pure-play pipestone - blackbird energy inc · market conditions blackbird life cycle blackbird...

TRANSCRIPT

Pure-Play Pipestone

TSX-V:BBI

Condensate, Growth, Achievement

Aug 2017

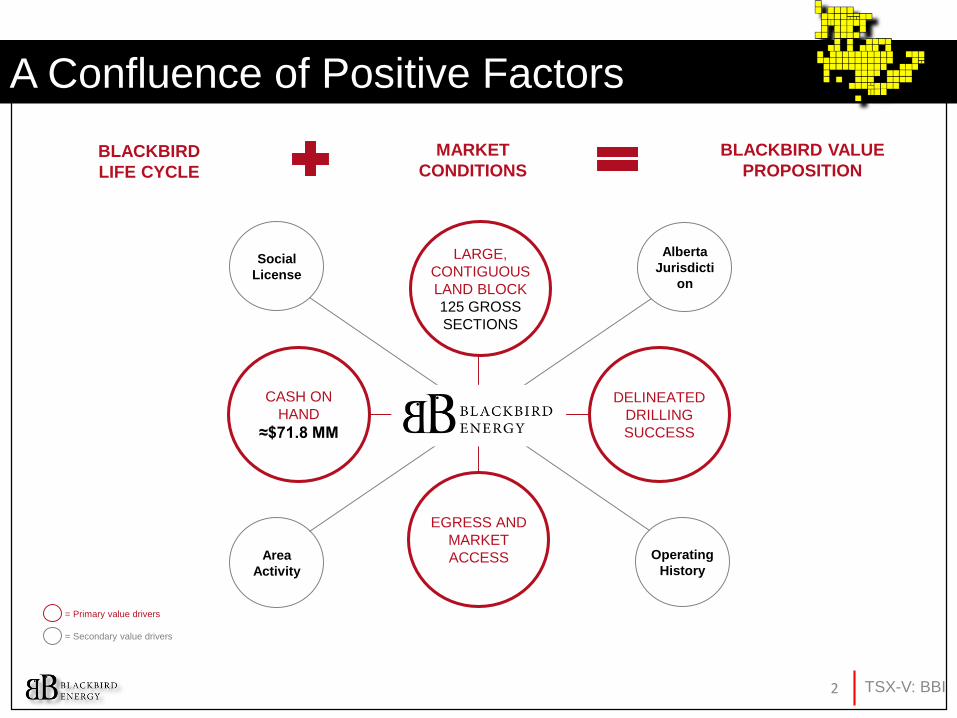

MARKET

CONDITIONSBLACKBIRD

LIFE CYCLE

BLACKBIRD VALUE

PROPOSITION

LARGE,

CONTIGUOUS

LAND BLOCK

125 GROSS

SECTIONS

EGRESS AND

MARKET

ACCESS

DELINEATED

DRILLING

SUCCESS

CASH ON

HAND

≈$71.8 MM

Alberta

Jurisdicti

on

Operating

History

Social

License

Area

Activity

= Primary value drivers

= Secondary value drivers

A Confluence of Positive Factors

TSX-V: BBI2

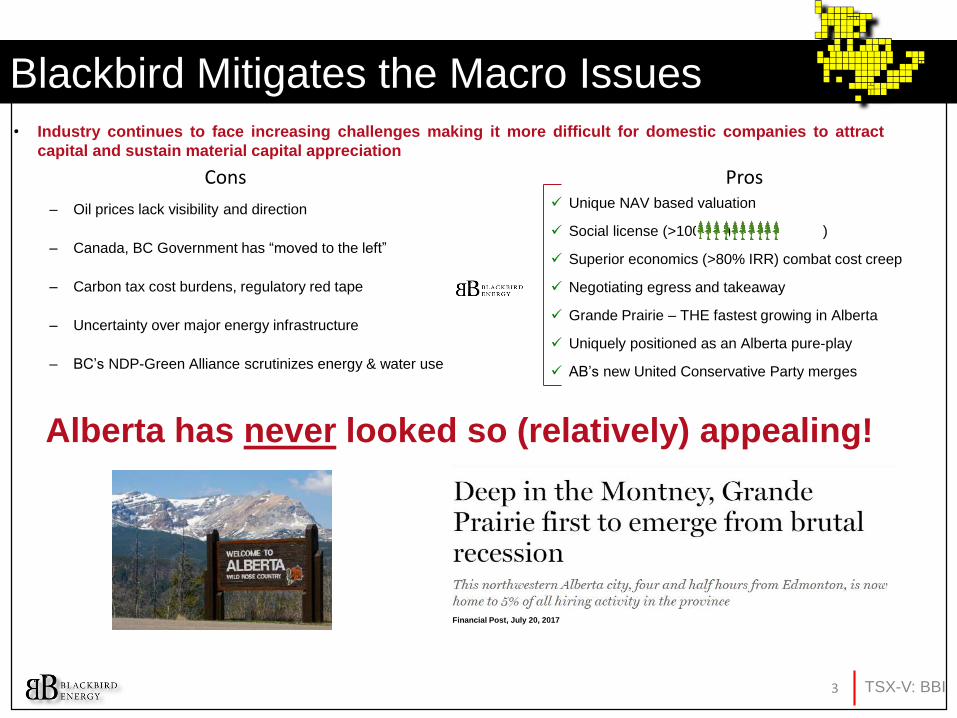

• Industry continues to face increasing challenges making it more difficult for domestic companies to attract

capital and sustain material capital appreciation

– Oil prices lack visibility and direction

– Canada, BC Government has “moved to the left”

– Carbon tax cost burdens, regulatory red tape

– Uncertainty over major energy infrastructure

– BC’s NDP-Green Alliance scrutinizes energy & water use

Blackbird Mitigates the Macro Issues

✓ Unique NAV based valuation

✓ Social license (>100K ) )

✓ Superior economics (>80% IRR) combat cost creep

✓ Negotiating egress and takeaway

✓ Grande Prairie – THE fastest growing in Alberta

✓ Uniquely positioned as an Alberta pure-play

✓ AB’s new United Conservative Party merges

Financial Post, July 20, 2017

Alberta has never looked so (relatively) appealing!

TSX-V: BBI3

ProsCons

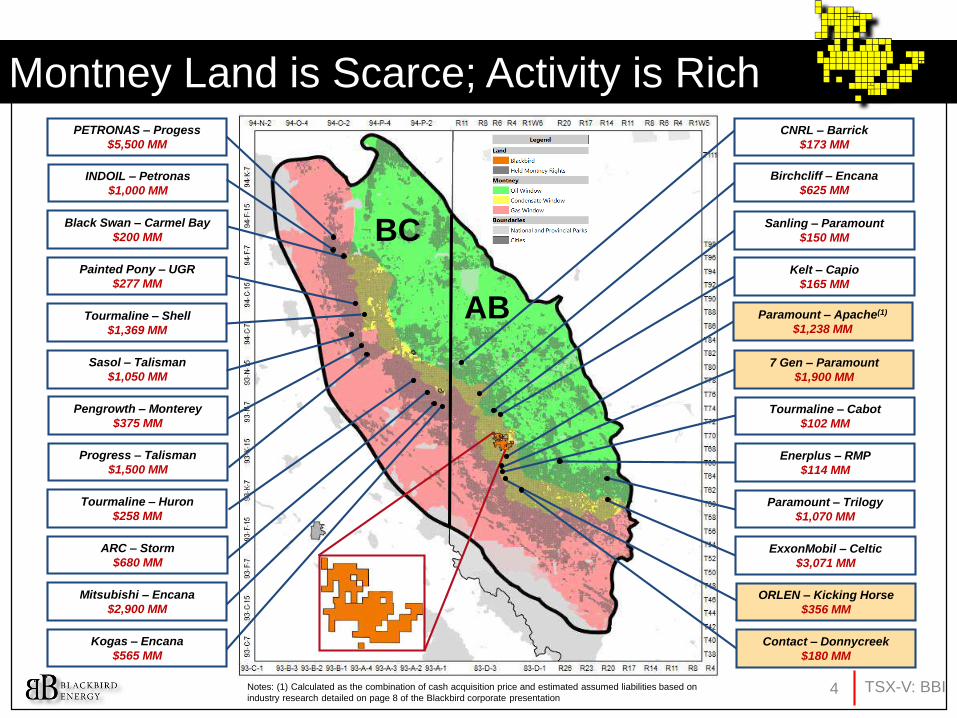

Sasol – Talisman

$1,050 MM

PETRONAS – Progess

$5,500 MM

Black Swan – Carmel Bay

$200 MM

Birchcliff – Encana

$625 MM

7 Gen – Paramount

$1,900 MM

Tourmaline – Shell

$1,369 MM

Painted Pony – UGR

$277 MM

Paramount – Trilogy

$1,070 MM

INDOIL – Petronas

$1,000 MM

Kogas – Encana

$565 MM

Sanling – Paramount

$150 MM

ORLEN – Kicking Horse

$356 MM

Kelt – Capio

$165 MM

ExxonMobil – Celtic

$3,071 MM

Tourmaline – Huron

$258 MM

Pengrowth – Monterey

$375 MM

ARC – Storm

$680 MM

Contact – Donnycreek

$180 MM

Tourmaline – Cabot

$102 MM

Progress – Talisman

$1,500 MM

CNRL – Barrick

$173 MM

Enerplus – RMP

$114 MM

Mitsubishi – Encana

$2,900 MM

Paramount – Apache(1)

$1,238 MM

Montney Land is Scarce; Activity is Rich

TSX-V: BBI4

BC

AB

Notes: (1) Calculated as the combination of cash acquisition price and estimated assumed liabilities based on

industry research detailed on page 8 of the Blackbird corporate presentation

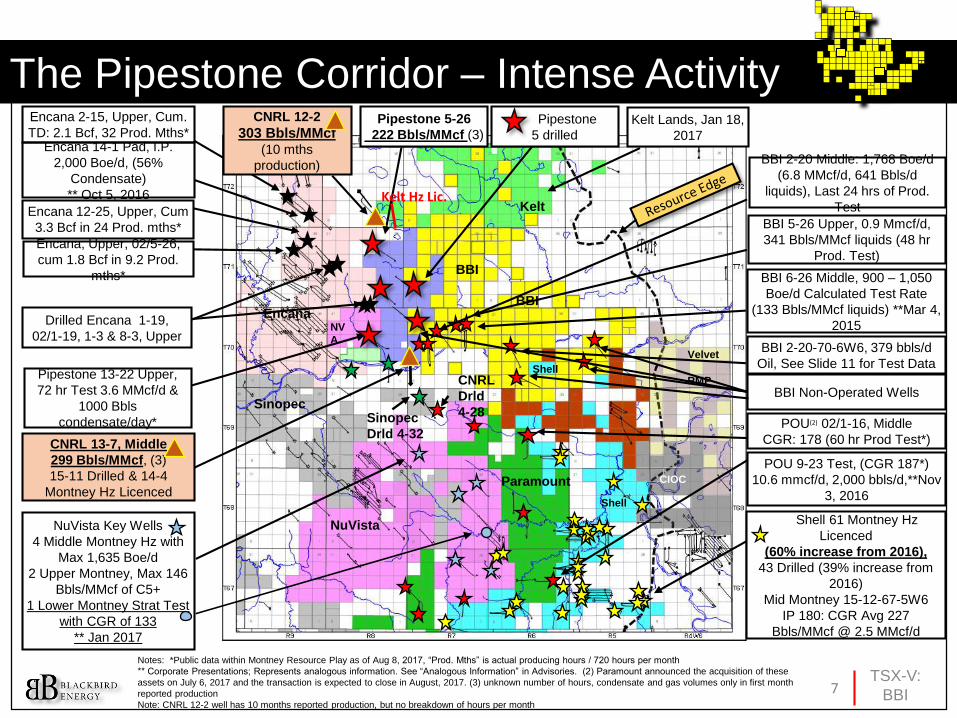

Industry Activity is Exploding in the Pipestone Corridor

• Seven Generations acquisition of Paramount Kakwa

– Sets a new high for undeveloped Montney land at $6.1 MM

per section

• Paramount acquisition of Apache Montney

– Pipestone Montney upside outweighs spending $460 MM

and assuming >$775 MM in liabilities

• ORLEN acquisition of Kicking Horse

– The ultra liquids-rich Montney continues to lure new

international capital investment at a premium

• Contact acquisition of Donnycreek

– Juniors merged to achieve the scale required to lure a larger

buyer to better finance efficient development

Blackbird Pipestone – One of the Most Actively Drilled Corridors in Canada

All Eyes on the Pipestone CorridorThe Highest Value Montney A&D Directly Offsets Blackbird

• Industry plans a major infrastructure investment at Pipestone

through 2020

– Five sour processing facilities & various condensate

pipelines already sanctioned or in FEED stages

– E&P’s require scale to strike a long term take-or-pay with

midstreamers – consolidation is upcoming

• NuVista plans >120 wells on 11 sections three miles west of

Blackbird – stacked pay boosts full-cycle economics

• Encana’s “Cube” development reduces costs and improves

economic recovery factors

– The Cube “will become the industry standard for stacked

pay development”, Doug Suttles, Encana, Pres. & CEO

Paramount’s acquisition of Apache Montney

for $460 MM and $775 MM in liabilities

Velvet’s eastern-most well confirms the

volatile oil window is prospective, validating

all of Blackbird’s lands

Pipestone has been actively licensing and

spudding wells

Three non-operated Blackbird wells extend

the fairway to the east

New Blackbird drill to the north will validate

the northern Wapiti lands

TSX-V: BBI5

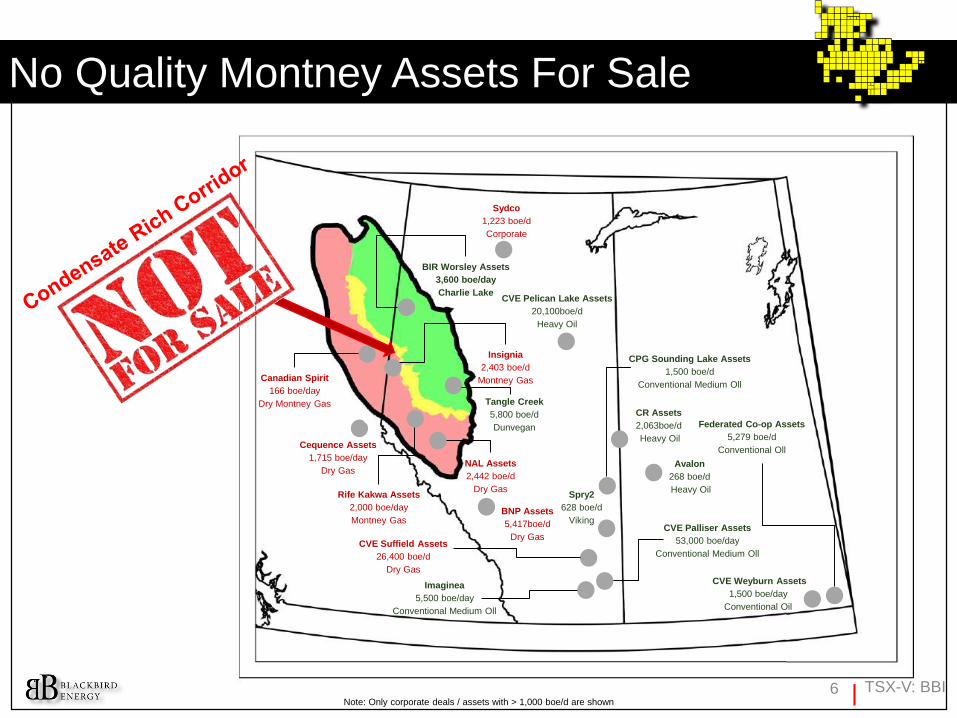

BIR Worsley Assets

3,600 boe/day

Charlie Lake

Insignia

2,403 boe/d

Montney Gas

NAL Assets

2,442 boe/d

Dry Gas

CVE Pelican Lake Assets

20,100boe/d

Heavy Oil

CR Assets

2,063boe/d

Heavy Oil

BNP Assets

5,417boe/d

Dry Gas

Cequence Assets

1,715 boe/day

Dry Gas

Sydco

1,223 boe/d

Corporate

CVE Weyburn Assets

1,500 boe/day

Conventional Oil

CVE Palliser Assets

53,000 boe/day

Conventional Medium Oll

Note: Only corporate deals / assets with > 1,000 boe/d are shown

CVE Suffield Assets

26,400 boe/d

Dry Gas

Canadian Spirit

166 boe/day

Dry Montney Gas

Avalon

268 boe/d

Heavy OilSpry2

628 boe/d

Viking

Rife Kakwa Assets

2,000 boe/day

Montney Gas

No Quality Montney Assets For Sale

Tangle Creek

5,800 boe/d

Dunvegan

Imaginea

5,500 boe/day

Conventional Medium Oll

CPG Sounding Lake Assets

1,500 boe/d

Conventional Medium Oll

Federated Co-op Assets

5,279 boe/d

Conventional Oll

TSX-V: BBI6

TSX-V:

BBI7

BBIEncana

NuVista

Paramount

Shell

CIOC

Sinopec

Encana 2-15, Upper, Cum.

TD: 2.1 Bcf, 32 Prod. Mths*Encana 14-1 Pad, I.P.

2,000 Boe/d, (56%

Condensate)

** Oct 5, 2016

Encana 12-25, Upper, Cum

3.3 Bcf in 24 Prod. mths*

Pipestone 13-22 Upper,

72 hr Test 3.6 MMcf/d &

1000 Bbls

condensate/day*

BBI 6-26 Middle, 900 – 1,050

Boe/d Calculated Test Rate

(133 Bbls/MMcf liquids) **Mar 4,

2015

BBI Non-Operated Wells

POU(2) 02/1-16, Middle

CGR: 178 (60 hr Prod Test*)

Kelt Lands, Jan 18,

2017

Shell 61 Montney Hz

Licenced

(60% increase from 2016),

43 Drilled (39% increase from

2016)

Mid Montney 15-12-67-5W6

IP 180: CGR Avg 227

Bbls/MMcf @ 2.5 MMcf/d

POU 9-23 Test, (CGR 187*)

10.6 mmcf/d, 2,000 bbls/d,**Nov

3, 2016

NuVista Key Wells

4 Middle Montney Hz with

Max 1,635 Boe/d

2 Upper Montney, Max 146

Bbls/MMcf of C5+

1 Lower Montney Strat Test

with CGR of 133

** Jan 2017

Pipestone 5-26

222 Bbls/MMcf (3)

CNRL 13-7, Middle

299 Bbls/MMcf, (3)

15-11 Drilled & 14-4

Montney Hz Licenced

Sinopec

Drld 4-32

BBI 2-20-70-6W6, 379 bbls/d

Oil, See Slide 11 for Test DataShell

Kelt

Pipestone

5 drilled

BBI

NV

A

Encana, Upper, 02/5-26,

cum 1.8 Bcf in 9.2 Prod.

mths*

BBI 2-20 Middle: 1,768 Boe/d

(6.8 MMcf/d, 641 Bbls/d

liquids), Last 24 hrs of Prod.

Test

RMP

Velvet

The Pipestone Corridor – Intense Activity

Notes: *Public data within Montney Resource Play as of Aug 8, 2017, “Prod. Mths” is actual producing hours / 720 hours per month

** Corporate Presentations; Represents analogous information. See “Analogous Information” in Advisories. (2) Paramount announced the acquisition of these

assets on July 6, 2017 and the transaction is expected to close in August, 2017. (3) unknown number of hours, condensate and gas volumes only in first month

reported production

Note: CNRL 12-2 well has 10 months reported production, but no breakdown of hours per month

CNRL

Drld

4-28

Kelt Hz Lic.

BBI 5-26 Upper, 0.9 Mmcf/d,

341 Bbls/MMcf liquids (48 hr

Prod. Test)

CNRL 12-2

303 Bbls/MMcf (10 mths

production)

Drilled Encana 1-19,

02/1-19, 1-3 & 8-3, Upper

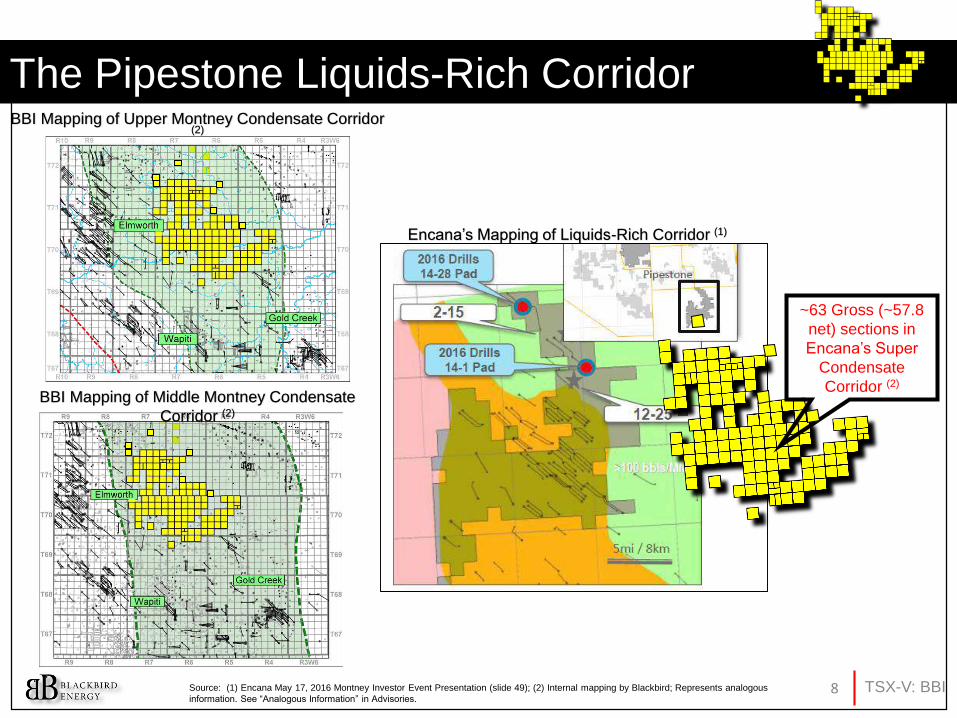

BBI Mapping of Upper Montney Condensate Corridor (2)

The Pipestone Liquids-Rich Corridor

Encana’s Mapping of Liquids-Rich Corridor (1)

BBI Mapping of Middle Montney Condensate

Corridor (2)

Source: (1) Encana May 17, 2016 Montney Investor Event Presentation (slide 49); (2) Internal mapping by Blackbird; Represents analogous

information. See “Analogous Information” in Advisories.

~63 Gross (~57.8

net) sections in

Encana’s Super

Condensate

Corridor (2)

TSX-V: BBI8

The Pipestone Liquids-Rich Corridor

Note: Sourced from Accumap.

A A’Four distinct intervals

Doig/Upper

Montney

Upper

Montney

Middle

Montney

Lower

Montney

10-4-7-8W6 13-22-70-8W6 6-21-70-6W68-25-70-7W602/10-8-70-

7W6

Potential Turbidites

in Lower Montney

Gamma Ray (Green), Bulk Density (Gray)

2

0

0

m

6

5

6

F

t

ECA 4-9 CNOR 13-22 BBI 02/2-

20BBI 5-

26

BBI 2-20 BBI 6-26BBI 2-20

East

A’A

TSX-V: BBI9

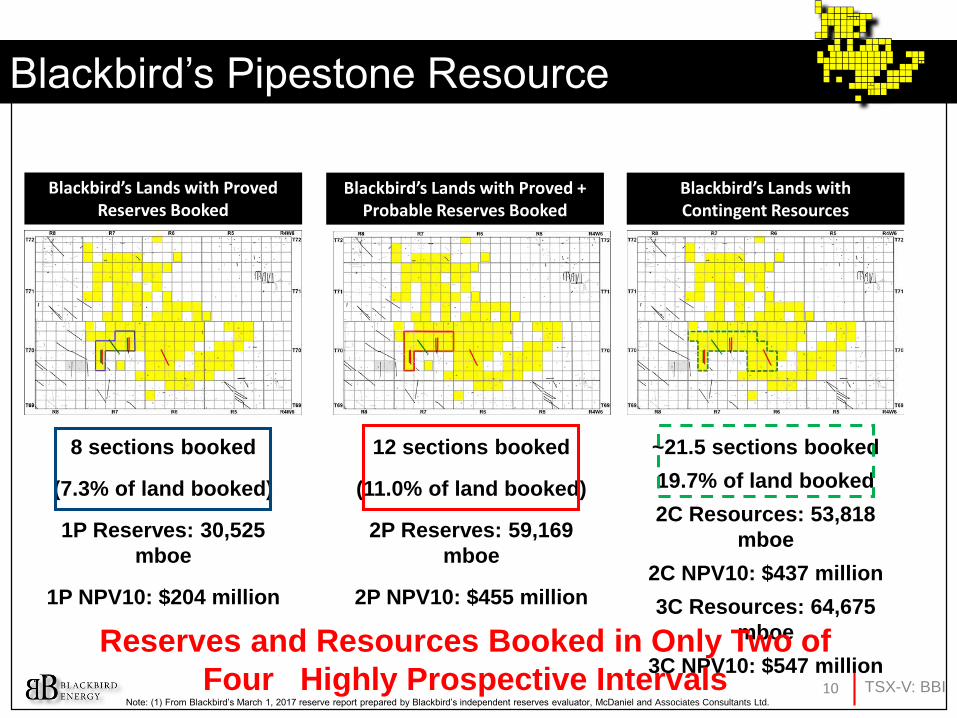

Blackbird’s Pipestone Resource

Blackbird’s Lands with Proved + Probable Reserves Booked

Blackbird’s Lands with Proved Reserves Booked

Blackbird’s Lands with Contingent Resources

8 sections booked

(7.3% of land booked)

1P Reserves: 30,525

mboe

1P NPV10: $204 million

12 sections booked

(11.0% of land booked)

2P Reserves: 59,169

mboe

2P NPV10: $455 million

~21.5 sections booked

19.7% of land booked

2C Resources: 53,818

mboe

2C NPV10: $437 million

3C Resources: 64,675

mboe

3C NPV10: $547 millionReserves and Resources Booked in Only Two of

Four Highly Prospective IntervalsNote: (1) From Blackbird’s March 1, 2017 reserve report prepared by Blackbird’s independent reserves evaluator, McDaniel and Associates Consultants Ltd.

TSX-V: BBI10

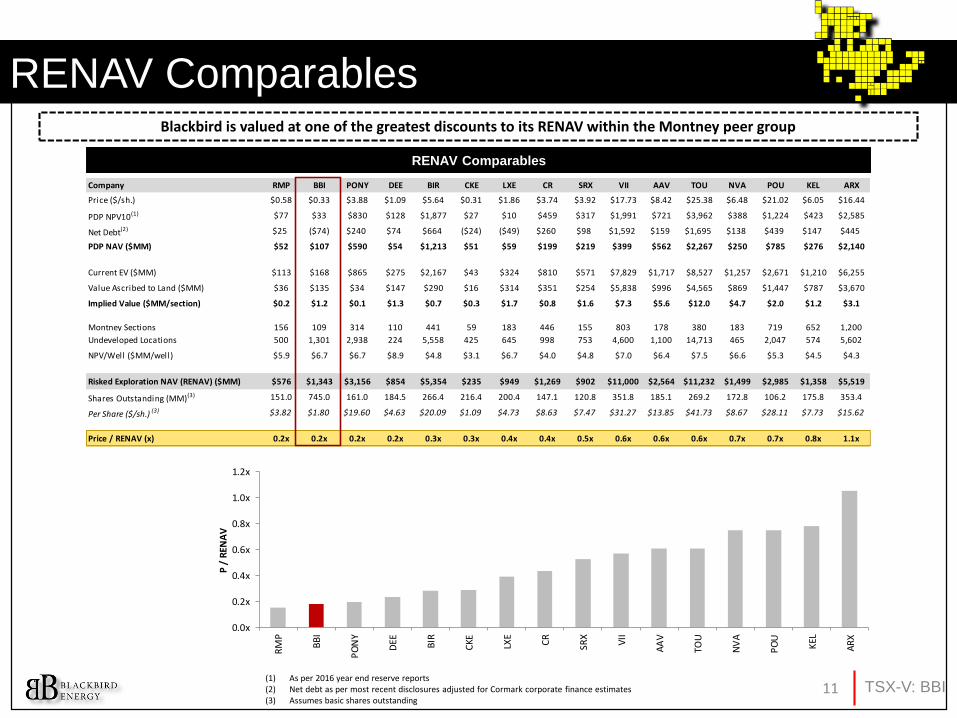

Company RMP BBI PONY DEE BIR CKE LXE CR SRX VII AAV TOU NVA POU KEL ARX

Price ($/sh.) $0.58 $0.33 $3.88 $1.09 $5.64 $0.31 $1.86 $3.74 $3.92 $17.73 $8.42 $25.38 $6.48 $21.02 $6.05 $16.44

PDP NPV10(1) $77 $33 $830 $128 $1,877 $27 $10 $459 $317 $1,991 $721 $3,962 $388 $1,224 $423 $2,585

Net Debt(2) $25 ($74) $240 $74 $664 ($24) ($49) $260 $98 $1,592 $159 $1,695 $138 $439 $147 $445

PDP NAV ($MM) $52 $107 $590 $54 $1,213 $51 $59 $199 $219 $399 $562 $2,267 $250 $785 $276 $2,140

Current EV ($MM) $113 $168 $865 $275 $2,167 $43 $324 $810 $571 $7,829 $1,717 $8,527 $1,257 $2,671 $1,210 $6,255

Value Ascribed to Land ($MM) $36 $135 $34 $147 $290 $16 $314 $351 $254 $5,838 $996 $4,565 $869 $1,447 $787 $3,670

Implied Value ($MM/section) $0.2 $1.2 $0.1 $1.3 $0.7 $0.3 $1.7 $0.8 $1.6 $7.3 $5.6 $12.0 $4.7 $2.0 $1.2 $3.1

Montney Sections 156 109 314 110 441 59 183 446 155 803 178 380 183 719 652 1,200

Undeveloped Locations 500 1,301 2,938 224 5,558 425 645 998 753 4,600 1,100 14,713 465 2,047 574 5,602

NPV/Well ($MM/well) $5.9 $6.7 $6.7 $8.9 $4.8 $3.1 $6.7 $4.0 $4.8 $7.0 $6.4 $7.5 $6.6 $5.3 $4.5 $4.3

Risked Exploration NAV (RENAV) ($MM) $576 $1,343 $3,156 $854 $5,354 $235 $949 $1,269 $902 $11,000 $2,564 $11,232 $1,499 $2,985 $1,358 $5,519

Shares Outstanding (MM)(3) 151.0 745.0 161.0 184.5 266.4 216.4 200.4 147.1 120.8 351.8 185.1 269.2 172.8 106.2 175.8 353.4

Per Share ($/sh.) (3) $3.82 $1.80 $19.60 $4.63 $20.09 $1.09 $4.73 $8.63 $7.47 $31.27 $13.85 $41.73 $8.67 $28.11 $7.73 $15.62

Price / RENAV (x) 0.2x 0.2x 0.2x 0.2x 0.3x 0.3x 0.4x 0.4x 0.5x 0.6x 0.6x 0.6x 0.7x 0.7x 0.8x 1.1x

0.0x

0.2x

0.4x

0.6x

0.8x

1.0x

1.2x

RM

P

BB

I

PO

NY

DEE BIR

CKE LX

E

CR

SRX

VII

AA

V

TOU

NV

A

PO

U

KEL

AR

X

P /

REN

AV

RENAV Comparables

(1) As per 2016 year end reserve reports(2) Net debt as per most recent disclosures adjusted for Cormark corporate finance estimates(3) Assumes basic shares outstanding

Blackbird is valued at one of the greatest discounts to its RENAV within the Montney peer group

RENAV Comparables

TSX-V: BBI11

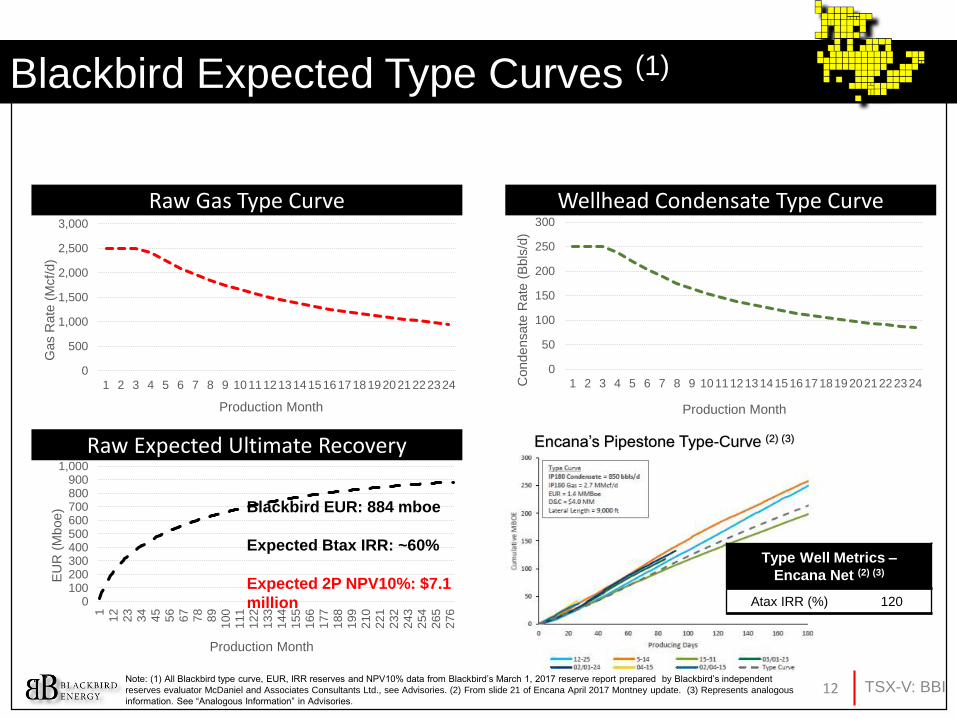

Blackbird Expected Type Curves (1)

0

500

1,000

1,500

2,000

2,500

3,000

1 2 3 4 5 6 7 8 9 101112131415161718192021222324

Gas R

ate

(M

cf/

d)

Production Month

Raw Gas Type Curve

0

50

100

150

200

250

300

1 2 3 4 5 6 7 8 9 101112131415161718192021222324Condensate

Rate

(B

bls

/d)

Production Month

Wellhead Condensate Curve

0100200300400500600700800900

1,000

11

22

3

34

45

56

67

78

89

100

111

122

133

144

155

166

177

188

199

210

221

232

243

254

265

276

EU

R (

Mboe)

Production Month

Raw Expected Ultimate Recovery

Raw Gas Type Curve Wellhead Condensate Type Curve

Raw Expected Ultimate Recovery

Note: (1) All Blackbird type curve, EUR, IRR reserves and NPV10% data from Blackbird’s March 1, 2017 reserve report prepared by Blackbird’s independent

reserves evaluator McDaniel and Associates Consultants Ltd., see Advisories. (2) From slide 21 of Encana April 2017 Montney update. (3) Represents analogous

information. See “Analogous Information” in Advisories.

Blackbird EUR: 884 mboe

Expected Btax IRR: ~60%

Expected 2P NPV10%: $7.1

million

Type Well Metrics –

Encana Net (2) (3)

Atax IRR (%) 120

Encana’s Pipestone Type-Curve (2) (3)

TSX-V: BBI12

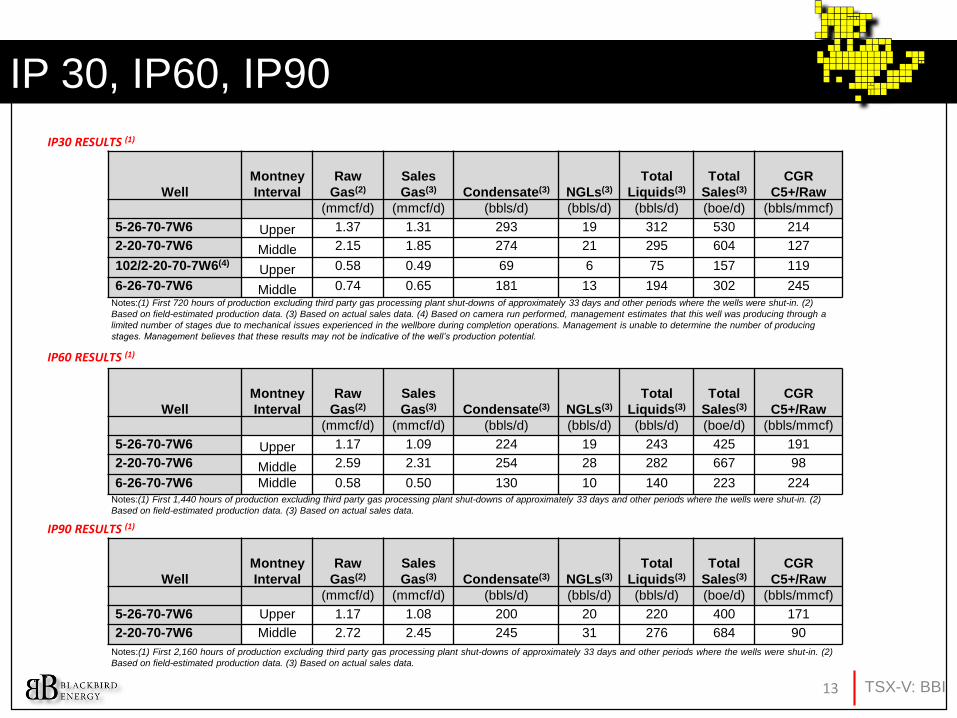

IP 30, IP60, IP90

Well

Montney

Interval

Raw

Gas(2)

Sales

Gas(3) Condensate(3) NGLs(3)

Total

Liquids(3)

Total

Sales(3)

CGR

C5+/Raw

(mmcf/d) (mmcf/d) (bbls/d) (bbls/d) (bbls/d) (boe/d) (bbls/mmcf)

5-26-70-7W6 Upper 1.37 1.31 293 19 312 530 214

2-20-70-7W6 Middle 2.15 1.85 274 21 295 604 127

102/2-20-70-7W6(4)Upper 0.58 0.49 69 6 75 157 119

6-26-70-7W6 Middle 0.74 0.65 181 13 194 302 245

IP30 RESULTS (1)

Notes:(1) First 720 hours of production excluding third party gas processing plant shut-downs of approximately 33 days and other periods where the wells were shut-in. (2)

Based on field-estimated production data. (3) Based on actual sales data. (4) Based on camera run performed, management estimates that this well was producing through a

limited number of stages due to mechanical issues experienced in the wellbore during completion operations. Management is unable to determine the number of producing

stages. Management believes that these results may not be indicative of the well’s production potential.

Well

Montney

Interval

Raw

Gas(2)

Sales

Gas(3) Condensate(3) NGLs(3)

Total

Liquids(3)

Total

Sales(3)

CGR

C5+/Raw

(mmcf/d) (mmcf/d) (bbls/d) (bbls/d) (bbls/d) (boe/d) (bbls/mmcf)

5-26-70-7W6 Upper 1.17 1.09 224 19 243 425 191

2-20-70-7W6 Middle 2.59 2.31 254 28 282 667 98

6-26-70-7W6 Middle 0.58 0.50 130 10 140 223 224Notes:(1) First 1,440 hours of production excluding third party gas processing plant shut-downs of approximately 33 days and other periods where the wells were shut-in. (2)

Based on field-estimated production data. (3) Based on actual sales data.

IP90 RESULTS (1)

IP60 RESULTS (1)

Well

Montney

Interval

Raw

Gas(2)

Sales

Gas(3) Condensate(3) NGLs(3)

Total

Liquids(3)

Total

Sales(3)

CGR

C5+/Raw

(mmcf/d) (mmcf/d) (bbls/d) (bbls/d) (bbls/d) (boe/d) (bbls/mmcf)

5-26-70-7W6 Upper 1.17 1.08 200 20 220 400 171

2-20-70-7W6 Middle 2.72 2.45 245 31 276 684 90

Notes:(1) First 2,160 hours of production excluding third party gas processing plant shut-downs of approximately 33 days and other periods where the wells were shut-in. (2)

Based on field-estimated production data. (3) Based on actual sales data.

TSX-V: BBI13

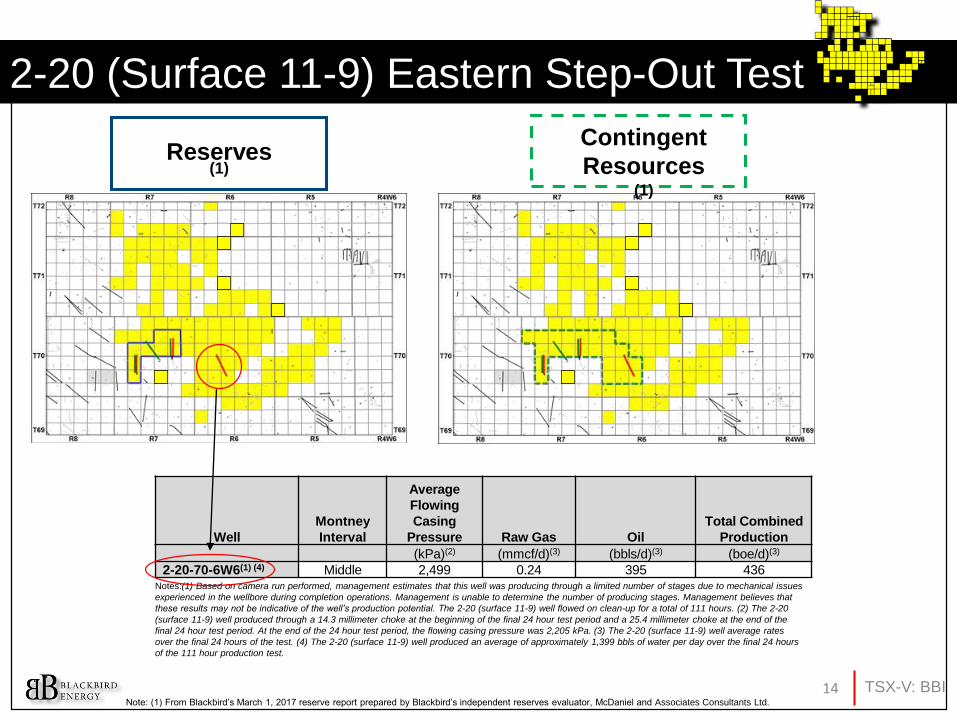

2-20 (Surface 11-9) Eastern Step-Out Test

Well

Montney

Interval

Average

Flowing

Casing

Pressure Raw Gas Oil

Total Combined

Production

(kPa)(2) (mmcf/d)(3) (bbls/d)(3) (boe/d)(3)

2-20-70-6W6(1) (4) Middle 2,499 0.24 395 436Notes:(1) Based on camera run performed, management estimates that this well was producing through a limited number of stages due to mechanical issues

experienced in the wellbore during completion operations. Management is unable to determine the number of producing stages. Management believes that

these results may not be indicative of the well’s production potential. The 2-20 (surface 11-9) well flowed on clean-up for a total of 111 hours. (2) The 2-20

(surface 11-9) well produced through a 14.3 millimeter choke at the beginning of the final 24 hour test period and a 25.4 millimeter choke at the end of the

final 24 hour test period. At the end of the 24 hour test period, the flowing casing pressure was 2,205 kPa. (3) The 2-20 (surface 11-9) well average rates

over the final 24 hours of the test. (4) The 2-20 (surface 11-9) well produced an average of approximately 1,399 bbls of water per day over the final 24 hours

of the 111 hour production test.

Contingent

Resources(1)

Reserves (1)

Note: (1) From Blackbird’s March 1, 2017 reserve report prepared by Blackbird’s independent reserves evaluator, McDaniel and Associates Consultants Ltd.

TSX-V: BBI14

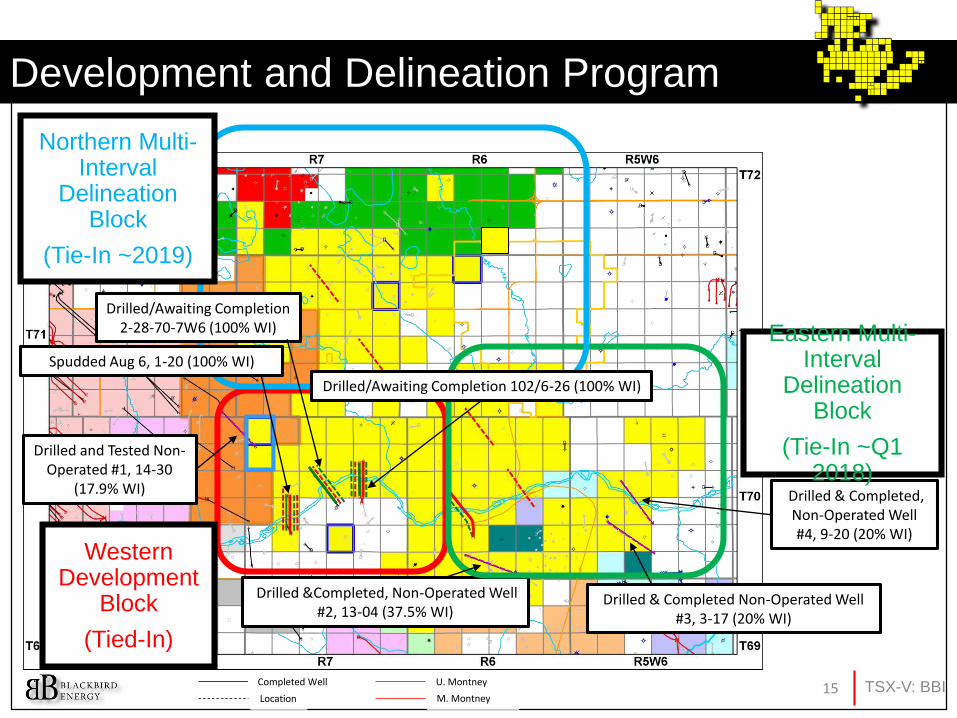

Drilled and Tested Non-Operated #1, 14-30

(17.9% WI)

Drilled &Completed, Non-Operated Well #2, 13-04 (37.5% WI)

Completed Well

Location

U. Montney

M. Montney

Development and Delineation Program

Northern Multi-Interval

Delineation Block

(Tie-In ~2019)

Western Development

Block

(Tied-In)

Drilled/Awaiting Completion 102/6-26 (100% WI)

Drilled & Completed, Non-Operated Well #4, 9-20 (20% WI)

Drilled/Awaiting Completion 2-28-70-7W6 (100% WI)

Spudded Aug 6, 1-20 (100% WI)

TSX-V: BBI15

Drilled & Completed Non-Operated Well #3, 3-17 (20% WI)

Eastern Multi-Interval

Delineation Block

(Tie-In ~Q1 2018)

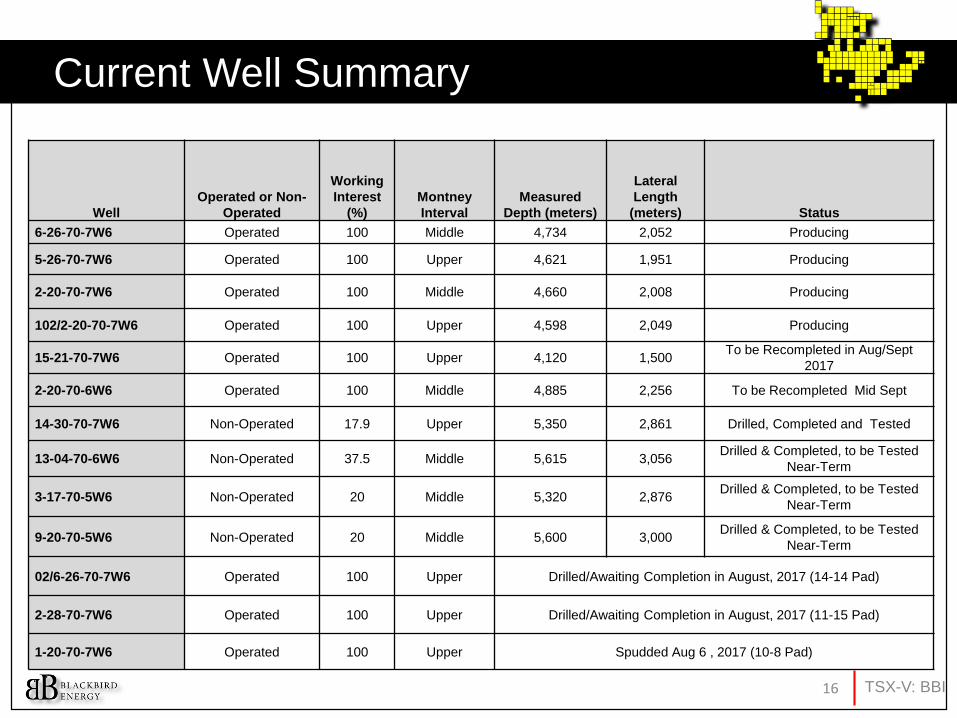

Current Well Summary

Well

Operated or Non-

Operated

Working

Interest

(%)

Montney

Interval

Measured

Depth (meters)

Lateral

Length

(meters) Status

6-26-70-7W6 Operated 100 Middle 4,734 2,052 Producing

5-26-70-7W6 Operated 100 Upper 4,621 1,951 Producing

2-20-70-7W6 Operated 100 Middle 4,660 2,008 Producing

102/2-20-70-7W6 Operated 100 Upper 4,598 2,049 Producing

15-21-70-7W6 Operated 100 Upper 4,120 1,500To be Recompleted in Aug/Sept

2017

2-20-70-6W6 Operated 100 Middle 4,885 2,256 To be Recompleted Mid Sept

14-30-70-7W6 Non-Operated 17.9 Upper 5,350 2,861 Drilled, Completed and Tested

13-04-70-6W6 Non-Operated 37.5 Middle 5,615 3,056Drilled & Completed, to be Tested

Near-Term

3-17-70-5W6 Non-Operated 20 Middle 5,320 2,876Drilled & Completed, to be Tested

Near-Term

9-20-70-5W6 Non-Operated 20 Middle 5,600 3,000Drilled & Completed, to be Tested

Near-Term

02/6-26-70-7W6 Operated 100 Upper Drilled/Awaiting Completion in August, 2017 (14-14 Pad)

2-28-70-7W6 Operated 100 Upper Drilled/Awaiting Completion in August, 2017 (11-15 Pad)

1-20-70-7W6 Operated 100 Upper Spudded Aug 6 , 2017 (10-8 Pad)

TSX-V: BBI16

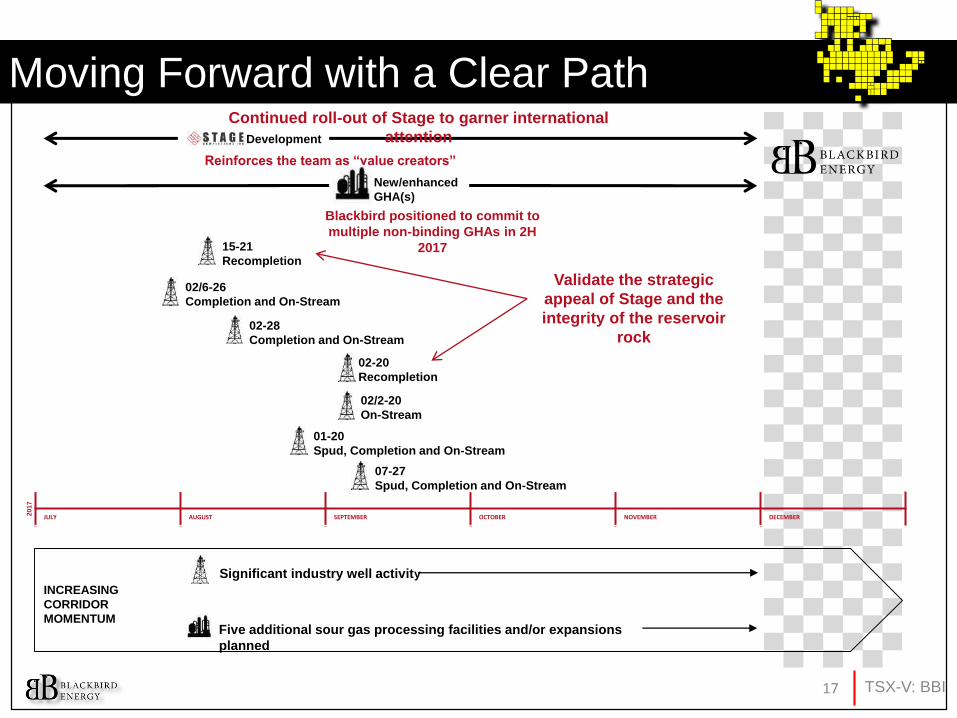

JULY AUGUST SEPTEMBER OCTOBER NOVEMBER DECEMBER

Development

02/2-20

On-Stream

15-21

Recompletion

02-20

Recompletion

New/enhanced

GHA(s)

02/6-26

Completion and On-Stream

02-28

Completion and On-Stream

01-20

Spud, Completion and On-Stream

Five additional sour gas processing facilities and/or expansions

planned

INCREASING

CORRIDOR

MOMENTUM

Significant industry well activity

Reinforces the team as “value creators”

Blackbird positioned to commit to

multiple non-binding GHAs in 2H

2017

Validate the strategic

appeal of Stage and the

integrity of the reservoir

rock

Moving Forward with a Clear Path

2017

07-27

Spud, Completion and On-Stream

Continued roll-out of Stage to garner international

attention

TSX-V: BBI17

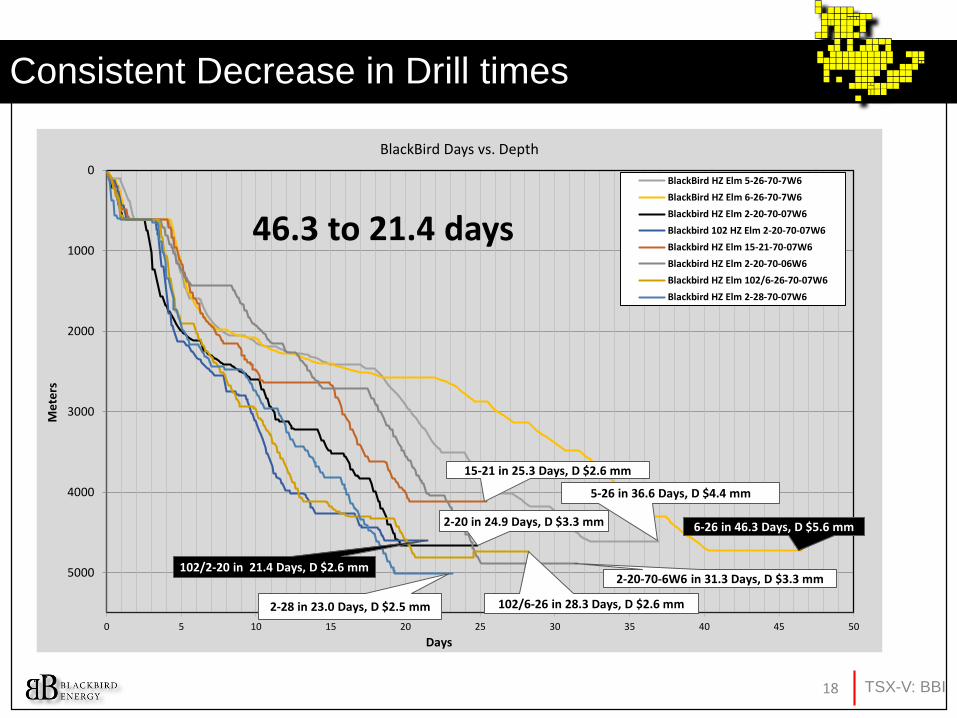

5-26 in 36.6 Days, D $4.4 mm

6-26 in 46.3 Days, D $5.6 mm2-20 in 24.9 Days, D $3.3 mm

102/2-20 in 21.4 Days, D $2.6 mm

15-21 in 25.3 Days, D $2.6 mm

2-20-70-6W6 in 31.3 Days, D $3.3 mm

102/6-26 in 28.3 Days, D $2.6 mm2-28 in 23.0 Days, D $2.5 mm

0

1000

2000

3000

4000

5000

0 5 10 15 20 25 30 35 40 45 50

Me

ters

Days

BlackBird Days vs. Depth

BlackBird HZ Elm 5-26-70-7W6

BlackBird HZ Elm 6-26-70-7W6

Blackbird HZ Elm 2-20-70-07W6

Blackbird 102 HZ Elm 2-20-70-07W6

Blackbird HZ Elm 15-21-70-07W6

Blackbird HZ Elm 2-20-70-06W6

Blackbird HZ Elm 102/6-26-70-07W6

Blackbird HZ Elm 2-28-70-07W6

Consistent Decrease in Drill times

46.3 to 21.4 days

TSX-V: BBI18

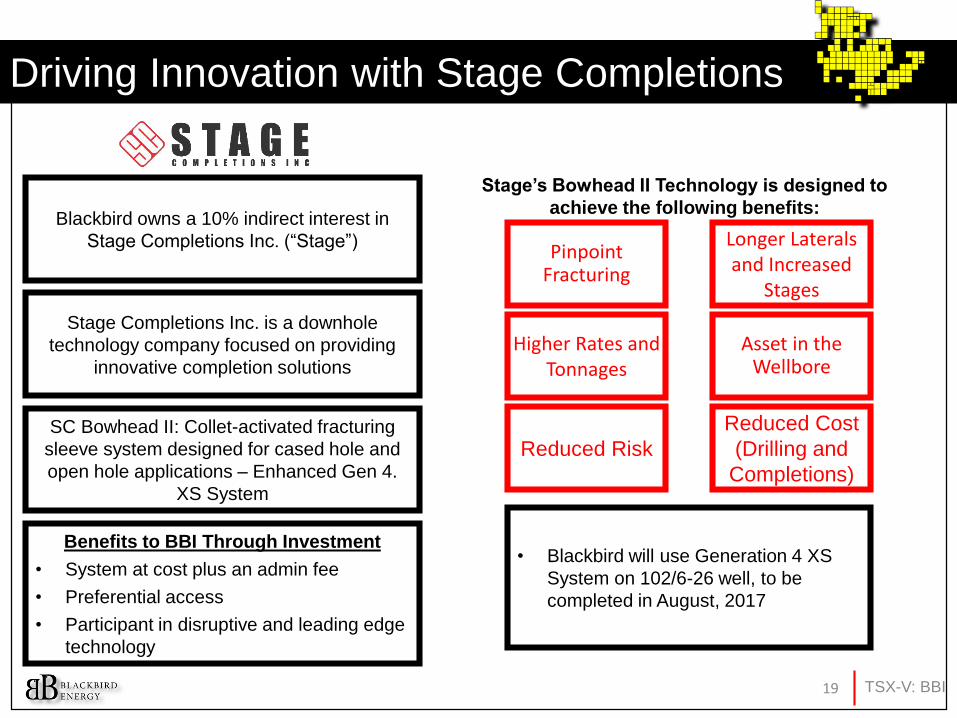

Benefits to BBI Through Investment

• System at cost plus an admin fee

• Preferential access

• Participant in disruptive and leading edge

technology

Stage’s Bowhead II Technology is designed to

achieve the following benefits:

Pinpoint fracturing

Longer Laterals and Increased

Stages

Asset in the Wellbore

Reduced Cost

Pinpoint Fracturing

Longer Laterals and Increased

Stages

Higher Rates and Tonnages

Asset in the Wellbore

Reduced Risk

Reduced Cost

(Drilling and

Completions)

Driving Innovation with Stage Completions

Blackbird owns a 10% indirect interest in

Stage Completions Inc. (“Stage”)

Stage Completions Inc. is a downhole

technology company focused on providing

innovative completion solutions

SC Bowhead II: Collet-activated fracturing

sleeve system designed for cased hole and

open hole applications – Enhanced Gen 4.

XS System

• Blackbird will use Generation 4 XS

System on 102/6-26 well, to be

completed in August, 2017

TSX-V: BBI19

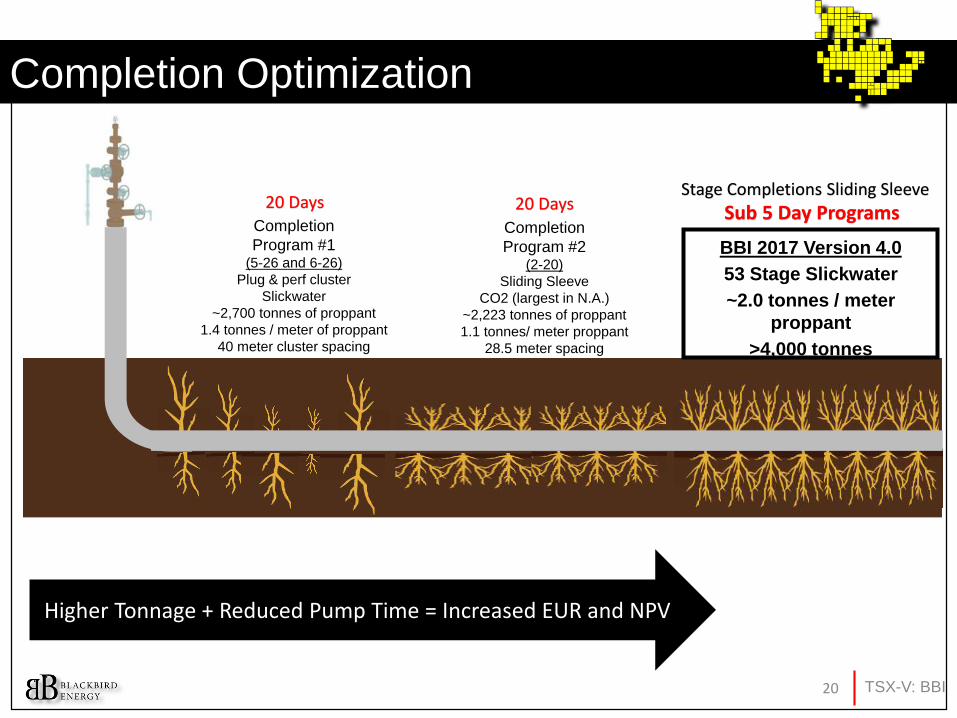

Completion

Program #1(5-26 and 6-26)

Plug & perf cluster

Slickwater

~2,700 tonnes of proppant

1.4 tonnes / meter of proppant

40 meter cluster spacing

Completion

Program #2(2-20)

Sliding Sleeve

CO2 (largest in N.A.)

~2,223 tonnes of proppant

1.1 tonnes/ meter proppant

28.5 meter spacing

BBI 2017 Version 4.0

53 Stage Slickwater

~2.0 tonnes / meter

proppant

>4,000 tonnes

20 Days 20 DaysStage Completions Sliding Sleeve

Completion Optimization

Sub 5 Day Programs

Higher Tonnage + Reduced Pump Time = Increased EUR and NPV

TSX-V: BBI20

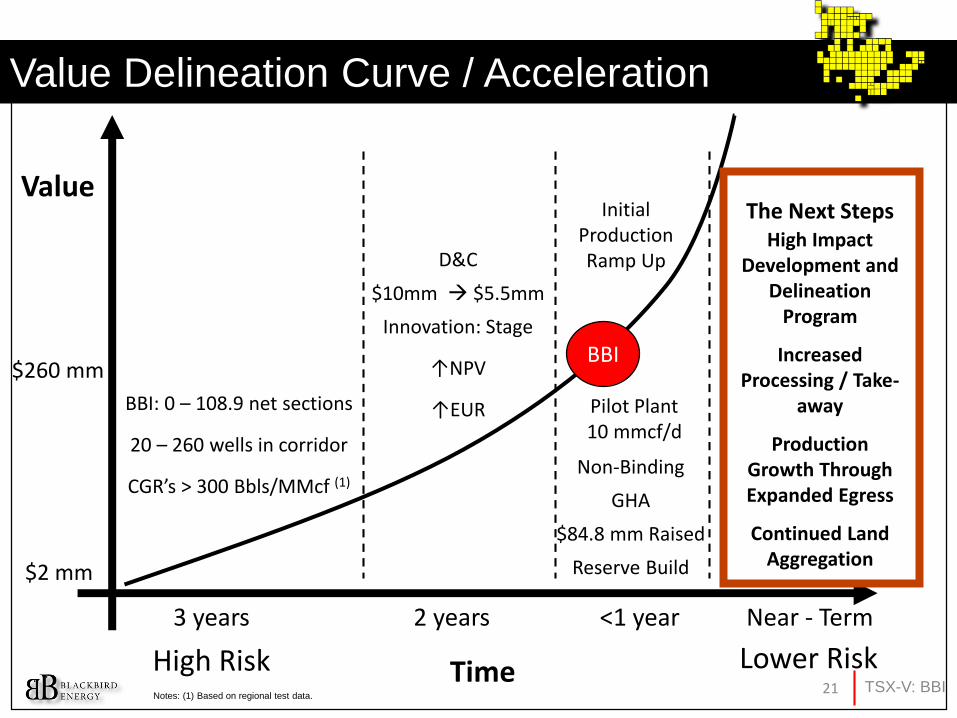

2 years <1 year

D&C

$10mm $5.5mm

Innovation: Stage

↑NPV

↑EUR

Value Delineation Curve / Acceleration

Value

High Risk Time

Initial Production Ramp Up

BBI

BBI: 0 – 108.9 net sections

20 – 260 wells in corridor

CGR’s > 300 Bbls/MMcf (1)

The Next StepsHigh Impact

Development and Delineation

Program

Increased Processing / Take-

away

Production Growth Through Expanded Egress

Continued Land Aggregation

Pilot Plant10 mmcf/d

Non-Binding

GHA

$84.8 mm Raised

Reserve Build

Lower Risk

3 years Near - Term

$2 mm

$260 mm

Notes: (1) Based on regional test data.TSX-V: BBI21

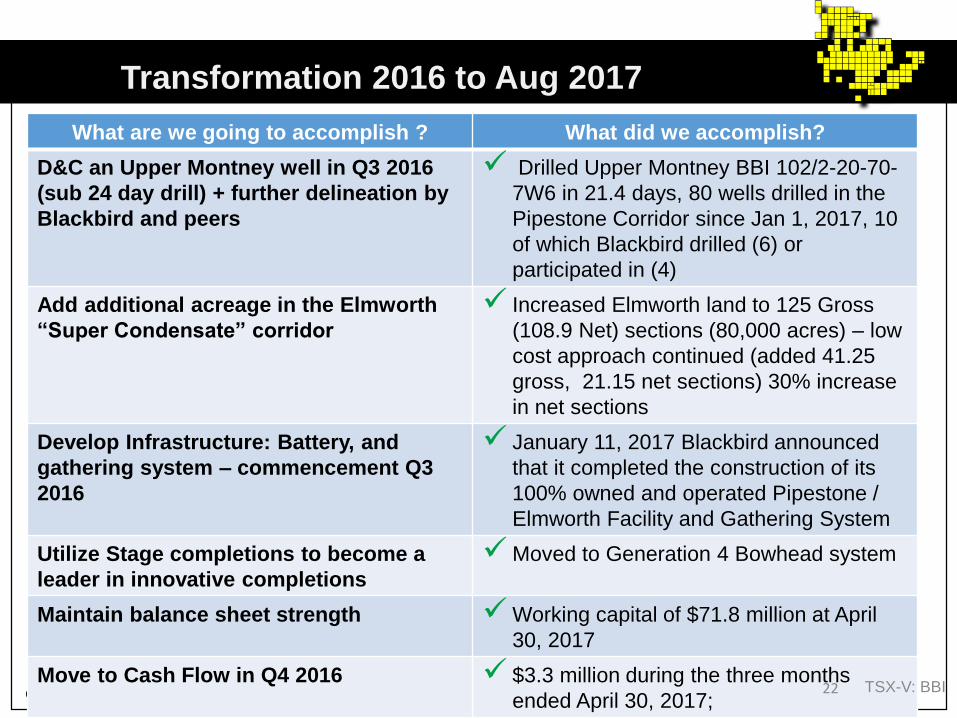

Transformation 2016 to Aug 2017

What are we going to accomplish ? What did we accomplish?

D&C an Upper Montney well in Q3 2016

(sub 24 day drill) + further delineation by

Blackbird and peers

✓ Drilled Upper Montney BBI 102/2-20-70-

7W6 in 21.4 days, 80 wells drilled in the

Pipestone Corridor since Jan 1, 2017, 10

of which Blackbird drilled (6) or

participated in (4)

Add additional acreage in the Elmworth

“Super Condensate” corridor

✓ Increased Elmworth land to 125 Gross

(108.9 Net) sections (80,000 acres) – low

cost approach continued (added 41.25

gross, 21.15 net sections) 30% increase

in net sections

Develop Infrastructure: Battery, and

gathering system – commencement Q3

2016

✓ January 11, 2017 Blackbird announced

that it completed the construction of its

100% owned and operated Pipestone /

Elmworth Facility and Gathering System

Utilize Stage completions to become a

leader in innovative completions

✓Moved to Generation 4 Bowhead system

Maintain balance sheet strength ✓Working capital of $71.8 million at April

30, 2017

Move to Cash Flow in Q4 2016 ✓ $3.3 million during the three months

ended April 30, 2017;TSX-V: BBI22

• Corporate Social Responsibility is critical to gain social

license to operate in any community

• Tree Planting Program: focused on reclaiming boreal forest and

replacing trees we take down;

• Planted 101,579 trees to date!

• Thank you Cormark, Pareto, TD, BMO, Scotia, Laurentian, &

Jett Capital

• Goal: 200,000 trees

• Movement to reduce flare volumes

• Reduction in water usage through technology

• Boring vs. cutlines

• Mitigation of traffic impact

• Extensive community consultation

• Noise mitigation

• Our plan gives us a significant competitive advantage as

we develop our resource – this is also the right way to

do business

Corporate Social Responsibility

TSX-V: BBI23

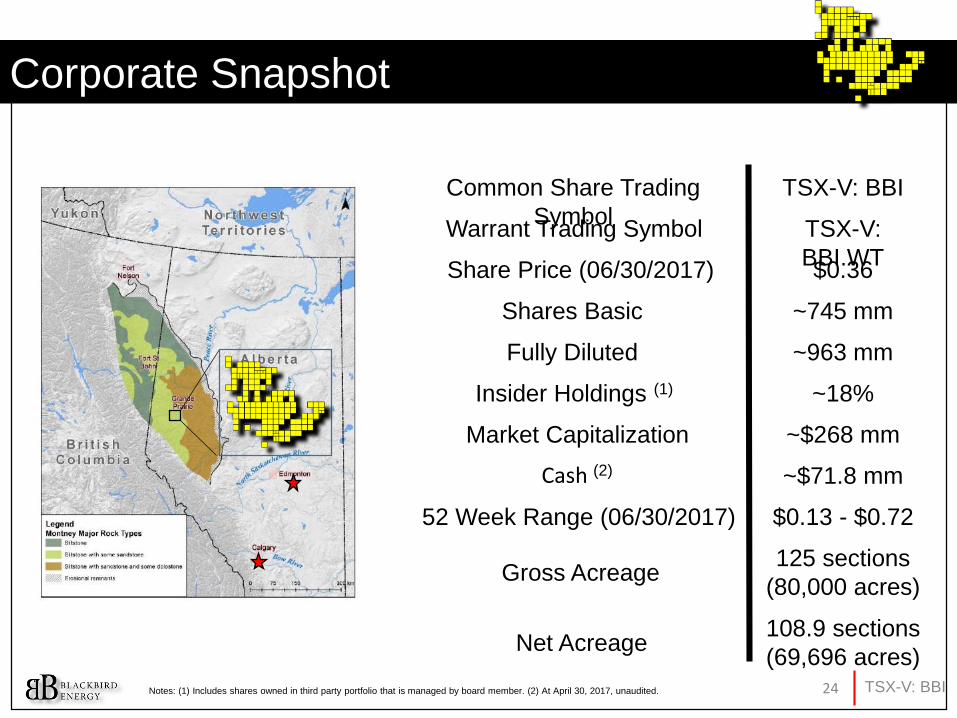

Common Share Trading

Symbol

TSX-V: BBI

Warrant Trading Symbol TSX-V:

BBI.WT

Shares Basic

Fully Diluted

Insider Holdings (1)

Market Capitalization

52 Week Range (06/30/2017)

Share Price (06/30/2017) $0.36

~745 mm

~963 mm

~18%

~$268 mm

$0.13 - $0.72

Notes: (1) Includes shares owned in third party portfolio that is managed by board member. (2) At April 30, 2017, unaudited.

Gross Acreage 125 sections

(80,000 acres)

Net Acreage 108.9 sections

(69,696 acres)

Cash (2) ~$71.8 mm

Corporate Snapshot

TSX-V: BBI24

Finance Operations Geology

Land

Garth BraunChairman, CEO & President

Ron SchmitzInterim CFO and Director

Travis Belak, CASenior Financial Accountant

Jeanette VanderveenOperational Accountant

Don Noakes, P.EngVP Operations

Craig Wiebe, P.GeoVP Exploration

Josh WylieVP Land

John BooneLandman

Arlene FurjanicSenior Land Analyst

Paul GoodmanManager, Completions & Production

Brad PetersonMarketing

Laura ShandroProduction Accountant

Ralph Allen, P.GeoVP Geosciences

Robert SzumilasSupervisor, Drilling & Completions

David Mills, P.EngManager, Facilities Engineering

Appendix: The TeamLeadership

TSX-V: BBI25

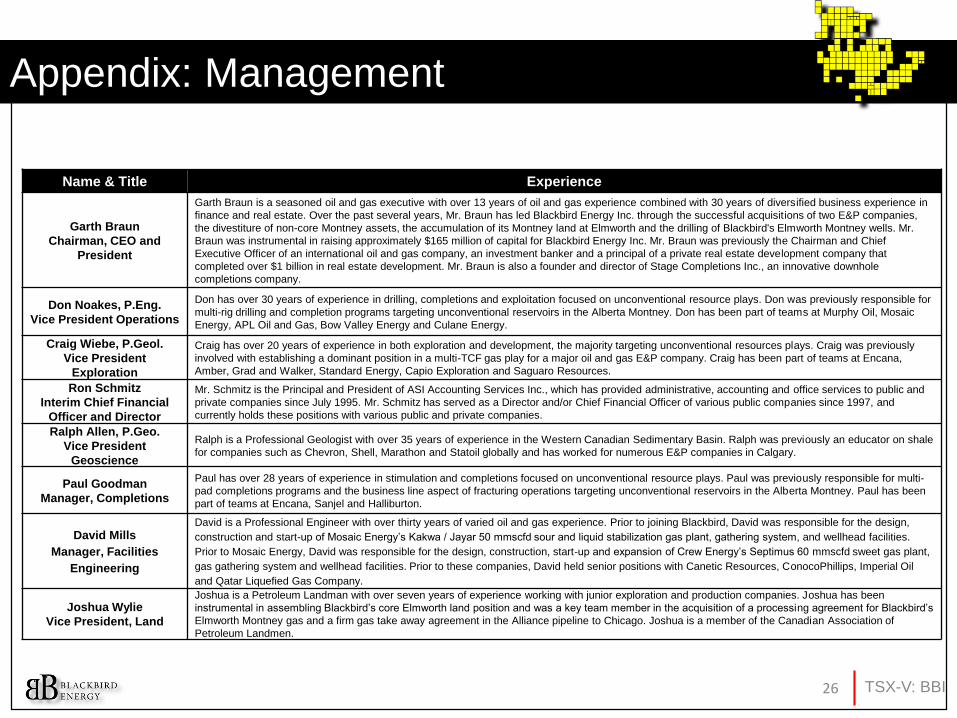

Name & Title Experience

Garth Braun

Chairman, CEO and

President

Garth Braun is a seasoned oil and gas executive with over 13 years of oil and gas experience combined with 30 years of diversified business experience in

finance and real estate. Over the past several years, Mr. Braun has led Blackbird Energy Inc. through the successful acquisitions of two E&P companies,

the divestiture of non-core Montney assets, the accumulation of its Montney land at Elmworth and the drilling of Blackbird's Elmworth Montney wells. Mr.

Braun was instrumental in raising approximately $165 million of capital for Blackbird Energy Inc. Mr. Braun was previously the Chairman and Chief

Executive Officer of an international oil and gas company, an investment banker and a principal of a private real estate development company that

completed over $1 billion in real estate development. Mr. Braun is also a founder and director of Stage Completions Inc., an innovative downhole

completions company.

Don Noakes, P.Eng.

Vice President Operations

Don has over 30 years of experience in drilling, completions and exploitation focused on unconventional resource plays. Don was previously responsible for

multi-rig drilling and completion programs targeting unconventional reservoirs in the Alberta Montney. Don has been part of teams at Murphy Oil, Mosaic

Energy, APL Oil and Gas, Bow Valley Energy and Culane Energy.

Craig Wiebe, P.Geol.

Vice President

Exploration

Craig has over 20 years of experience in both exploration and development, the majority targeting unconventional resources plays. Craig was previously

involved with establishing a dominant position in a multi-TCF gas play for a major oil and gas E&P company. Craig has been part of teams at Encana,

Amber, Grad and Walker, Standard Energy, Capio Exploration and Saguaro Resources.

Ron Schmitz

Interim Chief Financial

Officer and Director

Mr. Schmitz is the Principal and President of ASI Accounting Services Inc., which has provided administrative, accounting and office services to public and

private companies since July 1995. Mr. Schmitz has served as a Director and/or Chief Financial Officer of various public companies since 1997, and

currently holds these positions with various public and private companies.

Ralph Allen, P.Geo.

Vice President

Geoscience

Ralph is a Professional Geologist with over 35 years of experience in the Western Canadian Sedimentary Basin. Ralph was previously an educator on shale

for companies such as Chevron, Shell, Marathon and Statoil globally and has worked for numerous E&P companies in Calgary.

Paul Goodman

Manager, Completions

Paul has over 28 years of experience in stimulation and completions focused on unconventional resource plays. Paul was previously responsible for multi-

pad completions programs and the business line aspect of fracturing operations targeting unconventional reservoirs in the Alberta Montney. Paul has been

part of teams at Encana, Sanjel and Halliburton.

David Mills

Manager, Facilities

Engineering

David is a Professional Engineer with over thirty years of varied oil and gas experience. Prior to joining Blackbird, David was responsible for the design,

construction and start-up of Mosaic Energy’s Kakwa / Jayar 50 mmscfd sour and liquid stabilization gas plant, gathering system, and wellhead facilities.

Prior to Mosaic Energy, David was responsible for the design, construction, start-up and expansion of Crew Energy’s Septimus 60 mmscfd sweet gas plant,

gas gathering system and wellhead facilities. Prior to these companies, David held senior positions with Canetic Resources, ConocoPhillips, Imperial Oil

and Qatar Liquefied Gas Company.

Joshua Wylie

Vice President, Land

Joshua is a Petroleum Landman with over seven years of experience working with junior exploration and production companies. Joshua has been

instrumental in assembling Blackbird’s core Elmworth land position and was a key team member in the acquisition of a processing agreement for Blackbird’s

Elmworth Montney gas and a firm gas take away agreement in the Alliance pipeline to Chicago. Joshua is a member of the Canadian Association of

Petroleum Landmen.

Appendix: Management

TSX-V: BBI26

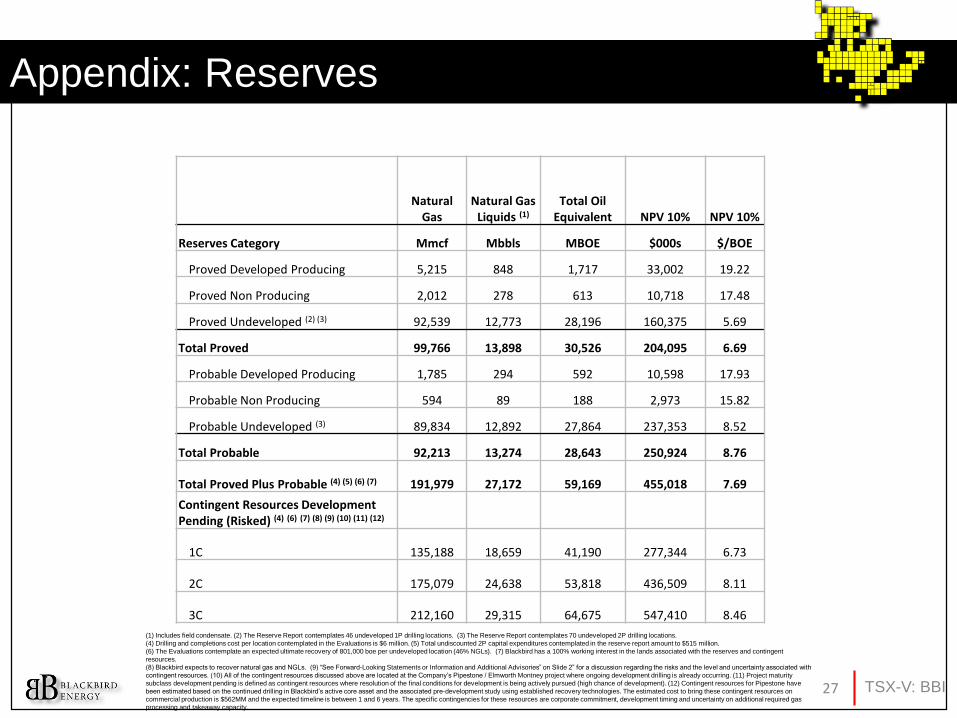

Appendix: Reserves

(1) Includes field condensate. (2) The Reserve Report contemplates 46 undeveloped 1P drilling locations. (3) The Reserve Report contemplates 70 undeveloped 2P drilling locations.

(4) Drilling and completions cost per location contemplated in the Evaluations is $6 million. (5) Total undiscounted 2P capital expenditures contemplated in the reserve report amount to $515 million.

(6) The Evaluations contemplate an expected ultimate recovery of 801,000 boe per undeveloped location (46% NGLs). (7) Blackbird has a 100% working interest in the lands associated with the reserves and contingent

resources.

(8) Blackbird expects to recover natural gas and NGLs. (9) “See Forward-Looking Statements or Information and Additional Advisories” on Slide 2” for a discussion regarding the risks and the level and uncertainty associated with

contingent resources. (10) All of the contingent resources discussed above are located at the Company’s Pipestone / Elmworth Montney project where ongoing development drilling is already occurring. (11) Project maturity

subclass development pending is defined as contingent resources where resolution of the final conditions for development is being actively pursued (high chance of development). (12) Contingent resources for Pipestone have

been estimated based on the continued drilling in Blackbird’s active core asset and the associated pre-development study using established recovery technologies. The estimated cost to bring these contingent resources on

commercial production is $562MM and the expected timeline is between 1 and 6 years. The specific contingencies for these resources are corporate commitment, development timing and uncertainty on additional required gas

processing and takeaway capacity.

Natural Gas

Natural Gas Liquids (1)

Total Oil Equivalent NPV 10% NPV 10%

Reserves Category Mmcf Mbbls MBOE $000s $/BOE

Proved Developed Producing 5,215 848 1,717 33,002 19.22

Proved Non Producing 2,012 278 613 10,718 17.48

Proved Undeveloped (2) (3) 92,539 12,773 28,196 160,375 5.69

Total Proved 99,766 13,898 30,526 204,095 6.69

Probable Developed Producing 1,785 294 592 10,598 17.93

Probable Non Producing 594 89 188 2,973 15.82

Probable Undeveloped (3) 89,834 12,892 27,864 237,353 8.52

Total Probable 92,213 13,274 28,643 250,924 8.76

Total Proved Plus Probable (4) (5) (6) (7) 191,979 27,172 59,169 455,018 7.69

Contingent Resources Development Pending (Risked) (4) (6) (7) (8) (9) (10) (11) (12)

1C 135,188 18,659 41,190 277,344 6.73

2C 175,079 24,638 53,818 436,509 8.11

3C 212,160 29,315 64,675 547,410 8.46

TSX-V: BBI27

Forward‐Looking Statements or Information and Additional Advisories

Certain statements included in this presentation constitute forward-looking statements or forward-looking information under applicable securities legislation. Such forward-looking statements or information are provided for thepurpose of providing information about management's current expectations and plans relating to the future. Readers are cautioned that reliance on such information may not be appropriate for other purposes, such as makinginvestment decisions. Forward-looking statements or information typically contain statements with words such as "anticipate", "believe", "expect", "plan", "intend", "estimate", "propose", "project" or similar words suggesting futureoutcomes or statements regarding an outlook. Forward-looking statements or information concerning Blackbird Energy Inc. (“Blackbird” or the “Company”) in this presentation may include, but are not limited to, statements orinformation with respect to: guidance, forecasts, and related assumptions; the potential value of Blackbird's assets in the context of the current Paramount/Appache transaction; present and future industry activity in the PipestoneCorridor; the attributes and potential of the Montney; the number of prospective Montney intervals on Blackbird’s lands; Blackbird's valuation at one of the greatest discounts to its RENAV within the Montney peer group; expectedtype curves; capital spending and availability of cash; the cost reduction, and drilling and completion optimization derived from use of the Stage Completions Inc. Bowhead II technology and the other benefits of the Stage Completionsinvestment including priority access to the technology and growth potential of the minority interest investment; proposed processing options, commodity pricing; costs associated with operating in the oil and natural gas business;Blackbird's plans for a high impact delineation and development program, continued land aggregation, production growth through egress and increased processing and take-away; and the ability of Blackbird's corporate socialresponsibility initiatives to provide a significant competitive advantage. In addition, references to reserves and resources are deemed to be forward-looking information, as they involve the implied assessment, based on certainestimates and assumptions, that the reserves and resources described exist in the quantities predicted or estimated. Forward-looking statements or information are based on a number of factors and assumptions which have beenused to develop such statements and information but which may prove to be incorrect. Blackbird believes that the expectations reflected in such forward-looking statements or information are reasonable; however, undue relianceshould not be placed on forward-looking statements because Blackbird can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified in this presentation,assumptions have been made regarding, among other things: the impact of increasing competition; the timely receipt of any required regulatory approvals; the ability of Blackbird to retain and obtain qualified staff, equipment andservices in a timely and cost efficient manner; the ability of Blackbird to operate in a safe, efficient and effective manner; the ability of Blackbird to obtain financing on acceptable terms; the timing and costs of operating Blackbird'sbusiness; the ability of Blackbird to secure adequate product transportation; future oil and natural gas prices; currency, exchange and interest rates; the regulatory framework regarding royalties, taxes and environmental matters;and the ability of Blackbird to successfully market its oil and natural gas products. Readers are cautioned that the foregoing list is not exhaustive of all factors and assumptions which have been used.

Forward‐looking statements or information are based on current expectations, estimates and projections that involve a number of risks and uncertainties which could cause actual results to differ materially from

those anticipated by Blackbird and described in the forward‐looking statements or information. These risks and uncertainties may cause actual results to differ materially from the forward‐looking statements or

information. The material risk factors affecting Blackbird and its business are contained in Blackbird's Annual Information Form which is available at SEDAR at www.sedar.com. The forward‐looking statements or

information contained in this presentation are made as of the date hereof and Blackbird undertakes no obligation to update publicly or revise any forward‐looking statements or information, whether as a result of new

information, future events or otherwise unless required by applicable securities laws. The forward‐looking statements or information contained in this presentation are expressly qualified by this cautionary statement.

Additional Advisories

This presentation contains statistical data, market research and industry forecasts that were obtained from government or other industry publications and reports or based on estimates derived from such publications

and reports and management’s knowledge of, and experience in, the markets in which Blackbird operates. Government and industry publications and reports generally indicate that they have obtained their

information from sources believed to be reliable, but do not guarantee the accuracy and completeness of their information. Often, such information is provided subject to specific terms and conditions limiting the

liability of the provider, disclaiming any responsibility for such information, and/or limiting a third party’s ability to rely on such information. None of the authors of such publications and reports has provided any form

of consultation, advice or counsel regarding any aspect of, or is in any way whatsoever associated with, Blackbird. Further, certain of these organizations are advisors to participants in the Canadian oil and gas

industry, and they may present information in a manner that is more favourable to that industry than would be presented by an independent source. Actual outcomes may vary materially from those forecast in such

reports or publications, and the prospect for material variation can be expected to increase as the length of the forecast period increases. While management believes this data to be reliable, market and industry

data is subject to variations and cannot be verified due to limits on the availability and reliability of data inputs, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any

market or other survey. None of Blackbird nor its affiliates has independently verified any of the data from third party sources referred to in this presentation or ascertained the underlying assumptions relied upon by

such sources.

The outlook and guidance in this presentation has been provided to assist investors in analyzing Blackbird's anticipated development strategies and prospects and it may not be appropriate for other purposes and

actual results could differ from the guidance provided herein.

The TSX Venture Exchange does not accept responsibility for the adequacy or accuracy of the information contained in this presentation.

Advisories

TSX-V: BBI28

Independent Reserves Evaluation

Estimates of the Company's reserves and contingent resources and the net present value of future net revenue attributable to the Company's reserves and contingent resources as at March 1, 2017, are based upon

the reports that were prepared by McDaniel & Associates Consultants Ltd. (“McDaniel”), dated March 24, 2017. The estimates of reserves and contingent resources provided in this document are estimates only and

there is no guarantee that the estimated reserves or contingent resources will be recovered. Actual reserves and contingent resources may be greater than or less than the estimates provided in this in this

document, and the differences may be material. The estimates of reserves or contingent resources and future net revenue for individual properties may not reflect the same confidence level as estimates of reserves

and future net revenue for all properties, due to the effects of aggregation. Estimates of net present value of future net revenue attributable to the Company's reserves and contingent resources do not represent the

fair market value of the Company's reserves and contingent resources and there is uncertainty that the net present value of future net revenue will be realized. There is no assurance that the forecast price and cost

assumptions applied by McDaniel in evaluating Blackbird's reserves, contingent resources and prospective resources will be attained and variances could be material. There is uncertainty that it will be commercially

viable to produce any portion of the contingent resources that are described herein.

Note Regarding Oil and Gas Metrics

Blackbird has adopted the standard of 6 Mcf:1 bbl when converting natural gas to boes. Condensate and other natural gas liquids (“NGLs”) are converted to boes at a ratio of 1 bbl:1 bbl. Boes may be misleading,

particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 bbl is based roughly on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at

the Company's sales point. Given the value ratio based on the current price of oil as compared to natural gas is significantly different from the energy equivalency of 6 Mcf: 1 bbl, utilizing a conversion ratio at 6 Mcf: 1

bbl may be misleading as an indication of value.

Oil and Gas Definitions

Terms that are used in this news release that are not otherwise defined herein are provided below:

Low estimate contingent resources, referred to herein as 1C, is a classification of estimated resources described in the Canadian Oil and Gas Evaluation Handbook, which is considered to be the best estimate of the

quantity that will actually be recovered. It is equally likely that the actual quantities recovered will be greater or less than the best estimate. Resources in the best estimate case have a 90% probability that the actual

quantities recovered will equal or exceed the estimate.

Best estimate contingent resources, referred to herein as 2C, is a classification of estimated resources described in the Canadian Oil and Gas Evaluation Handbook, which is considered to be the best estimate of the

quantity that will actually be recovered. It is equally likely that the actual quantities recovered will be greater or less than the best estimate. Resources in the best estimate case have a 50% probability that the actual

quantities recovered will equal or exceed the estimate.

High estimate contingent resources, referred to herein as 3C, is a classification of estimated resources described in the Canadian Oil and Gas Evaluation Handbook, which is considered to be the best estimate of the

quantity that will actually be recovered. It is equally likely that the actual quantities recovered will be greater or less than the best estimate. Resources in the best estimate case have a 10% probability that the actual

quantities recovered will equal or exceed the estimate.

Contingent resources are the quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations using established technology or technology under development, but which

are not currently considered to be commercially recoverable due to one or more contingencies. Contingencies are conditions that must be satisfied for a portion of contingent resources to be classified as reserves

that are: (a) specific to the project being evaluated; and (b) expected to be resolved within a reasonable timeframe. Contingencies may include factors such as economic, legal, environmental, political and regulatory

matters or a lack of markets. It is also appropriate to classify as contingent resources the estimated discovered recoverable quantities associated with a project in the early evaluation stage. There is no certainty that

it will be commercially viable to produce any portion of the contingent resources or that Blackbird will produce any portion of the volumes currently classified as contingent resources. The estimates of contingent

resources involve implied assessment, based on certain estimates and assumptions, that the resources described exists in the quantities predicted or estimated, as at a given date, and that the resources can be

profitably produced in the future. The risked net present value of the future net revenue from the contingent resources does not represent the fair market value of the contingent resources. Actual contingent

resources (and any volumes that may be reclassified as reserves) and future production therefrom may be greater than or less than the estimates provided herein.

Developed producing reserves are those gross reserves that are expected to be recovered from completion intervals open at the time of the estimate. These reserves may be currently producing or, if shut in, they

must have previously been on production, and the date of resumption of production must be known with reasonable certainty.

Developed non-producing reserves are those reserves that either have not been on production, or have previously been on production, but are shut in, and the date of resumption of production is unknown.

Advisories

TSX-V: BBI29

Developed reserves are those gross reserves that are expected to be recovered from existing wells and installed facilities or, if facilities have not been installed, that would involve a low

expenditure (for example, when compared to the cost of drilling a well) to put the reserves on production. The developed category may be subdivided into producing and non-producing.

Gross means (i) in relation to the Company's interest in production or reserves, its "company gross reserves", which are the Company's working interest (operating or non-operating) share before deduction of

royalties and without including any royalty interests of the Company; and (ii) in relation to wells, the total number of wells in which the Company has an interest.

Net means, in relation to the Company's interest in wells or lands, the number of wells obtained by aggregating the Company's working interest in each of its gross wells.

Probable reserves are those additional gross reserves that are less certain to be recovered than proved reserves. It is equally likely that the actual remaining quantities recovered will be greater or less than the sum

of the estimated proved plus probable reserves.

Proved reserves are those gross reserves that can be estimated with a high degree of certainty to be recoverable. It is likely that the actual remaining quantities recovered will exceed the estimated proved reserves.

In this presentation, proved plus probable reserves are also referred to as 2P reserves.

Reserves are estimated remaining quantities of oil and natural gas and related substances anticipated to be recoverable from known accumulations, as of a given date, based on: (i) analysis of drilling, geological,

geophysical and engineering data; (ii) the use of established technology; and (iii) specified economic conditions, which are generally accepted as being reasonable. Reserves are classified according to the degree of

certainty associated with the estimates.

Undeveloped reserves are those reserves expected to be recovered from known accumulations where a significant expenditure (for example, when compared to the cost of drilling a well) is required to render them

capable of production. They must fully meet the requirements of the reserves classification (proved, probable) to which they are assigned.

Analogous Information

Certain information in this document may constitute "analogous information" as defined in National Instrument 51-101 – Standards of Disclosure for Oil and Gas Activities ("NI 51-101"), including, but not limited to,

information relating to areas, wells and/or operations that are in geographical proximity to or on-trend with prospective lands held by Blackbird and production information related to wells that are believed to be on

trend with Blackbird's properties. Such information has been obtained from government sources, regulatory agencies or other industry participants, each of which is independent of Blackbird. Management of

Blackbird believes the information may be relevant to help define the reservoir characteristics in which Blackbird may hold an interest and such information has been presented to help demonstrate the basis for

Blackbird's business plans and strategies.

However, to Blackbird’s knowledge, such analogous information has not been prepared in accordance with NI 51-101 and the Canadian Oil and Gas Evaluation Handbook and Blackbird is unable to confirm that the

analogous information was prepared by a qualified reserves evaluator or auditor. Blackbird has no way of verifying the accuracy of such information. There is no certainty that the results of the analogous information

or inferred thereby will be achieved by Blackbird and such information should not be construed as an estimate of future production levels. Such information is also not an estimate of the reserves or resources

attributable to lands held or to be held by Blackbird and there is no certainty that the reservoir data and economics information for the lands held or to be held by Blackbird will be similar to the information presented

herein. The reader is cautioned that the data relied upon by Blackbird may be in error and/or may not be analogous to such lands to be held by Blackbird.

Initial Production Rates

Any references in this document to test rates, flow rates, initial and/or final raw test or production rates, early production, test volumes and/or "flush" production rates are useful in confirming the presence of

hydrocarbons, however, such rates are not necessarily indicative of long-term performance or of ultimate recovery. Such rates may also include recovered "load" fluids used in well completion stimulation. Readers

are cautioned not to place reliance on such rates in calculating the aggregate production for Blackbird. In addition, the Montney is an unconventional resource play which may be subject to high initial decline rates.

Such rates may be estimated based on other third party estimates or limited data available at this time and are not determinative of the rates at which such wells will continue production and decline thereafter.

Information Regarding Disclosure on Reserves

The reserve estimates contained herein are estimates only and there is no guarantee that the estimated reserves or resources will be recovered. Volumes of reserves have been presented based on a company

interest basis which includes Blackbird's royalty interests without deducting royalties payable by the Company. The estimates of reserves for individual properties may not reflect the same confidence level as

estimates of reserves for all properties, due to the effects of aggregation. Where discussed herein "NPV 10%" represents the net present value (net of capex) of net income discounted at 10%, with net income

reflecting the indicated oil, liquids and natural gas prices and IP rate, less internal estimates of operating costs and royalties. It should not be assumed that the future net revenues estimated by Blackbird's

independent reserve evaluators represent the fair market value of the reserves, nor should it be assumed that Blackbird's internally estimated value of its undeveloped land holdings or any estimates referred to

herein from third parties represent the fair market value of the lands.

Advisories

TSX-V: BBI30

Blackbird Energy Inc.

Garth Braun – Chairman, CEO &

President

Tel: 403.699.9929 ext. 101

Cell: 403.500.5550

Email: [email protected]

Blackbird Energy Inc.

400, 444 5th Avenue SW

Calgary, Alberta T2P 2T8

TSX-V: BBI31