procredit nvb angola 2006

DESCRIPTION

Annual Report 2006 NovoBanco Angola ProCredit NetworkTRANSCRIPT

An

nual

Rep

ort2

006

Ango

la

Annu

alR

epor

t200

6

An

gola

AnnualReport2006

Key Figures

USD ’000 2006 2005* Change Balance Sheet Data TotalAssets 14,055 7,763 81%GrossLoanPortfolio 7,583 4,367 74% BusinessLoanPortfolio 7,566 4,367 73% USD<10,000 5,163 2,723 90% USD>10,000<50,000 2,403 1,646 46% USD>50,000<150,000 – – – USD>150,000 – – – AgriculturalLoanPortfolio – – – HousingLoanPortfolio – – – Other 417 947 -56%AllowanceforImpairmentonLoans -489 -156 213%NetLoanPortfolio 7,094 4,163 70%LiabilitiestoCustomers 7,405 2,718 172%LiabilitiestoBanksandFinancialInstitutions 996 – –Shareholders’Equity 4,987 4,914 1%

Income Statement OperatingIncome 3,109 1,122 177%OperatingExpenses 3,066 1,357 126%OperatingProfitBeforeTax 43 -235NetProfit 43 -235

Key Ratios Cost/IncomeRatio 89.1% 106%ROE 0.4% -4.9%CapitalRatio 51.2% 83%

Operational Statistics NumberofLoansOutstanding 2,307 1,093 111%NumberofLoansDisbursedwithintheYear 2,839 1,365 108%NumberofBusinessandAgriculturalLoansOutstanding 2,305 1,093 111%NumberofDepositAccounts 23,661 11,169 112%NumberofStaff 115 49 135%NumberofBranchesandOutlets 3 2 50%

* Some figures differ slightly from those in the 2005 an-nualreportastheyhavebeenadjustedtoreflectnewcalcu-lationmethods.

A n n u a l R e p o r t 2 0 0 6�

Key Figures

MissionStatement 4

LetterfromtheBoardofDirectors 5TheBankanditsShareholders 6

TheProCreditGroup–NeighbourhoodBanksforOrdinaryPeople 8ProCreditinAfrica 10

TheYearinReview 14

ManagementBusinessReview 16

SpecialFeature 23 RiskManagement 24

BranchNetwork 26Organisation,StaffandStaffDevelopment 28BusinessEthicsandEnvironmentalStandards 29

OurClients 30

FinancialStatements 34

ContactAddresses 43

C o n t e n t s �

Mission StatementMission Statement

NovoBanco Angola is a development-oriented full-service bank. We offer excellent cus-

tomer service and a wide range of banking products. In our credit operations, we focus

on lending to very small, small and medium-sized enterprises, as we are convinced that

these businesses create the largest number of jobs and make a vital contribution to the

economies in which they operate.

Unlike other banks, our bank does not promote consumer loans. Instead we focus on

responsible banking, by building a savings culture and long-term partnerships with our

customers.

Our shareholders expect a sustainable return on investment, but are not primarily inter-

ested in short-term profit maximisation. We invest extensively in the training of our staff

in order to create an enjoyable and efficient working atmosphere, and to provide the

friendliest and most competent service possible for our customers.

M i s s i o n S tat e m e n t�

Mission StatementMission Statement

At NovoBanco Angola we believe in the value of consistently applying our unique approach to banking and to customer service. We are proud that, despite growing competition in the Angolan banking sector, we upheld our target-group focus and our commitment to responsible lending.

NovoBanco’s rapid expansion in 2006 demonstrates that the public values its innovative banking prod-ucts and customer-oriented account services. In line with its neighbourhood banking concept, NovoBanco launched a savings campaign aimed at children, the first of its kind in Angola. The campaign, supported by UNDP and Chevron, was very well received.

Although still a relatively young institution, NovoBanco is increasingly recognised by national policy- makers and international institutions as Angola’s market leader for small business finance. In 2006, NovoBanco’s second full year of operations, the bank nearly doubled its loan portfolio and more than doubled its deposit base. It disbursed over USD 14 million in small and very small loans to 2,850 entre-preneurs and welcomed nearly 12,000 new depositors. We opened a branch in the province of Benguela, the first branch outside the capital city, Luanda. NovoBanco’s presence outside Luanda is extremely important for the country’s reconstruction and economic development.

In 2006 total assets grew by more than 80%, and we earned a small profit for the first time. We do not take our success for granted; the bank’s dynamic development is attributable to our outstanding, hard-working staff, our trusting and appreciative customers, and a business model that is straightforward and unique. We are confident that we can sustain the upward trend in 2007, during which we will further expand our business.

I would like to express my gratitude to our shareholders for their ongoing support. Without their work on the bank’s governing bodies and their technical assistance contributions, the bank’s start-up phase would not have been possible. I thank all employees for their untiring efforts and their consistent imple-mentation of our corporate strategy. Finally, I would like to thank our customers for the trust they have placed in our bank.

Gabriele Heber Chairperson of the Board of Directors NovoBanco

Letter from the Board of Directors

Members of the

Board of Directors as at

December 31, 2006:

Gabriele Heber

Stefan Wolff

Jasper Snoek

Michael Callaghan

Tunde Onitiri

Members of the

Management Board as at

December 31, 2006:

Stefan Wolff

Simon Herrmann

L e t t e r f r o m t h e B o a r d o f D i r e c t o r s �

The Bank and its Shareholders

ProCredit Holding AG is theparentcompanyoftheglobal

group of ProCredit banks located in transitionand developing countries across three conti-nents. It was founded as Internationale MicroInvestitionen AG (IMI) in 1998. The ProCreditgroupofbanksaimtomakeadifferencebypro-viding banking services to people whom otherbanks either do not serve at all (usually on thegroundsofcostorrisk)oronlyserveinadequately.Theholdingcompany,workingcloselywithInter-nationaleProjektConsultGmbH(IPC),guidesthedevelopmentoftheProCreditinstitutions,provid-ingsupportinallkeyareasofbankingoperationsandhumanresourcesmanagement.Thecompanycurrently has an equity base of more thanEUR 200 million. Its shareholders consist of asoundmixofprivateandpublicinvestors.

The International Finance Corpora-tion (IFC)istheprivatesectorarmof

the World Bank Group and is headquartered inWashington,D.C.ThemissionofIFCistopromotesustainable private sector investment in devel-opingandtransitioncountries,helpingtoreducepovertyandimprovepeople’slives.IFCfinancesprivate sector investments in the developingworld, mobilises capital in the internationalfinancial markets, helps clients improve socialand environmental sustainability, and providestechnicalassistanceandadvicetogovernmentsandbusinesses.Fromitsfoundingin1956through

FY05, IFC has committed more than USD 49billionofitsownfundsandarrangedUSD24bil-lion insyndicationsfor3,319companies in140developingcountries.IFC’sworldwidecommittedportfolioasofFY05wasUSD19.3billionfor itsown account and USD 5.3 billion held for parti-cipantsinloansyndications.

DOEN Foundation promotesa liveable world in which

everyone can play a part, by subsidising andfinancing initiatives in the field of sustainabledevelopment, culture and welfare. DOEN Foun-dation receives financial contributions for thisfrom the Dutch charity lotteries: the NationalePostcodeLoterij(NationalPostcodeLottery),theBankGiroLoterij(BankGiroLottery)andtheSpon-sorLoterij(SponsorLottery).

DOENFoundationsupportsbothsmallandlargeinitiatives which contribute to a more colourfuland liveable society, focussing particularly oninitiatives that require active entrepreneurshipandhaveasustainablecharacter.Inimplement-ingsuchinitiatives,theemphasisisonpeople’sabilitytomotivatethemselves.

DOENFoundationwassetupin1991bytheNa-tionalePostcodeLoterij.ThenameDOEN(todo)reflects what the foundation stands for: actionandresults;steppinginwhereotherswillnot;de-terminationanddedicationtoaliveablesociety.

NovoBanco was established in 2004 as a full-fledgedcommercialbankbyastrongallianceofinternational shareholders. We provide creditand other financial services to small entre-preneurs and low-income households, a targetmarket that was not previously served by com-

mercial banks or microfinance organisations.As Angola emerges from decades of civil war,NovoBancoisplayingacriticalroleinthecoun-try’sprivatesectordevelopment,helpingtocre-ate prosperity and a stable economic environ-ment.

Sector

InvestmentBankingInvestmentInvestmentEnergy

Shareholder(as of Dec. 31, 2006) ProCreditHoldingIFCDOENBIOChevron

Total Capital

Headquarters

GermanyUSANetherlandsBelgiumGermany

Share

42.86%14.29%14.29%14.29%14.29%

100%

Paid-in Capital (in USD)

2,100,000700,000700,000700,000700,000

4,900,000

A n n u a l R e p o r t 2 0 0 6�

The Bank and its Shareholders

The Belgian Investment Company for Developing Countries (BIO), wassetup

inDecember2001asapublic-privatepartnershipbetween the Belgian government – through theDepartment of Development Cooperation – andtheBelgianCorporationforInternationalInvest-ment.BIO’smissionistosupportthesustainabledevelopment of the private sector in develop-ing countries by providing long-term financing(equity, quasi-equity and long-term loans) tomicro, small and medium-sized enterprises(MSMEs). BIO’s interventions are either director indirect (i.e. through investment funds andfinancial intermediaries).Todate,BIOhascom-mitmentsofoverEUR100million.

Chevron Sustainable Development Com-pany Ltd. (CSDC) isawholly-ownedsub-sidiary of Chevron Corporation, a lead-

ing U.S.-based oil company. Chevron has beenoperating in Angola since the 1950s and is oneof the largest foreign investors in the country.Foundedin2002,theCSDCispartofawideriniti-ative to support the reconstruction of Angolathrough community and private sector develop-ment.ChevronhascommittedUSD25millionto-wardsaUSD50millionprogrammeforAngola’sreconstruction.

Th e B a n k a n d i t s S h a r e h o l d e r sTh e B a n k a n d i t s S h a r e h o l d e r s �

The ProCredit Group – Neighbourhood Banks for Ordinary PeopleThe ProCredit Group – Neighbourhood Banks for Ordinary People

TheProCreditgroupcurrentlycomprises19tar-get group-oriented banks operating in as manycountries.Wefocusondevelopingcountriesandtransition economies in three regions: EasternEurope, Latin America and Africa. The grouphas 470 branches staffed by 12,600 employ-ees. Currently, ProCredit banks disburse morethan 60,000 loans totalling more than EUR 185million every month. By the end of 2006, thenumberofloansoutstandinghadgrowntomorethan740,000(amountingtoEUR2.1billion).Theaverage loan amount outstanding is EUR 2,850andthe loanportfolioquality remainsexcellentwitharatioofloansinarrears(>30days)tototalloanportfolioofonly1.2%.Over2006,thegroup’sdeposit base increased from EUR 1.3 billion toEUR 1.8 billion, with nearly one million newaccountshavingbeenopened.

TheProCreditgroupisledbytheFrankfurt-basedProCreditHoldingAG,foundedbytheconsultingfirm IPC in1998.ThestaffofProCreditHoldingand IPC provide centralised support, super-visionandmanagementofalltheProCreditbanks.ProCredit Holding is a private-public company,withinternationalshareholdersthatincludeKfW,IFC,FMO,andtheDOENFoundation.In2006,theshareholder group was joined by two new US-based private shareholders, TIAA-CREF and theOmidyar-TuftsMicrofinanceFund.

But what do these facts and figures mean andwhat are these shareholders trying to achieve?ProCreditisbuildingaglobalgroupofneighbour-hoodbanks.Butwhatisaneighbourhoodbank?Wherever we are, we aim to be the accessible,trusted, socially responsible bank for the localsmall businesses and the ordinary people wholiveandworkinthearea.Inourlendingbusiness,wefocusonverysmall,smallandmedium-sizedenterprises.AtthesametimeProCreditprovidesretailbankingservicesto“ordinary”people,witha focus on low-income families. In this way weaimtobethelong-termbankingpartnerfortar-getgroupswhichmostconventionalcommercialbanksneglect.Byprovidingsociallyresponsibleproducts we aim to contribute to the economicdevelopmentofthecountriesinwhichwework.

Inthedevelopingcountriesandtransitionecon-omies in which the ProCredit group operates,conventional commercial banks tend to neglectsmall and very small businesses because theyare thought to keep inadequate records, haveinsufficientcollateralandgeneratehighadmin-istrative costs. However, these businesses arethe main engine of economic growth and of jobcreation.Overtheyears,theProCreditgroupandIPC, which developed the lending methodologyusedbytheProCreditgroup,havegainedapro-foundunderstandingofboththeproblemsfacedbysmallbusinessesandtheopportunitiesavail-abletothem,andhavetailoredthecredittechnol-ogytoreflecttherealitiesoftheiroperatingenvi-ronment.Thankstothiscredittechnology,whichcombinescarefulanalysisofallcreditriskswithahighdegreeofstandardisationandefficiency,theProCreditinstitutionsareabletoreachalargenumberofsmallborrowers.

IncontrasttoProCredit,othercommercialbanksgivepriorityintheirlendingoperationstocorpo-ratefinanceandconsumerlending,especiallythelatter. Consumer finance is attractive becauseitusuallydoesnotrequireskilledstafformuchfinancial analysis of the client, allowing banksfocusedonmarketsharetogrowquickly.However,thisquestformarketsharecanleadtoirrespon-sible lending and overindebtedness on the partoftheclient.ProCreditneverforgetsthataloanis also a debt. We place great emphasis on thecarefulevaluationofaborrower’sdebtcapacityandonbuildinglastingrelationships.Inthisway,ProCreditischaracterisedbyaresponsible,long-termattitudetowardsbusinessdevelopmentandclientrelationships.

Furthermore,ProCreditinstitutionsstrivetofos-terasavingsculture.Weaimtobuildpubliccon-fidenceinbanksbysettingnewstandardsincus-tomerservice,transparencyandbusinessethics.ProCreditdepositfacilitiesareappropriateforabroadrangeofcustomers,especiallylow-incomegroups.Weoffersimplesavingsproductswithnominimumdepositrequirement.EightypercentofalldepositaccountshaveabalanceoflessthanEUR100.Thisillustratesourtargetgrouporien-tation and highlights the challenge of servingthistargetgroupofsmallsaverswhoaccountforonly1%ofourtotaldepositvolume.Inthespirit

A n n u a l R e p o r t 2 0 0 6�

ProCredit Bank Serbia

ProCredit Bank Bosnia and Herzegovina

ProCredit Bank Kosovo

ProCredit Bank Albania

ProCredit Bank Macedonia

ProCredit Bank Sierra Leone

ProCredit Savings and LoansGhana

ProCredit Bank DemocraticRepublic of Congo

NovoBanco Angola

Banco ProCredit Mozambique

ProCredit Bank Ukraine

ProCredit Moldova

ProCredit Bank Romania

ProCredit Bank Kyrgyzstan(planned)

ProCredit Bank Georgia

ProCredit Bank Armenia(planned)

ProCredit Bank Bulgaria

ProCredit Mexico(planned)

Banco ProCredit Honduras(planned)

Banco ProCredit El Salvador

Banco ProCreditNicaragua

Banco ProCredit Colombia(planned)

Banco ProCredit Ecuador

Banco Los AndesProCredit Bolivia

The ProCredit Group – Neighbourhood Banks for Ordinary PeopleThe ProCredit Group – Neighbourhood Banks for Ordinary People

of a neighbourhood bank, ProCredit banks place great emphasis on children’s savings products and education campaigns as well as on sponsor-ing local community events. In addition to deposit facilities, clients are offered a full range of stand- ard non-credit banking services.

The shareholders of the group aim to strike the right balance between their prime developmen-tal goals: reaching as many small enterprises and small savers as possible, and achieving commer-cial success. For 2006, the return on equity for the group as a whole, expressed in hard currency after deduction of profit taxes, is expected to reach 13%. This level of profitability is required to support our rapid growth, to ensure our long-term sustainability and to generate a reasonable return for our shareholders.

The neighbourhood bank concept is not limited to our target customers and how we reach them. It is also about our staff: how we work with one another and how we work with our customers. The neighbourhood bank approach requires a high degree of decentralised decision-making and therefore judgement and creativity from all staff, especially our branch managers. Our corporate values embed principles such as honest commu-nication, transparency and professionalism into

our day-to-day business. Key to our success is therefore the selection and training of the right staff. We maintain a corporate culture that har-nesses the creativity and entrepreneurial spirit of our staff, while fostering their deep sense of personal and social responsibility. This entails not only intensive training in technical and man-agement skills, but also a continuous exchange of personnel between our member institutions in order to take full advantage of the opportunities for staff development which are created by their membership of a truly international group.

A central plank in our approach to training is the group’s ProCredit Academy in Germany, which pro-vides a three-year, part-time “ProCredit Banker” training programme for its high-potential local personnel. The programme includes intensive technical training and also exposes participants to a very multicultural learning environment and to subjects such as anthropology and the human-ities. The programme provides an opportunity for our future leaders to develop their views of the world, as well as their communication and staff management skills. The continued success of ProCredit relies on a self-confident team of people who share a personal commitment to the target group and to the neighbourhood way of doing things.

The international group

of ProCredit institutions;

see also

www.procredit-holding.com

Th e P r o C r e d i t G r o u p – N e i g h b o u r h o o d B a n k s f o r O r d i n a r y P e o p l e �

A n n u a l R e p o r t 2 0 0 610

ProCredit in Africa

Aftergainingyearsofexperienceinestablishingtargetgroup-orientedbanksinLatinAmericaandSouth-EasternEurope,ProCreditHoldingdecidedto establish a third area of operations in Sub-Saharan Africa. We began operating in Mozam-biquein2000,andinGhanain2002.In2004/05,weestablishedinstitutionsinAngolaandCongo(DRC), and we plan to open a ProCredit Bank inSierraLeone–ourfifthinAfrica–in2007.

ItisalreadyclearthatitwillbepossibleinAfrica,asithasbeenelsewhere,tosetupstable,targetgroup-orientedfinancialinstitutionswhichhaveextensive branch networks and are largely ableto mobilise their own funds from local savingsdeposits.However, it isequallyclearthatdoingsowill require longerperiodsof timethanwereneededinLatinAmericaorEasternEurope.Someof the reasons for this are obvious, others aremoresubtle.

Undoubtedly, the lower average loan amount atsomeofourAfricanbanksisresponsiblefortheslowergrowthoftheloanportfoliointhisregion.Thereisnolackofdepositcustomers,butdepositamountsaresmallaswell.Bothsidesofthebal-ance sheet are affected by the combination oflabour-intensive processes and small individualamounts which characterises our banks’ opera-tions.

Infrastructureisweakandsuitablepremisesarescarce inAfrica,particularly in thepost-conflictcountriesonwhichwefocus–makingbranchnet-work expansion a slow and expensive process.Transport and communication costs are high.Politicalandeconomicinstabilityalsotaketheirtoll. Plainly, in many African countries there isalsoashortageofqualifiedindividuals.OurstaffarethekeytooursuccessinAfricaaselsewhereintheProCreditgroup.Wehaveagreatneedforloan officers and client advisers, co-ordinators,branchmanagers,andqualifiedheadofficestaff,butitishardtofindsuitablepersonnel.Further-more, companies compete strongly for the fewskilled members of the local workforce, oftendrivingupthe“price”ofsuchindividualstounaf-fordable levels.Thismeans thatwehave tode-velopandtrainourprofessionalstaffourselves.Weareproudoftheresults,butwehavetoinvestagreatdealoftimeinthetrainingprocess.

Among the more subtle factors which are lessthan conducive to the rapid spread of com-mercial credit facilities for small and verysmall enterprises in Africa are short-sightedbehaviour on the part of some donors and thepoliciesofmanyAfricangovernments,whichdolittle to promote small business. In Africa, theformal sector in general, and the formal smallbusiness sector in particular, tends to be verysmallandunderdeveloped.Ithashadtostruggleunderalltheburdensresultingfromthesecoun-tries’ colonial past, burdens which are all toooftenreinforced,albeitunwittingly,bythestand-ards demanded by international organisationstoday.Localauthoritiesalsoliketosetstringentformalrequirementsforsmallandmedium-sizedenterprises,leadingbusinessestosomehowfindways, sometimes informal, to get around theserequirements.

All of these factors serve to perpetuate infor-mal structures, in many countries even withinthe financial sector itself. We would like to ex-pand the ProCredit business model to otherAfrican countries more rapidly, but it is not al-ways easy. Numerous African countries haveinterest-rate ceilings, especially those in theCFA zone. Microfinance, which is necessarilycost-intensiveandexpensive,mustthenbecar-ried out de facto on a subsidised, informal orillegalbasis.Thisisoneofthereasonswhytherearea largenumberofNGOsissuingsmall loansinAfrica.ManydonorssubsidisetheseNGOsandtheirlendingoperationssoheavilythatthelocalsavings deposits which would be available areneverevenmobilisedorused,andtheyarethusrunning the risk of damaging or even destroy-ing serious commercial providers of financialservices.

P r o C r e d i t i n A f r i c a 11

DemocraticRepublic of Congo

Angola Mozambique

Ghana

Congo

Cameroon

Sudan

Ethiopia

KenyaUganda

Burundi

Madagascar

South Africa

Namibia Botswana

Malawi

Tanzania

Central Africa

Nigeria

NigerMali

Burkina Faso

EgyptLibya

ChadSenegal

Morocco

Mauritania

Algeria

Tunisia

Togo

Benin

Cote d’Ivoire

Liberia

Sierra Leone

Guinea

Western Sahara

Guinea-Bissau

Gabon

Equatorial Guinea

Lesotho

Swaziland

Zambia

RwandaDemocraticRepublic of Congo

Angola Mozambique

Ghana

Congo

Cameroon

Sudan

Ethiopia

KenyaUganda

Burundi

Madagascar

South Africa

Namibia Botswana

Malawi

Tanzania

Central Africa

Nigeria

NigerMali

Burkina Faso

EgyptLibya

ChadSenegal

Morocco

Mauritania

Algeria

Tunisia

Togo

Benin

Cote d’Ivoire

Liberia

Sierra Leone

Guinea

Western Sahara

Guinea-Bissau

Gabon

Equatorial Guinea

Lesotho

Swaziland

Zambia

RwandaDemocraticRepublic of Congo

Angola Mozambique

Ghana

Congo

Cameroon

Sudan

Ethiopia

KenyaUganda

Burundi

Madagascar

South Africa

Namibia Botswana

Malawi

Tanzania

Central Africa

Nigeria

NigerMali

Burkina Faso

EgyptLibya

ChadSenegal

Morocco

Mauritania

Algeria

Tunisia

Togo

Benin

Cote d’Ivoire

Liberia

Sierra Leone

Guinea

Western Sahara

Guinea-Bissau

Gabon

Equatorial Guinea

Lesotho

Swaziland

Zambia

Rwanda

Butweshouldnotonlytalkaboutthe“problems”inAfrica.Wearefirmlycommittedtothecontinent.Theopportunitiesaregreat,giventhatthereisathrivinginformalbusinesssectorinmanyAfricancountries.Thedemandforcreditisstrongandatpresentalmostnoneofthisdemandisbeingmetbytheformalfinancialsystems;atthesametimethereisagreatwillingnessonthepartofordinarypeople to entrust their savings to a sound andprofessional financial institution. Our potentialdevelopmentimpactisverysignificant:inmanycountries we are unique in providing modern,transparent and reliable banking services foreveryone,i.e.wehavenominimumdepositbal-ance and we provide loans to very small busi-nesses.Moreover,weplantoofferbothhousingimprovement loans and agricultural loans onan expanded scale in order to better meet the

demandforthistypeofcreditinthepost-conflicteconomies inwhichourbankstypicallyoperateinAfrica.

With788dedicatedstaffmembersattheendof2006managingsome165,000depositaccountsanddisbursing3,800loanspermonth,wealreadyhaveagoodteaminAfricaandastrongplatformonwhichwecanbuild.Inviewoftheexperiencewe have gained to date and our growing capac-itytotrainnewemployeesinourexistingbanks,and given that a regional training academy willbesetupinAfricain2007,ournextstepsintheregionwillbemoreambitious.We look forwardtosteadilyexpandingthebranchnetworkinthecountriesinwhichwealreadyworkandtoestab-lishingnewProCreditbanksinseveraladditionalAfricancountries.

A n n u a l R e p o r t 2 0 0 61�

Name

NovoBancoAngola

ProCredit Bank Congo S.A.R.L.

ProCredit Savings and Loans Company Ltd. Ghana

Banco ProCredit Mozambique

Highlights

FoundedinFebruary2004(opentothepublicsinceAugust2004)3branches2,307loans/USD7.6millioninloans23,661depositaccounts/USD7.4million115employees

Foundedin2004(opentothepublicsinceAugust2005)2branches2,782loans/USD7.4millioninloans16,512depositaccounts/USD14.8million105employees

FoundedinJuly2002(initiallynamed“SikamanSavingsandLoansCompanyLtd.”)7branchesand1savingsmobilisationunit10,133loans/USD14.0millioninloans68,533depositaccounts/USD12.9million326employees

FoundedinDecember20009branches21,293loans/USD13.3millioninloans64,347deposits/USD8.1million297employees

Contact

RuaN’Dunduma253LuandaTel.:+244222430040Fax:[email protected]

AvenuedesAviateurs4BKinshasa/GombeTel.:+Tel.:+243898996600Fax:[email protected]

P.O.BoxNT328,NewTownAccraTel.:+23321246860/62Fax:[email protected]

Av.ZedequiasManganhelaNr.267JatIV,6oandarDTel.+25821313344Fax.+25821313345Sede@bancoprocredit.co.mz

P r o C r e d i t i n A f r i c a 1�

The Year in Review

January

• Western Union inbound services are launched.• Aloanofficertrainingcoursebeginswith30 participants.

February

• After almost three years of service, Barbara Sajet and Koen Wasmus are replaced by Stefan Wolff, General Manager and Simon Herrmann, Chief Operational Officer/Deputy GeneralManager.• TheCentralBankconductsitsfirstinspection ofNovoBanco.

March

• NovoBanco opens a branch in Benguela, its firstoutsideLuanda,thecapital.

April

• Arevisedsalarystructureisapprovedbythe Board.• A branch manager visits ProCredit Bank Kosovo.

May

• Thelegaldepartmentisestablished.• 18newloanofficersarehired.

June

• Middlemanagementstaffmembersarehired andbegintraining.• Branch staff in Benguela and Luanda begin Englishcourses.

A n n u a l R e p o r t 2 0 0 61�

The Year in Review

July

• To coincide with the 2006 Football World Cup, NovoBanco organised a football cup forschoolsfromthebranchneighbourhoods. 15schoolsfromLuandaandBenguelapartici- patedinthetournament.

August

• Western Union outbound services are launched.• Thebankcelebratesitssecondanniversary.• The bank achieves its best monthly results inlending:itdisbursesmorethan300loans, amountingtomorethanUSD1.6million.

September

• In cooperation with IFC, the bank starts an educationalprogrammeagainstHIV/AIDS.

October

• Thebanklaunchesachildren’ssavingscam- paign, “MeuPorquinho 2006”, with a press conferencebroadcastcountrywide.• The100themployeejoinsNovoBanco.• ThefirstgroupofNovoBancoemployeestake English courses at the Regional Academy of theProCreditgroupinGhana.

November

• Two staff members are selected to partici- pateinthe“ProCreditBanker”programmeat theProCreditAcademyinFürth,Germany.• Twointernalauditorsbeginanexchangewith NovoBancoMozambique.

December

• The“MeuPorquinho2006”children’ssavings campaignconcludeswithbigcelebrationsin BenguelaundLuanda.

Th e Y e a r i n R e v i e w 1�

Management Business Review

Management Board

from left to right:

Stefan Wolff

General Manager

Simon Herrmann

Deputy General Manager

A n n u a l R e p o r t 2 0 0 61�

Management Business Review

Political and Economic Environment

2006 was characterised by continued macro-economic stability, a trend that began in 2004.GDP grew by more than 15%, and inflation waskeptundercontrolat17%.Thelocalcurrency,thekwanza,remainedstableinrelationtotheUSdol-lar. The Central Bank reduced inflation throughforeign-exchange intervention that lowered thecostofimports,ratherthanthroughgreaterfiscaldiscipline.Thispolicyiseffectivewhileoilexportearningsremainhigh,butisnotsustainableoverthelongrun.Theovervaluedexchangeratehasanegativeimpactonlocalnon-oilproductiveacti-vities,suchasmanufacturingandagriculture.

Duringthefirsttenmonthsof2006,interestrateson loans,depositsandtreasurybillsdecreasedsignificantly. This trend did not have an impactonbanks’earnings.

Thepoliticalenvironmentremainedstable.Sincethe2002peaceaccord,powerhasbeensharedbetween the ruling MPLA and its former adver-saryUNITA.Inalandmarkinitiative,thegovern-ment began online voter registration in Novem-ber 2006. This process will take at least oneyeartocomplete,however,andpresidentialandparliamentaryelectionswillnot takeplaceuntil2008 or 2009. International experts expect theMPLAtowin,andthecurrentpresident,JoséEdu-ardodosSantos–inpowersince1979–toretainpower.

Mineral resources, mainly oil and diamonds,remain Angola’s main export products. Oil out-put stands at 1.6 million barrels per day and isexpected to reach 2 million barrels per day by2008,confirmingthatAngolawillremainoneofAfrica’smajoroilproducers.In2005,thegovern-ment began drawing on a USD 2 billion line ofcreditfromChinatorebuildAngola’spublicinfra-structure,andseveral large-scaleprojectswerecompletedin2006.

The construction boom continued in Luanda,fuelledby large firmssuchasbanks, insurancecompanies and oil companies. The real estatemarket was overheated, and apartment rentswereamongthehighestintheworld.

Littlewasachievedinrebuildingpost-waragricul-turalandindustrialproduction.Angolacontinuedtorelyheavilyonimports,andalimitednumberoflargebusinesseskeptpricesartificiallyhigh.

Anegligiblepercentageofthepopulationbene-fits from Angola’s substantial oil revenue. Percapita income is USD 1,350 (2005), but An-gola still ranks among the bottom ten on manysocialanddevelopmentalindicators.Onlyathirdofthepopulationhasaccesstocleanwaterandadequatesanitation,lifeexpectancystandsat39years,and25%ofbabiesdiebefore they reachthe age of 5. In 2006 illnesses such as choleraand Marburg fever re-emerged. Angola has anextremelyhighfertilityrate(2006:6.35childrenborn/woman), and more than 50% of the popu-lationisunder20yearsofage.

Angola’senormousagriculturalpotentialremainslargelyuntapped,eventhoughsmall-scalefarm-ersarereturningtothecountry’sinterior,andthecountryno longerreceives large-scalefoodaid.Pervasivelandminesandalackoflandtitlesandinfrastructureslowthepaceofagriculturaldevel-opment.1

Informal and small businesses have receivedinadequate support from the government,which has done little topromote their integra-tion into the formal economy or to ease regula-tionsandlawsposinganobstacletotheirdevel-opment.Thesmallbusinesssectorcontinuedtogrow,however,especiallyinLuanda.Itisconcen-tratedinthetradeandservicesectors;fewsmallbusinessessucceedintheagricultural,manufac-turingandlow-scaleindustrialsectors.

Barrierstosmallbusinessdevelopmentinclude:

• Lack of information on the number of enter- prisesandtheircharacteristics• Lackofco-ordinationamonginstitutions• Excessiveregulation• Alimitedsupplyoffinancialservices

Asaresult,manysmallbusinessesremaininfor-mal and are marginalised from the authorities,largecompetitorsandthelegalsystem.Tradition-albankslargelyignorethismarketintheirlend-

1 Sources:CountryReportsfromTheEconomistIntelligenceUnit,UnicefandtheCIAWorldFactbook.

M a n a g e m e n t B u s i n e s s R e v i e w 1�

31.4%

62.3%

6.3%

Number of Loans Outstanding – Breakdown by Loan Size*

< USD 1,000 USD 10,001 – USD 50,000 USD 1,001 – USD 10,000 * 31 Dec 2006

Loan Portfolio Development

Number (in ’000) Volume (in USD million)

Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec 04 05 06

< USD 10,000 Total number outstanding USD 10,001 – USD 50,000

10 9 8 7 6 5 4 3 2 1 0

3.000 2.700 2.400 2.100 1.800 1.500 1.200 900 600 300 0

ing business and establish restrictive accountopeningrequirements.Smallentrepreneursthuscontinuetolackaccesstoformalfinancialservic-es,somethingthatNovoBancoaimstochange.

Financial Sector Developments

A national development bank and four new pri-vate banks began operations in 2006, bringingthetotalnumberofcommercialbanksto16.Noneof the new banks is dedicated to serving small

entrepreneurs.Totalassetsinthebankingsectorincreasedby61%toUSD10.4billion.

Although the combined loan portfolio of allbanks grew by 40%, loans still accounted fora relatively low 40% share of their total as-sets. More than 80% (2005: 56%) of loans arechannelled to the private sector. Most of theseloans are allocated to trade finance and con-sumer lending. Consumer loans and housingloans are aggressively marketed, especially byBancoFomentoAngolaandBancoBIC.

Banks Branches Loans Deposits as at Outstanding credit volume as at Deposits as at Amounts in million USD 30 Sept 2006 30 Nov 2006 30 Nov 2005 30 Nov 2006 30 Nov 2005 BancoAfricanodeInvestimentos 31 585 433 2,048 951 BancoComercialAngolano 5 54 92 188 167 BancodeComercioeIndustria 26 199 145 356 266 BancoFomentoAngola 37 966 770 1,863 1,269 BancoMilleniumAngola 3 80 54 114 56 BancodePoupançaeCredito 58 1,138 693 1,887 1,249 BancoTottaAngola 8 151 124 279 240 BancoSol 30 57 47 188 126 BancoEspiritoSantoAngola 10 360 338 635 339 BancoRegionaldoKeve 8 67 60 108 71 NovoBanco 3 8 5 7 2 BancoBIC 40 475 107 1,084 185 BancoPrivadoAtlântico BancodeNegóciosInternacional* BancoVTBÁfrica* BancodeDesenvolvimentodeAngola* Total 259 4,140 2,868 8,757 4,921 *Notyetoperational

A n n u a l R e p o r t 2 0 0 61�

Business Loan Portfolio – Breakdown by Maturity

< 12 months 12 – 24 months

in %

100 90 80 70 60 50 40 30 20 10 0

Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec 04 05 06

Loan Portfolio Quality (arrears >30 days)

in % of loan portfolio

8

7

6

5

4

3

2

1

0 Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec 04 05 06

Angola’s microfinance sector is undeveloped. AdedicatedunitwithintheCentralBankwasclosedinOctober2006,andadraftmicrofinanceregu-lationhasnotbeenpublishedyet.OneNGOservesverysmallbusinessesandwantstotransformitsmicrofinanceprogrammeintoaformalinstitution.In2006NovoBancoAngolacontinuedtobetheonlycommercialbankservingthemicrofinancesector.

Lending Performance

NovoBanco’sloanproductsaretailoredtosmallentrepreneurs, taking into account the environ-mentinwhichtheyoperate.Formalrequirementsare kept to an absolute minimum, and proce-dures are straightforward. NovoBanco Angolaissues loans to entrepreneurs with at least oneyearofbusinessexperienceintrade,services,orsmall-scaleproduction.LoansareavailablefromUSD100to15,000(anduptoUSD40,000forre-peatclientswithagoodcredithistory)tofinanceincreases in working capital or investments infixedassets.Most loansare repayable inequalmonthly instalments, and maturities vary fromsixmonthstotwoyears.

In November 2006 NovoBanco launched the“Instant Loan”, which offers between USD 100and 2,000 to very small entrepreneurs at vari-ous open markets in the Benguela region. Thisproduct uses simple and straightforward credit

assessment procedures so that a loan decisioncanbemadeimmediately.Disbursementusuallytakesplaceonthefollowingday.

Demand for loans was strong in 2006; the out-standing loan portfolio increased by over 70%fromUSD4.4milliontoUSD7.6million.Thebanksought to increase the number and productiv-ity of credit department staff. These efforts arean ongoing challenge due to the tight Angolanlabour market and logistical and infrastructuralbarriersinLuanda.

NovoBancolendstoawiderangeofbusinesses,from private hospitals to market vendors, andfrom fishermen to mini-markets. It therebyspreadscreditriskoverdifferentsectorsandseg-mentsoftheeconomy.Loansizesvary,withthemajorityfallingbetweenUSD1,000and10,000.

Loan portfolio quality was unsatisfactory in2006; the year ended with a portfolio at riskover30daysof5.66%.NovoBancoconsistentlyadjusted its credit methodology to manage theriskassociatedwithlendingtosmallbusinesses.Weestablishedaloanrecoveryteamtomanagearrears, introduced additional credit analysistrainingforloanofficers,reducedthegeographicareainwhichwerecruitnewclients,andrewardedgoodrepaymentperformancebyofferingsimpli-fiedloanrenewalprocedures.WeexpectPARtodecreasein2007asaresultofthesemeasures.

M a n a g e m e n t B u s i n e s s R e v i e w 1�

84.1%

0.2%2.9%

12.6%

< USD 100 USD 1,001 – USD 10,000 USD 101 – USD 1,000 USD 10,001 – USD 50,000

Number of Customer Deposits – Breakdown by SizeCustomer Deposits

Number (in ’000) Volume (in USD million)

Term Savings Sight Total number

Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec 04 05 06

8

7

6

5

4

3

2

1

0

32

28

24

20

16

12

8

4

0

Other Banking Services

NovoBancoAngolaoffersawiderangeofsimple,low cost banking products. We minimise docu-mentation requirements as much as possibletoensurethateveryAngolancanopena formalbankaccount.

In 2006 total deposits increased by 170% fromUSD2.7milliontoUSD7.40million,ofwhich58%washeldinlocalcurrency.Theshareofdepositsheld in time deposit accounts (maturities from1-12months)increasedfrom15%in2005to27%in 2006. More than 90% of term deposits wereheldinkwanza,whichdemonstratestheincreas-ingpublicconfidenceinAngola’slocalcurrency.

NovoBanco promotes its services to a widerange of clients, many of whom are consideredun-bankable by other commercial banks. Ourthreebranchesundertakeextensivepromotionsin their respective neighbourhoods. Traditionaladvertising,suchasbillboards,radiospotsandnewspaperads,arenoteffectiveforcommunicat-ingwith lower-incomeAngolans,manyofwhomhavenopriorexperienceofdoingbusinesswithabank.Thebranchesusedirectcommunicationandinformationalactivitiestofamiliarisepeoplewiththebankanditsservices.In2006theypro-vided financial education in local schools andorganised a football championship and savingscampaignforchildren(seethespecialfeatureinthisreport).

NovoBanco attracted many small savers whohadneverenteredabankbefore;2,000savingsaccounts were opened in 2006 with an averagebalanceofUSD75.

As a member of the national clearing house,NovoBanco offered domestic payments as ameansforsmallenterprisestopay localsuppli-ers.Theseclientscontinuedtoconsiderchequesa more attractive payment method, however;NovoBancoissuedover4,000chequesin2006.NovoBanco processed USD 5.6 million in inter-national transfers, not including Western Unionservices.Outgoingpaymentserviceswereusedby loan clients and small traders who importgoodsfromDubai,Korea,China,BrazilandPor-tugal, and by Angolans sending remittancesabroad.WesternUnionserviceswereintroducedin early 2006 for inbound transfers. In August,theservicealsoofferedoutboundtransfers.Thedemandwasenormous;byyear-endNovoBancohadprocessed2,100inboundtransfersand2,700outboundtransferswithacombinedvolumeofUSD2.5million.

A n n u a l R e p o r t 2 0 0 6�0

Domestic Money Transfers

Number (in ’000) Volume (in USD million)

Incoming Outgoing Number

2,0 1,8 1,6 1,4 1,2 1,0 0,8 0,6 0,4 0,2 0

200 180 160 140 120 100 80 60 40 20 0

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q404 05 06

International Money Transfers

Number (in ’000) Volume (in USD million)

Incoming Outgoing Number

5,0 4,5 4,0 3,5 3,0 2,5 2,0 1,5 1,0 0,5 0

1.000 900 800 700 600 500 400 300 200 100 0

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q404 05 06

M a n a g e m e n t B u s i n e s s R e v i e w �1

NovoBancoinvestednearlyUSD100,000ininter-national trainingandexchange,anamount thatwillincreaseinthefuture.

In2006NovoBancoAngolamadeamodestprofitofUSD43,012afterconservative loan losspro-visioning.

Outlook

The relative economic and political stability isexpected to continue in 2007, hopefully result-inginthefirstgeneralelectionsinoveradecade.Forecastsprojectstrongeconomicgrowth(above15%)andhigh-volumeoilproduction.Thegreat-estchallenge facingAngolawillbe toachieveamoreevendistributionofwealthacrossitspopu-lation,oneofthepoorestintheworld.

In2006NovoBancoreinforceditsreputationasareliablepartnerforbusinessesandprivateindi-viduals. Rapid growth in the loan portfolio anddeposit base confirmed the strong demand forourproductsandservices.Thebankopeneditsfirst branch outside the capital and preparedto open three more branches in 2007 – two inLuandaandoneinBenguelaprovince.

Toretainitspositionasthemarketleaderinsmallbusiness lending, NovoBanco must expand itsinternal capacity. In 2007 we will steadily in-creasethenumberofloanofficersandintroducehousing improvement loans for salary earners.TheoutstandingloanportfolioisprojectedtobeUSD16millionbyyear-end.

Our branches will continue to conduct informa-tionalandeducationaleventsthroughclosepart-nershipswith localschoolsandothercivilsoci-etyinstitutions.

With its attractive product portfolio and loyalcustomer base, NovoBanco is in an excellentpositiontoexpandaccesstofinancialservicesinLuandaandAngola’sprovinces.

Financial Results

NovoBanco’s balance sheet experienced stronggrowth, reachinga totalofUSD14.1millionbyyear-end. The balance sheet composition re-mained straightforward: liabilities were largelycustomerdeposits,whileassetsconsistedoftheloan portfolio, financial investments and fixedassets.

In2006interestincomefromloansreplacedinter-estincomefromtreasurybillsandforeignplace-ments as NovoBanco’s main source of income.WesternUnionandinternationalmoneytransferfeeswereanincreasinglysignificantsourceofin-come.Costsweremainlyoperationalexpenses,loan lossprovisionsand interestexpenses.Thelow share of interest-earning deposits kept thelatter at a modest level. Operational expenseswererelativelyhigh,albeittypicalintheAngolancontext.

M a n a g e m e n t B u s i n e s s R e v i e w��

NovoBancoAngolalauncheditsfirstlarge-scalesavingscampaignin2006.Thecampaigntargetedchildrenbetweentheagesofsixandtenandwasorganised in cooperation with the Angola Part-nership Initiative, a public-private partnershipbetweentheUNDPandChevron.

In Angola, which only recently emerged fromyearsofcivilwar, thedesire for immediatecon-sumptionispalpable.Savingforretirementorlifeinsuranceisaforeignconcept,particularlygiventheextremepoverty inwhichmanypeople live.A lowermiddleclassisemergingamongpeoplewith a fixed income from an independent busi-ness or a salaried job. But many of these indi-vidualsdonotsetasidesufficientsavingstopro-tectthemselvesandtheirfamiliesagainstmajorrisks,suchasdeathordisability.

Todrawnationwideattentiontotheimportanceofsaving, NovoBanco launched a two-month cam-paign with a press conference in October 2007.The campaign met with unexpectedly strongpublic interest. It received regular coverage ontelevision,ontheradioandinprintmedia.

As a central component of the campaign, thebank cooperated with state education authori-tiestoteachfinancialeducationinlocalprimaryschools.NovoBancoemployeesvisited21stateschools,wheretheytaughtmorethan4,000chil-dren about the importance of saving. The cam-paign’seducationalmaterialswereverypopular;childrenreceivedcolourfulpiggybanks,exerciseandcomicbooks,andsavingspassbooks,whichbankcashiersupdatebyhanduponeachdeposit.The branches complemented these activitieswithSaturdayopeninghoursforchildren,draw-ingcompetitionsandtheatreperformances.TwobigpartieswereheldinLuandaandBenguelatomarktheendofthecampaign.

NovoBancowasthefirstbankinAngolatopubliclyaddresstheissueofsavings.Over700savingsac-countswereopenedduringthecampaign,amajorsuccessconsideringAngolans’prevailinglackoftrustinbanks.Wereceivedextremelypositivefeed-back, particularly regarding the campaign’s funandfestiveatmosphere.Basedonthisresponse,we will launch a similar savings initiative in2007,butprobablywithadifferenttargetgroup.

Special Feature

Children’s savings campaign “MeuPorquinho 2006”

B u s i n e s s R e v i e wM a n a g e m e n t B u s i n e s s R e v i e wS p e c i a l F e at u r e ��

Risk Management

RiskmanagementisanintegralpartofNovoBancoAngola’s business procedures and processes.Thebank’smanagementisresponsiblefordevel-opingriskmanagementpoliciesandprocedures,and for establishing an effective organisationalstructuretoimplementthosepolicies.Itensuresthatriskmanagementisembeddedinthecultureoftheinstitution’sday-to-dayoperations.

NovoBancoAngola’scorebusinessis lendingtoverysmall,smallandmedium-sizedenterprisesthat operate in various economic sectors andlocations. Simply by virtue of the bank’s targetgroup,itsassetsandliabilitiesarehighlydiver-

sified.NovoBancodoesnotengageintradingorotherspeculativeactivities.Allotherbusinessesare reduced to a minimum and are undertakenonlytosupportlendingoperations.

The bank clearly communicates the importanceofinternalandexternaltransparencytoallstaffmembers. Compliance with operational proce-duresandtheCodeofConductismonitoredregu-larly.

NovoBanco’s Internal Audit Department checkscompliance with the bank’s policies and proce-duresandreviewsprocessestodetectpotential

A n n u a l R e p o r t 2 0 0 6��

Risk Management

risks.Itsindependentstatusallowsittoidentifyproblemsandreportitsfindingswithoutanyhin-drance.

In 2006 the bank’s senior management per-formed many of the duties associated with riskmanagement. A new Risk Management Unit willbe established in 2007. The Unit will prepareperiodicreportsandwillserveasariskconsul-tanttomanagement.ThebankwillcreatetworiskcommitteeswithintheRiskManagementUnittoidentifyandmanagerisksinamoreefficientandtransparentmanner.

Credit Risk

Lending to very small, small and medium-sizedenterprises exposes the bank to credit risk.NovoBanco takes various measures to addressrisksinthisarea.Thebankemploysanadvancedcredittechnologytoassessdetailedinformationabouttheclient,his/herhouseholdandhis/herbusiness activities. Credit committees make alllendingdecisions,andthecompositionofcreditcommitteesvariesaccordingtothesizeandriskprofile of the loan. Close monitoring of clients’repayment performance allows the bank to de-tectpotentialproblemsassoonastheyarise.Thediversificationoftheloanportfolioacrossmanysmall borrowers reduces the effects of a down-turninanygivenbusinesssector.

NovoBanco’s management aims to reduce itsportfolio at risk (>30 days) from the high levelof 5.66% at year-end 2006 to less than 4.00%atyear-end2007.Toimproveitscreditriskcon-trol, NovoBanco Angola will establish a CreditRiskUnitinearly2007.Asoundriskmanagementapproach will be crucial to achieve the bank’sambitiousgrowthtargets.

Liquidity Risk

Liquidity risk was managed by the OperationsManagerformostof2006.Thebanktransferredresponsibility for liquidityrisktoanewFinanceManager in late 2006. By removing liquiditymanagement from the Operations Department,NovoBanco clearly separated operational fromfinancial decision-making. In the first half of2007,thebankwillestablishanAssetandLiabil-ity Committee (ALCO). The committee will meetmonthlytoexamineandmanageliquidityrisk.

Operational Risk

Managementcloselymonitorsthebank’sopera-tional risk. Staff strictly apply the “four-eyes”principle to all transactions, and document allmajor processes. Every new employee receivesextensivetrainingonNovoBanco’sprinciplesandproceduresandhisorherspecificresponsibilities.Toensurecontinuedcompliance,thebankoffersrefreshercoursesatalllevelsonaregularbasis.

R i s k M a n a g e m e n t ��

Luanda (2)

Angola

Congo

Democratic Republic of Congo

Zambia

NamibiaBotswana

Atlantic Ocean

Benguela

Branch NetworkBranch Network

Finding the right locations for our branches isthe key to serving our target group efficiently.Wemustbeclosetoopenmarketsandtradecen-tresandofferattractiveandconvenientbranchestoourretailclients.OpeningbranchesisdifficultinAngola,duetoalackofownershipdocuments,bureaucraticobstaclesandextremelyhighrent.

AttheendofMarch,NovoBancoAngolaopeneditsthirdbranch.LocatedinthecityofBenguela,itisourfirstbranchoutsidethecapital.Benguelacity is the capital of Benguela province, about430 km south of Luanda. The province has750,000inhabitants,andthecityhasapopula-tionof200,000.

LikemanyAngolancities,Benguelaissmall.Lit-tle remains of its historic role as a trade centrefor fish, coffee, sugar cane, bananas, salt and

vegetables.TodayBenguelaisdependentonim-portsshippedfromabroadandtransportedfromLuanda. Public initiatives to rebuild infrastruc-ture, agriculture and the private sector areexpectedtostimulategreatereconomicactivity.

In2007thebankwillstrengthenitspresenceinLuandaandtheBenguelaregion.Thereisstrongdemandforourproductsamongthe4millionin-habitantsofLuanda.Thisuntappedmarketpoten-tialisnottheonlyreasontoopenmorebranchesthere:heavytrafficandlongdistancesareabur-denonourclientsandloanofficers.Tobeclosertoourclients,manymorebranchesarenecessary.

In2007wewillopenabranchinLobito,asecondcityinBenguelaprovince.Weexpecttoopenoneor two additional branches in Luanda, bringingthetotalnumbertofiveorsixbytheendof2007.

A n n u a l R e p o r t 2 0 0 6��

Branch NetworkBranch Network

B r a n c h N e t w o r k ��

NovoBanco is a young, fast-growing organisa-tion. Due to high demand for its services, thebankfacescontinuouspressuretoincreaseinter-nal capacity without compromising sound insti-tutional development. Our target group-orien-tation demands a sound institutional structure,goodgovernance,andeffectivebranchmanage-ment.

Thebanksignificantlyincreaseditsstaffin2006toopena thirdbranchand to increasecapacityattheheadoffice.Thebankexpandedtheauditdepartment, established legal and HR depart-ments,added twospecialistseach to the logis-tics,payments,andITdepartments,andrestruc-tured the financial department. This expansionphasewillconcludein2007whenwewillsetupanoperationsdepartment(credit,retail),expandtheHRandmarketingdepartments,hireasecu-rity expert and create a department to overseebranchnetworkexpansion.

In the branches, a “credit coordinator” positionwascreatedtosupportthebranchmanagerandtoofferhigh-performingloanofficerstheoppor-tunitytoadvance.Supervisoryroleswereestab-lished in retail operations to manage businessgrowth.

To prepare for three branch openings in 2007,thebankhiredadditionalpersonnel.Over2,000applications were screened. Staff grew from 49attheendof2005to115attheendof2006.Foritsbranchoperations,NovoBancorecruitsyoungpeoplewhohavefinishedmiddleorhighschool

andhavelittleworkexperience.Theypreparefortheirpositionsthroughintensivein-housetrain-ingcoursesfollowedbyon-the-jobtrainingunderthesupervisionofexperiencedcolleagues.Atthedepartmentmanagementlevel,werecruitexpe-rienced candidates with relevant education andknowledgeof the localcontext.Competition forskilled personnel is extremely high, dominatedby a small number of companies, mainly in theoil industry,thatpayhighsalaries. It isstillex-tremely difficult to recruit qualified personnel,andcompetitionforNovoBanco’strainedstaffisleadingtoabove-averagestaffturnover.

NovoBanco recognises the importance of stafftraining and development to underpin insti-tutional growth and development. A strong andcommittedteamisessentialforthebanktoreachits ambitious goals. We hold regular in-houseseminarsonspecifictopicsandinstitution-wideinformationordiscussionsessionsinaninformalsetting. NovoBanco benefits greatly from train-ingopportunitiesofferedbythewiderProCreditnetwork.Severalstaffparticipatedingroup-widetrainingseminars inFrankfurt. Internalauditorsspentthreeweeksinthebank’spartner institu-tioninMozambique,andabranchmanagervis-ited ProCredit Bank Kosovo to exchange expe-riences. Two employees from the Rocha Pintobranch attended the new ProCredit RegionalAcademy in Accra, Ghana, to participate in anintensiveeight-weekEnglishandbankingcourse.In2007threemanagerswillattendathree-yearprogrammeat theProCreditAcademy.Theywillspend12weeksayearinGermany.

Organisation, Staff and Staff Development

O r g a n i s at i o n , S ta f f a n d S ta f f D e v e l o p m e n t��

Organisation, Staff and Staff Development

PartoftheoverallmissionoftheProCreditgroupis to set standards in the financial sectors inwhichweoperate.Wewanttomakeadifferencenot only in terms of the target groups we serveandthequalityofthefinancialserviceswepro-vide,butalsowithregardtobusinessethics.Ourstrong corporate values play a key role in thisrespect.Wehaveestablishedsixessentialprinci-ples which guide the operations of ProCreditinstitutions:

• Transparency: We adhere to the principle of providingtransparentinformationbothtoour customersandthegeneralpublicandtoour employees, and our conduct is straight- forwardandopen;

• A culture of open communication: We are open, fair and constructive in our communi- cationwitheachother,anddealwithconflicts at work in a professional manner, working togethertofindsolutions;

• Social responsibility and tolerance:Wegive ourclientssoundadvice;theireconomicand financial situation, their potential and their capacities are assessed and are translated intoappropriate“products”;promotingacul- tureofsavingsisimportanttous;wearecom- mitted to treating all customers and em- ployees respectfully and fairly, irrespective of their origin, colour, language, gender or religiousorpoliticalbeliefs;

• Service orientation:Everyclient isservedin afriendly,competentandcourteousmanner. Our employees are committed to providing excellentservicetoallcustomers,regardless oftheirbackgroundorthesizeoftheirbusi- ness;

• High professional standards:Everyemployee takesresponsibilityforthequalityofhis/her workandstrivestodohis/herjobevenbetter;• A high degree of personal commitment:This goes hand-in-hand with personal integrity andhonesty–traitswhicharerequiredofall employeesinallProCreditinstitutions.

These ProCredit values represent the backboneof our corporate culture and are discussed andactively applied in our day-to-day operations.Moreover,theyarereflectedintheCodeofCon-duct, which translates the ProCredit group’sethicalprinciplesintopracticalguidelinesforallProCreditstaff.Inordertoensurethatstafffullyunderstand all of the principles that have beendefined,severaltrainingsessionswereconductedduringtheyearunderreviewatwhichcasestud-ieswerepresentedandgreyareasdiscussed.Wewill continue to conduct such training sessionsandincreasetheirfrequencyinthefuture.

Another aspect of ensuring that our institutionadheres to the highest ethical standards is ourconsistent application of international best-practicemethodsandprocedurestoprotectour-selves from being used as a vehicle for moneylaunderingorotherillegalactivitiessuchasthefinancingofterroristactivities.Theimportantfo-cushereisto“knowyourcustomer”,and,inlinewiththisprinciple, tocarryoutsoundreportingandcomplywiththeapplicableregulations.

We also set standards regarding the impactof our lending operations on the environment.NovoBancoAngolahasimplement-ed an environmental managementsystem based on continuous as-sessment of the loan portfolioaccording to environmental cri-teria, an in-depth analysis of alleconomic activities which po-tentially involve environmentalrisks, and the rejection of loanapplications from enterprisesengagedinactivitieswhicharedeemed environmentally haz-ardous and appear on ourinstitution’sexclusion list.Byincorporating environmentalissuesintotheloanapprovalprocess,NovoBancoAngolaisalsoabletoraiseitsclients’overall levelofenviron-mental awareness. We ensure that when loanapplicationsareevaluated,compliancewithethi-calbusinesspracticesisakeyconsideration.Noloansareissuedtoenterprisesorindividualsifitissuspectedthattheyaremakinguseofunsafeormorallyobjectionableformsoflabour,inparti-cularchildlabour.

Business Ethics and Environmental Standards

B u s i n e s s E t h i c s a n d E n v i r o n m e n ta l S ta n d a r d s ��

Our Clients

Ricardo Wambembe, a 29-year-old entrepre-neur, has been a NovoBanco client for twoyears.Hesubmittedhisfirst loanapplicationinJanuary2005.BeforeobtaininghisfirstloanforUSD 2,000, Mr. Wambembe ran “Ervanária Na-tura”,ashopfornaturalsupplementsandherbalconsulting, fromhishome.Hestarted thebusi-nessin1995.

Mr. Wambembe recently obtained a third loanforUSD6,500.Hehasusedtheloanstoincreasehisinventoryandbuynewequipmentforhiscon-sulting services. He opened another sales out-let in Kikolo, an area of northern Luanda wheredemandforhisservicesishigh.Mr.Wambembealsoboughtacar tohelpprocuremerchandise.Havinggrownhisbusiness,Mr.Wambembewasabletobuildhisownhouse.

PriortoapproachingNovoBanco,Mr.Wambembehadnoexperiencewithbanks.HewasattractedbyNovoBanco’sfocusonsmallentrepreneurs.Henow uses NovoBanco’s payment services, suchas cheques and international money transfers,to reimburse his suppliers in Brazil, Spain andPortugal.

Mr.Wambembehasmanyplansforhisbusiness.Hehopestoestablishaclinicfornaturaltherapies,settingupalaboratorytoproducehisownnaturalmedicines. He also hopes to plant a botanicalgardenforresearchpurposes.Mr.Wambembeisconfidentthat,withhisentrepreneurialspiritandNovoBanco’shelp,hewillachievehisgoals.

Ricardo Wambembe, Natural Herbs Consultant

A n n u a l R e p o r t 2 0 0 6�0

In a small shop in Bairro Mabor, Pedro Rosáriomanufactures beautiful leather sandals, bagsand belts, all of which he makes by hand. Helearned his profession in a training courseofferedbya localNGOthathelpstoreintegratethe physically handicapped into society. Aftercompleting his training, Mr. Rosário started hisbusinessin2003.

In2005AntónioDomingos joinedthebusiness.Thetwomenmeteachotheratthetrainingcen-tre.Theirrolesinthebusinessareclearlydefined;Mr. Rosário is responsible for the creative side,andMr.Domingosmanagesfinancialmattersandpurchasesmaterials.

At first, the business developed slowly since itlackedworkingcapital.Theycouldonlymanufac-turecustomers’ordersafterreceivinganadvancepaymentof50%toacquirethenecessarymateri-als.WithaNovoBancoloanforUSD200,Rosário

and Domingos acquired more leather and couldmanufacturedifferentmodelstoattractnewcli-ents.Mostoftheircustomersarefromthelocalneighbourhood, but some come from more re-moteareastopurchasethehandmadeproducts.

Both businessmen dream of a well-located andspaciousshopwheretheycanmanufactureandselltheirproductsonalargerscale.Withthehelpofemployeesandmoremodernequipment,theyhopetoincreaseproductionsothatclientsdonothavetowaitseveraldaysfortheirpurchases.Thetwomencountonalong-lastingrelationshipwithNovoBancotohelpthemfulfiltheirplans.

Pedro Rosário and António Domingos, Manufacturers of Leather Sandals

O u r C l i e n t s �1

Gabriel António Chinanga, Salt Trader

GabrielAntónioChinangastartedasmalltradingbusiness, buying articles in Luanda and sellingtheminBenguelaat theCapontemarkets.Withsavings from this business, he opened a smallshop, which he was forced to close when thearmedconflictescalated.

In2003hebegansellingsalt.Hepurchasedtheproduct from salt works and sold it at the BaiaFarta market. His clients were mainly womenwhoproducedriedfishforprovincesinAngola’sinterior.

Byreinvestinghisprofits,Mr.ChinangagrewhisworkingcapitaltomorethanUSD5,000.Sincehehadearnedareputationasareliableclientatthesaltworks,Mr.Chinangahadaccesstoasteadysupplyofsalt,Thiswasanimportantadvantagesincesalt isnotalwaysproduced in thequanti-tiesdesired.

Prior to banking with NovoBanco, Mr. Chinangareceived four loans from Banco de Poupançae Crédito. During a visit to Luanda, he learnedaboutNovoBancothroughthebank’smarketingcampaigns. When NovoBanco opened a branchin Benguela, he was one of the first clients. Heobtained a loan in April 2006, the Benguelabranch’sfirstmonthofoperations.HehassincetakenasecondloanfromNovoBancotopurchasesaltingreaterquantities.

With his growing income he was able to reno-vatehishomeandbuildasmallsnackbarinhisbackyard.Thesnackbarisalmostfinished;afterMr.Chinangabuysequipmentandmerchandise,itwillbeginoperations.

A n n u a l R e p o r t 2 0 0 6A n n u a l R e p o r t 2 0 0 6��

In1999ManuelAndradeopenedasmallmarketstallinBairroSamba.Henowrunsamini-marketwith the help of his wife, three daughters, sonandniece.

WhenMr.Andradewantedtoincreasehisinven-tory, he approached NovoBanco. He had heardabout the bank’s fast and simple credit pro-cedures. Having no previous experience withbanks, Mr. Andrade took out his first “MicroExpress” loan in April 2006. The loan was forUSD 1,000, and he repaid it in only four instal-ments. Mr. Andrade has since taken a second

loan for a higher amount and longer maturity.With this financing, he has increased his busi-nessvolumesubstantially.

Mr. Andrade works at a meat trading enter-priseandcannotalwaysbepresentatthemini-market. But he can count on the support of hisfamilymemberstorunthebusiness.Hiswife isresponsibleforweeklypurchasesfromdifferentwholesalersthroughoutthecity.

Mr.Andradeaimstoenlargethemini-marketandto become a wholesaler. To realise these ambi-tiousgoals,hewillcountonthehelpofhisfamilyandNovoBanco.

Manuel Andrade, Mini-Market Owner

O u r C l i e n t sO u r C l i e n t s ��

Financial StatementsFortheyearended31December2006

A n n u a l R e p o r t 2 0 0 6��

F i n a n c i a l S tat e m e n t s ��

A n n u a l R e p o r t 2 0 0 6��

Balance SheetAsat31December2006

Notes 2006 2005 in AKZ Assets CashandcashequivalentswiththeCentralBank 5 290,533,554 104,514,5143 Depositswithforeignbanks 6 43,462,508 39,333,994 Loansandadvancestocustomers 7 569,514,524 336,258,117 Placementsandsecurities 8 52,500,000 16,000,000 Intangibleassets AppA 17,519,156 20,513,287 Tangibleassets AppA 93,504,733 84,553,850 Accruedincomeanddeferredcosts 9 51,081,605 25,877,632 Otherassets 10 10,264,070 – Total assets 1,128,380,150 627,051,394 Equity and liabilities Deposits 11 594,486,440 219,596,363 Otherdeposits 1,668,438 1,747,280 Otherliabilities 18,381,124 1,320,943 Accruedcostsanddeferredincome 12 33,470,951 7,470,335 Provisionforgeneralbankingrisk 22,931,872 13,799,945 Debttobanks 13 80,000,000 – Total liabilities 750,938,825 243,934,866

Capital 14 391,058,220 391,058,220 Capitalmaintenancereserve 15 28,589,050 28,589,050 Accumulatedlosses (22,730,797) (2,248,826) Profit/Lossfortheyear 3,456,724 (20,481,971) Total equity 400,373,197 396,916,473

Total equity and liabilities 1,151,312,022 640,851,339

F i n a n c i a l S tat e m e n t s ��

Notes 2006 2005 in AKZ Interestandsimilarincome 227,212,679 106,753,134 Interestandsimilarcosts (26,371,368) (3,585,096) Interest margin 200,841,311 103,168,038

Feesandcommissionsreceived 16 53,357,289 25,031,670 Resultsfromfinancialoperations 17 (13,548,374) (16,104,159) Otherincomeandinterest 10,652,780 – Feesandcommissionspaid (1,443,807) (677,270) Operating banking revenue 249,859,200 111,418,279

Staffcosts 18 (91,927,216) (45,136,449) Administrativecosts 19 (104,005,091) (56,492,607) Fees,bonusesandothercosts (1,925,692) (1,367,864) Taxesandotherrelatedcosts (5,481,573) (3,403,398) Depreciation AppA (19,379,975) (11,909,774) Provisions 20 (23,682,929) (13,590,158) Operating profit/(loss) 3,456,724 (20,481,971)

Tax – – Profit/(loss) after tax 3,456,724 (20,481,971)

Income StatementFortheyearended31December2006

A n n u a l R e p o r t 2 0 0 6��

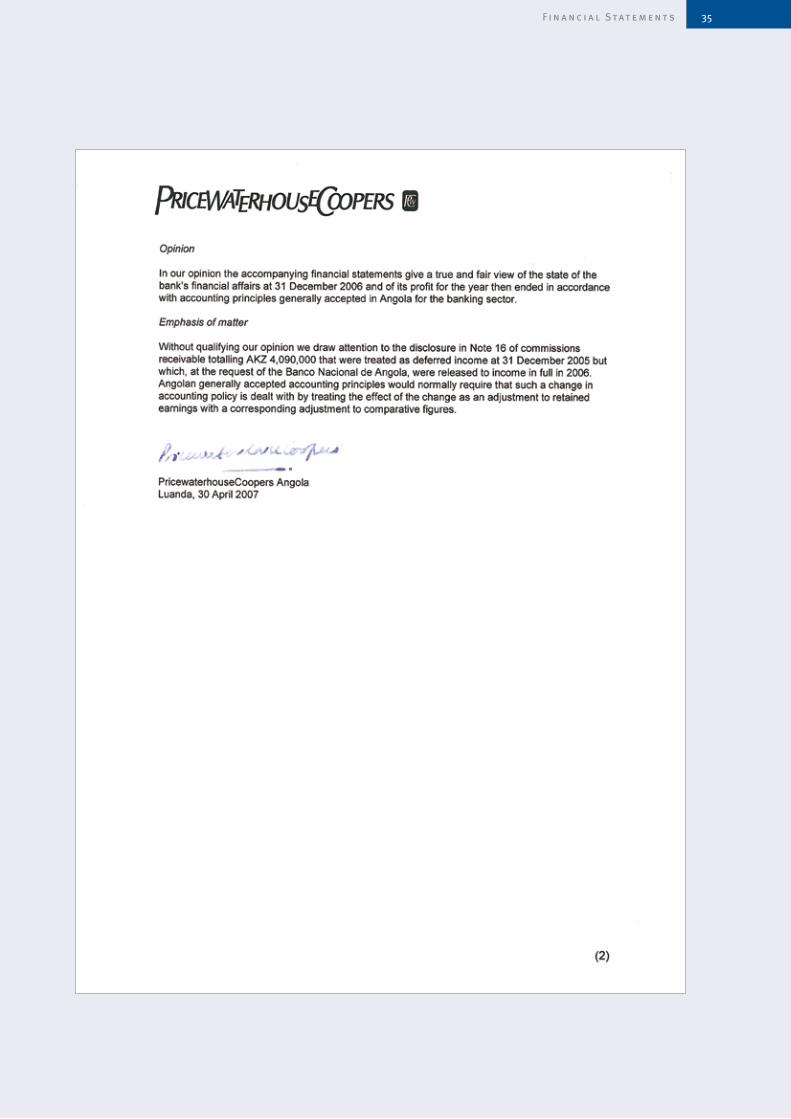

1. Constitution and activity

NovoBanco, S.A.R.L, is a Bank situated in Luanda and its share-holding is made up of private shareholders, some of which areinternational financial institutions. The Bank was constitutedon 19 February 2004 and commenced its commercial activity on20August2004.

2. Basis of presentation

The financial statements were prepared in accordance with theaccountingprinciplesestablishedintheAccountingRulesapplica-bletoFinancialInstitutionsinAngolaandotherregulationsestab-lishedandissuedbytheCentralBankofAngola(CentralBank).

3. Reporting currency

TheBankappliestheaccountingprinciplesandpoliciesestablishedby the regulations applicable to Angolan Financial Institutions.Theseregulationsrequirethepreparationoffinancialstatementsinlocalcurrency(AKZ),withinamulti-currencyreportingsystem.

4. Accounting policies

ThefollowingaretheprincipalaccountingpoliciesthathavebeenappliedinthepreparationoftheBank’sfinancialstatementsand,unlessspecificallystated,havebeenconsistentlyapplied.

a) Recognition of costs and expenses

Costsandincomeareaccountedforontheaccrualsbasis,irrespec-tiveofwhenitisactuallyreceivedorpaid.

b) Provision for general banking risks and overdue loans and interestProvisionsforgeneralbankingrisksweredeterminedinconformitywithDirective09/98,issuedbytheCentralBankon16November,1998.TherespectiveamountrecordedunderLiabilities-Provisionsforgeneralbankingriskscorrespondsto4%oftheloansandad-vancesgrantedbytheBank,includingamountsunderguaranteesissuedandotherreceivables.In2005,NovoBancohadprovidedfor3%oftheloansandadvancestocustomers.ThischangehasledtoanincreaseofAKZ5,732,968ingeneralbankingrisksprovisions.

c) Foreign currency transactionsMonetaryassetsandliabilities inothercurrenciesaretranslatedtoUSdollarsattheexchangeraterulingatthebalancesheetdate.Incomeandexpensesaretranslatedattheaverageexchangerateduringtheyear.TheAKZ/USDexchangeratesusedintheprepara-tionofthefinancialstatementsareasfollows:

Year ended at Average exchange Closing exchange rate rate 31.12.06 80.36 80.28 31.12.05 87.16 80.78

d) Fixed-income securitiesCentralBankSecurities(CBSs)andTreasuryBills(TBs)areissuedbytheCentralBankandaretradableontheAngolanmoneymarket.Thesesecuritiesarecarriedatnominalvalueinthefinancialstate-ments.Thediscount,whichisthedifferencebetweenthenominalvalueandtheamountpaid,isrecordedasdeferredrevenueandthenrecog-nizedasincomeonamonthlybasisuntilmaturityoftheinstrumentinaccordancewiththeCentralBank’srequirements.

e) Intangible and tangible assetsIn accordance with Angolan accounting requirements, intangibleassetsmainlycomprisepreliminaryexpensesandsoftware.Tangibleassetsareaccountedforattheirhistoricalcost.Duringtheyearnoassetswererevalued.Depreciation is calculated on the straight-line method using thedepreciationratesestablishedfor fiscalpurposes.Theseascribeusefullivesofbetween3and12yearstoNovoBanco’sfixedassetsand these are not considered to differ materially from the actualusefullivesoftheseassets.

f) Capital maintenance provision and reserveCapitalmaintenancereservesarecalculatedaccordingtoDirective01/2003issuedbytheCentralBankinordertomaintainthevalueof the original capital at the Kwanza equivalent of its historicalUSDollarvalue(SeeNote13).

g) Income taxThe bank is subject to taxation as provided for in the corporatetaxationcode.

5. Cash and cash equivalents with the Central Bank

2006 2005 Cash 187,864,850 54,626,603 Demanddepositswiththe CentralBank 102,668,704 49,887,911 290,533,554 104,514,514

DemanddepositswithCentralBank,at31December2006,includean amount of AKZ 44,114,657 (USD 549,487), which constitutesthestatutoryreserveasrequiredbytheCentralBank.According to Directive 10/2003, the coefficient of the statutoryreservesinlocalcurrencymustcorrespondto15%ofthebaseofassessment(customerdepositaccounts)and100%ofthecentralandlocalgovernmentdepositsregisteredinaccounts330000and330100,respectively,ofwhich7.5%maybemaintainedintreasurybillswitharemainingmaturityofatleast63days.TheBankmaydeductfromtheabove-mentionedreserves20%oftheaveragebal-ancesofcashinlocalcurrency.ThestatutoryreserveiscalculatedonaweeklybasisasrequiredbytheCentralBank.

6. Deposits with foreign banks

2006 2005 ProCreditBankGeorgia 32,079,544 33,064,054 DeutscheBankTrustCompany Americas 8,258,707 5,680,759 DeutscheBankAGFrankfurt 3,124,257 589,181 43,462,508 39,333,994

NovoBanco deposits surplus US Dollars with ProCredit BankGeorgia(CIS),whichisrelatedtothemajorityshareholder,when-everithassurplusliquidity.

Notes to the Financial StatementsFortheperiodended31December2006All amounts in AKZ unless otherwise stated

F i n a n c i a l S tat e m e n t s ��

7. Loans and advances to customers

2006 2005 Totalloans 608,783,867 352,961,760 Provisionfornon-performing loans (16,337,471) (2,903,698) 592,446,396 350,058,062

Loansinarrears (35,487,067) (7,963,125) 556,559,329 342,094,937

At31December2006thematurityofloansandadvanceswasasfollows: 2006 2005 In local currency Not indexed Upto3months 4,993,403 512,788 From3to6months 6,217,274 2,440,429 From6monthsto1year 5,571,207 3,255,737 Morethan1year – – 16,781,884 6,208,954 Indexed Upto3months 70,976,359 40,100,075 From3to6months 153,071,121 92,057,934 From6monthsto1year 289,319,385 202,731,261 Morethan1year 78,635,118 11,863,520 592,001,983 346,752,790

Total not indexed and indexed 608,783,867 352,961,760 Loans in arrears (35,487,067) (7,963,125) 573,296,800 344,998,635

Indexed loans and advances are loans granted in Kwanza butwhose value, repayments and interest are indexed to the USDexchangerate.

Loansandadvancesoverdueformorethan30daysat31Decem-ber 2006 amounted to AKZ 35,487,067 and were distributed asfollows:

2006 2005 From31to60days 6,553,154 4,801,218 From61to90days 7,458,044 352,744 From91to180days 16,572,653 2,228,650 From181to360days 4,903,216 580,513 35,487,067 7,963,125

8. Placements and securities

2006 2005 Treasurybills 52,500,000 16,000000

Treasurybillsonhandat31December2006matureasfollows:

9. Accrued income and deferred costs

2006 2005 Incomereceivable 32,107,793 6,685,273 Deferredcosts 18,973,812 19,192,359 Cashshortfalls – – 51,081,605 25,877,632

DeferredcostsincludeanamountofAKZ16,082,596(USD200,323)ofrentpaidinadvance.

Nominal value in AKZ Purchase price in AKZ Interest rate Purchase date Maturity date 21,500,000 20,904,020 5.70% 09-08-2006 07-02-2007 11,000,000 10,664,170 6.26% 04-10-2006 05-04-2007 20,000,000 19,327,600 6.96% 13-12-2006 13-06-2007 52,500,000 50,895,790

A n n u a l R e p o r t 2 0 0 6�0

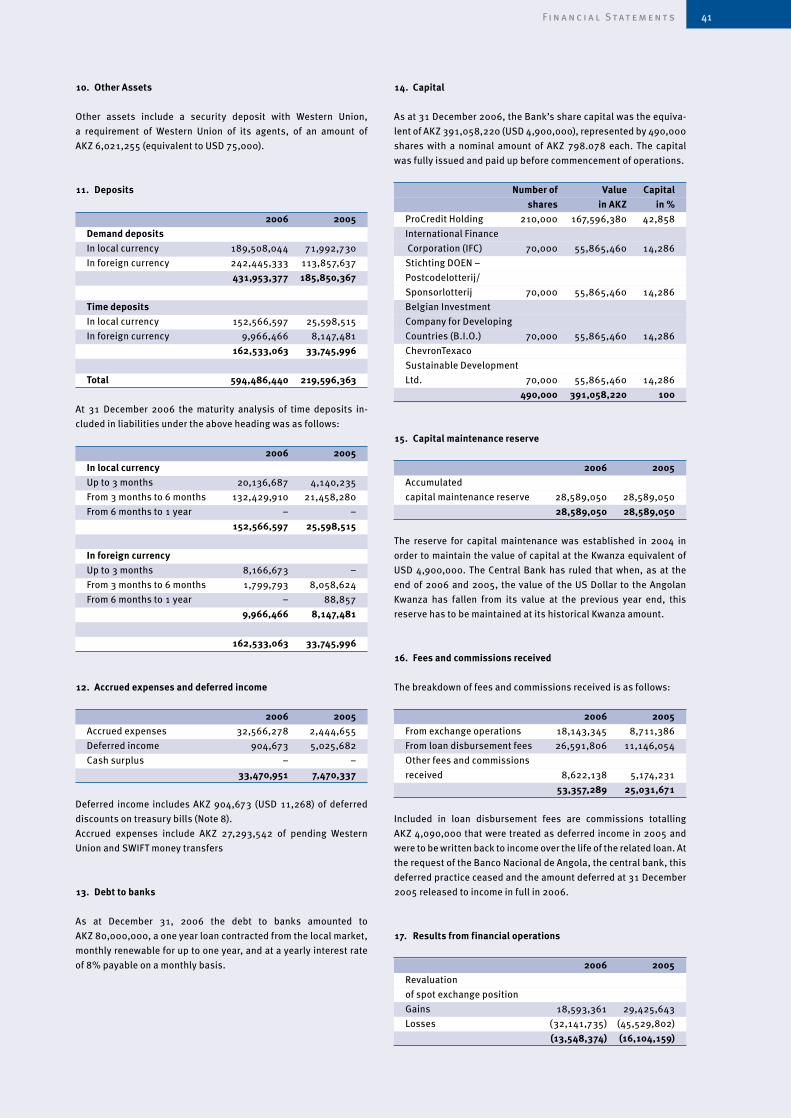

10. Other Assets

Other assets include a security deposit with Western Union,a requirement of Western Union of its agents, of an amount ofAKZ6,021,255(equivalenttoUSD75,000).

11. Deposits

2006 2005 Demand deposits Inlocalcurrency 189,508,044 71,992,730 Inforeigncurrency 242,445,333 113,857,637 431,953,377 185,850,367 Time deposits Inlocalcurrency 152,566,597 25,598,515 Inforeigncurrency 9,966,466 8,147,481 162,533,063 33,745,996 Total 594,486,440 219,596,363

At 31 December 2006 the maturity analysis of time deposits in-cludedinliabilitiesundertheaboveheadingwasasfollows:

2006 2005 In local currency Upto3months 20,136,687 4,140,235 From3monthsto6months 132,429,910 21,458,280 From6monthsto1year – – 152,566,597 25,598,515 In foreign currency Upto3months 8,166,673 – From3monthsto6months 1,799,793 8,058,624 From6monthsto1year – 88,857 9,966,466 8,147,481 162,533,063 33,745,996

12. Accrued expenses and deferred income

2006 2005 Accruedexpenses 32,566,278 2,444,655 Deferredincome 904,673 5,025,682 Cashsurplus – – 33,470,951 7,470,337

Deferred income includesAKZ904,673 (USD11,268)ofdeferreddiscountsontreasurybills(Note8).Accrued expenses include AKZ 27,293,542 of pending WesternUnionandSWIFTmoneytransfers

13. Debt to banks

As at December 31, 2006 the debt to banks amounted toAKZ80,000,000,aoneyearloancontractedfromthelocalmarket,monthlyrenewableforuptooneyear,andatayearlyinterestrateof8%payableonamonthlybasis.

14. Capital

Asat31December2006,theBank’ssharecapitalwastheequiva-lentofAKZ391,058,220(USD4,900,000),representedby490,000shares with a nominal amount of AKZ 798.078 each. The capitalwasfullyissuedandpaidupbeforecommencementofoperations.

Number of Value Capital shares in AKZ in % ProCreditHolding 210,000 167,596,380 42,858 InternationalFinance Corporation(IFC) 70,000 55,865,460 14,286 StichtingDOEN– Postcodelotterij/ Sponsorlotterij 70,000 55,865,460 14,286 BelgianInvestment CompanyforDeveloping Countries(B.I.O.) 70,000 55,865,460 14,286 ChevronTexaco SustainableDevelopment Ltd. 70,000 55,865,460 14,286 490,000 391,058,220 100

15. Capital maintenance reserve

2006 2005 Accumulated capitalmaintenancereserve 28,589,050 28,589,050 28,589,050 28,589,050

The reserve for capital maintenance was established in 2004 inordertomaintainthevalueofcapitalattheKwanzaequivalentofUSD 4,900,000. The Central Bank has ruled that when, as at theendof2006and2005, thevalueof theUSDollar to theAngolanKwanza has fallen from its value at the previous year end, thisreservehastobemaintainedatitshistoricalKwanzaamount.

16. Fees and commissions received

Thebreakdownoffeesandcommissionsreceivedisasfollows:

2006 2005 Fromexchangeoperations 18,143,345 8,711,386 Fromloandisbursementfees 26,591,806 11,146,054 Otherfeesandcommissions received 8,622,138 5,174,231 53,357,289 25,031,671

Included in loan disbursement fees are commissions totallingAKZ4,090,000thatweretreatedasdeferredincomein2005andweretobewrittenbacktoincomeoverthelifeoftherelatedloan.AttherequestoftheBancoNacionaldeAngola,thecentralbank,thisdeferredpracticeceasedandtheamountdeferredat31December2005releasedtoincomeinfullin2006.

17. Results from financial operations

2006 2005 Revaluation ofspotexchangeposition Gains 18,593,361 29,425,643 Losses (32,141,735) (45,529,802) (13,548,374) (16,104,159)

F i n a n c i a l S tat e m e n t s �1

Appendix AFixedassetsschedules–AKZ

Fixed assets Accumulated Fixed assets (gross) depreciation (net) Balance Acquisitions Balance Balance Charge for Balance as at as at as at the year as at 31 Dec 2005 31 Dec 2006 31 Dec 2005 31 Dec 2006 Preliminaryexpenses 5,444,408 – 5,444,408 2,570,970 1,814,803 4,385,773 1,058,635 Software 18,471,372 803,842 19,275,214 947,486 1,867,207 2,814,693 16,460,521 Intangibleassetsincourse 115,963 -115,963 – – – – – Total Intangible assets 24,031,743 687,879 24,719,622 3,518,456 3,682,010 7,200,466 17,519,156 Renovationofrentedpremises 27,969,256 13,504,712 41,473,969 2,743,314 3,733,696 6,477,010 34,996,959 Furnitureandmaterials 16,151,711 7,019,723 23,171,434 1,748,278 2,982,056 4,730,334 18,441,100 Equipment 37,917,220 17,865,749 55,782,968 6,734,081 8,982,213 15,716,294 40,066,674 Tangibleassetsincourse 13,741,336 -13,741,336 – – – – – Total tangible assets 95,779,523 24,648,848 120,428,371 11,225,673 15,697,965 26,923,638 93,504,733 Total fixed assets 119,811,266 25,336,727 145,147,993 14,744,129 19,379,975 34,124,104 111,023,889

ExchangerateasofDecember31,2006:1USD=80.28AKZ

18. Staff costs

2006 2005 Salariesandwages 71,051,746 39,461,856 Socialsecurityand otherrelatedcosts 7,219,212 3,859,694 Otherstaffcosts 13,656,258 1,814,899 91,927,216 45,136,449

Thenumberofemployeesasof31December2006was115(2005:49).

19. Administrative costs

2006 2005 Rentsandleasingcosts 19,511,286 13,971,912 Suppliesfromthirdparties 15,336,381 13,302,517 Communications 15,258,071 10,215,985 Securityservicesfees 12,311,902 6,794,082 Travelandentertainmentexpenses 7,345,127 1,049,763 Advertising 6,187,286 1,674,519 Repairsandmaintenance 3,520,113 4,038,813 Insurance 3,145,277 3,105,451 Notaryexpenses 503,642 1,113,929 Retainerfees 42,920 522,151 Otherservicesfromthirdparties 20,843,086 703,485 104,005,091 56,492,607

20. Provisions

2006 2005 Generalcreditrisks 23,682,929 13,590,158 Credit risks 23,682,929 13,590,158

21. Tax

Thereisnotaxtopayontheprofitfortheyearasprioryearlossesexceed 2006 profits. According to fiscal law in effect in Angola(Artigo46ºof“LegislaçãoFiscal:TributaçãodoRendimento),prioryears’lossescanbecarriedforwardforuptothree(3)years.

22. Other regulations

According to an exceptional authorization of the Central Bank,NovoBancocanmaintainanopenexchangepositionofupto50%ofthebank’sequityforaperiodnotlongerthan3years.TheamountinforeigncurrencyabovethelimitmustbesoldtotheCentralBank.Thespotpositionat31December2005was:

in USD 2006 2005 Assets Cashandcashequivalents atCentralBank 1,731,044 322,350 Currentaccount increditinstitutions 541,364 486,930 Total Assets 2,272,408 809,280 Equity & Liabilities Deposits (3,144,006) (1,424,590) Accrualsanddeferrals (375,478) (1,367) Total Liabilities (3,519,484) (1,425,957) Spot exchange position (1,247,077) (616,677) Global exchange position (1,247,077) (616,677)

F i n a n c i a l S tat e m e n t s����

Contact Addresses

Head Office

LuandaRuaN’Dunduma253MiramarTel.:(+244)222–430040Fax:(+244)222–430074

Branches

N’Dunduma BranchLuandaRuaN’Dunduma253MiramarTel.:(+244)222–430105Fax:(+244)222–430074

Rocha Pinto BranchLuandaRuadaPaviterra/RuadoParques/nBairroRochaPintoTel.:(+244)222–357420

Benguela BranchBenguelaLargo1ºdeMaios/n

C o n ta c t A d d r e s s e s ��

ProCredit Bank Serbia

ProCredit Bank Bosnia and Herzegovina

ProCredit Bank Kosovo

ProCredit Bank Albania

ProCredit Bank Macedonia

ProCredit Bank Sierra Leone

ProCredit Savings and LoansGhana

ProCredit Bank DemocraticRepublic of Congo

NovoBanco Angola

Banco ProCredit Mozambique

ProCredit Bank Ukraine

ProCredit Moldova

ProCredit Bank Romania

ProCredit Bank Kyrgyzstan(planned)

ProCredit Bank Georgia

ProCredit Bank Armenia(planned)

ProCredit Bank Bulgaria

ProCredit Mexico(planned)

Banco ProCredit Honduras(planned)

Banco ProCredit El Salvador

Banco ProCreditNicaragua

Banco ProCredit Colombia(planned)

Banco ProCredit Ecuador

Banco Los AndesProCredit Bolivia

An

nual

Rep

ort2

006

Ango

la

Annu

alR

epor

t200

6

An

gola