program - caribe federal credit union · president’s report i. ... lisa v. rodríguez sales and...

TRANSCRIPT

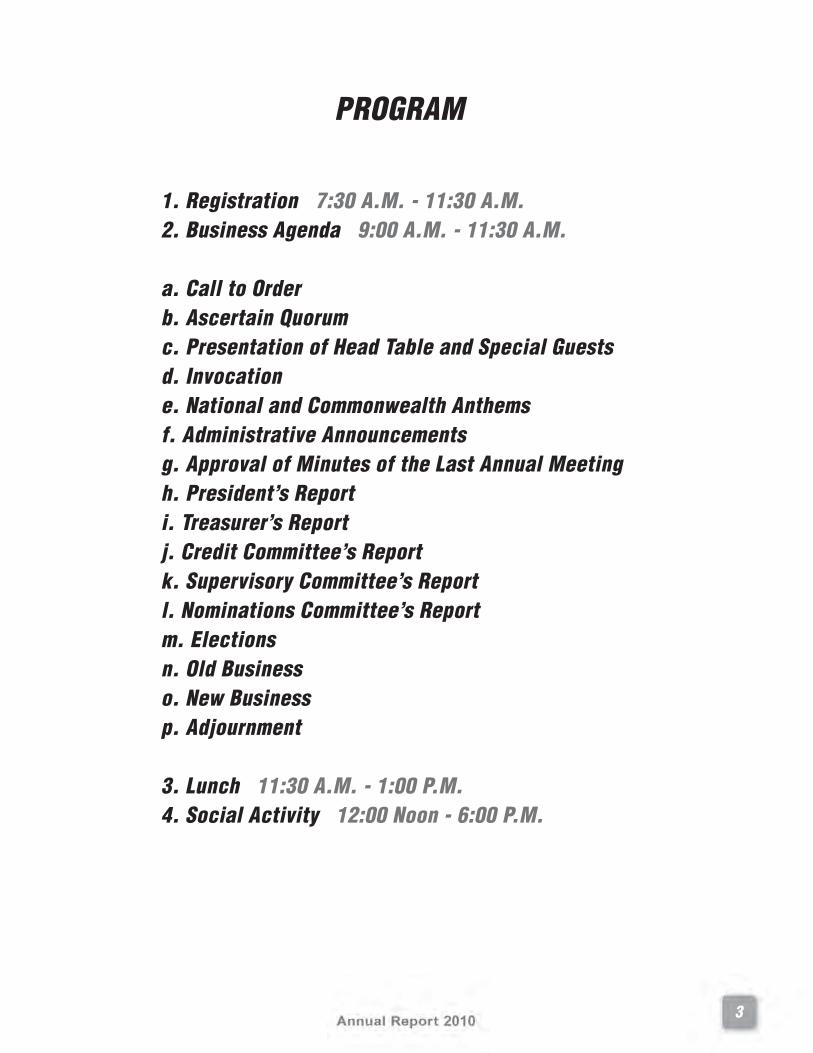

PROGRAM

1. Registration 7:30 A.M. - 11:30 A.M.2. Business Agenda 9:00 A.M. - 11:30 A.M.

a. Call to Orderb. Ascertain Quorumc. Presentation of Head Table and Special Guestsd. Invocatione. National and Commonwealth Anthemsf. Administrative Announcementsg. Approval of Minutes of the Last Annual Meetingh. President’s Reporti. Treasurer’s Reportj. Credit Committee’s Reportk. Supervisory Committee’s Reportl. Nominations Committee’s Reportm. Electionsn. Old Businesso. New Businessp. Adjournment

3. Lunch 11:30 A.M. - 1:00 P.M.4. Social Activity 12:00 Noon - 6:00 P.M.

3

WELCOME TO THE FIFTY NINETH ANNUAL MEETING OF

CARIBE FEDERAL CREDIT UNIONHELD THIS 5TH DAY OF JUNE 2011

AT THE CARIBE HILTON HOTEL & CASINOSAN JUAN, PUERTO RICO

In the occasion of our 59th Annual Meeting we take special pleasure in greeting you as we meet again, to fulfill our legal regulations as a federal credit union and to share, as co-workers, in the examination of our yearly, financial and service report. Paramount among our responsabilities at this time, is the election of a Board of Directors, which will direct the activities of the credit union in accordance with the law.

Your Credit Union is growing in size, services and technology. We must keep up with the times while striving to offer our members, the best possible service in the most favorable terms.

Thank you for joining us in celebrating Caribe Federal Credit Union’s 60th Anniversary.

Board of Directors Caribe Federal Credit Union

5

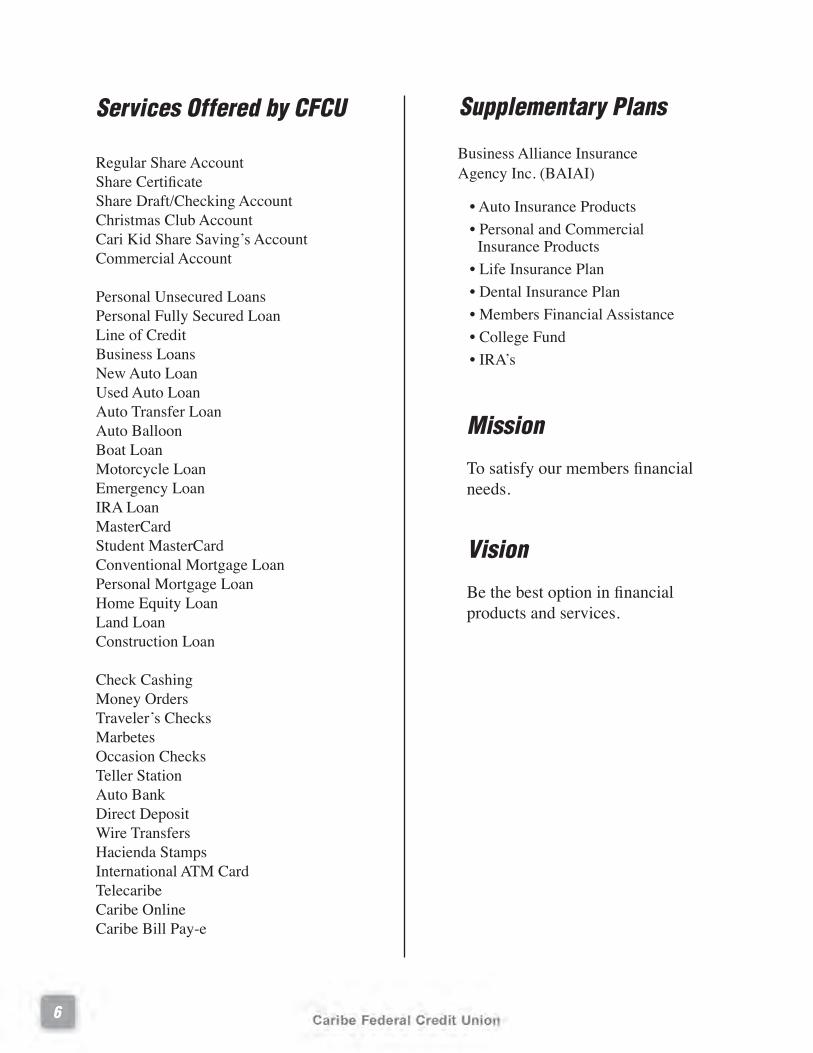

Business Alliance Insurance Agency Inc. (BAIAI) • Auto Insurance Products • Personal and Commercial Insurance Products • Life Insurance Plan • Dental Insurance Plan • Members Financial Assistance • College Fund • IRA’s

6

Regular Share Account Share Certificate Share Draft/Checking Account Christmas Club AccountCari Kid Share Saving’s Account Commercial Account

Personal Unsecured Loans Personal Fully Secured Loan Line of Credit Business Loans New Auto Loan Used Auto Loan Auto Transfer Loan Auto Balloon Boat Loan Motorcycle Loan Emergency Loan IRA Loan MasterCard Student MasterCard Conventional Mortgage Loan Personal Mortgage LoanHome Equity Loan Land Loan Construction Loan

Check CashingMoney Orders Traveler’s Checks Marbetes Occasion Checks Teller Station Auto Bank Direct Deposit Wire TransfersHacienda Stamps International ATM Card Telecaribe Caribe Online Caribe Bill Pay-e

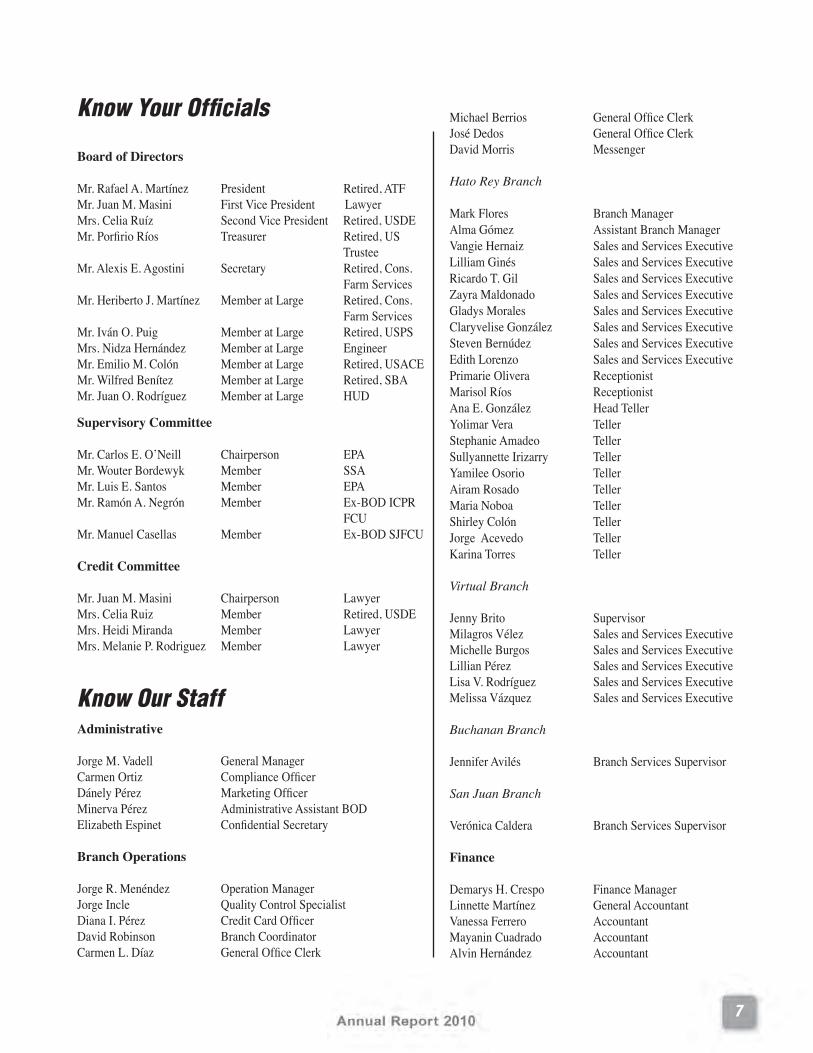

Michael Berrios General Office Clerk José Dedos General Office Clerk David Morris Messenger

Hato Rey Branch

Mark Flores Branch Manager Alma Gómez Assistant Branch Manager Vangie Hernaiz Sales and Services Executive Lilliam Ginés Sales and Services Executive Ricardo T. Gil Sales and Services Executive Zayra Maldonado Sales and Services Executive Gladys Morales Sales and Services Executive Claryvelise González Sales and Services Executive Steven Bernúdez Sales and Services Executive Edith Lorenzo Sales and Services Executive Primarie Olivera Receptionist Marisol Ríos ReceptionistAna E. González Head Teller Yolimar Vera Teller Stephanie Amadeo TellerSullyannette Irizarry Teller Yamilee Osorio Teller Airam Rosado Teller Maria Noboa TellerShirley Colón Teller Jorge Acevedo Teller Karina Torres Teller

Virtual Branch

Jenny Brito Supervisor Milagros Vélez Sales and Services ExecutiveMichelle Burgos Sales and Services Executive Lillian Pérez Sales and Services Executive Lisa V. Rodríguez Sales and Services Executive Melissa Vázquez Sales and Services Executive

Buchanan Branch

Jennifer Avilés Branch Services Supervisor San Juan Branch

Verónica Caldera Branch Services Supervisor

Finance

Demarys H. Crespo Finance Manager Linnette Martínez General Accountant Vanessa Ferrero Accountant Mayanin Cuadrado AccountantAlvin Hernández Accountant

Know Your Officials

Board of Directors

Mr. Rafael A. Martínez President Retired, ATF Mr. Juan M. Masini First Vice President Lawyer Mrs. Celia Ruíz Second Vice President Retired, USDEMr. Porfirio Ríos Treasurer Retired, US Trustee Mr. Alexis E. Agostini Secretary Retired, Cons. Farm ServicesMr. Heriberto J. Martínez Member at Large Retired, Cons. Farm Services Mr. Iván O. Puig Member at Large Retired, USPS Mrs. Nidza Hernández Member at Large EngineerMr. Emilio M. Colón Member at Large Retired, USACE Mr. Wilfred Benítez Member at Large Retired, SBA Mr. Juan O. Rodríguez Member at Large HUD

Supervisory Committee

Mr. Carlos E. O’Neill Chairperson EPA Mr. Wouter Bordewyk Member SSA Mr. Luis E. Santos Member EPA Mr. Ramón A. Negrón Member Ex-BOD ICPR FCUMr. Manuel Casellas Member Ex-BOD SJFCU

Credit Committee

Mr. Juan M. Masini Chairperson Lawyer Mrs. Celia Ruiz Member Retired, USDE Mrs. Heidi Miranda Member LawyerMrs. Melanie P. Rodriguez Member Lawyer

Know Our Staff Administrative Jorge M. Vadell General Manager Carmen Ortiz Compliance Officer Dánely Pérez Marketing OfficerMinerva Pérez Administrative Assistant BOD Elizabeth Espinet Confidential Secretary

Branch Operations Jorge R. Menéndez Operation ManagerJorge Incle Quality Control Specialist Diana I. Pérez Credit Card Officer David Robinson Branch CoordinatorCarmen L. Díaz General Office Clerk

7

Know Our Staff Loan José E. Febres Loan Manager Emma Y. Márquez Mortgage Processing Specialist Nereida Rivera Mortgage Processing Specialist Rubelisse Quiñones Loan Clerk

Collections Sol M. Morales Collection Manager Daisy I. Nieves Collection Officer Angel Aponte Collection OfficerJulio Ostalaza Collection Officer

ITS

Hilda Buriticá IT Manager Angel R. Escudero Network Administrator Ronald Cancel IT Programmer Specialist IILuis Vázquez IT Programmer Specialist I Georgie Mera IT Help Desk Specialist

BAIA

Victor Rosario Acting General ManagerLourdes Campos Administrative Assistant

8

MINUTES OF THE 58th ANNUAL MEETINGJUNE 6, 2010

The 58th Annual Meeting of Caribe Federal Credit Union (CFCU) was held at the Wyndham Río Mar Beach Hotel, Río Grande, P.R., on Sunday, June 6, 2010.

ADMINISTRATIVE ANNOUNCEMENTSSecretary of the BOD and Activities Committee President, Celia A. Ruíz presented the administrative announcements concerning the annual meeting and the social activity to all the members present, followed by a raffle for the “early bird” attendees.

QUORUM DETERMINATION AND CALL TO ORDERSecretary Celia A. Ruíz, certified that quorum was established with 189 members present. Chairman Emilio M. Colón called the meeting to order at 9:00 A.M. with a warm and sincere welcome to everyone present at the annual meeting.

Chairman of the Board, Emilio M. Colón, expressed his appreciation to all the members and special guests for their early attendance and wished everyone a pleasant experience at the annual meeting. Mr. Colón presented all the members of the Board, General Managers of Caribe Federal Credit Union (CFCU) and Business Consortium Alliance, Inc. (BCA).

The National Anthems of the Commonwealth of Puerto Rico and the United States of America were played. All members held a moment of silence in memory of the members who had passed away. Mr. Jorge Darío Ortíz delivered the invocation and the dedication of the 58th Anniversary.

MINUTES:The Chairman announced last year’s Annual Meeting minutes for consideration by the members. Since no comments or changes were proposed the minutes, they were approved unanimously without opposition. CHAIRMAN’S REPORT The Chairman commenced his 2009 report highlighting the main factors that continue to affect the global and local economy. He informed that modifications had to be made to CFCU’s strategic plan in order to maintain competitiveness. The most important areas that were identified as key factors were the increase of the net income, the reduction of operational costs, the increase of technology and the reduction of delinquent loans. The Chairman mentioned that CFCU had implemented strategies to expand services to members by the creation of Business Consortium Alliance, Business Alliance Insurance Agency and the alliances made with third party vendors such as Univeral Life, Mapfre, Delta Dental and Optima Insurance that are offering CFCU’s members competitive insurance programs that cover autos and properties, home assistance and a variety of health insurance products. He also presented statistical information on CFCU’s investments on its subsidiaries.

He informed that NCUA had increased the member’s account insurance from $100,000 to $250,000

9

per account which cost CFCU more than $240,000 per year.

The Chairman concluded his report informing that the main goals of the credit union are to improve member’s services, to reduce charge off on bad loans and to increase revenues. The Chairman encouraged members to continue to use the Home Financial Services and other automated services.

EMPLOYEES RECOGNITION PROGRAMA special recognition for employees who exceeded their 2009 evaluations was held. TREASURER’S REPORTTreasurer Porfirio Ríos welcomed everyone present. He began his presentation with CFCU’s financial situation for year 2009, including a comparison of the year 2008 financial situation. The financial statements were consolidated with CFCU’s subsidiary BCA and have been audited by Zayas, Morazzani & Co. CPA Auditors firm.

The Treasurer indicated that the financial statements have been available to members for their review since May 14, 2010 and expressed that year 2009 had been a year of great challenges especially for the credit unions. He said that during 2009, Puerto Rico and the United States has been enduring one of the worst periods of economic recession in the history that has affected adversely the financial industries. The Federal Reserve maintained low interest rates in the effort to help the financial industries. Bankruptcies and delinquencies are on the rise in all the banks and credit unions, where CFCU had to take aggressive measures to increase the collection efforts to avoid financial difficulties. The real estate and the automobile industry also were adversely affected by the recession.

Moreover, NCUA created a strategy to stabilize the Corporate Credit Union system which is an organization that provides services to the credit unions, which imposes that credit unions have to contribute a certain amount of money to help in the effort. CFCU’s contribution for year 2009 was $247,707 and another fee is expected to be determined by NCUA that can range from a 5% up to a 40 % on insurance savings.

He discussed the specifics relating to the growth in investments, loans, capital, and the solid financial situation of CFCU.

He informed that as of 12/31/09 CFCU had finalized the year with 19,262 members. When compared to last year, this represents a reduction of 338 members. The total assets of CFCU were $214.6 million, an increase of $6 million when compared to the previous year.

The Liabilities and Membership savings amount to $182.1 million, an increase of $5.3 million. The Capital & Reserve amounts to $32.5 million, an increase of $1.2 million.

The Statement of Income shows the amount of interest on loans for $11.4 million, a decrease of $1.2 million when compared to year 2008.

The dividend paid over shares and shares certificates amounts to $3.8 million.

The operational expenses amounted to $5.9 million in year 2009 when compared to 2008 there is an

10

increase of $200 thousand dollars. The Treasurer presented the distribution of income as follows: 27% for dividends, 41% for operational expenses, 16% for a provision for charged off accounts and 10% was net income due to the fact that 6% was imposed by NCUA for the corporate stabilization plan.

Finally, the net income was $1.3 million after deducting the amount paid for NCUA’s stabilization’s plan.

The Treasurer concluded his report expressing that in spite of the economic crisis that Puerto Rico is enduring, CFCU continues to be solid thanks to all the members that use our products and services and the dedication of our Board of Directors, Management and employees.

CREDIT COMMITTEE REPORTCredit Committee Chairman Juan M. Masini-Soler greeted and welcomed the members of the Annual Meeting. Mr. Masini-Soler introduced the members of the Credit Committee and Loan Division, and recognized their performance throughout the year. He then presented the statistics on the loan approvals and rejections for year 2009. He stated that a total of 3,593 loan applications were considered, of which 2,039 were favorable approved. Loans approved totaled $35,623,442, of which $11,041,198 represents personal loans, $462,800 emergency loans and $85,600 of credit; $17,689,818 in auto and $84,303 in boat loans; $1,359,200 in Master Cards; $3,410,473 in mortgage loans and $1,490,050 in commercial loans.

Mr. Masini-Soler informed that the Credit Committee and CFCU’s Management are constantly monitoring the changes in the market in order to provide members with the best products at the lowest cost and encouraged all members to take advantage of CFCU’s excellent loan offerings. He commented that as everyone knows 2009 was a year of great challenges due to the economic crisis and in particular Puerto Rico’s situation. CFCU had to make adjustments to the Loan Policy in order to stay competitive. He thanked the Loan officers, Managers and the Credit Committee members and shared the following thought “Remember that a good credit will open the door to a world of possibilities and CFCU is 100% committed to offer the best products and services and if by any reason you have clouds of economic situations in your horizons, do not hesitate to explain your problems to the Credit Committee who will be in the best spirit to try to help you as reasonably as possible”.

SUPERVISORY COMMITTEE REPORTSupervisory Committee Chairman, Carlos E. O’Neill, introduced the members of the committee and informed that according to the Credit Union Guide there are two essential goals: a) to assure that Management’s financial reporting objective are met and, b) that the practices and procedures safeguard members’ assets.

He explained that an annual audit of the financial statements is one of the methods used toward the safeguard of members’ funds. He commented that to satisfy the Supervisory Committee audit requirements, the Committee contracts a Certify Public Accountant firm. The Firm - Zayas, Morazzani & Co. conducted our external audit for years 2008 and 2009. The examiners concluded that the financial statements present fairly, in all material respects, the financial position of CFCU and

11

the results of the operations and its cash flows in conformity with Generally Accepted Accounting principles (GAAP) in the United States of America. The Supervisory Committee Chairman also informed that during this year, the Committee was focused in securing the services of a Certified Public Accounting firm, Barreto & Vélez, PSC, as our internal auditor and technology advisor to assure compliance in banking regulations and to monitor the interventions of our full time Compliance Officer. The Committee and the internal auditor have continued to monitor the activities of the department of Electronic Data Processing (EDP), which is considered to be the heart of CFCU’s accounting system. Until this day, Caribe Federal Credit Union has the latest software and hardware to provide for the financial accounting needs; and continues to provide secure electronic banking thru the Internet for the convenience of our members.

NOMINATIONS COMMITTEE REPORTThe President of the Nominations Committee, Nidza Hernández informed on the election process as follows: Option A2 - In-person elections; nominating committee and nominations by petition. The new election process states that the nominating committee files its nominations with the secretary of the credit union at least 90 days prior to the annual meeting, and the secretary notifies in writing all members eligible to vote at least 75 days prior to the annual meeting; and that nominations for vacancies may also be made by petition, said document should be accompanied with the signature of 1% of the active members with a minimum of 20 and a maximum of 500. The written notice must indicate that the election will not be conducted by ballot and there will be no nominations from the floor when there is only one nominee for each position to be filled. A brief statement of qualifications and biographical data in a form approved by the board of directors will be included for each nominee submitted by the nominating committee with the written notice to all eligible members. Each nominee by petition must submit a similar statement of qualifications and biographical data with the petition. The written notice must state the closing date for receiving nominations by petition. In all cases, the period for receiving nominations by petition must extend at least 30 days from the date that the petition requirement and the list of nominating committee’s nominees are mailed to all members. To be effective, a signed certificate must accompany such nominations from the nominee or nominees stating that they are agreeable to nomination and will serve if elected to office. Such nominations must be filed with the secretary of the Board of Directors at least 40 days prior to the annual meeting and the secretary will ensure that nominations by petition along with those of the nominating committee are posted in a conspicuous place in each credit union office at least 35 days prior to the annual meeting.

Nominations cannot be made from the floor unless insufficient nominations have been made by the nominating committee or by petition to provide for one nominee for each position to be filled or circumstances prevent the candidacy of the one nominee for a position to be filled. When only one member is nominated for each position to be filled, the chair may take a voice vote or declare each nominee elected by general consent or acclamation at the annual meeting.

DECLARATION OF NOMINEESMrs. Nidza Hernández declared that since there were four nominees to fill the four vacant positions, and in view that no elections has to be performed; the following members are the candidates to fill

12

the vacant positions of the Board of Directors: Mr. Emilio M. Colón, Mr. Juan O. Rodríguez, Mr. Alexis E. Agostini and Mr. Wilfred Benítez. NEW BUSINESSChairman Colón opened the session of new business however, no one presented any issue.

ADJOURNMENT:There being no further business discuss, the meeting was adjourned at 11:20 a.m.

Raffles, lunch and a social activity followed.

13

CARIBE FEDERAL CREDIT UNIONConsolidated Financial Statements

December 31, 2010 and 2009(With Independent Auditors’ Report Thereon)

15

16

17ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

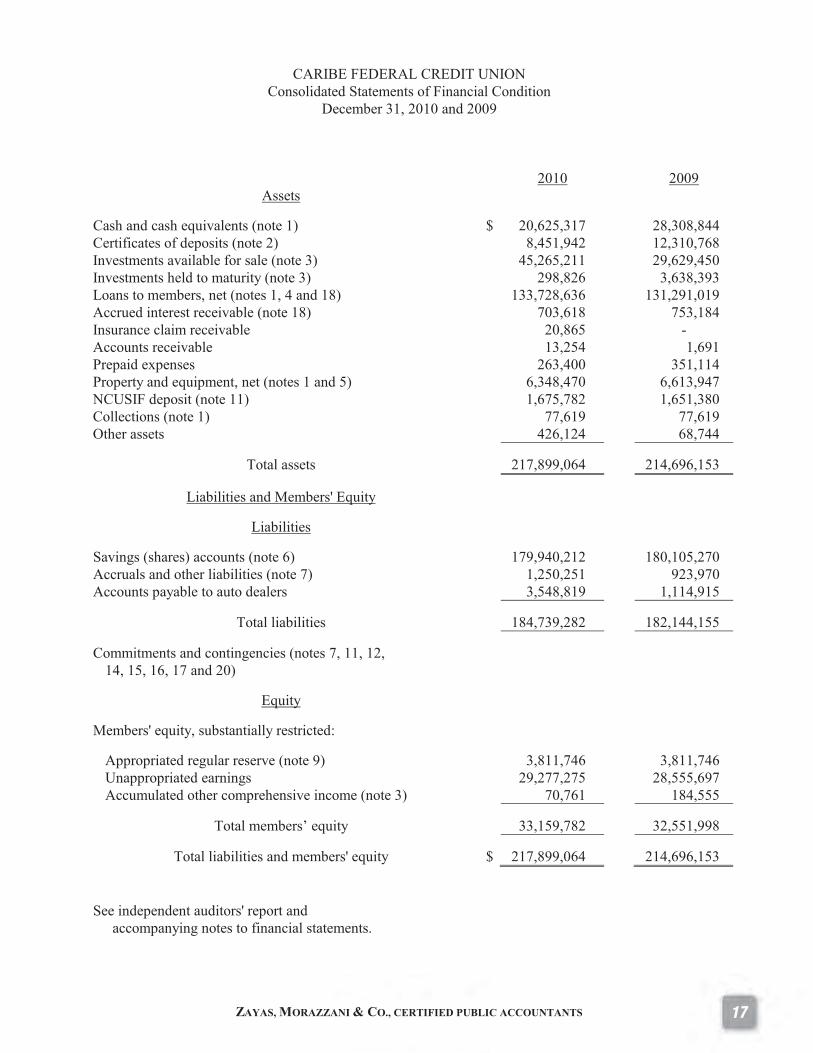

CARIBE FEDERAL CREDIT UNION Consolidated Statements of Financial Condition

December 31, 2010 and 2009

2010 2009 Assets

Cash and cash equivalents (note 1) $ 20,625,317 28,308,844 Certificates of deposits (note 2) 8,451,942 12,310,768 Investments available for sale (note 3) 45,265,211 29,629,450 Investments held to maturity (note 3) 298,826 3,638,393 Loans to members, net (notes 1, 4 and 18) 133,728,636 131,291,019 Accrued interest receivable (note 18) 703,618 753,184 Insurance claim receivable 20,865 - Accounts receivable 13,254 1,691 Prepaid expenses 263,400 351,114 Property and equipment, net (notes 1 and 5) 6,348,470 6,613,947 NCUSIF deposit (note 11) 1,675,782 1,651,380 Collections (note 1) 77,619 77,619 Other assets 426,124 68,744

Total assets 217,899,064 214,696,153

Liabilities and Members' Equity

Liabilities

Savings (shares) accounts (note 6) 179,940,212 180,105,270 Accruals and other liabilities (note 7) 1,250,251 923,970 Accounts payable to auto dealers 3,548,819 1,114,915

Total liabilities 184,739,282 182,144,155

Commitments and contingencies (notes 7, 11, 12, 14, 15, 16, 17 and 20)

Equity

Members' equity, substantially restricted:

Appropriated regular reserve (note 9) 3,811,746 3,811,746 Unappropriated earnings 29,277,275 28,555,697 Accumulated other comprehensive income (note 3) 70,761 184,555

Total members’ equity 33,159,782 32,551,998

Total liabilities and members' equity $ 217,899,064 214,696,153 See independent auditors' report and

accompanying notes to financial statements.

18 ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

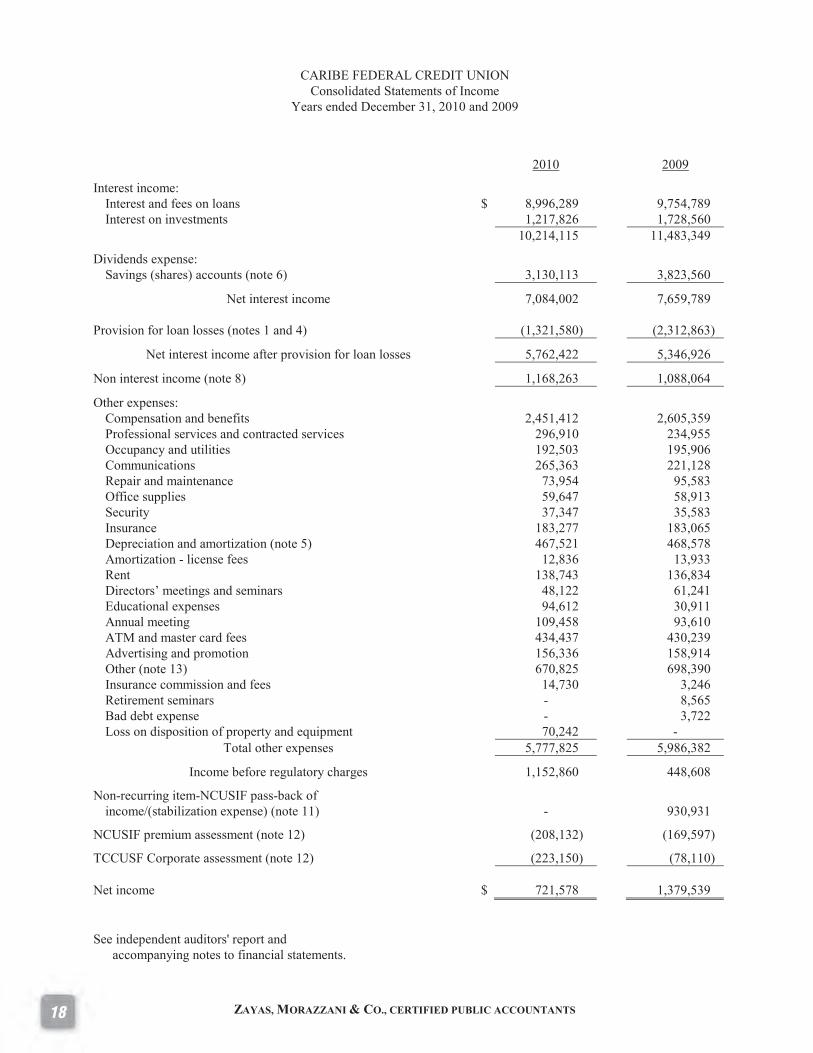

CARIBE FEDERAL CREDIT UNION Consolidated Statements of Income

Years ended December 31, 2010 and 2009

2010 2009

Interest income: Interest and fees on loans $ 8,996,289 9,754,789 Interest on investments 1,217,826 1,728,560

10,214,115 11,483,349

Dividends expense: Savings (shares) accounts (note 6) 3,130,113 3,823,560

Net interest income 7,084,002 7,659,789 Provision for loan losses (notes 1 and 4) (1,321,580) (2,312,863)

Net interest income after provision for loan losses 5,762,422 5,346,926

Non interest income (note 8) 1,168,263 1,088,064

Other expenses: Compensation and benefits 2,451,412 2,605,359 Professional services and contracted services 296,910 234,955 Occupancy and utilities 192,503 195,906 Communications 265,363 221,128 Repair and maintenance 73,954 95,583 Office supplies 59,647 58,913 Security 37,347 35,583 Insurance 183,277 183,065 Depreciation and amortization (note 5) 467,521 468,578 Amortization - license fees 12,836 13,933 Rent 138,743 136,834 Directors’ meetings and seminars 48,122 61,241 Educational expenses 94,612 30,911 Annual meeting 109,458 93,610 ATM and master card fees 434,437 430,239 Advertising and promotion 156,336 158,914 Other (note 13) 670,825 698,390 Insurance commission and fees 14,730 3,246 Retirement seminars - 8,565 Bad debt expense - 3,722 Loss on disposition of property and equipment 70,242 -

Total other expenses 5,777,825 5,986,382

Income before regulatory charges 1,152,860 448,608

Non-recurring item-NCUSIF pass-back of income/(stabilization expense) (note 11)

-

930,931

NCUSIF premium assessment (note 12) (208,132) (169,597)

TCCUSF Corporate assessment (note 12) (223,150) (78,110) Net income $ 721,578 1,379,539 See independent auditors' report and

accompanying notes to financial statements.

19ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

CARIBE FEDERAL CREDIT UNION Consolidated Statements of Members' Equity Years ended December 31, 2010 and 2009

Appropriated

Statutory

Unappropriated

Other Comprehensive

Income

Total

Balances, December 31, 2008 $ 3,811,746 27,176,158 328,734 31,316,638 Comprehensive Income:

Net income - 1,379,539 - 1,379,539 Other comprehensive income:

Net change in unrealized gain/loss on available for sale securities

-

-

(144,179)

(144,179) Total comprehensive income - - (144,179) 1,235,360

Balance, December 31, 2009 $ 3,811,746 28,555,697 184,555 32,551,998 Comprehensive Income:

Net income - 721,578 - 721,578 Other comprehensive income:

Net change in unrealized gain/loss on available for sale securities

-

-

(113,794)

(113,794) Total comprehensive income - 721,578 (113,794) 607,783

Balance, December 31, 2010 $ 3,811,746 29,277,275 70,761 33,159,782

See independent auditors' report and

accompanying notes to financial statements.

20 ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

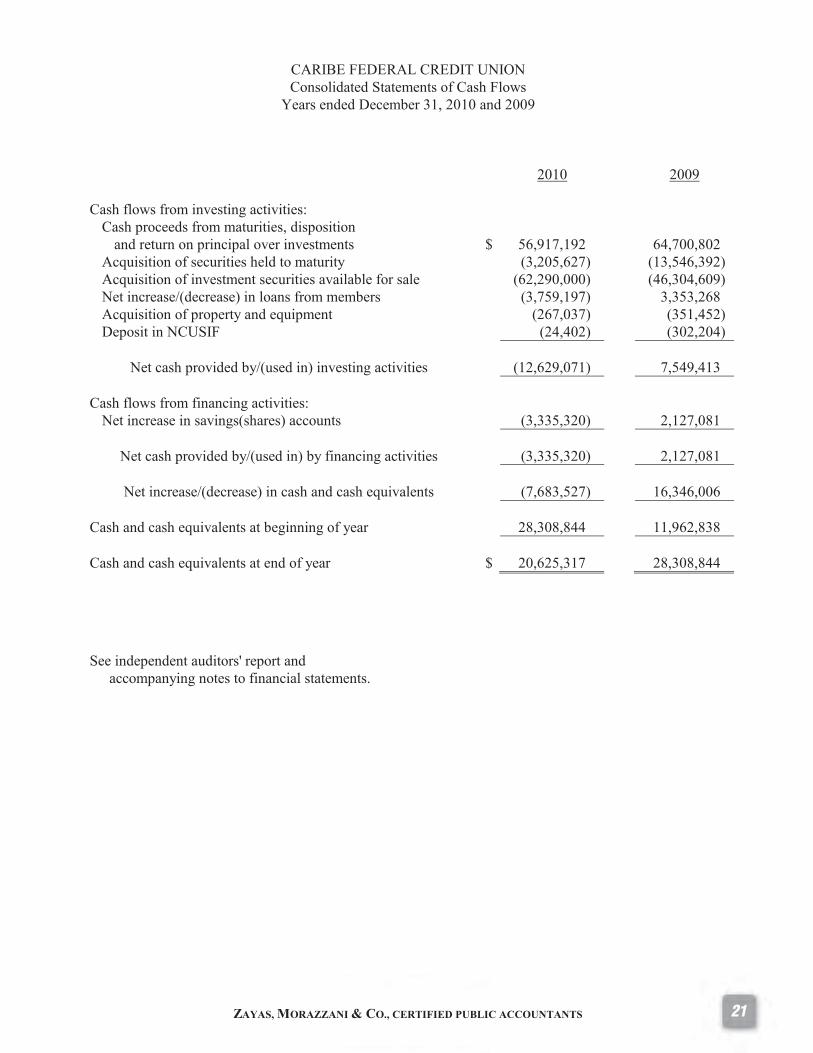

CARIBE FEDERAL CREDIT UNION Consolidated Statements of Cash Flows

Years ended December 31, 2010 and 2009

2010 2009 Cash flows from operating activities:

Net income $ 721,578 1,379,539 Adjustments to reconcile net income to net

cash provided by operating activities:

Depreciation and amortization 467,521 468,578 Loss on disposition of repossessed assets 70,242 - NCUSIF pass-back of income - (930,931) Provision for possible loan losses 1,321,580 2,312,863 Bad debt expense - 3,722 Dividends credited on members’ saving (shares) accounts 3,170,262 3,873,045 Premium amortization and discount accretion (net) 27,273 19,644 Changes in assets and liabilities:

Decrease on accrued interest receivable 49,566 183,374 (Increase)/decrease in insurance claim receivable (20,865) 25,221 Increase in account receivable (11,563) (3,285) (Increase)/decrease in prepaid expenses 87,714 (4,827) Increase in other assets (362,629) (38,400) Increase/(decrease) in accruals and other liabilities 326,281 (209,112) Increase/(decrease) in accounts payable to auto dealers 2,433,904 (409,919)

Total adjustments 7,559,286 5,289,973

Net cash provided by operating activities $ 8,280,864 6,669,512

(Continued)

See independent auditors' report and

accompanying notes to financial statements.

21ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

CARIBE FEDERAL CREDIT UNION Consolidated Statements of Cash Flows

Years ended December 31, 2010 and 2009

2010 2009 Cash flows from investing activities:

Cash proceeds from maturities, disposition and return on principal over investments

$

56,917,192

64,700,802

Acquisition of securities held to maturity (3,205,627) (13,546,392) Acquisition of investment securities available for sale (62,290,000) (46,304,609) Net increase/(decrease) in loans from members (3,759,197) 3,353,268 Acquisition of property and equipment (267,037) (351,452) Deposit in NCUSIF (24,402) (302,204)

Net cash provided by/(used in) investing activities (12,629,071) 7,549,413

Cash flows from financing activities:

Net increase in savings(shares) accounts (3,335,320) 2,127,081

Net cash provided by/(used in) by financing activities (3,335,320) 2,127,081

Net increase/(decrease) in cash and cash equivalents (7,683,527) 16,346,006 Cash and cash equivalents at beginning of year 28,308,844 11,962,838 Cash and cash equivalents at end of year $ 20,625,317 28,308,844

See independent auditors' report and accompanying notes to financial statements.

22 ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

December 31, 2010 and 2009

(1) Organization, Nature of Operations, Basis of Presentation and Significant Accounting Policies

Organization and Nature of Operations

Caribe Federal Credit Union (“Credit Union”) is a non profit organization established in 1951 organized and chartered under the Federal Credit Union Act. The Credit Union serves federal employees in Puerto Rico and the US Virgin Islands, members of the Liga de Estudiantes de Arte de San Juan, select employee groups in Puerto Rico and immediate family members. Its purpose is to promote thrift among its members by affording them an opportunity to accumulate their savings and create for them a source of credit for productive purposes. Business Consortium Alliance, Inc. (BCA), is a wholly-owned subsidiary of Caribe Federal Credit Union (parent Company). It is a credit union service organization (“CUSO”) under the United States Credit Union Act. It was engaged in the development of its lines of business and in providing services to the Credit Union. Effective October 31, 2010, BCA ceased its active operations. During the year ended December 31, 2008, Business Alliance Insurance Agency, Inc. (BAIA) was incorporated and began operations in 2009. The Company was created to conduct and operate a general insurance agency business for insurance companies organized or admitted to do business in the Commonwealth of Puerto Rico. It is a subsidiary of BCA. Principles of Consolidation The consolidated financial statements include the accounts of Caribe Federal Credit Union and Business Consortium Alliance, Inc. (BCA) (as consolidated with BAIA). All significant intercompany accounts and transactions have been eliminated.

Basis of Presentation

The accompanying financial statements are presented under accounting principles generally accepted in the United States of America.

(Continued)

23

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 2 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(1) Organization, Nature of Operations, Basis of Presentation and Significant Accounting Policies, Continued

Significant Accounting Policies

Caribe Federal Credit Union has adopted the following significant accounting policies:

Investments Held to maturity. Securities for which management has the intent and the ability to hold to maturity. These investments are reported at cost, adjusted for amortization of premiums and accretion of discounts, which are recognized as adjustments to interest income on investments. Available for sale. Investment securities that could be sold at any time in response to economic and strategic factors. These securities are reported at fair market value. Unrealized gains and losses on securities available for sale are recognized as a direct increase or decrease in other comprehensive income. Investments are made in accordance with the credit union's policies, which incorporate the regulations of NCUA, hence, they are principally in federally sponsored and guaranteed instruments. Gains or losses on disposition are based on the net proceeds and the adjusted carrying amount of the securities sold, using the specific identification method. Premiums and discounts are amortized or accreted using the effective interest method. Interest income is recorded on an accrual basis. Loans to Members, Allowance for Loan Losses and Loan Origination Fees Loans are stated at the amount of unpaid principal, reduced by an allowance for loan losses and net origination fees. Interest on loans is recognized over the term of the loan and is calculated using the simple-interest method on principal amounts outstanding. The allowance for loan losses is established through a provision for loan losses charged to expenses. Loans are charged against the allowance for loan losses when management believes that the collectability of the principal is unlikely. The allowance is an amount that management believes will be adequate to absorb possible losses on existing loans that may become uncollectible, based on evaluations of the collectability of loans and prior loan loss experience.

(Continued)

24

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 3 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(1) Organization, Nature of Operations, Basis of Presentation and Significant Accounting Policies, Continued

The evaluations take into consideration such factors as changes in the nature and volume of the loan portfolio, overall portfolio quality, review of specific problem loans, and current economic conditions that may affect the borrowers' ability to pay. Accrual of interest is dis-continued on a loan when management believes, after considering economics, business conditions and collection efforts that the borrowers' financial condition is such that collection of interest is doubtful. Regularly, this is applied to loans with a delinquency greater than 90 days. The revenue for such interests not accrued is recognized when collected. Loan origination fees are deferred and recognized over the life of the loan as an adjustment of yield. The unamortized balance of the net origination fees is reported as part of the loan balance to which it relates. The periodic amortization is reported on the income statement as interest income.

Accounts Receivable Accounts receivable are stated at their net realizable value. Property and Equipment Property and equipment are stated at cost less accumulated depreciation and amortization. Depreciation and amortization is computed on the straight-line method over the estimated useful life of the respective assets. Collections Art collections are capitalized at their cost at the date of purchase or, if the items were contributed, at their fair or appraised value at the contribution date. Cash and Cash Equivalents For purposes of the statements of cash flows, the credit union considers all highly liquid investment securities acquired with an original or remaining maturity of three months or less to be cash equivalents.

(Continued)

25

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 4 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(1) Organization, Nature of Operations, Basis of Presentation and Significant Accounting Policies, Continued

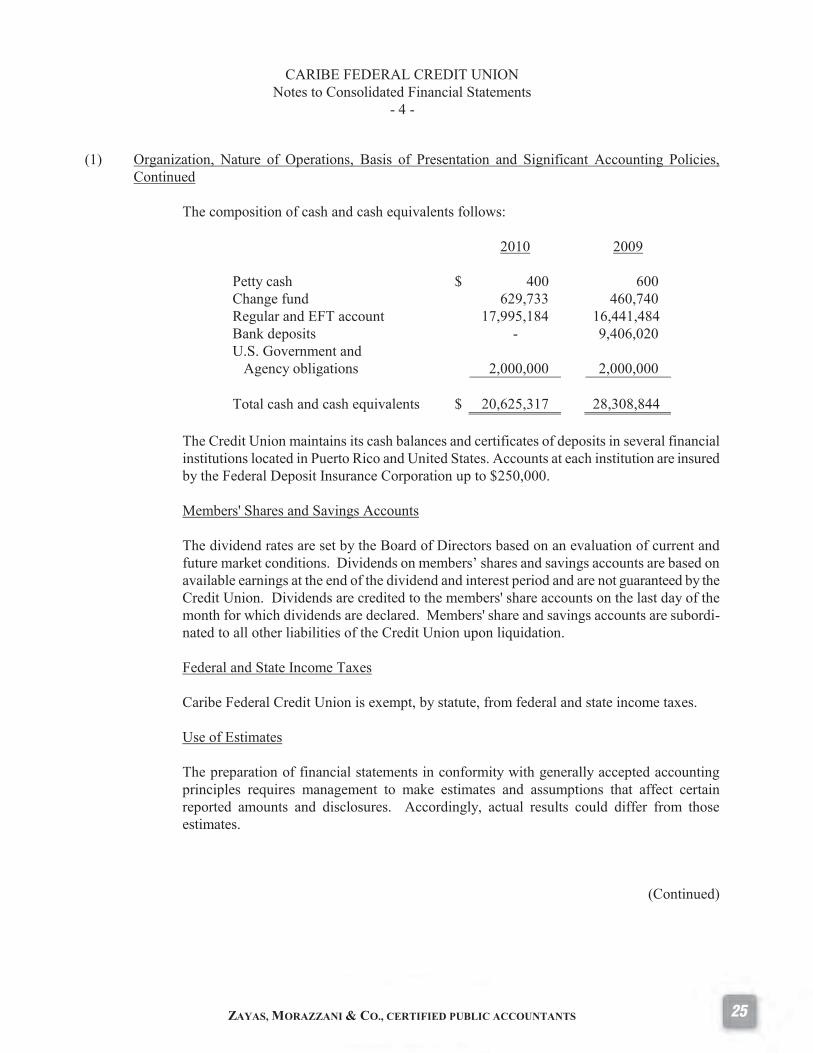

The composition of cash and cash equivalents follows:

2010 2009 Petty cash $ 400 600 Change fund 629,733 460,740 Regular and EFT account 17,995,184 16,441,484 Bank deposits - 9,406,020 U.S. Government and

Agency obligations

2,000,000

2,000,000 Total cash and cash equivalents $ 20,625,317 28,308,844

The Credit Union maintains its cash balances and certificates of deposits in several financial institutions located in Puerto Rico and United States. Accounts at each institution are insured by the Federal Deposit Insurance Corporation up to $250,000.

Members' Shares and Savings Accounts The dividend rates are set by the Board of Directors based on an evaluation of current and future market conditions. Dividends on members’ shares and savings accounts are based on available earnings at the end of the dividend and interest period and are not guaranteed by the Credit Union. Dividends are credited to the members' share accounts on the last day of the month for which dividends are declared. Members' share and savings accounts are subordi-nated to all other liabilities of the Credit Union upon liquidation. Federal and State Income Taxes Caribe Federal Credit Union is exempt, by statute, from federal and state income taxes.

Use of Estimates The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect certain reported amounts and disclosures. Accordingly, actual results could differ from those estimates.

(Continued)

26

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 5 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(1) Organization, Nature of Operations, Basis of Presentation and Significant Accounting Policies, Continued

Reclassifications In the accompanying financial statements, certain 2009 figures were reclassified to conform to the 2010 presentation.

Impairment of Long-lived Assets The Credit Union periodically reviews long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. No indications of impairment are evident at December 31, 2010 and 2009. Subsequent Events Management has evaluated subsequent events through April 14, 2011, the date the financial statements were available to be issued. No material subsequent events requiring further disclosure have been identified.

(2) Certificates of Deposits

At December 31, 2010, the Credit Union maintains certificates of deposits in denominations of $100,000 or higher. The scheduled maturities are as follows:

Due in one year or less $ 6,005,627 Due after one year

through three years

2,446,315 $ 8,451,942

(Continued)

27

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 6 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

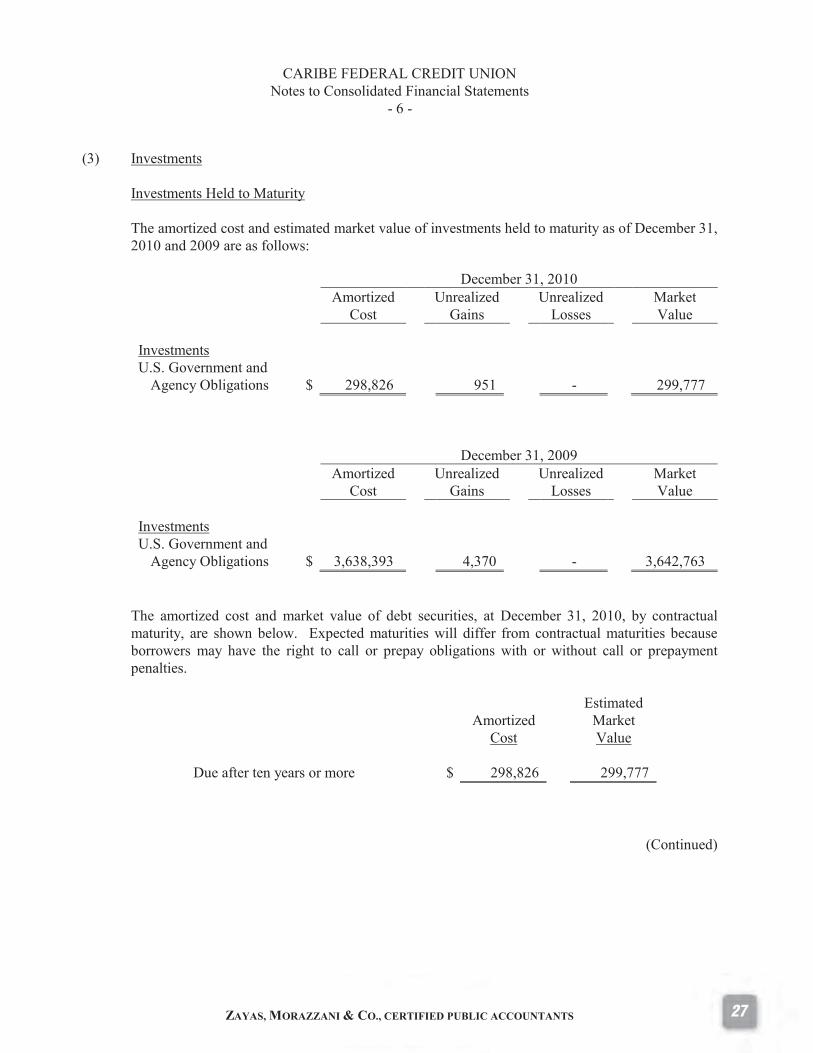

(3) Investments Investments Held to Maturity

The amortized cost and estimated market value of investments held to maturity as of December 31, 2010 and 2009 are as follows:

December 31, 2010 Amortized

Cost Unrealized

Gains Unrealized

Losses Market

Value Investments U.S. Government and

Agency Obligations

$

298,826

951

-

299,777

December 31, 2009 Amortized

Cost Unrealized

Gains Unrealized

Losses Market

Value Investments U.S. Government and

Agency Obligations

$

3,638,393

4,370

-

3,642,763 The amortized cost and market value of debt securities, at December 31, 2010, by contractual maturity, are shown below. Expected maturities will differ from contractual maturities because borrowers may have the right to call or prepay obligations with or without call or prepayment penalties.

Amortized

Cost

Estimated Market Value

Due after ten years or more $ 298,826 299,777

(Continued)

28

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 7 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

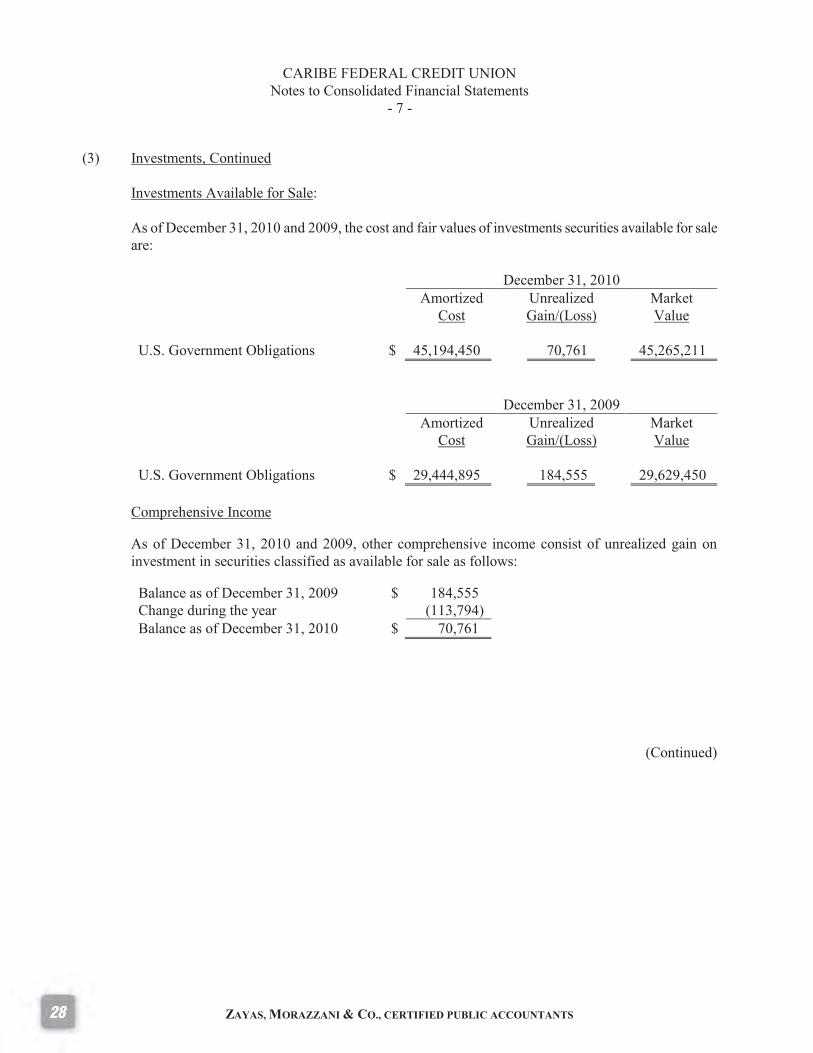

(3) Investments, Continued Investments Available for Sale: As of December 31, 2010 and 2009, the cost and fair values of investments securities available for sale are: December 31, 2010 Amortized

Cost Unrealized

Gain/(Loss) Market

Value U.S. Government Obligations $ 45,194,450 70,761 45,265,211

December 31, 2009 Amortized

Cost Unrealized

Gain/(Loss) Market

Value U.S. Government Obligations $ 29,444,895 184,555 29,629,450

Comprehensive Income As of December 31, 2010 and 2009, other comprehensive income consist of unrealized gain on investment in securities classified as available for sale as follows:

Balance as of December 31, 2009 $ 184,555 Change during the year (113,794) Balance as of December 31, 2010 $ 70,761

(Continued)

29

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 8 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

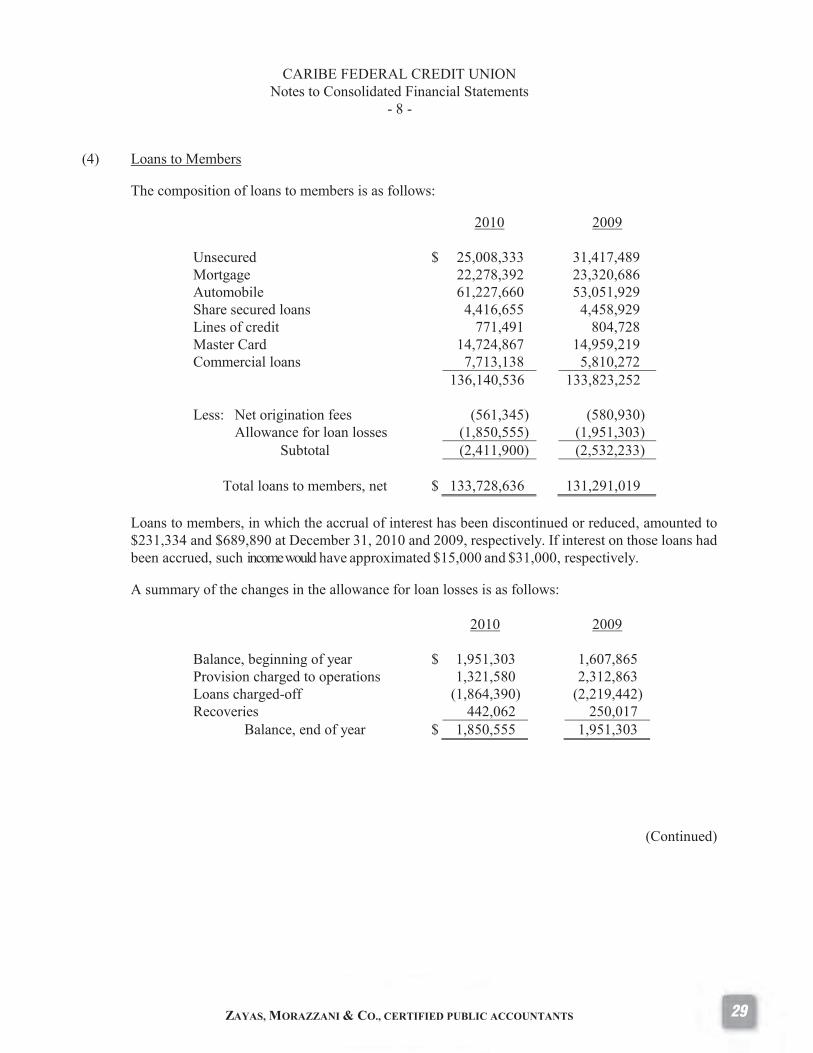

(4) Loans to Members

The composition of loans to members is as follows:

2010 2009 Unsecured $ 25,008,333 31,417,489 Mortgage 22,278,392 23,320,686 Automobile 61,227,660 53,051,929 Share secured loans 4,416,655 4,458,929 Lines of credit 771,491 804,728 Master Card 14,724,867 14,959,219 Commercial loans 7,713,138 5,810,272 136,140,536 133,823,252 Less: Net origination fees (561,345) (580,930)

Allowance for loan losses (1,850,555) (1,951,303) Subtotal (2,411,900) (2,532,233)

Total loans to members, net $ 133,728,636 131,291,019

Loans to members, in which the accrual of interest has been discontinued or reduced, amounted to $231,334 and $689,890 at December 31, 2010 and 2009, respectively. If interest on those loans had been accrued, such income would have approximated $15,000 and $31,000, respectively. A summary of the changes in the allowance for loan losses is as follows:

2010 2009 Balance, beginning of year $ 1,951,303 1,607,865 Provision charged to operations 1,321,580 2,312,863 Loans charged-off (1,864,390) (2,219,442) Recoveries 442,062 250,017

Balance, end of year $ 1,850,555 1,951,303

(Continued)

30

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 9 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

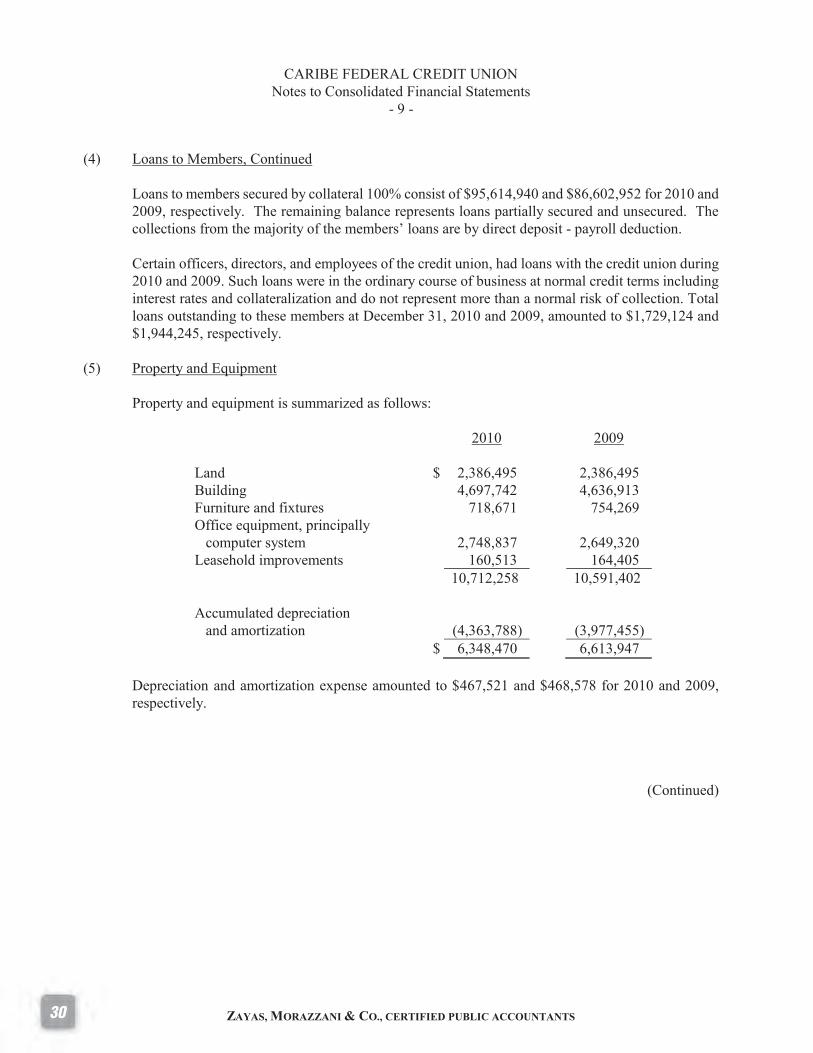

(4) Loans to Members, Continued Loans to members secured by collateral 100% consist of $95,614,940 and $86,602,952 for 2010 and 2009, respectively. The remaining balance represents loans partially secured and unsecured. The collections from the majority of the members’ loans are by direct deposit - payroll deduction. Certain officers, directors, and employees of the credit union, had loans with the credit union during 2010 and 2009. Such loans were in the ordinary course of business at normal credit terms including interest rates and collateralization and do not represent more than a normal risk of collection. Total loans outstanding to these members at December 31, 2010 and 2009, amounted to $1,729,124 and $1,944,245, respectively.

(5) Property and Equipment

Property and equipment is summarized as follows:

2010 2009 Land $ 2,386,495 2,386,495 Building 4,697,742 4,636,913 Furniture and fixtures 718,671 754,269 Office equipment, principally

computer system

2,748,837

2,649,320 Leasehold improvements 160,513 164,405 10,712,258 10,591,402 Accumulated depreciation

and amortization

(4,363,788)

(3,977,455) $ 6,348,470 6,613,947

Depreciation and amortization expense amounted to $467,521 and $468,578 for 2010 and 2009, respectively.

(Continued)

31

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 10 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(6) Savings (Shares) Accounts

Members' shares and savings accounts are summarized as follows:

Weighted-Average Rate at

December 31, 2010

2010

2009 Share savings 1.03% $ 99,731,247 89,143,847 Share draft 0.40% 8,844,931 8,223,462 108,576,178 97,367,309 Share certificates:

0.0% - 2.00% 36,113,798 23,408,101 2.1% - 3.00% 17,964,311 29,044,881 3.1% - 4.00% 4,063,968 11,781,021 4.1% - 5.00% 2,620,280 7,285,461 5.1% - 5.83% 10,601,677 11,218,497

71,364,034 82,737,961 Total savings (shares) accounts $ 179,940,212 180,105,270

As of December 31, 2010 and 2009 the NCUA insured the Credit Union shares members’ accounts to at least $250,000. As of December 31, 2010 and 2009, the aggregate amount of members’ shares and savings accounts over $250,000 was approximately $15,256,095 and $17,398,211, respectively. At December 31, 2010, scheduled maturities of share certificates are as follows:

Year Ending December 31 2011 2012 2013 2014 2015 Total 0.0% - 2.00% $ 34,558,698 1,299,289 255,811 - - 36,113,798 2.1% - 3.00% 12,353,398 2,901,645 944,914 151,744 1,612,610 17,964,311 3.1% - 4.00% 160,696 - 560,009 2,713,529 629,734 4,063,968 4.1% - 5.00% 1,475,890 638,452 452,000 53,938 - 2,620,280 5.1% - 5.83% 5,547,303 5,054,374 - - - 10,601,677

Total $ 54,095,985 9,893,760 2,212,734 2,919,211 2,242,344 71,364,034

(Continued)

32

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 11 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

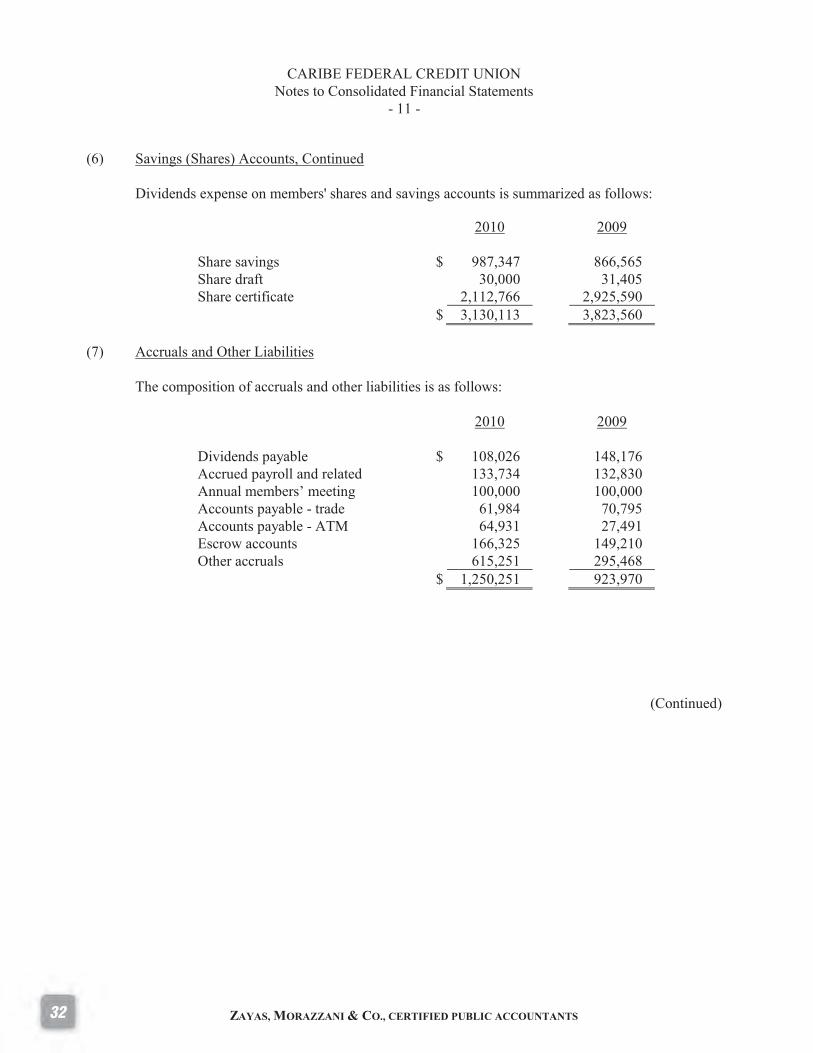

(6) Savings (Shares) Accounts, Continued Dividends expense on members' shares and savings accounts is summarized as follows:

2010 2009 Share savings $ 987,347 866,565 Share draft 30,000 31,405 Share certificate 2,112,766 2,925,590 $ 3,130,113 3,823,560

(7) Accruals and Other Liabilities

The composition of accruals and other liabilities is as follows:

2010 2009 Dividends payable $ 108,026 148,176 Accrued payroll and related 133,734 132,830 Annual members’ meeting 100,000 100,000 Accounts payable - trade 61,984 70,795 Accounts payable - ATM 64,931 27,491 Escrow accounts 166,325 149,210 Other accruals 615,251 295,468 $ 1,250,251 923,970

(Continued)

33

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 12 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(8) Non-Interest Income Non-interest income for the years ended December 31, 2010 and 2009 are as follows:

2010 2009 ATM card fees and charges $ 448,633 416,929 Master card fees and charges 291,723 295,187 Other fees and charges 310,461 304,942 Sponsorships and other 47,019 34,630 Seminar registration and

administrative fees

-

18,139 Insurance commissions and fees 40,860 5,441 Annual meeting 4,110 4,775 Other 25,457 8,021 $ 1,168,263 1,088,064

(9) Members' Equity

Caribe Federal Credit Union is required by regulation to maintain a statutory reserve. This reserve, which represents a regulatory restriction of retained earnings, is not available for the payment of dividends. The statutory reserve consists of $3,811,746 for 2010 and 2009.

(10) Pension Plan

The employees of Caribe Federal Credit Union and Business Consortium Alliance participate in a group pension plan through contributions to a life annuity accumulation contract administered by an insurance company. The plan was effective on October 1, 1993. Caribe Federal Credit Union matches the participant's contribution up to a 5% of the employee's compensation. All participants contribute at least 2% of their total gross compensation. In no event will the participants' annual deposit exceed 10% of the gross compensation or $9,000. Only full-time employees are eligible to enter the plan and must have attained eighteen (18) years old and completed twelve months of service. The normal retirement date is the first day of the month after the participants' 62nd birthday and after completing twenty (20) years of service.

(Continued)

34

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 13 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(10) Pension Plan, Continued

The plan also provides for early retirement. A participant may elect to retire at any time after attaining fifty-five (55) years old and completing seven (7) years of service.

Vesting is accumulated after the second year on the plan for a period of five years at 20% per year.

At termination of employment, the vested portion of a participant's account will be paid following the next annual benefit payment date.

During the years ended December 31, 2010 and 2009 Caribe Federal Credit Union contributed approximately $61,000 and $66,000, respectively, to the pension plan.

(11) NCUSIF Deposit

The deposit in the National Credit Union Share Insurance Fund (NCUSIF) is in accordance with National Credit Union Administration (NCUA) regulations, which require the maintenance of a deposit by each insured credit union in an amount equal to one percent (1%) of its insured shares. The deposit is refunded to the credit union if its insurance coverage is terminated, it converts its insurance coverage from another source, or the operations of the fund are transferred from the NCUA Board. In the first quarter of 2009, NCUA commenced a plan to stabilize the corporate credit unions system. As a result, the NCUA Board determined a depletion in the NCUSIF deposit to 31% of its balance. Thus, the credit union had to recognize an impairment of 69% of the existing NCUSIF deposit. The financial statements of 2008 reflected such impairment in the amount of $930,931 (as determined by NCUA). During the year ended December 31, 2009, NCUA Board took action to pass-back to insured credit unions an amount from the NCUSIF earnings recovery. Specifically, an amount equal to the depletion of 2008 was passed-back and credited to each insured credit union’s NCUSIF deposit account as a recapitalized NCUSIF deposit.

(Continued)

35

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 14 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(11) NCUSIF Deposit, Continued The NCUA Board’s new action resulted in a restored and fully refundable asset deposit. The American Institute of Certified Public Accountants (AICPA) Statement of Position (SOP) No. 01-6, “Accounting by Certain Entities that Lend to or Finance the Activities of Others”, paragraph 11(a), provides that:

“Amounts deposited with the NCUSIF should be accounted for and reported as assets as long as such amounts are fully refundable. Otherwise, they should be reviewed for impairment.”

This guidance requires insured credit unions to recognize the recapitalization of their NCUSIF deposit as an asset and income in the year ended December 31, 2009, not the reversal of the previous impairment. Based on NCUA Board determination, NCUSIF deposit was considered impaired in 2008, but recapitalized in 2009. The financial statements of 2009 recognized the recapitalization of NCUSIF deposit with a credit to income in the amount of $930,931.

(12) Corporate (TCCUSF) and NCUSIF Premium Assessments

During the year ended December 31, 2009, NCUA Board authorized the billing and collection of certain premium (NCUSIF-National Credit Union Share Insurance Fund) and corporate (TCCUSF-Temporary Corporate Credit Union Stabilization Fund) assessments, using a percentage charge over insured shares (up to $250,000 per account). During 2009 and 2010, the subject charges have fluctuated from approximately .12% to .15%.

(Continued)

36

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 15 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(13) Other Expenses For the years ended on December 31, 2010 and 2009, the other expenses consist of the following:

2010 2009 Travel and conferences $ 19,128 20,701 Dues and subscriptions 9,337 13,819 Loan servicing & collection 160,253 212,730 Software support 172,670 130,642 Monthly statements 105,813 103,700 Federal operating 50,296 49,755 Bank service charges 65,022 49,593 Employees activities 15,052 10,820 Other miscellaneous 45,053 85,381 Other operating losses 28,201 21,249 $ 670,825 698,390

(14) Subsidiaries

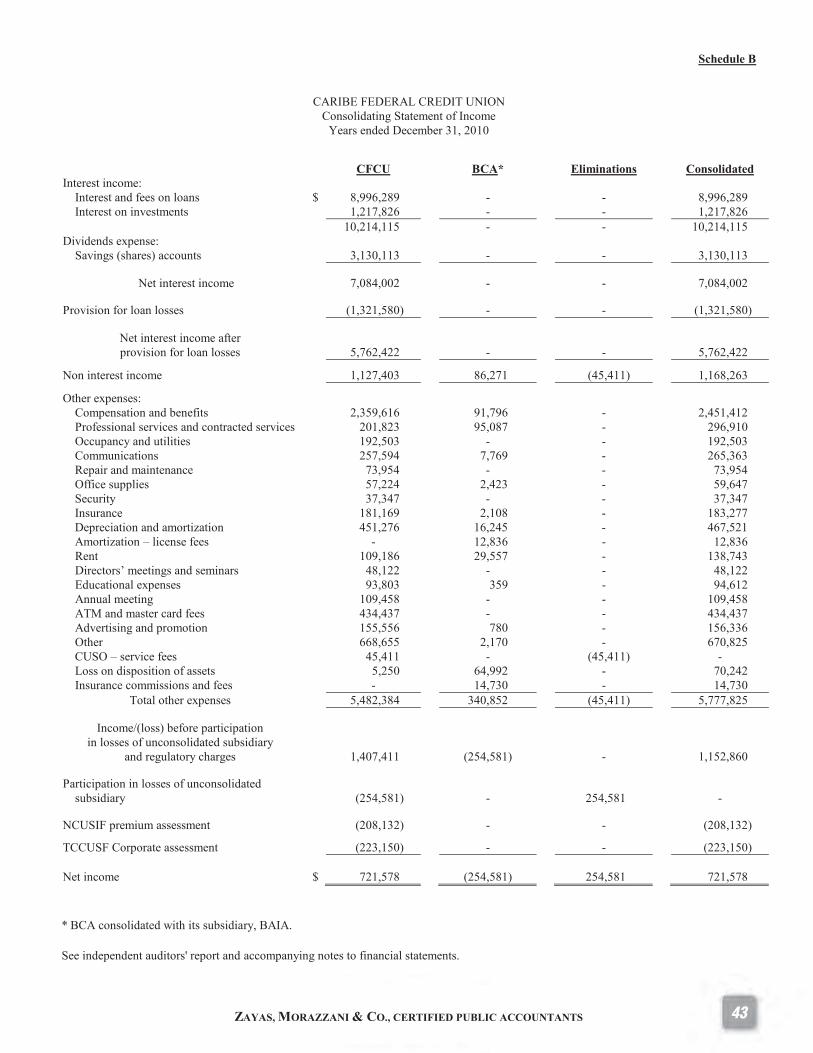

As stated in note 1, these consolidated financial statements, include the accounts of Caribe Federal Credit Union, and its subsidiaries, Business Consortium Alliance, Inc. and Business Alliance Insurance Agency, Inc. The accompanying schedules A and B summarize the participation of CFCU and BCA (as consolidated with BAIA) in the consolidated financial statements of CFCU as of and for the year ended December 31, 2010. The accompanying consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which contemplates continuation as a going concern. However, the consolidated subsidiaries have sustained recurring losses from operations since their inception and have accumulated operational deficits. No additional investment is contemplated by the Credit Union. Also, BCA ceased its active operations effective October 31, 2010. These factors, among other, raise substantial doubt about the ability of the Subsidiaries to continue going concerns.

(Continued)

37

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 16 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(14) Subsidiaries, Continued Management and the Board of Directors of the Consolidated Subsidiaries are working in the evaluation and implementation of plans regarding those matters. The Management of CFCU understands that the effect, if any, of such conditions in the accompanying consolidated financial statements as of and for the year ended December 31, 2010, will not be significant. Accordingly, the accompanying financial statements do not include any adjustments that might result from the outcome of these conditions.

(15) Loan Commitments

At December 31, 2010, Caribe Federal Credit Union had outstanding commitments with its members for unused lines-of-credit and credit cards that are not reflected in the accompanying financial statements as follows:

Lines-of-credit $ 374,767 Credit cards 15,096,925 $ 15,471,692

In addition, the Credit Union had pending to deliver certain payments to auto dealers subject to the presentation of required documents. As of December 31, 2010 and 2009 payments amounted to $3,548,819 and $1,114,915, respectively.

Caribe Federal Credit Union is a party to financial instruments with off-balance-sheet risk in the normal course of business to meet the financing needs of its members. These financial instruments include commitments to extend credit and involve, to varying degrees, elements of credit and interest rate risk in excess of the amount recognized in the statement of financial position. The contractual notional amounts of those instruments reflect the extent of involvement Caribe Federal Credit Union has in particular classes of financial instruments.

Caribe Federal Credit Union's exposure to credit loss in the event of nonperformance by the other party to the financial instrument for commitments to extend credit is represented by the contractual notional amount of those instruments. Caribe Federal Credit Union uses the same credit policies in making commitments as it does for on-balance-sheet instruments. Unless noted otherwise, Caribe Federal Credit Union does not require collateral or other security to support financial instruments with credit risk.

(Continued)

38

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 17 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(15) Loan Commitments, Continued

Commitments to extend credit are agreements to lend to a member as long as there is no violation of any condition established in the contract. Commitments generally have fixed expiration dates or other termination clauses and may require payment of a fee. Since many of the commitments are expected to expire without being drawn upon, the total commitment amounts do not necessarily represent future cash requirements. Caribe Federal Credit Union evaluates each member's credit worthiness on a case-by-case basis. The amount of collateral obtained, if deemed necessary by Caribe Federal Credit Union upon extension of credit, is based on management's credit evaluation of the counterpart.

(16) Line of Credit

Caribe Federal Credit Union has a line of credit facility with financial institutions. As of December 31, 2010 and 2009 there are not outstanding balances in the subject line of credit. The unused amount is $10,000,000. Interest is charged when applicable at prime rate.

(17) Litigation In the normal course of business, the Credit Union is a defendant in certain lawsuits. Management

understands that the effect, if any, of the subject cases, will not be significant for the financial statements.

(18) Fair Values of Financial Instruments

Cash and Cash Equivalents

The carrying amount approximates fair value due to the short-term nature of these instruments.

Investment Securities

Fair values have been determined using quoted market prices for all investment securities. Loan Receivables

The fair value of the loan receivables approximates the carrying amount in the financial statements. Accrued Interest Receivable The fair value of the accrued interest receivable approximates the carrying amount in the financial statements.

(Continued)

39

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 18 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

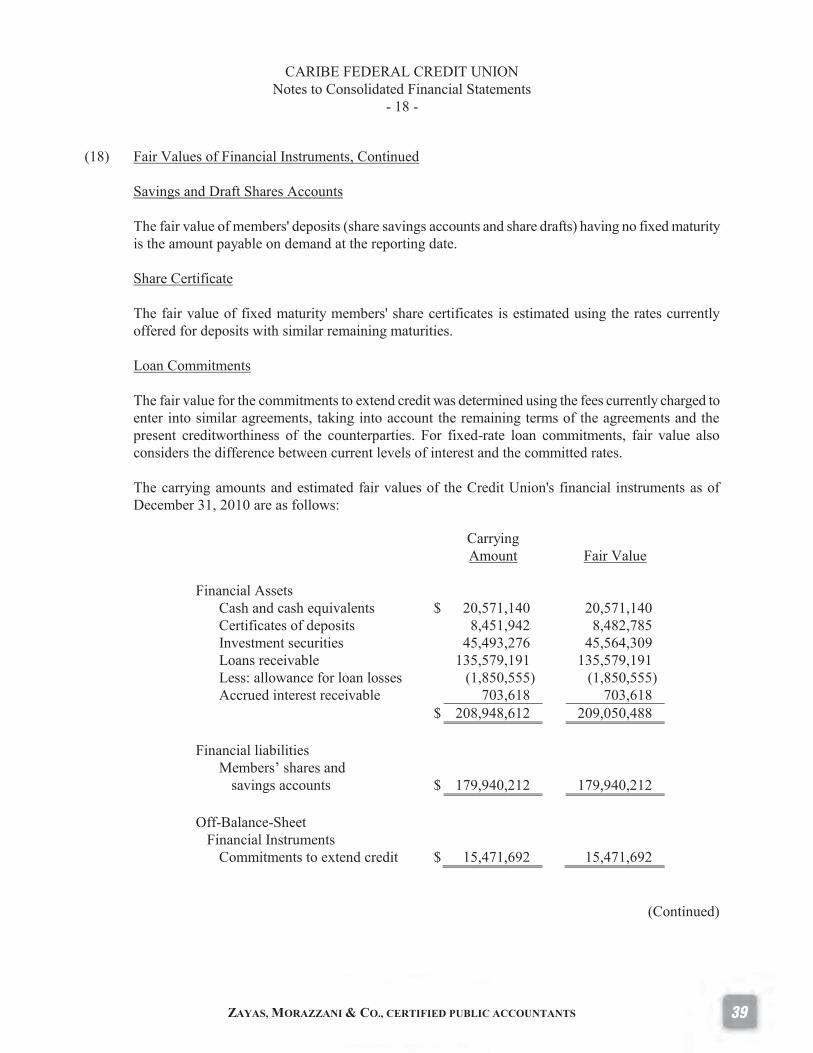

(18) Fair Values of Financial Instruments, Continued Savings and Draft Shares Accounts

The fair value of members' deposits (share savings accounts and share drafts) having no fixed maturity is the amount payable on demand at the reporting date.

Share Certificate

The fair value of fixed maturity members' share certificates is estimated using the rates currently offered for deposits with similar remaining maturities.

Loan Commitments The fair value for the commitments to extend credit was determined using the fees currently charged to enter into similar agreements, taking into account the remaining terms of the agreements and the present creditworthiness of the counterparties. For fixed-rate loan commitments, fair value also considers the difference between current levels of interest and the committed rates. The carrying amounts and estimated fair values of the Credit Union's financial instruments as of December 31, 2010 are as follows:

Carrying Amount

Fair Value

Financial Assets

Cash and cash equivalents $ 20,571,140 20,571,140 Certificates of deposits 8,451,942 8,482,785 Investment securities 45,493,276 45,564,309 Loans receivable 135,579,191 135,579,191 Less: allowance for loan losses (1,850,555) (1,850,555) Accrued interest receivable 703,618 703,618

$ 208,948,612 209,050,488 Financial liabilities

Members’ shares and savings accounts

$

179,940,212

179,940,212

Off-Balance-Sheet

Financial Instruments

Commitments to extend credit $ 15,471,692 15,471,692

(Continued)

40

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 19 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

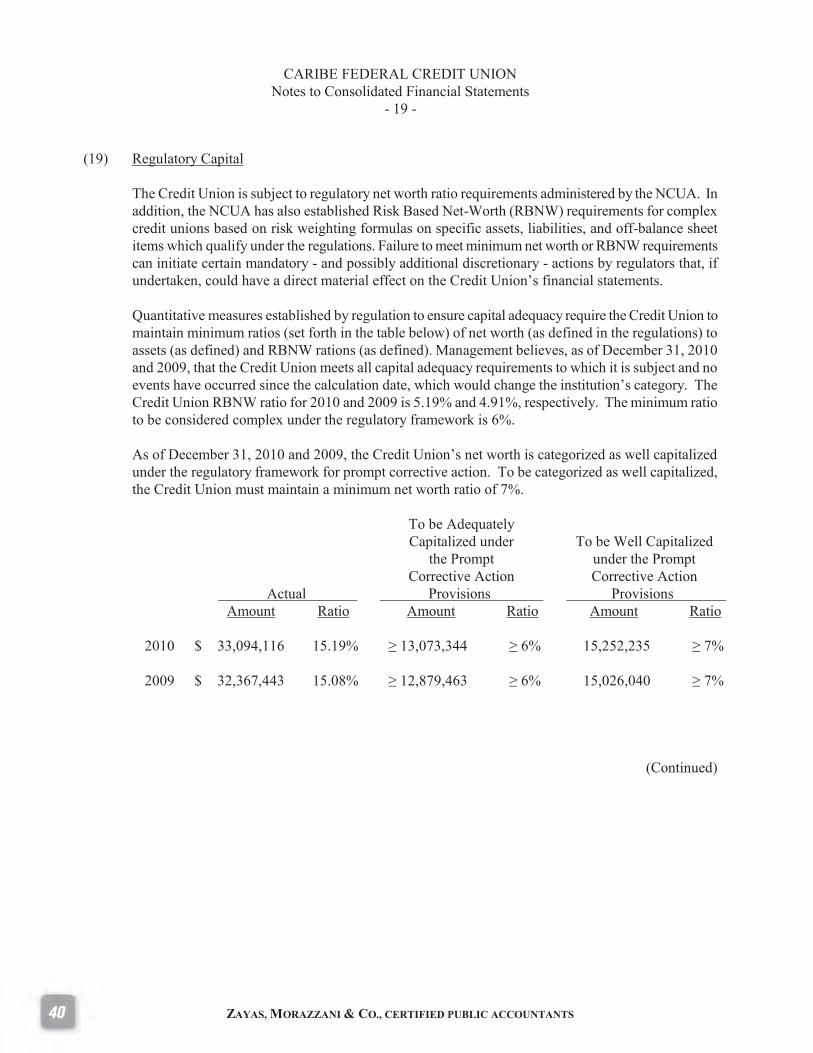

(19) Regulatory Capital

The Credit Union is subject to regulatory net worth ratio requirements administered by the NCUA. In addition, the NCUA has also established Risk Based Net-Worth (RBNW) requirements for complex credit unions based on risk weighting formulas on specific assets, liabilities, and off-balance sheet items which qualify under the regulations. Failure to meet minimum net worth or RBNW requirements can initiate certain mandatory - and possibly additional discretionary - actions by regulators that, if undertaken, could have a direct material effect on the Credit Union’s financial statements. Quantitative measures established by regulation to ensure capital adequacy require the Credit Union to maintain minimum ratios (set forth in the table below) of net worth (as defined in the regulations) to assets (as defined) and RBNW rations (as defined). Management believes, as of December 31, 2010 and 2009, that the Credit Union meets all capital adequacy requirements to which it is subject and no events have occurred since the calculation date, which would change the institution’s category. The Credit Union RBNW ratio for 2010 and 2009 is 5.19% and 4.91%, respectively. The minimum ratio to be considered complex under the regulatory framework is 6%. As of December 31, 2010 and 2009, the Credit Union’s net worth is categorized as well capitalized under the regulatory framework for prompt corrective action. To be categorized as well capitalized, the Credit Union must maintain a minimum net worth ratio of 7%.

Actual

To be Adequately Capitalized under

the Prompt Corrective Action

Provisions

To be Well Capitalized

under the Prompt Corrective Action

Provisions Amount Ratio Amount Ratio Amount Ratio 2010 $ 33,094,116 15.19% ≥ 13,073,344 ≥ 6% 15,252,235 ≥ 7%

2009 $ 32,367,443 15.08% ≥ 12,879,463 ≥ 6% 15,026,040 ≥ 7%

(Continued)

41

CARIBE FEDERAL CREDIT UNION Notes to Consolidated Financial Statements

- 20 -

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

(20) Lease Commitments During the year ended December 31, 2008, Caribe Federal Credit Union entered into a lease agreement on facilities for the administrative area. The lease term is for the five (5) years ending February 2013. Monthly rent includes associated costs such as utilities, cleaning, insurance and property tax. The future minimum lease payments required under such lease follow:

2011 $ 99,222 2012 102,695 2013 17,213

$ 219,130

BAIA operates on leased premises under a one year agreement with an entity related with a director, expiring on October 31, 2011 at a monthly charge of $500.

42

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

Schedule A

CARIBE FEDERAL CREDIT UNION Consolidating Statement of Financial Condition

December 31, 2010

CFCU BCA* Eliminations Consolidated Assets

Cash and cash equivalents $ 20,571,140 54,177 - 20,625,317 Certificates of deposits 8,451,942 - - 8,451,942 Investments available for sale 45,265,211 - - 45,265,211 Investments held to maturity 298,826 - - 298,826 Loans to members, net of allowance for

loan losses and net of origination fees

133,728,636

-

-

133,728,636 Accrued interest receivable 703,618 - - 703,618 Insurance claim receivable 20,865 - - 20,865 Account receivable, net - 13,254 - 13,254 Prepaid expenses 261,113 2,287 - 263,400 Property and equipment, net 6,340,839 7,631 - 6,348,470 NCUSIF deposit 1,675,782 - - 1,675,782 Collections 77,619 - - 77,619 Investment in unconsolidated subsidiary, net 71,736 - (71,736) - Other assets 416,660 9,464 - 426,124

Total assets $ 217,883,987 86,813 (71,736) 217,899,064

Liabilities and Members' Equity

Liabilities

Savings (shares) accounts $ 179,940,212 - - 179,940,212 Accruals and other liabilities 1,235,174 15,077 - 1,250,251 Account payable to auto dealers 3,548,819 - - 3,548,819

Total liabilities $ 184,724,205 15,077 - 184,739,282

Equity

Members' equity, substantially restricted:

Capital stock – authorized 10,000 shares with a par value of $100, issued and outstanding 5,000 shares

$

-

500,000

(500,000)

-

Additional paid-in capital - 1,000,000 (1,000,000) - Appropriated regular reserve (note 9) 3,811,746 - - 3,811,746 Unappropriated earnings 29,277,275 - - 29,277,275 Accumulated deficit - (1,428,264) 1,428,264 - Accumulated other comprehensive income 70,761 - - 70,761

Total members’ equity 33,159,782 71,736 (71,736) 33,159,782

Total liabilities and members' equity $ 217,883,987 86,813 (71,736) 217,899,064

* BCA consolidated with its subsidiary, BAIA.

See independent auditors' report and accompanying notes to financial statements.

43

ZAYAS, MORAZZANI & CO., CERTIFIED PUBLIC ACCOUNTANTS

Schedule B

CARIBE FEDERAL CREDIT UNION Consolidating Statement of Income

Years ended December 31, 2010

CFCU BCA* Eliminations Consolidated Interest income:

Interest and fees on loans $ 8,996,289 - - 8,996,289 Interest on investments 1,217,826 - - 1,217,826

10,214,115 - - 10,214,115 Dividends expense:

Savings (shares) accounts 3,130,113 - - 3,130,113

Net interest income 7,084,002 - - 7,084,002 Provision for loan losses (1,321,580) - - (1,321,580)

Net interest income after provision for loan losses

5,762,422

-

-

5,762,422

Non interest income 1,127,403 86,271 (45,411) 1,168,263

Other expenses: Compensation and benefits 2,359,616 91,796 - 2,451,412 Professional services and contracted services 201,823 95,087 - 296,910 Occupancy and utilities 192,503 - - 192,503 Communications 257,594 7,769 - 265,363 Repair and maintenance 73,954 - - 73,954 Office supplies 57,224 2,423 - 59,647 Security 37,347 - - 37,347 Insurance 181,169 2,108 - 183,277 Depreciation and amortization 451,276 16,245 - 467,521 Amortization – license fees - 12,836 - 12,836 Rent 109,186 29,557 - 138,743 Directors’ meetings and seminars 48,122 - - 48,122 Educational expenses 93,803 359 - 94,612 Annual meeting 109,458 - - 109,458 ATM and master card fees 434,437 - - 434,437 Advertising and promotion 155,556 780 - 156,336 Other 668,655 2,170 - 670,825 CUSO – service fees 45,411 - (45,411) - Loss on disposition of assets 5,250 64,992 - 70,242 Insurance commissions and fees - 14,730 - 14,730

Total other expenses 5,482,384 340,852 (45,411) 5,777,825

Income/(loss) before participation in losses of unconsolidated subsidiary

and regulatory charges

1,407,411

(254,581)

-

1,152,860 Participation in losses of unconsolidated

subsidiary

(254,581)

-

254,581

-

NCUSIF premium assessment (208,132) - - (208,132)

TCCUSF Corporate assessment (223,150) - - (223,150) Net income $ 721,578 (254,581) 254,581 721,578

* BCA consolidated with its subsidiary, BAIA.

See independent auditors' report and accompanying notes to financial statements.