public financial management reform … iv strategy.pdf · 2.0 situational analysis ... improved...

TRANSCRIPT

THE UNITED REPUBLIC OF TANZANIA

MINISTRY OF FINANCE

PUBLIC FINANCIAL MANAGEMENT REFORM

PROGRAMME STRATEGY PHASE IV

2012/13 - 2016/17

VOLUME I

JUNE, 2012

2

Table of Contents

Table of Contents ...............................................................................................2

ABBREVIATIONS AND ACRONYMS .................................................................4

EXECUTIVE SUMMARY ......................................................................................8

CHAPTER ONE .................................................................................................. 13

1.0 INTRODUCTION ........................................................................................ 13

1.1 Background ...........................................................................................................13

1.2 Purpose of the PFMRP IV ...................................................................................16

1.3 Main actors ...........................................................................................................16

1.4 Implementation Period .......................................................................................17

1.5 Financing of the Programme .............................................................................17

CHAPTER TWO .................................................................................................. 18

2.0 SITUATIONAL ANALYSIS ..................................................................... 18

2.1 Overview of current PFM ....................................................................................18

2.2 PFM Reforms ........................................................................................................19

2.2.1 Revenue Management and Tax Administration .............................................. 19

2.2.2 Planning and Budgeting ...................................................................................... 20

2.2.3 Budget Execution, Accountability and Transparency ..................................... 21

2.2.4 Budget Control and Oversight ........................................................................... 23

2.2.5 Change Management, Programme Monitoring and Communication ........... 24

2.3 Other Core Reforms in Tanzania .......................................................................25

2.4 Strengths identified in the Tanzania PFM systems .........................................27

2.5 Challenges identified in the Tanzania PFM systems .......................................28

CHAPTER THREE .............................................................................................. 30

3.0 PERSPECTIVES OF PFMRP IV .............................................................. 30

3.2 Goal ........................................................................................................................30

3.3 Main Objectives ....................................................................................................30

3.4 The PFM reform Key Result Areas ....................................................................30

3.5 Intermediate Results ...........................................................................................33

3.6 Key Drivers ...........................................................................................................34

3.6.1 Enabling Realisation of Tanzania Development Vision 2025 ........................ 34

3.6.2 Facilitating Implementation of the Five Years National ................................. 34

Development Plan ............................................................................................................ 34

3.6.3 Facilitating Implementation of MKUKUTA/MKUZA II ..................................... 35

3.6.4 Taxpayers Demands for Better Services .......................................................... 35

3.6.5 Enhancing Good Governance ............................................................................. 35

3.6.6 Effective and Efficient PFM System ................................................................... 36

3.6.7 Addressing PFM Challenges ............................................................................... 36

3

3.7 Anticipated Success Factors ...............................................................................37

3.7.1 Capacity Building ................................................................................................. 37

3.7.2 Enabling Legal Framework ................................................................................. 37

3.7.3 Effective Communication, Coordination and Dissemination .......................... 37

3.7.4 Commitment of Top Leadership and Key Stakeholders ................................. 38

3.7.5 Effective and Functional M&E System .............................................................. 38

3.8 Interventions of PFMRP IV .................................................................................38

3.8.1 KRA 1: Revenue Management ........................................................................... 38

3.8.2 KRA 2: Planning and Budgeting ........................................................................ 39

3.8.3 KRA 3: Budget execution, accountability and transparency ......................... 40

3.8.4 KRA 4: Budget control and oversight ............................................................... 41

3.8.5 KRA 5: Change Management, Programme Monitoring and Communication43

CHAPTER FOUR ................................................................................................ 46

4.0 INSTITUTIONAL ARRANGEMENTS ..................................................... 46

4.1 Internal Programme Implementation Arrangements .....................................46

4.2 Programme Governance Arrangements ...........................................................46

4.3 Joint Steering Committee (JSC) ........................................................................49

4.4 Programme Management Committee (PMC) ...................................................49

4.5 Technical Working Group (TWG) ......................................................................49

4.6 Programme Management ...................................................................................49

4.7 PFMRP and other core reforms..........................................................................50

CHAPTER FIVE .................................................................................................. 51

RESULT FRAMEWORK ..................................................................................... 51

5.1 INTRODUCTION ........................................................................................................51

5.2 The Development Objective ....................................................................................51

5.3 Link between PFMRP IV with other National Frameworks .................................51

5.4 Result Chain..........................................................................................................52

5.5 The Result Framework Matrix ............................................................................52

4

ABBREVIATIONS AND ACRONYMS

ACGEN Accountant General

AFROSAI African Organization of Supreme Audit Institutions

AMP Aid Management Platform

BoT Bank of Tanzania

CAG Controller and Auditor General

CB Commissioner for Budget

COA Chart of Accounts

CoFoG Classification of Functions of Government

CPAD Commissioner for Policy Analysis Department

CS Chief Secretary

CS-DRMS Commonwealth Secretariat-Debt Recording Management System

DAC Development Assistance Committee

DFID Department for International Development

DFMIS Director of Financial Management Information Systems

DIA Department of Internal Audit

DPs Development Partners

DPD Director of Planning Division

East-AFRITAC Eastern Africa Technical Assistance Centre

EFT Electronic Funds Transfer

EU European Union

FEC Finance and Economic Committee

GBS General Budget Support

GDP Gross Domestic Product

GFS Government Financial Statistics

GoT Government of Tanzania

HIPCs Highly Indebted Poor Countries

ICT Information and Communications Technology

IDA International Development Association

IEC Information, Education and Communication

IFMS Integrated Financial Management System

IMF International Monetary Fund

IMTC Inter-Ministerial Technical Committee

5

IMF/FAD International Monetary Fund/Fiscal Affairs Department

IPSAS International Public Sector Accounting Standards

IRBM Integrated Results Based Management

JAST Joint Assistance Strategy for Tanzania

JSC Joint Steering Committee

JSM Joint Supervision Mission

KRA Key Results Areas

LGAs Local Government Authorities

LAAC Local Authorities Accounts Committee

LGRP Local Government Reform Programme

LSRP Legal Sector Reform Programme

MACMOD Macroeconomic Modelling Tool

MDAs Ministries, Departments and Agencies

MDGs Millennium Development Goals

M&E Monitoring and Evaluation

MoF Ministry of Finance

MTEF Medium Term Expenditure Framework

MTFF Medium Term Fiscal Framework

MTSPBM Medium Term Strategic Planning and Budgeting Manual

NAO National Audit Office

OECD Organization for Economic Cooperation and Development

PAC

PAOB

Public Accounts Committee

Public Authorities and Other Bodies

PC Planning Commission

PBB Program-Based Budgeting

PEFA Public Expenditure and Financial Accountability

PFM Public Financial Management

PFMRP Public Financial Management Reform Program

PEs Procuring Entities

PER Public Expenditure Review

PLANREP Planning and Reporting system

PMIS Procurement Management Information System

PMO-RALG Prime Minister’s Office, Regional Administration and Local

6

Government

PO-PSM President Office -Public Service Management

PPAA Public Procurement Appeal Authority

PPP Public Private Partnership

PPRA Public Procurement Regulatory Agency

PPD Procurement Policy Division

PSPTB Procurement and Supplies Professionals and Technicians Board

RBBS Results-Based Budgeting System

RCU Reform Coordination Unit

RSs Regional Secretariats

SAI Supreme Audit Institution

SBAS Strategic Budget Allocation System

SP Strategic Plan

TA Technical Assistance

TISS Tanzania Inter-Bank Settlement System

TR Treasury Registrar

TRA Tanzania Revenue Authority

TRIMS Treasury Registrar Investment Management System

WB World Bank

7

8

EXECUTIVE SUMMARY

The Strategic Plan for reform of Public Financial Management, Phase IV, is the result of

a period of diagnostic analysis and consultations within Government and Development

Partners. The need for deepening reforms of the public finance management is

emphasized in MKUKUTA/MKUZA II and Vision 2025, as key elements for PFMRP to

achieve:

Fiscal sustainability and balance in the public economy;

Restructuring and reallocations for growth and poverty alleviation; and

Improved public sector performance, efficiency and effectiveness in public

administration leading to improved service delivery and development results for

Tanzanians.

A number of underlying reforms have been initiated, for example, those related to an

improved budget process along with simplified procedures, automated spending

commitment controls, financial reporting and other finance systems, legal reforms of

financial management, ethics, procurement, introduction of modern audit methods and

techniques. Some institutional reforms have been undertaken to promote good

governance and fight against corruption. These initiatives have resulted in some

improvements, as measured by international benchmarks and diagnostic reviews.

However, there are indications that the reforms undertaken had not fully reached the

desired end results. External diagnosis coupled with the problem analysis carried out

through specific audits, reviews, workshops and consultations to design Phase IV

indicate that many challenges still remain. In essence, the PFM system is still

inadequate; a number of improvements are needed before it becomes an effective and

efficient management tool for improved public service delivery.

Efforts to mobilize public financial resources have encountered challenges relating to tax

collection; accounting and reporting of non-tax revenues. There are still challenges to

comprehend fully the costing of priorities into the Government budget allocations and

the implementation and credibility of the recurrent and development budgets across key

sectors.

9

The quality, accuracy and timeliness of financial reports and accounting are generally

good, but require improvement. As EPICOR was rolled out to Ministries, Departments

and Agencies (MDAs) and are being rolled out to all Local Government Authorities

(LGAs) it faces serious challenges related to ICT infrastructure and interfacing with

other systems.

Efforts have been made to improve cash management. The present cash based

commitment system, which ensures commitment control on macro level, puts some

challenges to cash management as its side effect can distort execution of the budget

especially when cash is not available on a timely manner. Over the coming reform

period the Government will start the migration from Cash basis of accounting to Accrual

accounting. This will further improve the integrity and content of the Governments

financial statements. The migration towards program based budgeting will increase the

credibility of the budget to ensure that priorities are properly costed and attained. In

addition, a centralization of the management of public debt will reduce the borrowing

costs. Reforms in procurement are well underway and compliance rates have gone up

and efforts will continue to ensure improvement and sustainability. In addition, support

will be given to the Procurement Policy Division with the aim of ensuring value for

money in public procurement. There is opportunity to further enhance the quality of

financial internal controls following the establishment of Internal Audit Department in

the MoF, to further improve the timeliness and quality of audit reports and to ensure

that audit recommendations are implemented.

The Government is determined to step up reforms of the Public Finance Management

system. The analysis of the current needs and lessons learned has led to the

conclusion that the PFM reform shall be:

Comprehensive, including all those various key reforms and activities in the PFM

system as well as the cross-cutting issues related to capacity building, service

conditions, and the institutional policy legal and regulatory frameworks;

10

Captured in a well defined Monitoring and Evaluation framework Sequenced, to

manage priorities to ensure a more accurate cash forecasting and achievement of

results;

Linked and inter-dependent with clear demarcation of responsibilities and

accountability

Better standardized and automated systems to ensure attainment of desired results

in financial recording and reporting;

Well managed, with effective institutional arrangement to support implementation of

the programme

Focused, aiming at supporting agencies and initiatives which are likely to have a

great cross cutting impact on the PFM system.

This strategy is in line with the Five Year Development Plan (FYDP 2011/12-2015/16),

MKUKUTA/MKUZA II and the Vision 2025 and aims for achieving the following:

Economic growth and poverty reduction achieved through policy-based budget

management and resource mobilization and allocation, improved fiscal discipline and

sustainable budget balance;

Service delivery improvement through the introduction of results-based

management, program based budgets, accountability and performance audits;

Good governance through improved transparency, accountability and efficient

controls.

The new phase is an enabler towards enhancing revenue mobilization, planning and

budgeting, transparency, accountability, efficiency and effectiveness in the use of

resources and implementation will be through 5 Key Result Areas (KRAs) of the PFM

system; 1) Revenue management, 2) Budget and Planning, 3) Budget execution,

Transparency and Accountability, 4) Budget control and Oversight, 5) Change

management, Programme monitoring and Communication.

The identified KRA structure shall ensure that all the different aspects and dependencies

of PFM reform are contained and managed during the program implementation. In

11

essence, it concurs with the best model for the Public Financial Management system,

which is also reflected in the common assessment framework for PFM-PEFA. In

addition, it includes cross-cutting institutional issues such as IFMS, Information,

Education and Communication (IEC), Change management, Information Communication

Technology (ICT) and capacity building and training.

The reform program is led by a PFM Joint Steering Committee chaired by Permanent

Secretary – Treasury, MoF with members from wider PFM stakeholder group and with

representatives from the development partners.

The estimated total cost of PFMRP Phase IV amounts to Tshs 175 billion1 over a five

year period for the direct development activities including funds to allow the

Government of Zanzibar to conduct the necessary studies that could lead to the

preparation of a full-fledged Zanzibar Public Financial Management Reform project

(ZPFMRP), through Basket, Project and Government funds. This translates into roughly

Tshs. 35 billions per annum. The Government will commit the equivalent of Tshs 75

billion2 within the MTEF for the next five-year period.

This strategic plan will be accompanied by the following documents that serve to

facilitate the program implementation:

Results Performance Monitoring Framework, which specify Outputs, Performance

indicators, baselines, targets and milestones.

The PFM Reform Program Five Year Work Plan and Budget (2011/12-2015/16) that

details activities planned against the milestones. The plan contains the total

estimated budget for implementation of the program and an annual work plan will

be prepared (Volume II)

An Operations Manuals, that lead component leaders and provide a description of

the main policy and rules, specific roles and responsibilities, institutional

arrangements, and procedures and formats for procurement and financial

1 Subject to review depending on availability of funds and pace of implementation

2 Subject to review depending on availability of funds, exchange rate and pace of implementation

12

management and monitoring and evaluation for program implementation (Volume

III)

A Memorandum of Understanding (MOU) between GoT and Development Partners

which is a signed document outlining shared commitment in implementation of the

programme.

Flexibility and keeping the PFM program relevancy while maintaining a strategic focus at

all times is a challenge that continuously need to be kept on the dialogue agenda. It is

also expected that Development Partners will continue to play a constructive role in the

engagement with the Government. A mid-term review will evaluate progress and

challenges.

13

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background

Tanzania has established a solid macroeconomic record over the past decade, with key

macroeconomic indicators improving further particularly between 2006 and 2010 amid

the global downturn. Real GDP growth averaged 7 percent, attributed mainly to

impressive performance in agriculture, transportation, infrastructure, communications,

manufacturing and real estate sectors. Among others, inflation lowered to single digits,

revenue mobilization increased markedly, and overall fiscal deficits and public debt

levels were kept at sustainable levels. In spite of an overly stable macroeconomic

framework, the Government of the United Republic of Tanzania (GoT) has gone through

economic and financial challenges which necessitated structural reform interventions

including strengthening public financial management.

Despite the aforesaid development, challenges remain and these include the need to

expand economic infrastructure and create a more enabling and competitive

environment for achieving sustained and broad based growth. A more efficient

allocation of resources is crucial for the Government of Tanzania. In this context,

reforms in public finance management are intended to contribute more meaningfully

and geared towards better coordination of reforms that will improve public financial

management and hence a high level public service delivery. PFMRP IV strategic plan

represents a paradigm shift from previous plans in that it is driven by an integrated

results based management and monitoring framework. More efficient and effective

budget management is recognized as one of the best ways in which the Government

can contribute to realization of broad-based economic growth and development of a

vibrant private sector.

14

Government has implemented PFM reforms over the past two decades with significant

successes. Commendable are the enactment of Public Audit Act No. 11 of 2008 to

enhance operational independence of the National Audit Office; the enactment of Public

Finance Act No. 6 of 2001 and its amendment in 2010 and Public Procurement Act

No.21 of 2004 as amended in 2011 to enhance transparency and accountability; timely

submission of CAG annual audit reports; establishment of the independent Department

of Internal Auditor General; adoption of the Government Financial Statistics (GFS) codes

2001 and Classification of Functions of Government (CoFoG); introduction and

expansion of financial management systems to automate various key PFM processes

including IFMS, LAWSON, CS-DRMS, SBAS; use of EPICOR by all sub-treasuries MDAs

and 86 LGAs; strengthening the capacity of Parliamentary Accounts Committees to

execute the oversight function; identifying and closing down dormant bank accounts to

improve cash management; and provision of capacity building to staff involved in public

financial management.

In spite of the contribution of these reforms to improved PFM, a number of challenges

and concerns were observed during the implementation of PFMRP III that contributed

to programme underperformance. In fact, PFMRP in itself has evolved in different

phases as presented in Box 1 below. PFMRP IV is meant to sustain achievements made

and address the observed challenges in the previous phases and further strengthen the

public financial management systems and facilitate provision of high level of public

service delivery.

The need to strengthen and re-organize Tanzania’s PFM systems has been echoed in a

variety of documents and has attracted support from various stakeholders. The

documents include, among others:

i) the 2009 Tanzania Public Expenditure and Financial Accountability (PEFA) review

identified certain areas of weakness, including credibility and classification of the

budget; multi-year perspective in fiscal planning, expenditure policy, and budgeting;

15

transparency of inter-governmental fiscal

relations; consolidation of fiscal position

and the medium term debt management

strategy, and oversight over local

governments. Other areas are;

procurement and contract management;

in-year fiscal reporting; and the internal

audit function and follow up of audit

recommendations.

ii) The Public Expenditure Reviews (PERs)

and a Public Investment Management

(PIM) diagnosis report by the World

Bank point to the need to re-evaluate

public expenditure management

institutions to enable the Government to

fulfill a changing role, one more focused

with efficiency and effectiveness in

service delivery and supporting an

engaging competitive private sector.

These reports also highlight that budget

reform needs to be developed in tandem

with other public sector reforms.

iii) The IFMS/EPICOR Audit Report commissioned by the office of the Controller and

Auditor General (CAG) recommends critical areas for strengthening the institutional

capabilities and harmonization of IFMS systems and tools across MDAs and LGAs.

iv) A recent IMF review of Tanzania’s Public Financial Management underlines that

MDAs strategic plans are not always framed within an assessment of the likely

available medium – term financing. It is acknowledged that considerable emphasis is

put on aligning expenditure allocations with government’s strategic policies and

priorities focusing on activity –based budgeting process. Addressing these issues will

Box 1: Evolving of PFMRP

Tanzania’s PFMRP evolved in the following phases:

PFMRP I: 1998 - 2004

This Phase implemented from 1998-2004 had

an objective of controlling expenditure,

introducing aggregate fiscal discipline and

contributing to stable macro-economic

growth. PFMRP I focused on minimizing

resource leakage, strengthening financial

control and enhancing accountability by

reforming budget process and introducing an

Integrated Financial Management System

(IFMS).

PFMRP II: 2004- 2008

The objective of Phase II was to progressively

modernize the processes, procedures and systems

involved in PFM through the implementation and

use of ‘best practice’ tools, techniques and

methodologies to improve revenue forecasting and

resource allocation for strategic priorities.

PFMRP III: 2008- 2011

The objective of Phase III was to ensure greater

predictability and availability of medium term

resources to executing agencies. The thrust was

about getting the tools, techniques, methodologies

and systems that were introduced in the previous

phase to work efficiently and effectively in an

integrated manner.

16

require that greater emphasis is given to the initial strategic phase of budget

preparation with a stronger program level focus thereby enhancing the effectiveness

of the overall expenditure and having positive impacting on service delivery. The

Government has embarked on program based strategic planning and budgeting

processes which will facilitate linkage to MKUKUTA/MKUZA and the Five Year

Development Planning.

Following recommendations from the above reports, the Government has embarked on

a comprehensive and integrated PFM reform program to address major challenges by

developing PFMRP IV strategy.

1.2 Purpose of the PFMRP IV

The PFMRP IV aims at strengthening and improving public financial management

systems in a more coordinated manner in order to meet the current fiscal policy

challenges. Formulation and implementation of Phase IV will enable reforms in the

areas of revenue management, planning and budget management, budget execution

transparency and accountability, budget control and oversight and program

management, monitoring and communication including change management. Hence,

the reform agenda is programmed so as to attain a more effective and efficient budget

formulation, implementation and control in order to contribute to broad-based economic

growth as well as a vibrant private sector development in a sequenced manner.

1.3 Main actors

The Ministry of Finance (MoF), is responsible for public financial management within the

Government thus it has the overall role and mandate of coordinating implementation of

the PFM reform program. The Government intends to implement PFMRP IV focusing on

five Key Result Areas namely: Revenue Management; Planning and Budgeting; Budget

Execution, Transparency and Accountability; Budget Control and Oversight; and Change

Management and Program Monitoring and Communications including supporting

development of a comprehensive Public Financial Management Reform Program

strategy for Zanzibar (ZPFMRP). Thus the main actors will be all MDAs specifically

including TR, NAO, TRA, BoT, PPRA, PAC, LGAs, and Zanzibar.

17

1.4 Implementation Period

It is planned that the implementation cycle of Phase IV will be for five financial year

from July 2012 to June 2017. This period is intended to achieve both short term and

medium term results, recognising that short-term wins can be attained, while ensuring

that synergies and sequencing are maintained to ensure realistic results in the medium

and long term.

1.5 Financing of the Programme

PFMRP Phase IV is estimated to cost a total amount equivalent of Tsh 118 billion to

finance the five Key Result Areas. The Government and Development Partners are

committed to financing implementation of PFMRP IV. The five year work plan is found

in volume II.

18

CHAPTER TWO

2.0 SITUATIONAL ANALYSIS

2.1 Overview of current PFM

The Vision 2025 and MKUKUTA/MKUZA II affirm that new challenges are emerging

including the need for a greater focus on value for money and effectiveness in order to

maintain prudent management of public resources. Tanzania has maintained a strong

record of fiscal prudence including tax revenue collection performance which has in turn

firmed up the basis to furthering macroeconomic stability and sustained expansionary

economic policy. Literature recognizes that reforms in PFM has contributed to preserve

fiscal discipline and achieve poverty reduction and improved local governance in

Tanzania over the past decade3. Instruments such as the Public Expenditure Review

(PER) and the Medium Term Expenditure Framework (MTEF) and strategic plans have

been introduced as part of the enhanced Highly Indebted Poor Countries (HIPC)

initiatives since 2001 and implemented successfully in all Ministries, Departments and

Agencies (MDAs), with the purpose of maintaining spending under the prescribed limits

and linking policy objectives to multi-year budgets. Despite various reforms in PFM the

Government has nonetheless come to a point of realizing the importance of pursuing a

more inclusive, coordinated and integrated approach to implementation of PFMRP in

order to achieve greater gains in tax administration, make a more efficient use of public

resources, set a more appropriate fiscal policy framework and achieve greater

development results. This becomes more necessary as GoT continues to support

stimulus measures aiming at rapid public investment growth and less fiscal risks and

seeks to better respond against global shocks through improved fiscal adjustment and

developing other suitable fiscal policy and plans.

3 Andy Wynne (2005), “Public Financial Management Reforms in Developing Countries: Lessons from Ghana,

Tanzania and Uganda”; and De Renzio and Dorotinsky (2007), “Tracking Progress in the Quality of PFM Systems

in HIPCs”.

19

2.2 PFM Reforms

The Ministry of Finance has been steadfast and instrumental in spearheading past and

ongoing PFM reforms. Gaps in revenue administration, planning, budget preparation

and execution, backlogs in cash and debt management, reporting, procurement,

payment processes, and oversight have been the basis for initiating various PFM reform

interventions.

2.2.1 Revenue Management and Tax Administration

Domestic Revenue Collection

Tanzania faced fiscal challenges arising from the gap between low pace of domestic

revenues and large public expenditures. Low Tax compliance was endemic as a result of

weaknesses in the revenue collection system, poor infrastructure, and antiquated

business processes.

In tackling the challenges in revenue administration, the Government established

Tanzania Revenue Authority (TRA) in 1996, which has markedly improved tax

administration as evidenced by significant increase in revenue collection. Moreover, TRA

has demonstrated effectiveness in revenue administration by introducing Tax payers

Identification Number (TIN), e-filing, and diversifying modes of payment, and effecting

reforms in tax administration, it has however, not been able to resolve key issues

including strengthening of linkages between domestic taxes and customs databases

and other major central database e.g National Civil Registry, social security thus

enabling to improve tax registration and monitoring of medium- and small-size

taxpayers brewing tax evasion and avoidance. The Government continue to provide

guidance on how to better overcome long-pervading deficiencies in non tax revenue

collection by MDAs, RSs and LGAs. The structure of levies and user fees as well as

institutional capacities within MDAs, RSs and LGAs remain complex and deters

achievement of effective, efficient and transparent collection of non tax revenues. In

20

line with this, the productive capacities and corporate earnings within parastatal

companies and public corporations need to be strengthened.

External Resources Mobilization

In order to reduce transaction cost in mobilization of foreign resources, the GoT and the

Development Partners jointly developed the Joint Assistance Strategy for Tanzania

(JAST) in 2006. The JAST, as a medium term strategy, has put in place a framework for

dialogue between the GoT and DPs. The Aid Management Platform (AMP) System was

developed to enhance transparency on issues pertaining to disbursing and reporting of

foreign resources and projections in a more timely and regular basis and in

concordance with to the budget calendar.

2.2.2 Planning and Budgeting

The government has developed a Medium Term Strategic Planning and Budgeting

Manual (MTSPBM) that guides MDAs, RSs and LGAs in planning, budgeting, monitoring,

evaluation and reporting. The key documents include the Planning and Budgeting

Guideline (PBG), the budget speech; the estimate books and the background to the

budget and medium-term framework (BBMTF). The Government has also updated its

financial statistics by upgrading GFS codes from 1986 to 2001 series. Furthermore,

since 2010/11 the Government budget system has been upgraded so as to enable

reporting according to Classification of Functions of Government (CoFoG). A salient

feature in reforms of budget preparation is the stepped up commitment towards

transitioning to program-based budgeting, whose implementation is expected to start in

the financial year 2012/13.

The Government improved the Medium Term Expenditure Framework (MTEF) by

updating theMacroeconomic Modelling Tool (MACMOD) tool for projection of macro-

economic variables and building capacity on financial programming and projections; the

tool for resource allocation - Strategic Budget Allocation System (SBAS) and the

21

Planning and Reporting (PLANREP) system for LGAs. Expenditure tracking and

performance monitoring mechanisms have been instituted and institutional

arrangements are in place to conduct periodic follow-up of funds disbursed for budget

execution including inspection of projects.

2.2.3 Budget Execution, Accountability and Transparency

Procurement

The Government enacted the Public Procurement Act 2004 (PPA, 2004) along with its

2005 regulations which resulted into inter alia the establishment of the Public

Procurement Regulatory Authority (PPRA) and the Public Procurement Appeals Authority

(PPAA). In addition, the MoF established the Public Procurement division with a

mandate to oversee the development of public procurement policy and procurement

cadre. In 2007 the Government amended the Local Government Procurement

Regulations to enable LGAs use the PPA, CAP 410.

Procurement audits have been conducted in 219 entities, and these have confirmed

that the average level of compliance with the Act (PPA) increased from 39% in 2006/07

to 65% in 2009/10, to 68% in 2010/11 while follow up audits showed that compliance

level has improved from 71% in 2008/09 to 73% in 2009/10 and 75% in 2010/11.

A web-based Procurement Management Information System (PMIS) was developed in

2008 and 243 PEs have been registered as of June 2011. The system facilitates PEs to

submit procurement plans and implementation reports to PPRA. In addition, there has

been increased transparency, awareness and access to procurement information

published through the weekly Tanzania Procurement Journal and the PPRA website

(www.ppra.go.tz).

The Government has introduced a system for procurement of common use items and

services, by establishing the Government Procurement Services Agency (GPSA) which

arranges for Framework agreements with suppliers and services providers operating

22

under such system. The System has simplified procurement of common items, and

Procuring Entities (PEs) are now saving both time and transaction costs, normally

associated with carrying out tendering proceedings. The public Procurement Policy Unit

(PPU) was established under the Ministry of Finance to formulate and oversee

implementation of procurement policy. The Unit is also mandated to ensure that a

professional public procurement cadre is developed, coordinated and properly

supervised.

Debt Management

In the year 2004, the Government amended the Government Loans Guarantees and

Grants Act No. 30 of 1974 to empower the MoF to borrow and receive grants. This

aimed at curbing haphazard borrowing which landed the Government into the debt

crisis in the 1980s. The Act established among other things the Technical and National

Debt Management Committees (TDMC and NDMC); the latter acting as a technical arm

to the NDMC and the former taking an advisory function to the MoF on borrowing and

grant seeking matters.

Cash Management

Cash Management in the context of the Government entails an effective and efficient

management of the Government resources in the way and manner stipulated in the

Finance Act, Regulations and International Public Sector Accounting Standard (IPSAS).

During the financial year ended 30th June 2008 the Government adopted the

International Public Sector Accounting Standard (IPSAS) – Cash basis of accounting.

This has improved the content, credibility and quality of cash flow plans for revenues

and expenditures, good banking arrangement system and effective utilization, and

reporting of public funds. The Government aims to have right amount of cash and on

time for the service delivery units.

23

The Government has been implementing IFMS/EPICOR in the MDAs since the year

2000. Currently all MDAs and several LGAs use the IFMS/EPICOR to process the

financial transactions and provide input for the preparation of financial statements.

Implementation of the recommendations of a system audit carried out by NAO has

enhanced efficiency and effective use of the system.

Public Access to Fiscal Information (Accounting and Reporting)

The Government continues to facilitate improved public access to fiscal information

through website, local newspapers, Government gazette, notice boards, radio and

television. The information include planning and budget guidelines, financial

legislations, annual budgets, budget execution reports, financial statements, audit

reports and contract awards, and allocation of budget resources. In general, access to

fiscal information has improved in recent years, notwithstanding a few key missing

elements and quality controls which undermine integrity and accuracy of financial

reporting. A “Citizen Guide to the Budget” is published by a non-governmental

organization to enhance public awareness to fiscal information.

2.2.4 Budget Control and Oversight

Internal Control and auditing

In recent years, the importance of the internal audit profession has gained significantly

within the country. The Institute of Internal Audit (IIA) was established in 2006 to

promote greater awareness and facilitate accredited training to Internal Auditors.

Another salient feature in PFM reforms is the creation of a centralized internal audit

function within the MoF Department of Internal Auditor General established in 2010.

This is sought to strengthen the PFM mandate and capacity of the MoF so as to provide

technical guidance for internal auditors across MDAs and LGAs and be the only

responsible agent on behalf of Government suiting and channeling of new international

24

standards and unifying of national procedures and controls in accordance with best

practices.

External Audit and Oversight

The Government strengthened audit and oversight functions through enactment of the

Public Audit Act No.11 of 2008 which empowered and enhanced operational

independence of the Controller and Auditor General (CAG) and the functions of the

Parliamentary Accounts Committees in order to ensure accountability in PFM. The CAG

capacity was strengthened through recruitment, training and provision of tools,

equipment and office accommodation. Moreover, the CAG has taken measures to

improve external audit performance through the introduction of a risk-based audit

methodology and recently has embarked on the automation of the audit process as a

remedial measure and further training in other audit activities. As a result, there has

been increased compliance with financial legislation and regulations as evidenced by

CAG audit reports. The reports show that unqualified audit opinion for Central

Government (MDAs and RSs) increased from 70 percent in 2007/08 to 77 percent in

2009/10.

2.2.5 Change Management, Programme Monitoring and Communication

Program Administration and Management

The mainstreaming of PFMRP into MoF structures has been generally effective. The

capacity of the Government structures to design and implement reform activities

outside the enclave of Reform Secretariat has improved significantly. Furthermore,

there is improved coordination and dialogue between and among the various

stakeholders of the programme. Some of these initiatives include the Lushoto4 retreat

which intended for team building and introspection; joint sessions for development of

MTSPB Manual, MKUKUTA/MKUZA, strategic planning and MTEF; and other meetings.

4 Objective of Lushoto retreat was to build improved dialogue and trust between the various PFMRP stakeholders and improve

networking.

25

Despite some of the noted achievement regarding mainstreaming of PFMRP into

government structure, the design of previous phase posed a challenge in integrating

PFMRP into the existing institutional structure. Most of PFMRP III components were

designed according to functions and not necessarily matching with the program

expected results and apart from components that are within the Ministry of Finance, the

rest are seemingly projects in respective MDAs.

Communication

The Government established Information, Education and Communication units in all

MDAs with a view to improving public access to information. The capacity of the MoF

unit needs to be strengthened for smooth communication and improve timely

dissemination and sharing of information among all stakeholders.

Support to Zanzibar

Under the previous phases funds had been allocated to strengthen capacity building in

public financial management to the Zanzibar Accountant General and the Controller and

Auditor General. These efforts have resulted in installation of IFMS, improved budget

management and auditing in Zanzibar. Under PFMRP IV it is intended to support the

development of a strategy for a full fledged reform program designed for Zanzibar. The

proposed reforms are expected to include revenue management and strengthening

capacity in financial management.

2.3 Other Core Reforms in Tanzania

Apart from the Public Financial Management Reform Program the other core reforms

being undertaken in Tanzania are Local Government Reform Programme (LGRP), Public

Service Reform Programme (PSRP), Second Generation Financial Sector Reform

26

Program, Business Environment Strengthening for Tanzania (BEST), and Legal Sector

Reform Programme (LSRP).

The essence of the Local Government Reform Programme (LGRP) is to devolve

functions and responsibilities, political powers and authority, human and financial

resources from the central to the local government authorities levels and thus

enhancing accountability under the auspices of Government’s policy on Decentralization

by Devolution (D by D). The extent, to which these reform programs results into

improved service provision depends on the quality of local governance as well as status

of financial management in the public sector.

The public service reform program aims at enhancing capacity, performance and

accountability of MDAs and LGAs in the use of public resources and improves service

delivery to levels consistent with timely and effective implementation of strategies and

priorities. Enhanced performance could as well be evidenced by improvement in policy

making, improvement in the use of performance management systems by MDAs and

LGAs, improvement in the management of public servants, and greater access to

information and responsiveness to the demands of stakeholders.

The Second Generation Financial Sector Reform Program intend to improve the

management structure and financial growth of the financial sector and also to stop

further mismanagement in the financial sector which was experienced in the 1990s.

The Government of Tanzania with the support of donors is implementing the Program

for Business Environment Strengthening for Tanzania (BEST) whose objective is to

deliver a more conducive environment for doing business in Tanzania. The BEST

Program addresses key constraints in the legal and regulatory environment for business

and outlines the most effective measures to resolve them.

The Legal Sector Reform Program has the objective of ensuring speedy dispensation of

justice, affordability and access to justice for all social groups, integrity and

27

professionalism of legal officers, enhanced independence of the judiciary, and ensuring

high standards of legal and regulatory framework.

2.4 Strengths identified in the Tanzania PFM systems

The Government has implemented a number of PFM interventions which ultimately led

to gains in credibility of the budget, financial recording and reporting, and fiscal

oversight. Sound macroeconomic policies and a prudent fiscal management strategy

have underpinned Tanzania’s position as one of the best performing public financial

management system in Sub Saharan Africa (PEFA Report, 2006). As a result of the

impact of the global financial crisis and the stimulus recovery, policies are being

appropriately redirected away from short term demand management and expanding

resources towards medium term considerations and achieving higher quality standards

as a result of improved service delivery.

Significant reforms are still required to build on the strengths gained over time which

include the following:

i) Strong commitment by the Government of Tanzania to undertake PFM reforms to

a new stage;

ii) Strengthened MoF, macro-fiscal policy role and the introduction of a Medium-Term

Expenditure Framework so as to enable a more effective formulation and

disciplined use of the budget according to revenue and development targets on

the aggregate;

iii) Aligning planning timeframe with MKUKUTA/MKUZA II and by a global

performance framework for all public agencies and executing units including the

development of the five year development plan- ongoing review of the Public

Finance Act, the Public Procurement Act, Public Audit Act and other relevant

legislation concurrently with the formulation of a new phase of the PFMRP and

ensure a wide coverage and coordination of the newly revised components in the

reform agenda;

28

iv) Successful rollout of the IFMS/EPICOR to all MDAs, RSs and 86 LGAs with

simplified and automated means to ease financial recording and reporting and the

MOF to exert a major successful role in implementing commitment controls

throughout the payment system in a centralized manner. This will continue to

improve the quality of planning and budgeting controls as the new phase enter

into operation;

v) Adoption and use of International Public Sector Accounting Standards (IPSAS),

International Standards on Auditing (ISA), and International Professional Practices

Framework (IPPF) for Internal Auditors;

vi) Introduction of Electronic Fund Transfer (EFT) and Tanzania Interbank Settlement

System (TISS);

vii) Ongoing reforms to foster effective management of both external and domestic

debt;

viii) Ongoing reforms in payroll controls, procurement, and tax regimes;

ix) Strengthened oversight functions committees to enforce implementation of CAG

recommendations;

x) Revision of Legal and Regulatory Frameworks to enhance control and

accountability; and

xi) Continued strengthening of NAO and PPRA to carry out control and oversight

functions over the procuring entities.

2.5 Challenges identified in the Tanzania PFM systems

While the traditional budget system and the new features introduced in recent years

have enabled Tanzania to observe fiscal discipline and stability, the system’s continued

effectiveness and the management of public resources are being challenged. The main

challenges of the current PFM system can be summarized as follows:

i) Macroeconomic and fiscal forecasting;

ii) Linkages between development spending and the recurrent cost of the development

budget;

29

iii) Predictability of the budget execution;

iv) Harmonization of external and domestic debt systems;

v) Project and contract management; and

vi) Timely responding to audit recommendations.

To address these PFM challenges, the Government has embarked in the staging of a

comprehensive and integrated PFM reform program based on the PEFA analysis and the

other reports mentioned in the first Chapter. Five Key Result Areas have been identified

which are: Revenue Management; Planning and Budgeting; Budget Execution,

Transparency and Accountability; Budget Control and Oversight; and Change

Management and Programme Monitoring and Communications.

30

CHAPTER THREE

3.0 PERSPECTIVES OF PFMRP IV

3.2 Goal

The overarching goal of Tanzania’s PFMRP is to attain a Sound financial management

and discipline in public service delivery for sustainable development. Compared to

previous phases, the PFMRP IV will strategically focus on critical PFM actions which aim

at improving coordination primarily between revenue management, fiscal policy and

planning while prioritising those agencies and actions that will have cross cutting effect

on the full PFM system. Further, the programme will focus on improving MTEF

credibility, budget control and oversight, and deepening into better linking planning and

budgeting, cash and debt management, while migrating towards accrual accounting,

financial accountability and transparency.

3.3 Main Objectives

The main objective of the PFMRP IV is to support the National Strategy for Growth and

Reduction of Poverty – MKUKUTA/MKUZA II through implementation of the five year

National Development Plan to attain the objectives of Vision 2025.

3.4 The PFM reform Key Result Areas

The Government is defining its PFM reform priorities, subsequent reform activities and

sequencing of the implementation process according to MKUKUTA/MKUZA II. Further,

the PFM reform agenda will serve as a useful tool for dialogue between Government

and development partners about the provision of harmonized support to the

Government’s PFM reform efforts. PFMRP Phase IV is intended to address the identified

31

critical limitations in the public financial management systems based on five Key Result

Areas (KRAs): Revenue Management; Planning and Budgeting; Budget Execution,

Accountability and Transparency; Budget control and Oversight; Change Management

and Programme Monitoring and Communications as well as strengthening

Government’s capacity to improve service delivery.

Considering the need for attaining a comprehensive approach, the reform will address

the following Key Result Areas (KRAs) with Senior leads indicated in : 1) Revenue

Management (Commissioner Policy Analysis), Planning and Budgeting (Commissioner

for Budget), Budget execution, transparency and Accountability (Accountant General),

Budget control and oversight (Internal Audit General), Crosscutting issues (including

change management and Program management) (Director for Planning Division).

The identified KRA structure concurs with MoF structure PFM implementation

stakeholders and is reflected in the common assessment framework for PFM-PEFA. In

addition, it specifically focuses on cross-cutting institutional issues, such as training, ICT

systems, change management and communication etc.

The M and E details Outcomes, Outputs, Performance indicators, Baselines, Targets and

Milestones. Based on the M and E framework the work plan, details outputs, milestones,

timing, resources and responsible person.

The particular choice and inclusion of components in the PFMRP Phase IV was informed

by two main factors; i) functional considerations within the MoF and ii) the

organizational structures pertaining within the Government of Tanzania.

Accountability for performance and sustainability considerations also justify an emphasis

on reflecting the organizational structure in the particular breakdown of PFM reform

components. Hence most components have a departmental “home” and are linked to a

“KRA lead”, see Table 1.

32

Table 1: KRA and components overview

KRA

Major Component, Department and KRA-TWG

1. KRA 1: Revenue Management,

Leader: CPAD

Commissioner for Policy Analysis Department

(CPAD) – MoF Treasury Registrar (TR) - MoF

Prime Minister’s Office – Regional Administration

and Local Government (PMO-RALG)

Commissioner External Finance - MoF

MDAs

2. KRA 2: Planning and Budgeting,

Leader: BC

Commissioner for Budget (CB) – MoF

CPAD – MoF

PMO-RALG

3. KRA 3: Budget Execution,

Transparency and Accountability,

Leader: AccGen

Public Procurement Regulatory Authority (PPRA)

Public Procurement Policy Unit

Accountant General (ACCGEN) - MoF

CPAD - MoF

Government Asset Management - MoF

4. KRA 4: Budget Control and

Oversight,

Leader: IAG

Internal Auditor Department - MoF

National Audit Office (and Parliament PACs)

TR

5. KRA 5: Change Management

Programme Monitoring and

Communication,

Leader: DPD

Department for Financial Management

Information System (DFMIS) - MoF

Government Communication Unit - MoF

Department for Planning Division – MoF

Support to Zanzibar

PMO – RALG

ACGEN - MoF

DAHRM - MoF

As the table indicates most KRAs have many actors/stakeholders contribution to the

Outcomes. It is evident that linkages between and across most components will need

close collaboration in order to achieve the intended outcome. As such, IAG, NAO and

PPRA as well as the TR and the Parliament (PACs) need to converge efforts, liaise and

collaborate to contribute to improvement in budget control and oversight functions.

33

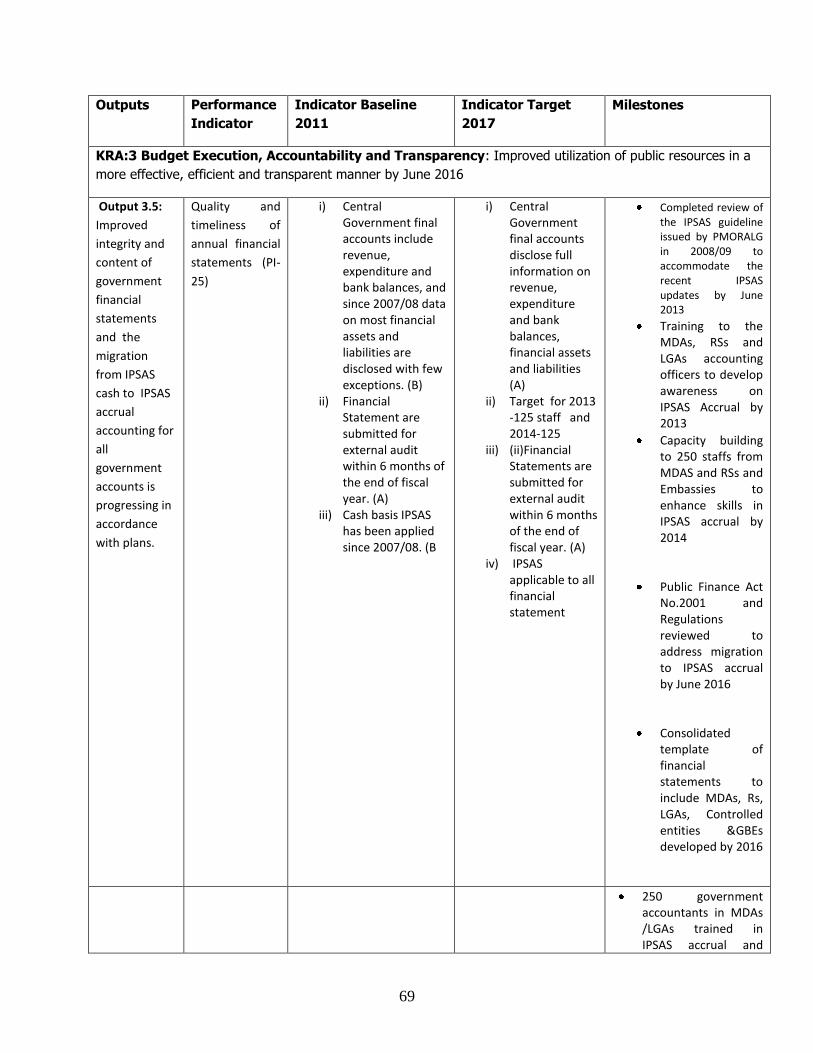

3.5 Intermediate Results

The intermediate results of PFMRP IV, to be achieved by fiscal year 2015/2016 are:

i) Coordinated, comprehensive PFMRP effectively sequenced and supported by a

consistent and harmonised legal and institutional framework;

ii) Utilisation of sound and comprehensive macroeconomic analysis, macro fiscal

forecasting for a credible and transparent budget process and utilisation of MTFF.

iii) Realistic revenue forecasting, collection and management;

iv) Enhanced accuracy in forecasting and reporting of domestic and external cash

resources;

v) Improved reporting and corrective action to enhance quality and completeness of

report on financial statements and audits; cash and debt management;

vi) Establishment of a clear sequenced and coordinated roadmap for support and

implementation of “high impact” implementing agencies and initiatives such as

program-based budgeting, Internal Audit, DFMIS, Treasury Registers, AcGEN,

PMORALG and Revenue management;

vii) A global performance and monitoring framework and establishing of strong

linkages between policy objectives and public expenditure by means of sector-led

MTEF and costed strategic plans; and

viii) Institutional and Standardized training modules established where relevant.

Therefore, Implementation of PFMRP IV will pursue achievement of the hierarchy of

results at Outputs, Outcomes and Impact level as indicated in M&E Result matrix.

PFMRP IV result chains follow the logical sequence of cause-effect relationships

between Impact, Outcomes, Outputs, Activities and Inputs which are monitored by the

M and E framework. PFMRP Stakeholders did a thorough problem analysis through a

logical framework approach to identify what the Programme is accountable for in

contributing to the Impact and Outcomes and what it is accountable for delivering

outputs. For each output, several milestones were identified as a means to achieve

34

short term results. The use of Results-Based Management from the design stage of

PFMRP IV is expected to improve program and management effectiveness and

accountability by orienting all the implementation cycle towards achieving the desired

results.

3.6 Key Drivers

The main drivers for PFMRP IV include the need to: enable realisation of Vision 2025;

develop an effective and efficient PFM system in the country; facilitate implementation

of MKUKUTA/MKUZA II; address taxpayers’ demands for better services; enhance good

governance; and address emerging PFM challenges associated with the changing needs

in a dynamic and evolving global economic environment.

3.6.1 Enabling Realisation of Tanzania Development Vision 2025

Realisation and operationalisation of Tanzania Development Vision 2025 (TDV 2025)

depends on a good public financial management system. The vision envisages Tanzania

to become a middle income country characterised by: high quality livelihood; peace,

stability and unity; good governance; well educated and learning society as well as

strong and competitive economy. These aspirations, in particular good governance

require transparency and accountability in public financial management. Similarly, a

strong and competitive economy is to be underpinned by robust planning, sound

resource prioritisation, financial discipline and ability to generate sufficient revenue. This

provides the first rationale for developing PFMRP IV.

3.6.2 Facilitating Implementation of the Five Years National

Development Plan

The Government has prepared the first Five Year Development Plan (FYDP 2011/12 –

2015/16) with the goal of unleashing the country’s resource potentials in order to fast

35

track the provision of the basic conditions for broad-based and pro-poor growth. PFMRP

IV is embracing all three salient features of FYDP which are : a shift from need based

planning to opportunity-based planning; strong emphasis on growth while focusing on

human resource skill development and high drive and scaling up on the role and

participation of private sector in economic growth. In order to attain the main goal of

FYDP, it is necessary to implement PFM interventions which will assure a sound PFM

system to enable effective and optimal resource utilization.

3.6.3 Facilitating Implementation of MKUKUTA/MKUZA II

MKUKUTA/MKUZA II translates Vision 2025 aspirations and MDGs into measurable

broad outcomes organised in three clusters. Cluster I: Growth for reduction of income

poverty; Cluster II: Improvement of quality of life and Social well being; and Cluster III:

Governance and accountability. Moreover, MKUKUTA/MKUZA II is linked to sector

policies and strategies through the operational targets. For effective implementation,

sectors align their strategic plans with MKUKUTA/MKUZA II. Therefore, in order to

attain MKUKUTA/MKUZA II goals, a sound PFM system is essential across the

MKUKUTA/MKUZA clusters.

3.6.4 Taxpayers Demands for Better Services

In the recent years there has been an increase in demand by taxpayers for better

services. The better services are manifested by enhanced transparency and

accountability, value for money on public expenditure and responding to amongst

others requirements of the Parliament regarding public resource management.

3.6.5 Enhancing Good Governance

Good governance has been emphasized in Tanzania Development Vision 2025 and

MKUKUTA/MKUZA II and is a fundamental component in shaping a favourable

environment for economic growth and poverty reduction. It is given the central role in

36

reaching national goals and objectives. These include ensuring systems and structures

of governance support and upholding the rule of law.

3.6.6 Effective and Efficient PFM System

The ability to generate sufficient revenue and external resource mobilisation still

remains a challenge in the country. PFMRP IV will assist in addressing the challenge

through articulating enforcement of tax laws, rules, laws and regulation, widening the

tax base, better management and control of retention and roll over funds, proper

channelling of revenue from collection points to the treasury and the management of

non tax revenue. Moreover, systems and procedures for optimal mobilisation, allocation,

funds flows, spending of and accounting for public resources are still required.

3.6.7 Addressing PFM Challenges

As PFM challenges are still in existence, there is a need to continue formulating

strategic interventions for addressing them. PFMRP IV strategy builds on internal and

external reviews in the last seven years which, besides the above mentioned reports

(primarily PEFA and CAG reports), include the Campo Review (2005), the Paul review

(2007), Hawkins report (2009), the Lushoto retreat report and the supervision mission

reports of 2010 and 2011. The reviews have acknowledged significant PFM

achievements in the country and remain challenges to be addressed. The government

has decided to develop this strategy which will address the observed PFM challenges in

the next five years (2011 – 2016). The strategy will consolidate achievement and

deepen reforms to take into account noted challenges and emerging development

issues. It is noteworthy appreciated that there will always be some PFM challenges as

the economy is dynamic and hence the need to keep PFM systems current and in

robust.

37

3.7 Anticipated Success Factors

The success of this strategy will depend on a number of strategic imperatives which

include: capacity building; enabling legal framework and supportive institutional setting;

effective communication, coordination and dialogue; commitment of top leadership and

key stakeholders; as well as an effective and functional M&E system.

3.7.1 Capacity Building

In the earlier phases focus was on implementing PFM capacity building initiatives in the

areas of human resources development, retooling and improving working environment.

However, inefficiency in the programme design resulted into failure in reporting on

training impacts. It is envisaged in the short term, mapping exercise for capacity

building and draw on identified institutions that will develop and deliver PFM specific

modules. In the long term, it is expected that local training institutions to pick up the

opportunity and offer public finance, accounting and procurement certificates/courses.

Hence, this will enable the training institutions to sustainably provide short and long

term PFM training.

3.7.2 Enabling Legal Framework

In cases where the existing laws, rules and regulations are not harmonised or do not

support public financial management, at the Central and Local Government, they will be

reviewed, amended and their enforcement will be pursued in earnest.

3.7.3 Effective Communication, Coordination and Dissemination

Effective communication, coordination, dissemination and sharing of information among

all stakeholders are vital towards the success of the programme. Further, dialogue

among key players is necessary for transparency and accountability of public finance

management.

38

3.7.4 Commitment of Top Leadership and Key Stakeholders

Commitment of the top leadership and implementing agencies is vital for the success of

the programme; this will also ensure ownership and commitment among technical staff

who will be implementing the programme. PFMRP IV intends to carry out change

management programme that will create change champions and also develop

comprehensive communication strategy.

3.7.5 Effective and Functional M&E System

An effective and functional program monitoring and evaluation system (M and E

Framework) has been developed. It has been based on the PFMRP IV strategy focus

and influenced by the PEFA framework. This will assess whether or not the Programme

objectives are being realized and thus will be the basis for decision making.

3.8 Interventions of PFMRP IV

The MoF will be the main actor of the PFM reform agenda in collaboration with the

Planning Commission, PMO-RALG, PO-PSM, the Tanzania Revenue Authority, and other

key stakeholders. The Programme should clearly bring out the enhanced role of the

MoF as the custodian of Government resources in respect of planning and

recommending sound revenue and financing policies, allocating resources judiciously

and carrying out the required monitoring and oversight functions. Phase IV reforms will

be implemented across the following Five Key Result Areas:

3.8.1 KRA 1: Revenue Management

Improved revenue forecasting and mobilization is critical to support a credible and

sound budgetary process. Realistic revenue and cash flow forecasting, as well as

opportunities for cost recovery and cost-benefit sharing is a key aspect of reforms in

revenue management. The need to streamline the existing revenue policy function

39

within MoF has been identified in the action plan, as adequate tax statistics needed to

perform tax policy and other fiscal policy analysis are facilitated also with a view to

supporting more realistic revenue and cash flow forecasts. MoF will review the existing

legal and institutional arrangements for revenue collection. This will enable

development of a more appropriate model for revenue forecasts.

The Government will continue collaborating with development partners to improve

external resources management, integration with budget preparation and

implementation, to enhance predictability, accounting for and reporting on of public

resources. Furthermore, PFMRP IV will implement specific activities aimed at improving

retention scheme arrangements.

3.8.2 KRA 2: Planning and Budgeting

Despite the achievements made in planning and budgeting at central and local levels,

challenges still remain. PFMRP IV deems necessary to prioritize basic actions targeting

on macro-fiscal policy, planning, improved MTEF credibility, and extend the course of

adopting GFS2001 and CoFoG standards to facilitate program-based budgeting and thus

broaden the scope of the chart of accounts for enabling improved budget planning,

monitoring, recording, reporting, and accountability.

Medium-term expenditure framework

MTEFs exist for most MDAs and LGAs operating though with weak linkages between

recurrent and development estimates and between administrative and executing units.

One enduring limitation of MTEFs relates to the recurrent budget format, which is

mainly administrative (i.e., not program based) hence, it fails to capture the recurrent

costs that arise from development expenditure. In response to this, PFMRP aims at

establishing a policy-driven system that adheres to major upstream programmatic goals

which integrates recurrent and development spending into central operations of priority

programs and activities that bear results.

40

Linking national development and institutional plans to budgeting

Concurrently, a methodology will be developed as part of the Medium Term Strategic

Planning and Budgeting Manual (MTSPBM) so as to enable the national development

planning and the budgeting system to articulate national targets and institutional plans

across public organizations. A global performance framework will also be formulated for

planning and linking the programmatic goals to the desired sector and institutional

results and measuring performance against national priorities at the various lines and

levels of accountability.

Results-based Budgeting System

All the above interventions will lay the ground for enabling the Government to gradually

transitioning to a Results-Based Budgeting System (RBBS) through a detailed action

plan. The objective of these activities are to make PFM systems more results-oriented

as well as to increase accountability and transparency; to provide and use information

on performance for policy planning and management in order to enhance efficiency and

effectiveness in budget preparation, execution and oversight. Introduction of RBBS will

ensure that financial resources are allocated on the basis of outcomes to be achieved,

by matching program costs with program results, and by comparative assessments of

program efficiencies, effectiveness and relative worth in producing the desired results.

3.8.3 KRA 3: Budget execution, accountability and transparency

This KRA aims at achieving greater predictability for spending units, increased efficiency

throughout the public sector and maintaining sustainable debt levels. Key activities will

address deficiencies in procurement processes, cash and debt management and

accounting and reporting.

Procurement

Most of MDAs and LGAs face capacity constraints in procurement and contract

management in implementing programs and ensuring achievement of value for money.

41

PFMRP IV will focus on building capacity in the Procurement Policy Unit and in

preparation of procurement plans, bidding /tendering documents, evaluation of

bids/proposals negotiation skills and contracts management as well as asset

management. The capacity for PPRA will also be enhanced to carry out procurement

compliance audit and facilitate infrastructure for e-procurement. The policy and legal

framework for public procurement will also be instituted.

Cash and debt management

PFMRP IV has set out critical activities that will gear towards improving consolidation

and reporting of Government cash balances by closing numerous bank accounts held by

spending units; devising a Treasury Single Account (TSA) structure inclusive of revenue

and expenditure sub-accounts managed and maintained through the Bank of Tanzania;

allowing overnight sweeping and clearance of tax collections on a daily basis; and

building capacity of MDAs, RSs, LGAs and PAOBs in the development of accurate and

realistic revenues and expenditures projections. PFMRP will facilitate establishment of a

debt management office, consolidation and reporting of public debts by establishing a

single unified data base.

Accounting and reporting

PFMRP IV will implement activities aimed at improving the scope and quality of financial

recording and reporting. Moreover, the PFMRP will support harmonization of existing

accounting and reporting systems, review the legal and regulatory framework, and build

capacity of accounting cadre and the migration towards accrual accounting. Other

activities will target financial reporting and presentation of key budget execution reports

as well as other review and fiscal reports.

3.8.4 KRA 4: Budget control and oversight

PFRMP IV will act promptly to strengthen Internal Audit Department, oversight function

of the National Audit Office and TR capabilities to oversee the public finances of Public

Enterprises.

42

Internal control and internal audit

The programme will strengthen the Internal Auditor General’s Department within MoF

that will provide technical guidance to internal auditors within MDAs, RSs, PAOBs and

LGAs. Other activities include capacity building to internal auditors so as to conduct

audits in a wide range of PFM areas and enhance governance.

External audit

The main intervention of National Audit Office (NAO) in PFM reforms is to conduct a

timely independent examination of the financial performance and report to the public to

ensure accountability and compliance with financial regulations. These reforms will

support NAO to become a well performing Supreme Audit Institution (SAI) in Africa

espousing the principles of good governance and accountability, implementation of

value for money, performance auditing and other modern methods of managing and

operating an audit institution.

Capacity to oversee Public Enterprises and Government Institutions

The Treasury Registrar (TR) is responsible for overseeing management and financial

accountability of the Government’s interests as a shareholder in public enterprises and

Government institutions. It advises the Government on all issues pertaining to those

investments. PFRMP IV will continue supporting TR in order to perform its core

functions effectively and efficiently. The support will include: developing Public

Investment Management Database; management of Public Enterprise; Reviewing and

harmonizing public investments Acts; implementing M&E system for Public investments;

and building the capacity of public enterprises and Government Institutions.

Parliamentary oversight

The Public Audit Act stipulates that CAG reports shall be followed up by the

Parliamentary Accounts Committees (PAC, POAC and LAAC). The enforcement of CAG

reports are facilitated by Parliamentary Accounts Committees during execution of their

duties. Parliamentary accounts Committees constitute new members after every three

43

years and after General election. These members are required to be trained in

understanding financial statements, CAG reports and on interrogation skills in order to

enable them execute their functions effectively. The main intervention in respect of

Parliamentary Oversight Committees in PFM reforms is to build capacity and also by

conducting training to their members and facilitating them to conduct physical visiting

to the projects implemented by the Central and Local Government as well as the

Parliament Secretariat.

3.8.5 KRA 5: Change Management, Programme Monitoring and Communication