produced by - institutional investor · ashland (ash) submitted july 2013 and ; won grand prize as...

TRANSCRIPT

Produced by

Institutional Investor and SumZero are not registered investment advisors or broker-dealers, and are not licensed nor qualified to provide investment advice. There is no requirement that any of the Information Providers presented here be registered investment advisors or broker-dealers. Nothing published or made available by or through Institutional Investor and SumZero should be considered personalized investment advice, investment services or a solicitation to BUY, SELL, or HOLD any securities or other investments mentioned by Institutional Investor, SumZero or the Information Providers. Nev-er invest based purely on our publication or information, which is provided on an “as is” basis without representations. Past performance is not indicative of future results. YOU SHOULD VERIFY ALL CLAIMS, DO YOUR OWN DUE DILIGENCE AND/OR SEEK YOUR OWN PROFESSIONAL ADVISOR AND CONSIDER THE INVESTMENT OBJECTIVES AND RISKS AND YOUR OWN NEEDS AND GOALS BEFORE INVESTING IN ANY SECURITIES MENTIONED. INVESTMENT DOES NOT GUARANTEE A POSITIVE RETURN AS STOCKS ARE SUBJECT TO MARKET RISKS, INCLUDING THE POTENTIAL LOSS OF PRINCIPAL. You further acknowledge that Institutional Investor, SumZero, the Information Providers or their respective affiliates, employers, employees, officers, members, managers and directors, may or may not hold positions in one or more of the securities in the Information and may trade at any time, without notification to you, based on the information they are providing and will not necessarily disclose this information, nor the time the positions in the securities were acquired. You confirm that you have read and understand, and agree to, this full disclaimer and terms of use and that neither Institutional Investor, SumZero nor any of the Information Providers presented here are in any way responsible for any investment losses you may incur under any circumstances.

On Tuesday, November 12, 2013, Institutional Investor and SumZero, the world’s largest online membership community of buy-side investment professionals, hosted an idea competition at Columbia University Business School’s Uris Hall Auditorium.

Nineteen emerging managers were selected from within the SumZero community on the basis of strong performance and high-quality peer reviews. Each manager gave a three minute pitch on their best idea to an audience of analysts and investors who rated their pitch for validity of the thesis, strength of the argument, feasibility of the trade and originality.

We invite you to view these ideas and register to download each presenter’s bio and full pitch paper. If you’re a professional investment officer or analyst, we invite you to register to vote for the winning idea.

Favorite Investment Book:Inside The Investor’s Brain By Richard L. Peterson

Favorite Quote/Author: “Each day you haven’t spent preparing is a day you’ve handed to the competition” —Uncited

Most Attractive Area of the Market Right Now:We are bottoms up, fundamental investors

Least Attractive Area of the Market Right Now:We are bottoms up, fundamental investors

Personal Investing Style:Long-term, highly idiosyncratic asymmetric opportunties

Areas of Personal Expertise:Equities and credit

Languages Spoken:English

Daniel W. Lawrence Elmrox Investment Group

Age: 32 Title: Managing Partner & Founder Location: New York

Education (Undergrad/Grad/Certifications): B.S. Commerce, University of Virginia

Bio: Daniel was most recently a managing director and co-founder of talara capital management, a long/short equity partnership (2009 –2013). Previously, daniel was a senior analyst at citadel investment group. His primary responsibilities were to conduct fundamental research and analyze a range of value, high yield, and distressed investments in various sectors, including consumer, materials, financials and technology. Daniel invested in both the equity and debt of publicly traded businesses (2005-2009). Prior to citadel, daniel was an investment banking analyst at merrill lynch in new york within the global multi-industry group. (2002-2005). Daniel earned a b.S. In commerce from the mcintire school of com-merce at the university of virginia (2002). He has since been a guest finance lecturer at the university and participates in the galant center for entrepreneurship. Daniel has served on the board of directors of sus since 2009. He is also a former coach for the iona preparatory school speech & debate team, where he coached several national champions. His per-sonal interests include crossfit, american history and u.S. Foreign policy, cinema and great oratory.

Firm Strategy: eig seeks to generate “alpha” focusing on fundamental characteristics of companies through a combina-tion of intensive research, deep diligence and strategic thinking designed to identify financial instruments with asymmet-ric risk/reward profiles over varying investment horizons. Elmrox pursues an intensive “private equity-like” research pro-cess that involves in-depth primary research through extensive diligence. This process emphasizes long-term structural business characteristics of companies rather than short-term data points and market “noise.” The typical characteristics of companies that are expected to comprise the fund’s “long” portfolio include, but are not limited to, some or all of the following: sustainable business models with competitive barriers; predictable and repeatable revenue streams with high returns on invested capital; management teams and culture focused on innovation and on having the best people; high quality boards with significant equity ownership stakes; asset and operational transformations not fully perceived; mis-understood balance sheets; growth companies with long-term earnings prospects and attractive reinvestment econom-ics; significant change in capital allocation policies that are shareholder friendly; downside protection from asset value, private market value and/or sustainable cash flow; and significant variant views between market estimates and eig’s own estimates.

Past Ideas Submitted on SumZero:Ashland (ash) submitted july 2013 and ; won grand prize as best stock idea for 2013 value investing challenge at value investing congress in september 2013

AUM: N/A Firm Focus: Global Fund Disclaimer: Please see section 6 of appendix.

Fund Description:Eig seeks to generate “alpha” focusing on fundamental characteristics of companies through a combination of inten-sive research, deep diligence and strategic thinking designed to identify financial instruments with asymmetric risk/reward profiles over varying investment horizons. Elmrox pursues an intensive “private equity-like” research process that involves in-depth primary research through extensive diligence. This process emphasizes long-term structural business characteristics of companies rather than short-term data points and market “noise.” The typical characteristics of companies that are expected to comprise the fund’s “long” portfolio include, but are not limited to, some or all of the following: sustainable business models with competitive barriers; predictable and repeatable revenue streams with high returns on invested capital; management teams and culture focused on innovation and on having the best people; high quality boards with significant equity ownership stakes; asset and operational transformations not fully perceived; mis-understood balance sheets; growth companies with long-term earnings prospects and attractive reinvestment econom-ics; significant change in capital allocation policies that are shareholder friendly; downside protection from asset value, private market value and/or sustainable cash flow; and significant variant views between market estimates and eig’s own estimates.

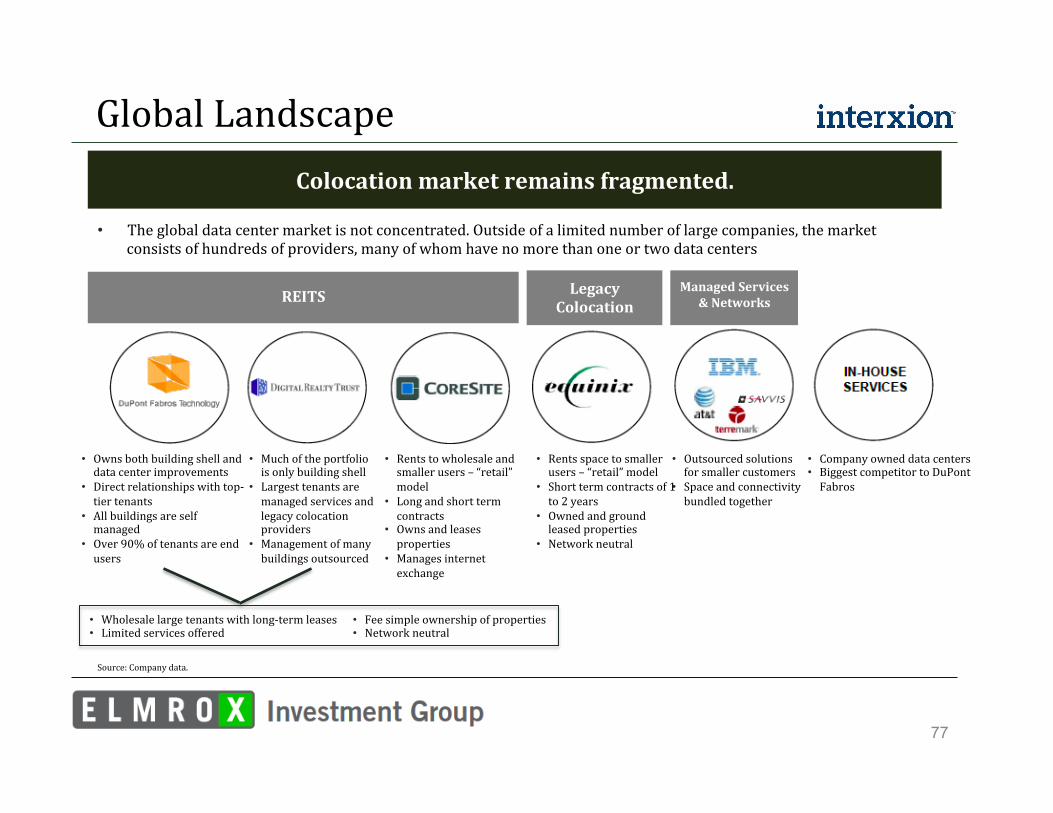

Interxion Holding NV

Elmrox Investment Group

”Secular Growth on Sale”

November 2013

Daniel W. Lawrence

© 2013 Elmrox Investment Group LLC. All rights reserved

Jim Huseby 813-‐644-‐9399

Disclaimer The analyses and conclusions of Elmrox Investment Group LLC (”Elmrox”) contained in this presentation are based on publicly available information. Elmrox recognizes that there may be conOidential information in the possession of the companies discussed in the presentation that could lead these companies to disagree with Elmrox’s conclusions. This presentation is for general informational purposes only, is not complete and does not constitute an agreement, offer, a solicitation of an offer, or any advice or recommendation to enter into or conclude any transaction or conOirmation thereof (whether on the terms shown herein or otherwise). This presentation should not be construed as legal, tax, investment, Oinancial or other advice. It does not have regard to the speciOic investment objective, Oinancial situation, suitability, or the particular need of any speciOic person who may receive this presentation, and should not be taken as advice on the merits of any investment decision. The views expressed in this presentation represent the opinions of Elmrox, and are based on publicly available information with respect to Interxion Holding NV (the "Issuer") and the other companies referred to herein. Certain Oinancial information and data used herein have been derived or obtained from Oilings made with the Securities and Exchange Commission ("SEC") or other regulatory authorities and from other third party reports. The analyses provided may include certain statements, estimates and projections prepared with respect to, among other things, the historical and anticipated operating performance of the companies, access to capital markets and the values of assets and liabilities. Such statements, estimates, and projections reOlect various assumptions by Elmrox concerning anticipated results that are inherently subject to signiOicant economic, competitive, and other uncertainties and contingencies and have been included solely for illustrative purposes. No representations, express or implied, are made as to the accuracy or completeness of such statements, estimates or projections or with respect to any other materials herein. Actual results may vary materially from the estimates and projected results contained herein. Accordingly, no party should purchase or sell securities on the basis of the information contained in this presentation. Elmrox expressly disclaims liability on account of any party’s reliance on the information contained herein with respect to any such purchases or sales. Elmrox has not sought or obtained consent from any third party to use any statements or information indicated herein as having been obtained or derived from statements made or published by third parties. Any such statements or information should not be viewed as indicating the support of such third party for the views expressed herein. Elmrox does not endorse third-‐party estimates or research which are used in this presentation solely for illustrative purposes. No warranty is made that data or information, whether derived or obtained from Oilings made with the SEC or any other regulatory agency or from any third party, are accurate. Elmrox hereby disclaims any duty to provide any updates or changes to the analyses contained here. Neither Elmrox nor any of its afOiliates shall be responsible or have any liability for any misinformation contained in any third party, SEC or other regulatory Oiling or third party report. There is no assurance or guarantee with respect to the prices at which any securities of the Issuer will trade, and such securities may not trade at prices that may be implied herein. The estimates, projections, pro forma information and potential impact of the opportunities identiOied by Elmrox herein are based on assumptions that Elmrox believes to be reasonable as of the date of this presentation, but there can be no assurance or guarantee that actual results or performance of the Issuer will not differ, and such differences may be material. This presentation does not recommend the purchase or sale of any security. Elmrox reserves the right to change any of its opinions expressed herein at any time as it deems appropriate. Elmrox disclaims any obligation to update the data, information or opinions contained in this presentation.

1

Underappreciated Secular Grower in Europe with Wide Moats; Leading Market Position in Industry with Strong Fundamentals -‐ BeneOiciary of powerful mega-‐trends: accelerating demand of cloud computing, increased content consumption via mobility, ongoing shift to online video and and other drivers of network trafOic

-‐ Scale: Largest Pan-‐European footprint in industry with 34 data centers in 13 cities across 11 European countries

-‐ Predictable model with > 90% recurring revenues; low churn (<1%) -‐ Focused on high growth customer segments (e.g., media, enterprises)

Competitive Advantages & Value Proposition Are Not Appreciated -‐ Entry barriers misunderstood: wide moats in Europe vs N. America -‐ Pan-‐European scale would take 10-‐15 years for new entrant to build -‐ Highly valuable customer “communities of interest” very difOicult to replicate creating signiOicant network effect and high switching costs

Valuation Does Not ReVlect Predictable Steady State Free Cash Flow (“SSFCF)” and Long-‐Term Secular Growth Opportunities -‐ US listing for European Oirm causes investors to overlook story -‐ Concerns related to Baker Capital’s 30% ownership are priced in

Disciplined & Proven Management Team -‐ Strong and consistent track record of thoughtful and patient capital allocation; target 30% to 40% IRR on each new data center

Strong Balance Sheet & Cash Flow = Value Creation Optionality -‐ Organic + inorganic opportunities; potential share repurchases -‐ Cash Olow could support considerably higher leverage

Unique and Highly Valuable Asset Base Creates Margin of Safety -‐ INXN footprint nearly impossible to replicate = high strategic value -‐ Global and European data center industry is ripe for consolidation

Big 4 vs. ROE

Situation Overview Current Price: $22.46 (10/31/13) Market Cap: $1.5bn Enterprise Value:$1.9bn

Thesis

Business Overview

N.B.: Financials LTM as of June 30, 2013. Enterprise value calculated using stock price as of October 31, 2013. Valuation multiples calculated using consensus sell side estimates as of October 31, 2013. Steady state free cash Olow (SSFCF) deOined as : (EBITDA – maintenance capex – cash interest – cash taxes) / (equity market capitalization).

Interxion (the “Company”) is a Leader in Data Centers in Europe -‐ Provides cloud-‐ and carrier-‐neutral colocation data center services -‐ Serves range of customers through unique “communities of interest” -‐ LTM Revenues 6/30/2013: €294mm -‐ LTM EBITDA 6/30/2013: €124mm (42% LTM EBITDA Margin)

Attractive Valuation Multiples Given Growth Rate (FYE 12/31/14E) -‐ 13x steady state free cash Olow (SSFCF) -‐ 9x EV / EBITDA -‐ Trades at discount to similar SSFCF businesses and below competitively disadvantaged North American data centers Oirms

42% 42% 42% 41% 41% 41% 40% 39% 40% 42% 40%

(Contribution %) Big 4 vs. ROE Revenue Contribution(1)

Big 4 ROE

58% 56% 55% 59% 59% 58% 57% 61% 56% 57% 58%

42% 44% 45% 41% 41% 42% 43% 39% 44% 43% 42%

(Contribution %) Big 4 vs. ROE Adj. EBITDA Contribution(1)

(1) Big 4 represents the Netherlands, UK, France and Germany. ROE represents Rest of Europe (Austria, Belgium, Denmark, Ireland, Spain, Sweden, Switzerland). Adj. EBITDA contribution based on costs allocated to the segments and excludes costs associated to corporate and other.

Business Overview

2

Variant Perception

• Consensus does not appreciate the structural barriers colocation providers in Europe beneOit from • Market concerns comparing worsening competitive environment in North America to Europe are misplaced • DeOlationary price competition concerns in Europe are exaggerated (this is an issue speciOic to North America) • Deceleration of global data center growth rates are short-‐term in nature relative to long-‐term secular trends • Market especially underappreciates INXN’s unique access to scarce physical Oiber placements • Investors often confuse data centers like INXN with managed service providers (managed services are INXN customers; colocation companies like INXN are beneOiciaries of heightened competition in managed services)

• Recurring revenue should re-‐accelerate in 2014 as utilization rate from recent expansion ramps • Consensus does not assume likely expansion into high growth and under-‐supplied markets (LatAm / Eastern Europe) • Long-‐term operating leverage in business model underestimated by market • Cash Olow generation improvement potential misunderstood • Valuation does not reOlect strong and recurring steady state cash Olow • Low leverage on balance sheet = potential for additional shareholder value creation • Shareholder concerns related to Baker Capital’s ownership stake and Board seats already priced in • High strategic value / replacement value create margin of safety

Underappreciated Secular Grower With Strategic Asset Value

Moats + Recurring Cash Flow Model + Disciplined Management = Good Business

3

Illustrative Potential Returns

Strategic Asset Value + Variant Perception = Asymmetric Return ProVile

15

25

35

45

55

65

INXN Current Price

Conservative Replacement Value (Facilities Only)

LBO / Private Market Value

Standalone INXN Sold to Strategic

Recurring Monthly Revenue (RMR)

Steady State Free Cash Flow (SSFCF)

REIT Conversion

$25-‐$32

$31 -‐$47

$34-‐$60

$34-‐$52

$12 -‐ $23

$28-‐$52

$26 -‐$54

$22.46

% Upside: 11% to 42% 24% to 131% 51% to 131% 38% to 109% 15% to 140% 51% to 167%

Attractive Multiple of Steady State Free Cash Flow (SSFCF) + Long Term Secular Growth Opportunities = Attractive Entry Point

4

Company Overview

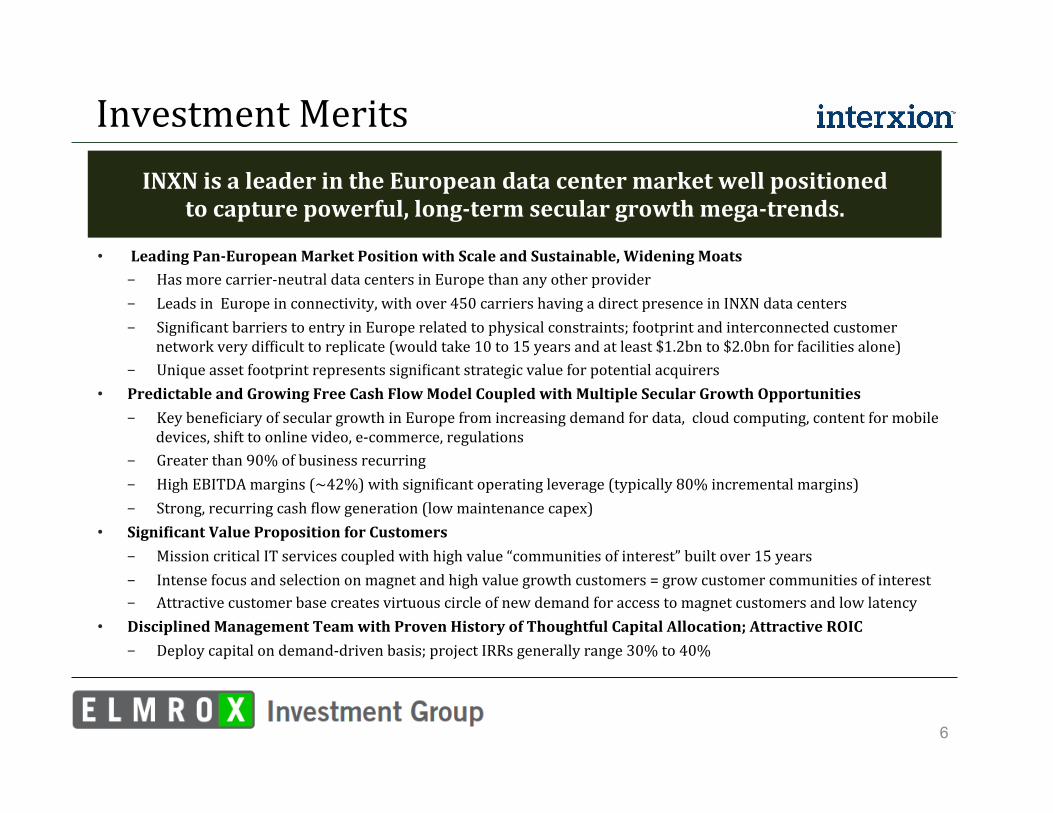

Investment Merits

• Leading Pan-‐European Market Position with Scale and Sustainable, Widening Moats - Has more carrier-‐neutral data centers in Europe than any other provider - Leads in Europe in connectivity, with over 450 carriers having a direct presence in INXN data centers - SigniOicant barriers to entry in Europe related to physical constraints; footprint and interconnected customer

network very difOicult to replicate (would take 10 to 15 years and at least $1.2bn to $2.0bn for facilities alone) - Unique asset footprint represents signiOicant strategic value for potential acquirers

• Predictable and Growing Free Cash Flow Model Coupled with Multiple Secular Growth Opportunities - Key beneOiciary of secular growth in Europe from increasing demand for data, cloud computing, content for mobile

devices, shift to online video, e-‐commerce, regulations - Greater than 90% of business recurring - High EBITDA margins (~42%) with signiOicant operating leverage (typically 80% incremental margins) - Strong, recurring cash Olow generation (low maintenance capex)

• SigniVicant Value Proposition for Customers - Mission critical IT services coupled with high value “communities of interest” built over 15 years - Intense focus and selection on magnet and high value growth customers = grow customer communities of interest - Attractive customer base creates virtuous circle of new demand for access to magnet customers and low latency

• Disciplined Management Team with Proven History of Thoughtful Capital Allocation; Attractive ROIC - Deploy capital on demand-‐driven basis; project IRRs generally range 30% to 40%

INXN is a leader in the European data center market well positioned to capture powerful, long-‐term secular growth mega-‐trends.

6

Overview of Interxion

Leading Pan-‐European Data Center Provider with Wide Moats

Sales by Geography

Customer Concentration

Adj. EBITDA by Geography

Other 67%

Top 2-‐10 Customers 19%

Top 11-‐20 Customers 10%

Top Customer 4%

Source: Company data. (1) Big 4 represents the Netherlands, UK, France and Germany. ROE represents Rest of Europe (Austria, Belgium, Denmark, Ireland, Spain, Sweden, Switzerland). Adj. EBITDA contribution based on costs allocated to the segments and excludes costs associated to corporate and other.

NYSE Ticker Symbol Total Employees Total Data Centers # of Customers INXN ~400 34 > 1,300

Largest Footprint of any European Player Covering ~75% of GDP

LTM 6/30/13 Sales: €294mm

LTM 6/30/13 Adj. EBITDA: €124mm

58% 58% 58% 59% 59% 59% 60% 61% 60% 58% 60%

42% 42% 42% 41% 41% 41% 40% 39% 40% 42% 40%

(Contribution %) Big 4 vs. ROE Revenue Contribution(1)

58% 56% 55% 59% 59% 58% 57% 61% 56% 57% 58%

42% 44% 45% 41% 41% 42% 43% 39% 44% 43% 42%

(Contribution %) Big 4 vs. ROE Adj. EBITDA Contribution(1)

7

• Typical Customer Functions:

- Servers and storage equipment that run application software and process and store data and content

- A simple cage or rack of equipment - A room housing a few or many cabinets, depending on the scale of the customer’s operation

• A data center space will typically have a raised Oloor with cabling ducts running underneath to feed power to the cabinets and carry the cables that connect the cabinets together

• The environment is generally controlled in terms of temperature & humidity both to ensure the performance and the operational integrity of the systems within

• Facilities usually include power supplies and access to signiOicant external sources of power, backup power, chillers, Oire and water detection systems, cabling, and security controls

What is a Data Center?

A data center is a dedicated space that houses technology infrastructure.

Sources: Company data and company website.

8

Types of Data Centers

Data centers can be in-‐house, located in a company’s own facility, or outsourced with equipment being colocated at a third-‐party site.

A colocation provider (like INXN) versus wholesaler is a critical distinction.

Sources: Company website and Focus Telecom’s “Colocation and Managed Hosting Report”. (1) 451 Research’s North American Multi-‐Tenant data center Supply Emerging Major Markets 2012” report.

Colocation / Retail Colocation

• Provides customers physical space for a customer’s internet-‐ focused technology infrastructure

• Provides power and cooling necessary to maintain infrastructure at high levels of performance and without interruption

• Given the proprietary nature of colocation activities, provides security, both at the facility level and within the facility at the suite, cage, or cabinet level.

• Sold on the basis of individual racks, cabinets, or cages; usually range 500 to 5,000 square feet

Wholesale Providers

• Provides leasable large space to large enterprises and commercial colocation providers

• Customers engineer their own data centers within facilities

• Large enterprises share cost of the land and the facility shell, power, and external security

• Facilities typically are large buildings (at 100,000 square feet plus) that are divided into private pods or cells; frequently are located near large cities

• Usually sold in pods or cells (empty rooms); typically range from 10,000 to 50,000 square feet

• Colocation data center is different from wholesale in that colocation customers do not provide their own infrastructure beyond servers, storage, and switch gear

• “best way to think of wholesale data centers is ‘data center space for rent.’… similar to leasing an ofOice or warehouse where the landlord provides facility maintenance”(1)

• Colocations have high value customer communities/ecosystems

• Given the large space requirements geography is often a barrier/hindrance for wholesalers to enter certain markets especially Europe

Differences

9

Carrier-‐neutral data center: • Is independent of the companies colocating in the data center (does not compete with them in any way) • Offers no packaged services and customers are free to contract directly with the internet providers of their choice • Result: wide range of connectivity and communication providers are attracted into INXN facilities; creates widest

choice of Oixed and mobile carriers, ISPs, Internet exchanges, content distribution networks (CDNs) and others, all competing to deliver the best connectivity performance, service and price for their applications and content

Cloud-‐neutral data center: • Is independent of any hardware or software vendors and IT service providers, traditional or cloud-‐based • As a result of not competing with cloud service providers, these Oirms are attracted to INXN’s wide range of

connectivity providers that its hosts • Result: INXN data centers are home to a wide range of IT service providers, including: public and private cloud

platform providers, system integrators, managed hosting providers, software-‐as-‐a-‐service providers, providers of data and information services to speciOic industries, and providers of IT security, business continuity and consultancy services

Combined result: INXN’s data centers effectively constitute a marketplace within a highly connected environment. Providers within INXN data centers competing for customer business and give customers the choice and Olexibility to choose the right service providers at the right price. Since customers are all in the same place, each one can interconnect quickly and easily with low-‐latency Cross Connects that improve the speed, Olexibility, cost reduction

Types of Data Centers (cont’d)

What is a carrier-‐neutral data center and a cloud-‐neutral data center?

Sources: Company data and company website.

Interxion is carrier-‐neutral and cloud-‐neutral.

10

• Connectivity and communities of interest

• Cost efOiciencies, lowers latency and augments performance

- Third party data centers allow a Oirm to pay for the space it needs and scale only as required. The costs of security and data center technology are shared with other colocation partners, while costs are further reduced by innovations in efOiciency, such as advanced power management.

• 24 hour monitoring and maintenance by highly trained technicians

• Wide range of power management

• Cost effective cooling; Oire detection & suppression

• Multiple layers of security to protect customer data

• Additional services including systems monitoring, systems management, engineering support services, data back-‐up and storage

Why Outsource to a Data Center?

Carrier-‐neutral data centers give customers access to wide range of connectivity providers; the customer selects the right connectivity for

multiple carriers to build in redundancy, ensure resilience, reduce costs.

Source: Company data.

A neutral data center is independent of any network, hardware or software vendor and attracts customers wanting access to this ecosystem.

11

Why Invest in Data Centers?

• Demand driven by long-‐term, secular mega-‐trends in early innings

• Consistent, predictable revenues and cash Olow

• Strong, sustainable margins with high incremental margins ~80% (depending on facility)

• SigniOicant hurdles for new entrants

• High value proposition with Olywheel of network effects that is difOicult to displace

Secular Growth

Barrier to Entry

Network Effects

Switching Costs

• Demand for data • Cloud computing • Mobile content • Shift to online video • E-‐Commerce • Social • Regulatory Driven • Software as Service (SaaS) • Hosting

• Highly specialized expertise required

• Specialized sites required (prime locations, power, Oiber connectivity)

• SigniOicant costs for development (land, base building, infrastructure)

• Communities of interest attract and retain customers

• Customer ecosystems attracts other customers wanting access to this cultivated community of media and content providers, enterprises, carriers, et all in one place

• Communities of interest take many years to build

• Magnetic customers cannot be re-‐created

• Proximity to business partners difOicult to replicate

Powerful Secular Growth Drivers

12

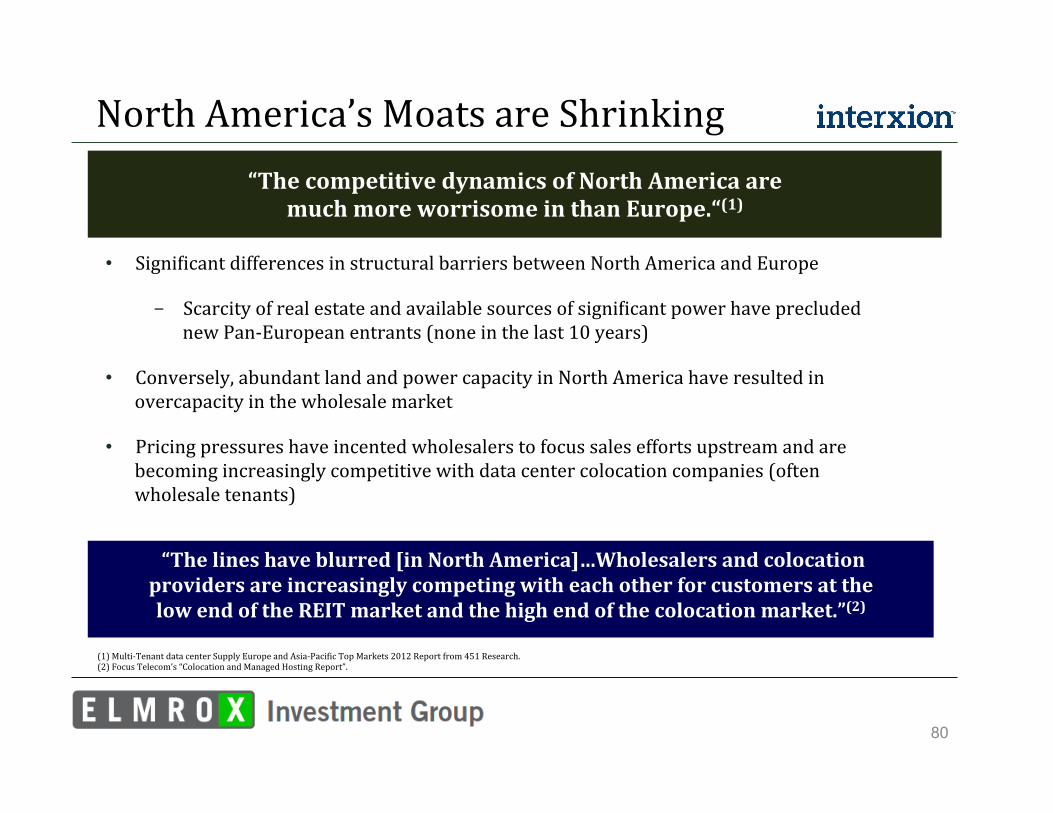

Why Invest in European Data Centers?

The European data center market has sustainable moats that insulate existing players like INXN from the increasing competitive forces that threaten the North American market.

Sources: BroadGroup “Western European data centre research” 2012, Tier 1 Research, Multi-‐Tenant data center Global Providers 2012. Cisco VNI Report, 2013, Cisco GCI Report, 2012.

European data center market has unique and signiVicant barriers to entry = no new Pan-‐European entry in the last 10 years.

Key Differentiators Europe North America Total Fixed Internet Users in 2016 319 million 269 million Mobile Connected Devices vs. Total Network Devices in 2016 39% 28% Mobile Data TrafOic in 2016 2.4EB 2.0EB Growth in Internet TrafOic (‘11-‐’16 CAGR) 27% 22% Cloud TrafOic Growth (‘11-‐’16 CAGR) 44% 34%

• Limited availability of prime space, limited access to signiOicant power sources, and limited access to critical underground telco Oiber connections have and continue to protect European market

• North American dynamics have led to intensifying competition: availability of space and power, new entrants, extra capacity, pricing pressure and augmented competition from wholesalers

13

Europe’s Moats Much Stronger Than U.S.

(1) Kelly Morgan, Research Manager, Multi-‐Tenant Datacenters on February 20, 2013. (2) 451 Research’s “Multi-‐Tenant data center Supply Europe and Asia-‐PaciOic Top Markets 2012” Report.

84% 72%

16% 28%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2011 2015E

3,459 4,068

4,808

5,690

6,717

-‐

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2010 2011 2012 2013 2014

CAGR 29%

European Outsourcing Opportunity

EMEA Multi-‐Tenant Data Center Revenue

User Owned Third Party

($ in M)

In Europe “Vinding a suitable site is hard, then convincing the local power company to provide enough power for a small town is a challenge. Getting all the requisite permits can take years. This is before taking into account the

difViculty convincing carriers to connect to the facility.” (1)

“It is unlikely that larger American-‐style data centers will become the norm [in Europe] due to localized space and power constraints.” (2)

14

Barriers to Entry are Highest in Europe

• Cloud computing market is highly fragmented and localized creating signiOicantly higher barriers to entry than U.S. - The absence of a single European hosting market contributes to this situation: each European country has its

own – often highly fragmented – market. Despite similar customer requirements, there are signiOicant local differences, including market size, cultural background and IT buying behavior

- The fragmented European market is characterized by a large number of players relative to market size, mostly with a relatively low number of customers

- Addressing the cloud opportunity requires hosters to make a signiOicant investment in technology and service innovation, but not many companies have been able to do so over the past few years

“Barriers to entry…as high in our business as it's always been. I don't see any new entrants. We're not seeing the wholesale guys nipping at our

heels on the retail side like they are in the United states.”(1)

Source: Netcraft Active Domains, August 2012. Netcraft IP Addresses, August 2012. (1) Vice Chairman, Chief Executive OfOicer and President, David C. Ruberg, on September 12, 2013 earnings call.

246 215

102 138

253

145

83 110

63 74 84 45 56 62 75

49 40 64

-‐

50

100

150

200

250

300

Germany UK Poland France Netherlands Russia Italy Spain Turkey Sweden Switzerland Romania Czech Republic

Denmark Belgium Ukraine Ireland Austria

European Hosting Market: Market Share and Size by Country

# of Hosting Provisions

Market Share 28% 13% 9% 5% 3% 2% 2% 1% 1% 10% 8% 3% 2% 2% 2% 1% 1% 1%

15

Europe Should Remain Tight Given Moats

The carrier-‐neutral colocation market in Europe remains constrained.

(1) Based on company Oilings and websites of Interxion, Tel;ecity and Equinix. Equinix EMEA cabinet equivalents assumed to be equal to 2.5 net square meters per cabinet. (2) European weighted average utilization rate is calculated as year-‐end revenue generating space as a percentage of total year-‐end equipped space for the aggregate Oigure of Interxion, Telecity and Equinix EMEA. (3) The Jones Long LaSalle Data Centre Barometer, Spring 2013, Issue 10.

• Major players remain disciplined

- Introductions of new supply largely demand driven (including INXN)

• Utilization remains tight in high 70s / low 80s

“The prevailing view amongst our IT service providers, hosting and colocation operators [in Europe] is one of rising demand against a diminishing supply.”(3)

75% 79%

75%

50%

60%

70%

80%

90%

2010 2011 2012

European Avg. Carrier and Cloud Neutral Colocation % Utilization(1)(2)

25 18

37 13%

8%

15%

-‐2%

3%

8%

13%

18%

1

11

21

31

41

2010 2011 2012

(‘000 m2)

European Carrier and Cloud Neutral Colocation Additional Supply(1)

New Supply % of Equipped Space As of 2Q 2013

Supply 667,818 sq. m.

Availability 102,232 sq. m.

Vacancy Rate 15.31%

Colocation Take-‐up: Quarterly 6,300 sq. m.

Colocation Take-‐up: Annual YTD 15,095 sq. m

16

Bolstered by Continued Strong Demand

European carrier neutral colocation market opportunity is signiVicant.

Sources: BroadGroup “Western European data centre research” 2012, Tier1 Research, Multi-‐Tenant data center Global Providers 2012, Cisco VNI Report, 2013, Cisco GCI Report, 2012.

Key Differentiators Provide Long-‐Term Upside Relative to North America

Europe North America

Broadband Subscribers 130 million 93 million

Smart Phones 201 million 109 million

Growth in Internet TrafVic 2009-‐20014E CAGR 35% 30%

€ 922

€ 2,245

€ -‐

€ 500

€ 1,000

€ 1,500

€ 2,000

€ 2,500

2009 2014E

(€ in millions)

European Demand for Carrier-‐Neutral Colocation

CAGR +19%

European Outsourcing Opportunity

European Demand for Carrier-‐Neutral Colocation

In-‐House 88%

Top 2-‐10 Customers 19%

Carrier Neutral Colocation

3%

Breakdown of Average Data Center Capacity by Type

17

Long Term Demand in Europe

Western Europe data center market has strong long-‐term demand trends.

Source: BroadGroup.

-‐

200

400

600

800

1,000

1,200

2011 2012 2013 2014 2015 2016

M2 (thousands)

Carrier Neutral Colocation

Carrier Owned Wholesale Managed Services

18

• INXN’s data centers have become critical exchange points for Internet and data trafOic in across Europe as well as a gateway into and out of Europe

• INXN’s exchange points attract enterprises, media and content providers, IT services providers and other groups wanting to access these diverse networks and other enterprises in a single location versus connecting these parties in multiple locations

• This high level of connectivity fosters the development of value-‐added communities of interest within each customer segments

• These communities of interest create virtuous circle by then attracting additional carriers and customers which makes them increasingly more valuable

Location & Scale in Europe Matters

Data centers located near key business hubs, interconnection points of telecom Viber routes, and power sources provide customers with

high levels of connectivity and the requisite power to meet their needs.

“Barrier to entry… if you want to build a carrier-‐rich data center environment, it's almost impossible to replicate. If you've got a 10-‐year roadmap, then maybe. And the reason for that is because between '97 and 2002, the carriers in Europe built their network and their network backbones into data centers, like Interxion, and they're not going to be doing it again in a hurry. That's the fundamental basis of the moat that is around our business.”(1)

``

(1) Vice Chairman, Chief Executive OfOicer and President, David C. Ruberg, on May 8, 2013 earnings call.

19

Interxion History

“Our aspirations are to be a global company, not just European-‐based… when we realize that goal, our choice

to list in the United States would prove to be a wise one.”(1)

1998: Company founded

2001: Fully operational footprint of 20 facilities

2006: 1,000 customers 2009: 5 new builds

2011: IPO on NYSE under symbol “INXN”

EBITDA Margins:

2006 17.8%

2008 34.9%

2011 40.0%

2007 28.8%

2009 36.5%

2010 38.0%

LTM(2)

42.2% Recurring Sales %: 87% 93%

(1) Vice Chairman, Chief Executive OfOicer and President, David C. Ruberg, on September 12, 2013. (2) Last twelve months (LTM) as of June 30, 2013.

90% 92% 94% 93%

2008: €90mm expansion

2007: €50mm expansion

2013: Largest footprint in Europe: 34 data centers in 11 countries

2012: Baker Capital distributes 10mm shares

2012 41.5% 94% 94%

20

Drivers

Levered to some of the world’s most powerful secular growth trends.

Cloud Computing

Mobility

Content Demand

Regulatory

• Enterprise Private Clouds

• Public Cloud Infrastructures

• Private Clouds • Hybrid Clouds • Personal Cloud adoption in infancy - 12x increase by

2017 (Dropbox, Google Drive, Amazon Cloud)

General Demand

• Smartphones - SigniOicant

ongoing growth in mobile data

• Mobile Business - Connect workers

to corporate assets

- Software as Services (Saas)

• Social

• Digital Video - Shift to online

video consumption ramping fast

• E-‐Commerce • Social Networking • Photos - Accelerating

growth and in early innings

• Digital Sound - Emerging demand

• Basel III - Pressure on banks

to increase amount of stored data and the duration they store it for

• Disaster Recovery - Movement

towards speciOied distances for DR sites

• Big Data: - Emerging

• US Expansion to EUR - US businesses

pushing for European colocation

• Shift Towards Outsourcing - Intermediaries

• World Becoming More IT Dependent - Government

“Our ability to consistently drive the top line, even in an uncertain macroeconomic and broader business environment, demonstrates the strong secular trends underpinning the carrier-‐neutral colocation business in Europe, the demand for high-‐quality services like

Interxion's and most importantly, our ability to execute on our strategies.”(1)

(1) Vice Chairman, Chief Executive OfOicer and President, David C. Ruberg, on February 29, 2013 earnings call.

21

Competitive Advantages & Moats

SigniVicant barriers to entry exist in the European data center market.

ü Largest pan-‐European footprint

ü Hosts 19 of Europe’s internet exchanges

ü Premium location spaces

ü Unique access to mission critical power sources

Leading Economies of Scale

High Switching Costs

High Barriers to Entry

ü Communities of interest cannot be replicated

ü Carrier-‐ and cloud-‐ neutrality

ü Magnetic customers cannot be re-‐created

ü Proximity to business partners difOicult to replicate

ü Scarcity of adequate locations

ü Long lead time to build carrier critical mass (10 to 15 years)

ü Design and permitting expertise

ü No new Pan-‐European entry in the last 10 years in data centers

In Europe “Vinding a suitable site is hard, then convincing the local power company to provide enough power for a small town is a challenge.

Getting all the requisite permits can take years. This is before taking into account the difViculty convincing carriers to connect to the facility.” (1)

(1) Kelly Morgan,451 Research Manager, Multi-‐Tenant Data Centers on February 20, 2013.

22

Leading Pan-‐European Scale

INXN is in the most countries with the most carriers.

11

7

5 2

-‐ 2 4 6 8 10 12

(# of Countries)

% European GDP Coverage(

75% 69% 56% 28%

450

234 200 175

-‐ 100 200 300 400 500 (# of Carriers)

# of Internet Exchanges

19 13 7 11

85.0

64.2 52.2

64.0

-‐ 20.0 40.0 60.0 80.0 100.0 (‘000 Sqm)

28 26 24

7 -‐ 5 10 15 20 25 30

European Country Presence and GDP Coverage Access to Carriers & Internet Exchanges

Equipped Space Number of European Data Centers

Sources: Company Oilings, company website and Wall Street research, Eurostat.

23

Unique Footprint Creates Scarcity Value

INXN has unique access to expensive underground Viber networks that took many years and hundreds of millions of euros to build.

Largest Pan-‐European footprint of any data center Virm.

Amsterdam & Hilversum

London

Dublin

Brussels

Paris

Madrid

Stockholm

Copenhagen

Dusseldorf

Frankfurt

Vienna

Zurich

24

Highly Predictable Business

Greater Than 90% of Revenues Are Recurring with Churn < 1%.

€ 31.10 € 33.30 € 35.70 € 38.10

€ 40.40 € 42.50 € 43.70 € 45.10 € 47.80

€ 50.40 € 54.60 € 55.60 € 57.90

€ 60.00 € 62.00 € 64.40 € 65.80 € 68.00

€ 70.40 € 72.90 € 74.40 € 76.50

€ -‐

€ 20.00

€ 40.00

€ 60.00

€ 80.00

1Q'08 2Q'08 3Q'08 4Q'08 1Q'09 2Q'09 3Q'09 4Q'09 1Q'10 2Q'10 3Q'10 4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12 1Q'13 2Q'13

(€ in M)

CAGR(1) 19% Revenue by Quarter

New Supply % of Equipped Space

€ 10.30 € 11.90 € 12.90 € 13.10 € 14.10

€ 15.70 € 16.00 € 16.90 € 17.40 € 19.60 € 20.80 € 21.40

€ 22.20 € 23.30 € 25.00

€ 27.10 € 27.30 € 27.80 € 28.70 € 31.20 € 31.70 € 32.70

€ -‐

€ 10.00

€ 20.00

€ 30.00

€ 40.00

1Q'08 2Q'08 3Q'08 4Q'08 1Q'09 2Q'09 3Q'09 4Q'09 1Q'10 2Q'10 3Q'10 4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12 1Q'13 2Q'13

(€ in M)

CAGR(1) 25%

Adjusted EBITDA by Quarter

39% 13% 40% 32% 28% 18% 19% 23% 19% 16% 14% 14% 13% 13% 13% 39% 30% 22% 18% 25% 21% 13% 60% 62% 59% 58% 59% 59% 60% 58% 60% 62% 61% 62% 62% 63% 63% 58% 58% 59% 60% 60% 60% 59%

33% 41% 36% 34% 37% 37% 39% 38% 39% 42% 42% 41% 43% 43% 43% 36% 35% 37% 36% 38% 38% 40% Adjusted EBITDA

Margin(3)

Y/Y Growth

Big 4 %(2)

(1) CAGR calculated as of 2Q’13 vs. 1Q’08. (2) Big 4 % deOined as percentage of total revenue from France, Germany, Netherlands, and U.K. reporting segment. (3) Adjusted EBITDA margin calculated as Adjusted EBITDA divided by Revenue.

25

Value Proposition

INXN is able to charge premium rates by focusing on:

Connectivity

Community

Coverage

• Hosts 19 Internet exchanges (points of connection to exchange network trafOic)

• 450+ carrier-‐customers provide choice of connectivity partners

• Footprint across 13 cities and 11 countries

• Access to 90 million broadband subscribers and 75%+ EU GDP

• 1,300+ customers across a range of key sectors

• Manages physical connections between customers

• Magnet customers draw business partners to INXN data centers

26

Value Proposition (cont’d)

INXN’s carrier neutral colocation services creates signiVicant value.

• Customers save on the cost of: - Constructing a data center - 24/7 maintenance - Telecommunication required to access multiple

networks - Connections to other participants in the communities of

interest • Engenders Vlexible and scalable offering tailored to

each customer’s unique needs - Delivers better performance from lower network

latency - Improves customer service

Value Creation

Communities of Interest + Largest Pan-‐European Footprint + Carrier Neutrality + Cloud Neutrality = Strong Value Proposition for Customers

27

Value Proposition (cont’d)

Since INXN has spent over 10 years building a high quality and diverse customer base, it can introduce new customers

to a large, varied and highly interactive community.

INXN is focused on delivering value to its customers by building communities of interest to enable revenue growth and by being responsive to the needs of its customers.

• Develops Communities of Interest (or “hubs”) - All INXN data centers are located in near-‐city center locations giving customers direct and low-‐latency access to Europe’s leading business and residential centers

- Locations in Frankfurt, Vienna and Stockholm provide access to carriers serving Central & Eastern Europe as well as the Far East, and act as perfect gateways to these regions

• Carrier Neutrality - Remaining neutral across carriers, different cloud solutions and platforms, allows INXN to offer customers a wide choice of connectivity providers and cloud platforms to give the Olexibility, performance and cost efOiciencies

- Neutrality creates access to over 450 carriers and ISPs across Europe; INXN hosts 19 Internet exchanges (more than any other European data center provider), which means a customer can reach over 90 million broadband subscribers and around 76% of the European GDP

• Connectivity - Exceptional choice of connectivity partners and suppliers under one roof - Assistance when negotiating leased lines, IP transit and peering

28

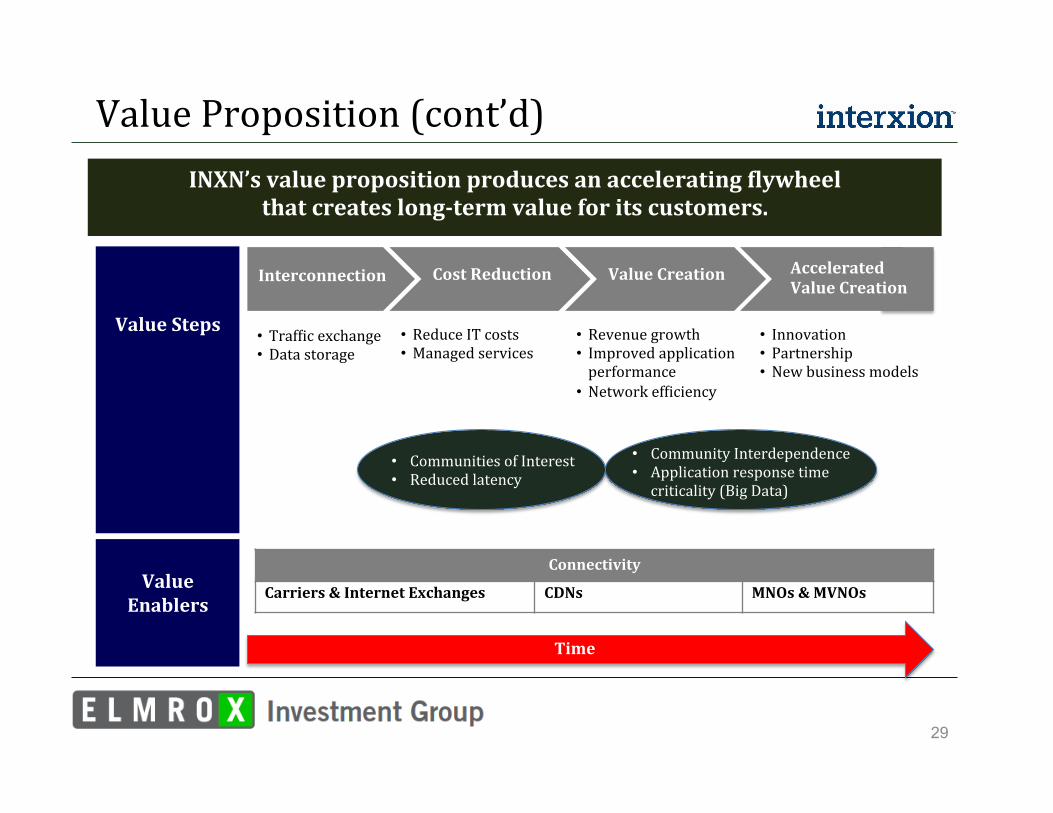

Value Proposition (cont’d) INXN’s value proposition produces an accelerating Vlywheel

that creates long-‐term value for its customers.

Value Steps

Interconnection Accelerated Value Creation

Value Creation Cost Reduction

Value

Enablers

• TrafOic exchange • Data storage

• Reduce IT costs • Managed services

• Revenue growth • Improved application performance

• Network efOiciency

• Innovation • Partnership • New business models

Time

Connectivity

Carriers & Internet Exchanges CDNs MNOs & MVNOs

• Communities of Interest • Reduced latency

• Community Interdependence • Application response time criticality (Big Data)

29

Neutrality as Value Creator

IT Buyers & Users

Corporate Enterprises Public Entities Communities

Community Services

Financial Trading Hubs Digital Media Hubs

Cloud Hubs Content Hubs

Online Gaming & Gambling

Connectivity Services

Internet Exchanges International Carriers

Telco’s Internet Service Providers

Mobile Operators

IT Services

Managed Service Providers System Integrators Cloud Providers Hosting Services

Content Distributors While Labeling Services

Connect Transact

Integrate Optimize

The Neutral Data Center

Traditional Private Cloud Public Cloud Hybrid Cloud Community Cloud

Neutrality Creates SigniVicant Value for Customers = Home of Suppliers, Buyers, IT Services Hubs and Ecosystems

30

High Quality and Growing Customer Base

INXN’s customer base is in high-‐growth markets including Vinancial services, cloud and managed services providers, digital media and carriers.

10% 9% 11% 23% 34%

4% 14% 4% 46% 5%

Interxion’s Target

Segments

Digital Media & CDNs

Financial Services

Managed Service Providers

Enterprises

Network Providers

% Monthly Recurring Revenue

Growth Rate

31

Driven by “Communities of Interest”

INXN’s carrier-‐neutrality and cloud-‐neutrality leads to the creation of “communities of interest” within its data centers. The

data center acts as a marketplace for companies to Vind one another.

ü INXN host communities of customers from across digital media value chain within its data centers to help digital media customers achieve the highest pan-‐European performance and reach

ü Provides ideal environment for effective content aggregation, exchange, storage, management and distribution and opportunity to interconnect with a growing community of content owners

Finance Hubs

Cloud Hubs

ü In the main European Oinancial centers, INXN hosts close-‐knit Oinancial services communities including exchanges, clearing houses, commercial and investment banks, brokers, proprietary trading Oirms, insurance Oirms and key industry vendors

ü Offer sub-‐millisecond, low-‐latency access to a wide range of execution venues and real-‐time data feeds

ü Bring together a wide range of hosters, infrastructure providers, hyper scale platforms, software providers and networks

ü Offer fast and easy interconnection to other cloud providers and to wide choice of carriers and ISPs within INXN data centers

ü Based around major business and consumer centers for fast access to local markets

Communities of interest bring together companies operating in same sector; they beneVit from fast and low-‐cost interconnectivity and establish valuable business relationships.

Sources: Company data and company website.

Content Hubs

• INXN has thriving and growing communities for the Oinance, digital media and cloud sectors within its data centers across Europe. These industry players colocate their infrastructure to form a hub all in close proximity to a wide range of carriers, ISPs and other connectivity providers

32

Community Focus Drives Customer Value “Magnet” companies are a community catalyst and proximity to business partners is highly valued by customers = attracts other high growth companies with robust low latency connectivity needs

Communities of interest bring together companies operating in the same sector so that they can beneVit from fast and low-‐cost

interconnectivity and establish valuable business relationships.

Interxion Focuses on Communities of Interest to Drive Customer Value and Stickiness

Segment, Customer & Application Focused

Disciplined Approach to Identifying

Target Segments

Build Communities of Interest in Target

Segments

• High growth • Need robust connectivity • BeneOit from communities of interest

• Value proximity to business partners

• Rely on real time applications

• Have Pan-‐European / global footprint

• Win magnetic companies • Magnetic companies are a catalyst for communities

• Win other community member companies

Value Creation

1

1

2

3

In Addition to Providing Premium Colocation Services, Connectivity & Coverage…

…Interxion Targets Magnetics Because They Attract Community Members…

…Interxion Fosters Communities of Interest That Add Value to Members

Financial Hub Community -‐ London

1

3 2

33

Community of Interest Draws Customers

INXN’s communities of interest represent signiVicant competitive advantages with network effects and high switch costs for existing customers.

Platform Providers

Public Infrastructure Platform as a Service

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

Global Outsourcers

Multi-‐Tennant Private Cloud

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

SaaS Providers

Vertically Integrated Public Cloud

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

Cloud Enablers

Orchestration and Virtualization

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

Cloud Providers

Public Cloud

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

Enterprises

Enterprise IT Departments

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

System Integrators

Professional and Managed Services

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

Hosting Providers

DNS, Web hosting, Email and Backup

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

IP

Internet Exchanges

Mobile

Carrier Ethernet

Direct Connect CDNs

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test LabsSource: Company data.

Enabling the ecosystem …

IP

CDN’s

Mobile

Direct Connect

Internet Exchanges

CarrierEthernet

Platform Providers

Public Infrastructure Platform as a

Service

Global Outsourcers

Multi-TennantPrivate Cloud

SaaS Providers

Vertically Integrated public cloud

Cloud Enablers

Orchestration and Virtualisation

Hosting Providers

DNS, Web hosting, Email, and Backup

SystemsIntegrators

Professional and Managed Services

Cloud Providers

Public Cloud

Enterprises

Enterprise IT Departments

Test Labs

34

Resulting in Low Customer Churn

Customer churns runs less than 1% given the strong value proposition.

Customer Concentration

Other 67%

Top 2-‐10 Customers 19%

Top 11-‐20 Customers 10%

Top Customer 4%

Source: Company data.

Sector-‐speciVic companies derive beneVit from being colocated close to one another as it provides them with the opportunity to connect and transact with other community members and customers.

Top Customer 4% 9 10

Top 2-‐10 Customers 19% ~6 ~11

Top 11-‐20 Customers 10% ~4 ~7

% of Recurring Revenue

Number of Countries

Number of Data

Centers

Customers

35

Products & Services Overview

• Highly Secure, Best-‐in-‐Class Facilities: Multi-‐level physical security including 24x7 onsite security, surveillance cameras, locked cabinets and private suites. Advanced Data Center infrastructure with multiple layers of redundancy for power, cooling and Oire-‐suppression

• Flexibility to Build Customized Solutions: Ensures that every customer's precise needs are met and their expectations are exceeded

• Market Leading Service Levels: Interxion sets rigorous Service Level Agreements for all its services, designed to offer cost-‐effective, Olexible ICT infrastructure

• Unrivalled Access & Connectivity: Hosts nineteen of Europe's Internet Exchanges, offering outstanding peering opportunities. Unprecedented connections with wide access to Internet Service Providers; hosts the largest number of peering partners across Europe

• Local Market Expertise & Strong Customer Service Team: Each data center is fully staffed with trained professionals who know the local regulations and are Oluent in the local language. Data centers are also supported by a central European Customer Service Center with a multilingual team offering technical assistance to customers 24 hours a day

• Full Support Services: Equipment housing, engineering, maintenance, connectivity solutions and a range of monitoring services provide customers with solutions to better manage ICT and internet infrastructures

Highly Valuable, Mission Critical Services for Customers

34 Data Centers in 13 Cities Across 11 European Countries

36

Products & Services Overview (cont’d)

Equipment Housing Connectivity Security & Backup Monitoring • Choice of suite, cage, or cabinet space, with three service levels:

• Basic: One power feed per cabinet, 99.9% availability of power

• Standard: Two separate power feeds to each cabinet, 99.9% availability of power

• Advanced: Two separate power feeds from separate distribution networks,99.9% availability of power

Service Center • Offers connection services to Interxion customers within its sites through a variety of services, including: - Metropolitan Connect: private ethernet connections in the metropolitan area

- IP Transit - Interxion Exchanges: ability to exchange trafOic with all other participants

• Remotely managed Oirewall service delivering cost-‐effective protection without requiring an in-‐house solution

• 24x7 monitoring generates immediate alerts and response for potential threats or service outages

• Easy to use, reliable pay-‐as-‐you-‐grow, backup and restore service using a secure interface through the internet

• Agentless technology to create successful backups of standard Oile systems, Customer is completely in control of the data

• Interxion provides round-‐the-‐clock monitoring and support to customers systems located in its Europe-‐side locations

• Based on the level of services, Interxion can monitor and maintain applications, operating systems and hardware itself

• Interxion’s state-‐of-‐the-‐art monitoring and management center (ESC) is located in London, staffed 24 hours per day, 7 days per week, by multilingual staff

• The ESC connects to all Interxion sites and is responsible for commissioning maintenance and security operations for hosted clients

• Colocation contracts with customers are typically for three to Oive years, but can last up to 10 years. Contracts usually include price escalators that adjust for inOlation

• Typically 60-‐70% of new bookings in any given year are generated from existing customers

“Our strategy of building resilient communities of interest…we do so by focusing our sales and marketing efforts against speciVic target market segments.”(1)

“We are able to attract magnet customers and their communities of interest members because of the value they receive from our

leadership and connectivity and customer service.(1) (1) Vice Chairman, Chief Executive OfOicer and President, David C. Ruberg, on May 8, 2013 earnings call.

37

Cost Structure

Fixed Cost Model + Strong Revenue Growth = Growing EBITDA Margins

Fixed Cost Model

Other, 30% Personnel, 28%

Property, 20% Power, 22%

Operating Expense Breakdown(1) Fixed / Semi-‐Fixed

Source: Company data. (1) CFO Josh Josh, August 7, 2013 earnings call. (2) Vice Chairman, Chief Executive OfOicer and President, David C. Ruberg, August 7, 2013.

• All power costs are recovered from customers • Once a data center is established, rental and

most staff costs are Oixed / semi-‐Oixed leading to increase in incremental proOit

• SG&A as % of sales should decline in 2014 and 2015 as the utilization rate recent capacity expansions increases

• “We plan, as we've done for the last 6 years, to grow our adjusted EBITDA margins somewhere between 100 and 150 to 200 basis points each year.”(1)

“There's a world of difference between the wholesalers and retailers. Wholesalers don't care who comes into their data centers. We're really picky about it…. our focus on communities of interest, which we are geared throughout the company to make sure that we have a consistent

population that has the potential to interconnect and create value over time.” (2)

38

SigniOicant Operating Leverage

Incremental Margins Generally ~80%

A visible path to 50% plus EBITDA margins from ~42% in 2013.

Multiple Drivers to Deliver Revenue & Margin Growth

• Favorable industry fundamentals

• Attractive supply/demand dynamics

• New customer acquisition in target, growing segments

• Favorable contracts enabling increased revenue per Sqm

• Disciplined expansion 15% 13% 12% 11% 11%

20% 19% 18% 17% 17%

13% 16% 14% 14% 15%

18% 16% 18% 17% 15%

2008 2009 2010 2011 2012

Other

Energy

Personnel

Property

Adj. EBITDA Margin 35% 42% 37% 38% 40%

Adjusted EBITDA Margin Expands by 660 Basis Points

39

Strong Balance Sheet & Liquidity

SigniVicant Balance Sheet Capacity for Shareholder Value Creation

(€ in millions) Actuals Jun 30, 2013

As Adjusted* Jun 30, 2013

Actuals Dec.31, 2012

Cash & Cash Equivalents 59.8 89.2 68.7

Total Borrowings(1)(2) 302.8 363.1 286.8

Shareholders Equity 390.3 367.1 375.6

Total Capitalization 693.1 730.2 662.4

Total Borrowings / Total Capitalization 43.7% 49.7% 43.3%

Gross Leverage Ratio(3) 2.5x 3.0x 2.5x

Net Leverage Ratio(4) 2.0x 2.3x 1.9x

• ReOinanced bonds with €325 million 6.0% Senior Secured Notes due 2020

• Solid cash position and substantial additional liquidity from undrawn €100 million Revolving Credit Facility

• New €6 million mortgage on recently purchased property in Amsterdam

• SigniOicant room under covenant (maximum leverage ratio of 4.0x)

* As adjusted Oigures represent June 30, 2013 balance sheet adjusted for reOinancing completed on July 3, 2013: the purchase of the 9.5% Senior Secured Notes due 2017 Oinanced by the issue of the 6.0% Senior Secured Notes due 2020 and the new €100 million revolving credit facility (which remained undrawn), the net cash proceeds excluding payment of interest up to redemption date to the 9.5% Senior Secured Notes holders and the after tax impact of the one-‐off Oinancial charges (1) Total Borrowings = 9.50% Senior Secured Notes due 2017 including premium on additional issue and are shown after deducting underwriting discounts and commissions, offering fees and expenses + Mortgages + Financial Leases + Other

Borrowings – Revolving credit facility deferred Oinancing costs. (2) Total Borrowings “As adjusted” = 6.0 % Senior Secured Notes due 2020 and are shown after deducting underwriting discounts and commissions, offering fees and expenses + Mortgages + Financial Leases + Other Borrowings” – €100 million

Revolving credit facility deferred Oinancing costs. (3) Gross Leverage Ratio = (9.50% Senior Secured Notes due 2017 at face value + Mortgages + Financial Leases + Other Borrowings) / Last Twelve Months Adjusted EBITDA. (6.0% Senior Secured Notes due 2020 for the “As adjusted” Oigures. (4) Net Leverage Ratio = (9.50% Senior Secured Notes due 2017 at face value + Mortgages + Financial Leases + Other Borrowings – Cash & Equivalents) / Last Twelve Months Adjusted EBITDA . (6.0% Senior Secured Notes due 2020 for the “As

adjusted” Oigures).

40

Predictable & Growing Free Cash Flow

“We are focused on creating shareholder value and that translates into sustainable cash per share growing over the next 3 to 5 years.”(1)

(1) Vice Chairman, Chief Executive OfOicer and President, David C. Ruberg, on September 12, 2013. (2) 26 data centers in operation as of December 31, 2009: VIE1, BRU1, CPH1, PAR1, PAR2, PAR3, PAR4, PAR5, PAR6, DUS1, FRA1, FRA2, FRA3, FRA4, FRA5, DUB1, AMS1, AMS2, AMS3, AMS4, AMS5, HIL1, MAD1, STO1, ZUR1, AND LON1.

Maintenance capex low at low single digits % of sales.

(13)

Cumulative Data Centre Investment

Revenue Gross ProOit (56% Margin)

Maintenance Capex Annual Cash return

(€ in millions)

24%

FY 2009 Returns

517 264

173 165 (8)

Cumulative Data Centre Investment

Revenue Gross ProOit (66% Margin)

Maintenance Capex Annual Cash return

32%

2Q 2013 LTM Returns

Case Study: How Cash Generation Improves as Data Centers Mature(2)

(€ in millions)

• 26 total data centers in operation • 54,800 sqm of equipped space • 70% utilization • 24% annual cash return • Same group as at end 2009 • 60,700 sqm of equipped space after phased expansions

• 81% utilization • 32% annual cash return

41

Attractive Cash Returns

35% Annual Cash Return on Original Data Center Investment

N.B.: “Full” data centers deOined as those at 85% or greater utilization. Data center gross Oixed asset cost (Gross PP&E) at historic exchange rates.

€ 100

€ 60 € 40 € 35

Original Data Center Investment

Annual Recurring Revenue Gross ProOit (65% Gross Margin)

Annual Cash Return

(€ in millions)

35%

FY 2009 Returns

% of Original Data Center Investment

40% 60% 100%

42

Illustrative Revenue Ramp of Expansion Revenue grows over time as energy consumption increases.

Source: Company presentation.

Three Components • Space (sqm billed in advance) • Power Reservation (Cooling Capacity) (MW billed in advance) • Energy Consumption (KWh billed in arrears) Deployment Maturation & Revenue Development Occurs Over Multiple Quarters • Mix initially tilted toward space • As contracted space Oills, energy consumption increases, requiring greater cooling capacity

• Over time, power reservation and energy consumption become a larger share

Applies to Both Customers and Data Centers

43

Capital Allocation

“The target…generate returns 30% to 40% on capital that you invest.”(1)

• New projects have highly attractive return proOiles: management typically will only do deals with a minimum 30% IRR generally over 10 years

• Management focus on reinvesting cash Olow into the business for growth

“For the next couple of years, the best return of the capital that we currently have…is to build data centers or to buy an opportunity.”(1)

(1) Vice Chairman, Chief Executive OfOicer and President, David C. Ruberg, on September 12, 2013.

Expansion Strategy

• Disciplined approach to expansion - Sized to existing customer demand - Based on target IRR

• Low execution risk - Uniform design - Campus-‐oriented - Phase build and capex deployment

44

Long-‐Term, Disciplined Growth Mindset

“Interxion looks to deploy its capital on a demand-‐driven basis.”(1)

Market Project Project

CapEx (€m)

Equipped Space (sqm)

Initial Customer Availability Project Opened

Frankfurt FRA 7: New Build 21 1,500 1,500 1Q 2012

Stockholm STO 1: Phase 4 Expansion 5 500 500 2Q 2012

Paris PAR 7: Phase 1 New Build 70 4,700 4,700 2Q 2012

Amsterdam AMS 6: New Build 60 4,400 4,400 3Q 2012

London LON 2: New Build 38 1,500 1,500 3Q 2012

Madrid MAD 2: Phase 1 New Build 10 800 800 4Q 2012

Frankfurt FRA 6: Phase 3 Expansion 5 600 600 1Q 2013

Copenhagen CPH 1: Expansion 2 300 300 2Q 2013

Stockholm STO 2: Phase 1 New Build 11 500 500 2Q 2013

Vienna VIE 1: Phase 4 Expansion 1 400 400 3Q 2013

Zurich ZUR 1: Phase 4 Expansion 4 500 -‐-‐ 4Q 2013

Stockholm STO 2: Phase 2 Expansion 6 500 -‐-‐ 1Q 2014

Frankfurt FRA 8: Phase 1 & 2 New Build 30 1,800 -‐-‐ H1 2014

Source: Company data. (1) Vice Chairman, Chief Executive OfOicer and President, David C. Ruberg, on May 8, 2013 earnings call.

45

Intense Focus on New Customers

“Ecosystems such as Interxion's are increasingly important to Vinancial service providers looking to expand… allow them to connect with current

and potential customers, secure a variety of services to meet the requirements and growing demands of customers.”(1)

(1) 451 Research Market Insight on August 4, 2013.

Strategic long-‐term focus on cloud deployments.

• Public Cloud Services - Growing demand from customers that want public cloud services but remain reticent due to concerns

around network performance and security

- Digital media companies, online gaming companies, system integrators are key players

• Hybrid Cloud - Primary future demand driver of enterprise use of direct connections to third-‐party cloud providers

• Enterprise Customers - INXN’s DirectConnect program with Amazon could augment its proOile with enterprise customers

- Such new business would further diversify an already variegated customer base

46

Big Geographic Growth Opportunities

SigniVicant runway to expand given growth opportunities in Eastern Europe, Latin America, the Middle East, and Asia.

Latin America has been traditionally underserved and offer signiVicant opportunities especially if the tax regime in Brazil becomes favorable. Multi-‐tenant data center capacity remains tight across the continent at

more than 80% utilization in the top markets in Latin America.

• We believe that Interxion is extremely well positioned to expand beyond its core European footprint into adjacent markets and new geographies

• Cash Olow generation should accelerate in 2014 and 2015 as recent expansion opportunties ramp towards full utilization. This increased cash Olow can fund geographic expansion

• INXN also has ample balance sheet capacity for acquisitions with room to 4.0x covenants

• Markets outside of Europe and North America are highly fragmented

• Eastern Europe is rapidly growing and is a natural extension of INXN’s current western European footprint

47

Valuation & Financials

We Believe INXN is Undervalued

• Predictable, recurring business model

• Consistent and growing cash Olows

• SigniOicant competitive advantages and moats relative to North America data center market

• Long runway of secular growth opportunities in early innings of adoption (cloud, digital media, big data, etcetera)

• BeneOits of growth capex

• Likely growth expansion into new markets either organically and/or inorganically

• Low balance sheet leverage relative to trading multiples of other recurring, high cash Olow stream businesses

• Recovery on European economy

• Strategic value of the business

We believe Interxion is undervalued with long-‐term upside from secular growth opportunities. At current prices, a long-‐term shareholder

pays ~13x consensus FYE 12/31/14E SSFCF, which does not account for:

49

Why This Opportunity Exists

• Overlooked because is European domiciled Oirm with U.S. stock listing

• Overcapacity and pricing concerns in North American market have incorrectly been applied to European data center market

• Investors overlooking INXN’s steady-‐state free cash Olow because it is masked by signiOicant growth capital expenditures

• Misguided concerns over weak macroeconomic environment in Europe affecting INXN demand

• 30% private equity ownership creates overhang / valuation discount

• Misplaced concerns that Europe-‐only footprint is a growth headwind

• Mixed sell side coverage: some U.S., some Europe

Market incorrectly places concerns over competitive issues speciVic to the North American data center market onto INXN.

50

Why are INXN Shares Attractive?

• Overcapacity and pricing risk

• Provider of commoditized wholesale data

• Builds speculative capacity