prospects for the world jute industry wbg number...

TRANSCRIPT

SCP-14

Prospects for the World Jute Industry WBG

M. Elton Thigpen and Takamasa Akiyama

WORLD BANK STAFF COMMODITY WORKING PAPERSNumber 14

C.hokel BoF omirH k l-001

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

WORLD BANK STAFF COMMODITY WORKING PAPERS

1. The World Tin Economy: An Econometric Analysis (out of print)

2. International Cotton Market Prospects

3. An Econometric Model of the World Rubber Economy

4. Industrial Processing of Natural Resources

5. The World Sugar Economy: An Econometric Analysis of Long-term Developments

6. World Bank Commodity Models (2 volumes)

7. Analysis of the World Coffee Market

8. Analysis of the World Cocoa Market

9. The Outlook for Primary Commodities

10. World Rubber Market Structure and Stabilisation: An Econometric Study

11. The Outlook for Primary Commodities, 1984 to 1995

12. The Outlook for Thermal Coal

13. Jute Supply Response in Bangladesh

WORLD BANK STAFF COMMODITY WORKING PAPERSNumber 14

Prospects for the World Jute Industry

M. Elton Thigpen and Takamasa Akiyama

The World BankWashington, D.C., U.S.A.

Copyright CC 1986The International Bank for Reconstructionand Development / THE WORLD BANK

1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

All rights reservedManufactured in the United States of AmericaFirst printing January 1986

This is a document published informally by the World Bank. In order that theinformation contained in it can be presented with the least possible delay, thetypescript has not been prepared in accordance with the procedures appropriate toformal printed texts, and the World Bank accepts no -, sponsibility for errors. Thepublication is supplied at a token charge to defray part of the cost of manufacture anddistribution.

The World Bank does not accept responsibility for the views expressed herein, whichare those of the author(s) and should not be attributed to the World Bank or to itsaffiliated organizations. The findings, interpretations, and conclusions are the resultsof research supported by the Bank; they do not necessarily represent official policy ofthe Bank. The designations employed, the presentation of material, and any maps usedin this document are solely for the convenience of the reader and do not imply theexpression of any opinion whatsoever on the part of the World Bank or its affiliatesconcerning the legal status of any country, territory, city, area, or of its authorities, orconcerning the delimitation of its boundaries or national affiliation.

The full range of World Bank publications, both free and for sale, is described in theCatalog of Publications; the continuing research program is outlined in Abstracts ofCurrent Studies. Both booklets are updated annually; the most recent edition of each isavailable without charge from the Publications Sales Unit, Department T, The WorldBank, 1818 H Street, N.W, Washington, D.C. 20433, U.S.A., or from the EuropeanOffice of the Bank, 66 avenue d'1lna, 75116 Paris, France.

M. Elton Thigpen and Takamasa Akiyama are economists in the Commodity Studiesand Projections Division of the World Bank.

Library of Congress Cataloging-in-Publication Data

Thigpen, M. Elton, 1932-Prospects for the world jute industry.

(World Bank staff commodity working paper,ISSN 0253-3537 ; no. 14)

Bibliography: p.1. Jute industry. I. Akiyama, T. (Takamasa),

1944- . II. Title. III. Series.HD9156.J7T45 1986 338.4'767713 85-31467ISBN 0-8213-0701-0

- iii -

ABSTRACT

Prospects for the world jute industry to the mid-1990s are analyzedto identify trends likely to follow the confusion in the jute market originat-ing from the 1984/85 fiber supply crisis. These prospects are derived fromanalysis of information obtained from surveys of jute demand in severalcountries and from simulation results from a recently built econometric modelof the world jute economy.

Jute fiber is used primarily as a textile raw material for makingpackaging products, carpets, industrial fabrics and twine. Its main demandbase is derived from the need to package agricultural inputs and produce incountries where storage and distribution to wholesale and retail markets is inpackaged form. Structural changes occurring in the world demand for jute areidentified. Prospects for the expansion of jute consumption for packaginguses in developing countries are fairly bright since the scope for earlychanges to bulk-handling and synthetic substitution are limited.

The rapid loss of markets for jute sacks and bags to bulk handling inthe industrial countries and grain-exporting developing countries during the1970s has about run its course. So have the losses of fabric markets wheresynthetic products held distinct advantages in technical performance or cost.The resulting structural shifts in the regional distribution of consumptionand changes in the product composition of final demand suggest that the growthin world demand for jute to the mid-1990s should be somewhat higher than wasattained during the 1970s and early 1980s.

The sharp output decline in India and Bangladesh in 1984 appears tohave started another price/supply cycle. On past performance it is likelythat the high prices of 1984/85 will lead to large output increases in the1985/86 and 1986/87 harvests causing prices to fall and leading to a period oflow prices and low output in the late 1980s.

- iv -

ACRONYMS AND ABBREVIATIONS

BWD - Bangladesh White Grade D Raw JuteCBC - Carpet Backing ClothCPEs - Centrally Planned Economies of Eastern Europe and USSREPDCS - Economic Analysis and Projections Department

Commodity Studies and Projections Divisionfob - Free On BoardFAO - Food and Agriculture OrganizationGNP - Gross National ProductMT - Metric Tonoz. - ounceP.A. - Per AnnumSq. Yds. - Square YardsUSSR - Union of Soviet Socialist Republic% - Percent$ - United States Dollar

CONVERSION FACTORS

I maund = 37.326 kg1 bale = 18t) kg = 4.822 maunds1 long ton = 1.016 metric ton

TABLE OF CONTENTS

ABSTRACT............................................................ iii

ACRONYMS AND ABBREVIATIONS........ ............. ........................... iv

LIST OF TABLES. ..................................................... vii

LIST OF FIGURES .................. ... viii

I. INTRODUCTION AND SUMMARY ........................ .................... I

II. ASSUMPTIONS IN KEY EXOGENOUS VARIABLES .............................. 6

III. JUTE PRODUCTION: RECENT TRENDS AND PROSPECTS... ..................... 8

Future Prospects for Jute Production........................... 11

IV. WORLD DEMAND FOR JUTE: RECENT TRENDS ............................... 17

V. ANALYSIS OF DEMAND FOR JUTE: BY COUNTRIES AND REGIONS.oO... NS...0..0 26

Industrial Countries.... ... o.. ..out ri........... o....es..e... 26

ad North A 27b. Western Eart peopee..........*............ 31Co3aa 38do utai 41

Developing Countriesa....o.o.....o..o......................... 43

as B p ndlthesSSR.l a d e sh.. . .. . . . . . . o. . ... oo ... . 43be ondia 44c.ohi ln 45d.oai sa 46e Cia47f. Near Eat48g.ofrc 49h. Latin Amerca..... 50

Brazil ~~~~~~~~~~~~~~~51Cuba ~~~~~~~~~~~~~~~52

Eastern Europe and the USSSSRooo.oooosooooeee 52

Rest of the Worrld. 54

- vi -

TABLE OF CONTENTS

Annex I: AN ECONOMETRIC MODEL FOR THE WORLD JUTE ECONOMY ............... 57

The Demand Block ......... ...... ... 58The Supply Block ......... ...... ... ......... 62Stocks and Prices ................................... O ... 66

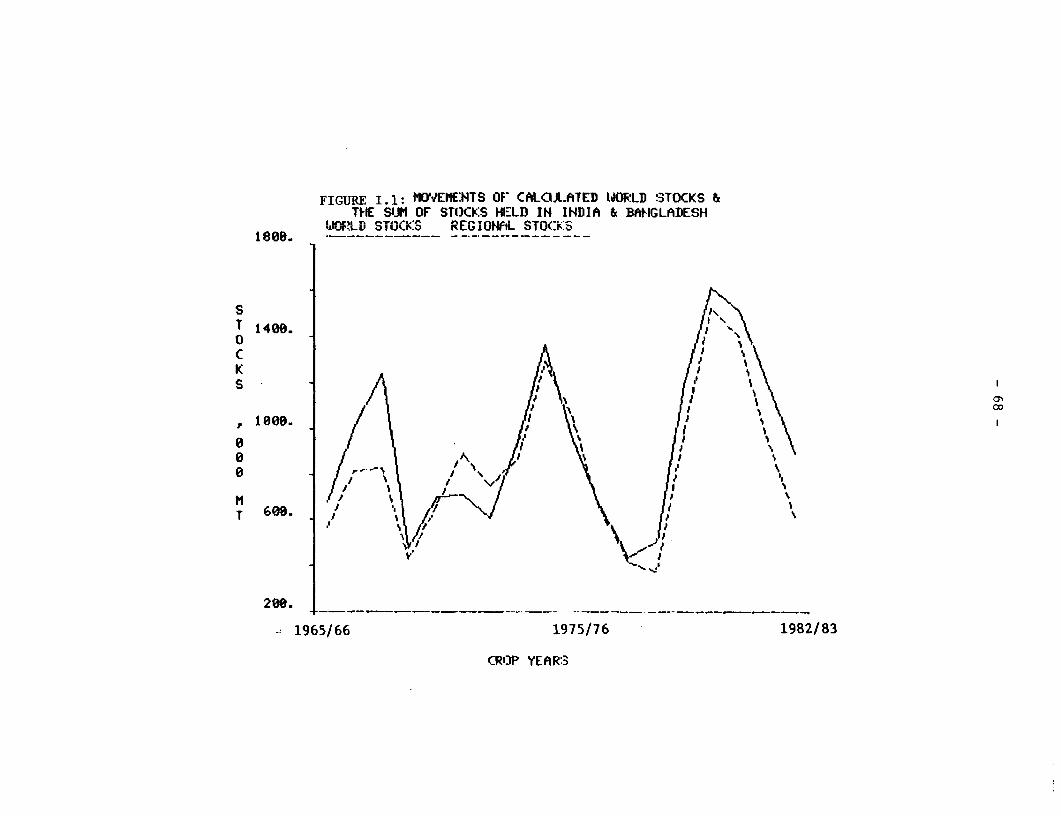

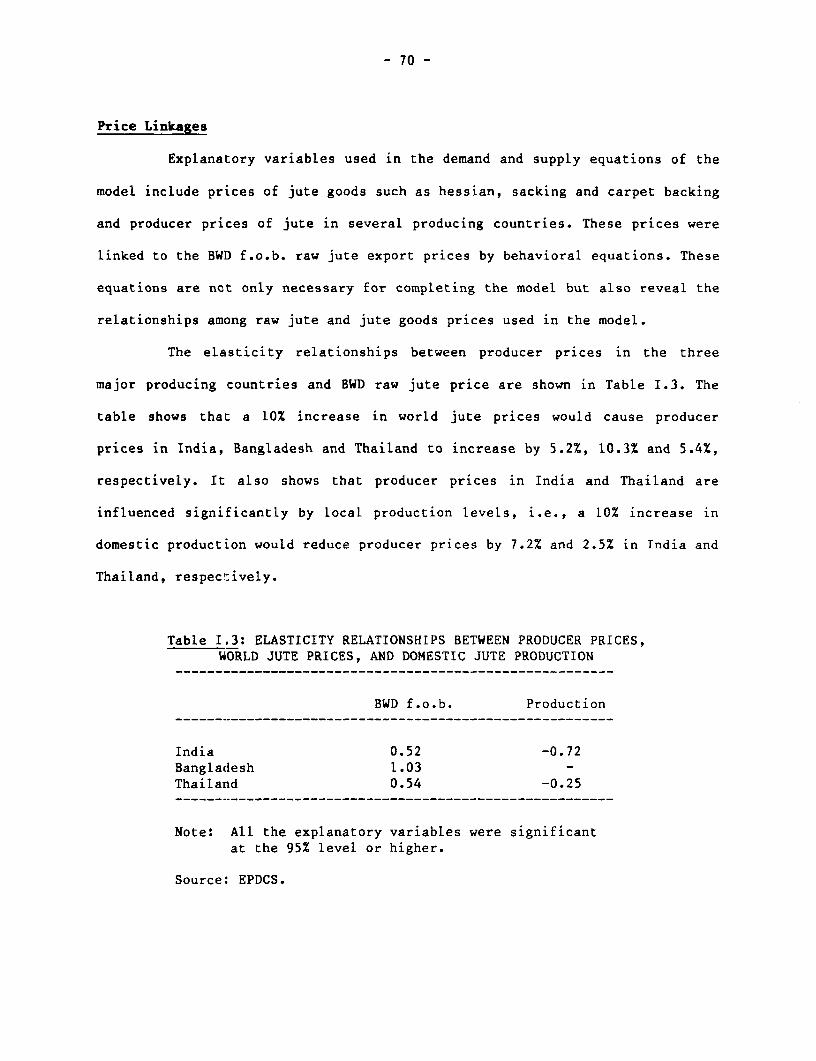

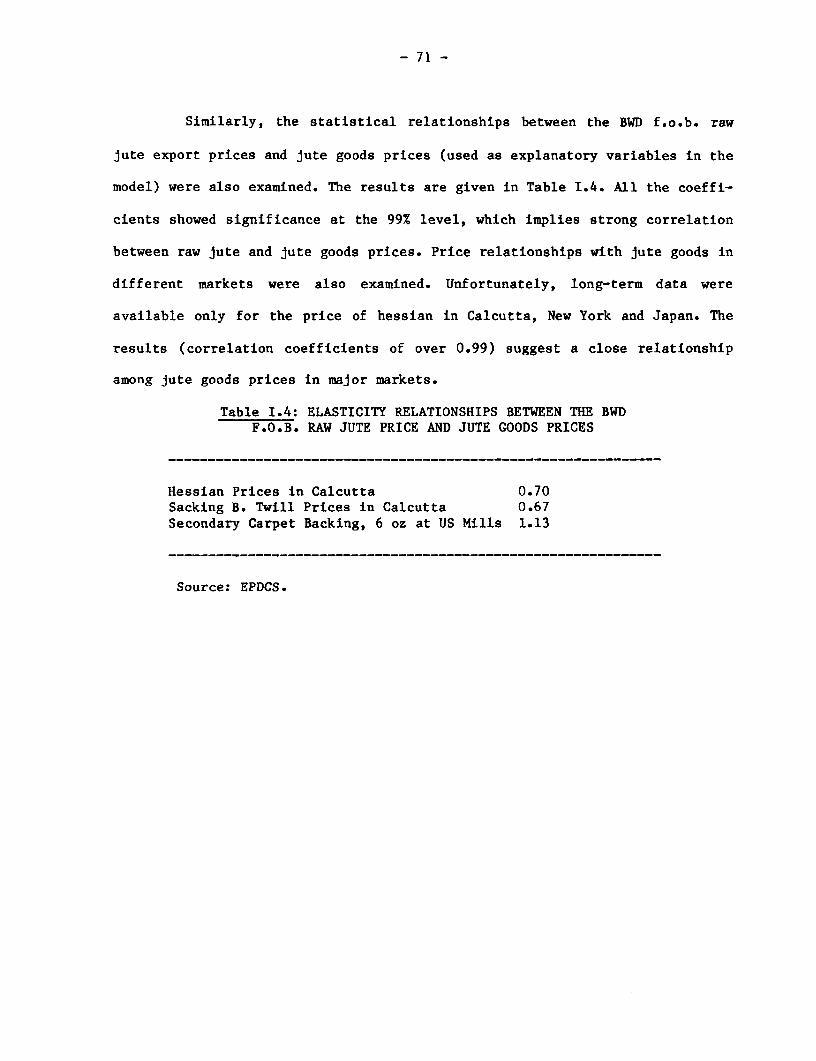

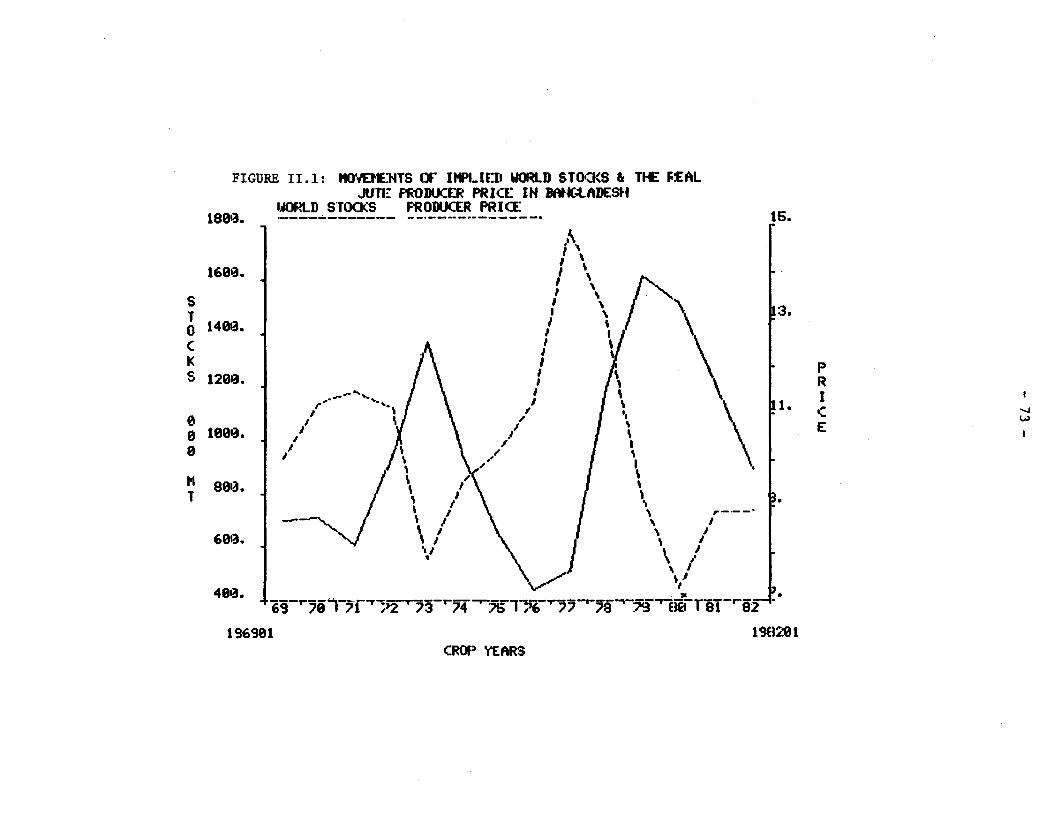

Price Linkages CFLTUIO IN ..E WORL .JUT MRE......... 70

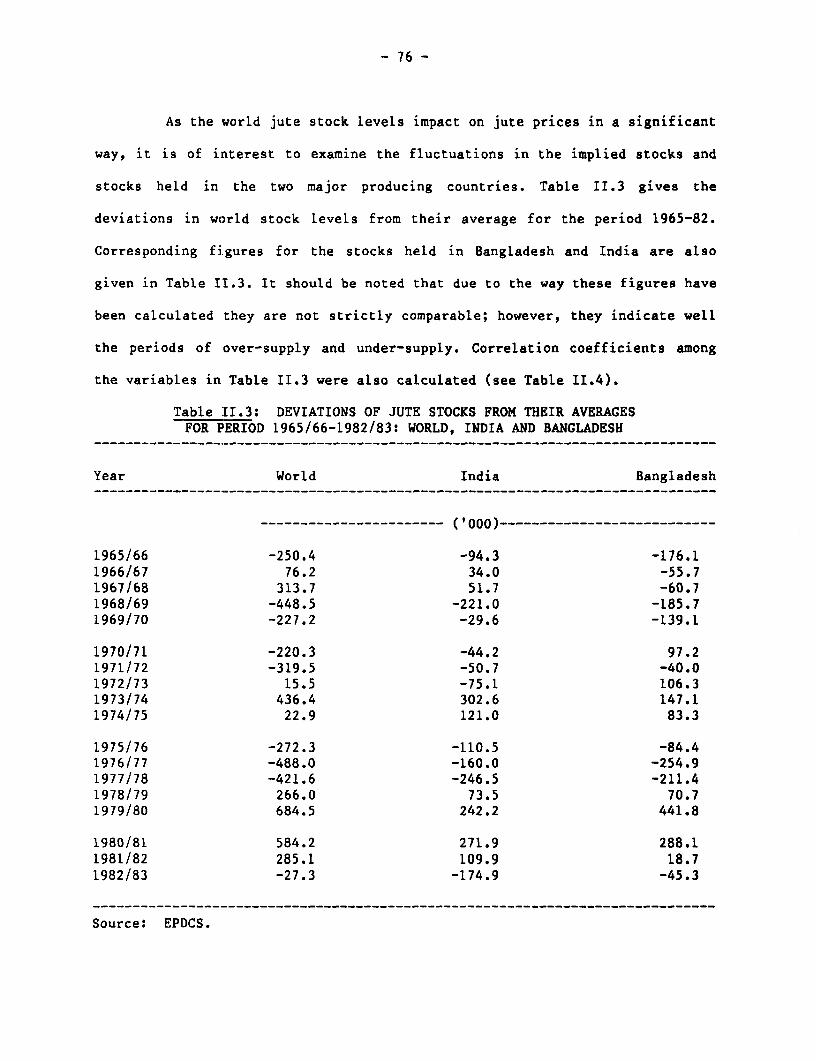

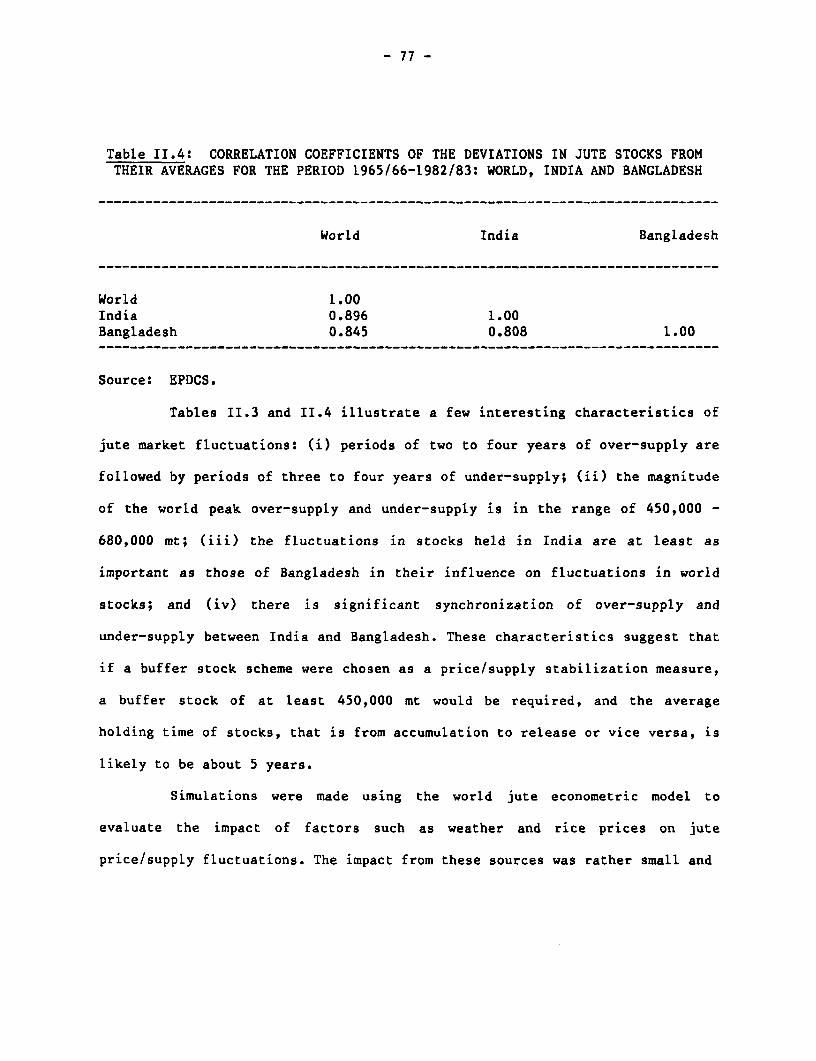

Annex II: ANALYSIS OF PRICE FLUCTUATIONS IN THE WORLD JUTE MARKET. T.. 72

REFERENCES: ... ... 00000.0.. 79

- vii -

LIST OF TABLES

Table

Table 1: Average Historical and Projected Jute Consumption and GrowthRates in Major Countries and Regions......**................ 4

Table 2: Major Exogenous Variable Growth Assumptions 1983 to 1995 ..... 7

Table 3: Jute Production in Major Countries ....... . ...... .... 10

Table 4: Average Historical and Projected Jute Production andGrowth Rates in Major Producing Countries*r........ e..*.... 14

Table 5: Jute Fiber and Product Imports 1981-83 and Implied ImportRequirements to Meet Projected Demand in 1993-95.............. 16

Table 6: Jute Goods Production by Type of Products .................... 17

Table 7: Jute Goods Production and Shares by MajorProducing Countries.*.. .. e.......... 18

Table 8: Jute - Apparent Consumption and Shares by Major ConsumingCountries/Regions..o..o.. .......................... .... ..... 20

Table 9: Jute Goods Exports by Origin. ............................. 22

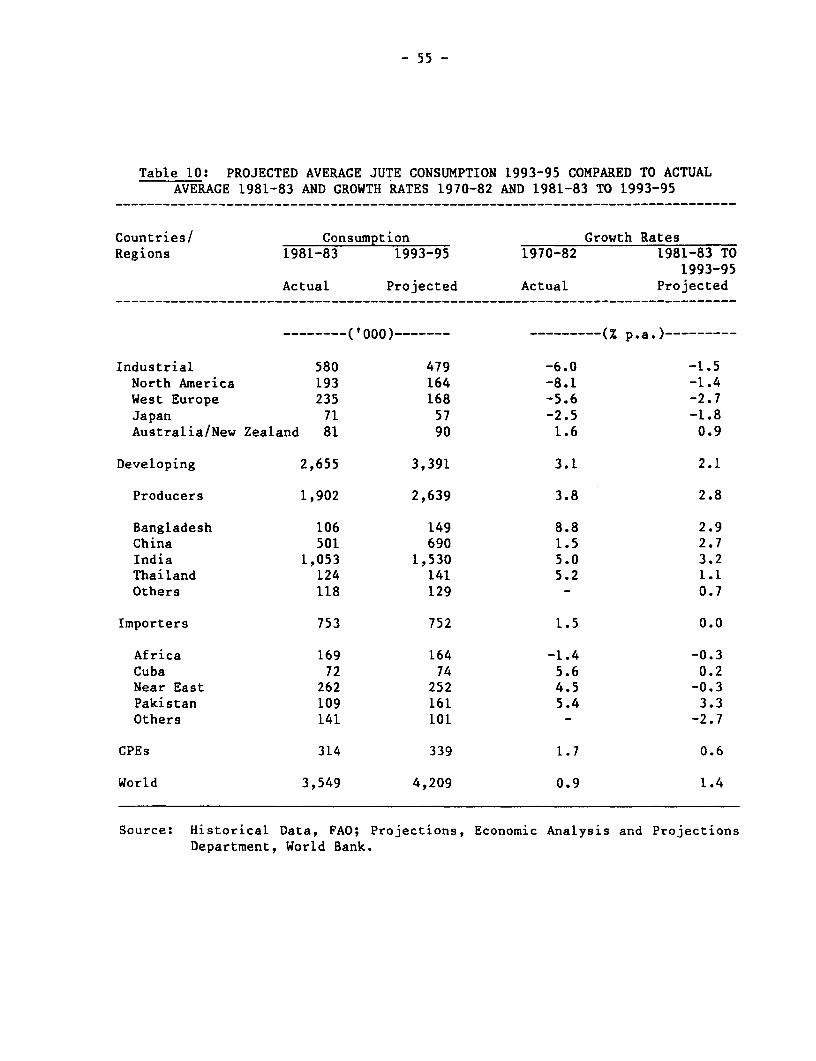

Table 10: Projected Average Jute Consumption 1993-95 Compared toActual Average 1981-83 and Growth Rates 1970-82 and1981-83 to 1993-95 ........ .................... 55

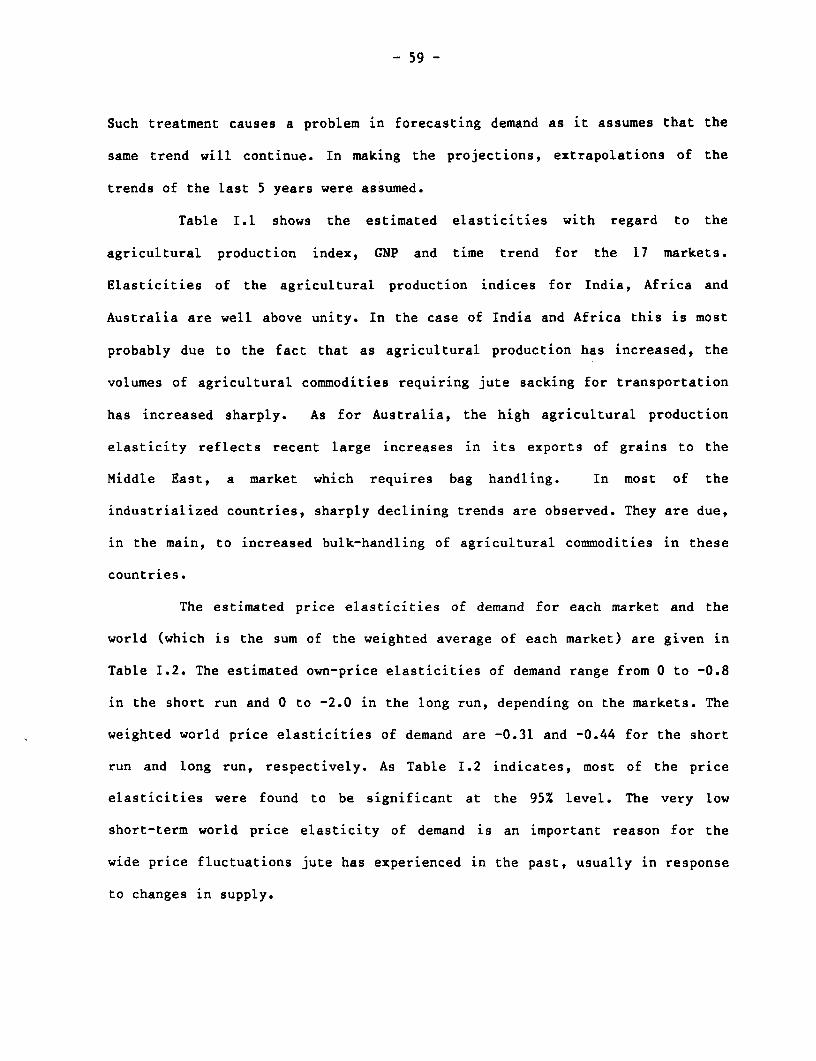

Table 1.1: Elasticities with Regard to the Agricultural ProductionIndex, GNP and Time Trend .... .. .... ....... ............. 60

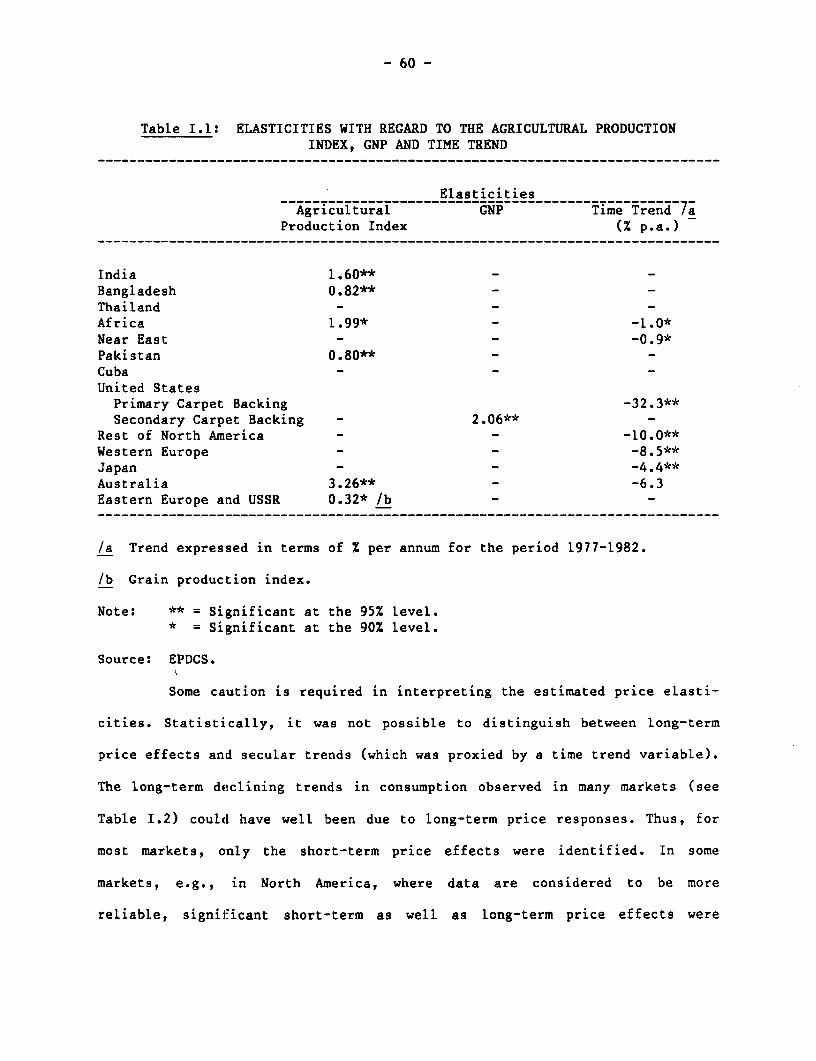

Table I.2: Short and Long Term Own-Price Elasticitiesof Demand for Jute..................................... 61

Table I.3: Elasticity Relationships between Producer Prices, WorldJute Prices, and Domestic Jute Production........o..o..o.. 70

Table I.4: Elasticity Relationships between the BWD F.O.B. Raw JutePrice and Jute Goods Prices..r. *.*# ............. o. .o. .o.*oo 71

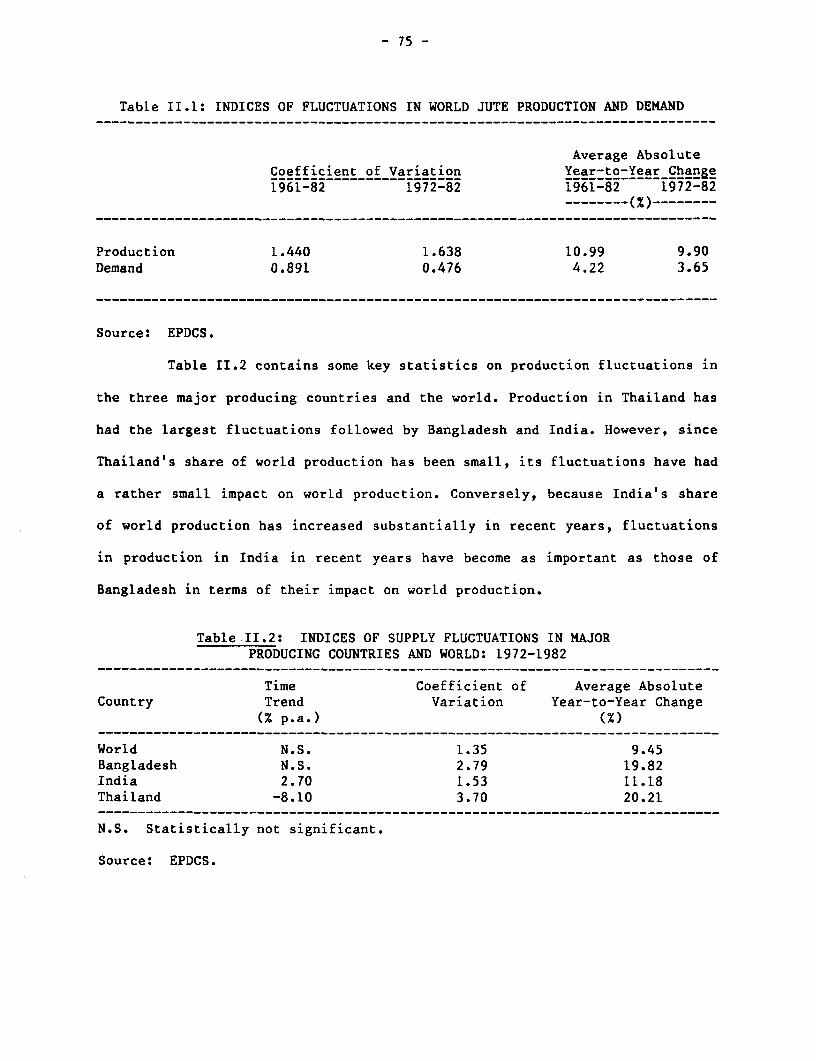

Table 11.1: Indices of Fluctuations in World Jute Productionand Demne...m.............ndooo.s 75

Table II.2: Indices of Supply Fluctuations in Major ProducingCountries and World: 1972-1982 .............................. 75

- viii -

LIST OF TABLES

Table

Table II.3: Deviations of Jute Stocks from their Averages forPeriod 1965/66-1982/83: World, India and Bangladesh......... 76

Table II.4: Correlation Coefficients of the Deviations in Jute Stocksfrom their Averages for the Period 1965/66-1982/83:World, India and Bangladesh. ............ . . . . . .............. . .. ...... 77

LIST OF FIGURES

Figure 1: Jute Production in Major Countries and the World............. 12

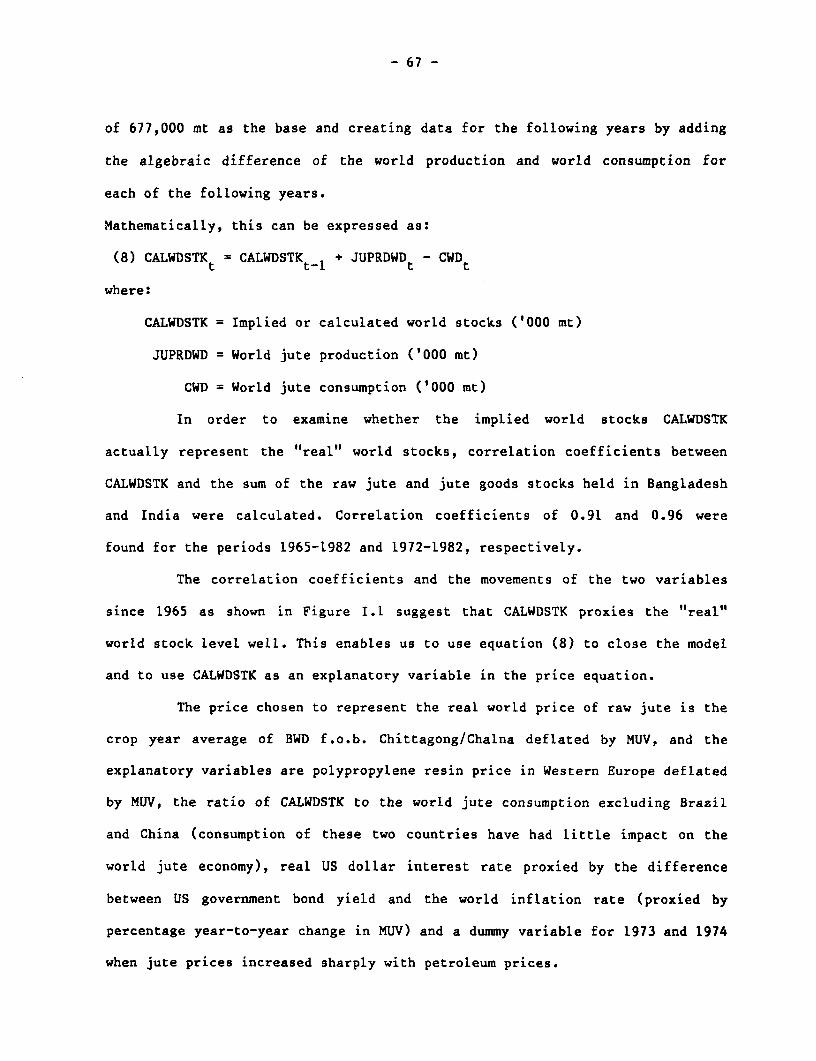

Figure I.l: Movements of Calculated World Stocks & the Sum of StocksHeld in India & Bangladesh. . . .. . . . . .. s... . . . . ... . . . . . . . . . . . . . . 68

Figure II.1: Movements of Implied World Stocks & the Real Jute ProducerPrice in Bangladesh ............................. .............. 73

- 1 -

I. INTRODUCTION AND SUMMARY

The world jute economy was severely shocked in 1984 when dry weather

during the sowing period, combined with very serious flooding during the

growing season, reduced jute production in Bangladesh and India to well below

growers' intended levels. The impact of the production shortfall on the jute

market was particularly strong because the stocks accumulated through 1979/80

had been liquidated during the next three years of relatively low prices and

output. As a result, with sharply reduced supplies faced with inelastic

short-term demand, raw jute prices climbed to record levels before export

sales by private traders were banned by the two largest fiber exporting

countries, Bangladesh and Thailand. In view of the ensuing disarray in the

jute market, an assessment of jute's medium and long-term outlook is of

particular importance at this time.

In this paper, prospects for the world jute industry to the mid-1990s

are presented in the light of information obtained from surveys of jute demand

in several countries and from simulation results of an econometric model

recently built at the World Bank. The regional and global prospects are

presented along with a description of the underlying assumptions and an

analysis of their implications. A description of the jute model is contained

in Annex I. Annex II contains an analysis aimed at identifying causes of

instability in the jute economy.

The key jute variables are projected to fluctuate rather widely in

response to the extremely tight supply position reached during 1984/85 and the

resulting record nominal prices. A sharp production decline in both India and

- 2 -

Bangladesh in 1984 thus appears to have started another price/supply cycle. 1/

Typically, the response to current price levels would carry through at least

to the next two crops in the major producing countries. The fiber

supply/demand imbalance in 1983/84 should result in attractive producer prices

for the 1985/86 crop, which should, in turn, encourage grower efforts to pro-

duce a second consecutive large crop in 1986/87. Barring disastrous weather,

large crops during those two years will exceed consumption requirements,

restore stocks and cause prices to fall to more moderate levels. On past per-

formance it would be most unusual, however, if the response of jute production

to the shock of current high prices did not lead to an overshooting of demand,

providing the conditions for another cycle of low prices and production in the

late 1980s. Based on historical levels of response, the simulations indicate

that the accumulation of excess stocks could cause real jute prices to decline

to around $250 per ton by 1988/89. Such a price level would again make jute

growing less attractive relative to rice and reduce jute production. Barring

further weather-induced shocks, the simulations indicate that the cyclical

movements should continue, with another real price peak of around $400 per ton

in 1991/92. The long-run average real prices necessary to stimulate production

to the level of projected demand appears to be around $300-$330 per ton, in

terms of 1984 US dollars, basis BWD, f.o.b. Bangladesh.

There are promising prospects that world demand for jute will grow

faster over the next decade than the rate achieved during 1970-82, due to

structural shifts in the regional distribution of consumption and changes in

1/ As discussed in detail in Annex II, world jute price fluctuations aremainly caused by supply fluctuations in Bangladesh and India.

- 3 -

the product composition of final demand in the industrial countries. Even so,

the direction of trends is expected to change in only a few countries/regions.

The expectation for improved growth in jute consumption derives from the

circumstances which resulted in jute's sharp losses during the 1970s having

about run their course. For example, the technical performance and cost

advantages of synthetic substitutes for jute primary carpet backing for tufted

carpets and for cotton bale covers under United States trading conditions have

reduced jute's share of these uses to only marginal proportions. On the other

hand, jute's outstanding performance in secondary carpet backing has increased

the share of this product in the total demand for jute in the industrial

countries and the expected future growth of secondary carpet backing should

offset some of the further decline expected in the use of other jute products-

-moderating the rate of decline in overall jute consumption in North America,

Western Europe and Japan.

The other major cause of erosion in jute demand in recent years was

the rapid adoption of bulk-handling methods for grains and materials formerly

packaged in jute bags. This transition is virtually complete in the industrial

countries and in the major grain-exporting developing countries. Growth in

demand for jute sacking and wrapping fabrics is still favorable in the jute-

producing countries and in the agricultural producing countries where storage

and distribution to wholesale and retail markets is in packaged form. Con-

sidering these changes in the geographical distribution and product

composition of jute consumption, world demand is projected to grow at an

average of 1.4% per year from 1981-83 to 1993-95 compared to 0.9% per year in

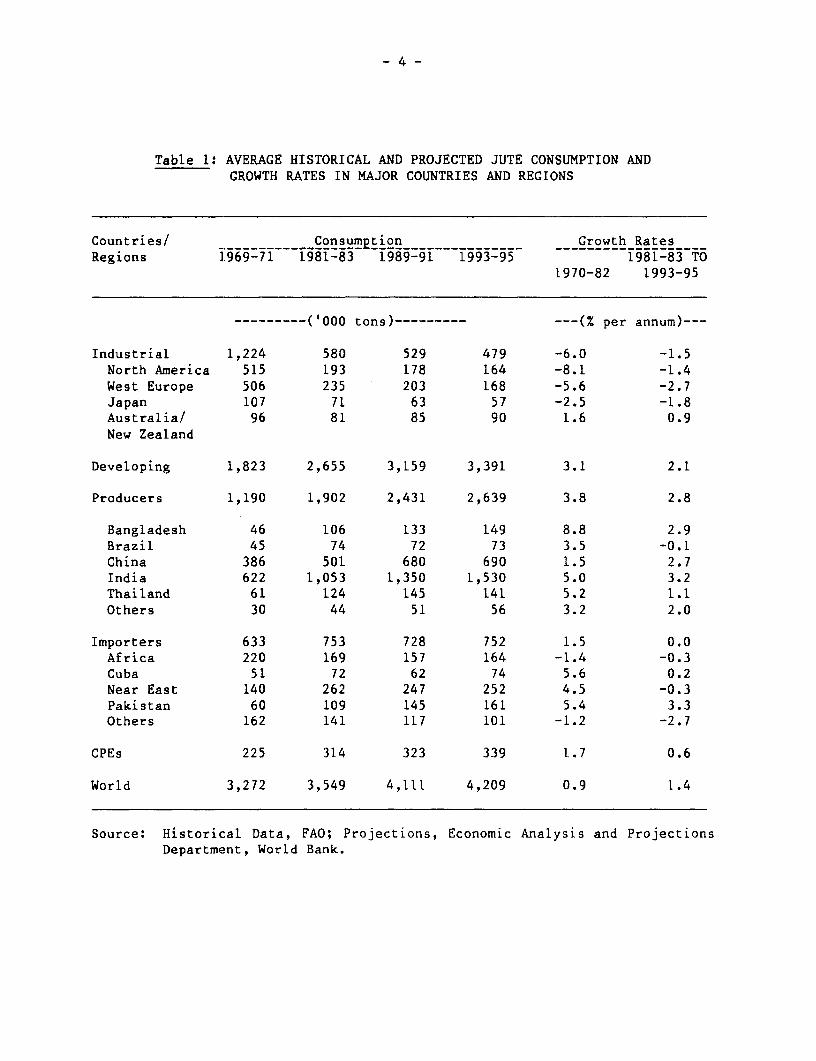

the 1970-82 period (Table 1).

- 4 -

Table 1: AVERAGE HISTORICAL AND PROJECTED JUTE CONSUMPTION ANDGROWTH RATES IN MAJOR COUNTRIES AND REGIONS

Countries/ ConsunpLtion Growth RatesRegions 1969-71 1981-83 1989-91 1993-95 1981-83 TO

1970-82 1993-95

---------('000 tons) --------- ---(% per annum)---

Industrial 1,224 580 529 479 -6.0 -1.5North America 515 193 178 164 -8.1 -1.4West Europe 506 235 203 168 -5.6 -2.7Japan 107 71 63 57 -2.5 -1.8Australia/ 96 81 85 90 1.6 0.9New Zealand

Developing 1,823 2,655 3,159 3,391 3.1 2.1

Producers 1,190 1,902 2,431 2,639 3.8 2.8

Bangladesh 46 106 133 149 8.8 2.9Brazil 45 74 72 73 3.5 -0.1China 386 501 680 690 1.5 2.7India 622 1,053 1,350 1,530 5.0 3.2Thailand 61 124 145 141 5.2 1.1Others 30 44 51 56 3.2 2.0

Importers 633 753 728 752 1.5 0.0Africa 220 169 157 164 -1.4 -0.3Cuba 51 72 62 74 5.6 0.2Near East 140 262 247 252 4.5 -0.3Pakistan 60 109 145 161 5.4 3.3Others 162 141 117 101 -1.2 -2.7

CPEs 225 314 323 339 1.7 0.6

World 3,272 3,549 4,111 4,209 0.9 1.4

Source: Historical Data, FAO; Projections, Economic Analysis and ProjectionsDepartment, World Bank.

The projected increase in demand for jute is seen to be largely

generated by the need to package agricultural inputs and produce in the jute-

producing countries, as well as Pakistan and the USSR. India and China are

expected to account for most of the projected increase in demand for jute.

Increases in domestic production should be enough to meet their demand growth

leaving combined annual export supply at around 200-300,000 tons.

Simulation results from the jute model indicate that Bangladesh will

be next in importance to India in meeting the projected increase in world

demand for jute. A comparison of the jute production and consumption projec-

tions indicates that most of the increase in production in Bangladesh will be

available for export as fiber and manufactured products. Export supplies (both

fiber and manufactured products) from Bangladesh during the mid-1990s are

projected to rise to around one million tons per year.

World import requirements in the mid-1990s are expected to total

around 1.1 million tons of jute goods (fiber equivalent) and over 400,000 tons

of jute fiber. The estimated volumes of imports of hessian, sacking, carpet

backing and fiber required by each region are presented in Table 5. The

product break-down is based on past trends, expected further shifts in market

requirements and continuation of import policies that discriminate against

trade in manufactured products. In general, carpet backing is expected to

account for an increasing share of jute requirements in the industrial

countries. Many developing countries could meet their jute product require-

ments at lower cost by importing manufactured goods, but such a shift is being

discouraged by escalating tariff structures.

-6-

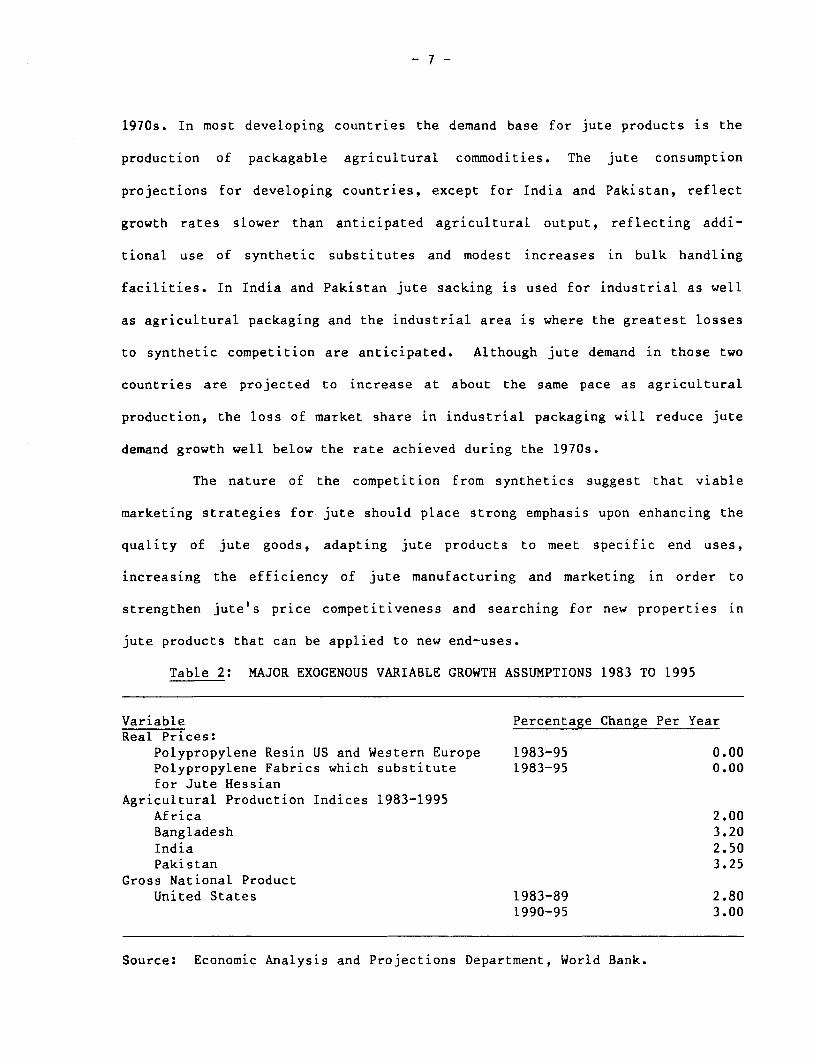

II. ASSUMPTIONS ON KEY EXOGENOUS VARIABLES

Some of the key variables that impact on the jute economy and assump-

tions regarding their growth prospects to the mid-1990s are presented in

Table 2.

Among these exogenous, variables the polypropylene resin price is the

most important one in terms of its impact on the jute market. Polyolefin

plastics, mainly polypropylene and polyethylene, challenge jute products for

market share in each major jute end-use. Polypropylene is the single most

important synthetic substitute for jute. It is a product of the petrochemical

industry, its resin form being derived by the polymerization of propylene. The

derivation of its feedstock from the petroleum and gas industries links its

prospects to the outlook for these industries. Polypropylene's potential com-

petitiveness is also greatly influenced by recent technical developments in

manufacturing processes and the third generation of catalysts. These cost-

efficient processes and materials are being rapidly adopted and will add to

the near-term weakness of feedstock costs to keep polypropylene substitute

products highly cost-competitive with jute goods. The assumption in the model

is that the real prices of the synthetic resin and products will remain at the

1984 level in the projection period. The impact of anticipated higher feed-

stock costs on real prices of resin and products in the first half of the

1990s is expected to be fully offset by the industry-wide adoption of the new

process technologies.

The model-generated projections of jute demand and real prices take

into account this competition from synthetic substitutes. The competition

between jute and polypropylene has been most severe in the industrial and

grain-exporting developing countries and jute consumption is projected to

continue declining in those regions, although at a slower rate than in the

-7 -

1970s. In most developing countries the demand base for jute products is the

production of packagable agricultural commodities. The jute consumption

projections for developing countries, except for India and Pakistan, reflect

growth rates slower than anticipated agricultural output, reflecting addi-

tional use of synthetic substitutes and modest increases in bulk handling

facilities. In India and Pakistan jute sacking is used for industrial as well

as agricultural packaging and the industrial area is where the greatest losses

to synthetic competition are anticipated. Although jute demand in those two

countries are projected to increase at about the same pace as agricultural

production, the loss of market share in industrial packaging will reduce jute

demand growth well below the rate achieved during the 1970s.

The nature of the competition from synthetics suggest that viable

marketing strategies for jute should place strong emphasis upon enhancing the

quality of jute goods, adapting jute products to meet specific end uses,

increasing the efficiency of jute manufacturing and marketing in order to

strengthen jute's price competitiveness and searching for new properties in

jute products that can be applied to new end-uses.

Table 2: MAJOR EXOGENOUS VARIABLE GROWTH ASSUMPTIONS 1983 TO 1995

Variable Percentage Change Per YearReal Prices:

Polypropylene Resin US and Western Europe 1983-95 0.00Polypropylene Fabrics which substitute 1983-95 0.00for Jute Hessian

Agricultural Production Indices 1983-1995Africa 2.00Bangladesh 3.20India 2.50Pakistan 3.25

Gross National ProductUnited States 1983-89 2.80

1990-95 3.00

Source: Economic Analysis and Projections Department, World Bank.

- 8 -

III. JUTE PRODUCTION: RECENT TRENDS AND PROSPECTS

Jute 1/ has been grown in Bengal and other areas for centuries. It is

an annual plant which grows best in hot, damp climates. It requires relatively

large amounts of agricultural labor for cultivation and industrial labor for

processing into a variety of products. The jute plant contains a bast fiber

that is separated from the stem and bark after retting in water. Although over

30 species are known, only two, Corchorus capsularis (white jute) and

Corchorus olitorius (tossa jute) are widely grown.

Jute production is centered in Asia, with the four major producing

countries--Bangladesh, China, India and Thailand--accounting for 92% of world

output during 1981-83. Another 2% of world output was in Latin America,

mostly in Brazil. In South Asia, jute is produced mainly by subsistence

farmers as a cash crop in competition for land with food crops, primarily rice

(paddy). The acreage devoted to jute cultivation is quite responsive to

changes in relative prices of jute and paddy at the farm level and, hence, to

each crop's expected contribution to net profitability of the farm operation.

In addition to relatively large shifts in jute acreage, year-to-year

variations in production are also caused by changes in yields due to seasonal

differences in growing conditions. Both flooding and, to a lesser extent,

drought are hazards to jute growing. The quality of jute fiber is also

strongly influenced by the availability and quality of retting water used to

prepare the plant for separation of the fiber from the stem and bark. Jute

I/ In this report, jute includes similar fibers such as kenaf (grownprincipally in Thailand), malva (grown in Brazil) and mesta (grown inBangladesh and India) which are used mainly in the manufacture of sacksand bags.

-9-

sticks--the wood stem from which the fiber is separated--are about twice the

weight of the fiber. Historically, jute sticks have been used for such

household purposes as firewood, fencing and roofing and were of substantially

lower value than the fiber. More recently, jute sticks have been a source of

wood fiber for making paper. This use, combined with the increasing scarcity

of firewood in producing areas, has raised the value of sticks relative to the

value of the fiber.

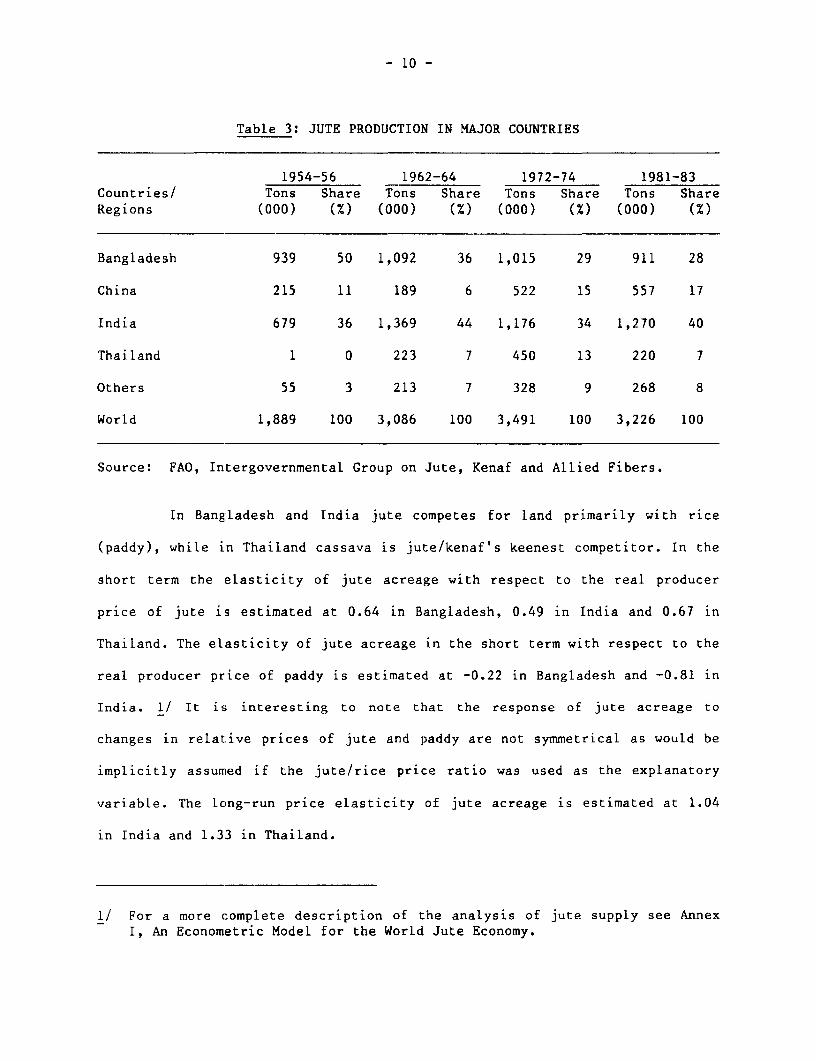

Although jute production is concentrated in a few countries, crop

developments in these countries have been diverse. Prior to the 1950s, more

than half of the world's supply was produced in the area now constituting

Bangladesh and nearly one-third was grown in India. At that time Indian mills,

concentrated in the Calcutta area, accounted for about one-half of world

consumption and mills in Western Europe accounted for about one-fifth of the

total. The expansion of jute production from the mid-1950s to the mid-1960s

centered on the efforts made by India to achieve self-sufficiency in produc-

tion and on the emergence of Thailand as an important exporter of fiber.

Average yields remained stagnant during that period and nearly aLl the

expansion in production resulted from increased jute acreage. World production

of jute grew very slowly (0.4X per annum) over the period 1961-82, despite a

surge in production in China (Table 3). I/

1/ Caution is indicated since Chinese production estimates are derived fromcombined production statistics for jute and ambry hemp.

- 10 -

Table 3: JUTE PRODUCTION IN MAJOR COUNTRIES

1954-56 1962-64 1972-74 1981-83Countries/ Tons Share Tons Share Tons Share Tons ShareRegions (000) (%) (000) (%) (000) (%) (000) (M)

Bangladesh 939 50 1,092 36 1,015 29 911 28

China 215 11 189 6 522 15 557 17

India 679 36 1,369 44 1,176 34 1,270 40

Thailand 1 0 223 7 450 13 220 7

Others 55 3 213 7 328 9 268 8

World 1,889 100 3,086 100 3,491 100 3,226 100

Source: FAO, Intergovernmental Group on Jute, Kenaf and Allied Fibers.

In Bangladesh and India jute competes for land primarily with rice

(paddy), while in Thailand cassava is jute/kenaf's keenest competitor. In the

short term the elasticity of jute acreage with respect to the real producer

price of jute is estimated at 0.64 in Bangladesh, 0.49 in India and 0.67 in

Thailand. The elasticity of jute acreage in the short term with respect to the

real producer price of paddy is estimated at -0.22 in Bangladesh and -0.81 in

India. 1/ It is interesting to note that the response of jute acreage to

changes in relative prices of jute and paddy are not symmetrical as would be

implicitly assumed if the jute/rice price ratio was used as the explanatory

variable. The long-run price elasticity of jute acreage is estimated at 1.04

in India and 1.33 in Thailand.

1/ For a more complete description of the analysis of jute supply see AnnexI, An Econometric Model for the World Jute Economy.

- 11 -

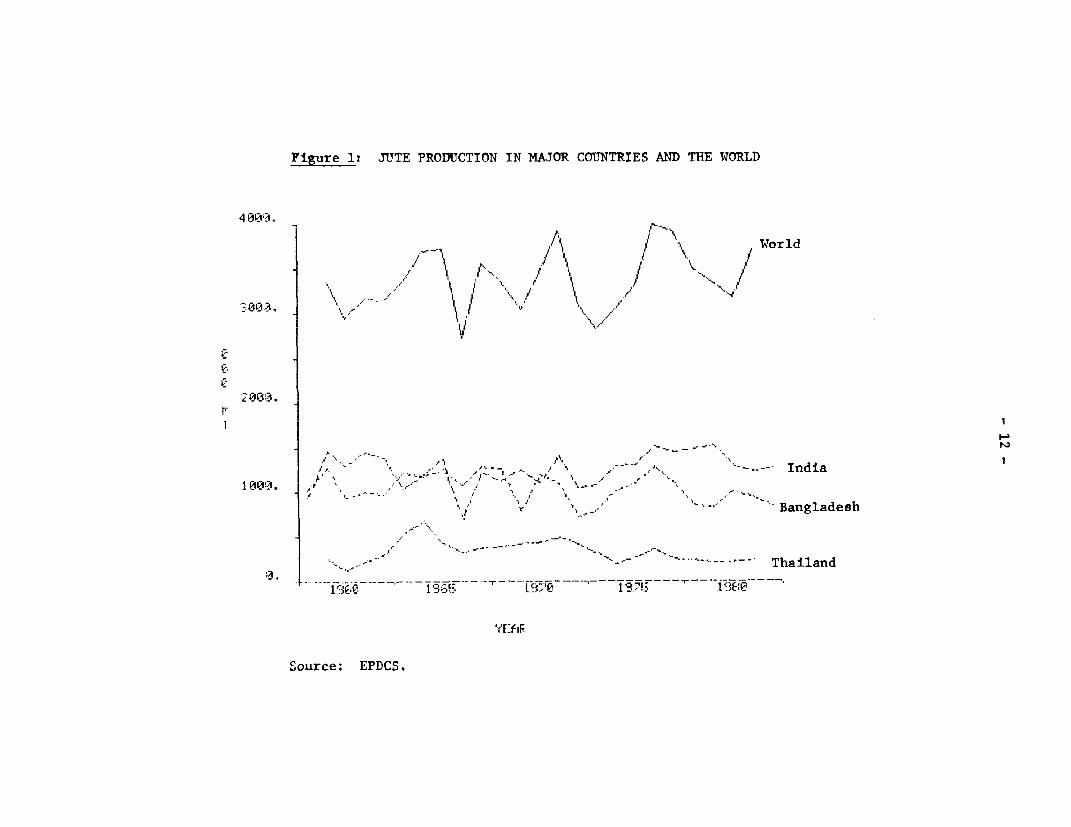

Jute production is determined by both the area harvested and yields

per unit of land. While jute area is influenced by growers' expectation of

jute's relative profitability, yields are influenced substantially by crop

husbandry and seasonal growing conditions. Farmers' efforts in crop husbandry

may be partly determined by their expectations of profitability of jute

growing, but they have no control over seasonal conditions; drought and

flooding periodically have dramatic effects on jute yields. Therefore, jute

production is subject to wide fluctuations from one season to the next due to

variable growing conditions. As a result, world supply fluctuations are

sometimes pronounced. This is especially so for the proportion of total jute

supply that enters international trade since the production fluctuations are

highly correlated in the two most important jute fiber and goods exporting

countries--Bangladesh and India (Figure 1). The current fiber shortage and

record high prices are basically the result of the poor 1984/85 crop

conditions in those countries following a prolonged period of unusually low

prices, during which stocks were run down to low levels.

Future Prospects for Jute Production

The model simulation results indicate that the response of jute

production in the next two years to the present high prices will likely

overshoot current consumption and normal stock needs. This would set the stage

for continuation of the price and supply cycles so often observed in the jute

economy. In the absence of a major weather shock, the phenomenon of adaptative

expectations among jute growers will likely result in cyclical peaks in pro-

duction with accompanying low prices in the late 1980s and mid-1990s, alter-

nating with below average production and price peaks around the turn of the

decade.

Figure 1: JUTE PRODUCTION IN MAJOR COUNTRIES AND THE WORLD

4 0 o" / ., ~World

-- 003z \s ,.i ~/ \II / 'us! \ \ /

,~~~~~~~~~~~~~~~~~~~~~~~~

12.~~~~~~~~~~~~~~~~~~~~~~~~~.

I -. ~~~~~India1 003

Bangladesh

Thailand

YSc PiF

,Source: EPDCS.

- 13 -

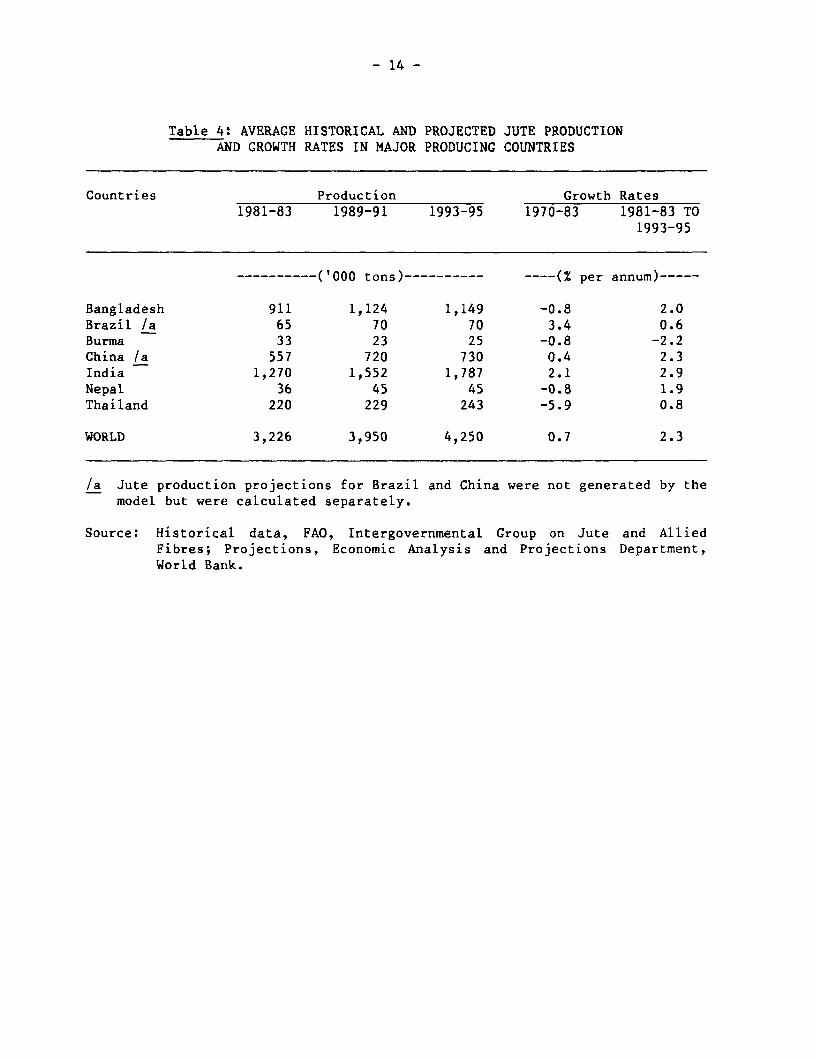

Average annual production projections derived from the simulations

for the main jute growing countries in 1989-91 and 1993-95 are presented in

Table 4 along with average annual output during 1981-83. The production

projections for Brazil and China were not generated by the model but were

calculated separately at levels roughly equivalent to expected domestic

consumption. These production assumptions imply no significant impact on

international trade in jute fiber or product markets from these two countries

during the projection period.

The simulations indicate that the greatest increases in jute produc-

tion and consumption will occur in India, which already has the world's

largest jute sector. With all of the increase in jute production being

required to meet domestic demand, India's volume of exports of jute products

are likely to remain relatively stable at 200-300,000 tons during the projec-

tion period. In Bangladesh, however, the jute requirements for local uses are

likely to remain a relatively small proportion of total output. Therefore,

most of the 200,000 tons of projected increase in production by the mid-1990s

will be available to meet international demand for jute fiber and manufactured

goods. This will raise Bangladesh's export supply, on a fiber equivalent

basis, to around one million tons per year. Thailand's exportable supply of

jute/kenaf is projected to remain around 100,000 tons per year. The additional

jute fiber and product requirements to meet the level of demand implied by the

simulation results of around 100-200,000 tons per year should be shared by the

other smaller suppliers, including Western Europe, the USSR and the other jute

producing countries.

- 14 -

Table 4: AVERAGE HISTORICAL AND PROJECTED JUTE PRODUCTIONAND GROWTH RATES IN MAJOR PRODUCING COUNTRIES

Countries Production Growth Rates1981-83 1989-91 1993-95 1970-83 1981-83 TO

1993-95

…--------- ('000 tons)---------- ---- (% per annum)…

Bangladesh 911 1,124 1,149 -0.8 2.0Brazil /a 65 70 70 3.4 0.6Burma 33 23 25 -0.8 -2.2China /a 557 720 730 0.4 2.3India 1,270 1,552 1,787 2.1 2.9Nepal 36 45 45 -0.8 1.9Thailand 220 229 243 -5.9 0.8

WORLD 3,226 3,950 4,250 0.7 2.3

/a Jute production projections for Brazil and China were not generated by themodel but were calculated separately.

Source: Historical data, FAO, Intergovernmental Group on Jute and AlliedFibres; Projections, Economic Analysis and Projections Department,World Bank.

- 15 -

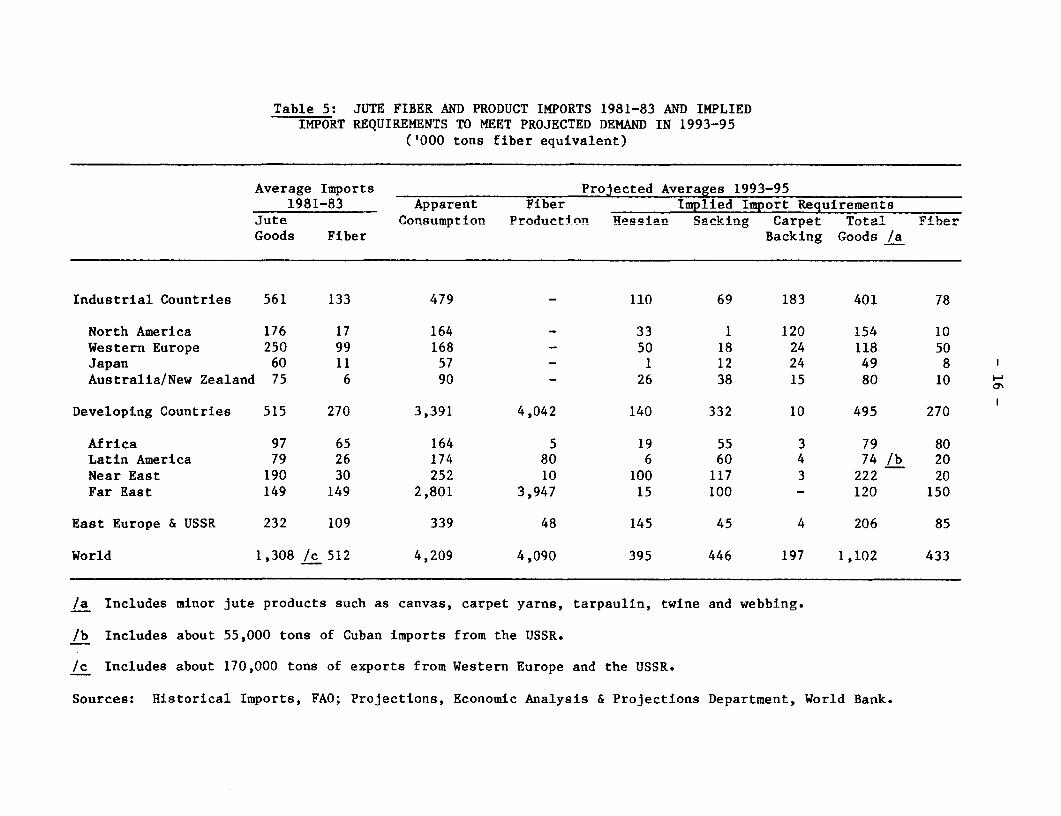

The share of jute fiber in total jute trade declined sharply from the

late 1960s due largely to the attrition of jute manufacturing capacities in

Western Europe and Japan. In the late 1960s, jute fiber accounted for 80% of

import demand in Western Europe and 83% in Japan. By the early 1980s the fiber

share in total imports had declined to 43% in Western Europe and to 22% in

Japan. The advanced stage of the capacity reduction in those countries limits

the impact of additional losses during the projection period (Table 5).

The tendency for fiber demand to increase relative to manufactures in

the developing countries since the late 1960s was reinforced by the

significant expansion of jute manufacturing capacity in Pakistan and the

generally high level of nominal protection afforded to local manufacturers in

those countries. Unless duty structures are made less discriminatory against

jute goods, lower manufacturing costs in the jute-producing countries will be

of little consequence in the competition against synthetic substitutes in

those markets.

The country/regional distribution of jute production and consumption

derived from the simulations to the mid-1990s implies an annual level of

international trade in jute fiber and manufactures of over 1.5 million tons.

An analysis of the trends in the product distribution of jute trade between

the late 1960s and the early 1980s indicates that manufactures should account

for around 1.1 million tons of world jute exports in the mid-1990s and raw

fiber exports should remain at over 400,000 tons (see Table 5). The share of

manufactures in total trade (on a fiber equivalent basis) is expected to

increase to around 72% in the mid-1990s from 68% in the early 1980s. Within

the manufactures, sacking and carpet backing cloth are expected to increase

their share of trade, while hessian and other products such as carpet yarns

are expected to lose shares. The share of raw fibers will also decline.

Table 5: JUTE FIBER AND PRODUCT IMPORTS 1981-83 AND IMPLIEDIMPORT REQUIREMENTS TO MEET PROJECTED DEMAND IN 1993-95

('000 tons fiber equivalent)

Average Imports Projected Averages 1993-951981-83 Apparent Fiber Implied Import Requirements

Jute Consumption Production Hessian Sacking Carpet Total FiberGoods Fiber Backing Goods /a

Industrial Countries 561 133 479 - 110 69 183 401 78

North America 176 17 164 - 33 1 120 154 10Western Europe 250 99 168 - 50 18 24 118 50Japan 60 11 57 - 1 12 24 49 8Australia/New Zealand 75 6 90 - 26 38 15 80 10

Developing Countries 515 270 3,391 4,042 140 332 10 495 270

Africa 97 65 164 5 19 55 3 79 80Latin America 79 26 174 80 6 60 4 74 /b 20Near East 190 30 252 10 100 117 3 222 20Far East 149 149 2,801 3,947 15 100 - 120 150

East Europe & USSR 232 109 339 48 145 45 4 206 85

World 1,308 /c 512 4,209 4,090 395 446 197 1,102 433

/a Includes minor jute products such as canvas, carpet yarns, tarpaulin, twine and webbing.

/b Includes about 55,000 tons of Cuban imports from the USSR.

/c Includes about 170,000 tons of exports from Western Europe and the USSR.

Sources: Historical Imports, FAO; Projections, Economic Analysis & Projections Department, World Bank.

- 17 -

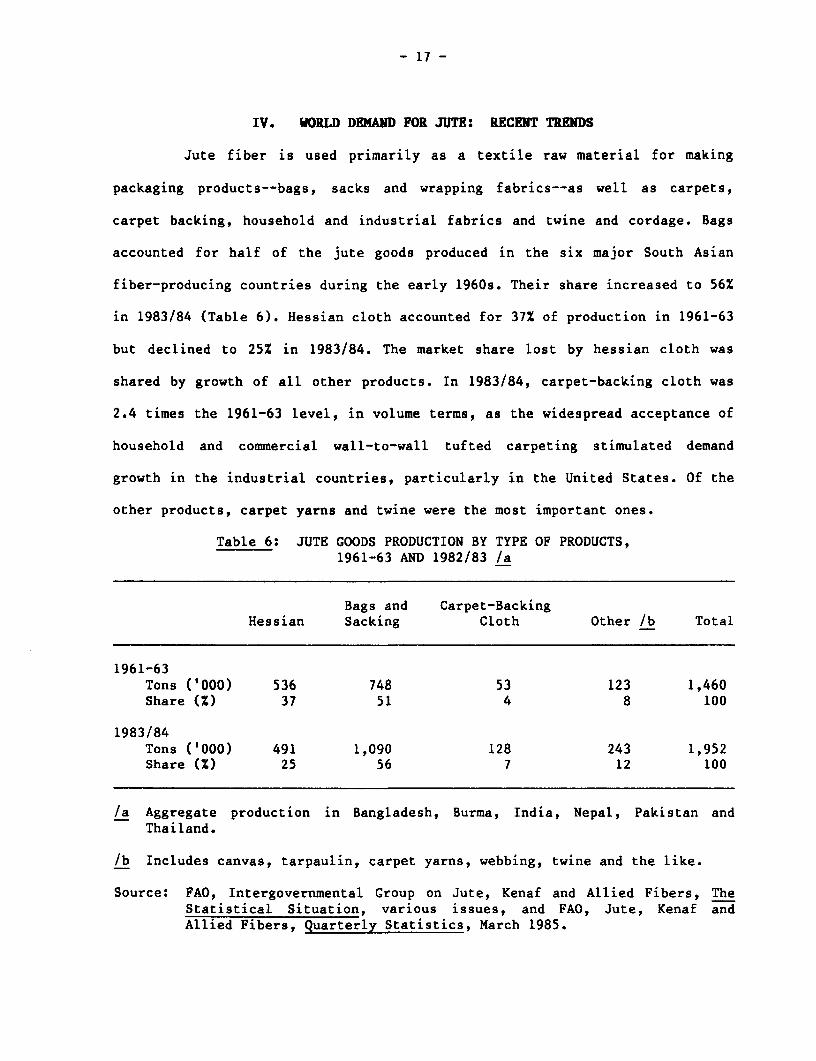

IV. WORLD DEMAND FOR JUTE: RECENT TRENDS

Jute fiber is used primarily as a textile raw material for making

packaging products--bags, sacks and wrapping fabrics--as well as carpets,

carpet backing, household and industrial fabrics and twine and cordage. Bags

accounted for half of the jute goods produced in the six major South Asian

fiber-producing countries during the early 1960s. Their share increased to 56%

in 1983/84 (Table 6). Hessian cloth accounted for 37% of production in 1961-63

but declined to 25% in 1983/84. The market share lost by hessian cloth was

shared by growth of all other products. In 1983/84, carpet-backing cloth was

2.4 times the 1961-63 level, in volume terms, as the widespread acceptance of

household and commercial wall-to-wall tufted carpeting stimulated demand

growth in the industrial countries, particularly in the United States. Of the

other products, carpet yarns and twine were the most important ones.

Table 6: JUTE GOODS PRODUCTION BY TYPE OF PRODUCTS,1961-63 AND 1982/83 /a

Bags and Carpet-BackingHessian Sacking Cloth Other /b Total

1961-63Tons ('000) 536 748 53 123 1,460Share (Z) 37 51 4 8 100

1983/84Tons ('000) 491 1,090 128 243 1,952Share tX) 25 56 7 12 100

/a Aggregate production in Bangladesh, Burma, India, Nepal, Pakistan andThailand.

/b Includes canvas, tarpaulin, carpet yarns, webbing, twine and the like.

Source: FAO, Intergovernmental Group on Jute, Kenaf and Allied Fibers, TheStatistical Situation, various issues, and FAO, Jute, Kenaf andAllied Fibers, Quarterly Statistics, March 1985.

- 18 -

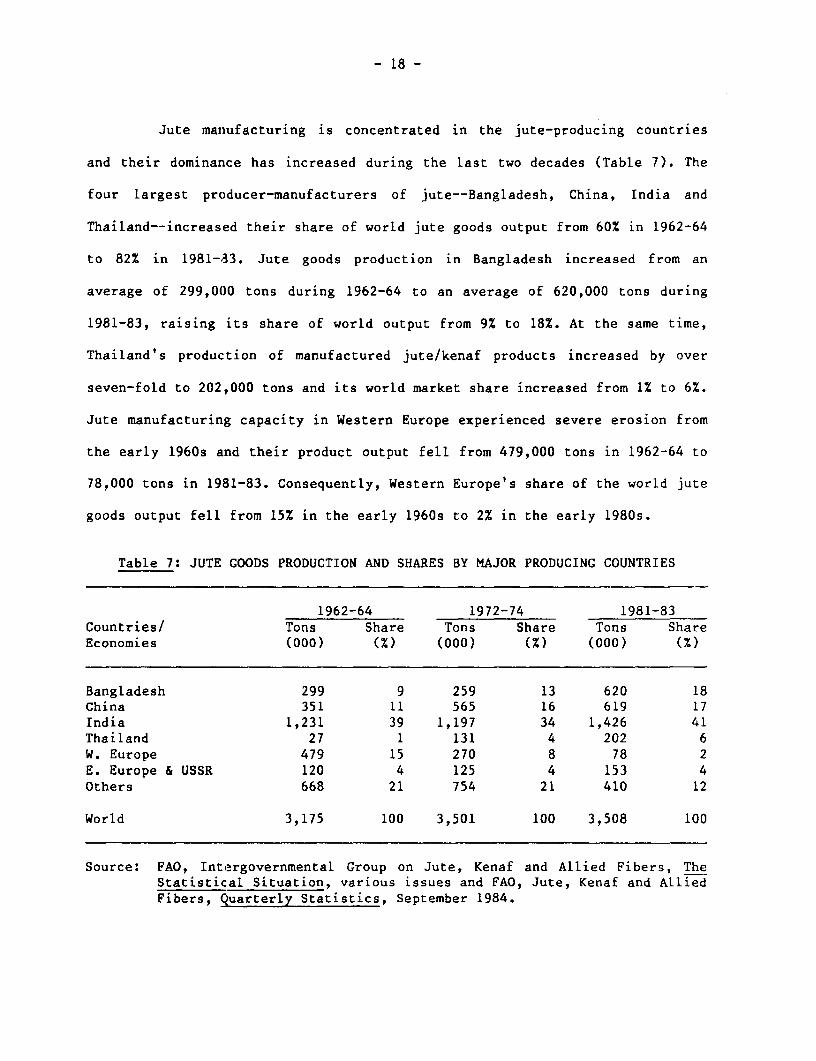

Jute manufacturing is concentrated in the jute-producing countries

and their dominance has increased during the last two decades (Table 7). The

four largest producer-manufacturers of jute--Bangladesh, China, India and

Thailand--increased their share of world jute goods output from 60% in 1962-64

to 82% in 1981-83. Jute goods production in Bangladesh increased from an

average of 299,000 tons during 1962-64 to an average of 620,000 tons during

1981-83, raising its share of world output from 9% to 18%. At the same time,

Thailand's production of manufactured jute/kenaf products increased by over

seven-fold to 202,000 tons and its world market share increased from 1% to 6%.

Jute manufacturing capacity in Western Europe experienced severe erosion from

the early 1960s and their product output fell from 479,000 tons in 1962-64 to

78,000 tons in 1981-83. Consequently, Western Europe's share of the world jute

goods output fell from 15% in the early 1960s to 2% in the early 1980s.

Table 7: JUTE GOODS PRODUCTION AND SHARES BY MAJOR PRODUCING COUNTRIES

1962-64 1972-74 1981-83Countries/ Tons Share Tons Share Tons ShareEconomies (000) (Z) (000) (Z) (000) (%)

Bangladesh 299 9 259 13 620 18China 351 11 565 16 619 17India 1,231 39 1,197 34 1,426 41Thailand 27 1 131 4 202 6W. Europe 479 15 270 8 78 2E. Europe & USSR 120 4 125 4 153 4Others 668 21 754 21 410 12

World 3,175 100 3,501 100 3,508 100

Source: FAO, Intergovernmental Group on Jute, Kenaf and Allied Fibers, TheStatistical Situation, various issues and FAO, Jute, Kenaf and AlliedFibers, Quarterly Statistics, September 1984.

- 19 -

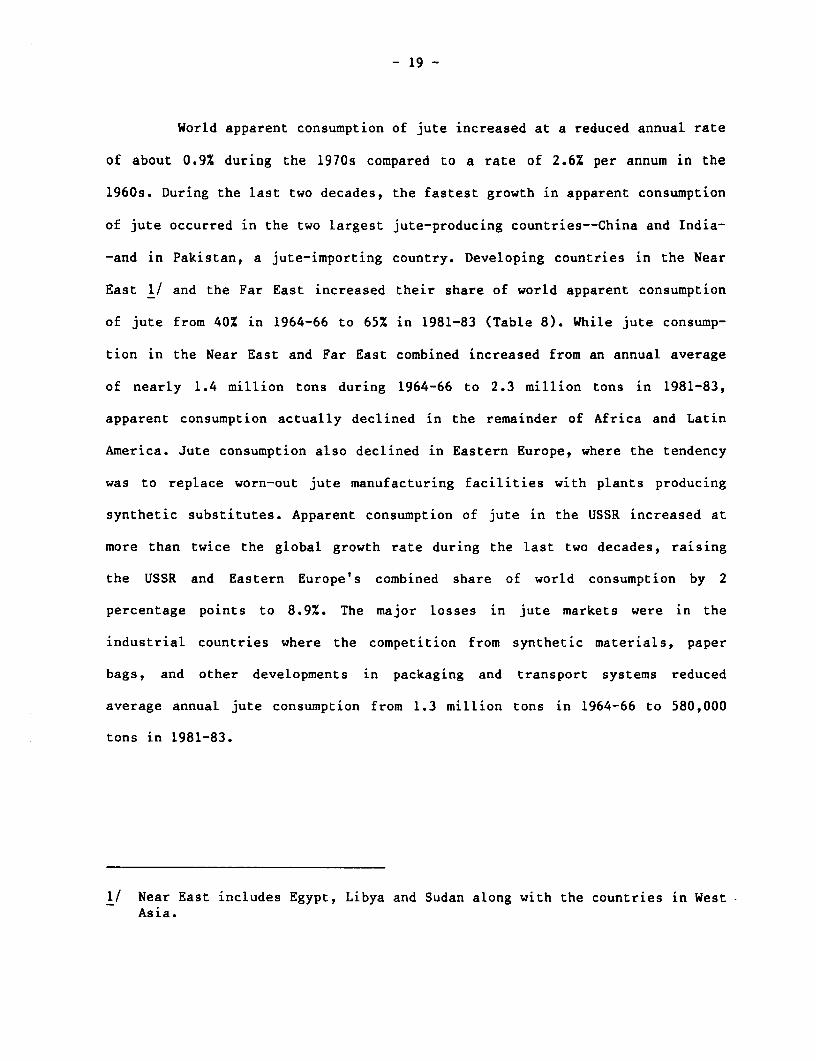

World apparent consumption of jute increased at a reduced annual rate

of about 0.9% during the 1970s compared to a rate of 2.6% per annum in the

1960s. During the last two decades, the fastest growth in apparent consumption

of jute occurred in the two largest jute-producing countries--China and India-

-and in Pakistan, a jute-importing country. Developing countries in the Near

East 1/ and the Far East increased their share of world apparent consumption

of jute from 40% in 1964-66 to 65% in 1981-83 (Table 8). While jute consump-

tion in the Near East and Far East combined increased from an annual average

of nearly 1.4 million tons during 1964-66 to 2.3 million tons in 1981-83,

apparent consumption actually declined in the remainder of Africa and Latin

America. Jute consumption also declined in Eastern Europe, where the tendency

was to replace worn-out jute manufacturing facilities with plants producing

synthetic substitutes. Apparent consumption of jute in the USSR increased at

more than twice the global growth rate during the last two decades, raising

the USSR and Eastern Europe's combined share of world consumption by 2

percentage points to 8.9%. The major losses in jute markets were in the

industrial countries where the competition from synthetic materials, paper

bags, and other developments in packaging and transport systems reduced

average annual jute consumption from 1.3 million tons in 1964-66 to 580,000

tons in 1981-83.

1/ Near East includes Egypt, Libya and Sudan along with the countries in WestAsia.

- 20 -

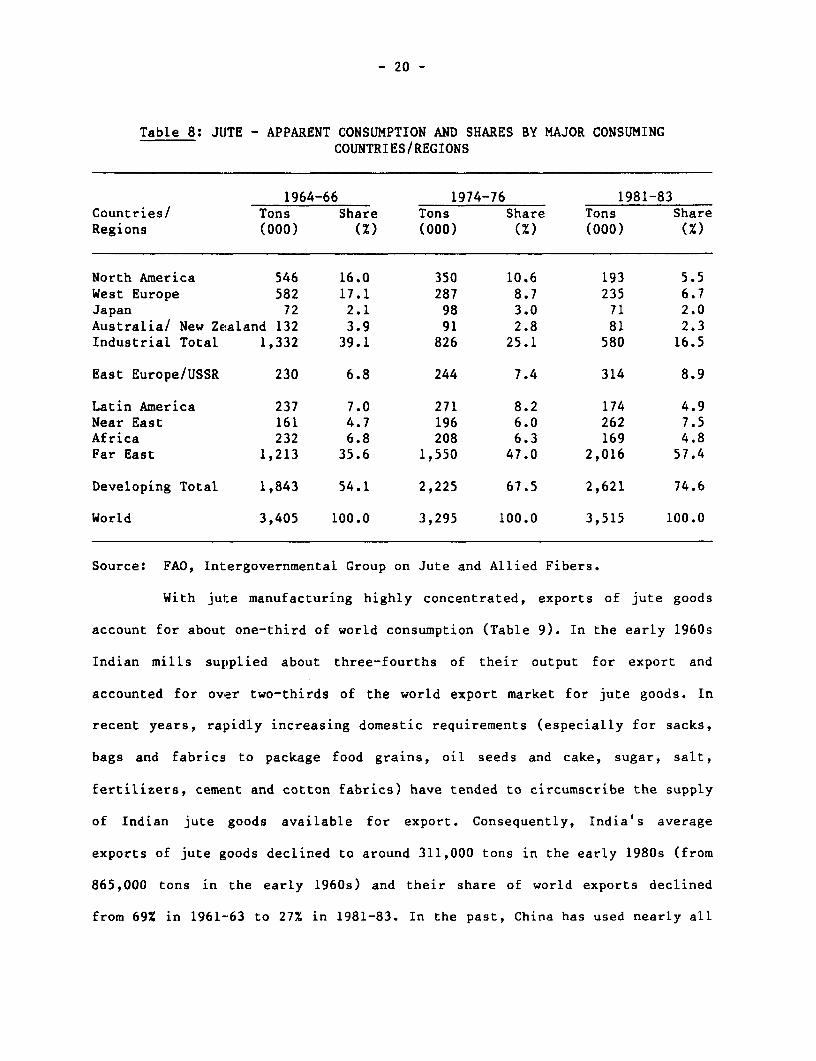

Table 8: JUTE - APPARENT CONSUMPTION AND SHARES BY MAJOR CONSUMINGCOUNTRIES/REGIONS

1964-66 1974-76 1981-83Countries/ Tons Share Tons Share Tons ShareRegions (000) (Z) (000) (%) (000) (Z)

North America 546 16.0 350 10.6 193 5.5West Europe 582 17.1 287 8.7 235 6.7Japan 72 2.1 98 3.0 71 2.0Australia/ New Zealand 132 3.9 91 2.8 81 2.3Industrial Total 1,332 39.1 826 25.1 580 16.5

East Europe/USSR 230 6.8 244 7.4 314 8.9

Latin America 237 7.0 271 8.2 174 4.9Near East 161 4.7 196 6.0 262 7.5Africa 232 6.8 208 6.3 169 4.8Far East 1,213 35.6 1,550 47.0 2,016 57.4

Developing Total 1,843 54.1 2,225 67.5 2,621 74.6

World 3,405 100.0 3,295 100.0 3,515 100.0

Source: FAO, Intergovernmental Group on Jute and Allied Fibers.

With jule manufacturing highly concentrated, exports of jute goods

account for about one-third of world consumption (Table 9). In the early 1960s

Indian mills supplied about three-fourths of their output for export and

accounted for over two-thirds of the world export market for jute goods. In

recent years, rapidly increasing domestic requirements (especially for sacks,

bags and fabrics to package food grains, oil seeds and cake, sugar, salt,

fertilizers, cement and cotton fabrics) have tended to circumscribe the supply

of Indian jute goods available for export. Consequently, India's average

exports of jute goods declined to around 311,000 tons in the early 1980s (from

865,000 tons in the early 1960s) and their share of world exports declined

from 69% in 1961-63 to 27% in 1981-83. In the past, China has used nearly all

- 21 -

the jute goods produced in local mills, but in recent years exports of sacks,

hessian and yarn have increased, reaching about 64,000 tons in 1983 compared

to estimated internal consumption of 455,000 tons. 1/

Bangladesh, the third largest producer of jute, depends on export

markets for most of its output. Although Bangladesh mills have more than

doubled their output of jute manufacturers since the early 1960s, throughout

the 1970s roughly 90% of their jute goods were exported. During 1981-83

Bangladesh accounted for 44% of world jute goods exports--up from an 18% share

in 1961-63. Bangladesh has also remained the largest exporter of jute fiber,

accounting for 73% of world exports during the last three seasons (1981/82 -

1983/84). The market for raw fiber has been shrinking, however, and

Bangladesh's exports declined by an average of 4.3% per year between 1961 and

1983. The main reason for the decline in fiber exports was the contraction of

jute manufacturing in the industrial countries, especially in Western Europe.

Those countries received two-thirds of the world's total fiber exports in

1961-63 but only 25% in 1981-83. Concurrent with the reduction in jute manu-

facturing in Western Europe, Pakistan expanded its jute mill capacity and is

now the world's largest importer of raw jute.

Thailand exported only fiber in the early 1960s but developed

substantial export capacity for sacks, yarns and twine by the early 1970s.

With the decline in fiber production in the later years of the 1970s, largely

because of competitive losses of growing area to cassava and maize, jute goods

became the predominent export items as fiber exports declined. Although

1/ FAO CCP:JU/QS 85/1, March 1985.

- 22 -

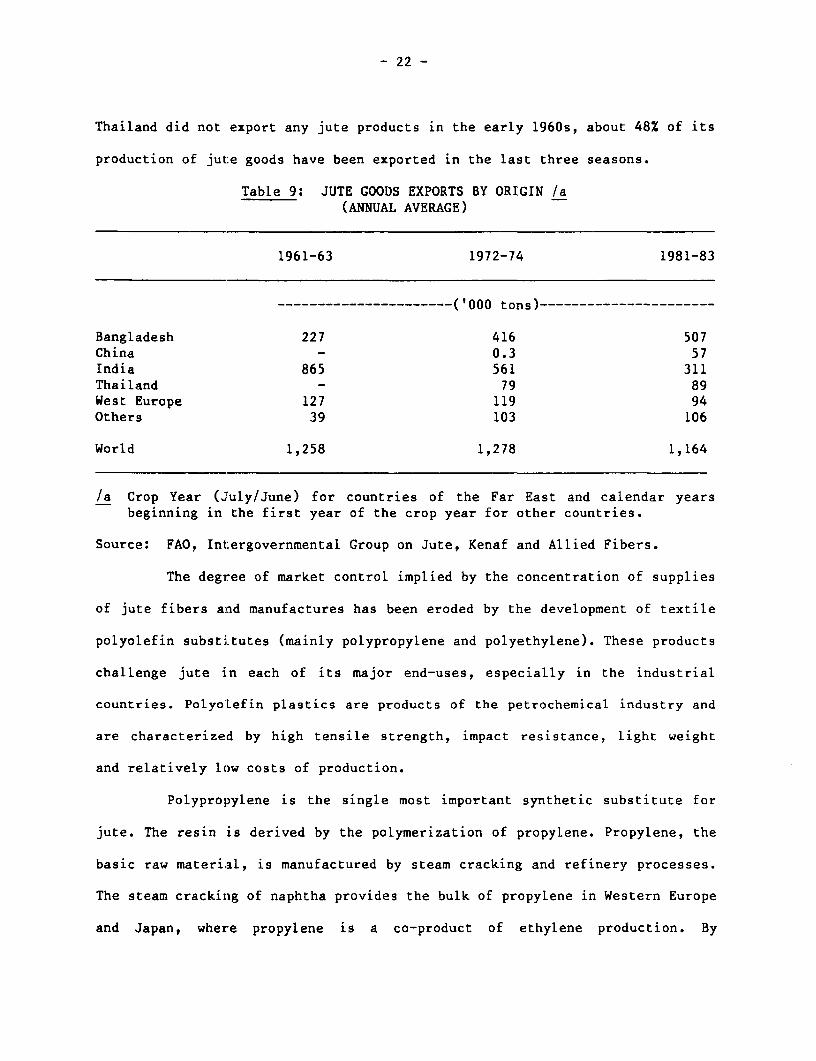

Thailand did not export any jute products in the early 1960s, about 48% of its

production of jute goods have been exported in the last three seasons.

Table 9: JUTE GOODS EXPORTS BY ORIGIN /a(ANNUAL AVERAGE)

1961-63 1972-74 1981-83

----------------------('000 tons)----------------------

Bangladesh 227 416 507China 0.3 57India 865 561 311Thailand - 79 89West Europe 127 119 94Others 39 103 106

World 1,258 1,278 1,164

/a Crop Year (July/June) for countries of the Far East and calendar yearsbeginning in the first year of the crop year for other countries.

Source: FAO, Int:ergovernmental Group on Jute, Kenaf and Allied Fibers.

The degree of market control implied by the concentration of supplies

of jute fibers and manufactures has been eroded by the development of textile

polyolefin substitutes (mainly polypropylene and polyethylene). These products

challenge jute in each of its major end-uses, especially in the industrial

countries. PolyoLefin plastics are products of the petrochemical industry and

are characterized by high tensile strength, impact resistance, light weight

and relatively low costs of production.

Polypropylene is the single most important synthetic substitute for

jute. The resin is derived by the polymerization of propylene. Propylene, the

basic raw material, is manufactured by steam cracking and refinery processes.

The steam cracking of naphtha provides the bulk of propylene in Western Europe

and Japan, where propylene is a co-product of ethylene production. By

- 23 -

comparison, in the United States much of the propylene is supplied by

refineries and it is derived from natural gas liquids and from liquified

petroleum gases.

Polypropylene was a late-comer in the family of synthetic fibers.

Research and development efforts have proven very successful in increasing the

efficiency of production processes and in adapting various forms of the fiber

to specific end-use requirements. These improved efficiencies in production,

increased economies of scale as the polypropylene industry matured and the

incentive to sell products below total costs when demand was slackened by

recession have tended to keep prices relatively low for extended periods when

manufacturing capacities surpassed demand. Cost-efficient processes and

materials--vapor phase technology and third generation catalysts--will keep

polypropylene costs highly competitive as they continue to be adopted as the

industry standard, offsetting the effects of higher feedstock prices in the

first half of the 1990s.

The polyolefin product producers fielded aggressive marketing efforts

to penetrate new use areas. Their market promotion included technical assis-

tance to users and substantial research in product development and adaption.

Each disruption in jute supplies or sharp rise in jute prices since the mid-

1960s has provided the synthetics an opportunity for further penetration of

jute markets, particularly in the industrial countries. The expanded use of

polypropylene products as substitutes for jute goods has expanded sharply

during the late 1970s and early 1980s. In those cases where the synthetic

products combined technical advantages and lower prices the effect on jute was

devastating. This is clearly illustrated by the market for primary backing for

tufted carpets. In the United States jute accounted for 89X of this end-use in

- 24 -

1967, but the development and effective marketing of a lower-priced synthetic

fabric that performed well technically in the manufacturing processes caused a

sharp erosion of this market. In 1983, use of jute as the primary backing for

carpets was confined to specialty items and accounted for less than 5% of the

total. The use of jute primary backing for tufted carpets also declined

sharply during the 1970s in Japan and Western Europe. By contrast, jute's

superior technicaL performance as a secondary backing for tufted carpets and

the jute manufactures' responsiveness in developing lighter-weight fabrics to

meet cost competition kept 55% of this market in the United States for jute in

1983. However, the rise in jute carpet backing prices associated with the

1984/85 fiber shortage has resulted in a loss of competitiveness and a severe

decline in jute's market share. Based on past experience, an extended period

of assured supplies of jute secondary backing fabrics at competitive prices

will be required to recover most of jute's former share of this market. Jute

secondary backing had begun making gains vis-a-vis foam cushion backings in

Western Europe prior to the current period of high prices and it has also been

a growth item in Japan during recent years.

Jute also faces serious competition from synthetic products in its

largest markets--bags, sacks, bale wraps and industrial cloths--in virtually

all consuming countries. At the same time, the total market for bags has

declined in those countries where bulk handling of agricultural and industrial

products--especially grains, cement and fertilizers--have become predominant

handling methods and extensive processing and prepackaging of groceries have

become common merchandising factors. The cost competitiveness of polyolefin

synthetic fibers has been particularly intense since the mid-1970s because

excess production capacity often resulted in short-term marketing strategies

- 25 -

based on recovery of direct costs when full-cost recovery was impossible. The

effects of this competition have been widespread; they have been a major

factor limiting the demand for jute bags in African, Asian and Latin American

countries as well as in the industrial countries.

- 26 -

V. ANALYSIS OF DEMAND FOR JUTE: BY COUNTRIES AND REGIONS

The slow-down in world demand growth for jute since the mid-1960s is

largely attributable to technological changes in the transportation,

packaging, storage and handling of agricultural and industrial products

traditionally packaged in jute bags or fabrics and to the substitution of

paper and synthetic products for those made from jute. These technological

developments, including synthetic substitution, were initially introduced in

the industrial countries and it is there that the impact on jute consumption

has been the greatest. The substitution of synthetic products for jute

products was accelerated periodically by the scarcity of and sharply higher

prices for jute fiber and goods in the consuming countries. These scarcities

have arisen fronn unusually small jute crops due to unfavorable growing condi-

tions and the interruptions to manufacturing and/or transport of products

during strikes aand Bangladesh's independence struggle.

Recent trends in the end-use markets are described in detail by

region and count:ry in this section. Trends in demand for jute during the last

two decades have! been analyzed econometrically for 15 countries/regions. These

econometric estimates, together with other information about likely demand

behavior in these markets, for both jute and its substitutes, are then used to

make projectionsi for jute demand in these markets (see Annex 1 for a detailed

listing of the various parameters estimated in the jute model).

Industrial Countries

The importance of the industrial countries as consumers of jute has

eroded seriously since the mid-1060s. Apparent consumption of jute in these

countries averag;ed 1.33 million tons per year during 1964-66 and accounted for

39% of total world demand. By 1981-83 average apparent consumption in the

- 27 -

industrial countries had declined to 579,000 tons, about 16% of the world

total.

a. North America

A full range of jute products are used in North America, but carpet

backing cloth and burlap accounted for 83% of imports of fiber and products

during 1981-83. Jute is not produced locally and manufacturing activities are

limited to specialized yarn spinning, bag sewing operations and converting

jute butts and waste into felts and padding products. Imports of raw jute and

waste account for about 10% of the jute fiber and products imported into

Canada and the United States.

Apparent consumption of jute in North America declined from the 1964-

66 average of 546,000 tons per year to an average of 192,000 tons during 1981-

83. Although jute consumption has declined by 65% since the mid-1960s, the use

of jute secondary carpet backing exhibited relative strength. In the mid-1960s

average imports of 131,000 tons of jute carpet backing cloth accounted for

nearly 26% of total jute fiber and goods imported. On a yardage basis those

imports were about equally divided between primary and secondary backing

cloths, although on a tonnage basis the primary, generally a 9.0 oz. fabric

compared to secondary of 7.0 oz, was more important. During the late 1960s a

price-competitive, woven polypropylene primary-backing cloth with technical

advantage for fine gauge tufted carpets began rapidly to replace jute primary

backing cloth in broadloom tufted carpets. Jute's share in this end use fell

from around 90% in the mid-1960s to less than 5% in the 1980s. Price and

technical competitiveness were better maintained by jute in the secondary

carpet backing, however, and jute's market share in the early 1980s was around

55% compared to over 70% in the late 1960s. Costs of jute secondary carpet

- 28 -

backing cloth were kept under control by the progressive development of

lighter-weight fabrics of adequate technical competitiveness. Jute's market

share has dipped seriously during periods of inadequate supply and uncompeti-

tive prices, as in 1969/70 and in 1984, and the long-term ability of jute to

recover and maintain a significantly larger share is yet uncertain. Although

jute lost a major portion of its primary backing market, the growth in

secondary backing raised carpet backing's share of the total jute fiber and

goods imports into North America to 45% in the early 1980s.

The demand for carpet-backing cloth is derived from the demand for

broadloom tufted carpets, and jute's share of that market is essentially

determined by its price and technical competitiveness vis-a-vis synthetic

substitutes. Broadloom carpet shipments in the United States increased at a

rate of over 16% per year during the 1960s, when real incomes were rising

favorably, new synthetic face yarns came into use at declining real prices,

wall-to-wall carpeting became fashionable and construction (residential and

commercial) was growing rapidly. Since 1970, real income growth has moderated

and increased saturation of carpeting on existing floor space has reduced the

rate of growth of broadloom tufted carpet shipments to around 3% per year.

During the early 1980s broadloom carpet shipments declined due to the economic

recession's effect: on incomes and the adverse effect of high real interest

rates on home and commercial construction. Since the mid-1970s, 92% of the

variation in jute secondary carpet backing consumption in the United States

can be explained by broadloom tufted carpet shipments and the ratio of the

prices of jute and polypropylene secondary carpet backing cloth, with a price

elasticity of -0.3.

- 29 -

Jute burlap (fabrics up to 100 inches wide) imports into North

America declined from an average of 250,000 tons during 1964-66 to around

80,000 tons in the early 1980s. With about two-thirds of the burlap consumed

in the United States and most of it consumed in Canada being used for making

bags, this sharp decline in burlap imports reflects the erosion of the jute

bag market. The jute bag market has declined along with total bag use due to

extensive bulk handling of agricultural products and industrial materials. At

the same time, jute's share of the smaller bag market was further eroded by

increasing use of paper and synthetic substitutes. Only potato bags, made from

iight-weight hessian, were able to maintain a greater share of the US market

than the synthetics. Heavy-weight jute bags lacked price competitiveness with

synthetic products.

Jute dominated the US cotton bale wrap market up to the mid-1970s;

1970-74 imports averaged 72,500 tons per year, but subsequently the shift of

cotton trading to a net weight basis encouraged the use of lighter weight

synthetic bale wraps. Rapid adoption of improved synthetic bale wraps resulted

in the decline of jute material to 8,600 tons in 1979 and only 800 tons in

1983. Regulations have been introduced such that, in 1985, cotton bale wraps

must cover the entire bale, and the polyolefin coating used to prevent

fibrillation must be thermally bonded to the woven polypropylene fabric by

extrusion coating. The cost of this additional requirement for the synthetic

product may be sufficient to make new lighter-weight jute construction cost

competitive.

A small proportion of the jute burlap market is for decorative

fabrics. These fabrics accounted for about 8 million square yards of burlap in

the United States annually in the early 1980s and about one million square

- 30 -

yards in Canada. The demand for decoratives is subject to the sudden shifts of

fashion trends but it is not likely to become a high volume item in the North

American market.

The divergent trends in the demand for jute secondary carpet backing

cloth and for other jute products in the North American market are expected to

continue into the 1990s. The model simulations indicate that broadloom tufted

carpet shipments in the United States should increase to around 1.3 billion

square yards by 1990 and by a further 300 to 400 million square yards in the

mid-1990s. Therefore, jute's opportunities in the North American secondary

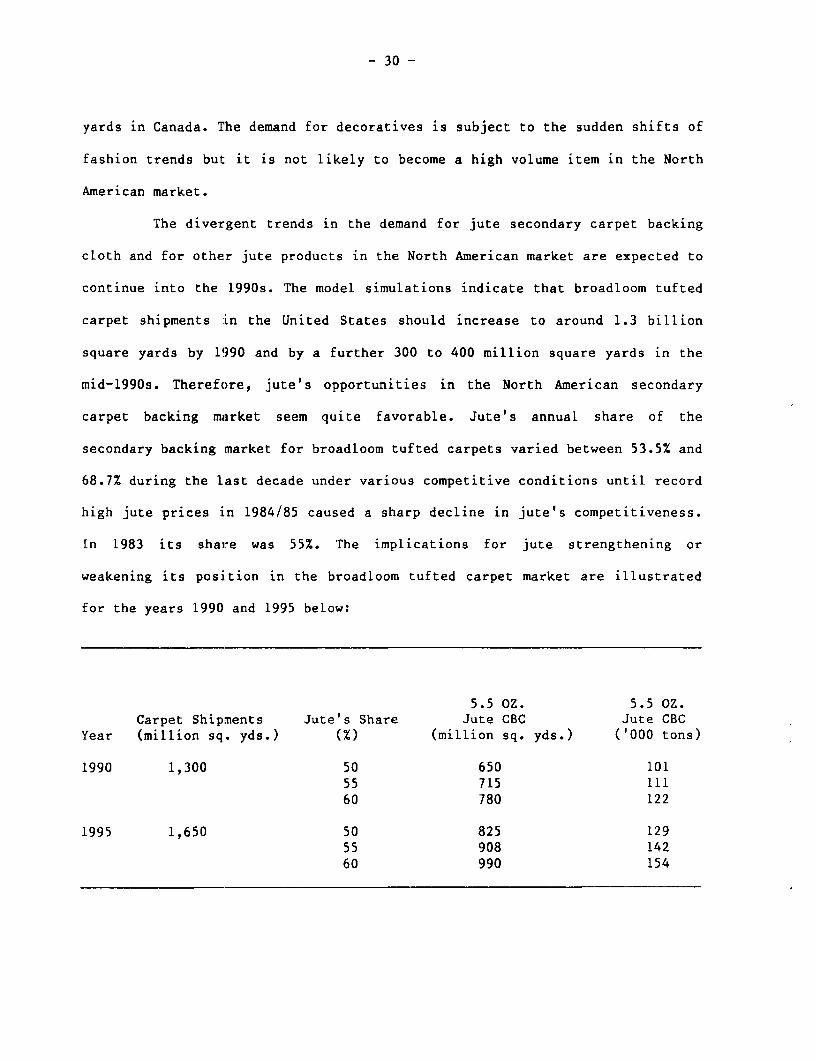

carpet backing market seem quite favorable. Jute's annual share of the

secondary backing market for broadloom tufted carpets varied between 53.5% and

68.7% during the last decade under various competitive conditions until record

high jute prices in 1984/85 caused a sharp decline in jute's competitiveness.

In 1983 its share was 55%. The implications for jute strengthening or

weakening its position in the broadloom tufted carpet market are illustrated

for the years 1990 and 1995 below:

5.5 OZ. 5.5 OZ.Carpet Shipments Jute's Share Jute CBC Jute CBC

Year (million sq. yds.) (Z) (million sq. yds.) ('000 tons)

1990 1,300 50 650 10155 715 11160 780 122

1995 1,650 50 825 12955 908 14260 990 154

- 31 -

By maintaining their 1983 level of competitiveness, the jute manufacturing

industries can expect a market in the United States for over 700 million

square yards of secondary carpet backing by the end of the 1980s and around

900 million square yards in the mid-1990s. Should the 5.5 oz. cloth still be

the standard jute secondary carpet backing construction in 1995, it would

amount to 142,000 tons of fabric, which is more than double the average

1980-83 imports of all carpet-backing cloth. By regaining the competitive

position of the 1970s (say a share of 60%), jute carpet backing use would be

substantially higher.

A new carpet underlay for glue-down installations, consisting of a

dense sponge rubber pad with a woven jute scrim on each side, is now being

promoted in the US market and trial samples have been shown in the European

market. This pad can be released from the floor and carpet with relative ease

and it has increased installation productivity by eliminating the need for

stretching or heat-bond seaming. If the full market potential for this new

underlay is realized it could increase the annual demand for 6 oz. jute carpet

backing cloth by several thousand tons in the United States alone.

Prospects for other traditional jute products in the North American

market are less promising than those for secondary carpet backing. There is no

apparent development that would be expected to reverse the downward trend in

use of these products over the projection period, which is likely to keep

total jute consumption in a moderate decline when the cyclical peaks and

valleys are averaged out.

b. Western Europe

Jute utilization in Western Europe experienced a sharp decline from

the late 1960s until it tended to level-out in the early 1980s. European jute

- 32 -

manufacturers' ability to compete against paper and synthetic substitutes was

hindered by rising processing costs and higher raw material prices. Moreover,

jute consumers were unable to obtain jute products at world market prices

because of the protectionist measures taken on behalf of domestic jute

manufactures. Therefore, imports of jute goods did not fully compensate for

the lower indigenous production. In these circumstances, the substitution of

polyolefin textiles for jute goods proceeded rapidly from the late 1960s when

synthetic prices became highly competitive. The trend toward bulk handling of

agricultural commodities and the pre-packaging of groceries also cut sharply

into the need for jute sacks and bags. These developments reduced apparent

consumption of jute in Western Europe from an annual average of 582,000 tons

during 1964-66, representing 17% of the world total, to 235,000 tons, or 6.6%

of the world total during 1981-83.

The dramatic retrenchment in jute manufacturing in Western Europe is

indicated by the changes in equipment and employment in the industry. The

availability of spindles and looms in the industry declined by 83% and 91%,

respectively, between 1965 and 1980, while employment declined by 80%. As a

result, jute fiber imports fell from 521,000 tons in 1965 to 84,000 tons in

1983.

Sacks and bags provided the largest market for jute goods in Western

Europe during the 1970s and was estimated to account for one-third of its

total use in the four major jute consuming countries in the early 1980s. The

demand for jute sacks has been sustained by their use for packaging European

products for export. Most of these bags are sent to developing countries, with

Africa being the largest destination. The reusability of jute bags is

important to their preferences in these markets.

- 33 -

The growth in domestic demand for jute sacks has been constrained by

increased use of intermediate bulk containers (in one or two ton units) for

packaging, handling and storage of powder or granular materials. In this form

they can be lifted and transported by fork lift trucks or cranes and stored

without pallets.

The increased use of synthetic bags and bale wraps has also impacted

adversely on jute demand in Western Europe. The increase in polyolefins used

in bags and bale wraps between 1970 and 1980 is conservatively estimated to

have replaced 135,000 tons of jute-sacking materials. This penetration of the

market by synthetics was strongly aided by very competitive pricing,

especially so for imported bags. Jute sacks were not fully price competitive

with woven polypropylene bags in the early 1980s, even before the sharp

increase in product prices due to tight jute supplies in 1984.

Jute carpet yarns have long been the preferred weft yarn for making

woven carpets. Production of woven carpets in Western Europe, however,

declined by 25% between 1971 and 1980, and the down-trend is expected to

continue in the current decade as tufted carpets now dominate the market.

A marked change in the origin of jute yarns used in Western Europe

has occurred in recent years. Prior to the relaxation of trade restrictions,

most jute yarns were spun domestically. Now a larger share of the available

supply is imported from the jute-producing countries. The continued penetra-

tion of imported jute yarns into the West European market depends importantly

on manufacturers supplying yarns of good quality and free of slubs and

uneveness. Elimination of poorly tied knots and improved packaging also

requires urgent attention. Any excessive down time of weavers' high-speed

looms, caused by poor quality yarns, will jeopardize jute's position in this

- 34 -

market. A main attraction of polypropylene yarn is the extra yardage without a

join on the yarns, which speeds production. The synthetic producers also

emphasize that their yarns are rot-proof, do not shrink when wet and impart

dimensional stability. Jute yarns, on the other hand, are not stiffened by the

application of latex, are more bulky and are very supple, giving jute yarns

and the carpet a better "hand". Synthetics are estimated to be the predominant

warp yarn in European woven carpets, but jute accounts for a major share of

the weft carpet yarns.

Jute primary carpet backing has not been price competitive with woven

polypropylene in recent years and typically has accounted for less than 2% of

the West European market.

Jute's position in West European secondary carpet backing

deteriorated rapid]Ly in the early 1970s as domestic jute manufacturing costs

were rising and imports of jute cloth from lower-cost producers, which could

have competed with synthetic backing, were limited by import barriers. In this

case, the protection of the European jute industry from imported jute cloth

acted to protect t:he synthetic-backing producers from effective competition

from jute. Under these conditions, foam cushion became the predominant

secondary backing fior tufted carpets. In the early 1980s, foam cushion backing

accounted for over 90% of secondary backings in Belgium, France and the

Federal Republic of Germany, although other backings had penetrated substan-

tially more in the Netherlands and the United Kingdom.

There are some favorable factors at work that should encourage jute

manufacturers to make a serious effort to exploit the movement of the European

carpet industry toward woven backing for tufted carpets. The problems

experienced with the first generation of foam backings are surfacing at the

- 35 -

time replacement carpets are required. The cost of lifting the old carpets is

often twice the cost of installation, due to the deterioration of the foam

backing. This difficulty has raised interest in woven backings. Exports of

European-made carpets are expanding, particularly to the Middle East, which

has a distinct preference for carpets with a woven jute secondary backing.

Also, growing concern over the dangers of flammability and smoke

density/toxicity favor the selection of jute cellulosic fibers over synthetic

materials.

In the highly competitive carpet market of the early 1980s, the

standard jute secondary backing in West Europe shifted from a 7 oz. to a 6 oz.

cloth and trials were made with a 5.5 oz. fabric. These efforts helped jute to

maintain a small price advantage over woven polypropylene secondary backing.

With jute-backing prices increasing faster than those of the synthetic

substitute, however, the advantage had largely disappeared by the third

quarter of 1984.

Total carpet production in Western Europe nearly doubled between 1970

and 1980 and tufted carpets increased their share of the market from 48% to

70% during that period. Industry estimates suggest that all the growth in

carpet production during the current decade will be of tufted construction. A

decline in woven carpet output is expected to be led by lower Axminster

production in the United Kingdom and a more modest decline in needlefelt

output generally in the carpet manufacturing countries. Assuming moderate

economic growth during the remainder of the decade, tufted carpet production

could increase by 50% from the 1981 level. These growth prospects represent a

strong challenge to jute secondary carpet backing manufacturers.

- 36 -

The breakthrough in the use of jute in decorative fabrics and other

end uses envisaged at the start of the 1970s now appears unlikely, unless

technical advance!ment is made in controlling light fastness. There has been a

movement away from bleached jute weft fabrics because of the irregular fading

of the material on the wall. Although in many instances the wall covering

might still have a jute warp, the weft is now mainly viscose or a similar

material with the required color fastness. France is the major wall covering

producer with the Federal Republic of Germany second, followed by Sweden and

the United Kingdom.

With the European producers of decorative jute fabrics doing their

own weaving, they will require a steady supply of jute yarns, most likely from

the jute-producing countries. The sales of specialized yarns to the small

sophisticated weavers depend importantly on quality.

Other decorative end uses are small and consume a very minor tonnage

of jute goods. Mobile office partitions are on some occasions made with a dyed

jute covering. This is also the case with window display cloth for department

stores or specialty shops. Lampshades are another area severely handicapped by

poor light fastness of cellulostic fabric. Drapes also suffer from fading and

the effects of the hydroscopic nature of jute. Currently popular throughout

Europe are the "'shopping" type carrier bags, either plain or with a printed

motif.

The price and technical competitiveness of jute secondary carpet

backing and carpet weft yarns, and the requirement that agricultural product

exports to certain countries be packaged in jute sacks, helped stabilize jute

demand in Western Europe in the early 1980s. The current tight supply of and

high prices for jute products are undercutting jute's position. Therefore,

- 37 -

jute producers and manufacturers need to make a concerted effort to reesta-

blish jute's competitiveness in order to minimize the possible permanent

damage that would occur to their market position if the situation were to

persist long enough to attract capital investments to supply substitute

products. The model simulations indicate that success in this effort could

maintain a jute market of around 200,000 tons per year into the early 1990s.

The most promising area for increased jute consumption in Western

Europe is in secondary backing cloth for tufted carpets. A substantial growth

in the production of these carpets during the rest of the 1980s seems assured.

Given the demands of the export market for woven secondary backing and the

disaffection of local consumers with the foam backings at replacement time,

jute manufacturers have a unique opportunity to penetrate this market. The

growth will not automatically accrue to jute, however; keenly competitive

synthetic backing manufacturers will prevent that. Jute's success will depend

upon how well the market's needs are met for an uninterrupted supply of

competitively-priced fabric of acceptable quality. Technological developments

also change market requirements over time and the successful commercialization

of carpet backing cloth incorporating twistless jute yarns could make a dif-

ference in jute's market share into the 1990s. In any case, customer service

activities commensurate with those of the synthetic competitors would improve

the jute industry's communication of market developments to manufacturers and

vice-versa, thereby, improving jute's prospects for successfully exploiting

this opportunity. With so much depending on the successful management of the

market penetration effort, consumption of jute in carpet backing is highly

uncertain and could range from 50 to 80,000 tons in Western Europe at the end

of the decade.

- 38 -

In the bag market, demand is closely tied to the export of

commodities to areas not yet provided with bulk handling facilities and the

maintenance of price competitiveness with sacks of substitute materials.

Jute's comparative advantage here is in the lighter-weight bags, which should

keep consumption in this market at around 60,000 tons in 1990.

Jute consumption in carpet yarns, its other major end-use in Western

Europe, is projected to decline further during the 1980s due to falling

production of woven carpets. If jute maintains its recent share in weft yarns,

consumption would amount to around 35,000 tons at the end of the decade.

C. Japan

Japan's consumption of jute products peaked at 136,000 tons in 1968

and then trended irregularly downward to an average of 74,480 tons during the

first four years of the 1980s. Individual products experienced divetgent

trends; increased demand for jute carpet backing offset some of the impact of

the sharply declining use of jute bags.

During the 1970s jute manufacturing in Japan declined at a much

faster rate than the consumption of jute products. The import emphasis,

therefore, shifted from raw jute to products manufactured in the jute-produc-

ing countries. Raw jute imports were equivalent to 86% of apparent consumption

during 1967-69 but declined to only 15% of consumption during 1981-83.

Jute and kenaf bags for packaging foodgrains is the most important

single use for jute products in Japan. Indeed, this is the market on which the

domestic industry's rapid development in the early 1960s was largely based.

After six years of testing and official approval, jute bags were introduced

for packaging foodgrains in 1961. Jute bags made rapid gains against the

traditional straw bags, which required considerable farmers' time to make and

- 39 -

were more costly to buy than bags of other materials. During the 1970s, both

paper and synthetic bags gained importance as rice packaging materials.

Although price series for jute, paper and synthetic bags are unobtainable,

traders confirmed that jute bags were more expensive than either paper or

synthetic bags. Nevertheless, jute bags were often preferred since they could

be used three times and the others could be used only once. In 1980 it was

estimated that 55% of the jute bags used to package foodgrains were new and

45% had been used previously. Paper bags are not reusable and synthetic bags

are damaged in use and the government does not permit their reuse. Although

rice production declined by 26% between 1970 and 1980 paper bags used for

foodgrain packaging increased by 58% and synthetic bags in this use increased

by over six-fold, contributing to jute's decline of 50%.

While the total demand for bags for packaging and storage of

foodgrains in Japan has been adversely affected by declining domestic

production of rice, the development of bulk handling for imported grains has

also been important. Imports of foodgrains into Japan trended upward over the

last decade. Arrivals in 1969 totaled 5.1 million tons and in 1980, 7.0

million tons. Despite the rise in import volume, jute bags for this use fell

from 22 million in 1969 to 3.8 million in 1980 as increased bulk-handling

reduced the proportion of imported foodgrains packaged in bags (from 38% in

1969 to less than 5% in 1980).

In the 1970s, changing home-furnishing styles in Japan fostered

rapidly increasing production of tufted carpets. At the beginning of the

decade over 90 percent of the tufted carpets used a jute primary backing and

the more expensive one-fourth of those carpets also had a jute secondary

backing. Less costly backings such as latex coating or cotton and rayon mesh,

were used on the lower-priced carpets. By the mid-1970s, however, use of jute

- 40 -

primary carpet backing was negligible due to jute's inability to compete with

polypropylene in the heavier fabrics. During most years since 1970 jute

primary carpet backing has been priced at 30% to 100% higher than the

polypropylene substitute fabric.

Jute has been more competitive in the lighter-weight fabrics used as

a secondary backing for tufted carpets. Even so, the exports of jute carpet

backing cloth (primary and secondary) from the two main producing countries to

Japan increased from an average of 4,700 tons during 1967/68 to 1969/70 to an