product key facts - fwd · this statement provides you with key information about this product....

TRANSCRIPT

This statement provides you with key information about this product.

This statement is a part of the offering document.

You should not invest in this product based on this statement alone.

There is a "Glossary" section at the end of this statement. For those terms which are capitalized, please

refer to the "Glossary" section on page 8 for explanations.

Quick facts

(PMH010BB1309)Page 1

September 2013

PRODUCT KEY FACTSi.Wealth Regular Investment Savings Plan*

FWD Life Insurance Company (Bermuda) Limited

Name of insurance company: FWD Life Insurance Company (Bermuda) Limited

Single or regular premium: Regular premium

Regular premium frequency: Annually, semi-annually or monthly

Minimum premium payment term: 5 years

Policy currency: USD

Minimum investment: For premium term of 5 years:

Annually: US$2,400 Semi-annually: US$1,200 Monthly: US$200

For premium terms of 10 years, 15 years, 20 years and 25 years:

Annually: US$1,800 Semi-annually: US$900 Monthly: US$150

Maximum investment: For premium term of 5 years:

Annually: US$6,000,000 Semi-annually: US$3,000,000 Monthly: US$500,000

For premium term of 10 years:

Annually: US$2,000,000 Semi-annually: US$1,000,000 Monthly: US$166,666

For premium terms of 15 years, 20 years and 25 years:

Annually: US$1,000,000 Semi-annually: US$500,000 Monthly: US$83,333

Period with surrender charge The entire period of the selected premium term (early redemption charge):

Death benefit: 101% of the account value

Governing Law of policy: The policy is issued under, and will be construed in accordance with, the laws of the Hong Kong Special Administrative Region

* This is an investment-linked assurance scheme and is not a bank deposit or savings account. It is not a capital guaranteed/protected product and is not a protected deposit for the purpose of Deposit Protection Scheme.

Important

Page 2

i.Wealth Regular Investment Savings Plan

o This investment-linked assurance scheme (“ILAS policy”) is a long-term investment-cum-life insurance product.

It is only suitable for investors who:

- understand that the principal will be at risk

- are prepared to hold the investment for a long-term period

- have both investment and estate planning objectives as it is a packaged product that includes both

investment and insurance element with death benefits payable to third party beneficiaries.

o This ILAS policy is not suitable for investors with short- or medium- term liquidity needs.

o Fees and charges –

Up to 20% of your premiums after taking into account all applicable guaranteed bonuses will be paid to FWD Life

Insurance Company (Bermuda) Limited (herein after called “FWD”) to cover all the fees and charges at the ILAS

policy level, of which the cost of life protection is 0%, and this will reduce the amount available for investment.

Please note that the above figure(s) are calculated based on the following assumptions: (a) the payment of regular premium of

USD12,500 per annum; (b) you hold your ILAS policy for 25 years; (c) an assumed rate of return of 3% per annum throughout 25

years; (d) any optional supplementary benefits are not included; and (e) there is no early withdrawal / termination of your ILAS policy.

You must understand that these ILAS level charges are on top of, and in addition to, the underlying funds level

charges. The above figures do not take into account any early surrender / withdrawal charges.

The above percentage(s) of your premiums for covering the total fees and charges are calculated

based on the assumptions above for illustration purposes. The actual percentage(s) may change

depending on individual circumstances of each case, and will be significantly higher if the premium

amount is lower.

o Long-term features –

Early surrender (early redemption) / withdrawal charges:

(a) There will be an early surrender (early redemption) / withdrawal charge of up to 100% of the account value

of the Initial Contribution Account in case of surrender within the premium term. You may also lose your

entitlement to the special bonus and loyalty bonus.

Loyalty bonus:

(b) At the end of the premium term, a loyalty bonus will be credited to your ILAS policy. The loyalty bonus is

equal to 100% of the total policy fees deducted throughout the premium term. The loyalty bonus will be

used to allocate additional notional units to the Accumulation Contribution Account according to your

investment choice allocation instructions in effect at the time, provided that your ILAS policy is in force. The

payment of loyalty bonus is non-guaranteed and is made at the sole discretion of FWD. It is subject to

change by giving 1 month's prior written notice or such shorter period of notice in compliance with the

relevant regulatory requirements.

Page 3

i.Wealth Regular Investment Savings Plan

Important (Cont.)

o Intermediaries’ remuneration

Although you may pay nothing directly to the intermediary who sells/distributes this ILAS policy to you, the

intermediary will receive remuneration which, in effect, will be borne out of the charges you pay. You should ask

your intermediary before taking up your ILAS policy to know more about the level or amount of the remuneration

that the intermediary will receive in respect of your ILAS policy. If you ask, your intermediary should disclose the

requested information to you.

What is this product and how does it work?

o This product is an investment-linked assurance scheme. It is a life insurance policy issued by FWD. This is not a fund authorized by the SFC pursuant to the Code on Unit Trusts and Mutual Funds (“UT Code”).

o Although your ILAS policy is a life insurance policy, because your death benefit is linked to the performance of the underlying funds you selected from time to time, your death benefit is subject to investment risks and market fluctuations. The death benefit payable may be significantly less than your premiums paid and may not be sufficient for your individual needs.

o "Underlying funds" available for selection are the funds listed in the investment choices brochure. These may include funds authorized by the SFC pursuant to the UT Code, but may also include other portfolios internally managed by FWD on a discretionary basis not authorized by the SFC under the UT Code.

o Due to the various fees and charges levied by FWD on your ILAS policy, the return on your ILAS policy as a whole may be lower than the return of the underlying funds you selected. Please see page 6 - 7 of this statement for details of the fees and charges payable by you.

o Note, however, that all premiums you pay towards your ILAS policy, and any investments made by FWD in the underlying funds you selected, will become and remain the assets of FWD. You do not have any rights or ownership over any of those assets. Your recourse is against FWD only.

o The premiums you pay, after deduction of any applicable fees and charges of your ILAS policy, will be invested by FWD in the "underlying funds" you selected (see below) and will accordingly go towards accretion of the value of your ILAS policy. Your ILAS policy value will be calculated by FWD based on the performance of your selected underlying funds from time to time and the ongoing fees and charges which will continue to be deducted from your ILAS policy value.

What are the key risks?

Investment involves risks. Please refer to the principal brochure for details including the risk factors.

o Foreign exchange risks - The investment returns of your ILAS policy may be subject to foreign exchange risks as some of the underlying funds may be denominated in a currency which is different from that of your ILAS policy.

o Market risks - Return of this ILAS policy is contingent upon the performance of the underlying funds and therefore there is a risk of capital loss.

o Premium holiday (suspension of premium) - With no premium contribution during premium holiday, the value of this ILAS policy may be significantly reduced due to fees and charges, which are still deductible during premium holiday, and your entitlement to bonuses may also be affected. If the account value at any point in time is not sufficient for FWD to cover all the fees and charges (for details of fees and charges, please refer to "What are the fees and charges?" section on page 6 - 7 of this statement), you will have to resume paying your premiums as and when notified by FWD, failing which your ILAS policy will terminate when your account value reaches zero.

o Early surrender (early redemption)/withdrawal penalty - This ILAS policy is designed to be held for a medium/long term period. Early surrender or withdrawal of the ILAS policy/suspension of or reduction in premium may result in a significant loss of principal and bonuses awarded. Poor performance of underlying funds/assets may further magnify your investment losses, while all charges are still deductible.

o The investment choices available under this product can have very different features and risk profiles. Some may be of high risk. Please read the principal brochure and the offering document of the underlying funds involved for details.

o Credit and insolvency risks - This product is an insurance policy issued by FWD. Your investments are subject to the credit risks of FWD.

o i.Wealth Regular Investment Saving Plan is not a bank deposit or savings account and is not a protected deposit for the purpose of Deposit Protection Scheme.

Is there any guarantee?

This product does not have any guarantee of the repayment of principal. You may not get back the full amount of premium you pay and may suffer investment losses.

Page 4

i.Wealth Regular Investment Savings Plan

Other features

o Account structure:

➤ This ILAS policy has a two-part account structure consisting of the Initial Contribution Account and the

Accumulation Contribution Account. Regular Investment Premiums payable during the Initial Contribution

Period are allocated to the Initial Contribution Account, and Regular Investment Premiums payable

thereafter are allocated to the Accumulation Contribution Account.

o Special bonus:

➤ A special bonus will be credited to your ILAS policy at the end of the 1st policy year. Please refer to page 2 of

the product brochure of i.Wealth Regular Investment Savings Plan for details.

The special bonus will be used to allocate additional notional units to the Initial Contribution Account according

to your investment choice allocation instructions in effect at the time, provided that your ILAS policy is in force.

In the event of death of the insured within the first two policy years, the death benefit payable will be reduced

by any special bonus previously paid.

o Loyalty bonus:

➤ At the end of the premium term, a loyalty bonus will be credited to your ILAS policy. Please refer to page 2 of

the product brochure of i.Wealth Regular Investment Savings Plan for details.

The loyalty bonus will be used to allocate additional notional units to the Accumulation Contribution

Account according to your investment choice allocation instructions in effect at the time, provided that

your ILAS policy is in force. The payment of loyalty bonus is non-guaranteed and is made at the sole

discretion of FWD. It is subject to change by giving 1 month's prior written notice or such shorter period

of notice in compliance with the relevant regulatory requirements.

o Accidental death benefit:

➤ While this ILAS policy is in force and before the 5th policy anniversary, in the event of the death of the insured

as a consequence of an Accident, an additional 10% of the account value, subject to a maximum of

US$12,500 will be payable as accidental death benefit. Such account value is the redeemed value of all

notional units in the Policy Account on the next dealing date after the receipt of a duly completed claims

form.

o Partial withdrawal:

➤ You can make partial withdrawals by redeeming notional units from the Accumulation Contribution Account

any time after the Initial Contribution Period. After the premium term, partial withdrawals can also be made

from the Initial Contribution Account. Currently, there are no charges applicable to partial withdrawals. The

minimum amount to be withdrawn is currently US$250 and the Minimum Remaining Account Value of the

Accumulation Contribution Account is currently US$2,500.

Page 5

i.Wealth Regular Investment Savings Plan

Please refer to the "Summary of charges" section (page 4 to 6) of the product brochure of i.Wealth Regular Investment Savings Plan for details of the charges.

Deducted on the first policy charges due date after policy inception and thereafter on each Monthiversary by redeeming notional units from the Initial Contribution Account during the Initial Contribution Period, and thereafter from the Accumulation Contribution Account until the end of the premium term.

Deducted on the first policy charges due date after policy inception and thereafter on each Monthiversary by redeeming notional units from the Initial Contribution Account during the premium term. Deducted on the first policy charges due date after policy inception and thereafter on each Monthiversary by redeeming notional units from the Policy Account while the ILAS policy is in force.

Deducted from the Initial Contribution Account by redeeming notional units.

N/A

N/A

Upon policy termination and before the end of the selected premium term, except in the case of death of the insured, surrender charge (early redemption charge) will be charged as a percentage of the account value of the Initial Contribution Account. The charge will depend on the premium term and the policy year.

Please refer to the "Summary of charges" section (page 4 to 6) of the product brochure of i.Wealth Regular Investment Savings Plan for details and illustrative examples of early redemption charge.

Currently waived

Currently waived

1st to 10th policy year

From 11th policy year onwards

0.1% of the account value per month, which is equivalent to an annual rate of 1.2% 0.8% divided by 12, of the account value per month, which is equivalent to an annual rate of 0.8%

US$6 per month, which is equivalent to an

annual charge of US$72

3.8% divided by 12, of the account value of the Initial

Contribution Account per month, which is equivalent to

an annual rate of 3.8%

Policy fee

Administrative charge

Investment portfolio management charge

Surrender charge (early redemption charge)

Partial withdrawal charge

Switching / reallocation charge

FWD reserves the right to vary the policy charges or impose new charges with not less than 1 month's prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

What are the fees and charges?

Scheme level

Page 6

Fees & charges Applicable rates Deducted from

i.Wealth Regular Investment Savings Plan

What are the fees and charges? (Cont.)

Underlying fund level

You should note that the underlying funds of the investment choices may have separate charges on management fee, performance fee, bid-offer spread and/or switching fee. You do not pay these fees directly either (1) the fees will be deducted and such reduction will be reflected in the unit price of the underlying funds or (2) units will be redeemed from your investment choices to pay these fees. Please refer to the investment choices brochure for details of the specified valuation day for the investment choices. For details, please refer to the offering document of the underlying funds and/or the principal brochure of i.Wealth Regular Investment Savings Plan, which are available from FWD upon request.

What if you change your mind?

Cooling-off period

o Cooling-off period is a period during which life insurance policyholders may cancel their policies and get back their original investments (subject to market value adjustment) within the earlier of 21 days after the delivery of the ILAS policy or issue of a notice to you or your representative. Such notice should inform you of the availability of the ILAS policy and expiry date of the cooling-off period. Please refer to the cooling off initiative issued by HKFI from time to time for reference.

o You have to tell FWD by giving a written notice. Such notice must be signed by you and received directly by FWD at 1/F Customer Service, FWD Financial Centre, 308 Des Voeux Road Central, Hong Kong.

o You may get back the amount you paid, or less if the value of the investment choices has gone down.

Insurance company’s information

FWD Life Insurance Company (Bermuda) Limited

Address: 28/F., FWD Financial Centre, 308 Des Voeux Road Central, Hong Kong

Phone: 2850 2333 Fax: 2850 3999

Email: [email protected]

Website: www.fwd.com.hk

Important

FWD is subject to the prudential regulation of the Insurance Authority. However, the Insurance Authority does not give

approval to individual insurance products, including the FWD ILAS plan referred to in this statement.

If you are in doubt, you should seek professional advice.

The SFC takes no responsibility for the contents of this statement and makes no representation as to its accuracy or

completeness.

Page 7

i.Wealth Regular Investment Savings Plan

Glossary

The following terms have the meanings set out below:

Terms Meanings

An unforeseen and unexpected event or contiguous series of events of violent,

accidental, external and visible nature which shall be the sole cause of a bodily injury

while the ILAS policy is in force.

An account set up for the policyholder and used to maintain the notional units

allocated in respect of all premiums contributed after the Initial Contribution Period.

An account set up for the policyholder and used to maintain the notional units

allocated in respect of all premiums contributed during the Initial Contribution Period.

The period during which the premiums payable are used for the allocation of notional

units to the Initial Contribution Account. The Initial Contribution Period varies by the

premium term.

An amount set to limit the partial withdrawal from the Accumulation

Contribution Account.

The same date each month as the commencement date (the date of premium

commencing and the date used for determining the issue age of the insured). If the

Monthiversary is not a business day, it will be postponed to the next business day. If

the Monthiversary does not exist in a particular month, it will be the last day of

the month.

An account set up for the policyholder and used to maintain the total notional units

of the Initial Contribution Account and the Accumulation Contribution Account.

The premiums regularly made into the Policy Account for the allocation of notional

units and are payable until the end of the premium term or the death of the insured,

whichever is earlier.

Page 8

Accident

Accumulation

Contribution Account

Initial Contribution Account

Initial Contribution Period

Minimum Remaining

Account Value

Monthiversary

Policy Account

Regular Investment Premium

i.Wealth Regular Investment Savings Plan

INSURANCE

WWW.FWD.COM.HK 3123 3123

i.Wealth 愛豐裕 (PMH010AB1308)

The principal brochure of i.Wealth Regular Investment Savings Plan# (the “Policy”) consists of this product brochure and the investment choices brochure. This product brochure is issued and should be read in conjunction with the investment choices brochure and the product key facts, which are part of the offering documents. Such documents are available on the FWD Life Insurance Company (Bermuda) Limited (hereafter “FWD”) website at www.fwd.com.hk. Investors should refer to the “General information - Glossary” section on pages 10 for the capitalized terms used in this product brochure.

i.Wealth Regular Investment Savings Plan is an investment-linked assurance scheme under Class C linked long-term business as defined in Part 2 of Schedule 1 to the Insurance Companies Ordinance offered by FWD as an authorized insurer in Hong Kong. Your investments are therefore subject to the credit risks of FWD.

# This is an investment-linked assurance scheme and is not a bank deposit or savings account. It is not a capital guaranteed/protected product and is not a protected deposit for the purpose of Deposit Protection Scheme.

Company BackgroundFWD HK and Macau are the member companies of Pacific Century Group (PCG). With the strong foundation of PCG, FWD Hong Kong and Macau currently manage over USD 5 billion# in assets and have a solvency ratio well above the regulatory requirements.

Our operations in Hong Kong and Macau include:

Life Insurance Since its establishment in 1984, FWD Life Insurance has always been committed to offering customers a comprehensive range of quality insurance products and services. The company’s extensive portfolio of insurance products - which includes individual life, medical and employee benefits schemes - is tailored to meet customers’ needs throughout the different stages of their lives. The company is one of the top 10 insurance players in Hong Kong*.

The Macau office, since starting operations in 2000, has been committed to offering a full range of quality insurance products and services to the locals, including life insurance, health benefits, disability insurance and crisis insurance.

General Insurance Established in 1989, FWD General Insurance provides quality services and offers most types of non-life insurance products to individuals and businesses in the local market.

Pension Trust FWD Pension Trust is committed to contributing its expertise to provide quality pension trust services to corporate and individual customers.

Financial Planning Established in 2002, FWD Financial Planning is committed to setting the standard as a market leader in Independent Financial Advice, and attracting the best financial advisors in the industry to deliver quality financial planning advice to clients. The customer-centric focus of the Company ensures that clients receive the best solution from advisors, based on a broad suite of products from many companies.

# Figure as at 31 December 2012

* Source: Office of the Commissioner of Insurance - Provisional Statistics for Long Term Business Q4 2012

• Start your investment savings with as little as US$150 per month• Your choice of premium terms according to your personal needs• No subscription charge means all your savings are working for you right from the start. For details of other applicable fees

and charges, please refer to the “Summary of charges” section• A wide range of well-known investment choices helps you take every chance to boost your wealth

Your choice of premium

You may select a premium term of 5, 10, 15, 20 or 25 years at your own choice, and your Regular Investment Premiums can be made monthly, semi-annually or annually to meet your personal needs. You can start your investment savings as little as US$150 per month according to the table below. FWD reserves the right to change the requirements, subject to 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

i.Wealth Regular Investment Savings Plan has a two-part account structure consisting of the Initial Contribution Account and the Accumulation Contribution Account. Regular Investment Premiums payable during the Initial Contribution Period are allocated to the Initial Contribution Account, while Regular Investment Premiums payable thereafter are allocated to the Accumulation Contribution Account. The length of the Initial Contribution Period is determined according to your selected premium term. During the Initial Contribution Period, if premiums are unpaid 30 days after the premium due date, FWD reserves the right to terminate the Policy.

Please note:• FWDwillinvestthenetpremiumreceivedfromyouintotheunderlyingfundscorrespondingtotheinvestmentchoicesas

selected by you for FWD’s asset liability management.• Premiums paid by you towards the Policy will become and remain the assets of FWD. You are not investing in the

underlying funds and do not have any rights or ownership over any of those assets. Your recourse is against FWD only.• YoushouldinvestinthisPolicyonlyifyouintendtopaythepremiumforthewholeofthepremiumterm.Earlysurrender

or withdrawal of the Policy/suspension of or reduction in Premium may result in significant loss of principal and/or bonuses awarded. Poor performance of underlying funds may further magnify your investment losses, while all charges are still deductible.

• ThisPolicyisintendedtobealongterminvestment(aminimumof5years).IfyousurrenderthisPolicybeforethefullpremium term, you may not get back the full amount invested.

Your personal goals, such as overseas vacation, buying a new house, getting married, sending children to universities and perhaps taking early retirement, are likely to change from time to time as you pass through different stages in life. i.Wealth Regular Investment Savings Plan is an investment-linked assurance scheme which is specially customized for you to meet these changing needs throughout your lifetime.

One single Policy can help accomplish your personal goals

Regular Investment Savings Plan

Premium term 5 years 10 years 15 years 20 years 25 years

Minimum Regular Investment Premium

Annually US$2,400 US$1,800

Semi- annually

US$1,200 US$900

Monthly US$200 US$150

Maximum Regular Investment Premium

Annually US$6,000,000 US$2,000,000 US$1,000,000

Semi- annually

US$3,000,000 US$1,000,000 US$500,000

Monthly US$500,000 US$166,666 US$83,333

1

Premium term Initial Contribution Period

5 years 24 months

10 years 26 months

15 years 28 months

20 years 30 months

25 years 32 months

2

Your choice of investment choices This Policy offers a wide range of investment choices, all managed by professional investment managers, for your selection. You can allocate your premiums to a single investment choice or multiple investment choices as provided, subject to a minimum allocation per investment choice of 10% of your total premium. FWD reserves the right to change the requirements, subject to 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

Please note:

• The investmentchoicesavailableunder i.WealthRegularInvestment Savings Plan can have very different features and risk profiles. Some may be of high risk.

• The unit allocation to your Policy is notional in natureand solely for the purpose of determining the account value of your Policy. For details of the investment choices, please refer to the investment choices brochure, the corresponding appendix and the prospectuses of the underlying funds that are made available by FWD.

Special bonus to boost your savings A special bonus will be credited to your Policy at the end of the 1st policy year. The amount of bonus depends on the premium term and the annualized Regular Investment Premium according to the following formula and bonus rate table.

Annualized Regular Investment Premium

Bonus rate (as a % of annualized Regular Investment Premium) by premium term

5 years 10 years 15 years 20 years 25 years

US$1,800 - less than US$3,000

1.2% 2.5% 4.5% 10.0% 12.0%

US$3,000 - less than US$6,000

2.0% 4.0% 8.5% 14.5% 18.0%

US$6,000 - less than US$12,000

4.0% 8.0% 15.5% 25.5% 32.0%

US$12,000 - less than US$20,000

5.0% 10.0% 21.5% 35.0% 44.0%

US$20,000 or above

6.0% 12.0% 24.0% 40.0% 50.0%

Special bonus =bonus rate x annualized Regular Investment Premium

The special bonus will be used to allocate additional notional units to the Initial Contribution Account according to your investment choice allocation instructions in effect at the time, provided that the Policy is in force.

Please note:

• Intheeventofdeathoftheinsuredwithinthefirsttwopolicy years, the death benefit payable will be reduced by any special bonus previously paid.

• ThespecialbonusispartoftheaccountvalueoftheInitialContribution Account, therefore they are subject to the fees and charges as listed in the “Summary of charges” section.EarlysurrenderofthePolicymayresultinalossofall or part of the special bonus.

• The specialbonus ratesmentionedabovearebasedonthe annualized Regular Investment Premium, and do not represent the rate of return or the performance of your investment.

Loyalty bonus to reward your long term commitment At the end of the premium term, a loyalty bonus equals to the total policy fees deducted throughout the premium term will be credited to your Policy.

The loyalty bonus will be used to allocate additional notional units to the Accumulation Contribution Account according to your investment choice allocation instructions in effect at the time, provided that the Policy is in force. The payment of loyalty bonus is non-guaranteed and is made at the sole discretion of FWD. It is subject to change by giving 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

3

Life protection up to age 100While the Policy is in force, the life coverage is equal to 101% of the total account value of your Policy. In addition, an extra 10% of the account value, subject to a maximum of US$12,500, will be payable as an accidental death benefit in the event of death of the insured as a consequence of an Accident before the 5th policy anniversary.

Please note:

• Yourdeathbenefit is linked to theperformanceofthe underlying funds you selected from time to time and is therefore subject to investment risks and market fluctuations. The death benefit payable may be significantly less than your premiums paid and may not be sufficient for your individual needs.

Manage flexibly to fit your goalsTo manage your portfolio with flexibility, you can reduce your Regular Investment Premium anytime after the Initial Contribution Period, provided that such premium meets the minimum amount required. You can also temporarily suspend your Regular Investment Premium anytime after the Initial Contribution Period, provided that the account value of the Accumulation Contribution Account is sufficient to cover all the relevant fees and charges.

Moreover, you can partially withdraw your notional units from the Accumulation Contribution Account anytime after the Initial Contribution Period. After the premium term, partial withdrawals can also be made from the Initial Contribution Account. Currently, there are no charges applicable to partial withdrawals.The minimum amount to be withdrawn is currently US$250 and the Minimum Remaining Account Value of the Accumulation Contribution Account is currently US$2,500. FWD reserves the right to change the requirements, subject to 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

Please note:

• While you temporarily suspend your RegularInvestment Premium payments, if the account value at any point in time is not sufficient for FWD to cover all the fees and charges, you will have to resume paying your premiums as and when notified by FWD, failing which your Policy will terminate when your account value reaches zero.

Tailor-made online service platformInvestment opportunities are constantly changing. i.Wealth Regular Investment Savings Plan offers an unlimited number of free switching and reallocation that gives you the flexibility to adjust your investment portfolio anytime, for any reason, and at no extra cost. FWD understands the importance of making swift responses to market changes. You can request switching/reallocation of investment choices via our online platform, the customer online service, allowing you to re-align your investment strategy anytime and anywhere.

Currently, there is no charge on switching/reallocation, nor is there a limit on the frequency of switching investment choices. The minimum switching amount is currently US$125. FWD reserves the right to change the requirements, subject to 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

Scheme Level

Summary of charges

Fees & charges Applicable rates Deducted from

Policy feeUS$6 per month, which is equivalent to an annual charge of US$72

Deducted on the first policy charges due date after policy inception and thereafter on each Monthiversary by redeeming notional units from the Initial Contribution wInitial Contribution Period, and thereafter from the Accumulation Contribution Account until the end of the premium term.

Administrative charge

3.8% divided by 12, of the account value of the Initial Contribution Account per month, which is equivalent to an annual rate of 3.8%

Deducted on the first policy charges due date after policy inception and thereafter on each Monthiversary by redeeming notional units from the Initial Contribution Account during the premium term.

Investment portfolio management charge

1st to 10th policy year

0.1% of the account value per month, which is equivalent to an annual rate of 1.2%

Deducted on the first policy charges due date after policy inception and thereafter on each Monthiversary by redeeming notional units from the Policy Account while the Policy is in force.From 11th policy year onwards

0.8% divided by 12, of the account value per month, which is equivalent to an annual rate of 0.8%

4

Fees & charges Applicable rates Deducted from

Surrender charge (early redemption charge)

Upon policy termination and before the end of the selected premium term, except in the case of death of the insured, surrender charge (early redemption charge) will be charged as a percentage of the account value of the Initial Contribution Account. The charge will depend on the premium term and the policy year as stated below:

As at the beginning of policy

year

Premium term

5 years 10 years 15 years 20 years 25 years

1 100% 100% 100% 100% 100%2 27% 61% 100% 100% 100%3 11% 29% 46% 62% 78%4 8% 24% 37% 48% 57%5 4% 21% 35% 46% 56%6 0% 18% 32% 44% 54%7 15% 30% 42% 52%8 11% 27% 40% 50%9 8% 24% 37% 48%10 4% 21% 35% 46%11 0% 18% 32% 44%12 15% 30% 42%13 11% 27% 40%14 8% 24% 37%15 4% 21% 35%16 0% 18% 32%17 15% 30%18 11% 27%19 8% 24%20 4% 21%21 0% 18%22 15%23 11%24 8%25 4%26 0%

Deducted from the Initial Contribution Account by redeeming notional units.

For termination which occurs before the end of a policy year, the surrender charge (early redemption charge) will be determined by pro-rating the rates as at the beginning and the end of that policy year.

Example of early redemption charge calculation:Premium term 10 years

Surrender dateAt the end of the 3rd month of the 2nd policy year

Earlyredemptioncharge rate calculation

= 61% x (12-3) /12 + 29% x (3 / 12)

= 53%

Account value of theInitial Contribution Account

= US$25,000

Earlyredemptioncharge= US$25,000 x 53%= US$13,250

5

Fees & charges Applicable rates Deducted from

Partialwithdrawalcharge

Currently waived N/A

Switching / reallocationcharge

Currently waived N/A

6

Underlying fund levelFees & charges Applicable rates Deducted from

Bid - offer spread Currently waived N/A

Underlying fund management charge

The underlying fund management charge will vary according to the underlying funds.

For details of the underlying fund management charge, and other fees and expenses relating to the underlying funds, please refer to the investment choices brochure, and the respective prospectuses of the underlying funds, available from FWD.

Reflected in the unit price of the underlying fund.

Please note:

• FWD reserves the right to vary the policy charges or impose new charges with not less than 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

• YourPolicywillremaininforceproviededtheaccountvaluesofboththeInitialContributionAccountandAccumulationContribution Account are sufficient to pay the relevant fees and charges.

General information

7

Allocation of premiumsYou can allocate your premiums to a single or multiple investment choice(s) up to a maximum of 10 investment choices. For each investment choice selected, you should allocate at least 10% of your premium and the sum of the premiums to all selected investment choices must be 100%. Under normal circumstances, the allocation of units will be

Premium termi.Wealth Regular Investment Savings Plan is an investment-linked assurance scheme with premium terms of 5, 10, 15, 20, or 25 years.

Reduction of premiumYou can reduce your Regular Investment Premium anytime after the Initial Contribution Period, provided that such premium meets the minimum amount required. Currently, the minimum annualized Regular Investment Premium is US$2,400 for 5 year premium term and US$1,800 for other premium terms. FWD reserves the right to change the requirements, subject to 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

Suspension of premiumAfter the Initial Contribution Period, you can exercise the premium holiday option by temporarily suspending your premiums, provided that the account value of the Accumulation Contribution Account is sufficient to cover all the relevant fees and charges. During the suspension period, all relevant fees and charges and premiums of riders (if any) will be automatically deducted from the Policy Account to keep your Policy effective. If the account value of the Accumulation Contribution Account at any point in time is not sufficient for FWD to cover all the fees and charges, you will have to resume paying your premiums as and when notified by FWD, failing which your Policy will terminate when your account value of the Accumulation Contribution Account reaches zero.

Currencyi.Wealth Regular Investment Savings Plan is available in US dollars while the investment choice currency is based on the denominated currency of the underlying fund.

Eligible age for policy application i.Wealth Regular Investment Savings Plan is available to individuals for the following age at next birthday at the time of application depending on the premium term:

effected on the next Dealing Date after the receipt of clear funds and the duly completed forms by 4:00p.m. Hong Kong time on a business day. FWD reserves the right to change the requirements and/or the relevant procedure, subject to 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

Investment choice switching/reallocationi.Wealth Regular Investment Savings Plan gives you the flexibility in changing your investment portfolio to meet your investment strategy. Currently, there is no charge on switching/reallocation, nor is there a limit on the frequency of switching investment choices. The minimum switching amount is currently US$125.

To request switching/reallocation of investment choices, you need to complete and sign the “Investment-Linked Policy Services Request Form”, which can be obtained from your wealth planner or FWD’s customer service, or submit your request by other means, such as electronic form, as prescribed by FWD from time to time. Currently, you can request switching/reallocation of investment choices via FWD’s online platform, the customer online service, on the FWD website (www.fwd.com.hk).

The switching-out instruction will normally be executed on the next Dealing Date after the receipt of your duly completed switching request by 4:00p.m. Hong Kong time on a business day. The switching-in instruction will normally be executed on the next Dealing Date after the completion of the switching-out transaction, except for dealing suspension or other circumstances which may be considered exceptional.

FWD reserves the right to change the requirements and/or the relevant procedure, subject to 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

Partial withdrawalYou can make partial withdrawals by redeeming notional units from your Policy Account. To request partial withdrawal, you need to complete and sign the “Investment-Linked Policy Services Request Form”, which can be obtained from your wealth planner or FWD’s customer service. This will normally be executed on the next Dealing Date after the receipt of your duly completed partial withdrawal request by 4:00p.m. Hong Kong time on a business day.

Currently, there are no charges applicable to partial withdrawals. The minimum amount to be withdrawn is currently US$250 and the Minimum Remaining Account Value of the Accumulation Contribution Account is

Premium term Age at next birthday at the time of application

5 or 10 years 1 to 7015 years 1 to 6520 years 1 to 6025 years 1 to 55

8

currently US$2,500. FWD reserves the right to change the requirements and/or the relevant procedure, subject to 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

Policy terminationThe Policy will terminate on the earliest of the followings:1. The policy anniversary of this Policy immediately

preceding the hundredth (100th) birthday of the insured; or

2. The date of policy surrender; or 3. Non-payment of premiums during the Initial Contribution

Period; or4. The death of the insured; or5. If the account value of the Accumulation Contribution

Account (after the Initial Contribution Period) is equal to or less than zero on any Valuation Date.

If your Policy is terminated, all notional units of the investmentchoicesinyourPolicywillberedeemed.Except in the case of the death of the insured, if your Policy is terminated before the end of the premium term, the redeemed value will be subject to a surrender charge. For details of the surrender charge, please refer to the “Summary of charges” section.

Investment choice selectionA wide range of selected investment choices, of which the underlying funds are all managed by professional investment managers, is available for investment. For more information of the investment choices, please refer to the investment choices brochure, the corresponding appendix and the prospectuses of the underlying funds which are made available by FWD.

Rounding of units and unit pricesThe number of notional units of investment choices redeemed or subscribed is currently rounded to the nearest 5 decimal places. The rounding method for determining the unit price is prescribed by the respective underlying fund manager. Please refer to the prospectus of the respective underlying fund for details.

Borrowing poweri.Wealth Regular Investment Savings Plan has no borrowing powers. For details of the borrowing powers and investment restrictions of the underlying funds, please refer to the relevant prospectuses.

Suspension of dealingUnder circumstances which FWD will act in good faith and may consider exceptional, the date and frequency of the Valuation Date and Dealing Date are at the absolute discretion of FWD.

Account value checkingTo check your account value, simply log in to your customer online service account on the FWD’s website (www.fwd.com.hk). You can also click into FWD’s website for the up-to-date unit prices of the investment choices. Your account value is calculated by multiplying the notional units of investment choices in your account by the most up-to-date unit prices. The unit prices of the investment choices will be exactly the same as those of the respective underlying funds. Please note that the returns on investments under the Policy are subject to the charges of your Policy, and may be lower than the returns from the underlying investments.

Application procedureTo apply for i.Wealth Regular Investment Savings Plan, simply return to FWD a completed policy application form and a signed illustration document together with the relevant payment.

Surrender procedureIf you wish to surrender your Policy, simply return a completed surrender form to FWD and all the notional units of the investment choices in your investment account will be redeemed. This will normally be executed on the next Dealing Date after the receipt of the duly completed surrender request by 4:00p.m. Hong Kong time on a business day, and your Policy will be terminated.

The surrender value will normally be payable within 1 month after the receipt of your completed surrender form. No interest is payable for the period between the date the notional units are cancelled from your account and the date of payment of the surrender value. FWD reserves the right to change the relevant procedure, subject to 1 month’s prior written notice or such shorter period of notice in compliance with the relevant regulatory requirements.

Cooling-off periodCooling-off period is a period during which life insurance policyholders may cancel their policies and get back their original investments (subject to market value adjustment) within the earlier of 21 days after the delivery of the Policy or issue of a notice to you or your representative. Such notice should inform you of the availability of the Policy and expiry date of the cooling-off period. Please refer to the cooling off initiative issued by HKFI from time to time for reference.

You have to tell FWD if you decide to cancel your Policy by giving a written notice. Such notice must be signed by you and received directly by FWD at 1/F., Customer Service, FWD Financial Centre, 308 Des Voeux Road Central, Hong Kong.

9

i.Wealth Regular Investment Savings Plan is authorized by the SFC. SFC authorization is not a recommendation or endorsement of i.Wealth Regular Investment Savings Plan, nor does it guarantee the commercial merits of i.Wealth Regular Investment Savings Plan or its performance. It does not mean i.Wealth Regular Investment Savings Plan is suitable for all investors nor is it an endorsement of its suitability for any particular investor or class of investors.

The SFC does not take any responsibility for the contents of the offering document, make no representation as to its accuracy or completeness, expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of the offering document.

The principal brochure is not a policy. For detailed terms, conditions, exclusions and charges, please refer to the policy provisions.

You may get back the amount you paid, or less if the value of the investment choices has gone down.

Exchange rateThe denominating currency of each investment choice may differ from the currency of the Policy. Please refer to the investment choices brochure for details. Changes in foreign currency exchange rates may therefore affect the unit price of the investment choices with investments denominated in other currencies.

Governing lawYour Policy is issued under, and will be construed in accordance with, the laws of the Hong Kong Special Administrative Region.

Taxation Interest, income and capital gains from redemption and disposal of investment choices are exempt from taxation under the current Inland Revenue Ordinance. However, you are advised to seek professional guidance regarding your own particular tax circumstances.

Parties involved

Your return on investments is calculated or determined by FWD with reference to the performance of the underlying funds. Investment involves risks. Past performance should not be taken as an indication of future performance. Each investment choice is subject to marketfluctuations and to risks inherent in all investments. The prices of units of any investment choice and the income accrued from investing in such investment choice may go down as well as up.

FWD accepts full responsibility for the accuracy of the information shown in the principal brochure, including this product brochure and the investment choices brochure at the date of its publication. Please note that FWD has the discretion to waive the requirements and limits in this product brochure from time to time. FWD also confirms, having made all reasonable enquiries, that to the best of FWD’s knowledge and belief there are no other facts the omission of which would make any statement misleading. Neither the delivery of the principal brochure nor the agreement to issue the Policy shall constitute a representation that the information contained in this principal brochure is correct as of anytime subsequent to such date.

This product brochure is issued by FWD Life Insurance Company (Bermuda) LimitedAug 2013

For any enquiries and complaints in relation to this product or FWD’s services, please contact FWD by telephone (852) 3123 3123, fax (852) 2290 7091 or email at [email protected]

Insurer FWD Life Insurance Company (Bermuda) Limited 28/F., FWD Financial Centre, 308 Des Voeux Road Central,Hong Kong.

Investment managers

The investment managers vary according to the underlying funds. Please refer to the investment choices brochure for details.

The following terms have the meanings set out below:

Glossary

Terms Meanings

AccidentAn unforeseen and unexpected event or contiguous series of events of violent, accidental, external and visible nature which shall be the sole cause of a bodily injury while the Policy is in force.

Accumulation Contribution Account

An account set up for the policyholder and used to maintain the notional units allocated in respect of all premiums contributed after the Initial Contribution Period.

Dealing Date

It is the date on which FWD or its delegate buys or sells the units of the respective investment choice on behalf of the policyholder. Dealings of an investment choice are only available on a Valuation Date. The cut-off time in respect of each Dealing Date is 4:00p.m. Hong Kong time. Under circumstances which FWD may consider exceptional, the date and frequency of the Dealing Date are at the absolute discretion of FWD.

Initial Contribution Account

An account set up for the policyholder and used to maintain the notional units allocated in respect of all premiums contributed during the Initial Contribution Period.

Initial Contribution Period

The period during which the premiums payable is used for the allocation of notional units to the Initial Contribution Account. The Initial Contribution Period varies by the premium term.

Minimum Remaining Account Value

An amount set to limit the partial withdrawal from the Accumulation Contribution Account.

Monthiversary

The same date each month as the commencement date (the date of premium commencing and the date used for determining the issue age of the insured). If the Monthiversary is not a business day, it will be postponed to the next business day. If the Monthiversary does not exist in a particular month, it will be the last day of the month.

Policy AccountAn account set up for the policyholder and used to maintain the total notional units of the Initial Contribution Account and the Accumulation Contribution Account.

Regular Investment Premium

The premiums regularly made into the Policy Account for the allocation of notional units and are payable until the end of the premium term or the death of the insured, whichever is earlier.

Valuation Date

The Valuation Date of an investment choice is the day on which the unit price is determined. The frequency of the Valuation Date shall be on each business day under normal circumstances. Where a particular day is not a business day, the Valuation Date is postponed to the next business day. Under circumstances which FWD may consider exceptional, the date and frequency of the Valuation Date are at the absolute discretion of FWD. Please refer to the investment choices brochure for details of the specified valuation day for the investment choices.

10

下列詞彙具有以下涵義:

詞彙表

詞彙 詞彙涵義

意外在保單生效期間所發生的一宗或連串猛烈、外在及可見、且不可預見及預料的意外事

故,導致身體受傷。

累積供款戶口一個為保單持有人而設的戶口,用於保存保單持有人於最初供款期後所有以供款分配

之名義單位。

交易日

交易日為富衛或其他指定人員�機構,代表保單持有人,購入或賣出其有關投資選擇

的單位的當日。每一項投資選擇只可在該投資選擇的每個估值日作出交易。交易日之

截止時間為下午四時(香港時間)。在某些特殊情況下,富衛擁有絕對酌情權決定投

資選擇交易的日子及次數。

最初供款戶口一個為保單持有人而設的戶口,用於保存保單持有人於最初供款期內所有以供款分配

之名義單位。

最初供款期於最初供款期內的供款會用作分配名義單位至最初供款戶口內。最初供款期則因應不

同的供款年期而異。

最低剩餘戶口價值 此價值為於累積供款戶口作部分提款之限額。

週月日

每月與保單生效日(即開始繳付保費之日,此日亦用作釐定被保人的投保年齡。)

相同的日子。若週月日並非工作日,則順延至下一個工作日。倘週月日不存在於某一

個月份,該週月日則為該月份的最後一日。

保單戶口一個為保單持有人而設的戶口,用於保存保單持有人於最初供款戶口及累積供款戶口

內之所有名義單位。

定期投資保費定期存入保單戶口用作分配名義單位之供款。定期投資保費需繳付至供款期滿或被保

人身故,以較先者作準。

估值日

投資選擇的估值日是指計算該投資選擇的單位價格的日子。估值日在一般情況下為每

個工作日。若該日並非工作日,該估值日將順延至下一個工作日。在某些特殊情況

下,富衛擁有絕對酌情權決定投資選擇的估值日的日子及次數。如欲查詢個別投資選

擇之估值日詳情,請參閱投資選擇刊物。

10

9

冷靜期在冷靜期內,保單持有人可取消已購買的保單,取回原

來的投資金額(須按市值調整);冷靜期為保單發出後

21天內,或向閣下或閣下的代表發出通知書後的21天

內,以較先者為準。通知書應說明保單已備妥,並列明

冷靜期的屆滿日期。請參閱香港保險業聯會就冷靜期權

益發出的最新指引。

閣下須以書面知會保險公司有關取消保單的決定。該通

知必須由閣下簽署及直接送達富衛的客戶服務部,香港

中環德輔道中308號富衛金融中心1樓。

閣下可取回已付金額,但若閣下所選的投資選擇的價值

下跌,可取回的金額將會減少。

兌換率每項投資選擇的計算貨幣可能與保單貨幣有異,有關詳

情請參閱投資選擇刊物。貨幣匯率的變動可能會對使用

以其他貨幣計值的投資選擇的單位價格構成影響。

管制法例本保單及其詮釋以香港特別行政區之法律為管制法例。

稅項根據現時之香港稅務條例,由投資選擇買賣所獲得之利

息、收益及盈利均可獲豁免利得稅,但您應就有關個人

稅務情況諮詢專業意見。

參與機構

閣下之投資回報.是由富衛參照相關基金的表現而計算

或釐定。投資涉及風險。往績不應視作未來業績表現的指

標。每項投資選擇是受市場價格波幅及其固有的風險所影

響。任何投資選擇的單位價格或其盈利均可升可跌。

本產品介紹乃由

富衛人壽保險(百慕達)有限公司

刊發。

2013年8月

若您對本產品及富衛的服務有任何查詢及投訴,

請致電 3123 3123、傳真至 2290 7091

或電郵至 [email protected] 通知富衛

保險公司

富衛人壽保險(百慕達)有限公司

香港中環德輔道中308號富衛金融中心28樓

投資經理

投 資 經 理 因 應 不 同 投 資 選 擇 而 異 , 詳 細 資 料 可 參 閱 投

資選擇刊物。

富衛對主要銷售刊物包括本產品介紹及投資選擇刊物

於刊發日期所載資料的準確性承擔一切責任。請注意,

富 衛 擁 有 酌 情 權 可 隨 時 豁 免 此 產 品 介 紹 內 的 規 定

及限制。富衛經作出一切合理查詢後,確認就富衛所

知及所信,並無遺漏任何事實致使所載的內容產生誤

導。惟送呈本主要銷售刊物或同意簽發保單,並不構

成本主要銷售刊物所載資料於上述日期後任何時間仍

屬正確陳述。

愛豐裕定期投資相連計劃已獲證券及期貨事務監察委員

會(「證監會」)認可,惟獲得認可並不意味獲得官方推

介或認許,亦不是對愛豐裕定期投資相連計劃的商業價

值或表現作出保證,更不代表愛豐裕定期投資相連計劃

適合所有投資者、或認許愛豐裕定期投資相連計劃適合

任何個別投資者或任何類別的投資者。

證監會對銷售文件的內容概不負責,對其準確性或完整

性亦不作出任何申述,並且明確表示,因銷售文件全部

或部分內容而產生或因依賴這些內容而引致的損失,證

監會概不承擔任何法律責任。

主要銷售刊物並非保單。有關詳細條款、細則、不保事

項和收費,請參閱保單條款。

8

部分提款您可從保單戶口中贖回名義單位作部分提款以應付個

人所需。您只需填妥並簽署「投資相連保單服務申請

表」,即可申請部分提款。申請表可從客戶服務部或

您的財富策劃顧問取得。於每一個工作日下午四時前

收妥的部分提款申請一般會在下一個交易日執行。

現時,部分提款並不收取費用。而現行最低提款金額及

最低剩餘戶口價值分別為250美元及2,500美元。富衛

保留權利,藉事先給予不少於一個月的書面通知或符

合相關監管規定的較短通知期而更改上述規定及�或

相關程序。

終止保單保單將在下列其中一個日期終止,以較早者為準:

1. 被保人一百歲生日前之保單週年日;或

2. 保單的退保日;或

3. 於最初供款期內未有繳付供款;或

4. 被保人身故;或

5. 於最初供款期後,當累積供款戶口內之戶口價值於

任何一個估值日等於或低於零。

當您終止保單時,保單內的所有名義單位將會隨保單終

止而被贖回。若於供款年期內終止保單,除因被保人身

故外,富衛將從被贖回金額中扣除提早贖回費用。有關

退保費用的詳情,請參閱「收費總覽」部分。

投資選擇此 保 單 提 供 一 系 列 投 資 選 擇 , 並 由 專 業 的 投 資 經 理

管理。有關投資選擇的詳細資料,可參閱由富衛提供

的 投 資 選 擇 刊 物 、 相 關 附 錄 及 個 別 相 關 基 金 的 發 行

章程。

單位數目及單位價格之調整每項投資選擇之贖回及認購之名義單位數目將被調整

至最接近的5個小數位。而單位價格的小數位之調整方

法由相關基金投資經理決定並會因應不同相關基金而

異。詳情請參閱個別相關基金的發行章程。

借貸權力愛豐裕定期投資相連計劃並無借貸權力。有關各相關

基金借貸權力及投資限制的詳情,請參閱個別相關基

金的發行章程。

暫停交易在某些特殊情況下,富衛擁有絕對酌情權決定投資選

擇的估值日及交易日的日子及次數。

查閱戶口價值您只需於富衛的網址(www . fwd . c om . h k)登入客

戶 網 上 服 務 戶 口 便 可 得 知 您 的 戶 口 價 值 ; 您 亦 可

於富衛的網址查詢投資選擇的最新單位價格。您的

戶口價值相等於保單戶口內的名義單位數目乘以最新

單位價格。投資選擇之單位價格相等於各相關基金之

單位價格。請注意,此保單設有相關費用及收費。閣

下的投資回報有可能低於相關投資的回報。

投保申請程序申請愛豐裕定期投資相連計劃的手續簡易,只須填妥

投保申請書及簽署保單利益說明,連同有關款項交回

富衛即可。

退保安排如申請退保,您只須填妥退保申請表格並交回富衛。

於每一個工作日下午四時(香港時間)前收妥的退保

申請一般會在下一個交易日執行。您的保單戶口內的

名義單位將會被贖回,而保單亦會終止。

在一般情況下,富衛將由接獲您的退保申請起計1個

月內支付退保價值。由註銷戶口內名義單位起直至發

放退保價值,期間之利息概不計算。富衛保留權利,

藉事先給予不少於一個月的書面通知或符合相關監管

規定的較短通知期而更改相關程序。

一般資料

7

供款年期 於投保時的下次生日年齡

5 或 10 年 1 至 70 歲

15 年 1 至 65 歲

20 年 1 至 60 歲

25 年 1 至 55 歲

供款年期

愛豐裕定期投資相連計劃是一項與投資有關的人壽保險

計劃,提供5年、10年、15年、20年及25年之供款

年期以供選擇。

調減供款

您可於最初供款期後調低定期投資保費,惟須符合最低

供款要求。現時,供款年期為5年及超過5年之保單,

其最低每年定期投資保費分別為2,400美元及1,800美元。

富衛保留權利,藉事先給予不少於一個月的書面通知或

符合相關監管規定的較短通知期而更改上述規定。

暫停供款

若於最初供款期後,累積供款戶口內之戶口價值足以

支付所有相關費用及收費,您可因應個人需要,行使

供款假期而暫停繳付供款。於暫停供款期間,富衛將

從保單戶口自動扣除保單之所有相關費用及收費及附

約保費(如有)以令您的保單繼續生效。然而,若累積

供款戶口內之戶口價值不足以支付所有費用及收費附約

保費(如有),您必須於收到富衛通知時恢復供款。否則,您

的保單將於累積供款戶口內之戶口價值等於零時終止。

貨幣

愛豐裕定期投資相連計劃之貨幣為美元,而投資選擇

貨幣則以該相關基金之報價貨幣為準。

保單申請年齡

愛豐裕定期投資相連計劃按照不同的供款年期,可供

以下於投保時下次生日年齡之人士投保。

供款分配

您可將您的供款分配至一項或最多十項投資選擇,您必須

分配至少10%的供款至各投資選擇,而所有投資選擇所

分配比例必須為100%。在一般情況下,名義單位之分

配將於每一個工作日的下午四時(香港時間)前收到已

清算之資金及已填妥的申請表後的下一個交易日進行。

富衛保留權利,藉事先給予不少於一個月的書面通知或

符合相關監管規定的較短通知期而更改上述規定及�或

相關程序。

投資選擇轉換�重新調配

愛豐裕定期投資相連計劃讓您可因應個人的投資目標,

轉換投資選擇或更改投資組合。現時,投資選擇轉換及

重新調配均不收取任何費用,而轉換�重新調配次數亦

無限制。現行最低轉換金額為125美元。

您只需填妥並簽署「投資相連保單服務申請表」,或按

由富衛不時指定的其他方式如電子表格,即可作投資

選擇轉換�重新調配的申請。「投資相連保單服務申請

表」可於客戶服務部或您的財富策劃顧問取得。現時,

您亦可以透過網上平台,在富衛網站(www.fwd.com.hk)

的客戶網上服務,申請投資選擇轉換�重新調配。

於每一個工作日下午四時(香港時間)前收妥的投資選擇

轉換申請一般會在下一個交易日執行轉出指示。若非

交易暫停或某些特殊情況,轉入指示一般會在轉出指示

完成後的下一個交易日內執行。

富衛保留權利,藉事先給予不少於一個月的書面通知或

符合相關監管規定的較短通知期而更改上述規定及�或

相關程序。

6

費用及收費 收費率 從以下金額扣減

部分提款費用 現時豁免 不適用

轉換�重新調配

投資選擇費用現時豁免 不適用

請注意:

• 富衛保留權利,藉事先給予不少於一個月的書面通知或符合相關監管規定的較短通知期而更改保單收費或施加 新收費。

• 如最初供款戶口及累積供款戶口內之戶口價值足夠繳付有關費用及收費,閣下之保單會繼續生效。

相關基金方面

費用及收費 收費率 從以下金額扣減

買賣差價 現時豁免 不適用

相關基金管理費用

相關基金管理費用因應不同相關基金選擇而異。

如欲查閱相關基金管理費用、其他收費及支出詳情,請參閱由富

衛提供的投資選擇刊物、相關附錄及個別相關基金之發行章程。

已於相關基金的

單位價格內反映

費用及收費 收費率 從以下金額扣減

提早退保費用

(提早贖回費用)

除因被保人身故外,若於所選定之供款年期內終止保單,提早退保

費用(提早贖回費用)將根據最初供款戶口之戶口價值的某個百分比收

取,此費用的百分比按供款年期及保單年度而釐定:

於保單年度

開始時

供款年期

5年 10年 15年 20年 25年

1 100% 100% 100% 100% 100%2 27% 61% 100% 100% 100%3 11% 29% 46% 62% 78%4 8% 24% 37% 48% 57%5 4% 21% 35% 46% 56%6 0% 18% 32% 44% 54%7 15% 30% 42% 52%8 11% 27% 40% 50%9 8% 24% 37% 48%10 4% 21% 35% 46%11 0% 18% 32% 44%12 15% 30% 42%13 11% 27% 40%14 8% 24% 37%15 4% 21% 35%16 0% 18% 32%17 15% 30%18 11% 27%19 8% 24%20 4% 21%21 0% 18%22 15%23 11%24 8%25 4%26 0%

從最初供款戶口中

透過贖回名義單位扣除。

若保單於一個保單年度完結前終止,提早退保費用(提早贖回費

用)將根據該保單年度開始及完結時之百分比按比例計算。

提早贖回費用計算例子:

供款年期 10年

退保日於第二個保單年度的第三個 月份完結

提早贖回費用百分比計算= 61% X (12-3) /12 +

29% X (3 / 12) = 53%

最初供款戶口之戶口價值 = 25,000 美元

提早贖回費用= 25,000 美元 X 53% = 13,250 美元

5

保險計劃方面

收費總覽

費用及收費 收費率 從以下金額扣減

保單費用 每月6美元,相等於每年72美元

在最初供款期內,於保單

繕發後的首個保單收費到

期日及其後於每個週月日

從最初供款戶口中透過贖

回名義單位扣除,隨後則

從累積供款戶口中扣除直

至供款年期完結。

行政費用 每月最初供款戶口之戶口價值的3.8%除以12,

相等於每年3.8%

在供款年期內,於保單繕

發後的首個保單收費到期

日及其後於每個週月日從

最初供款戶口中透過贖回

名義單位扣除。

投資組合

管理費用

第1至第10個保單年度每月戶口價值的0.1%,相等於

每年1.2% 在保單生效期間,於保單

繕發後的首個保單收費到

期日及其後於每個週月日

從保單戶口中透過贖回名

義單位扣除。由第11個保單年度起

每月戶口價值的0.8%除以12,

相等於每年0.8%

4

3

保單戶口 靈活管理

您可靈活地管理您的投資組合,於最初供款期後調減定

期投資保費,惟須符合最低供款要求。您亦可於最初供

款期後暫停繳付定期投資保費,惟累積供款戶口內之戶

口價值必須足以支付所有相關費用及收費。

此外,當需要調動資金時,您可於最初供款期後從累

積供款戶口中贖回名義單位作部分提款,您亦可於

供款年期後從最初供款戶口提款,以應不時之需。現

時,部分提款並不收取任何費用。現行最低提款金額及

最低剩餘戶口價值分別為250美元及2,500美元。富衛

保留權利,藉事先給予不少於一個月的書面通知或符合

相關監管規定的較短通知期而更改上述規定。

請注意:

• 當暫停繳付定期投資保費時,若戶口價值不足以支

付所有相關的費用及收費,閣下必須於收到富衛通

知時恢復供款。否則,閣下之保單將於戶口價值等

於零時終止。

度身定造的網上服務平台

愛豐裕定期投資相連計劃為您提供無限次免費投資選擇

轉換及重新調配的彈性。無論何時何地,您均可以不費

分毫,調整您的投資組合,以捕捉稍瞬即逝的投資機

會。富衛深明對市場作出迅速反應的重要性,您現可透

過富衛的網上平台客戶網上服務,申請轉換�重新調配

投資選擇,隨時隨地重新調整投資策略。

現時,投資選擇轉換及重新調配均不收取任何費用,而

轉換�重新調配次數亦無限制。最低投資選擇轉換金額

為125美元。富衛保留權利,藉事先給予不少於一個月

的書面通知或符合相關監管規定的較短通知期而更改上

述規定。

長期獎賞回饋忠誠客戶

於供款年期完結時,富衛會派發相等於供款年期內繳付

之所有保單費用至您的保單作長期獎賞。

長期獎賞將根據當時您的投資選擇分佈指示用作分配額

外的名義單位至累積供款戶口,惟保單必須生效。獎賞

並非保證,富衛保留派發獎賞之權利,並會藉事先給予

不少於一個月的書面通知或符合相關監管規定的較短通

知期而作出更改。

終身保障高至100歲

於保單生效期間,人壽保障額相等於您的保單之戶口價

值的101%。若被保人不幸於第5個保單週年日前因意外

身故,除上述人壽保障外,更可獲額外發放相等於10%

之戶口價值作為意外身故權益,以12,500美元為上限。

請注意:

• 由 於 身 故 權 益 與 閣 下 所 選 相 關 基 金 不 時 的 表 現 掛

鈎 , 因 此 身 故 權 益 會 受 投 資 風 險 及 市 場 波 動 所 影

響。最終獲得的身故權益或會遠低於閣下已繳付的

供款,並可能不足以應付閣下的個別需要。

2

特別獎賞=獎賞百分比 x 每年定期投資保費

特別獎賞助您增強儲蓄潛力

於首個保單年度完結時,富衛會派發特別獎賞至閣下的

保單內。獎賞金額按供款年期及每年定期投資保費的金

額而定,有關計算根據下列方程式及獎賞百分比。

特別獎賞將根據當時您的投資選擇分佈指示用作分配額

外的名義單位至最初供款戶口內,惟保單必須生效。

請注意:

• 若被保人於首兩個保單年度內身故,一切已派發的

特別獎賞將從身故權益中扣除。

• 特別獎賞屬於最初供款戶口之戶口價值的一部分,

故 此 , 該 獎 賞 亦 須 根 據 「 收 費 總 覽 」 部 分 而 收 取

有關費用,提早退保或會導致損失全部或部分特別

獎賞。

• 以上的獎賞金額的百分比是根據每年定期投資保費

而釐定,並不代表閣下之投資回報或表現。

自選投資選擇

此保單提供一系列由專業投資經理所管理的投資選擇供

您挑選。您更可分配您的供款至一項或多項投資選擇,

而每個投資選擇的分配比例最少為10%。富衛保留權

利,藉事先給予不少於一個月的書面通知或符合相關監

管規定的較短通知期而更改上述規定。

請注意:

• 愛豐裕定期投資相連計劃所提供的各個投資選擇的

特點及風險狀況或會有很大差異,部分選擇可能涉

及高風險。

• 分配至閣下保單的單位為名義性質並純粹用作釐定

閣下保單之戶口價值。有關投資選擇之詳情,請參

閱由富衛提供的投資選擇刊物、相關附錄及個別相

關基金的發行章程。

每年定期 投資保費

按供款年期的獎賞百分比 (每年定期投資保費的百分比)

5年 10年 15年 20年 25年

1,800美元-少於 3,000美元

1.2% 2.5% 4.5% 10.0% 12.0%

3,000美元-少於 6,000美元

2.0% 4.0% 8.5% 14.5% 18.0%

6,000美元-少於 12,000美元

4.0% 8.0% 15.5% 25.5% 32.0%

12,000美元- 少於 20,000美元

5.0% 10.0% 21.5% 35.0% 44.0%

20,000美元 或以上

6.0% 12.0% 24.0% 40.0% 50.0%

一份保單便能助您實現人生目標。

定期投資相連計劃

1

隨著人生每個階段的不同需要,您亦會有著不同的目標:到外地旅遊、置業、結婚、安排子女

入讀大學,甚至希望提早退休等。愛豐裕定期投資相連計劃是一項與投資有關的人壽保險計

劃,是為希望達成人生不同目標的人士而設,讓您輕鬆走過人生的不同階段。

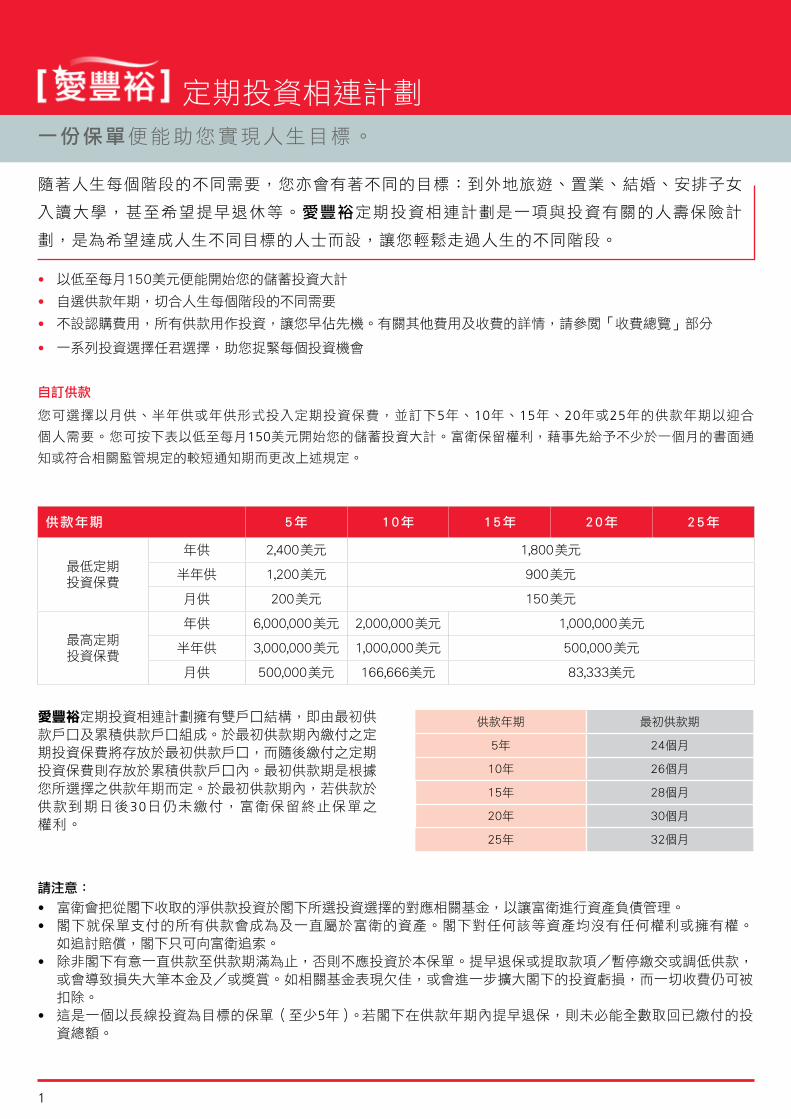

供款年期 最初供款期

5年 24個月

10年 26個月

15年 28個月

20年 30個月

25年 32個月

• 以低至每月150美元便能開始您的儲蓄投資大計

• 自選供款年期,切合人生每個階段的不同需要

• 不設認購費用,所有供款用作投資,讓您早佔先機。有關其他費用及收費的詳情,請參閱「收費總覽」部分

• 一系列投資選擇任君選擇,助您捉緊每個投資機會

自訂供款

您可選擇以月供、半年供或年供形式投入定期投資保費,並訂下5年、10年、15年、20年或25年的供款年期以迎合

個人需要。您可按下表以低至每月150美元開始您的儲蓄投資大計。富衛保留權利,藉事先給予不少於一個月的書面通

知或符合相關監管規定的較短通知期而更改上述規定。

供款年期 5年 10年 15年 20年 25年

最低定期 投資保費

年供 2,400美元 1,800美元

半年供 1,200美元 900美元

月供 200美元 150美元

最高定期 投資保費

年供 6,000,000美元 2,000,000美元 1,000,000美元

半年供 3,000,000美元 1,000,000美元 500,000美元

月供 500,000美元 166,666美元 83,333美元

愛豐裕定期投資相連計劃擁有雙戶口結構,即由最初供款戶口及累積供款戶口組成。於最初供款期內繳付之定期投資保費將存放於最初供款戶口,而隨後繳付之定期投資保費則存放於累積供款戶口內。最初供款期是根據您所選擇之供款年期而定。於最初供款期內,若供款於供款到期日後30日仍未繳付,富衛保留終止保單之權利。

請注意:

• 富衛會把從閣下收取的淨供款投資於閣下所選投資選擇的對應相關基金,以讓富衛進行資產負債管理。• 閣下就保單支付的所有供款會成為及一直屬於富衛的資產。閣下對任何該等資產均沒有任何權利或擁有權。

如追討賠償,閣下只可向富衛追索。• 除非閣下有意一直供款至供款期滿為止,否則不應投資於本保單。提早退保或提取款項�暫停繳交或調低供款,

或會導致損失大筆本金及�或獎賞。如相關基金表現欠佳,或會進一步擴大閣下的投資虧損,而一切收費仍可被 扣除。

• 這是一個以長線投資為目標的保單(至少5年)。若閣下在供款年期內提早退保,則未必能全數取回已繳付的投資總額。

愛豐裕定期投資相連計劃(「保單」)的主要銷售刊物包括本產品介紹及投資選擇刊物。本產品介紹與投資選擇刊物及產品資料

概要同時發出,並應一併細閱。它們為銷售文件的一部分,並可從富衛人壽保險(百慕達)有限公司(下稱「富衛」)之網頁時

www.fwd.com.hk下載。有關詞彙的解釋,投資者應參閱載於產品介紹第10頁的「一般資料 - 詞彙表」。

愛豐裕定期投資相連計劃是一項與投資有關的人壽保險計劃,按照保險公司條例中附表一第二部之定義,屬於類別C

相連長期業務性質,並由富衛(根據《保險公司條例》在香港獲授權的保險公司)提供。閣下之投資因此需承受富衛之信

貸風險。

#本計劃是一項與投資有關的人壽保險計劃,而並不是銀行存款或儲蓄戶口。本計劃並非保證/保本產品,且不是獲「存款保障計劃」所保障的存款。

公 司 背 景富衛香港及澳門為盈科拓展集團成員。憑藉集團的雄厚實力,富衛香港及澳門兩地業務目前管理超過50億美元資產#,

並擁有遠較監管要求為高的償債能力比率。

我們在港澳經營多元化業務,當中包括:

人壽保險 自1984年成立至今,富衛人壽保險致力為客戶提供全面及優質的保險產品及服務;所提供的保險

產品包羅萬有,包括個人壽險、醫療保險及僱員退休福利計劃,能充份照顧客戶於人生各階段之不

同需要。現為香港十大保險公司之一*。

澳門辦事處成立於2000年,竭誠為當地居民提供種類豐富、質素卓越的保險產品及服務,當中包

括人壽保險、住院保障、傷殘保障及危疾保障等。

一般保險 成立於1989年,富衛保險致力為本港之企業及個人客戶提供多元化的一般保險產品和優質服務。

退休金信託 富衛退休金信託致力以其專才為機構及個人客戶提供優質的退休金計劃信託服務。

財務策劃 成立於2002年,富衛財務策劃致力確立作為獨立理財意見的市場領導者的標準,以及吸納行業中

最優秀的財務專才,為客戶提供具質素的財務策劃意見。其「以客為本」的服務理念,確保客戶從

多家機構所提供之一系列理財產品中,獲得最佳的理財方案。

# 截至2012年12月31日* 資料來源: 保險業監理處2012年長期保險業務第四季度臨時統計數字

定期投資相連計劃

保險

i.Wealth 愛豐裕 (PMH010AB1308)

WWW.FWD.COM.HK 3123 3123