public disclosure authorized - world...

TRANSCRIPT

Document of

THE WORLD BANK

FOR OFFICIAL USE ONLY

Report No. P-7451-MOR

REPORT AND RECOMMENDATION

OF THE PRESIDENT OF THE

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMMENT

TO THE

EXECUTIVE BOARD OF DIRECTORS

ON A PROPOSED

INFORMATION INFRASTRUCTURE SECTOR DEVELOPMENT LOAN

IN THE AMOUNT OF US$65 MILLION

TO THE

KINGDOM OF MOROCCO

April 16,2001

Finance, Private Sector and InfiasttureMiddle East and North Africa Region

This document has a restricted distribution and may be used by recipients only in the perfbrmance oftheirofficial duties. Its contents may not otherwise be disclosed without World Bank authorizatioaL

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Curresiy and Excdawn Rakt(as of March 28,2001 )

Currency Unit = Dirham (MUAD)US$1.00 = MAD 10.9

FiSCAL YEARJuly I - June 30

ABBREVIATIONS AND ACRONYMS

AFDB African Development BankADM Societt des Autoroutes du MarocAl Alternative InfrastructuresANRT Agence Nationale de Reglementation du Secteur des TMlecommunicationsAOL Administration on lineBAJ Barnamaj al Aoulaouiyat al Ijtimaiya (Social Priority Program)BAM Barid Al-Maghrib (the postal operator)CAS Country Assistance StrategyCCP Comptes Cheques PostauxCDG Caisse de Dipot et de GestionCEN Caisse d'Epargne NationaleCMU Country Management UnitCTF Consultant Trust FundsEU European UnionFDI Foreign Direct InvestmentGIPE Gestion Integree du Personnel de I 'EtatGDP Gross Domestic ProductGMPCS Global Mobile Personal Communications SystemGOL Government on lineGOM Government of MoroccoGPCS Global Personal System for Mobile CommunicationsGSM Global System for Mobile CommunicationsIAM ItissalatAl-Maghrib (the incumbent telecommunications operator in Morocco)ICT Information and Communication TechnologiesIDA Interchange of Data between AdministrationsIDF Institutional Development FundIFC International Finance CorporationINPT Institut Nationai des Posies et TelhicommimicationsIIS Information Infrastructure SectorIISDL Information Infrastructure Sector Development LoanIMF International Monetary FundIPO Initial Public OfferingIT Information TechnologyMAD Moroccan DirhamsMSPP Ministere du Secteur Public et de la PrivatisationOED Operation Evaluation DepartmentONCF Office National des Chemins de FerONE Office National de l 'ElectriciteONPT Office National des Postes et Telecommunications

PA Public AdministrationPBAX Private Branche Automatic ExchangePHRD Policy and Human Resources DevelopmentPTO Public Telecommunications OperatorSEPTI Secretariat d'Etat Charge de la Poste et des Nouvelles Technologies de lI 'nformationTA Technical AssistanceTPI-SAL Telecommunications, Post and Information Technology Sector Adjustment LoanUNCITRAL United Nations Commission on International Trade LawUSAID United States Agency for International DevelopmentVAS Value-added ServicesVSAT Very Small Aperture TerminalWTO World Trade Organization

Vice President: Jean Louis SarbibCountry Director: Christian DelvoieSector Director: Emmanuel ForestierTask Team Leader: Clemencia Tonres

FOR OFFICIAL USE ONLY

KINGDOM OF MOROCCOINFORMATION INFRASTRUCTURE SECTOR

DEVELOPMENT LOAN

TABLE OF CONTENTS

Loan Summiary

I. INTRODUCTION 1

H. POLMCAL AND ECONOMIC CONTEXT 2

A Political Context 2B. Recent Economic Performance 2

C. Economic Outlook Fimcncing Requirements, and Risks 4

Ill. REFORM PROGRAM IN THE 1NFORMATION INFRASTRUCTURE SECTOR 5

A. Government's Strategy 5B. Poverty Impact of the Reforms in the Information Infrastructure Sector 6C. Progress to Date 6D. Reform Agenda 7E. BankStrategy 11

IV. THE PROPOSED LOAN 12

A Loan Rationale and Country Assistance Strategy 12B. Loan Objectives andActions to be taken prior to the Board 12

C. Technical Assistance 13D. Fiscal Impact of the Reforms 14E Disbursement andAuditing 14

. Cofinancing 15G. EnvironmentalAspects 15H. Social Aspects: Program Objectives and Poverty Category 15I Monitorable Indicators 15J Benefits andRisks 16

V. RECOMMENDATIONS 17

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not be otherwise disclosed withoutWorld Bank authorization.

KINDGOM OF MOROCCOINFORMATION UNFRASTRUCTURE SECTOR

DEVELOPMENT LOAN

TABLE OF CONTENTSANNEXES

Annex I Letter of Sector Development PolicyAnnex II Matrix of Policy Objectives And ActionsAnnex III Key Information Infrastructure Program Milestones (2000 - 2002)Annex IV Key Sector Data: Information Infrastructure Sector OverviewAnnex V Monitorable IndicatorsAnnex VI Fiscal Impact of the ReformsAnnex VII Timetable of Key Processing EventsAnnex VIII Status of Bank Group Operations in Morocco: Operations PortfolioAnnex IX Key Macroeconomic IndicatorsAnnex X Morocco at a GlanceAnnex XI Map of Morocco

TEXT FIGURES AND TABLES

Table ll.1. Morocco - Financing PlanTable 111.1. TPI-SAL IndicatorsTable IV. 1. Monitorable Indicators

This report is based on the work of missions to Morocco during July 1999 to March 2001. The mission teamcomprises: Clemencia Torres (Task Team Leader) (LCSFE, since October 2000); Pierre Guislain i(PSAEU),Paolo Zacchia, Karim El Aynaoui, Amine Khene (MNSED); Carlo Maria Rossotto, JUrgen Lohmeyer, IsabelleAndress, Catherine T. Doody (CITPO), Lorenzo Savorelli, Leila El-Hafi (MNSIF) and Bjorn Wellenius(consulant). Maude Jean-Baptiste (MNSIF) contributed to the editing of the document. Nicole Wautiez deBlaye translated the main document into French.

KINGDOM OF MOROCCOINFORMATION INFRASTRUCTURE SECTOR DEVELOPMENT

ADJUSTMENT LOAN

LOAN SUMMARY

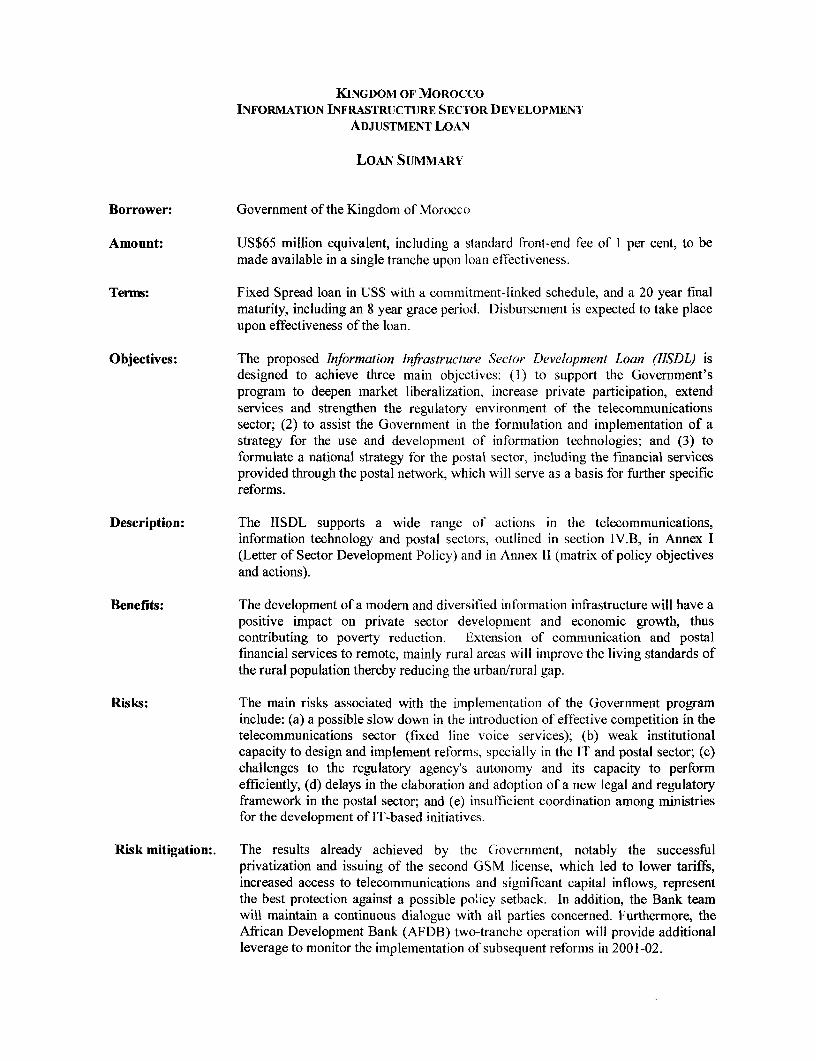

Borrower: Government of the Kingdom of Morocco

Amount: US$65 million equivalent, including a standard front-end fee of I per cent, to bemade available in a single tranche upon loan effectiveness.

Terms: Fixed Spread loan in US$ with a commitment-linked schedule, and a 20 year finalmaturity, including an 8 year grace period. Disbursement is expected to take placeupon effectiveness of the loan.

Objectives: The proposed Information Infrastructure Sector Development Loan (IISDL) isdesigned to achieve three main objectives: (1) to support the Government'sprogram to deepen market liberalization, increase private participation, extendservices and strengthen the regulatory environment of the telecommunicationssector; (2) to assist the Government in the formulation and implementation of astrategy for the use and development of information technologies; and (3) toformulate a national strategy for the postal sector, including the financial servicesprovided through the postal network, which will serve as a basis for further specificreforms.

Description: The IISDL supports a wide range of actions in the telecommunications,information technology and postal sectors, outlined in section IV.B, in Annex I(Letter of Sector Development Policy) and in Annex II (matrix of policy objectivesand actions).

Benefits: The development of a modern and diversified information infrastructure will have apositive impact on private sector development and economic growth, thuscontributing to poverty reduction. Extension of communication and postalfinancial services to remote, mainly rural areas will improve the living standards ofthe rural population thereby reducing the urban/rural gap.

Risks: The main risks associated with the implementation of the Government programinclude: (a) a possible slow down in the introduction of effective competition in thetelecommunications sector (fixed line voice services); (b) weak institutionalcapacity to design and implement reforms, specially in the IT and postal sector; (c)challenges to the regulatory agency's autonomy and its capacity to performefficiently, (d) delays in the elaboration and adoption of a new legal and regulatoryframework in the postal sector; and (e) insufficient coordination among ministriesfor the development of IT-based initiatives.

Risk mitigation:. The results already achieved by the Government, notably the successfulprivatization and issuing of the second GSM license, which led to lower tariffs,increased access to telecommunications and significant capital inflows, representthe best protection against a possible po!icy setback. In addition, the Bank teamwill maintain a continuous dialogue with all parties concerned. Furthermore, theAfrican Development Bank (AFDB) two-tranche operation will provide additionalleverage to monitor the implementation of subsequent reforms in 2001-02.

Poverty Category: The loan supports a program of targeted intervention aimed at facilitating theaccess of poor peri-urban and rural areas to a modern means of information andcommunication services, as well as to basic financial services provided through thepostal network.

ii

I. INTRODUCTION

1. Morocco is at the forefront of the liberalization reforms in the telecommunications, postal andinformation technology sectors in the MENA Region. The Government's program of market-orientedpolicies and regulatory capacity building in telecommunications has transformed the sector in less thanthree years. The introduction of competition in the mobile market was an unmitigated success. In asingle year, prices dropped four times, the number of mobile customers grew by over 2 million, capitalinflow surpassed US$1.3 billion and 20,000 new jobs were created. Private participation was introducedin several market segments as the competent independent regulator, Agence Nationale de Reglementationdes T6lecommunications (ANRT) awarded several licenses to VSAT and GMPCS operators. In 1999, theBank supported this program through the Telecommunications, Post and Information Technology SectorAdjustment Loan (TPI-SAL), now fully disbursed.] Building on these achievements, Morocco recentlyintroduced a second phase of reforms aimed at bringing the benefits of the information andcommunication revolution to a larger share of its population, in particular low income groups, and atestablishing the foundation for a knowledge-based economy. This program, supported by the proposedIISDL, includes three components: (a) further liberalization of the telecommunications market and theprivatization of the incumbent operator through a transparent and competitive tender; (b) theimplementation of a strategy for broadening the use and access of information technologies; and (c) theformulation of a national strategy for the postal sector, including postal financial services.

2. The IISDL was originally designed in 1999, jointly with the AFDB, as a US$100 million two-tranche operation. Balancing the Government request for further Bank support in a sector where itsperformance has been very good with the overall fiscal triggers of the base case program being advocatedby the new CAS was a delicate question. It was decided to restructure the operation as a one-trancheloan, to reduce its size, and to present it jointly with the CAS. This decision is predicated upon (i)Morocco's substantial sector achievements underpinned by a strong policy dialogue with the Bank; (ii)the new avenue for economic development that ICT offers in terms of growth, job creation and potentialto reduce exclusion by extending access to communication services to remote areas and low-incomegroups at an affordable cost; and (iii) the quality benchmark and demonstration effect that the reformprogram in the ICT sector has had throughout the MENA region and beyond. While the operation hasbeen redesigned as a single-tranche loan, it maintains its original purpose of supporting the reformprogram of the Government in the IIS, as defined in the Sector Development Policy Letter of May 2001(Annex II). The AFDB has maintained the two tranche structure and the original amount of its loan (US$100 million equivalent), with a first set of actions and policies identical to those supported by the IISDL,and a second tranche supporting actions and policies that are fully consistent with the overall Governmentreform program agreed with the Bank. Finally, the proposed operation will enable the Bank to continue adialogue in the area of ICT applications, notably in postal modernization, and E-Government which isexpected to lead to the preparation of follow-up operations, consistent with the new CAS.

i The US$10 Imillion TPI-SAL was approved by the Board on May 12, 1999 (Reort No P-7265-MOR and SeM2000-734).The second tranche of US$50 million was released on December 20,2000.

II. POLITICAL AND ECONOMIC CONTEXT

A. Political Context

3. Morocco's political context has undergone a phase of extraordinary opening during the past threeyears, with important potential effects on development policies. In September 1997, the Hlouse ofRepresentatives was elected by universal suffrage for the first time, as called for under the newConstitution of 1996. Following the elections, late King Hassan II appointed Abderrahmane Youssoufi,the leading opposition figure and a onetime exile, as Prime Minister in February 1998. Mr. Youssoufiheads a Government backed by a seven-party center-left coalition, the Koutla, which holds 102 of thelower chamber of parliament's 325 seats. This Government marks the first time in independentMorocco's 42-year history that the historical opposition has had the opportunity to govern. Following alimited reshuffle in September 2000, which inter alia brought a new secretary of state for p)ost andinformation technologies and saw the absorption of the privatization ministry into the ministry of finance,Mr. Youssoufi's Government is generally expected to remain in office until the next legislative cilectionsin 2002.

4. Political democratization and modernization have been gaining further momentum sinceMohammed VI's accession to the throne in July 1999. The new King has strongly stressed social,poverty, governance and gender issues in his speeches, as well as the need for 'a new concept ofauthority' based on the rule of law, and on a public administration supporting development rather thanmaintaining tight control on society. These are precisely the huge challenges the Government is f-acing inits pursuit of policies aiming at strengthening economic growth and fostering social development whilemaintaining a sound macroeconomic framework. In this context, foreign investment and the opening ofMorocco to information technologies will be crucial to a successful program of economic restruicturing,liberalization and trade opening that should lend to faster growth, that would in turn reduceunemployment, social disparities, and poverty.

5. The Government's general economic and social program combines: (i) commitment to maintain astable macroeconomic framework, and current policies that ensure a satisfactory degree of short-termmacroeconomic stability, (ii) reforms to improve public sector performance and promote administrativedecentralization; (iii) economic and social reforms that have achieved clear progress on access to basicsocial services, an acceleration of rural infrastructure development, and an active partnership of theGovernment with civil society; and (iv) measures to harness the potential for private-sector-ledl growthincluding the liberalization of the financial markets, reforms in the customs and tax administration,establishment of commercial courts, adoption of competition laws, and introduction of privateparticipation in many infrastructure sectors. The liberalization and privatization of thetelecommunications sector has brought a windfall of license and privatization revenues. The way theGovernment uses these resources will, to a great extent, determine its future prospects. The servicessectors, however, such as tourism and information technologies, are emerging strengths, showing greatpotential for diversifying Morocco's economic structure in the years ahead.

B. Recent Economic Performance

6. Starting in 1983, and triggered by external financing pressures, Morocco implemented a forcefuladjustment program that implemented deep structural reforms, cut the fiscal deficit, devalued the Dirham,and liberalized trade. Growth was driven by a very good performance of agriculture, and by adiversification of the country's exports, with a strong surge in manufacturing goods. Total exportsexpanded at an impressive 15 percent per year in dollar terms over the period This performance enabled

2

Morocco to make encouraging progress towards poverty reduction, with the poverty incidence decreasingfrom 21 to 13 percent of total population between 1984/85 and 1990/91.

7. But, whereas GDP grew at an annual average rate of 4.4 percent during the second half of the1980's, it dropped to well below 2% p.a. in the 1990's. This slower economic growth and the drought-induced rising volatility translated into decreasing private consumption, and in turn into an increase inpoverty, that soared to 19% of total population in 1998/99. While the slowdown in economic growth waspartly driven, directly or indirectly, by the situation in agriculture, non-agriculture GDP growth also sloweddown: the trend of non-agriculture GDP growth was roughly 3 percent in the 1990's.

8. Stabilization has remained a paramount objective of economic policy. It has been by and largesuccessful, and allowed Morocco to regain strong international credibility. As a result, in the 2nd half ofthe 1990s, Morocco has kept inflation under 3 percent p.a. and the current account deficit at around 1percent of GDP, and further reduced central Government external debt below 40 percent of GDP by theend of 2000. However, despite the pursuit of a prudent fiscal policy, fiscal management remains moreconstrained than suggested by the deficit figures that, until recently, remained in the range of about 3percent of GDP.2 Consequently, the underlying fiscal problems have started to surface, and havetranslated into much higher deficits in the 2000 and 2001 budget laws. In 2000 (annualized), the budgetdeficit is estimated to have reached a record level of 6.4 percent of GDP. Due to the delay in theprivatization of IAM Telecom, the debt creating deficit increased from less than 1 percent of GDP in1999/00 to 6.4 percent in 2000.

9. Structural reforms have continued to be implemented but with less momentum than in the late1980s. Private participation in infrastructure has been promoted much more forcefully and recently,privatization picked up remarkably with the partial sale of IAM. However, a recent private sector surveysuggests that administrative procedures remain the main constraint impeding business development. Theunfinished agenda of structural reforms remains in any case substantial. There remains an importantportfolio of public participation in 700-odd enterprises, and very large public groups or conglomerates.Trade liberalization has clearly lost pace since the turn of the 1990s, with protection typically remainingat 30-35% for one-third of non-agricultural imports. It was recently revived through the AssociationAgreement with the EU, now in force, and the conclusion of several international trade treaties with otherArab countries.

10. In the balance of payments, the current account deficit improved to 0.4 percent of GDP in 1998(from 1.7 percent in 1996), reflecting faster growth in phosphate and re-exports, and slower growth inimports. Despite slow exports growth and an acceleration of imports, the current account deficitremained well below 1 percent of GDP in 1999. Morocco's external position has remained sound in 2000,despite a significant deterioration in the trade balance mainly driven by unfavorable terms of tradedevelopments resulting from rising oil prices, subdued export performance, and the growing structuraleffect on imports of the tariff reduction under the partnership agreement with the EU. As a result, anddespite substantial tourism receipts and migrant transfers, the current account deficit is estimated to havegrown to 2.5% of GDP in 2000. In the meantime, external financing needs were eased by lower long-term debt amortization and the use of external reserves, which remain however at a conformable levelafter an all time high in 1999.

2The last two budgets relied heavily on one-time measures, such as exceptional 'dividends' imposed on public enterprises; lump sums paid byprivate enterprises as part of a tax amnesty scheme; and the sale of State assets. The INF has estimated the 'structural' deficit at 4.8 percent ofGDP for FYOO, and 5.5 per:ent for the curent fiscal year.

3

C. Economic Outlook, Financing Requirements, and Risks

11. Following the two consecutive years of drought, characterized by almost no grov,th, theMoroccan economy is expected to expand by 8 percent in 2001, mainly reflecting a rebound in agricultureproduction, a slight increase in non-agriculture GDP and strong recovery in key services sectors, such astourism. Non agricultural GDP is foreseen to increase moderately from 3.5 percent in 1999, to 3.9percent, mainly reflecting the impact of the fiscal impulse and the 5 percent adjustment of the exchangerate. At the sector level, the expansion rebound in the tourism, communication, and construction sectorsis expected to continue. The current account deficit, fuelled to 1.6 percent of GDP in 2000 by the (irought,higher oil prices, and subdued export performance, would remain at this level in 2001, mainly clue to ahigher fiscal deficit.

12. The 2001 budget law plans a deficit of 8.4 percent of GDP. However, thanks to the privatizationof IAM, for an amount of DH23.3 billions, or 5.4% of GDP, non-debt creating deficit should be set at 3percent. While the debt-creating fiscal deficit remains manageable, and despite a track record of strictbudgetary execution in the last three years, the new budget confirmed the serious deterioration- in thestructure of public expenditures started in 2000: it results in a very low level of government savings thatcould, in the medium-term, represent a threat to fiscal sustainability.

13. In the medium term, it is projected that, barring any significant modification of the macroframework, trend GDP growth would not increase much, and average around 3.5 percent from 2002 tom2004. A detailed account of medium-term prospects is provided in the 2001 CAS document.

14. Risks. The reliance on exceptional revenues (exceptional tax amnesty in 1998/99, GSM licensereceipts in 1999/2000, privatization of IAM in 2001) to finance increased deficits is not sustainable in themedium term. On the macroeconomic side, the situation should remain manageable in 2001. However,with this fiscal policy, the country's exposition to exogenous shocks, such as further increases in oilprices, a surge in international interest rates, is higher. In the medium term, a pursuit of the current policycould lead to instability by stimulating inflation, eroding further the external competitiveness and lead toan increased current account deficit.

15. Major exogenous risks on Morocco's growth performance and external position include: (i)vulnerability to consecutive severe droughts and related volatility of output; (ii) contingent liabilities; and(iii) external shocks, such as a hike in international interest rates, fast deterioration of terms of trade, andan important dependency on EU economic performances. Also, the fact that the Hassan II Fund is nowentitled to receive half of all privatization receipts constitutes an important reduction in the margin ofmaneuver of the fiscal policy, and a potential source of higher expenditures with weak Parliament control.On the whole, the Government has the capacity to ensure base line fiscal sustainability but it would bedamageable if the adjustment is again realized by cutting drastically public investment.

16. Financing requirements and Bank support. The current account deficit is predicted to improveslightly from its projected 2001 level, -1.5 percent of GDP, to around -1 percent in the medium term.Tourism receipts would be sustained and workers remittances would grow moderately. The currentaccount deficit would remain manageable thanks to substantial net foreign capital inflows - around 2percent of GDP p.a. - resulting from privatization operations and foreign direct investment. In addition,important concessional funding from the EU is expected as the MEDA program is projected to improveits disbursement ratios. Morocco's financing needs would also be driven by external debt repaymentsincreasing from around US$2 billion to US$2.8 billion between 2000 and 2003, especially as rescheduledLondon Club private debt comes on stream in the next few years. Total external debt outstanding wouldas a result decrease further by 2003 to reach 46 percent of GDP. In the context of the CAS, the

4

Government and the Bank have drafted a medium term financing plan which projects IBRD commitmentsof the order of 250m US$ per year in the base case.

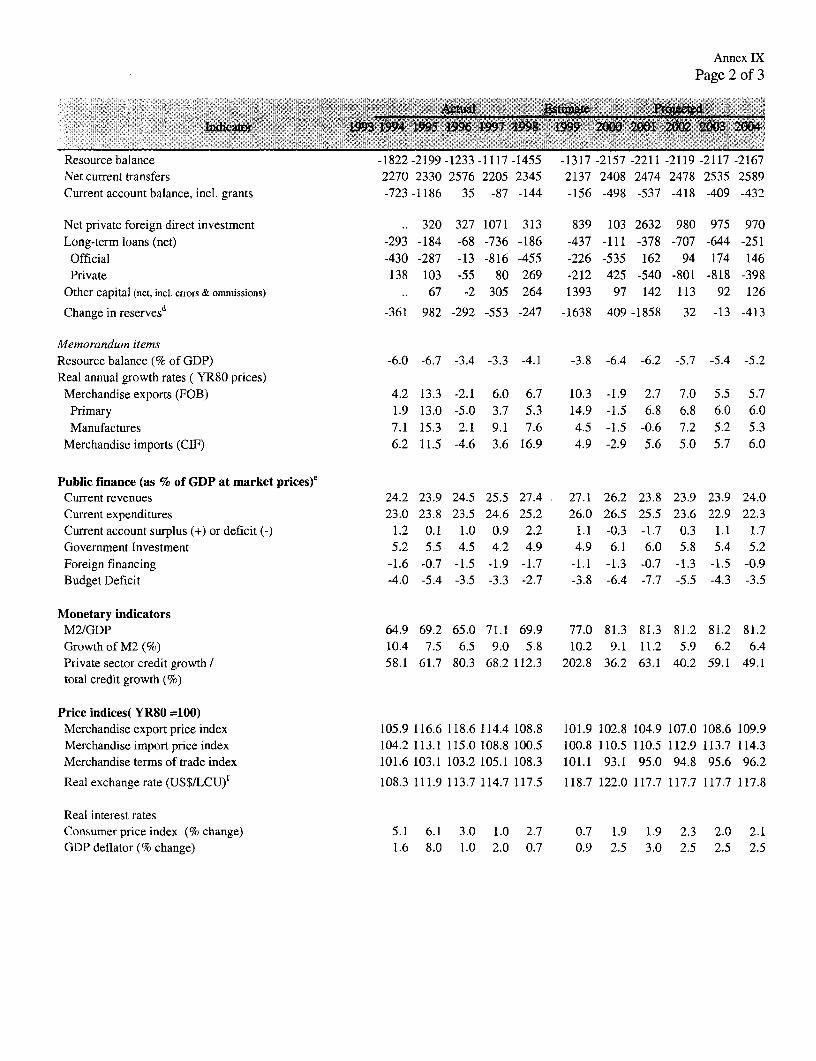

Table 11.1: Morocco - Financing Plan (Mln US$)

:~ ~~~~~~~~~ _

Financing Requirement 2263 2763 2152 3766 2552 4937 2866 3129 3284

Current Account (excl. grants) 35 -87 -144 -156 -548 -537 418 -409 432Debt Servicea 3352 3190 2782 3047 3534 3614 3496 3656 3344Amortization 2006 2123 1761 1971 2413 2541 2480 2706 2440Interest 1346 1068 1021 1076 1121 1073 1016 949 905

Reserve Build_Upb 292 553 247 1638 -409 1858 -32 13 413

Financing Sources 2263 2763 2152 3766 2552 4937 2866 3129 3284

FDI and Portfolio Capital 469 1108 337 846 113 2647 1000 1000 1000Medium and Long Term Loans 1757 1313 1586 2541 2290 2199 1766 2057 2178a. Multilateral 797 568 641 781 594 776 717 738 789b. Bilateral 532 283 214 243 575 558 497 552 493c. Private Guaranteed 337 187 393 432 892 595 437 547 501d. Private Non-Guaranteed 91 275 338 1085 230 270 115 220 395

Official Capital Grants 0 0 0 0 50 0 0 0 0Other Capitalc 38 342 228 380 99 91 100 73 106

a. Includes IMF interest paymentsb. Includes IMF credit purchases and repurchasesc. Mostly net short term capital, changes in assets holdings of commercial banks and private citizens

III. REFORM PROGRAM IN THE INFORMATION INFRASTRUCTURE SECTOR

A. Government's Strategy

17. Developing a high-performance information infrastructure sector (IIS) is a centerpiece of theGovernment's economic and social agenda. A modern IIS will make a major contribution to acceleratingeconomic growth and reducing social disparities. It will enhance the competitiveness of Moroccanenterprises, bring them closer to international markets, and facilitate the integration of the country in aglobal information-based economy. A modern and extended IIS will also bring additional benefits to thesociety as a whole through a more efficient provision of social services like education and health andthrough the modernization of the public administration. Additionally, the modernization of the postalsector will lead to a more efficient provision of some basic financial services, taking advantage of anextended postal network that reaches many marginal and remote areas without access to other forms ofbanking services.

18. The Government has adopted an integrated approach to telecommunications, postal and ITreforms. Such a comprehensive approach is necessary, as the convergence of technologies used by thethree sectors is increasingly blurring traditional boundaries among them, and businesses often demandintegrated solutions to their communication, information and delivery needs. As detailed below, the sharp

5

decline in the cost of these technologies represents not only an opportunity for accelerated growth and jobcreation but also for reaching out to lower income populations in remote areas and extendingcommunication services at an affordable cost. In sum, in terms of creating opportunities, reducing thecost of exclusion borne by the poor and improving access to government and public services, ICT offers awhole new avenue for economic development with particular relevance to the poor.

B. Poverty Impact of the Reforms in the Information Infrastructure Sector

19. Growth and job creation. IIS reforms are expected to foster growth and employment creation, akey contribution to poverty reduction. As an example, with the introduction of competition in the m-nobilemarket, the total of IAM's GSM subscribers jump from 116,600 in 1998 to over 2.4 million by endDecember 2000. There has been around 6,200 new direct and indirect jobs created since 2000 in thetelecommunications sector.3

20. Development of sustainable business opportwities in remote areas, through increased access tocommunication, information and delivery services. IIS reforms facilitate the extension of telecommun.icationand postal services to the poor, especially in rural areas. The liberalization of all segments of thetelecommunications market can also lower the cost of doing business in remote areas. This, in turnfacilitates information and retail opportunities for farmers and artisans in more remote areas. The VirtualSouk, launched in 1998 as a collaborative effort between the World Bank Institute and local commnunityassociations in various MENA countries, is an example of the potential that the internet offers to smallbusinesses and micro entrepreneurs from isolated areas. 4

21. Contribution to other sectors of the economy. The Government intends to promote the sectoralapplications of ICT. Expanding the use of computers in schools through a country wide program is apriority outlined in the Government's strategy for the development of the IT sector. The Government willpromote the provision of basic financial services to populations without access to any other b;mkingservices, taking advantage of an extended postal network that reaches many poor urban and ruraml areasthroughout the country.

C. Progress to Date

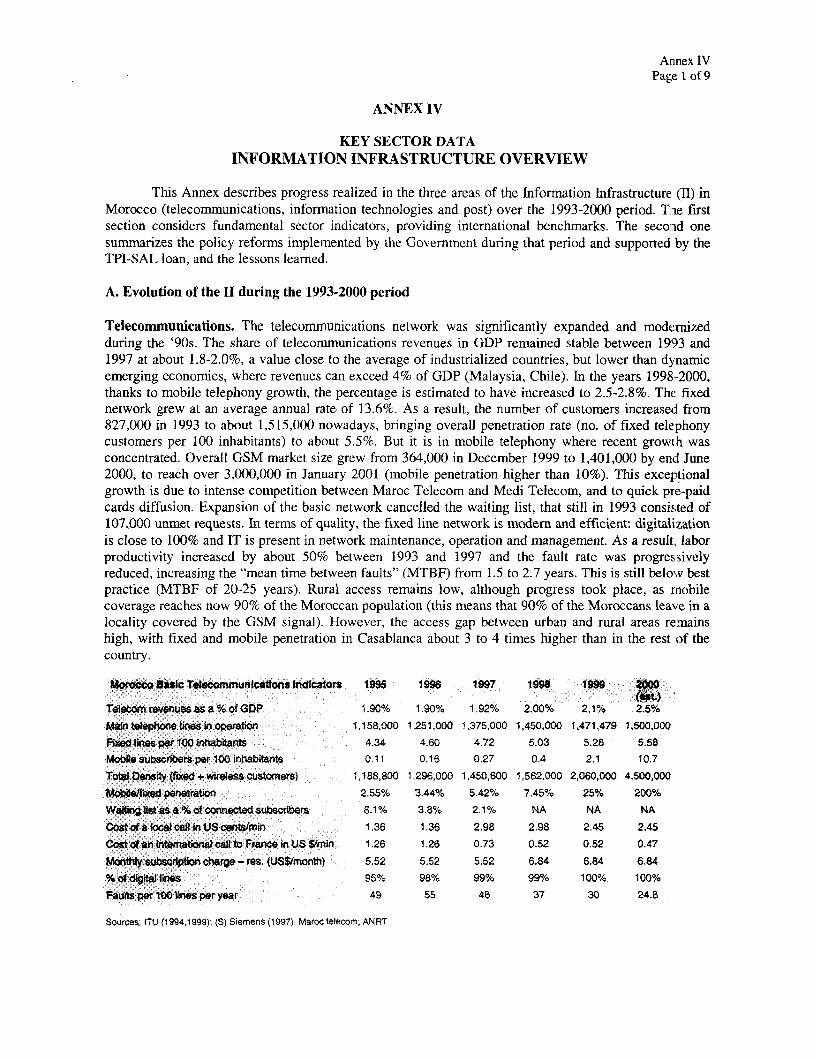

22. Telecommunications, information technologies and postal activities are emerging as a modernand vibrant sector of the Moroccan economy. A description of the sectors' performance and of the mostrecent developments is presented in Annex IV. In 1999-2000, the Government implemented an ambitiousreform program supported by the Bank with the TPI-SAL. This program focused on (i) fosteringcompetition in the telecommunication sector; (ii) establishing the legal and regulatory foundation ofcompetitive telecommunication markets; and (iii) laying groundwork for development of the informationtechnology (IT) and postal sectors. As shown below in Table 111. 1, most of the indicators agreed at thetime of TPI-SAL have been met. The Government, and in particular ANRT, have been widely praised forthe openness and transparency of the bidding process for the second GSM license. These were importantfactors in explaining the success of introducing competition in wireless as shown by the price of the

3 Medi Telecom, the operator of the second GSM license began operations on March 29, 2000 employing 2:30 andgenerating indirect employment for about 2000 people. Atento, a subsidiary of Telefonica de Espana, has openedtheir first call center in Casablanca which is expected to generate over 4000 direct and indirect jobs by the end of theyear 2001.

4 This intemet site gives poor artisans, often illiterate women, of Morocco, Tunisia, Lebanon and Egypt, the oppornity to showand sell their handicrafts on the Web ( http://www.elsouk.comi/elsouk.htm).

6

license - US$ 1.1 billion and by the unprecedented subscriber growth that followed competition.5 As aresult of the Government' sound performance, the second tranche of TPI-SAL was disbursed inDecember, 2000.

Table 111.1 TPI-SAL Indicators

Indicator Measure 1998 1999 2000Actual Planned Actual Planned Actual

Market share of Revenue Share (%/o) 0 10 0 22 30the new operator inthe cellular marketNumber of fixed Number of lines 690 747 860 804 906lines outside 2 (000)main cities _ _

Fault Rate No. of faults per 100 lines 42 35 37 30 24.5per year

Suppliers of No. of suppliers of leased I At least 3 1 At least 4 4Leased Lines lines

D. Reform Agenda

23. In a second phase of its reform program, which the proposed IISD loan supports, the Governmentintends to: (i) deepen the pro-competitive reforms, including privatization, in the telecommunicationssector; (ii) bring the benefits of the information and communications revolution to lower income groups,in particular in rural areas, by redefining its universal service policies in both the telecommunications andpostal sectors; and (iii) establish the legal foundation of an information society. The Government hasspelled out its reform agenda with respect to telecommunications, post and IT in its Letter of SectorDevelopment Policy (Annex I). The main components of this program are detailed below.

1. Telecommunications

24. Privatization of Itissalat Al Maghrib (Maroc Telecom) As part of its overall sectorliberalization program, the Government decided to transfer 35 per cent of the capital, as well as a majorityon the management board (directoire), of historical operator Itissalat Al Maghrib (IAM) to a strategicprivate investor, following an international competitive bidding process. The arrival of the strategicpartner in February 2001 provides IAM with the financial and managerial resources needed to faceincreasing competition in its domestic market and to expand in other markets. 6 IAM's regional ambitionshave been expressed through its recent acquisition of a majority stake in Mauritel, the Mauritanianincumbent operator.

5 See Wellenius B. and Rossotto C-M.: "Introducing Telecommunications Competition through a Wireless License: Lessonsfrom Morocco" ViewPoint N. 199, November 1999. The World Bank Group, Wasing D.C.

6 After an expression of interest phase lastng about 6 months, the formal tender was launched in October 2000 with a biddingdeadline of December 20, 2000. The Govemment had set a minimum price of 20 billion DH . Vivendi Universal, the buyer,paid 15% above this price, or US$2.1 billion. Financial closure took place on February 20, 2001. The strategic partner controlsthe management board, and the government the supervisory board All major decisions require agreement of both.

7

25. Following the strategic sale, the Government will continue to lower its ownership in IAM. Inconsultation with the strategic investor, it will offer shares to IAM's employees and retirees. In addition,to favor wider spread ownership and to attract additional capital, the Government intends to sell anadditional 15% to 20% of IAM's capital through an initial public offering (IPO). The IPO will probablybe launched in 2002, depending on market conditions, on the Casablanca stock market and on aninternational exchange.

26. Deepening competition in telecommunications infrastructure and services. The Governmenthas adopted a timetable to grant new licenses for networks and services to accelerate liberalization. Thenew licenses will include fixed telephony licenses (local access licenses especially in large metropolitanareas, as well as a second national license) to be launched in 2001. In a first phase (up to end-2002), thenew fixed license-holders would not be allowed to provide public telephony services (i.e. public voice toend customers), but would provide data, Internet, leased lines, private network and other services. Thelicensees will be required to deploy broadband networks enabling fast Internet access and multimediaapplications, which should set the stage for a major growth in the use and application of these newtechnologies. From January 2003 on, the prohibition of these new operators to provide voice serv ices toend-users would terminate and they would thus become full-fledged competitors to L&M in theirrespective market segments. Additionally, starting January 1, 2002, the second GSM operator will launchan international services for its own customers, introducing competition in this segment for the first time.This trend will be reinforced with the award of additional international licenses in 2002.

27. To promote the introduction of competition, the Government is taking measures (includinglegislative) to facilitate the use of "alternative infrastructures": other utility and transport companies (suchas the power, water, railways or highways companies and authorities) will in this way be encouraged tomake their networks and rights of way available to new telecommunications operators, hence reducing thecost and lead time needed for infrastructure roll-out.

28. Extending access to telecommunication services in poor and rural areas: The Governmenthas set objectives to increase rural teledensity from 0.6% in 2000 to 7% in 2012, and to have at least onepayphone per 250 inhabitants by 2005. Additionally, the Government will present to Parliament a draftlaw to expand the definition of universal service to include telecommunications and information servicesin general, rather than telephony only. The Government considers that telecommunications liberalizationis the most effective tool to achieve increased access to services. The award of the second GSM licensedemonstrates the effectiveness of this approach. In two years, due to rapid expansion of the GSMnetwork, the percentage of the population without access to telephone service has decreased from; about25% to 10%.

29. The Government expects that competition among private operators will achieve most of itsuniversal access objectives. Nonetheless, some gaps will remain and to address these GOM has taken thefollowing steps. First, prior to privatization, IAM's license conditions were modified to includeobligations to maintain existing services in all covered areas and to extend services to 700 additional ruralvillages. In return, IAM is temporarily exempted from the levy on turnover which other licensedoperators have to pay. From 2003, IAM may also seek authorization from ANRT to end rural pavphoneservices and subject these to the prevailing rules for universal service support. Second, a decree is beingdrafted defining a new universal service regime, under which operators will contribute initially 4% ofturnover to a universal service fund. This percentage is set to decline over time, as access to servicesreaches Government targets. This fund will be used to provide limited investment subsidies to com panies(including IAM if interested) bidding for universal service licenses.

30. Strengthening the telecommunications legal and regulatory environment. ANRT has been apioneer in Morocco (and the region) in making extensive use of the Internet and meetings to consult with

8

industry and other parties and to disclose its policies and decisions. ANRT is committed to expand thisconsultation process and adopt more systematic procedures for public consultations and records onimportant decisions of the Agency. New staff rules were adopted by ANRT in 2000, strengthening theability of the agency to hire and retain qualified staff and providing a code of ethics. Parliament is in theprocess of approving a proposed amendment to the telecommunications law (Law 24-96) that wouldremove the a priori financial controls on ANRT and replace them with a posteriori controls. Moreover,the Government intends to submit to Parliament additional amendments in order to strengthen ANRT'spowers and effectiveness in dealing with operators. Under the proposed amendments, ANRT would beable to impose a wide range of sanctions (including financial penalties) for non-compliance, in addition tosuspension of the license.

31. To strengthen the financial autonomy and accountability of ANRT, the Government intends toreview by March 2002 the sources of funding of the agency and adjust regulatory fees to bring them morein line with the cost of regulation. The financial review of ANRT will be preceded by an evaluation ofthe economic value of the spectrum, as well as an assessment of the appropriate mechanism for spectrumallocation, the level of spectrum fees and the distribution of revenues between spectrum management andregulation fees accruing to ANRT, and spectrum scarcity fees accruing to the Treasury.

2. Information Technology

32. The Government's Program in Information Technology development is focused on three mainareas: (1) development of an enabling environment for information and communications based industries,including electronic commerce; (2) establishment of inter-administration networks; and (3) promotion ofICT applications.

33. Development of an enabling environment for information and communication basedindustries, including electronic commerce. The Government program of reforms in this area addressestwo critical factors of a dynamic IT sector: an adequate legal and regulatory framework for e-commerce,and a low cost and modern broadband information and communications network. To this end, an inter-agency commission7, created in June 1999 has prepared a draft Law on data transmission, whichaddresses various issues, including the recognition of electronic signature, and incorporates the principlesof the UNCITRAL Model Law in the areas of electronic commerce. Further activities in this area includethe elaboration of other draft laws addressing, inter alia, certification of electronic transactions,cryptography, privacy, technology neutrality, and consumer protection in the field of electronic media.These additional legal initiatives will complement and integrate the draft Law on data transmission andconstitute a coherent and reliable legal framework for electronic commerce in Morocco.

34. Establish inter-administration networks. A second key area of the IT Strategy for Morocco, isthe introduction of IT to reform and modernize the Moroccan public administration. The importance ofimproving the performance of the Public Administration is reflected in the National Strategy for the ITsector, which includes the implementation of the administration on line initiative (AoL) as one of thepriority areas for policy actions in the sector. The AoL initiative aims to gradually develop a government-wide information system, connect different ministries at central and local level, and establish commoninteroperable procedures. This is expected to streamline administrative procedures, reduce the cost of thepublic administration and benefit citizens and enterprises. In addition, this infrastructure will allow the

7 This iter-agency commisson, involves SEPTJ, ANRT, Mnistner du Comierce et de l'hndustrie, Minist6re des Finances (inparticular, Customs), MNnistere de la Justice, Ministre des Transjrts, BAM and private banks.

9

development of e-government applications and improve services to the public. In terms of implem,ntationof the AoL initiative, the Government has: (a) started to identify key administrative procedures wh ich willmost benefit from the implementation of the AoL initiative; and (b) developed a legal framework for theofficial recognition of administrative documents in electronic fornat. The next step of the iritiative,expected in November-December 2001, will be the launching of a pilot project focused on the IntegratedManagement of the Government's Human Resources (Gestion Integee du Personnel de l'Etat - GIl'E).

35. Promote the development of ICT-related applications through public-private partnerships.As a first step in developing high-end ICT applications, the Government has created a cyber park nearCasablanca and is planning a second park in Bouznika. The parks will host incubators for new ICTenterprises and SMEs. An info)Dex grant is funding a feasibility analysis for the creation of theseincubators. Second, the Government has also signed a contract with two enterprises to dev-.lop e-commerce portals for the benefit of economic co-operatives (groups of local artisans, craftsman, ilrmers,etc.). These electronic portals are ready, certified and in operation as of April 2001. To promote their useamong cooperatives, the Government has launched a program of ICT-education for cooperative managersand a communications campaign to increase awareness, amongst cooperatives, of the benefits of using e-commerce. Additionally, as part as its long term development strategy for the ICT sector, the Governmentalso intends to promote the developmnent of community-based telecenters, including the provision ofinternet access.

3. Postal Sector

36. Elaboration of a development strategy. The objectives of the Government are fourfold: (I) toprovide a postal universal service in line with international standards; (2) to gradually open the postalservice to competition and increased private participation; (3) to strengthen the historical postal operator,notably through its corporatization, as a credible competitor in a liberalized environment; and (4) toincrease rural savings mobilization and to allow greater management autonomy of the postal financialservices. As in telecommunicationis, a central goal of the strategy is to ensure the provision of adequateand affordable postal and financial services provided through the postal network, in poor urban and ruralareas. SEPTI has several studies underway which will provide the basis for the design of a nationalstrategy for the development of the postal sector, including proposals on universal service and marketliberalization.

37. Modernizing the main postal operator. To remain competitive in a market-orientedenvironment which includes universal service obligations, the postal operator has completed, mxith theassistance of external consultants, an action plan for business development and internal restructuring.Increased use of telecommunication services and IT applications play a critical role in this plan toenhance the internal efficiency ( infor.m-ation systems) and to improve the quality of postal services (value-added services).

38. Developing the financial services provided through the postal network. The Ministry ofFinance will launch a study, in collaboration with BAM and SEPTI, to identify actions aimed at (1)ensuring the access to financial instruments for a broader range of consumers, without undue distortionsto fair competition with the banking and financial system; (2) allowing the historical postal operator todiversify its revenue sources ir, a context of postal sector liberalization, and (3) increasing savingsmobilization and improving the allocation of resources towards productive activities.

10

E. Bank Group Strategy

39. Current Involvement. The Bank has been involved in Morocco's telecommunications sectorsince the 1980s, initially through two investment projects, which focussed on the development of thenetwork and the strengthening of the historical operator. Both operations were implemented successfully.The first was rated satisfactory by OED and the second highly satisfactory. 8

40. From 1993 to 1998, the Bank focussed on assisting the Government in developing a soundinstitutional and legal framework for opening the telecommunications sector to broad competition. Themain instruments used included: (a) the implementation of the 1993 Telecommunications SectorRestructuring Project; (b) several pieces of economic and sector work presentation;9 (c) the award of anIDF grant for the preparation of telecommunications privatization; and (d) the implementation of the 1999TPI-SAL. Since 1999, the Bank has supported the implementation of the Government program ofreforms in the sector through the TPI-SAL (paragraph 22) and the IISDL (paragraph 23).

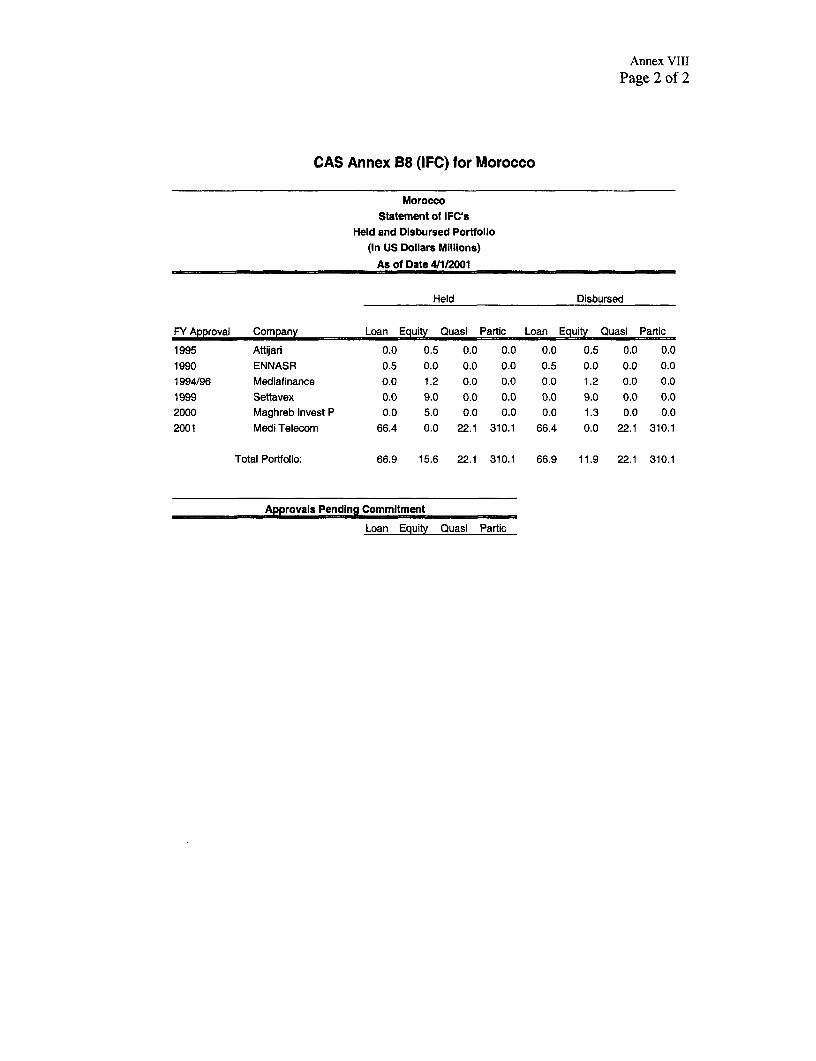

41. In 2000, the IFC played a critical role helping MediTelecom, the winning consortium for thesecond GSM license, put together a long term financing package, given the limited availability in thecapital markets of sufficient financing with the necessary terms and long term tenor and withoutmultilateral involvement. The total cost of the project was Euro $ 1.1 billion, and the value of the IFCpackage was Euro $450 million, of which 75 million in Loans A, 25 million in Loans C and 350 millionin Loans B. As in the case of the second GSM, the use of IFC's instruments to support operatorsinterested in bidding for the new licenses could also contribute to foster private participation in the sector.The same is true for the development of IT-related industries, or in joint private-public ventures in thepostal sector, where IFC could consider contributing to the funding of the investments.

42. Future involvement. The Government has identified the following priorities for the IT sector:(i) enhance the business and competitive environment for firms in the ICT sector; (ii) develop technologyparks; and (iii) implement the "Administration on Line initiative". Building on past achievements, someof these initiatives could be supported by the Bank Group.

43. In the postal sector, the SEPTI expressed interest in continuing collaboration with the Bank toimplement the strategy to be agreed following the completion of the on-going study. BAM has as wellexpressed interest in an investment project focused on IT development and universal access. Moreprecisely, BAM intends to develop an e-commerce platform including: on-line tariffs, secured payments,third party certification, an efficient logistical network through which parcels would be delivered andinvestments in the rural areas.

44. Coordination with development partners. The Bank prepared the IISDL jointly with theAfrican Development Bank, continuing the collaboration initiated with the TPI-SAL. The AFDBoperation, which was approved on April 4, 2001, includes a second tranche which will provide additionalleverage to monitor the impact of the reforms supported by the one-tranche IISDL and theimplementation of additional reforms in 2001-02. Special efforts have been made to coordinate thepreparation of the proposed loan with the European Commission, as there are strong complementaritiesbetween the EC's ongoing technical assistance to ANRT and several of the policy actions supported in the

See OED Evaluative Memrandum L2798-MOR (1995) and OED Evaluation Summary L3557-MOR (1998).9 Kingdom of Morocco, Preparinfor the 21st Cenzey - S&egtlinZgthe Private Sector in Morocco, Report 11894-MOR, World Bank June1994; Royawne du Maroc, Participation d secteur prive dans les infrastructures, Eh4cks &conomiques & la Banque mondiale sur le MoyenOrient et I'Afrique du Nord World Bang 1997; Kingdom of Morocco, Private Sector Assessment Update, Fudflling the Promise of PrivateSector-led Growh Report 17950-MOR, World Bank, December 1999.

11

proposed loan to strengthen the regulatory environment in the telecommunication sector (See sectionIVC). The Japanese authorities approved a PHRD grant which was used for preparation of the operation.Finally, the proposed IISDL also converges with the program that USAID has launched in Morocco forthe development of e-commerce.

IV. THE PROPOSED LOAN

A. Loan Rationale and Country Assistance Strategy

45. The present one-tranche operation is at the juncture of the 1997 and 2001 CAS. The suistaineddialogue during the preparation of the operation supported the complex process that led to the recentprivatization of the main operator, and related reforms. This is fully part of the 1997 CAS (R97-2 Boarddiscussion date January 30, 1997) that sought enhanced private sector participation in infrastructure, andbroader private sector development. On the other hand, by setting the stage for downstream and retaildevelopment of IT-based services, the reforms set forth in the operation will provide the necessaryunderpinning to the 2001 CAS objectives of supporting a decentralized and participatory approach tofight poverty and exclusion. In particular, this operation would lead towards improving the livingstandards of rural populations by expanding access to a broad range of information infrastructure services.Although concerns over fiscal management have led to link Bank policy based lending to,) strictmacroeconomic triggers under the 2001 CAS, the present operation is justified by the strong track recordand excellent dialogue in the sector, and by the possibility of Bank Group follow-up investmentoperations. Morocco's macro economic framework also remains stable and financing requirementsremain important (paragraph 46). The 2001 CAS recognizes the development of IT based-services as oneof the main business lines of Bank support over the next three years, and both the Bank and IFC plan tosupport investment operations in the sector, which can have an important cross-sectoral impact fordecentralized economic opportunities, diffusion of basic services, employment and growth.

46. The macroeconomic rationale for a quick disbursing loan operation follows from the overallfinancing plan of Morocco's balance of payments as presented in section II.C. With limited access tointernational capital markets, Morocco relies on both bilateral and multilateral donors to ensure a stablefinancing of its external requirements. This is important, as Morocco's external position is still vulnerableto shocks originating from changes in oil and phosphates prices, and from changes in market conditionsfor emerging countries. In this respect, allowing Morocco's international reserves to remain above 5months of imports, while continuing to reduce external debt, is a positive trend that the loan wouldsupport.

B. Loan Objectives and Actions to be taken prior to the Board

47. The overall objective of this proposed single-tranche US$65 million IISDL is to support theGovernment's new phase of reforms in the IIS. As detailed in Part III, this program has three maincomponents: (i) deepen market liberalization, increase private participation, extend services andstrengthen the regulatory environment of the telecommunications sector; (ii) formulate and implement anambitious strategy for the development of IT; and (iii) formulate a national strategy for the postal sector.The Government is showing a strong public commitment to this reform program and has agreed to widelydisseminate its reform program for the development of the Information Infrastructure Sector.

12

48. Prior to the Board, the Govermnent has carried out a series of actions summarized below andpresented in further detail in Annex I.

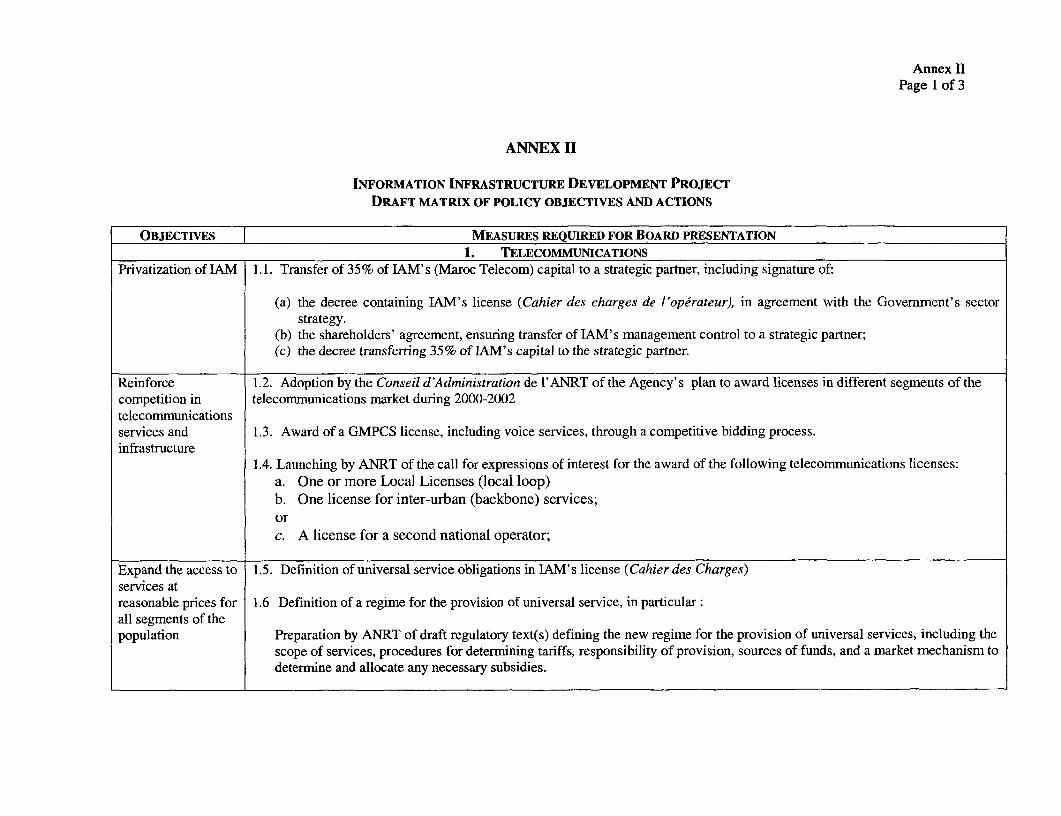

In the telecommunications sector:* Transfer of 35% of IAM's capital to a strategic partner, including signature of: the decree

containing IAM's license (Cahier des charges de l'operateur), reflecting the Government'ssector strategy; the shareholders' agreement, ensuring transfer of IAM's management control toa strategic partner; and the decree transferring 35% of IAM's capital to a strategic partner.

* Definition of universal service obligations included in IAM's license (Cahier des Charges)* Adoption by the Conseil dA'dministration de l'ANRT of the Agency's plan to award licenses

in different segments of the telecommunications market during 2000-2002* Award of a GMPCS license, including voice services, through a competitive bidding process.* Preparation by ANRT of a draft decree defining the new regime for the provision of universal

services.* Adoption by ANRT's Board and effective implementation of a new Statute of Personnel,

including a professional ethics code.* Adoption by the Council of Government of an amendment to Law 24-96, replacing a priori by a

posteriori financial control of ANRT.

In the information technology sector:* Elaboration by the Inter-ministerial Committee on Electronic Commerce of a draft Law on data

transmission, including principles on recognition of electronic signature and its certification.

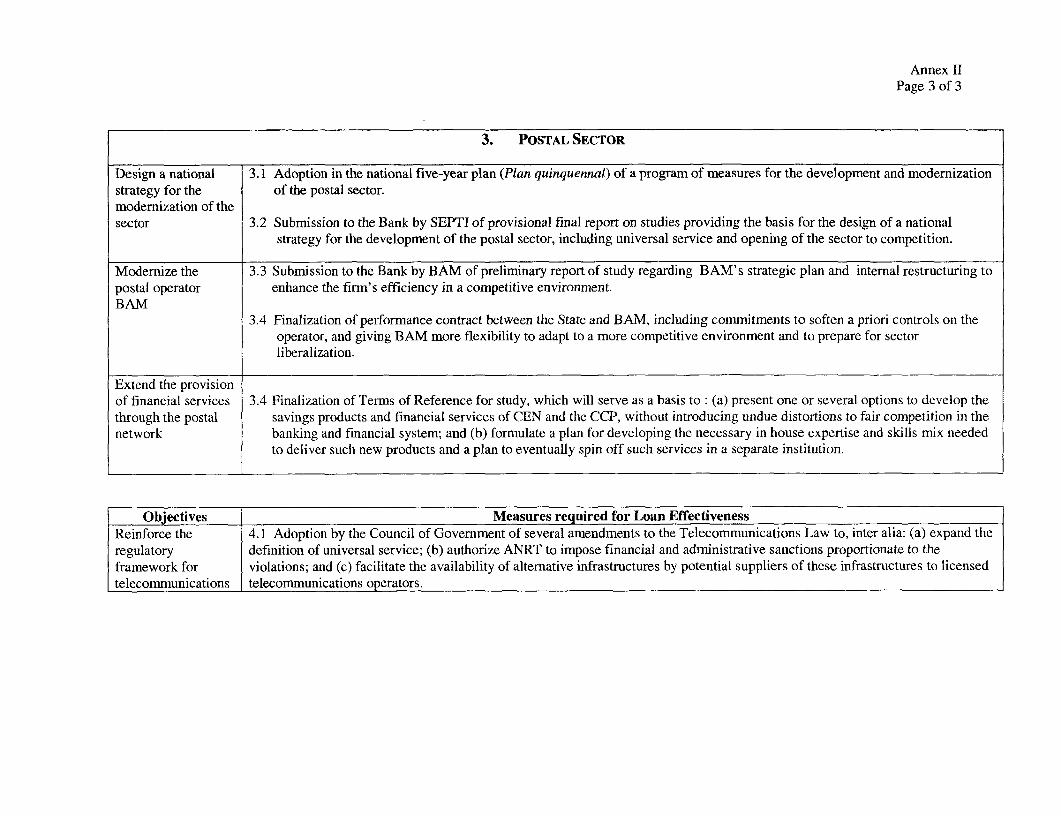

In the Postal Sector:* Preparation by SEPTI of a national strategy for the development of the postal sector in

consultation with the Bank.a Finalization of the terms of reference by an inter-agency committee (headed by the Treasury in

collaboration with BAM and SEPTI) for a study to present several scenarios for thedevelopment of postal financial services.

49. Prior to the effectiveness of the loan, the Government will have undertaken the following action:

Adoption by the Council of Government of several amendments to the TelecommunicationsLaw to, inter alia: (a) broaden the definition of universal service; (b) authorize ANRT toimpose financial and administrative sanctions proportionate to the violations; and (c)facilitate the availability of alternative infrastructures to potential suppliers of theseinfrastructures and to telecommunications operators.

C. Technical Assistance

50. Various technical assistance initiatives are currently underway or will be launched shortly tofacilitate the implementation of the above reforms and ensure their sustainability. They include:

* Assistance of an external consultant to ANRT to define a position on competition policy that has beenreflected in LAM's license. (funded by ANRT).

* Launching oftwo studies on international experience regarding the impact of accelerated liberalization onthe fiscal flows to the Treasury and on the progress towards universal service. (Funded by PPLAF)

* Long-term (2001-2004) assistance to ANRT by the EU, to be launched in September 2001.* Study on new universal service regime for ANRT on own fnancing, completed in Febraty 2001.* Assistance to ANRT on design and launch of new licenses, started in February 2001 on own financing.

13

* Assistance of an external legal expert to the inter-ministerial commission led by SEPTI, to draft the Lawon data transmission (funded by Belgian and Danish CTFs).

* Assistance to the SEPTI to develop an action plan for implementation of its national strategy on theinformation society (funded by PHRD grant).

* Assistance to the SEPTI for the elaboration of a postal sector strategy, including postal financial sevices.

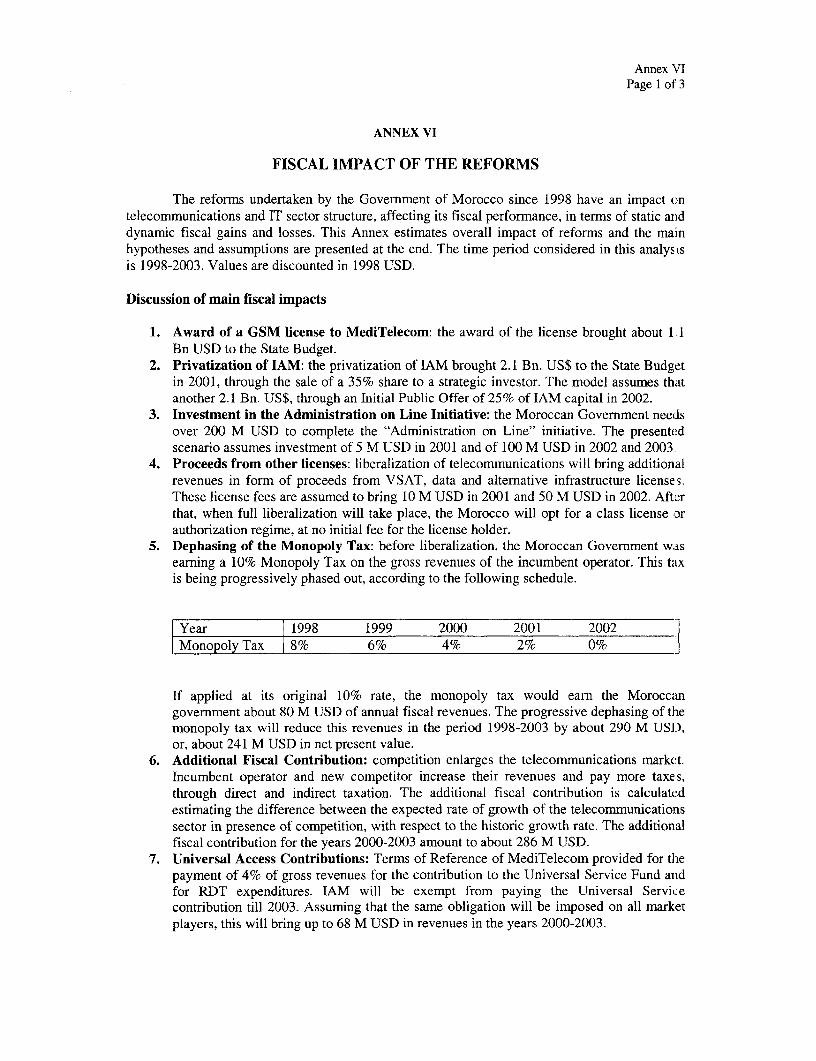

D. Fiscal Impact of the Reforms

51. The net fiscal impact of the reforms is expected to be largely positive, as the revenues :rrom apartial sale of IAM are substantial, and additional tax revenues will be paid by new competitors erteringthe liberalized market. (See Annex VI). A fiscal cost can be expected in the short run due to: (i) phasingout of the monopoly tax for telecommunications services; (ii) transaction costs of privatizing IAM, and(iii) investment needed for the establishment of inter-administration networks (Administration on lineinitiative). These costs will be more than compensated by the privatization proceeds of IAM, and in themedium term by: (i) higher tax revenues, both from IAM and from new operators, due to overall mnarketenlargement; (ii) contribution from all licensed telecommunication operators of 5 percent of re,enues(decreasing over time) to fund universal service and R&D; and (iii) additional license proceeds fronm data,VSAT and GMPCS providers and new network operators.

E. Disbursement and Auditing

52. Disbursement arrangements will follow the simplified procedures approved by the Board onFebruary 1, 1996. The Borrower will open an account in the Central Bank of Morocco. Uponeffectiveness, proceeds will be deposited by the Bank in this account at the request of the Borrower. Ifthe proceeds of the loan are used for ineligible purposes (i.e., to finance items imported from non-membercountries, or goods or services in the standard negative list), the Bank will require the Borrower to either(i) return that amount to the account to use for eligible purposes, or (ii) refund the amount directly to theBank, in which case the Bank will cancel an equivalent undisbursed amount of the loan. Although aroutine audit of the deposit account is not automatically required, the World Bank reserves the right torequire it. The closing date for the IISDL is December 31, 2001.

53. During negotiations, discussions with the borrower took place about specific measures that willhelp IBRD to track the flow of funds from the Central Bank of Morocco to the borrower's budgetaryaccounts, so as to ensure that these funds are used for legitimate purposes and that withdrawals madefrom the account are used for purposes acceptable to the Bank. To achieve this objective, the followingprocedures will be established:

a) the borrower will open and maintain a dedicated Deposit Account in the Central Banlk ofMorocco to receive the proceeds of the adjustment credit;

b) the borrower will report the exact sum received into the Deposit account;c) the borrower will indicate to the Bank details of the Government Bank account to which the

local currency equivalent of the loan proceeds will be credited. This account will be subject tobudget control;

d) the borrower will ensure that all withdrawals from the deposit account are for budgetedexpenditures, and not for purposes such as military expenditures or for other items cn theBank's negative list;

e) the borrower will report to the Bank the equivalent in the local currency of the US$ amountwithdrawn from the Deposit Account producing evidence that the local currency sum was paidinto a treasury account used to fund budgetary expenditures;

14

f) the borrower will submit regular reports on receipts and disbursements from the dedicatedDeposit Account to enable the Bank to review the consistency of these withdrawals with theLoan agreement and the objectives of the adjustment operation;

g) the borrower will provide the Bank with information regarding the Terms of Reference forcarrying out and timing of regular audits, and will provide auditors with access to thenecessary officials and staff for carrying out this audit.

F. Cofinancing

54. The African Development Bank (AFDB) is cofinancing the IISDL with a US$100 million twotranche loan which was approved on April 4, 2001. Disbursement of the first tranche is predicated uponthe adoption of the same measures as the single tranche IISDL. AFDB participated jointly with the Bankin the preparation and evaluation missions of the project.

G. Environmental Aspects

55. The IISDL is an environmental category C, which does not require an environmental assessment.The proposed policy reforms will not have a negative impact on the environment and the proposed projectwill not finance any investments derived from these policy reforms.

H. Social Aspects: Program Objectives and Poverty Category

56. The proposed loan contributes to the overall development objectives of the Government forsustainable growth, employment generation and reduced social disparities in several ways. First, thereforms will enhance the competitiveness of private firms, and actively promote growth and new jobopportunities in the IIS sector and in the economy in general. Second, they will facilitate the extension oftelecommunication, postal and basic financial services to the poor, especially in the rural areas. This, inturn, can contribute to a reduction in rural-urban disparities, because it facilitates the development ofsustainable business opportunities in remote areas. Third, the policy and actions supported by the IISDLshould provide the foundations for using new means of communication and information in sectors with astrong social and economic impact such as health and education. The actual realization of this potential,however, extends beyond the time horizon of the IISDL, and could be further supported in the context offuture Bank Group operations. (See CAS and section III.E.). Finally, no significant lays-off are to beexpected as a result of IAM's privatization, because the company was a relatively well run companyalready under public ownership and did not suffer significant over-staffing problems. Adequate severancepackages will be provided in the case of eventual lays-off, which will mainly target early retirees. In sum,as a sector reform loan, the proposed IISDL project does not entail any direct or indirect complianceissues with respect to the social safeguard policies of the Bank.

I. Monitorable Indicators

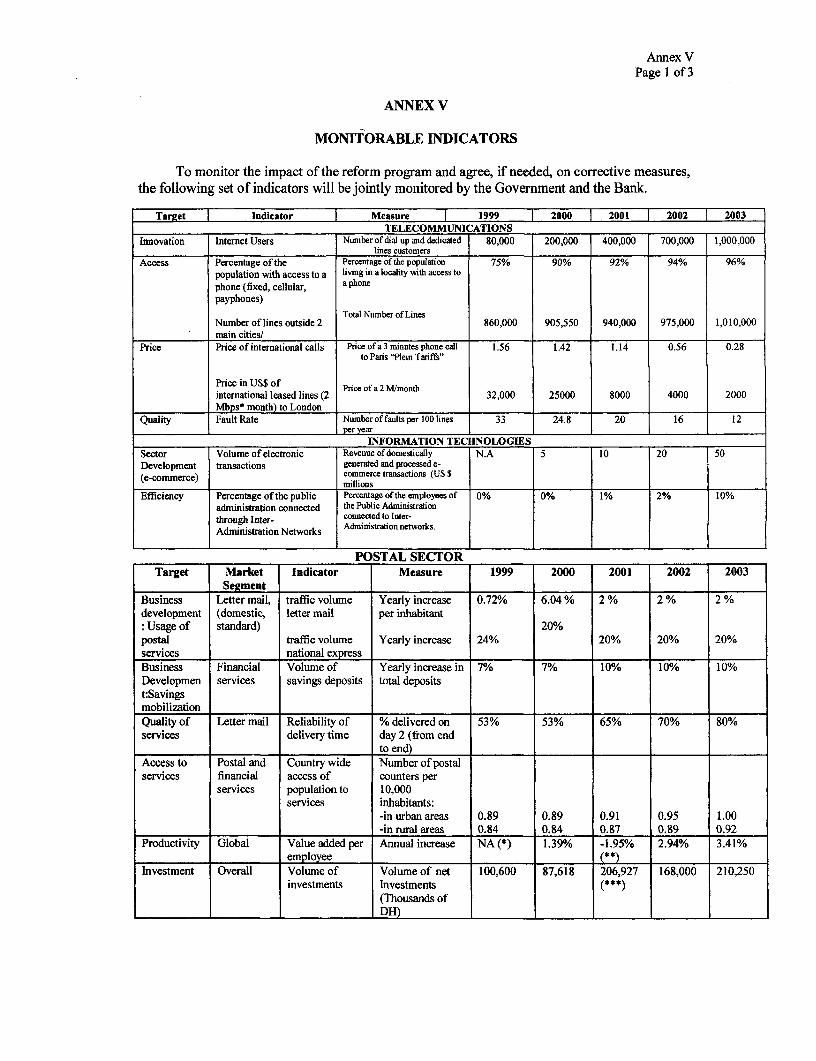

57. To monitor the impact of the reform program and agree, if needed, on corrective measures, a setof indicators have been identified by the Bank team and agreed upon with the Government during thenegotiations of the loan. These indicators will be jointly monitored by the Government and the Bank.They are designed to help monitor the evolution over the next three years of the structure of thetelecommunications, IT and postal sectors, the efficiency of new investments in the sector, as well as thequality, price, and coverage of services. The set of proposed monitorable indicators are summarized inTable IV. 1 below, and detailed in Annex V.

15

Table IV.1: Monitorable Indicators

Indicator Measure 1999 2000 2001 2002 2003Internet Users Number of dial up and 80,000 200,000 400,000 700,000 1,000,000

dedicated lines customersPercentage of the Percentage of the population 75% 90% 92% 94% 96%population with living in a locality with accessaccess to a phone to a phone(fixed, cellular,payphones)Price in US$ ofinternational Price of a 2 M/month 32,000 25,000 8,000 4,000 2,000leased lines (2Mbps* month) toLondonVolume of Revenue of domestically NA 5 20 0electronic generated and processed e-transactions commerce transactions (US $

millionsLetter mail % delivered on day 2 (from end 53 53 65 70 80

to end))Access to postal Number of postal counters perand financial 10,000 inhabitants:services -- in urban areas 0.89 0.89 0.91 0.95 1.00

-- in rural areas 0.84 0.84 0.87 0.89 0.92

J. Benefits and Risks

58. Benefits. Competitiveness and Growth. The development of a modern and competitiveinformation infrastructure network will provide a wider range of communication, information anddelivery services of higher quality and at more competitive prices. It will also provide Moroccan firmswith a greater exposure to international markets. The program of reforms supported by the proposedoperation will also bring additional flows of domestic and foreign direct investment associated with theprivatization of IAM and the issuing of new licenses for a wide range of services and the developrient ofinfrastructures. The presence of new cellular, VSAT, and VAS operators, as well as new developments inthe IT sector, should stimulate the service industry, which accounts for an increasingly important share ofGDP in rapidly developing economies.

59. Additional fiscal revenues. The Treasury will gain substantial fiscal revenues fromimplementation of the reforms, stemming mainly from higher taxes, caused by a competition-inducedenlargement of the telecommunications, IT and postal markets, from the fees obtained with the issuing ofnew licenses, and from the proceeds of the IAM's privatization (Annex VI).

60. Access. Poor residents of rural and outlying urban areas will gain greater access tocommunications services as more intense competition and reliance on market mechanisms in the sectorspur network development and improve quality of service in remote areas. Higher penetration oftelecommunications, as well as postal and IT services, will strengthen the informational and economiclinks between these areas and the rest of the country, thus facilitating the development of local businessesand improving the management capacity of local governments. Improved access to communications willalso enable the more effective provision of social services such as health and education, which are c riticalfor reducing social disparities and stemming the flow of migrants to cities.

16

61. More efficient Public Administration and reduction of transaction costforfirms and citizens. Thebenefits related to the establishment of inter-administration networks are essentially three-fold.'0 First,significant cost savings for the Public Administration (PA) from the elimination of unnecessaryduplication in information gathering and maintenance. Second, higher efficiency of PA, which facilitatesthe streamlining of administrative procedures. Third, competitive gains for business and better servicesfor citizens, thanks to more efficient procedures, on-line forms and the recognition of electronic signature.

62. Risks. The main risks associated with the implementation of the Government program include:(a) a possible slow down in the introduction of effective competition in the telecommunications sector(fixed line voice services); (b) weak institutional capacity to design and implement reforms, specially inthe IT and postal sector; (c) challenges to the regulatory agency's autonomy and its capacity to performefficiently, (d) delays in the elaboration and adoption of a new legal and regulatory framework in thepostal sector; and (e) insufficient coordination among ministries for the development of IT-basedinitiatives.

63. Risk mitigation. The success and results already achieved by the Government, notably thesuccessful privatization and issuing of the second GSM license, which led to lower tariffs, increasedaccess to telecommunications and significant capital inflows, represent the best protection against apossible policy setback. In addition, the Bank team will maintain a continuous dialogue with all partiesconcerned, and the AFDB two-tranche operation will provide additional leverage to monitor the impact ofthe reforms supported by the one-tranche IISDL and the implementation of additional reforms in 2001-02.The strong interest manifested by the Moroccan authorities and the postal operator to pursue thecollaboration with the Bank in the postal and IT sectors through follow up operations shows acommitment to continue the implementation of reforms in these two sectors, including the strengtheningof inter-agency coordination and securing of necessary financial resources.

V. RECOMMENDATIONS

64. I am satisfied that the proposed loan would comply with the Articles of Agreement of the Bank,and recommend that the Executive Directors approve it.

James D. WolfensohnPresident

by

Shengman Zhang

Washington, D.C.April 16, 2001

10These benefits have been evaluated by European Countries (e.g. France, Italy) and are the core of the European UnionProgramme 'nterchange of Data between Administrations" (1DA).

17

Annex 1Page 1 of 16

ANNEX I

KINGDOM OF MOROCCO

INFORMATION INFRASTRUCTURE DEVELOPMENT PROGRAM

SECTOR POLICY LETTER

Mr. President:

Morocco is committed to an open trade policy and integration in the global economy as themeans of ensuring sustained economic growth and an improved standard of living for the lessfortunate. In this context, information infrastructure becomes a key element in the success of theGovernment's development strategy. It is expected to increase the competitiveness of Moroccanbusinesses by lowering their production costs and putting them in closer contact with bothdomestic and international clients. It is also expected to facilitate the modernization ofgovernment services and lessen the burden weighing on the private sector, to secure Morocco'splace in the information society, and to lower the cost of delivering social and infrastructureservices to the segments of the population that are marginalized today, particularly in the mostremote rural areas.

Given the new challenges created by the liberalization process set in motion by theenactment of Law 24-96, the Government has adopted a clear strategy and plan of action toenergize the telecommunications, postal and information technology sector, the key objectives forwhich were set out in the Sector Policy Letter of February 24, 1999.

This present Policy Letter updates and expands both the Governments major objectives inthis field and the measures that have already been introduced. In addition, it describes thestrategy the Government proposes to put into effect to achieve these objectives.

I Introduction

1. General objectives

The Government believes that the telecommunications, postal and information technologysectors are key activities of the Moroccan economy, and that sound policies in these fields areessential to achievement of two of its major objectives, namely to accelerate growth and reducedisparities. The Government wishes to secure Morocco's place in the information society, fosterthe development of a competitive and dynamic telecommunications sector that will enable thecountry to meet the challenges of the 21 't century, and increase the competitiveness of its postalservices by improving management methods and bringing them into line with internationalstandards. It will also:

* Provide Moroccan enterprises with access to the telecommunications, postal and informationtechnology services they require to become more competitive. The Government believes thatdemand by the business community for such services should be met as rapidly as possible,and that the services themselves must be of high quality and competitively priced. Finally, asufficiently broad range of services should be available to meet business demands.

Annex 1Page 2 of 16

* Provide poor groups in the population and those living in remote areas with access tomodem means of communication and information. To accomplish this, it is important tocarefully define the regional development and public service obligations of thetelecommunications et postal sector, and to meet these obligations in such a way that :heneeds of operators and the country as a whole are covered satisfactorily and at a reasonal]ecost. It is equally important to put mechanisms in place which will ensure that providers oftelecommunications and postal services contribute to the sector's public service missionefficiently and in a manner in keeping with the needs of the population.

* Continue with the telecommunications sector liberalization program.

* Foster modernization and greater efficiency in the delivery of government services,including social services such as education and health care, by expanding reliance oninformation technologies and increasing capacity to utilize these technologies effectively.

* Promote the emergence of new economic activities in Morocco based on the developmentand use of information technologies.

- Improve the overall performance of the postal sector by developing all segments of t;hepostal market (new and better-quality services, sustainable upgrading of the general quality ofservice) and by achieving higher resource productivity.

Define what is meant by public postal service and specify the resulting obligations that f allon postal operators, including the historical postal operator BAM (Barid Al-Maghrib), interms of types of services, availability of access to them, and ways and means of financirigthem.

- Foster progressive opening up of the postal market, simplify the regulations in force, reviewthe present postal legislation, and offer the private sector opportunities for greaf erparticipation.

* Convert the historical postal operator, BAM into a modern, dynamic enterprise, by vesting itwith greater financial and commercial autonomy and providing it with a legal status suited toa commercial and increasingly competitive environment.

* Foster the development of postal financial services so as to provide a larger proportion of tliepopulation, particularly in the country's most remote rural areas, with access to financialservices (savings, loans, and insurance products), and to improve the mobilization of savingsand their use in the vitalization of private investment and the development of financialmarkets.

* Generate revenues for the Treasury in the field of telecommunications and informationtechnology, primarily in the form of taxes levied on the activities of operators, in the sarmethey are levied on other economic activities.

2. Results already achieved

Considerable efforts have already gone into achieving the objectives listed above. Forexample, the number of telephone lines in service rose from 266,000 at the end of 1987 to1,500,000 in 2000. Average connection time dropped from 80 months to 1.4 months (rural areas

Annex 1Page 3 of 16

included). Network transmission capacity increased from nearly 4,000 circuits to 466,000,mainly through the use of fiber-optic technology. The use of fiber-optic technology and thedigitalization of virtually all transmission and switching systems has greatly improved networkreliability and made it possible to expand the range of services offered, including videotex, ISDN,the Internet, and broadband connections. The number of rural municipal districts with automatednetworks has risen from 65 to 1,298, in other words, all rural municipalities. The number of rurallocalities with automated systems has risen from 69 to 1923, or 6.3% of all 32,000 rural localities.In addition, expansion of the public telephone network increased the number of public phonebooths from 484 at the end of 1987 to 46,000 at the end of 2000, 83% of these booths beingmanaged by private promoters.

At the end of 2000, NMT-450 and GSM-900 mobile cellular radiotelephone networkshad over three million subscribers. These networks cover the major highways and all urbancenters serving as the administrative seats of prefectures and provinces. Thanks to the virtuallycomplete digitalization of transmission and switching systems and the establishment of newnetworks, the quality and reliability of the services available have improved significantly. Use ofthe Internet, access to which became available in November 1995, is developing at a sustainedpace, with a current group of 1,200 Internet service providers (ISPs) attending to approximately200,000 users.

Since 1991, computer use has increased notably, as a result partly of the drop in hardwareand software prices and partly of the lowering of import duties from 42.5% to 17.5% as ofJanuary 1, 1996. Current estimates put the total number of personal computers in Morocco at200,000 units, representing an incidence rate of 0.7%, with annual sales of between 40,000 and50,000 units. More than 800 information technology companies are estimated to be active in thesector, with an estimated 4,000 persons on their payrolls and roughly DH 2.8 billion in sales.

Initiatives are also in progress to upgrade the management of the country's postalservices. The creation of BAM (Barid Al-Maghrib) in 1998 provided a platform from which tointroduce sustainable improvements focused on greater effectiveness of the services offered. Inthis context, BAM developed business plan and investment strategy for the years 2000 to 2004.A study currently under way will serve as a basis for recommendations for organizational unitsand business systems through which strategic options can be put into effect efficiently.