prudential immediate income annuity · note: the forms referenced are included with your sales kit...

TRANSCRIPT

Annuities are issued by The Prudential Insurance Company of America

APPLICATIONFOR USE IN KENTUCKY AND NEW JERSEY ONLY

PRUDENTIALIMMEDIATE INCOME ANNUITY

Key Elements For A Good Order Application: We know how important it is to have your new business paperwork done right, the first time. The following information is being provided to assist you. For additional information regarding Prudential Immediate Income Annuity, consult the Important Information Disclosure Statement. If you have questions about completing this application or other new business support forms, please contact our National Sales Desk @ 1-800-513-0805. In order for Prudential to issue the Prudential Immediate Income Annuity contract, the Annuities Service Center must receive all premium(s) and paperwork in good order by 4:00 p.m eastern time. The payout option, frequency and commencement date may not be changed once the annuity contract is issued. An Illustration must be submitted at the time of application. Pre-Sale: Please be sure to complete all required state and product training prior to solicitation of new business.

SECTION NAMETYPE OF OWNERSHIP SECTION 1A • If Trust is checked, a Certificate of Entity Form must be completed and returned with the application.

ANNUITANT SECTION 1BNOTE: Prudential does not accept co-annuitants

JOINT ANNUITANT SECTION 1C

JOINT OWNER SECTION 1E • A Joint Owner is not available for Entity owned Annuities.

• Once the contract is issued the annuitant may not be changed.

• Joint Annuitants are allowed on all types of business and is a required designation for any contracts that select a “Joint” Life Payout.

OWNER SECTION 1D

BENEFICIARY INFORMATION SECTION 2

PURCHASE PAYMENT SECTION 3B

• Use Section 8 of this Application to list additional beneficiaries. • On an UTMA or UGMA account, the Minor’s estate must be the sole Primary Beneficiary.• A Contingent Beneficiary is not allowed on an UTMA or UGMA.• If a Beneficiary is not Designated, the Estate of the Owner will be named

• 1035: Non-qualified exchange with like ownership. • Transfer: Qualified funds going from institution to institution - same market.• Rollover: Qualified funds where client obtains constructive receipt.• Direct Rollover: An eligible rollover distribution that is paid directly to an eligible retirement plan.

OWNER & FINANCIAL PROFESSIONAL REPLACEMENT INFORMATION

SECTION 11

• Use Section 8 of this Application to specify additional coverage.• Responses are required for BOTH QUESTIONS. • Please make sure that these responses are consistent between OWNER and FINANCIAL

PROFESSIONAL.• If applicable, please ensure that replacement paperwork is consistent with Section 11 of the application.

TYPE OF CONTRACT TO BE ISSUED SECTION 3A

• Indicate the type of contract selected and if applicable, be sure the selection matches the type indicated on the Transfer and Exchange Form.

ANNUITY PAYOUT OPTIONS SECTION 4

• A Payout Option must be selected and cannot be changed after issuance of the contract. • If any Individual Life or Joint Life Payout Option is chosen, the annuity contract will not be issued

unless proof of age of the Annuitant and Joint Annuitant, if any, are attached. The following government-issued forms of I.D. are acceptable as proof of age: a copy of a birth certificate, driver’s license, military I.D., green card or passport.

• For additional information on the Payout Options see the Important Information Disclosure Statement provided in the Sales Kit.

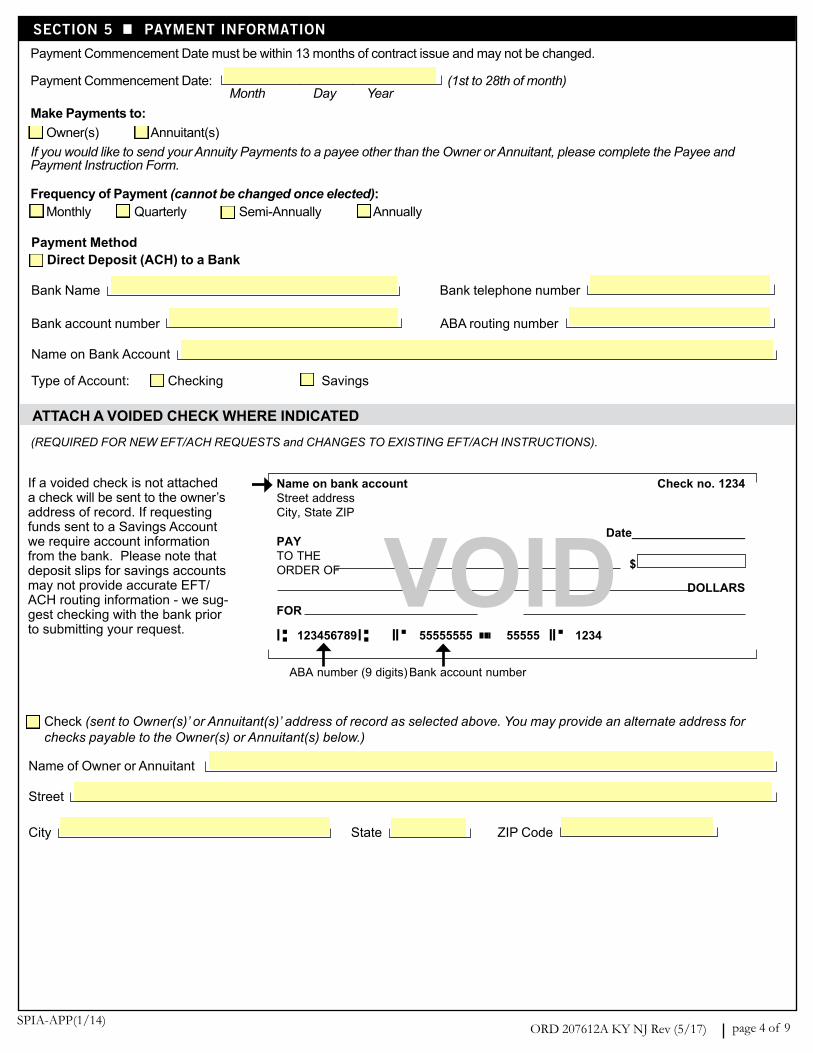

PAYMENT INFORMATION SECTION 5

PAYMENT INFORMATION: WITHHOLDING ELECTION AND TAX NOTIFICATION SECTION 6

OWNER ACKNOWLEDGEMENTS & SIGNATURE(S) SECTIONS 10 & 12

• The Owner(s) signature is required on the Owner signature line. The Annuitant’s signature is not required if the Owner and Annuitant are the same person.

• If the person signing as Owner is signing the application in his/her fiduciary capacity (such as a trustee) and is also the designated Annuitant, he/she must sign as Annuitant in his/her individual capacity.

• The State where application is signed must be completed in Section 12. • If application is signed in a State other than the Owner’s residence, a Contract Situs Form may be required. • Massachusetts and Utah require that the application is signed in the client’s resident state.

• Financial Professional information, signature(s) and commission options.• License and appointment is required in the Resident State of Issue and in any other state where

solicitation and/or contract delivery occurs.

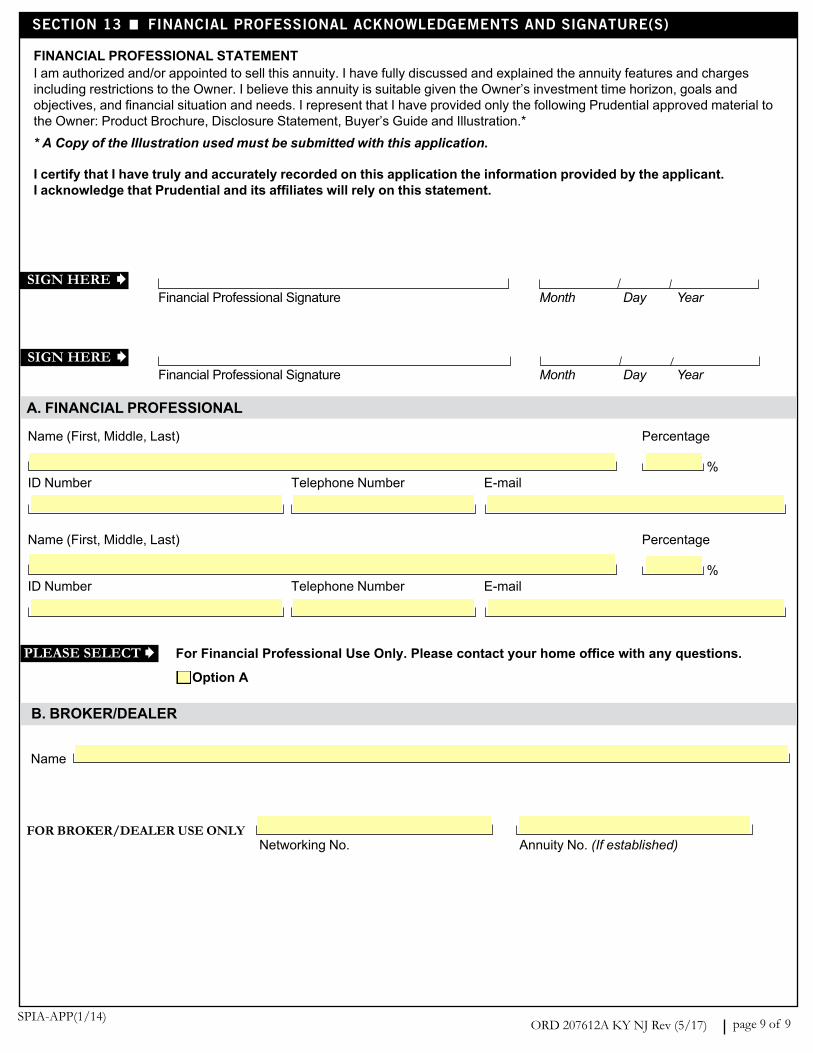

FINANCIAL PROFESSIONAL ACKNOWLEDGEMENT & SIGNATURE(S) SECTION 13

Note: The forms referenced are included with your Sales Kit unless otherwise noted. Additional forms may be required. Please see the application for details.

• Select the Payment Commencement Date. Annuity Payments begin on the Payment Commencement Date. You can expect to receive your Annuity Payment via EFT within approximately 3 business days, or via a check within approximately 5 business days after the Payment Commencement Date.

• Provide Banking or address information as to where the Payment should be sent.

• If not completed, Prudential will automatically withhold federal income taxes at the default status of Married with 3 exemptions and any mandatory state income taxes from your payments.

• For an UTMA/UGMA use: Name of Custodian C/F Name of Minor, State UTMA, e.g., “John Doe C/F John Doe, Jr., CT UTMA.” Provide the Minor’s Social Security Number in the SSN/TIN box.

• If Owner is a Non-Resident Alien, submit IRS Form W-8 (BEN, ECI, EXP or IMY). This form is available at www.IRS.gov.

SPIA-APP(1/14)ORD 207612A KY NJ Rev (5/17)

SECTION 1 ANNUITANT / OWNERSHIP INFORMATION

page 1 of 9

A. TYPE OF OWNERSHIP - Select One

Immediate Income AnnuityApplication Form

Annuities are issued by The Prudential Insurance Company of America (“Prudential”), Newark, NJ

Non Entity: Natural Person(s) UTMA/UGMA Entity: Custodian Trust* SEP-IRA* *If the Owner is a Trust or SEP-IRA, you must complete and submit the Certificate of Entity form with this application.

B. ANNUITANT

C. JOINT ANNUITANT - Complete this Section only if a Joint Life Payout Option is chosen.

Name (First, Middle, Last) Male Female Birth Date (Mo - Day - Yr) SSN / TIN

Street Address City State ZIP

Telephone Number E-mail Address

U.S. Citizen Resident Alien/Citizen of:

Non-Resident Alien/Citizen of: (Submit IRS Form W-8 (BEN, ECI, EXP or IMY))

Name (First, Middle, Last) Male Female Birth Date (Mo - Day - Yr) SSN / TIN

Street Address City State ZIP

Telephone Number E-mail Address

U.S. Citizen Resident Alien/Citizen of:

Non-Resident Alien/Citizen of: (Submit IRS Form W-8 (BEN, ECI, EXP or IMY))

Relationship to Annuitant

Annuities Service CenterFinancial Professionals: 1-800-513-0805 Fax 1-800-576-1217 www.prudentialannuities.com

Regular Mail DeliveryPrudential Annuity Service Center P.O. Box 7960 Philadelphia, PA 19176

Overnight Service, Certified or Registered Mail DeliveryPrudential Annuity Service Center 2101 Welsh Road Dresher, PA 19025

SPIA-APP(1/14)ORD 207612A KY NJ Rev (5/17) page 2 of 9

D. OWNER

E. JOINT OWNER - Not available for entity-owned Annuities or Qualified Annuities. Check here to designate the Joint Owners as each other’s Primary Beneficiary.

Name (First, Middle, Last) Male Female Birth Date (Mo - Day - Yr) SSN / TIN

Street Address City State ZIP

U.S. Citizen Resident Alien/Citizen of:

Non-Resident Alien/Citizen of: (Submit IRS Form W-8 (BEN, ECI, EXP or IMY))

Relationship to Owner:

SECTION 1 ANNUITANT / OWNERSHIP INFORMATION (continued)

• ForCustodialIRAcontracts,theCustodianmustbelistedastheBeneficiary.IndicateclassificationsofeachBeneficiary.PercentageofbenefitforallPrimaryBeneficiariesmusttotal100%.PercentageofbenefitforallContingentBeneficiariesmusttotal100%.IftheJointOwnershavebeenchosenaseachother’sPrimaryBeneficiary,thenonlyContingentBeneficiariesmaybedesignatedbelow.

SECTION 2 BENEFICIARY INFORMATION - NOTE: If more than 3 beneficiaries see section 8

Name (First, Middle, Last) Male Female Birth Date (Mo - Day - Yr)

Street Address City State ZIP

Primary Contingent Telephone Number SSN/TIN

Relationship Percentage %

Name (First, Middle, Last) Male Female Birth Date (Mo - Day - Yr)

Street Address City State ZIP

Primary Contingent Telephone Number SSN/TIN

Relationship Percentage %

Name (First, Middle, Last) Male Female Birth Date (Mo - Day - Yr)

Street Address City State ZIP

Primary Contingent Telephone Number SSN/TIN

Relationship Percentage %

Name (First, Middle, Last, or Trust / Entity) Male Female Birth Date (Mo - Day - Yr) SSN / TIN

Street Address City State ZIP

Telephone Number E-mail Address

U.S. Citizen Resident Alien/Citizen of:

Non-Resident Alien/Citizen of: (Submit IRS Form W-8 (BEN, ECI, EXP or IMY))

SPIA-APP(1/14)ORD 207612A KY NJ Rev (5/17) page 3 of 9

SECTION 3 ANNUITY INFORMATION

A. TYPE OF CONTRACT TO BE ISSUED

EmployerPlanNo.(ifavailable)Employer Plan Name

Street Address City State ZIP

Non-Qualified SEP-IRA* IRA Roth IRA*The following information is only required if the contract is being issued under a Simplified Employee Pension Plan (SEP):

Are you Self Employed? Yes No

Transfer . . . . . . . . . . . . $

Rollover............$

DirectRollover.......$

IRA / Roth IRA Contribution . . . . . . . . . $ for tax year

Make all checks payable to The Prudential Insurance Company of America. Purchase Payments may be restricted byPrudential.

QUALIFIED CONTRACT PAYMENT TYPE Indicate type of initial estimated payment(s).

B. PURCHASE PAYMENTS

NON-QUALIFIED CONTRACT PAYMENT TYPE Indicate type of initial estimated payment(s).

1035Exchange..........$

Amount Enclosed . . . . . . . . .$

CD Transfer or Mutual Fund Redemption . . .$

If no year is indicated, contribution defaults to current tax year.

SOURCE OF FUNDS Non-Qualified SEP-IRA 403(b) Traditional IRA 401(a) Roth IRA 401(k)

Other

If Purchase Payment is not included, please check one or both of these boxes:

Transfer of Asset Paperwork Submitted Applicant Requesting Funds (If permitted)

CheckhereifmultiplePurchasePaymentswillbereceivedbyPrudential(asaresultofatransfer,exchangeorrollover)andtoauthorizePrudentialtodelayissuanceofyourcontractfortheearlierof(a)60daysor(b)untilthenumberofexpectedPurchasePaymentsindicatedbelowhavebeenreceived.NointerestwillaccrueonanyPurchasePaymentsreceivedbeforetheissuedateofyourcontractandyourpaymentswillnotbeotherwiseadjusted.AnysubsequentPurchasePaymentsreceivedafterthe60th day or after the indicated number of expected Purchase Payments will require a new application.

Number of expected Purchase Payments:

SECTION 4 ANNUITY PAYOUT OPTIONS - CHOOSE ONE OF THE OPTIONS BELOW. CERTAIN OPTIONS MAY BE SUBJECT TO ADDITIONAL LIMITATIONS. CONSULT YOUR FINANCIAL PROFESSIONAL. THE ANNUITY PAYOUT OPTION MAY NOT BE CHANGED.

IMPORTANT: If any Individual Life or Joint Life Payout Option is chosen below, the annuity contract will not be issued unless proof of age of the Annuitant and Joint Annuitant, if any, are attached. The following government-issued forms of I.D. are acceptable as proof of age: a copy of a birth certificate, driver’s license, military I.D., green card or passport.

Period Certain Only, Payment for Years (5 to 25 Years. Must be in whole years.)

IndividualLifeOnly IndividualLifewithCashRefund IndividualLifewithInstallmentRefund

IndividualLifewithPeriodCertainfor Years (5 to 25 Years. Must be in whole years.)

The below Payout Options are only available if a Joint Annuitant is named in section 1C. Joint Life Only JointLifewith662/3%toSurvivor JointLifewith50%toSurvivor Joint Life with Cash Refund Joint Life with Installment Refund

Joint Life with Period Certain for Years (5 to 25 Years. Must be in whole years.)

Joint Life with Period Certain for Yearswith662/3%toSurvivor(5 to 25 Years. Must be in whole years.)

Joint Life with Period Certain for Yearswith50%toSurvivor(5 to 25 Years. Must be in whole years.)

SPIA-APP(1/14)ORD 207612A KY NJ Rev (5/17) page 4 of 9

PaymentCommencementDatemustbewithin13monthsofcontractissueandmaynotbechanged.

Payment Commencement Date: (1st to 28th of month) Month Day YearMake Payments to:

Owner(s) Annuitant(s)If you would like to send your Annuity Payments to a payee other than the Owner or Annuitant, please complete the Payee and Payment Instruction Form.

Frequency of Payment (cannot be changed once elected): Monthly Quarterly Semi-Annually Annually

SECTION 5 PAYMENT INFORMATION

Payment Method Direct Deposit (ACH) to a Bank

Bank Name Bank telephone number

Bank account number ABA routing number

Name on Bank Account

Type of Account: Checking Savings

ATTACH A VOIDED CHECK WHERE INDICATED

Check (sent to Owner(s)’ or Annuitant(s)’ address of record as selected above. You may provide an alternate address for checks payable to the Owner(s) or Annuitant(s) below.)

Name of Owner or Annuitant

Street

City State ZIP Code

Ifavoidedcheckisnotattached a check will be sent to the owner’s address of record. If requesting fundssenttoaSavingsAccountwe require account information from the bank. Please note that depositslipsforsavingsaccountsmaynotprovideaccurateEFT/ACH routing information - we sug-gest checking with the bank prior to submitting your request.

(REQUIRED FOR NEW EFT/ACH REQUESTS and CHANGES TO EXISTING EFT/ACH INSTRUCTIONS).

SPIA-APP(1/14)ORD 207612A KY NJ Rev (5/17) page 5 of 9

SECTION 6 PAYMENT INFORMATION: WITHHOLDING ELECTION AND TAX NOTIFICATION

If you do not complete this section, Prudential will automatically withhold federal income taxes at the default status of Married with 3 exemptions and any mandatory state income taxes from your payments.Generally, the taxable portion of a payment from an annuity contract is considered ordinary income for tax purposes. Federal and some state laws require that Prudential withhold income tax from certain cash distributions, unless the recipient requests that we notwithhold.YoumaynotoptoutofwithholdingunlessyouhaveprovidedPrudentialwithaU.S.residenceaddressandaSocialSecurityNumber/TaxpayerIdentificationNumber.Ifyourequestadistributionthatissubjecttowithholdinganddonotinformusinwriting NOT to withhold Federal Income Tax before the date payment must be made, the legal requirements are for us to withhold taxfromsuchpayment.IfyouelectnottohavetaxwithheldfromadistributionoriftheamountofFederalIncomeTaxwithheldisinsufficient,youmayberesponsibleforpaymentofestimatedtax.Youmayincurpenaltiesundertheestimatedtaxrulesifyourwithholdingestimatedtaxpaymentsarenotsufficient.Youmaywishtoconsultwithyourtaxadvisor.SomestateshaveenactedStatetaxwithholding.Generally,however,anelectionoutofFederalwithholdingisanelectionoutofStatewithholding.ThewithholdingelectionyoumakebelowcanbechangedatanytimebutwillapplyuntilanewelectionisreceivedatourServiceOfficeinGoodOrder.

Withholding Allowances: Please complete the following information. This information will be used to compute the applicable income tax withholding on your payments.

Withhold federal income taxes on the taxable portion of my annuity payments based on the following criteria:

Marital Status: Married Single Total allowances you are claiming: or Percentage: %* Specificdollaramount:$

IdonotwishtohaveanyfederalincometaxeswithheldIfyouwanttohavestate income taxes withheld from the taxable portion of your annuity payments, please check the appropriate box(es)belowandcompleteanyotherapplicableboxes.Pleasebeadvisedthatifyourresidentstaterequiresmandatory withholding, we will withhold the default amount your state requires if you elect no withholding.

Withhold state income taxes on the taxable portion of my annuity payments based on the following criteria: Marital Status: Married Single

Exemptions: Other (please specify): or Percentage: %* Specificdollaramount:$ Idonotwishtohaveanystateincometaxeswithheld*Percentage/Dollar amount cannot be less than the minimum required by your state of residence. If the amount above is less, we will withhold the default amount required by your state.

Michigan Residents Must CompleteMichigan law now requires 4.25% income tax withholding from pension and retirement benefits, unless your payments are not taxable, or you opt out, by checking the box below.

Your pension or annuity payments are not taxable or you wish to opt out. Note: Opting out may result in a balance due on your MI-1040 as well as penalties and interest.

% Totalpercentageyouwantwithheldfromyourannuitypayment(s)(mustbeatleast4.25%).If no selection is made, we will withhold 4.25%

If not checked we will assume that your answer is “YES”.Fordefinitions,seeDefinitionsandDisclosures.

DO YOU AUTHORIZE your Financial Professional to perform Contract Maintenance? Yes No

SECTION 7 FINANCIAL PROFESSIONAL AUTHORIZATION

SPIA-APP(1/14)ORD 207612A KY NJ Rev (5/17) page 6 of 9

SECTION 8 ADDITIONAL INFORMATION

SECTION 9 NOTICES & DISCLAIMERS

ALABAMA: Any person who knowingly presents a false or fraudulent claim for payment of a loss or benefit or who knowingly presents false information in an application for insurance is guilty of a crime and may be subject to restitution fines or confinement in prison, or any combination thereof.ALASKA: All statements and descriptions in an application for an insurance policy or annuity contract, or in negotiations for the policy or contract, by or in behalf of the insured or annuitant, shall be considered to be representations and not warranties. Misrepresentations, omissions, concealment of facts, and incorrect statements may not prevent a recovery under the policy or contract unless either (1) fraudulent; (2) material either to the acceptance of the risk, or to the hazard assumed by the insurer; or (3) the insurer in good faith would either not have issued the policy or contract, or would not have issued a policy or contract in as large an amount, or at the same premium or rate, or would not have provided coverage with respect to the hazard resulting in the loss, if the true facts had been made known to the insurer as required either by the application for the policy or contract or otherwise.ARIZONA: Upon written request an insurer is required to provide, within a reasonable time, factual information regarding the benefits and provisions of the annuity contract to the contract owner.If for any reason you are not satisfied with this contract, you may return it to us within 10 days (or 30 days for applicants 65 or older) of the date you receive it. All you have to do is take it or mail it to one of our offices or to the representative who sold it to you, and it will be canceled from the beginning. If this is not a variable contract, any monies paid will be returned promptly. If this is a variable contract, any monies paid will be returned promptly after being adjusted according to state law.

CALIFORNIA: If any Participant(s)/Owner(s) (or Annuitant for entity-owned contracts) is age 60 or older, you are required to complete the “Important Information for Annuities Issued or Delivered in California” form.COLORADO: It is unlawful to knowingly provide false, incomplete, or misleading facts or information to an insurance company for the purpose of defrauding or attempting to defraud the company. Penalties may include imprisonment, fines, denial of insurance, and civil damages. Any insurance company or agent of an insurance company who knowingly provides false, incomplete, or misleading facts or information to a policy holder or claimant for the purpose of defrauding or attempting to defraud the policy holder or claimant with regard to a settlement or award payable from insurance proceeds shall be reported to the Colorado Division of Insurance within the Department of Regulatory Agencies.FLORIDA: Any person who knowingly and with intent to injure, defraud or deceive any insurer, files a statement of claim or an application containing any false, incomplete or misleading information is guilty of a felony of the third degree.KANSAS: Any person who knowingly presents a false or fraudulent claim for payment of a loss or benefit or knowingly presents false information in an application for insurance may be guilty of insurance fraud as determined by a court of law and may be subject to fines and confinement in prison.

KENTUCKY: Any person who knowingly and with intent to defraud any insurance company or other person files an application for insurance containing any materially false information or conceals, for the purpose of misleading, information concerning any fact material thereto commits a fraudulent insurance act, which is a crime.MAINE, TENNESSEE, VIRGINIA, and WASHINGTON: It is a crime to knowingly provide false, incomplete or misleading information to an insurance company for the purpose of defrauding the company. Penalties may include imprisonment, fines or a denial of insurance benefits.

MARYLAND: Any person who knowingly or willfully presents a false or fraudulent claim for payment of a loss or benefit or who knowingly or willfully presents false information in an application for insurance is guilty of a crime and may be subject to fines and confinement in prison.

NEW JERSEY: Any person who includes any false or misleading information on an application for an insurance policy is subject to criminal and civil penalties.

NORTH CAROLINA: North Carolina residents must respond to this question:1. Do you believe the annuity meets your financial objectives and anticipated future financial needs? Yes No

OHIO: Any person who, with intent to defraud or knowing that he is facilitating a fraud against an insurer, submits an application or files a claim containing a false or deceptive statement is guilty of insurance fraud.

OKLAHOMA: WARNING — Any person who knowingly, and with intent to injure, defraud or deceive any insurer, makes any claim for the proceeds of an insurance policy containing any false, incomplete or misleading information is guilty of a felony.

OREGON, GEORGIA and VERMONT: — Any person who knowingly presents a materially false statement in an application for insurance may be guilty of a criminal offense and subject to penalties under state law.

PENNSYLVANIA: Any person who knowingly and with intent to defraud any insurance company or other person files an application for insurance or statement of claim containing any materially false information or conceals for the purpose of misleading, information concerning any fact material thereto commits a fraudulent insurance act, which is a crime and subjects such person to criminal and civil penalties.

ALL OTHER STATES: Any person who knowingly and willfully presents a false or fraudulent claim for payment of a loss or benefit or who knowingly and willfully presents false information in an application for insurance is guilty of a crime and may be subject to fines and confinement in prison.

• Special Instructions • Annuity Replacement • EntityAuthorizedIndividuals• BeneficiariesIf needed for:

SPIA-APP(1/14)ORD 207612A KY NJ Rev (5/17) page 7 of 9

SECTION 10 OWNER ACKNOWLEDGEMENTS

• IacknowledgethatIhavereceivedonlyaProductBrochure,DisclosureStatement,Buyer’sGuideandIllustrationandhavehad an opportunity to ask my Financial Professional questions about the annuity Payout Options and other contract features availabletome;and

• Irepresenttothebestofmyknowledgeandbeliefthatthestatementsmadeinthisapplicationaretrueandcomplete;and

• Thisannuityissuitableformyinvestmenttimehorizon,goalsandobjectivesandfinancialsituationandneeds;and

• IunderstandthatthePaymentCommencementDatemustbewithin13monthsofcontractissue;and

• IunderstandthatthePayoutOptionandFrequencyofPaymentcannotbechanged;and

• Iunderstandthat,dependingonthepayoutoptionIselect,theAnnuityforwhichIamapplyingmaynotprovideanyannuity paymentsordeathbenefitiftheowner(orannuitant)diesaftertheAnnuityStartDate;and

• Iunderstandthepolicyhasnocashvalue,loanvalueorsurrendervalue;and

• I understand that annuity payments are guaranteed at purchase and Prudential will neither increase nor decrease such paymentsinresponsetointerestratesorinflation;and

• IrepresentthattheAnnuityforwhichIamapplyingisnotbeingpurchasedforspeculation,arbitrage,viaticationoranyother typeofcollectiveinvestmentschemenoworatanytimepriortoitstermination;and

• IacknowledgethattheAnnuityforwhichIamapplyingmaynotbetradedonanystockexchangeorsecondarymarket;and

• I represent that I am not being compensated in any way for the purchase of the Annuity for which I am applying.

• By signing below, I authorize Prudential to initiate credit entries and if necessary, adjustments for any credit entries made in errortomybankaccountasindicatedinSection5.IalsodirectthebanknamedinSection5tocreditand/ordebitthesame tosuchaccount.Thisauthorizationwillremainineffectuntilfurtherwrittennoticefrommeisreceivedandprocessedbythe PrudentialAnnuityServiceCenter.IunderstandthatPrudentialisrelyingontheinformationthatIhaveprovidedonthis application, and further understand that Prudential will not be liable for any losses or charges due to incorrect, outdated, or incompletebankinginformationthathasbeenprovidedonthisapplication.

SECTION 11 OWNER & FINANCIAL PROFESSIONAL - REPLACEMENT INFORMATION

Both the Owner Response and the Financial Professional Response columns must be completed. REQUIRED

Replacement Questions Owner Response Financial ProfessionalResponse

DoestheOwnerhaveanyexistingindividuallifeinsurancepoliciesorannuity contracts?(If yes, a State Replacement Form is required for NAIC model regulation states.)

YES NO YES NO

Willthisannuityreplaceorchangeanyexistingindividuallifeinsurancepolicies or annuity contracts?(If yes, complete the following and submit a State Replacement Form, if required.)

If yes - Company:

Policy #: Year Issued :

YES NO YES NO

ORD 207612A KY NJ Rev (5/17) page 8 of 9

SECTION 12 OWNER SIGNATURE(S)

Underpenaltyofperjury,Icertifythatthetaxpayeridentificationnumber(TIN)IhavelistedonthisformismycorrectTIN. Ifurthercertifythatthecitizenship/residencystatusIhavelistedonthisformismycorrectcitizenship/residencystatus.IhavebeennotifiedbytheInternalRevenueServicethatIamsubjecttobackupwithholdingduetounderreportingofinterest ordividends.

(If contract is issued in a State other than the Owner’s State of Residence, a Contract Situs Form may be required.)State where signed

SPIA-APP(1/14)

The Internal Revenue Service does not require your consent to any provision of this document other than the certifications required to avoid backup withholding.

Owner Signature Month Day Year

Joint Owner Signature Month Day Year

Annuitant Signature Month Day Year

Joint Annuitant Signature Month Day Year

Ifsigningonbehalfofanentity,youmustindicateyourofficialtitle/positionwiththeentity;ifsigningasaTrusteeforaTrust,pleaseprovidetheTrusteedesignation.

REQUIRED

Owner’s Tax Certification (Substitute W-9)

SIGN HERE

SIGN HERE

SIGN HERE

SIGN HERE

TITLE (if any)

SPIA-APP(1/14)ORD 207612A KY NJ Rev (5/17) page 9 of 9

B. BROKER/DEALER

SECTION 13 FINANCIAL PROFESSIONAL ACKNOWLEDGEMENTS AND SIGNATURE(S)

A. FINANCIAL PROFESSIONAL

Name

FINANCIAL PROFESSIONAL STATEMENTIamauthorizedand/orappointedtosellthisannuity.IhavefullydiscussedandexplainedtheannuityfeaturesandchargesincludingrestrictionstotheOwner.IbelievethisannuityissuitablegiventheOwner’sinvestmenttimehorizon,goalsandobjectives,andfinancialsituationandneeds.IrepresentthatIhaveprovidedonlythefollowingPrudentialapprovedmaterialtothe Owner: Product Brochure, Disclosure Statement, Buyer’s Guide and Illustration.** A Copy of the Illustration used must be submitted with this application.

I certify that I have truly and accurately recorded on this application the information provided by the applicant. I acknowledge that Prudential and its affiliates will rely on this statement.

Financial Professional Signature Month Day Year

Financial Professional Signature Month Day Year

FOR BROKER/DEALER USE ONLY Networking No. Annuity No. (If established)

For Financial Professional Use Only. Please contact your home office with any questions.

Option A

SIGN HERE

SIGN HERE

Name (First, Middle, Last) Percentage

%ID Number Telephone Number E-mail

Name (First, Middle, Last) Percentage

%ID Number Telephone Number E-mail

PLEASE SELECT

DEFINITIONS AND DISCLOSURES

You are advised to consult the Disclosure Statement or annuity for explanations of any of the terms used, or contact Prudential with any questions.AUTHORIZATION: In Section 7, you may grant or deny your Financial Professional access to your Annuity Contract Information and give that person the ability to perform Contract Maintenance.Neither Prudential nor any person authorized by Prudential will be responsible for, and you agree to indemnify and hold Prudential harmless from and against, any claim, loss, taxes, penalties or any other liability or damages in connection with, or arising out of, any act or omission if we acted on an authorized individual’s instructions in good faith and in reliance on this Authorization. “Contract Maintenance” is currently limited to changes to the Address-of-Record for the Owner(s), Additional maintenance activities may be available in the future.This authorization may be revoked by calling 1-800-513-0805. Proper identification of the caller will be required to revoke this authorization.

BENEFICIARIES • The Owner reserves the right to change the Beneficiary unless the

Owner notifies Prudential in writing that the Beneficiary designation is irrevocable.

• If an Attorney-in-Fact signs the enrollment, the Attorney-in-Fact may only be designated as a Beneficiary if the Power-of-Attorney instrument and the relevant state law permit it.

DEATH BENEFITPrior to the Annuity Start Date, death benefit proceeds are payable to the surviving Owner, if any, otherwise to the named Beneficiaries.Depending on the Annuity Payout Option chosen, the contract may not provide for any annuity payments, including any death benefit, after the death of the annuitant. Life Only or Joint Life Only Payout Options do not provide any annuity payments or death benefit if the annuitant’s death occurs between the Annuity Start Date and the Payment Commencement Date and all Purchase Payments made in connection with the contract will be forfeited. Please see the Disclosure Statement or consult your Financial Professional for more information. Please see the Disclosure Statement or consult your Financial Professional for more information.For Federal tax purposes, the term “spouse” includes any individuals who are lawfully married under state law. Federal law does not recognize domestic partnerships or civil unions that are not designated as “married” under state law. Therefore, we cannot permit a civil union partner or domestic partner who is not recognized under state law as “married” to continue the annuity within the meaning of the tax law under the annuity’s “spousal continuance” provision. An alternative distribution option referred to as “Taxable Contract Continuation” is available to domestic partners and civil unions.

IRS CODE 501: Section of the Internal Revenue Code that generally exempts certain corporations and trusts from Federal income tax. This exemption covers charitable organizations.

TAX REPORTING AND WITHHOLDING STATEMENT: There may be tax implications as a result of certain cash distributions, including systematic withdrawals, and the request(s) (including tax reporting and withholding) cannot be reversed once processed.Federal and some state laws require that Prudential withhold income tax from certain cash distributions, unless the recipient requests that we not withhold. You may not opt out of withholding unless you have provided Prudential with a U.S. residence address and a Social Security Number/ Taxpayer Identification Number.

If you do not inform us in writing NOT to withhold Federal Income Tax before the date payment must be made, the legal requirements are for us to withhold tax from such payment.If you elect not to have tax withheld from a distribution or if the amount of Federal Income Tax withheld is insufficient, you may be responsible for payment of estimated tax. You may incur penalties under the estimated tax rules if your withholding estimated tax payments are not sufficient. For this purpose you may wish to consult with your tax advisor.Some states have enacted State tax withholding. Generally, however, anelection out of Federal withholding is an election out of State withholding. SITUS RULES: Contracts solicited, signed and issued outside of the client’s resident state require that a fully completed Situs Form be submitted with the application. In the event that the financial professional is licensed in both the client’s resident state and the state of solicitation, and where the Situs Form criteria is not applicable, the annuity may be issued in the client’s resident state. The Additional Information Section of the application should be noted to reflect that the contract should be issued in the client’s resident state and not the state of signing.

Please note that all state specific requirements apply to the state in whichthe contract is being issued.

ADDITIONAL INFORMATIONWe may apply certain limitations, restrictions, and/or standards as a condition of our issuance of an Annuity and/or acceptance of Purchase Payments.

We have the right to reject this application.Annuity Payments begin on the Payment Commencement Date. You can expect to receive your Annuity Payment via EFT within approximately 3 business days, or via a check within approximately 5 business days after the Payment Commencement Date.

Prudential Annuities, Prudential, the Prudential logo and the Rock symbol are service marks of Prudential Financial, Inc. and its related.

This form, and the information contained within, does not take into account the investment objectives or financial situation of any client or prospective clients. The information is not intended as investment advice and is not a recommendation about managing or investing your retirement savings. Clients seeking information regarding their particular investment needs should contact a financial professional.

Annuities Service Center P.O. Box 7960Philadelphia, PA 19176

ORD 207612A KY NJ

New Business Kit (5/18)

ANNUITIES:•NOT A DEPOSIT •NOT FDIC INSURED • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • NOT BANK OR CREDIT UNION GUARANTEED • MAY LOSE VALUE

Buyer’s Guide for

DeferredAnnuitiesDeferredAnnuities

Fixed

Prepared by the

NAIC

National Association of Insurance Commissioners

The National Association of Insurance Commissioners is an association of state insurance regulatory officials. This association helps the various insurance departments to coordinate insurance laws for the benefit of all consumers.

This guide does not endorse any company or policy.

Reprinted by ... The Prudential Insurance Company of America

NAIC Buyer’s Guide for Fixed Deferred Annuities

It’s important that you understand how annuities can be different from each other so you can choose the type of annuity that’s best for you. The purpose of this Buyer’s Guide is to help you do that. This Buyer’s Guide isn’t meant to offer legal, financial, or tax advice. You may want to consult independent advisors that specialize in these areas.

This Buyer’s Guide is about fixed deferred annuities in general and some of their most common features. It’s not about any particular annuity product. The annuity you select may have unique features this Guide doesn’t describe. It’s important for you to carefully read the material you’re given or ask your annuity salesperson, especially if you’re interested in a particular annuity or specific annuity features.

This Buyer’s Guide includes questions you should ask the insurance company or the annuity salesperson (the agent, producer, broker, or advisor). Be sure you’re satisfied with the answers before you buy an annuity.

Revised 2013

© 1999, 2007, 2013 National Association of Insurance Commissioners. All rights reserved.

Printed in the United States of America

No part of this book may be reporduced, stored in a retrieval system, or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording or any storage or retrieval system, without written permission from the NAIC.

NAIC Executive Office444 North Capitol Street, NWSuite 701Washington, DC 20001-1509202.471.3990

NAIC Central Office1100 Walnut StreetSuite 1500Kansas City, MO 64106-2197816.842.3600

NAIC Capital Markets &Investment Analysis Office48 Wall Street, 6th FloorNew York, NY 10005-2906212.398.9000

Buyer’s Guide for Deferred Annuities

© 2013 National Association of Insurance Commissioners

Tab

le o

f C

on

ten

ts

Table of Contents

What Is an Annuity? ........................................................................................ 1 When Annuities Start to Make Income Payments ...................................................................1

How Deferred Annuities Are Alike ..........................................................................................1

How Deferred Annuities Are Different ....................................................................................2

How Does the Value of a Deferred Annuity Change? ........................................ 3 Fixed Annuities .........................................................................................................................3

Fixed Indexed Annuities ...........................................................................................................3

What Other Information Should You Consider? ............................................... 4 Fees, Charges, and Adjustments ................................................................................................4

How Annuities Make Payments ...............................................................................................4

How Annuities Are Taxed ........................................................................................................5

Finding an Annuity That’s Right for You ..................................................................................6

Questions You Should Ask .......................................................................................................6

When You Receive Your Annuity Contract ..............................................................................7

Buyer’s Guide for Deferred Annuities

© 2013 National Association of Insurance Commissioners1

Wh

at I

s an

An

nu

ity?

What Is an Annuity?

An annuity is a contract with an insurance company. All annuities have one feature in common, and it makes annuities different from other financial products. With an annuity, the insurance company promises to pay you income on a regular basis for a period of time you choose—including the rest of your life.

When Annuities Start to Make Income Payments

Some annuities begin paying income to you soon after you buy it (an immediate annuity). Others begin at some later date you choose (a deferred annuity).

How Deferred Annuities Are Alike

There are ways that most deferred annuities are alike.

They have an accumulation period and a payout period. During the accumulation period, the value of your annuity changes based on the type of annuity. During the payout period, the annuity makes income payments to you.

They offer a basic death benefit. If you die during the accumulation period, a deferred annuity with a basic death benefit pays some or all of the annuity’s value to your survivors (called beneficiaries) either in one payment or multiple payments over time. The amount is usually the greater of the annuity account value or the minimum guaranteed surrender value. If you die after you begin to receive income payments (annuitize), your chosen survivors may not receive

anything unless: 1) your annuity guarantees to pay out at least as much as you paid into the annuity, or 2) you chose a payout option that continues to make payments after your death. For an extra cost, you may be able to choose enhanced death benefits that increase the value of the basic death benefit.

You usually have to pay a charge (called a surrender or withdrawal charge) if you take some or all of your money out too early (usually before a set time period ends). Some annuities may not charge if you withdraw small amounts (for example, 10% or less of the account value) each year.

Any money your annuity earns is tax deferred. That means you won’t pay income tax on earnings until you take them out of the annuity.

You can add features (called riders) to many annuities, usually at an extra cost.

An annuity salesperson must be licensed by your state insurance department. A person selling a variable annuity also must be registered with FINRA1 as a representative of a broker/dealer that’s a FINRA member. In some states, the state securities department also must license a person selling a variable annuity.

1. FINRA (Financial Industry Regulatory Authority) regulates the companies and salespeople who sell variable annuities.

Sources of Information

Contract: The legal document between you and the insurance company that binds both of you to the terms of the agreement.

Disclosure: A document that describes the key features of your annuity, including what is guaranteed and what isn’t, and your annuity’s fees and charges. If you buy a variable annuity, you’ll receive a prospectus that includes detailed information about investment objectives, risks, charges, and expenses.

Illustration: A personalized document that shows how your annuity features might work. Ask what is guaranteed and what isn’t and what assumptions were made to create the illustration.

Buyer’s Guide for Deferred Annuities

© 2013 National Association of Insurance Commissioners 2

Wh

at I

s an

An

nu

ity?

Insurance companies sell annuities. You want to buy from an insurance company that’s financially sound. There are various ways you can research an insurance company’s financial strength. You can visit the insurance company’s website or ask your annuity salesperson for more information. You also can review an insurance company’s rating from an independent rating agency. Four main firms currently rate insurance companies. They are A.M. Best Company, Standard and Poor’s Corporation, Moody’s Investors Service, and Fitch Ratings. Your insurance department may have more information about insurance companies. An easy way to find contact information for your insurance department is to visit www.naic.org and click on “States and Jurisdictions Map.”

Insurance companies usually pay the annuity salesperson after the sale, but the payment doesn’t reduce the amount you pay into the annuity. You can ask your salesperson how they earn money from the sale.

How Deferred Annuities Are Different

There are differences among deferred annuities. Some of the differences are:

Whether you pay for the annuity with one or more than one payment (called a premium).

The types and amounts of the fees, charges, and adjustments. While almost all annuities have some fees and charges that could reduce your account value, the types and amounts can be different among annuities. Read the Fees, Charges, and Adjustments section in this Buyer’s Guide for more information.

Whether the annuity is a fixed annuity or a variable annuity. How the value of an annuity changes is different depending on whether the annuity is fixed or variable.

Fixed annuities guarantee your money will earn at least a minimum interest rate. Fixed annuities may earn interest at a rate higher than the minimum but only the minimum rate is guaranteed. The insurance company sets the rates.

Fixed indexed annuities are a type of fixed annuity that earns interest based on changes in a market index, which measures how the market or part of the market performs. The interest rate is guaranteed to never be less than zero, even if the market goes down.

Variable annuities earn investment returns based on the performance of the investment portfolios, known as “subaccounts,” where you choose to put your money. The return earned in a variable annuity isn’t guaranteed. The value of the subaccounts you choose could go up or down. If they go up, you could make money. But, if the value of these subaccounts goes down, you could lose money. Also, income payments to you could be less than you expected.

premium bonus, which usually is a lump sum amount the insurance company adds to your annuity when you buy it or when you add money. It’s usually a set percentage of the amount you put into the annuity. Other annuities offer an interest bonus, which is an amount the insurance company adds to your annuity when you earn interest. It’s usually a set percentage of the interest earned. You may not be able to withdraw some or all of your premium bonus for a set period of time. Also, you could lose the bonus if you take some or all of the money out of your annuity within a set period of time.

Buyer’s Guide for Deferred Annuities

© 2013 National Association of Insurance Commissioners3

Val

ue

of a

Def

erre

d A

nn

uit

yHow Does the Value of a Deferred Annuity Change?

Fixed Annuities

Money in a fixed deferred annuity earns interest at a rate the insurer sets. The rate is fixed (won’t change) for some period, usually a year. After that rate period ends, the insurance company will set another fixed interest rate for the next rate period. That rate could be higher or lower than the earlier rate.

Fixed deferred annuities do have a guaranteed minimum interest rate—the lowest rate the annuity can earn. It’s stated in your contract and disclosure and can’t change as long as you own the annuity. Ask about:

initial interest rate – What is the rate? How long until it will change?renewal interest rate – When will it be announced? How will the insurance

company tell you what the new rate will be?

Fixed Indexed Annuities

Money in a fixed indexed annuity earns interest based on changes in an index. Some indexes are measures of how the overall financial markets perform (such as the S&P 500 Index or Dow Jones Industrial Average) during a set period of time (called the index term). Others measure how a specific financial market performs (such as the Nasdaq) during the term. The insurance company uses a formula to determine how a change in the index affects the amount of interest to add to your annuity at the end of each index term. Once interest is added to your annuity for an index term, those earnings usually are locked in and changes in the index in the next index term don’t affect them. If you take money from an indexed annuity before an index term ends, the annuity may not add all of the index-linked interest for that term to your account.

Insurance companies use different formulas to calculate the interest to add to your annuity. They look at changes in the index over a period of time. See the box “Fixed Deferred Indexed Formulas” that describes how changes in an index are used to calculate interest.

The formulas insurance companies use often mean that interest added to your annuity is based on only part of a change in an index over a set period of time. Participation rates, cap rates, and spread rates (sometimes called margin or asset fees) all are terms that describe ways the amount of interest added to your annuity may not reflect the full change in the index. But if the index goes down over that period, zero interest is added to your annuity. Then your annuity value won’t go down as long as you don’t withdraw the money.

When you buy an indexed annuity, you aren’t investing directly in the market or the index. Some indexed annuities offer you more than one index choice. Many indexed annuities also offer the choice to put part of your money in a fixed interest rate account, with a rate that won’t change for a set period.

Fixed Deferred Indexed Formulas

Annual Point-to-Point – Change in index calculated using two dates one year apart.

Multi-Year Point-to-Point – Change in index calculated using two dates more than one year apart.

Monthly or Daily Averaging – Change in index calculated using multiple dates (one day of every month for monthly averaging, every day the market is open for daily averaging). The average of these values is compared with the index value at the start of the index term.

Monthly Point-to-Point – Change in index calculated for each month during the index term. Each monthly change is limited to the “cap rate” for positive changes, but not when the change is negative. At the end of the index term, all monthly changes (positive and negative) are added. If the result is positive, interest is added to the annuity. If the result is negative or zero, no interest (0%) is added.

Buyer’s Guide for Deferred Annuities

© 2013 National Association of Insurance Commissioners 4

Fee

s, C

har

ges,

an

d A

dju

stm

ents

What Other Information Should You Consider?

Fees, Charges, and Adjustments

Fees and charges reduce the value of your annuity. They help cover the insurer’s costs to sell and manage the annuity and pay benefits. The insurer may subtract these costs directly from your annuity’s value. Most annuities have fees and charges but they can be different for different annuities. Read the contract and disclosure or prospectus carefully and ask the annuity salesperson to describe these costs.

A surrender or withdrawal charge is a charge if you take part or all of the money out of your annuity during a set period of time. The charge is a percentage of the amount you take out of the annuity. The percentage usually goes down each year until the surrender charge period ends. Look at the contract and the disclosure or prospectus for details about the charge. Also look for any waivers for events (such as a death) or the right to take out a small amount (usually up to 10%) each year without paying the charge. If you take all of your money out of an annuity, you’ve surrendered it and no longer have any right to future income payments.

Some annuities have a Market Value Adjustment (MVA). An MVA could increase or decrease your annuity’s account value, cash surrender value, and/or death benefit value if you withdraw money from your account. In general, if interest rates are lower when you withdraw money than they were when you bought the annuity, the MVA could increase the amount you could take from your annuity. If interest rates are higher than when you bought the annuity, the MVA could reduce the amount you could take from your annuity. Every MVA calculation is different. Check your contract and disclosure or prospectus for details.

How Annuities Make Payments

Annuitize

At some future time, you can choose to annuitize your annuity and start to receive guaranteed fixed income payments for life or a period of time you choose. After payments begin, you can’t take any other money out of the annuity. You also usually can’t change the amount of your payments. For more information, see “Payout Options” in this Buyer’s Guide. If you die before the payment period ends, your survivors may not receive any payments, depending on the payout option you choose.

Full Withdrawal

You can withdraw the cash surrender value of the annuity in a lump sum payment and end your annuity. You’ ll likely pay a charge to do this if it’s during the surrender charge period. If you withdraw your annuity’s cash surrender value, your annuity is cancelled. Once that happens, you can’t start or continue to receive regular income payments from the annuity.

How Insurers Determine

Indexed Interest

Participation Rate – Determines how much of the increase in the index is used to calculate index-linked interest. A participation rate usually is for a set period. The period can be from one year to the entire term. Some companies guarantee the rate can never be lower (higher) than a set minimum (maximum). Participation rates are often less than 100%, particularly when there’s no cap rate.

Cap Rate – Typically, the maximum rate of interest the annuity will earn during the index term. Some annuities guarantee that the cap rate will never be lower (higher) than a set minimum (maximum). Companies often use a cap rate, especially if the participation rate is 100%.

Spread Rate – A set percentage the insurer subtracts from any change in the index. Also called a “margin or asset fee.” Companies may use this instead of or in addition to a participation or cap rate.

Buyer’s Guide for Deferred Annuities

© 2013 National Association of Insurance Commissioners

Partial Withdrawal

You may be able to withdraw some of the money from the annuity’s cash surrender value without ending the annuity. Most annuities with surrender charges let you take out a certain amount (usually up to 10%) each year without paying surrender charges on that amount. Check your contract and disclosure or prospectus. Ask your annuity salesperson about other ways you can take money from the annuity without paying charges.

Living Benefits for Fixed Annuities

Some fixed annuities, especially fixed indexed annuities, offer a guaranteed living benefits rider, usually at an extra cost. A common type is called a guaranteed lifetime withdrawal benefit that guarantees to make income payments you can’t outlive. While you get payments, the money still in your annuity continues to earn interest. You can choose to stop and restart the payments or you might be able to take extra money from your annuity. Even if the payments reduce the annuity’s value to zero at some point, you’ll continue to get payments for the rest of your life. If you die while receiving payments, your survivors may get some or all of the money left in your annuity.

How Annuities Are Taxed

Ask a tax professional about your individual situation. The information below is general and should not be considered tax advice.

Current federal law gives annuities special tax treatment. Income tax on annuities is deferred. That means you aren’t taxed on any interest or investment returns while your money is in the annuity. This isn’t the same as tax-free. You’ll pay ordinary income tax when you take a withdrawal, receive an income stream, or receive each annuity payment. When you die, your survivors will typically owe income taxes on any death benefit they receive from an annuity.

There are other ways to save that offer tax advantages, including Individual Retirement Accounts (IRAs). You can buy an annuity to fund an IRA, but you also can fund your IRA other ways and get the same tax advantages. When you take a withdrawal or receive payments, you’ll pay ordinary income tax on all of the money you receive (not just the interest or the investment return). You also may have to pay a 10% tax penalty if you withdraw money before you’re age 59½.

5

How

An

nu

itie

s M

ake

Pay

men

ts

Annuity Fees and Charges

Contract fee percentage charged once or annually.

Percentage of purchase payment – A front-end sales load or other charge deducted from each premium paid. The percentage may vary over time.

Premium tax – A tax some states charge on annuities. The insurer may subtract the amount of the tax when you pay your premium, when you withdraw your contract value, when you start to receive income payments, or when it pays a death

Transaction fee – A charge for certain transactions, such as transfers or withdrawals.

Payout Options

You’ll have a choice about how to receive income payments. These choices usually include:

lifetime or your spouse’s lifetime

lifetime or a set time period

Buyer’s Guide for Deferred Annuities

© 2013 National Association of Insurance Commissioners 6

Fin

din

g th

e A

nn

uit

y fo

r Y

ou

Finding an Annuity That’s Right for You

An annuity salesperson who suggests an annuity must choose one that they think is right for you, based on information from you. They need complete information about your life and financial situation to make a suitable recommendation. Expect a salesperson to ask about your age; your financial situation (assets, debts, income, tax status, how you plan to pay for the annuity); your tolerance for risk; your financial objectives and experience; your family circumstances; and how you plan to use the annuity. If you aren’t comfortable with the annuity, ask your annuity salesperson to explain why they recommended it. Don’t buy an annuity you don’t understand or that doesn’t seem right for you. Within each annuity, the insurer may guarantee some values but not others. Some guarantees may be only for a year or less while others could be longer. Ask about risks and decide if you can accept them. For example, it’s possible you won’t get all of your money back or the return on your annuity may be lower than you expected. It’s also possible you won’t be able to withdraw money you need from your annuity without paying fees or the annuity payments may not be as much as you need to reach your goals. These risks vary with the type of annuity you buy. All product guarantees depend on the insurance company’s financial strength and claims-paying ability.

Questions You Should Ask

achieve that goal if the income from the annuity isn’t as much as I expected it to be?

appropriate for me?

such as 401(k)s, 403(b)s, and IRAs?

paying a surrender charge? Is there a limit on the total amount I can withdraw during the surrender charge period?

any surrender charges?

will affect my tax liability?

payment from my annuity if I die?

If you don’t know the answers or have other questions, ask your annuity salesperson for help.

Buyer’s Guide for Deferred Annuities

© 2013 National Association of Insurance Commissioners7

Wh

en Y

ou R

ecei

ve Y

our

Co

ntr

act

When You Receive Your Annuity Contract

When you receive your annuity contract, carefully review it. Be sure it matches your understanding. Also, read the disclosure or prospectus and other materials from the insurance company. Ask your annuity salesperson to explain anything you don’t understand. In many states, a law gives you a set number of days (usually 10 to 30 days) to change your mind about buying an annuity after you receive it. This often is called a free look or right to return period. Your contract and disclosure or prospectus should prominently state your free look period. If you decide during that time that you don’t want the annuity, you can contact the insurance company and return the contract. Depending on the state, you’ll either get back all of your money or your current account value.

ORD 208024 FIXED ed. (03/2014)