public expose 2014 - chandra asri petrochemical · public expose 2016 pt chandra asri petrochemical...

TRANSCRIPT

Public Expose 2016

PT Chandra Asri Petrochemical Tbk Jakarta, 6 June 2016

1. Company Profile

2. Operational & Financial Performance

3. Project Updates

4. Industry Outlook

2

1. Company Profile 2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

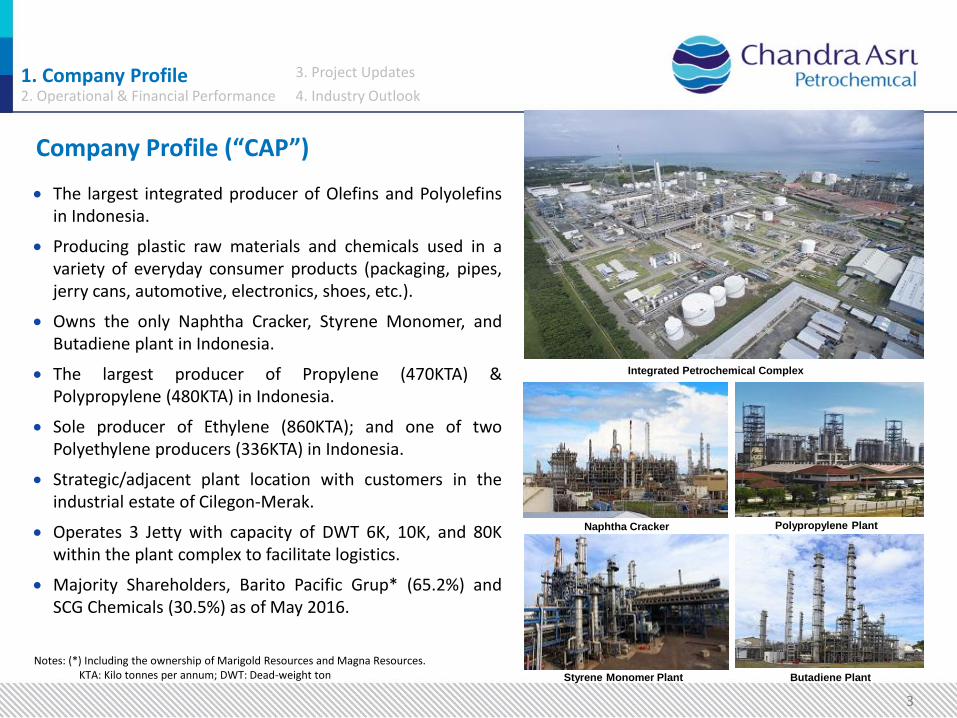

Company Profile (“CAP”)

The largest integrated producer of Olefins and Polyolefins in Indonesia.

Producing plastic raw materials and chemicals used in a variety of everyday consumer products (packaging, pipes, jerry cans, automotive, electronics, shoes, etc.).

Owns the only Naphtha Cracker, Styrene Monomer, and Butadiene plant in Indonesia.

The largest producer of Propylene (470KTA) & Polypropylene (480KTA) in Indonesia.

Sole producer of Ethylene (860KTA); and one of two Polyethylene producers (336KTA) in Indonesia.

Strategic/adjacent plant location with customers in the industrial estate of Cilegon-Merak.

Operates 3 Jetty with capacity of DWT 6K, 10K, and 80K within the plant complex to facilitate logistics.

Majority Shareholders, Barito Pacific Grup* (65.2%) and SCG Chemicals (30.5%) as of May 2016.

Integrated Petrochemical Complex

Styrene Monomer Plant Butadiene Plant

Naphtha Cracker Polypropylene Plant

Notes: (*) Including the ownership of Marigold Resources and Magna Resources. KTA: Kilo tonnes per annum; DWT: Dead-weight ton

3

Integrated Business Operations “Integrated business operations from upstream to downstream resulting in higher efficiency, lower costs, and value-added”.

4

New Generation Synthetic Rubber

Polypropylene Polyethylene Styrene Monomer

Up

stre

am

Pe

tro

che

mic

al

Ethylene Propylene Py-Gas Mixed C4

Mid

stre

am

Pe

tro

che

mic

al

O

il &

Gas

CAP Products Future products by SRI

Crude Oil

Diesel Kerosene Gasoline

Refinery

Naphtha Cracker

Naphtha LPG

Raffinate - 1 Butadiene

Condensate

CAP Facility Legend:

1. Company Profile 2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

Integrated Business Operations (cont’d)

Notes: (1) LLDPE: Linear Low Density Polyethylene (2) HDPE: High Density Polyethylene

Homopolymer

Random

Copolymer

Impact (Block) Copolymer

Ethylene

Key Products Plant Main Process Key Markets

330 KTPA

860 KTPA

430 KTPA

100 KTPA

Propylene

470 KTPA

Py-Gas

400 KTPA

Crude C4

315 KTPA

Domestic

Exporr

Domestic

Domestic

Export

Export

Domestic

Export

Domestic

Naphtha Cracker

licensed by Lummus and

KBR. Polypropylene

W.R. Grace

480 KTPA

Styrene Monomer

Licensed by Mobil-Badger and Lummus

340 KTPA

LLDPE(1)

HDPE(2)

Polyethylene

Licensed by Univation

336 KTPA

Naphtha

2,300 KTPA

Butadiene

BASF/Lummus

100 KTPA

Improved margins along the integration of the production value chain

5

1. Company Profile 2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

Strategic Location “Adjacent and interlinked with customer’s facilities (45 km Ethylene pipeline)”.

6

Anyer

Cilegon

Merak

Jetty CAP Pipeline New Toll Road Existing Road

Puloampel-

Serang

Main Plant

Main Plant Capacity (ktpa)

– Ethylene: 860

– Propylene: 470

– Py-Gas: 40 0

– Mixed C4: 315

– Polyethylene: 336

– Polypropylene: 480

Butadiene Plant: 100 ktpa

On-Site Power

Styrene Monomer Plant

Capacity 340 ktpa

Sriwie

Dongjin Lautan Otsuka

Asahimas Polypet PET

Polyprima PTA ARCO PPG

Amoco Mitsui TITAN PE

Mitsubishi Kasei PIPI PS and SBL

Unggul Indah AB Prointail

Statomer PVC Buana Sulfindo

Santa Fe

Rhone Poulenc SBL Sulfindo Adiusaha

NAOH, CL2

Golden Key ABS Multisidia

Risjad Brasali EPS, SAN

Trans Bakrie Cont Carbon CB

Indochlor

Sintetikajaya

Showa Esterindo Sulfindo Adi. PVC

Polychem Redeco

Cabot

Siemens

Hoechst

KS

Dow Chemical

Air Liquide

UAP

Existing customers with pipeline access

NSI

Sulfindo Adi.

EDC, VCM

Indonesia

Cilegon

Main Plant

CAP’s Petrochemical Complexes

N

1. Company Profile 2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

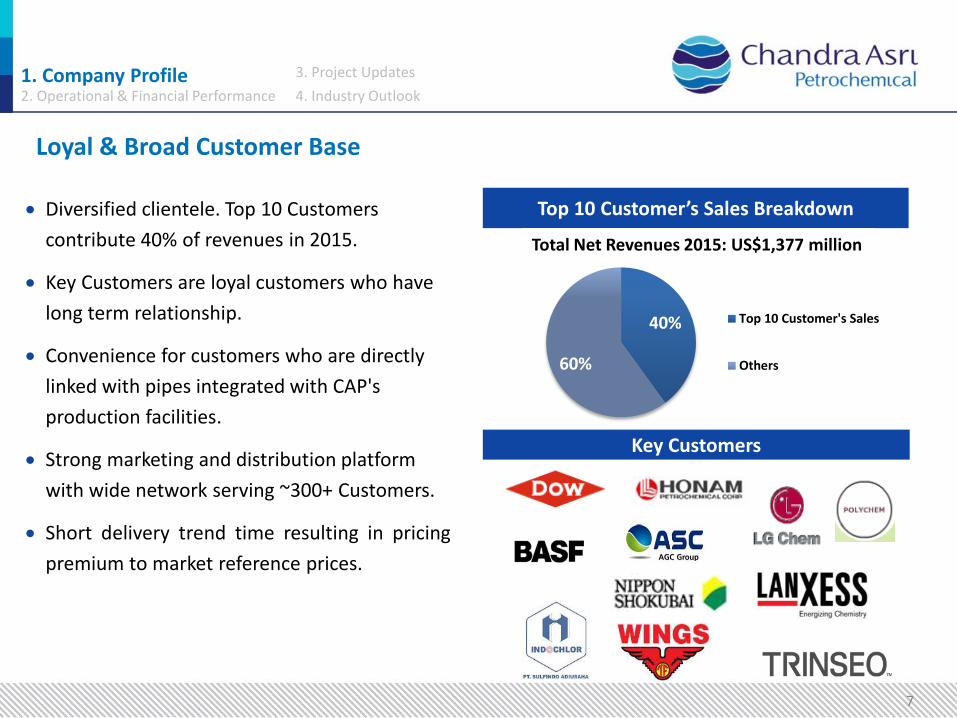

Loyal & Broad Customer Base

7

Top 10 Customer’s Sales Breakdown Diversified clientele. Top 10 Customers

contribute 40% of revenues in 2015.

Key Customers are loyal customers who have

long term relationship.

Convenience for customers who are directly

linked with pipes integrated with CAP's

production facilities.

Strong marketing and distribution platform

with wide network serving ~300+ Customers.

Short delivery trend time resulting in pricing

premium to market reference prices.

Key Customers

40%

60%

Top 10 Customer's Sales

Others

Total Net Revenues 2015: US$1,377 million

1. Company Profile 2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

1. Company Profile

2. Operational & Financial Performance

3. Project Updates

4. Industry Outlook

8

Ethylene

Plan Utilization Rate

Polyethylene, Polypropylene, Styrene Monomer, Butadiene

Decline of utilization in 2015 was due to shutdowns in the 4th quarter for Tie-in work of the Cracker Expansion project. In addition, within the 85-day shutdowns period were also conducted a Turnaround Maintenance (TAM).

1st Quarter -2016, plant utilization showed an increase post Expansion completion in Dec-2015. Cracker plant has a new capacity of 860 KTA (up to 43%) and ramp up gradually to optimum capacity.

Butadiene Plant operates since Sept-2013.

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

9

(dalam %)

94 93

80 89

95 99

92 89 95

74 69 72 76 79

47

76

2013 2014 2015 1Q-16

Polyethylene Polypropylene Styrene Monomer Butadiene

99 94

57 66

2013 2014 2015 1Q-16

10

Ethylene

Volume (KT)

Price & spread (US$/ton)

Propylene

Volume (KT)

Price & spread (US$/ton)

109 139

19 51

1Q-15A 1Q-16

296

182

32 32

2014A 2015A

59 78

4 18

1Q-15A 1Q-16

447 479

931

552

1.378

1.031

2014A 2015A

375 550

574 376

949 926

1Q-15A 1Q-16

415 256

931

552

1.345

808

2014A 2015A

182 268

574 376

756 644

1Q-15 1Q-16

561

339

189

82

2014A 2015A

Volume and Price by products Olefins

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

11

Volume and Price by products Polyolefins

Polypropylene

Volume (KT)

Price & spread (US$/ton)

Polyethylene

Volume (KT)

Price & spread (US$/ton)

477 444

471 449

2014A 2015A

118 105 124 110

1Q-15A 1Q-16

311

224

314

227

2014A 2015A

74 74 74 68

1Q-15A 1Q-16

739 697

931

552

1.670

1.249

2014A 2015A

694 642

574 376

1.268

1.018

Q1-15A Q1-16

711 807

931

552

1.642

1.359

2014A 2015A

712 825

574 376

1.286 1.201

Q1-15A Q1-16

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

12

Volume and Price by products Styrene Monomer and Butadiene

79

47

82

46

2014A 2015A

Butadiene

Volume (KT)

Price & spread (US$/ton)

(1)Styrene Monomer and by products (Toluene and Ethyl Benzene)

Styrene Monomer(1)

Volume (KT)

Price & spread (US$/ton)

(3)

16 19 13 17

1Q-15A 1Q-16

250 234 257

230

2014A 2015A

52 60 50 62

1Q-15A 1Q-16

398 391

931

552

1.329

943

2014A 2015A

231 370

574 376

805 746

Q1-15A Q1-16

326 373

1.280

721

1.605

1.094

2014A 2015A

238 390

733 567

971 957

Q1-15A Q1-16

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

Financial Highlights: Financial Position FY-2015 and 1Q-2016

31-Dec-2014 (US$ ‘000)

31-Dec-2015 (US$ ‘000)

31-Mar-2016 (US$ ‘000)

Changes Yoy (%)

Changes Ytd (%)

Cash and cash equivalents 207,939 96,835 141,242 -53.4 45.9

Current Assets (exclude Cash and cash equivalents)

458,495 319,799 339,572 -30.3 6.2

Non Current Assets 1,257,077 1,445,752 1,461,442 15.0 1.1

TOTAL ASSETS 1,923,511 1,862,386 1,942,256 -3.2 4.3

Current Liabilities 477,912 377,753 440,255 -21.0 16.5

Non Current Liabilities 579,737 597,787 579,753 3.1 -3.0

Equity 865,862 886,846 922,248 2.4 4.0

TOTAL LIABILITIES AND EQUITY 1,923,511 1,862,386 1,942,256 -3.2 4.3

13

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

Financial Highlights: Profit or Loss FY-2015 and 1Q-2016

FY-2014 (US$ ‘000)

FY-2015 (US$ ‘000)

Changes (%)

3M-2015 (US$ ‘000)

3M-2016 (US$ ‘000)

Changes (%)

Net Revenues 2,460,051 1,377,573 -44.0 357,933 358,895 0.3

Cost of Revenues 2,342,587 1,231,844 -47.4 341,186 296,396 -13.1

Gross Profit 117,464 145,729 24.1 16,747 62,499 273.2

Operating Profit (Loss) 50,187 79,222 57.9 (531) 45,894 8,742.9

Profit (Loss) For The Year 18,439 26,256 42.4 2,849 35,402 1,142.6

EBITDA 133,762 154,825 15.7 31,299 68,091 117.6

Gross Profit Margin (%) 4.8 10.6 4.7 17.4

Operating Profit Margin (%) 2.0 5.8 -0.1 12.8

Net Profit Margin (%) 0.7 1.9 0.8 9.9

EBITDA Margin (%) 5.4 11.2 8.7 19.0

14

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

Diverse Product Portfolio

Olefins Polyolefins Butadiene Styrene Monomer

Ethylene

Py-Gas

Propylene

Mixed C4 Polypropylene

Polyethylene

Established PT Synthetic Rubber Indonesia, JV between SMI and Michelin, to build Styrene Butadiene Rubber plant.

Net Revenues US$869 million

Net Revenues US$171 million

Net Revenues US$256 million

Net Revenues US$78 million

63% 12% 19%

Net Revenues FY-2015: US$1,377 million (100%)

6%

15

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

358

359

4.7%

17.4%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

18,0%

20,0%

357

358

358

358

358

358

359

359

1Q-2015 1Q-2016

18

26

0.7%

1.9%

0,2%0,3%0,4%0,5%0,6%0,7%0,8%0,9%1,0%1,1%1,2%1,3%1,4%1,5%1,6%1,7%1,8%1,9%2,0%

-

4

8

12

16

20

24

28

2014 2015

2.8

35.4

0.8%

9.9%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

-

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

1Q-2015 1Q-2016

Financial Performance

16

2,460

1,378

4,8%

10.6%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

- 50 100 150 200 250 300 350 400 450 500 550 600 650 700 750 800 850 900 950 1.000 1.050 1.100 1.150 1.200 1.250 1.300 1.350 1.400 1.450 1.500 1.550 1.600 1.650 1.700 1.750 1.800 1.850 1.900 1.950 2.000 2.050 2.100 2.150 2.200 2.250 2.300 2.350 2.400 2.450 2.500 2.550 2.600

2014 2015

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

Net Revenues (million US$) & Gross Profit Margin (%)

Net Profit (million US$) & Net Profit Margin (%)

1. Company Profile

2. Operational & Financial Performance

3. Project Updates

4. Industry Outlook

17

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook 3. Project Updates

18 18

DA-415 New Propylene Tower EBR Compressor BA-109 New Furnace

Achieved Mechanical Completion on 9 December 2015.

TAM/Expansion tie-in works successfully completed on

schedule. Cracker re-started with on-spec products on

19 December, 5-days ahead of plan.

Total spending US$378m vs budget of US$380m as of

31 December 2015.

Cracker facility capacity increased to 860 KTA (up to

43%) since early 2016.

Cracker Expansion Project

"With Cracker capacity equivalent to world-class capacity added with plant

modernization, CAP further established its position in the

petrochemical industry in Indonesia".

19 19

Cracker Expansion Project

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook 3. Project Updates

20 20

EPC contract awarded to Toyo Engineering & IKPT in

June 2015.

CAP has fully injected total equity of US$54m.

Overall progress 27% as of May 2016.

Drainage work & temporary site facility completed.

Soil improvement work, civil construction work,

structure and building erection, on-going.

Future SBR Plant Facility Area

Soil Improvement CCR & Substation Temporary Site Facility

SBR plant project

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook 3. Project Updates

1. Company Profile

2. Operational & Financial Performance

3. Project Updates

4. Industry Outlook

21

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

80%

82%

84%

86%

88%

90%

0

100

200

300

400

500

600

700

2009 2011 2013 2015 2017F 2019F 2021F

% U

tilis

atio

n ra

tes

Gap

ove

r na

phth

a (D

olla

rs p

er to

n)

Ethylene Delta Over Net Raw Material Cost Global utilisation rates

Note:

- 2015 is based on actual on year to date basis (Jan-Nov)

- Forecast price is based on Brent Crude at $30 (2016-2020) and $50 (2021-2022) per barrel

60%

70%

80%

90%

0

200

400

600

800

1000

1200

2009 2011 2013 2015 2017F 2019F 2021F

% U

tilis

atio

n ra

tes

Gap

ove

r na

phth

a (D

olla

rs p

er to

n)

Polyolefins Delta Over Net Raw Material Cost

Global polyolefins utilisation ratesNote:

- 2015 is based on actual on year to date basis (Jan-Nov)

- Forecast price is based on Brent Crude at $30 (2016-2020) and $50 (2021-2022) per barrel

SEA Ethylene price spreads over naphtha

“Demand fundamental remain good for petrochemical industry over the next few years, new capacity additions post 2015 resulting in modest decline in average margins following period of sustained higher profitability”

Source: Nexant (Feb 2016)

SEA Polyolefins price spreads over naphtha

Industry Outlook

22

70%

80%

90%

100%

0

100

200

300

400

500

600

2009 2011 2013 2015 2017F 2019F 2021F

% U

tilis

atio

n ra

tes

Gap

ove

r ne

t raw

mat

eria

l cos

t (D

olla

rs p

er to

n)

Styrene Delta Over Net Raw Material Cost* Global utilisation rates

Note: - 2015 is based on actual on year to date basis (Jan-Nov)

- Forecast price is based on Brent Crude at $30 (2016-2020) and $50 (2021-2022) per barrel

* Styrene market price less net raw material prices (benzene*.0.78 + ethylene*0.28)

23

60%

70%

80%

90%

100%

0

500

1000

1500

2000

2500

2009 2011 2013 2015 2017F 2019F 2021F

% U

tilis

atio

n ra

tes

Gap

ove

r na

phth

a (D

olla

rs p

er to

n)

Butadiene Delta Over Net Raw Material Cost Global utilisation rates

Note:

- 2015 is based on actual on year to date basis (Jan-Nov)

- Forecast price is based on Brent Crude at $30 (2016-2020) and $50 (2021-2022) per barrel

SEA Butadiene price spreads over Net Raw Material Cost SEA SM price spreads over Net Raw Material Cost

Source: Nexant (Feb 2016)

Industry Outlook (Cont’d)

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

24

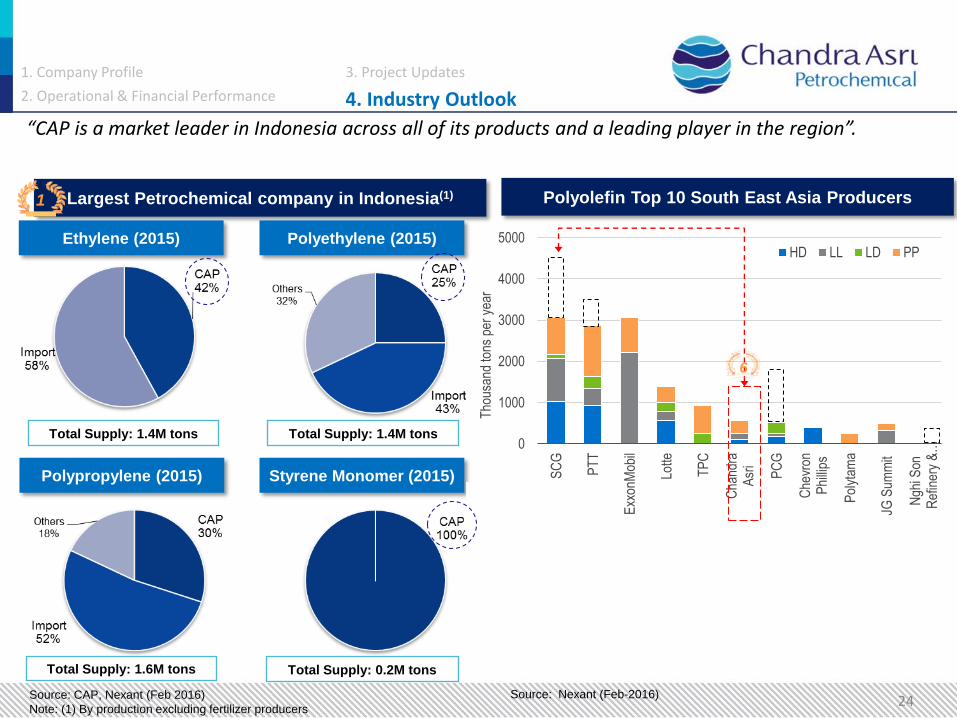

“CAP is a market leader in Indonesia across all of its products and a leading player in the region”.

0

1000

2000

3000

4000

5000

SC

G

PT

T

Exx

onM

obil

Lotte

TP

C

Cha

ndra

Asr

i

PC

G

Che

vron

Phi

llips

Pol

ytam

a

JG S

umm

it

Ngh

i Son

Ref

iner

y &

…

Tho

usan

d to

ns p

er y

ear

HD LL LD PP

Polyolefin Top 10 South East Asia Producers Largest Petrochemical company in Indonesia(1)

Ethylene (2015) Polyethylene (2015)

1

Polypropylene (2015) Styrene Monomer (2015)

Source: CAP, Nexant (Feb 2016)

Note: (1) By production excluding fertilizer producers

Total Supply: 1.4M tons

Total Supply: 1.6M tons Total Supply: 0.2M tons

6

Source: Nexant (Feb-2016)

Total Supply: 1.4M tons

1. Company Profile

2. Operational & Financial Performance 4. Industry Outlook

3. Project Updates

Thank You

Disclaimer: Important Notice • This document was prepared solely and exclusively for the parties presently being invited for the purpose of discussion. Neither this document nor any

of its content may be reproduced, disclosed or used without the prior written consent of PT Chandra Asri Petrochemical Tbk. • This document may contain statements that convey future oriented expectations which represent the Company’s present views on the probable future

events and financial plans. Such views are presented on the basis of current assumptions, are exposed to various risks and are subject to considerable changes at any time. Presented assumptions are presumed correct, and based on the data available on the date, which this document is assembled. The company warrants no assurance that such outlook will, in part of as a whole, eventually be materialized. Actual results may diverge significantly from those projected. The information in this document is subject to change without notice, its accuracy is not verified or guaranteed, it may be incomplete or condensed and it may not contain all material information concerning the Company.

• None of the Company, PT Chandra Asri Petrochemical Tbk or any person connected with any of them accepts any liability whatsoever for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith.

Address: PT Chandra Asri Petrochemical Tbk Wisma Barito Pacific Tower A, Lt. 7 Jl. Let. Jend. S. Parman Kav. 62-63 Jakarta 11410

Contact: Investor Relations Email: [email protected] Tel: +62 21 530 7950 Fax: +62 21 530 8930

Visit our website at www.chandra-asri.com