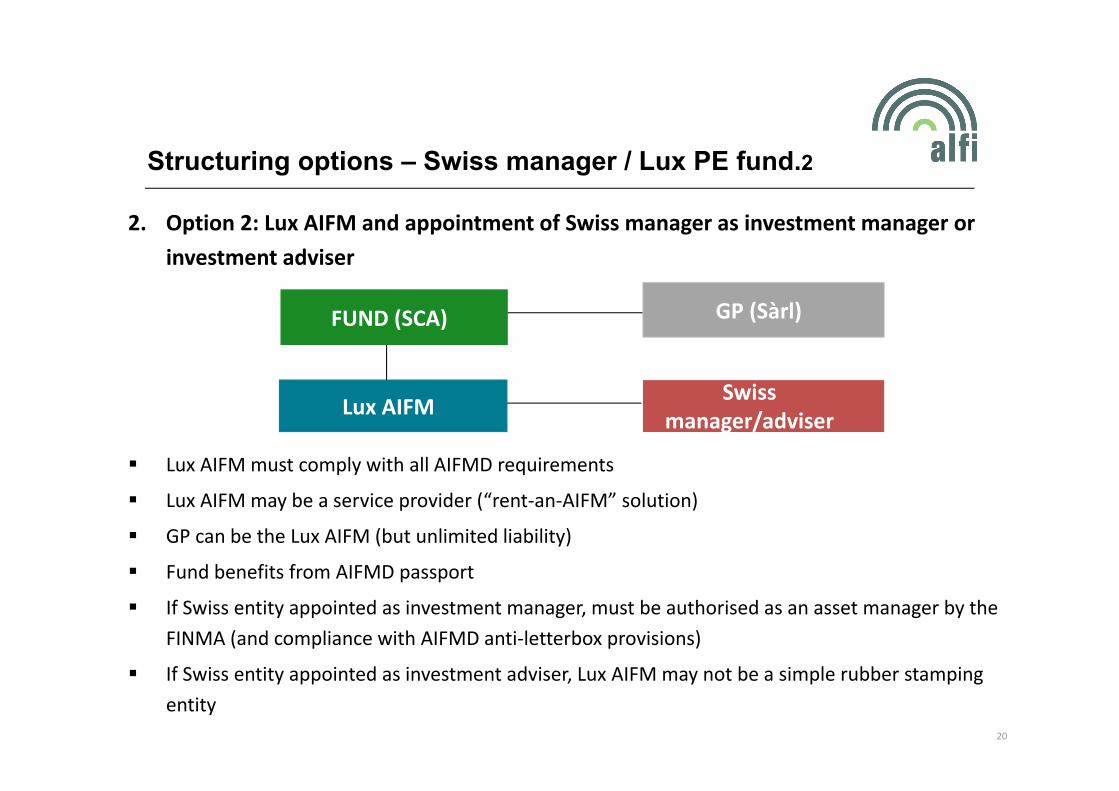

2. Option 2: Lux AIFM and appointment of Swiss manager as investment manager or investment adviser

Lux AIFM must comply with all AIFMD requirements

Lux AIFM may be a service provider (“rent‐an‐AIFM” solution)

GP can be the Lux AIFM (but unlimited liability)

Fund benefits from AIFMD passport

If Swiss entity appointed as investment manager, must be authorised as an asset manager by the FINMA (and compliance with AIFMD anti‐letterbox provisions)

If Swiss entity appointed as investment adviser, Lux AIFM may not be a simple rubber stamping entity

20

Swissmanager/adviserLux AIFM

Structuring options – Swiss manager / Lux PE fund.2

FUND (SCA) GP (Sàrl)

Peru: 64%

Chile: 73%

Sweden: 71%

Germany: 67%

France: 70%Switzerland: 70%

Bahrain: 76%

Singapore: 71%

South Korea: 100%Japan: 61%

Taiwan: 75%Hong Kong: 73%

Distribution options …the big picture

Private Placement Mapping

14

Limited market access

Barriers to market

Private placement

13

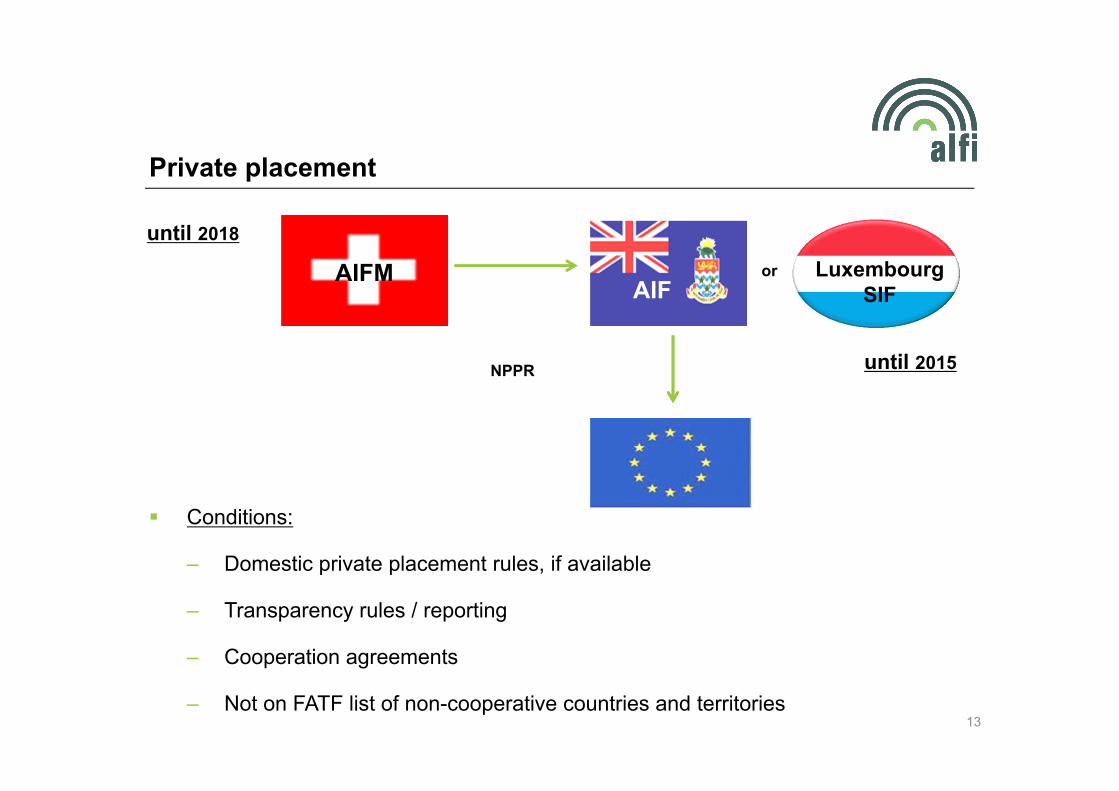

Conditions:

– Registered (small) Luxembourg AIFM (not authorized)

– Domestic private placement rules, if available

until 2018

AIFAIFM Luxembourg

SIF

NPPR

Registered AIFM

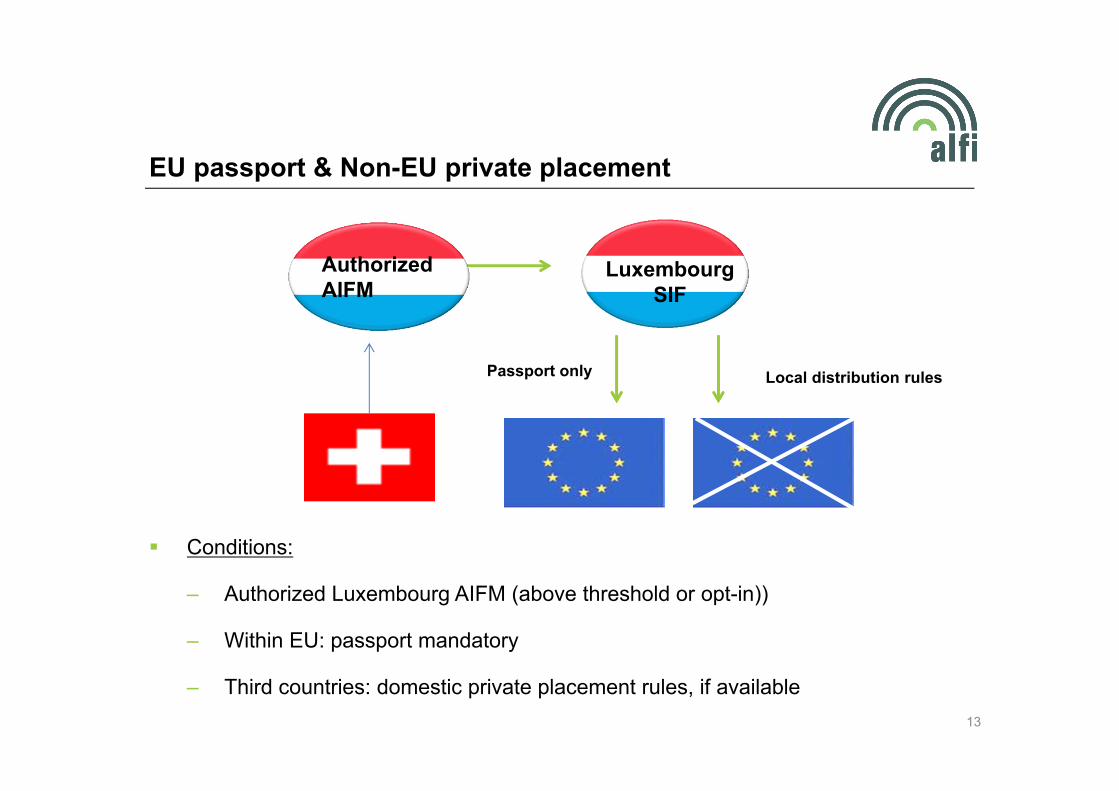

EU passport & Non-EU private placement

13

Conditions:

– Authorized Luxembourg AIFM (above threshold or opt-in))

– Within EU: passport mandatory

– Third countries: domestic private placement rules, if available

AIFAIFM Luxembourg

SIF

Passport only

Authorized AIFM

Local distribution rules

Private placement

13

Conditions:

– Domestic private placement rules, if available

– Transparency rules / reporting

– Cooperation agreements

– Not on FATF list of non-cooperative countries and territories

until 2018

AIForAIFM Luxembourg

SIF

NPPR until 2015

Third country passport

15

AIFM

AIF

EU AIF 2015 = subject to confirmation

Conditions:

– At AIFM level: full AIFMD compliance; for Non-EU AIFM: additional conditions (MSR)

– At AIF level:

– cooperation agreements

– not on FATF list

– Article 26 of OECD Model Tax Convention

– Stricter rules possible on a country by country basis

via passportor

As of 2015

Thank you for attending!