product market competition and corporate social...

TRANSCRIPT

1

PRODUCT MARKET COMPETITION

AND CORPORATE SOCIAL RESPONSIBILITY

Marion Dupire Declerck1

Bouchra M'Zali2

This draft: September 14, 2012

Abstract

We investigate the link between industry competitiveness and corporate social

performance. Fernandez and Santalo (2010) show that firms in more competitive environments

have better social ratings, consistent with the strategic purpose of social initiatives. We show

that competition alone is not a sufficient mechanism to improve all dimensions of corporate

social responsibility. Using the Hoberg and Phillips' fitted HHI as a proxy for competition, our

results suggest that competitive pressure, on average, leads to an increase in social strengths but

not necessarily to a decrease in social concerns (1). We do find a positive association between

overall social performance and product market competition but this relationship does not hold

with all dimensions of social responsibility. More specifically, the positive impact of competition

is significant for both shareholder- and employee-related social actions (corporate governance,

diversity, employee relations, human rights) but is not verified for actions affecting other

stakeholders (community, environment) (2). In more competitive environments, product quality

and safety concerns are decreased, but product strengths are not significantly increased (3).

Interestingly, concerns with alcohol, gambling and tobacco do not appear to be affected by

competition whereas involvement in firearms, military and nuclear power is reduced under

competitive pressure (4).

1 Université Lille Nord de France, [email protected] 2 Université du Québec à Montréal (UQAM), [email protected]

2

1. Introduction

Corporate social responsibility (CSR) is one of the most important corporate trends of

the last decade. Microsoft, Chevron, Pepsico, Nike and many other companies are now publishing

sustainability, environmental or citizenship reports, beside their usual annual report. In parallel,

America's economy is recognized as being "the world's most competitive market society" (Sachs,

2011). A positive relationship between market competition and firms' social performance has

been raised in recent empirical research (Fernandez and Santalo, 2010). This suggests a

strategic rather than altruistic purpose of corporate social initiatives. In this paper, we provide a

further investigation of the link between competition and social actions based on alternative

measurement of product market competition and detailed measures of the different dimensions

of corporate social responsibility.

Existing literature has emphasized the strategic nature of corporate social responsibility.

What is referred to as corporate social responsibility actually includes many different

dimensions that should be studied as different constructs. Prior research has shown that a lack

of social strengths is not systematically associated to more social concerns and vice versa

(Mattingly and Berman, 2006), it has even been shown that negative social action is positively

related to positive social action: firms invest in social initiatives in order to offset their negative

social impact (Kotchen and Moon, 2011). In this perspective, studying the different dimensions

of CSR independently does make sense.

While confirming the positive association of CSR to product market competition, our

study provides additional insights on how the different dimensions of social responsibility are

affected by competition and which of these dimensions are more or less likely to be used as part

of a competitive strategy. Our results can be summarized in four axes. -1- A more intense

competitive pressure leads to more social strengths but not necessarily less social concerns; -2-

the positive association of social performance to competition does not hold for all dimensions of

social responsibility: it is verified for shareholder- and employee-related social initiatives,

namely corporate governance, diversity, employee relations and human of rights, but not

significantly for actions affecting other stakeholders like customers, suppliers and community

(generous giving, environment, product quality strengths); -3- product quality and safety

concerns decrease under the competitive pressure but product strengths are not significantly

increased; -4- concerns with alcohol, gambling and tobacco are not significantly related to

competitive intensity, whereas involvement in firearms, military and nuclear power is

significantly lower in more competitive environments. Overall, these results indicate that

competition alone is not a sufficient mechanism to maintain or improve every dimension of

social welfare.

To the best of our knowledge, this is the first study that offers an in depth investigation

of the effect of competition on the different dimensions of CSR. Another contribution lies into the

measurement of product market competition, based on a recently developed measure of market

concentration that accounts for all public and private firms, on a yearly basis and on all

industries beside the manufacturing ones.

This study may be of particular interest for investors and regulators who are concerned

by the implicit "social contract" between business and society. Investing in socially responsible

organizations requires to understand the underlying dynamics that prompt firms to engage in

3

social actions. Understanding which responsible actions are initiated under external constraints

such as competitive pressure is a first step to the design of appropriate incentives that would

lead to improved social welfare.

The paper is organized as followed. The first section reviews the existing literature

related to the definition of CSR, its purpose and its link to product market competition. The

second section provides details about data and methodology. The third section describes the

sample. The fourth section presents the results and the last part concludes.

2. Literature Review

Prior literature has defined corporate social responsibility as a set of policies, programs

and other observable initiatives toward a firm's societal relationships (communities,

environment, employees) that go beyond what is required by law (McWilliams and Siegel, 2001;

McWilliams et al., 2006; Siegel and Vitaliano, 2007). It is sometimes referred to as a component

of an implicit "social contract" between business and society with mutual gains for both sides

(Baron, 2001; Davis, 2005).

Corporate social responsibility can be motivated by different purposes. It can either be

used in a moral perspective, in response to a threat from government and activists, by managers

as a way to improve their private reputation or as a competitive strategy. Under the first motive,

firms altruistically sacrifice profits for social interest (Elhauge, 2005). The second motive has

been put forward by Baron (2001), Heal (2005) and Kotchen & Moon (2011). Social actions may

be initiated in anticipation of social pressure, in order to avoid external conflicts. Thirdly, the

decision to engage in social actions may be taken by managers who want to extract private

reputational benefits. In that case, these decisions may represent agency costs for shareholders

(Barnea and Rubin, 2010). Under the strategic view of CSR, firms "do well by doing good" and

engage in profit-maximizing social actions. This latter view has been the most emphasized in the

recent literature (Baron, 2001; McWilliams and Siegel, 2001; Bagnoli and Watts, 2003; Fisman et

al., 2005; McWilliams et al., 2006; Siegel & Vitaliano, 2007). In this perspective, a significant

effort has been devoted to the study of whether financial performance is indeed positively

associated to social performance. The corresponding literature found mixed results but a

majority of studies confirms the superior financial performance of socially responsible

corporations (see Margolis and Walsh, 2003 for a complete literature review on this

relationship).

Under the strategic-CSR view, firms in more competitive environment have more

incentives to invest in social actions. The theoretical literature has argued that product market

competition and social performance are closely linked with each other: the ethical behavior of

firms enable them to achieve a competitive advantage (Jones 1995), companies compete for

socially responsible customers (Baron 2001). Russo and Fouts (1997) show empirically that

social performance can constitute a source of competitive advantage especially in high growth

industries, Fernandez and Santalo (2010) show that firms in more competitive environments

have better social ratings and present evidence that CSR is at least in part a profit motivated

decision. In contrast, Delios (2010) argues that the nature of industry and institutional

environments harm the competitiveness of organizations that "dare to care", Hillman and Keim

(2001) find evidence that while caring about primary stakeholders such as employees,

4

customers, suppliers and communities can lead to increased shareholder value, social issue

participation reduces shareholder value.

In this paper, we further analyze the relationship between product market competition

and corporate social responsibility by using alternative measures of both industry

competitiveness and social performance.

3. Data and method

3.1. Measuring product market competition

Measuring competitive intensity on the product markets present empirical issues arising

notably from the difficulty to gather information on all firms, including the non listed ones.

Concentration is generally characterized by the Herfindahl-Hirschman Index (HHI),

constructed by adding the squared market shares of all firms operating in an industry for a given

year. The US Census Bureau provides, every five years, the index for all manufacturing

industries, including data on all public and private companies. The Census' HHI is the most

precise existing measure of industry concentration but is limited because of its magnitude (only

manufacturing industries) and frequency (every five years). Compustat data on annual sales

allow to compute an alternative HHI, but the resulting index only includes data on listed

companies. In the financial literature, Ali et al. 2009 showed that given this limitation, the

Compustat-based HHI is a poor proxy for actual industry concentration, with a correlation of

only 13 percent with the corresponding US Census measures. Another issue arises from whether

total sales of diversified firms are included in the measure of industry concentration. If they are

included, the concentration is biased downward, but if they are not, the concentration is biased

upward.

Hoberg and Phillips combined Compustat with Herfindahl data from the Census Bureau

(US Department of Commerce) and employee data from the Bureau of Labor statistics (BLS), and

computed a measure of industry concentration that accounts for all public and private firms on

all industries. The resulting fitted-HHI is made available on the authors' website. This indicator

of industry concentration offers significant improvements to existing Census- and Compustat-

based HHI. First it covers all industries, second it over performs Compustat-based concentration

measure. Hoberg and Phillips (2010b) indeed show that the correlation with Census' HHI is

54.2% for the fitted-HHI. The fitted-HHI is computed with a two-step procedure. In a first step,

the authors regress, on a manufacturing subsample, the Census' HHI on: the Compustat's HHI

computed with firm segment tapes, the average number of employees for public firms according

to the BLS, the average number of employees per firm according to Compustat, and interaction

variables of each of these size variables with the Compustat's HHI. In a second step, they use the

coefficient estimates from step 1 and compute a fitted-HHI for all industries.

3.2. Measuring social performance

Prior literature has raised specific issues related to the measurement of social

performance. It turns out that the most widely used database for social ratings is provided by

MSCI, formerly KLD Research and Analytics, Inc.. Companies are assessed based on several

dimensions distributed under 12 headings, namely community, corporate governance, diversity,

employee relations, environment, human rights, product, alcohol, firearms, gambling, military,

5

nuclear power, tobacco. Under each heading, strengths and/or concerns are identified and

counted. Each heading contains unequal number of strengths and concerns, and some headings

only include concerns (alcohol, firearms, gambling, military, nuclear power, tobacco). The latter

categories, that only include concerns, are called Controversial Business Issues (CBI).

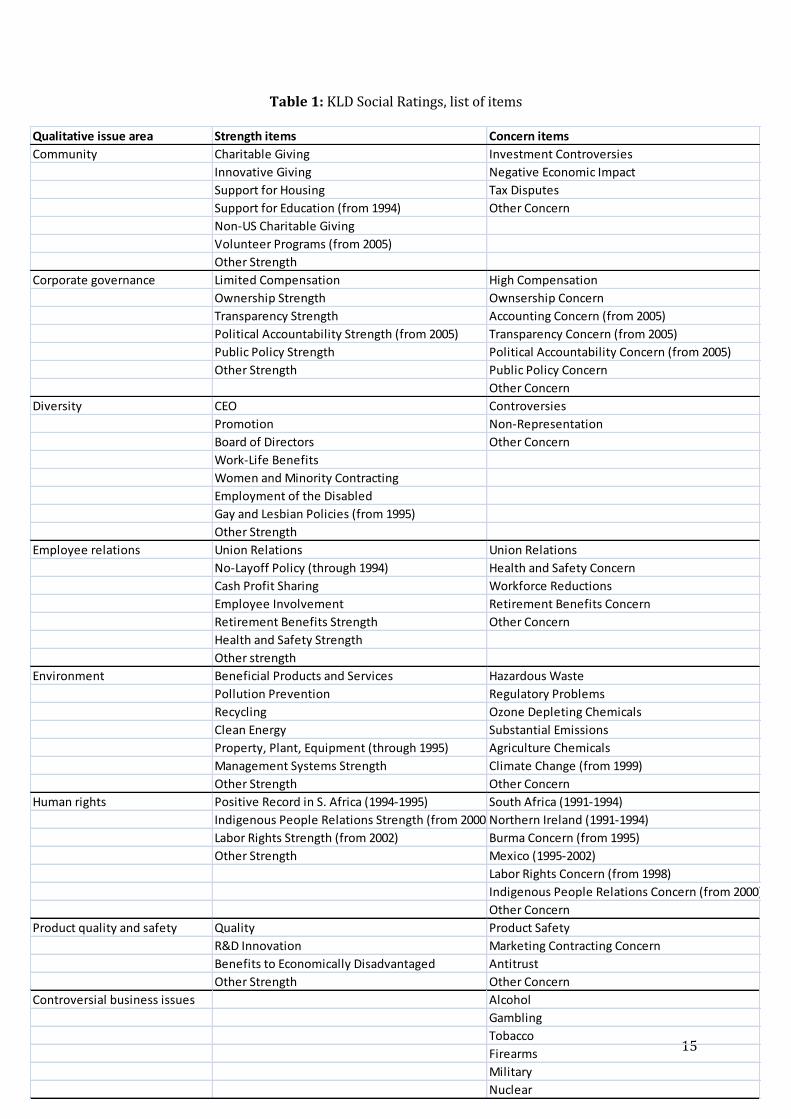

Insert Table 1

Table 1 provides the list of the qualitative issues under each of the mentioned headings.

The community section records generous giving for charities, innovation, housing, education, as

well as, since 2005, the presence of strong volunteer programs. Until 2002, the respect for the

sovereignty, land, culture, human rights, and intellectual property of indigenous people was

included in this section, it was then moved into the Human Rights area. Involvement in tax

disputes, major controversies on lending or investment practices (for financial institutions), on

the economic impact (environment, quality of life, tax, property values), and other controversies

that have mobilized community opposition are also accounted for.

The corporate governance heading considers top management and board members

remuneration levels, ownership by or of companies rated as having social strengths or concerns,

social, environmental and political transparency, attitude toward public policy issues,

involvement in accounting related controversies and other noteworthy corporate initiatives.

Some of these items were renamed in 2002 or added in 2006 (see table 1).

The diversity area notifies the presence in the company of women, members of minority

groups and disabled, it records outstanding employee benefits (including childcare, elder care,

or flextime), progressive policies toward gay and lesbian employees or other commitment to

diversity as well as involvement in diversity controversies.

Fair treatment of the workforce is assessed in the employee relations' section. It includes

layoff, health, safety and retirement policies, profit-sharing programs, employee involvement in

the financial performance (stock options, gain sharing, stock ownership, sharing financial

information, participation to management decisions) and other major employee relations

initiatives or controversies.

Attitude toward the environment is also examined. The development of products and

services with environmental benefit or harm, pollution prevention programs, the use of

renewable energy and clean fuels, and other noteworthy environmental commitments are taken

into account, as well as waste management, disrespect of environmental regulations, ozone

depleting chemicals manufacturing, toxic chemicals production, impact on climate change and

other environmental controversies.

The human rights section considers social record and controversies in South Africa from

1991 to 1994, relation with indigenous people (added in 2004), labor rights overseas, concerns

for having operations in Northern Ireland, Burma, controversies in Mexico toward employees or

environment, and other human rights commitment or controversies.

The quality and safety of products is also evaluated, by looking at long-term company-

wide programs, research and development, provision of products or services for the

economically disadvantaged, advertising policies, consumer fraud and government contracting,

6

antitrust violations (pricing, collusion), franchises, nuclear safety or other product-related

issues.

Finally, KLD ratings deal with controversial business issues with alcohol, gambling,

tobacco, firearms, military and nuclear power. Licensing the company or brand name to alcohol,

gambling or tobacco products; manufacturing, retailing, having ownership in or supporting

companies related to alcoholic beverages (beer, distilled spirits, or wine) and/or products

necessary for production of alcoholic beverages, goods used for gambling (slot machines,

roulette wheels, lottery terminals), tobacco products (cigarettes, cigars, pipe tobacco, smokeless

tobacco products), small arms ammunition or firearms, weapons or weapons systems or related

components; building, owning or designing nuclear power plants, or providing nuclear power

service are all considered as controversial business issues' concerns.

Further details on how these issues are rated are made available online by KLD Research

& Analytics (now MSCI).

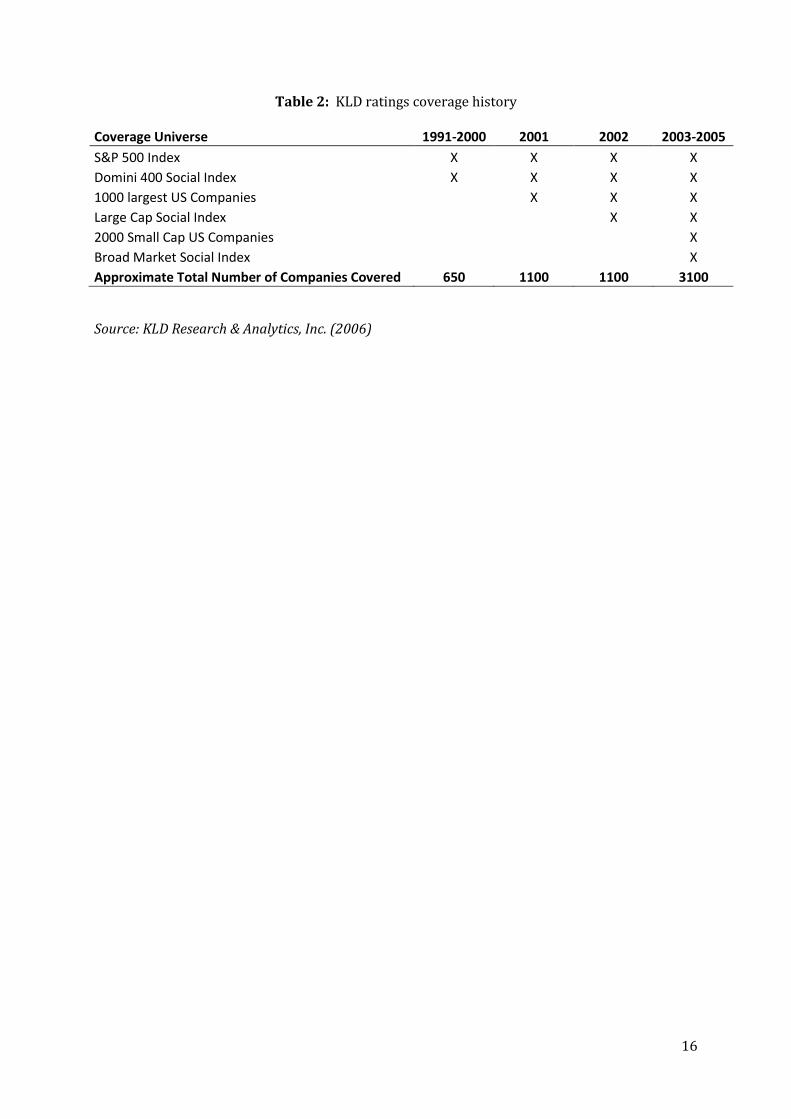

Insert Table 2

Table 2 presents the coverage history of KLD statistics. The coverage has expanded over

time, starting with 650 companies including the Domini 400 Social Index and S&P500 from 1991

to 2001, and recording now 3100 companies by adding US companies in the 1000 largest, Large

Cap Social Index, 2000 Small Cap Social Index and Broad Market Social Index.

The use of aggregate measures of CSR based on KLD data is problematic for two reasons.

First, positive and negative social actions are independent constructs (Mattingly and Berman

2006). Strengths and weaknesses may have contradictory effects on the dependent variable.

Effects associated with positive social actions are different from those associated with negative

social actions. In our case, we might expect that firms engage strategically in social activities

when they face intense competition, this could lead to more social strengths but not necessarily

to the absence of social concern, or vice versa. Second, adding raw KLD scores across domains

overweights some domains and underweights others because the maximum number of

strengths and concerns is not equal across domains (Fernandez and Santalo 2010).

Prior research has designed several alternatives. In our analysis, we will compare the

results that we obtain with both aggregate and disaggregate measures of CSR. The first part of

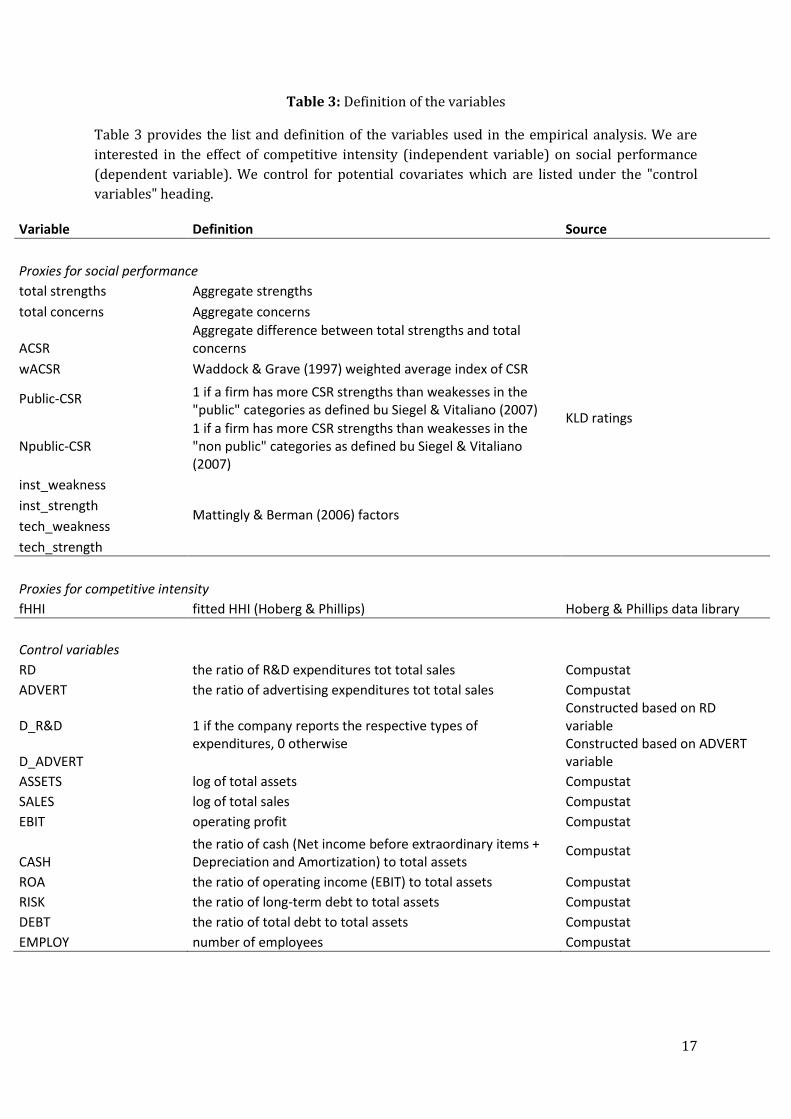

table 3 lists and defines the variables used as proxies for social performance and the following

paragraph explains how these variables are computed in more details and what each can bring

to the analysis.

Insert Table 3

Aggregate strengths and aggregate concerns can be studied as separate variables as in

Mattingly and Berman (2006) or Fernandez and Santalo (2010). The substraction of total

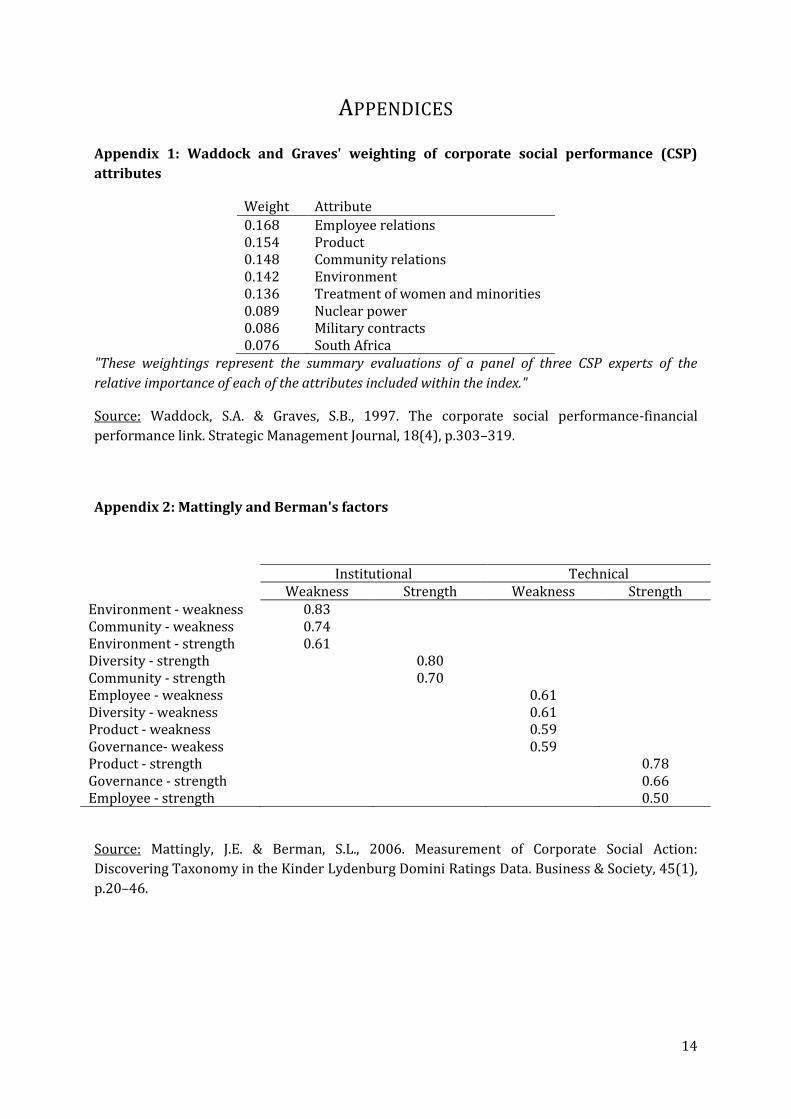

concerns to total strengths gives the aggregate CSR (ACSR). Waddock and Grave (1997) created

an index based on eight CSP attributes: community relations, employee relations, environment,

product characteristics, women and minorities, military contracting, nuclear power, and human

rights. A weighting scheme (see appendix 1) is used to deal with the problem of relative

importance of each items in the KLD rating over time and with changing social standards. We

compute a weighted aggregate CSR based on the same weighting scheme and include the

7

variable in the analysis (wACSR). Following Siegel and Vitaliano (2007), we consider a proxy for

"public CSR" with a dummy variable taking the value of 1 if a firm has more strengths than

weaknesses in community relations, diversity, environment and human rights (Public-CSR). We

also include a proxy for "non public CSR" focusing on the other KLD dimensions: employee

relations, corporate governance and product quality and safety (NPublic-CSR). Mattingly and

Berman (2006) show that the 12 KLD variables can be reduced to 4 distinct factors, underlying

patterns in corporate social actions. Institutional weakness corresponds to weak or negative

social action toward environment and community, institutional strength consists in strong or

positive social activity toward community and diversity stakeholders, technical weakness is

defined as weak social action toward stakeholders that are primarily engaged in resource

exchanges with the firm (employees, consumers, stockholders (governance), diversity), and

technical strength means positive social action toward technical stakeholders (consumers,

stockholders and employees). We compute the four factors based on the weighting scheme

detailed in appendix 2, reported in Mattingly and Berman's paper.

3.3. Control Variables

Corporate social responsibility has been shown to be affected by several other factors

that need to be included to the analysis:

Research and development (RD): firms operating in more competitive industries might

invest more in R&D in addition to implementing socially responsible policies

(McWilliams and Siegel 2001, Fernandez and Santalo 2010). We measure R&D intensity

using the ratio of R&D expenditures to total sales.

Advertising (ADVERT): the inclusion of a variable capturing advertising intensity is

motivated by two issues. First, under higher competitive pressures, firms are more likely

to invest in advertising (Fernandez and Santalo 2010). Second, in more advertising

sensitive industries, visible social performance has more impact (Fisman et al. 2005). We

capture advertising intensity with a ratio of advertising expenditures to total sales.

Servaes and Tamayo (2012) recently showed that advertising expenditures are

determinant in the relationship between corporate social responsibility and financial

performance.

D_RD and D_ADVERT: as reporting advertising and R&D expenditures to the SEC is not a

mandatory requirement, a large fraction of observations have missing values for these

variables. Following prior literature, instead of dropping observations, we assign them a

zero value and create two dummies, one for each variable, that is equal to 1 if the

company reports each respective type of expenditures, and 0 otherwise.

Operating performance (EBIT, CASH and ROA): firms in more competitive environments

are likely to have lower excess resources available to spend on CSR. We employ three

different measures of operating performance: operating profits (Fernandez and Santalo

2010), the ratio of cash to total assets (Fisman et al. 2005) and the return on assets

(Harjoto and Jo 2011).

Firm size (ASSETS and SALES): size is related to both competitive intensity and social

performance: less competitive industries are more likely to have fewer and larger firms,

larger firms have greater visibility, larger operational impact and are expected to invest

more in socially responsible actions. The most commonly used proxies for firm size are

the logarithm of total value of assets and the logarithm of total net sales.

8

Firm risk (RISK): we control for firm risk using the ratio of long-term debt to total assets.

The management's risk tolerance influences its attitude toward social activities

(Waddock and Graves 1997).

Industry characteristics: unobserved industry characteristics, other than product market

competition can be correlated at the same time with CSR and competition proxies. We

neutralize this effect by adding industry dummies using 3-digit SIC codes.

3.4. Method

In this paragraph, we develop the method employed to assess the effect of product

market competition on social performance. We run both univariate and multivariate analyses.

Hoberg and Phillips' fitted HHI was estimated empirically by the authors and contains some

measurement error. A way to mitigate this problem is to classify industries into concentrated

and competitive terciles, rather than using raw values of the index. In the univariate tests, we

compare average social performance indicators between concentrated and competitive

industries. To construct the two subsamples, we use the thresholds defined by the US

department of justice: a market can be considered as concentrated with an Herfindahl-

Hirschman index below 1000 and competitive above 1800. We compute correlations between

different measures of social performance to assess the independence or relationship between

strengths, concerns, aggregate and disaggregate indicators. We also calculate correlation

coefficients with the indicator of competitive intensity but correlation does not mean causation.

In the multivariate analysis, we investigate the effect of competition on social

performance indicators. Ordinary least squared (OLS) estimation can be used in our case but

some empirical issues must be taken into consideration. Firstly, we need to consider the

endogeneity problem resulting from a potential simultaneous relationship between the

dependent and independent variables. Competition may, at least partially, be determined as a

function of social actions. Social actions can indeed be used by firms as a way to introduce or

intensify existing competition on the industry. In order to neutralize this effect, we

systematically use lagged independent variables in all our regressions. Secondly, we are dealing

with panel data i.e. our sample provides information on a set of firms in the cross-section and on

several time-periods (yearly basis). In such a situation, observations are not independent,

coefficients and standard errors are biased. We cluster standard errors by considering that

observations are independent across firms but not within firms and across time. In the

specification, we take into account time and industry effects. The introduction of year dummies

allows to neutralize the time-period period effect across the whole sample. Industry dummies

isolate unobserved factors that are fixed within each industry and that affect the dependent

variable. Our model therefore captures the intra-industry variation across time.

4. Sample

Our sample includes all firms reported in both Compustat and KLD data from 1995 to

2009 and whose industry-level fitted HHI is available in Hoberg and Phillips' data. Industries are

defined by their 3-digit SIC code.

The matching between Compustat, KLD and Hoberg and Phillips data is based on firms'

cusip and 3-digit SIC-codes as reported by Compustat's historical SIC codes. More specifically,

we match KLD to Compustat data by first converting KLD's cusip into Compustat's permno

9

based on Compustat's recorded cusips and then by merging converted permno-based KLD

variables to Compustat's sample.

Before matching the databases, Compustat's data on all recorded firms from 1995 to

2009 include 58,096 firm-year observations on 3,873 unique firms. KLD data include 26,895

firm-year observations on 4,790 unique firms. Hoberg and Phillips' data contain 6,807 industry-

year observations on 255 unique industries. Panel A of table 4 gives descriptive statistics on the

sample after the matching procedure. Missing values may result from either the absence of

record in the database, or for KLD data the impossibility to convert the cusip into the

corresponding Compustat's permno based on Compustat's recorded historical cusips. The

reason why we have unequal number of observations for social performance proxies is that the

"firearms" category was only added in 1999 to KLD ratings. Aggregate measures of social

performance that include the "firearms" section are therefore not observed before this date.

Insert Table 4

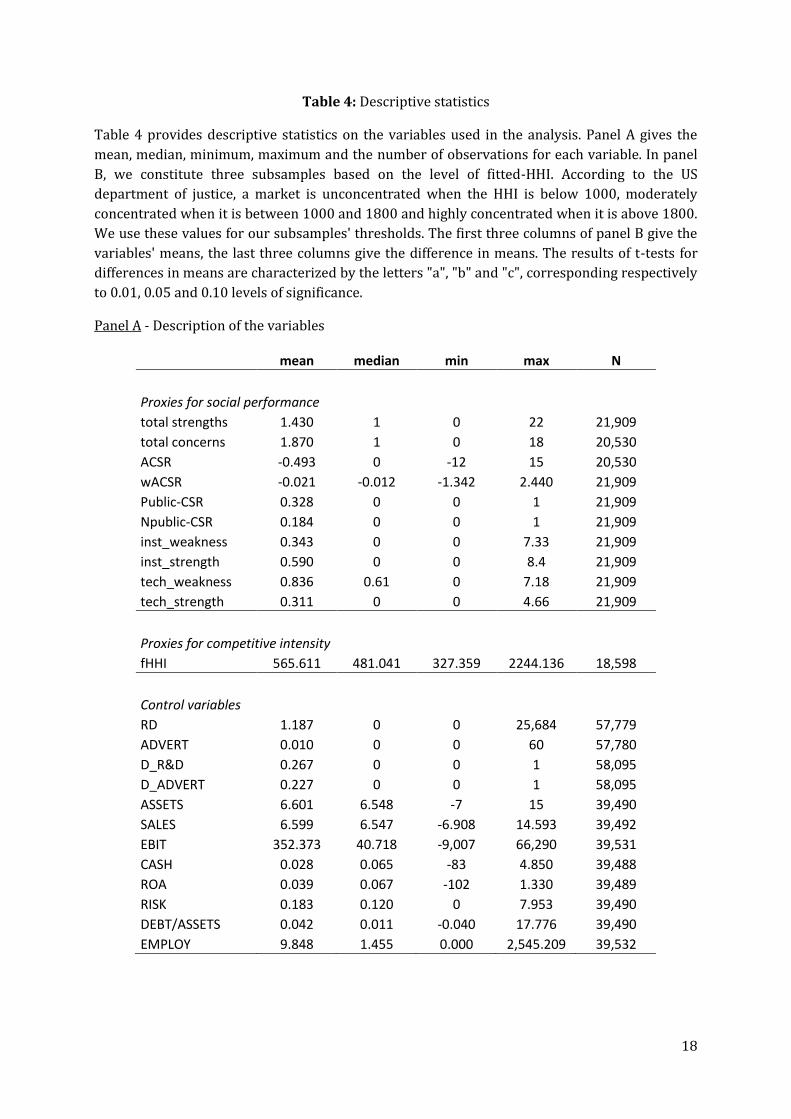

On table 4, we can see that the median difference between total strengths and total concerns

(ACSR) is 0, the most negative values for this variable are actually pulling the mean downward.

Its negative value suggests that there are on average more concerns than strengths in our

sample. Not surprisingly, the public corporate social responsibility (Public-CSR) seems to be

higher than the non public one on average. This is consistent with social actions being a way to

improve a firm's public image. Technical weakness has the highest mean, suggesting particularly

weak social action toward employees, consumers, stockholders in our sample. Statistics on

market concentration indicate the presence of highly concentrated industries, the average fitted-

HHI being higher than its median and the maximum value being almost four times bigger than

the mean.

5. Results

5.1. Univariate statistics

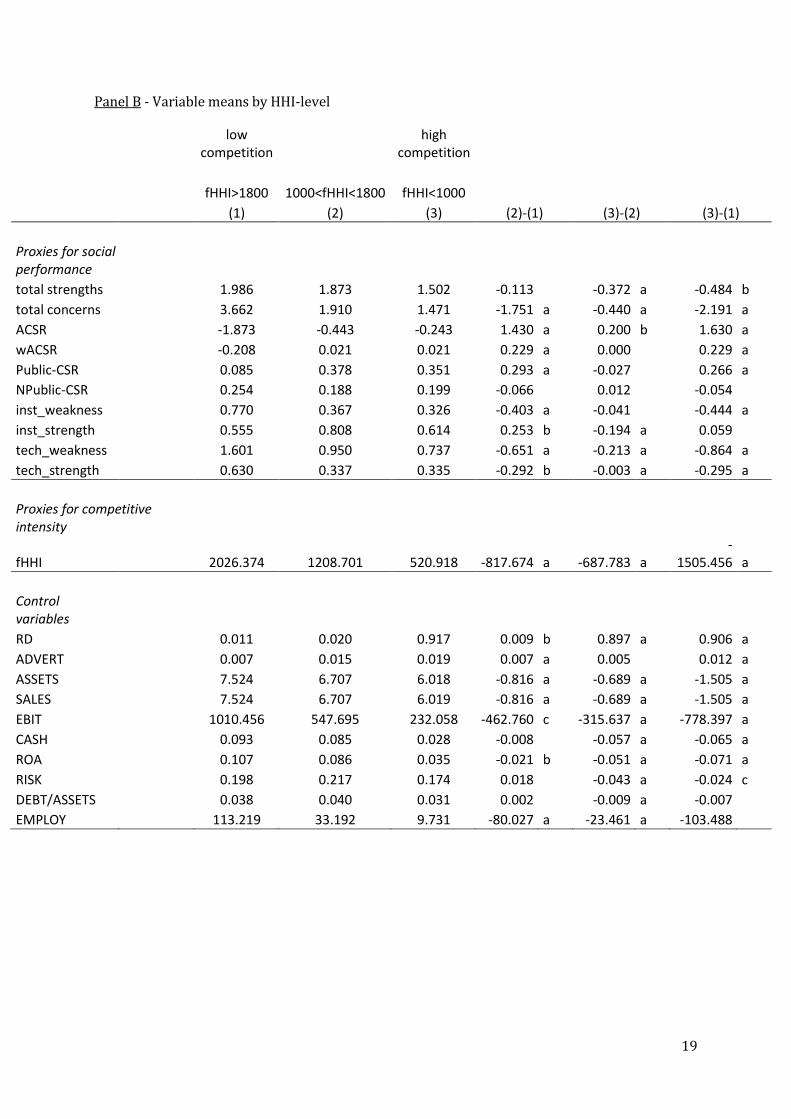

In Panel B of table 4, we observe in the last column the difference between the variables'

means of the most competitive industries and those of the most concentrated ones. Letters "a",

"b", or "c" indicate the significance level of the means' differences. Overall social performance

(ACSR) is on average significantly higher in competitive industries (+1.630). When there is more

competition, there seems to be fewer social strengths on average (-0.484), but also fewer

concerns and in a bigger proportion (-2.191). The use of Waddock and Graves weights to

compute an aggregate social performance (wACSR) confirms the improved social performance

in more competitive markets but at a lower level (0.229). Interestingly, public CSR is

significantly better in competitive markets (+0.266) but there is no significant difference for non

public CSR. Both institutional and technical weaknesses are lower in more competitive

environment but technical strength is also lower.

Concerning the control variables, we can see that firms in more competitive industries

spend more on average in research and development and in advertising, are lower in size

(ASSETS and SALES), have lower profits (EBIT), less cash available and a lower profitability

(ROA).

Insert Table 5

10

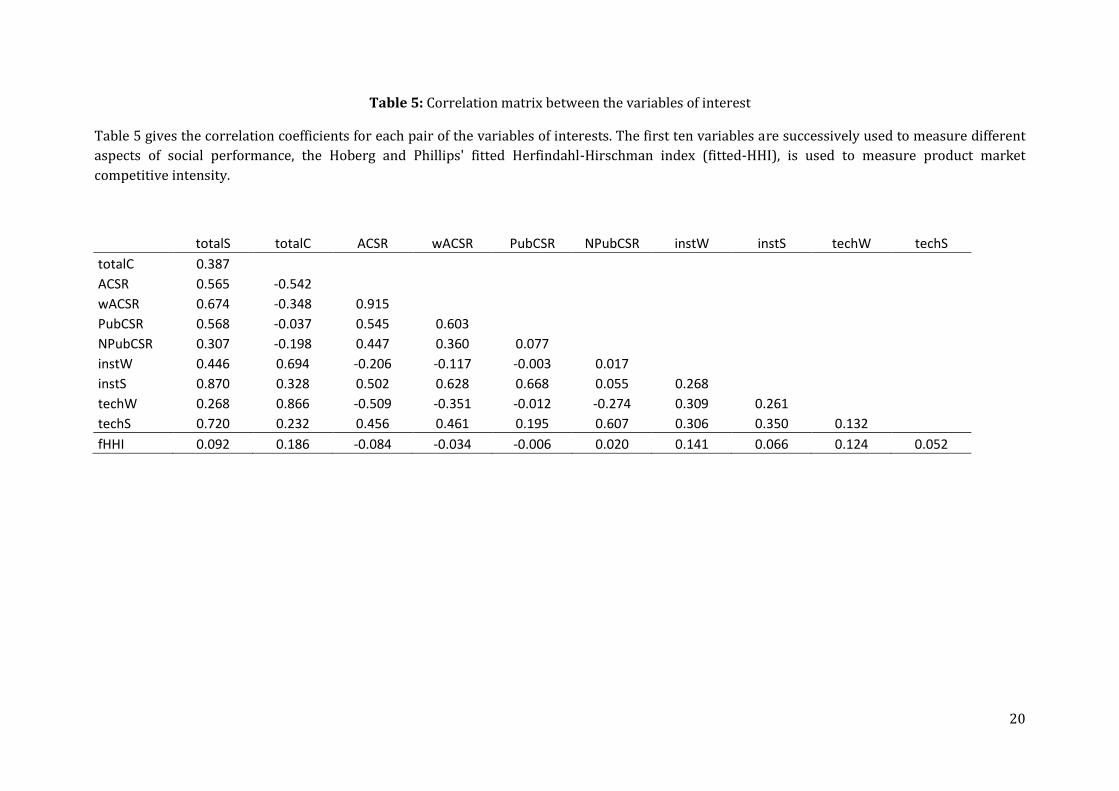

Table 5 presents the correlation coefficients between our variables of interest. It is interesting to

notice a positive correlation between total strengths and total concerns, consistent with the

findings of Kotchen and Moon (2011) that social responsibility is associated to social

irresponsibility. It is also consistent with Mattingly and Berman (2006) that positive social

action is not necessarily associated to less negative social action. The correlation of fitted HHI

with total strengths is small but positive, the correlation with total concern is positive and

bigger, consistent with the results of Table 4 - Panel B: the improved social performance of

competitive markets seems to be explained by less concerns, rather than by more strengths.

5.2. Multivariate statistics

Insert Table 6

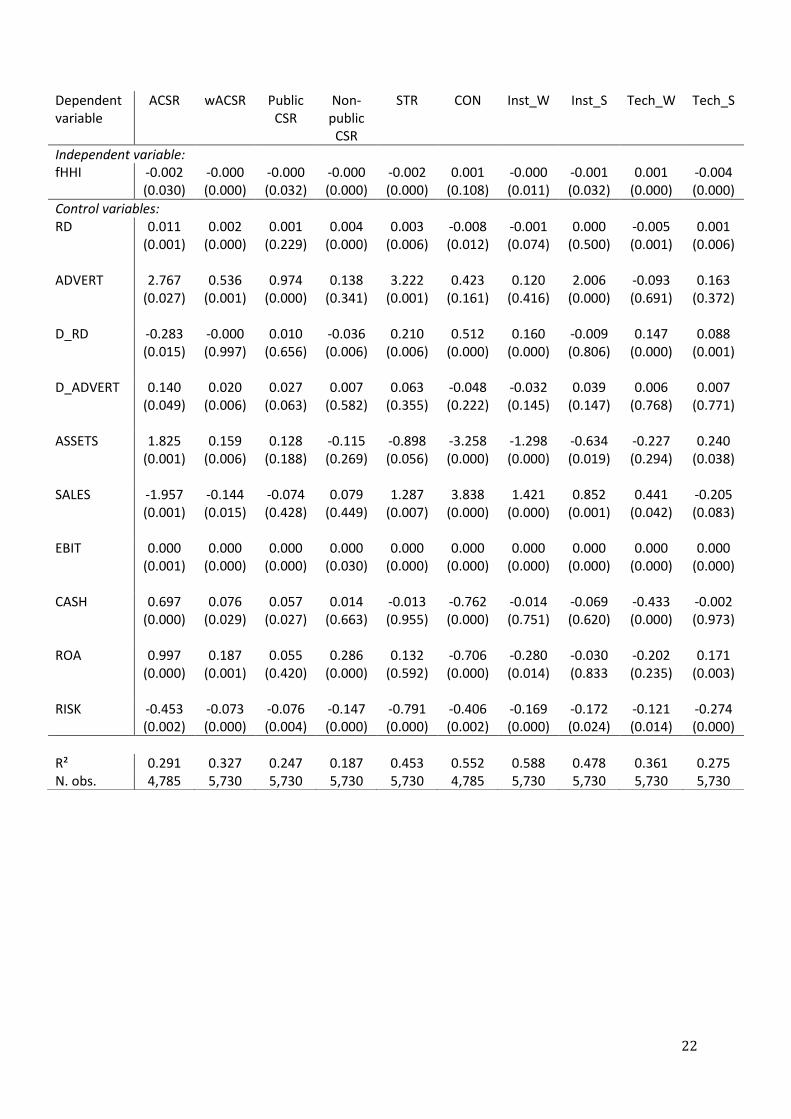

In Table 6, the results of the OLS regressions are presented. This table shows very

consistent results with the idea that intensified competition increase social performance. The

negative and significant coefficients of the fitted HHI for total strengths, both aggregate and

weighted differences between total strengths and total concerns, both public and non-public CSR

indicate that firms operating on less concentrated (more competitive) markets have better social

performance. The coefficient for total concerns is positive but weakly significant. This result

invalidates conclusions in the univariate analysis that the improvement of social performance in

more competitive environments is driven by a decrease in total concerns. Here we observe on

the contrary that it is driven by a very significant increase of total strengths and a weakly

significant decrease of total concerns. These results support the idea that considering positive

and negative social actions as different constructs provides additional insights on how social

performance varies. Institutional and technical strengths appear to be improved in more

competitive environments (negative coefficient with concentration index) and technical

weakness is lower. Interestingly, institutional weakness is significantly related to the fitted HHI

but the coefficient is negative. The sign of this coefficient shows that negative social action

toward environment and community (definition of institutional weakness) is actually more

developed under competitive pressure.

Table 6 also provides details on the coefficients of the control variables. Consistent with

prior literature, research & development and advertising expenditures are positively associated

to indicators of social performance. As mentioned by McWilliams and Siegel (2001), in more

competitive environments firms increase these expenditures in addition to undertaking socially

responsible initiatives. Moreover, there is a positive impact of visible social responsibility in

industries where advertising activity is more intense (Fisman et al., 2005). Interestingly, the log

of total assets is positively associated to social performance, whereas the log of total sales is

negatively associated with social performance. The first result is consistent with the idea that

bigger firms have more public visibility and need to worry about their social impact. The second

result seems to be driven by a significant increase of social concerns, despite an increase in

social strengths but in a smaller proportion. Indicators of operating performance (EBIT, cash,

ROA) are significantly positively related to aggregate social performance, consistent with the

idea that investing in socially responsible initiatives is more likely when the firm has excess

resources available. The negative relationship with risk can be explained by a similar argument.

Riskier firms in terms of the ratio of long-term debt to total assets will prefer to save resources

to compensate this risk, rather than investing it in social actions.

11

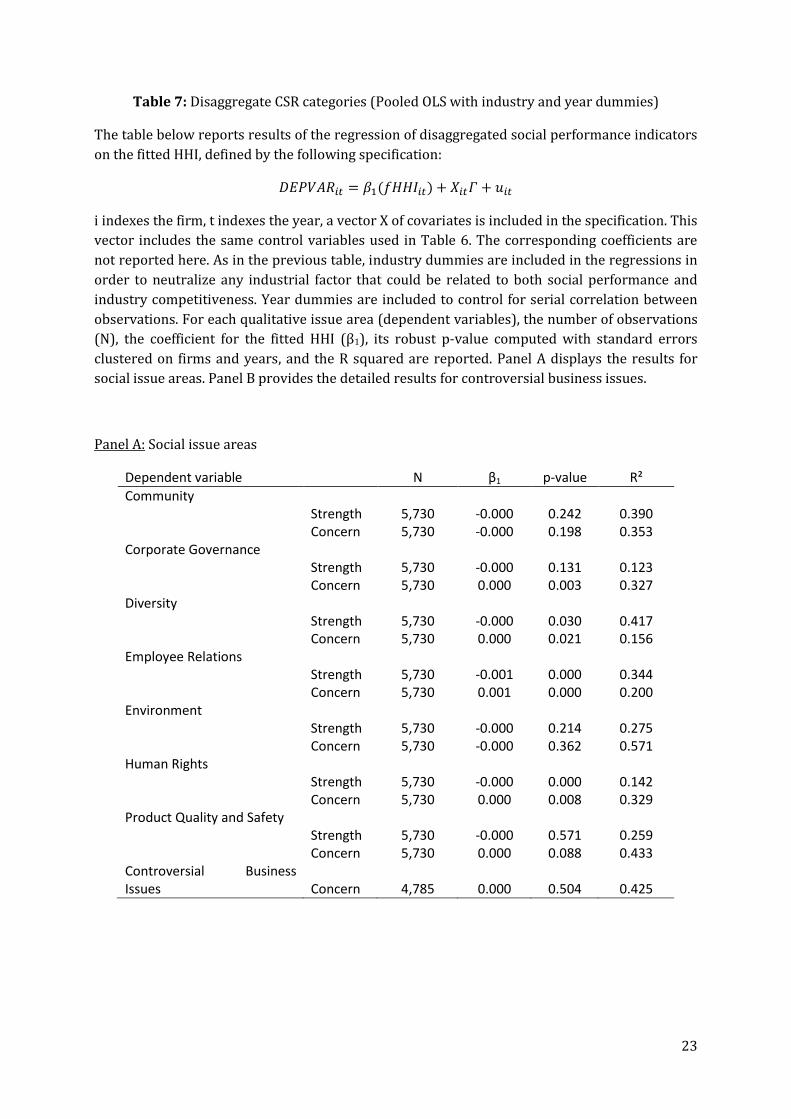

Insert table 7

Table 7 examines the effect of competitive intensity on the separate dimensions of

corporate social performance. If competition drives social performance, we expect a negative

relationship between social strengths and our indicator of industry concentration (the fitted

HHI), and a positive relationship between concerns and the fitted HHI. Interestingly, this

relationship is significantly verified for corporate governance, diversity and human rights but is

not true for the community and environment sections. Product quality and safety strengths is

not significantly associated to market competition whereas product concerns are significantly

reduced in more competitive environment. The relationship with controversial business issues

(CBI) does not appear to be significant when computed as an aggregate score. Panel B allows to

understand what underlines the high p-value associated to the CBI coefficient (0.504).

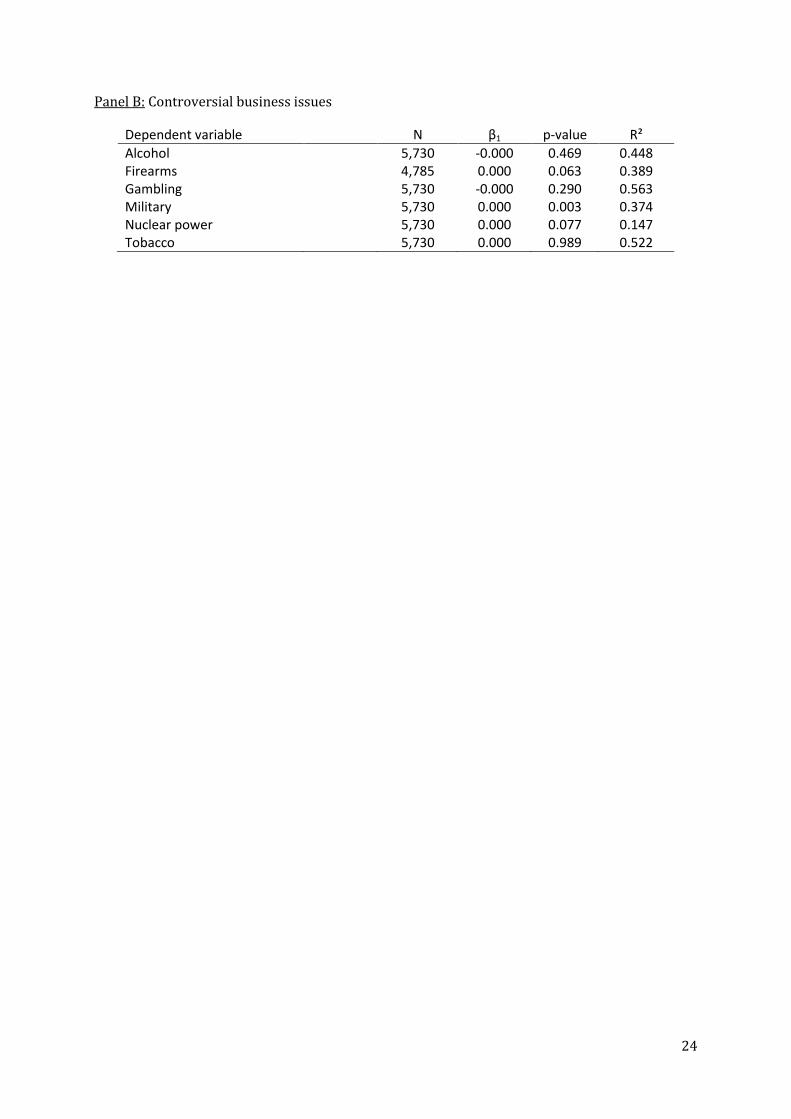

Indeed, we observe in panel B that some controversial business issues are not

significantly related to competition. Namely, issues related to alcohol, gambling and tobacco do

not appear to be related to competitive intensity, whereas firearms, military and nuclear power

issues do show significant positive coefficients i.e. positive association with concentration:

negative association with competition.

Overall, panels A and B of table 7 show that the positive relationship between

competition and social performance does not hold every separate dimension of social

responsibility. More specifically, shareholder- and employee-related social actions are improved

in more competitive environment while community and environment sections are not

significantly different depending on industry competition. Product quality and safety strengths

do not vary significantly with competition but product concerns are significantly reduced.

6. Conclusion

The aim of this paper is to analyze the link between product market competition and the

different dimensions of corporate social responsibility. Positive and negative corporate social

actions are different constructs and what is referred to as corporate social responsibility

includes different areas whose strategic interest may vary. The measurement of product market

competition present many empirical issues notably because of the difficulty to access to data on

companies that are not publicly listed.

Given these empirical issues, we use different measures of CSR, including detailed

indicators for every dimensions that are included in MSCI (formerly KLD) social ratings. For the

measurement of industry competitiveness, we use a recently developed measure of

concentration that provides information on all public and private firms, all industries, and every

year from 1975 to 2005. We carry out OLS regressions, taking into account endogeneity

concerns and serial correlation of panel data.

Our results provide additional insights on the strategic purpose of CSR. Specifically, we

show that -1- competition increases corporate social strengths but does not significantly reduces

social concerns, -2- the positive relationship between social performance and market

competition does not hold for environment, community, -3- product quality and safety strengths

12

are not significantly improved in more competitive environments while product concerns are

reduced, -4- involvement in firearms, military and nuclear power is not related to competition.

Corporate social initiatives can be strategic and competition exerts a positive pressure

on some dimensions of corporate social responsibility. However, some other dimensions are not

affected by competition, which suggests that those dimensions are not considered by firms as of

strategic competitive interest. Competitive motives may not be sufficient to maintain or improve

every dimension of social welfare.

References

Ali, A., Klasa, S. & Yeung, E., 2009. The Limitations of Industry Concentration Measures

Constructed with Compustat Data: Implications for Finance Research. The Review of

Financial Studies, 22, p.3839–3871.

Bagnoli, M. & Watts, S.G., 2003. Selling to Socially Responsible Consumers: Competition and The

Private Provision of Public Goods. Journal of Economics & Management Strategy, 12(3),

p.419–445.

Barnea, A. & Rubin, A., 2010. Corporate Social Responsibility as a Conflict Between Shareholders.

Journal of Business Ethics, 97(1), p.71-86.

Baron, D.P., 2001. Private politics, corporate social responsibility, and integrated strategy.

Journal of Economics & Management Strategy, 10(1), p.7-45.

Davis, I., 2005. Business and society: The biggest contract. The Economist.

Delios, A., 2010. How Can Organizations Be Competitive but Dare to Care? Academy of

Management Perspectives, 24(3), p.25-36.

Elhauge, E.R., 2005. Corporate managers’ operational discretion to sacrifice corporate profits in

the public interest. Environmental Protection and the Social Responsibility of Firms.

Washington: Resources for the Future, p.13–76.

Fernández-Kranz, D. & Santaló, J., 2010. When Necessity Becomes a Virtue: The Effect of Product

Market Competition on Corporate Social Responsibility. Journal of Economics &

Management Strategy, 19(2), p.453–487.

Fisman, R., Heal, G. & Nair, V., 2005. Corporate social responsibility: doing well by doing good?

Working Paper (Wharton School, University of Pennsylvania).

Harjoto, M.A. & Jo, H., 2011. Corporate Governance and CSR Nexus. Journal of Business Ethics,

100(1), p.45–67.

Heal, G., 2005. Corporate social responsibility: An economic and financial framework. The

Geneva papers on risk and insurance-Issues and practice, 30(3), p.387–409.

Hillman, A. & Keim, G., 2001. Shareholder value, stakeholder management, and social issues:

what’s the bottom line? Strategic Management Journal, 22(2), p.125-139.

13

Hoberg, G. & Phillips, G., 2010a. Product Market Synergies and Competition in Mergers and

Acquisitions: A Text-Based Analysis. Review of Financial Studies, 23(10), p.3773 –3811.

Hoberg, G. & Phillips, G.M., 2010b. Real and Financial Industry Booms and Busts. Journal of

Finance, Forthcoming.

Jones, T.M., 1995. Instrumental stakeholder theory: a synthesis of ethics and economics.

Academy of Management Review, 20(2), p.404-437.

Kotchen, M.J. & Moon, J.J., 2011. Corporate social responsibility for irresponsibility, National

Bureau of Economic Research.

Margolis, J.D. & Walsh, J.P., 2003. Misery Loves Companies: Rethinking Social Initiatives by

Business. Administrative Science Quarterly, 48(2), p.268-305.

Mattingly, J.E. & Berman, S.L., 2006. Measurement of Corporate Social Action: Discovering

Taxonomy in the Kinder Lydenburg Domini Ratings Data. Business & Society, 45(1),

p.20–46.

McWilliams, A. & Siegel, D., 2001. Corporate Social Responsibility: A Theory of the Firm

Perspective. The Academy of Management Review, 26(1), p.117-127.

McWilliams, A., Siegel, D.S. & Wright, P.M., 2006. Corporate Social Responsibility: Strategic

Implications. Journal of Management Studies, 43(1), p.1-18.

Russo, M.V. & Fouts, P.A., 1997. A resource-based perspective on corporate environmental

performance and profitability. Academy of Management Journal, 40(3), p.534-559.

Sachs, J.D., 2011. The Price of Civilization: Reawakening American Virtue and Prosperity,

Random House.

Servaes, H. & Tamayo, A.M., 2012. The Impact of Corporate Social Responsibility on Firm Value:

The Role of Customer Awareness. Management Science, Forthcoming.

Siegel, D.S. & Vitaliano, D.F., 2007. An Empirical Analysis of the Strategic Use of Corporate Social

Responsibility. Journal of Economics & Management Strategy, 16(3), p.773–792.

Waddock, S.A. & Graves, S.B., 1997. The corporate social performance-financial performance

link. Strategic Management Journal, 18(4), p.303–319.

14

APPENDICES

Appendix 1: Waddock and Graves' weighting of corporate social performance (CSP)

attributes

Weight Attribute

0.168 0.154 0.148 0.142 0.136 0.089 0.086 0.076

Employee relations Product Community relations Environment Treatment of women and minorities Nuclear power Military contracts South Africa

"These weightings represent the summary evaluations of a panel of three CSP experts of the

relative importance of each of the attributes included within the index."

Source: Waddock, S.A. & Graves, S.B., 1997. The corporate social performance-financial

performance link. Strategic Management Journal, 18(4), p.303–319.

Appendix 2: Mattingly and Berman's factors

Institutional Technical Weakness Strength Weakness Strength Environment - weakness Community - weakness Environment - strength Diversity - strength Community - strength Employee - weakness Diversity - weakness Product - weakness Governance- weakess Product - strength Governance - strength Employee - strength

0.83 0.74 0.61

0.80 0.70

0.61 0.61 0.59 0.59

0.78 0.66 0.50

Source: Mattingly, J.E. & Berman, S.L., 2006. Measurement of Corporate Social Action:

Discovering Taxonomy in the Kinder Lydenburg Domini Ratings Data. Business & Society, 45(1),

p.20–46.

15

Qualitative issue area Strength items Concern items

Community Charitable Giving Investment Controversies

Innovative Giving Negative Economic Impact

Support for Housing Tax Disputes

Support for Education (from 1994) Other Concern

Non-US Charitable Giving

Volunteer Programs (from 2005)

Other Strength

Corporate governance Limited Compensation High Compensation

Ownership Strength Ownsership Concern

Transparency Strength Accounting Concern (from 2005)

Political Accountability Strength (from 2005) Transparency Concern (from 2005)

Public Policy Strength Political Accountability Concern (from 2005)

Other Strength Public Policy Concern

Other Concern

Diversity CEO Controversies

Promotion Non-Representation

Board of Directors Other Concern

Work-Life Benefits

Women and Minority Contracting

Employment of the Disabled

Gay and Lesbian Policies (from 1995)

Other Strength

Employee relations Union Relations Union Relations

No-Layoff Policy (through 1994) Health and Safety Concern

Cash Profit Sharing Workforce Reductions

Employee Involvement Retirement Benefits Concern

Retirement Benefits Strength Other Concern

Health and Safety Strength

Other strength

Environment Beneficial Products and Services Hazardous Waste

Pollution Prevention Regulatory Problems

Recycling Ozone Depleting Chemicals

Clean Energy Substantial Emissions

Property, Plant, Equipment (through 1995) Agriculture Chemicals

Management Systems Strength Climate Change (from 1999)

Other Strength Other Concern

Human rights Positive Record in S. Africa (1994-1995) South Africa (1991-1994)

Indigenous People Relations Strength (from 2000)Northern Ireland (1991-1994)

Labor Rights Strength (from 2002) Burma Concern (from 1995)

Other Strength Mexico (1995-2002)

Labor Rights Concern (from 1998)

Indigenous People Relations Concern (from 2000)

Other Concern

Product quality and safety Quality Product Safety

R&D Innovation Marketing Contracting Concern

Benefits to Economically Disadvantaged Antitrust

Other Strength Other Concern

Controversial business issues Alcohol

Gambling

Tobacco

Firearms

Military

Nuclear

Table 1: KLD Social Ratings, list of items

16

Table 2: KLD ratings coverage history

Coverage Universe 1991-2000 2001 2002 2003-2005

S&P 500 Index X X X X

Domini 400 Social Index X X X X

1000 largest US Companies

X X X

Large Cap Social Index

X X

2000 Small Cap US Companies

X

Broad Market Social Index

X

Approximate Total Number of Companies Covered 650 1100 1100 3100

Source: KLD Research & Analytics, Inc. (2006)

17

Table 3: Definition of the variables

Table 3 provides the list and definition of the variables used in the empirical analysis. We are

interested in the effect of competitive intensity (independent variable) on social performance

(dependent variable). We control for potential covariates which are listed under the "control

variables" heading.

Variable Definition Source

Proxies for social performance total strengths Aggregate strengths

KLD ratings

total concerns Aggregate concerns

ACSR Aggregate difference between total strengths and total concerns

wACSR Waddock & Grave (1997) weighted average index of CSR

Public-CSR 1 if a firm has more CSR strengths than weakesses in the "public" categories as defined bu Siegel & Vitaliano (2007)

Npublic-CSR 1 if a firm has more CSR strengths than weakesses in the "non public" categories as defined bu Siegel & Vitaliano (2007)

inst_weakness

Mattingly & Berman (2006) factors inst_strength

tech_weakness

tech_strength

Proxies for competitive intensity

fHHI fitted HHI (Hoberg & Phillips) Hoberg & Phillips data library

Control variables RD the ratio of R&D expenditures tot total sales Compustat

ADVERT the ratio of advertising expenditures tot total sales Compustat

D_R&D 1 if the company reports the respective types of expenditures, 0 otherwise

Constructed based on RD variable

D_ADVERT Constructed based on ADVERT variable

ASSETS log of total assets Compustat

SALES log of total sales Compustat

EBIT operating profit Compustat

CASH the ratio of cash (Net income before extraordinary items + Depreciation and Amortization) to total assets

Compustat

ROA the ratio of operating income (EBIT) to total assets Compustat

RISK the ratio of long-term debt to total assets Compustat

DEBT the ratio of total debt to total assets Compustat

EMPLOY number of employees Compustat

18

Table 4: Descriptive statistics

Table 4 provides descriptive statistics on the variables used in the analysis. Panel A gives the

mean, median, minimum, maximum and the number of observations for each variable. In panel

B, we constitute three subsamples based on the level of fitted-HHI. According to the US

department of justice, a market is unconcentrated when the HHI is below 1000, moderately

concentrated when it is between 1000 and 1800 and highly concentrated when it is above 1800.

We use these values for our subsamples' thresholds. The first three columns of panel B give the

variables' means, the last three columns give the difference in means. The results of t-tests for

differences in means are characterized by the letters "a", "b" and "c", corresponding respectively

to 0.01, 0.05 and 0.10 levels of significance.

Panel A - Description of the variables

mean median min max N

Proxies for social performance total strengths 1.430 1 0 22 21,909

total concerns 1.870 1 0 18 20,530

ACSR -0.493 0 -12 15 20,530

wACSR -0.021 -0.012 -1.342 2.440 21,909

Public-CSR 0.328 0 0 1 21,909

Npublic-CSR 0.184 0 0 1 21,909

inst_weakness 0.343 0 0 7.33 21,909

inst_strength 0.590 0 0 8.4 21,909

tech_weakness 0.836 0.61 0 7.18 21,909

tech_strength 0.311 0 0 4.66 21,909

Proxies for competitive intensity fHHI 565.611 481.041 327.359 2244.136 18,598

Control variables RD 1.187 0 0 25,684 57,779

ADVERT 0.010 0 0 60 57,780

D_R&D 0.267 0 0 1 58,095

D_ADVERT 0.227 0 0 1 58,095

ASSETS 6.601 6.548 -7 15 39,490

SALES 6.599 6.547 -6.908 14.593 39,492

EBIT 352.373 40.718 -9,007 66,290 39,531

CASH 0.028 0.065 -83 4.850 39,488

ROA 0.039 0.067 -102 1.330 39,489

RISK 0.183 0.120 0 7.953 39,490

DEBT/ASSETS 0.042 0.011 -0.040 17.776 39,490

EMPLOY 9.848 1.455 0.000 2,545.209 39,532

19

Panel B - Variable means by HHI-level

low competition

high competition

fHHI>1800 1000<fHHI<1800 fHHI<1000

(1) (2) (3) (2)-(1) (3)-(2) (3)-(1)

Proxies for social performance

total strengths

1.986 1.873 1.502 -0.113

-0.372 a -0.484 b

total concerns

3.662 1.910 1.471 -1.751 a -0.440 a -2.191 a

ACSR

-1.873 -0.443 -0.243 1.430 a 0.200 b 1.630 a

wACSR

-0.208 0.021 0.021 0.229 a 0.000

0.229 a

Public-CSR

0.085 0.378 0.351 0.293 a -0.027

0.266 a

NPublic-CSR

0.254 0.188 0.199 -0.066

0.012

-0.054 inst_weakness

0.770 0.367 0.326 -0.403 a -0.041

-0.444 a

inst_strength

0.555 0.808 0.614 0.253 b -0.194 a 0.059 tech_weakness

1.601 0.950 0.737 -0.651 a -0.213 a -0.864 a

tech_strength 0.630 0.337 0.335 -0.292 b -0.003 a -0.295 a

Proxies for competitive intensity

fHHI 2026.374 1208.701 520.918 -817.674 a -687.783 a

-1505.456 a

Control variables

RD

0.011 0.020 0.917 0.009 b 0.897 a 0.906 a

ADVERT

0.007 0.015 0.019 0.007 a 0.005

0.012 a

ASSETS

7.524 6.707 6.018 -0.816 a -0.689 a -1.505 a

SALES

7.524 6.707 6.019 -0.816 a -0.689 a -1.505 a

EBIT

1010.456 547.695 232.058 -462.760 c -315.637 a -778.397 a

CASH

0.093 0.085 0.028 -0.008

-0.057 a -0.065 a

ROA

0.107 0.086 0.035 -0.021 b -0.051 a -0.071 a

RISK

0.198 0.217 0.174 0.018

-0.043 a -0.024 c

DEBT/ASSETS

0.038 0.040 0.031 0.002

-0.009 a -0.007 EMPLOY 113.219 33.192 9.731 -80.027 a -23.461 a -103.488

20

Table 5: Correlation matrix between the variables of interest

Table 5 gives the correlation coefficients for each pair of the variables of interests. The first ten variables are successively used to measure different

aspects of social performance, the Hoberg and Phillips' fitted Herfindahl-Hirschman index (fitted-HHI), is used to measure product market

competitive intensity.

totalS totalC ACSR wACSR PubCSR NPubCSR instW instS techW techS

totalC 0.387 ACSR 0.565 -0.542

wACSR 0.674 -0.348 0.915 PubCSR 0.568 -0.037 0.545 0.603

NPubCSR 0.307 -0.198 0.447 0.360 0.077 instW 0.446 0.694 -0.206 -0.117 -0.003 0.017

instS 0.870 0.328 0.502 0.628 0.668 0.055 0.268 techW 0.268 0.866 -0.509 -0.351 -0.012 -0.274 0.309 0.261

techS 0.720 0.232 0.456 0.461 0.195 0.607 0.306 0.350 0.132 fHHI 0.092 0.186 -0.084 -0.034 -0.006 0.020 0.141 0.066 0.124 0.052

21

Table 6: Firm-level OLS with industry and year dummies

Table 6 presents the results of the OLS regressions that focus on the effect of competitive

intensity, as measured by the fitted HHI, on corporate social performance, successively proxied

by eleven different indicators. A set of control variables is included in the regression and the

corresponding coefficients are also reported hereafter. To account for endogeneity problems, all

dependent variables in every regression are lagged 1 year. For each coefficient, the table also

reports the corresponding robust p-value computed based on clustered standard errors (in

parentheses). In the computation of clustered standard errors, observations are considered to

be independent across firms but not within firms and across time. Industry dummies are

included in the regressions in order to neutralize any industrial factor that could be related to

both social performance and industry competitiveness. Year dummies are included to control for

serial correlation between observations.

22

Dependent variable

ACSR wACSR Public CSR

Non-public

CSR

STR CON Inst_W Inst_S Tech_W Tech_S

Independent variable: fHHI -0.002

(0.030) -0.000 (0.000)

-0.000 (0.032)

-0.000 (0.000)

-0.002 (0.000)

0.001 (0.108)

-0.000 (0.011)

-0.001 (0.032)

0.001 (0.000)

-0.004 (0.000)

Control variables: RD 0.011

(0.001) 0.002

(0.000) 0.001

(0.229) 0.004

(0.000) 0.003

(0.006) -0.008 (0.012)

-0.001 (0.074)

0.000 (0.500)

-0.005 (0.001)

0.001 (0.006)

ADVERT 2.767 (0.027)

0.536 (0.001)

0.974 (0.000)

0.138 (0.341)

3.222 (0.001)

0.423 (0.161)

0.120 (0.416)

2.006 (0.000)

-0.093 (0.691)

0.163 (0.372)

D_RD -0.283 (0.015)

-0.000 (0.997)

0.010 (0.656)

-0.036 (0.006)

0.210 (0.006)

0.512 (0.000)

0.160 (0.000)

-0.009 (0.806)

0.147 (0.000)

0.088 (0.001)

D_ADVERT

0.140 (0.049)

0.020 (0.006)

0.027 (0.063)

0.007 (0.582)

0.063 (0.355)

-0.048 (0.222)

-0.032 (0.145)

0.039 (0.147)

0.006 (0.768)

0.007 (0.771)

ASSETS

1.825 (0.001)

0.159 (0.006)

0.128 (0.188)

-0.115 (0.269)

-0.898 (0.056)

-3.258 (0.000)

-1.298 (0.000)

-0.634 (0.019)

-0.227 (0.294)

0.240 (0.038)

SALES -1.957

(0.001)

-0.144 (0.015)

-0.074 (0.428)

0.079 (0.449)

1.287 (0.007)

3.838 (0.000)

1.421 (0.000)

0.852 (0.001)

0.441 (0.042)

-0.205 (0.083)

EBIT 0.000 (0.001)

0.000 (0.000)

0.000 (0.000)

0.000 (0.030)

0.000 (0.000)

0.000 (0.000)

0.000 (0.000)

0.000 (0.000)

0.000 (0.000)

0.000 (0.000)

CASH 0.697

(0.000)

0.076 (0.029)

0.057 (0.027)

0.014 (0.663)

-0.013 (0.955)

-0.762 (0.000)

-0.014 (0.751)

-0.069 (0.620)

-0.433 (0.000)

-0.002 (0.973)

ROA 0.997 (0.000)

0.187 (0.001)

0.055 (0.420)

0.286 (0.000)

0.132 (0.592)

-0.706 (0.000)

-0.280 (0.014)

-0.030 (0.833

-0.202 (0.235)

0.171 (0.003)

RISK -0.453 (0.002)

-0.073 (0.000)

-0.076 (0.004)

-0.147 (0.000)

-0.791 (0.000)

-0.406 (0.002)

-0.169 (0.000)

-0.172 (0.024)

-0.121 (0.014)

-0.274 (0.000)

R² 0.291 0.327 0.247 0.187 0.453 0.552 0.588 0.478 0.361 0.275 N. obs. 4,785 5,730 5,730 5,730 5,730 4,785 5,730 5,730 5,730 5,730

23

Table 7: Disaggregate CSR categories (Pooled OLS with industry and year dummies)

The table below reports results of the regression of disaggregated social performance indicators

on the fitted HHI, defined by the following specification:

i indexes the firm, t indexes the year, a vector X of covariates is included in the specification. This

vector includes the same control variables used in Table 6. The corresponding coefficients are

not reported here. As in the previous table, industry dummies are included in the regressions in

order to neutralize any industrial factor that could be related to both social performance and

industry competitiveness. Year dummies are included to control for serial correlation between

observations. For each qualitative issue area (dependent variables), the number of observations

(N), the coefficient for the fitted HHI (β1), its robust p-value computed with standard errors

clustered on firms and years, and the R squared are reported. Panel A displays the results for

social issue areas. Panel B provides the detailed results for controversial business issues.

Panel A: Social issue areas

Dependent variable N β1 p-value R²

Community Strength Concern

5,730 5,730

-0.000 -0.000

0.242 0.198

0.390 0.353

Corporate Governance Strength Concern

5,730 5,730

-0.000 0.000

0.131 0.003

0.123 0.327

Diversity Strength Concern

5,730 5,730

-0.000 0.000

0.030 0.021

0.417 0.156

Employee Relations Strength Concern

5,730 5,730

-0.001 0.001

0.000 0.000

0.344 0.200

Environment Strength Concern

5,730 5,730

-0.000 -0.000

0.214 0.362

0.275 0.571

Human Rights Strength Concern

5,730 5,730

-0.000 0.000

0.000 0.008

0.142 0.329

Product Quality and Safety Strength Concern

5,730 5,730

-0.000 0.000

0.571 0.088

0.259 0.433

Controversial Business Issues

Concern

4,785

0.000

0.504

0.425

24

Panel B: Controversial business issues

Dependent variable N β1 p-value R²

Alcohol 5,730 -0.000 0.469 0.448 Firearms 4,785 0.000 0.063 0.389 Gambling 5,730 -0.000 0.290 0.563 Military 5,730 0.000 0.003 0.374 Nuclear power 5,730 0.000 0.077 0.147 Tobacco 5,730 0.000 0.989 0.522