prodding the giant - dhanlaxmi bank - nov 1.pdf · prodding the giant. 2 contents 1. introduction:...

TRANSCRIPT

Knowledge Series 9

DhanBank PRU Tracks The

Renewed Blossoming Of The Indian

Automobile Market.

Prodding The

Giant

2

Contents

1. Introduction: Ignition

2. The Road Till Now

3. Engine Check: Regulatory Framework

4. On The Road: Current Status

5. Major Players

6. How Deep Are Their Pockets?

7. First Cousins: Auto Ancillary

8. SWOT Analysis

9. The Road Ahead

Page

3

4

5

6

11

13

14

15

16

3

Ignition

A robust transport system is an imperative for any nation’s rapid development. In the Indian economy, the

automotive industry — comprising the main vehicle manufacturers as well as companies making and

supplying spare parts and components to vehicle makers (called the auto components sector) — occupies

a critical place.

It has profound and meaningful backward and forward linkages to various sectors. Due to this it has a strong mul-

tiplier effect, qualifying to be called an economic growth driver.

Besides, the auto sector provides large-scale direct and

indirect employment and is one the largest India’s in-

dustries.

After the industry was delicensed in 1991, the Indian

auto sector has witnessed huge growth, as it underwent

restructuring, absorbed latest technology, strived to

meet global standards and realise its potential. Deregu-

lation has also paved the way for the entry of global

auto giants into the Indian market.

India has the second-fastest growing automobile market

in the world after China. It has developed a globally

competitive auto ancillary industry.

The country is the world’s largest manufacturer of tractors and 3-wheelers, second largest 2-wheeler maker, fourth

largest maker of commercial vehicles and seventh largest producer of passenger vehicles. It is Asia’s fourth largest

and the world’s eleventh largest passenger car market. India has also established automobile testing and research

& development centres.

The major growth drivers of the Indian automobile market are:

rising middle class working population and urbanisation;

increasing disposable incomes in the hands of people, even rural sector;

growing per capita income;

cheaper financing alternatives;

favourable government policies;

a wide array of models to meet diverse preferences, needs and aspirations;

increased road network over the years that has catalysed integration of domestic markets;

weak public transport system to sustain the movement of people and commodities.

4

The Road Till Now

B efore the 1980’s, the only models to be found on Indian roads were the grandfatherly Ambassador from

Hindustan Motors and the vintage Premier Padmini. These were the domestic versions of popular inter-

national brands Morris Oxford of the 1950s, and Fiat Milicento 1100 respectively.

The sector was severely restricted by ‘licence raj’. Production was confined to three manufacturers – Hindustan

Motors, Premier Automobiles and Standard Motors -- and could not exceed 40,000 a year for almost three dec-

ades.

Pricing was state-controlled and there was no indigenous expertise. Employing scientific know-how and techni-

cians from abroad was cumbersome. The end of the 1970s witnessed failing JVs for light commercial vehicles.

However, as the 80s dawned, new models such as Contessa, Premier 118NE, and the Rover were launched in the

market.

The launch of Maruti 800 in 1983 changed the face of India’s car market forever. From the presence of mainly two

models before 1983, India has come a long way in offering a wide product portfolio of passenger cars.

The Changing Curves

5

Engine Check: Regulatory Framework

T he auto industry was delicensed under the New Industrial Policy of 1991, but passenger car manufacturing

got delicensed only in 1993. Except in some special cases, no licence is required to set up a manufacturing

facility for automobiles.

100% FDI is permissible under the automatic route.

Till December 2009, the government automatically allowed payments of up to $2 million along with roy-

alty of 5% on domestic sales and 8% on exports

for technology transfers. In case of no technol-

ogy transfers, royalty of up to 1% on domestic

sales and 2% for exports was automatically al-

lowed on use of trademarks and brands of the

foreign partner. Beyond these limits, government

approval was required. But in December 2009,

the government decided to waive off these re-

strictions. Royalty payment without caps was

automatically approved.

The customs duty on import of various automo-

biles and components ranges from 10% to 100%.

This is a way of protecting Indian manufacturers

from the onslaught of international players as it

makes their automobiles expensive in compari-

son.

Even the import of second-hand cars is discour-

aged through a complex, unfavourable deprecia-

tion formula, coupled with a steep and multi-

layered customs duty tariff card.

In Budget 2010-11, the ad valorem component

of excise duty on large cars, MUVs, SUVs was

increased by 2% to reach 22%.

The royalty payment clause has hit Maruti’s Q2 FY11 profits as it surprisingly raised the royalty payments on few

models of cars in Q1.

The Indian automobile sector has mainly four segments: Passenger vehicles, CVs, two-wheelers and three-

wheelers. Post delicensing, the industry has had a mix of Indian and foreign companies operating in the country.

They are present either individually, or through JVs, or collaborations, or wholly-owned subsidiaries (the last one

in case of MNCs).

A different kind of track

6

On The Road: Current Status

O ver a seven-year period, production has almost doubled to 140.5 lakh units, growing at a CAGR of 12%.

Over the same period, sales grew at a CAGR of 10% while exports registered an impressive 25% growth.

During the years of slowdown (2007-08) the industry faced a decline of 2.4 lakh units in production,

owing to reduced domestic demand.

The situation remained almost same the following year. However, the mood turned upbeat by 2009-10. In the past

seven years, 2009-10 witnessed the best growth in production and sales -- 26%. There was lot of pent-up demand

in the system, and once the economy began to improve, demand was unleashed. It was further supported by the

stimulus package, release of the Sixth Pay Commission arrears, lower interest rates, and new model launches.

7

The pie charts on page 6 show the change in market share of various segments. A major share of the domestic auto

market was garnered by two-wheelers. Two-wheelers have remained a favourite medium of transport mainly on

poor rural roads. However, over the past seven years, the share of passenger vehicles has risen consistently but it is

still quite less compared to other economies of the world, which leaves a huge scope for penetration in the market.

Segment-wise Scenario

Passenger Vehicles

The passenger vehicle segment comprises passenger cars and multi-utility vehicles (MUVs, which includes sports

utility vehicles). Post delicensing, this sector witnessed entry of foreign carmakers through JVs, collaborations and

wholly-owned subsidiaries. This has not overwhelmed domestic players (such as Maruti, Tata or M&M) which

have emerged as market leaders, adapting through alliances with foreign companies for technology. Now some

domestic players have also started entering foreign markets.

As per SIAM, passenger cars are classified on the basis of length into mini (</=3,400mm), compact (3,400-

4,000mm), mid-size (4,001-4,500mm), executive (4,501-4,700mm), premium (4,701-5,000mm) and luxury

(>5,000mm).

Earlier cars were classified on the basis of price into segments A (< `3 lakh), B (`3-5 lakh), C (`5-10 lakh), and E

(>`25 lakh). MUVs are classified on the basis of seating capacity — seven, nine, and 13-seaters.

Passenger vehicle production and sales have more than doubled over the past seven years, while exports have treb-

led. Production has grown at a CAGR of 16%, sales at 14%, and exports by a massive 23% -- all highlighting the

euphoria in the sector over the past few years.

And what’s better, the trend seems to be strengthening as market penetration in India is still very low at eight cars

per 1,000 persons. Vigorous competition among companies has proved better for customers as prices have re-

mained competitive. Sales, which had remained stagnant during the recent slowdown, picked up impressively in

2009-10 -- by 26% -- owing to positive customer sentiment.

For 2009-10, European nations were the main destination for passenger car exports and this growth was led

mainly by the scrappage scheme rolled out by these nations, under which incentives were offered by the govern-

ments there to buy new cars in exchange of old ones.

Governments of some European nations, such as the UK, introduced the scrappage scheme in May 2009 to boost

8

their ailing car industry and remove polluting vehicles from the road. It was declared to have ended successfully in

March 2010. The UK government declared a grant of £2,000 for scrapping an old car in exchange for a new one.

This pushed up sales and accounted for one fifth of the total new car registrations. The scheme was successful in

Germany and France too.

Compact cars account for the major chunk of the sales (at present 72%) as India has been a small-car market, ow-

ing to high demand for cost-effective means of transport. But now, customers are upgrading, driven by higher per-

sonal disposable incomes, changing preferences in the process. Nine and seven seaters account for three-fourth of

total MUV sales.

Growth will be driven mainly by urbanisation, changing lifestyles, expanding rural demand, increasing exports,

government support and, finally, improved road infrastructure. Increasing pressure on public transport infrastruc-

ture, which is almost on the brink of collapse, could also prompt individuals to opt for private vehicles.

The major car-makers operating in India are Maruti Suzuki (market leader), Hyundai, Tata Motors, General Mo-

tors, Ford, Skoda Auto, Honda, Toyota, Fiat, Mahindra Renault, Hindustan Motors etc.

The major MUV players are Mahindra & Mahindra (market leader), Toyota Kirloskar, Tata Motors, General Mo-

tors, Maruti Suzuki, Force Motors, Ford, Hindustan Motors etc.

Commercial Vehicles

This segment comprises light commercial vehicles (LCVs) and medium & heavy commercial vehicles (M&HCV).

They are classified on the basis of gross vehicle weight (GVW) -- LCVs have less than 8 tonnes of GVW, MCVs

have between 8-16 tonnes, and HCV have GVW of over 16 tonnes. LCVs are mostly goods carriers or passenger

carriers, and M&HCV are either trucks or buses.

LCVs are found quite suitable for Indian roads as they are compact compared to M&HCV, making them smoother

and more efficient. But the purpose served by the two categories is quite different. LCVs are used mainly for intra-

city transport – most commonly as pick-up trucks, small ambulances and delivery vans. M&HCVs are used for

transportation of heavy commodities such as cement, steel and fertilisers.

In the LCV category Tata Ace is an innovation that has changed the tone of the trucking business. It was launched

in May 2005 by Tata Motors to not only counter competition from the three-wheeled goods carriers from Bajaj

Auto, Piaggio, Mahindra and Force Motors, but to also boost the company’s flagging LCV sales. It created a

whole new mini sub-segment in India and filled the gap in the small commercial vehicles. Tata Ace, India’s first

9

mini truck, is ideal for short, narrow village roads as well as for negotiating traffic on city roads, for the small yet

bulky loads. It created history by selling five lakh units within five years of launch. Mahindra & Mahidnra

launched Maxximo in 2010 to compete with Tata Ace and is doing quite well.

The growth of the CV industry is mainly dependent on industrial growth and road infrastructure development; in

turn it’s a barometer of economic growth. Since India has emerged as the second fastest growing economy after

China, it has witnessed an increase in demand for CVs. Although there is some competition in the LCV market,

the M&HCV segment is dominated by two companies which comprise the entire segment – Tata Motors and

Ashok Leyland. There are a few other LCV manufacturing companies, such as M&M, Eicher Motors, Swaraj

Mazda and Force Motors. Most of the domestic demand is met through local production.

Among all segments in the automobiles sector, CVs was the only one to witness a sharp decline when the econ-

omy faced troubled times. This again reaffirms the fact that its fortunes are closely, and directly, tied to that of the

broader economy. The year 2008-09 saw a sharp decline of 24% in production and 22% in sales due to low indus-

trial activity and dipping business sentiment thanks to the worldwide slowdown.

However, due to improvement in 2009-10, the sector grew 36% in production and 38% in sales, surpassing the

peak of 2007-08 in terms of absolutes. Although exports showed improvement, it was lower than 2007-08, owing

to the continuing bleak situation in the developed world.

When assessed over a period of seven years, the sector registered an impressive 13% CAGR in production as well

as sales. Exports have grown at a CAGR of 17%. Market share of CVs improved over the years, and with the pros-

pects for growth in the Indian economy, the only way forward for this segment is upwards.

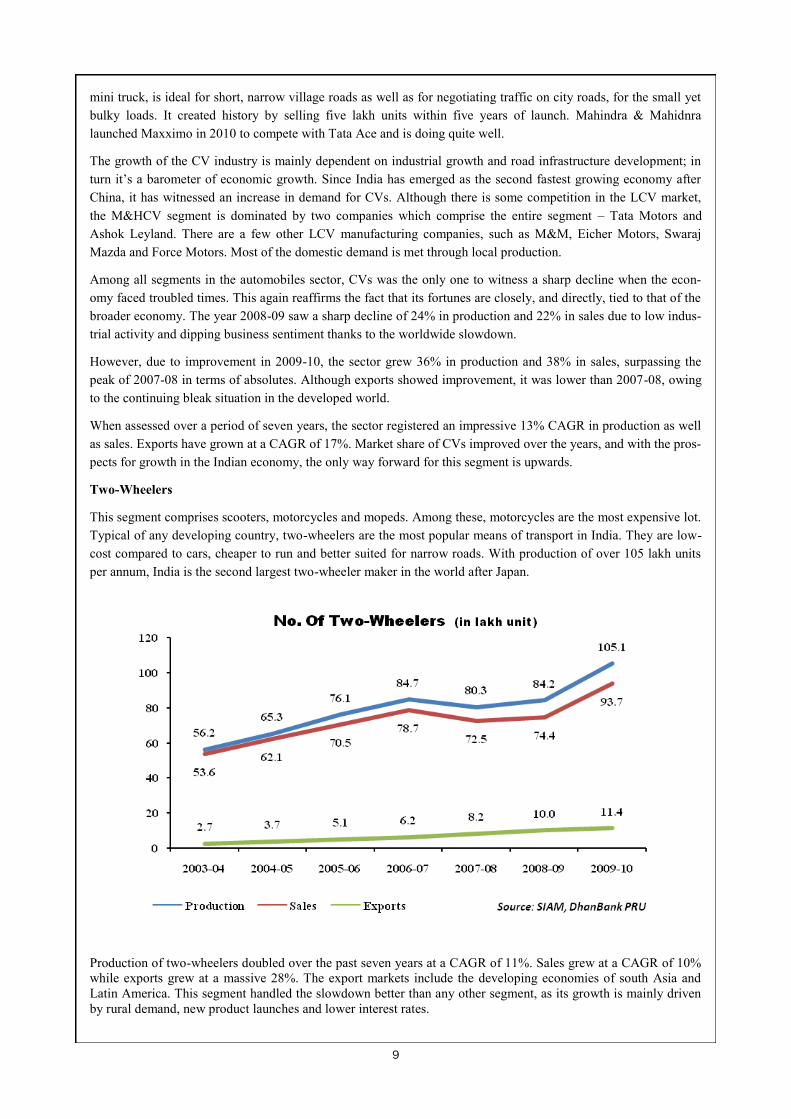

Two-Wheelers

This segment comprises scooters, motorcycles and mopeds. Among these, motorcycles are the most expensive lot.

Typical of any developing country, two-wheelers are the most popular means of transport in India. They are low-

cost compared to cars, cheaper to run and better suited for narrow roads. With production of over 105 lakh units

per annum, India is the second largest two-wheeler maker in the world after Japan.

Production of two-wheelers doubled over the past seven years at a CAGR of 11%. Sales grew at a CAGR of 10%

while exports grew at a massive 28%. The export markets include the developing economies of south Asia and

Latin America. This segment handled the slowdown better than any other segment, as its growth is mainly driven

by rural demand, new product launches and lower interest rates.

10

Although the segment contributes the largest chunk towards the Indian automobile sector in terms of units manu-

factured, it still has a lot of potential as demand for two-wheelers for regular mobility still remains high. Promi-

nent companies are Hero Honda (market leader), Bajaj Auto and TVS Motor.

Three-wheelers

Not many countries in the world make three-wheelers. India is the largest manufacturer and seller of this category.

Three-wheelers are used mainly for public transportation in rural and semi-urban areas and some metros. They are

also used as intra-city goods carriers. Prominent players include Bajaj Auto, Piaggio Vehicles, Mahindra &

Mahindra, TVS Motors, Atul Auto, Scooters India and Force Motors. This segment has not seen much innovation.

And if it does innovate, the segment runs the risk of facing competition from small commercial vehicles in the

goods carrier segment.

Over the past seven years, production in the segment improved at a CAGR of 10% while sales rose 8%. Exports

had a better CAGR of 17%. During the slowdown, this segment remained stagnant but picked up in 2009-10 with

25% growth in production and 26% in sales.

11

Major Players

Maruti Suzuki

The largest passenger car maker in India, it had a market share of over 50% in FY10. However, Q1 FY11 saw its

market share shrink to 47.7% on a YoY basis. It has the widest portfolio in passenger cars, with a special focus on

the compact car segment. It has an installed capacity of one million units per annum, the largest dealer network,

and the most extensive after-sales service network in the country. Suzuki Motor Corporation of Japan holds 54%

stake in it.

Maruti Suzuki offers Alto, Omni, Versa, Wagon-R, Estilo, Swift, A-Star, Ritz (launched in May 2009), SX4, and

DZire in the passenger cars category (Baleno withdrawn). It decided to stop the production of Maruti 800 and

phase it out from 13 major cities effective April 1, 2010, mainly because India adopted the Bharat Stage IV emis-

sion standards (equivalent to Euro IV standards), which requires car makers to upgrade their vehicles accordingly.

It offers Gypsy and Grand Vitara (launched in July 2009) in the MUV segment.

Maruti Suzuki made history in 2009-10 by be-

coming the first Indian car maker to achieve sales

of over 10 lakh (one million) units. It sold 10.2

lakh cars – 8.7 lakh units in the domestic market,

and exported 1.5 lakh units, both highest ever by

an Indian company. It sold 2.78 lakh units in July

-September 2010, registering the highest ever

domestic quarterly volume sales, growing 33%

over the previous corresponding quarter.

However, input prices have been rising; and any

further increase may put pressure on margins.

Also, the market is getting more competitive and

with the launch of newer compact cars by com-

petitors, Maruti’s position could be threatened. A price war cannot be ruled out in such a scenario. Maruti reported

a modest 5% rise in net profit for Q2FY11 ended September 30, 2010, due to increased royalty payments, rising

input costs and exchange rate fluctuations.

Hyundai

It is the second largest player in India, with around 25% of the market share. It has remained the largest exporter

of cars from India, mainly to European Union, Africa, west Asia, Latin America, Asia and Australia. Its portfolio

includes Santro, i10, Getz, i20, Accent, Verna, Elantra and Sonata Transform in the passenger car category, while

Tucson and Terracan are in the SUV segment. The car has recently launched its famed Sante Fe SUV model.

Hyundai recorded an 18% growth in the July-September 2010 quarter in the domestic sales category with 0.89

lakh units.

Tata Motors

It is the third dominant company in passenger vehicles, with a wide portfolio that ranges from SUVs to the world’s

cheapest car – Nano. The passenger cars category includes Indica, Indigo and Nano. Also, it jointly owns an as-

sembly line with European automaker Fiat to manufacture Palio Stile, 500, Linea and Grande Punto. In MUVs, it

offers Safari, Sumo, and Xenon. Its products are considered value-for-money and run mainly on diesel, which is

cheaper then petrol. In the luxury car segment, it offers the celebrated Jaguar and Land Rover models worldwide

and now in India too (it acquired JLR from Ford Motors in 2008).

12

In the commercial vehicles segment it offers Prima, Construck, and Tata Novus in the M&HCV category, and TL

4*4 in the LCV category. Tata Motors dominates the M&HCV segment with a market share of over 60%.

Tata Motors recorded an impressive YoY growth of 36% to 0.83 lakh units in the July-September 2010 period in

the passenger cars segment.

M&M

In the passenger vehicles category, Mahindra & Mahindra (M&M) is a large local manufacturer and derives a ma-

jor chunk of sales from SUVs, where it is a clear market leader with a share of 52%. It has a sizeable share of 30%

in LCVs. Its portfolio includes Scorpio, Bolero, and Xylo in MUVs and Alpha and Champion in 3-wheelers. It has

a tie-up with Renault to make passenger cars (Logan) and Navistar for CVs.

Ashok Leyland

It is the second largest CV player after Tata motors. It is focused on the M&HCV segment, with a share of 29% of

the market and has a significant presence in the bus segment. It formed a JV with Nissan in 2008, which will now

see them roll out three LCVs in three years starting from mid-2011.

Hero Honda

Hero Honda is the world’s largest two-wheeler maker in volume terms. It has a production capacity of 5.5 million

two-wheelers per annum. Almost half of the motorcycles sold every month in India are made by this company . Its

portfolio covers all three major segments of motorcycles -- CD Dawn and CD Deluxe in the entry level category;

Passion, Splendor and Glamour in the executive segment; and Achiever, Hunk, CBZ and Karizma in the premium

segment.

Hero Honda was promoted by a JV between the Hero group and the Honda Motor Company, with each holding

26% stake in the venture. Hero Honda will see lot of competition in the executive segment and rising input costs

will remain a cause of worry. The margins and profit growth may slow.

Honda Motorcycle and Scooters (HMSI) has planned a Rs 500-crore, six lakh units per annum two-wheeler plant

in Rajasthan. In the next phase, the investment will be raised to Rs 1,100 crore and production to 12 lakh units p.a.

Bajaj Auto

With a market share of 25%, Bajaj Auto is India’s second largest two-wheeler maker. It also offers products in all

three segments of motorcycles – Platina in the entry segment, Discover in the executive segment and Pulsar in the

premium segment. It is the largest manufacturer of 3-wheelers in India. While its performance is improving rap-

idly, increasing input costs and higher selling costs due to intense competition may hit margins.

Bajaj dominated the scooters market till the 1990s with brands like Chetak and Super. However, with the coming

of motorcycles, mainly in the 1990s, it suffered and its sales have since dropped to a mere couple of hundred units

per month in 2009. It stopped making the iconic Bajaj scooters in December 2009 and now aims to be the world’s

top motorcycle maker.

13

How Deep Are Their Pockets?

F inancials of the top automobile makers show that the sector has been in a boom mode in 2009-10, due to

higher demand, improving economy, increased industrial activity, cheap financing (lower interest rates on car

loans, etc., and zero financing charges by financiers), and higher disposable incomes. Following are a few parame-

ters reflecting the financial performance of the industry. The industry profit is lower than the top six companies’

profit due to losses registered by companies such as Hindustan Motors, LML, Scooters India and VCCL (owned

by LML group). Despite that the industry as a whole registered an impressive performance as a major chunk of the

business is contributed by the top six players.

Annual (in Rs crore)

Company

March

2010 Growth

March

2010 Growth

March

2010 Growth

March

2010 Growth

March

2010

Growt

h

Income FYoFY Net sales FYoFY Raw

materials FYoFY

PBDIT FYoFY

Net

profit FYoFY

Tata Motors 37,447 41% 35,593 39% 24,906 36% 4,967 94% 2,240 124%

Maruti Suzuki 30,120 40% 29,623 42% 22,607 42% 4,451 83% 2,498 105%

M&M 19,021 41% 18,602 42% 12,357 36% 3,374 126% 2,088 141%

Hero Honda 16,117 28% 15,861 28% 10,730 22% 3,023 54% 2,232 74%

Bajaj Auto 12,065 35% 11,921 35% 8,118 26% 2,553 131% 1,700 160%

Ashok Leyland 7,315 21% 7,245 21% 5,211 16% 830 64% 424 123%

Financial Performance For Full Year (Rs cr)

Important Parameters Mar-09 Mar-10 Fy-o-FY

Income 96,537 130,142 35%

Net Sales 93,748 126,566 35%

Other & extra-ordinary income 2,788 3,577 28%

Expenses 90,590 119,606 32%

Raw materials 68,330 89,413 31%

Salaries and wages 5,230 6,025 15%

Total other expenses 11,693 14,867 27%

Interest expenses 1,167 1,529 31%

Depreciation 2,609 2,980 14%

Total tax provision 1,557 3,916 151%

PBDIT 10,524 19,820 88%

Net profit 5,190 11,395 120%

Source: CMIE, DhanBank PRU

Source: CMIE, DhanBank PRU

Note: Note: companies which are listed on Indian bourses and have comparable results for

the two years have been taken. Companies such as Hyundai and few other prominent com-

panies are not listed on Indian bourses, so the actual size of the sector is much bigger than

what is depicted here."

14

First Cousins: Auto Ancillary

T his industry is closely linked to the automobile industry. India is fast emerging as a global manufacturing

hub for auto components, although currently the industry is highly fragmented. The Automotive Manufac-

turers Association of India (ACMA) represents the organised segment of the industry with 500 companies

as members. These companies are known for their value-added precision engineering products and account for

over 70% of the total auto component production. The unorganised segment, comprising over 2,000 players, caters

mainly to the replacement market. MNCs too have entered the field and are actively involved in manufacturing.

The market can be classified into original equipment manufacturers (OEMs), replacement market and export mar-

ket, which account for 40%, 50% and 10% respectively, of the total demand for auto components.

Classification of product segments as per ACMA can be depicted by the following diagram.

The industry grew at a CAGR of 21% over the

past seven years, and reached $22 billion in

2009-10. Exports increased at a CAGR of

21% to $4 billion in 2009-10. There has been

a shift in the composition of exports over the

past years, with OEM segment accounting for

80% and aftermarket accounting for 20% of

the exports. Europe accounted for 37% of the

total exports from India, followed by Asia at

28%, North America at 24%, Africa at 7%,

South America at 2.5%, and Australia at 1%.

Imports improved at a CAGR of 34% over the

past six years to $8 billion in 2009-10. Invest-

ments in this industry have grown at a CAGR

of 20% over the past seven years, to reach $9

billion in 2009-10. A number of global companies have announced plans to invest in this industry in India.

Indian components suppliers are well conversant with all global automotive standards. They are also increasingly

adopting information technology for design, development and simulation. They have been able to maintain quality

even while catering to large-volume orders.

The biggest players are Bosch, Motherson Sumi Systems and Bharat Forge. There are other companies too such as

Amtek Auto, Sona Steering, Sundaram Fasteners and Subros.

Global automakers are increasingly using India-made components in their units so as to remain cost competitive.

This augurs well for the auto ancillary industry.

However, few issues will have to be tackled to ensure robust growth – infrastructure deficit, scaling-up the indus-

try, shortage of talent, access to world-class technology and quality practices, access to and availability of cost

effective capital, remaining cost competitive, and trade policy.

15

SWOT Analysis

Strengths

India has a large domestic market with tremendous demand

Produces goods at low cost but with high efficiency

Availability of cheap but skilled labour

Strong engineering skills in designing

Well-developed and globally competitive auto ancillary industry

Weaknesses

Infrastructural constraints

Increasing cost of production due to increasing input prices

Low investment in R&D when compared to other economies

Opportunities

All segments, especially passenger vehicles and commercial vehicles (ban on overloading in CV seg-

ment)

Government is supportive

Improving income levels

Rising rural demand especially for two-wheelers

Increasing road network

Removal of ban on transporting agri-products from one state to another (need to discuss with Sir)

Market opening up for hybrids

Threats

Rising interest rates and inflation

Competition may put pressure margins

Threat from Chinese low-cost manufacturing

Pressure on cost competitiveness

Pressure to innovate consistently

Falling of customs duty

Volatility of petrol and diesel prices

Weak service network of some automobile manufacturers

16

The Road Ahead

T he industry holds lot of promise, even as it has registered sterling performances in the past few years.

Penetration of two-wheelers and cars is low in India. It is expected that the economy will continue to grow

at a good pace, leading to increasing disposable incomes and higher demand. Globally too, India has been

considered as a low-cost manufacturing hub, and sourcing of auto parts has already begun. In addition to this, ex-

ports will also increase. As per SIAM, growth in 2010-11 should be in the range of 10-14%. It is expected that a

capacity of 1.75 lakh cars, worth Rs 6,026 crore, will be commissioned in 2010-11.

To meet the higher domestic and global demand, lots of companies have chalked out their expansion plans.

Maruti Suzuki, with a capacity of 10 lakh units -- lower than its total sales of 10.2 lakh units in 2009-10,

may find it difficult to maintain its market share in 2010-11. It has planned to expand its capacity to 17.5

lakh units by end of FY2013, at a total cost of Rs 3,625 crore.

Toyota Kirloskar’s compact car project at Bidadi (Bangalore), worth Rs 2,800 crore, will be completed

by December 2010. This plant will have a production capacity of 70,000 cars per annum. Toyota has

plans to launch ‘Etios’, its small car in the Indian market by January 2011, from this manufacturing unit.

General Motors will set up Beat concept mini car project, worth Rs 250 crore, by January 2011. It wants

to make India its export base to supply its mini car globally.

Tata Motors plans to start LCVs, vans & components project at Belur (Karnataka), with a production

capacity of 38,000 units per annum, worth Rs 2,500 crore by January 2011.

Two and three-wheeler companies have scheduled capacities of 15.7 lakh units per annum to come on

stream during July 2010 to March 2011. Bajaj Auto has planned the biggest capacity expansion -- by 11

lakh units by March 2011.

17

Disclaimer Clause

This report is for customer ‘information’ only and does not constitute investment advice or an offer to purchase or subscribe

for any investment. This document is not intended to provide professional advice and should not be relied upon in that regard.

Persons accessing this document are advised to obtain appropriate professional advice where necessary. This document is not

directed to or intended for display, downloading, printing, reproducing or for distribution to or use by any person or entity

who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication,

reproduction, availability or use would be contrary to law or regulation or would subject Dhanlaxmi Bank Limited or its associ-

ates or group companies to any registration or licensing requirement within such jurisdiction. If this document is inadvertently

sent or has reached any individual in such country, the same may be ignored and brought to the attention of the sender. This

document may not be reproduced, distributed or published for any purpose without prior written approval of Dhanlaxmi Bank

Limited.