professional - yellow capital · professional summer 2010 investor the new investment landscape...

TRANSCRIPT

T H E O F F I C I A L J O U R N A L O F T H E C F A S O C I E T Y O F T H E U K

w w w . c f a u k . o r g s u p p o r t i n g A S I P , C F A a n d I M C p r o f e s s i o n a l sw w w . c f a u k . o r g s u p p o r t i n g A S I P , C F A a n d I M C p r o f e s s i o n a l s

PROFESSIONAL INVESTORSUMMER 2010

THE NEW INVESTMENT LANDSCAPE

“I think many people didn’t really understand what was happening in the

markets. Emotions were running high.” Ken Kinsey-Quick, CFA, ASIP,

head of multi-manager, Thames River Capital

BEST PRACTICEIt is time for a new approach

THE FINANCIAL CRISISHow various problems were all interconnected

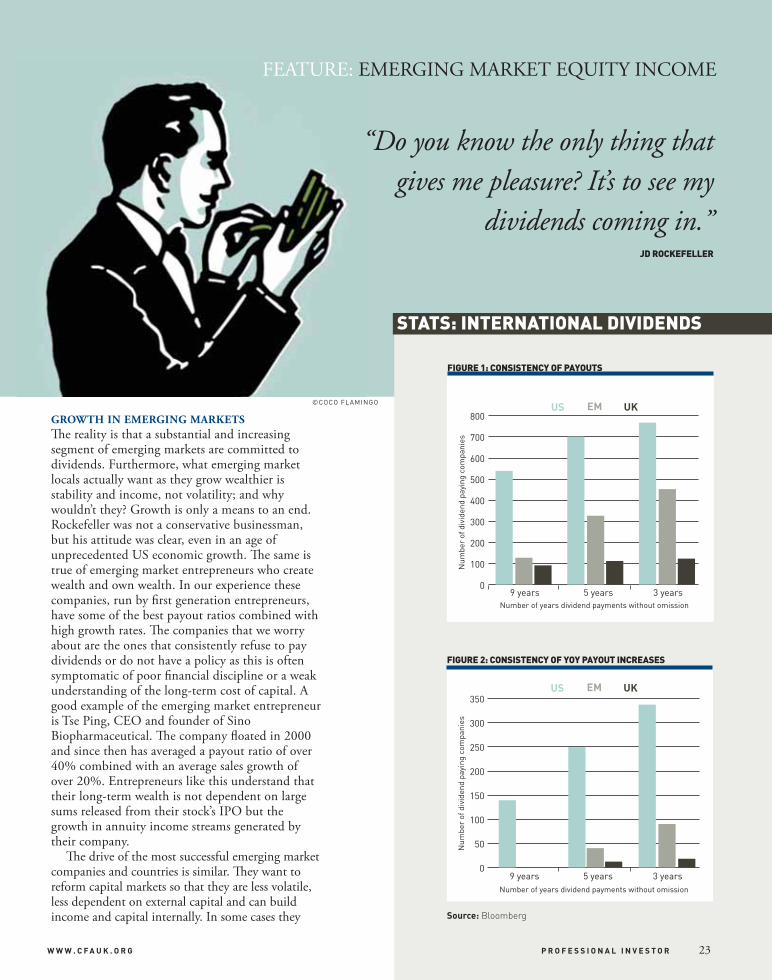

DIVIDENDS IN EMERGING MARKETSIs emerging market equity income the Holy Grail?

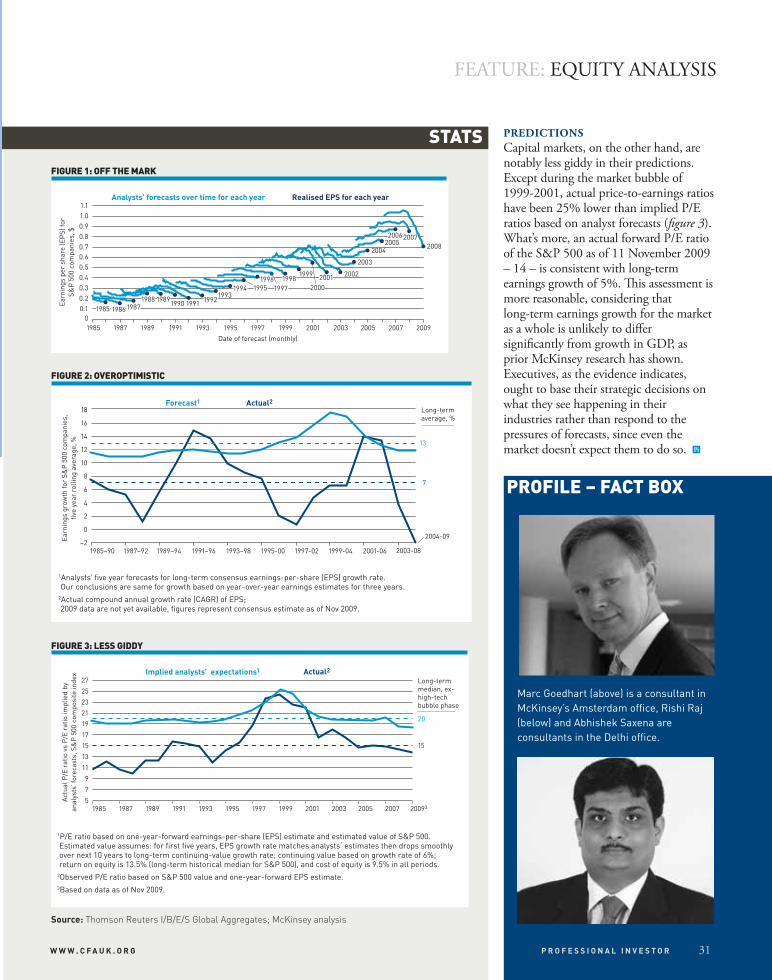

EQUITY ANALYSTSWhy they are still too bullish

SOURCES OF RETURN ROUNDTABLEWhy there are diffi cult times ahead for investors

cover.indd Sec5:3cover.indd Sec5:3 1/6/10 09:29:181/6/10 09:29:18

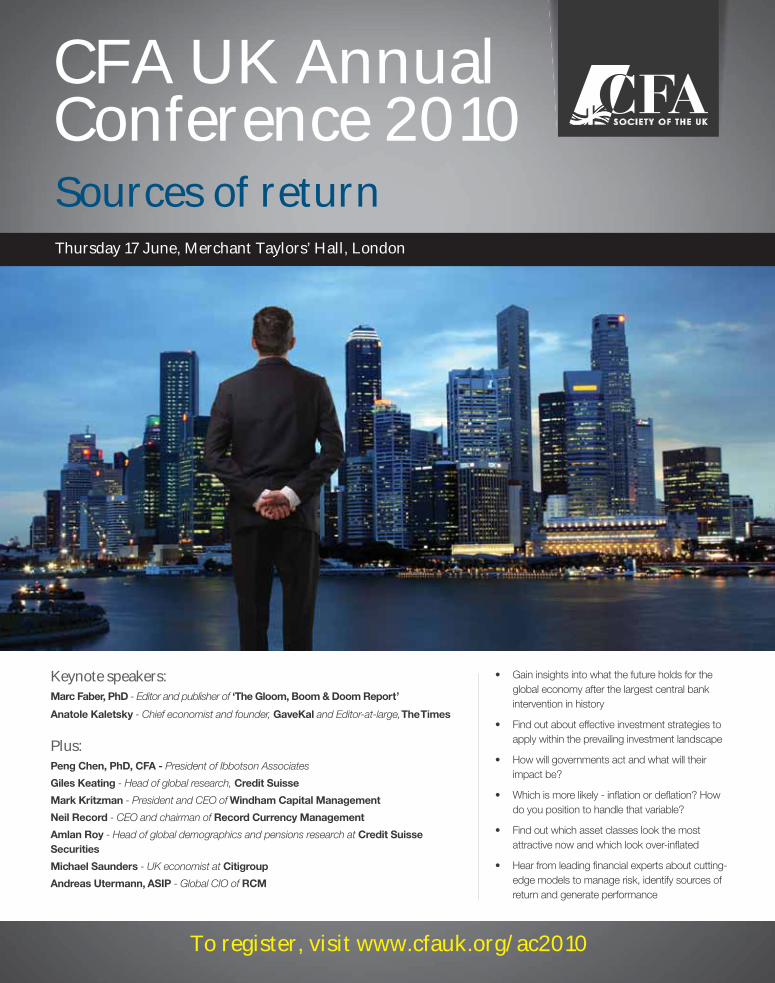

CFA UK Annual Conference 2010Sources of return

To register, visit www.cfauk.org/ac2010

Thursday 17 June, Merchant Taylors’ Hall, London

Keynote speakers:Marc Faber, PhD - Editor and publisher of ‘The Gloom, Boom & Doom Report’

Anatole Kaletsky - Chief economist and founder, GaveKal and Editor-at-large, The Times

Plus:Peng Chen, PhD, CFA - President of Ibbotson Associates

Giles Keating - Head of global research, Credit Suisse

Mark Kritzman - President and CEO of Windham Capital Management

Neil Record - CEO and chairman of Record Currency Management

Amlan Roy - Head of global demographics and pensions research at Credit Suisse Securities

Michael Saunders - UK economist at Citigroup

Andreas Utermann, ASIP - Global CIO of RCM

6134 AW.indd 1 24/05/2010 13:33

1P R O F E S S I O N A L I N V E S T O RW W W . C F A U K . O R G

WELCOME

George Spentzos, CFACHAIRMAN

Editor Maha Khan PhillipsSub editor Tom PumphreyEditorial assistant Laura MaddrellDesign editor Catriona Dickson, Dojo DesignPhotography Abi Hardwick, Abi Imaging

Professional Investor is published byCFA Society of the UK, 2nd Floor135 Cannon Street, London EC4N 5BP.Tel: 020 7280 9620 Fax: 020 7280 9636Email: [email protected]: www.cfauk.org

Chief executive Will Goodhart

SubscriptionsProfessional Investor is published fourtimes a year. Subscription rates are:£145 for UK/Europe,£195 for the rest of the world

CFA UK members and otherpractitioner readers are invited tosubmit articles for possible inclusion. Please email the society on [email protected]. Contributed articles will be reviewed for possible inclusion by the Marketing and Communications Committee.

Marketing & Communications CommitteeAnnabel Gillard, CFA (Chair), Claudine Delavy, CFA, Anouschka Elliott, CFA, Eric Foran, CFA, Nick Henderson, CFA, Guy McCulloch, Tim Nuding, CFA, Jane Thorburn, Steve Wellard

The society is not responsible for anymaterial published in Professional Investor, and publication of any material or expression of opinions does notnecessarily imply that the society agreeswith them. Neither the society nor thepublishers are jointly or severallyauthorised to conduct investmentbusiness and do not provide investmentadvice or recommendations to anyone.

Original designCG Business Communcations

Printed by Wyndeham Grange, Southwick, West Sussex.

The CFA Society of the UK represents the interests of more than 8,500 leading members of the investment industry. The society, which was founded in 1955, is a leading member society of CFA Institute and is committed to the development of the investment industry through the promotion of the highest ethical standards and through the provision of education, professional development, advocacy, information and career support on behalf of its members. CFA UK supports the CFA, ASIP and IMC designations.

Articles are published without responsibilityon the part of the publishers or authors forloss occasioned by any person acting orrefraining from action as a result of anyview expressed therein. Volume 20, Number 2.issn 0958-2541. © 2010 CFA UK

This issue of Professional Investor will be distributed

at the society’s Annual Conference on June 17th. This is the third year that the society has run an Annual Conference and we are delighted with the

quality of speakers that have taken part and at the response from members. I recently

returned from CFA Institute’s Annual Conference in Boston. We took part in the

meetings to help us prepare for the 2011 CFA Institute Annual Conference in

Edinburgh. The chairman of the Scottish Committee and I presented to delegates at the

meeting and showed a welcome video featuring Alex Salmond, fi rst minister of Scotland.

You can view the video on the society’s website.

CFA UK is honoured and excited to host next year’s conference (May 8th to 11th).

Having the conference in the UK gives us an opportunity to provide members with an

even more extensive speaker programme and with additional opportunities to network

with clients and counterparts from around the world. The Annual Conference is

always an opportunity to learn from leading investment professionals and to refocus

on core truths. This year’s event was no exception. For me, there were several

particular highlights. First, Jeremy Grantham of GMO reminded us that our

profession is littered with confl icts and simple ethical failures. As Grantham points

out: ‘We have allowed this deterioration in ethical conduct without a whimper. We

have made no protest into the general slide into the rathole where we fi nd ourselves

today’. He called for greater leadership in dealing with confl icts and the ineffi ciencies

arising from perceived career risk.

Elsewhere, Niall Fergusson warned us that while the present sovereign debt

situation is bad, it is likely to get much worse. As Fergusson says ‘If you can’t stabilise

public fi nances because too may people are receiving too much [from the state], then

reform is forced upon you by the bond market. The case for pre-emption is

overwhelming.’ But, Fergusson is not confi dent that the case will be heard and

forecasts higher infl ation for the UK as the only route acceptable to politicians for

dealing with the debt crisis.

These are the types of challenging issues that will likely be discussed at next year’s

conference in Edinburgh. We hope to see you there.

CE letter.indd Sec1:1CE letter.indd Sec1:1 1/6/10 09:40:401/6/10 09:40:40

2 S U M M E R 2 0 1 0

“T h e i n d u s t r y h a s b e h a v e d l a r g e l y l i k e a Alan Brown, FSIPShaking the trees (or rethinking the basics) | page 18

1525

15

19

featureTHE NEW INVESTMENT LANDSCAPE

10 SOURCES OF RETURN ROUNDTABLE Katherine Garrett-Cox, ASIP, Sunil Krishnan, CFA, Joe Biernat, CFA, and Robin Young, ASIP, discuss key investment trends, sources of returns, and challenges for investors in the future.

SHAKING THE TREESThe best practise model of today is fatally fl awed, and is based on unrealistic expectations, argues Alan Brown, FSIP. It is time to concentrate on what is important, rather than easy, and that means pension funds need to be focused on liabilities.

22

INTERNATIONAL SAVINGS AND INVESTMENT IN THE BALANCEThere are many diverse reasons for the recent fi nancial crisis, but it is a mistake to think that they are unconnected, argues Andrew Smithers.

UNEXPECTED DIVIDENDS FROM GLOBAL EMERGING MARKETSEmerging market companies paid out $150 billion in dividends last year, more than twice the UK fi gure. Despite this however, little attention is paid to emerging market equity income as an asset class. Edward Lam discusses why.

198

7

02-3 contents.indd 202-3 contents.indd 2 1/6/10 10:00:261/6/10 10:00:26

3P R O F E S S I O N A L I N V E S T O R

CONTENTS

PROFESSIONAL INVESTOR | SUMMER 2010

the regulars

W W W . C F A U K . O R G

36

4

32

33

34

38

40

d e e r c a u g h t i n t h e h e a d l i g h t s”

MEMBER PROFILESPI interviews Ken Kinsey-Quick, CFA, ASIP, Rohini Rathour, ASIP, Nick Carmichael, CFA, Gemma Game, CFA, Stephen Peters, CFA, and Stephanie Niven, CFA.

NEW RESEARCHPapers on compulsory and voluntary annuities markets in the UK, domestic credit and private investment, and causal relationships between stock prices and exchange rates.

VOLUNTEER REPORTTimothy Nuding, CFA.

CFA UK REPORTSurvey results show improvement in CFA UK services.

CFA INSTITUTE REPORTThe launch of CFA Institute’s website and member’s portal – My CFA.

BOOK REVIEWSJ Mark Wiltshire, CFA, CAIA, FRM, highlights fi ve books which relive the summers of 2007 and 2008 and offer lessons for today’s investor.

NEW MEMBERSProfi les of members who have joined CFA UK in the last quarter.

25

30

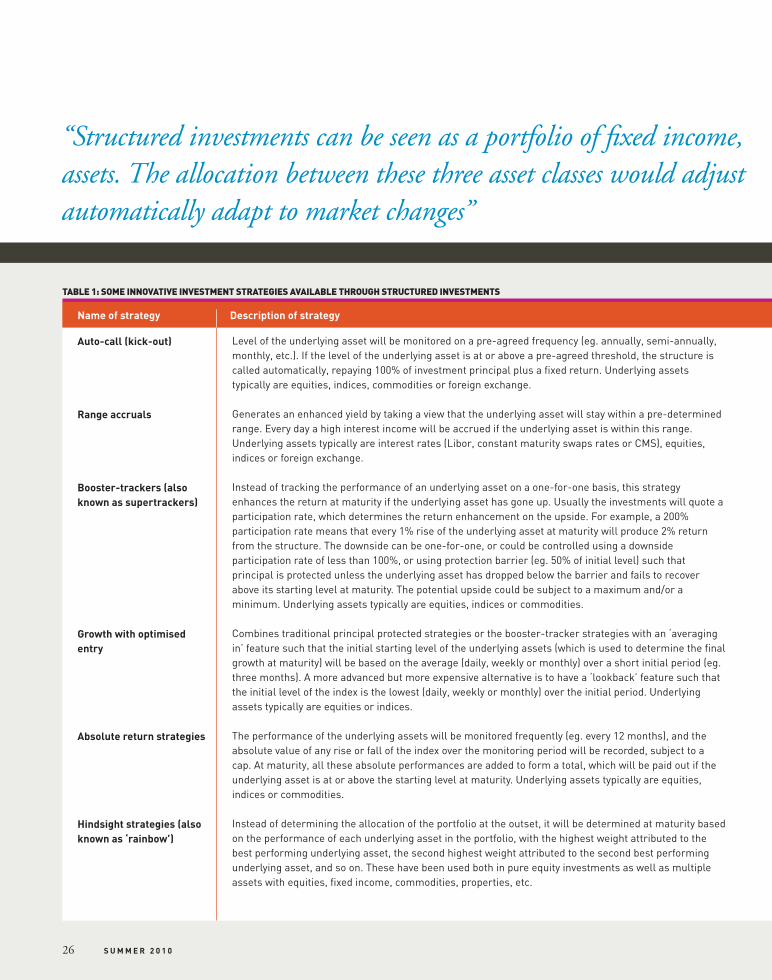

30IN SEARCH OF RETURNS IN UNCERTAIN MARKETSA new breed of structured investments could bring an edge to portfolio management, says James Chu, CFA.

EQUITY ANALYSTS: STILL TOO BULLISHAfter almost a decade of stricter regulation, analysts’ earnings forecasts continue to be excessively optimistic, argue Mark Goedhart, Rishi Raj, and Abhishek Saxena.

02-3 contents.indd 302-3 contents.indd 3 1/6/10 10:00:281/6/10 10:00:28

4 S U M M E R 2 0 1 0

IN BRIEF. KEN KINSEY-QUICK, CFA, ASIP

1991 Blue Circle Pension Fund1994 Ifabanque2000 Redwood Investments2000 Coronation Fund Managers2003 Thames River Captial

“In the 1990s hedge funds were a cottage industry, so much so that if you asked a manager about their operations and back offi ce and infrastructure, they would look at you quizzically”

04-9 profile.indd 404-9 profile.indd 4 1/6/10 10:12:101/6/10 10:12:10

5P R O F E S S I O N A L I N V E S T O RW W W . C F A U K . O R G

Head of multi-manager, Thames River CapitalINTERVIEW BY: MAHA KHAN PHILLIPS • PHOTOGRAPHY: ANDY LANE

Ken Kinsey-Quick, CFA, ASIP

MEMBER PROFILE

For Ken Kinsey-Quick, CFA, ASIP, hedge funds were always of interest, right from the early days, when managers only employed two or three strategies. He gained exposure to the asset class after moving to the UK from his native South Africa in 1991. Kinsey-Quick had taken a job

with the Blue Circle Pension Fund.“Blue Circle had farmed out some management to Barings,

where Crispin Odey was. He said he was leaving to launch a hedge fund. It was a bear market, and I noticed that pension funds with long-term investment horizons were losing millions of pounds because of their long-term bias in the short term,” he explains. “Hedge funds seemed like a really interesting proposition.”

Kinsey-Quick joined Paris-based Haussmann Holdings, one of the oldest funds of hedge funds in the world. He spent the next six years working at Ifabanque, one of the co-managers of Haussmann. “Th e great thing was that we had all the big names in those days, Soros, Robertson, and Bacon, for example. So we were heavily infl uenced by the original fathers of the industry.” Haussmann then gave some of its young guns 10% of the business to fi nd the industry’s future stars.

“What we found was that managers in the early part of their life cycle generate much better risk-adjusted returns than those who are established. Th ey are hungry and they have to succeed. As the fund gets bigger, the real talent moves from being a CIO to a CEO, and the quality of the DNA of the fi rm starts to go down as it starts to grow.”

Kinsey-Quick also launched and managed the Challenger fund range. By the time he left in 1999, Challenger US was ranked number one by the TASS hedge fund database.

He decided to set up his own shop in London, Redwood, but the timing was bad. “I launched in January 2000 and we went right into the bear market. At the same time, there was a company called Coronation which I had been advising, and they wanted me to join. So I sold Redwood to them and became CIO.” Despite the bear market, the fi rm grew from approximately $700 million when Kinsey-Quick joined to $1.3 billion in 2002.

DIFFICULT TIMESKinsey-Quick then joined Th ames River Capital as head of multi-manager, watching the the multi-manager business grow from $50 million in assets under management to $2.9 billion at its peak in 2008. Th en came a year of client redemptions

and underperformance. “2008 was my fi rst negative year and it was very diffi cult. I think many people didn’t really understand what was happening in the markets. Emotions were running high.”

Fund managers could not manage their strategies properly, he says, because prime brokers, and market makers’ had their balance sheets slashed. “Th ere was no liquidity, and banks were pulling in all their leverage. Th e system broke down. Th en it got repaired, and at the beginning of 2009 hedge funds were making money while markets were still falling out of bed.”

Kinsey-Quick has watched the industry evolve over time. “In the 1990s hedge funds were a cottage industry, so much so that if you asked a manager about their operations and back offi ce and infrastructure, they would look at you quizzically. It was a bit more freewheeling,” he says.

But he is against regulation for regulation’s sake. “If you look at the regulation coming out of Europe it is just messy. Hopefully, it will go through at some stage, but it will help with the public if hedge funds came onshore.”

ACQUISITIONIn May, UK quoted fund manager F&C Management announced that it was buying Th ames River Capital for an initial consideration of £53.6 million. Kinsey-Quick says that Th ames River’s model will not change. “We really wanted to take the business to the next level, which was to get involved in the institutional market. F&C is a really good fi t because they don’t have a fund of hedge funds business and while our business is currently around 80% wholesale versus institutional, with F&C it’s literally the other way around.”

Kinsey-Quick holds both the ASIP and CFA designations, which he says are extremely important. “I trained as an accountant, and working in investment management, I wanted to make sure I had all the right tools at my disposal.” He is now a board member of CFA UK and chairs the investment policy committee. “I felt that it was time to give something back. I also felt that hedge funds are often misunderstood, and that now is the time to really start the knowledge going. Hedge funds are here to stay.”

Kinsey-Quick is married with three children, with another on the way. He also explains that he is ‘mad enough’ to establish a vineyard down in Surrey, and enjoys getting involved in the more extreme. “I hiked to the South Pole a couple of years ago,” he says. “I took up kite surfi ng recently so now I am thinking of kiting to the pole,” he laughs.

04-9 profile.indd 504-9 profile.indd 5 1/6/10 10:12:131/6/10 10:12:13

6 S U M M E R 2 0 1 0

Rohini Rathour’s career path took an unexpected turn when she moved to the UK in 1991. “I didn’t really intend to live here. My father used to be in the

Indian navy and he was appointed naval attaché to the Indian commission in the UK. I thought it might be a good idea to come to London and get some work experience and just have some fun,” she explains.

Rathour had just completed an MBA from the Indian Institution of Management, Bangalore. Unfortunately, the move coincided with the recession here. She got a job selling insurance with Albany Life Assurance Company, but realised it was not for her. She then met her future husband, and decided it was time to get some further qualifi cations and settle into a career.

While doing a number of temporary jobs, Rathour sat the IIMR exam. “I really enjoyed doing it. What you learn you can actually relate to what is happening in the world.”

In 1995 Rathour was given the opportunity to train at Regent Kingpin Capital Management as an emerging markets analyst, focusing on the Indian sub-continent and Eastern European regions, thanks to the generosity of its founders, who were “willing to give me a foot in the door. I learnt a lot, it was very valuable.”

In May 1997 Rathour got what she says was her big break. She was hired by Ely Place Investments as an assistant investment manager, where she helped manage private client portfolios and a UK income fund. “Th e most humbling aspect of it is that people trust you to look after their money! But the initial focus for me was mainly the UK market. It was a great learning curve getting to know the big UK companies, and I love the fact that every day something diff erent was happening and the role was so varied. To this

INTERVIEW BY: MAHA KHAN PHILLIPS • PHOTOGRAPHY: ABI HARDWICK

Head of UK equities, Sarasin & PartnersHead of UK equities, Sarasin & Partners

Rohini Rathour, ASIP

day I feel privileged to work in this industry.”Rathour moved to Sarasin Investment Management

following its takeover of Ely Place in July 1998. Sarasin has always been a huge proponent of global investing. Rathour initially worked as assistant fund manager for the fi rm’s global balanced charity fund. She also worked as an analyst, using Sarasin’s thematic approach to picking pan-European stocks. In 2001 she helped manage the assets of the fi rm’s fl agship EquiSar fund, and in 2002 took over responsibility for pan-European equity selection for global thematic products.

In 2005, Rathour was asked to help manage the £1.3 billion UK equities portfolios that were inherited as a result of Sarasin’s merger with Chiswell Associates in 2004 using the fi rm’s global thematic investment approach. “Th ey asked me if I would be interested in leading this team to bring a thematic fl avour to the way their portfolios were being managed. It was a slow process, you can’t change the way people think overnight. But I wanted to prove that the global thematic process would also work for the UK market.”

In 2007, Rathour was promoted to head of UK equities. She says that if a company is not thematically interesting enough, then she simply won’t own it, pointing out that the UK market is very global in composition. “Th ere are many companies in the UK equity benchmark that don’t buy or sell anything in the UK. Th ey are driven by global events.”

When the fi nancial crisis hit, Rathour held her nerve. “2008 was awful but the steps we took meant that 2009 was a really good year for UK equities, because of some of the positioning that we did. Th ere were some real opportunities in that crisis and if you were brave enough to take them then you came through the other side a lot better.”

Rathour is married, with two children.

04-9 profile.indd 604-9 profile.indd 6 1/6/10 10:12:131/6/10 10:12:13

W W W . C F A U K . O R G

raise an independent credit fund to gain exposure to some of the opportunities that were apparent in the dislocated market,” he explains. Getting off the ground has been very tough, largely because of liquidity constraints. “At the moment I think it may not get off the ground the way we initially envisaged but we’re looking for opportunities to build a business within institutions and I have been engaged with some such institutions. We’ll see what happens.”

In 2009, personal tragedy struck Carmichael’s family, when his sister-in-law, Camilla Milbank, fell off a horse and broke her neck and damaged her spinal cord. Today, the eff ects of Camilla’s injuries are such that she has movement and feeling of her arms and wrists only. In a very sad twist of fate, Camilla’s father, Charles, also suff ered a broken neck and damage to his spinal cord after falling down a fl ight of stairs, returning home from visiting Camilla in

hospital. Both Charles and Camilla ended up in the National Spinal Injuries Centre at Stoke Mandeville Hospital.

In an eff ort to raise money for their care and the care of others aff ected by such injuries, Carmichael and a friend are competing in the Gobi March, a 250km self-supported footrace across the Gobi desert over seven days. Th is comes down to six marathons in as many days in searing heat, carrying all they need to survive on their backs. “I’m looking forward to it but it will be very tough. We’ll have some dark moments out there when we’ll question what we are doing, but the goal for us is just to cross the fi nish line.”

CFA members who would like to support Nick Carmichael’s cause can do so by sending money either to the Back-Up Trust via www.justgiving.com/Gobi2010 or directly for the benefi t of Camilla and Charles through www.friendsofcamillamilbankappeal.com

MEMBER PROFILE

INTERVIEW BY: MAHA KHAN PHILLIPS • PHOTOGRAPHY: ABI HARDWICK

7P R O F E S S I O N A L I N V E S T O R

Nick Carmichael, CFA, began his investment career as an associate in private equity at

Crédit Agricole Indosuez (now Calyon) in 2000 in London. “Finding the way to fi nance was perhaps slightly unusual, given that my degree was in French, but as long as you have a strong level of numeracy and analytical skills you can transfer that to many diff erent career paths,” he explains.

Carmichael joined the graduate recruitment scheme, and remained with the company that became Calyon until November 2006, during which time his career ranged from being a manager in distressed asset management to an associate in leveraged fi nance. “I did a graduate rotation at the bank and one of the small private equity funds off ered me a permanent role, which I jumped at. We had real closeness and proximity with the management teams and we were analysing alot of diff erent companies and looking at a huge variety of industries and businesses.”

Carmichael completed the CFA Program in 2007. “Th e CFA exams are a tough ask, I think. You need to work pretty hard and it’s challenging. But the knowledge I gained was very useful. Th e CFA curriculum lends itself very well to fund management, and even though my career has not been in fund management, there are some fundamentals that are exceptionally useful for private equity and leveraged fi nance.”

In November 2006 the team moved together to CIBC World Markets. Carmichael became director of European leveraged fi nance. Th en, in early 2008, CIBC closed down its European operation and part of the team moved to the Royal Bank of Canada, where Carmichael held a similar role. He left the job in July 2009. “I wanted to explore whether it would be possible to

Nick Carmichael, CFA Independent fundraiser, private equity

04-9 profile.indd 704-9 profile.indd 7 1/6/10 10:12:141/6/10 10:12:14

Gemma Game, CFA, completed a masters degree in Natural Sciences from

Cambridge University, but then, she says, “I realised that I didn’t want to work in a lab all day. I decided to explore diff erent careers, and see where else I could use my background in pharmacology.”

A summer internship at JP Morgan Asset Management, working with a portfolio manager responsible for a healthcare fund, showed Game that she could combine her passion for healthcare with a fund management career.” It was really exciting to realise you could be a specialist in the City in a sector where you have real passion,” she says.

Game joined Merrill Lynch Investment Managers’ graduate programme in 2001, working on the global equities team, with responsibility for the healthcare sector. During that time, she also became a CFA charterholder. “Studying and working a full time job was demanding, but the CFA Program was incredibly helpful in teaching me the basic foundations of investment management,” she explains.

In 2005 Game became a portfolio manager. “Th e more I managed money the more I realised the importance of getting your timing right. Healthcare is a complex, news fl ow driven sector and is constantly evolving – that’s what makes it interesting”

She says she loves looking at the most recent discoveries and clinical trial data, and spending time with chief executives who translate all that medical knowledge into something practical. In 2006, MLIM was merged into BlackRock, and Game continued in her role as a portfolio manager and healthcare specialist. In October 2007, she moved to AXA Framlington to run a healthcare fund as a senior portfolio manager.

“Healthcare will always be what I do. I love my current role; it’s global and takes me everywhere. Th is is a fascinating sector right now. Th e US has just reformed its healthcare system so the next few years it is going to be an evolving environment for all the companies we own. At the same time, globally, there is an incredible amount of investment in healthcare infrastructure in the developing world that off ers some fantastic opportunities.”

When she’s not working, Game loves music. She is a soprano with the Royal Choral Society, travelling globally with them on performances.

S U M M E R 2 0 1 08

Although he studied psychology at university, Stephen Peters, CFA, was always interested in fi nance.

His father had worked in the City, and he enjoyed investing his own money. “At university, I realised that psychology was a long and not particularly rewarding career path for me. So I applied for a graduate job in investment management, one that off ered a free lunch and not much else.”

Peters joined an IFA that is now Towry Law. “It was a two-year full time graduate scheme, and I rotated around the diff erent departments. I realised I wanted to do more fund research, but there wasn’t an opportunity at the fi rm.” Peters moved to Hewitt Associates in 2002, initially doing research on defi ned contribution schemes and then both fund manager and product research

Stephen Peters, CFA Investment trust analyst, Charles StanleyINTERVIEW BY: MAHA KHAN PHILLIPS • PHOTOGRAPHY: ABI HARDWICK

INTERVIEW BY: MAHA KHAN PHILLIPS • PHOTOGRAPHY: ABI HARDWICK

Gemma Game, CFAPortfolio manager, AXA Framlington

04-9 profile.indd 804-9 profile.indd 8 1/6/10 10:12:141/6/10 10:12:14

when the two teams were integrated.“It was a real eye opener. It’s amazing when you

are 22 years old and you don’t know anything, and you get a lot of the time of very senior fund managers. You get to know people and products very quickly.”

He initially focused on equities, but then his focus expanded to include other asset classes, such as hedge funds, private equity, currency and infrastructure. “Th e most important thing that I found was that the best fund managers were honest. A combination of over enthusiastic marketing departments and some less than brilliant fund managers could lead, three years down the line, with performance not turning out the way they wanted it to. Th e best fund managers did not try to tell you that they were something that they were not.”

He says it was an interesting time to be a consultant, with the industry going from being reactive to being proactive. “Th ere were banks, trying to sell LDI solutions and derivatives, and consultants were forced to increase their level of skill and knowledge.”

Peters decided to sit the CFA exam. “Historically, graduates always took the actuarial exams. What was being realised was that actuarial exams were great for people who wanted to be scheme actuaries but not as useful for those who wanted to be on the investment consulting side of the business.”

He says the qualifi cation has been helpful. “I was speaking to fund managers, all day, every day.

W W W . C F A U K . O R G

Stephanie Niven, CFA, entered the fund management industry after a summer internship with Goldman Sachs Asset Management in 2004. She was in the middle of completing a history degree at Oxford University. “History is all

about taking a great deal of information and distilling it, and the skills were transferable. I was very lucky to be placed in GSAM. I loved the team I was working for, and although I was supposed to rotate, I stayed!” she says.

After graduating, Niven joined the European active equity team full-time as an analyst, responsible for the materials and industrials sector. “Th e one thing that surprised me is that you are thrown in at the deep end. You don’t know what you know, and what you don’t know! You are expected to know things without anyone telling you, so you really have to be a self-starter.”

Niven sat the CFA exams early in her career. “It was encouraged to do the CFA. It was helpful because as an analyst in fund management, there wasn’t any formal training programme. Th e CFA became that training programme for us and we learnt things that we wouldn’t have otherwise.”

Niven began to focus on hedge funds and emerging markets, and ran a basket in

P R O F E S S I O N A L I N V E S T O R 9

MEMBER PROFILE

Stephanie Niven, CFAPortfolio manager, Javelin Capital INTERVIEW BY: MAHA KHAN PHILLIPS

the emerging markets long/short equity fund. In July 2009 she joined Javelin as part of a trio from the GSAM team. “We are still setting up our fund at the moment, but what we are doing is quite unusual. We want to understand what strategy works best and where, so we each have a diff erent approach within the fund. One colleague looks at tactical trading whereas I look at sectors from a fundamental point of view and try to understand when industries shift from being well behaved to trending. Another colleague looks at mean reverting stocks.”

When she is not working, Niven is a keen athlete. She was a British Universities National Champion in water polo, has completed three marathons and a number of triathlons, and is entered for Ironman Nice in June.

Having the knowledge that the CFA provides gave me a useful grounding to talk to fund managers about what they do, without actually having had the experience of being a fund manager.”

Peters says that eventually, he became frustrated with the time it took from doing investment research to actually implementing solutions for clients. “I decided to move on. I wanted to do an analyst role in a smaller organisation.”

He joined Charles Stanley in July 2007 and is responsible for all investment trust and closed-end fund research. “It is an interesting time to be in the sector. Th e demise of investment trusts has been predicted time and time again, but they keep re-inventing themselves.”

Peters has also started running money internally for the fi rm using a growth model and an income model. “So far the performance has been pretty good, so I’d like to continue to build a track record and hopefully make them into portfolios. I don’t run the funds against any benchmark. Th ey are relative return but not benchmark relative.”

Peters is married, with one daughter, with another baby due in September. He is a big cricket fan, and is currently learning Portuguese.

04-9 profile.indd 904-9 profile.indd 9 1/6/10 10:12:151/6/10 10:12:15

10 S U M M E R 2 0 1 0

PI – What are the challenges for growth in the current investment environment?

GARRETT-COX – With concerns still being expressed about the possibility of a double-dip recession, we believe that 2010 will be subdued in terms of growth in developed economies. Th e challenge is that so much of global growth stems from the US consumer and until we see a recovery in jobs and the housing market, both of which seem some way off , it is diffi cult to see how any of the current signs of increased consumer activity can be sustainable. Some Asian and emerging market economies will produce stronger growth fi gures but this will not be suffi cient to completely off -set the eff ect of the reduction in US consumer spending. From an equity investor’s perspective the growth challenge comes from maintaining the current positive earnings momentum, which will be the main driver of the equity market in the coming months.

KRISHNAN – Th ere are three main issues facing the developed economies, in particular. First, the fi nancial crisis highlighted the extent to which the previous 20 years of prosperity had depended on increasing leverage in the household sector across most of the western world. Th e process of rebuilding savings and paying down debt is

reducing the proportion of household income which can be spent. As well as diminished demand for credit, the supply of credit has been restricted by banks looking to rebuild capital bases. Th is issue may well be resolved more quickly given the advances in bank profi tability in the recovery. Last, economies are facing the challenge of unsustainable public sector debt paths given current entitlements and demographics. Whether this is resolved through austerity or higher real interest rates (or, as with Greece, both), the outcome is to depress trend growth in the coming years.

YOUNG – Challenges for global growth centre on three key adjustments – the easing of both internal and external imbalances between developed and emerging economies; the phased withdrawal of fi scal and monetary stimulus; and, the internal adjustment between the core and periphery in the euro-zone.

A benign workout would involve a multi-year appreciation in emerging currencies (particularly the yuan) and rising Asian interest rates; some

tightening of developed country fi scal policy along with relatively low interest rates to aid de-leveraging; and, a recognition from Germany that a euro-zone solution requires both retrenchment (lower labour costs and stricter fi scal discipline) from the periphery and expansion from the core (transfer payments and faster domestic demand growth).

So far there has been an improvement in external imbalances. Interest rate expectations are rising faster in the East and phased fi scal tightening is being discussed in the West. Savings ratios have adjusted upwards in the US and UK and private sector de-leveraging has moderated. Our central case is for the global economy to continue to improve, but at a diminishing pace by year-end.

However, a more malign adjustment would involve protectionism, a market-driven tightening in policy and political paralysis in the euro-zone. Greece has highlighted how markets can become impatient and political tensions remain; not least over China’s exchange rate policy. Recent market moves increase the risk of a malign outcome.

Navigating in diffi cult landscapes

In a complex investment environment, senior members of CFA UK discuss what the key obstacles are to growth and the

biggest challenges investors face

“Greece has highlighted how markets can become impatient and political tensions remain; not least over China’s exchange rate policy” ROBIN YOUNG

10-15 roundtable.indd 1010-15 roundtable.indd 10 1/6/10 09:49:021/6/10 09:49:02

W W W . C F A U K . O R G 11P R O F E S S I O N A L I N V E S T O R

ROUNDTABLE

KRISHNAN – It seems intuitive that with trillion-dollar bailout packages and quantitative easing, real production of goods and services cannot keep up and rising prices must be the consequence. But there are two issues with this argument. First, despite the explosion of narrow money (funds credited to banks by central bank activity), most Western economies are still seeing a deceleration in broad money – the measure most relevant to economic activity. Only if bank lending reaccelerates will broad money expansion resume, and at that point central banks will have to focus on stimulus withdrawal. Second, with central banks now focused on CPI objectives, infl ation manifests itself increasingly in asset prices – such as the housing bubble. Here there is scope for monetary policy and regulation to monitor and manage frothy capital markets – but at present they lack a rigorous theoretical rationale to guide this.

GARRETT-COX – Sub-trend economic forecasts and a signifi cant amount of spare capacity in the system point to a limited risk from the threat of infl ation in the UK over the medium term. Infl ation in the UK is around 3.7% which is above the upper band of the MPC’s stated range but the governor of the Bank of England is not concerned for the moment. In fact Alliance Trust is forecasting infl ation in the UK to peak at around the current levels and drift lower in the second half of the year as a number of one-off measures (including the return of VAT to 17.5%) drop out of the data.

PI – Is infl ation an issue and if so how should we be dealing with it?

YOUNG – Infl ation is an issue in the developing economies and, ultimately, will be a problem in the developed markets. Policymakers cannot aff ord to make a 1930s US, or 1990s Japan defl ationary policy mistake so are likely to err on the side of overly-loose monetary policy. BIERNAT – While infl ation is under control today and infl ationary pressures are likely to be subdued over the short term, the aggressive fi scal and monetary policies of the major central banks raise the risk of infl ation over the long term. Even as economic activity has begun to move positive, the risk of an economic setback or even a prolonged recession cannot be ignored. Over the next year the US and European central banks must begin to withdraw the massive liquidity that was extended to the markets in the crisis.

Never before in economic history has such massive stimulus been extended and economists are heavily split in their opinion on how the market will react to this stimulus being pulled back. To use an analogy from the space program, the question being asked by market strategists is will the US economy, the European economy and the world economy reach ‘escape velocity’ (suffi cient positive momentum) by the time the booster engines (extraordinary liquidity) are turned off .

As recent events in Greece have shown, economic risks may extend beyond the withdrawal of central bank liquidity. If Europe’s economic recovery suff ers a signifi cant setback, as a result of the sovereign debt crisis sparked by Greece’s problems, then the positive momentum in the remainder of the world’s economy may also fi zzle. Th e economic setback from the oil spill in the Gulf of Mexico may also pose an unexpected economic drag. In summary, 2010 will not be an easy time for investors. Th is is not to say it will be a year of negative returns, but most likely modest returns with relatively few great opportunities and many real risks.

“2010 will not be an easy time for investors. This is not to say it will be a year of negative returns but

likely modest returns with relatively few great opportunities and many real risks” JOE BIERNAT

10-15 roundtable.indd 1110-15 roundtable.indd 11 1/6/10 09:49:031/6/10 09:49:03

12 S U M M E R 2 0 1 0

PI – What about exchange rate volatility?

KRISHNAN – Exchange rates are back in focus, partly because here, as elsewhere, volatility has picked up with the crisis and since. But the other reason is that economic fundamentals now have more to say about FX movements. For years, with broadly similar economic policies and globalised product markets, FX volatility was more driven by trade fl ows than by investor judgements about the long-term prospects for an economy. But with even close neighbours coming out of the crisis in varying states of health, and a range of monetary and fi scal responses being deployed, macroeconomic fundamentals are back as a key driver of FX markets. We should expect this to continue, as many of the themes are long-term in nature. Investors will be best served by avoiding complacency about the contribution of currency to total returns, and remaining well diversifi ed internationally unless there is a compelling value case for a particular currency (and the patience needed to allow it to work!)

GARRETT-COX – When there is high degree of uncertainty concerning political stability, fi nancial market conditions and the global macro outlook, there will be exchange rate volatility. Th e lack of a clear winner in the UK general election put pressure on sterling but the Conservative/Lib Dem coalition is the best result as it has a chance of surviving intact through the end of the year. Th e markets will be cautiously optimistic about the news, but we do not expect a signifi cant bounce. Th e euro has endured a weak start to the year and may attract further selling pressure in the second half as the euphoria, following the announcement of the bail-out of the peripheral European countries, subsides. Th e US dollar is a net benefi ciary of the global uncertainty so we expect it to continue to do well. Finally, we may get some news of a Chinese revaluation which would boost demand for most of the Asian currencies including the yen.

YOUNG – Recent exchange rate volatility refl ects the huge underlying economic dislocations. Sterling, for example, has moved from being signifi cantly overvalued on a real (infl ation-adjusted) broad trade-weighted basis to being considerably undervalued as the UK economy moved from a fi nance-fuelled economy to one that requires a signifi cant lift from net exports. Th e benign workout outlined above would lead to lower exchange rate volatility as the world adjusts to a controlled appreciation in Asian currencies, some depreciation of the euro and a period of stability between the other developed currencies.

PI – Are emerging markets going to be the alpha producers of future, as some would suggest?

GARRETT-COX – Th ere are many ways of producing alpha in a global portfolio and we think that a process that encourages high conviction stock selection within a robust framework for asset allocation across developed as well as emerging markets is the key. For these markets to take on the role of sole alpha producers of the future they are going to have to do more than show higher growth characteristics. Th e de-coupling argument currently surrounding emerging markets is not a new story although it has become of greater focus as the divergence in growth between some emerging and developed markets widens. As we know from previous experience, there is a link between strong economic growth and relative outperformance from stock markets. However, the correlation is not as high as is assumed by the excess premium paid for certain emerging market stocks.

YOUNG – Th e secular backdrop remains supportive for emerging markets and if another ‘bubble’ is being blown then emerging equities (and commodities) are likely to be the key recipients. Over the past decade China has experienced near double-digit growth through a combination of rapid investment and export growth, aided by low real interest rates. However, China will need to re-orientate its economy from net exports to domestic (consumption) demand and contain infl ationary pressures. During this process interest and exchange rates need to rise and the extent of any mal-investment may come to the fore. Th e other BRICs have proved in the past that the top of the economic cycle often masquerades as secular high growth.

KRISHNAN – Th e argument that the baton of economic leadership has passed to emerging economies is compelling, given trends in demographics, credit

“For [emerging] markets to take on the role of sole alpha producers of the future they are going to have to do more than show higher growth characteristics” KATHERINE GARRETT-COX

10-15 roundtable.indd 1210-15 roundtable.indd 12 1/6/10 09:49:031/6/10 09:49:03

13P R O F E S S I O N A L I N V E S T O RW W W . C F A U K . O R G

ROUNDTABLE

expansion and productivity growth. As such, with Western economies facing slowing growth, emerging markets are already the most likely source of revenue growth for companies and exchange rate appreciation. We should expect emerging market assets to play an increasing role in global portfolios – not just equities, but bonds and alternatives as well. We will come to see emerging markets as largely emerged, and with that will come greater diff erentiation between diff erent regions and countries – increasing the scope for allocation alpha within the universe. At the same time, it would be foolish to forget that economic growth does not drive investment returns unless valuations are reasonable at the time of entry. Chasing the latest hot theme will be less rewarding than patient accumulation.

PI – Is this the end of an era for bonds?

YOUNG – No in the short-term; yes in the medium-term. Large negative output gaps, Greece-like austerity plans, memories of the Japan experience and continuing private sector de-leveraging are likely to keep bond yields contained for a while. However, the ultimate outcome is likely to be infl ation as policy makers try to avoid defl ation and fi nance public sector defi cits.

KRISHNAN – Two decades of disinfl ation have delivered exceptional returns to sovereign bonds, but have also left us with yields which are extremely low in a long-term historical context. Since yields are a good guide to medium-term nominal returns, it follows that only if defl ation arises will real returns from here be strong. Put another way, longer-term uncertainties about infl ation

and fi scal sustainability are not refl ected in today’s rates. Yet it would be a mistake to look only at developed sovereigns. Th e crisis exposed a bubble in non-government fi xed income, but the aftermath created remarkable opportunities in corporate bonds and convertibles which have not fully diminished. Similarly, yields in emerging market debt are high enough to allow attractive returns if, as seems likely in many cases, infl ation is now better managed than in the past.

GARRETT-COX – With the threat of a double-dip recession, infl ation falling and interest rates anchored for the time being at sub 1%, we are not at ‘the end of an era for bonds’. Investors should take a look at the last 15 years in the Japanese government bond market to get an idea of what could happen if growth remains sub-trend or the economy moves into a defl ationary environment. Th e overhang of UK government issuance to fund the rising defi cit is a signifi cant negative for the market and is one of the reasons that we believe corporate bonds will continue to be an attractive investment with an average yield on an investment grade bond at above 6%. We believe the outlook is mixed for gilt yields and therefore our strategy will be to actively manage the interest rate exposure of the underlying bonds in which we invest.

BIERNAT – Looking specifi cally at credit, while the market has made an enormous recovery from 2009 crisis levels, this recovery is more of a risk than an opportunity. Absolute returns from credit were in excess of 16% for 2009. European corporate spreads (as measured by IBOXX) have moved in to 150 bps versus the wides of 484 bps in March of

last year. On an absolute basis non-fi nancial yields are 3.5% versus a long-term average of 5.1%. Th e new issue market is robust with new issue premiums versus secondary cash spreads at minimal levels versus premiums of more than 100 bps points in the comparable period last year.

All is not well however with signifi cant doubts about the future of the fi nancial market despite very strong support from central banks and assurances from government offi cials. European T1 and T2 spreads are today 551 bps and 291 bps respectively. While this is an enormous recovery from 3,500 and 885 at the wide it’s a long way from 103 bps and 52 bps for T1/T2 spreads before the fi nancial crisis. Th e real quandary for fi xed income credit investors is how to position the portfolio from this point forward. Although credit spreads may have some room to tighten if economic conditions improve it is easy to see returns from credit turning negative in the event of a double dip recession. Compounding this dilemma is the very low level of interest rates. Most fi xed income investors do not want to be in largely fl oating instruments but any rise in rates will negatively impact returns. Even if economic conditions move in a favourable direction there could be signifi cant technical factors limiting or even eliminating further positive returns from the credit market.

PI – Where will returns come from over the next three years?

BIERNAT – It’s extraordinarily diffi cult to predict where returns will come from over the next 12 months let alone the next several years. Many markets appear to be either fully-valued or over-valued. Playing volatility will likely to be the source of returns for investors who have portfolios that can be shifted quickly. In the fi rst quarter of this year the US equity market sold off then rallied sharply to hit new cyclical highs despite sovereign debt concerns in Europe,

“Longer term uncertainties about infl ation andfi scal sustainability are not refl ected intoday’s rates” SUNHIL KRISHNAN

10-15 roundtable.indd 1310-15 roundtable.indd 13 1/6/10 09:49:031/6/10 09:49:03

14 S U M M E R 2 0 1 0

policy tightening in China and a surprise hike in the discount rate by the US Federal Reserve. Th e currency markets were choppy in the fi rst quarter and due to the continued fi nancial stress in Europe look to be as volatile for the remainder of the year. Emerging markets which have performed relatively well are likely to feel the weight of the Greek debt crisis. Government bonds may perform well over the short term as new government money is pumped into the fi nancial system as a result of the sovereign crisis but this money and previous funds must be withdrawn over the next several years.

GARRETT-COX – We are not in a normal economic recovery situation therefore it will not be as easy as it was in previous cycles to predict where the best returns will come from. We aim to retain a degree of fl exibility and implement an active asset allocation strategy as none of the regions or any single asset class off ers long-term consistent returns. We foresee that the interest rate environment and infl ation will be relatively benign going forward. We may see some spikes in high growth areas and we need to be vigilant about infl ationary pressure reoccurring, however, we think that the backdrop for investors is reasonably secure. We have a preference for companies that will benefi t from the Asian growth story, wherever they may be listed. In developed markets the ‘lower for longer’ regime from central banks will persist in the short term and equities will attract greater infl ows and potentially add further to market gains.

KRISHNAN – Our approach to medium-term allocation is to focus on the interaction of reasonable valuations and supportive economic fundamentals. Th is implies that equities will continue to off er returns of at least the historic average, although it is likely that volatility remains above the levels of three to six years ago. Sovereign bonds will remain challenged and may perform no better than cash on average. Emerging markets should outperform developed – especially in the context of bonds, and credit remains attractive relative to governments. Alternatives will have a useful diversifying role in portfolios – now that we have a better idea of when beta is disguised as alpha – though more limited leverage will probably reduce expected returns. But given the ongoing macro uncertainties, it is unlikely that a buy-and-hold strategy will be optimal. More sensitivity to market conditions and timing will be key, and our conversations with clients suggest that they are increasingly aware of this.

YOUNG – We are past the sweet spot of the economic cycle when all assets other than cash rise in value with low-grade credit, equities and cyclicals experiencing rapid gains. Th e next phase usually involves some consolidation in risk assets before a renewed, more modest and discerning rise as the economic cycle matures. Th e ultimate end-game is infl ation although, at the global level, this is probably two-three years away. Th is phase is usually associated with weak returns from equities and bonds.

SUNIL KRISHNAN, CFAPortfolio manager, BlackRock Multi-Asset Client Solutions group

ROBIN YOUNG, ASIPInvestment director, Aerion Fund Management

Sunil Krishnan, CFA, is a portfolio manager in the BlackRock Multi-Asset Client Solutions (BMACS) group, which is responsible for developing, assembling and managing investment solutions involving multiple strategies and asset classes. His service with the fi rm dates back to 2001, including his years with Merrill Lynch Investment Managers (MLIM), where he was fi nancial markets economist and co-manager of GTAA accounts. He holds an MSc in economics from the University of London and an MA degree, with fi rst class honours, in philosophy, politics and economics from Oxford University.

Robin Young, ASIP, is an investment director at Aerion Fund Management. He has over 25 years’ investment experience working initially as a bond fund manager for Friends Provident and at British Gas Pension Fund Management (now known as Aerion Fund Management). He joined the fi rm in 1995 as an economist. Following a sabbatical to study for a master’s degree in economics, he has, since 2000, focused on asset allocation.

JOE BIERNAT, CFAIndependent fi nancial consultant

KATHERINE GARRETT-COX, ASIPChief executive offi cer, Alliance Trust

Joe Biernat, CFA, is an independent fi nancial consultant. He was formerly chief investment strategist at European Credit Management (ECM) and a former head of its research department. Before this he was global head of credit research at BNP Paribas, co-head of global credit research at Deutsche Bank, and head of European credit research at Merrill Lynch. He was chairman of the CFA Society of the UK and a founding board member of the European High Yield Association.

Katherine Garrett-Cox, ASIP, joined Alliance Trust as chief investment offi cer in 2007, and was appointed chief executive offi cer in 2008. Her early career was spent with Fidelity Investments and UNI Storebrand before moving to Hill Samuel Asset Management. In 2000 she joined Aberdeen Asset Management and became chief executive of Aberdeen Asset Management. In 2004, she became chief investment offi cer for Morley Fund Management. She holds a BA degree in history from Durham University.

THE PANEL

10-15 roundtable.indd 1410-15 roundtable.indd 14 1/6/10 09:49:031/6/10 09:49:03

15P R O F E S S I O N A L I N V E S T O RW W W . C F A U K . O R G

Pension funds have been brought to their knees by falling asset prices, declining interest rates, a series of legislative and

regulatory changes all leading to higher costs. Oh, and the inconvenient truth that we are all living longer. It may be too late to save the defi ned benefi t fund, but it is not too late to learn some very important lessons from the experience of the last decade. Th e best practice model of today is badly fl awed and based on some totally unrealistic assumptions.

When I started out in this business 35 years ago investment management agreements were encapsulated in a one-and-a-half page letter and almost every mandate was ‘balanced’, investing across multiple asset classes. We still manage £12 billion of traditional balanced accounts. Mind you, the world was a lot simpler then and we limited our asset class defi nitions to gilts, UK

and overseas equities, and property. Th e fi rst and most important decision we made was how much to invest in our four asset classes and there was a real willingness to change the asset mix in a meaningful way.

WHAT WENT WRONG?All this began to change with the passing of ERISA (Th e Employee Retirement Income Security Act) in the United States in 1974. Th is was a powerful catalyst for the growth of the investment consulting industry, which in turn set about redefi ning the best practice model to the standard we are familiar with today:• Conduct an asset/liability study to

determine a strategic benchmark.• Construct an implementation plan

around that benchmark.• Conduct a manager search to fulfi l

the implementation plan.

• Fund and monitor managers.• Repeat every three to fi ve years.

On the face of it, this was an appealing model built around some ap parently common sense principles:• No one can time markets. • No single manager could be the best

at everything so managers would be chosen for their capabilities in specialist areas.

• While markets were not perfectly effi cient, some areas were clearly more effi cient than others. It made sense to use one’s alpha risk budget in areas where rewards were likely to be greatest. How could anyone fi nd fault with

this model? Well, it is riddled with problems. Th is article looks at these, starting with the least important and working up to the really big howlers. We conclude by proposing a better best practice model.

The best practice model of today is fatally fl awed, says Alan Brown, FSIP. It is time to concentrate on what is

important rather than what is (relatively) easy

BY: ALAN BROWN, FSIP

Shaking the trees (or re-thinking the basics)

EXECUTIVE SUMMARY• The current best practice model is

based on unrealistic assumptions• The growth in asset classes has

introduced greater complexity, making changes to portfolio structure diffi cult and adding signifi cant additional costs

• You can’t pay pensions out of relative returns; funds need to be more focused on what really matters, the liabilities

© A

RT

GL

AZ

ER

FEATURE: BEST PRACTICE

15-18 best practice.indd 1515-18 best practice.indd 15 1/6/10 09:30:481/6/10 09:30:48

16 S U M M E R 2 0 1 0

Inde

x R

etur

ns S

&P

500

0

500

1,000

1,500

2,000

2,500

3,000Fully invested Miss +/- 100 days

1964

1969

1974

1979

1984

1989

1994

1999

2004

2008

STATS.

COMPLEXITY AND COSTOver time, the level of complexity has grown dramatically. Our defi nitions of asset classes have ballooned from the four that I started out with to include private equity, infrastructure, hedge funds, currency, credit, emerging market debt and equity. And within a single asset class we sub-divide again into large, small, growth and value. Th is makes changes to portfolio structure diffi cult to implement and layers on signifi cant additional costs. If all of this was being compensated for by superior returns, all well and good, but looking at returns at the fund level suggests that any benefi ts being earned at the specialist level are being eroded through infl exible asset allocation and higher costs. It is the complexity and associated high costs and infl exibility of such structures we dislike, not the high degree of diversifi cation, which we applaud.

THE 80:20 RULEToday’s best practice model devotes most of its eff ort to controlling risks from the actual portfolio to the benchmark that came out of the asset liability study. Only intermitently, every three to fi ve years, do we manage the risks from the benchmark to the liabilities when we redo our asset liability work. Yet the lesson of the past 10 years is that the risks from the actual portfolio to the strategic benchmark are small, whereas the risks from the strategic benchmark to the liabilities are large.

In short, we have the 80:20 rule back to front. By spending most of our time worrying about market benchmark relative returns, we are missing the point that you can’t pay pensions out of relative returns; we need to be much more focused on the benchmark that really matters, the liabilities. As interest rates have declined over the last 25 years, pension liabilities have ballooned. By holding assets of much shorter duration, we missed out on substantial compensating increases in asset values.

OUR RISK APPETITE NEVER CHANGESImplicit in a static strategic benchmark is that our risk appetite doesn’t change even as our wealth changes or as return expectations change. Th is makes no sense at all. Surely we can all agree that our risk appetite should respond to changing return prospects and surely most of us will acknowledge that our risk appetite does change as our wealth rises or falls, even if the manner in which it changes will be diff erent for diff erent investors.

As one starts to think of risk in a more dynamic sense we fi nd ourselves having to think of the investment management problem in a much more holistic way. Should our risk appetite then be governed more by changes in our funding ratio or changes in return prospects? Th e answer will depend on the risk preferences of the trustees and this is likely to be conditioned on the strength of the implied covenant with the fund sponsor and the regulatory environment the fund operates in.

If the implied covenant with the fund sponsor is strong, then it is possible that trustees will not feel obliged to reduce risk budgets as funding ratios decline. But if the implied

0

500

1,000

1,500

2,000

2,500

Inde

x R

etur

ns S

&P

500

Fully invested Miss +/- 100 days

1964

1969

1974

1979

1984

1989

1994

1999

2004

2008

FIGURE 1: US EQUITY RETURN GRAPH

FIGURE 2: US EQUITY RETURN GRAPH

covenant is weak or the regulatory environment harsh, trustees may well feel that they have no choice in the face of declining funding ratios other than to reduce risk budgets and so limit potential further declines in wealth. We should never forget that asset allocation overwhelmingly determines the return earned on a fund, typically accounting for over 90% of the outcome.

BUT WE CAN’T TIME MARKETS, CAN WE?It is often held out that it is time in the markets that counts and any attempt to time markets is doomed to failure. To provide support for this argument one often sees charts of returns from an index set against returns from the same index minus just the top 10 days.

Th e argument goes that since you can’t possibly know when the best days will be and the price for

Source: Global fi nancial data, Schroders, nominal terms, no dividends

15-18 best practice.indd 1615-18 best practice.indd 16 1/6/10 09:30:481/6/10 09:30:48

W W W . C F A U K . O R G P R O F E S S I O N A L I N V E S T O R 17

missing them is so high, you had better stay fully invested. Of course no one operates a daily asset allocation policy. So what happens if you look at returns where you come out of the market 100 days before a top 10 day and go back in 100 days after? Th is equates to a 200 day investment horizon, or a little over nine months, a rather more realistic period.

Th e picture completely reverses and you make substantial gains by missing the 10 best days! I present this not as a case for market timing but to demonstrate that you can prove what you want if you torture the data long enough.

However, I will make an argument shortly that we can say something about equity and other markets, which is better than the very static return assumptions used in asset liability modelling. First though lets look at how eff ective or not asset/liability modelling has been.

ASSET/LIABILITY MODELLINGTh e great risk with modelling is that one can get caught up in the sophistication of the model and the precision of the numbers that emerge. Yet the ‘GIGO’ principle holds: garbage in, garbage out. Th e return assumptions used are of course critical. Typically an A/L model will use something close to the current redemption yield as the forecast for bond returns, and for equities something like a Gordon model. Th e Gordon model simply says that the long-run real return from equities will equal the current dividend yield plus the long-run growth rate. Th e idea is that in the very long run returns are dominated by income which dwarf changes in valuation. Th e current dividend yield is of course observable, and the long-run growth is usually derived from looking at long-run historical growth rates in earnings or GDP.

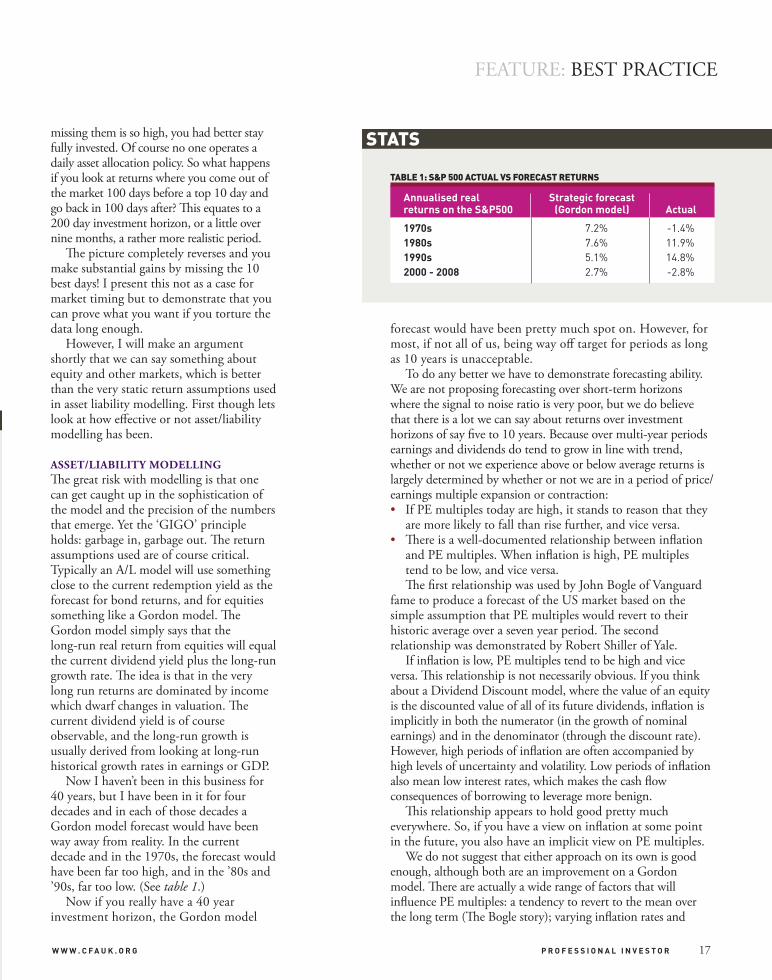

Now I haven’t been in this business for 40 years, but I have been in it for four decades and in each of those decades a Gordon model forecast would have been way away from reality. In the current decade and in the 1970s, the forecast would have been far too high, and in the ’80s and ’90s, far too low. (See table 1.)

Now if you really have a 40 year investment horizon, the Gordon model

Annualised real Strategic forecastreturns on the S&P500 (Gordon model) Actual

1970s 7.2% -1.4%1980s 7.6% 11.9%1990s 5.1% 14.8%2000 - 2008 2.7% -2.8%

STATS.

TABLE 1: S&P 500 ACTUAL VS FORECAST RETURNS

forecast would have been pretty much spot on. However, for most, if not all of us, being way off target for periods as long as 10 years is unacceptable.

To do any better we have to demonstrate forecasting ability. We are not proposing forecasting over short-term horizons where the signal to noise ratio is very poor, but we do believe that there is a lot we can say about returns over investment horizons of say fi ve to 10 years. Because over multi-year periods earnings and dividends do tend to grow in line with trend, whether or not we experience above or below average returns is largely determined by whether or not we are in a period of price/earnings multiple expansion or contraction:• If PE multiples today are high, it stands to reason that they

are more likely to fall than rise further, and vice versa.• Th ere is a well-documented relationship between infl ation

and PE multiples. When infl ation is high, PE multiples tend to be low, and vice versa.Th e fi rst relationship was used by John Bogle of Vanguard

fame to produce a forecast of the US market based on the simple assumption that PE multiples would revert to their historic average over a seven year period. Th e second relationship was demonstrated by Robert Shiller of Yale.

If infl ation is low, PE multiples tend to be high and vice versa. Th is relationship is not necessarily obvious. If you think about a Dividend Discount model, where the value of an equity is the discounted value of all of its future dividends, infl ation is implicitly in both the numerator (in the growth of nominal earnings) and in the denominator (through the discount rate). However, high periods of infl ation are often accompanied by high levels of uncertainty and volatility. Low periods of infl ation also mean low interest rates, which makes the cash fl ow consequences of borrowing to leverage more benign.

Th is relationship appears to hold good pretty much everywhere. So, if you have a view on infl ation at some point in the future, you also have an implicit view on PE multiples.

We do not suggest that either approach on its own is good enough, although both are an improvement on a Gordon model. Th ere are actually a wide range of factors that will infl uence PE multiples: a tendency to revert to the mean over the long term (Th e Bogle story); varying infl ation rates and

FEATURE: BEST PRACTICE

15-18 best practice.indd 1715-18 best practice.indd 17 1/6/10 09:30:491/6/10 09:30:49

18 S U M M E R 2 0 1 0

interest rates (Th e Shiller story); higher or lower perceived equity market growth potential; changing accounting standards; impact of leverage/deleveraging.

We use these as examples only. Quite likely you, the reader, can add to this list.

TAKING A VIEW – A BETTER BEST PRACTICE MODELSo, if we are to take a more dynamic view of asset allocation, how are we to do this? First, we distinguish between dynamic asset allocation (DAA) and tactical asset allocation (TAA). TAA approaches tend to be quite short-term, high turnover strategies. Th e signal to noise ratio over short horizons is very poor and these strategies try to make up for that by having high breadth through high turnover and many moving parts.

DAA takes a much more medium term view. It is an approach which remains focused on the real world outcome a fund is trying to achieve. So, for example, if you were trying to earn a return of infl ation +5%, you might consider the following list of assets (again not exclusive) as having the potential to deliver the desired outcome: quoted equity, private equity, high yield, emerging market debt, property, infrastructure, hedge funds, commodities.

Most likely you would not consider investment grade debt as a candidate.

What we propose is that one continually appraises likely future returns of these asset classes against whether they are likely to deliver a return greater than or equal to infl ation +5%. If the answer is yes, they remain a candidate asset class; if the answer is no, they are removed or scaled right back. And if an asset, such as investment grade debt, not normally a candidate asset class, off ers returns in excess of the required threshold (as investment grade off ered in Q4 ’08 and Q1 ’09), then it gets added to the list. Now from the eligible list of assets, we go

on to construct a suitably well-diversifi ed portfolio.

Assets are continually appraised against the desired real world outcome and are included or excluded based on an assessment of whether realistically they meet the required threshold.

What if very few assets qualify? Th ere may be a time when there is a generalised asset price bubble so that most risky assets are overpriced and are off ering very low forward looking returns. Th e analogy here is of a tide going in and out. If you have been pushed well up the beach on the back of a big wave, as the wave retreats your goal should be not to get sucked all the way back down again. Th at is the time to settle for hanging on to the ground made until asset prices have retreated to more reasonable levels.

Is this a high turnover strategy? Not especially. Over the last decade there would probably have been only a few major calls that one would have wanted to make, but they would have made a big diff erence. Equities overvalued at the end of the ’90s. Credit undervalued Q4 ’08 and Q1 ’09. Long dated government bonds overvalued now.

You would probably have called the top in equities at the end of the ’90s a year or two early. What then? It is true that an investment approach which is materially diff erent to the consensus is bound to have its uncomfortable moments. However, if the approach is sensible one needs to have a governance budget which allows for an investment committee to stand fi rm during the diffi cult times. Second, the portfolio should be suffi ciently diversifi ed at all times that one is not a hostage to a single investment decision.

CONCLUSIONFocusing on market related benchmarks, rather than the real world outcomes we

PROFILE – FACT BOX

Alan Brown, FSIPCareer highlights: Alan Brown, FSIP, serves as chief investment offi cer, executive director and member of group management committee at Schroders. He joined Schroders in 2005 and was appointed to the board in July 2005. Between 1974 and 1995, he worked at Morgan Grenfell, Posthorn Global Asset Management, and PanAgora Asset Management before joining State Street Global Advisors where he served as group chief investment offi cer.

“...the industry has behaved largely like a dear caught in the headlights”

desire has cost us dearly. It has led to overly complex and costly structures.

By concentrating on market related risk measures we have largely ignored the huge risks we have assumed with our pools of capital when measured against their liabilities.

During the roller coaster ride of the last 10 years, the industry has behaved largely like a deer caught in the headlights. Not to have changed asset allocations in the face of such dramatic changes in pricing seems bizarre.

Th e idea that we cannot make a reasonable stab at forecasting whether returns will be above or below our required target is simply not right.

We can, and simply must do better. A return to a simpler world, where we concentrate on what is important rather than what is (relatively) easy would be a good start.

15-18 best practice.indd 1815-18 best practice.indd 18 1/6/10 09:30:491/6/10 09:30:49

19P R O F E S S I O N A L I N V E S T O RW W W . C F A U K . O R G

To have a reasonable chance of assessing the future, it is essential to understand the past. We are just recovering

from the worst recession for 80 years and investors wishing for future success need therefore to be clear about the causes of this collapse.

Asset bubbles, excesses and imbalances in international savings, and China’s exchange rate have all been justly blamed for our present troubles. Seeing them as separate and distinct issues is common, unjustifi ed and pernicious. It is, for example, often claimed that it is not the renmimbi, but the lack of US savings that is the problem. Such statements treat the various imbalances as if they were separate and unconnected, which they are not.

It is fair and reasonable that both individuals and countries should be free to decide to save whatever proportion of their incomes seems to them to be right. However, if intentions to save exceed intentions to invest, they will be thwarted by a fall in incomes and output, causing widespread unemployment. It is generally agreed that fi scal and monetary policies should be introduced to off set this. But if the

countries that have the excess savings rely on the rest of the world to take the necessary off setting action, the result will not be fair and reasonable, as the cost of thwarting the aggregate excess of savings intentions will fall on some populations and not on others.

If the required ex-post balance between savings and investment was achieved by higher investment, there would probably be no serious problem. Th e additional investment would boost future labour incomes as well as profi ts. In the corporate sector labour takes about 70% of the gross incremental return from additional investment so, despite the higher fl ow of income which would, in the future, fl ow from the importer of capital to the exporter, the recipients would still be large net gainers from the investment fl ow. If, however, the adjustment comes through the thwarting of savings intentions, then there will be a fall, rather than a rise, in the future incomes of the capital importing countries.

Leaving individuals and countries to save whatever proportion of their incomes they choose is not always therefore fair and reasonable. It can create huge problems if countries with current

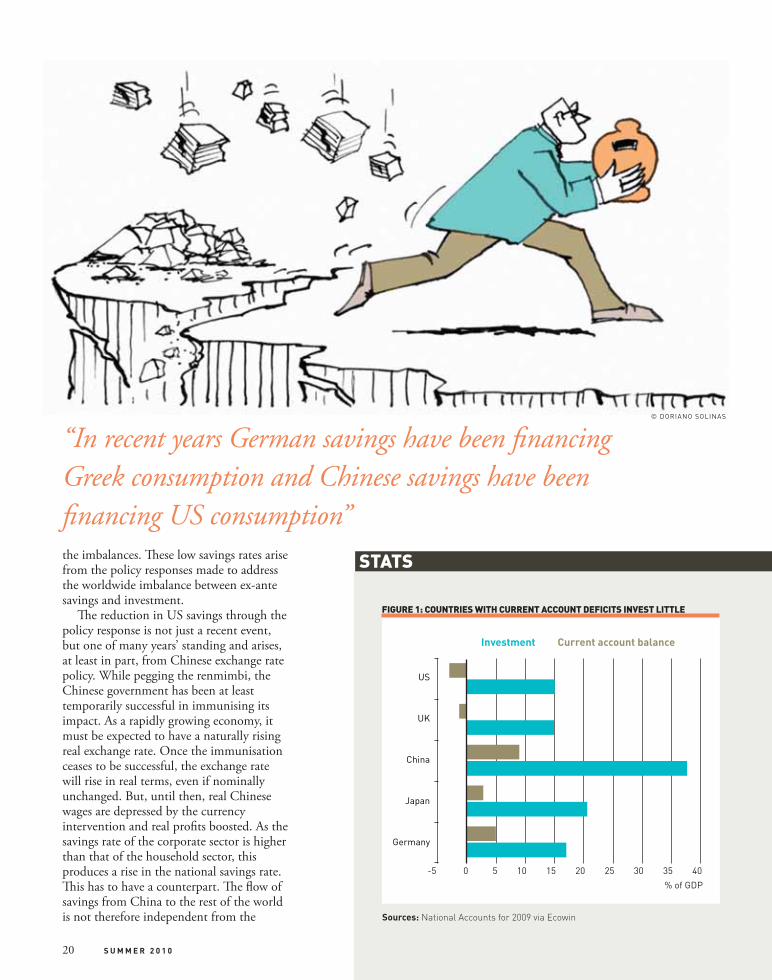

account defi cits have low domestic savings rates and this has been the case in recent years, both within the eurozone, whereby German savings have been fi nancing Greek consumption, and internationally, where Chinese savings have been fi nancing US consumption. I show in fi gure 1 how the UK and US have combined low domestic investment ratios with current account defi cits, while China, Germany and Japan, with their high investment ratios, have nonetheless run current account surpluses.

UNFAIR DISTRIBUTIONTh e massive fi scal stimuli that have been introduced worldwide have been successful in moderating the rise in unemployment and the loss of income and output, but this has been achieved by reduced savings rather than boosted investment. Th e burden has also been unfairly distributed between countries. It is not therefore sensible to claim that it is low US savings that is to blame for

The reasons for the recent fi nancial crisis are legion, says Andrew Smithers. It is wrong, however, to treat the various problems as separate and unconnectedBY: ANDREW SMITHERS

International savings and investment in the balance EXECUTIVE SUMMARY

• Leaving individuals and countries to save whatever proportion of their incomes they choose is not always fair and reasonable

• The fl ow of savings from China to the rest of the world is not independent from the country’s exchange rate policy, but is one of its results

• The unwillingness of countries with savings surpluses, and those with defi cits, to adjust their policies in the desired direction suggests that the outlook for the world economy is far from rosy

FEATURE: INVESTMENT

19-21 investment.indd 1919-21 investment.indd 19 1/6/10 09:32:251/6/10 09:32:25

S U M M E R 2 0 1 020

STATS.the imbalances. Th ese low savings rates arise from the policy responses made to address the worldwide imbalance between ex-ante savings and investment.

Th e reduction in US savings through the policy response is not just a recent event, but one of many years’ standing and arises, at least in part, from Chinese exchange rate policy. While pegging the renmimbi, the Chinese government has been at least temporarily successful in immunising its impact. As a rapidly growing economy, it must be expected to have a naturally rising real exchange rate. Once the immunisation ceases to be successful, the exchange rate will rise in real terms, even if nominally unchanged. But, until then, real Chinese wages are depressed by the currency intervention and real profi ts boosted. As the savings rate of the corporate sector is higher than that of the household sector, this produces a rise in the national savings rate. Th is has to have a counterpart. Th e fl ow of savings from China to the rest of the world is not therefore independent from the

-5 0 5 10 15 20 25 30 35 40

US

UK

China

Japan

Germany

Investment Current account balance

% of GDP

FIGURE 1: COUNTRIES WITH CURRENT ACCOUNT DEFICITS INVEST LITTLE

“In recent years German savings have been fi nancing Greek consumption and Chinese savings have been fi nancing US consumption”

Sources: National Accounts for 2009 via Ecowin

© DORIANO SOLINAS

19-21 investment.indd 2019-21 investment.indd 20 1/6/10 09:32:251/6/10 09:32:25

21P R O F E S S I O N A L I N V E S T O RW W W . C F A U K . O R G

PROFILE – FACT BOX

Andrew SmithersCareer highlights: Andrew Smithers is chairman and founder of Smithers & Co, an adviser to investment managers on international asset allocation. Prior to starting the fi rm in 1989, he was at SG Warburg from 1962 to 1989. He is co-author of Valuing Wall Street with Stephen Wright, published in 2000, and Japan’s Challenges for the 21st Century with David Asher, published in 1999. His latest book Wall Street Revalued – Imperfect Markets and Inept Central Bankers was published by John Wiley & Sons in July 2009.

country’s exchange rate policy, but is one of its results.