procurement & distribution interest group autumn symposium 2007

TRANSCRIPT

PROCUREMENT & DISTRIBUTION INTEREST

GROUP

Autumn Symposium 2007

http://www.pdig.org.uk/

Performance Management of Branded Medicines

PDIG Award

Kirsteen Docherty,

Procurement Services Manager,

UCLH Trust

Medicines Procurement

Free market Oligopoly Monopoly

Potential for Purchase/Contracting

Supplier Strategy

Generic Branded Branded

NationalSCEP

Trust or regional consortia• Therapeutic• P.I. tendering• Economies in

physical practice

Trust or regionalconsortia• P.I. tenders• Economies in

physical practice

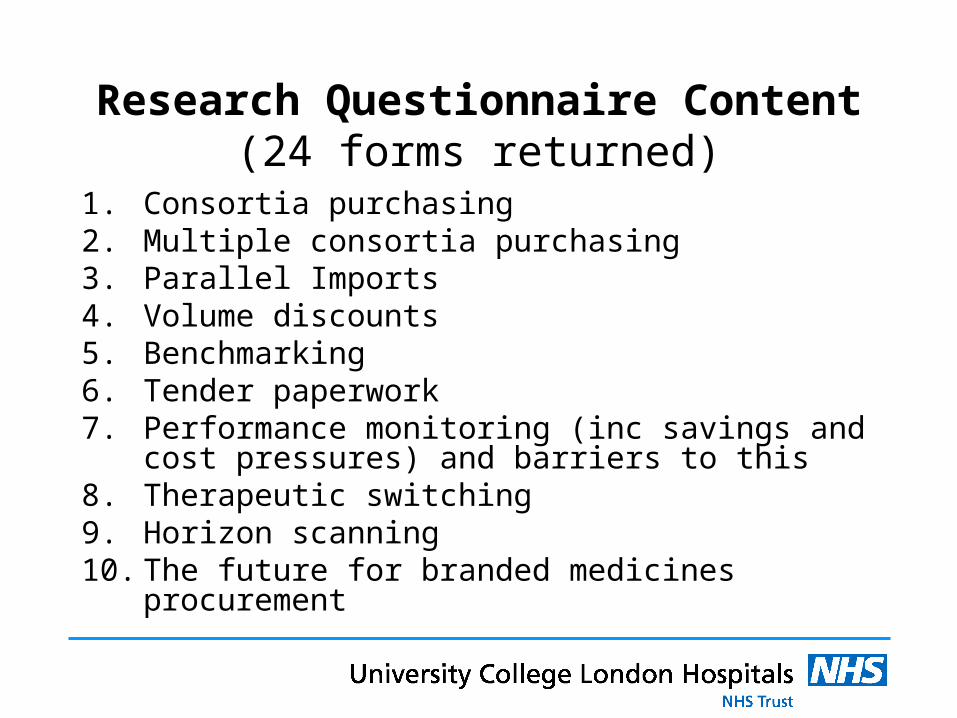

Research Questionnaire Content (24 forms returned)

1. Consortia purchasing2. Multiple consortia purchasing3. Parallel Imports4. Volume discounts5. Benchmarking6. Tender paperwork7. Performance monitoring (inc savings and cost

pressures) and barriers to this8. Therapeutic switching9. Horizon scanning10. The future for branded medicines procurement

Consortia purchasing

% of Trusts who are part of a purchasing consortium

88%

8%4%

YesNo (Trust not located in a consortia area)No (No perceived benefit)

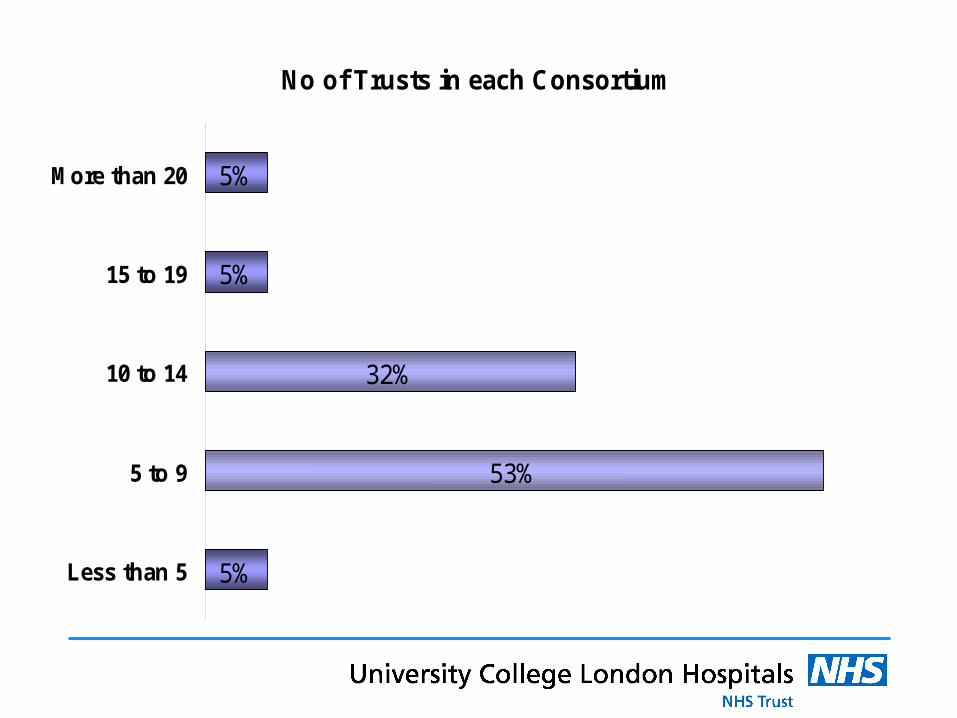

No of Trusts in each Consortium

5%

53%

32%

5%

5%

Less than 5

5 to 9

10 to 14

15 to 19

More than 20

Impact of size of purchasing organisation

SingleHospital Trust

Consortium Regional/ Division

National/Division

Purchasing Power

Size of Organisation

Ease of Co-ordination

22%

11%

17% 17%

33%

0-10% 10-25% 25-50% 50-75% 75%+

% of contracts tendered by consortium rather than individual trust

Reasons for not tendering all contracts as consortia?

0% 10% 20% 30% 40% 50% 60% 70%

Contract start and end dates do not coincide

Other

Award decisions more complex with more Trusts

Difficult to co-ordinate the different Trust

No perceived benefit for certain products

Different products used within the Trusts

Multiple consortium purchasing together

% of Trusts interested in becoming involved in multiple consortium purchasing.

Yes – 86% No – 14%

Respondents perceptions on effectiveness of multiple consortia purchasing

Price transparency

2, marginally effective

9%

3, fairly effective

23%

4, mostly effective

49%

5, highly effective

14%

1, not effective

5%

Achieve same price regardless of Trust size

1, not effective

0%

4, mostly effective

45%

5, highly effective

32%

2, marginally effective

9%

3, fairly effective

14%

Higher savings

1, not effective

5%

2, marginally effective

14%

3, fairly effective

23%4, mostly effective

44%

5, highly effective

14%

Reducing tender work load within Trusts

3, fairly effective

32%4, mostly effective

27%

5, highly effective

27%

1, not effective

5%

2, marginally effective

9%

Potential problems with multiple consortia purchasing?

54%

54%

29%

8%

17%

17%

0% 10% 20% 30% 40% 50% 60%

Other

Monitoring uptake of contract

Reluctance of Trusts to take part

Agreement on contract award

Adherence to contract award by individual trusts

Reluctance of companies to take part

Parallel Importing

% of Trusts who tender for parallel imports?

Yes – 83% No – 17%

Factors that may prevent the purchase of PI’s?

• Continuity of supply 54%

• Labelling/packaging 54%

• Counterfeiting 42%

• Reputation of supplier 8%

• Sourcing 4%

• Limited discounts available 4%

Volume Discounts

• Ability to take advantage of large volume discounts?Yes – 79% No – 21%

• Approx 50% of those who can take advantage stated this was because of access to a regional store

Benchmarking pricesFrequency of price benchmarking

Never37%

Quarterly21%

6 monthly4%

Yearly21%

Other17%

Reporting on procurement performance?

62% of respondents compile a yearly report on procurement performance.

Information included in the report;• Savings achieved 100%• Tendering work undertaken 80%• Further savings opportunities 80%• Work plan for next year 53%• Other 13%

Reporting on procurement performance?

Who is interested in seeing the report?

• Senior pharmacy managers 93%

• Finance director 87%

• CEO 33%

• Trust procurement mgr 27%

• Procurement hub 20%

• Other 13%

Savings

• 83% of respondents measured contract savings

• 34% were given a savings target per annum from the medicines budget

• 31% had medicines savings removed from the medicines budget

Price increases

1. 71% of respondents measured price increases

2. How often price increases are measured?

18%

18%

0%

12%

53%

2 monthly

Quarterly

6 monthly

Yearly

Other

Cost pressure analysis

Definition: Monitoring the medicines budget using price changes and volume changes.

43% of respondents use cost pressure analysis (30% of these use this for all branded medicines)

Who is cost pressure analysis work shared with?

• Finance director 80%

• Senior pharmacy mgr 70%

• Trust procurement mgr 20%

• Other 20%

• CEO 10%

Other performance monitoring tools

• Compilation and review of high expenditure 96% branded products e.g. Top 100.

• Value, number or % of high expenditure branded 71%products without a contract

• The number/ % of branded lines tendered per annum 25%

• The average % discount for branded lines as a whole 13%

• The average % discount for branded lines per company 4%

• The average % discount per therapeutic group 0%

Suggested other performance measurements

• Supplier performance monitoring

• Price tracking in relation to patent expiry

• Impact of entry of competitor products

• Opportunities for therapeutic switching

Barriers to measuring branded medicines contracting performance

0%

0%

25%

38%

46%

88%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Other

Concerns about poorperformance

Data management skill

Inflexible IT systems

Low priority

Insufficient staffresources

Therapeutic Switching

• 83% of Trusts are currently involved in therapeutic switching

• For 73% of those Trusts the pharmacy procurement team are involved

Therapeutic switching, easy or difficult?

2, fairly easy24%

3, neither easy or hard

47%

4, fairly hard19%

5, very hard10%

Key problems with implementation of therapeutic switching

• Reluctance to change 50%• Clinical concerns 42%• Insufficient resources 42%• Industry funding (linked to product) 13%• Other 13%• Lack of clinical data 8%• Other priorities 4%• Insufficient savings 4%

Respondents views on future structures for branded medicines procurement

• Involvement of NPSG & PMSG 88%• Collaboration between Trust procurement, 83%

consortium and PaSA• Collaboration between Trusts in form of 67%

consortium• Multiple consortia purchasing 67%• CPH involvement 21%• NHS Supply Chain involvement 17%• Trusts supply dept involvement 17%

What are the current trends in branded pharmaceuticals management?

• More collaboration between Trusts and Consortium e.g. LPP. Trust contracting likely to decrease further.

• Increased use of branded medicine tendering

• Companies increasingly offer volume based frameworks

What are the current trends in branded pharmaceuticals management?

• Introduction of payback schemes e.g. Velcade.

• Increase in treatment of patients within their home environment

• Increase in development of biotech drugs – decreased competition, limited tender/negotiation opps.

• Encouragement of therapeutic switching across multi-consortia e.g. LPP.

Why are we contracting for branded medicines?

• Current PPRS profit cap model is not effective at controlling prices?

• OFT proposal for value/ evidence based pricing by NICE. Takes

branded medicine management work load from local and multi-consortia to national level.

• Reference pricing in New Zealand & Australia and cross product strategic agreements in New Zealand.

• Govt/PPRS and manufacturer price negotiations prior to product launch e.g. French model.