propositions & programs that really work in...

TRANSCRIPT

Advancing Channel Value Propositions & Programs that really work in Distribution Julian Dent VIA International

Advancing Compelling Propositions

To advance a compelling proposition, first you have to: • Think like a distributor, understand their business model • Focus on the outcomes they are measured on • Focus on the metrics they use to assess vendor performance • Identify where they are hurting right now

Then you can put together a proposition that: • Addresses the above • Leverages your unique strengths and assets • Is clear, consistent and can be communicated by your front line

teams

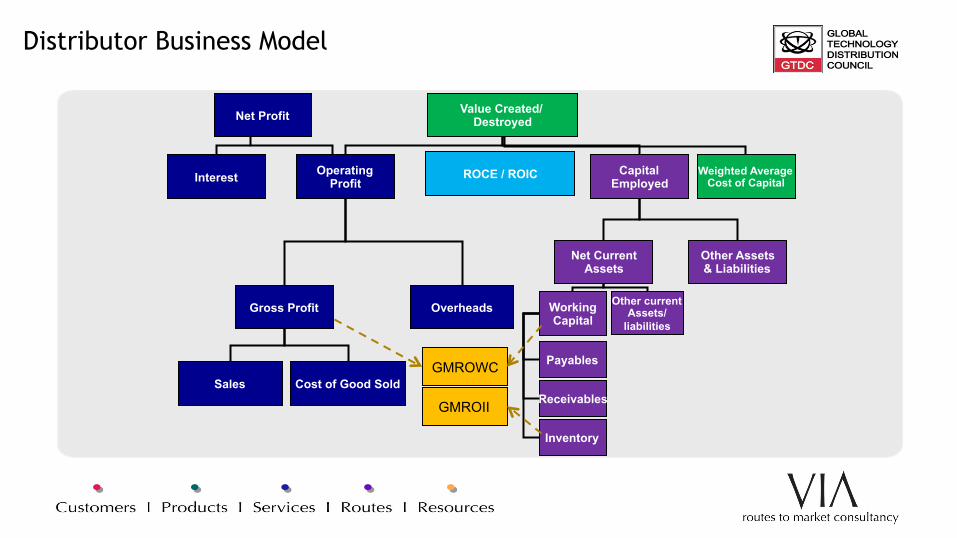

Distributor Business Model

Sales Cost of Good Sold

Gross Profit Overheads

Interest

Net Profit

Capital Employed

Net Current Assets

Payables

Receivables

Inventory

Other Assets & Liabilities

Other current Assets/

liabilities Working Capital

Weighted Average Cost of Capital

Operating Profit

Value Created/ Destroyed

ROCE / ROIC

GMROII

GMROWC

Global Broadline distributor model: Ingram Micro 2015

Global Broadline distributor model: Tech Data 2015

Global Value-Added Distributor model: Avnet 2014/15

Avnet

Year 2 June 27 , 2015 AccountsYear 1 June 28 , 2014 Accounts

Year 2 $687 2.5% $6,528 $5,422Year 1 $635 2.3% $6,272 $5,152

Year 2 $828 3.0% $10,800 $5,378Year 1 $790 2.9% $11,251 $6,099

Year 2 $3,194 11.4% $2,366 8.5% $4,272 $1,106Year 1 $3,226 11.7% $2,436 8.9% $4,979 $1,120

Year 2 $27,925 100% $24,731 88.6% $2,482 37 $934Year 1 $27,500 100% $24,274 88.3% $2,613 39 $1,577

Year 2 $5,054 66 Year 1 $5,221 69

Year 2 $3,338 49 $3,338Year 1 $3,402 51 $3,402

Year 2 $4,198 53 Year 1 $4,432 57

GMROWC Working capital

76%73%

Receivables

GMROII Payables Payables

129%123%

$1,106$1,120

Revenue Cost of Sales Inventory Other current liabilities

$2,297

Gross profit Overheads Cash Non interest liabilities Cash

10.1%

Operating profit Fixed assets Total Assets

Excess cash & non int liabs

$2,158

Net Operating profit after tax ROCE Capital

employedInvested capital

10.5%

ROIC

12.7%12.3%

Global Value-Added Distributor model: Arrow 2015

4. CEO for a Day

See if you can put yourselves into shoes of the distributor CEO

Activity: The new Distributor CEO

You have been appointed CEO of CenterState:

ê Review the 2 years of financial statements & ratios

ê Identify your three most significant positive trends over the period

ê Identify your three major areas of concern

ê Be prepared to share your answers

CenterState Distribution business model

CenterState Distribution business model

Debrief: CenterState CEO 1. Revenue up 10% and Gross

Margins up $131m

2. Operating margin up 0.2%

ê Operating Profit up 29%

ê Overheads down as % of sales and only up $56m

3. ROCE improved by 21% (6.7% à 8.1%)

DPO up 1 day

1. Cash reserves down by $471m

ê Additional $479m of WC (up 24%) to do $2.3bn (up 10%) additional turnover

2. Gross margin down 0.3%

3. Working capital up 4 days as DPO up only 1 day

ê DIO up 4 days, to 53 days

ê DSO up 1 day

GMROII down 9% & GMROWC down by 16%

ROIC down 0.1%

Key business model insights

Profit is a very small number between big numbers Capital intensive, cash flow matters Many small changes add up Earn and turn matter Key ratios and metrics

(GM%, NM%, DIO, DSO, DPO, WC Days) Combination measures are used to manage the business model

and measure vendors (ROCE, GMROII, GMROWC)

Margin trends - All Distributors

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

-5%

0%

5%

10%

15%

2008 2009 2010 2011 2012 2013 2014 2015

Reve

nue

$Thousands

Mar

gin

%Distributor Margin Trend - Total

Revenue $ Gross Margin % Overheads % Operating Margin % Net Margin % (Pre Tax)

Working Capital Broadline Distributors

0

10

20

30

40

50

60

70

80

90

2008 2009 2010 2011 2012 2013 2014 2015

Days

Distributor Working Capital Trend - Broadline

InventoryDIO

ReceivablesDSO

PayablesDPO

WorkingCapital Days

Working Capital Value Added Distributors

0

10

20

30

40

50

60

70

80

90

2008 2009 2010 2011 2012 2013 2014 2015

Days

Distributor Working Capital Trend - VAD

InventoryDIO

ReceivablesDSO

PayablesDPO

WorkingCapital Days

Developing your own Programs

• What are the distributor’s objectives?

• Which measures matter most?

• How do we as a vendor perform inside the distributor’s business model?

Business case

Vendor program Strategies Business

Priorities

• What are the distributor’s strategies?

• How does it plan to execute them?

• Which measures will change?

• What should be the business impact?

• How well does the program fit the distributor’s strategies?

• How will other distributors respond to this program?

• What measures will be affected & how?

• What is the timing and cash flow impact?

• What are the risks?

How do we perform inside the distributor’s business model?

Category report card – How are vendors performing?

How will our Vendor Program impact the distributors’ business model?

Profitability impact Working Capital impact Risks Revenues Gross Margins

(FE & BE) Cost structure Inventory Receivables Payables

Example: Assessing Vendor Programs

Program 1: • Extended credit (25 days) or Consignment stock to support channel take-up

of cloud-centric offerings • Have to take on additional specialist sales & product management headcount

(which vendor funds only 50%) • Have to support resellers delivering projects with longer implementation

cycles (resulting in increased receivables) Program 2 • PFR program which drives growing the SMB-focused reseller base because

vendor is taking larger resellers direct • Marketing funds are available to support well-engineered programs Program 3 • Quarter-end inventory loading, with additional lucrative rebate for achieving

certain volumes. Rebate to be paid on normal basis (ie 90 days after earning)

First Question: What are the distributor’s objectives (from the previous analysis)?

Profitability impact Working Capital impact Risks Revenues Gross Margins

(FE & BE) Cost structure Inventory Receivables Payables

Debrief: What are the distributor’s objectives (from the previous analysis)?

Profitability impact Working Capital impact Risks Revenues Gross Margins

(FE & BE) Cost structure Inventory Receivables Payables

Continued growth Reverse declining Gross Margins

Further reduction dependent on growth

Inventory days need reducing urgently

DSO needs reducing

Need credit lines to grow with sales

Cash facilities constrain growth

Second Question: How will the program impact the business measures of the distributor?

Debrief: Business impact of Program 1 (cloud-centric offering)

Profitability impact Working Capital impact Risks Revenues Gross Margins

(FE & BE) Cost structure Inventory Receivables Payables

Continued growth Reverse declining Gross Margins

Further reduction dependent on growth

Inventory days need reducing urgently

DSO needs reducing

Need credit lines to grow with sales

Cash facilities constrain growth

New growth from cloud services

Higher margins on new offerings

Incremental headcount costs

Neutral at best – may have to take on new SKUs

Will increase unless strong credit management on traditional business

Extended credit Cash tied up Credit limits exhausted Revenues below targets New sales staff unproductive

Debrief: Business impact of Program 2 (PFR program)

Profitability impact Working Capital impact Risks Revenues Gross Margins

(FE & BE) Cost structure Inventory Receivables Payables

Continued growth Reverse declining Gross Margins

Further reduction dependent on growth

Inventory days need reducing urgently

DSO needs reducing Need credit lines to grow with sales

Cash facilities constrain growth

Loss of revenue from larger resellers

Higher margins from SMB focused resellers

Higher account handling cost from more accounts

Neutral Will increase unless strong credit management on SMB resellers

Neutral Cannot replace lost revenue fast enough Threat to net profit if extra cost > extra funding Rebates

MDF funding to offset marketing activities

Debrief: Business impact of Program 3 (Quarter-end inventory loading)

Profitability impact Working Capital impact Risks Revenues Gross Margins

(FE & BE) Cost structure Inventory Receivables Payables

Continued growth Reverse declining Gross Margins

Further reduction dependent on growth

Inventory days need reducing urgently

DSO needs reducing Need credit lines to grow with sales

Cash facilities constrain growth

Likely to increase… or bulge

Under threat from discounting to hit volume targets

Neutral Will bulge due to loading

Will increase with vendor debit and sales bulge

Neutral Rebates passed to street so not available for financing stock Over-trading exhausts cash limits

Rebates may be consumed by discounts

Advancing Compelling Propositions

To advance a compelling proposition, first you have to: • Think like a distributor, understand their business model • Focus on the outcomes they are measured on • Focus on the metrics they use to assess vendor performance • Identify where they are hurting right now

Then you can put together a proposition that: • Addresses the above • Leverages your unique strengths and assets • Is clear, consistent and can be communicated by your front line teams How can you develop this level of mastery?

GTDC Certificate & Diploma in Distribution

This is to certify that

Julian Dent

Chairman

VIA International Ltd

Tim Curran

CEO Global Technology Distribution Council

Has achieved the GTDC accreditation standard of

Certificate

in Technology Distribution

Date awarded: 28/11/2013 Certificate no: 344991/C

BRIDGET MELLITCHEY

This is to certify that

Has achieved the GTDC accreditation standard ofDiplomain Technology Distribution

Julian DentChairmanVIA International Ltd

Tim CurranCEOGlobal Technology Distribution Council

RENTON D’SOUZA

Date awarded: 29/06/2015Diploma no: 797476/D

Gaining momentum with Vendors..

• Acer • Apple • Canon • Cisco • Eaton • Fujitsu • Hewlett-Packard • Hitachi Data Systems

• Juniper Networks • Intel • Lexmark • McAfee • Microsoft • Netapp • StarTech • Symantec • VMware

Course content

• Certificate • The role of distribution • Distributor business model • Margins & profitability • Working capital and the cash-to-cash

cycle • Productivity & capital efficiency

measures

• Diploma • The value of different distribution

models (to vendors and final tier) • Optimizing vendor–distributor

engagement • Leveraging the distribution business

model • Category management • Effective vendor propositions and

programs • New business models (services and

cloud)

Day 1 Day 2

10:30

TRAVEL 9:00 10:45

REVIEW OF DAY 1

6 PRODUCT MANAGER FOR A DAY - how to improve the numbers

1 INTRODUCTION

2 THE ROLE & VALUE OF DISTRIBUTION - Broadline & Value added - Value to vendors - Value to final tier

7 MANAGING GROWTH

3 DISTRIBUTION BUSINESS MODELS - ROCE, ROIC, Economic Profit - Benchmarks & trends

8 Business model evolution - services, - infrastructure - cloud, etc 4 CEO FOR A DAY

12:40 LUNCH

13:15 16:20

5 DISTRIBUTOR MICRO-ECONOMICS - Front end, Back end margins - Contribution profits - Stock & Working capital management - Prompt payment incentives - Portfolio Management

13:00 15:00

9 HOW TO ASSESS VENDOR PROGRAMS - compensation programs - marketing programs

10 APPLICATION TO YOUR OWN ROLE

11 PRE-EXAM PREPARATION

6 PRODUCT MANAGER FOR A DAY

TRAVEL

17:15 End of day

GTDC Diploma Course Agenda

Accreditation process

Take Diploma F2F Course

Take Diploma exam

Diploma

Take Certificate Self-study

Take Certificate

exam

Certificate

Take Certificate F2F Course

Take Certificate

Webinar

Take Certificate on-

line course

Refresher course

Typical benefits from adopting the Diploma

It helps to:

• “Change the conversation” with distributors from Margins to ROCE

• “Drive a much richer conversation with distributors about their business model, key financial metrics and the levers to improve our attractiveness as a vendor”

• “Access new levers” in the relationship

• Go into the conversations with “a Point of view” about what they want, and how to achieve it

• Think about which levers the Account Managers can control themselves, and which levers the Vendor can control

How to progress interest?

• Check out information on GTDC.org or viaint.com

• Course information leaflet

• Contact Julian for further information: • [email protected]

Thank you! Next steps:

This is to certify that

Has achieved the GTDC accreditation standard of

Diplomain Technology Distribution

Julian DentChairmanVIA International Ltd

Tim CurranCEOGlobal Technology Distribution Council

RENTON D’SOUZA

Date awarded: 29/06/2015 Diploma no: 797476/D

Your name here!