pt indoritel makmur internasional tbk -...

TRANSCRIPT

PT Indoritel Makmur InterCompany presentationCompany presentationSeptember 2013

For interna

rnasional Tbk

al use only

Disclaimer

This presentation and its contents may not be forwarded or distributed to any other person and mreproduction of this presentation in whole or in part is unauthorised and may result in a violation ofp p p ysecurities laws. This presentation is for information purposes only and for your reading only during thpresentation is not intended for potential investors and does not constitute or form part of an advertisemnor should it or any part of it form the basis of, or be relied in any connection with, any contract ordecision in securities in PT Indoritel Makmur Internasional Tbk (the "Company"). The information conta

No representation or warranty expressed or implied is made as to, and no reliance should be placed opresentation. None of the Company, Deutsche Bank AG, Hong Kong Branch, PT Buana Capital, Cradvisers or representatives shall have any liability whatsoever (in negligence or otherwise) for anyadvisers or representatives shall have any liability whatsoever (in negligence or otherwise) for anypresentation or its contents or otherwise arising in connection with this presentation.

The third party information and statistical data in this presentation have been obtained from sources thof the included information. This presentation does not contain all material information concerning thinformation in this document is presented as of 30 June 2013; its accuracy is not guaranteed; and itBuana Capital, Credit Suisse (Singapore) Limited or PT CIMB Securities Indonesia is under any obliga

Neither this presentation nor any copy or portion of it may be sent or taken, transmitted or distributedpublic offer for the sale of securities of the Company in the Republic of Indonesia or an offer for sale ofmay not be publicly offered in the Republic of Indonesia absent of a registration statement under theoffered or sold in the United States absent registration or an exemption from registration under the UnRepublic of Indonesia and the United States would be made by means of a prospectus that could binformation about the Company and its management, as well as financial statements. The Company dosecurities in the Republic of Indonesia and the United States.

This presentation may contain forward-looking statements that involve risks, uncertainties and other fincluding words such as “target,” “believe,” “expect,” “aim,” “intend,” “may,” “anticipate,” “estimate,” “plmeaning or the negative thereof.

Actual results, performance or achievements of the Company may be materially different from any fuSuch forward-looking statements are based on numerous assumptions regarding the Company's preseand must be read together with such assumptions. Predictions, projections or forecasts of the economand must be read together with such assumptions. Predictions, projections or forecasts of the economthe Company. Past performance is not necessarily indicative of future performance. The future financthese forward-looking statements.

This presentation also contains certain statistical data (the “Statistical Information”) which have beengiven as to the Statistical Information’s accuracy, appropriateness or completeness in any particular coreflect present market conditions or future market performance.

For interna

may not be copied or reproduced in any manner whatsoever. Any forwarding, distribution, copying orf applicable laws. Any failure to comply with these restrictions may constitute a violation of applicablepp y p y y pphe presentation and will be taken back by the Company (as defined below) after the presentation. Thisment, recommendation, offer, solicitation or invitation of any offer, to buy or subscribe for any securities,r commitment whatsoever. This presentation should not be relied upon as the basis of an investmentained in this presentation has not been independently verified.

on, the fairness, accuracy, completeness or correctness of the information or opinions contained in thisredit Suisse (Singapore) Limited or PT CIMB Securities Indonesia or any of their respective affiliates,y loss howsoever arising whether directly or indirectly from any use reliance or distribution of thisy loss howsoever arising, whether directly or indirectly, from any use, reliance or distribution of this

he Company believes to be reliable but there can be no assurance as to the accuracy or completenesshe Company and the information set forth in these materials is subject to change without notice. Themay be incomplete or condensed. None of the Company, Deutsche Bank AG, Hong Kong Branch, PTtion to update or keep current the information contained herein.

d, directly or indirectly, into Indonesia, Japan, Canada or the United States. This presentation is not af the securities of the Company in the United States or any other jurisdiction. Securities of the CompanyLaw Number 8 of 1995 on Capital Markets and prevailing capital markets regulations, as amended, or

nited States Securities Act of 1933, as amended. Any public offering of securities of the Company in thee obtained from the Company or the selling shareholder, as relevant, and that would contain detailedoes not intend to register any offering of securities in the United States or to conduct a public offering of

factors. These statements may include, without limitation, any statements preceded by, followed by oran,” “project,” “will,” “can have,” “likely,” “should,” “would,” “could” and other words and terms of similar

uture results, performance or achievements expressed or implied by such forward-looking statements.ent and future business strategies and the environment in which the Company will operate in the future,

my or economic trends of the markets are not necessarily indicative of the future or likely performance ofmy or economic trends of the markets are not necessarily indicative of the future or likely performance ofcial performance of the Company is not guaranteed. You are cautioned not to place undue reliance on

n prepared in reliance upon information from other third party sources. As such, no assurance can beontext, nor as to whether the Statistical Information and/or the assumptions upon which they are based

al use only

S ti 1Indoritel at a GlanceSection 1

Indoritel at a glanceg

M b d dMi i k t

One of Indonesia’s l

40 0% Mass-bread produMinimarket

1

40.0% stake

Largest m92.0% marke

Market cap: R

N b f i

Largest minimarket chain operator32.4% market share(a)

Number of stores: 8,039(c)

FY12 PATMI R 547b / US$56

1

1

Number of poi

FY12 PATMI:

FY12 PATMI: Rp547bn / US$56m

Market leadership across key consumer segmen

For interna

Note: Exchange rate as at 31 Dec 2012 for PATMI and as at 4 Sep 2013 for market cap(a) Based on the number of minimarket stores as of Dec 2012(b) Based on 2012 retail sales(c) Operating data as of Jun 2013Source: Bloomberg, FactSet as at 30 Jun 2013 and 4 Sep 2013

Q i k i t t

leading consumer groups

31.5% 35.8%ucer Quick service restaurant31.5% stake

35.8%stake

mass-bread produceret share(b)

Rp6.2trn / US$558.1m

t f l 45 895(c)

Largest QSR chain28.8% market share(b)

Market cap: Rp3.8trn / US$351.6m

N b f t t 446(c)

1

nts of sale: 45,895(c)

Rp149bn / US$15m

Number of restaurants: 446(c)

FY12 PATMI: Rp206bn / US$21m

ts of Indonesia supported by iconic household brands

al use only

1

Indoritel intends to actively support thedevelopment of our Associate Companp p

Board of CommissionersBoard of Commissioners

Benny Setiawan Santoso President Commissioner

Ferry Noviar Yosaputra(a) Commissioner

Soedarsono Commissioner

Budi Santosa Heryanto Commissioner

Bambang Subianto Independent Commissioner

Adi Pranono Leman Independent Commissioner

40.0% 31.5%

Common Commissioner

(2nd largest shareholder)

Board of CommissionersDjisman Simanjuntak President Commissioner

Soenardi Winato Commissioner

Board of Com

Benny Setiawan Santoso

Tan Huang HuatSoenardi Winato Commissioner

Soedarsono Commissioner

Tan Huang Huat

Seah Kheng Hong Conrad

PT Indomarco Perdana (55.6%) Bonlight Investments (26.5%

PT Lentera Bumi Mas (3.1%) Shikishima Baking (8.5%)

Sinarman Jonatan (1.3%) Sojitz Corporation (4.25%)

For interna

Public (29.25%)

(a) Ferry Noviar Yosaputra is also Vice President Director of FAST(b) Haliman Kustejo is also Director of Indomaret

e continued growth and ies

Board of Directors

Indoritel board representation in all A i t C iBoard of Directors

Alex Wreksoremboko President Director andNon-Affiliated Director

Evensius Go Director

Haliman Kustedjo(b) Director

Associate Companies

One of top 2 shareholders in each Associate Company

Associate Companies to share market insights

35.8%

share market insights through common Indoritel commissioners

(Largest shareholder) (2nd largest shareholder)

Director of Associate Companies

mmissioners

President Commissioner

Commissioner

Board of Commissioners

Anthony Salim President Commissioner

Eli b th G l l Vi P id t C i iCommissioner

Independent Commissioner

Elizabeth Gelael Vice President Commissioner

Rudy Tanudjaja Saputra Commissioner

Benny Setiawan Santoso Commissioner

Ken Leksono Independent Commissioner

P.L. Gunawan Solaiman Independent Commissioner

PT Gelael Pratama (43.9%)%)

Public (20.3%)

al use only

2

S ti 2Investment highlights and growth strategySection 2

Key investment highlights

Attractive exposure to large and

y g g

Attractive exposure to large and in Indonesia1

Dominant market leaders2

Extensive nationwide s3

Large-scale operation an4

Proven business models that r5

For interna

growing middle-income class and underpenetrated marketsgrowing middle income class and underpenetrated markets

hip positions complemented by iconic brands

store network supported by efficient distribution platform

d market leadership positions drive operational synergies

reinforce market positions and drive future growth

al use only

3

Attractive exposure to large and grocompelling consumption trends1 p g p

Attractive Indonesia macro story…

4th most populated in the world c. 247 million people as of 2012

VAST

GROWING

18.9

25.46.9%

Real GDP CAGR Disposable income per capita

13.3

2008 2012 2015E

5.8%

2008 – 12 2012 – 15E

Rp

(m)

RISING CONSUMER EXPENDITURE

3 107 3,484 3,905 4,369

R tr

illion

939 1,018 1,138 1,276 1,403 1,561 1,739 1,930 2,079 2,285 2,518 2,793 3,107 ,

2008 2009 2010 2011 2012 2013F 2014F 2015F

IDR

Expenditure on food items Expenditure on non-food items

For interna

(a) Based on expenditure per capita per monthSource: Frost & Sullivan

owing middle-income class driving

…supporting favourable industry outlook

MinimarketR 73 0 t

CAGR

26.0%2008 – 12

Rp 73.0 trnmarket size

(2012) 13.5%2012 – 15E

BreadRp 10.6 trnmarket size

(2012)

10.0%

8 7%

2008 – 12

2012 15E

QSR

8.7%2012 – 15E

11.4%2008 – 12QSR

Rp 15.1 trnmarket size

(2012)9.9%2012 – 15E

al use only

4

Significantly underpenetrated marke1 g y p

Minimarkets Bread

60

102

Indonesia

Philippines

2012E modern retail sales per capita (US$) 2012E bread sales

Strong growth potential

Stron

4

5

Philipines

Indonesia102

206

325

781

Philippines

Malaysia

Thailand

Singapore

Stron5

6

8

Indonesia

Thailand

Malaysia

Hong Kong

844Hong Kong

% of total modern retail sales % of total b% of retail value

Singapore

47% 50% 51% 53% 54% 55% 56%

59% 53% 51% 49% 47% 46% 45% 44%

92% 92% 91% 8

41% 47% 50% 51% 53% 54% 55%

2008 2009 2010 2011 2012 2013E 2014E 2015E

Minimarkets Supermarket / Hypermarket

Minimarket is the winning modern retail format Rising popularity o

8% 8% 9% 1

2009 2010 2011 2

Mass-produced

For interna

Minimarket is the winning modern retail format g p p ypackaged bread

Source: Frost & Sullivan

ets with strong growth potentialg g p

QSR

s per capita (US$) 2012E QSR sales per capita (US$)

g growth potential

Strong growth potential 7

27

Indonesia

Philippinesg growth potential

29

27

38

49

169

Philippines

Thailand

Malaysia

Singapore

bread sales % of total QSR sales

22% 21% 20% 19% 18% 17% 16% 16%

34 319 Hong Kong

78% 79% 80% 81% 82% 83% 84% 84%

22% 21% 20% 19% 18% 17% 16% 16%

88% 87% 85% 84%

of mass-produced Chained QSR continues to dominate with

2008 2009 2010 2011 2012 2013E 2014E 2015E

Chained Independent

12% 13% 15% 16%

2012 2013E 2014E 2015E

Home / Boutique

al use only

5

p better brand exposure

Dominant market leadership positio2 p p

1 1

32.4% 31.6%Market share by 2012 number of stores Market share by 2012 sa

92.0%

3.1%1.4%

Alfamart Alfamidi Circle K

Iconic brands with unique and distinctive value propositions reinforce our ma

Good value merchandise at easily accessible locations

High quality and ioffering with distin

various

For interna

Source: Frost & Sullivan

ons complemented by iconic brandsp y

1

ales (mass-production) Market share by 2012 number of stores12.1% KFC has 28.8%

market shared based

8.0%

6.6%5.9% 5.6%

on retail value

arket-leading positions

Others California Fried Chicken

Baskin Robbins

Pizza hut

innovative product nctive packaging of s brands

Innovative menu offerings catering to Indonesian taste

al use only

6

Extensive nationwide store network distribution platform

3p

1,239 stores

Sumatra

23 stores

Kalimantan

,

4,703 POS

84 outlets

26 outlets

2,985 stores

27,389 POS

155 outlets

Greater Jakarta

155 outlets

Our nationwide presence supported by efficient distribution infrastructure pro

18 Indomaret DCs 24 ROTI Note: As at 30 Jun 2013

Better access and service our customers

Identify key trends that may affect our operations and business model

Our nationwide presence supported by efficient distribution infrastructure pro

For interna

supported by efficient

243 stores

Sulawesi

10 outlets

East Indonesia

904 POS

32 outlets

3,549 stores

12,899 POS

Java

ovides a platform to ...

139 outlets

production lines 25 KFC warehouses

Identify new market opportunities in Indonesia in a timely and cost-efficient manner

Supply merchandise and raw materials nationwide with short lead times and cost-effective manner

ovides a platform to ...

al use only

and cost effective manner

7

Large-scale operations and market leadesynergies

4

1 1

Operationa

Market leade

Increased bargaining power

Favorable prices from suppliers through bulk purchases

Stronger access to new retail locations and distribution channels

Talent recruitment for key executive positions

Supplier management Merchandising / raw material procurement

Supply chain management system is scal

For interna

pp y g y

ership positions drive operational

1

al scale

ership

Economies of scale

Maintain per unit fixed costs low and competitive

Maximise efficiency of operations

Sustainability of strong profit margins

Warehousing / distribution centres Retail network

lable to support future growth and expansion

al use only

8

pp g p

Proven business models that reinforgrowth

5g

Standardised minimarket store format → limits fit-out time and capex → faster speed to market

Successful franchising model → faster and li ht i f t

Solid brand equity → and barriers to entry

Strong access to rapii i k t h i

capex-light expansion of new stores

Advanced merchandise data system and distribution infrastructure → just-in-time delivery and optimal stock level

minimarket chains →

State-of-the-art autom→ cost efficiency to

Indomaret stores Sari Roti pro

Proven business models supported by strong track record of execution posit

4,955

6,003

7,245 8,039

2,146

2,554 2,837

11

17

3,058 3,857

4,691 5,202

1,897

2010 2011 2012 1H 2013

11

2010 2011

For interna

Owned Franchised

(a) Cleanliness, Hospitality, Accuracy, Maintenance, Products and Speed

rce market positions and drive future

strong pricing power

dly expanding hi h t ti

Strategic support from YUM! → product R&D and operational excellence

Standardised CHAMPS(a) implementation lid ti i t i

higher penetration

mated production linesdrive expansion

→ solid execution in new store openings

Constant innovation of product and menu offerings → reinforce dominance in QSR

duction lines KFC outlets

tions us for future profitable growth

24 24

398421 441 446

2012 1H 2013 2010 2011 2012 1H 2013

al use only

9

Three-prong growth strategy to further leading consumer company in Indonesg p y

Enhance brand equity and market leading positions Enhance brand equity and market leading positions 1

Support the continued growth and development of Associate Companies

1) Continuous and rapid expansion across Indonesia

2) Further increasing customer demand and sales productivity

3) Continued focus on operational and distribution efficiency

A

B

C

Continue to improve profitability and return on capitalContinue to improve profitability and return on capital

3) Continued focus on operational and distribution efficiencyC

2

Leverage on scale, market-leading positions and pan-Indonesian presence of Associate Companies

Increase productivity of Associate Companies to improve profit margins and capital efficiency

Opportunistically consider and evaluate expansion into new business

Evaluate new and complementary business opportunitiesEvaluate new and complementary business opportunities3

pp y psegments

Complementary to existing business and leverage on competencies residing within the Group

For interna

cement our position as the ia

Indoritel will offer an attractive exposure to fast-growing consumer

i i I d icompanies in Indonesia

Focus on delivering profitability, sustainable growth and return to shareholders

al use only

10

S ti 3Overview of Associate CompaniesSection 3

Indomaret is the largest minimarket chag

Key highlights

Extensive nationwide store footprint with established di t ib ti l tf

Largest minimarket chain operator with 32.4%

k t h (a)

1 2

Unrivalled supply chain management for deeper store penetration

Effective and attractive franchise business model

distribution platformmarket share(a)

3 4

Minimarkets Convenience stores

No of stores: 7,953 No of stores: 86

Store selling area (sqm): 60 – 200

Product mix: food and non-food merchandise, groceries, fresh produce

Store selling area (sqm): 160 – 350

Product mix: groceries, ready-to-eat, ready-to-drink

For interna

(a) Frost & Sullivan

ain operator in Indonesiap

Product mix focus on young patrons and family consumption

2012 sales mixBeverages

13%

Tobacco10%

Other37%

Food

d

Baby food9%

Snacks8%

Margerine and cooking oilBody care

4%MilkPhone vouchers

Detergent4%

Baby and child care3%

Non

-foo

resh

du

ce

Large selection of c.4,000 merchandise items at affordable prices

Tailored to each store’s local target market at appropriate price points

4%4%Milk4%

Phone vouchers4% Fr pr

o

IT-driven integrated distribution system

18 DCs with total capacity of 94,313m3

Each DC supports 500-600 Indomaret stores

100-110 trucks per DC

Efficient digital picking system

Daily tracking of inventory levels per store and automated order requests

al use only

11

automated order requests

Indomaret has clear growth strategies tg g

Continuous and rapid store expansion across IndonesiaContinuous and rapid store expansion across Indonesia1

Target 3 – 5 new store openings daily

Expect to open up to 1,600 new stores for 2013 and up to 1,300 – 1,400 new stores p.a. for 2014 and 2015

Focus on store expansion outside Greater Jakarta with greater growthFocus on store expansion outside Greater Jakarta with greater growth potential and under-served areas

New stores typically cash flow positive in 1st year with 3 – 4 years payback period

New store expansion focus on outside Greater Jakarta

36.0% 47.0%2010 26.6%

35.9%

2012 28.3%

34.5%

2013E

16.9% 37.4% 37.2%

1,152New stores

1,366New stores

1,600New stores

Greater Jakarta Java Outside Java(a)

For interna

(a) Excludes Greater Jakarta

Greater Jakarta Java Outside Java

to strengthen its market leadershipg p

Drive customer traffic and sales productivityDrive customer traffic and sales productivity2

Targeted marketing campaigns

Develop suite of innovative value-added services

– Indomaret card, Indomaret ATM, jakcard, t-cash, Indomaret Order Delivery Collect (PAAI)

Continuously tailor and optimise merchandise mix at individual store level

Increase sales of private label brands (currently >300 SKUs)

– Key products include facial tissue, mineral water and sugar

– Higher margins than regular merchandise

Increasing sales productivityIncreasing private label sales

3.3%

3.7%4.0%

4.3%

% to

tal s

ales

9.0 9.711.7 11.0

Rpm

/day

/sto

re

2010 2011 2012 1H 2013 2010 2011 2012 1H 2013

al use only

12

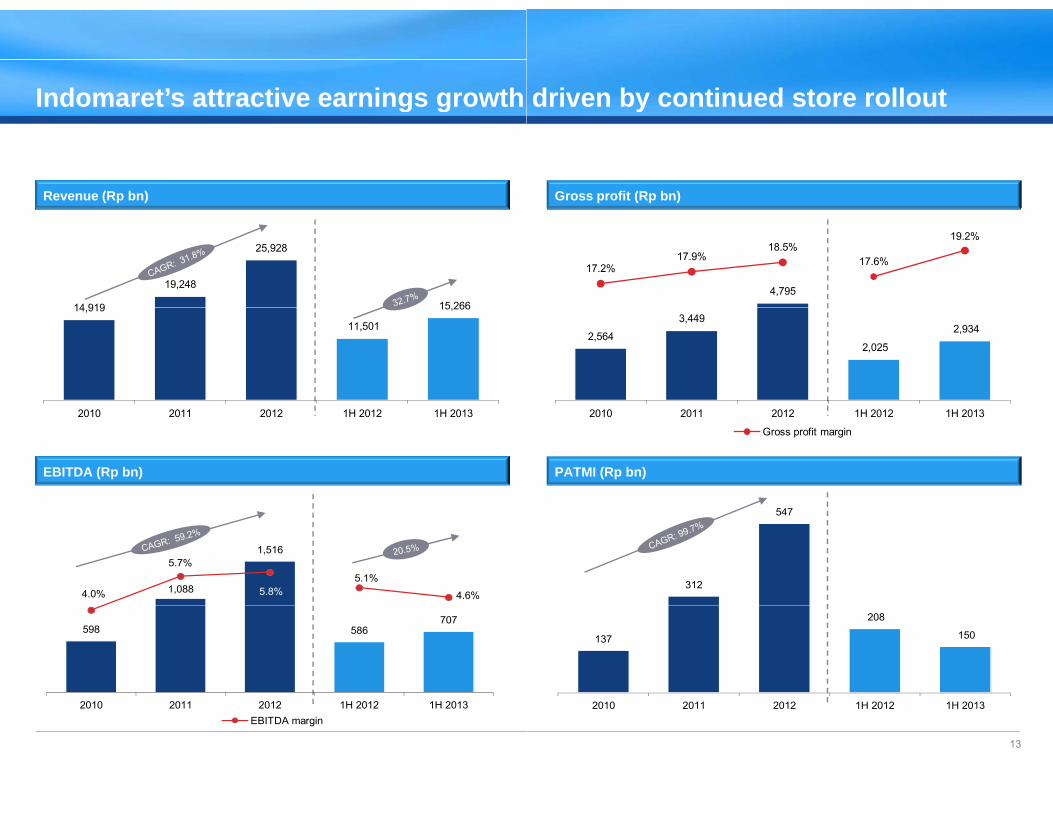

Indomaret’s attractive earnings growth g g

Revenue (Rp bn)

14 919

19,248

25,928

15 26614,919

11,501

15,266

EBITDA (Rp bn)

2010 2011 2012 1H 2012 1H 2013

1,088

1,516

4.0%

5.7%

5.8%5.1%

4.6%

598 586707

2010 2011 2012 1H 2012 1H 2013

For interna

2010 2011 2012 1H 2012 1H 2013EBITDA margin

driven by continued store rollouty

Gross profit (Rp bn)

4,795

17.2% 17.9%

18.5% 17.6%

19.2%

2,564

3,449

2,025

2,934

PATMI (Rp bn)

2010 2011 2012 1H 2012 1H 2013

Gross profit margin

312

547

137

208

150

2010 2011 2012 1H 2012 1H 2013

al use only

13

2010 2011 2012 1H 2012 1H 2013

Indomaret has a robust capital structurp

Total debt and cash (Rp bn)

1,996

2,995 2,558 2,706

Rp2.6trn equity injection

1,563

474 607

1,163

2010 2011 2012 1H 2013

Total debt / EBITDA

Total debt Cash

2.6x

1.8x 2.0x

1.6x

2010 2011 2012 LTM 1H 2013

For interna

re to support future expansionpp p

Total debt / equity

1.3x 1.3x1.5x

1.1x

2010 2011 2012 LTM 1H 2013

Capital expenditure (Rp bn)

342

253

381

255

158

2010 2011 2012 1H 2012 1H 2013

al use only

14

Benchmarking of Indomaret and Alfama

M k h (a) 32 4%

g

Market share(a) 32.4%

38.3% 35.7% 35.% franchise

7 2

Store expansion 4,9556,003

7,2

2010 2011 20

Geographical split of stores Greater Jakarta (37%); Outside Greater Jaka

Distribution centers(b) 18 DCs with capacity of 94,313m3

2012 daily sales productivity Rp11 7mper store Rp11.7m

Revenue CAGR (FY10-12) 37.2%

FY12 Gross profit margin 18.5%

FY12 EBITDA margin 5 8%FY12 EBITDA margin 5.8%

FY12 PATMI (Rp bn) 547

PATMI CAGR (FY10-12) 99.7%

For interna

(a) Based on number of stores as at Dec 2012(b) Based on latest information available; Indomaret as at 30 Jun 2013, Alfamart as at 31 Dec 201Source: Company announcements, Frost & Sullivan

art

31 6%31.6%

7 063

.3% 26.7% 28.9% 29.1%

245

% franchise

4,8125,797

7,063

2010 2011 2012

245

012

arta (63%) Greater Jakarta (57%); Outside Greater Jakarta (43%)

21 DCs with capacity of 102,000m3

Rp9 9mRp9.9m

28.9%

15.4%

5 1%5.1%

481

37.1%

al use only

1512

ROTI is the most dominant mass-bread

Key highlights

Dominant market leader in mass-bread market with 92%

1Nationwide distribution network

2

mass-bread market with 92% market share(a)

Advanced technology and bread-making process with

3

with high penetration

Innovative and well-executed sales and marketing strategy

4

world-class production facilities sales and marketing strategy

Distribution channel mix (% FY12 sales)

14,563 minimarkets

667 supermarkets / hypermarkets30%

1%

Dec2012

667 supermarkets / hypermarkets

19,639 grocery shops

3,070 tricycles

56 institutions (e.g. restaurants)69%

%

For interna

(a) Frost & Sullivan(b) % of FY12 sales

Modern Traditional Others

d producer in Indonesiap

Wide range of >40 products across 3 categories

White bread(35%) (b)

Sweet bread(64%) (b)

Cake and sandwich

(1%) (b)

Sari Roti is the main brand, launched in 1996, targeted towards middle-upper income consumer segment

State-of-the-art factories and production lines

8 factories with 24 production lines and capacity of 3.4m pieces of bread per day as of 30 June 2013

Advanced and highly-automated breadAdvanced and highly automated bread making process ensures maximum product quality and freshness

Technical support from Shikishima Baking Company

Efficient distribution network critical given

al use only

16

bread’s short shelf life of 3-5 days

ROTI has clear growth strategies to streg g

Penetrate into underPenetrate into under--served regions of Indonesiaserved regions of Indonesia1

Plans to open 3 new factories in Java and Kalimantan (currently no factory present) and 6 additional production lines by end 2013

– Increase capacity to 4.3m pieces of bread per day by end of 2013

Targets to build 5 10 new production lines each year to supportTargets to build 5 – 10 new production lines each year to support expansion outside Java

Further growth through minimarkets as ROTI only covered 46% of all minimarkets as of end 2012

Expansion of factories outside Java

Location 2010 2011 2012

Greater Jakarta 2 3 3

Java 1 2 2

Sumatra – 1 2

Sulawesi – – 1

Total 3 6 8

For interna

Outside Java

engthen its market leadershipg p

Enhance product offering to strengthen customer loyaltyEnhance product offering to strengthen customer loyalty2

Strong brand name provides unique leverage to effectively roll out new product launches in the Indonesian bread market

Continual research and development to produce new and innovative bread products in line with industry trends

– Evaluate 6 – 10 new products each year

Development of healthy products that contain dietary fiber, high calcium, DHA, Omega 3 fatty acids and other health beneficial elements

Constant rollout of new innovative products

2013Sandwich Blueberry Double soft white bread

2013

2012

Sobek Coklat Blueberry

Sandwich Krim Keju Double sandwich

Tawar Kurma Tawar Keju

Roti Isi Mix Fruit Tawar 6 slice

2010

2011

Chiffon Coklat dan Pandan

Sobek Coklat Blueberry Roti Isi Chicken Teriyaki Roti Isi Beef Barbeque Chiffon Strawberry, Mei

Sandwich Coklat Sandwich Kacang

Roti Tawar Pandan

al use only

17

2010Sobek Coklat Nanas

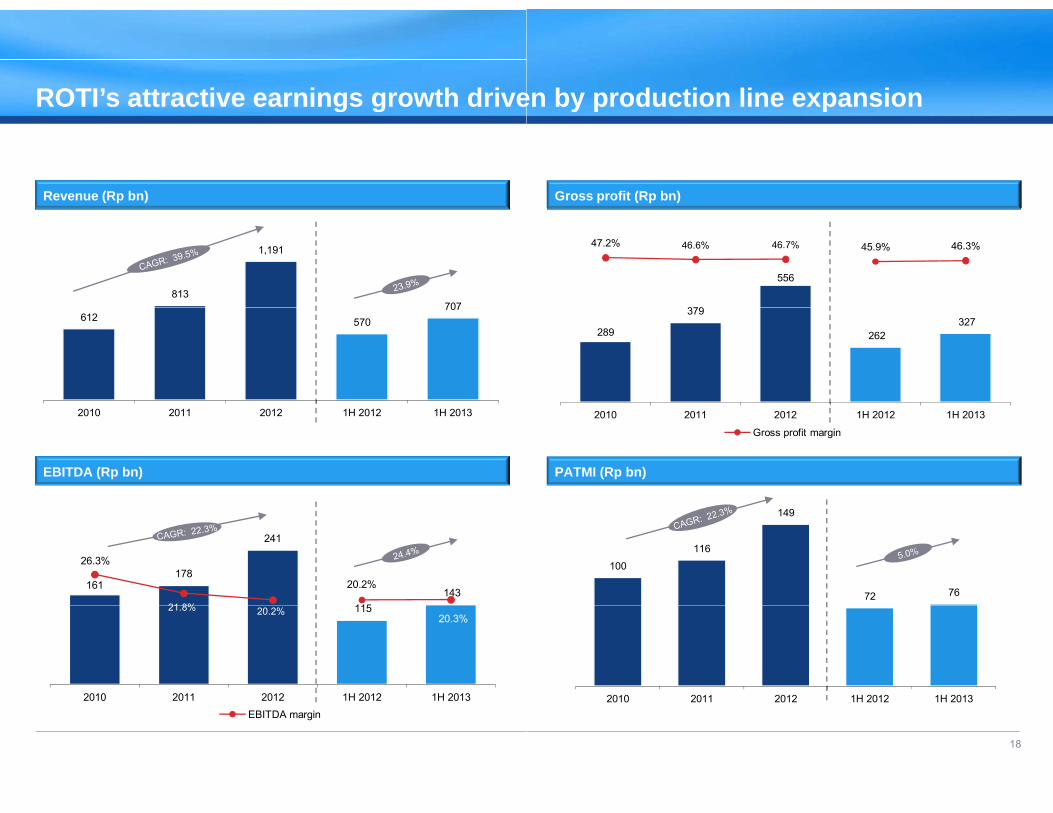

ROTI’s attractive earnings growth driveg g

Revenue (Rp bn)

813

1,191

707612 570

707

EBITDA (Rp bn)

2010 2011 2012 1H 2012 1H 2013

161 178

241

115143

26.3%

21 8%

20.2%

115 21.8% 20.2% 20.3%

2010 2011 2012 1H 2012 1H 2013

For interna

EBITDA margin

en by production line expansiony p p

Gross profit (Rp bn)

379

556

47.2% 46.6% 46.7% 45.9% 46.3%

289

379

262 327

PATMI (Rp bn)

2010 2011 2012 1H 2012 1H 2013

Gross profit margin

100

116

149

72 76

2010 2011 2012 1H 2012 1H 2013

al use only

18

ROTI has a robust capital structure to sp

Total debt and cash (Rp bn)

Higher debt to fund expansion of new factories

and production lines937

493

0 33

303

12148 38

493

2010 2011 2012 1H 2013

Total debt / EBITDA

Total debt Cash

3.5x

0.0x0.2x

1.3x

For interna

2010 2011 2012 LTM 1H 2013

support future expansionpp p

Total debt / equity

1.3x

0.0x 0.1x

0.5x

2010 2011 2012 LTM 1H 2013

Capital expenditure (Rp bn)

224

389

212

163 164

al use only

19

2010 2011 2012 1H 2012 1H 2013

FAST is the leading QSR chain and sole

Key highlights

g

Largest QSR chain in Indonesia with 28.8% Extensive nationwide store

t k ith 446 tl t

1 2

market share(a)

Unrivalled distribution platform to support future expansion

network with 446 outlets

Sole KFC franchise with strategic support from YUM!

3 4

Internationally reputable and highly recognized KFC brand

Dominant market share of 85.2% in chicken-based QSR

>50% customers’ share of QSR visits according to BITS(b)

Consistently won franchise awards from YUM!

Highest CMS(c) score of 99.2 in 2012 - highest score for KFC franchisees in Asia Pacific

For interna

(a) Frost & Sullivan(b) Defined as Brand Image Tracking Study(c) Defined as CHAMPS Management System

e KFC franchise in Indonesia

Focus on innovative product and menu offerings

Consistently ranked for the best tasting fried chicken

Catering to Indonesian taste and preference

“Value for money” packaged menu combinations (e.g. Super Besar,

Value for money packaged menu combinations (e.g. Super Besar, Goceng, Praktis, Kids Meal, Krushers)

Strategic benefits from YUM! franchise relationship

Access to innovativeAccess to innovative products developed by

YUM! R&D

Access to YUM! global procurement capabilities

Participation in KFC advertising and marketing

promotions

Regular audit by YUM! to achieve best-in-class

customer services and operations

al use only

20

p operations

FAST has clear growth strategies to strg g

Disciplined rollout of new restaurantsDisciplined rollout of new restaurants1

Plans to open 34 new KFC restaurants by end 2013, of which 11 – 12 restaurants are free standing format

Target to open 50% of new KFC restaurants in Java and 50% outside Java

Continue to renovate/refurbish existing restaurants to maintain contemporary design and feel, increase seat capacity and service speed

Focus on free-standing restaurant format

40% 36%

16%8%

Jun2013

446 outlets

33% 52%

8%7%

Dec 2010

398 outlets

Cheaper than restaurant opening in shopping malls

More flexible hours of operation

446 outlets398 outlets

Mall In-line Airport Free standing Foodcourt

For interna

More latitude in adding additional facilities (e.g. KFC coffee counter)

rengthen its market leadershipg p

Strengthen KFC brand image and grow sales productivityStrengthen KFC brand image and grow sales productivity2

Optimise dining experience and focus on consistent quality products

Focus on exceptional customer-focused services

Continue to offer new products and limited time promotions to maintain and improve SSSG %and improve SSSG %

Work closely with YUM! for R&D to launch new tailored product offerings that cater to local tastes and preferences

Maintaining strong SSSG% over the past years

8.6%8.0% 7.9%

(%)

2010 2011 2012

al use only

21

FAST’s attractive earnings growth driveg g

Revenue (Rp bn)

2,827 3,184

3,559

1,668 1,849

EBITDA (Rp bn)

2010 2011 2012 1H 2012 1H 2013

315

384 387

11 1%12.1%

10 9%9.4%

157 131

11.1% 10.9%7.1%

2010 2011 2012 1H 2012 1H 2013

For interna

2010 2011 2012 1H 2012 1H 2013

EBITDA margin

en by continued outlet rollouty

Gross profit (Rp bn)

1,657 1,877

2,083

58.6% 58.9% 58.5%

58.8% 59.7%

981 1,104

PATMI (Rp bn)

2010 2011 2012 1H 2012 1H 2013

Gross profit margin

200

229206

78

49

2010 2011 2012 1H 2012 1H 2013

al use only

22

2010 2011 2012 1H 2012 1H 2013

FAST has a robust capital structure to sp

Total debt and cash (Rp bn)

374

559 568 569

Dividend recapitalisation funded by Rp200bn

bond issuance

5

203 209 201

2010 2011 2012 1H 2013

Total debt / EBITDA

Total debt Cash

0.5x 0.5x

0.6x

0.0x

For interna

2010 2011 2012 LTM 1H 2013

support future expansionpp p

Total debt / equity

0.2x 0.2x 0.2x

0.0x

2010 2011 2012 LTM 1H 2013

Capital expenditure (Rp bn)

376

252

292

193

108

al use only

23

2010 2011 2012 1H 2012 1H 2013

Key investment highlights

Attractive exposure to large and

y g g

Attractive exposure to large and in Indonesia1

Dominant market leaders2

Extensive nationwide s3

Large-scale operation an4

Proven business models that r5

For interna

growing middle-income class and underpenetrated marketsgrowing middle income class and underpenetrated markets

hip positions complemented by iconic brands

store network supported by efficient distribution platform

d market leadership positions drive operational synergies

reinforce market positions and drive future growth

al use only

24

A di IAdditional materialsAppendix I

Experienced and dedicated managemep g

Alex WreksorembokoPresident Director and Non-Affiliated Director

Evensius Go

Sinarman JonatanPresident Director

Hendarto JosojuwunoEvensius GoDirector

Hendarto JosojuwunoFinance Director

Laurensius Tirta WidjajaMerchandise Director

Haliman KustedjoDirector

Haliman KustedjoPolicy System Director

Darmawie AlieDarmawie AlieBusiness Development Director

Stephanus KrisgiantoroOperational Director

Wiwiek YusufMarketing Director

For interna

Demonstrated ability to grow business, develop brand recognit

nt teams with strong track records g

Wendy Sui Cheng YapPresident Director

Indrayana

Dick GelaelPresident Director

Ferry Noviar YosaputraIndrayanaDirector of Compliance

Kaneyoshi MoritaDirector of Product and Technology Development

Ferry Noviar YosaputraVice President Director

Ricardo GelaelOperational Director

Takao OkabeDirector of Procurement

Yenni Husodo

Leonny EliminHR Director

Justinus Dalimin JuwonoYenni HusodoDirector of Finance

Alex ChinNon-affiliated Director

Justinus Dalimin JuwonoFinance Director

Adhi IndrawanBusiness Development Di tDirector Director

Erundine Ros RafalesNon-Affiliated Director

al use only

tion and drive economics of scale from our market leading businesses

25

FAST showcase

Free standing Drive thru

Coffee counter Marketing promotions

For interna

Renovation of existing restaurants

After

Before

al use only

26

ROTI showcase

Product offering

For interna

Production facilities

al use only

27

Indomaret showcase

Store layout

Indomaret cardIndomaret card

For interna

Promotions

Private label offeringsPrivate label offerings

al use only

28