public sector plan : resources and allocations - of planning

TRANSCRIPT

75

Overview

3.1. The chapter 2 of the volume has indicatedthe required level of public sector investments inthe Tenth Plan to be consistent with 8 per centgrowth of gross domestic product (GDP). Theseestimates form the basis for the minimum size ofpublic sector plan resources which are required tobe mobilised to achieve the plan objectives. Thischapter projects the public sector resources for theTenth Plan at Rs.15,92,300 crore (Rupees fifteenlakh, ninety-two thousand and three hundred crore,or approximately, Rs. 16 trillion) at 2001-02 prices.At comparable prices it amounts to an increase of67.4 per cent over the Ninth Plan realisation. Giventhe twin requirements of securing a sustainable debtburden and restricting the public sector draft onprivate savings to a reasonable limit, contributionof debt resources to the projected increase accountsfor 6.6 per cent only. Consequently, non-debtresources must contribute 93.4 per cent of theprojected increase in the Tenth Plan resources overthe Ninth Plan realization.

3.2. If the poor realisation of non-debtresources vis-à-vis the projections during the NinthPlan is anything to go by, the task of raising non-debt resources to the Tenth Plan target levels isquite difficult, although definitely not impossible.However, fiscal reforms in this regard assumecritical importance and are most crucial to attainingthe Tenth Plan targets. Reforms for raising the taxto GDP ratio, increasing user charges, compressingexpenditure on administration and establishmentand adherence to commercial principles by publicsector enterprises must attract focused attentionand generate time-bound results. This chapterreviews the Ninth Plan performance of both theCentre and States and Union Territories (UTs),projects the Tenth Plan resources, measures theincremental effort required over Ninth Planrealisation levels, proposes a set of policies for

attaining the Tenth Plan targets, and indicates theallocation of the public sector plan resources.

Resources of the Centre during the Ninth Plan

3.3. The Centre’s gross budgetary support(GBS) to the Ninth Plan was projected atRs.3,74,000 crore at 1996-97 prices includingRs.1,70,018 crore of Central assistance to theStates and UTs. With the Ninth Plan resources ofCentral Public Sector Units (CPSUs) projected atRs.2,85,379 crore, resources available for theCentral Plan was arrived at Rs.4,89,361 crore. TheNinth Plan realisation places the Centre’s GBS atRs.3,16,286 crore or 84.6 per cent of the projectedlevel. Central assistance to States’ and UTs wasrealised at Rs.1,38,394 crore or 81.4 per cent ofthe projected level. With realisation of CPSUsresources at Rs.2,28,795 crore or 80.2 per cent ofthe projected level, the resources available for theCentral Plan works out to 83.1 per cent of theprojected level or Rs.4,06,687 crore at 1996-97prices. Table 3.1 indicates the projection andrealisation of the Ninth Plan resources and itsfunding of the Centre.

3.4. The realised pattern of funding the GBSreflects a significant deterioration of non-debtcontribution vis-à-vis the Ninth Plan projections. Theshare of balance from current revenues (BCR) inGBS reduced to a negative 49.6 per cent as againsta projected share of a negative 0.7 per cent only.The realised share of borrowings therefore had toincrease to 144.1 per cent as against a projectedshare of 84.7 per cent, to bridge the BCR gap.

3.5. The 5,544 percent deterioration in BCRwas caused by stagnant level of revenue receiptsand substantial growth in non-plan revenueexpenditure (NPRE) in relation to GDP. Net Centralrevenues declined by 0.43 percentage points ofGDP from 9.23 per cent in 1996-97 to 8.80 in 2001-

CHAPTER 3

PUBLIC SECTOR PLAN : RESOURCES AND ALLOCATIONS

TENTH FIVE YEAR PLAN 2002-07

76

02. Tax revenue (net) decreased by more than 1percentage point from 6.85 per cent in 1996-97 to5.80 per cent in 2001-02. The fall in tax revenue(net) could not be compensated by a 0.69percentage points increase in non-tax revenue from2.38 per cent to 3.07 per cent during the sameperiod. As against a 1.05 percentage points fall intax revenue (net), the gross tax revenue of theCentre fell by 1.21 percentage points from 9.41 percent in 1996-97 to 8.20 per cent in 2001-02. Thisimplied that the impact of the fall in gross Centraltax revenues on Central finances was somewhatshared with the States.

3.6. The deterioration of the gross Central taxrevenues in relation to GDP has given rise toconcern on the following issues.

l Shrinkage of the tax base, as implied byinadequate coverage of the service tax base.

l Growth in various types of tax concessions andexemptions.

l Increase in the coverage of Modified ValueAdded Tax (MODVAT) without upwardadjustment of tax rates.

l General slackening of the tax administrationleading to revenue leakage.

3.7. The NPRE grew rapidly by 1.30percentage points of GDP from 9.30 per cent in1996-97 to 10.60 per cent in 2001-02. Thebreakdown of this increase is summarised in Table3.2.

3.8. Almost 40 per cent of the increase inNPRE was due to the growth in pension and salarypayments brought about by the implementation ofthe Fifth Pay Commission’s recommendations.Along with the growth in subsidies and other NPRE,mainly comprising defence, the massivedeterioration of BCR was the outcome of thestagnant levels of Centre’s revenue receipts.Borrowings had to increase to bridge the gap, whichconsequently raised the interest burden and led tofurther increase in NPRE, resulting in still sharperdeterioration of BCR. Increase in interest paymentsaccounted for a quarter of the total growth of NPREduring the Ninth Plan.

3.9. The debt-servicing burden, as reflectedby the percentage of interest payments torevenue receipts, increased from 47.1 per centin 1996-97 to 50.5 per cent in 2001-02, underliningthe fragile sustainability of the Centre’s debtburden. The debt burden of the Centre increasedby almost 8 percentage points from 49.4 to 57.5

Table 3.1Ninth Plan Resources of the Centre

(Rs. crore at 1996-97 prices)

Sources of Funding Projection Realization % Realisation

1. Balance from current revenues -2,778 -1,56,790 -5,544.0(-0.7) (-49.6)

2. Borrowings including net MCR 3,16,760 4,55,624 143.8(84.7) (144.1)

3. Net inflow from abroad 60,018 17,452 29.1(16.0) (5.5)

4. Gross budgetary support to plan 3,74,000 3,16,286 84.6 (1 to 3) (100.0) (100.0)

5. Central assistance to States & UTs -1,70,018 -1,38,394 81.4(45.5) (43.8)

6. GBS for Central plan (4+5) 2,03,982 1,77,892 87.2

7. Resources of public sector enterprises 2,85,379 2,28,795 80.2

8. Resources for Central Plan (6+7) 4,89,361 4,06,687 83.1

Note : Figures in parentheses are percentage of Gross Budgetary Support .

PUBLIC SECTOR PLAN : RESOURCES AND ALLOCATIONS

77

per cent of GDP during the same period. Thegross fiscal deficit of the Centre, which causedthis, grew from 4.88 per cent of GDP in 1996-97to 5.76 per cent in 2001-02, an increase of 0.88percentage points. Consequently, borrowings forfunding the GBS was 43.8 per cent above theprojected level.

3.10. The net inflow from abroad on governmentaccount, which is deployed for funding externallyaided projects (EAP) was projected to contribute16.0 per cent of the GBS in the Ninth Plan. However,its realization is placed at 29.1 per cent of the target,which reduces its realised share in plan resourcesto 5.5 per cent. The fall in net inflow from abroadhas been attributed to international sanctions,following the Pokharan nuclear tests and inadequateprovision for counterpart funding of EAP projectsthrough domestic resources.

3.11. Following from the lower realisation of theCentre’s GBS, Central assistance to the State andUT Plans also recorded a similar level ofachievement at around 81.4 per cent. Centralassistance as a percentage of GBS, which wasprojected at 45.5 per cent, declined to a level of43.8 per cent. The proportional impact of a shrinkingGBS on the quantum of Central assistance is clearlyin evidence here.

3.12. After accounting for the Centralassistance to States and UTs, the GBS left forthe Central sector Plan was projected to accountfor 41.7 per cent of the Central Plan resources.Internal and extra-budgetary resources (IEBR)of the CPSUs provided the remaining share at58.3 per cent. The realised share of IEBR in theNinth Plan is placed at 56.3 per cent indicating,

by and large, a similar deterioration as that ofGBS. In absolute terms, IEBR was realised at80.2 percent. Operational inefficiencies of theCPSUs accounted significantly for a lowerrealization of internal resources (IR).

Projection of the Tenth Plan (2002-07)Resources of the Centre

3.13. In keeping with the requirement ofstepping up public sector investments forattaining an 8 per cent GDP growth during theTenth Plan, the GBS of the Centre has beenprojected to grow from 4.33 per cent of GDP in2001-02 to 5.39 per cent in 2006-07. Thus, theTenth Plan projected average GBS stands at 4.93per cent of GDP as against the Ninth Planrealisation of 4.02 per cent.

3.14. Fiscal sustainability considerationsdemand a reduction in debt financing for funding ofGBS for the Tenth Plan. Accordingly, the grossfiscal deficit, which stood at 5.90 per cent of GDPin 2001-02 has been projected to reduce to 4.32per cent in 2006-07, obtaining a Tenth Plan averageof 4.73 per cent. The Ninth Plan average realisationhad stood at 5.82 per cent. The gross fiscal deficitis implicit in own borrowings, inclusive of netmiscellaneous capital receipts (MCR). Ownborrowings inclusive of MCR in the Tenth Plan areprojected at 4.78 per cent of GDP, down from 5.78per cent realised during the Ninth Plan. Net inflowfrom abroad, in the form of external assistance, isprojected at 0.19 per cent of GDP, slightlydiminished from 0.22 per cent realised during theNinth Plan.

3.15. The BCR is arrived at as a small negativeof 0.04 per cent of the GDP as against anegative1.98 per cent realised in the Ninth Plan.To achieve a BCR of this order, Central revenues(net) must grow from 8.80 per cent of GDP in 2001-02 to 9.98 per cent in 2006-07, an increase of 1.18percentage points. NPRE must come down from10.60 per cent of GDP in 2001-02 to 9.06 per cent,a decrease of 1.54 percentage points. Thus, animprovement of 2.72 percentage points in BCRduring the Tenth Plan is being sought mainly froma contraction of NPRE.

Table 3.2NPRE and its components of the Centre

(As a percentage of GDP)

Items 1996-97 2001-02 Increase

1. Interest 4.35 4.69 0.34

2. Pension 0.37 0.64 0.27

3. Salary 0.48 0.76 0.28

4.Subsidies 1.13 1.33 0.20

5.Other NPRE 2.97 3.18 0.21

6.(Total) NPRE 9.30 10.60 1.30

TENTH FIVE YEAR PLAN 2002-07

78

3.16. Central assistance to States and UTsduring the Tenth Plan has been projected at 42.5per cent of the Centre’s GBS. In relation to GDP,Central assistance to States and UTs is projectedat 2.09 percent in the Tenth Plan, up from 1.76per cent realised during the Ninth Plan. Afterdeducting Central assistance to States and UTs,GBS available for the Central Plan is arrived at2.82 per cent of GDP, an increase of 0.56percentage points over the Ninth Plan realizationof 2.26 per cent.

3.17. In order to meet the public sectorinvestment and savings requirements, IR of CPSUsis placed at 2.85 per cent of the GDP in the TenthPlan, up from 2.15 per cent realised during the NinthPlan. The railways and power sector CPSUs mustraise their operational efficiency to meet this target.The extra-budgetary resources (EBR) of CPSUswas projected at 0.75 per cent of the GDP, sameas the realised level obtained in the Ninth Plan.Thus, the IEBR of CPSUs is placed at 3.60 per centof GDP in the Tenth Plan.

3.18. With a GBS net of Central assistanceto State and UT plans projected at 2.79 per cent

and IEBR of CPSUs indicated at 3.60 per cent,resources available for the Central Plan arearrived at 6.39 per cent of GDP, up from 5.16per cent realized during the Ninth Plan, anincrease of 1.23 percentage points. Table 3.3indicates the resources of the Centre and itsfunding in the Tenth Plan.

3.19. The GBS of the Centre is placed atRs.7,06,000 crore at 2001-02 prices. Centralassistance to State & UT plans works out toRs.3,00,265 crore. After deducting Centralassistance to States and UTs, the GBS availablefor the Central plan is Rs.4,05,735 crore at 2001-02 prices. With an IEBR of CPSUs indicated atRs.5,15,556 crore at 2001-02 prices, totalresources available for the Central Plan isprojected at Rs.9,21,291 crore at 2001-02 prices.The Central Ministries have indicated an IEBRof Rs.4,87,448 crore, which falls short byRs.28,108 crore vis-à-vis the required IEBR. TheIEBR currently indicated by the Central Ministries,if taken in place of the projected IEBR, reducesthe Central resources for the Tenth Plan toRs.8,93,183 crore.

Table 3.3Projection of Tenth Plan Resources of the Centre

(Rs. crore at 2001-02 prices)

Sources of Funding Projection

1. Balance from Current Revenues -6,385(-0.9)

2. Borrowings including net MCR 6,85,185(97.0)

3. Net inflow from abroad 27,200(3.9)

4. Gross Budgetary Support to Plan(1 to 3) 7,06,000(100.0)

5. Central Assistance to States & UTs -3,00,265(42.5)

6. GBS for Central Plan (4+5) 4,05,735

7. Resources of Public Sector Enterprises 5,15,556

7.1. Internal Resources 4,09,000

7.2. Extra Budgetary Resources 1,06,556

8. Resources for Central Plan (6+7) 9,21,291

Note : Figures in parentheses are percentage of GBS.

PUBLIC SECTOR PLAN : RESOURCES AND ALLOCATIONS

79

3.20. A funding pattern as envisaged in Table3.3 is a challenging task, the extent of which couldbe gauged by comparing the Tenth Plan projectedlevels to the Ninth Plan realisation. Table 3.4indicates the Ninth Plan realization and the Tenth

Plan projection of resources of the Centre in relationto GDP.

3.21. The steps detailed in Box 3.1 will benecessary for achieving these targets.

BOX 3.1

l Comprehensive computerisation of the income tax system and universal usage of tax identificationnumbers in monetary transactions must be employed for facilitating improved enforcement of theincome-tax administration.

l The policy direction for removing unnecessary exemptions under corporate tax must continue sothat corporate income, liable to taxation, comes nearer to book profits as declared by the companies.

l The current policy of moving progressively to a truly single excise rate should continue to be pursuedwhile tightening up much more on existing exemptions, particularly those under small enterprises,all for improving tax compliance.

l The coverage of the service tax must be extended continuously under the union excise system sothat much greater tax buoyancy can be achieved through increased coverage of the economy as awhole.

l The extension of VAT at the State level must be taken up at the earliest for facilitating its integrationwith the Central VAT and bringing about harmonisation of tax rates levied by different tax jurisdictions.

l Peak customs tariff must be continuously lowered for enabling greater integration with the worldeconomy and consequently raising customs revenue through larger volumes of imports as wouldarise from expansion of international trade.

Table 3.4 Ninth Plan Realisation and Tenth Plan projection of Resources of Centre

(As a percentage of GDP)

Sources of Funding Ninth Plan realization Tenth Plan projections Increases(+)/Decreases(-)

1.Balance from Current Revenues -1.98 -0.04 (+)1.94

2.Borrowings including net MCR 5.78 4.78 (-)1.00

3. Net Inflow from Abroad 0.22 0.19 (-)0.03

4.Gross Budgetary Support to Plan 4.02 4.93 (+) 0.91

5.Central Assistance to States & UTs -1.76 -2.09 (-) 0.33

6.GBS for Central Plan (4+5) 2.26 2.84 (+) 0.57

7.Resources of Public Sector Enterprises 2.90 3.60 (+) 0.70

7.1. Internal Resources 2.15 2.85 (+) 0.70

7.2. Extra Budgetary Resources 0.75 0.75 -

8. Resources for Central Plan (6+7) 5.16 6.44 (+) 1.27

TENTH FIVE YEAR PLAN 2002-07

80

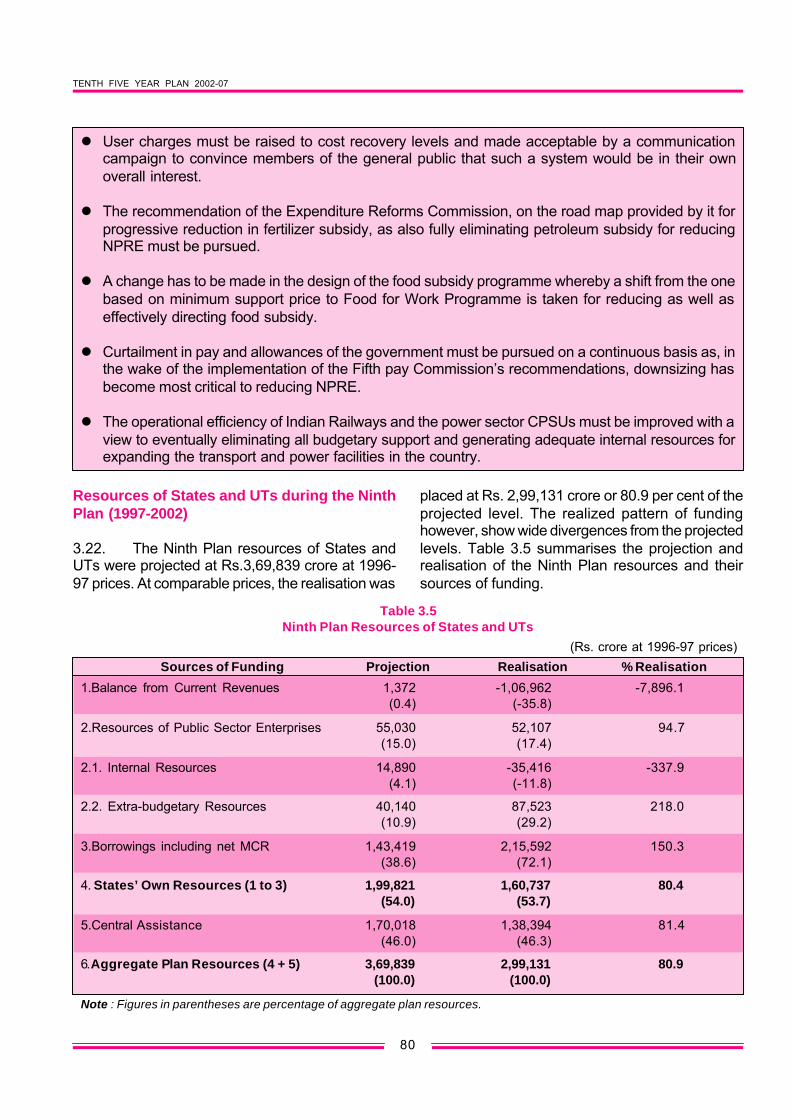

Resources of States and UTs during the NinthPlan (1997-2002)

3.22. The Ninth Plan resources of States andUTs were projected at Rs.3,69,839 crore at 1996-97 prices. At comparable prices, the realisation was

placed at Rs. 2,99,131 crore or 80.9 per cent of theprojected level. The realized pattern of fundinghowever, show wide divergences from the projectedlevels. Table 3.5 summarises the projection andrealisation of the Ninth Plan resources and theirsources of funding.

l User charges must be raised to cost recovery levels and made acceptable by a communicationcampaign to convince members of the general public that such a system would be in their ownoverall interest.

l The recommendation of the Expenditure Reforms Commission, on the road map provided by it forprogressive reduction in fertilizer subsidy, as also fully eliminating petroleum subsidy for reducingNPRE must be pursued.

l A change has to be made in the design of the food subsidy programme whereby a shift from the onebased on minimum support price to Food for Work Programme is taken for reducing as well aseffectively directing food subsidy.

l Curtailment in pay and allowances of the government must be pursued on a continuous basis as, inthe wake of the implementation of the Fifth pay Commission’s recommendations, downsizing hasbecome most critical to reducing NPRE.

l The operational efficiency of Indian Railways and the power sector CPSUs must be improved with aview to eventually eliminating all budgetary support and generating adequate internal resources forexpanding the transport and power facilities in the country.

Table 3.5Ninth Plan Resources of States and UTs

(Rs. crore at 1996-97 prices)Sources of Funding Projection Realisation % Realisation

1.Balance from Current Revenues 1,372 -1,06,962 -7,896.1(0.4) (-35.8)

2.Resources of Public Sector Enterprises 55,030 52,107 94.7(15.0) (17.4)

2.1. Internal Resources 14,890 -35,416 -337.9(4.1) (-11.8)

2.2. Extra-budgetary Resources 40,140 87,523 218.0(10.9) (29.2)

3.Borrowings including net MCR 1,43,419 2,15,592 150.3(38.6) (72.1)

4. States’ Own Resources (1 to 3) 1,99,821 1,60,737 80.4(54.0) (53.7)

5.Central Assistance 1,70,018 1,38,394 81.4(46.0) (46.3)

6.Aggregate Plan Resources (4 + 5) 3,69,839 2,99,131 80.9(100.0) (100.0)

Note : Figures in parentheses are percentage of aggregate plan resources.

PUBLIC SECTOR PLAN : RESOURCES AND ALLOCATIONS

81

3.23. As indicated in the Table, the BCRdeteriorated by 7,896.1 per cent, significantlydrawing borrowings away from plan resources.Borrowings therefore had to increase to 150.3 percent of the projected level in order to provide somesupport to plan resources. The Ninth Plan saw aconsiderable shift from non-debt to debt funding.The non-debt funding reflected by BCR, which wasprojected to contribute a small surplus realised acontribution of negative 35.8 per cent.Consequently, borrowings, which were projected tocontribute 38.6 per cent, ended up contributing 72.1per cent of the Ninth Plan resources.

3.24. Available evidence suggests thatdeterioration of BCR was a result of both revenueand expenditure related slippages. The growth inNPRE was much more than the growth in currentrevenues during the Ninth Plan period. Theimplementation of the Fifth Pay Commission’srecommendations significantly contributed to therapid growth of NPRE. In one single year, salaryand pension payments rose by almost one-third ofthe pre-Pay Commission level. The effect couldhave been largely mitigated but for the inability inreducing the staff strength. Further, interestpayments in the terminal year of the Ninth Plan roseby as much as two and a half times the base yearlevel in absolute terms, due to mobilisation of largeborrowings.

3.25. Under revenue receipts, States’ share ofCentral taxes reduced by 0.14 percentage pointsof GDP across the Ninth Plan period. This was dueto industrial recession, which could not impart muchbuoyancy to the growth in union excise revenues.Revenue losses on account of expansion in thecoverage of MODVAT without commensurateupward adjustment of tax rates has also beenargued as another reason behind the falling ratio ofthe Centre’s gross tax revenue to GDP. Own taxrevenues of States and UTs also failed to exceedthe buoyancy factor of 1. Excessive tax competitionamong States resulting in lowering of tax rates aswell as various fiscal concessions provided to attractindustrial investment were instrumental in notboosting the own tax revenues. Growth in own non-tax revenues was driven down due to the Centre’sinability to raise royalty rates on minerals. Statesand UTs also could not raise user charges

adequately on irrigation and other departmentalservices.

3.26. Contribution of the resources of Statepublic sector enterprises (SPSEs) was realised at94.7 per cent of the projected level. The realizationhowever could have significantly exceeded 100 percent had it not been for the deterioration of IR. TheIR of SPSEs, which were projected to contribute4.1 per cent of plan resources, realized acontribution of negative 11.8 per cent. Thedeterioration of almost 16 percentage points in IRwas largely funded by an increase in the contributionof EBR of PSEs. The contribution of EBR to planresources, which was projected at 10.9 per centrealised a contribution of 29.2 per cent, an increaseof almost 19 percentage points.

3.27. The deterioration in IR brings into focusthe poor performance of State Electricity Boards(SEBs), whose current costs have increasinglyfailed to be covered by current revenues.Unproductive expenditure on administration andestablishment has grown rapidly withoutcommensurate increase in user charges. Suchevents accentuate the importance of power sectorreforms, which should enable SEBs to earn at leasta minimum rate of 3 per cent on their assets.

3.28. The trebling of the contribution of EBR toplan resources vis-à-vis the Ninth Plan projections,despite a massive deterioration of IR implies animprudent use of guarantees, which States issuefor SPSEs to raise borrowings. The contingentliability embodied in the issue of guarantees is mostlikely to fall on State budgets if SPSEs do notimprove the mobilisation of internal resources. Insuch an event, the fiscal balance of States’ financescan come under severe strain.

3.29. As against a projected contribution of 38.6per cent of borrowings to plan resources, Ninth Planrealisation places it at 72.1 per cent, an increase ofalmost 34.0 percentage points. Unfortunately, sucha sizeable growth in borrowings was used tobridging the BCR gap rather than augmenting planresources. Rapid increase in borrowings also ledto an increase in public sector draft on privatesavings as is implied by growth in States’outstanding debt as a percentage of GDP from 17.8

TENTH FIVE YEAR PLAN 2002-07

82

per cent in the beginning to 25.9 percent at the endof the Ninth Plan. Simultaneously, a larger debtburden increasingly became unsustainable, as theaccompanying growth of interest payments was notmatched by a commensurate growth in revenues.Interest payments as a percentage of revenuereceipts increased from 16.7 per cent in thebeginning to 22.8 per cent at the end of the NinthPlan.

3.30. Central assistance to States and UTsrealised 81.4 per cent of the projected level.However, its realised contribution to plan resourcesremained the same as the projected contributionat around 54 per cent. The significance of GBS toStates and UTs Plan remained unchanged duringthe Ninth Plan period. However, a shortfall inabsolute terms underlines the growing budgetarystrain of the Centre in meeting the targets of Centralassistance.

Projection of Tenth Plan (2002-07) Resourcesof States and UTs

3.31. In keeping with the requirement ofstepping up public sector investment for attainingan 8 per cent GDP growth during the Tenth Plan,budgetary resources for the States & UTs plan hasbeen projected to grow from 3.85 per cent of GDPin 2001-02 to 4.20 per cent in 2006-07. The TenthPlan average stands at 4.10 per cent, as againstthe Ninth Plan realization of 3.14 per cent.

3.32. The fiscal sustainability of States and UTsis considerably more vulnerable than for the Centreand requires greater fiscal correction. Accordingly,the gross fiscal deficit, which stood at 4.47 per centof GDP in 2001-02 has been projected to reduce to2.19 per cent in 2006-07, obtaining a Tenth Planaverage of 3.19 per cent. The Ninth Plan averagehad stood at 3.37 per cent. The projected target ofgross fiscal deficit is implicit in own borrowingsinclusive of MCR and the loan component of Centralassistance. Own borrowings inclusive of MCR inthe Tenth Plan are arrived at 1.82 per cent of GDP,down from 2.74 per cent realised during the NinthPlan. Central assistance in the Tenth Plan is placedat 2.09 per cent of GDP, up from 1.76 per centrealized during the Ninth Plan.

3.33. BCR is arrived at 0.19 per cent of GDP.To achieve a BCR of this order, non-plan revenuereceipts must grow from 10.27 per cent of GDP in2001-02 to 11.00 per cent in 2006-07, an increaseof 0.73 percentage points. NPRE must come downfrom 12.15 per cent of GDP in 2001-02 to 10.32per cent, a decrease of 1.83 percentage points.Thus an improvement of 2.56 percentage points inBCR during the Tenth Plan is mainly sought from acontraction of NPRE.

3.34. IR and EBR of SPSEs were determined inconsultation with State Governments. The need forimproving IR, particularly of SEBs was emphasized.Accordingly, IR was projected at –0.05 per cent ofGDP for the Tenth Plan, a much improved level from–0.45 per cent realised during the Ninth Plan. After aconsidered view, which favored a reduction in thecontingent liabilities of States and UTs, EBR wasprojected at 0.63 per cent of GDP in the Tenth Plan,down from 1.11 per cent realised during the NinthPlan. Total resources of SPSEs in the Tenth Plan aretherefore projected at 0.58 per cent of GDP, slightlydiminished from 0.66 per cent realised during the NinthPlan. Table 3.6 indicates the Tenth Plan resourcesand its funding of States and UTs in the Tenth Plan.

Table 3.6Tenth Plan Projection of Resources of States and UTs

(Rs.crore at 2001-02 prices)Sources of Funding Tenth Plan

Projections

1.Balance from Current Revenues 26,578(4.0)

2.Resources of Public Sector Enterprises 82,684(12.3)

2.1. Internal Resources -7,760(-1.2)

2.2. Extra-budgetary Resources 90,444(13.5)

3.Borrowings including net MCR 2,61,482(39.0)

4. States’ Own Resources (1 to 3) 3,70,744(55.3)

5.Central Assistance 3,00,265(44.7)

6.Aggregate Plan Resources (4 + 5) 6,71,009(100.0)

Note : Figures in parentheses are percentage of aggregateplan resources.

PUBLIC SECTOR PLAN : RESOURCES AND ALLOCATIONS

83

3.35. Aggregate plan resources of States and UTsare arrived at Rs.6,71,009 crore at 2001-02 prices,comprising Rs.3,70,744 crore of own resources andRs.3,00,265 crore of Central assistance. Of the totalaggregate plan resources, budgetary resources areplaced at Rs.5,88,325 crore.

3.36. A funding pattern, as envisaged is ademanding task, whose extent could be gaugedby comparing the Tenth Plan projected levels toNinth Plan realization. Table 3.7 indicates the NinthPlan realisation and Tenth Plan projection ofresources of the States and UTs in relation to GDP.

3.37. The steps detailed in Box 3.2 arenecessary to achieve these targets.

3.38. The Planning Commission helddiscussions with States and UTs about projectingthe core Tenth Plan resources. The projection ofthe core Tenth Plan resources was at a level lowerthan what was required to achieve 8 per cent growthof GDP. This was due to the apprehension thatimprovement in BCR, as required under the 8 percent GDP growth scenario may not be achievable.Thus, as against a BCR of 0.20 per cent in the 8per cent growth scenario, core plan resources

BOX 3.2

l Improving tax/GDP ratio of the Centre and States/UTs through inclusion of services in the tax base,removal of tax exemptions and concessions, harmonisation of tax rates, tightening of taxadministration, and adopting an integrated VAT regime.

l Reduction of budget-based subsidies by raising user charges of departmental services, reducingexpenditure by cutting administrative and establishment cost and privatization and through Centre’sinitiative switching over to ad valorem rates of royalty on minerals.

l Reducing staff strength through adoption of a policy of net attrition and constituting a pension andamortisation fund to make committed payments like terminal benefits and debt servicing, self-financing.

l Enacting a ‘Fiscal Responsibility and Budget Management’ bill under which borrowings shall berestricted to attain a non-rising debt to GDP ratio from current levels in order to reduce the burden ofinterest payments.

l Improving internal resources of States PSUs by implementing power sector reforms and reducingthe burden of contingent liabilities on State budgets through a legislative or administrative ceiling onthe issue of State guarantees.

Table 3.7Ninth Plan Realisation and Tenth Plan Projection of Resources of States and UTs

(As a percentage of GDP)

Sources of Funding Ninth Plan Realisation Tenth Plan Projections Increases(+)/Decreases(-)

1.Balance from Current Revenues -1.36 0.20 (+)1.56

2.Resources of Public Sector Enterprises 0.66 0.58 (-) 0.08

2.1. Internal Resources -0.45 -0.05 (+) 0.40

2.2. Extra-budgetary Resources 1.11 0.63 (-) 0.48

3.Borrowings including net MCR 2.74 1.82 (-) 0.92

4. States’ Own Resources (1 to 3) 2.04 2.60 (+) 0.56

5.Central Assistance 1.76 2.09 (+) 0.33

6.Aggregate Plan Resources (4 + 5) 3.80 4.69 (+) 0.89

TENTH FIVE YEAR PLAN 2002-07

84

indicated its level at negative 0.11 per cent. Furtherit was also recognised that the level of Centralassistance indicated at 2.09 per cent of GDP mayalso not be available if the Centre’s GBS fails torise to the Tenth Plan projected levels.Consequently, the core plan resources arrived at aCentral assistance level of 1.80 per cent of GDP,by and large the same level realized in the NinthPlan. Table 3.8 gives a break-down of the fundingof plan resources of States and UTs under the coreplan scenario.

3.39. The core Tenth Plan resources of Statesand UTs are projected at Rs.5,90,948 crore,Rs.80,061 crore less than the level consistentwith the 8 per cent GDP growth scenario. To be

consistent with the 8 per cent growth target,States and UTs are required to raise Rs. 38,553crore of own resources and the Centre requiredto provide Rs. 41,508 crore of Central assistanceto make up for the balance. States & UTs wisedisbursement of the Central assistancecomponent of the balance, inter-alia, may haveto be linked to their respective abilities inmobilising the own resources component.

Overall Financing Pattern

3.40. Table 3.9 revisits the Ninth Plan realisationlevels of plan resources of the Centre and Statesand UTs. Total resources realised for the public

Table 3.8Core Tenth Plan Resources of States & UTs

(Rs.crore at 2001-02 prices)

Sources of Funding States UTs(1) UTs(2) Total

1.Balance from Current Revenues -37,099 21,804 - -15,295

2.Resources of Public Sector Enterprises 85,566 -2,882 - 82,684

2.1. Internal Resources -4,878 -2,882 - -7,760

2.2. Extra-budgetary Resources 90,444 - - 90,444

3.Borrowings including net MCR 2,62,013 2,789 - 2,64,802

4. States’ Own Resources (1 to 3) 3,10,480 21,711 - 3,32,191

5.Central Assistance 2,51,093 3,195 4,469 2,58,757

6.Aggregate Plan Resources (4 + 5) 5,61,573 24,906 4,469 5,90,948

Note : UTs(1)-With Legislature; UTs(2)-Without Legislature.

Table 3.9 Ninth Plan Realiastion of Resources for the Public Sector Plan

(Rs. crore at 1996-97 prices)

Sources of Funding Centre States / UTs Total

1.Balance from Current Revenues -1,56,790 -1,06,962 -2,63,752

2.Borrowings including net MCR 4,55,624 2,15,592 6,71,216

3. Net Inflow from Abroad 17,452 - 17,452

4.Centre’s GBS (1+2+3) 3,16,286 - -

5.Resources of Public Sector Enterprises 2,28,795 52,107 2,80,902

5.1. Internal Resources 1,69,046 -35,416 1,33,630

5.2. Extra budgetary Resources 59,749 87,523 1,47,272

6. States’ Own Resources (1+2+5) - 1,60,737 -

7.Central Assistance to States & UTs -1,38,394 1,38,394 -

8. Resources for the Public Sector Plan (1+2+3+5+7) 4,06,687 2,99,131 7,05,818

Note : The Centre’ GBS available for the Central Plan works out to Rs.177892 crore.

PUBLIC SECTOR PLAN : RESOURCES AND ALLOCATIONS

85

sector’s Ninth Plan indicates the large presence ofnegative BCR, which has been bridged by asubstantially high level of borrowings. Had the BCRrealisation been in alignment with what wasprojected, the contracted borrowings would havesignificantly stepped up the resources for the publicsector plan, much higher than what was projected.In that event, the increase in overall debt burdenwould have been accompanied by a larger publicsector investment, which would have built theproductive capacities of the economy rather thanfunding the consumption expenditure of thegovernment.

3.41. Table 3.10. projects the overall resourcesfor the Tenth Plan on the presumption that thenegative BCR gap would be erased, leavingborrowings exclusively for the public sectorinvestment and not for meeting the consumptionexpenditure of the government. The projection alsorequires the public sector enterprises to substantiallyenhance their internal resources for limiting the needfor raising EBR.

Allocation of Public Sector Resource

3.42. The projected requirement of resourcesof the public sector for the Tenth Plan atRs.15,92,300 crore at 2001-02 prices comprisethe Centre’s share at Rs.9,21,291 crore and

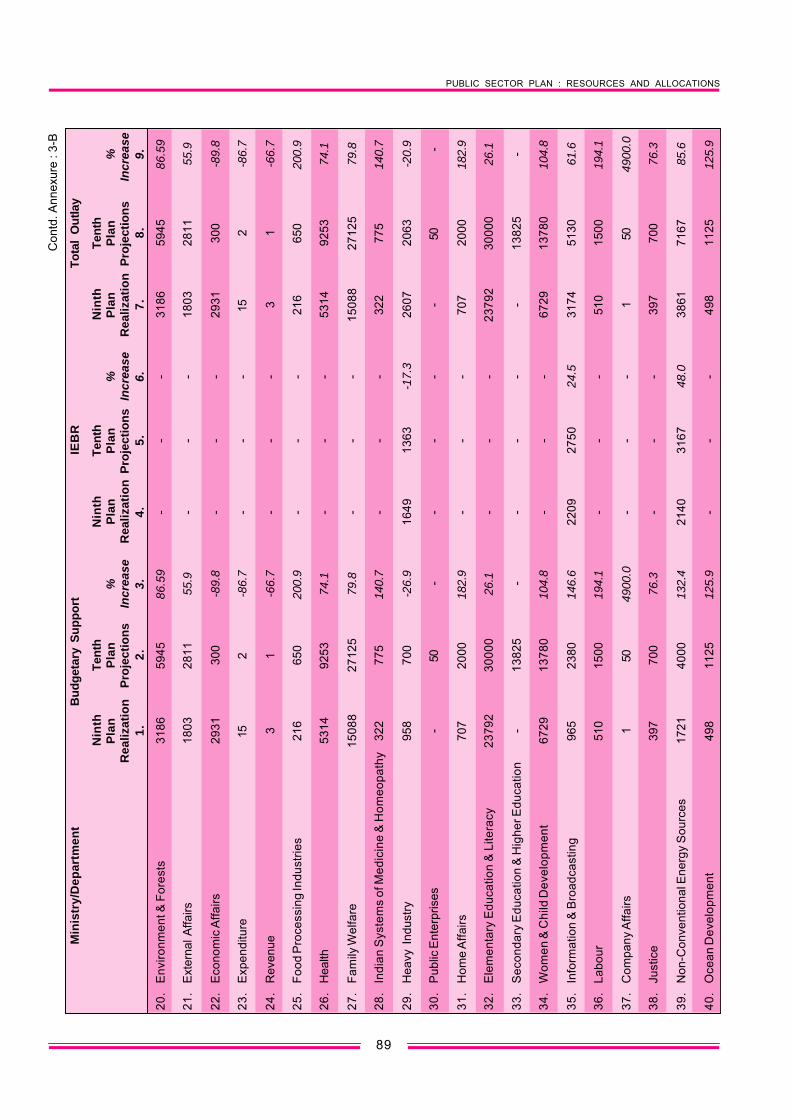

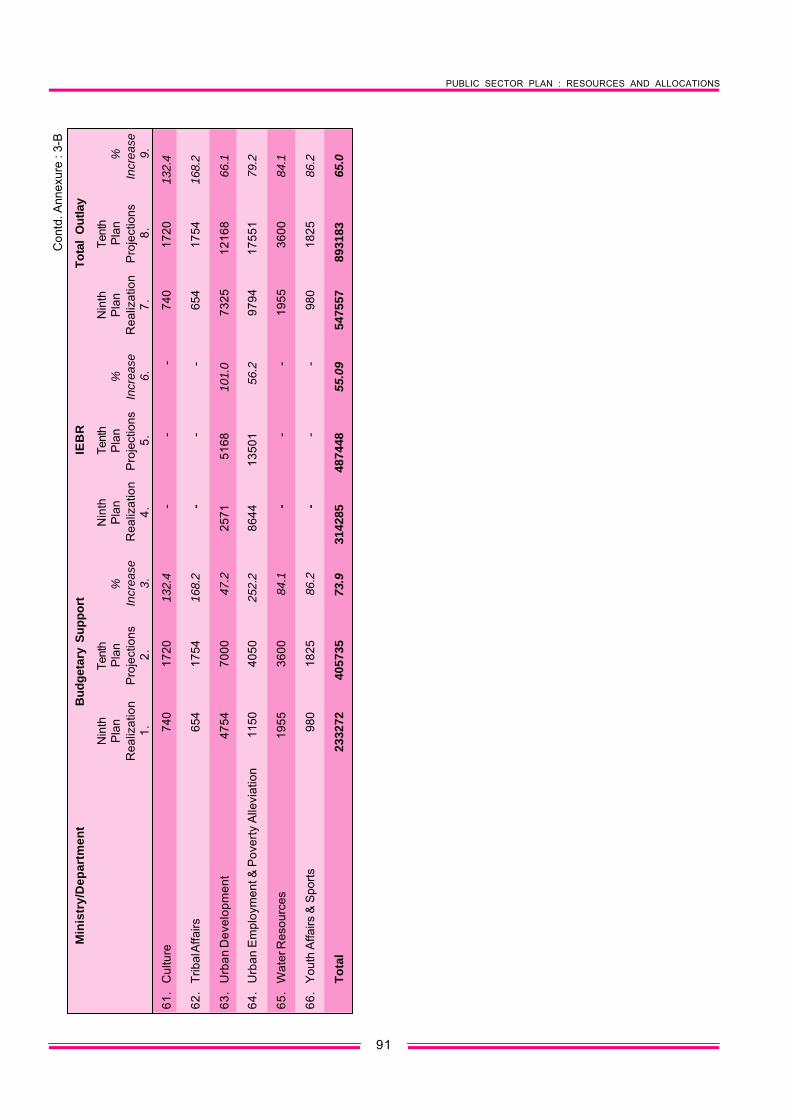

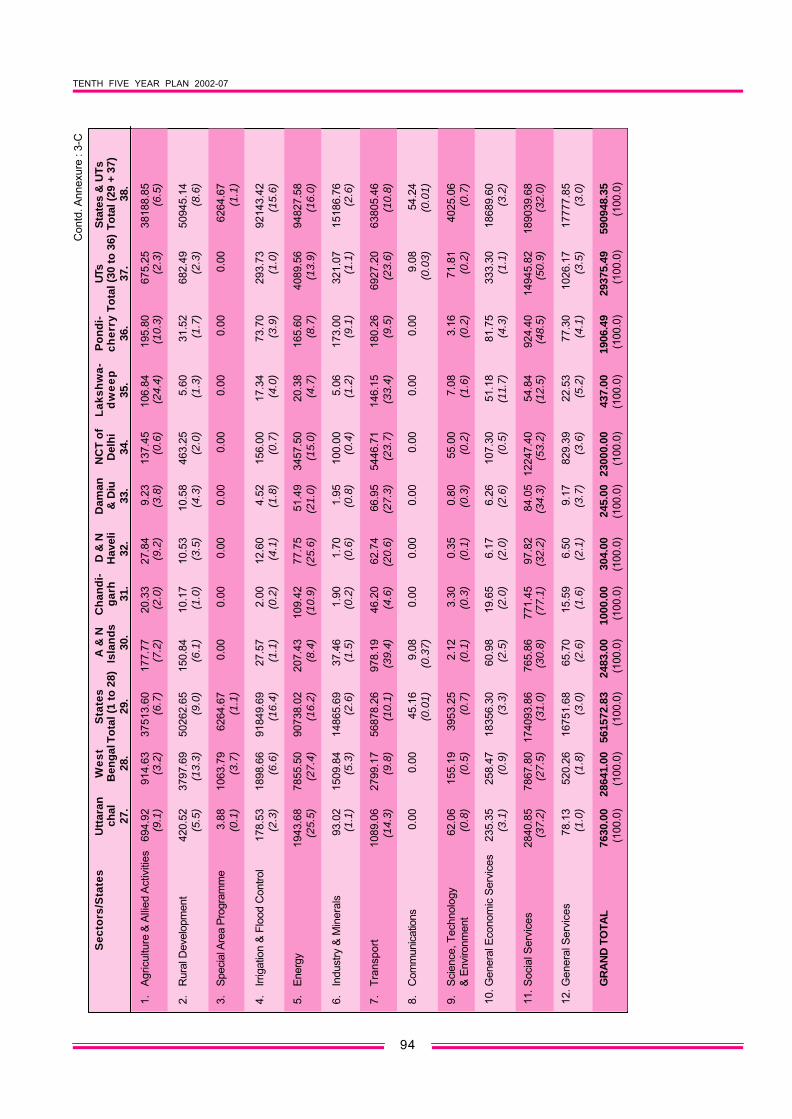

States and UTs share at Rs.6,71,009 crore. Theresources for the Central Plan includes the GBScomponent of Rs.4,05,735 crore and the IEBRcomponent of Rs.5,15,556 crore. The IEBRcomponent as currently assessed by CentralMinistries is Rs.4,87,448 crore, which isRs.28,108 crore lower than the level consistentwith the 8 percent growth of GDP in the TenthPlan.. Thus, the resource allocation in the Centralsector amounts to Rs.8,93,183 crore, which isindicated in Annexure 3-A with details ofbudgetary support and IEBR furnished inAnnexure 3-B.

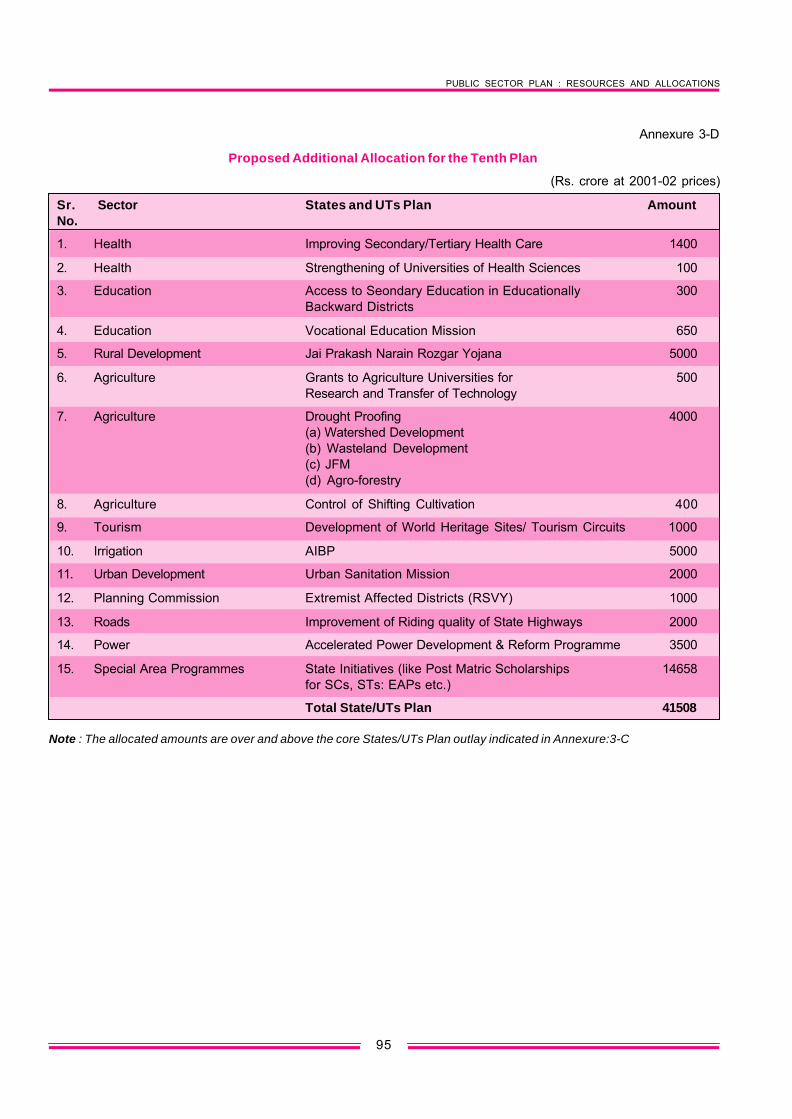

3.43. The Tenth Plan resources of the Statesand UTs are projected at Rs.6,71,009 crore at2001-02 prices. Core plan estimates, however,arrive at a resource figure of Rs.5,90,948 crore,leaving a balance of Rs.80,061 crore. Sectoralallocation in the States/UTs sector includes thecore plan resources and the Central Assistancecomponent of the balance, that is, Rs.41,508crore. This component has been allocated tocertain critical sectors identified by the PlanningCommission. The allocation of the own resourcescomponent of the balance, which is placed at Rs.38,553 crore, will have to await its actualmobilization by the States and UTs.Consequently, sectoral allocations in the States/UTs sector is arrived at Rs.6,32,456 crore. This

Table 3.10Tenth Plan Projection of Resources for the Public Sector Plan

(Rs. crore at 2001-02 prices)

Sources of Funding Centre States/UTs Total

1.Balance from Current Revenues -6,385 26,578 20,193

2.Borrowings including net MCR 6,85,185 2,61,482 9,46,667

3. Net Inflow from Abroad 27,200 - 27,200

4.Centre’s GBS (1+2+3) 7,06,000 - 7,06,000

5.Resources of Public Sector Enterprises 5,15,556 82,684 5,98,240

5.1. Internal Resources 4,09,000 -7,760 4,01,240

5.2. Extra budgetary Resources 1,06,556 90,444 1,97,000

6. States’ Own Resources (1+2+5) - 3,70,744 -

7.Central Assistance to States & UTs -3,00,265 3,00,265 -

8.Resources for the Public Sector Plan (1+2+3+5+7) 9,21,291 6,71,009 15,92,300

Note : The Centre’s GBS available for the Central Plan works out to Rs.4,05,735 crore.Allocations of Public Sector Resources.

TENTH FIVE YEAR PLAN 2002-07

86

allocation in the States/UTs sector is indicated inAnnexure 3-A with States/UTs wise core plan detailsfurnished in Annexure 3-C. Annexure 3-D indicatesthe details of Central assistance component of thebalance in the States/UTs sector.

3.44. Thus, as against the public sectorresources of Rs.15,92,300 crore for the Tenth Plan,allocations aggregate to Rs.15,25,639 crore. Table3.11 indicates the resources and allocation of thepublic sector Tenth Plan.

Table 3.11Public Sector Resources & Allocations

Tenth Plan (2002-07) (Rs. crore at 2001-02 prices)

Sources of funding Required Allocated

CENTRE1. Budgetary Support 4,05,735 4,05,7352. IEBR 5,15,556 4,87,4483. Total-Centre (1+2) 9,21,291 8,93,183

STATES & UTs4. Core Plan 5,90,948 5,90,9485. Balance (5.1+5.2) 80,061 41,5085.1 Own Resources 38,553 -5.2 Central Assistance 41,508 41,5086.Total-States & UTs (4+5) 6,71,009 6,32,456

TOTAL PUBLIC SECTOR7. Grand Total (3+6) 15,92,300 15,25,639

PUBLIC SECTOR PLAN : RESOURCES AND ALLOCATIONS

87

Ann

exur

e : 3

-A

Sec

tora

l Allo

cati

on

s o

f Pu

blic

Sec

tor'

s R

eso

urc

es: N

inth

Pla

n R

ealiz

atio

n (1

997-

2002

) an

d T

enth

Pla

n (2

002-

07) P

roje

ctio

ns

(Rs.

cro

re a

t 200

1-02

pric

es)

CE

NTR

EST

ATE

S A

ND

UTs

CE

NTR

E,

STA

TES

& U

Ts

Hea

ds

of D

evel

op

men

tB

ud

get

ary

Su

pp

ort

IEB

RT

ota

l O

utla

yT

ota

l O

utla

yT

ota

l O

utla

yN

inth

Tent

hN

inth

Tent

hN

inth

Tent

hN

inth

Tent

hN

inth

Tent

hP

lan

Pla

n%

Pla

nP

lan

%P

lan

Pla

n%

Pla

nP

lan

%P

lan

Pla

n%

Rea

li.P

roje

ctio

nIn

crea

seR

eali.

Pro

ject

ion

Incr

ease

Rea

li.P

roje

ctio

nIn

crea

seR

eali.

Pro

ject

ion

Incr

ease

Rea

li.P

roje

ctio

nIn

crea

se1

23

45

67

89

1011

1213

1415

1.A

gric

ultu

re &

Alli

ed A

ctiv

ities

1200

821

068

75.4

--

-12

008

2106

875

.425

231

3786

550

.137

239

5893

358

.3

2.R

ural

Dev

elop

men

t56

404

7972

441

.3-

--

5640

479

724

41.3

3256

142

204

29.6

8896

512

1928

37.1

3.S

peci

al A

rea

Pro

gram

mes

--

--

--

--

-54

0820

879

286.

154

0820

879

286.

1

4.Ir

rigat

ion

& F

lood

Con

trol

1955

3600

84.1

--

-19

5536

0084

.167

875

9971

546

.969

830

1033

1548

.0

5.E

nerg

y25

632

5160

010

1.3

1187

5726

6583

124.

514

4389

3181

8312

0.4

7485

485

744

14.5

2192

4340

3927

84.2

6.In

dust

ry a

nd M

iner

als

7362

1178

660

.126

102

2858

69.

533

464

4037

220

.611

231

1856

765

.344

695

5893

931

.9

7.Tr

ansp

ort

3678

465

350

77.7

6162

782

098

33.2

9841

114

7448

49.8

4483

878

529

75.1

1432

4922

5977

57.8

8.C

omm

unic

atio

ns35

5979

4412

3.2

8926

391

012

2.0

9282

298

956

6.6

1412

-14.

392

836

9896

86.

6

9.S

cien

ce, T

echn

olog

y &

Env

ironm

ent

1456

327

570

89.3

11-

-14

574

2757

089

.210

9328

5416

1.1

1566

730

424

94.2

10.

Gen

eral

Eco

nom

ic S

ervi

ces

4091

1058

715

8.8

960

500

-47.

950

5111

087

119.

586

8327

543

17.2

1373

438

630

181.

3

11.

Soc

ial S

ervi

ces

6492

712

0333

85.3

1121

518

669

66.5

7614

213

9002

82.6

1183

8720

8389

76.0

1945

2934

7391

78.6

12.

Gen

eral

Ser

vice

s59

8761

733.

1-

--

5987

6173

3.1

9659

1015

55.

115

646

1632

84.

4

To

tal

2332

7240

5735

73.9

3079

3548

7448

158

.354

1207

8931

8385

.039

9834

6324

562

58.2

9410

4115

2563

962

.1

So

urc

e :

(1) C

ore

IEB

R in

dica

ted

by th

e C

entr

al M

inis

trie

s, w

hich

is R

s. 2

8108

cro

re le

ss th

an th

e le

vel c

onsi

sten

t with

8 p

erce

nt g

row

th o

f GD

P in

the

Ten

th P

lan,

that

is R

s.51

5556

cro

re.

(2) I

nclu

des

allo

catio

n of

Rs.

590

948

cror

e of

cor

e P

lan

reso

urce

s of

Sta

tes/

UT

s an

d R

s. 4

1508

cro

re, a

dditi

onal

out

lays

pro

pose

d by

the

Pla

nnin

g C

omm

issi

on.

TENTH FIVE YEAR PLAN 2002-07

88

Ann

exur

e : 3

-B

Bud

get

Sup

port

, IE

BR

and

Out

lay

for

Cen

tral

Min

istr

ies/

Dep

artm

ent

: N

inth

Pla

n R

ealiz

atio

n &

Ten

th P

lan

Pro

ject

ions

(Rs.

cro

re a

t 200

1-02

pric

es)

Min

istr

y/D

epar

tmen

tB

ud

get

ary

Su

pp

ort

IEB

RT

ota

l O

utla

y

Nin

thT

enth

Nin

thT

enth

Nin

thT

enth

Pla

nP

lan

%P

lan

Pla

n%

Pla

nP

lan

%R

ealiz

atio

nP

roje

ctio

ns

Incr

ease

Rea

lizat

ion

Pro

ject

ion

sIn

crea

seR

ealiz

atio

nP

roje

ctio

ns

Incr

ease

1.2.

3.4.

5.6.

7.8.

9.

1.A

gric

ultu

re &

Coo

pera

tion

8308

1320

058

.9-

--

8308

1320

058

.9

2.A

gric

ultu

re R

esea

rch

& E

duca

tion

2673

5368

100.

8-

--

2673

5368

100.

8

3.A

nim

al H

usba

ndry

& D

airy

ing

1027

2500

143.

4-

--

1027

2500

143.

4

4.A

gro

& R

ural

Indu

strie

s26

7529

5010

.3-

--

2675

2950

10.3

5.A

tom

ic E

nerg

y67

7121

550

218.

316

7110

820

547.

584

4232

370

283.

4

6.C

hem

ical

s &

Pet

ro-C

hem

ical

s19

130

057

.155

1627

44-5

0.3

5707

3044

-46.

7

7.Fe

rtiliz

ers

1013

1050

3.7

4474

4850

8.4

5487

5900

7.5

8.C

ivil

Avi

atio

n20

440

096

.192

2812

528

35.8

9432

1292

837

.1

9.C

oal

2233

1050

-53.

014

823

3054

110

6.0

1705

631

591

85.2

10.

Min

es95

012

7133

.848

7381

8768

.058

2394

5862

.4

11.

Com

mer

ce18

7645

4714

2.4

169

15-9

1.1

2045

4562

123.

1

12.

Indu

stria

l Pol

icy

& P

rom

otio

n21

1320

00-5

.3-

--

2113

2000

-5.3

13.

Info

rmat

ion

Tec

hnol

ogy

1236

2714

119.

661

927

7834

8.8

1855

5492

196.

1

14.

Pos

t44

313

5020

4.7

--

-44

313

5020

4.7

15.

Tele

com

mun

icat

ions

915

1500

63.9

8643

585

484

-1.1

8735

086

984

-0.4

16.

Foo

d &

Pub

lic D

istr

ibut

ion

236

250

5.9

620

485

-21.

885

673

5-1

4.1

17.

Con

sum

er A

ffairs

5255

5.8

--

-52

555.

8

18.

Dis

inve

stm

ent

--

--

--

-0

-

19.

Dev

elop

men

t of N

orth

-Eas

tern

Reg

ion

-15

0-

--

--

150

-

PUBLIC SECTOR PLAN : RESOURCES AND ALLOCATIONS

89

Con

td. A

nnex

ure

: 3-B

Min

istr

y/D

epar

tmen

tB

ud

get

ary

Su

pp

ort

IEB

RTo

tal

Out

lay

Nin

thTe

nth

Nin

thTe

nth

Nin

thTe

nth

Pla

nP

lan

%P

lan

Pla

n%

Pla

nP

lan

%R

ealiz

atio

nP

roje

ctio

ns

Incr

ease

Rea

lizat

ion

Pro

ject

ion

sIn

crea

seR

ealiz

atio

nP

roje

ctio

ns

Incr

ease

1.2.

3.4.

5.6.

7.8.

9.

20.

Env

ironm

ent &

For

ests

3186

5945

86.5

9-

--

3186

5945

86.5

9

21.

Ext

erna

l Affa

irs18

0328

1155

.9-

--

1803

2811

55.9

22.

Eco

nom

ic A

ffairs

2931

300

-89.

8-

--

2931

300

-89.

8

23.

Exp

endi

ture

152

-86.

7-

--

152

-86.

7

24.

Rev

enue

31

-66.

7-

--

31

-66.

7

25.

Foo

d P

roce

ssin

g In

dust

ries

216

650

200.

9-

--

216

650

200.

9

26.

Hea

lth53

1492

5374

.1-

--

5314

9253

74.1

27.

Fam

ily W

elfa

re15

088

2712

579

.8-

--

1508

827

125

79.8

28.

Indi

an S

yste

ms

of M

edic

ine

& H

omeo

path

y32

277

514

0.7

--

-32

277

514

0.7

29.

Hea

vy I

ndus

try95

870

0-2

6.9

1649

1363

-17.

326

0720

63-2

0.9

30.

Pub

lic E

nter

pris

es-

50-

--

--

50-

31.

Hom

e A

ffairs

707

2000

182.

9-

--

707

2000

182.

9

32.

Ele

men

tary

Edu

catio

n &

Lite

racy

2379

230

000

26.1

--

-23

792

3000

026

.1

33.

Sec

onda

ry E

duca

tion

& H

ighe

r Edu

catio

n-

1382

5-

--

--

1382

5-

34.

Wom

en &

Chi

ld D

evel

opm

ent

6729

1378

010

4.8

--

-67

2913

780

104.

8

35.

Info

rmat

ion

& B

road

cast

ing

965

2380

146.

622

0927

5024

.531

7451

3061

.6

36.

Labo

ur51

015

0019

4.1

--

-51

015

0019

4.1

37.

Com

pany

Affa

irs1

5049

00.0

--

-1

5049

00.0

38.

Just

ice

397

700

76.3

--

-39

770

076

.3

39.

Non

-Con

vent

iona

l Ene

rgy

Sou

rces

1721

4000

132.

421

4031

6748

.038

6171

6785

.6

40.

Oce

an D

evel

opm

ent

498

1125

125.

9-

--

498

1125

125.

9

TENTH FIVE YEAR PLAN 2002-07

90

Con

td. A

nnex

ure

: 3-B

Min

istr

y/D

epar

tmen

tB

udge

tary

Sup

port

IEB

RTo

tal O

utla

y

Nin

thTe

nth

Nin

thTe

nth

Nin

thTe

nth

Pla

nP

lan

%P

lan

Pla

n%

Pla

nP

lan

%R

ealiz

atio

nP

roje

ctio

ns

Incr

ease

Rea

lizat

ion

Pro

ject

ion

sIn

crea

seR

ealiz

atio

nP

roje

ctio

ns

Incr

ease

1.2.

3.4.

5.6.

7.8.

9.

41.

Per

sonn

el, P

ublic

Grie

vanc

es &

Pen

sion

s78

250

220.

5-

--

7825

022

0.5

42.

Pet

role

um &

Nat

ural

Gas

-

-

-

7033

810

3656

47.4

7033

810

3656

47.4

43.

Pla

nnin

g C

omm

issi

on61

434

0-4

4.6

--

-61

434

0-4

4.6

44.

Pow

er14

907

2500

067

.729

785

1183

9929

7.5

4469

214

3399

220.

9

45.

Rai

lway

s16

491

2760

067

.434

120

3300

0-3

.350

611

6060

019

.7

46.

Roa

d Tr

ansp

ort &

Hig

hway

s19

393

3500

080

.518

279

2470

035

.137

672

5970

058

.5

47.

Drin

king

Wat

er S

uppl

y80

5214

200

76.4

--

-80

5214

200

76.4

48.

Land

Res

ourc

es24

0465

2617

1.5

--

-24

0465

2617

1.5

49.

Rur

al D

evel

opm

ent

4327

356

748

31.1

--

-43

273

5674

831

.1

50.

Bio

-Tec

hnol

ogy

669

1450

116.

7-

--

669

1450

116.

7

51.

Sci

ence

& T

echn

olog

y16

3534

0010

8.0

11-

-16

4634

0010

6.6

52.

Sci

entif

ic &

Indu

stria

l Res

earc

h14

7825

7574

.2-

--

1478

2575

74.2

53.

Shi

ppin

g69

623

5023

7.6

6350

1187

086

.93

7045

.87

1422

010

1.8

54.

Sm

all S

cale

Indu

strie

s-

2200

-66

638

4-4

2.3

666

2584

288.

0

55.

Soc

ial J

ustic

e &

Em

pow

erm

ent

5404

8530

57.8

--

-54

0485

3057

.8

56.

Spa

ce70

9713

250

86.7

--

-70

9713

250

86.7

57.

Sta

tistic

s &

Pro

gram

me

Impl

emen

tatio

n21

572

523

7.2

--

-21

572

523

7.2

58.

Ste

el85

65-2

3.5

8882

1097

823

.689

6711

043

23.2

59.

Text

iles

1836

3500

90.6

4280

90.5

1878

3580

90.6

60.

Tour

ism

640

2900

353.

117

1-

-81

129

0025

7.6

PUBLIC SECTOR PLAN : RESOURCES AND ALLOCATIONS

91

Con

td. A

nnex

ure

: 3-B

Min

istr

y/D

epar

tmen

tB

ud

get

ary

Su

pp

ort

IEB

RTo

tal

Out

lay

Nin

thTe

nth

Nin

thTe

nth

Nin

thTe

nth

Pla

nP

lan

%P

lan

Pla

n%

Pla

nP

lan

%R

ealiz

atio

nP

roje

ctio

nsIn

crea

seR

ealiz

atio

nP

roje

ctio

nsIn

crea

seR

ealiz

atio

nP

roje

ctio

nsIn

crea

se1.

2.3.

4.5.

6.7.

8.9.

61.

Cul

ture

740

1720

132.

4 -

--

740

1720

132.

4

62.

Trib

al A

ffairs

654

1754

168.

2

-

-

-65

417

5416

8.2

63.

Urb

an D

evel

opm

ent

4754

7000

47.2

2571

5168

101.

073

2512

168

66.1

64.

Urb

an E

mpl

oym

ent &

Pov

erty

Alle

viat

ion

1150

4050

252.

286

4413

501

56.2

9794

1755

179

.2

65.

Wat

er R

esou

rces

1955

3600

84.1

-

-

-

1955

3600

84.1

66.

You

th A

ffairs

& S

ports

980

1825

86.2

-

-

-

980

1825

86.2

To

tal

2332

7240

5735

73.9

3142

8548

7448

55.0

954

7557

8931

8365

.0

TENTH FIVE YEAR PLAN 2002-07

92

Ann

exur

e : 3

-C

Ten

th P

lan

(20

02-0

7) O

utl

ays

by

Sta

tes/

UT

s(M

ajo

r H

ead

s o

f D

evel

op

men

t)

(Rs.

Cro

re a

t 200

1-02

pric

es)

Sec

tors

/Sta

tes

An

dh

raA

run

ach

alA

ssam

Bih

arC

hat

tis-

Goa

Gu

jara

tH

arya

na

Him

ach

alJ

& K

Jhar

khan

dK

arn

atak

aK

eral

aP

rad

es

hP

rad

es

hg

arh

Pra

de

sh

1.2.

3.4.

5.6.

7.8.

9.10

.11

.12

.13

.

1.A

gric

ultu

re &

Alli

ed A

ctiv

ities

2333

.21

515.

3166

4.98

536.

1186

0.97

158.

3435

48.7

146

9.53

1201

.69

1507

.80

824.

8523

46.9

411

25.0

0(5

.0)

(13.

3)(8

.0)

(2.6

)(7

.8)

(4.9

)(8

.9)

(4.6

)(1

1.7)

(10.

4)(5

.6)

(5.4

)(4

.7)

2.R

ural

Dev

elop

men

t45

92.0

715

8.17

582.

6141

36.5

011

58.9

184

.50

1361

.94

305.

8543

8.16

374.

1032

72.3

322

27.7

256

9.75

(9.9

)(4

.1)

(7.0

)(1

9.7)

(10.

5)(2

.6)

(3.4

)(3

.0)

(4.3

)(2

.6)

(22.

4)(5

.1)

(2.4

)

3.S

peci

al A

rea

Pro

gram

me

1123

.52

65.0

056

.40

40.6

90.

0018

.00

38.3

014

7.37

20.8

077

1.87

0.00

640.

7410

0.00

(2.4

)(1

.7)

(0.7

)(0

.2)

(0.6

)(0

.1)

(1.4

)(0

.2)

(5.3

)(1

.5)

(0.4

)

4.Irr

igat

ion

& F

lood

Con

trol

1084

4.98

184.

3764

5.33

6016

.87

2506

.65

222.

9088

10.0

515

41.0

445

3.18

805.

7920

76.7

014

176.

5793

0.00

(23.

3)(4

.7)

(7.8

)(2

8.7)

(22.

8)(7

.0)

(22.

0)(1

5.0)

(4.4

)(5

.6)

(14.

2)(3

2.5)

(3.9

)

5.E

nerg

y71

41.7

249

8.12

837.

0427

35.4

413

3.25

405.

0060

18.9

314

00.4

712

35.0

028

85.7

481

4.00

2266

.95

3500

.00

(15.

3)(1

2.8)

(10.

1)(1

3.0)

(1.2

)(1

2.7)

(15.

0)(1

3.6)

(12.

0)(1

9.9)

(5.6

)(5

.2)

(14.

6)

6.In

dust

ry &

Min

eral

s16

55.1

176

.36

237.

0424

1.50

214.

1211

6.40

2068

.45

84.3

410

4.73

435.

6547

3.87

1452

.87

1328

.75

(3.6

)(2

.0)

(2.9

)(1

.2)

(1.9

)(3

.6)

(5.2

)(0

.8)

(1.0

)(3

.0)

(3.2

)(3

.3)

(5.5

)

7.Tr

ansp

ort

3994

.19

824.

4287

9.32

1303

.12

451.

6439

2.84

1851

.39

1286

.65

1635

.94

1640

.70

1287

.64

4854

.44

2660

.00

(8.6

)(2

1.2)

(10.

6)(6

.2)

(4.1

)(1

2.3)

(4.6

)(1

2.5)

(15.

9)(1

1.3)

(8.8

)(1

1.1)

(11.

1)

8.C

omm

unic

atio

ns0.

000.

000.

000.

000.

000.

0034

.05

0.00

2.11

0.00

0.00

0.00

0.00

(0.0

9)(0

.02)

9.S

cien

ce, T

echn

olog

y &

11.2

04.

628.

150.

0010

.83

4.75

326.

018.

486.

4236

.19

330.

0025

.78

120.

00E

nviro

nmen

t(0

.0)

(0.1

)(0

.1)

(0.1

)(0

.1)

(0.8

)(0

.1)

(0.1

)(0

.2)

(2.3

)(0

.1)

(0.5

)

10.

Gen

eral

Eco

nom

ic S

ervi

ces

804.

8023

1.70

217.

5935

2.89

169.

1915

9.75

838.

8751

2.35

223.

7417

34.9

118

9.52

895.

6311

68.0

5(1

.7)

(6.0

)(2

.6)

(1.7

)(1

.5)

(5.0

)(2

.1)

(5.0

)(2

.2)

(12.

0)(1

.3)

(2.1

)(4

.9)

11.

Soc

ial S

ervi

ces

1363

4.04

1239

.33

4157

.11

5076

.73

5256

.15

1526

.52

1508

9.45

4311

.08

4893

.48

4016

.43

4847

.14

1418

2.98

4360

.45

(29.

2)(3

1.9)

(50.

0)(2

4.2)

(47.

8)(4

7.7)

(37.

7)(4

1.9)

(47.

5)(2

7.7)

(33.

1)(3

2.6)

(18.

2)

12.

Gen

eral

Ser

vice

s47

9.16

90.9

229

.65

560.

1523

8.29

111.

0020

.85

217.

8484

.75

290.

8251

6.69

487.

6081

38.0

0(1

.0)

(2.3

)(0

.4)

(2.7

)(2

.2)

(3.5

)(0

.1)

(2.1

)(0

.8)

(2.0

)(3

.5)

(1.1

)(3

3.9)

GR

AN

D T

OTA

L46

614.

0038

88.3

283

15.2

421

000.

0011

000.

0032

00.0

040

007.

0010

285.

0010

300.

0014

500.

0014

632.

7443

558.

2324

000.

00(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)

PUBLIC SECTOR PLAN : RESOURCES AND ALLOCATIONS

93

Con

td. A

nnex

ure

: 3-C

Sec

tors

/Sta

tes

Mad

hya

Mah

a-M

anip

ur

Meg

ha-

Miz

o-

Nag

a-O

riss

aP

un

jab

Raj

asth

anS

ikki

mT

amil

Tri

pu

raU

ttar

Pra

de

sh

ras

htr

ala

yara

mla

nd

Nad

uP

rad

es

h14

.15

.16

.17

.18

.19

.20

.21

.22

.23

.24

.25

.26

.

1.A

gric

ultu

re &

Alli

ed A

ctiv

ities

1581

.52

4248

.62

113.

8629

9.60

161.

9825

5.50

1165

.20

635.

4116

49.4

817

4.99

3932

.05

450.

0051

42.4

0(6

.0)

(6.4

)(4

.1)

(10.

0)(7

.0)

(11.

5)(6

.1)

(3.4

)(6

.0)

(10.

6)(9

.8)

(10.

0)(8

.6)

2.R

ural

Dev

elop

men

t28

81.1

669

19.7

212

0.91

208.

1815

6.65

180.

0589

7.91

1276

.50

2298

.84

74.0

041

00.0

054

0.00

7127

.91

(11.

0)(1

0.4)

(4.3

)(6

.9)

(6.8

)(8

.1)

(4.7

)(6

.8)

(8.4

)(4

.5)

(10.

3)(1

2.0)

(11.

9)

3.S

peci

al A

rea

Pro

gram

me

0.00

373.

2222

.88

44.7

040

.37

44.5

50

134.

3716

9.22

30.0

00.

0031

5.00

1000

.00

(0.6

)(0

.8)

(1.5

)(1

.8)

(2.0

)(0

.7)

(0.6

)(1

.8)

(7.0

)(1

.7)

4.Irr

igat

ion

& F

lood

Con

trol

4915

.89

1525

5.01

368.

5497

.40

28.2

841

.00

4099

.21

2611

.51

2767

.88

31.0

023

75.0

036

0.00

7607

.35

(18.

8)(2

2.9)

(13.

1)(3

.2)

(1.2

)(1

.8)

(21.

6)(1

4.0)

(10.

1)(1

.9)

(5.9

)(8

.0)

(12.

7)

5.E

nerg

y55

06.2

010

163.

5123

0.51

505.

7719

4.85

248.

4528

64.8

859

82.7

372

60.7

424

2.90

8029

.65

225.

0096

11.9

9(2

1.0)

(15.

3)(8

.2)

(16.

8)(8

.5)

(11.

2)(1

5.1)

(32.

1)(2

6.6)

(14.

7)(2

0.1)

(5.0

)(1

6.1)

6.In

dust

ry &

Min

eral

s20

2.38

716.

5633

2.94

144.

0060

.38

192.

0510

9.33

55.9

895

5.66

62.0

055

5.00

135.

0012

62.4

6(0

.8)

(1.1

)(1

1.9)

(4.8

)(2

.6)

(8.6

)(0

.6)

(0.3

)(3

.5)

(3.7

)(1

.4)

(3.0

)(2

.1)

7.Tr

ansp

ort

1353

.05

5217

.21

223.

4854

0.30

481.

9017

0.35

1959

.91

2711

.50

3039

.79

265.

0067

30.0

049

5.00

6740

.25

(5.2

)(7

.8)

(8.0

)(1

8.0)

(21.

0)(7

.6)

(10.

3)(1

4.5)

(11.

1)(1

6.0)

(16.

8)(1

1.0)

(11.

3)

8.C

omm

unic

atio

ns0.

000.

000.

000.

000.

000.

000.

000.

000.

000.

000.

009.

000.

00(0

.20)

9.S

cien

ce, T

echn

olog

y59

.70

55.2

517

.22

7.90

5.32

4.50

43.1

138

.75

12.1

711

.00

160.

4013

.50

2414

.75

& E

nviro

nmen

t(0

.2)

(0.1

)(0

.6)

(0.3

)(0

.2)

(0.2

)(0

.2)

(0.2

)(0

.0)

(0.7

)(0

.4)

(0.3

)(4

.0)

10.

Gen

eral

Eco

nom

ic S

ervi

ces

759.

6628

49.5

124

5.21

59.7

012

5.55

228.

0322

85.0

415

0.15

1079

.89

40.4

017

5.60

67.5

022

97.2

5(2

.9)

(4.3

)(8

.7)

(2.0

)(5

.5)

(10.

2)(1

2.0)

(0.8

)(4

.0)

(2.4

)(0

.4)

(1.5

)(3

.8)

11.

Soc

ial S

ervi

ces

7634

.97

1923

3.21

1032

.00

1034

.35

956.

8773

8.40

5075

.89

4858

.37

7996

.77

666.

2513

653.

5518

22.5

016

091.

19(2

9.2)

(28.

9)(3

6.8)

(34.

4)(4

1.6)

(33.

1)(2

6.7)

(26.

0)(2

9.3)

(40.

2)(3

4.1)

(40.

5)(2

6.9)

12.

Gen

eral

Ser

vice

s12

95.4

016

00.1

896

.45

67.1

087

.88

124.

7749

9.52

201.

8387

.56

58.2

028

8.75

67.5

041

2.45

(4.9

)(2

.4)

(3.4

)(2

.2)

(3.8

)(5

.6)

(2.6

)(1

.1)

(0.3

)(3

.5)

(0.7

)(1

.5)

(0.7

)

GR

AN

D T

OTA

L26

189.

9366

632.

0028

04.0

030

09.0

023

00.0

122

27.6

519

000.

0018

657.

0027

318.

0016

55.7

440

000.

0045

00.0

059

708.

00(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)(1

00.0

)

TENTH FIVE YEAR PLAN 2002-07

94

Con

td. A

nnex

ure

: 3-C

Sec

tors

/Sta

tes

Utt

aran

We

st

Sta

tes

A &

NC

han

di-

D &

ND

aman

NC

T o

fL

ak

sh

wa

-P

on

di-

UTs

Sta

tes

& U

Ts

chal

Ben

gal

To

tal (

1 to

28)

Isla

nd

sg

arh

Hav

eli

& D

iuD

elh

id

we

ep

ch

err

yT

ota

l (30

to

36)

To

tal (

29 +

37)

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

1.A

gric

ultu

re &

Alli

ed A

ctiv

ities

694.

9291

4.63

3751

3.60

177.

7720

.33

27.8

49.

2313

7.45

106.

8419

5.80

675.

2538

188.

85(9

.1)

(3.2

)(6

.7)

(7.2

)(2

.0)

(9.2

)(3

.8)

(0.6

)(2

4.4)

(10.

3)(2

.3)

(6.5

)

2.R

ural

Dev

elop

men

t42

0.52

3797

.69

5026

2.65

150.

8410

.17

10.5

310

.58

463.

255.

6031

.52

682.

4950

945.

14(5

.5)

(13.

3)(9

.0)

(6.1

)(1

.0)

(3.5

)(4

.3)

(2.0

)(1

.3)

(1.7

)(2

.3)

(8.6

)

3.S

peci

al A

rea

Pro

gram

me

3.88

1063

.79

6264

.67

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

6264

.67

(0.1

)(3

.7)

(1.1

)(1

.1)

4.Irr

igat

ion

& F

lood

Con

trol

178.

5318

98.6

691

849.

6927

.57

2.00

12.6

04.

5215

6.00

17.3

473

.70

293.

7392

143.

42(2

.3)

(6.6

)(1

6.4)

(1.1

)(0

.2)

(4.1

)(1

.8)

(0.7

)(4

.0)

(3.9

)(1

.0)

(15.

6)

5.E

nerg

y19

43.6

878

55.5

090

738.

0220

7.43

109.

4277

.75

51.4

934

57.5

020

.38

165.

6040

89.5

694

827.

58(2

5.5)

(27.

4)(1

6.2)

(8.4

)(1

0.9)

(25.

6)(2

1.0)

(15.

0)(4

.7)

(8.7

)(1

3.9)

(16.

0)

6.In

dust

ry &

Min

eral

s93

.02

1509

.84

1486

5.69

37.4

61.

901.

701.

9510

0.00

5.06

173.

0032

1.07

1518

6.76

(1.1

)(5

.3)

(2.6

)(1

.5)

(0.2

)(0

.6)

(0.8

)(0

.4)

(1.2

)(9

.1)

(1.1

)(2

.6)

7.Tr

ansp

ort

1089

.06

2799

.17

5687

8.26

978.

1946

.20

62.7

466

.95

5446

.71

146.

1518

0.26

6927

.20

6380

5.46

(14.

3)(9

.8)

(10.

1)(3

9.4)

(4.6

)(2

0.6)

(27.

3)(2

3.7)

(33.

4)(9

.5)

(23.

6)(1

0.8)

8.C

omm

unic

atio

ns0.

000.

0045

.16

9.08

0.00

0.00

0.00

0.00

0.00

0.00

9.08

54.2

4(0

.01)

(0.3

7)(0

.03)

(0.0

1)

9.S

cien

ce, T

echn

olog

y62

.06

155.

1939

53.2

52.

123.

300.

350.

8055

.00

7.08

3.16

71.8

140

25.0

6&

Env

ironm

ent

(0.8

)(0

.5)

(0.7

)(0

.1)

(0.3

)(0

.1)

(0.3

)(0

.2)

(1.6

)(0

.2)

(0.2

)(0

.7)

10.G

ener

al E

cono

mic

Ser

vice

s23

5.35

258.

4718

356.

3060

.98

19.6

56.

176.

2610

7.30

51.1

881

.75

333.

3018

689.

60(3

.1)

(0.9

)(3

.3)

(2.5

)(2

.0)

(2.0

)(2

.6)

(0.5

)(1

1.7)

(4.3

)(1

.1)

(3.2

)

11.S

ocia

l Ser

vice

s28

40.8

578

67.8

017

4093

.86

765.

8677

1.45

97.8

284

.05

1224

7.40

54.8

492

4.40

1494

5.82

1890

39.6

8(3