ptl case (a).doc

TRANSCRIPT

PTL CASE (A)

DIVESTMENT AT PUNJAB TRACTORS

10:30 a.m. 25th July 2003, the deadline for submitting the final bid for the divestment of Punjab State Industrial Development Corporation (PSIDC)’s entire 23.49% stake in Punjab Tractors Limited (PTL). The entire top brass of the Punjab government’s divestment team is waiting in anticipation. Six months ago, 11 suitors- including the Who’s who of India’s tractor industry and three foreign private equity investors – expressed interest in buying out PTL. But on the D-day, just two representatives walked into the committee room. One from London based private equity firm CDC Group Plc and second from India’s largest tractor manufacturer Mahindra & Mahindra (M&M).

4:00 p.m. 25th July 2003, the bid opening ceremony for the divestment of PSIDC’s entire 23.49% stake in PTL. PTL’s profile as Punjab’s biggest divestment project even prompted chief minister Captain Amarinder Singh to fly in especially from Delhi to take part in the bid opening ceremony. The outcome was a big disappointment for all. As it turned out, the M&M’s bid contained three sealed envelopes titled: ‘commercial bid’, ‘financial bid’ and ‘technical bid’. But inside these envelopes were letters withdrawing M&M’s entry. That left CDC as the sole bidder in the race with a bid of Rs. 218.39 crore (at Rs. 153 per share whereas BSE closing price on 25 th July 2003 for PTL was Rs. 158.4). Soon after, Punjab’s Core Committee on Disinvestment chaired by Captain Amarinder Singh accepted CDC’s Rs. 218.39 crore bid raising a catalogue of questions.

ECONOMY OF INDIA

Indian economic policy after independence (1947) was influenced by the colonial experience which was seen by Indian leaders as exploitative in nature. Policy tended towards protectionism, with a strong emphasis on import substitution, industrialization, state intervention in labor and financial markets, a large public sector, business regulation, and central planning.

In the late 80s, the government led by Rajiv Gandhi eased restrictions on capacity expansion for incumbents, removed price controls and reduced corporate taxes. While this increased the rate of growth, it also led to high fiscal deficits and a worsening current account. The collapse of the Soviet Union, which was India's major trading partner, and the first Gulf War, which caused a spike in oil prices, caused a major balance-of-payments crisis for India, which found itself facing the prospect of defaulting on its loans. India asked for a $1.8 billion bailout loan from IMF, which in return demanded reforms.

In response, the Indian Government initiated the economic liberalisation of 1991. The reforms did away with the Licence Raj (investment, industrial and import licensing). The new policies included opening for international trade and investment, deregulation, initiation of privatization, tax reforms, and inflation-controlling measures. Since 1990 India has emerged as one of the fastest-growing economies in the developing world; during this period, the economy has grown constantly, but with a few major setbacks. This has been accompanied by increases in life expectancy, literacy rates and food security

PRIVATIZATION

The primary objectives for privatizing the Public Sector Enterprises (PSEs) are releasing the large amount of public resources locked up in non-strategic PSEs, for redeployment in areas that are much higher on the social priority and reducing the public debt that is threatening to assume unmanageable proportions. Further disinvestment would expose the privatized companies to market discipline, thereby forcing them to become more efficient and survive on their own financial and economic strength or cease.

Disinvestment would result in wider distribution of wealth through offering of shares of privatised companies to small investors and employees. Disinvestment would have a beneficial effect on the capital market; the increase in floating stock would give the market more depth and liquidity, give investors easier exit options, help in establishing more accurate benchmarks for valuation and pricing, and facilitate raising of funds by the privatised companies for their projects or expansion, in future. Opening up the public sector to appropriate private investment would increase economic activity and have an overall beneficial effect on the economy, employment and tax revenues in the medium to long term.

In many areas, e.g., the telecom sector, the end of public sector monopoly would bring relief to consumers by way of more choices, and cheaper and better quality of products and services - as has already started happening.

DIVESTMENT SCENARIO IN INDIA: at the centre

Divestment at the centre started way back in early 1990’s but at that time basically sale of minority shareholding was done. Strategic sale and majority shareholding sale began mostly in 1999-00. Divestments of Central PSEs (CPSEs) were done in order to reduce the ever increasing fiscal deficit and heavy debt burden. With a maximum divestment receipts of Rs. 5657.69 crore that took place in 2001-02 alone by 2002-03 the total divestment receipts from the divestments of CPSEs were Rs. 29,359.68 crores.

In the union budget speech of 1998-99 it was announced that the Government shareholding in CPSEs should be brought down to 26% on case to case basis, excluding strategic CPSEs where Government would retain majority shareholding. For this purpose on 16th March, 1999 the Government classified the PSEs into strategic and non-strategic areas. Strategic PSEs would be those in areas of 1) Arms and ammunition and Defense equipment; 2) Atomic energy and 3) Railway transport. All other PSEs would be considered non strategic.

After 2002 there was a slowdown in the strategic sale of PSEs. The method adopted for privatisation in general was heavily criticized. The foremost allegation was against the Disinvestment Ministry’s preference for strategic sales (in which the controlling stake of a company is sold to the buyer) as against the public issue route (in which the stake is dispersed among a large number of investors). Though the former gets the highest possible price for the company, the small investor is denied the benefit of owning at least a part of such PSUs.

DIVESTMENT SCENARIO IN THE STATE OF PUNJAB

The Government of Punjab had been under fiscal stress since 1984-85, when it became a ‘Revenue Deficit State’ from ‘Revenue Surplus State’, for the first time. Punjab had the dubious distinction of being the first among all States in terms of deficit in 1990-91. There was some fiscal consolidation in the early 1990s, but the deficit problem intensified in late 1990s again.

The factors, which have been adversely impacting the State’s fiscal over the last decade and a half were ever increasing salaries and wage bill of the employees, mounting debt burden, heavily subsidized social and economic services, slow growth of revenue and loss making Public Sector Undertakings. Punjab’s finances are afflicted both by structural problems and problems of cash-flow management.

The Government had by 31st March, 2001 received only a small amount of Rs. 8.40 crore as dividend on the huge investment of over Rs.3300 crore in the state PSEs. This investment does not include loans provided by the Government, which stood at Rs. 4864.25 crore as on 31st March, 2001. The outstanding loans of other Institutions were Rs. 19464.95 crore as on 31st March, 2001 and out of these loans Rs. 18707.12 crore was against Government Guarantee.

The fiscal position of the state could not permit any more profligacy. The State Government constituted Public Sector Disinvestment Commission in 2001 to finalize a comprehensive disinvestments program keeping in view the policies and priorities of the State Government. Sh. S. Lal Singh, Finance Minister, Punjab, in his Budget speech (June 2002), proposed fast-track disinvestments in Punjab Communications Limited, Punjab Alkalies and Chemicals Limited, Punjab Tourism Development Corporation Limited, CONWARE and PSIDC’s holding in the PTL. EXIHIBIT 1 gives the procedure for disinvestment in Punjab approved by the Government of Punjab.

TRACTOR INDUSTRY IN INDIA

With arable land of 166 million hectares (second only to the US), India is the largest international market for tractors with a peak total of 270,000 tractors sold each year, as compared with 150,000 in the US. Large part of cultivable land is not yet mechanized and current penetration is 10-12 tractors per 1000 hectares against world average of over 18 tractors per 1000 hectares.

Since late 1960s, factors such as build-up of rural infrastructure, spread of fertilizers and high yielding seeds, improved terms of trade for farm output and easier availability of credit have driven India's tractorisation process. Tractors contribute to farm operations, transportation and in building rural infrastructure, besides acting as a power source. Rising output and income from this investment in farm mechanization has in turn accelerated tractor sales. From a level of 30,000 in 1974-75, tractor industry had grown to a size of 270,000 by 1999-00, the World's largest. Indian Tractor Industry today comprises of 14 players, 3 of whom are multi national corporations. Given the size of farm holdings and geo-climatic conditions, 30 to 40 HP segment is the largest one, accounting for around 55% of the total sales, while below 30 HP segment represent around 23% of total sales. The balance 22% comes from the +40 HP range.

While the demand pattern during 1970s and 1980s was heavily skewed in favor of the northern states (principally Punjab, Haryana and Western parts of Uttar Pradesh), tractorisation spread during the 1990s was towards Central, Southern, Western and Eastern states. After posting a strong growth of 14% per annum during 1993-99 period, tractor industry has been on a declining curve. After achieving good growth in the decade 1990-1999, when Agricultural-GDP grew at the rate of 3.5% per annum,

sluggishness in the Industry started from January 2000 due to poor agricultural growth. This was caused by an unprecedented stretch of monsoon failures and draught in the year 2002-03.

On a durable supply industry like tractors, the adverse impact was inevitably maximum. After reaching a peak of 2,70,000 in 1999-00, tractor industry volumes crashed to as low as 1,60,000 in 2002-03, posting industry's sharpest ever annual drop of about 60,000 tractors. Industry woes were further compounded by the large inventory in the system, built up during 1998-2002 period when wholesale billings (supported by extended credit) were consistently higher than retail sales. But with better monsoons during July 2003 the upturn in the industry can be expected soon. EXHIBIT 2 gives the geographic and segment-wise trends in the tractor industry.

Strategic analysis of the tractor industry using Porter’s five forces model

Threat of new entrants: Access to technology is not an entry barrier in tractors, and capital investment requirements are low. The key entry barriers are developing products suitable for diverse regional requirements, build a brand name and set up an extensive rural distribution network.

Threat of substitutes: Tractors are used for agricultural and commercial purposes, based on which the threat of substitutes has been assessed. Human labour in the case of agriculture and commercial vehicles [tippers for goods and 3-wheelers, light commercial vehicles (LCVs) and utility vehicles for passengers] in the case of commercial usage act as substitutes. But tractors help in increasing agriculture productivity, save time and improve efficiently. They are used for the transportation of goods and passengers, construction activities and hauling of luggage when not used for farming purposes. Hence, as a result, the presence of substitutes is not a major concern for tractor players.

Bargaining power of suppliers: Almost all major tractor players have long term relationships with suppliers, several of which are group companies (in case of critical inputs). This results in players being sure of timely and quality supplies of major inputs.

Bargaining power of buyers: The top six players (in terms of market share) - M&M, PTL, TAFE, Escorts, Eicher and International Tractors Ltd (ITL) - accounted for around 93% of the tractor industry volumes in 2002-03. As against this, buyers of tractors (farmers) are highly fragmented, which reduces their bargaining power with the tractor manufacturers. EXIHIBIT 3 shows the market shares of the tractor industry players in 2002-03.

Intensity of rivalry among players: As per CRISIL Research reports from 2000-01 to 2002-03 the Herfindahl-Hirschman Index (HHI) has reduced from about 2100 to about 1500 thus signifying a healthy rise in competition during the period. The key differentiating factors among the players are product portfolio and distribution reach.

SWARAJ-PTL-PSIDC

August 1965, the Indian government sought Russian technological and financial aid for a 20 crore plant manufacturing 20000 tractors per year. When the Russians did not respond, the Central Mechanical Engineering Research Institute (CMERI), Durgapur began to design an indigenous tractor. Mr. Chandra Mohan was the head of Production and Engineering Division at CMERI then. CMERI came up with a first prototype in May 1967, which failed. They came up with a second prototype in October 1968 which worked. Subsequently, independent field trials with three prototypes began in May 1969 at Budni and

the agricultural universities at Pantnagar and Ludhiana. By April 1970, field experience of over 1500 hours had been gained. And the tractor was named SWARAJ.

“there were no takers for our indigenous technology…. every one was interested only in CKD import-based production”-Chandra Mohan

In early 1969, when the public sector HMT decided to diversify onto tractors, Swaraj was compared with Zetor technologies and rejected. In August 1969, during his visit to CMERI, the PSIDC Managing Director, Mr. Tejendra Khanna told CMERI that Punjab Government was keen on trying out their technology. Punjab badly wanted a plant to meet its farmers’ insatiable demand for tractors. Mr. Khanna said that PSIDC was ready to take up SWARAJ for commercialization on one condition: Mr. Chandra Mohan and his team should themselves come and implement the project.

On 28 February, 1970 the technology licensing agreement was signed after which PTL was incorporated and Mr. Chandra Mohan was its CEO from Day Zero.

PSIDC

Punjab State Industrial Development Corporation Limited (PSIDC) was established in the year 1966 to promote planned industrial development in the organised sector and to speed up industrialization in the State of Punjab. Today, PSIDC’S name is synonymous in the corporate world and it is engaged in the promotion of large and medium scale projects. PSIDC is responsible for making major projects happen in the new economic environment. PSIDC promoted PTL to commercialize the indigenous tractor developed by CMERI and bring to the state of Punjab a tractor manufacturing plant. Initially, PSIDC contributed 42% equity capital against the total paid up capital of Rs. 11.0 million. At present, it has an equity stake of 23.49% in PTL.

PTLPunjab Tractors Limited (PTL) is into the manufacturing, marketing and servicing of tractors. It was promoted by PSIDC to commercialize the indigenous tractor developed by CMERI. The company’s plant is situated at S.A.S. Nagar (Mohali) where production commenced in the year 1974. The facility was initially created to manufacture 5000 tractors per annum at a capital outlay of Rs. 37.0 million. The production capacity of tractors increased from 5000 to 60000 over the last 28 years. The company’s product line also includes Combine Harvesters and Forklifts. In the 28 years till March 2003, it has sold more than 500,000 tractors. While the journey commenced in the north, PTL today has an all India presence. Its 377 strong dealer network sells and services a wide portfolio of 6 tractor models with more than 100 variants.

PTL’s beginning was indeed humble, with the commercial introduction of SWARAJ 724 model, tractor sales barely reached 600 in 1974-75. However, over the years, on the strength of introduction of new tractor models, product performance and reliable service, SWARAJ brand started receiving favour with the farmers leading to an increase in both volume and market share. In 1995, PTL set up a second plant at Village Chappercheri with an annual capacity of 12000 tractors per annum. By 2000 expansion of annual tractor capacity to 60000 was completed. In 1999, two new models SWARAJ 733 and SWARAJ 744 were added to SWARAJ portfolio. By financial 1998-99, all these initiatives took SWARAJ to the No. 2 slot in the industry, hitting a peak sale of 50,700 tractors in 1999-00 (market share18.6%). In 2001,

Economic Times and Boston Consulting Group selected PTL as one of the India’s finest companies out of Economic Times top 500 companies. EXHIBIT 4 gives the evolving journey of PTL.

PTL’s investee companiesIn 1980, PTL took over PSIDC’s sick scooters unit- Punjab Scooters Ltd. and subsequently renamed it as SWARAJ Automotives Ltd. (SAL). PTL’s equity participation in SAL is 24%. Originally set up to manufacture scooters SAL diversified into manufacturing of enamel cookware in 1980. Later, as a major diversification in 1995, SAL started manufacturing of high technology seats for tractors, commercial vehicles, passenger cars and railways.

In 1984 PTL promoted SWARAJ Mazda Ltd. (SML) in technical and financial collaboration with Mazda Motor Corporation & Sumitomo Corporation Japan for the manufacture of Light Commercial Vehicles. Initially PTL’s equity participation in SML was 29% and that of Mazda & Sumitomo was 26%.

In 1986 PTL promoted SWARAJ Engines Ltd. (SEL) in technical and financial collaboration with Kirloskar Oil Engines Ltd. (KOEL) for manufacture of diesel engines. PTL’s equity participation in SEL is 33% and KOEL’s is 17%. Originally set up to manufacture engines for PTL, in recent years, SEL has also been a supplier of hi-tech engine components to SML.

Motivations for disinvesting PSIDC’s holding in PTL

When the present Congress Government headed by Captain Amarinder Singh took over the state of Punjab in February 2002 its fiscal position was quite depressing. State revenue deficit was Rs.3781.19 crore and state fiscal deficit was Rs. 4958.97 crore in 2001-02. Huge amounts of government funds locked in PSEs like PTL could be divested to restore the financial health of the state.

PSIDC was set up to promote industry in the state through grant of capital subsidies, concessional finance, supply of raw material etc. The State was no longer in a position to provide capital subsidies and nor was it meaningful to do so any longer, as the critical requirement for industrial growth was no longer availability of such incentives but adequate infrastructure. Similarly, providing concessional finance through State financial institutions was no longer justified in the presence of a vibrant private sector with much lower administrative costs.

Moreover PSIDC was incurring huge losses. Viswajeet Khanna, MD, PSIDC said, “we are in dire need of money. We have a staggering Rs. 1600 crore tied up in equity investments worth Rs. 960 crore and Rs. 650 crore of debt, including penal interest, in about 400 companies. The accumulated losses are about Rs. 150 crore. So we have to sell even good investments.” (5th August 2002, The Economic Times Online)

PTL was engaged in manufacturing of tractors. There was no core or strategic reason for continuance of the public sector in that industry. Tractors were being manufactured by a large number of private companies and the presence of a PSE in this industry was neither resulting in better quality nor greater affordability of these units and in any case tractors are not essential items.

PTL was a profit making firm with high brand value. PTL’s profit after tax was Rs. 100 crore in 2001-02. PTL was the second largest tractor manufacturer in the country with a market share of 18% in 2001-02. PTL’s brand SWARAJ had dealership network spread all over the country to a total of 352 by March 2002

from the 1974-75 level of 15. The Government of Punjab could expect a high price for this jewel of theirs.

The idea of disinvestment was gaining momentum in India during 2001-02.The Disinvestment Ministry at the centre raised Rs. 5657.69 crore from disinvestments in 2001-02 alone. Indian British Petroleum a profit making CPSE was sold to Indian Oil Corporation at four times the market price in February 2002. Similarly, good returns could be expected from PTL’s divestment.

Mahindra & Mahindra

Mahindra & Mahindra Limited is part of the $ 6 billion Mahindra Group, an automotive, farm equipment, financial services, trade and logistics, automotive components, after-market, IT and infrastructure conglomerate. Initially set up to manufacture general-purpose utility vehicles, Mahindra & Mahindra (M&M) was first known for assembly under licence of the iconic Willys Jeep in India. The company later branched out into manufacture of light commercial vehicles (LCVs) and agricultural tractors, rapidly growing from being a manufacturer of army vehicles and tractors to an automobile major with a growing global market.

M&M is one of the leading tractor brands in the world. It is also the largest manufacturer of tractors in India with sustained market leadership of over 25 years with a consistent market share of about 30%. It designs, develops, manufactures and markets tractors as well as farm implements. It holds the distinction of being the first tractor company globally to win the Deming Application Prize in 2003.

CDC Group Plc

Commonwealth Development Corporation (CDC) now CDC Group is UK’s development finance institution. Owned by UK Government’s Department for International Development, it provides capital to invest in promising businesses, with a particular emphasis on sub-Saharan Africa and South Asia. It started its investments in India in 1987. In India, CDC has so far invested $250 million in companies like Glenmark Pharmaceuticals, UTI bank, Satyam Infoway, BPL Mobile, Indiainfoline.com, DSQ Software and Daksh eServices. CDC had a 26% stake in UTI Bank Ltd.

SYNERGESTIC BENEFITS TO A STRATEGIC BIDDER

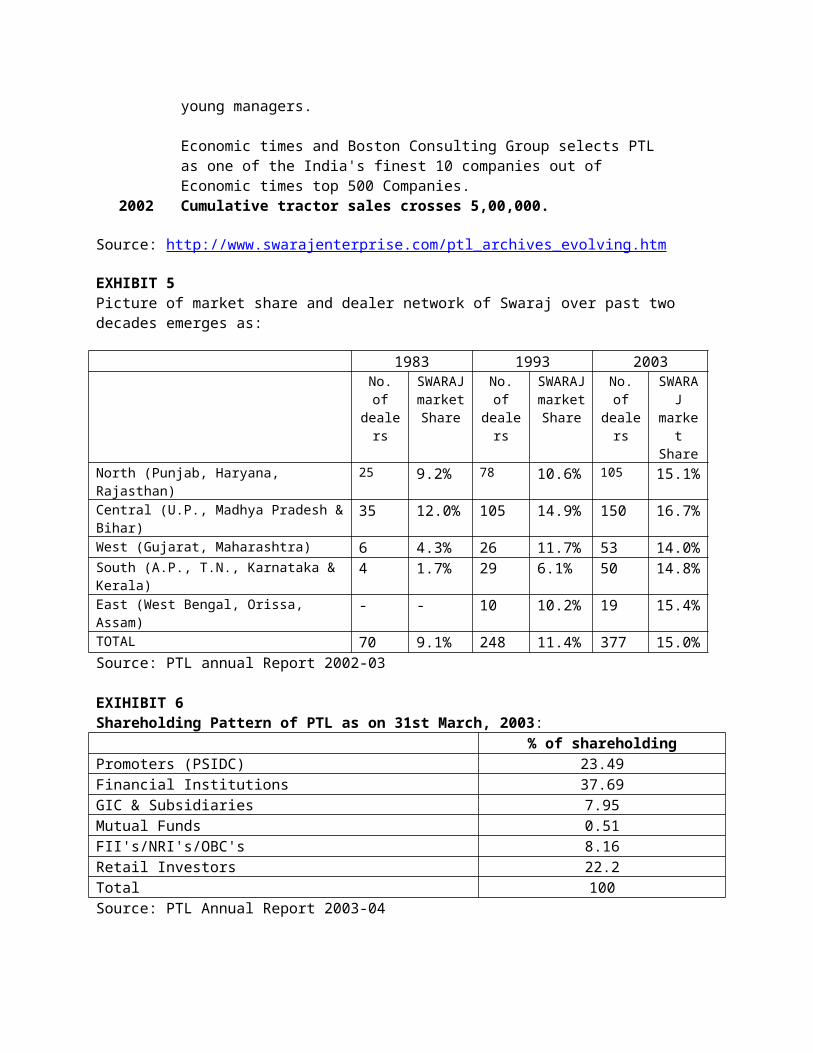

SWARAJ Brand: PTL was the second largest tractor manufacturer in the country with a 15% market share and a dealership network of 377 dealers spread all across India in 2003. EXIHIBIT 5 shows the geographic spread of PTL’s dealers in 2003.

Product Range: By 2003 PTL manufactured six tractor models with more than 100 variants.

R&D Facilities: PTL had built its own indigenous R&D facility which continuously worked on developing new tractor models for diverse consumer needs.

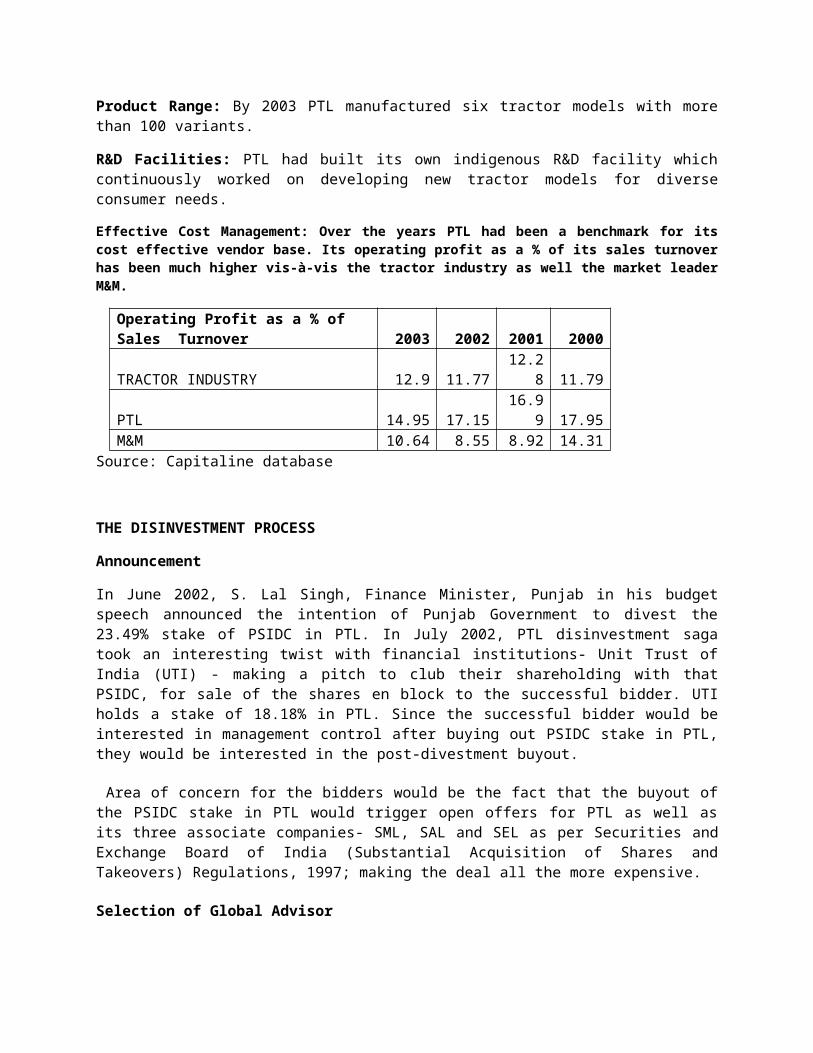

Effective Cost Management: Over the years PTL had been a benchmark for its cost effective vendor base. Its operating profit as a % of its sales turnover has been much higher vis-à-vis the tractor industry as well the market leader M&M.

Operating Profit as a % of Sales Turnover 2003 2002 2001 2000TRACTOR INDUSTRY 12.9 11.77 12.28 11.79

PTL 14.95 17.15 16.99 17.95M&M 10.64 8.55 8.92 14.31

Source: Capitaline database

THE DISINVESTMENT PROCESS

Announcement

In June 2002, S. Lal Singh, Finance Minister, Punjab in his budget speech announced the intention of Punjab Government to divest the 23.49% stake of PSIDC in PTL. In July 2002, PTL disinvestment saga took an interesting twist with financial institutions- Unit Trust of India (UTI) - making a pitch to club their shareholding with that PSIDC, for sale of the shares en block to the successful bidder. UTI holds a stake of 18.18% in PTL. Since the successful bidder would be interested in management control after buying out PSIDC stake in PTL, they would be interested in the post-divestment buyout.

Area of concern for the bidders would be the fact that the buyout of the PSIDC stake in PTL would trigger open offers for PTL as well as its three associate companies- SML, SAL and SEL as per Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 1997; making the deal all the more expensive.

Selection of Global Advisor

In August 2002, the Punjab Government invited expressions of interest from merchant bankers to be appointed as global advisors for the sale of PSIDC stake in PTL. Vini Mahajan, Director Disinvestment, Government of Punjab said, “the issue of PSIDC going alone or bundling its stake with any other FIs is to be sorted out based on the advice of the global advisors.” Further she also clarified that the Punjab Government was also open to the idea of selling its stake to the highest bidder irrespective of the bidder’s experience or track record in the industry.(5th August 2002, The Economic Times Online)

In October 2002, the State government of Punjab selected the consulting firm KPMG as the global advisor for the sale of PSIDC’s stake in PTL. The initial shortlist included Lazard India, Price Water Coopers, HSBC Securities and Capital Markets, DSP Merrill Lynch, JM Morgan Stanley and Deloitte Touche Tohmatsu.

Invitation of EOIs

The Directorate of Disinvestment, Government of Punjab, on 4th December, 2002 invited expressions of interest for strategic sale of the PSIDC stake in PTL. The Congress Government in Punjab decided to move ahead with the deal on the profit-making tractor maker despite the fact that its central leadership (which was not the ruling party at the centre in 2002-03) had been against the NDA Government (the ruling party then) at the Centre for privatising profit-making central PSEs. However, a Punjab Government official said that PTL could not be strictly classified as an entity promoted by the State Government. "PTL was promoted by PSIDC, a State Government undertaking," the official said.

Entities having a minimum net worth of Rs 200 crore were eligible to take part in the bidding process. While PSIDC was selling its stake independently in PTL, other stakeholders such as UTI, mutual funds,

GIC and foreign institutional investors had the freedom to respond to the open offer following the strategic sale and exit from the company. Expressions of Interest for the strategic sale of PSIDC’s 23.49% stake in PTL were invited by 5th January, 2003.

In February, 2003 all serious bidders out of 11 companies, which had submitted expression of interest (EOI), were shortlisted on the recommendations of the global adviser for the disinvestment of PTL. These included Mahindra & Mahindra, Escorts, Sonalika, New Holland, TAFE in league with Agco, SAME, FIIs Warburg Pincus, J. P. Morgan and CDC and a consortium led by NewBridge Llc, a private US equity fund of which Eicher Motors was a part. According to the international norms, these shortlisted companies were asked to sign confidentiality agreement, before sharing the financial documents of PTL so that they could bid for the final round.

Due Diligence

Adding another twist to the ongoing process in February, 2003 UTI said it had no plans to offload its stake in PTL. "We have no plans to sell our stake (in Punjab Tractors). It is a good company," UTI Chairman M. Damodaran. When asked whether the UTI might consider selling its shares in PTL if a good offer comes through, Mr Damodaran said in that scenario a number of things have to be taken into account before taking a final decision. (23rd February, 2003 Tribune)

Post-Disinvestment government itself was not clear about the management control of PTL as the domestic financial institutions held 46.15% of the equity in PTL who were not very keen on selling their stake. The shareholding pattern as on 31st March 2003 is shown in EXIHIBIT 6.

“The successful bidders (for PTL) can buy the equity required for effective management control through other sources or we would see what can be done (regarding management control),” Punjab Chief Minister Captain Amarinder Singh said. (18th April, 2003 Tribune)

FIIs Warburg Pincus and J. P. Morgan did not participate in due-diligence program held in May-June. By mid June, 2003 the due diligence exercise for PTL had been completed. All bidders had studied the technical and financial capability of the company. The Core Committee on Disinvestment met on 18 th

June, 2003 to take a decision about the issues raised by the bidders for disinvestment in PTL and other units.

Issues Raised by Bidders

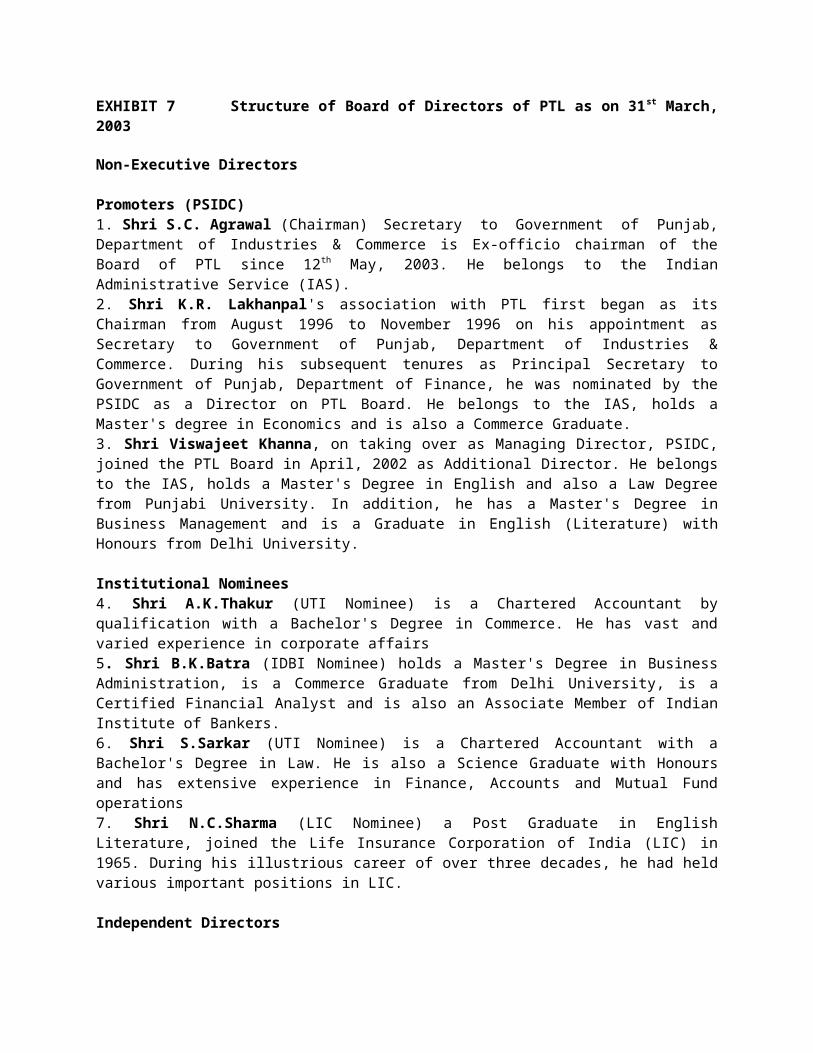

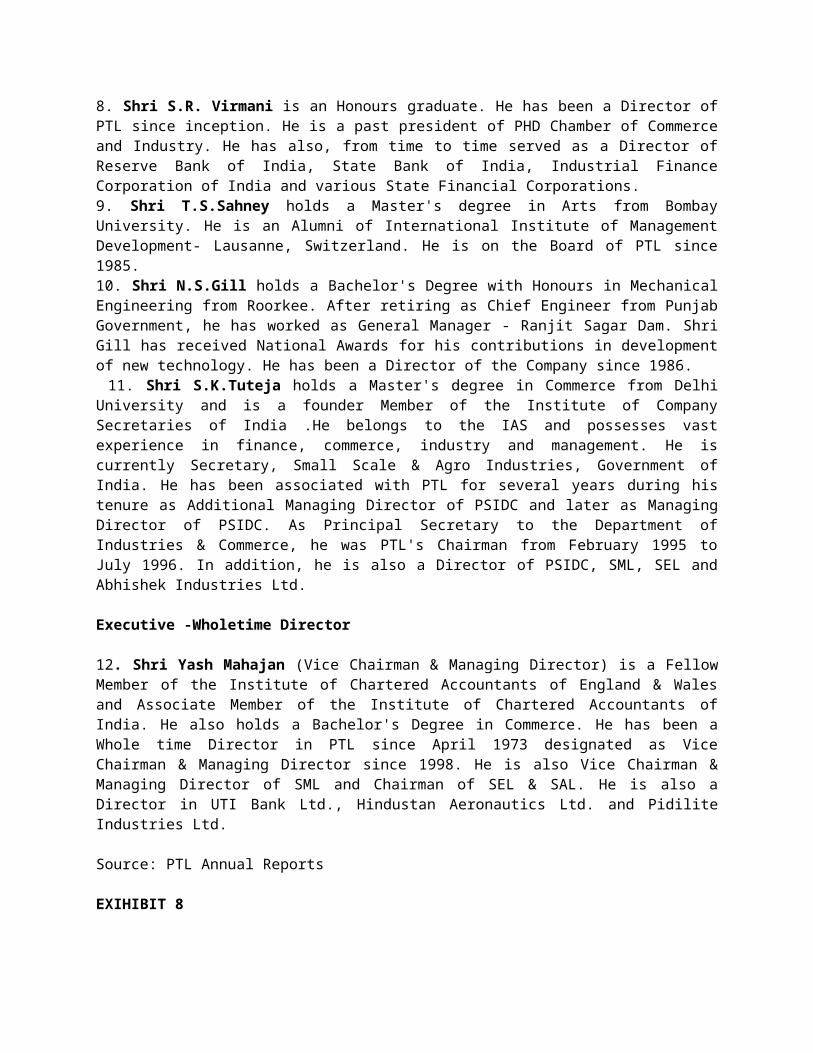

Issues raised by the bidders were mostly regarding the management control and inventory breakup. Many bidders were not convinced about securing an absolute control on PTL’s 12-member board. The PSIDC had three members on the board of PTL (one of them being the Secretary of the Government of Punjab Industries who was the Ex-Officio Chairman of the PTL Board) the rest being Financial Institutions’ (FIs) nominees and independent directors. Given this scenario, the acquirer would have to be dependent on the FIs for critical decisions. Detailed structure of the Board of Directors of PTL is given in EXHIBIT 7. As per clause 96 (b) of PTL’s Article of Association (AoA) given in EXHIBIT 8 PSIDC was entitled to appoint only two directors. And PSIDC was not keen on changing the AoA. Vini Mahajan, Director Disinvestment, Government of Punjab said, “There was no confusion in the minds of the qualified bidders as they were well-informed that post-divestment, for the PSIDC stake, two directors can be appointed.”

Bidders were not satisfied with the information provided on receivables and inventory in the data rooms. But PTL’s management disagreed with such allegations. Yash Mahajan, Vice-Chairman and Managing Director of PTL quoted a letter from Gaurav Khungar, associate director (corporate finance) of KPMG India dated 27th may 2003 saying, “We have been informed by some of the bidders who attended the data rooms at PTL that they were very happy with the way the data room had been conducted.”

Whereas an investment banker associated with the due diligence said, “The data room was not managed well. The right amount of information was not made available. PTL’s balance sheet had a lot of dealer inventory last year. Their inventory has been lying in the open with their dealers. So one doesn’t really know the exact condition of the goods.” To that S.C. Agarwal, Chairman of PTL replied, “The total (dealer) outstanding amount was provided to them but they wanted dealer-wise break up…it would not have been correct to give this information to competition.”

New Holland Tractors (India) Limited, one of the bidders for the PSIDC 23.49% share in PTL, expressed concern about the Punjab Government's move to club the shares of PTL with its subsidiaries. It apprehended that the move may discourage the tractor giant to buy the company's share, said Mr. Mario Gasparri, Managing Director of the company. He said the company would rather prefer to buy the share of other financial institutions in the company to have financial control.

Share Purchase Agreement Finalization

By end of June 2003, draft Share Purchase Agreement was sent to all interested parties. 30 th June, 2003 PTL informed BSE that the Board of Directors of the company in their meeting held on 27 th June, 2003 have decided to recommend for approval of shareholders an amendment in the clause 114(1) on page 20 of the company’s Article of Association whereby the acquirer of PSIDC’s stake shall be entitled to nominate for appointment two Directors on the Board of company in place of PSIDC. The Directors may elect from amongst the directors one of their members as the Chairman of the Board in place of the existing provision according to which Secretary of the Government of Punjab Industries is the Ex-Officio Chairman of the Board.

On 14th July, 2003 the final Share Purchase Agreement (SPA) was sent to the prospective bidders with one vital change from the draft SPA- that of reducing the lock-in period of shares from three years to one year. The deadline for the submission of the financial bids, which was earlier fixed for 22nd July 2003, was postponed to 25th July 2003 by PSIDC.

25th July, 2003: final bid deadline

On the deadline for financial bid for PSIDC’s entire equity stake of 23.49% in PTL only one bid of CDC of Rs. 218.39 crore (at Rs. 153 per share whereas BSE closing price on 25th July 2003 for PTL was Rs. 158.4) is received. Government of Punjab accepted the bid and divested PSIDC’s entire 23.49% equity stake in PTL in favor of CDC. Along with their bid CDC gave PSIDC a copy of SEBI’s letter wherein they had a blanket exemption from making an open offer. SEBI, vide its letter dated December 31, 2002, had clarified to CDC Capital Partners that acquisition of shares by CDC Group Plc. and its wholly owned subsidiaries in the ordinary course of business would be eligible for exemption under Regulation 3(1)(f)(v) of the SEBI (SAST) Regulations,1997. EXIHIBIT 9

POST DIVESTMENT REACTIONS

This disinvestment raised a host of questions regarding why was PTL not made unattractive for a strategic bidder. Most tractor makers who bid for PTL were seriously interested in the stake but it was not clear why they withdrew at the last moment. Another worrying question was the Punjab Government which could have scrapped the whole disinvestment process citing lack of competition, opted not to pull out.

Post Divestment various tractor makers were asked the reason of their withdrawal from the bidding process. Rakesh Chopra, head of agribusiness, Escorts said “If you wanted to know the quality of receivables, the information was not shared for us to make up our mind. In a normal due diligence exercise- like in the case of HMT- such information is provided. That wasn’t the only reason why we didn’t bid.”

K. J. Davasia, executive director, M&M said “We had a group working on it. We debated on the board and decided (against bidding)… I will not comment on whether it was a fair disinvestment.” Kamal Bali, commercial director (Asia), Same Deutz-Fahr India said “There was no clarity on management control. We concluded that management would be difficult. The FIs are sitting tight.”

Whereas Vini Mahajan, Director Disinvestment, Government of Punjab said “The auction process was as per international norms. Everybody who pre-qualified was taken through the due diligence process and each party’s concerns were fully addressed to the extent possible. If they did not bid it is their decision. There was no intention to have only one bid, but that has happened and it is not a bad bid.”

Captain Amarinder Singh expressed his happiness on the divestment; he said “I think it is good for Punjab. This opens up avenues for further investments from the UK and other countries which is what Punjab wants.”

Chander Mohan, Founder CEO of PTL said, “I am happy that none of the domestic manufacturers has bought the PSIDC stake. They would have destroyed the SWARAJ brand.”

The opposition government displayed their discontent over the whole process. “Instead of creating competition among the bidders, they did away with it. Why were issues like… who will control the company not clarified? Why was there only one bidder? They should have gone for rebidding. This issue will be raised in the next session of Vidhan Sabha,” said Kwaljit Singh, former finance minister of Punjab (a leader in the opposition Shiromani Akali Dal party).

Many felt that the Congress Government in Punjab pushed through the privatization whereas the Congress Government at the centre had been opposing the sale of profitable PSEs. This being the first divestment in favor of a financial investor rather than a strategic investor became a unique feature of this privatization. This also raised questions about what will be the financial investor’s future plans with PTL.

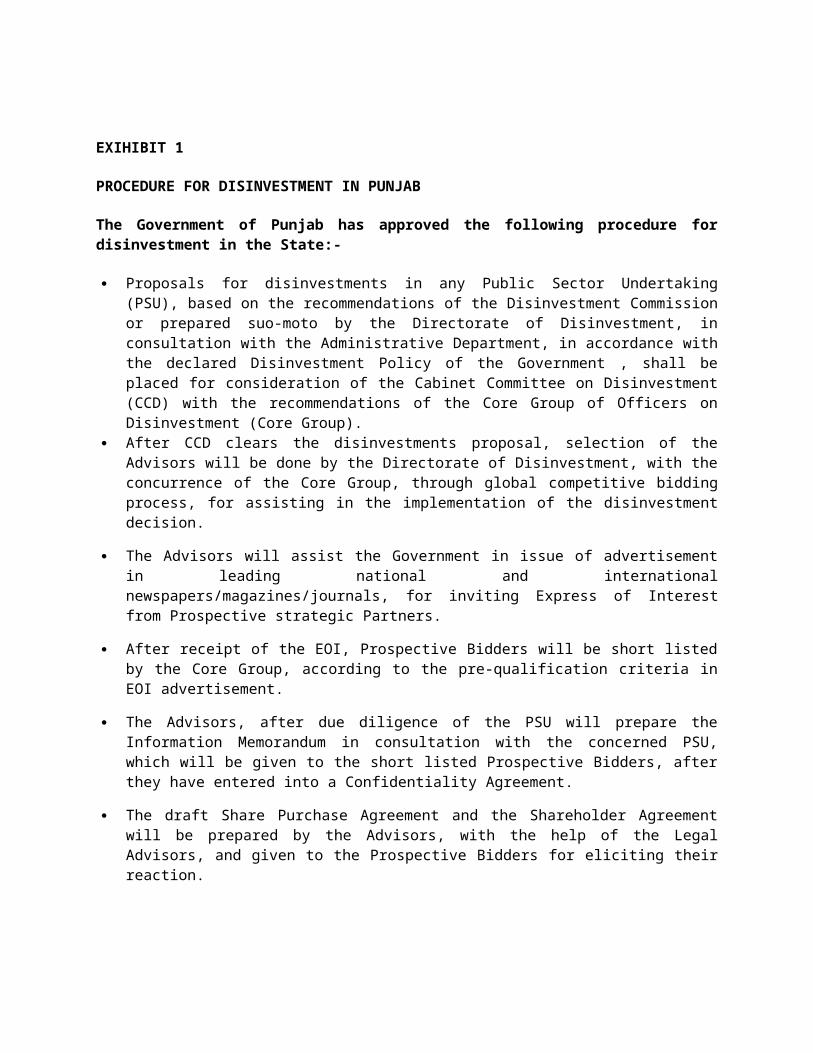

EXIHIBIT 1

PROCEDURE FOR DISINVESTMENT IN PUNJAB

The Government of Punjab has approved the following procedure for disinvestment in the State:-

Proposals for disinvestments in any Public Sector Undertaking (PSU), based on the recommendations of the Disinvestment Commission or prepared suo-moto by the Directorate of Disinvestment, in consultation with the Administrative Department, in accordance with the declared Disinvestment Policy of the Government , shall be placed for consideration of the Cabinet Committee on Disinvestment (CCD) with the recommendations of the Core Group of Officers on Disinvestment (Core Group).

After CCD clears the disinvestments proposal, selection of the Advisors will be done by the Directorate of Disinvestment, with the concurrence of the Core Group, through global competitive bidding process, for assisting in the implementation of the disinvestment decision.

The Advisors will assist the Government in issue of advertisement in leading national and international newspapers/magazines/journals, for inviting Express of Interest from Prospective strategic Partners.

After receipt of the EOI, Prospective Bidders will be short listed by the Core Group, according to the pre-qualification criteria in EOI advertisement.

The Advisors, after due diligence of the PSU will prepare the Information Memorandum in consultation with the concerned PSU, which will be given to the short listed Prospective Bidders, after they have entered into a Confidentiality Agreement.

The draft Share Purchase Agreement and the Shareholder Agreement will be prepared by the Advisors, with the help of the Legal Advisors, and given to the Prospective Bidders for eliciting their reaction.

The Prospective Bidders may undertake due diligence of the PSU and hold discussions with the Advisors/the Government/the management of the PSU for any clarifications. .

Concurrently, the task of valuation of the PSU will be undertaken in accordance with the standard national and international practices.

Based on the response received from the Prospective Bidders, the Share Purchase and Shareholders Agreement will be finalized and vetted by the Legal Rememberancer and approved by the Government and then sent to the Prospective Bidders for inviting the final binding bids (Technical and Financial). After examination, analysis and evaluation, the recommendations of the Core Group will be placed before the CCD for a final decision regarding selection of the Strategic Partner, signing of the Share Purchase or Shareholders Agreements and other ancilliary issued.

In case the disinvested PSUs shares are listed on SE, an open offer would be required to be made by the bidder before closing the transaction.

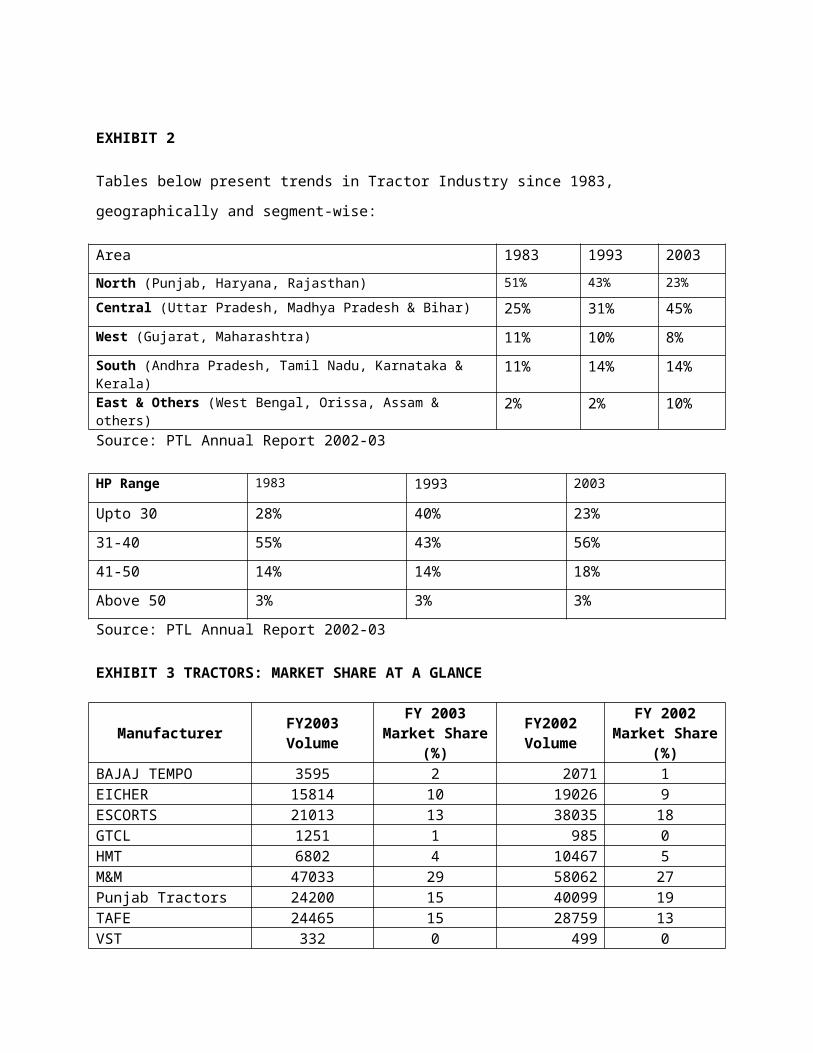

EXHIBIT 2

Tables below present trends in Tractor Industry since 1983, geographically and segment-wise:

Area 1983 1993 2003

North (Punjab, Haryana, Rajasthan) 51% 43% 23%

Central (Uttar Pradesh, Madhya Pradesh & Bihar) 25% 31% 45%

West (Gujarat, Maharashtra) 11% 10% 8%

South (Andhra Pradesh, Tamil Nadu, Karnataka & Kerala) 11% 14% 14%

East & Others (West Bengal, Orissa, Assam & others) 2% 2% 10%

Source: PTL Annual Report 2002-03

HP Range 1983 1993 2003

Upto 30 28% 40% 23%

31-40 55% 43% 56%

41-50 14% 14% 18%

Above 50 3% 3% 3%

Source: PTL Annual Report 2002-03

EXHIBIT 3 TRACTORS: MARKET SHARE AT A GLANCE

Manufacturer FY2003Volume

FY 2003 Market Share (%)

FY2002Volume

FY 2002 Market Share (%)

BAJAJ TEMPO 3595 2 2071 1EICHER 15814 10 19026 9ESCORTS 21013 13 38035 18GTCL 1251 1 985 0HMT 6802 4 10467 5M&M 47033 29 58062 27Punjab Tractors 24200 15 40099 19TAFE 24465 15 28759 13VST 332 0 499 0Sonalika 16464 10 17002 8Total Industry 160969 100 215005 100Source: Tractor Manufacturer’s Association (TMA)

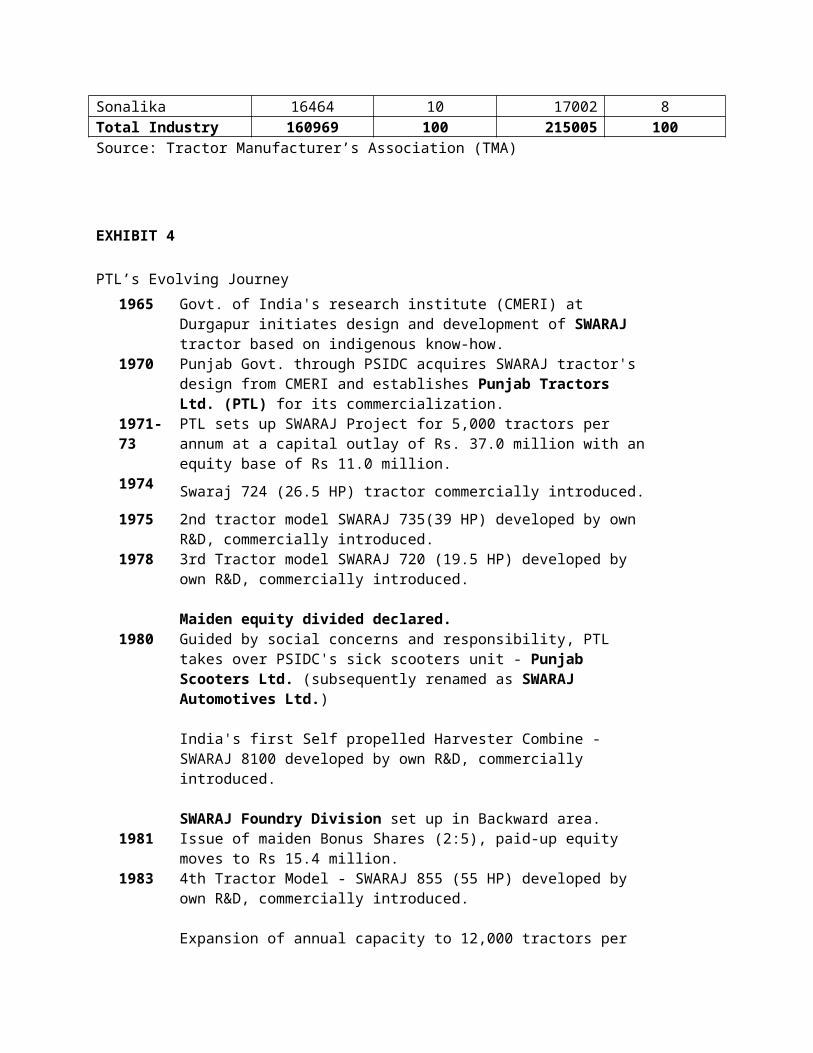

EXHIBIT 4

PTL’s Evolving Journey

1965

Govt. of India's research institute (CMERI) at Durgapur initiates design and development of SWARAJ tractor based on indigenous know-how.

1970

Punjab Govt. through PSIDC acquires SWARAJ tractor's design from CMERI and establishes Punjab Tractors Ltd. (PTL) for its commercialization.

1971-73

PTL sets up SWARAJ Project for 5,000 tractors per annum at a capital outlay of Rs. 37.0 million with an equity base of Rs 11.0 million.

1974 Swaraj 724 (26.5 HP) tractor commercially introduced.

1975

2nd tractor model SWARAJ 735(39 HP) developed by own R&D, commercially introduced.

1978

3rd Tractor model SWARAJ 720 (19.5 HP) developed by own R&D, commercially introduced.

Maiden equity divided declared.

1980

Guided by social concerns and responsibility, PTL takes over PSIDC's sick scooters unit - Punjab Scooters Ltd. (subsequently renamed as SWARAJ Automotives Ltd.)

India's first Self propelled Harvester Combine - SWARAJ 8100 developed by own R&D, commercially introduced.

SWARAJ Foundry Division set up in Backward area.

1981 Issue of maiden Bonus Shares (2:5), paid-up equity moves to Rs 15.4 million.

1983

4th Tractor Model - SWARAJ 855 (55 HP) developed by own R&D, commercially introduced.

Expansion of annual capacity to 12,000 tractors per annum at Plant 1.

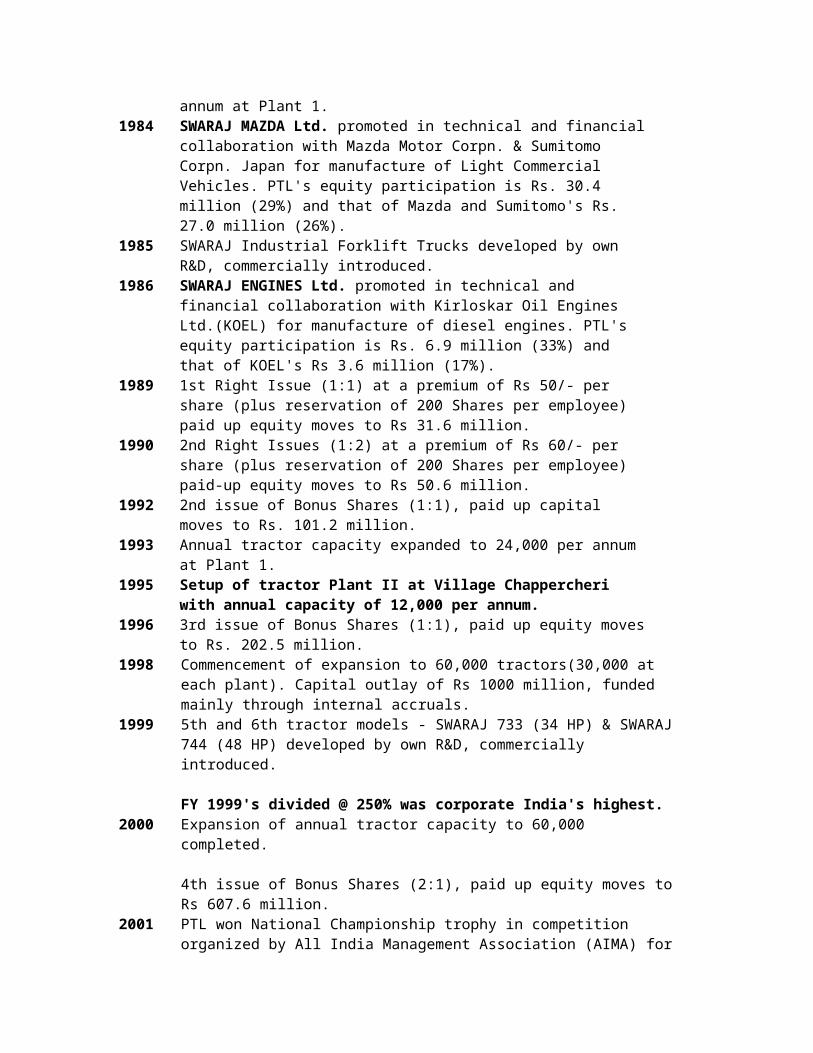

1984

SWARAJ MAZDA Ltd. promoted in technical and financial collaboration with Mazda Motor Corpn. & Sumitomo Corpn. Japan for manufacture of Light Commercial Vehicles. PTL's equity participation is Rs. 30.4 million (29%) and that of Mazda and Sumitomo's Rs. 27.0 million (26%).

1985

SWARAJ Industrial Forklift Trucks developed by own R&D, commercially introduced.

1986

SWARAJ ENGINES Ltd. promoted in technical and financial collaboration with Kirloskar Oil Engines Ltd.(KOEL) for manufacture of diesel engines. PTL's equity participation is Rs. 6.9 million (33%) and that of KOEL's Rs 3.6 million (17%).

1989

1st Right Issue (1:1) at a premium of Rs 50/- per share (plus reservation of 200 Shares per employee) paid up equity moves to Rs 31.6 million.

1990

2nd Right Issues (1:2) at a premium of Rs 60/- per share (plus reservation of 200 Shares per employee) paid-up equity moves to Rs 50.6 million.

1992 2nd issue of Bonus Shares (1:1), paid up capital moves to Rs. 101.2 million.

1993 Annual tractor capacity expanded to 24,000 per annum at Plant 1.

1995

Setup of tractor Plant II at Village Chappercheri with annual capacity of 12,000 per annum.

1996 3rd issue of Bonus Shares (1:1), paid up equity moves to Rs. 202.5 million.

1998

Commencement of expansion to 60,000 tractors(30,000 at each plant). Capital outlay of Rs 1000 million, funded mainly through internal accruals.

1999

5th and 6th tractor models - SWARAJ 733 (34 HP) & SWARAJ 744 (48 HP) developed by own R&D, commercially introduced.

FY 1999's divided @ 250% was corporate India's highest.

2000

Expansion of annual tractor capacity to 60,000 completed.

4th issue of Bonus Shares (2:1), paid up equity moves to Rs 607.6 million.

2001

PTL won National Championship trophy in competition organized by All India Management Association (AIMA) for young managers.

Economic times and Boston Consulting Group selects PTL as one of the India's finest 10 companies out of Economic times top 500 Companies.

2002 Cumulative tractor sales crosses 5,00,000.

Source: http://www.swarajenterprise.com/ptl_archives_evolving.htm

EXHIBIT 5Picture of market share and dealer network of Swaraj over past two decades emerges as:

1983 1993 2003No. of

dealersSWARAJ market Share

No. of dealers

SWARAJ market Share

No. of dealers

SWARAJ market Share

North (Punjab, Haryana, Rajasthan) 25 9.2% 78 10.6% 105 15.1%Central (U.P., Madhya Pradesh & Bihar) 35 12.0% 105 14.9% 150 16.7%West (Gujarat, Maharashtra) 6 4.3% 26 11.7% 53 14.0%South (A.P., T.N., Karnataka & Kerala) 4 1.7% 29 6.1% 50 14.8%East (West Bengal, Orissa, Assam) - - 10 10.2% 19 15.4%TOTAL 70 9.1% 248 11.4% 377 15.0%Source: PTL annual Report 2002-03

EXIHIBIT 6Shareholding Pattern of PTL as on 31st March, 2003:

% of shareholdingPromoters (PSIDC) 23.49Financial Institutions 37.69GIC & Subsidiaries 7.95Mutual Funds 0.51FII's/NRI's/OBC's 8.16

Retail Investors 22.2Total 100Source: PTL Annual Report 2003-04

EXHIBIT 7 Structure of Board of Directors of PTL as on 31st March, 2003

Non-Executive Directors

Promoters (PSIDC)1. Shri S.C. Agrawal (Chairman) Secretary to Government of Punjab, Department of Industries & Commerce is Ex-officio chairman of the Board of PTL since 12 th May, 2003. He belongs to the Indian Administrative Service (IAS).2. Shri K.R. Lakhanpal's association with PTL first began as its Chairman from August 1996 to November 1996 on his appointment as Secretary to Government of Punjab, Department of Industries & Commerce. During his subsequent tenures as Principal Secretary to Government of Punjab, Department of Finance, he was nominated by the PSIDC as a Director on PTL Board. He belongs to the IAS, holds a Master's degree in Economics and is also a Commerce Graduate.3. Shri Viswajeet Khanna, on taking over as Managing Director, PSIDC, joined the PTL Board in April, 2002 as Additional Director. He belongs to the IAS, holds a Master's Degree in English and also a Law Degree from Punjabi University. In addition, he has a Master's Degree in Business Management and is a Graduate in English (Literature) with Honours from Delhi University.

Institutional Nominees4. Shri A.K.Thakur (UTI Nominee) is a Chartered Accountant by qualification with a Bachelor's Degree in Commerce. He has vast and varied experience in corporate affairs5. Shri B.K.Batra (IDBI Nominee) holds a Master's Degree in Business Administration, is a Commerce Graduate from Delhi University, is a Certified Financial Analyst and is also an Associate Member of Indian Institute of Bankers.6. Shri S.Sarkar (UTI Nominee) is a Chartered Accountant with a Bachelor's Degree in Law. He is also a Science Graduate with Honours and has extensive experience in Finance, Accounts and Mutual Fund operations7. Shri N.C.Sharma (LIC Nominee) a Post Graduate in English Literature, joined the Life Insurance Corporation of India (LIC) in 1965. During his illustrious career of over three decades, he had held various important positions in LIC.

Independent Directors8. Shri S.R. Virmani is an Honours graduate. He has been a Director of PTL since inception. He is a past president of PHD Chamber of Commerce and Industry. He has also, from time to time served as a Director of Reserve Bank of India, State Bank of India, Industrial Finance Corporation of India and various State Financial Corporations.9. Shri T.S.Sahney holds a Master's degree in Arts from Bombay University. He is an Alumni of International Institute of Management Development- Lausanne, Switzerland. He is on the Board of PTL since 1985.10. Shri N.S.Gill holds a Bachelor's Degree with Honours in Mechanical Engineering from Roorkee. After retiring as Chief Engineer from Punjab Government, he has worked as General Manager - Ranjit Sagar

Dam. Shri Gill has received National Awards for his contributions in development of new technology. He has been a Director of the Company since 1986. 11. Shri S.K.Tuteja holds a Master's degree in Commerce from Delhi University and is a founder Member of the Institute of Company Secretaries of India .He belongs to the IAS and possesses vast experience in finance, commerce, industry and management. He is currently Secretary, Small Scale & Agro Industries, Government of India. He has been associated with PTL for several years during his tenure as Additional Managing Director of PSIDC and later as Managing Director of PSIDC. As Principal Secretary to the Department of Industries & Commerce, he was PTL's Chairman from February 1995 to July 1996. In addition, he is also a Director of PSIDC, SML, SEL and Abhishek Industries Ltd.

Executive -Wholetime Director

12. Shri Yash Mahajan (Vice Chairman & Managing Director) is a Fellow Member of the Institute of Chartered Accountants of England & Wales and Associate Member of the Institute of Chartered Accountants of India. He also holds a Bachelor's Degree in Commerce. He has been a Whole time Director in PTL since April 1973 designated as Vice Chairman & Managing Director since 1998. He is also Vice Chairman & Managing Director of SML and Chairman of SEL & SAL. He is also a Director in UTI Bank Ltd., Hindustan Aeronautics Ltd. and Pidilite Industries Ltd.

Source: PTL Annual Reports

EXIHIBIT 8

According to clause 96 (b) on page 17 of PTL’s Article of Association (AoA):

“During such time as…. PSIDC …. continue(s) to hold any proportion of the paid up capital of the company and subject to the provisions contained in the Act and these Articles, (PSIDC) shall be entitled to appoint two directors.”

The AoA is a binding contract between the company and the shareholders and between the shareholders. It can be amended only by a special resolution- which can only be passed with a 75% majority.

Source: BUSINESS WORLD 11th August, 2003

EXHIBIT 9

Relevant Regulations of Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 1997

Applicability of the regulation.3. (1) Nothing contained in regulations 10, 11 and 12 of these regulations shall apply to:(f) acquisition of shares in the ordinary course of business by,—(v) the International Finance Corporation, Asian Development Bank, International Bank for Reconstruction and Development, Commonwealth Development Corporation and such other international financial institutions;

Acquisition of fifteen per cent or more of the shares or voting rights of any company

10. No acquirer shall acquire shares or voting rights which (taken together with shares or voting rights, if any, held by him or by persons acting in concert with him), entitle such acquirer to exercise fifteen per cent or more of the voting rights in a company, unless such acquirer makes a public announcement to acquire shares of such company in accordance with the regulations.

Consolidation of holdings11.Explanation.—for the purposes of regulation 10 and regulation 11, acquisition shall mean and include,—(a) direct acquisition in a listed company to which the regulations apply;(b) indirect acquisition by virtue of acquisition of companies, whether listed or unlisted, whether in India or abroad.

Acquisition of control over a company.12. Irrespective of whether or not there has been any acquisition of shares or voting rights in a company, no acquirer shall acquire control over the target company, unless such person makes a public announcement to acquire shares and acquires such shares in accordance with the regulations.

EXHIBIT 10

Source: Capitaline Database

EXHIBIT 11 Beta estimate for PTL (Beta is a relative measure of risk associated with the PTL’s shares as against the market as a whole)

MARKET INDEX taken as a proxy for market BSE_SENSEX NIFTYTIME PERIOD 25/07/00 to 25/07/03 25/07/00 to 25/07/03BETA ESTIMATE 0.4884 0.4980

Source: Capitaline Database

EXHIBIT 12 Market Risk Premium used by firms in India in 2002-03

Company Market Risk Premium usedInfosys Technologies Limited (Infosys) 7%Hindustan Unilever Limited (HUL) 9%Source: Infosys and HUL Annual Report 2002-03

EXHIBIT 13 Implicit yields on Government of India Securities

2002-03 2001-02 2000-0191 day Treasury Bills Minimum 5.1 6.05 7.91

Maximum 7 8.5 10.47Average 5.73 6.88 8.98

< 10 year maturity Minimum 6.57 6.98 9.47

(8 years) (FRB, 8 years) (2 years, 11 months)

Maximum 7.72 9.81 11.69 (9 years, 11

months)(7 years, 5 months) (9 years, 10

months)

10 year maturity Minimum 6.72 9.39 11.3Maximum 8.14 9.39 11.3

> 10 year maturity Minimum 6.05 7.18 10.47

(12 years, 8 months)

(14 years, 11 months)

(14 years)

Maximum 8.62 11 11.7 (24 years, 3

months)(19 years, 8 months) (11 years, 9

months)Source: Reserve Bank of India Annual Report 2002-03

EXHIBIT 14: Financial Statements of PTLPunjab Tractors Ltd- BALANCE SHEET

(Rs in Crs) Year FY2003 FY2002 FY2001 FY2000 FY1999 SOURCES OF FUNDS : Share Capital 60.76 60.76 60.76 20.25 20.25 Reserves Total 415.76 393.2 373.56 351.77 278.4 Total Shareholders Funds 476.52 453.96 434.32 372.02 298.65 Secured Loans 84.78 0 0.05 0 0 Unsecured Loans 39.7 194.35 12.99 12.75 7.79 Total Debt 124.48 194.35 13.04 12.75 7.79 Total Liabilities 601 648.31 447.36 384.77 306.44 APPLICATION OF FUNDS : Gross Block 281.57 276.58 262.15 244.14 219.23

Less : Accumulated Depreciation 141.85 125.56 107.27 90.54 75.27 Net Block 139.72 151.02 154.88 153.6 143.96 Capital Work in Progress 3.38 4.61 8.25 6.64 9.11 Investments 7.54 7.53 7.73 10.85 49.53 Current Assets, Loans & Advances Inventories 70.49 69.09 96.88 120.53 123.64 Sundry Debtors 471.69 484.21 297.59 88.28 3.99 Cash and Bank 38.96 36.95 4.2 18.4 11.78 Loans and Advances 26.73 85.7 59.55 71.09 70.13 Total Current Assets 607.87 675.95 458.22 298.3 209.54 Total Current Liabilities 120.41 152.62 181.72 84.62 105.7 Net Current Assets 487.46 523.33 276.5 213.68 103.84 Net Deferred Tax -37.1 -38.18 0 0 0 Total Assets 601 648.31 447.36 384.77 306.44

Punjab Tractors Ltd- Profit & Loss Statement

(Rs in Crs) Year FY2003 FY2002 FY2001 FY2000 FY1999 INCOME : Sales Turnover 641.02 1,032.45 1,119.46 1,170.21 1,080.57 Excise Duty 94.23 144.28 154.99 153.36 124.5 Net Sales 546.79 888.17 964.47 1,016.85 956.07 Other Income 6.54 7.85 7.52 14.79 16.74 Stock Adjustments 9.3 2.51 -6.09 -2.9 9.3 Total Income 562.63 898.53 965.9 1,028.74 982.11 EXPENDITURE : Raw Materials 356.1 596 645.18 693.54 682.54 Power & Fuel Cost 8.77 9.9 10.3 10.03 8.38 Employee Cost 60.59 61.17 57.12 53.19 46.14 Other Manufacturing Expenses 9.06 18.1 18.97 23.24 19.59 Selling and Administration Expenses 30.97 35.39 40.19 36.6 31.05 Miscellaneous Expenses 1.32 0.97 3.89 2.09 0.84 Less: Pre-operative Expenses Capitalised 0 0.02 0 0.02 0.07 Total Expenditure 466.81 721.51 775.65 818.67 788.47 Operating Profit 95.82 177.02 190.25 210.07 193.64 Interest 16.54 15.81 5.31 3.68 3.13 Gross Profit 79.28 161.21 184.94 206.39 190.51 Depreciation 17.04 17.66 16.92 15.98 13.68 Profit Before Tax 62.24 143.55 168.02 190.41 176.83 Tax 20.2 43.2 55.5 57.15 51 Deferred Tax -1.08 0.33 0 0 0

Reported Net Profit 43.12 100.02 112.52 133.26 125.83

Source: Capitaline Database

EXIHIBIT 15: Financial Statements of other players in tractor industry

TRACTOR INDUSTRY COMPARATIVE BALANCE SHEET (Rs in Crs)

Escorts Sonalika M&M TAFEFY2003 FY2003 FY2003 FY2003

SOURCES OF FUNDS :Share Capital 90.71 5.8 272.62 12Reserves Total 1,353.48 490.6 4,989.46 984.5Equity Application Money 0 0 0 0Total Shareholders Funds 1,444.19 496.4 5,262.08 996.5Secured Loans 253.79 0 981 60.41Unsecured Loans 10.36 15.12 3,071.76 15.46Total Debt 264.15 15.12 4,052.76 75.87Total Liabilities 1,708.34 511.52 9,314.84 1,072.37APPLICATION OF FUNDS :Gross Block 2,059.83 267.55 4,893.89 454.53Less : Accumulated Depreciation 602.93 68.64 2,326.29 210.67Less:Impairment of Assets 0 2.53 0 0Net Block 1,456.90 196.38 2,567.60 243.86Capital Work in Progress 10.71 18.4 646.73 6.04Investments 235.8 3.3 5,786.41 387.97Current Assets, Loans & AdvancesInventories 199.49 260.41 1,060.67 168.64Sundry Debtors 329.15 149.6 1,043.65 290.35Cash and Bank 164.8 47.74 1,574.43 357.42Loans and Advances 137.27 70.44 1,402.29 108.25Total Current Assets 830.71 528.19 5,081.04 924.66Total Current Liabilities 859.04 216.04 4,797.76 470.16Net Current Assets -28.33 312.15 283.28 454.5Miscellaneous Expenses not written off 5.42 0 12.55 0Deferred Tax Assets 76.87 4.35 411.65 0Deferred Tax Liability 49.03 23.06 393.38 20Net Deferred Tax 27.84 -18.71 18.27 -20Total Assets 1,708.34 511.52 9,314.84 1,072.37

TRACTOR INDUSTRY PROFIT & LOSS STATEMENT (Rs in Crs)

Escorts Sonalika M&M TAFE

FY2003 FY2003 FY2003 FY2003INCOME :Sales Turnover 2,177.03 966.59 14,513.87 2,412.91Excise Duty 18.59 8.12 1,587.05 50.19Net Sales 2,158.44 958.47 12,926.82 2,362.72Other Income 45.8 7.57 600.93 74.23Stock Adjustments 14.33 52.35 -156.29 -0.16Total Income 2,218.57 1,018.39 13,371.46 2,436.79EXPENDITURE :Raw Materials 1,456.10 733.95 9,117.94 1,723.47Power & Fuel Cost 26.25 6.83 98.69 22.01Employee Cost 234.58 50.4 1,018.41 122.32Other Manufacturing Expenses 48.93 43.57 212.3 63.65Selling and Administration Expenses 231.29 53.4 877.74 150.69Miscellaneous Expenses 11.42 17.31 596.38 76.38Less: Pre-operative Expenses Capitalised 0 0 42.83 0Total Expenditure 2,008.57 905.46 11,878.63 2,158.52Operating Profit 210 112.93 1,492.83 278.27Interest 61.1 3.2 134.12 12.44Gross Profit 148.9 109.73 1,358.71 265.83Depreciation 37.84 19.04 291.51 22.79Profit Before Tax 111.06 90.69 1,067.20 243.04Tax 0.4 30.04 58.51 81Fringe Benefit tax 1.27 1.15 0 1.36Deferred Tax 19.66 -2.3 141.18 8.06Reported Net Profit 89.73 61.8 867.51 152.62

Source: Capitaline Database

EXHIBIT 16

SOME DIVESTMENTS IN INDIA DURING 2000s

Bharat Aluminium Company Limited (BALCO)

The strategic sale of 51 per cent stake in the aluminium major, Bharat Aluminium Company Limited (BALCO), to Sterlite Industries Limited for a consideration of Rs 551.5 crore on 21 st February 2001 was the second privatization in the country. First being the strategic sale of Modern Food Industries Ltd to Hindustan Lever Ltd in March 2000. Sterlite emerged the winner pipping two heavyweights -- the A.V. Birla group's Hindalco and the US-based Alcoa.

“The bid of Sterlite compares well with the expectation that the Government had formed with the reserve price,” the Divestment Minister Mr Arun Shourie said on the same day. He said the bids were valued by four different methods -- the discounted cash flow method, comparable valuation method,

balance sheet valuation method and asset valuation method. “Apart from the highest price, the business plan of Sterlite was the most credible,” he said.

Dispelling fears on the employees' future post-disinvestment, Mr Shourie said the shareholders' agreement has provided several safety clauses for the workers. In the first year after the takeover, there will not be any retrenchment at all. After the first year, if any retrenchment takes place, the VRS package offered would be as generous as the VRS package prevalent in PSUs.

The Union Government incorporated a three-year lock-in period in its shareholders' agreement with Sterlite, barring the latter from selling any of its 51 per cent stake in BALCO during this period.

Indian British Petroleum (IBP)

On 5th February, 2002 IBP was offered to Indian Oil Corporation as its bid for the 33.58 per cent stake was the highest — Rs 558 crore more than the second highest bid of Rs 595 crore by Royal Dutch Shell. The other offers, including Reliance Industry's, were much lower. This IBP bid amounts to a whopping Rs 1,551 an IBP share.

The IBP share was traded on the BSE and the NSE at around Rs 410 in January 2002 second week. Even this price was arrived at on the basis of divestment news. The share has traded as low as Rs 145 in the 2001. Thus, the IOC's offer price of Rs 1,551 is four times that of the price just quoted and about 10 times that the lowest traded price in the last 52 weeks. It is almost the double the price of the second-highest bidder. The valuations will differ from bidder to bidder based on the different assumptions and perceptions about the future value to the acquirer. But it is true that IOC can utilise IBP's 1,500-strong retail outlet. This will prove an advantage, especially after the administered price mechanism is dismantled with effect from 1st April, 2002

However, the exorbitant difference in the bid price makes it questionable. Either the other bidders undervalued IBP, which is unlikely as there are about half a dozen serious bidders from India and abroad. This makes it appear IOC overbid for IBP and raises questions about the decision.

Videsh Sanchar Nigam Limited (VSNL)

Panataone Finvest (a Tata Group Co) bid price of Rs 1,439.25 crore at Rs 202 per share for buying 25 per cent of the Government stake in VSNL was approved by the Cabinet Committee on Disinvestment (CCD) at a meeting on 5th February, 2002. The Government had fixed a reserve price of Rs 1,218.375 crore for its 25 per cent stake in VSNL.

Divestments in other Punjab PSUs before PTL

Punjab Communications Limited (PUNCOM)

On the deadline for financial bid, 7th March, 2003 sole bid was received from Shyam Telecommunications for Punjab government’s 69.4% stake in PUNCOM. The bid was rejected due to its low price. Though Videocon, HFCL, Bharat Hotels, Reliance Infocom and Motorala had expressed interest in the company, yet after signing ‘confidentiality agreement’ with the Directorate of Disinvestment, Punjab, these firms did not submit financial bids.

“We will call the bids for Punjab Communications (PUNCOM) again. Though the company’s technology may not be the latest, it has assets that are worth much more than the bid of Rs 24 crore,” state Chief Minister Amarinder Singh said on 17th April, 2003. “Even the cash balance of the company is 90 crore,’’ Chief Minister said.

Later the company’s MD was sacked for not providing the correct picture of the company’s strength to the prospective bidders.

Punjab Alkalies and Chemicals Limited (PACL)

On the deadline for financial bid was 24th April, 2003 no bid was received for 44.26% stake of the state government in PACL. PACL manufactures caustic soda, liquid chlorine and hydrochloric acid. PACL has been making losses over the last few years in a row. With losses accumulating, the company's book value per share has been eroded to below par. The book value per share stood at Rs 7.50 as on 31st March, 2002. The PACL scrip lost 35.5% on the same day.

Source: Various sources

EXHIBIT 17

Capacity utilization for major players in Indian Tractor industry in 2002-03

M&M TAFE Escorts PTL ITLCapacity (units) 112000 52800 72000 60000 30000Production (units) 45626 24031 19369 24583 16624Total sales (units) 47033 24465 21013 24200 16464Capacity Utilization 40.74% 45.51% 26.9% 40.97% 55.41%Source: TMA